Embed Size (px)

Citation preview

Corporate Finance: The Core (Berk/DeMarzo)Chapter 5 - Interest Rates

5.1 Interest Rate Quotes and Adjustments

2)

Which of the following equations is incorrect? A)

- 1= APR B)

Equivalent n-Period Discount Rate = (1 + r)n - 1 C)

1 + EAR =

D)

Interest Rate per Compounding Period =

Answer:

A Explanation:

A)

B)

C)

D)

Diff: 2 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Conceptual

3)

The effective annual rate (EAR) for a loan with a stated APR of 8% compounded monthly is closest to: A)

8.30%

B)

8.33% C)

8.00% D)

8.24% Answer:

A Explanation:

A)

EAR = (1 + APR / k)k - 1 = (1 + .08 / 12)12 - 1 = .083 or 8.3% B)

C)

D)

Diff: 1 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

4)

The effective annual rate (EAR) for a loan with a stated APR of 10% compounded quarterly is closest to: A)

10.52% B)

10.25% C)

10.38% D)

10.00% Answer:

C Explanation:

A)

B)

C)

EAR = (1 + APR / k)k - 1 = (1 + .10 / 4)4 - 1 = .1038 or 10.38% D)

Diff: 1 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

5)

The effective annual rate (EAR) for a savings account with a stated APR of 4% compounded daily is closest to:

A)

4.00% B)

4.10% C)

4.08% D)

4.06% Answer:

C Explanation:

A)

B)

C)

EAR = (1 + APR / k)k - 1 = (1 + .04 / 365)365 - 1 = .04088 or 4 .08% D)

Diff: 1 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

Use the table for the question(s) below.

Consider the following investment alternatives:

Investment Rate

Compounding

A 6.25% AnnualB 6.10% DailyC 6.125 QuarterlyD 6.120 Monthly

6)

Which alternative offers you the highest effective rate of return? A)

Investment A B)

Investment B C)

Investment C D)

Investment D Answer:

D Explanation:

A)

B)

C)

D)

EAR (A) = (1 + APR / k)k - 1 = (1 + .0625 / 1)1 - 1 = .0625 or 6.250%EAR (B) = (1 + APR / k)k - 1 = (1 + .0610 / 365)365 - 1 = .06289 or 6.289%EAR (C) = (1 + APR / k)k - 1 = (1 + .06125 / 4)4 - 1 = .06267 or 6.267%EAR (D) = (1 + APR / k)k - 1 = (1 + .0612 / 12)12 - 1 = .06295 or 6.300%

Diff: 2 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

You are purchasing a new home and need to borrow $250,000 from a mortgage lender. The mortgage lender quotes you a rate of 6.25% APR for a 30-year fixed rate mortgage. The mortgage lender also tells you that if you are willing to pay 2 points, they can offer you a lower rate of 6.0% APR for a 30-year fixed rate mortgage. One point is equal to 1% of the loan value. So if you take the lower rate and pay the points you will need to borrow an additional $5000 to cover points you are paying the lender.

17)

Assuming you don't pay the points and borrow from the mortgage lender at 6.25%, then your monthly mortgage payment (with payments made at the end of the month) will be closest to:

A)

$1570 B)

$1530 C)

$1540 D)

$1500 Answer:

C Explanation:

A)

B)

C)

First we need the monthly interest rate = APR / k = .0625 / 12 = .005208 or .5208%.

Now:PV = 250000 (no points)I = .5208FV = 0N = 360 (30 years × 12 months)Compute PMT = $1539.29

D)

Diff: 2 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

18)

Assuming you pay the points and borrow from the mortgage lender at 6.00%, then your monthly mortgage payment (with payments made at the end of the month) will be closest to:

A)

$1540 B)

$1530 C)

$1570 D)

$1500 Answer:

B Explanation:

A)

B)

First we need the monthly interest rate = APR / k = .0600 / 12 = .005000 or 0.50%.

Now:PV = 255000 (2 points)I = .50FV = 0N = 360 (30 years × 12 months)Compute PMT = $1528.85

C)

D)

Diff: 2 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

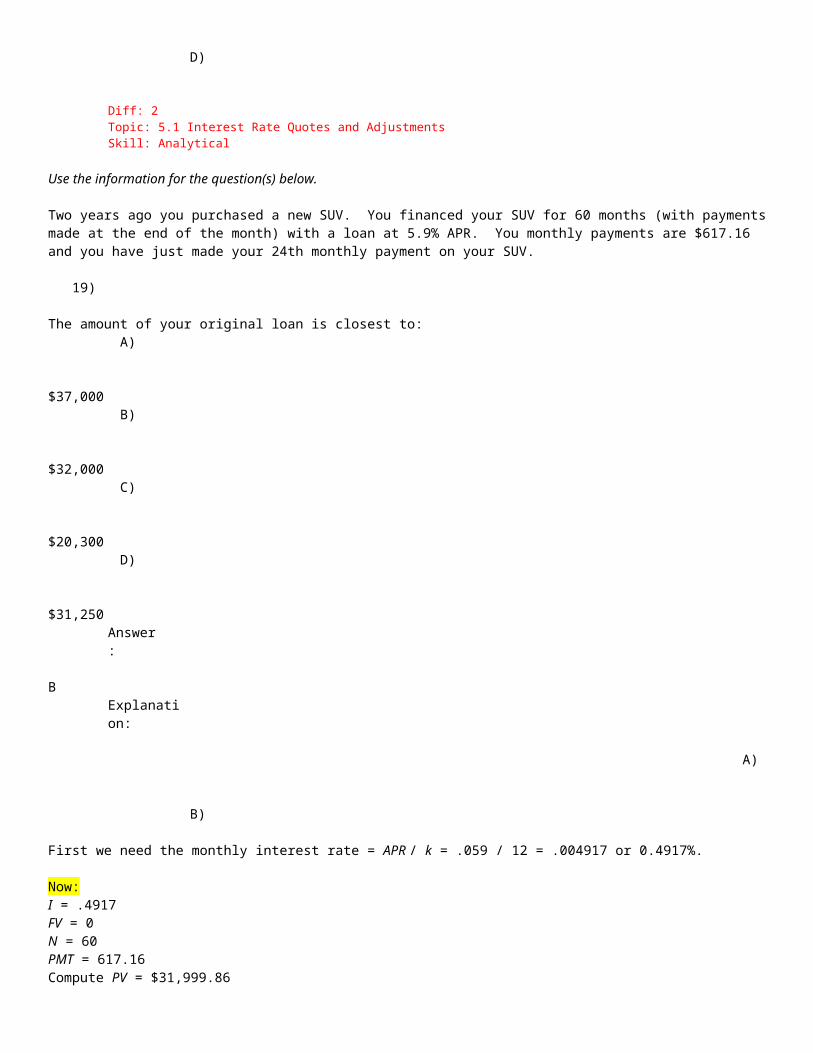

Use the information for the question(s) below.

Two years ago you purchased a new SUV. You financed your SUV for 60 months (with payments made at the end of the month) with a loan at 5.9% APR. You monthly payments are $617.16 and you have just made your 24th monthly payment on your SUV.

19)

The amount of your original loan is closest to: A)

$37,000

B)

$32,000 C)

$20,300 D)

$31,250 Answer:

B Explanation:

A)

B)

First we need the monthly interest rate = APR / k = .059 / 12 = .004917 or 0.4917%.

Now:I = .4917FV = 0N = 60PMT = 617.16 Compute PV = $31,999.86

C)

D)

Diff: 2 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

20)

Assuming that you have made all of the first 24 payments on time, then the outstanding principal balance on your SUV loan is closest to:

A)

$31,250 B)

20,300 C)

$19,200 D)

$32,000

Answer:

B Explanation:

A)

B)

First we need the monthly interest rate = APR / k = .059 / 12 = .004917 or 0.4917%.

Now:I = .4917FV = 0N = 36 (remaining payments 60 - 24 = 36)PMT = 617.16 Compute PV = $20,316.92

C)

D)

Diff: 2 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

Use the information for the question(s) below.

22)

You are in the process of purchasing a new automobile that will cost you $25,000. The dealership is offering you either a $1,000 rebate (applied toward the purchase price) or 3.9% financing for 60 months (with payments made at the end of the month). You have been pre-approved for an auto loan through your local credit union at an interest rate of 7.5% for 60 months. Should you take the $2000 rebate and finance through your credit union or forgo the rebate and finance through the dealership at the lower 3.9% APR?

Answer:

Take the rebate!

Credit Union:First we need the monthly interest rate = APR / k = .075 / 12 = .00625 or .625%.

Now:PV = 24000 (rebate 25,000 - 1,000)I = .625FV = 0N = 60Compute PMT = $480.91

Dealership:First we need the monthly interest rate = APR / k = .039 / 12 = .00325 or .325%.

Now:PV = 25000 (no rebate)I = .325FV = 0N = 60Compute PMT = $459.29

Since 459.29 < 480.91, go with the dealership and forgo the rebate. Diff: 3 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

23)

You are purchasing a new home and need to borrow $325,000 from a mortgage lender. The mortgage lender quotes you a rate of 6. 5% APR for a 30-year fixed rate mortgage (with payments made at the end of each month). The mortgage lender also tells you that if you are willing to pay 1 point, they can offer you a lower rate of 6.25% APR for a 30-year fixed rate mortgage. One point is equal to 1% of the loan value. So if you take the lower rate and pay the points you will need to borrow an additional $3250 to cover points you are paying the lender. Assuming that you do not intend to prepay your mortgage (pay off your mortgage early), are you better off paying the 1 point and borrowing at 6.25% APR or just taking out the loan at 6.5% without any points?

Answer:

Pay the points!

Points (6.25% APR)First we need the monthly interest rate = APR / k = .0625 / 12 = .00520833 or .5208%.

Now:PV = 328250 ( 325,000 + 1 point)I = .5208FV = 0N = 360 (30 years × 12 months)Compute PMT = $2,021.01

No PointsFirst we need the monthly interest rate = APR / k = .065 / 12 = .005417 or .5417%.

Now:PV = 325000 (no points)I = .5417FV = 0N = 360 (30 years × 12 months)Compute PMT = $2,054.22

Since $2,021.01 < $2,054.22, pay the points! Diff: 3 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytical

Use the information for the question(s) below.

Two years ago you purchased a new SUV. You financed your SUV for 60 months (with payments made at the end of the month) with a loan at 5.9% APR. You monthly payments are $617.16 and you have just made your 24th monthly payment on your SUV.

24)

Assuming that you have made all of the first 24 payments on time, then how much interest have you paid over the first two years of your loan?

Answer:

$3,128.78

First figure out the outstanding balance:We need the monthly interest rate = APR / k = .059 / 12 = .004917 or 0.4917%.

NowI = .4917FV = 0N = 36 (remaining payments = 60 - 24 = 36)PMT = 617.16 Compute PV = $20,316,80

Next figure out the original loan amount:

First we need the monthly interest rate = APR / k = .059 / 12 = .004917 or 0.4917%.

NowI = .4917FV = 0N = 60 (original number of payments)PMT = 617.16 Compute PV = $31,999.55

So the amount of principal paid = 31,999.55 - 20,316.80 = 11,682.75.

You have paid a total of 24 × 617.16 = $14,811.84.

So amount of Interest = 14,811.84 - 11,682.75 = 3,129.09. Diff: 3 Topic: 5.1 Interest Rate Quotes and Adjustments Skill: Analytica

5.2 The Determinants of Interest Rates

3)

Which of the following statements is false? A)

The yield curve changes over time. B)

The formulas for computing present values of annuities and perpetuities cannot be used in situations in which cash flows need to be discounted at different rates.

C)

We can use the term structure to compute the present and future values of a risk-free cash flow over different investment horizons.

D)

The yield curve tends to be inverted as the economy comes out of a recession. Answer:

D Explanation:

A)

B)

C)

D)

Diff: 2 Topic: 5.2 The Determinants of Interest Rates

Skill: Conceptual

46)

Which of the following formulas is incorrect? A)

i = - 1

B)

1 + rr =

C)

rr ≈ i - r D)

rr =

Answer:

C Explanation:

A)

B)

C)

D)

Diff: 2 Topic: 5.2 The Determinants of Interest Rates Skill: Conceptual

7)

If the current inflation rate is 5%, then the nominal rate necessary for you to earn an 8% real interest rate on your investment is closest to:

A)

13.0% B)

13.4% C)

4.9% D)

3.0% Answer:

B Explanation:

A)

B)

nominal = (1 + inflation)(1 + real) - 1 = (1.05)(1.08) - 1 = .134 or 13.4% C)

D)

Diff: 1 Topic: 5.2 The Determinants of Interest Rates Skill: Analytical

8)

If the current inflation rate is 4% and you have an investment opportunity that pays 10%, then the real rate of interest on your investment is closest to:

A)

10.0% B)

14.0% C)

6.0% D)

5.8% Answer:

D Explanation:

A)

1 + nominal = (1 + inflation)(1 + real)

real interest rate = - 1 = .057692 or 5.77%

B)

C)

D)

Diff: 1 Topic: 5.2 The Determinants of Interest Rates Skill: Analytical

Use the table for the question(s) below.

Suppose the term structure of interest rates is shown below:Term 1 year 2 years 3 years 5 years 10 years 20 yearsRate (EAR%) 5.00% 4.80% 4.60% 4.50% 4.25% 4.15%

9)

What is the shape of the yield curve and what expectations are investors likely to have about future interest rates?

A)

Inverted; Higher B)

Normal; Higher C)

Inverted; Lower D)

Normal; Lower Answer:

C Explanation:

A)

B)

C)

D)

Diff: 2 Topic: 5.2 The Determinants of Interest Rates Skill: Conceptual

11)

Consider an investment that pays $1000 certain at the end of each of the next four years. If the investment costs $3,500 and has an NPV of $74.26, then the four year risk-free interest rate is closest to:

A)

4.5% B)

4.58% C)

4.55% D)

4.53% Answer:

D Explanation:

A)

B)

C)

D)

NPV = 74.26 = -3500 + 1000 / (1.05)1 + 1000 / (1.048)2 + 1000 / (1.046)3 + 1000 / (1 + x)4

3574.26 - 1000 / (1.05)1 + 1000 / (1.048)2 + 1000 / (1.046)3 = 1000 / (1 + x)4

837.60 = 1000 / (1 + X)4 ==>> (1 + X)4 = 1000 / 837.60 ==>> X = .0453 or 4.53% Diff: 3 Topic: 5.2 The Determinants of Interest Rates Skill: Analytical

Use the table for the question(s) below.

Suppose the term structure of interest rates is shown below:

Term 1 year 2 years 3 years 5 years 10 years 20 yearsRate (EAR%) 5.00% 4.80% 4.60% 4.50% 4.25% 4.15%

14)

After examining the yield curve, what predictions do you have about interest rates in the future? About future economic growth and the overall state of the economy?

Answer:

This is an inverted yield curve, which implies that interest rates should be falling in the future. An inverted yield curve is often interpreted as a negative forecast for economic growth. Since each of the last six recessions in the U.S. were proceeded by a period with an inverted yield curve it could be a leading indicator of a future recession.

Diff: 2 Topic: 5.2 The Determinants of Interest Rates Skill: Conceptual

15)

What is the NPV of an investment that costs $2500 and pays $1000 certain at the end of one, three, and five years ?

Answer:

NPV = -2500 + 1000 / (1.05)1 + 1000 / (1.046)3 + 1000 / (1.045)5 = 128.62 Diff: 2 Topic: 5.2 The Determinants of Interest Rates Skill: Analytical

5.3 Risk and Taxes

2)

Which of the following statements is false? A)

The equivalent after-tax interest rate is r - (τ × r). B)

Interest rates vary based on the identity of the borrower. C)

The ability to deduct the interest expense increases the effective after-tax interest rate paid on the loan. D)

For loans to borrowers other than the U.S. Treasury, the stated interest rate is the maximum amount that investors will receive.

Answer:

C Explanation:

A)

B)

C)

D)

Diff: 2 Topic: 5.3 Risk and Taxes Skill: Conceptual

3)

Which of the following statements is false? A)

U.S. Treasury securities are widely regarded to be risk-free because there is virtually no chance the government will default on these bonds.

B)

In general, if the interest rate is r and the tax rate is τ, then for each $1 invested you will earn interest equal to r and owe taxes of τ × r on the interest.

C)

Investors may receive less than the stated interest rate if the borrowing company has financial difficulties and is unable to fully repay the loan.

D)

Taxes reduce the amount of interest the investor can keep, and we refer to this reduced amount as the tax effective interest rate.

Answer:

D Explanation:

A)

B)

C)

D)

Diff: 2 Topic: 5.3 Risk and Taxes Skill: Conceptual

5)

Assume that you presently have a monthly home mortgage with a stated interest rate of 7% APR. If your income tax rate is 20%, then the after tax EAR for your home mortgage is closest to:

A)

5.6% B)

7.2% C)

5.8% D)

7.0% Answer:

C Explanation:

A)

B)

C)

Step #1 find the EAR

EAR = (1 + .07 / 12)12 - 1 = 7.2%

Step #2 find the after tax cost

aftertax = before tax (1 - T) = .072 (1 - .2) = .0578 or approximately 5.8% D)

Diff: 2 Topic: 5.3 Risk and Taxes Skill: Analytical

Use the table for the question(s) below.

Suppose you have the following Loans / Investments

Credit Card14.90% APR (Monthly Compounding)

Automobile Loan5.90% APR (Monthly Compounding)

Home Equity Loan8.25% APR (Monthly Compounding)

Money Market Fund 5.10% EAR

6)

If your income tax rate is 30%, then the after-tax EAR for your home equity loan is closest to: A)

6.0% B)

5.9% C)

8.6% D)

5.8% Answer:

A Explanation:

A)

Step #1 find the EAR

EAR = (1 + .0825 / 12)12 - 1 = 8.569%

Step #2 find the after tax cost

aftertax = before tax (1 - T) = .08569 (1 - .3) = .0599 or approximately 6.0% B)

C)

D)

Diff: 2 Topic: 5.3 Risk and Taxes Skill: Analytical

7)

If your income tax rate is 30%, then the after-tax return you receive on your money market fund is closest to:

A)

3.7% B)

5.1% C)

3.6% D)

4.2% Answer:

C Explanation:

A)

B)

C)

This is already stated as an EAR, so aftertax = before tax (1 - T) = .051 (1 - .3) = .0357 or approximately 3.6%

D)

Diff: 2 Topic: 5.3 Risk and Taxes Skill: Analytical

8)

What is the effective after-tax rate of each instrument, expressed as an EAR? Answer:

Credit CardInterest is not deductible so,EAR = (1 + .149 / 12)12 - 1 = 15.96%

Car LoanInterest is not deductible so,EAR = (1 + .059 / 12)12 - 1 = 6.06%

Home Equity LoanStep #1 find the EAREAR = (1 + .0825 / 12)12 - 1 = 8.569%Step #2 find the after tax costaftertax = before tax (1 - T) = .08569 (1 - .3) = .0599 or approximately 6.0%

Money Market FundThis is already stated as an EAR, so aftertax = before tax (1 - T) = .051 (1 - .3) = .0357 or approximately 3.6%

Diff: 2 Topic: 5.3 Risk and Taxes Skill: Analytical