Embed Size (px)

Citation preview

Business OrganizationsBusiness Organizations

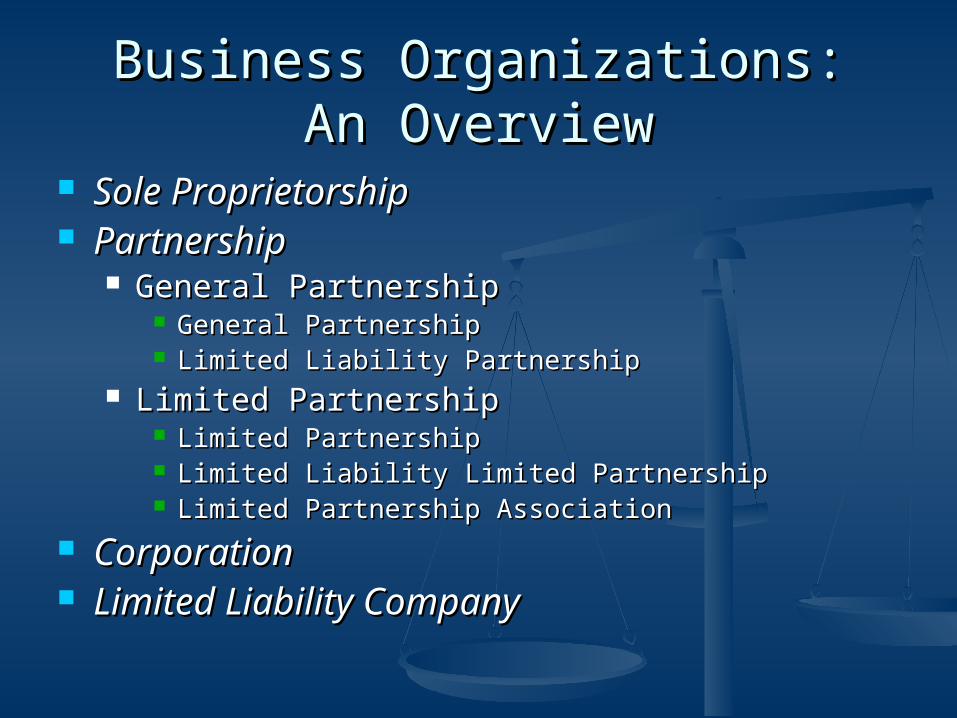

Business Organizations:Business Organizations:An OverviewAn Overview

Sole ProprietorshipSole Proprietorship PartnershipPartnership

General PartnershipGeneral Partnership General PartnershipGeneral Partnership Limited Liability PartnershipLimited Liability Partnership

Limited PartnershipLimited Partnership Limited PartnershipLimited Partnership Limited Liability Limited PartnershipLimited Liability Limited Partnership Limited Partnership AssociationLimited Partnership Association

CorporationCorporation Limited Liability CompanyLimited Liability Company

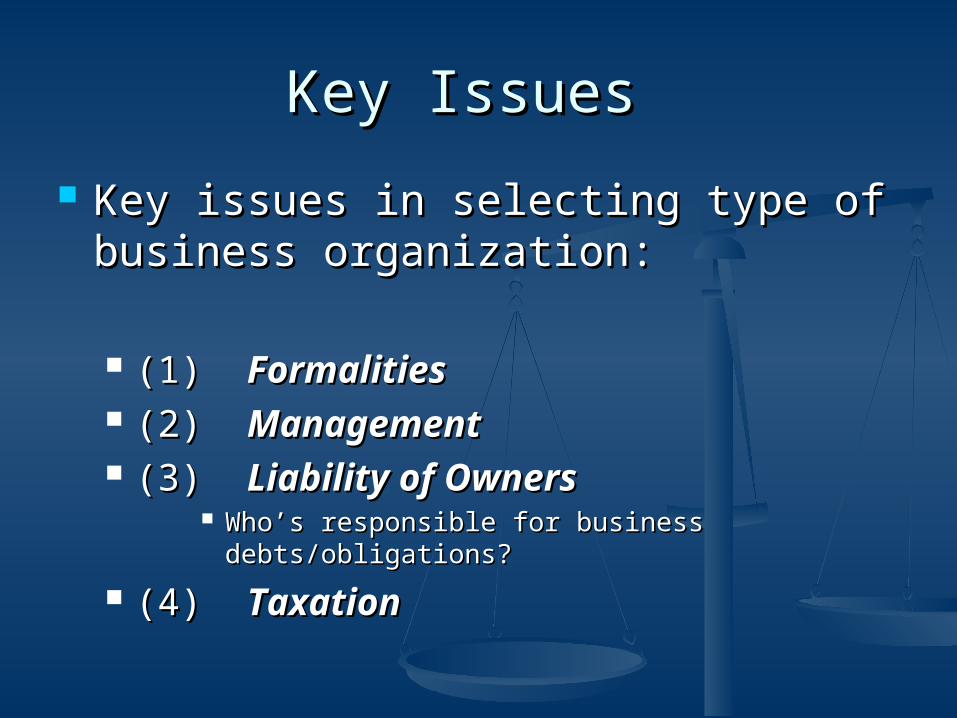

Key Issues Key Issues

Key issues in selecting type of Key issues in selecting type of business organization:business organization:

(1) (1) FormalitiesFormalities (2) (2) ManagementManagement (3) (3) Liability of OwnersLiability of Owners

Who’s responsible for business debts/obligations?Who’s responsible for business debts/obligations?

(4) (4) TaxationTaxation

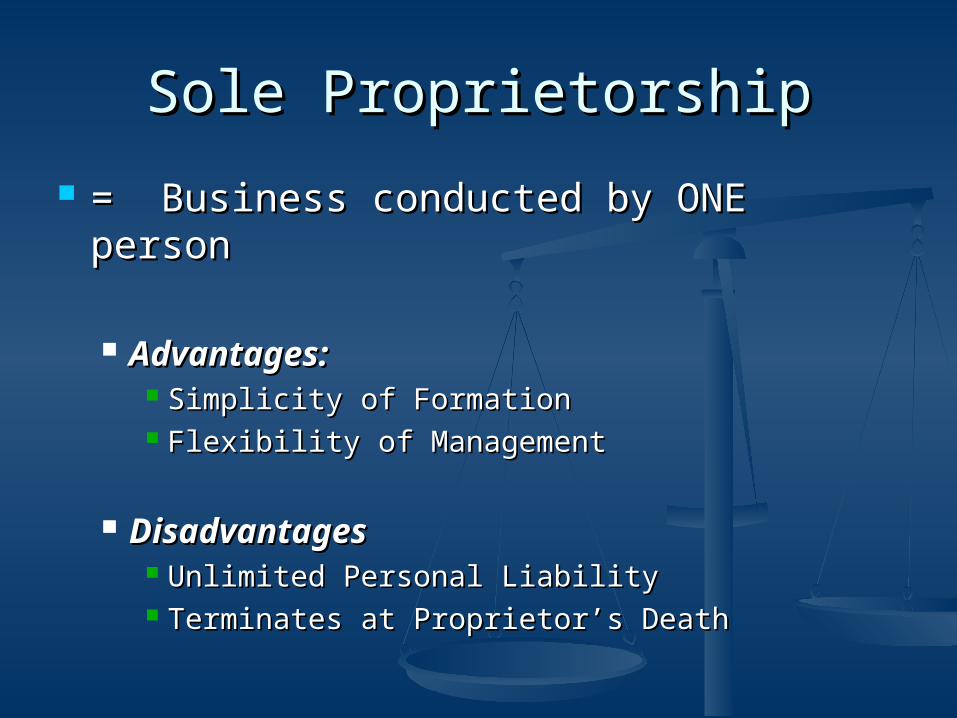

Sole ProprietorshipSole Proprietorship

= Business conducted by ONE person= Business conducted by ONE person

Advantages:Advantages: Simplicity of FormationSimplicity of Formation Flexibility of ManagementFlexibility of Management

DisadvantagesDisadvantages Unlimited Personal LiabilityUnlimited Personal Liability Terminates at Proprietor’s DeathTerminates at Proprietor’s Death

PartnershipPartnership

Association of two or more persons (including Association of two or more persons (including corporations, associations) for profitcorporations, associations) for profit

AdvantagesAdvantages Management rightsManagement rights

DisadvantagesDisadvantages Personal LiabilityPersonal Liability Terminates on death or withdrawal of partner(s)Terminates on death or withdrawal of partner(s)

Partnership FormsPartnership Forms

General PartnershipGeneral Partnership Limited Liability PartnershipLimited Liability Partnership

Limited PartnershipLimited Partnership Limited PartnershipLimited Partnership Limited Liability Limited PartnershipLimited Liability Limited Partnership Limited Partnership AssociationLimited Partnership Association

General PartnershipGeneral Partnership

In the traditional general partnership:In the traditional general partnership:

All partners manageAll partners manage

ANDAND

All partners have personal liabilityAll partners have personal liability

Limited Liability PartnershipLimited Liability PartnershipA General Partnership FormA General Partnership Form

Partnership without liability for Partnership without liability for negligence or malfeasance of other negligence or malfeasance of other partnerspartners

General PartnersGeneral Partners ManageManage Liable for partnership contracts & own negligenceLiable for partnership contracts & own negligence

Some states, known as full-shield states, provide Some states, known as full-shield states, provide partners of an LLP personal liability protections partners of an LLP personal liability protections from all obligations of the partnership, whether from all obligations of the partnership, whether arising in tort or contractarising in tort or contract

Limited PartnershipsLimited Partnerships

In the traditional limited partnership:In the traditional limited partnership:

General PartnersGeneral Partners Manage and have personal liabilityManage and have personal liability

Limited PartnersLimited Partners Investors without personal liabilityInvestors without personal liability

New Forms ofNew Forms ofLimited PartnershipsLimited Partnerships

Limited Liability Limited PartnershipLimited Liability Limited Partnership General PartnersGeneral Partners

ManagersManagers Limited PartnersLimited Partners

Investors who manageInvestors who manage LP vs. LLLPLP vs. LLLP::

Neither general or limited partners have vicarious Neither general or limited partners have vicarious liability for the negligence or malfeasance of other liability for the negligence or malfeasance of other partners partners

Partners are only liable for partnership contract and Partners are only liable for partnership contract and their own negligence or malfeasancetheir own negligence or malfeasance

Limited Partnership AssociationLimited Partnership Association No personal liability of members or managersNo personal liability of members or managers

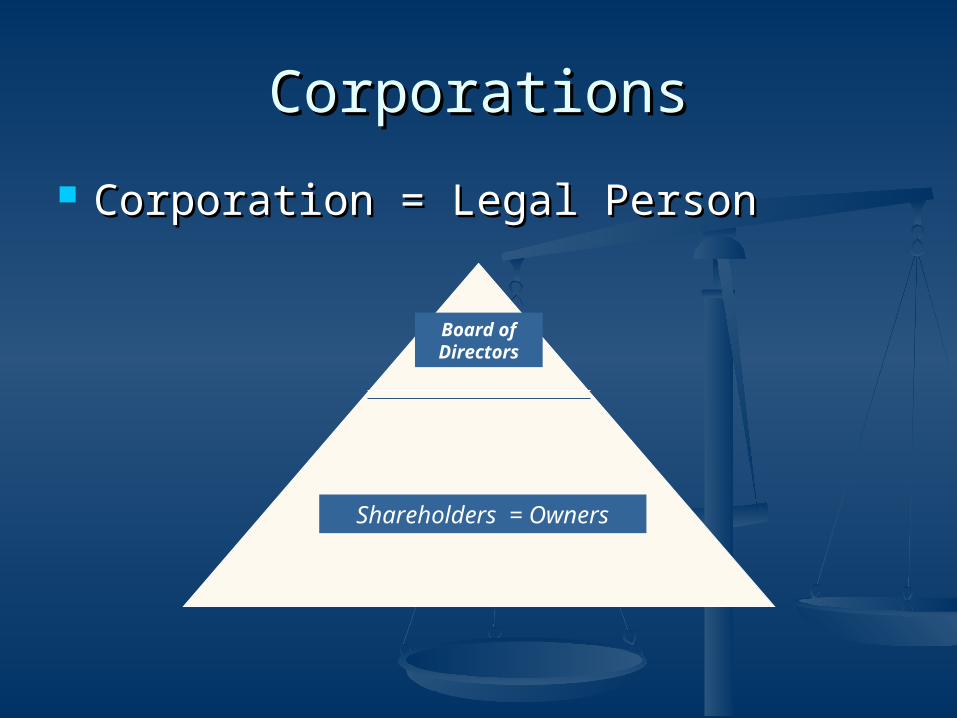

CorporationsCorporations

Corporation = Legal PersonCorporation = Legal Person

Board of Directors

Shareholders = Owners

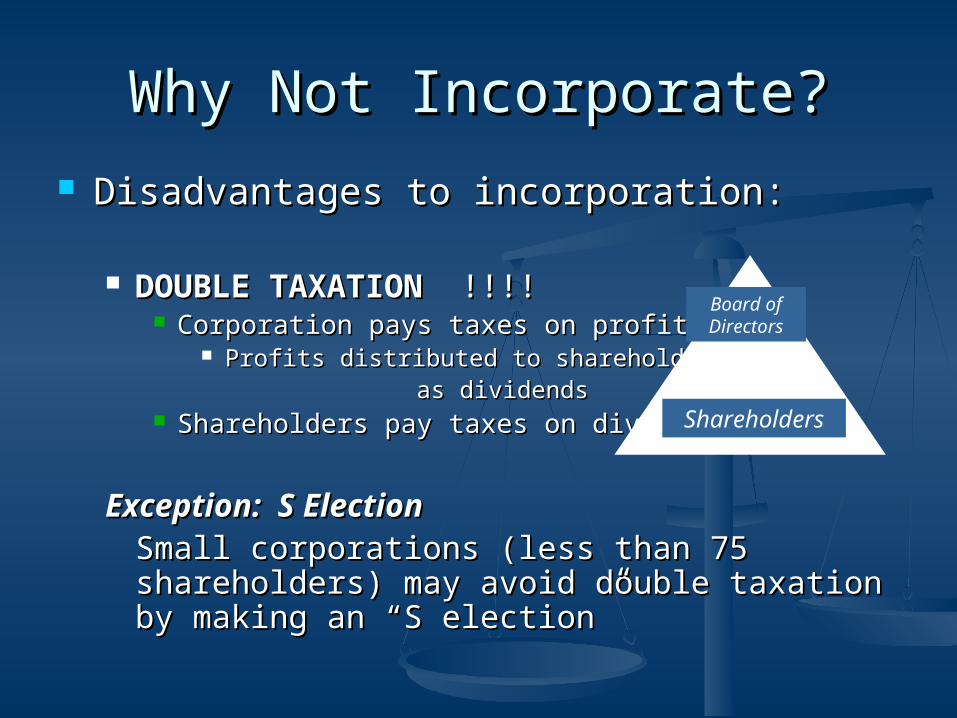

Why Not Incorporate?Why Not Incorporate?

Disadvantages to incorporation:Disadvantages to incorporation:

DOUBLE TAXATIONDOUBLE TAXATION !!!! !!!! Corporation pays taxes on profitsCorporation pays taxes on profits

Profits distributed to shareholders Profits distributed to shareholders as dividendsas dividends

Shareholders pay taxes on dividendsShareholders pay taxes on dividends

Exception: S ElectionException: S ElectionSmall corporations (less than 75 shareholders) Small corporations (less than 75 shareholders) may avoid double taxation by making an “S may avoid double taxation by making an “S election” election”

Board of Directors

Shareholders

Corporate CharacteristicsCorporate Characteristics

Advantages of incorporation:Advantages of incorporation:(identifying characteristics of a (identifying characteristics of a

corporation)corporation)

Continuity of LifeContinuity of Life Centralization of ManagementCentralization of Management Limited Liability for ShareholdersLimited Liability for Shareholders Free Transferability of InterestsFree Transferability of Interests

Sole ProprietorshipsSole ProprietorshipsBusiness Conducted by One PersonBusiness Conducted by One Person

FormationFormation Begin businessBegin business

General formation requirements for all business General formation requirements for all business forms:forms:

Registration of Assumed Business Name (with SOS)Registration of Assumed Business Name (with SOS) Note: Not required in NevadaNote: Not required in Nevada Assumed Business NameAssumed Business Name (avoids deceptively similar (avoids deceptively similar

names)names) Information:Information:

NameName Type of businessType of business Counties of OperationCounties of Operation Name/address of applicantName/address of applicant

Limited Liability CompanyLimited Liability Company Managers without personal liabilityManagers without personal liability

Advantages:Advantages: All members manageAll members manage Limited liability (with proper liability insurance)Limited liability (with proper liability insurance) Taxed once Taxed once

Disadvantages:Disadvantages: Limited duration (some states)Limited duration (some states) Limited transferability of interestsLimited transferability of interests

An LLC offers the advantages of a An LLC offers the advantages of a partnership (management + taxation)partnership (management + taxation)

and the advantages of a corporation (limited liability)and the advantages of a corporation (limited liability)

Licensing RequirementsLicensing Requirementsfor all business entitiesfor all business entities

LicensingLicensing

Business LicensesBusiness Licenses Required by Secretary of State and CountyRequired by Secretary of State and County

Purposes:Purposes: Regulation of businessesRegulation of businesses Safeguards for consumersSafeguards for consumers Regulate quality and standardsRegulate quality and standards Protect existing business interestsProtect existing business interests

Sales Tax LicensesSales Tax Licenses Purpose: assess and collect taxesPurpose: assess and collect taxes

LiabilityLiabilitySole ProprietorshipsSole Proprietorships

Who is liable for the debts and obligations of the Who is liable for the debts and obligations of the sole proprietorship?sole proprietorship? Proprietor Proprietor

Business LiabilityBusiness Liability: business assets (desks, money): business assets (desks, money) Personal LiabilityPersonal Liability: personal assets (home, car, : personal assets (home, car, etcetc.).)

Limiting Personal LiabilityLimiting Personal Liability ContractsContracts can limit personal liability for debts: can limit personal liability for debts:

““obligations due on or created by the contract, or a breach obligations due on or created by the contract, or a breach thereof, will be limited to and payable solely from the thereof, will be limited to and payable solely from the business’ assets” OR “personal assets of proprietor shall business’ assets” OR “personal assets of proprietor shall not be liable for debts created by this contract, or a not be liable for debts created by this contract, or a breach thereof.”breach thereof.”

Bonding and InsuranceBonding and Insurance BondingBonding: contract will be performed: contract will be performed InsuranceInsurance: liability (property damage, theft): liability (property damage, theft) Disadvantages: Insurance is generally not available to high Disadvantages: Insurance is generally not available to high

risk or new businessesrisk or new businesses

Taxation ConsiderationsTaxation ConsiderationsSole ProprietorshipsSole Proprietorships

Profits = Personal IncomeProfits = Personal Income

Advantages:Advantages: Individual tax rates are generally lower than Individual tax rates are generally lower than

business rates business rates Business income/losses may offset other Business income/losses may offset other

incomeincome

Tax Identification Number:Tax Identification Number: A businesses should obtain a tax ID number A businesses should obtain a tax ID number

when hiring employees when hiring employees IRS Form SS-4IRS Form SS-4

TerminationTerminationSole ProprietorshipsSole Proprietorships

TerminationTermination Upon death of proprietorUpon death of proprietor

Termination is automatic upon death of ownerTermination is automatic upon death of owner

Upon saleUpon sale Sales Price: Sales Price:

Business Assets PLUS Goodwill (reputation)Business Assets PLUS Goodwill (reputation) Goodwill is generally based upon:Goodwill is generally based upon: (1) comparison with other business sales(1) comparison with other business sales (2) business income for specified time ((2) business income for specified time (e.g.,e.g., 10 10

yrs)yrs)

PartnershipsPartnerships

Association of two or more persons or Association of two or more persons or entities who operate a business for profitentities who operate a business for profit

Governed by:Governed by: Partnership Agreement ORPartnership Agreement OR Uniform Partnership Act (1914) – UPA Uniform Partnership Act (1914) – UPA

Nevada has adopted a version of the UPANevada has adopted a version of the UPA Revised Uniform Partnership Act (1997) Revised Uniform Partnership Act (1997)

RUPARUPA

Traditional CharacteristicsTraditional CharacteristicsPartnershipsPartnerships

Partnership FormsPartnership Forms

General PartnershipsGeneral Partnerships General PartnershipGeneral Partnership Limited Liability PartnershipLimited Liability Partnership

Limited PartnershipsLimited Partnerships Limited PartnershipLimited Partnership Limited Liability Limited PartnershipLimited Liability Limited Partnership Limited Partnership AssociationLimited Partnership Association

General PartnershipsGeneral PartnershipsThe Traditional PartnershipThe Traditional Partnership

Requires NO formalitiesRequires NO formalities

FormationFormation Voluntary Agreement (to co-own business)Voluntary Agreement (to co-own business) Registration of Assumed Business Name Registration of Assumed Business Name (not in NV)(not in NV) Foreign Registration (if operating in another state)Foreign Registration (if operating in another state)

State in which the partnership is not formedState in which the partnership is not formed Regulates and creates revenueRegulates and creates revenue

LicensesLicenses Business LicensesBusiness Licenses Sales Tax LicensesSales Tax Licenses

Partnership AgreementPartnership Agreement Cornerstone of partnership relationshipCornerstone of partnership relationship

AgencyAgencyPartnershipPartnership

Apparent AuthorityApparent Authority:: Each partner has the authority to bind the partnership to Each partner has the authority to bind the partnership to

obligations obligations within the scope of the partnership businesswithin the scope of the partnership business Purpose: protect third parties Purpose: protect third parties Apparent authority can be limited by:Apparent authority can be limited by:

Partnership AgreementPartnership Agreement Statement of Partnership Authority (filed with SOS)Statement of Partnership Authority (filed with SOS)

Actual Authority (Express Authority)Actual Authority (Express Authority) Authority granted by:Authority granted by:

Partnership AgreementPartnership Agreement Majority VoteMajority Vote

Exceeding actual authority can lead to expulsion or suit Exceeding actual authority can lead to expulsion or suit for damages caused by using excess authorityfor damages caused by using excess authority

ManagementManagementPartnershipPartnership

General partners have General partners have (1) (1) equal management rightsequal management rights

Note: Management is often delegated to a small groupNote: Management is often delegated to a small group (2) (2) equal participation rightsequal participation rights (voting rights) (voting rights)

Note: The Partnership Agreement can alter the management and voting rightsNote: The Partnership Agreement can alter the management and voting rights

VotingVoting Decisions made by majority voteDecisions made by majority vote

Voting violations = void transactionsVoting violations = void transactions Except:Except:

Votes affecting continuation of business (Votes affecting continuation of business (e.ge.g., selling ., selling business)business)

Partnership activities beyond the partnership agreementPartnership activities beyond the partnership agreement

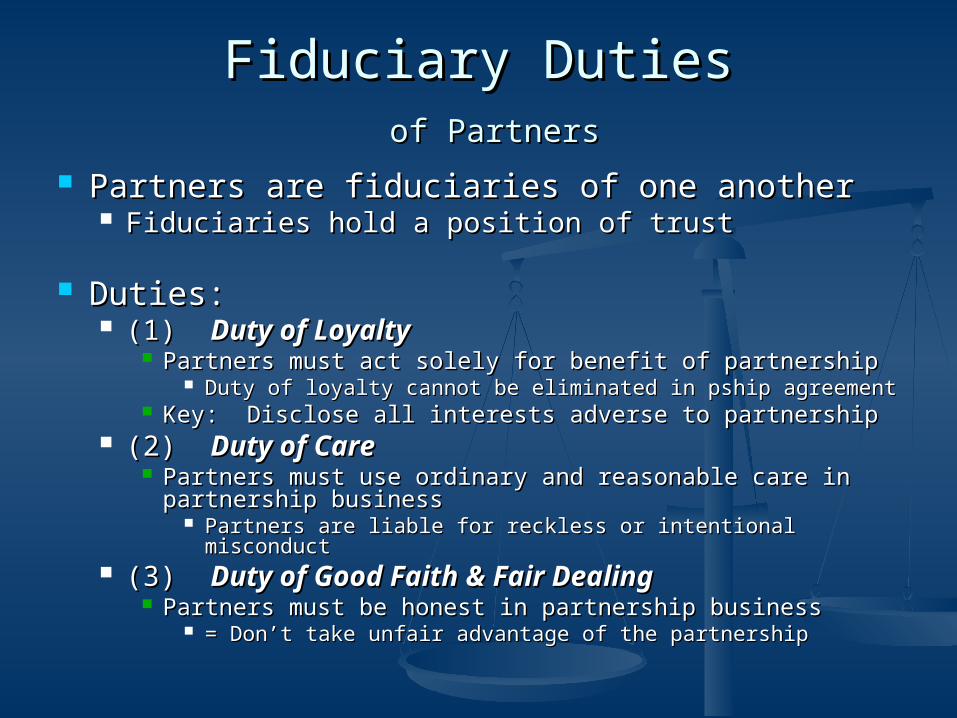

Fiduciary DutiesFiduciary Duties of Partnersof Partners

Partners are fiduciaries of one anotherPartners are fiduciaries of one another Fiduciaries hold a position of trustFiduciaries hold a position of trust

Duties:Duties: (1) (1) Duty of LoyaltyDuty of Loyalty

Partners must act solely for benefit of partnershipPartners must act solely for benefit of partnership Duty of loyalty cannot be eliminated in pship agreementDuty of loyalty cannot be eliminated in pship agreement

Key: Disclose all interests adverse to partnershipKey: Disclose all interests adverse to partnership (2) (2) Duty of CareDuty of Care

Partners must use ordinary and reasonable care in Partners must use ordinary and reasonable care in partnership businesspartnership business

Partners are liable for reckless or intentional misconductPartners are liable for reckless or intentional misconduct (3) (3) Duty of Good Faith & Fair DealingDuty of Good Faith & Fair Dealing

Partners must be honest in partnership businessPartners must be honest in partnership business = Don’t take unfair advantage of the partnership= Don’t take unfair advantage of the partnership

LiabilityLiabilityof Partnersof Partners

Business Liability vs. Personal LiabilityBusiness Liability vs. Personal Liability Business Liability:Business Liability:

Use of business assets to pay partnership debtsUse of business assets to pay partnership debts Personal Liability:Personal Liability:

Use of personal assets to pay partnership debtsUse of personal assets to pay partnership debts Exhaustion RuleExhaustion Rule (R.U.P.A.) (R.U.P.A.)

Business assets must be used to pay business obligations Business assets must be used to pay business obligations before personal assets can be takenbefore personal assets can be taken

Each partner is personally liable for all:Each partner is personally liable for all: (1) Contract obligations of partnership and (1) Contract obligations of partnership and (2) Tort obligations of partnership(2) Tort obligations of partnership

Note: Liability is equal unless partnership agreement specifies Note: Liability is equal unless partnership agreement specifies otherwiseotherwise

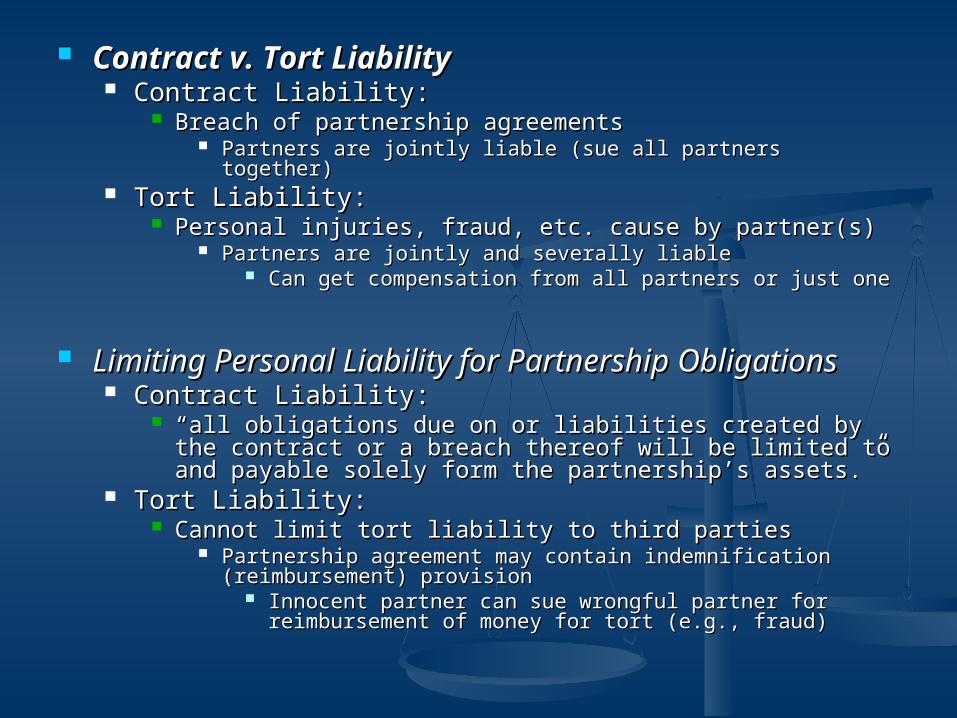

Contract v. Tort LiabilityContract v. Tort Liability Contract Liability:Contract Liability:

Breach of partnership agreementsBreach of partnership agreements Partners are jointly liable (sue all partners together)Partners are jointly liable (sue all partners together)

Tort Liability:Tort Liability: Personal injuries, fraud, etc. cause by partner(s)Personal injuries, fraud, etc. cause by partner(s)

Partners are jointly and severally liablePartners are jointly and severally liable Can get compensation from all partners or just oneCan get compensation from all partners or just one

Limiting Personal Liability for Partnership Limiting Personal Liability for Partnership ObligationsObligations Contract Liability:Contract Liability:

““all obligations due on or liabilities created by the contract all obligations due on or liabilities created by the contract or a breach thereof will be limited to and payable solely or a breach thereof will be limited to and payable solely form the partnership’s assets.”form the partnership’s assets.”

Tort Liability:Tort Liability: Cannot limit tort liability to third partiesCannot limit tort liability to third parties

Partnership agreement may contain indemnification Partnership agreement may contain indemnification (reimbursement) provision(reimbursement) provision

Innocent partner can sue wrongful partner for Innocent partner can sue wrongful partner for reimbursement of money for tort (e.g., fraud)reimbursement of money for tort (e.g., fraud)

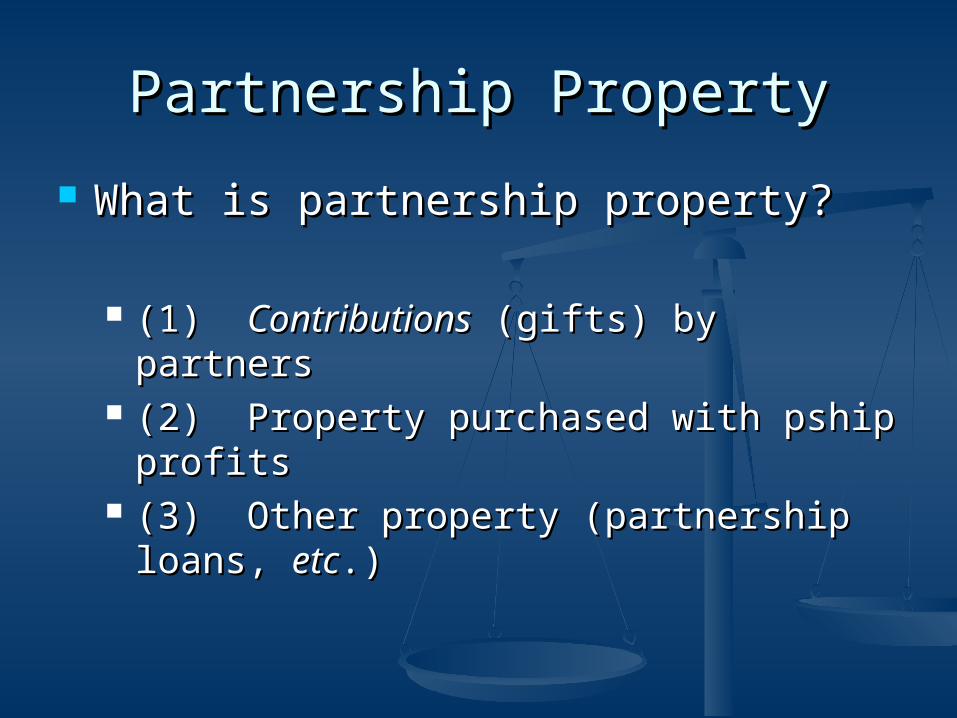

Partnership PropertyPartnership Property

What is partnership property?What is partnership property?

(1) (1) ContributionsContributions (gifts) by partners (gifts) by partners (2) Property purchased with pship (2) Property purchased with pship

profitsprofits (3) Other property (partnership loans, (3) Other property (partnership loans,

etcetc.).)

Partnership PropertyPartnership Property

Contributions = partnership capitalContributions = partnership capital Investments by individual partnersInvestments by individual partners Contributions are owned by partnershipContributions are owned by partnership

Partners cannot withdraw their contributions until Partners cannot withdraw their contributions until partnership is dissolvedpartnership is dissolved

Pship Interest = Contributions + % Profits – LiabilitiesPship Interest = Contributions + % Profits – Liabilities

Based upon partner’s investment (capital contribution)Based upon partner’s investment (capital contribution) E.g. Partner A invests 40% of partnership moneyE.g. Partner A invests 40% of partnership money= 40% partnership interest (40% profits/losses)= 40% partnership interest (40% profits/losses) Dollar value of all contributions should be set in pship Dollar value of all contributions should be set in pship

agreementagreement DefaultDefault: partnership profits and losses are divided equally: partnership profits and losses are divided equally

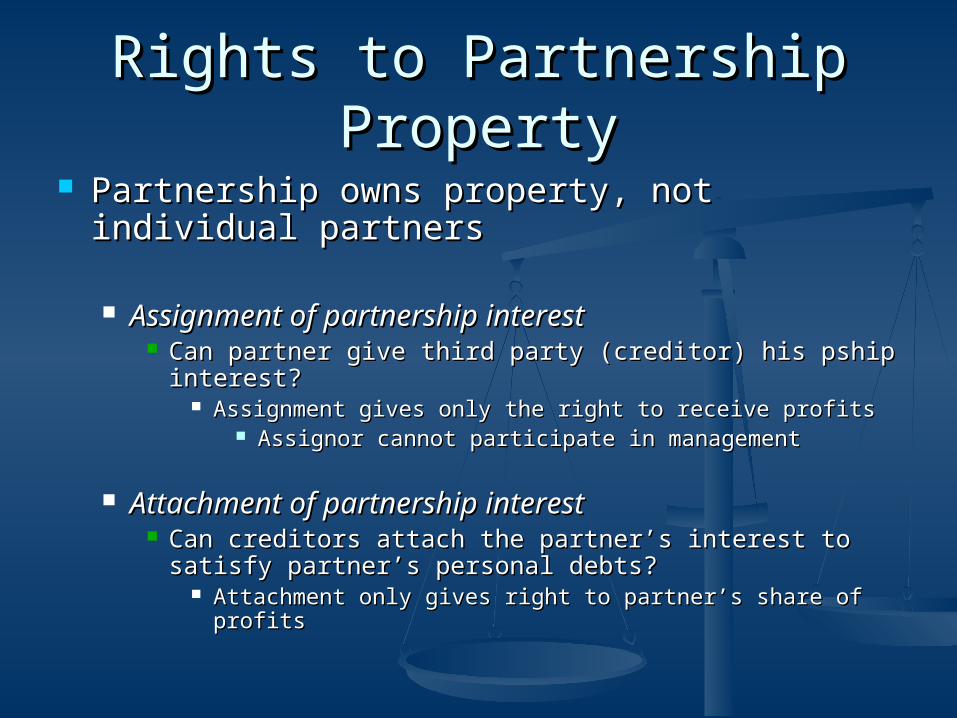

Rights to Partnership PropertyRights to Partnership Property

Partnership owns property, not individual Partnership owns property, not individual partnerspartners

Assignment of partnership interestAssignment of partnership interest Can partner give third party (creditor) his pship Can partner give third party (creditor) his pship

interest?interest? Assignment gives only the right to receive profitsAssignment gives only the right to receive profits

Assignor cannot participate in managementAssignor cannot participate in management

Attachment of partnership interestAttachment of partnership interest Can creditors attach the partner’s interest to satisfy Can creditors attach the partner’s interest to satisfy

partner’s personal debts?partner’s personal debts? Attachment only gives right to partner’s share of profitsAttachment only gives right to partner’s share of profits

Taxation ConsiderationsTaxation Considerations

Partnership profits and lossesPartnership profits and losses = personal income of partners= personal income of partners

Advantages:Advantages: (1) profits taxes once(1) profits taxes once (2) profits taxed at lower individual rates(2) profits taxed at lower individual rates (3) partnership losses offsets other personal (3) partnership losses offsets other personal

incomeincome

Partnership must file an informational tax returnPartnership must file an informational tax return

Termination of PartnershipTermination of Partnership

Partnerships have to :Partnerships have to :

DissolveDissolve Change in the partnership associationChange in the partnership association

E.gE.g., partners leaves/joins partnership., partners leaves/joins partnership

Wind UpWind Up End businessEnd business

E.gE.g., collect accounts receivables, pay debts., collect accounts receivables, pay debts

Options to TerminationOptions to Termination

R.U.P.A. TerminationR.U.P.A. Termination = Partnership Reorganization= Partnership Reorganization

Provides remaining partners buyout exiting Provides remaining partners buyout exiting partner’s interestpartner’s interest

Buyout priceBuyout price = partner’s interest = partner’s interest (contribution + profits – liabilities)(contribution + profits – liabilities)

OR Price established in Partnership AgreementOR Price established in Partnership Agreement

Partnership AgreementPartnership Agreement Partnership agreement may allow Partnership agreement may allow

continuation of partnership after continuation of partnership after dissolutiondissolution

Winding UpWinding Up

= concluding partnership business= concluding partnership business

Completing existing partnership contractsCompleting existing partnership contracts Collecting accounts receivable (due)Collecting accounts receivable (due) Liquidating partnership assetsLiquidating partnership assets

PLUSPLUS

Distributing profitsDistributing profits

Limited Liability PartnershipsLimited Liability PartnershipsDefinedDefined

Managers without vicarious liabilityManagers without vicarious liability = General Partnership with liability protections= General Partnership with liability protections

PartnersPartners All partners manageAll partners manage All partners are personally liable for:All partners are personally liable for:

Partnership contractsPartnership contracts Own Negligence/malfeasanceOwn Negligence/malfeasance

BUT NOTBUT NOT Negligence or malfeasance of other partnersNegligence or malfeasance of other partners

Unless they supervised or participated in itUnless they supervised or participated in it

Full-Shield StatesFull-Shield States Offer statutory protection for all partnership obligations, Offer statutory protection for all partnership obligations,

whether arising in tort or contractwhether arising in tort or contract

LiabilityLiabilityLimited Liability PartnershipsLimited Liability Partnerships

Liability = legal responsibilityLiability = legal responsibility

Business LiabilityBusiness Liability All partners are liable to the amount of their investment All partners are liable to the amount of their investment

for the contractual obligations PLUSfor the contractual obligations PLUS

Personal LiabilityPersonal Liability Partners liable for their own negligence/malfeasancePartners liable for their own negligence/malfeasance

Partial-Shield StatesPartial-Shield States: personally liable for contractual : personally liable for contractual obligations of partnershipobligations of partnership

NOT liable for negligence/malfeasance of their partnersNOT liable for negligence/malfeasance of their partners Unless they supervised or participated Unless they supervised or participated

Limited Liability Limited PartnershipsLimited Liability Limited Partnerships

Hybrid: LLP & LPHybrid: LLP & LP Key: All partners manage w/o vicarious liabilityKey: All partners manage w/o vicarious liability

General Partners = ManagersGeneral Partners = Managers Limited Partners = InvestorsLimited Partners = Investors

LiabilityLiability Partners are liable for:Partners are liable for:

Partnership contractsPartnership contracts Own negligence/malfeasanceOwn negligence/malfeasance

Not liable for negligence/malfeasance of other Not liable for negligence/malfeasance of other partnerspartners

Limited Liability PartnershipsLimited Liability PartnershipsFormationFormation

RequirementsRequirements Register assumed business name/LLPRegister assumed business name/LLP Obtain required business/professional licenses Obtain required business/professional licenses

and permits (county/state)and permits (county/state) Draft a comprehensive partnership agreementDraft a comprehensive partnership agreement Consult tax advisorConsult tax advisor

Apply for a sales tax permit, if goods will be soldApply for a sales tax permit, if goods will be sold Apply for tax identification number with the IRS/stateApply for tax identification number with the IRS/state

Establish employee withholding as well as Establish employee withholding as well as unemployment/workers’ compensation unemployment/workers’ compensation coveragecoverage

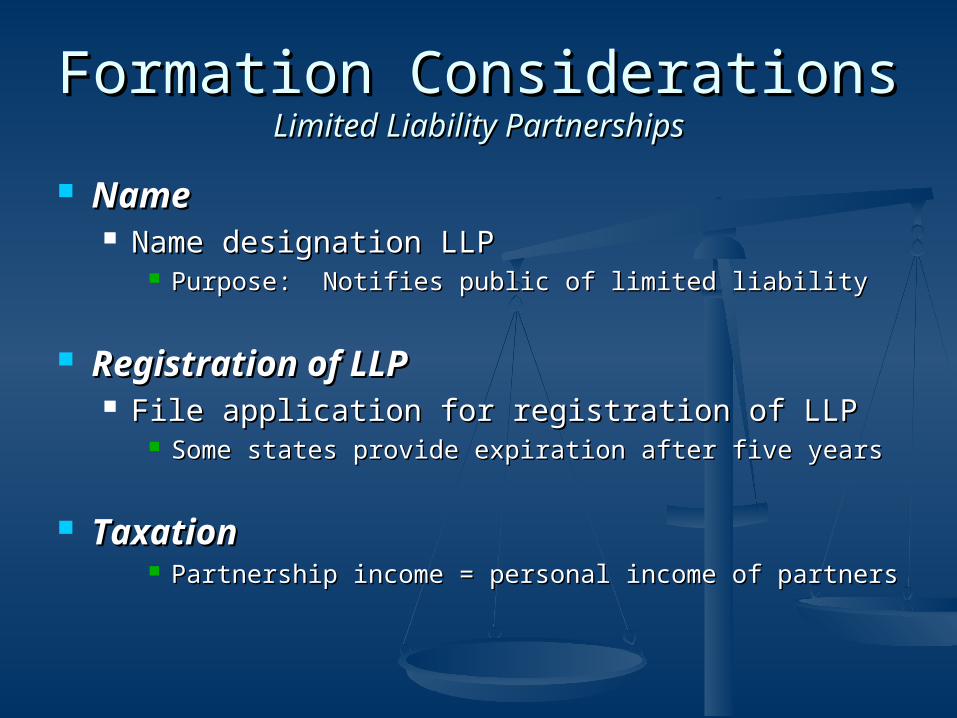

Formation ConsiderationsFormation ConsiderationsLimited Liability PartnershipsLimited Liability Partnerships

NameName Name designation LLPName designation LLP

Purpose: Notifies public of limited liabilityPurpose: Notifies public of limited liability

Registration of LLPRegistration of LLP File application for registration of LLPFile application for registration of LLP

Some states provide expiration after five yearsSome states provide expiration after five years

TaxationTaxation Partnership income = personal income of partnersPartnership income = personal income of partners

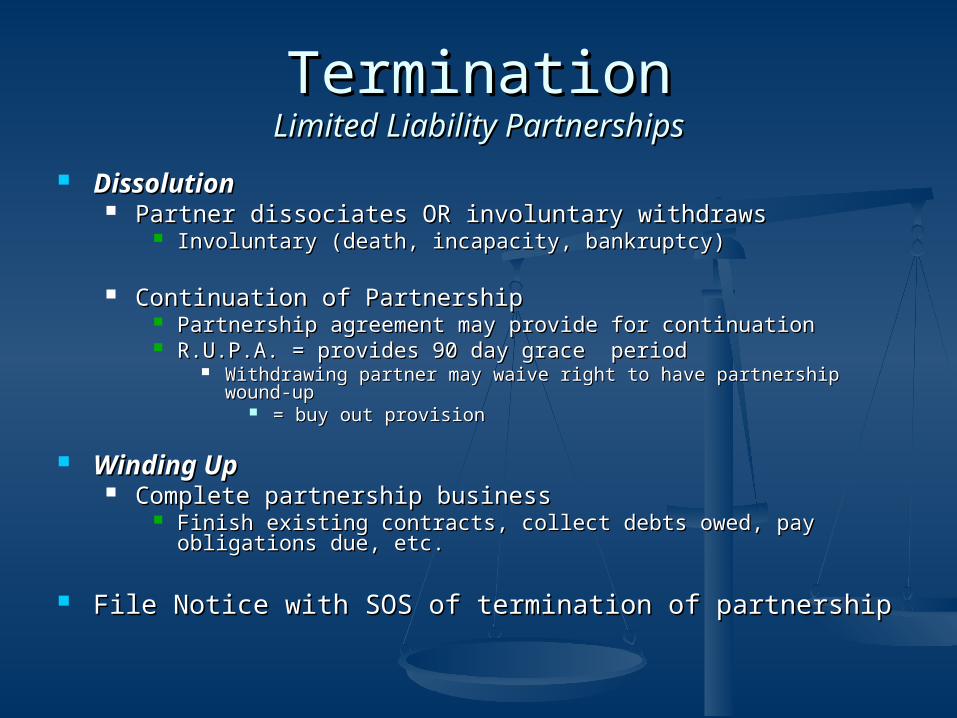

TerminationTerminationLimited Liability PartnershipsLimited Liability Partnerships

DissolutionDissolution Partner dissociates OR involuntary withdrawsPartner dissociates OR involuntary withdraws

Involuntary (death, incapacity, bankruptcy)Involuntary (death, incapacity, bankruptcy)

Continuation of PartnershipContinuation of Partnership Partnership agreement may provide for continuationPartnership agreement may provide for continuation R.U.P.A. = provides 90 day grace periodR.U.P.A. = provides 90 day grace period

Withdrawing partner may waive right to have partnership wound-upWithdrawing partner may waive right to have partnership wound-up = buy out provision= buy out provision

Winding UpWinding Up Complete partnership businessComplete partnership business

Finish existing contracts, collect debts owed, pay obligations due, Finish existing contracts, collect debts owed, pay obligations due, etc.etc.

File Notice with SOS of termination of partnershipFile Notice with SOS of termination of partnership

PartnershipsPartnershipsLiability Protection EvolutionLiability Protection Evolution

Association of two or more persons or entities Association of two or more persons or entities

who operate a business for profitwho operate a business for profit

Forms of PartnershipForms of Partnership General PartnershipGeneral Partnership

(Limited Liability Partnership)(Limited Liability Partnership) Limited PartnershipLimited Partnership

(Limited Liability Limited Partnership)(Limited Liability Limited Partnership) (Limited Partnership Association)(Limited Partnership Association)

Limited PartnershipsLimited PartnershipsFormsForms

Limited PartnershipsLimited Partnerships General Partners: Managers w/ personal liabilityGeneral Partners: Managers w/ personal liability Limited Partners: Investors w/o personal liabilityLimited Partners: Investors w/o personal liability

Limited Liability Limited PartnershipsLimited Liability Limited Partnerships General Partners: ManagersGeneral Partners: Managers Limited Partners: InvestorsLimited Partners: Investors Liability only for partnership contracts and own Liability only for partnership contracts and own

negligence/malfeasancenegligence/malfeasance No personal liability for the negligence/malfeasance of No personal liability for the negligence/malfeasance of

other partnersother partners

Limited Partnership AssociationsLimited Partnership Associations No personal liability of partnersNo personal liability of partners

Limited PartnershipsLimited PartnershipsDefinitionDefinition

An association of two or more persons An association of two or more persons carrying on a business as carrying on a business as

co-owners for profit with:co-owners for profit with:

(1)(1) ManagersManagersOne or more general partners One or more general partners

(2)(2) InvestorsInvestorsOne or more limited partners One or more limited partners

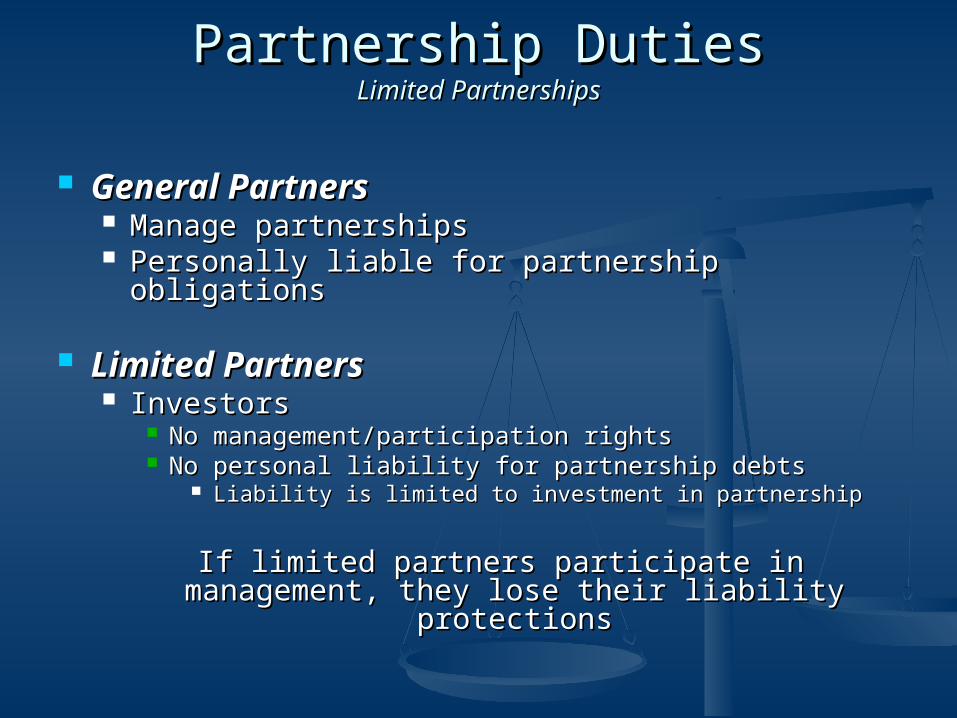

Partnership DutiesPartnership DutiesLimited PartnershipsLimited Partnerships

General PartnersGeneral Partners Manage partnershipsManage partnerships Personally liable for partnership obligationsPersonally liable for partnership obligations

Limited PartnersLimited Partners InvestorsInvestors

No management/participation rightsNo management/participation rights No personal liability for partnership debtsNo personal liability for partnership debts

Liability is limited to investment in partnershipLiability is limited to investment in partnership

If limited partners participate in management, If limited partners participate in management, they lose their liability protectionsthey lose their liability protections

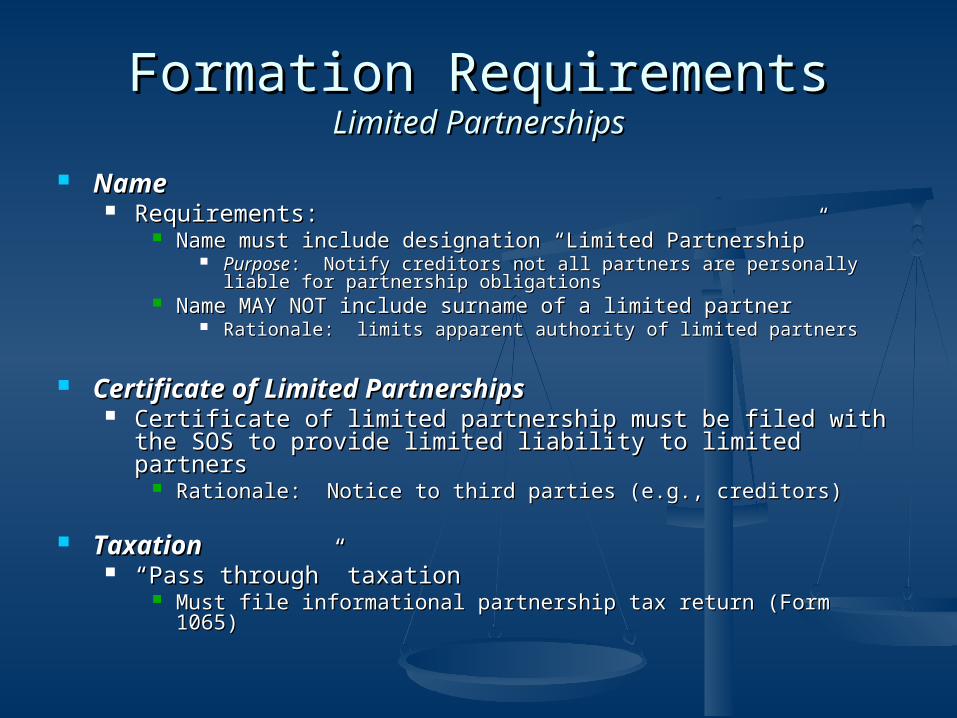

Formation RequirementsFormation RequirementsLimited PartnershipsLimited Partnerships

NameName Requirements:Requirements:

Name must include designation “Limited Partnership”Name must include designation “Limited Partnership” PurposePurpose: Notify creditors not all partners are personally liable for : Notify creditors not all partners are personally liable for

partnership obligationspartnership obligations Name MAY NOT include surname of a limited partnerName MAY NOT include surname of a limited partner

Rationale: limits apparent authority of limited partnersRationale: limits apparent authority of limited partners

Certificate of Limited PartnershipsCertificate of Limited Partnerships Certificate of limited partnership must be filed with the SOS to Certificate of limited partnership must be filed with the SOS to

provide limited liability to limited partnersprovide limited liability to limited partners Rationale: Notice to third parties (e.g., creditors)Rationale: Notice to third parties (e.g., creditors)

TaxationTaxation ““Pass through” taxationPass through” taxation

Must file informational partnership tax return (Form 1065)Must file informational partnership tax return (Form 1065)

Changes in Partnership AssociationChanges in Partnership AssociationLimited PartnershipsLimited Partnerships

Admission of New PartnersAdmission of New Partners

General Partners General Partners (Managers)(Managers) Admission = dissolution of partnershipAdmission = dissolution of partnership

Unless all partners consentUnless all partners consent Rationale: Avoids involuntary partnershipRationale: Avoids involuntary partnership

Limited Partners Limited Partners (Investors)(Investors) New investor DOES NOT dissolve partnershipNew investor DOES NOT dissolve partnership

Rationale: provides additional capital without Rationale: provides additional capital without change in management change in management

TerminationTerminationLimited PartnershipsLimited Partnerships

Partnership may terminate if:Partnership may terminate if: All partners agreeAll partners agree Partnership Agreement has ending datePartnership Agreement has ending date Duration/Purpose of partnership is completeDuration/Purpose of partnership is complete Courts order dissolutionCourts order dissolution General partner withdraws/diesGeneral partner withdraws/dies

General PartnerGeneral Partner Withdrawal = dissolutionWithdrawal = dissolution

Limited PartnerLimited Partner Withdrawal DOES NOT require dissolutionWithdrawal DOES NOT require dissolution

Rationale: Investors are not active participantsRationale: Investors are not active participants

Limited Partnership AssociationLimited Partnership Association

Indefinite DurationIndefinite Duration Key distinction from LLP/LLLPKey distinction from LLP/LLLP

No Personal LiabilityNo Personal Liability For debts, obligations, or other liabilitiesFor debts, obligations, or other liabilities

May jeopardize IRS status as partnershipMay jeopardize IRS status as partnership

““the most corporate-like form of a partnership entity”the most corporate-like form of a partnership entity”

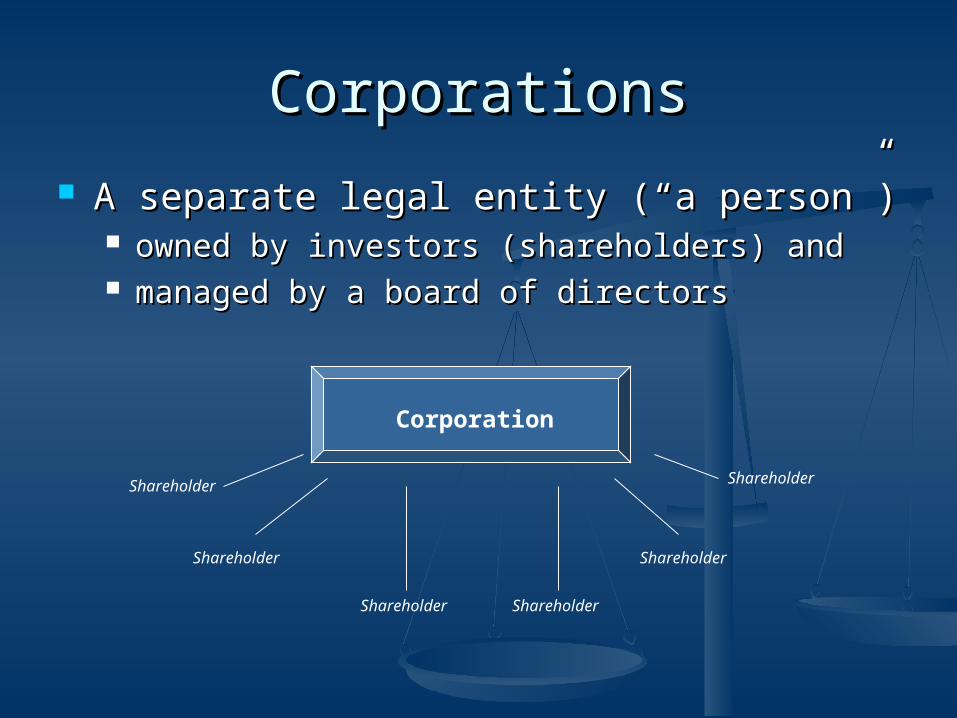

CorporationsCorporations

A separate legal entity (“a person”) A separate legal entity (“a person”) owned by investors (shareholders) and owned by investors (shareholders) and managed by a board of directorsmanaged by a board of directors

Shareholder

Shareholder

Shareholder Shareholder

Shareholder

Shareholder

Corporation

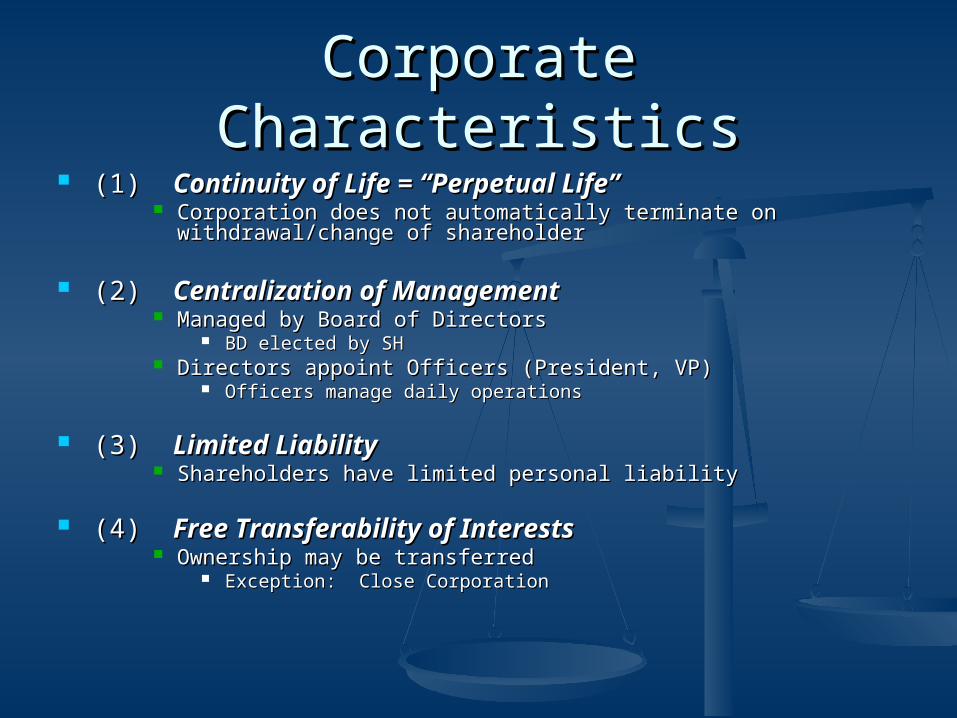

Corporate CharacteristicsCorporate Characteristics (1) (1) Continuity of Life = “Perpetual Life”Continuity of Life = “Perpetual Life”

Corporation does not automatically terminate on Corporation does not automatically terminate on withdrawal/change of shareholderwithdrawal/change of shareholder

(2) (2) Centralization of ManagementCentralization of Management Managed by Board of DirectorsManaged by Board of Directors

BD elected by SHBD elected by SH Directors appoint Officers (President, VP)Directors appoint Officers (President, VP)

Officers manage daily operationsOfficers manage daily operations

(3) (3) Limited LiabilityLimited Liability Shareholders have limited personal liabilityShareholders have limited personal liability

(4) (4) Free Transferability of InterestsFree Transferability of Interests Ownership may be transferredOwnership may be transferred

Exception: Close CorporationException: Close Corporation

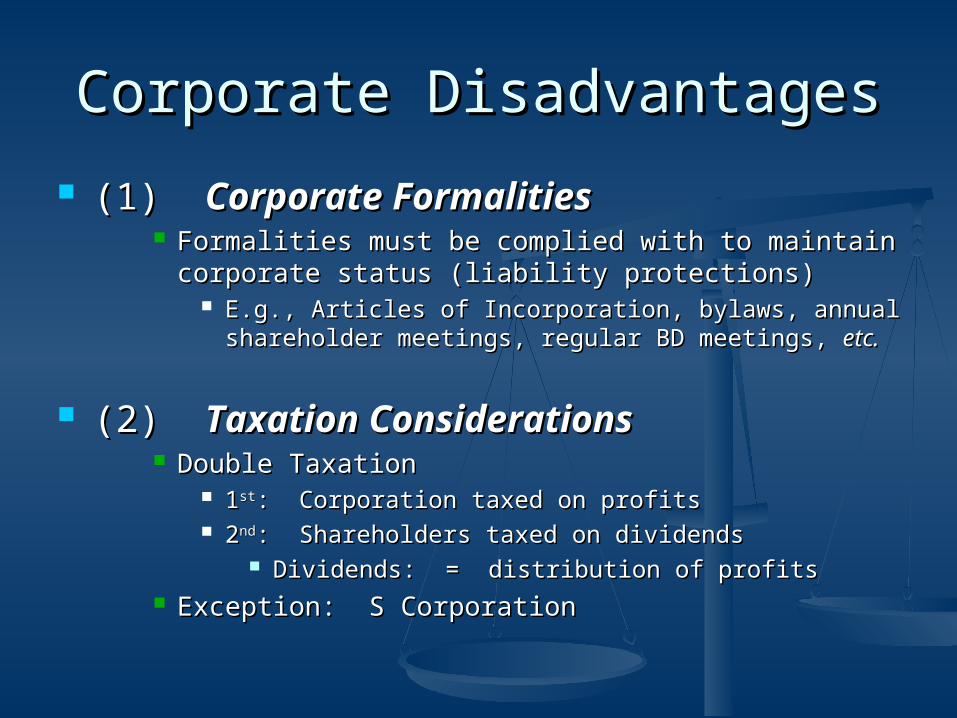

Corporate DisadvantagesCorporate Disadvantages

(1) (1) Corporate FormalitiesCorporate Formalities Formalities must be complied with to maintain Formalities must be complied with to maintain

corporate status (liability protections)corporate status (liability protections) E.g., Articles of Incorporation, bylaws, annual E.g., Articles of Incorporation, bylaws, annual

shareholder meetings, regular BD meetings, shareholder meetings, regular BD meetings, etc.etc.

(2) (2) Taxation ConsiderationsTaxation Considerations Double TaxationDouble Taxation

11stst: Corporation taxed on profits: Corporation taxed on profits 22ndnd: Shareholders taxed on dividends : Shareholders taxed on dividends

Dividends: = distribution of profitsDividends: = distribution of profits Exception: S CorporationException: S Corporation

Corporate FormsCorporate Forms Basic FormsBasic Forms

Business CorporationBusiness Corporation Statutory Close CorporationStatutory Close Corporation

Specific Categories of CorporationsSpecific Categories of Corporations Non-profit CorporationNon-profit Corporation Professional CorporationProfessional Corporation

IRS DesignationIRS Designation S CorporationS Corporation

Receives “pass-through” taxationReceives “pass-through” taxation

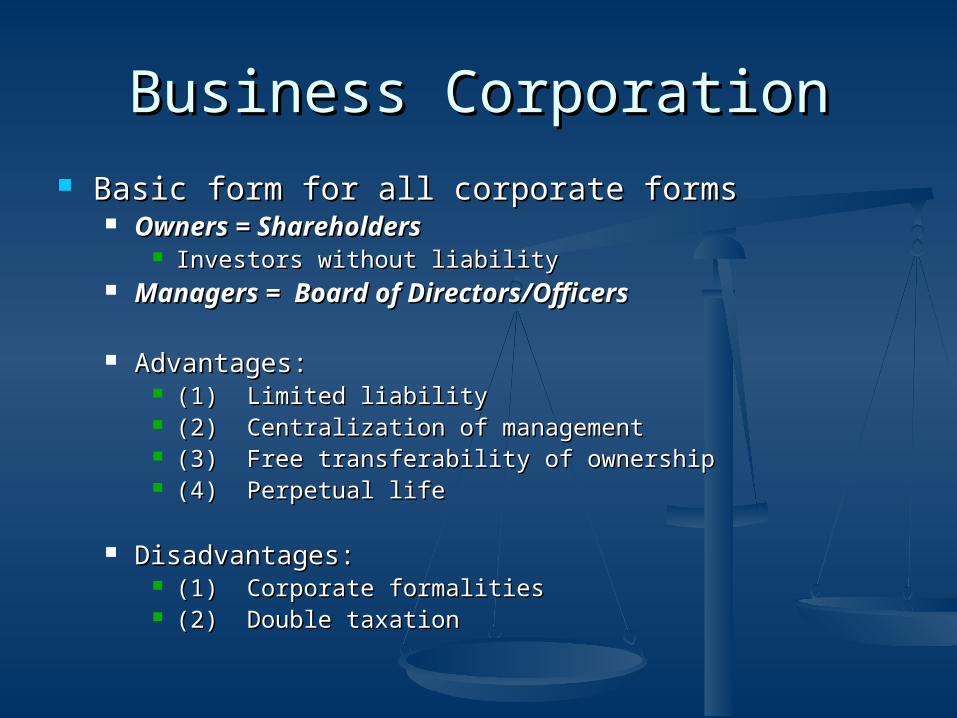

Business CorporationBusiness Corporation Basic form for all corporate formsBasic form for all corporate forms

Owners = ShareholdersOwners = Shareholders Investors without liabilityInvestors without liability

Managers = Board of Directors/OfficersManagers = Board of Directors/Officers

Advantages:Advantages: (1) Limited liability(1) Limited liability (2) Centralization of management(2) Centralization of management (3) Free transferability of ownership(3) Free transferability of ownership (4) Perpetual life(4) Perpetual life

Disadvantages:Disadvantages: (1) Corporate formalities(1) Corporate formalities (2) Double taxation(2) Double taxation

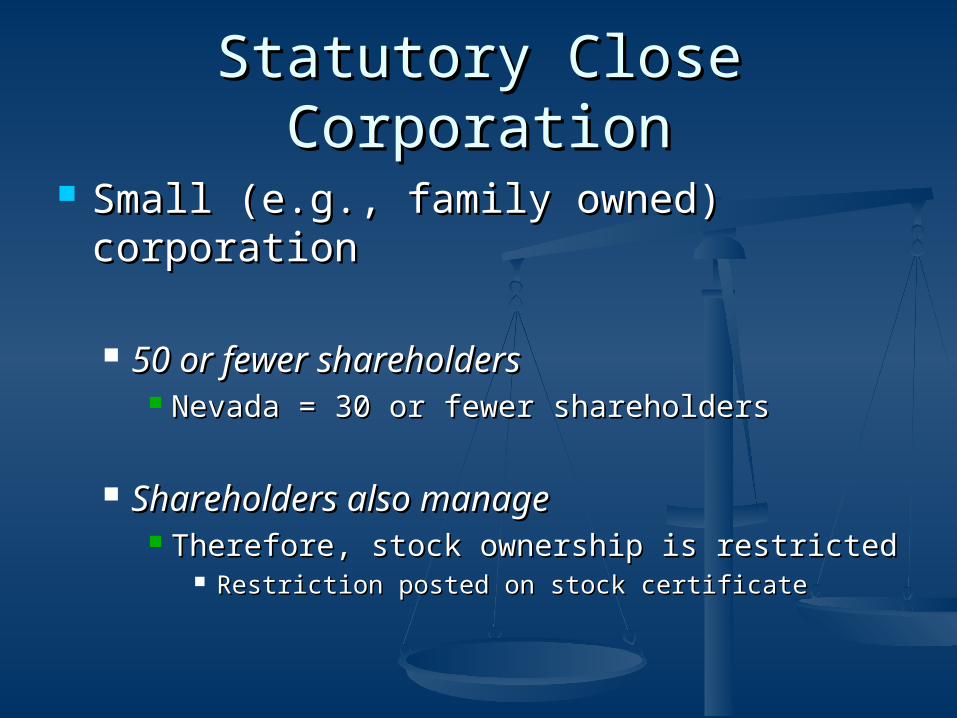

Statutory Close CorporationStatutory Close Corporation

Small (e.g., family owned) Small (e.g., family owned) corporationcorporation

50 or fewer shareholders50 or fewer shareholders Nevada = 30 or fewer shareholdersNevada = 30 or fewer shareholders

Shareholders also manageShareholders also manage Therefore, stock ownership is restrictedTherefore, stock ownership is restricted

Restriction posted on stock certificateRestriction posted on stock certificate

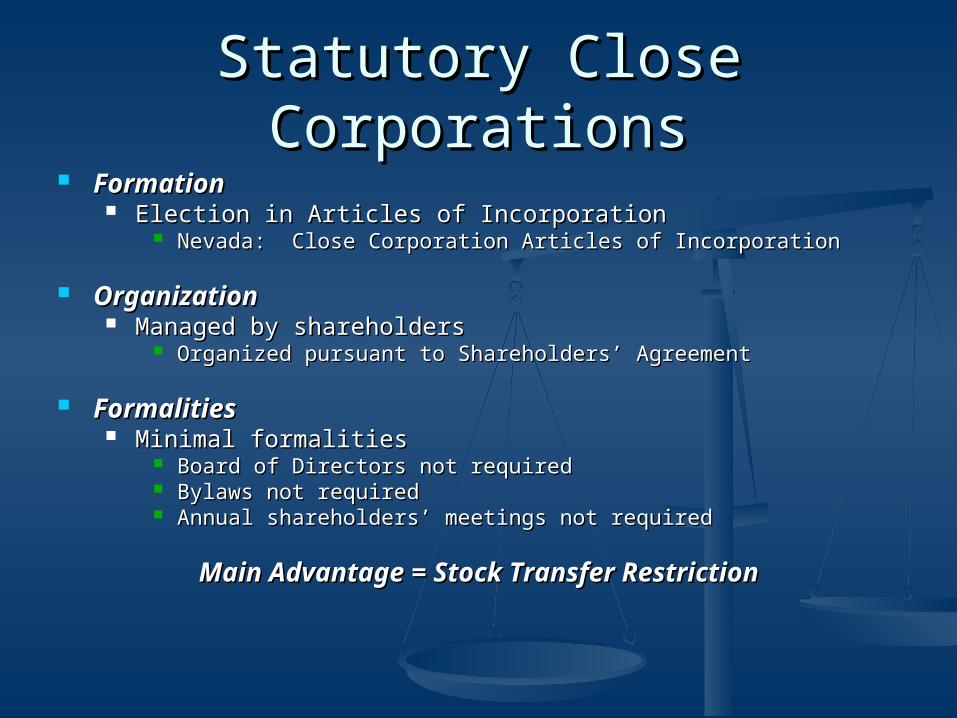

Statutory Close CorporationsStatutory Close Corporations FormationFormation

Election in Articles of IncorporationElection in Articles of Incorporation Nevada: Close Corporation Articles of IncorporationNevada: Close Corporation Articles of Incorporation

OrganizationOrganization Managed by shareholdersManaged by shareholders

Organized pursuant to Shareholders’ AgreementOrganized pursuant to Shareholders’ Agreement

FormalitiesFormalities Minimal formalitiesMinimal formalities

Board of Directors not requiredBoard of Directors not required Bylaws not requiredBylaws not required Annual shareholders’ meetings not requiredAnnual shareholders’ meetings not required

Main Advantage = Stock Transfer RestrictionMain Advantage = Stock Transfer Restriction

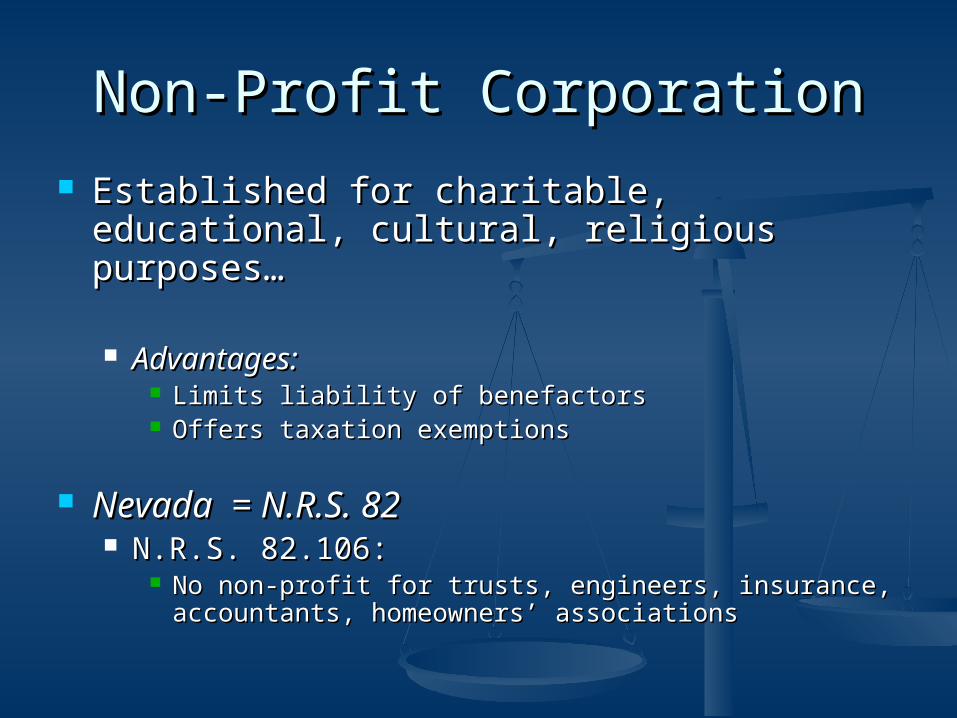

Non-Profit CorporationNon-Profit Corporation

Established for charitable, educational, Established for charitable, educational, cultural, religious purposes…cultural, religious purposes…

Advantages:Advantages: Limits liability of benefactorsLimits liability of benefactors Offers taxation exemptionsOffers taxation exemptions

Nevada = N.R.S. 82Nevada = N.R.S. 82 N.R.S. 82.106:N.R.S. 82.106:

No non-profit for trusts, engineers, insurance, No non-profit for trusts, engineers, insurance, accountants, homeowners’ associationsaccountants, homeowners’ associations

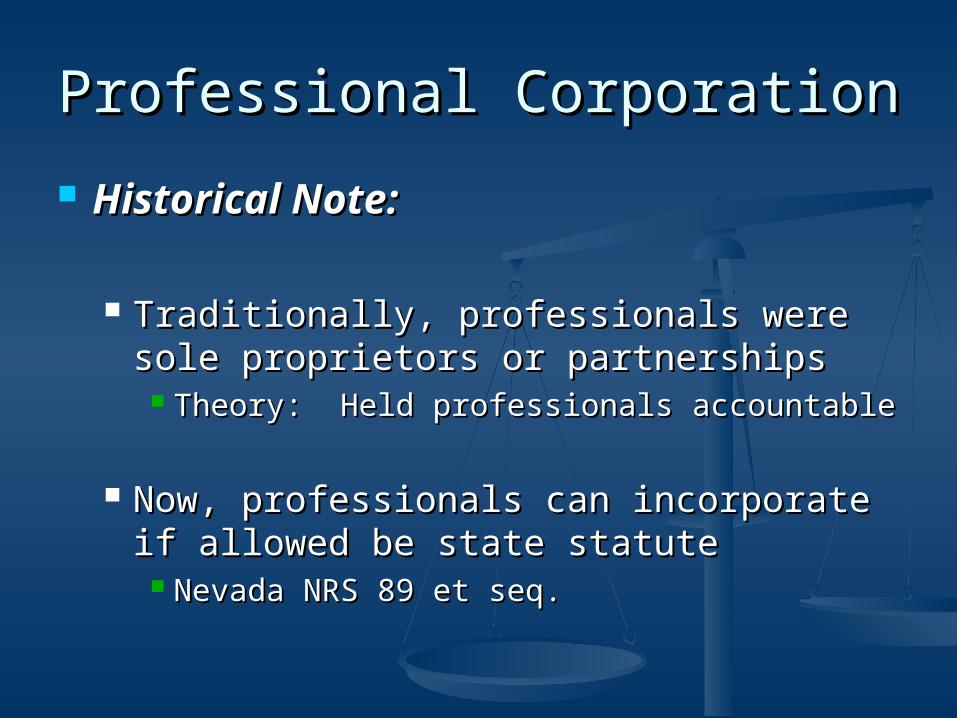

Professional CorporationProfessional Corporation

Historical Note:Historical Note:

Traditionally, professionals were sole Traditionally, professionals were sole proprietors or partnershipsproprietors or partnerships

Theory: Held professionals accountableTheory: Held professionals accountable

Now, professionals can incorporate if Now, professionals can incorporate if allowed be state statuteallowed be state statute

Nevada NRS 89 et seq.Nevada NRS 89 et seq.

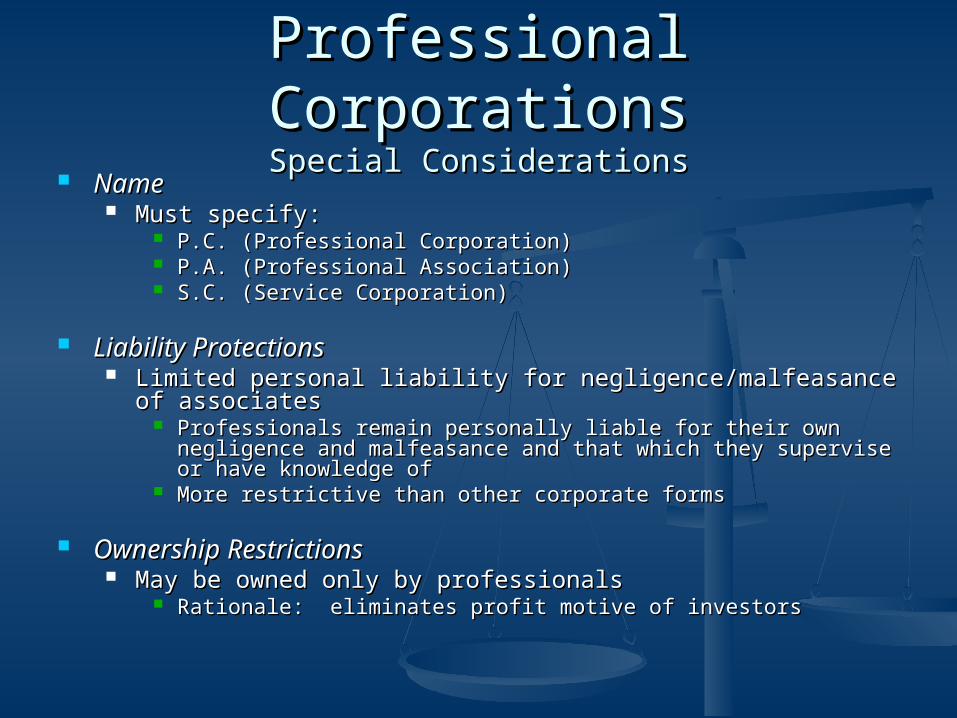

Professional CorporationsProfessional CorporationsSpecial ConsiderationsSpecial Considerations

NameName Must specify: Must specify:

P.C. (Professional Corporation)P.C. (Professional Corporation) P.A. (Professional Association)P.A. (Professional Association) S.C. (Service Corporation)S.C. (Service Corporation)

Liability ProtectionsLiability Protections Limited personal liability for negligence/malfeasance of Limited personal liability for negligence/malfeasance of

associatesassociates Professionals remain personally liable for their own negligence and Professionals remain personally liable for their own negligence and

malfeasance and that which they supervise or have knowledge ofmalfeasance and that which they supervise or have knowledge of More restrictive than other corporate formsMore restrictive than other corporate forms

Ownership RestrictionsOwnership Restrictions May be owned only by professionalsMay be owned only by professionals

Rationale: eliminates profit motive of investorsRationale: eliminates profit motive of investors

S CorporationsS Corporations

IRS Tax DesignationIRS Tax Designation

Not a separate corporate formNot a separate corporate form Requirements:Requirements:

Small corporations (less than 75 Small corporations (less than 75 shareholders)shareholders)

Shareholders must be individuals or Shareholders must be individuals or extensions of individuals (trusts, estates)extensions of individuals (trusts, estates)

Formation of a CorporationFormation of a Corporation

Creating the CorporationCreating the Corporation Pre-Incorporation ConsiderationsPre-Incorporation Considerations

OrganizationOrganization 1. 1. Corporate OrganizersCorporate Organizers

PromotersPromoters: Organize corporation, lease business : Organize corporation, lease business property, buy business equipment, hire employees, property, buy business equipment, hire employees, solicit investors [promoters generally found only in solicit investors [promoters generally found only in large corporations]large corporations]

IncorporatorsIncorporators: Sign and file Articles of : Sign and file Articles of IncorporationIncorporation

Note: Promoters and incorporators are generally the same Note: Promoters and incorporators are generally the same personal and generally become shareholders in the corporationpersonal and generally become shareholders in the corporation

2. 2. Selection of JurisdictionSelection of Jurisdiction MBCA and RMBCA create uniform laws and reduce MBCA and RMBCA create uniform laws and reduce

forum shoppingforum shopping

CorporationCorporationFormationFormation

3. 3. Corporate FinancingCorporate Financing Potential investors agree to purchase corporate shares Potential investors agree to purchase corporate shares

once corporation is formedonce corporation is formed = pre-incorporation share subscription= pre-incorporation share subscription

4. 4. Corporate NameCorporate Name Designate: “Corporation”, “Incorporated”, “Company”Designate: “Corporation”, “Incorporated”, “Company” Name may not be deceptively similar to another Name may not be deceptively similar to another

business namebusiness name Rationale: prevents consumer confusionRationale: prevents consumer confusion

Reservation of corporate nameReservation of corporate name Generally by large companies intending to expandGenerally by large companies intending to expand

Pre-Incorporation: Pre-Incorporation: Document PreparationDocument Preparation

FormationFormation Articles of IncorporationArticles of Incorporation

Informational filing with Secretary of StateInformational filing with Secretary of State Beginning of corporate lifeBeginning of corporate life

Look to state statuteLook to state statute Name of corporationName of corporation Purpose of corporationPurpose of corporation Capital structure of corporation (stock)Capital structure of corporation (stock) Registered agentRegistered agent Initial board of directorsInitial board of directors

Drafting Note: Provide minimal information because A/I Drafting Note: Provide minimal information because A/I are available for public inspection and are difficult to are available for public inspection and are difficult to amendamend

Filing with Secretary of StateFiling with Secretary of State Acceptance of A/I by SOS = corporate beginningAcceptance of A/I by SOS = corporate beginning

Post-Incorporation:Post-Incorporation:FormalitiesFormalities

Organizing = A/I, bylaws and meetingsOrganizing = A/I, bylaws and meetings

1. 1. BylawsBylaws = Operating procedures = Operating procedures Written guidelines and procedures for operation/managementWritten guidelines and procedures for operation/management

Dates/places of SH and BD meetingsDates/places of SH and BD meetings Voting of Board of DirectorsVoting of Board of Directors Duties of Board of Directors/OfficersDuties of Board of Directors/Officers Stock issuance/ownershipStock issuance/ownership Corporate finances (e.g., bank accounts)Corporate finances (e.g., bank accounts)

2. 2. Organizational MeetingOrganizational Meeting By incorporators/initial directorsBy incorporators/initial directors

Elect directors (if not appointed in Articles of Incorporation)Elect directors (if not appointed in Articles of Incorporation) Appoint corporate officersAppoint corporate officers Approve Articles of IncorporationApprove Articles of Incorporation Bylaws adoptedBylaws adopted Pre-incorporation transactions ratifiedPre-incorporation transactions ratified

Defective IncorporationDefective IncorporationDoctrinesDoctrines

De Jure CorporationDe Jure Corporation = valid corporation= valid corporation

Complies with all state statutory requirementsComplies with all state statutory requirements Corporation cannot be set asideCorporation cannot be set aside

E.g., shareholders cannot be held liable for corp debtsE.g., shareholders cannot be held liable for corp debts

But if corporation does not comply with But if corporation does not comply with statutory requirements…statutory requirements…

Corporate structure may be set aside and Corporate structure may be set aside and shareholders may be personally liable for obligations shareholders may be personally liable for obligations of the corporationof the corporation

Shielding ShareholdersShielding Shareholdersof a Defective Corporationof a Defective Corporation

A defective corporate structure may be A defective corporate structure may be upheld under the following doctrines:upheld under the following doctrines: 1. 1. De Facto CorporationDe Facto Corporation

Business owner has, in good faith:Business owner has, in good faith: (1) attempted to comply with state statutory (1) attempted to comply with state statutory

requirementsrequirements (2) operated as a corporation (e.g., uses corporate name)(2) operated as a corporation (e.g., uses corporate name)

2. 2. Corporation by EstoppelCorporation by Estoppel Applicable only to contract disputesApplicable only to contract disputes

If a party to a contract represents itself as a coporation, If a party to a contract represents itself as a coporation, other party cannot set aside the corporate existenceother party cannot set aside the corporate existence

Reflects contract expectationsReflects contract expectations

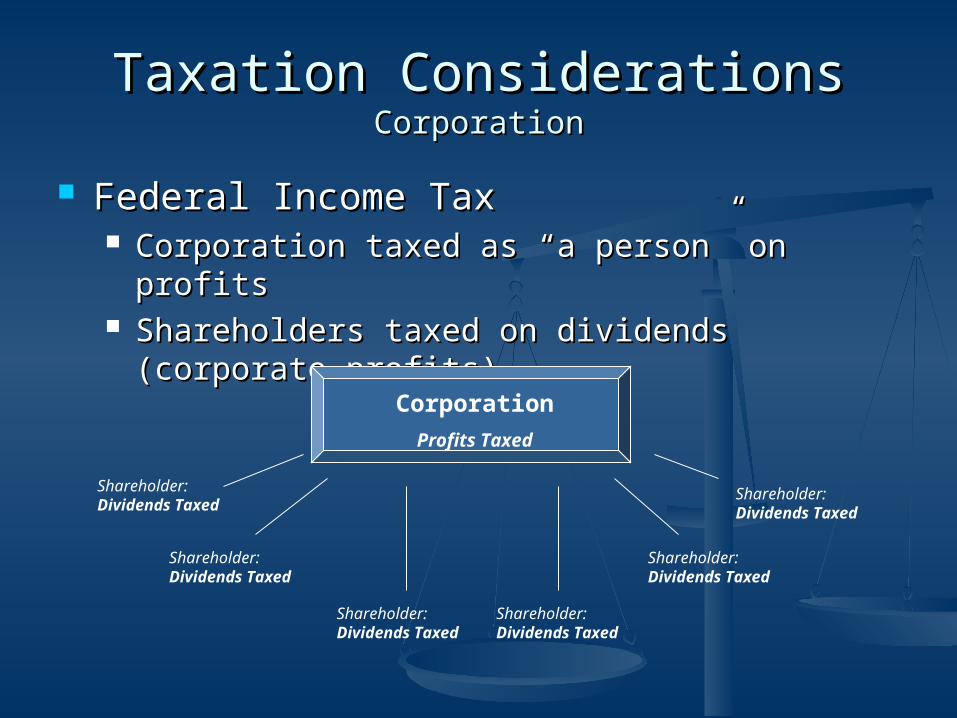

Taxation ConsiderationsTaxation ConsiderationsCorporationCorporation

Federal Income TaxFederal Income Tax Corporation taxed as “a person” on profitsCorporation taxed as “a person” on profits Shareholders taxed on dividends (corporate Shareholders taxed on dividends (corporate

profits)profits)

Shareholder: Dividends Taxed

Corporation

Profits Taxed

Shareholder: Dividends Taxed

Shareholder: Dividends Taxed

Shareholder: Dividends Taxed

Shareholder: Dividends Taxed

Shareholder: Dividends Taxed

Taxation ConsiderationsTaxation ConsiderationsCorporationCorporation

State Income TaxationState Income Taxation

Prorated State TaxingProrated State Taxing Each state in which the corporation Each state in which the corporation

transacts business may tax corporationtransacts business may tax corporation Corporate residence vs. sales profitsCorporate residence vs. sales profits

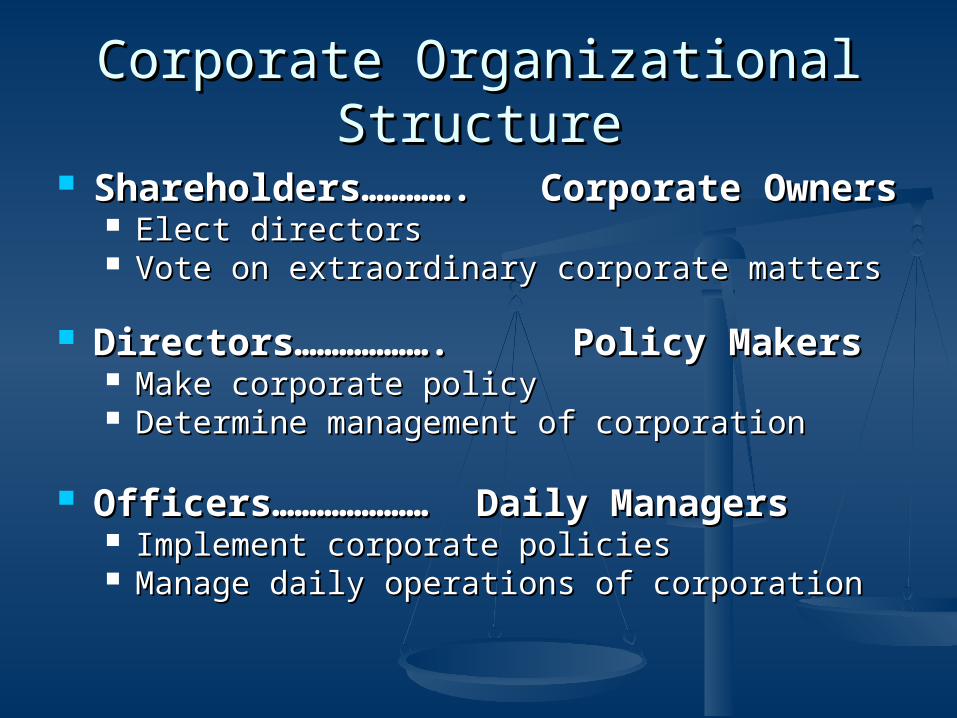

Corporate Organizational StructureCorporate Organizational Structure

Shareholders…………. Corporate Shareholders…………. Corporate OwnersOwners Elect directorsElect directors Vote on extraordinary corporate mattersVote on extraordinary corporate matters

Directors………………. Directors………………. Policy MakersPolicy Makers Make corporate policyMake corporate policy Determine management of corporationDetermine management of corporation

Officers…………………Officers………………… Daily ManagersDaily Managers Implement corporate policiesImplement corporate policies Manage daily operations of corporationManage daily operations of corporation

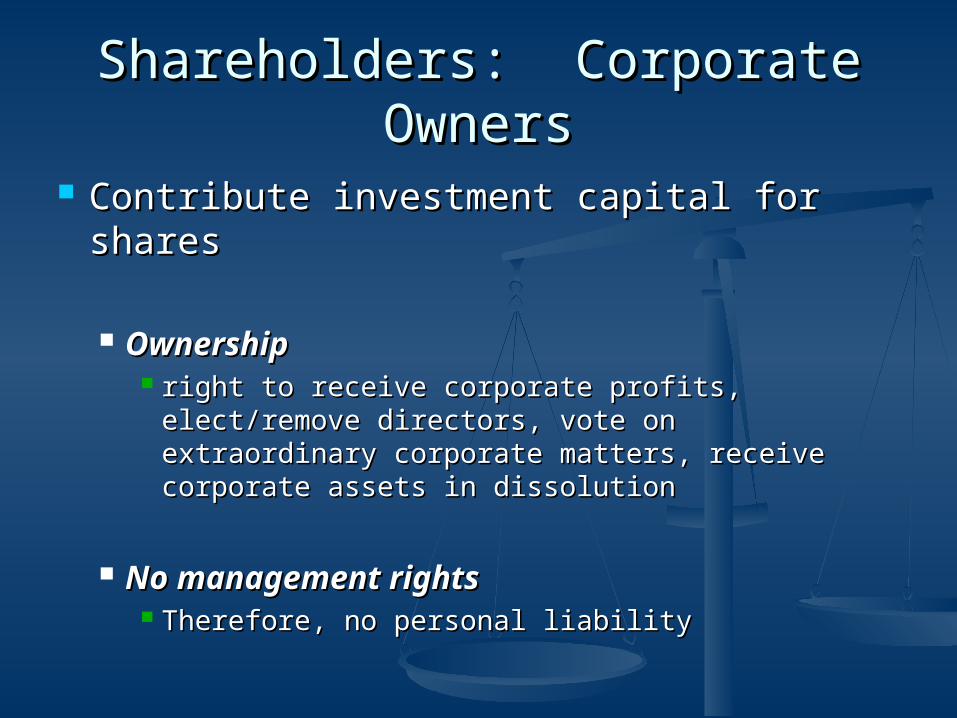

Shareholders: Corporate OwnersShareholders: Corporate Owners

Contribute investment capital for sharesContribute investment capital for shares

OwnershipOwnership right to receive corporate profits, elect/remove right to receive corporate profits, elect/remove

directors, vote on extraordinary corporate directors, vote on extraordinary corporate matters, receive corporate assets in dissolutionmatters, receive corporate assets in dissolution

No management rightsNo management rights Therefore, no personal liabilityTherefore, no personal liability

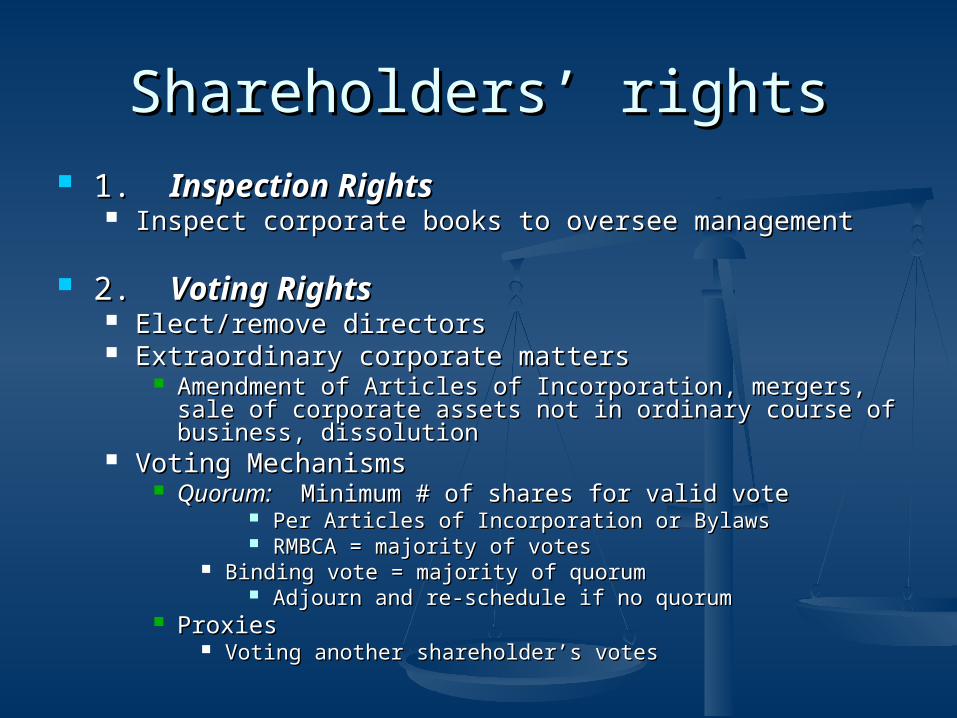

Shareholders’ rightsShareholders’ rights 1. 1. Inspection RightsInspection Rights

Inspect corporate books to oversee managementInspect corporate books to oversee management

2. 2. Voting RightsVoting Rights Elect/remove directorsElect/remove directors Extraordinary corporate mattersExtraordinary corporate matters

Amendment of Articles of Incorporation, mergers, sale of Amendment of Articles of Incorporation, mergers, sale of corporate assets not in ordinary course of business, corporate assets not in ordinary course of business, dissolutiondissolution

Voting MechanismsVoting Mechanisms Quorum:Quorum: Minimum # of shares for valid vote Minimum # of shares for valid vote

Per Articles of Incorporation or BylawsPer Articles of Incorporation or Bylaws RMBCA = majority of votesRMBCA = majority of votes

Binding vote = majority of quorumBinding vote = majority of quorum Adjourn and re-schedule if no quorumAdjourn and re-schedule if no quorum

ProxiesProxies Voting another shareholder’s votesVoting another shareholder’s votes

3. 3. Preemptive RightsPreemptive Rights Shareholders’ right to maintain Shareholders’ right to maintain

proportionate ownership interest (control proportionate ownership interest (control of corporation)of corporation)

Prevents outsiders from taking over Prevents outsiders from taking over corporationcorporation

4. 4. Meeting RightsMeeting Rights Meeting prerequisitesMeeting prerequisites

Shareholders eligible to voteShareholders eligible to vote Shareholders owning stock on date of notice of Shareholders owning stock on date of notice of

meeting (record date) may votemeeting (record date) may vote Notice of meeting (date, place, time)Notice of meeting (date, place, time)

Shareholders must have reasonable noticeShareholders must have reasonable notice May waive noticeMay waive notice

Shareholders MeetingsShareholders Meetings Annual MeetingsAnnual Meetings

Purpose: elect new directors, amend articles, Purpose: elect new directors, amend articles, consider mergers, etc.consider mergers, etc.

Special MeetingsSpecial Meetings Between annual meetingsBetween annual meetings

Meetings by Written ConsentMeetings by Written Consent Votes must be unanimous (all shareholders)Votes must be unanimous (all shareholders)

**Minutes of all corporate meetings must be **Minutes of all corporate meetings must be maintained**maintained**

Shareholders’ LiabilityShareholders’ Liability No personal liabilityNo personal liability

Shareholders generally have no personal liabilityShareholders generally have no personal liability VEIL between corporation and shareholdersVEIL between corporation and shareholders

Veil may be pierced Veil may be pierced (1) prevent fraud/injustice(1) prevent fraud/injustice (2) shareholder personally guarantees loans(2) shareholder personally guarantees loans

Piercing the Corporate Veil Piercing the Corporate Veil To prevent fraud/injustice:To prevent fraud/injustice:

3 reasons:3 reasons: 1. Lack of corporate formalities1. Lack of corporate formalities 2. Commingling of corporate/personal assets2. Commingling of corporate/personal assets 3. Inadequate capitalization3. Inadequate capitalization

Personal guarantee by shareholderPersonal guarantee by shareholder Voluntary agreement by shareholder to be personally liable for Voluntary agreement by shareholder to be personally liable for

specific debts of corporation specific debts of corporation maintains liability protection for other debtsmaintains liability protection for other debts

Purpose: Financing for corporationPurpose: Financing for corporation

Directors: Directors: Corporate PolicymakersCorporate Policymakers

Election of Directors:Election of Directors: Appointed in Articles of Incorporation andAppointed in Articles of Incorporation and Elected by shareholders at annual Elected by shareholders at annual

meetingsmeetings Voting mechanisms:Voting mechanisms:

Plurality of outstanding sharesPlurality of outstanding shares Cumulative voting vs. straight votingCumulative voting vs. straight voting

Removal of DirectorsRemoval of Directors 10% vote of shareholders to remove director10% vote of shareholders to remove director

Directors’ DutiesDirectors’ Duties

Management ResponsibilitiesManagement Responsibilities Make corporate policyMake corporate policy Declare corporate dividendsDeclare corporate dividends Elect and remove officers of the corporationElect and remove officers of the corporation Initiate extraordinary corporate mattersInitiate extraordinary corporate matters

Director’s MeetingsDirector’s Meetings (look to bylaws) (look to bylaws) Voting requirements and restrictionsVoting requirements and restrictions

Majority of directors must at meeting for valid Majority of directors must at meeting for valid votevote

Fiduciary DutiesFiduciary Duties Duty of CareDuty of Care

Would RPP act the same?Would RPP act the same? Business Judgment RuleBusiness Judgment Rule

Duty of LoyaltyDuty of Loyalty Conflict of InterestConflict of Interest

1. Personal interest in corporate transaction1. Personal interest in corporate transaction Full Disclosure:Full Disclosure:

1. Disclosure Interest1. Disclosure Interest 2. Transaction fair to corporation2. Transaction fair to corporation

2. Usurpation of corporate opportunity2. Usurpation of corporate opportunity 3. Insider Trading3. Insider Trading

Trading on corporation’s stock with inside information Trading on corporation’s stock with inside information (information not available to general public)(information not available to general public)

Director’s Liability Director’s Liability

Director’s liability insuranceDirector’s liability insurance

Ultra ViresUltra Vires Acts Acts Director exceeds authority grantedDirector exceeds authority granted

Breach of Fiduciary DutiesBreach of Fiduciary Duties Duty of CareDuty of Care Duty of LoyaltyDuty of Loyalty

Conflict of InterestConflict of Interest Usurpation of Corporate OpportunityUsurpation of Corporate Opportunity Insider TradingInsider Trading

Officers:Officers:Corporate ManagersCorporate Managers

Officers:Officers: PresidentPresident Vice-PresidentVice-President Secretary Secretary TreasurerTreasurer

Appointment and Removal of OfficersAppointment and Removal of Officers By Board of DirectorsBy Board of Directors

Officers’ DutiesOfficers’ Duties President: oversees general managementPresident: oversees general management Vice-President: variable dutiesVice-President: variable duties Secretary: maintains records of corporationSecretary: maintains records of corporation Treasurer: Responsible for financialTreasurer: Responsible for financial

Officers: AgencyOfficers: Agency Express AuthorityExpress Authority

Granted by: Granted by: Articles of IncorporationArticles of Incorporation BylawsBylaws Board of DirectorsBoard of Directors

Implied AuthorityImplied Authority Authority public assumes officers haveAuthority public assumes officers have

Apparent AuthorityApparent Authority Corporation gives impression officer has Corporation gives impression officer has

authorityauthority Purpose: protect public from unauthorized acts of Purpose: protect public from unauthorized acts of

officersofficers

Officers: Fiduciary DutiesOfficers: Fiduciary Duties

Duty of CareDuty of Care Directors must use reasonable careDirectors must use reasonable care

Duty of LoyaltyDuty of Loyalty Directors must be loyal to the corporation’s Directors must be loyal to the corporation’s

interestsinterests

Breach of Fiduciary DutiesBreach of Fiduciary Duties Creates personal liabilityCreates personal liability Business Judgment RuleBusiness Judgment Rule

Protects officers if they exercise business judgmentProtects officers if they exercise business judgment

Fundamental ChangesFundamental Changesin Corporate Structurein Corporate Structure

Fundamental ChangesFundamental Changes MergerMerger ConsolidationConsolidation Sale, lease, exchange of corporate assets not in the ordinary course of businessSale, lease, exchange of corporate assets not in the ordinary course of business Amendment to Articles of IncorporationAmendment to Articles of Incorporation DissolutionDissolution

Standard Approval ProcedureStandard Approval Procedure (1) (1) Board of DirectorsBoard of Directors must approve change must approve change

Standard: Is change in the best interests of shareholders?Standard: Is change in the best interests of shareholders? If approved by Board, then submit to shareholdersIf approved by Board, then submit to shareholders

(2) (2) ShareholdersShareholders must approve change must approve change Approval by majority (2/3)Approval by majority (2/3) Dissenters’ RightsDissenters’ Rights

Articles of Amendment must be filed with Secretary of Articles of Amendment must be filed with Secretary of StateState

Fundamental ChangesFundamental Changesin Corporate Structurein Corporate Structure

1. 1. MergerMerger One or more corporations (merged corporations) One or more corporations (merged corporations)

absorbed into another corporation (surviving corporation)absorbed into another corporation (surviving corporation) File Articles of Merger with SOSFile Articles of Merger with SOS

2. 2. ConsolidationConsolidation One or more corporations merge and form a new One or more corporations merge and form a new

corporationcorporation File Articles of Consolidation with SOSFile Articles of Consolidation with SOS

3. 3. Sale of Corporate AssetsSale of Corporate Assets Corporation buys all or substantially all of the assets of Corporation buys all or substantially all of the assets of

another corporation (not in ordinary course of business)another corporation (not in ordinary course of business) Purpose: Escape liabilities of selling corporationPurpose: Escape liabilities of selling corporation

4. 4. Amendment to Articles of Amendment to Articles of IncorporationIncorporation Articles create and organize, therefore Articles create and organize, therefore

amendment = fundamental changeamendment = fundamental change File Articles of Amendment with SOSFile Articles of Amendment with SOS

5. 5. Hostile TakeoversHostile Takeovers Take over management and/or ownership of Take over management and/or ownership of

corporation without approval of BD or SHcorporation without approval of BD or SH

6. 6. Dissolution of CorporationDissolution of Corporation 2-step process:2-step process:

(1) Dissolve corporate form(1) Dissolve corporate form (2) Liquidate corporate assets(2) Liquidate corporate assets

DissolutionDissolutionof Corporationof Corporation

Voluntary Voluntary By Board of Directors or ShareholdersBy Board of Directors or Shareholders

InvoluntaryInvoluntary [caused by poor/ineffective management][caused by poor/ineffective management] Parties:Parties:

By stateBy state By shareholders By shareholders By corporate creditorsBy corporate creditors

Dissolution ProceduresDissolution Procedures

LiquidationLiquidation of corporate assets of corporate assets Turning assets into cashTurning assets into cash

(1) Creditors’ Claims(1) Creditors’ Claims Paid before distribution made to SHPaid before distribution made to SH

(2) Distributions to shareholders(2) Distributions to shareholders

File File Articles of DissolutionArticles of Dissolution with with SOSSOS

Limited Liability CompaniesLimited Liability Companies

Member-ManagersMember-Managers Nevada allows single member LLCsNevada allows single member LLCs

Unincorporated entity offering Unincorporated entity offering members:members: (1) Limited personal liability(1) Limited personal liability (2) Management rights(2) Management rights (3) Partnership taxation (3) Partnership taxation

““pass through” taxationpass through” taxation

LiabilityLiabilityLLCsLLCs

Members are not personally liable for Members are not personally liable for debts/obligations of LLCdebts/obligations of LLC Exceptions:Exceptions:

(1) capital contributions(1) capital contributions (2) violation of environmental laws(2) violation of environmental laws (3) unpaid taxes(3) unpaid taxes (4) fraud(4) fraud

Statutes generally require INSURANCE coverage to protect Statutes generally require INSURANCE coverage to protect publicpublic Optional in NevadaOptional in Nevada

Management & TaxationManagement & TaxationLLCLLC

ManagementManagement All members have the right to participate All members have the right to participate

in managementin management Right may be waived by electing:Right may be waived by electing:

Board of ManagersBoard of Managers Fiduciary Duties: Duty of Loyalty & Duty of CareFiduciary Duties: Duty of Loyalty & Duty of Care

TaxationTaxation Entity Classification Election (“check-the-Entity Classification Election (“check-the-

box”)box”) Pass through taxation if electedPass through taxation if elected

LLC vs. CorporationLLC vs. Corporation LLC shares 2 of 4 corporate characteristics:LLC shares 2 of 4 corporate characteristics:

(1) (1) Continuity of LifeContinuity of Life LLC generally must have limited duration (e.g., 30 years)LLC generally must have limited duration (e.g., 30 years)

Nevada allows perpetual existenceNevada allows perpetual existence (2) (2) Centralization of ManagementCentralization of Management

LLC generally is member-managedLLC generally is member-managed Nevada requires only managers be disclosed in SOS Nevada requires only managers be disclosed in SOS

reportingreporting (3) (3) Limited LiabilityLimited Liability

LLC offers limited liability from tort or contractLLC offers limited liability from tort or contract NRS 86.371 Liability of member or manager for debts or liabilities of company. Unless NRS 86.371 Liability of member or manager for debts or liabilities of company. Unless

otherwise provided in the articles of organization or agreement signed by the member of otherwise provided in the articles of organization or agreement signed by the member of manager to be charged, no member or manager of any limited liability company formed manager to be charged, no member or manager of any limited liability company formed under the laws of this state is individually liable for the debts or liabilities of the company.under the laws of this state is individually liable for the debts or liabilities of the company.

(4) (4) Free Transferability of InterestsFree Transferability of Interests Ownership transfer only gives right to receive profitsOwnership transfer only gives right to receive profits

Management rights cannot be transferred w/o consentManagement rights cannot be transferred w/o consent

FormationFormationLLCLLC

RequirementsRequirements Register assumed business name (state specific)Register assumed business name (state specific) Obtain business/professional license/permitsObtain business/professional license/permits Apply for tax identification number with IRS/stateApply for tax identification number with IRS/state Establish employee withholding/unemployment & Establish employee withholding/unemployment &

worker’s compensationworker’s compensationPLUSPLUS LLC Requirements:LLC Requirements:

Designate LLC in nameDesignate LLC in name File Articles of Organization with SOSFile Articles of Organization with SOS Draft Operating AgreementDraft Operating Agreement

Formation ConsiderationsFormation ConsiderationsLLCLLC

NameName Designate as LLC/Ltd. Liability Co.Designate as LLC/Ltd. Liability Co.

Nevada: LLC may be formed by one or more personsNevada: LLC may be formed by one or more persons PurposePurpose

““Any and all lawful business”Any and all lawful business” Potential liability problems because each member can bind LLCPotential liability problems because each member can bind LLC Nevada: LLC cannot be organized for insurance purposesNevada: LLC cannot be organized for insurance purposes

Registration of LLCRegistration of LLC File Articles of Organization with SOSFile Articles of Organization with SOS

LLC existence begins with Certificate of AcceptanceLLC existence begins with Certificate of Acceptance Nevada: Annual reports are dueNevada: Annual reports are due

Operating Agreement Operating Agreement signed by all memberssigned by all members = Partnership Agreement= Partnership Agreement

Include: Voting/management rights of members, capital Include: Voting/management rights of members, capital contributions of members, profit sharing, durationcontributions of members, profit sharing, duration

Termination of LLCTermination of LLC

DissolutionDissolution Due to: Due to:

Termination per Operating AgreementTermination per Operating Agreement Statutory duration period expiredStatutory duration period expired Death, bankruptcy, etc. of membersDeath, bankruptcy, etc. of members Agreement by membersAgreement by members Court orderCourt order

Election for ContinuationElection for Continuation Members may agree to continue businessMembers may agree to continue business

Creates new LLC therefore no continuity of lifeCreates new LLC therefore no continuity of life Winding UpWinding Up