Embed Size (px)

Citation preview

Chapter 11

Accounting for Equity

Business Entity Forms

Sole Proprietorship

Sole Proprietorship

PartnershipPartnership CorporationCorporation

C 5

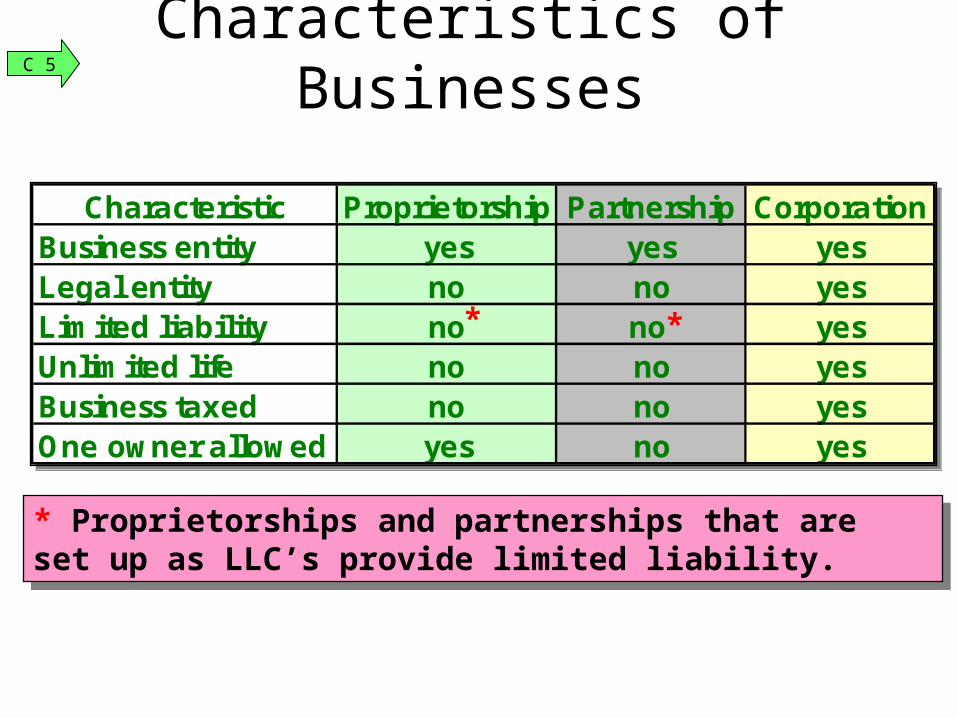

* Proprietorships and partnerships that are set up as LLC’s provide limited liability.

* Proprietorships and partnerships that are set up as LLC’s provide limited liability.

Characteristics of Businesses

Characteristic Proprietorship Partnership CorporationBusiness entity yes yes yesLegal entity no no yesLimited liability no no yesUnlimited life no no yesBusiness taxed no no yesOne owner allowed yes no yes

Characteristic Proprietorship Partnership CorporationBusiness entity yes yes yesLegal entity no no yesLimited liability no no yesUnlimited life no no yesBusiness taxed no no yesOne owner allowed yes no yes

**

C 5

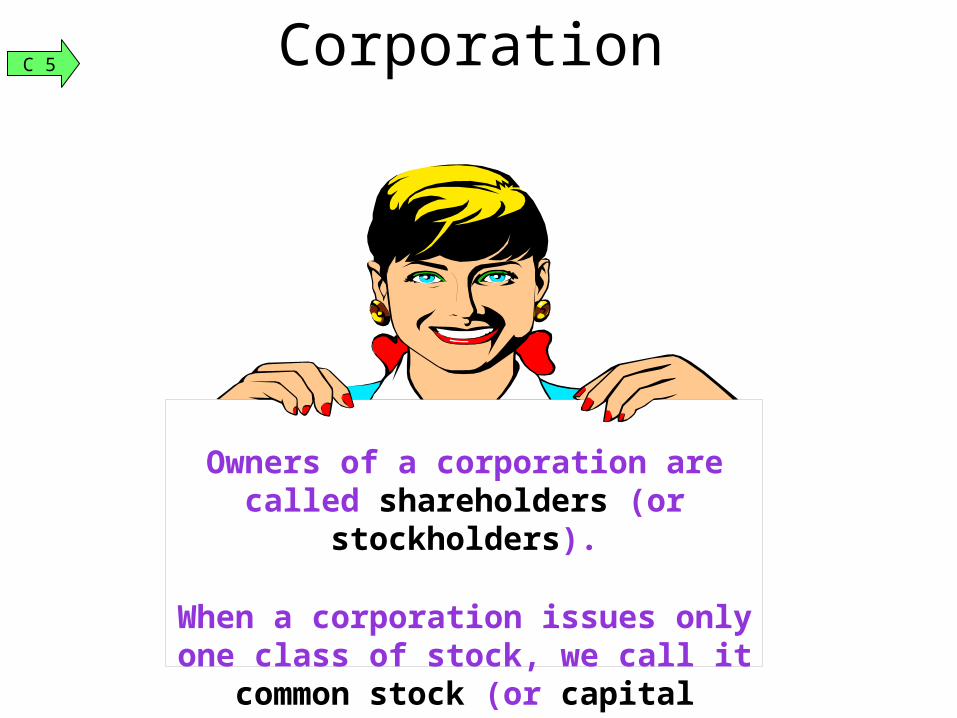

Owners of a corporation are called shareholders (or stockholders).

When a corporation issues only one class of stock, we call it common stock

(or capital stock).

CorporationC 5

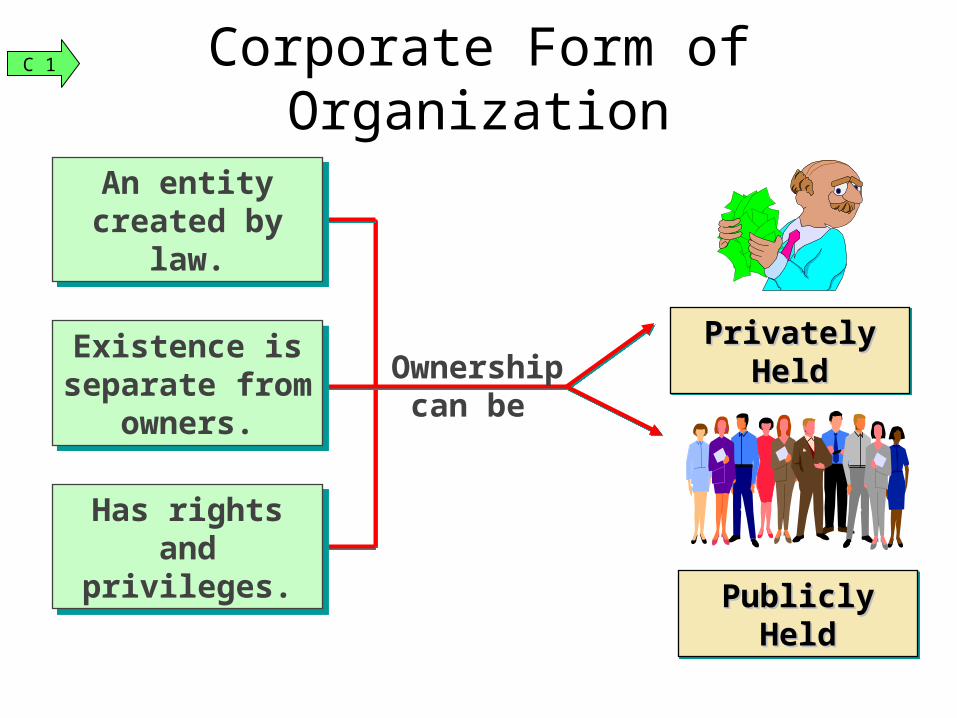

Privately HeldPrivately HeldPrivately HeldPrivately Held

Publicly HeldPublicly HeldPublicly HeldPublicly Held

Ownership can be

Corporate Form of Organization

Existence is separate from

owners.

Existence is separate from

owners.

An entity created by law.

An entity created by law.

Has rights and privileges.

Has rights and privileges.

C 1

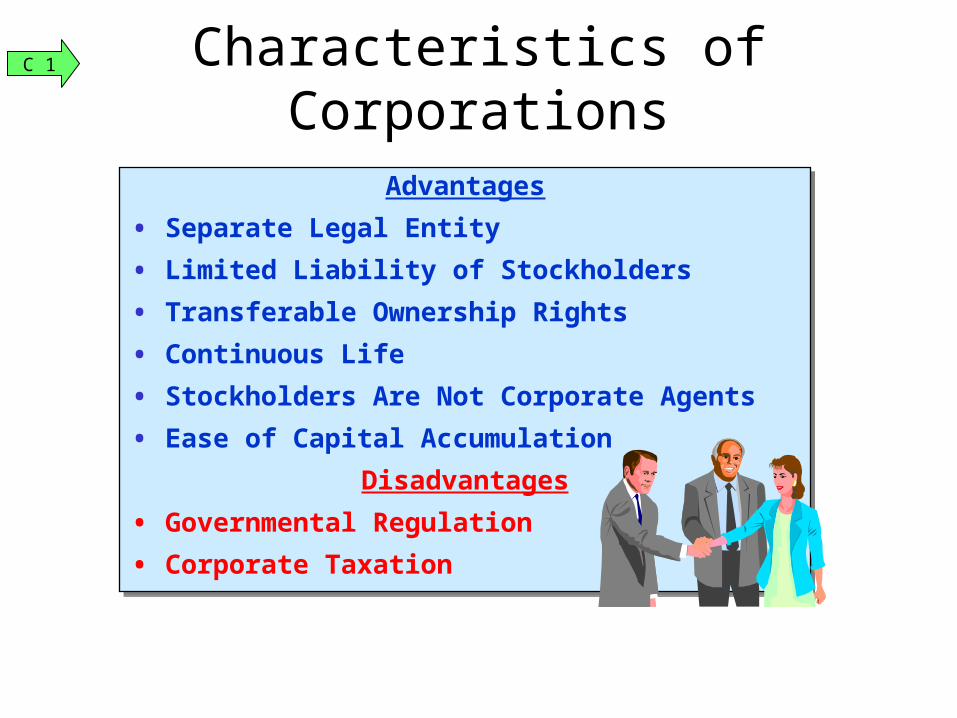

Advantages

• Separate Legal Entity

• Limited Liability of Stockholders

• Transferable Ownership Rights

• Continuous Life

• Stockholders Are Not Corporate Agents

• Ease of Capital Accumulation

Disadvantages

• Governmental Regulation

• Corporate Taxation

Advantages

• Separate Legal Entity

• Limited Liability of Stockholders

• Transferable Ownership Rights

• Continuous Life

• Stockholders Are Not Corporate Agents

• Ease of Capital Accumulation

Disadvantages

• Governmental Regulation

• Corporate Taxation

Characteristics of CorporationsC 1

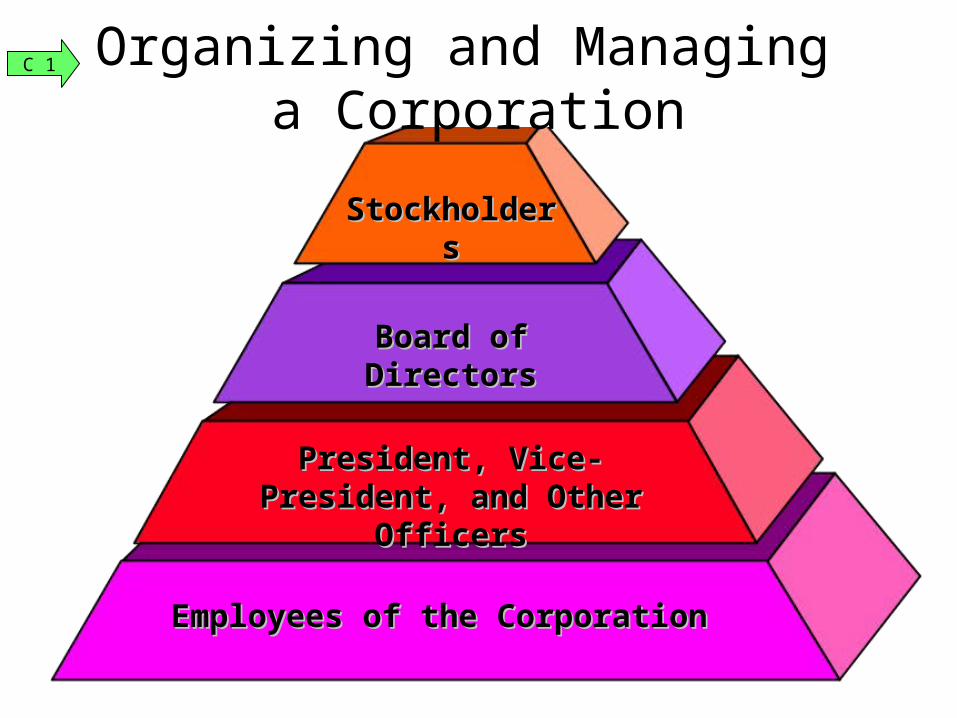

StockholdersStockholders

Board of DirectorsBoard of Directors

President, Vice-President, President, Vice-President, and Other Officersand Other Officers

Employees of the CorporationEmployees of the Corporation

Organizing and Managing a Corporation

C 1

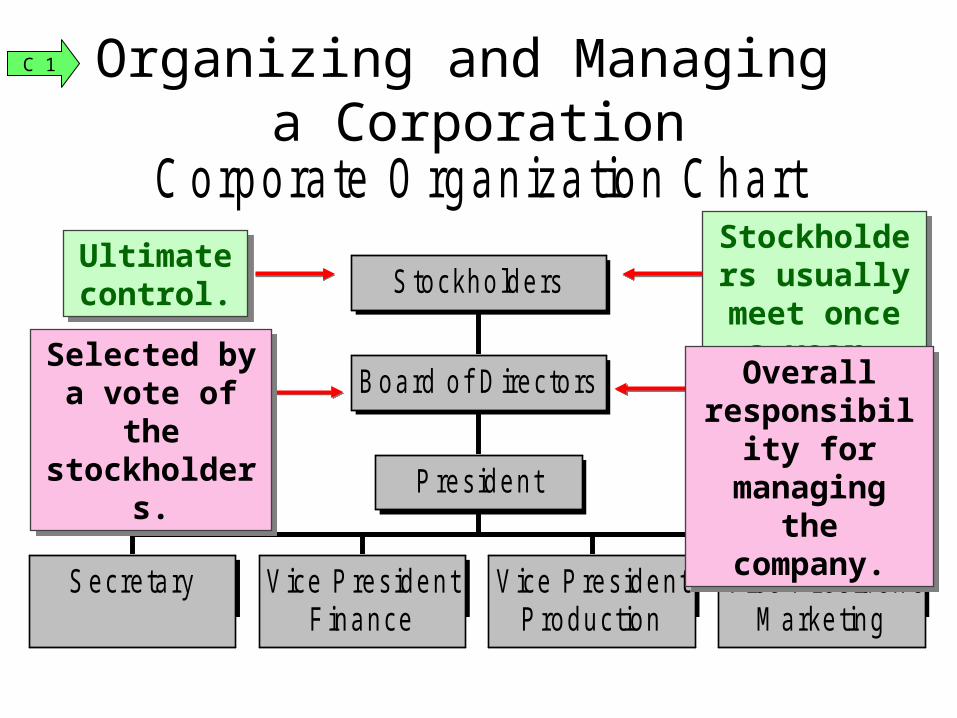

C orpo ra te O rgan iza tion C hart

Secretary V ice P residentF inance

V ice P residentP roduction

V ice P residentM arketing

President

Board of D irectors

S tockholdersUltimate control.

Ultimate control.

Stockholders usually meet once a year.

Stockholders usually meet once a year.

Organizing and Managing a Corporation

Selected by a vote of the

stockholders.

Selected by a vote of the

stockholders.

Overall responsibility for managing the company.

Overall responsibility for managing the company.

C 1

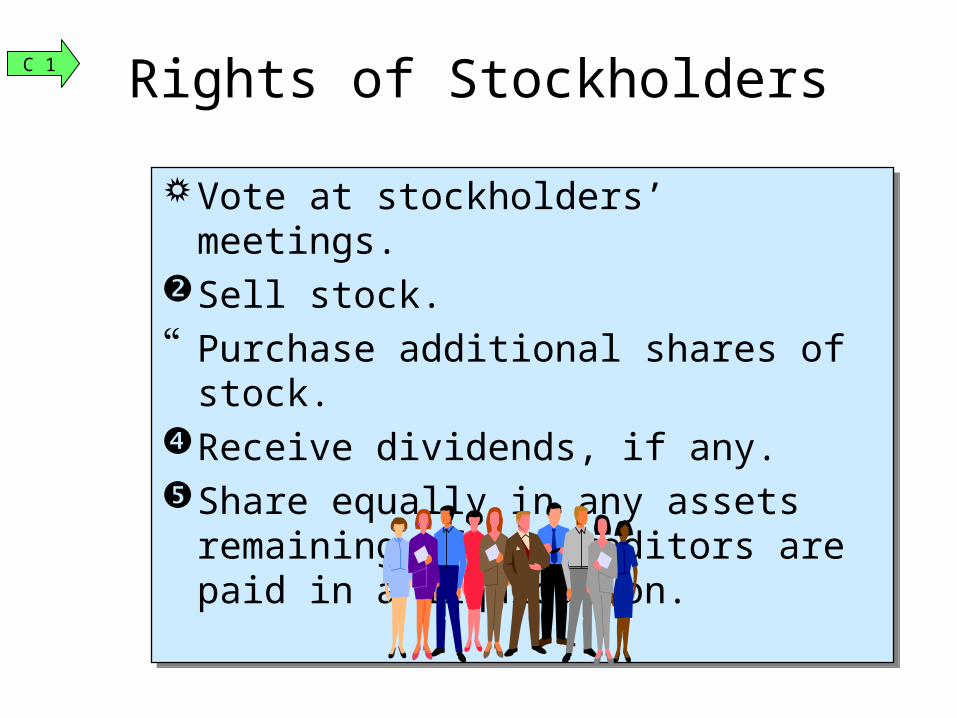

Vote at stockholders’ meetings.Sell stock. Purchase additional shares of stock.Receive dividends, if any.Share equally in any assets remaining

after creditors are paid in a liquidation.

Vote at stockholders’ meetings.Sell stock. Purchase additional shares of stock.Receive dividends, if any.Share equally in any assets remaining

after creditors are paid in a liquidation.

Rights of StockholdersC 1

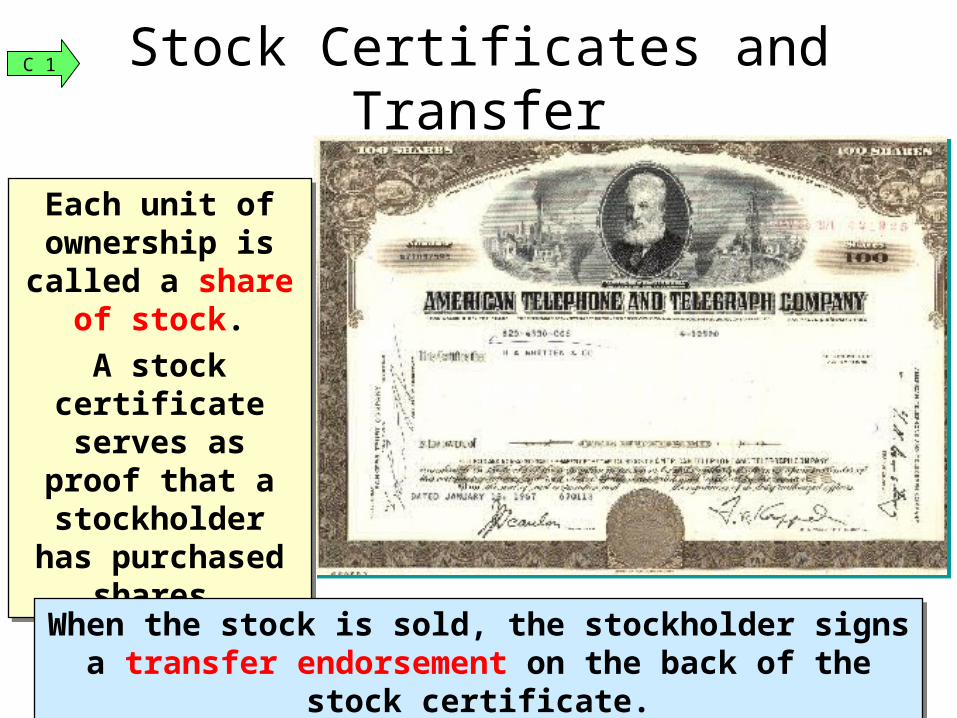

Each unit of ownership is

called a share of stock.

A stock certificate serves as proof

that a stockholder has purchased

shares.

Each unit of ownership is

called a share of stock.

A stock certificate serves as proof

that a stockholder has purchased

shares.

Stock Certificates and Transfer

When the stock is sold, the stockholder signs a transfer endorsement on the back of the stock certificate.

When the stock is sold, the stockholder signs a transfer endorsement on the back of the stock certificate.

C 1

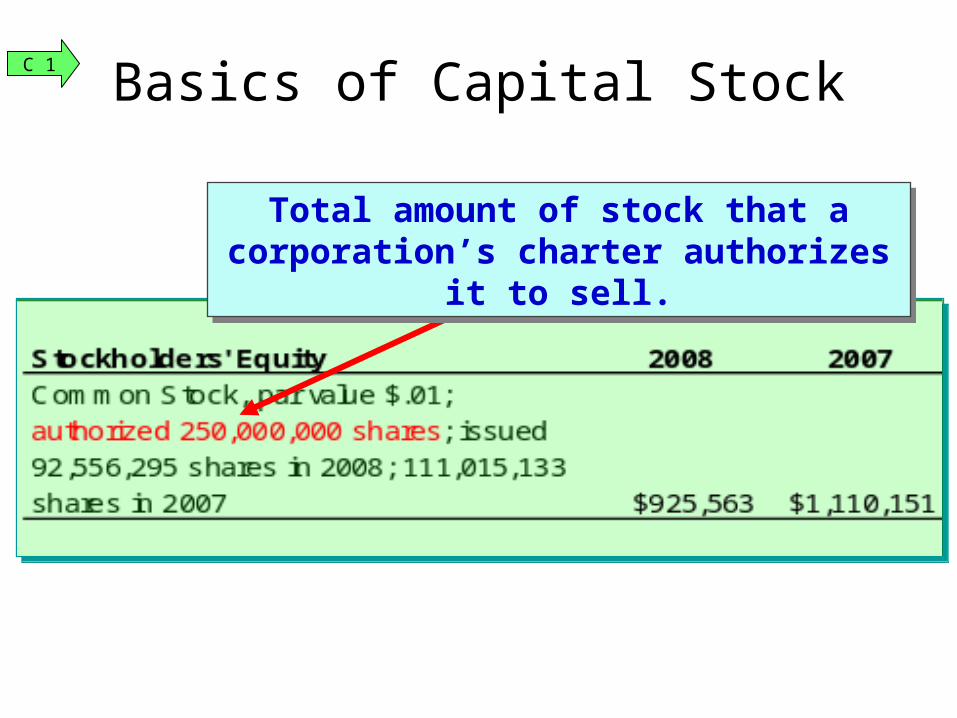

Basics of Capital Stock

Total amount of stock that a corporation’s charter authorizes it to sell.

Total amount of stock that a corporation’s charter authorizes it to sell.

C 1

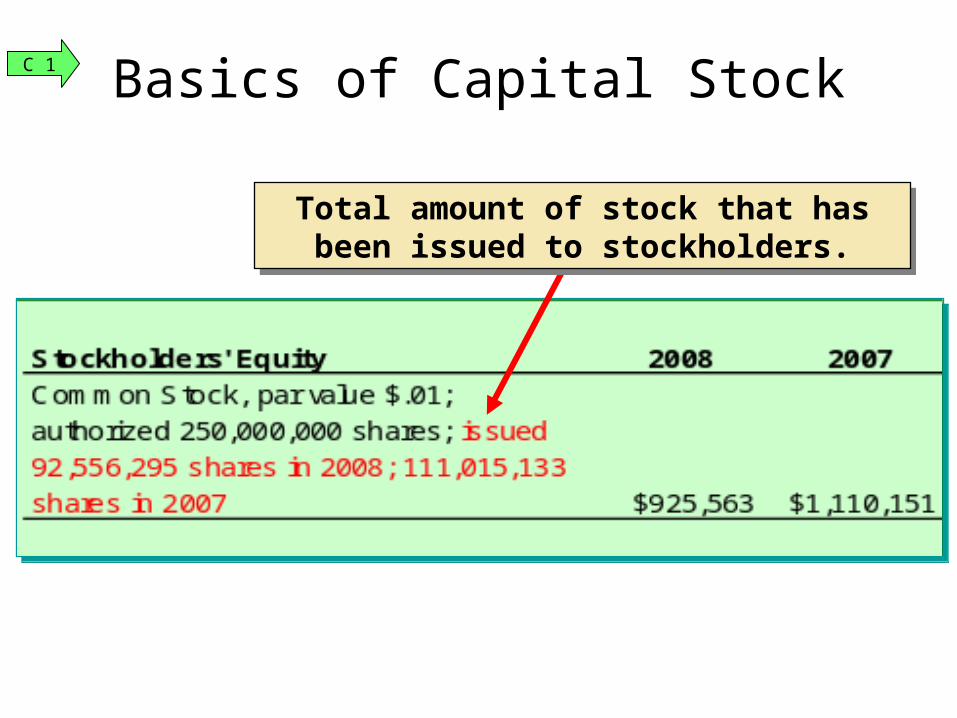

Basics of Capital Stock

Total amount of stock that has been issued to stockholders.

Total amount of stock that has been issued to stockholders.

C 1

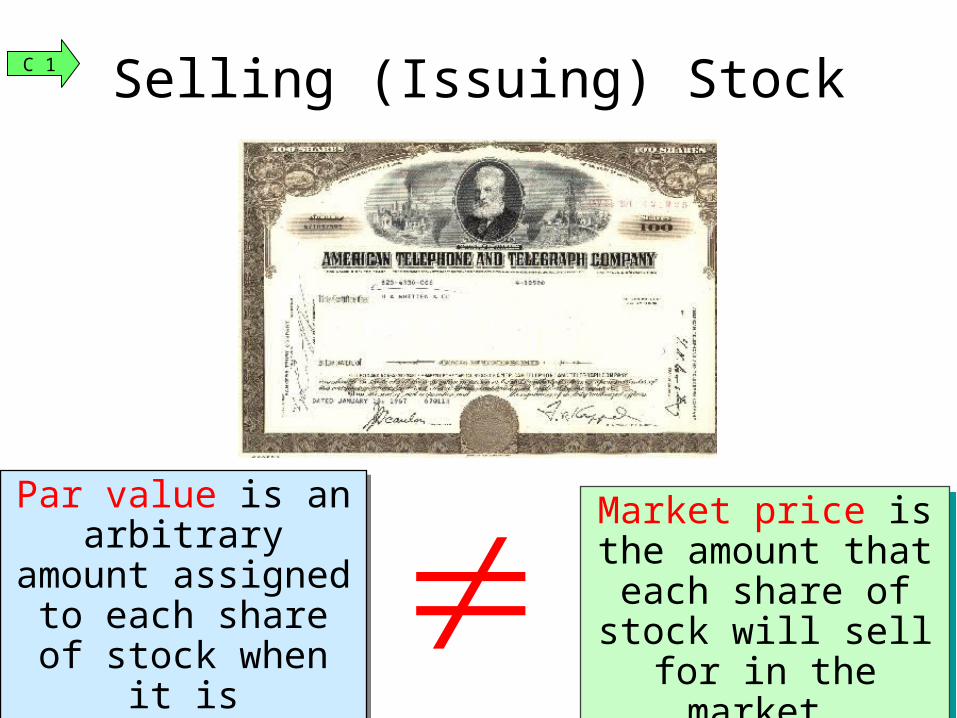

Par value is an arbitrary amount assigned to each

share of stock when it is authorized.

Par value is an arbitrary amount assigned to each

share of stock when it is authorized.

Market price is the amount that each share of stock will

sell for in the market.

Market price is the amount that each share of stock will

sell for in the market.

Selling (Issuing) Stock

C 1

Par Value

No-Par Value

Stated Value

Classes of StockP1

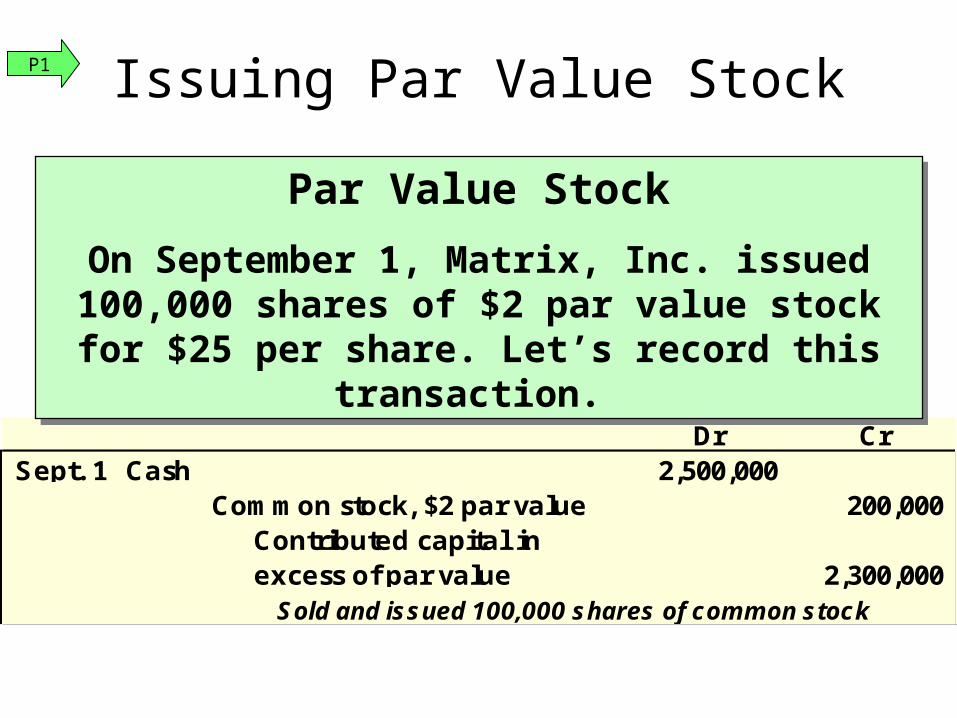

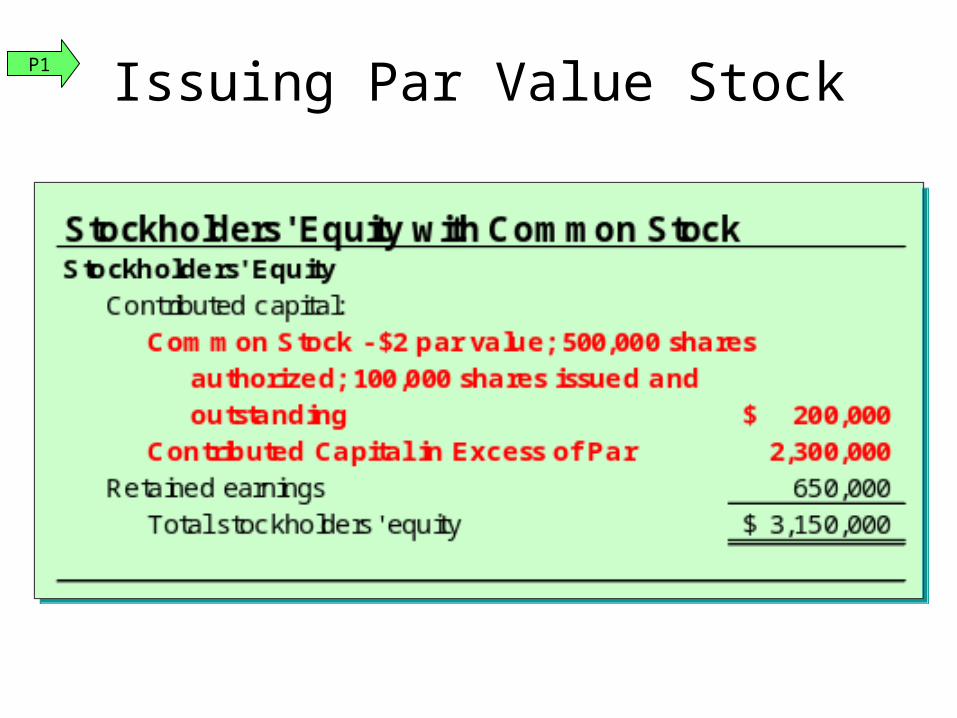

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for $25 per share.

Let’s record this transaction.

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for $25 per share.

Let’s record this transaction.

Record:1. The cash received.

2. The number of shares issued × the par value per share in the Common Stock account.

3. The remainder is assigned to Contributed Capital in Excess of Par.

Record:1. The cash received.

2. The number of shares issued × the par value per share in the Common Stock account.

3. The remainder is assigned to Contributed Capital in Excess of Par.

Issuing Par Value StockP1

Issuing Par Value Stock

Dr CrSept. 1 Cash 2,500,000

Common stock, $2 par value 200,000 Contributed capital in excess of par value 2,300,000

Sold and issued 100,000 shares of common stock

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for $25 per share.

Let’s record this transaction.

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for $25 per share.

Let’s record this transaction.

P1

Issuing Par Value StockP1

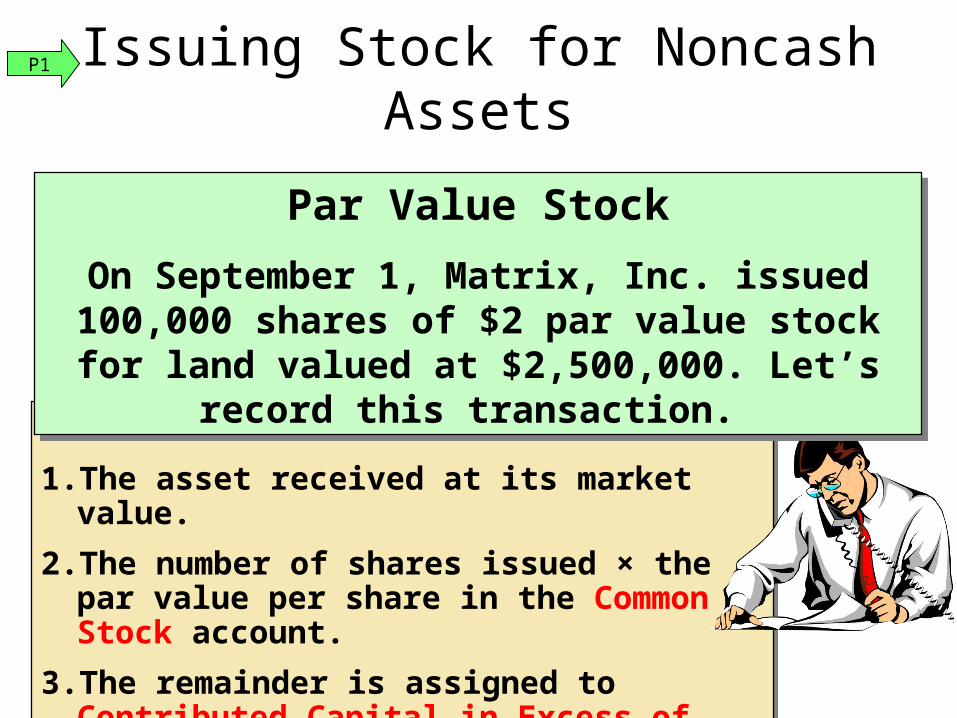

Record:1. The asset received at its market value.

2. The number of shares issued × the par value per share in the Common Stock account.

3. The remainder is assigned to Contributed Capital in Excess of Par.

Record:1. The asset received at its market value.

2. The number of shares issued × the par value per share in the Common Stock account.

3. The remainder is assigned to Contributed Capital in Excess of Par.

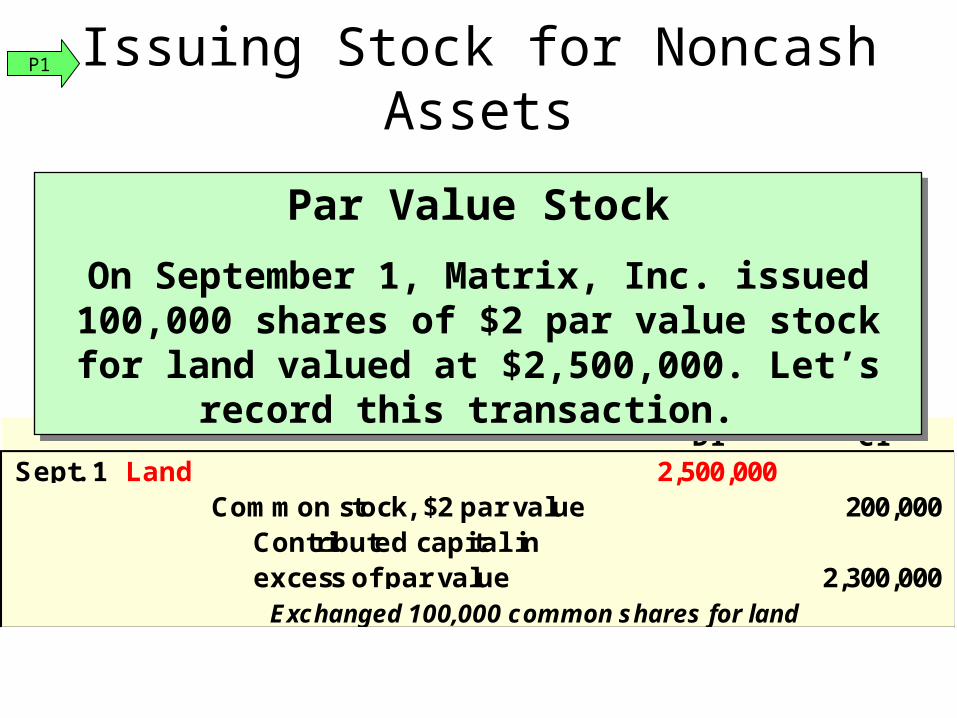

Issuing Stock for Noncash Assets

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for land valued at

$2,500,000. Let’s record this transaction.

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for land valued at

$2,500,000. Let’s record this transaction.

P1

Issuing Stock for Noncash Assets

Dr Cr Sept. 1 Land 2,500,000

Common stock, $2 par value 200,000 Contributed capital in excess of par value 2,300,000

Exchanged 100,000 common shares for land

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for land valued at

$2,500,000. Let’s record this transaction.

Par Value Stock

On September 1, Matrix, Inc. issued 100,000 shares of $2 par value stock for land valued at

$2,500,000. Let’s record this transaction.

P1

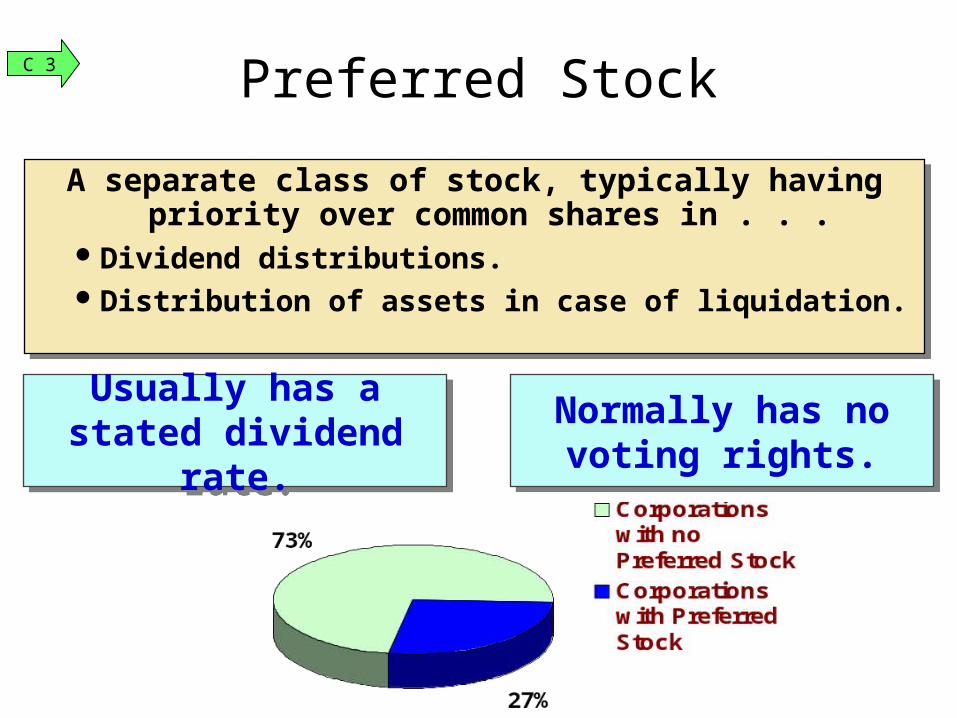

A separate class of stock, typically having priority over common shares in . . .

Dividend distributions.Distribution of assets in case of liquidation.

A separate class of stock, typically having priority over common shares in . . .

Dividend distributions.Distribution of assets in case of liquidation.

Usually has a stated dividend rate.

Usually has a stated dividend rate.

Normally has no voting rights.

Normally has no voting rights.

Preferred StockC 3

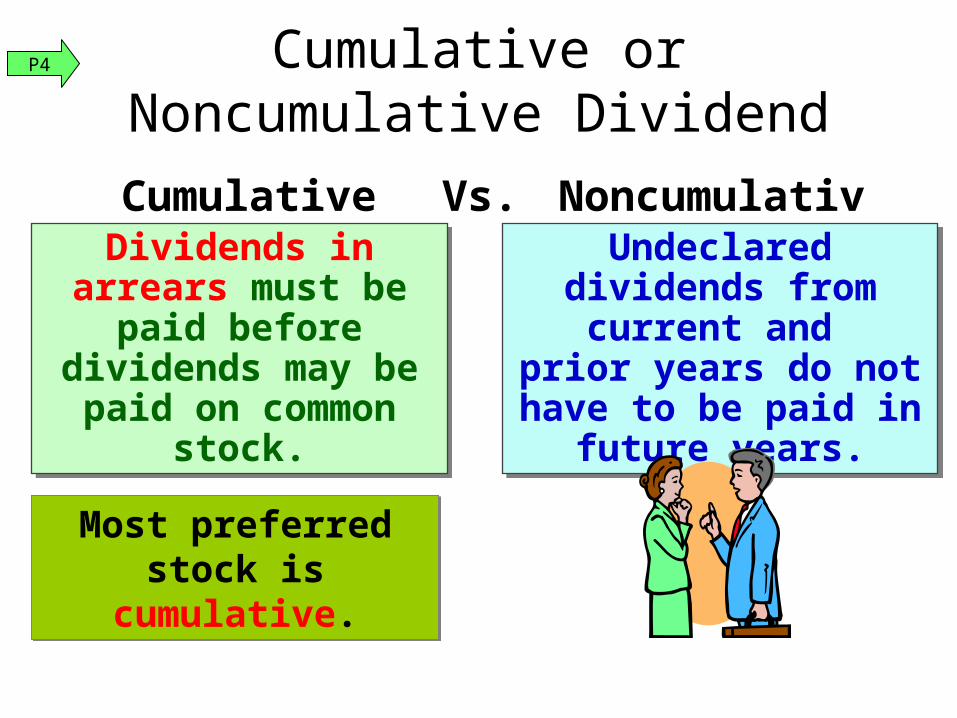

Vs. NoncumulativeCumulativeDividends in arrears must be paid before

dividends may be paid on common

stock.

Dividends in arrears must be paid before

dividends may be paid on common

stock.

Undeclared dividends from current and

prior years do not have to be paid in future

years.

Undeclared dividends from current and

prior years do not have to be paid in future

years.

Cumulative or Noncumulative Dividend

Most preferred stock is cumulative.

Most preferred stock is cumulative.

P4

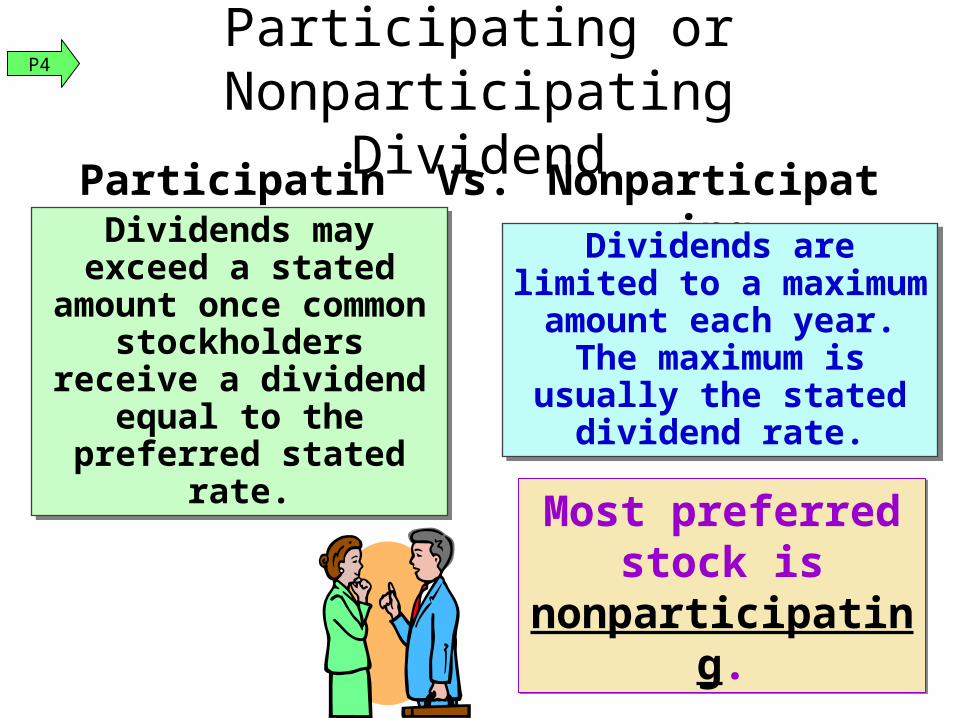

Vs. NonparticipatingParticipatingDividends may exceed a stated amount once common stockholders

receive a dividend equal to the preferred

stated rate.

Dividends may exceed a stated amount once common stockholders

receive a dividend equal to the preferred

stated rate.

Dividends are limited to a maximum amount each

year. The maximum is usually the stated

dividend rate.

Dividends are limited to a maximum amount each

year. The maximum is usually the stated

dividend rate.

Participating or Nonparticipating Dividend

Most preferred stock is

nonparticipating.

Most preferred stock is

nonparticipating.

P4

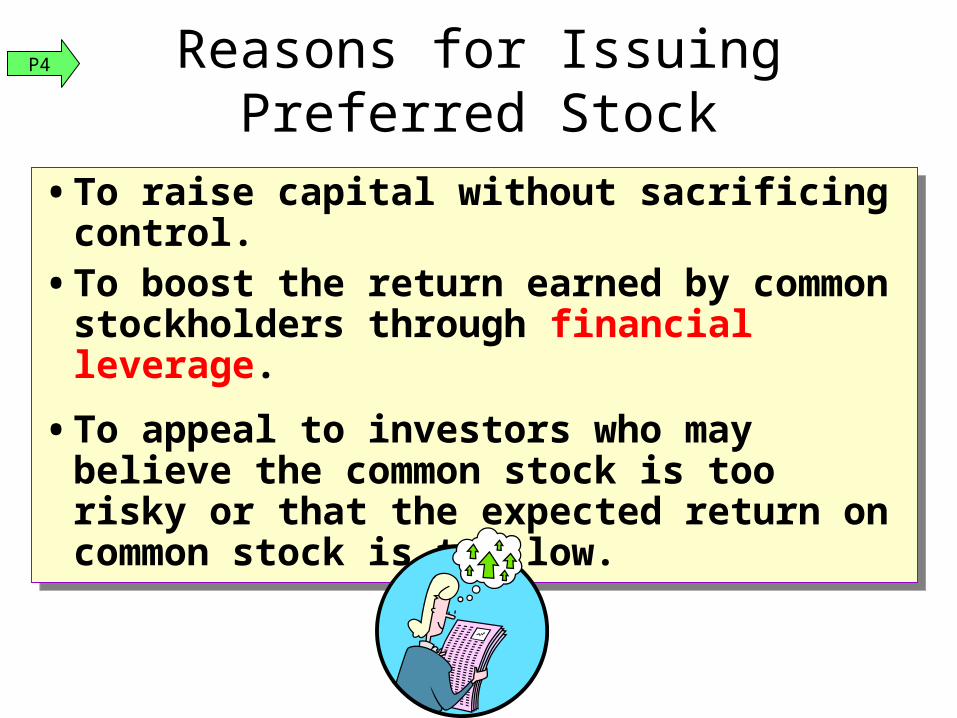

Reasons for Issuing Preferred Stock

• To raise capital without sacrificing control.

• To boost the return earned by common stockholders through financial leverage.

• To appeal to investors who may believe the common stock is too risky or that the expected return on common stock is too low.

• To raise capital without sacrificing control.

• To boost the return earned by common stockholders through financial leverage.

• To appeal to investors who may believe the common stock is too risky or that the expected return on common stock is too low.

P4

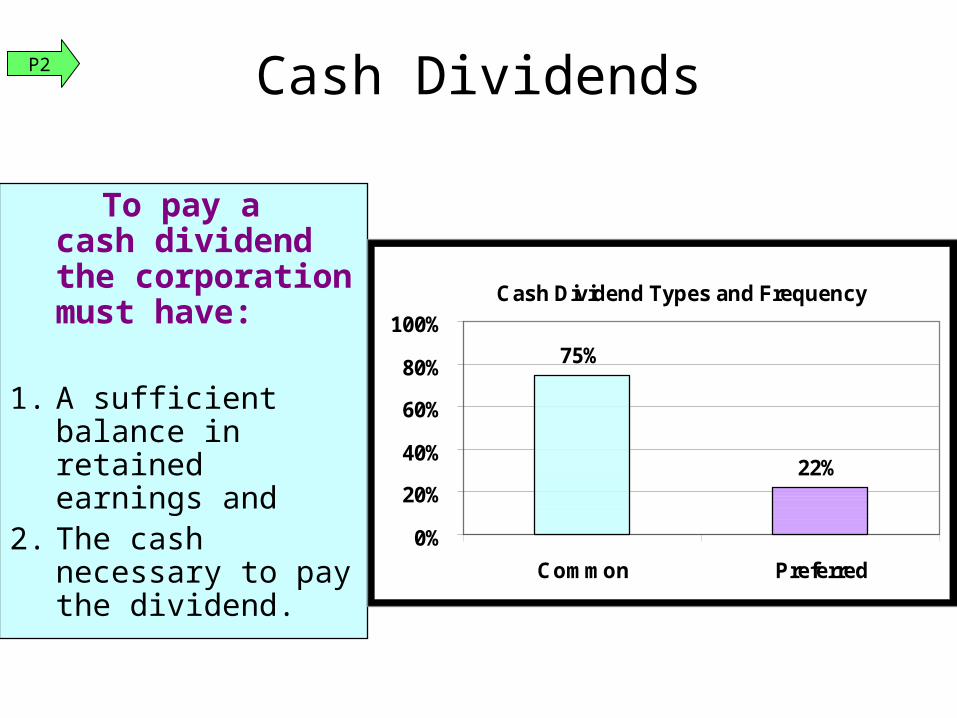

To pay a cash dividend the corporation must have:

1. A sufficient balance in retained earnings and

2. The cash necessary to pay the dividend.

Cash Dividend Types and Frequency

75%

22%

0%

20%

40%

60%

80%

100%

Common Preferred

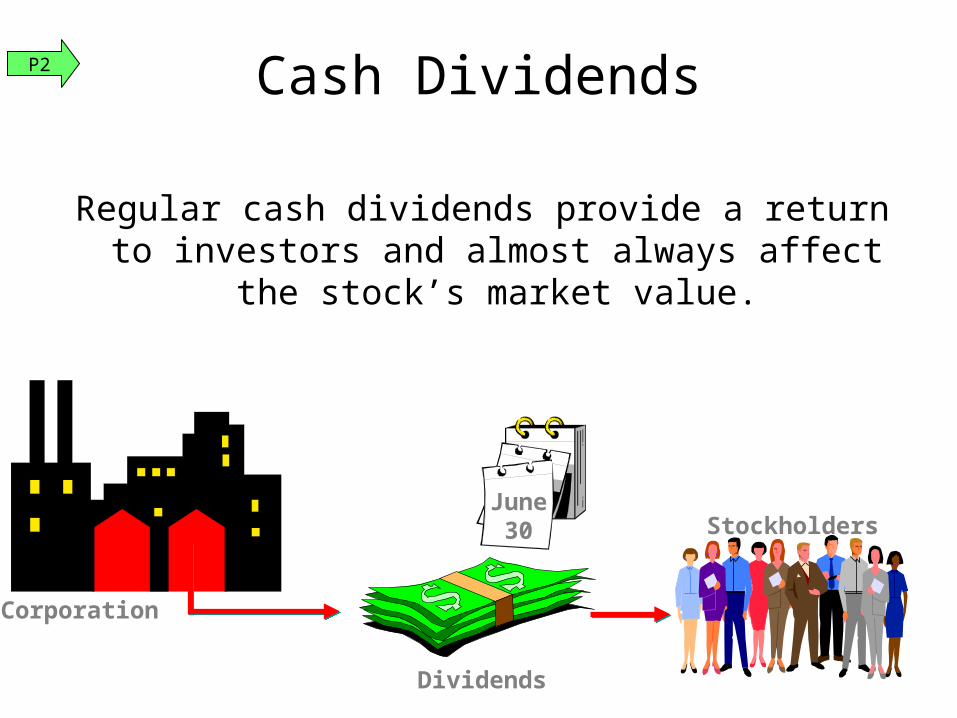

Cash DividendsP2

Regular cash dividends provide a return to investors and almost always affect the stock’s

market value.

Dividends

StockholdersJune

30

Cash Dividends

Corporation

P2

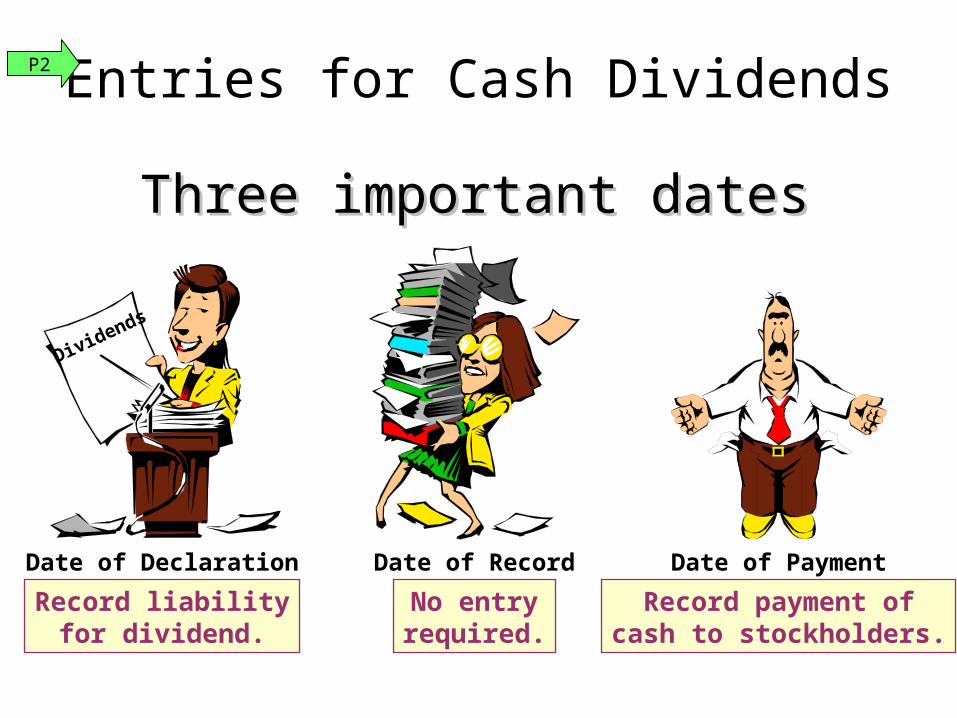

Three important datesThree important dates

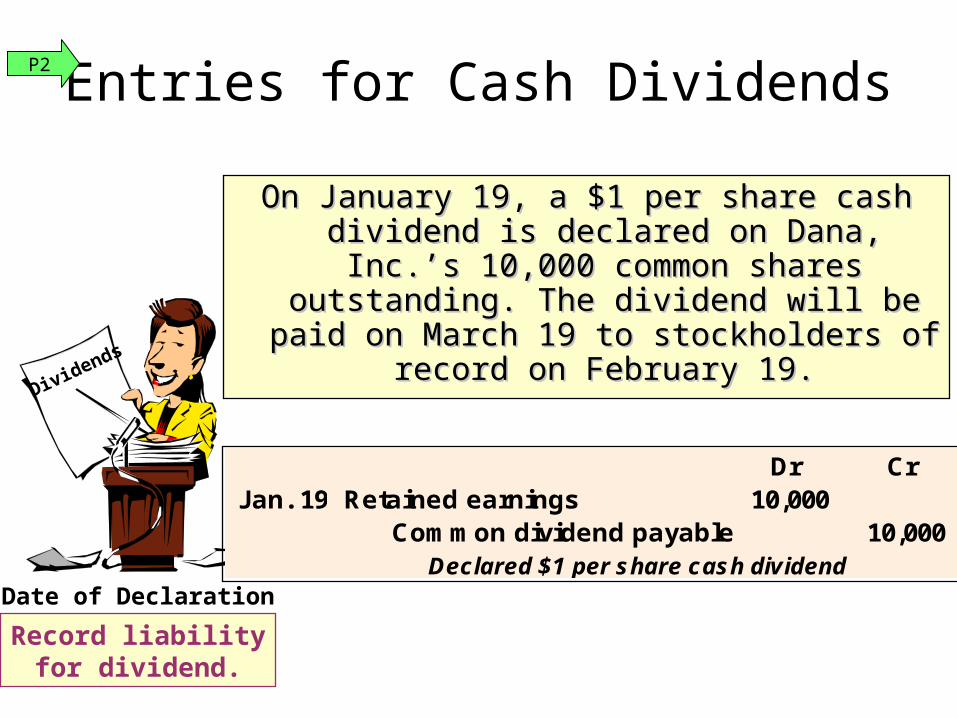

Date of Declaration

Record liabilityfor dividend.

Dividends

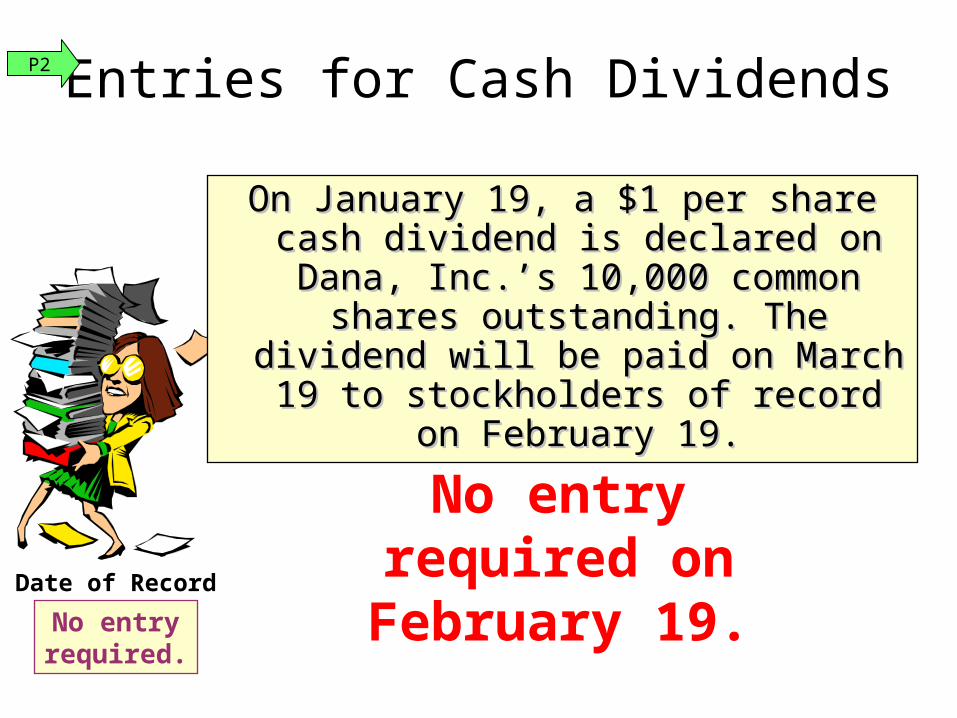

Date of Record

No entryrequired.

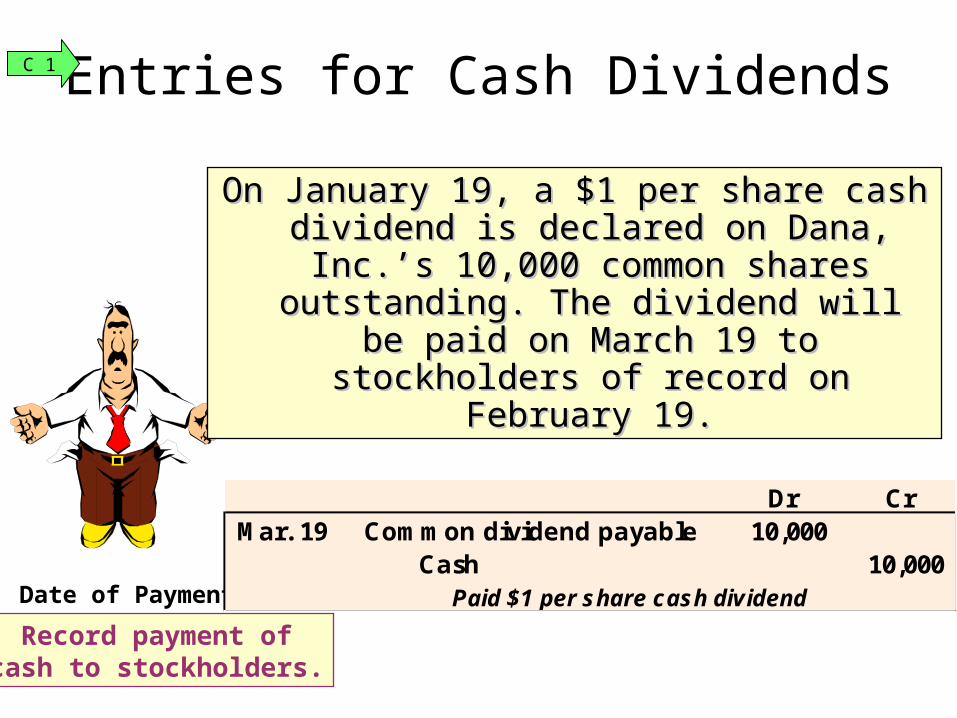

Date of Payment

Record payment ofcash to stockholders.

Entries for Cash DividendsP2

Date of Declaration

Record liabilityfor dividend.

Dividends

On January 19, a $1 per share cash dividend is On January 19, a $1 per share cash dividend is declared on Dana, Inc.’s 10,000 common declared on Dana, Inc.’s 10,000 common

shares outstanding. The dividend will be paid shares outstanding. The dividend will be paid on March 19 to stockholders of record on on March 19 to stockholders of record on

February 19.February 19.

Entries for Cash Dividends

Dr Cr Jan. 19 Retained earnings 10,000

Common dividend payable 10,000 Declared $1 per share cash dividend

P2

Date of Record

No entryrequired.

Entries for Cash Dividends

On January 19, a $1 per share cash On January 19, a $1 per share cash dividend is declared on Dana, Inc.’s dividend is declared on Dana, Inc.’s 10,000 common shares outstanding. 10,000 common shares outstanding. The dividend will be paid on March The dividend will be paid on March

19 to stockholders of record on 19 to stockholders of record on February 19.February 19.

No entry required on February 19.

P2

Date of Payment

Record payment ofcash to stockholders.

Entries for Cash Dividends

On January 19, a $1 per share cash On January 19, a $1 per share cash dividend is declared on Dana, Inc.’s dividend is declared on Dana, Inc.’s 10,000 common shares outstanding. 10,000 common shares outstanding.

The dividend will be paid on March 19 The dividend will be paid on March 19 to stockholders of record on February to stockholders of record on February

19.19.

Dr CrMar. 19 Common dividend payable 10,000

Cash 10,000 Paid $1 per share cash dividend

C 1

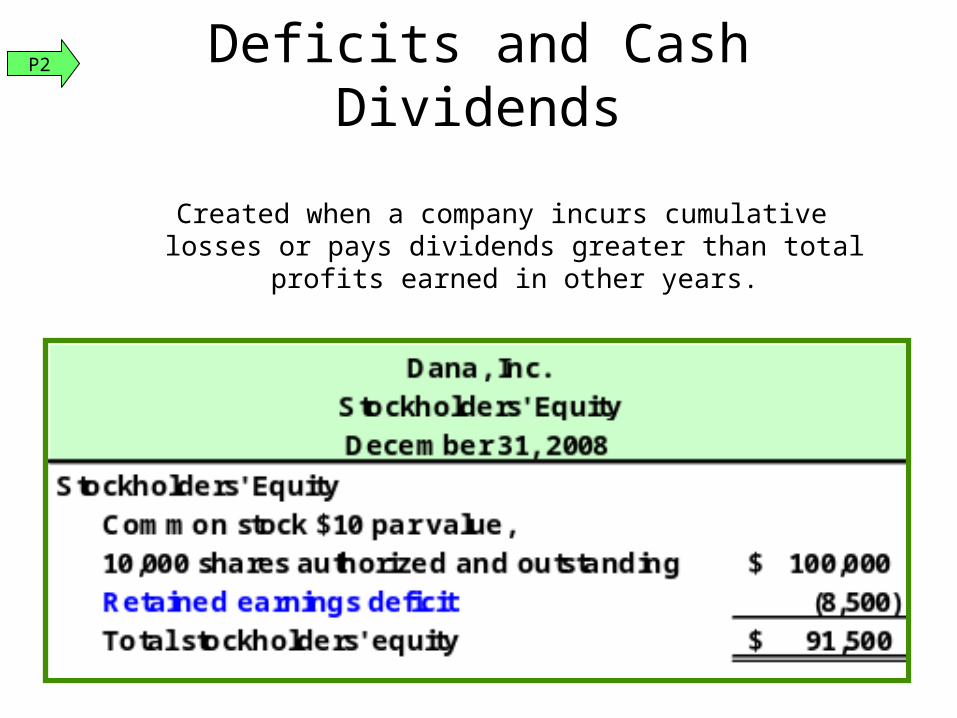

Created when a company incurs cumulative losses or pays dividends greater than total profits earned in other years.

Deficits and Cash DividendsP2

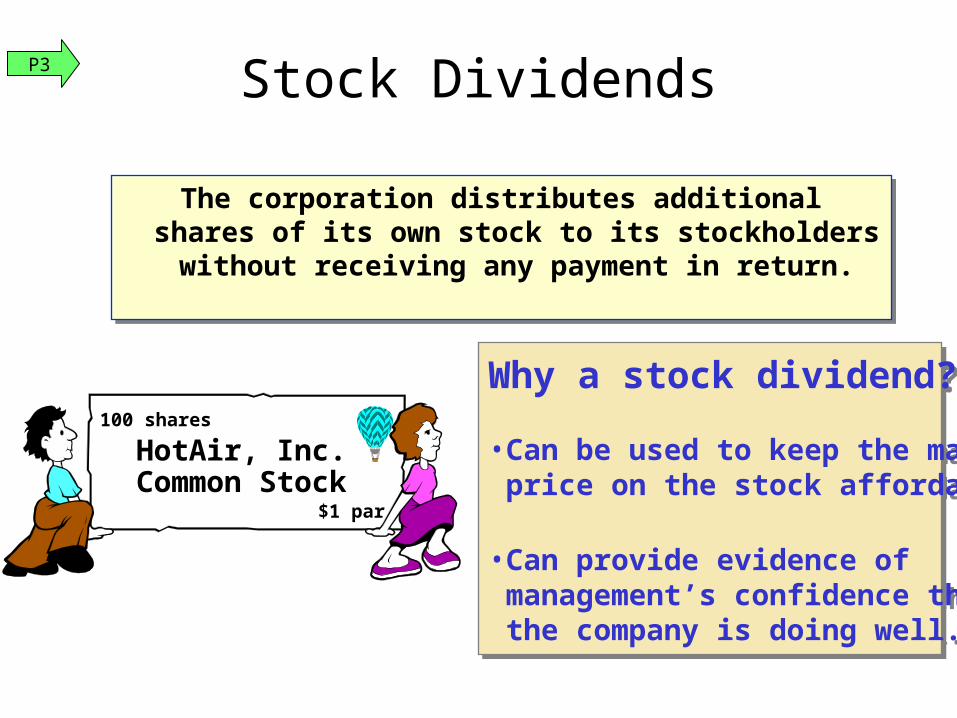

The corporation distributes additional shares of its own stock to its stockholders without

receiving any payment in return.

The corporation distributes additional shares of its own stock to its stockholders without

receiving any payment in return.

Stock Dividends

Why a stock dividend?

•Can be used to keep the market price on the stock affordable.

•Can provide evidence of management’s confidence that the company is doing well.

Why a stock dividend?

•Can be used to keep the market price on the stock affordable.

•Can provide evidence of management’s confidence that the company is doing well.

HotAir, Inc.Common Stock

100 shares

$1 par

P3

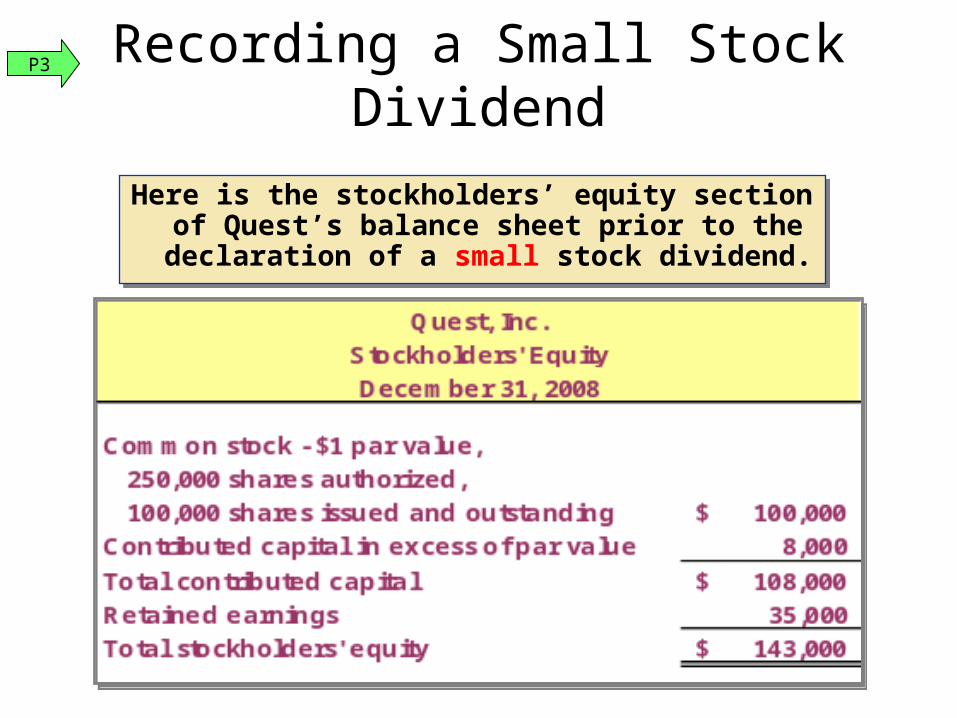

Here is the stockholders’ equity section of Quest’s balance sheet prior to the

declaration of a small stock dividend.

Here is the stockholders’ equity section of Quest’s balance sheet prior to the

declaration of a small stock dividend.

Recording a Small Stock DividendP3

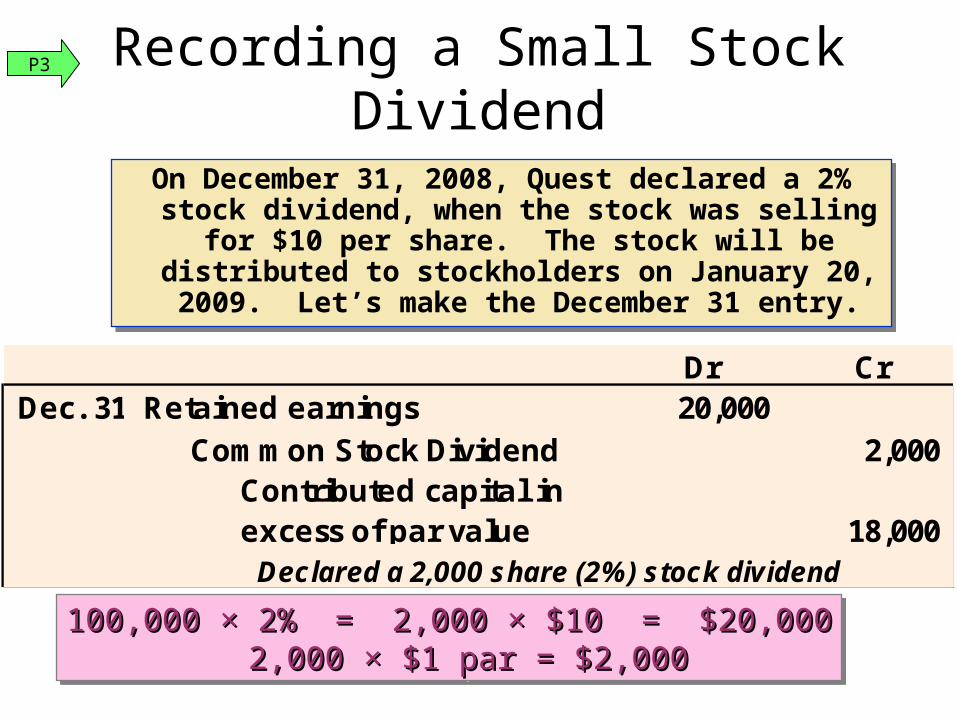

On December 31, 2008, Quest declared a 2% stock dividend, when the stock was selling for $10 per

share. The stock will be distributed to stockholders on January 20, 2009. Let’s make the December 31

entry.

On December 31, 2008, Quest declared a 2% stock dividend, when the stock was selling for $10 per

share. The stock will be distributed to stockholders on January 20, 2009. Let’s make the December 31

entry.

Recording a Small Stock Dividend

100,000 × 2% = 2,000 × $10 = $20,000100,000 × 2% = 2,000 × $10 = $20,000 2,000 × $1 par = $2,0002,000 × $1 par = $2,000

100,000 × 2% = 2,000 × $10 = $20,000100,000 × 2% = 2,000 × $10 = $20,000 2,000 × $1 par = $2,0002,000 × $1 par = $2,000

Dr CrDec. 31 Retained earnings 20,000

Common Stock Dividend 2,000 Contributed capital in excess of par value 18,000

Declared a 2,000 share (2%) stock dividend

P3

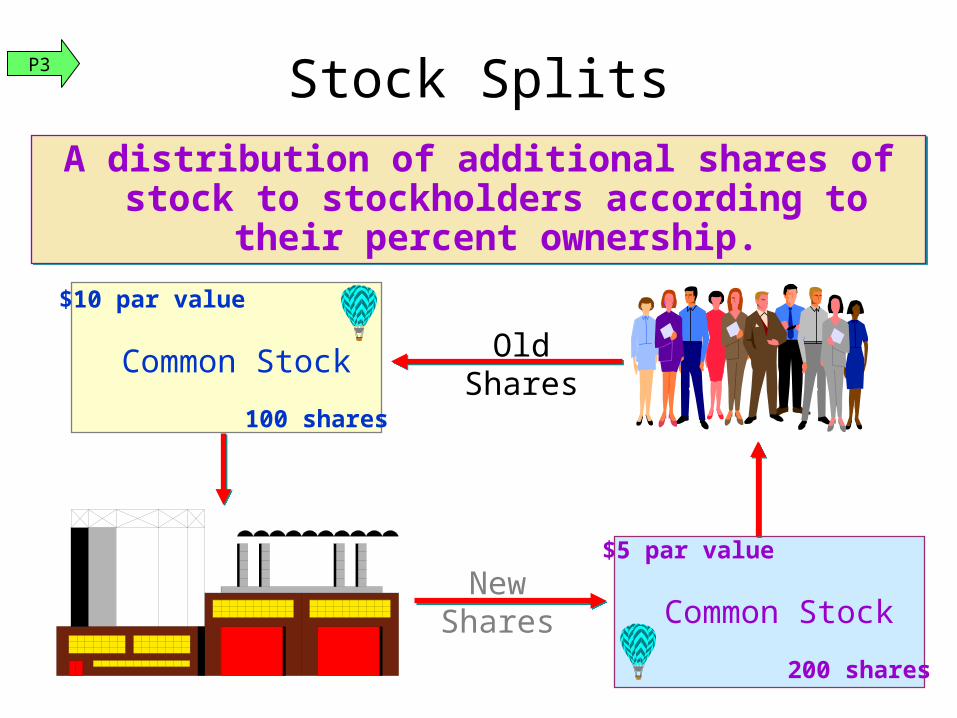

A distribution of additional shares of stock to stockholders according to their percent

ownership.

A distribution of additional shares of stock to stockholders according to their percent

ownership.

Common Stock

$10 par value

100 shares

OldShares

NewShares Common Stock

$5 par value

200 shares

Stock SplitsP3

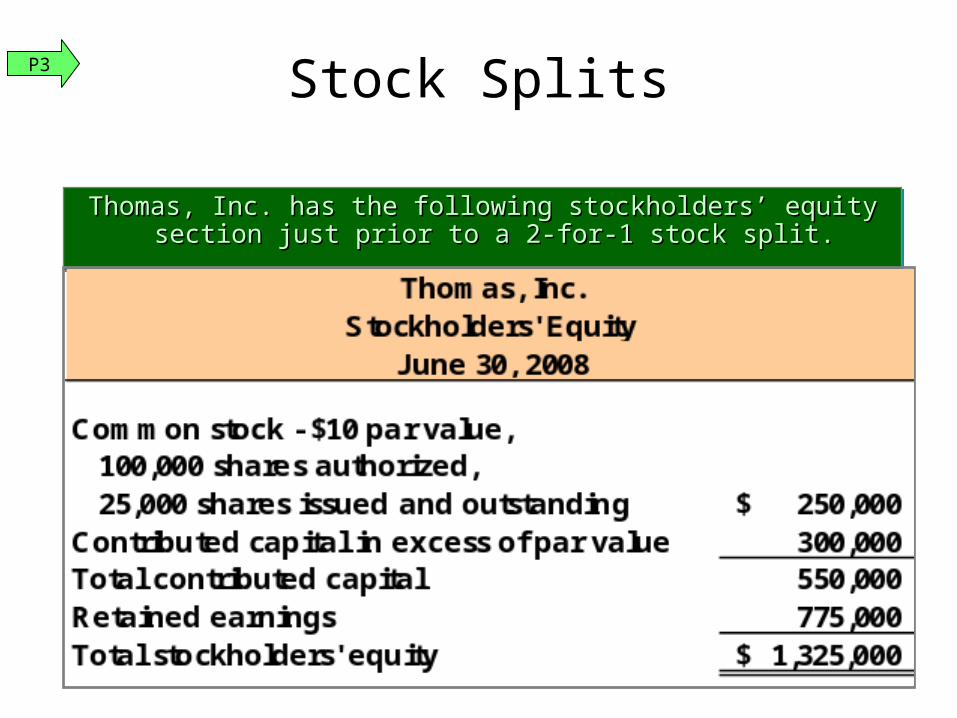

Thomas, Inc. has the following stockholders’ equity Thomas, Inc. has the following stockholders’ equity section just prior to a 2-for-1 stock split.section just prior to a 2-for-1 stock split.

Thomas, Inc. has the following stockholders’ equity Thomas, Inc. has the following stockholders’ equity section just prior to a 2-for-1 stock split.section just prior to a 2-for-1 stock split.

Stock SplitsP3

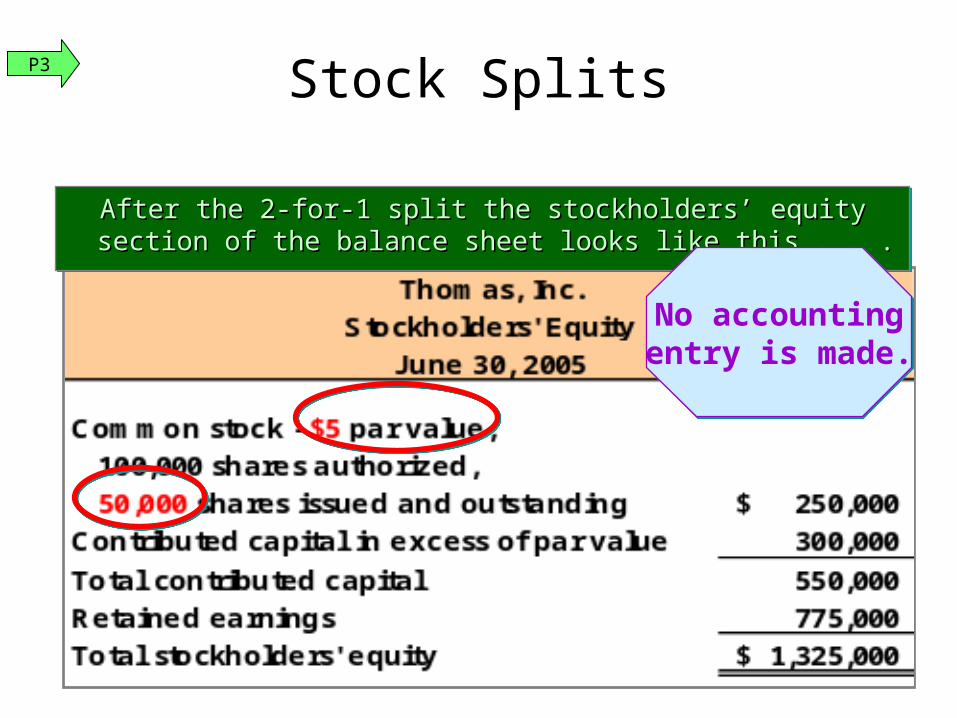

After the 2-for-1 split the stockholders’ equity section of the After the 2-for-1 split the stockholders’ equity section of the balance sheet looks like this . . .balance sheet looks like this . . .

After the 2-for-1 split the stockholders’ equity section of the After the 2-for-1 split the stockholders’ equity section of the balance sheet looks like this . . .balance sheet looks like this . . .

No accountingentry is made.No accountingentry is made.

Stock SplitsP3

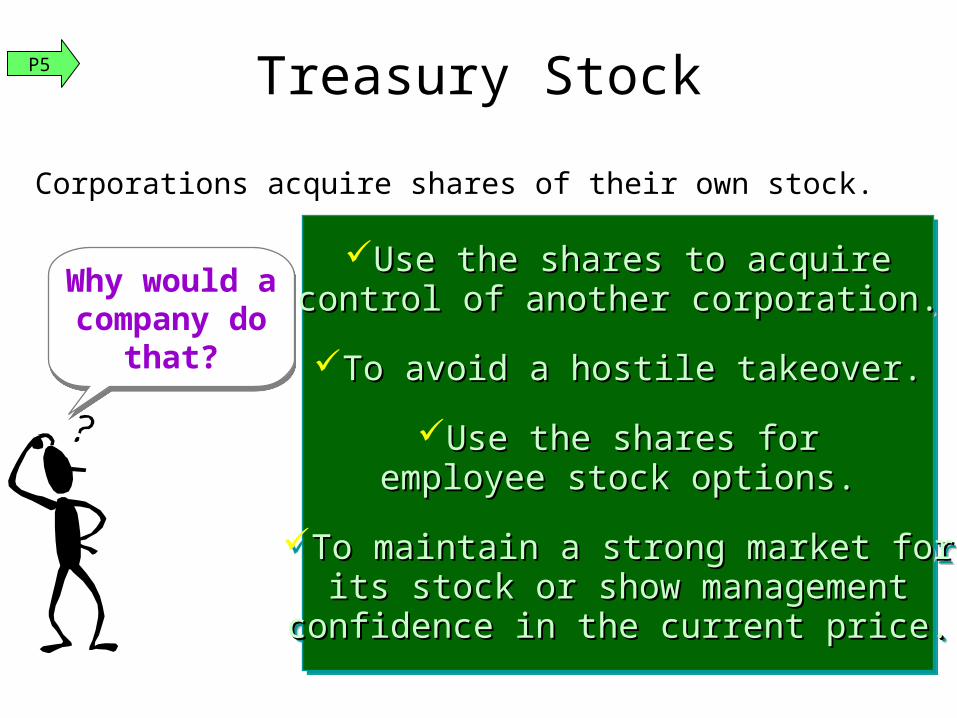

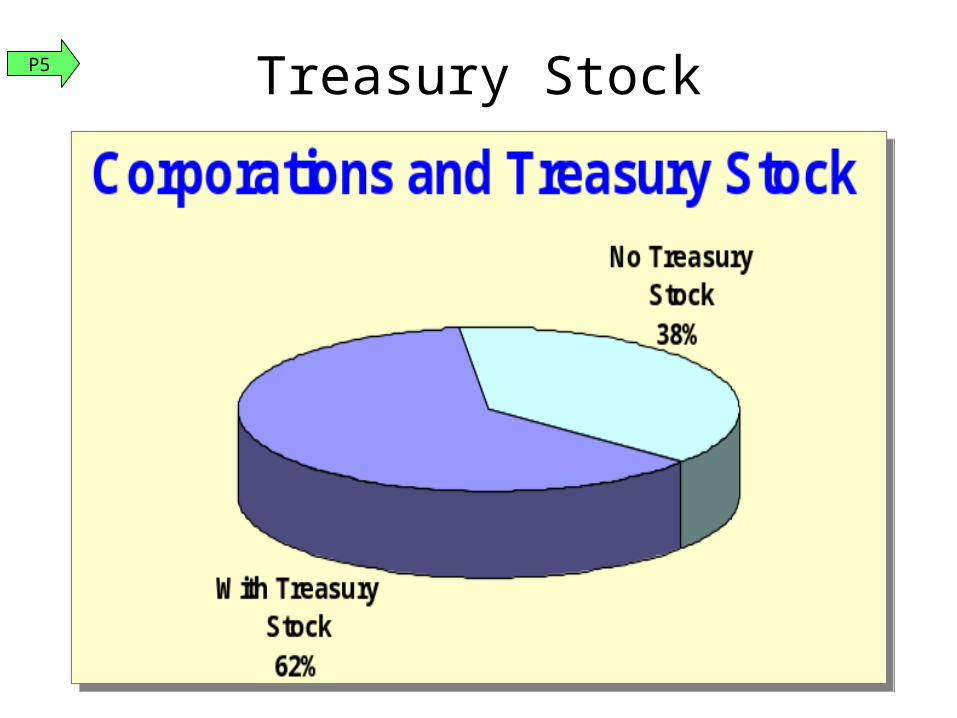

Corporations acquire shares of their own stock.

Why would acompany do

that?

Why would acompany do

that?

Use the shares to acquireUse the shares to acquirecontrol of another corporation.control of another corporation.

To avoid a hostile takeover.To avoid a hostile takeover.

Use the shares forUse the shares foremployee stock options.employee stock options.

To maintain a strong market forTo maintain a strong market forits stock or show managementits stock or show managementconfidence in the current price.confidence in the current price.

Use the shares to acquireUse the shares to acquirecontrol of another corporation.control of another corporation.

To avoid a hostile takeover.To avoid a hostile takeover.

Use the shares forUse the shares foremployee stock options.employee stock options.

To maintain a strong market forTo maintain a strong market forits stock or show managementits stock or show managementconfidence in the current price.confidence in the current price.

Treasury StockP5

Treasury StockP5

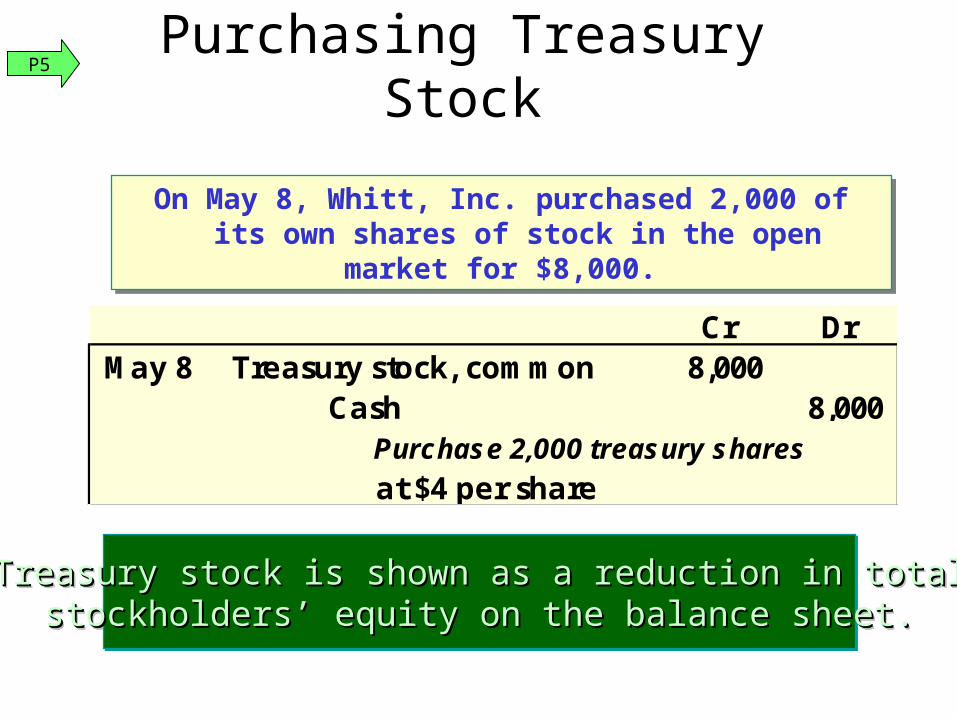

On May 8, Whitt, Inc. purchased 2,000 of its own shares of stock in the open market for $8,000.

On May 8, Whitt, Inc. purchased 2,000 of its own shares of stock in the open market for $8,000.

Purchasing Treasury Stock

Treasury stock is shown as a reduction in totalTreasury stock is shown as a reduction in totalstockholders’ equity on the balance sheet.stockholders’ equity on the balance sheet.

Treasury stock is shown as a reduction in totalTreasury stock is shown as a reduction in totalstockholders’ equity on the balance sheet.stockholders’ equity on the balance sheet.

Cr DrMay 8 Treasury stock, common 8,000

Cash 8,000 Purchase 2,000 treasury shares

at $4 per share

P5

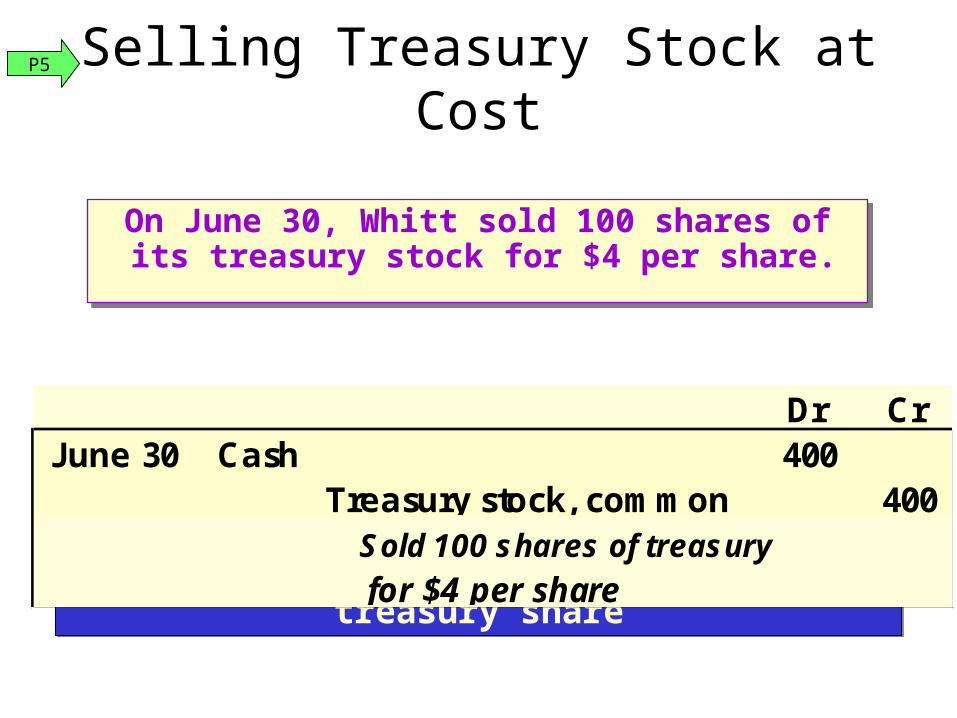

On June 30, Whitt sold 100 shares of its treasury stock for $4 per share.

On June 30, Whitt sold 100 shares of its treasury stock for $4 per share.

Selling Treasury Stock at Cost

$8,000 ÷ 2,000 shares = $4 cost per treasury share$8,000 ÷ 2,000 shares = $4 cost per treasury share

Dr CrJune 30 Cash 400

Treasury stock, common 400 Sold 100 shares of treasury

for $4 per share

P5

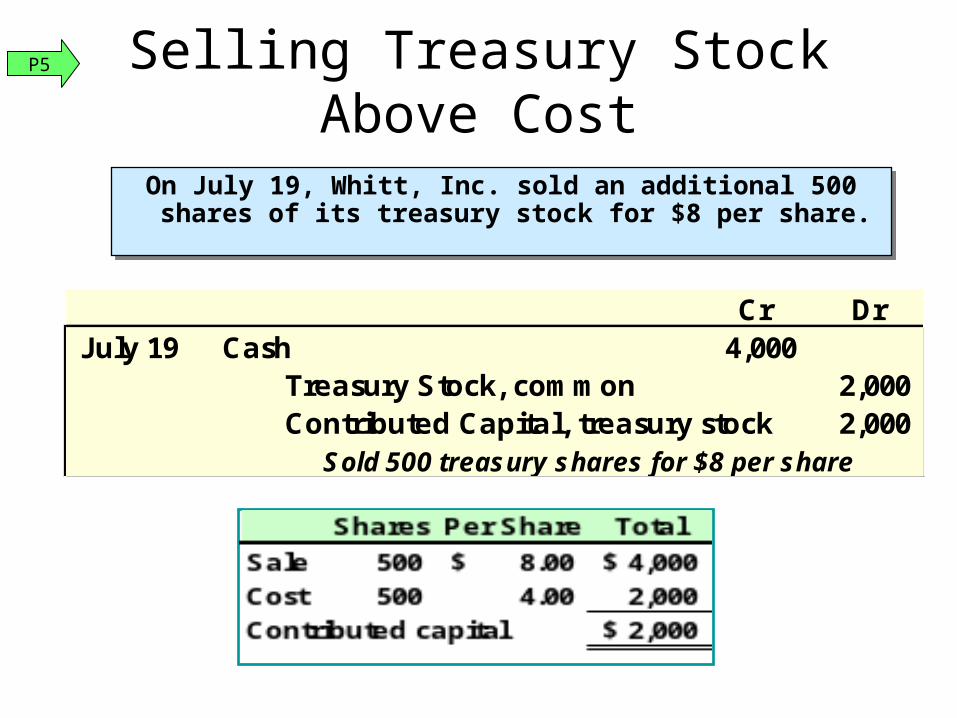

On July 19, Whitt, Inc. sold an additional 500 shares of its treasury stock for $8 per share.

On July 19, Whitt, Inc. sold an additional 500 shares of its treasury stock for $8 per share.

Selling Treasury Stock Above Cost

Cr DrJuly 19 Cash 4,000

Treasury Stock, common 2,000 Contributed Capital, treasury stock 2,000 Sold 500 treasury shares for $8 per share

P5

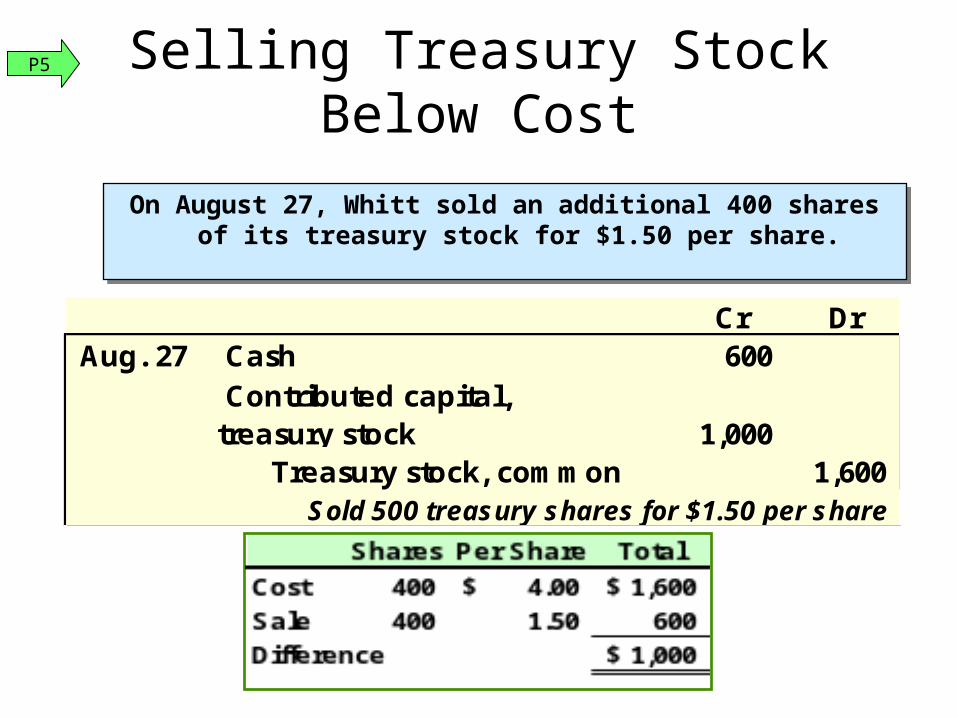

On August 27, Whitt sold an additional 400 shares of its treasury stock for $1.50 per share.

On August 27, Whitt sold an additional 400 shares of its treasury stock for $1.50 per share.

Selling Treasury Stock Below Cost

Cr DrAug. 27 Cash 600

1,000 Treasury stock, common 1,600 Sold 500 treasury shares for $1.50 per share

Contributed capital, treasury stock

P5

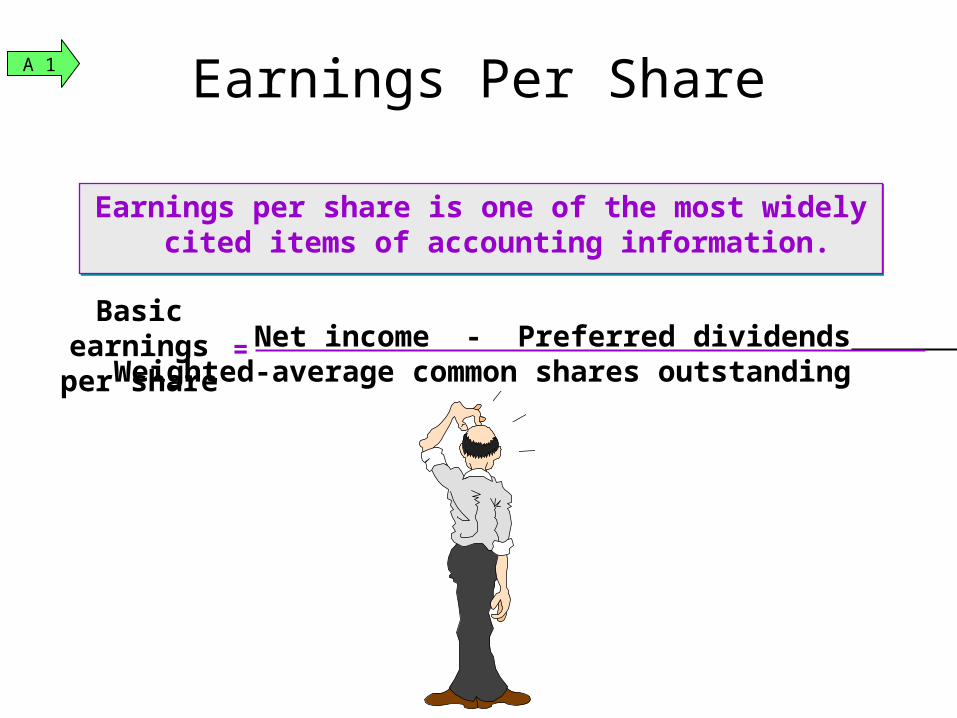

Earnings per share is one of the most widely cited items of accounting information.

Earnings per share is one of the most widely cited items of accounting information.

Earnings Per Share

Basicearningsper share

= Net income - Preferred dividends Weighted-average common shares outstanding

A 1

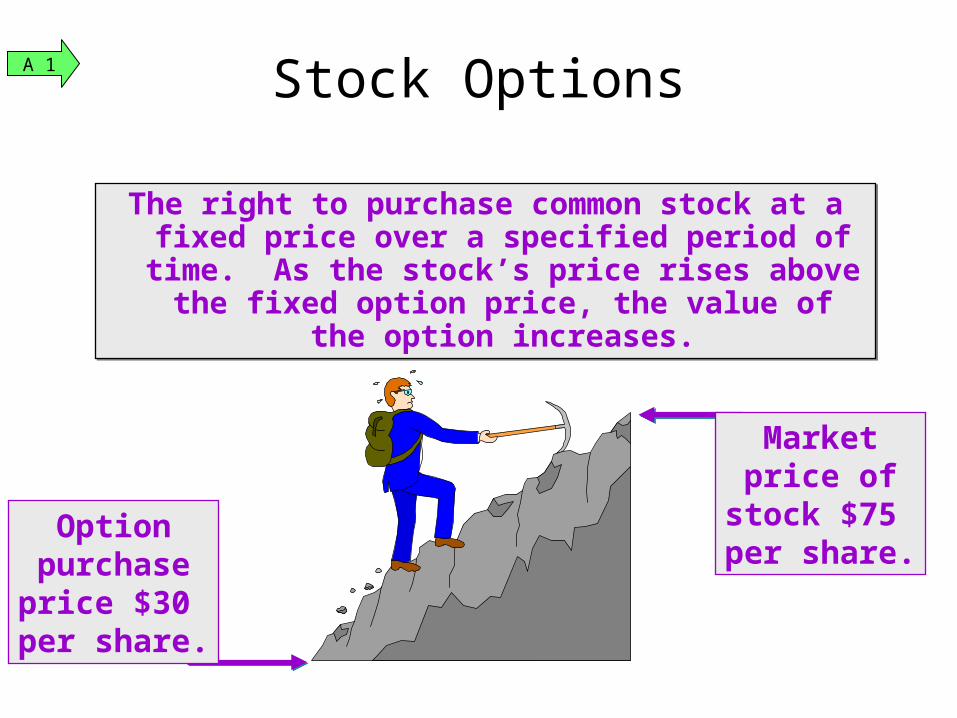

The right to purchase common stock at a fixed price over a specified period of time. As the

stock’s price rises above the fixed option price, the value of the option increases.

The right to purchase common stock at a fixed price over a specified period of time. As the

stock’s price rises above the fixed option price, the value of the option increases.

Optionpurchaseprice $30 per share.

Stock Options

Marketprice of

stock $75 per share.

A 1

Options are given to key employees to motivate them to:

focus on company performance,take a long-run perspective, andremain with the company.

Options are given to key employees to motivate them to:

focus on company performance,take a long-run perspective, andremain with the company.

Stock OptionsA 1