Embed Size (px)

DESCRIPTION

accounting

Citation preview

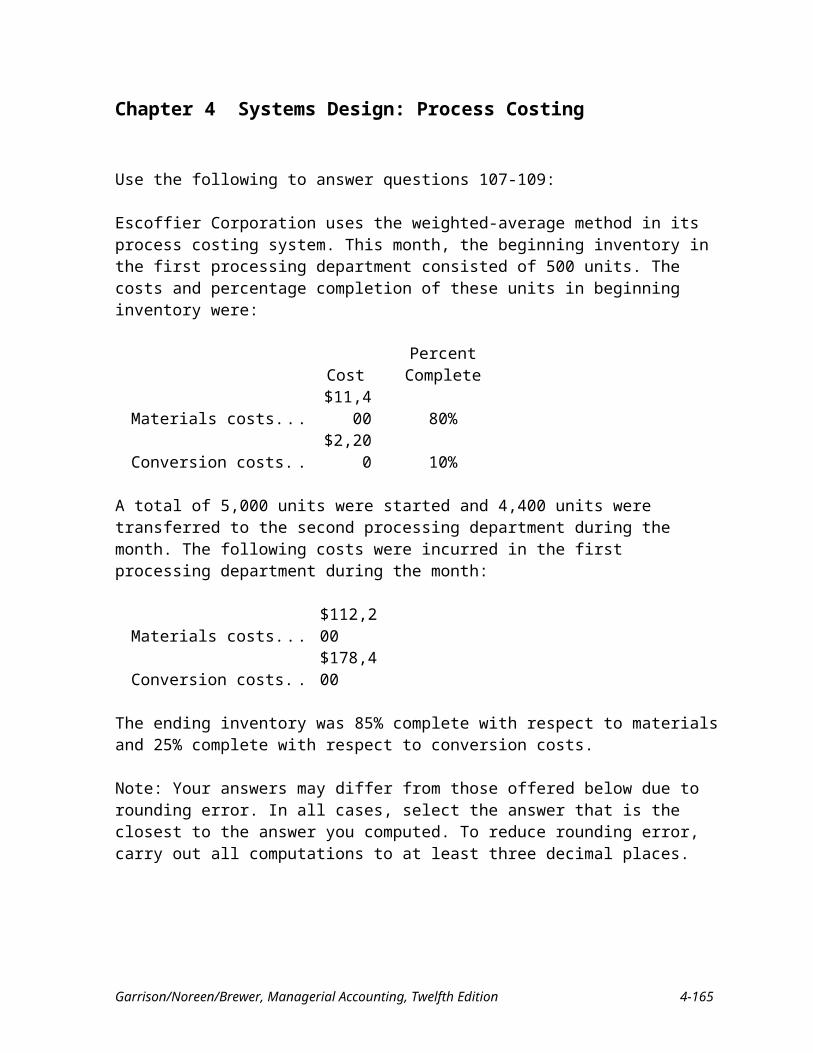

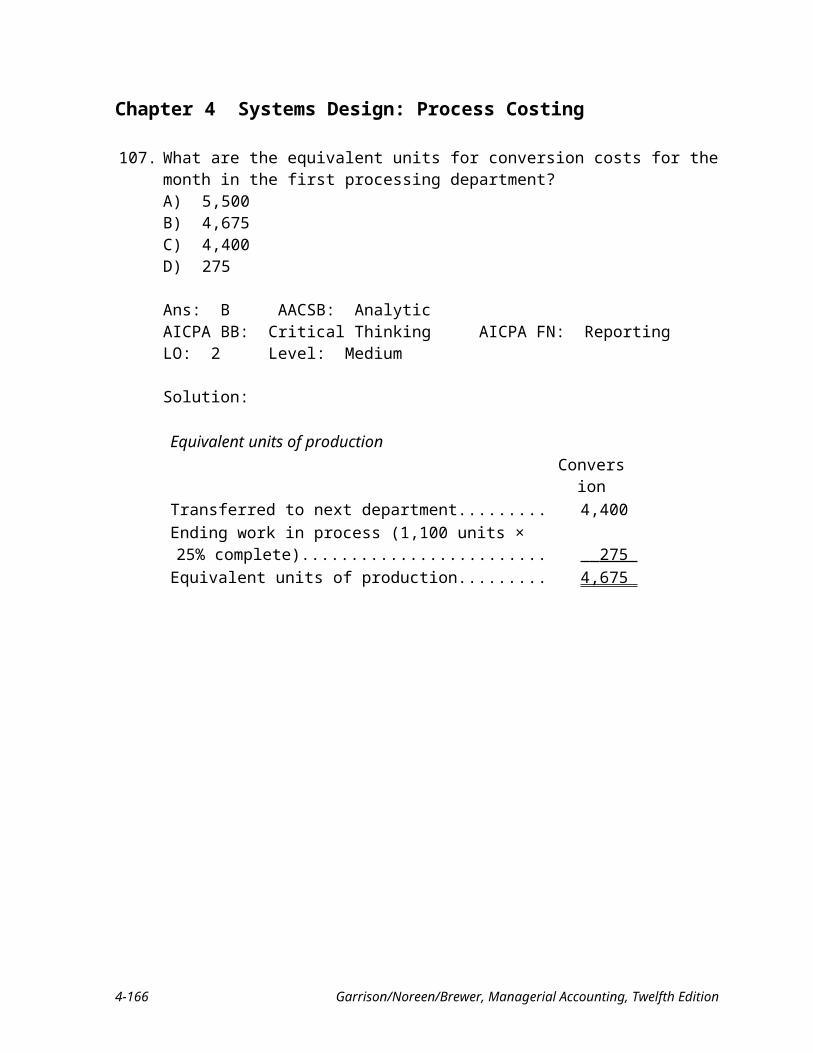

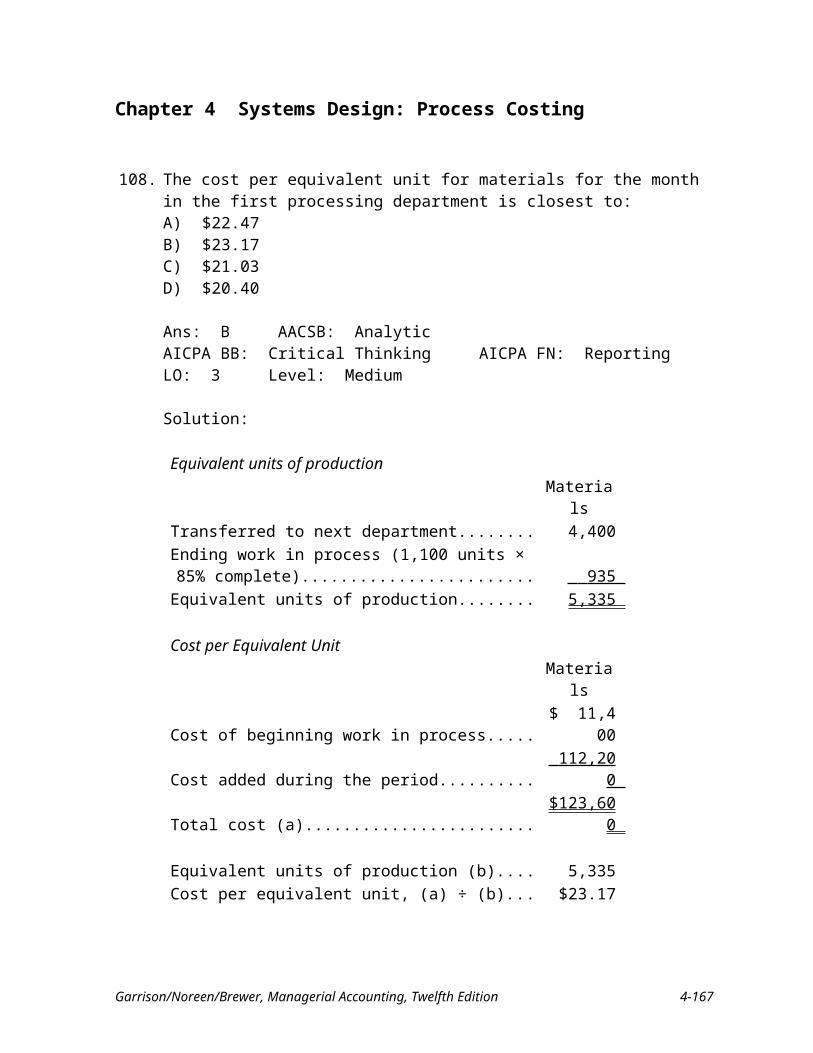

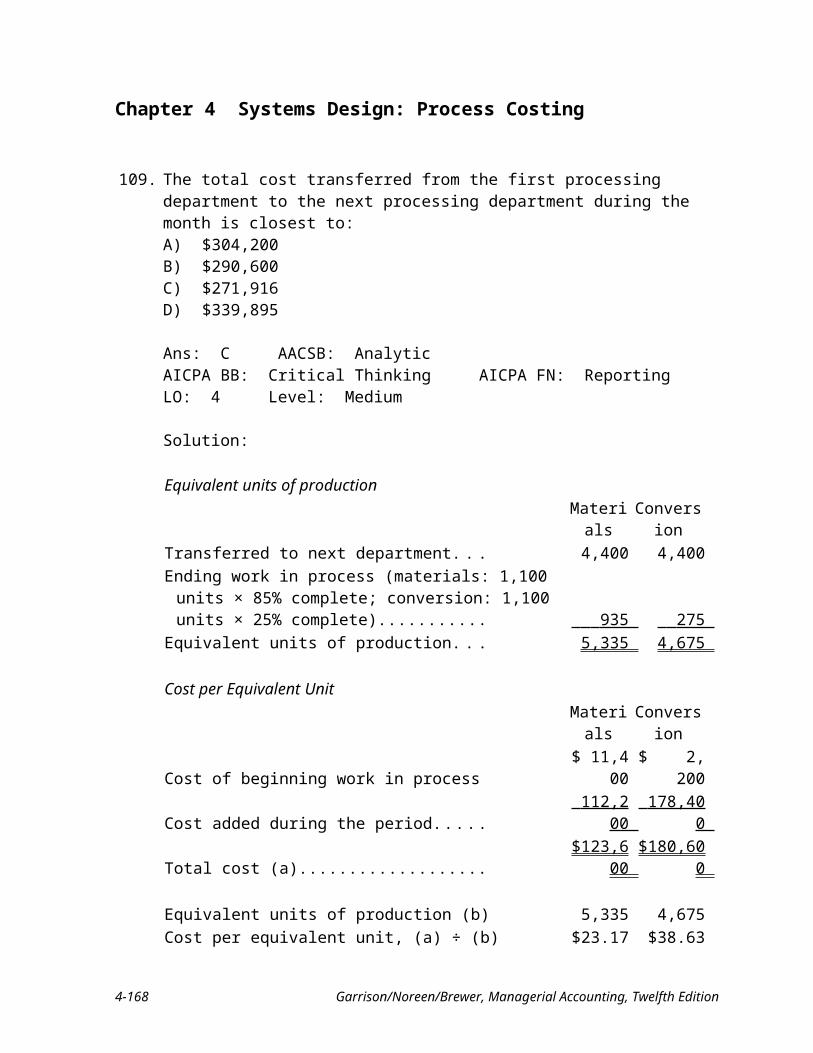

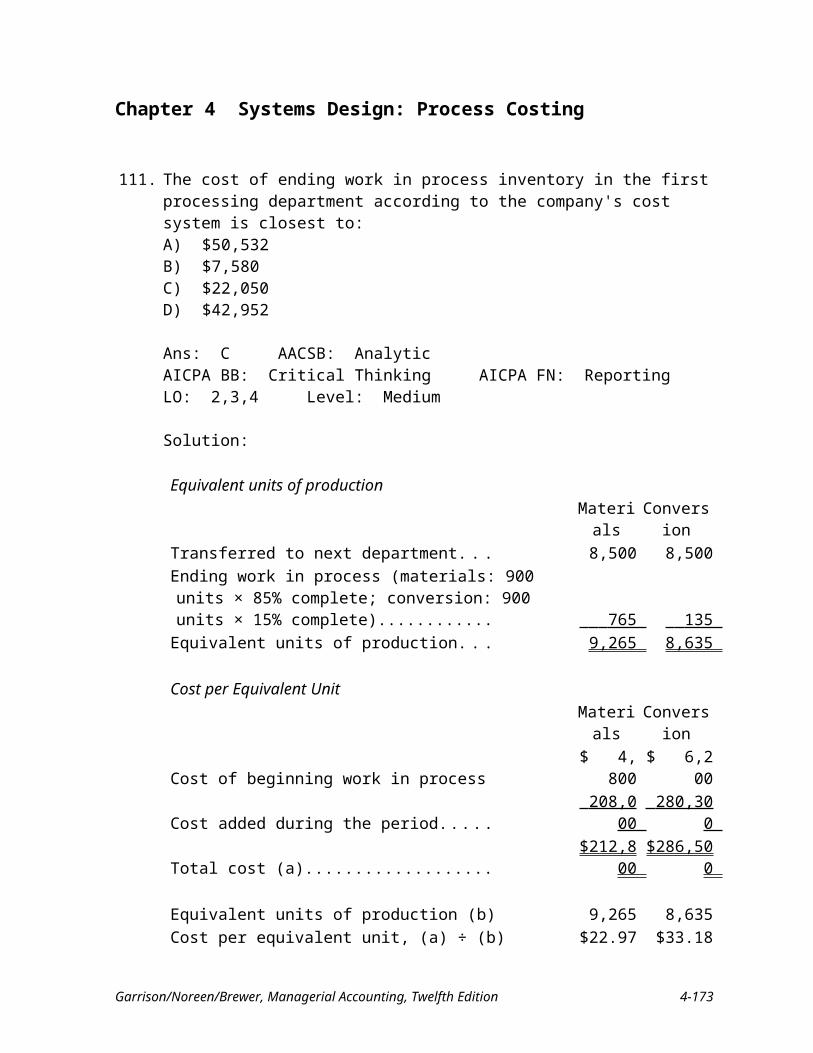

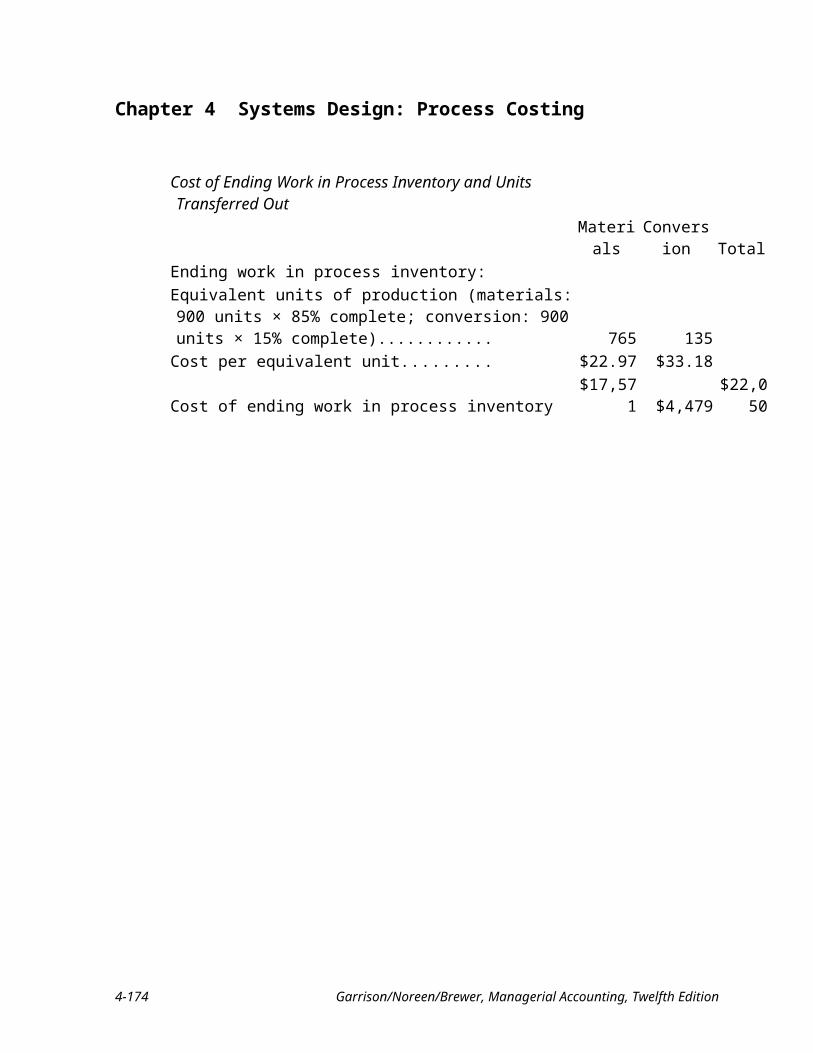

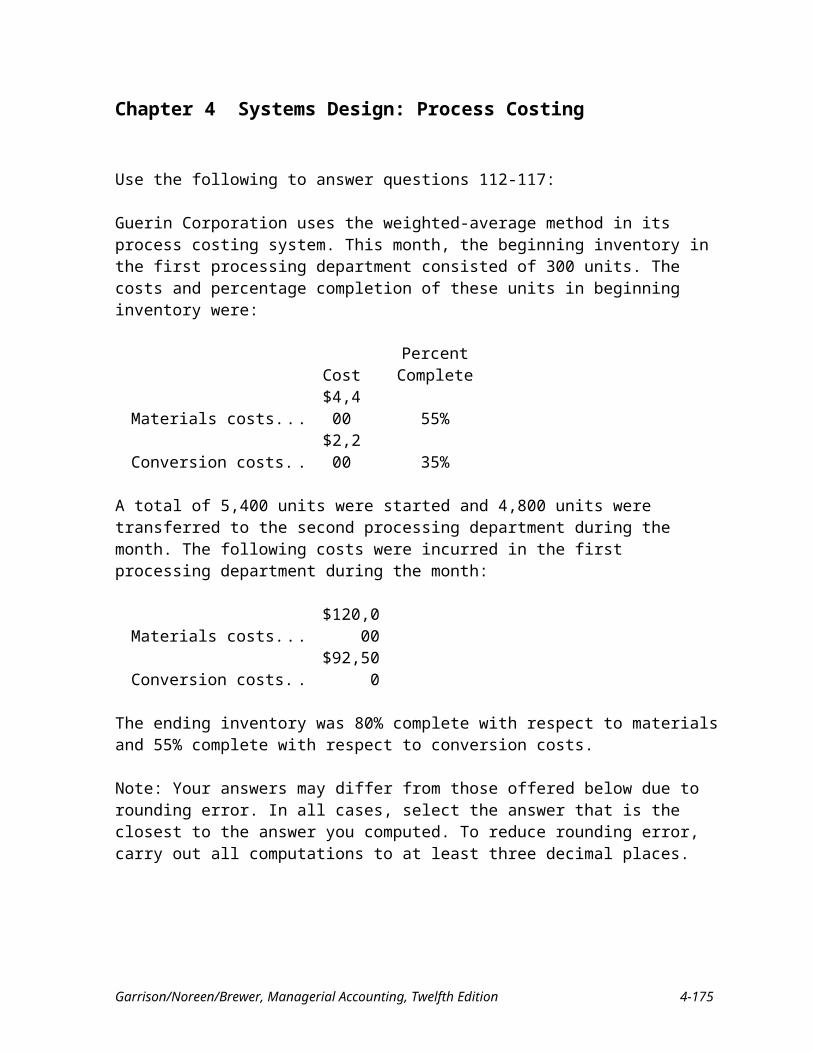

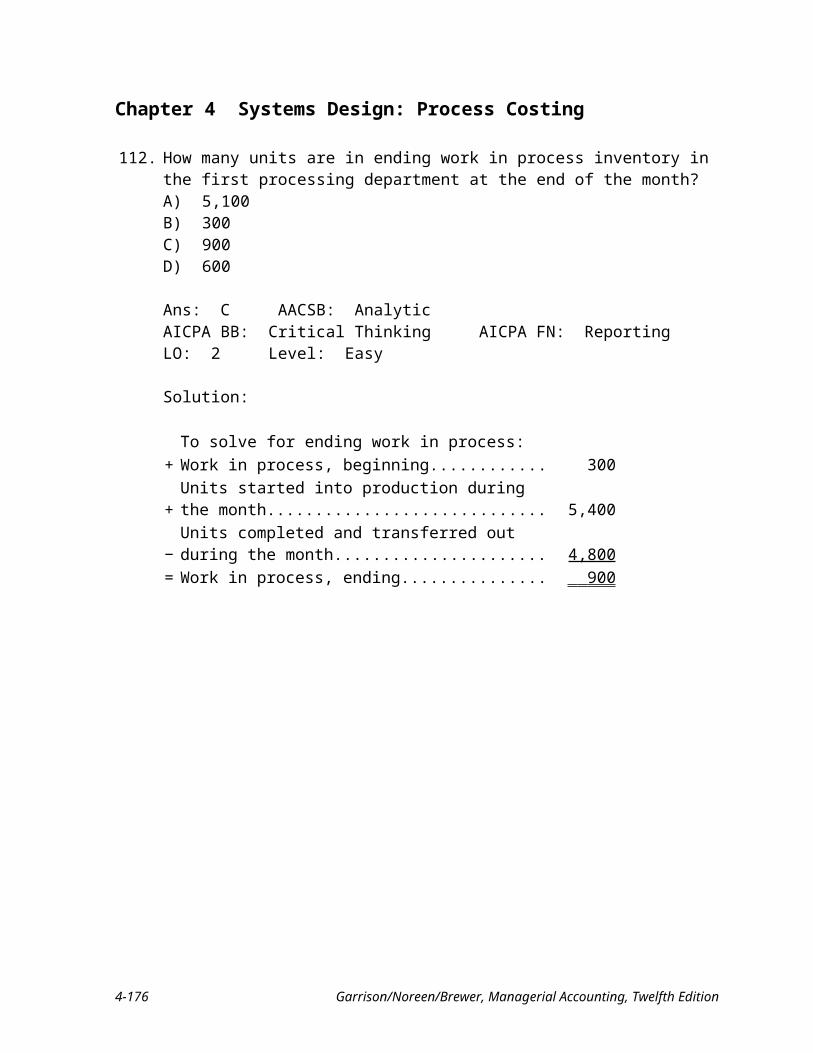

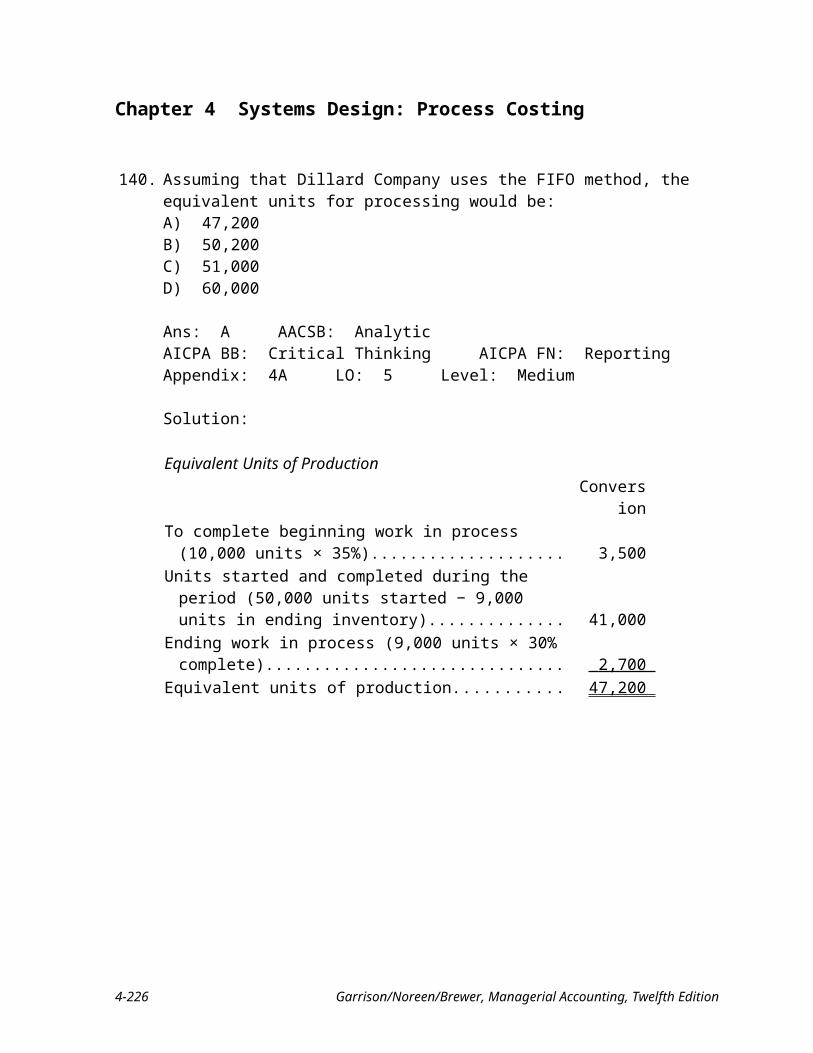

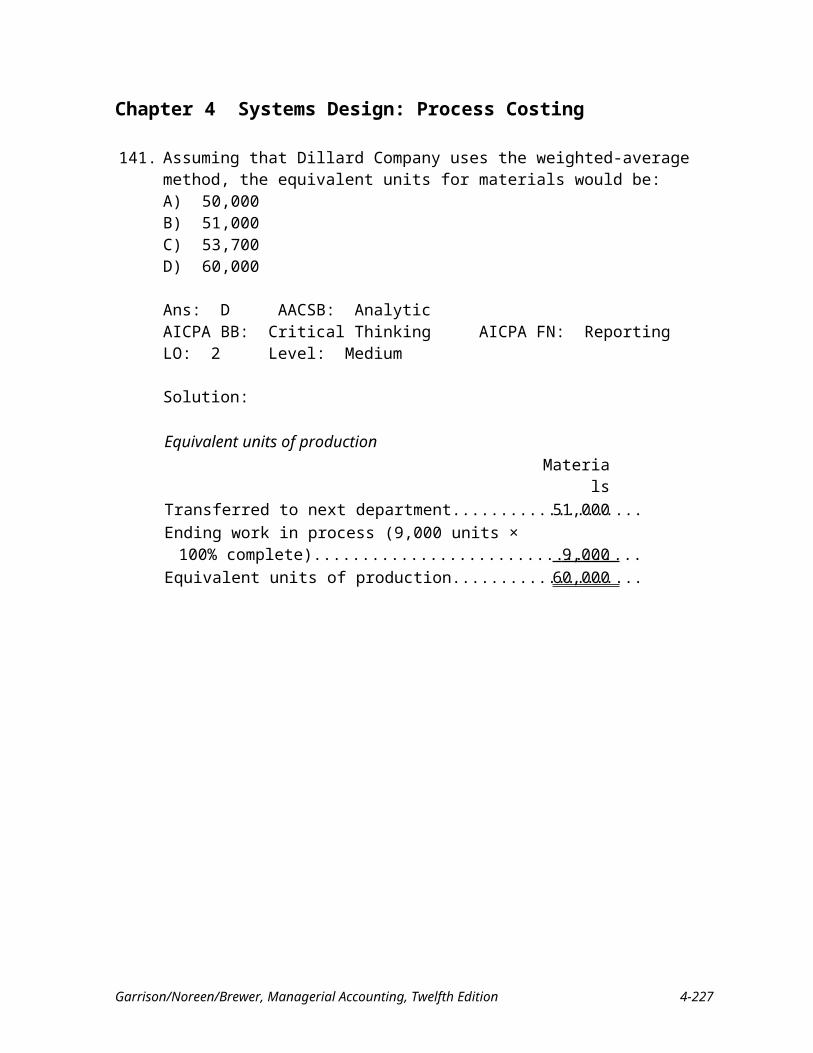

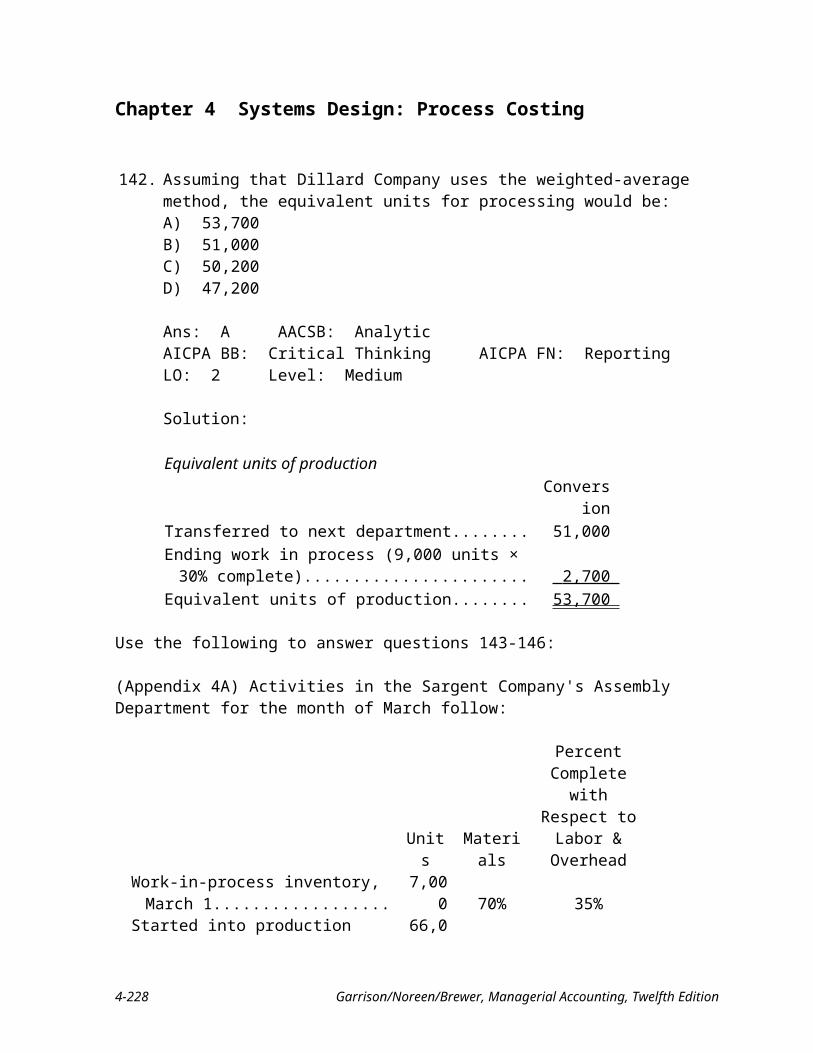

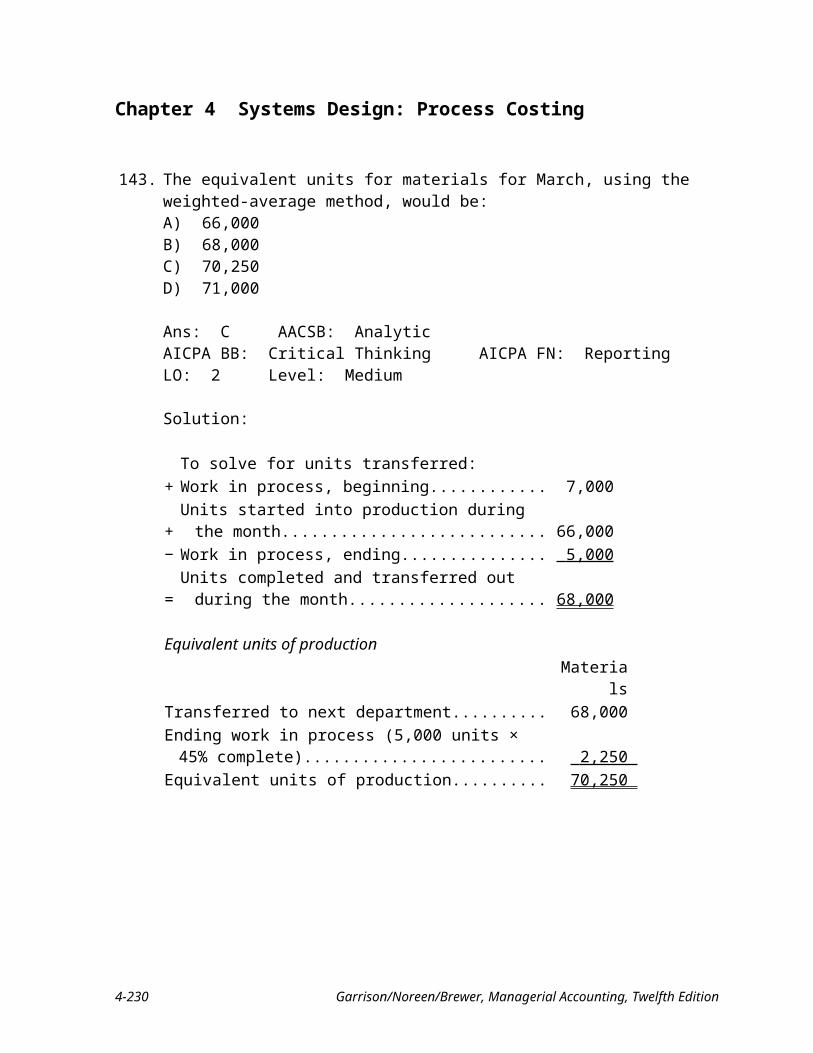

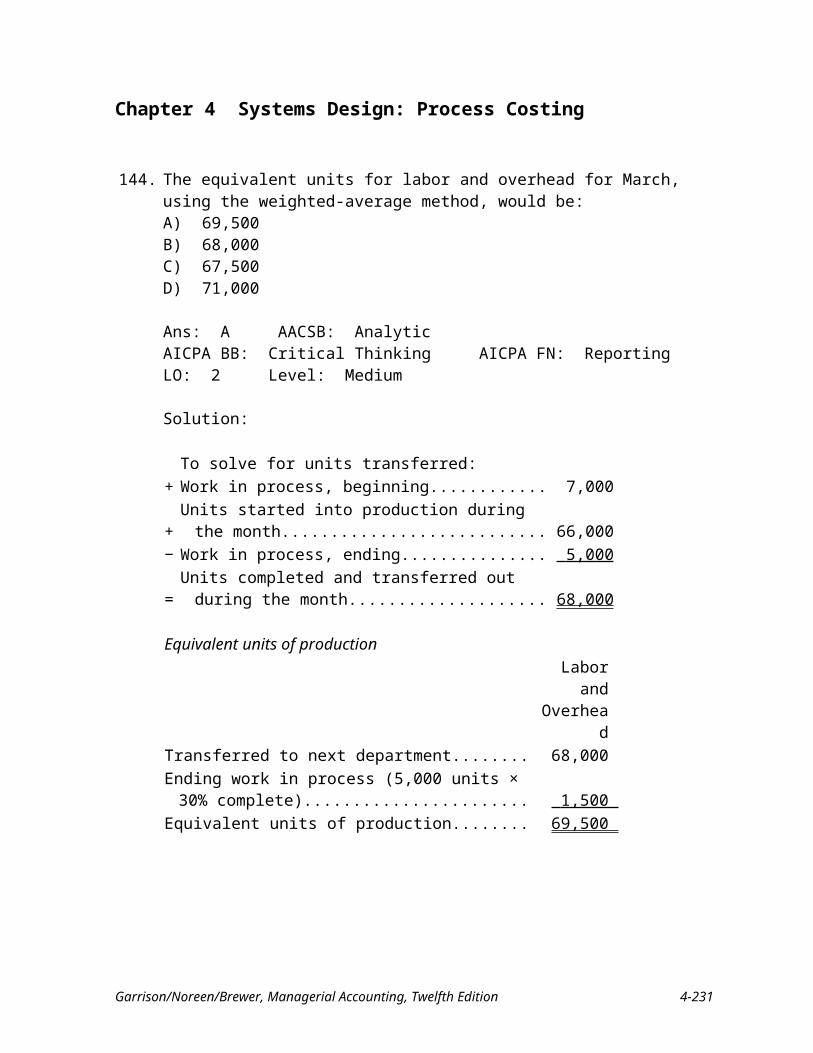

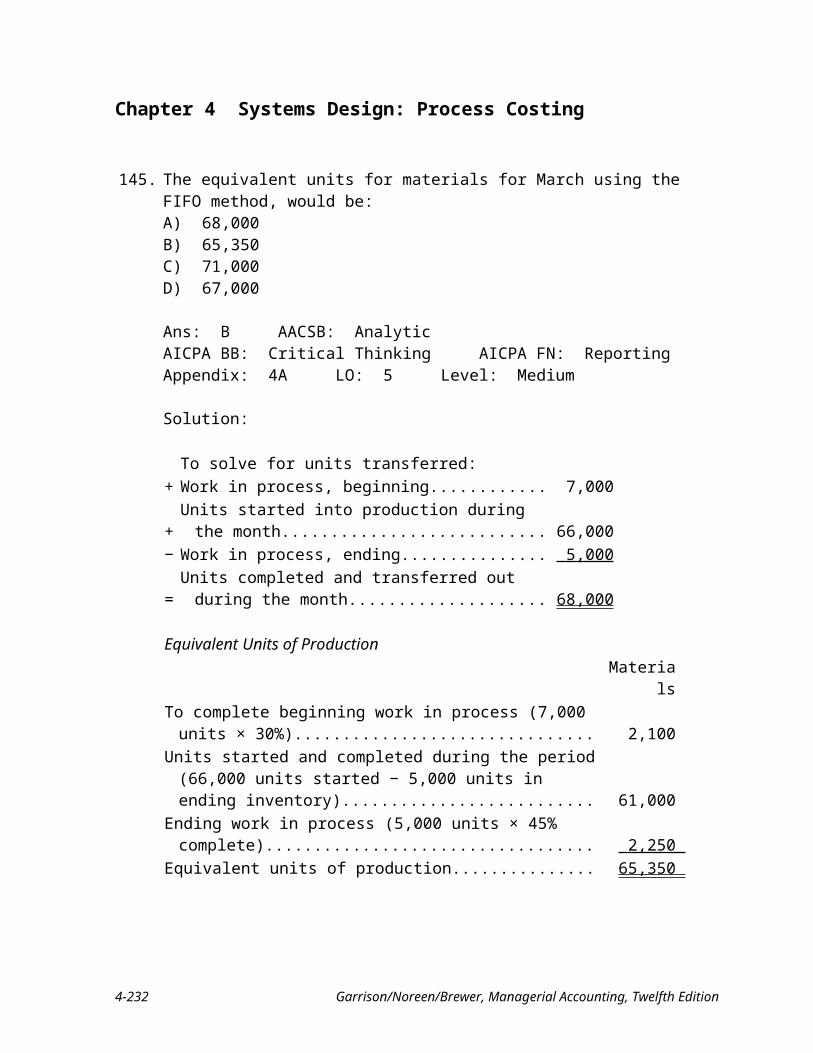

Chapter 4 Systems Design: Process Costing

True/False Questions

1. In a process costing system, the costs of one processing department become part of the costs of the next processing department.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1 Level: Easy

2. The equivalent units of production will be the same under the weighted-average and the FIFO method if there is no beginning work in process inventory.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 2,5 Level: Medium

3. Under the weighted-average method, the equivalent units used to compute the unit costs of ending inventories relate only to work done during the current period.

Ans: False AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Hard

4. In order to equitably allocate costs in a process costing system, dissimilar products are restated in terms of equivalent units by weighting the number of units produced by their market values.

Ans: False AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Easy

5. In a process costing system, units transferred to the next processing department are presumed to be 100% complete with respect to the work performed by the transferring department.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Easy

6. Under a weighted-average process costing system when all materials are added at the beginning of the production process, the equivalent units for materials is equal to the units completed and transferred out.

Ans: False AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Hard

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-7

Chapter 4 Systems Design: Process Costing

7. In calculating cost per equivalent unit under the weighted-average method, prior period costs are combined with current period costs.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3 Level: Easy

8. The equivalent units of production for a department using the FIFO process costing method is equal to the number of units completed plus the equivalent units in the ending inventory.

Ans: False AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5 Level: Hard

9. The step-down method of cost allocation is more accurate than the direct method since the step-down method considers services that service departments provide to each other.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4B LO: 8,9 Level: Easy

10. The step-down method and the direct method of cost allocation will result in the same amount of service department cost being allocated to a given operating department, although the step-down method is easier to apply than the direct method.

Ans: False AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4B LO: 8,9 Level: Medium

11. The order in which the costs of service departments are allocated will affect the amounts allocated to an operating department when the direct method is used.

Ans: False AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4B LO: 8 Level: Medium

12. The units in beginning work in process inventory plus the units started into production must equal the units transferred out of the department plus the units in ending work in process inventory.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 10 Level: Easy

4-8 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

13. In a process costing system, direct labor cost combined with manufacturing overhead cost is known as conversion cost.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 10 Level: Easy

14. Process costing is employed in industries that produce basically homogeneous products such as bricks, flour, or cement but would not be appropriate for assembly-type operations such as those that manufacture computers.

Ans: False AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 10 Level: Medium

15. Process costing is used where many different products are produced each period to customer specifications.

Ans: False AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 10 Level: Easy

Multiple Choice Questions

16. Which of the following statements related to job-order costing and process costing are true?A) Under both costing methods, manufacturing overhead costs are included in the

computation of unit product costs.B) Under both costing methods, the journal entry to record the completion of

production will involve crediting a work in process account.C) Under both costing methods, the journal entry to record the cost of goods sold

will involve crediting the finished goods account.D) All of the above are true.

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1 Level: Hard

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-9

Chapter 4 Systems Design: Process Costing

17. The completion of goods is recorded as a decrease in the work in process inventory account when using:

Job-order costing Process costingA) Yes NoB) Yes YesC) No YesD) No No

Ans: B AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1 Level: Easy Source: CPA, adapted

18. In process costing, a separate work in process account is kept for each:A) individual order.B) equivalent unit.C) processing department.D) cost category (i.e., materials, conversion cost).

Ans: C AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1 Level: Easy

19. The weighted-average method of process costing differs from the FIFO method of process costing in that the weighted-average method:A) does not consider the degree of completion of beginning work in process

inventory when computing equivalent units of production.B) considers ending work in process inventory to be fully complete.C) will always yield a higher cost per equivalent unit.D) All of the above.

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 2,3,5,6 Level: Hard

4-10 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

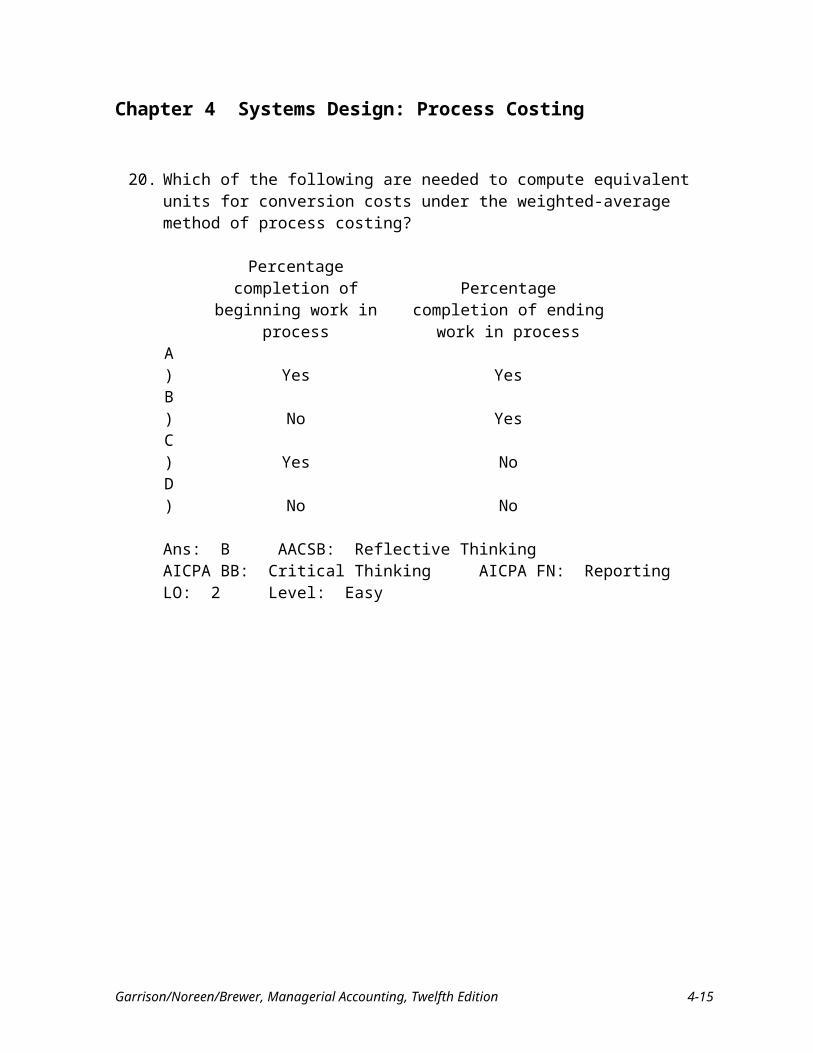

20. Which of the following are needed to compute equivalent units for conversion costs under the weighted-average method of process costing?

Percentage completion of beginning work in process

Percentage completion of ending work in process

A) Yes YesB) No YesC) Yes NoD) No No

Ans: B AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Easy

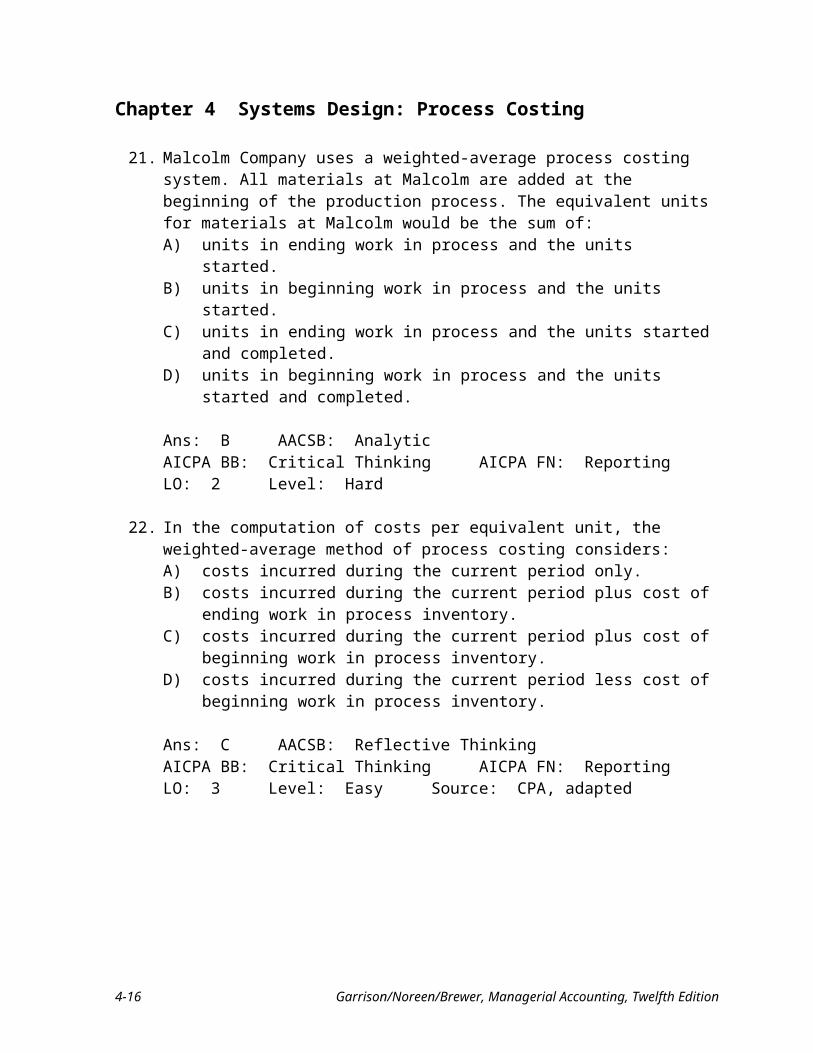

21. Malcolm Company uses a weighted-average process costing system. All materials at Malcolm are added at the beginning of the production process. The equivalent units for materials at Malcolm would be the sum of:A) units in ending work in process and the units started.B) units in beginning work in process and the units started.C) units in ending work in process and the units started and completed.D) units in beginning work in process and the units started and completed.

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Hard

22. In the computation of costs per equivalent unit, the weighted-average method of process costing considers:A) costs incurred during the current period only.B) costs incurred during the current period plus cost of ending work in process

inventory.C) costs incurred during the current period plus cost of beginning work in process

inventory.D) costs incurred during the current period less cost of beginning work in process

inventory.

Ans: C AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3 Level: Easy Source: CPA, adapted

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-11

Chapter 4 Systems Design: Process Costing

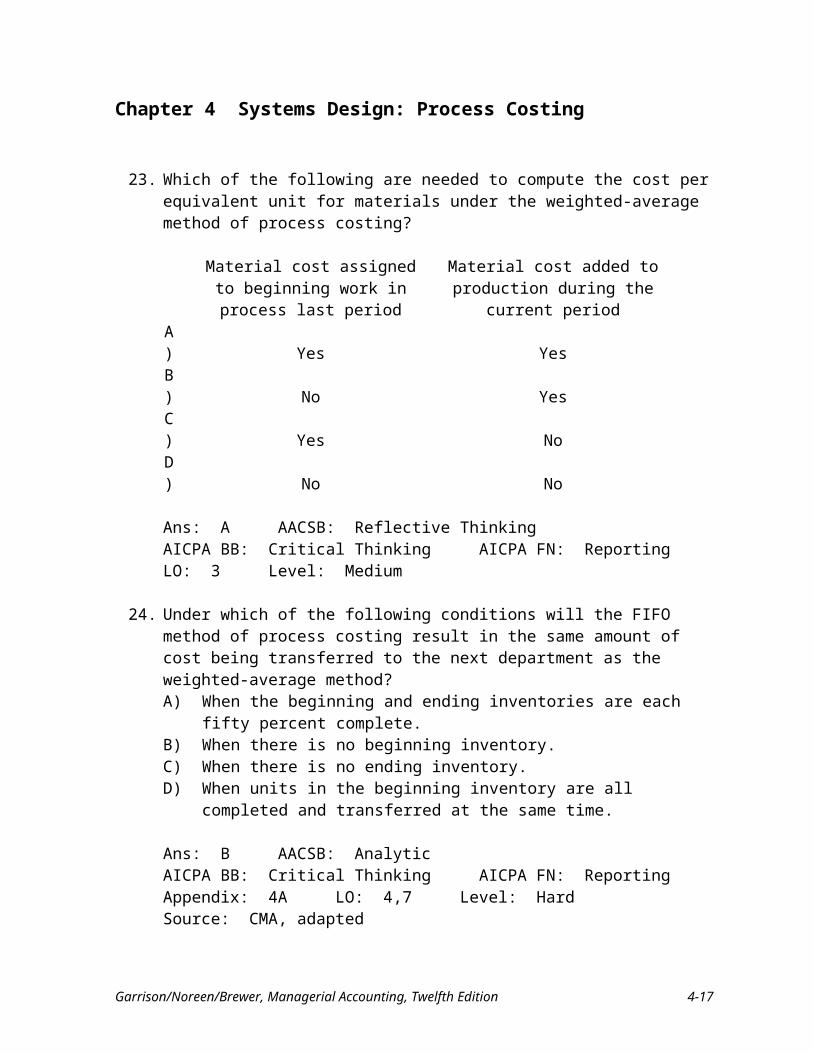

23. Which of the following are needed to compute the cost per equivalent unit for materials under the weighted-average method of process costing?

Material cost assigned to beginning work in process last period

Material cost added to production during the current period

A) Yes YesB) No YesC) Yes NoD) No No

Ans: A AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3 Level: Medium

24. Under which of the following conditions will the FIFO method of process costing result in the same amount of cost being transferred to the next department as the weighted-average method?A) When the beginning and ending inventories are each fifty percent complete.B) When there is no beginning inventory.C) When there is no ending inventory.D) When units in the beginning inventory are all completed and transferred at the

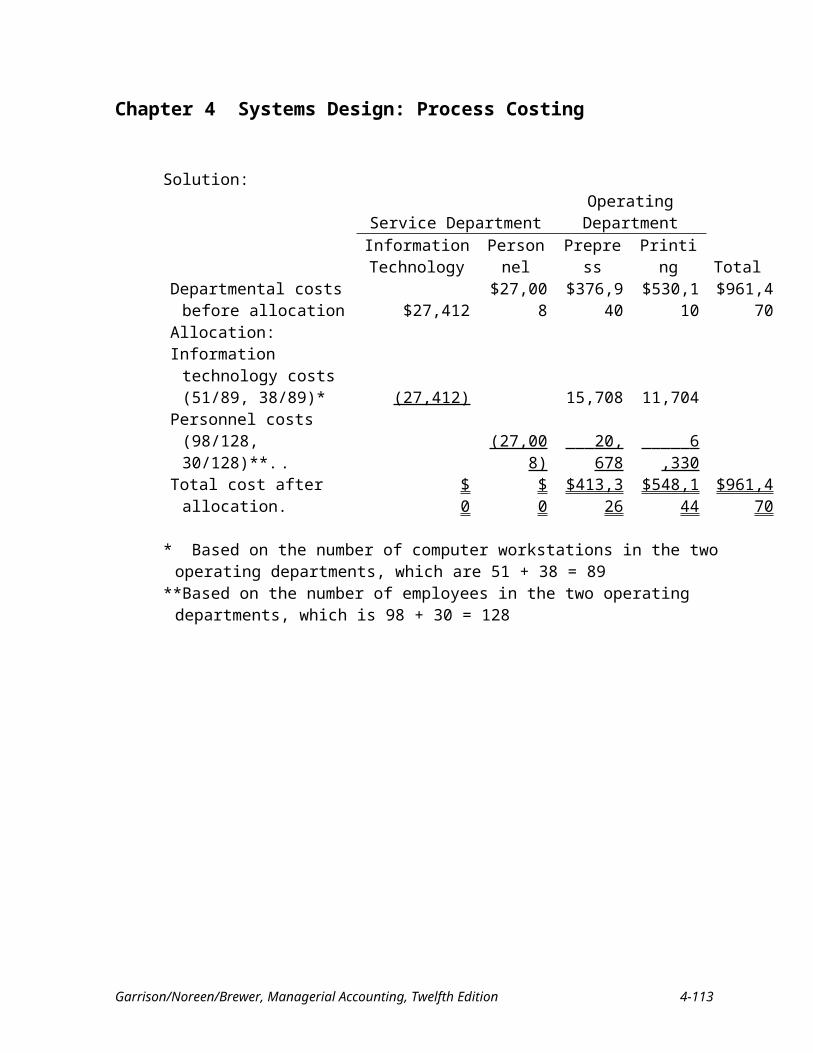

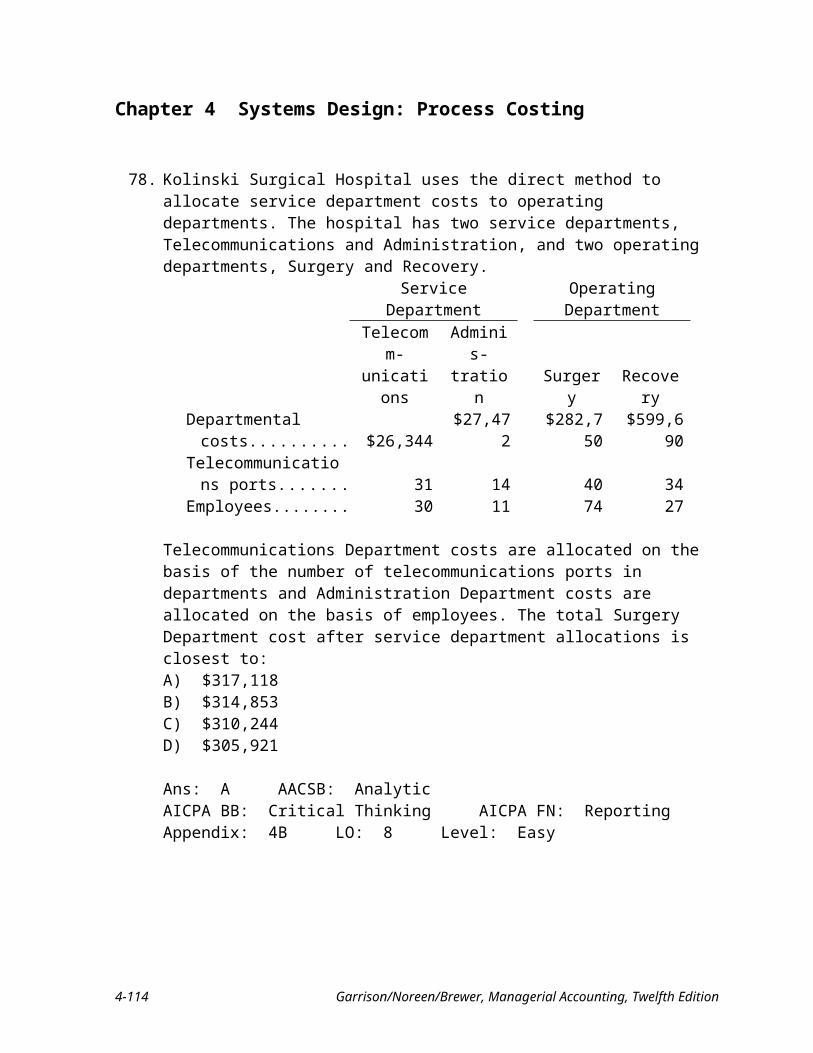

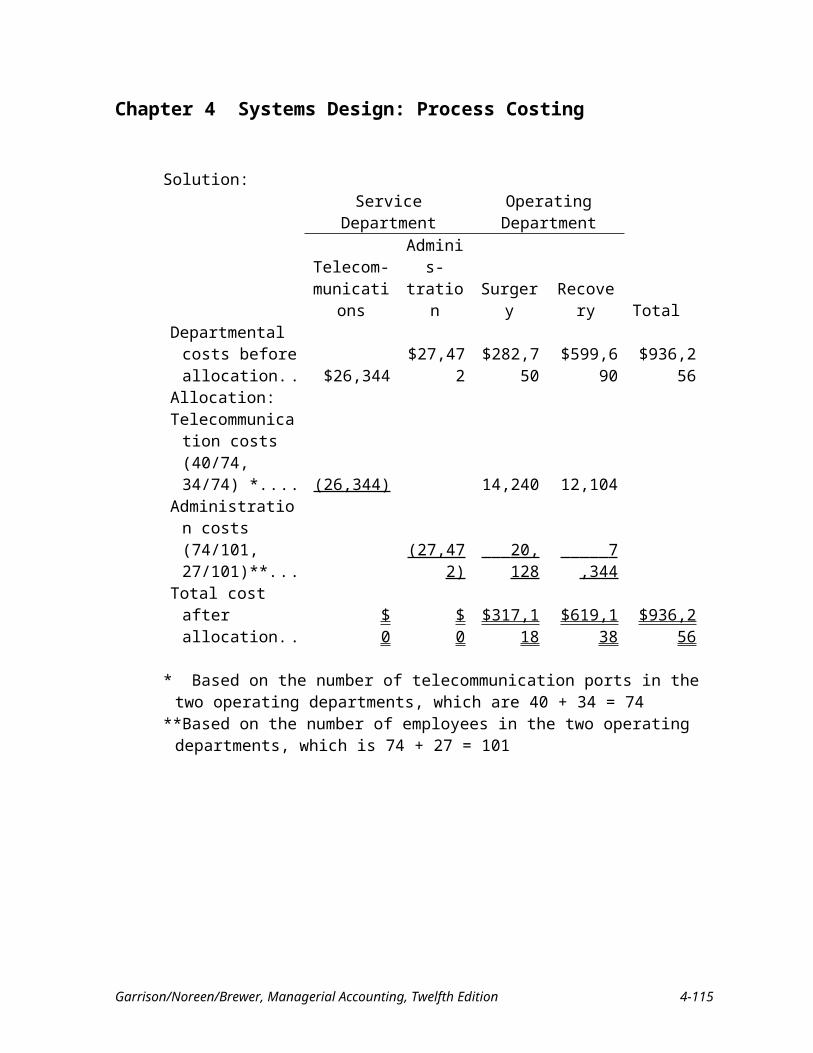

same time.

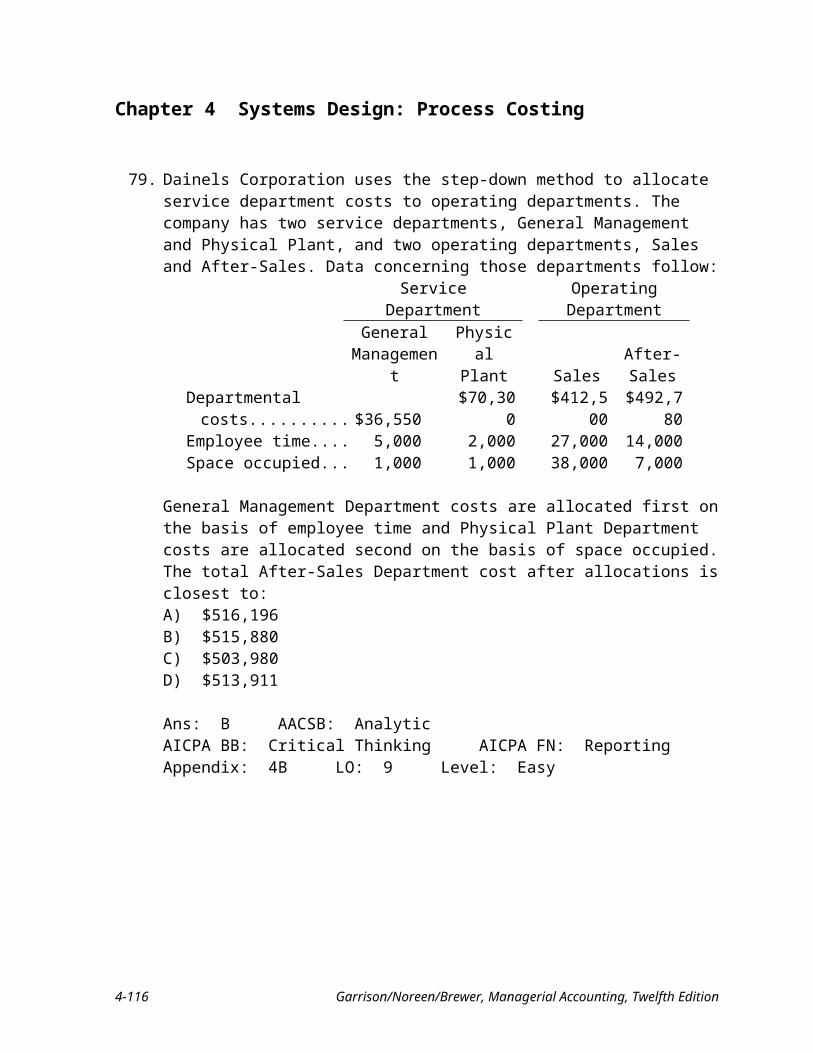

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 4,7 Level: Hard Source: CMA, adapted

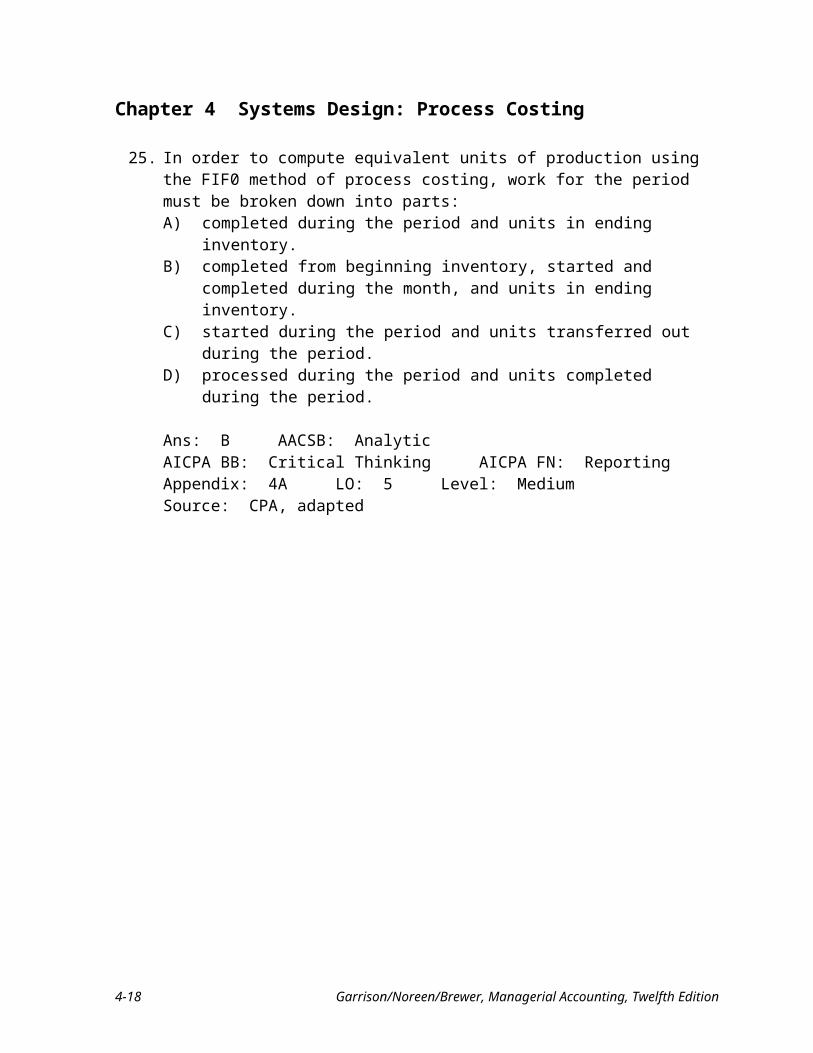

25. In order to compute equivalent units of production using the FIF0 method of process costing, work for the period must be broken down into parts:A) completed during the period and units in ending inventory.B) completed from beginning inventory, started and completed during the month,

and units in ending inventory.C) started during the period and units transferred out during the period.D) processed during the period and units completed during the period.

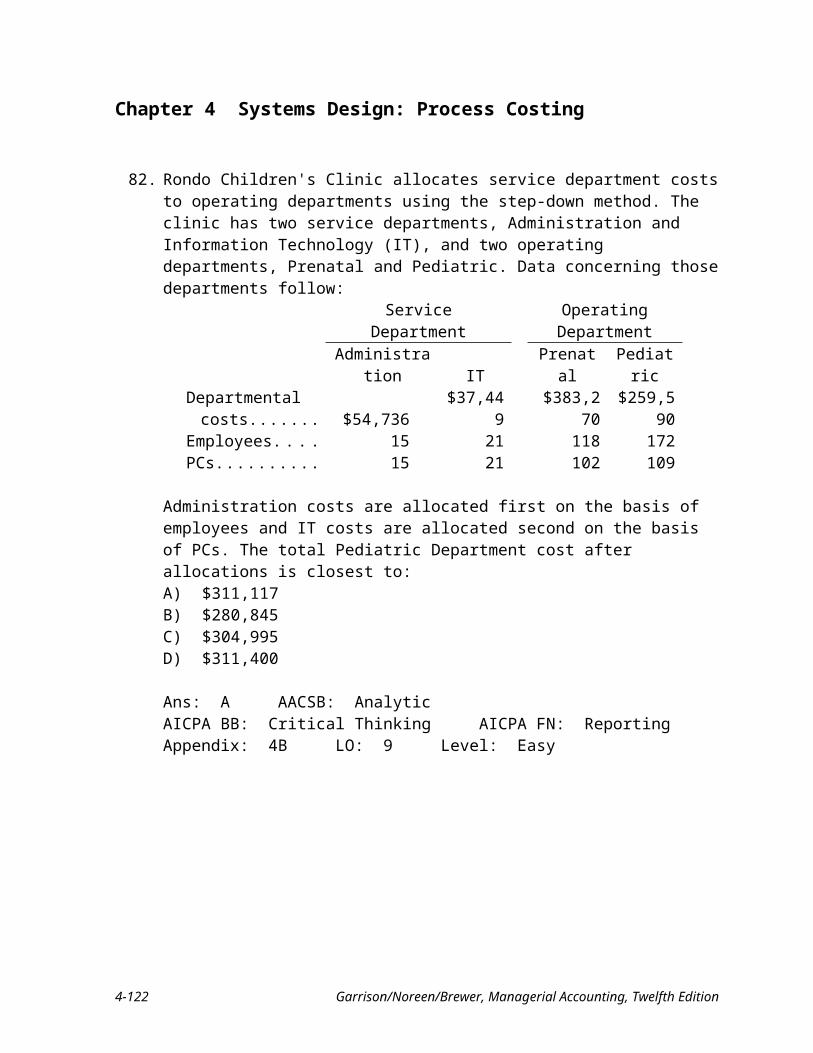

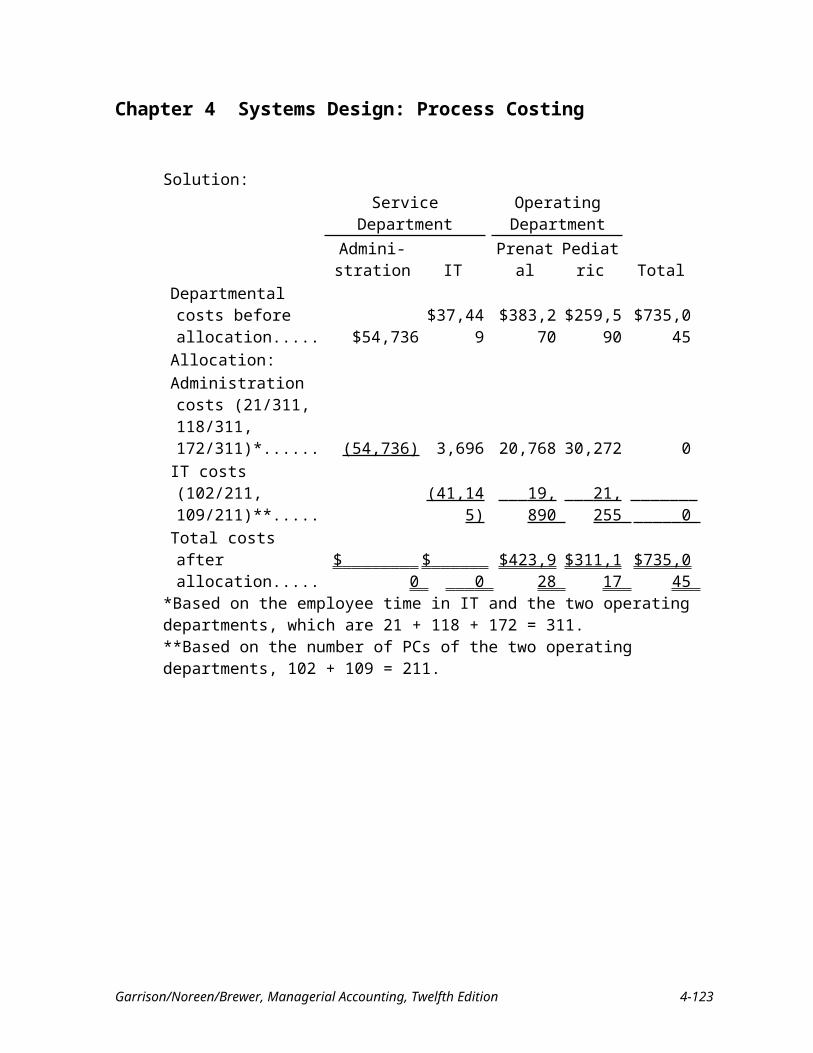

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5 Level: Medium Source: CPA, adapted

4-12 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

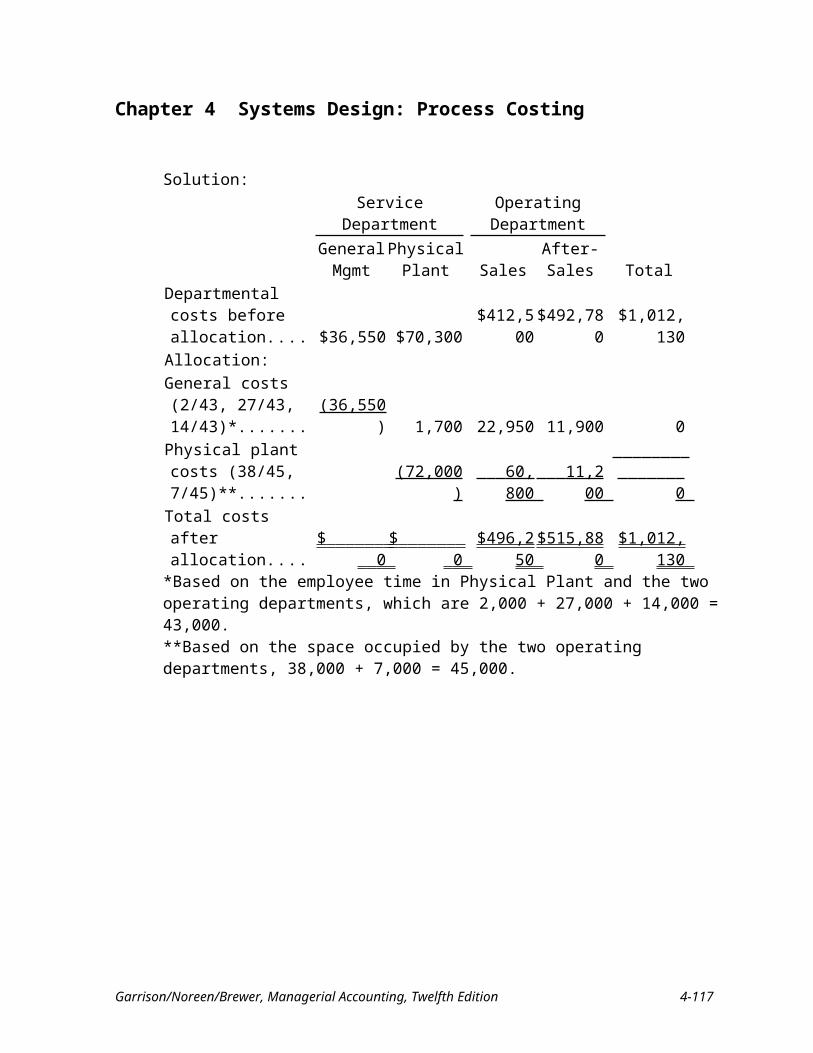

26. Which of the following methods of allocating service departments take into account all of the effects of interdepartmental services?

Direct Step-DownA) Yes YesB) Yes NoC) No YesD) No No

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4B LO: 8,9 Level: Medium

27. All of the following statements are correct when referring to process costing except:A) Process costing would be appropriate for a jeweler who makes custom jewelry

to order.B) A process costing system has the same basic purposes as a job-order costing

system.C) Units produced are indistinguishable from each other.D) Costs are accumulated by department.

Ans: A AACSB: Reflective Thinking AICPA BB: Critical Thinking AICPA FN: Reporting LO: 10 Level: Medium

28. For which of the following would it be best to use an operation costing system?A) home remodelingB) automobile productionC) cement used for roadwaysD) trash bags used for yard waste

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 10 Level: Medium

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-13

Chapter 4 Systems Design: Process Costing

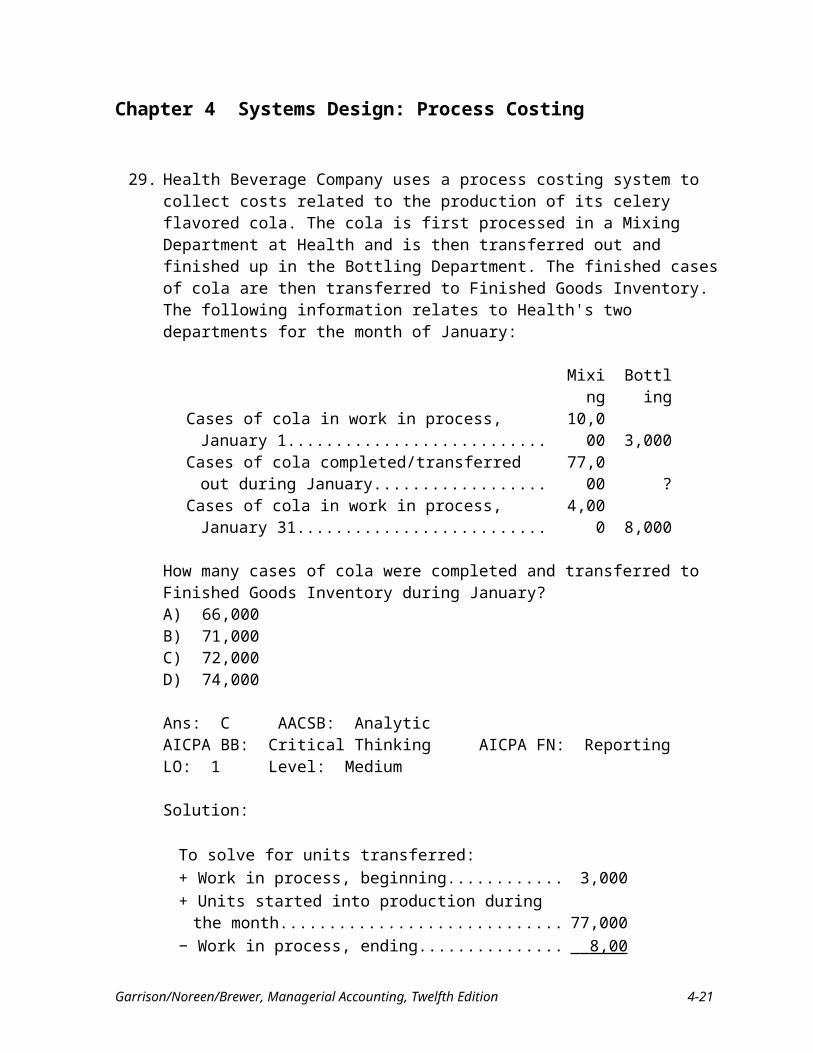

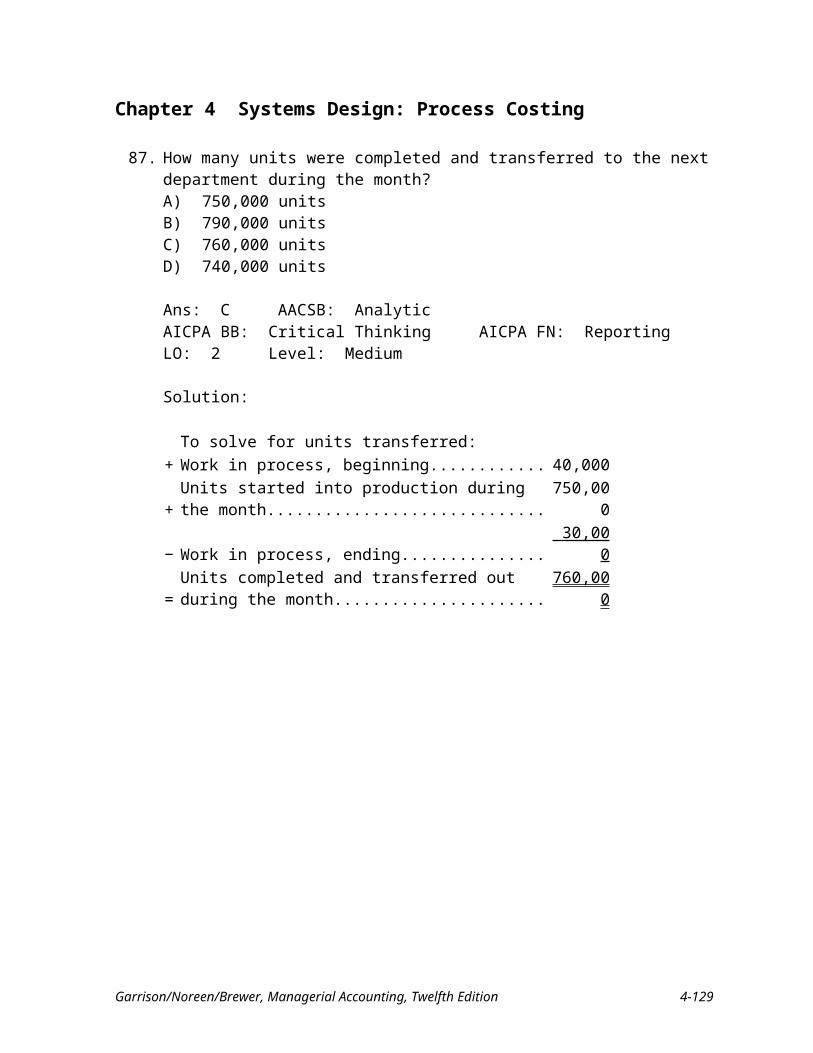

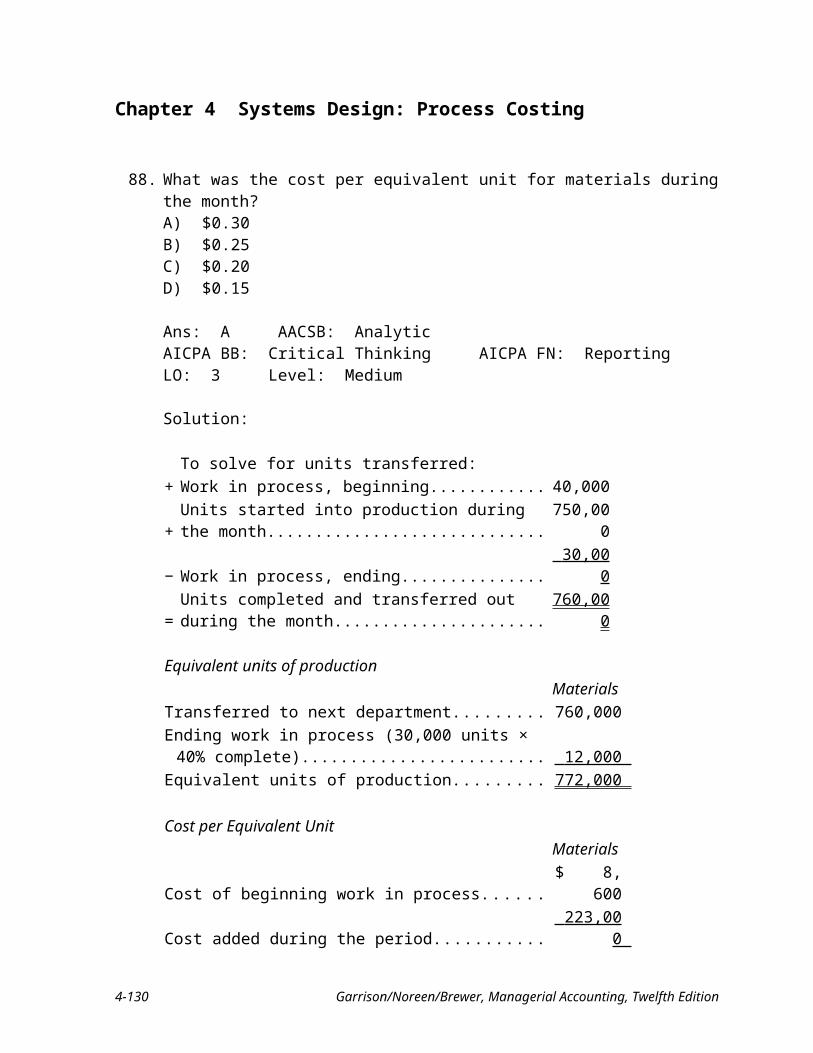

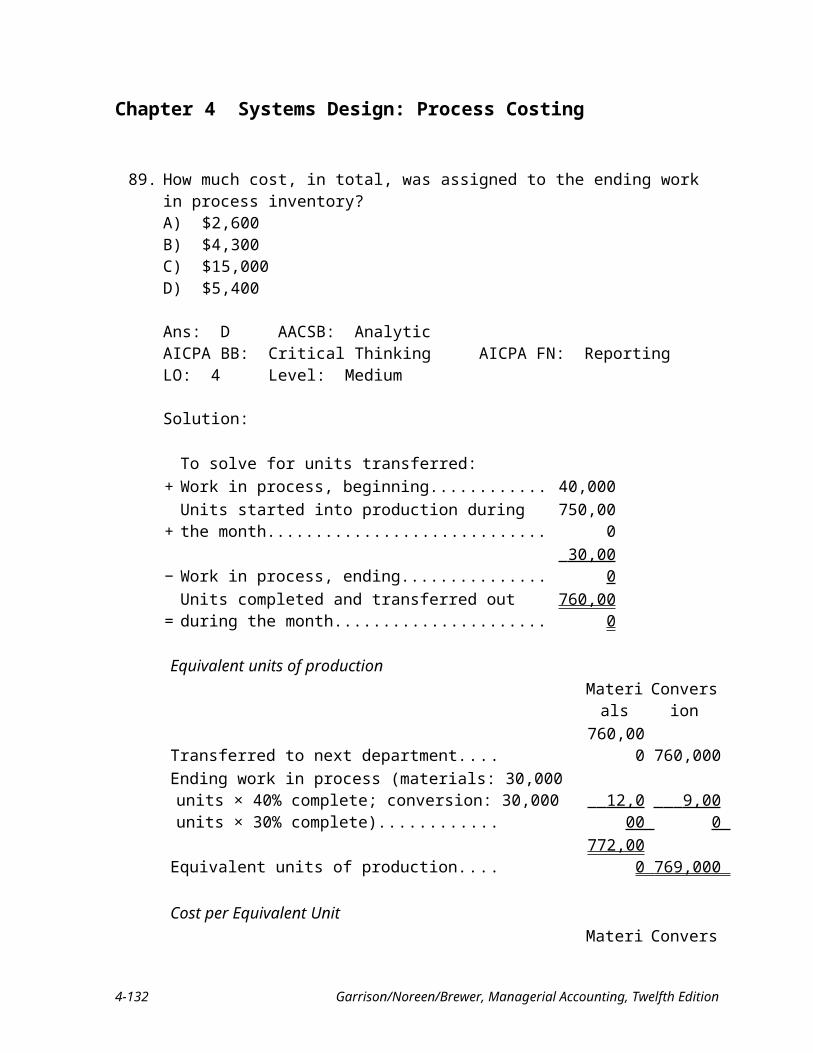

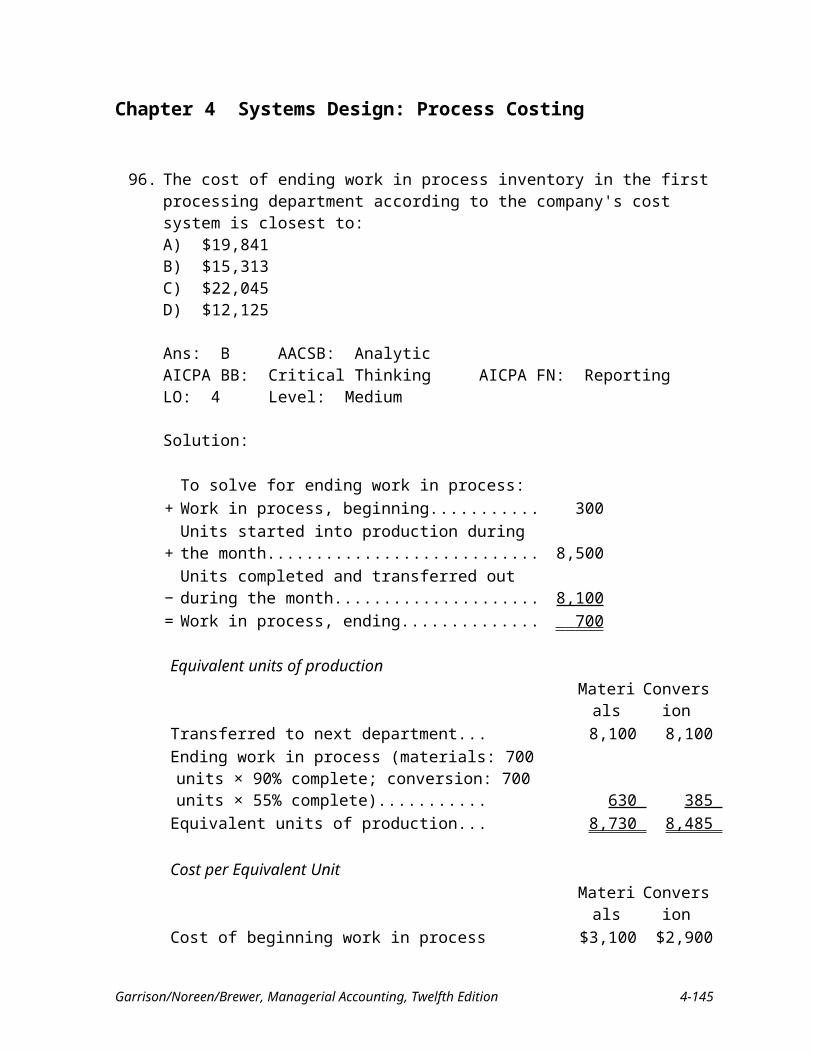

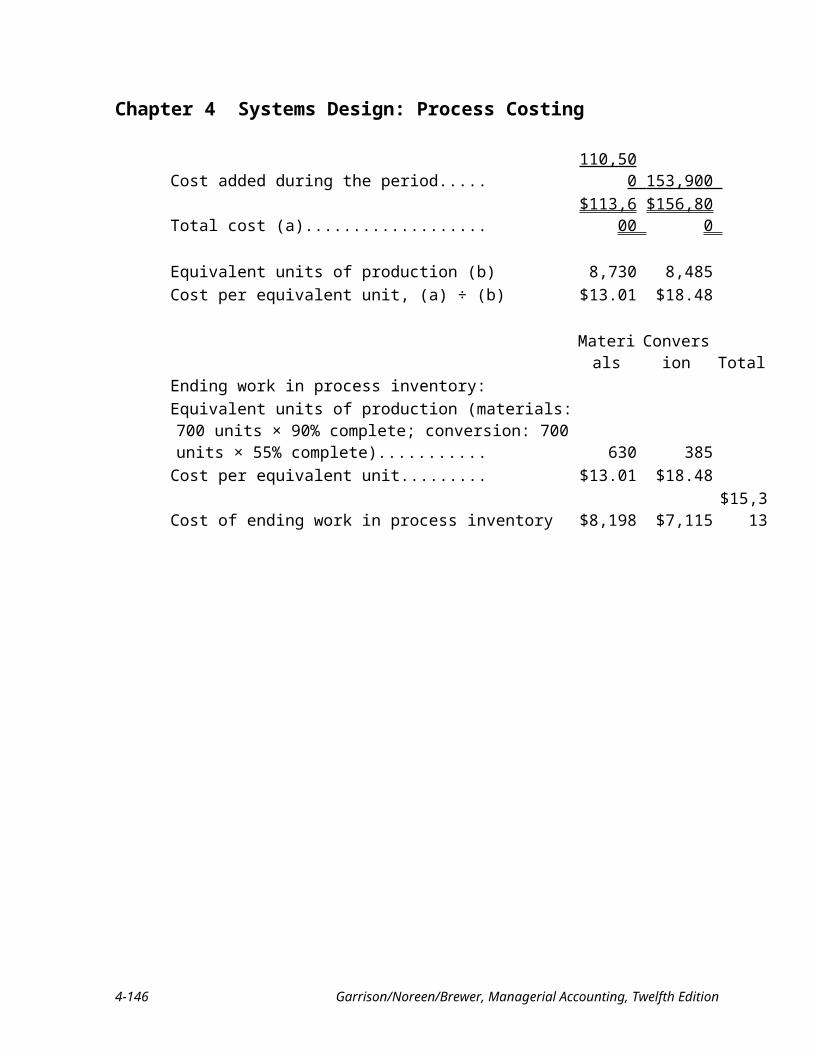

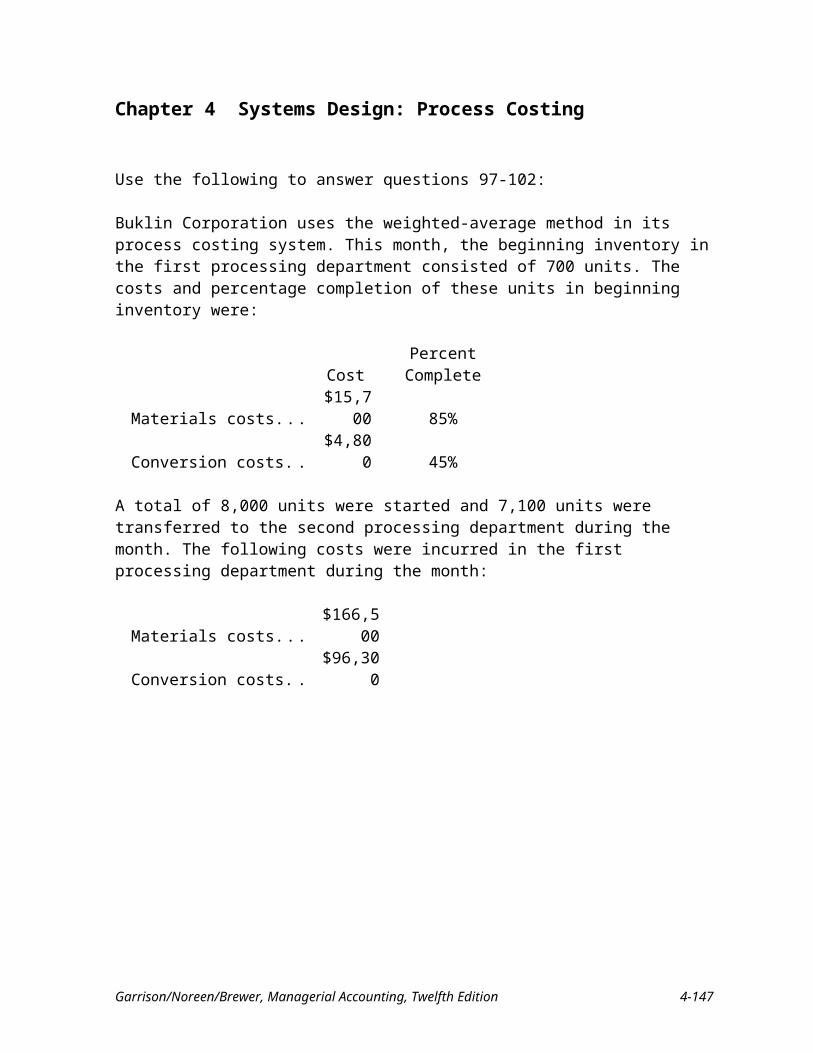

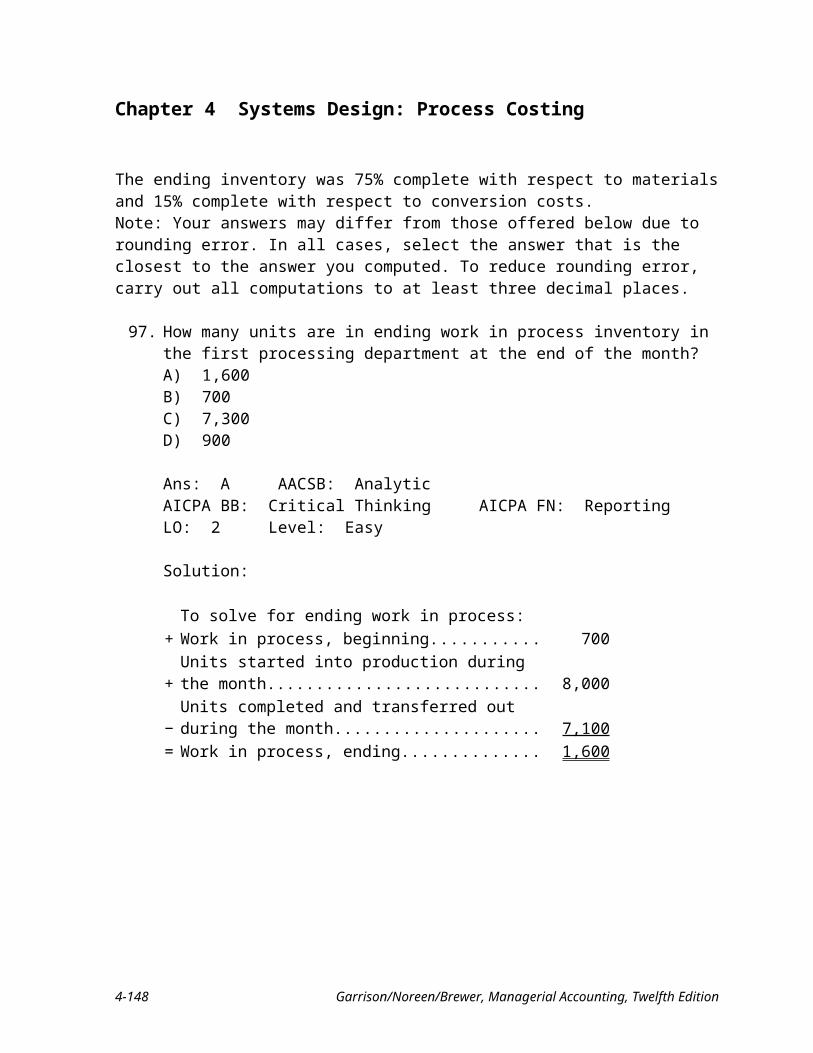

29. Health Beverage Company uses a process costing system to collect costs related to the production of its celery flavored cola. The cola is first processed in a Mixing Department at Health and is then transferred out and finished up in the Bottling Department. The finished cases of cola are then transferred to Finished Goods Inventory. The following information relates to Health's two departments for the month of January:

Mixing BottlingCases of cola in work in process, January 1..................... 10,000 3,000Cases of cola completed/transferred out during January.. 77,000 ?Cases of cola in work in process, January 31................... 4,000 8,000

How many cases of cola were completed and transferred to Finished Goods Inventory during January?A) 66,000B) 71,000C) 72,000D) 74,000

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1 Level: Medium

Solution:

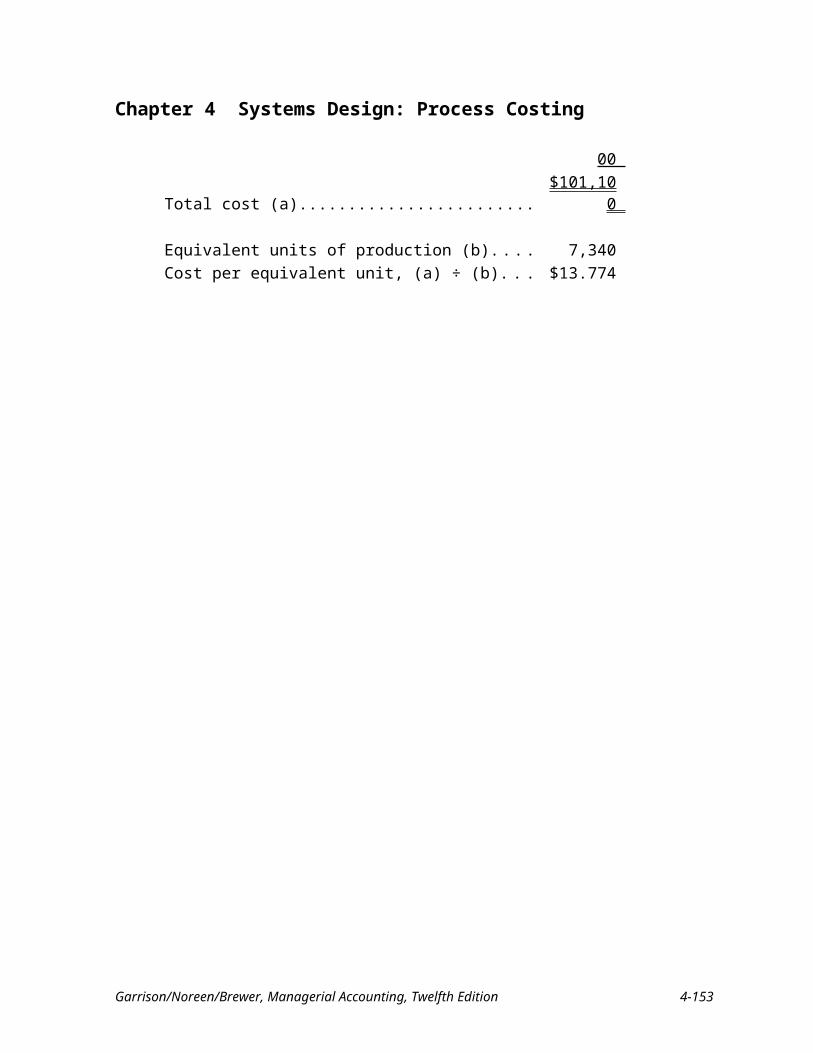

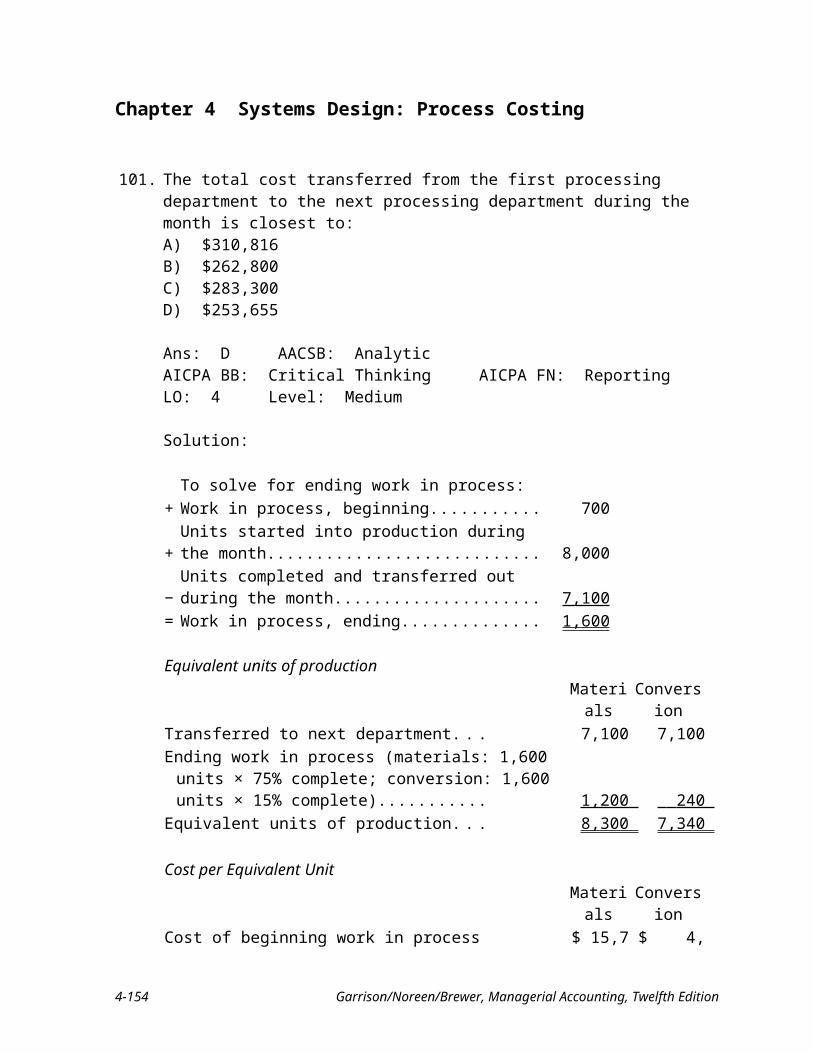

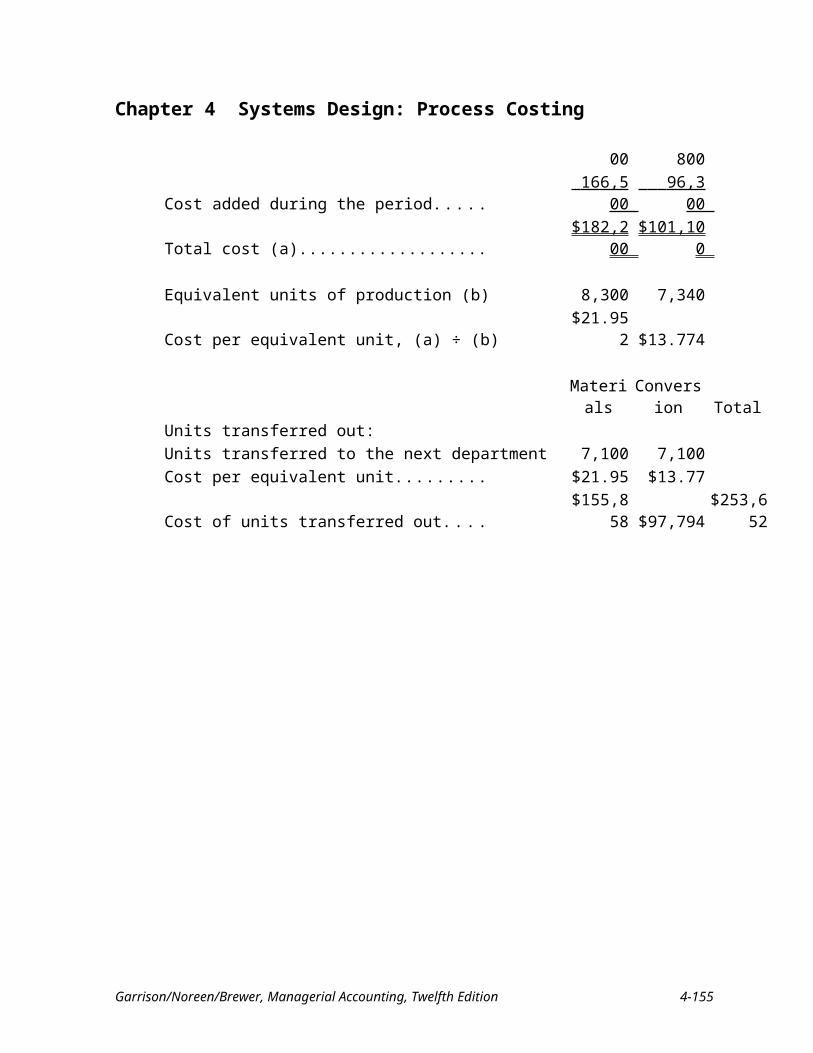

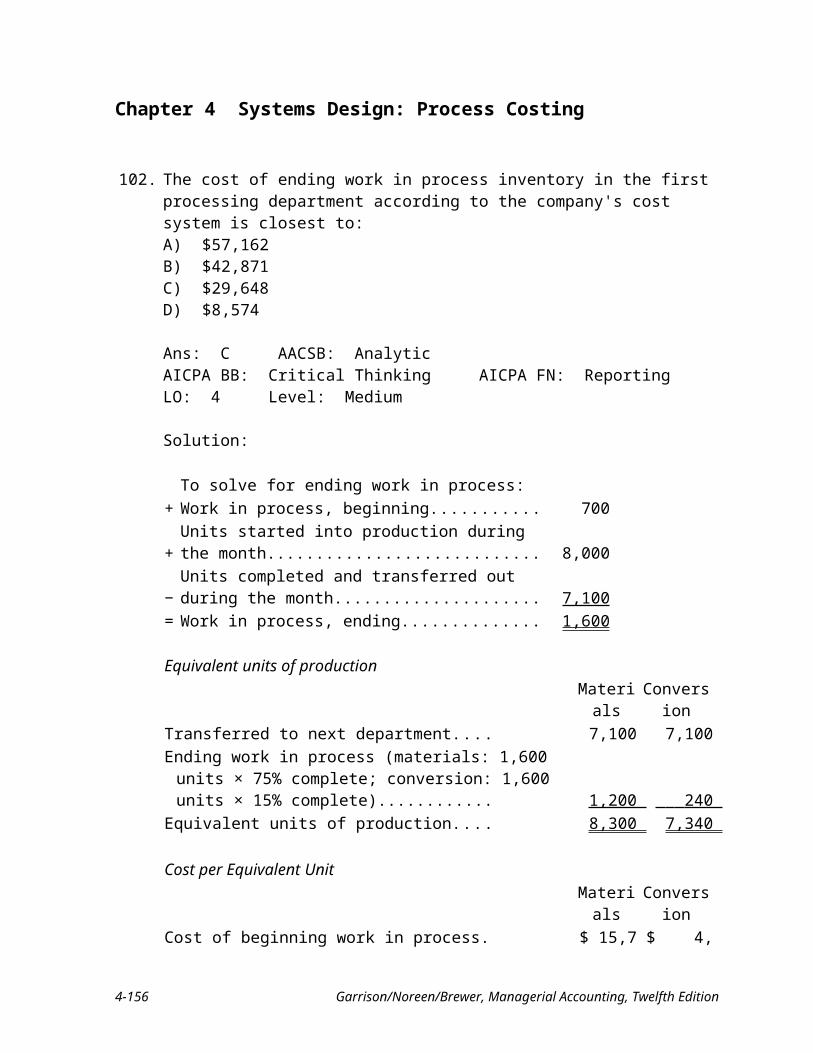

To solve for units transferred:+ Work in process, beginning................................................. 3,000+ Units started into production during the month.................. 77,000− Work in process, ending...................................................... 8,000 = Units completed and transferred out during the month....... 72,000

4-14 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

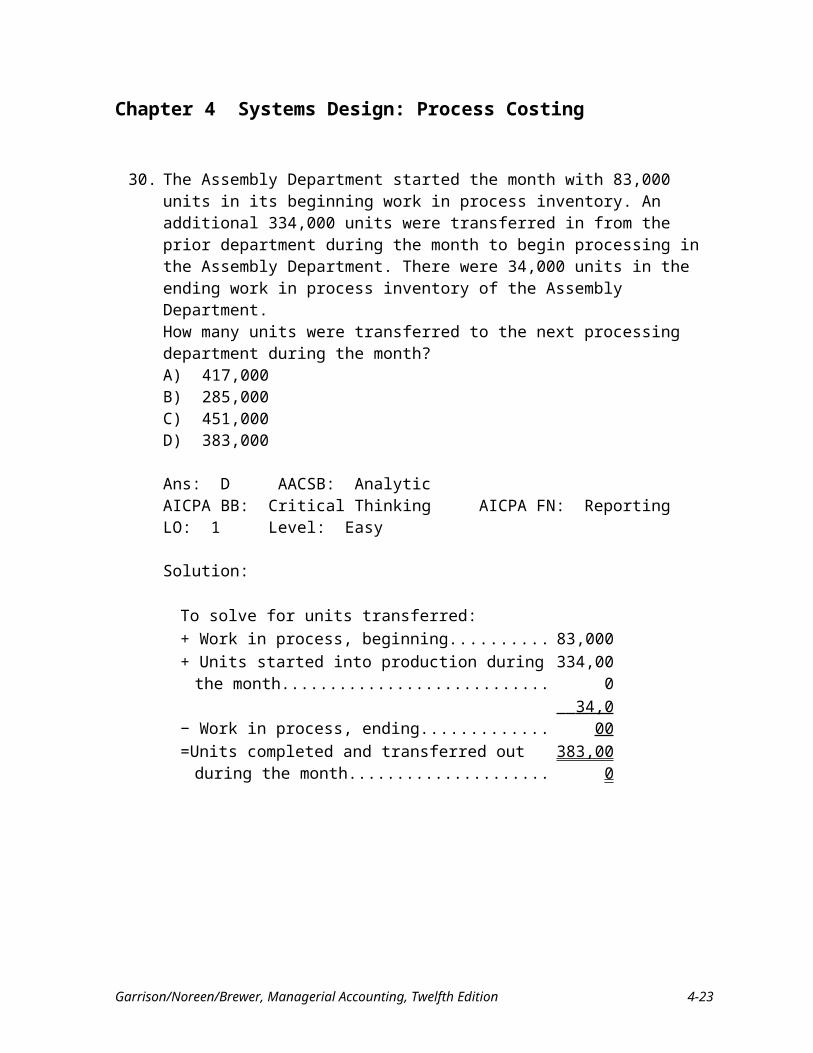

30. The Assembly Department started the month with 83,000 units in its beginning work in process inventory. An additional 334,000 units were transferred in from the prior department during the month to begin processing in the Assembly Department. There were 34,000 units in the ending work in process inventory of the Assembly Department.How many units were transferred to the next processing department during the month?A) 417,000B) 285,000C) 451,000D) 383,000

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 1 Level: Easy

Solution:

To solve for units transferred:+ Work in process, beginning............................................. 83,000+ Units started into production during the month.............. 334,000− Work in process, ending.................................................. 34,000 =Units completed and transferred out during the month.... 383,000

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-15

Chapter 4 Systems Design: Process Costing

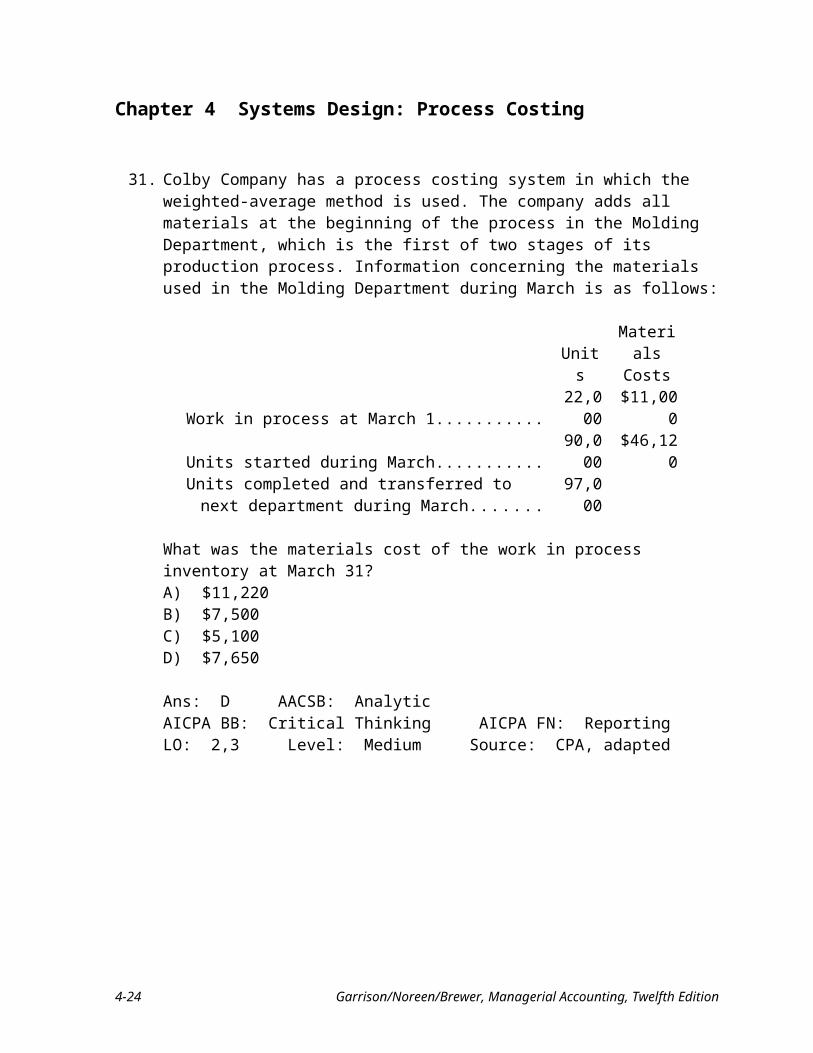

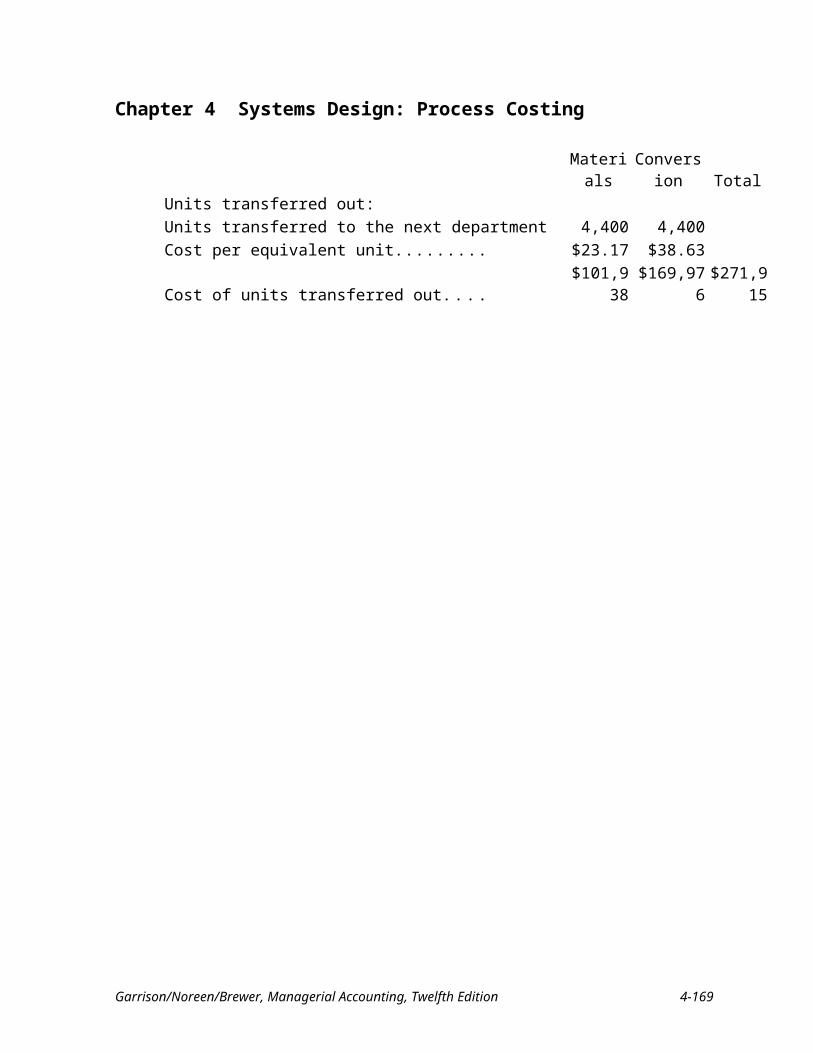

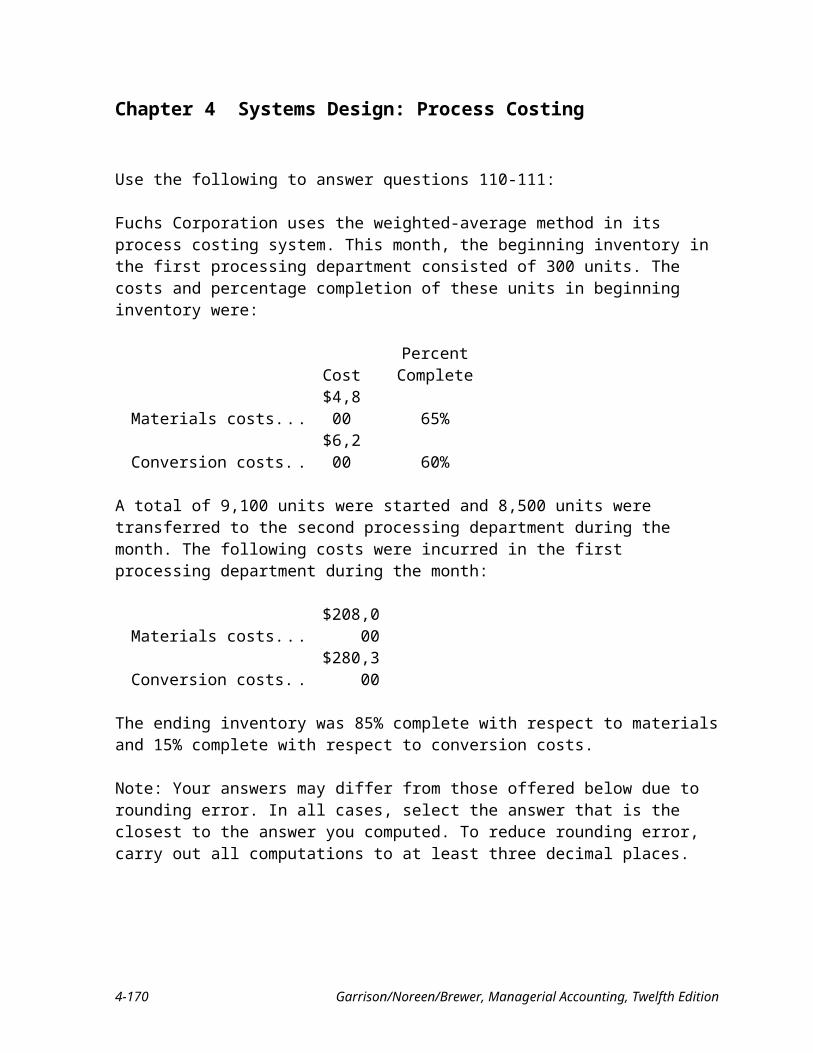

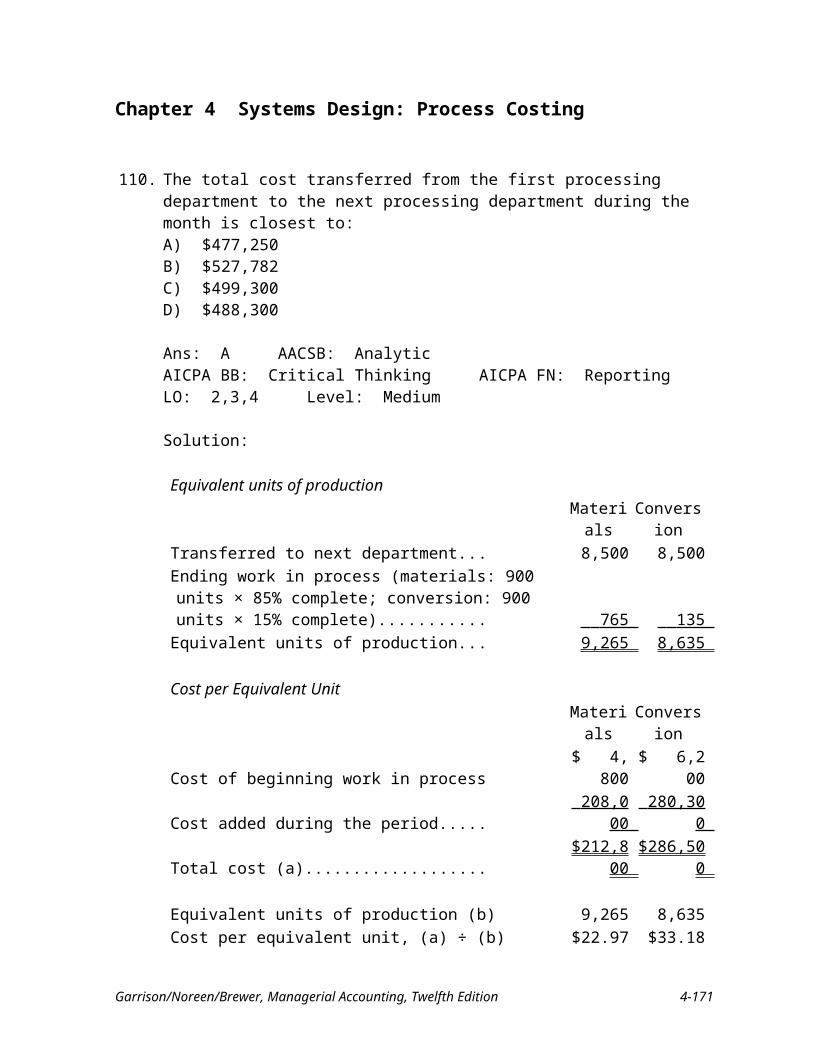

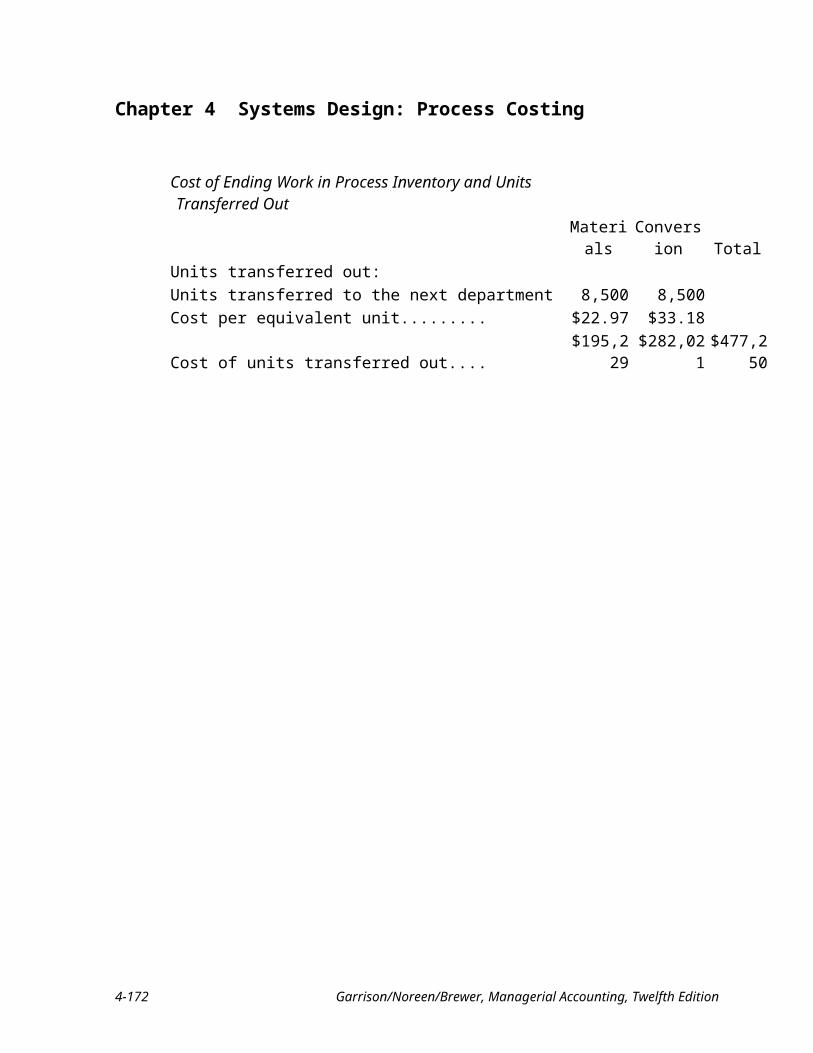

31. Colby Company has a process costing system in which the weighted-average method is used. The company adds all materials at the beginning of the process in the Molding Department, which is the first of two stages of its production process. Information concerning the materials used in the Molding Department during March is as follows:

UnitsMaterials

CostsWork in process at March 1............................................. 22,000 $11,000Units started during March.............................................. 90,000 $46,120Units completed and transferred to next department

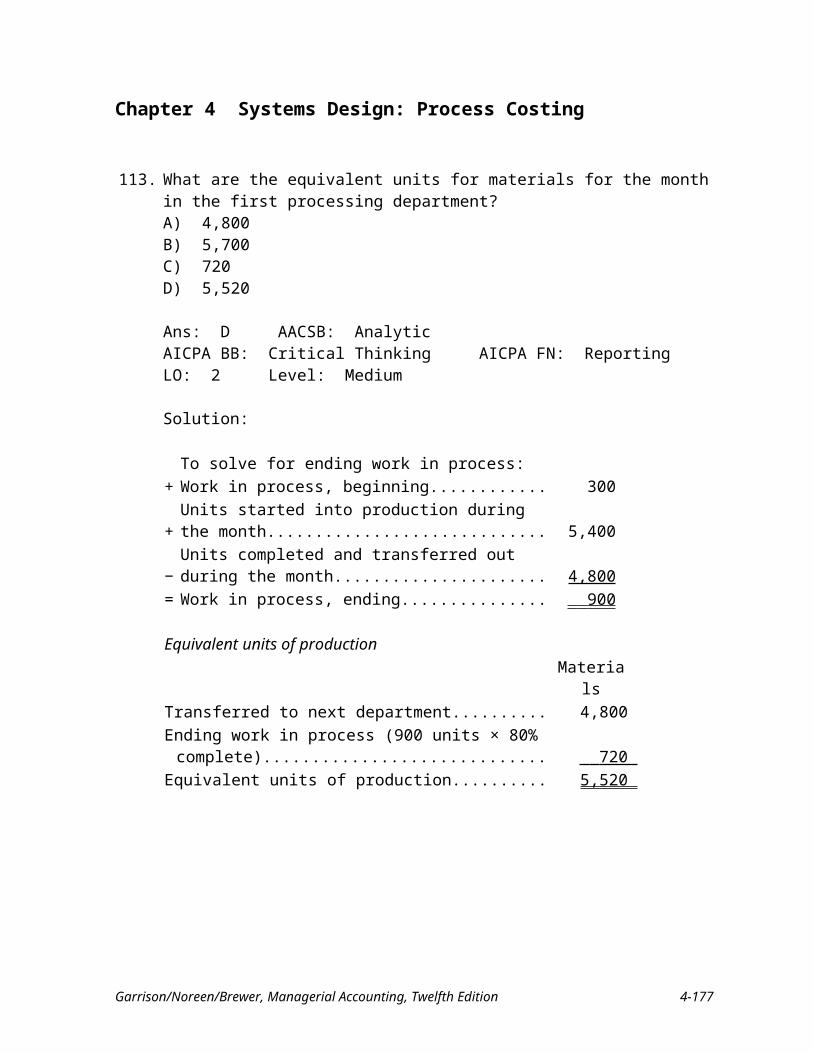

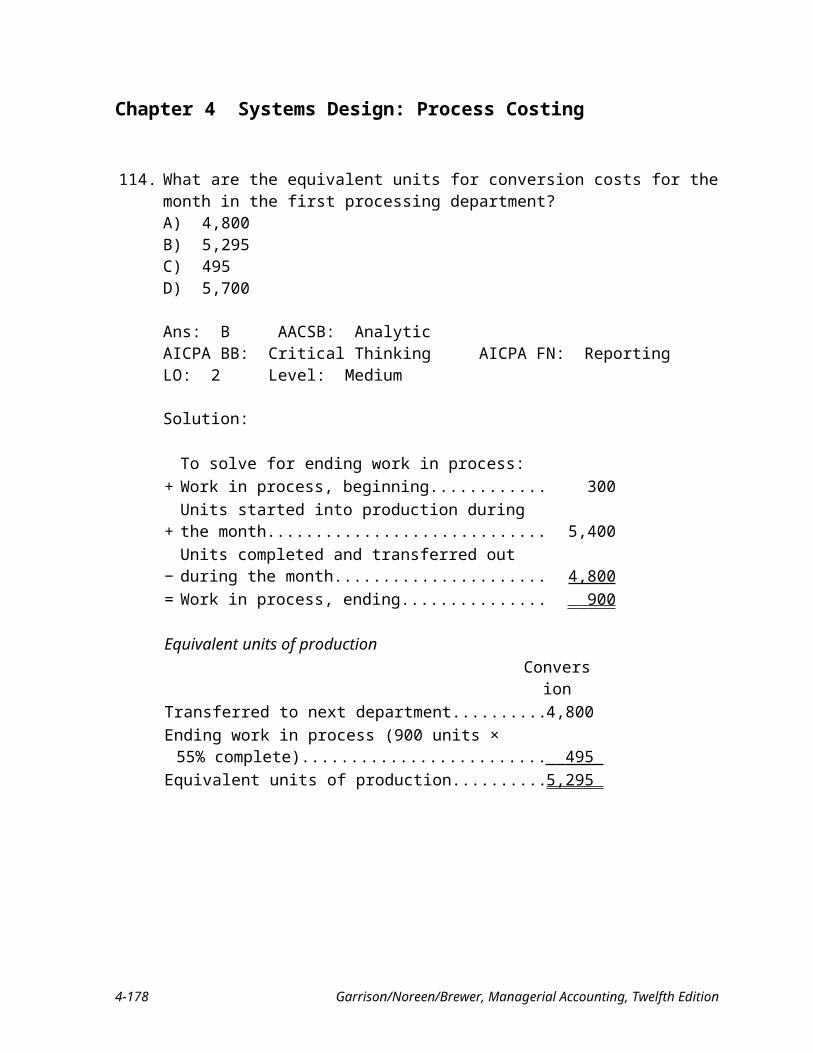

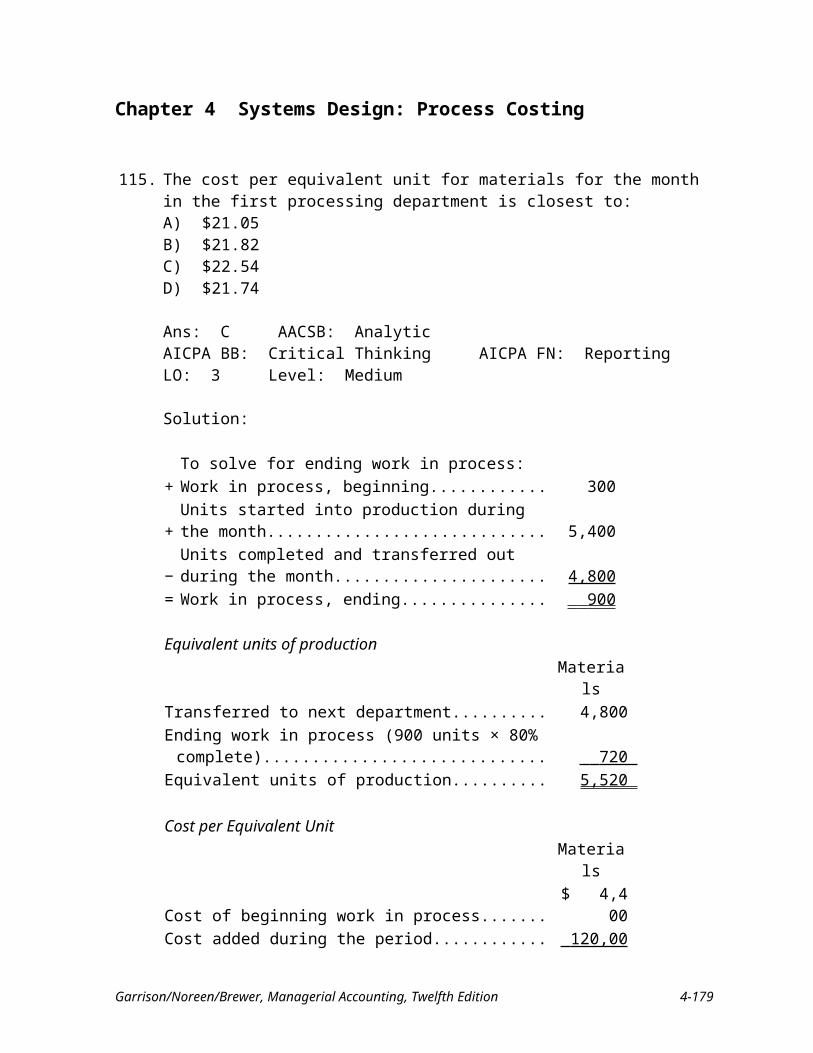

during March................................................................ 97,000

What was the materials cost of the work in process inventory at March 31?A) $11,220B) $7,500C) $5,100D) $7,650

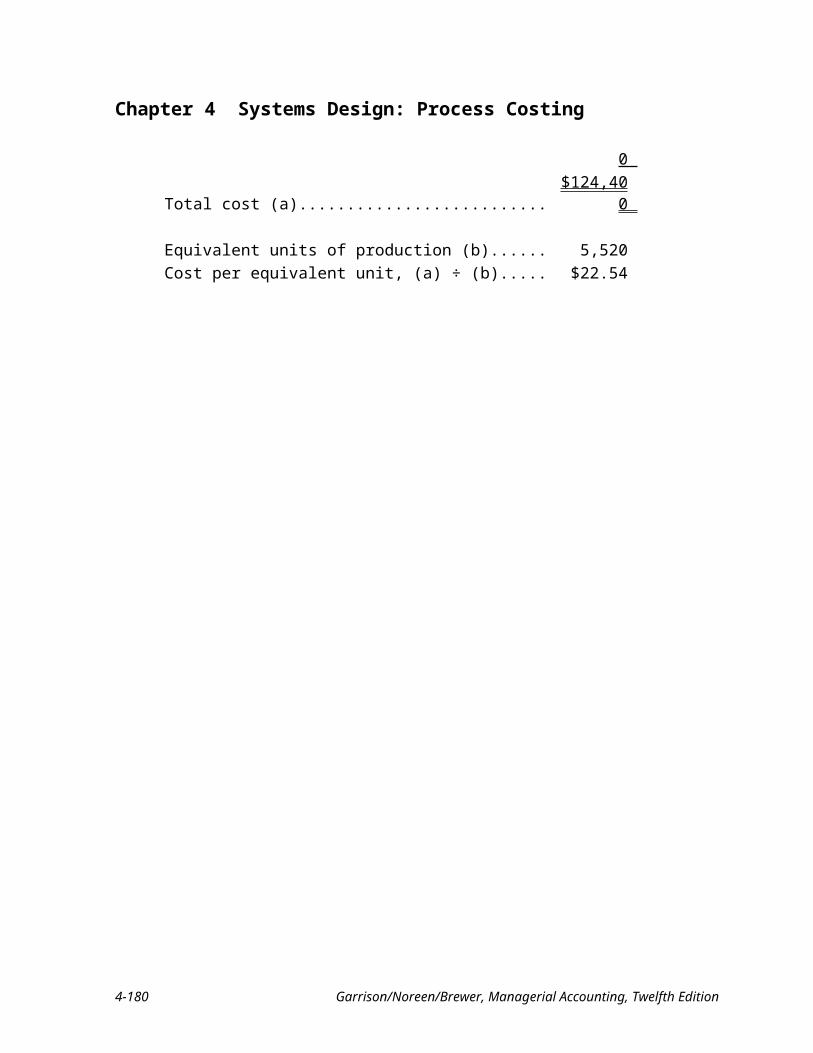

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,3 Level: Medium Source: CPA, adapted

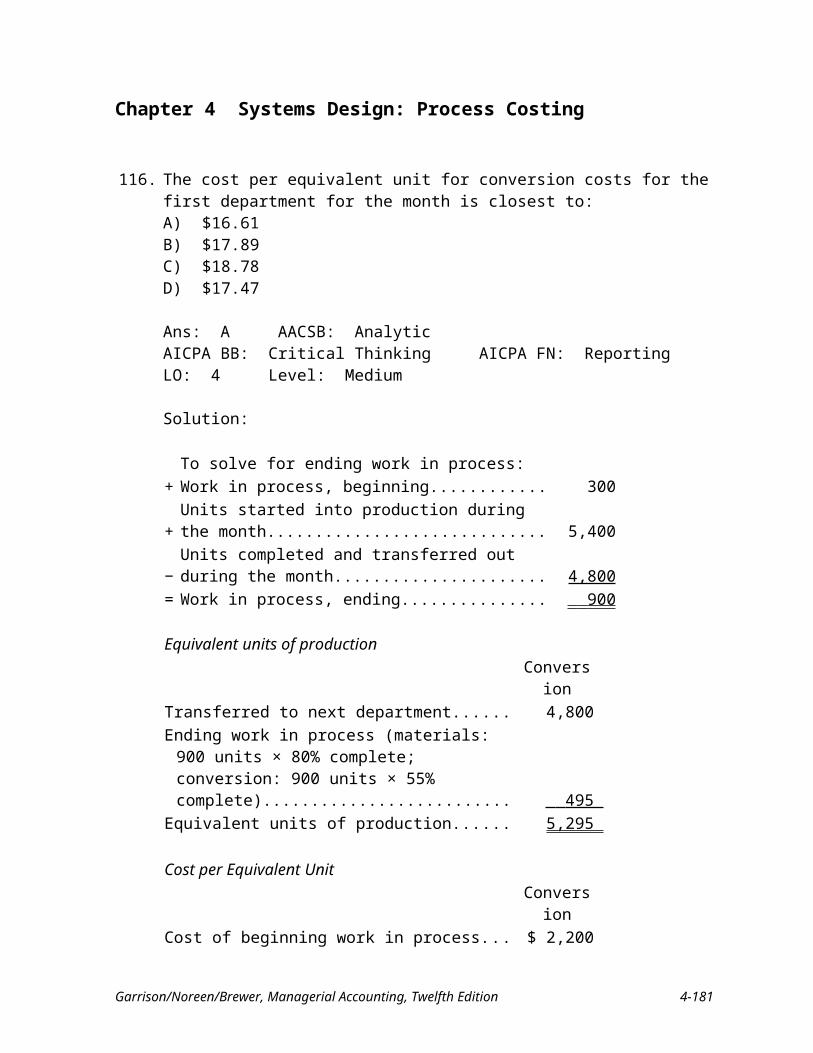

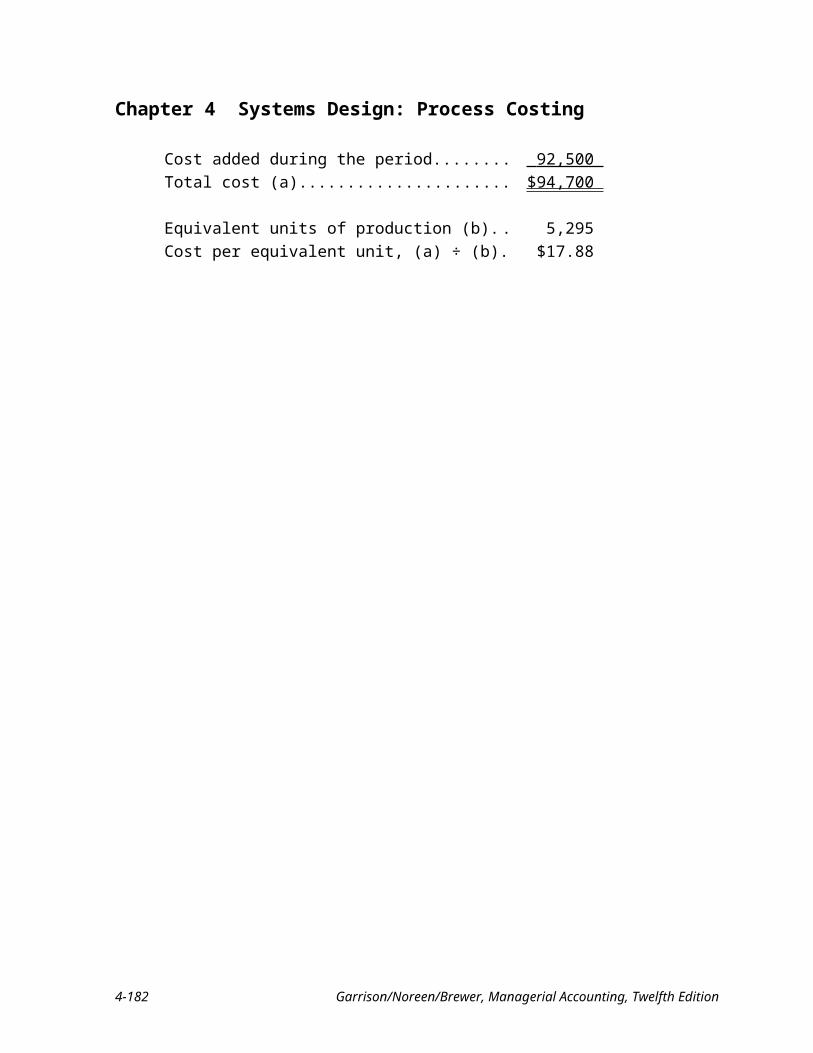

4-16 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

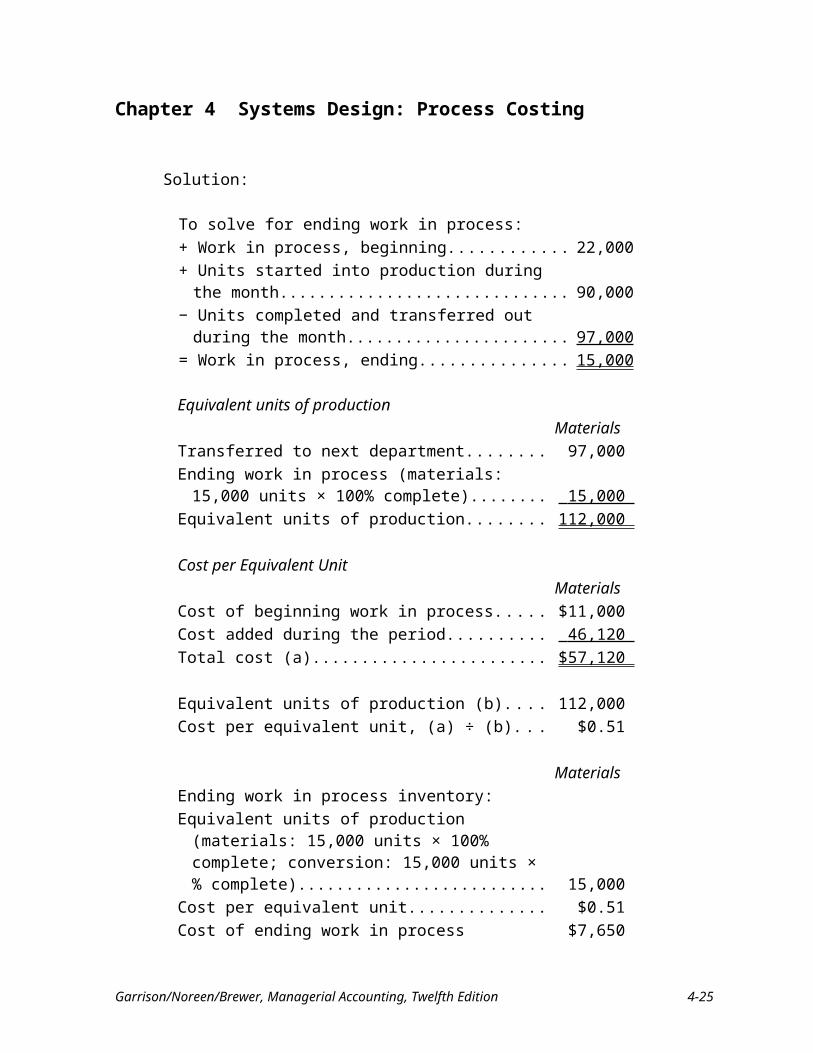

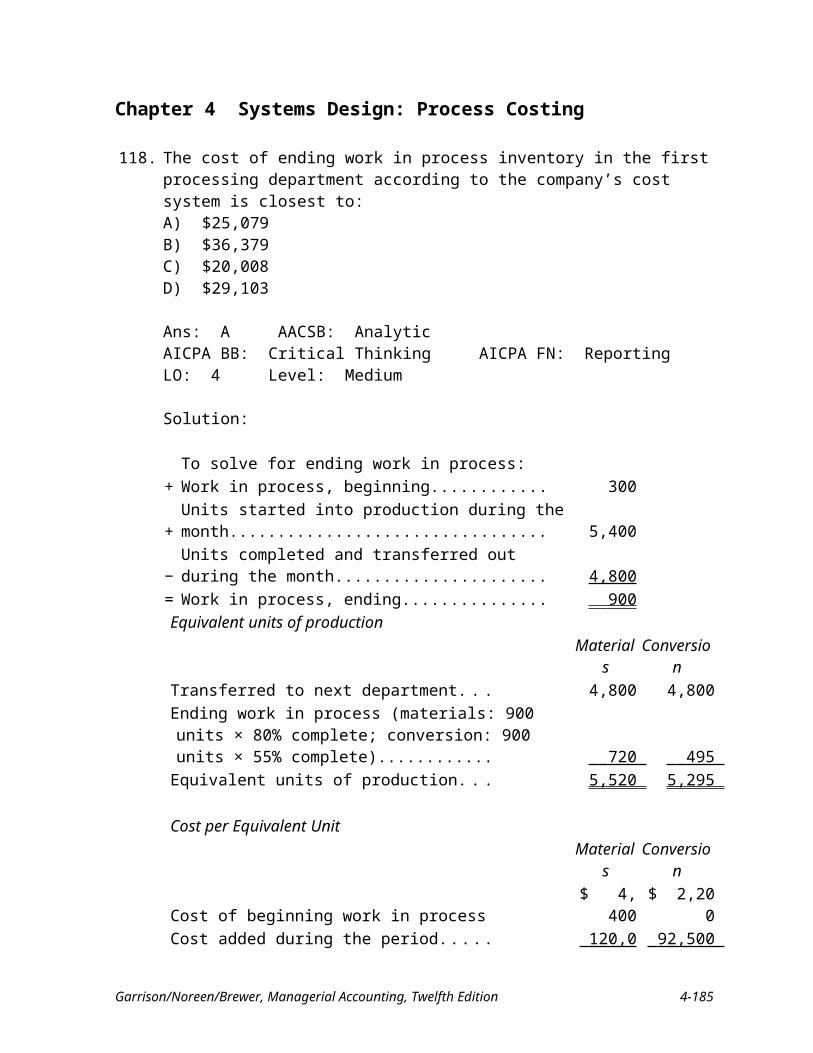

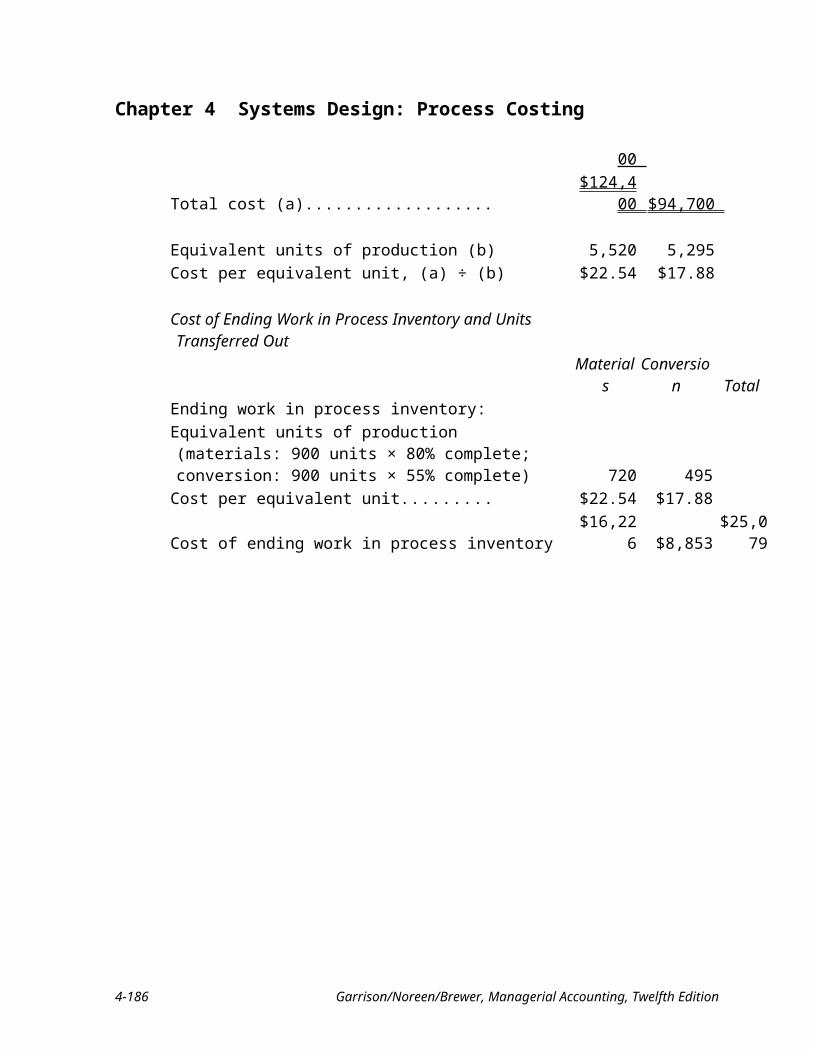

Solution:

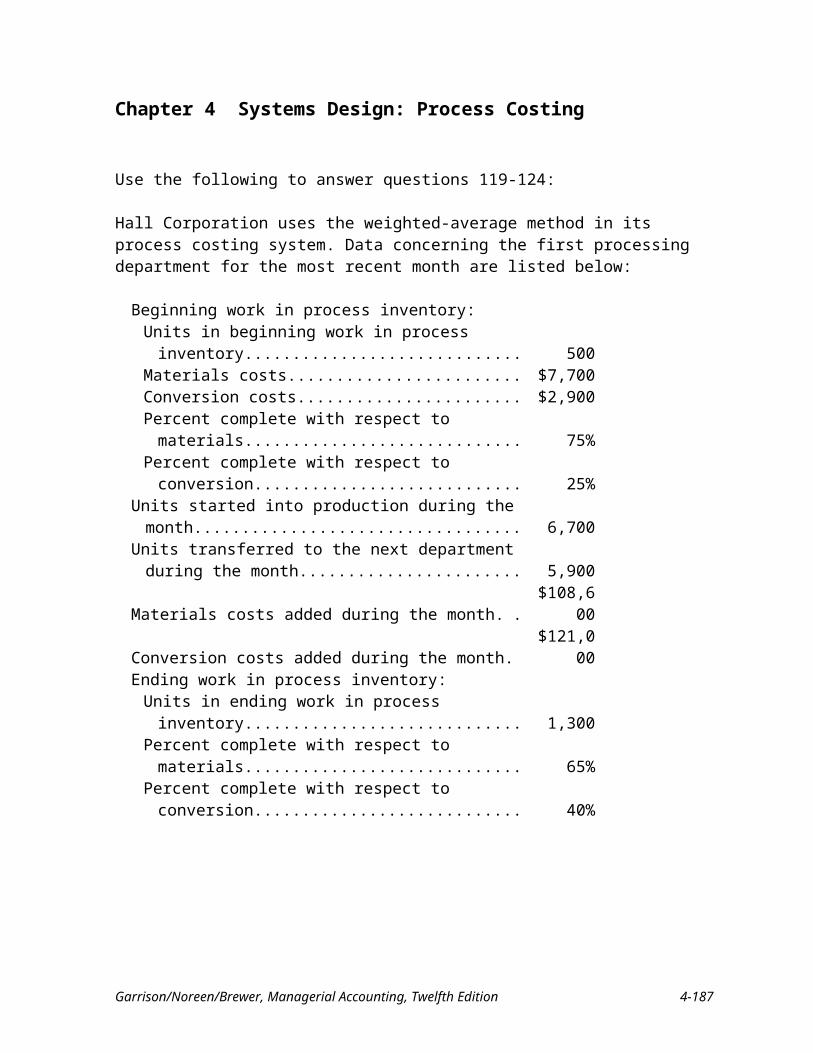

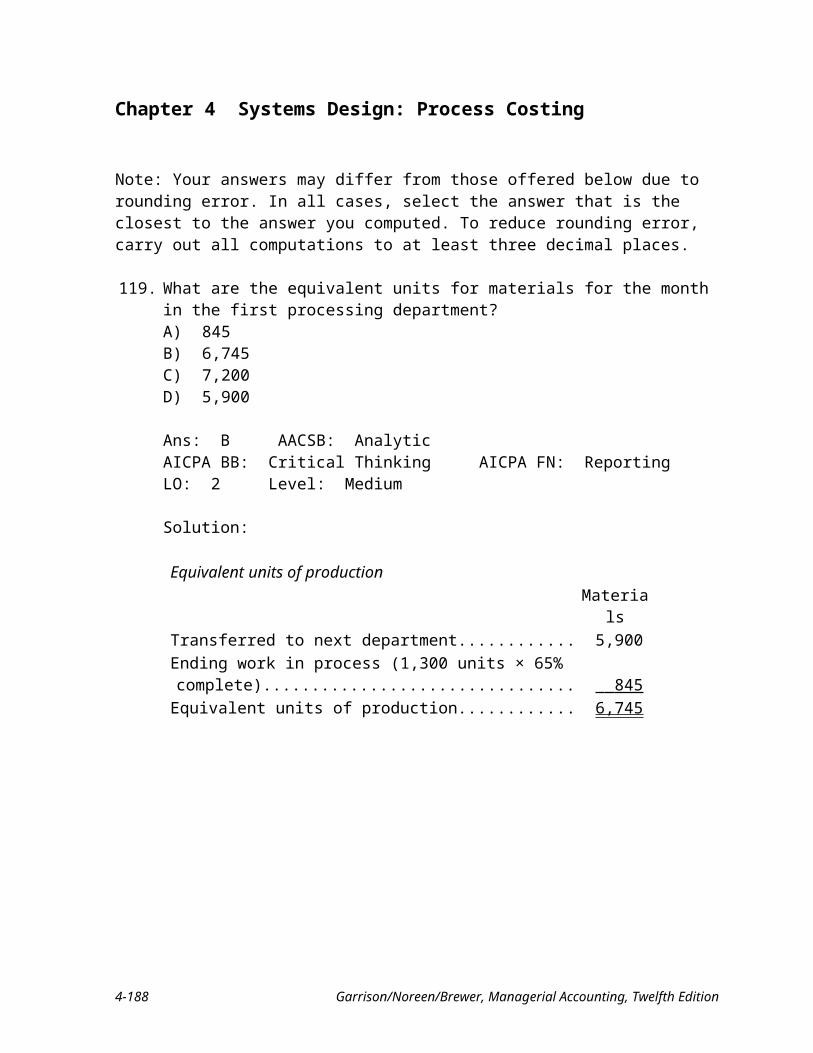

To solve for ending work in process:+ Work in process, beginning.................................................. 22,000+ Units started into production during the month.................... 90,000− Units completed and transferred out during the month........ 97,000= Work in process, ending....................................................... 15,000

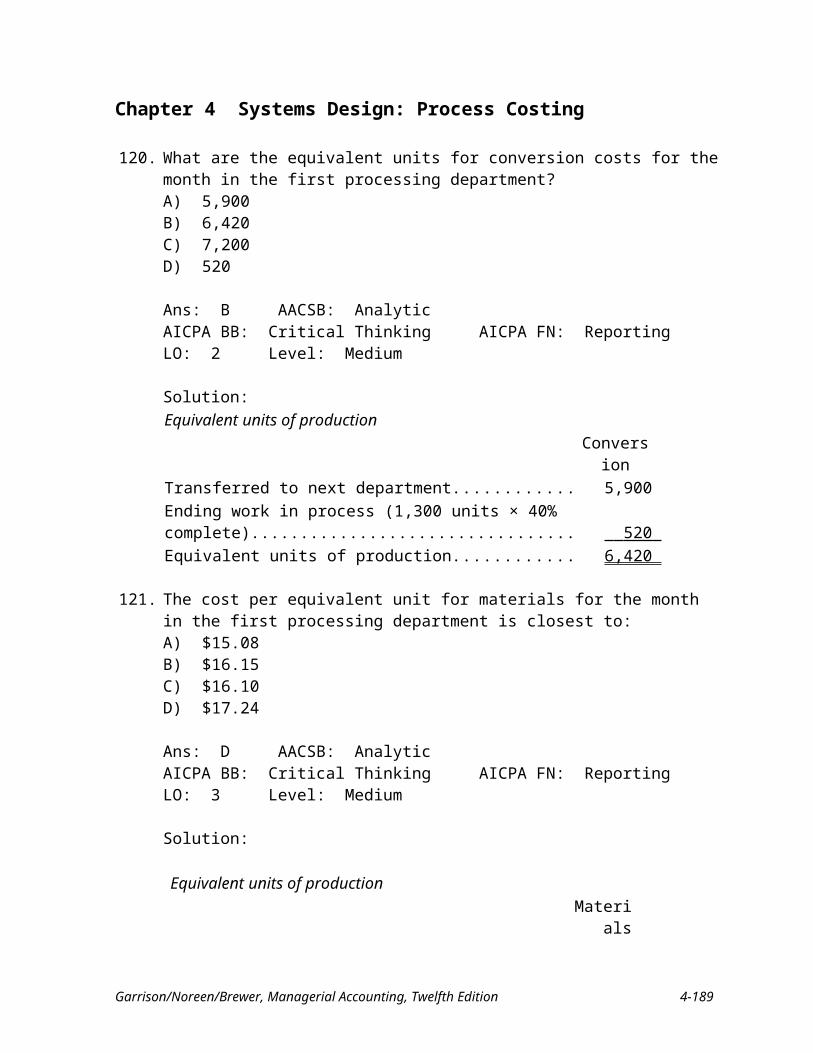

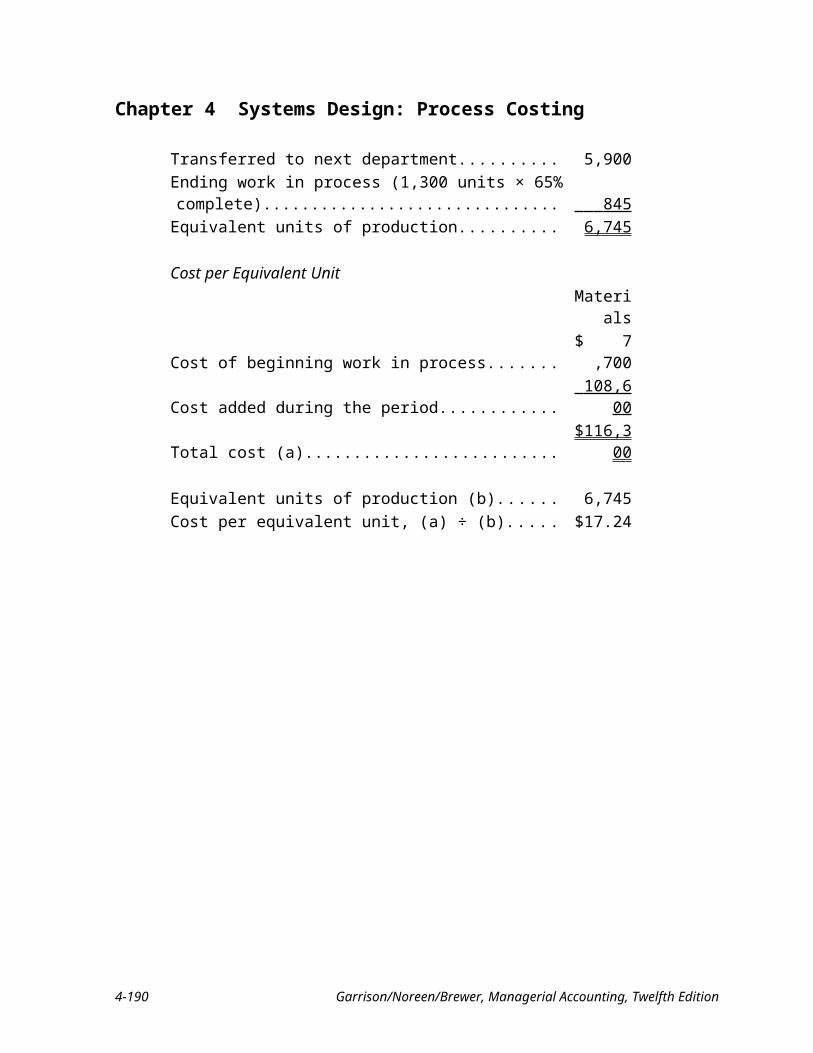

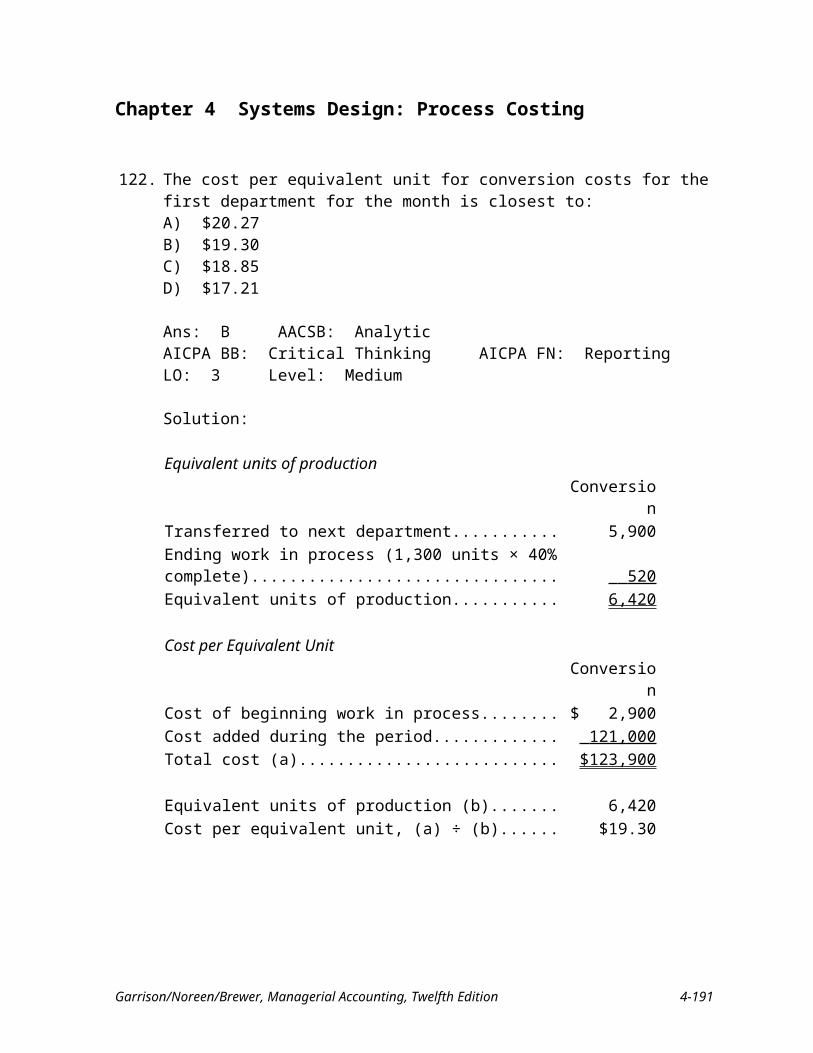

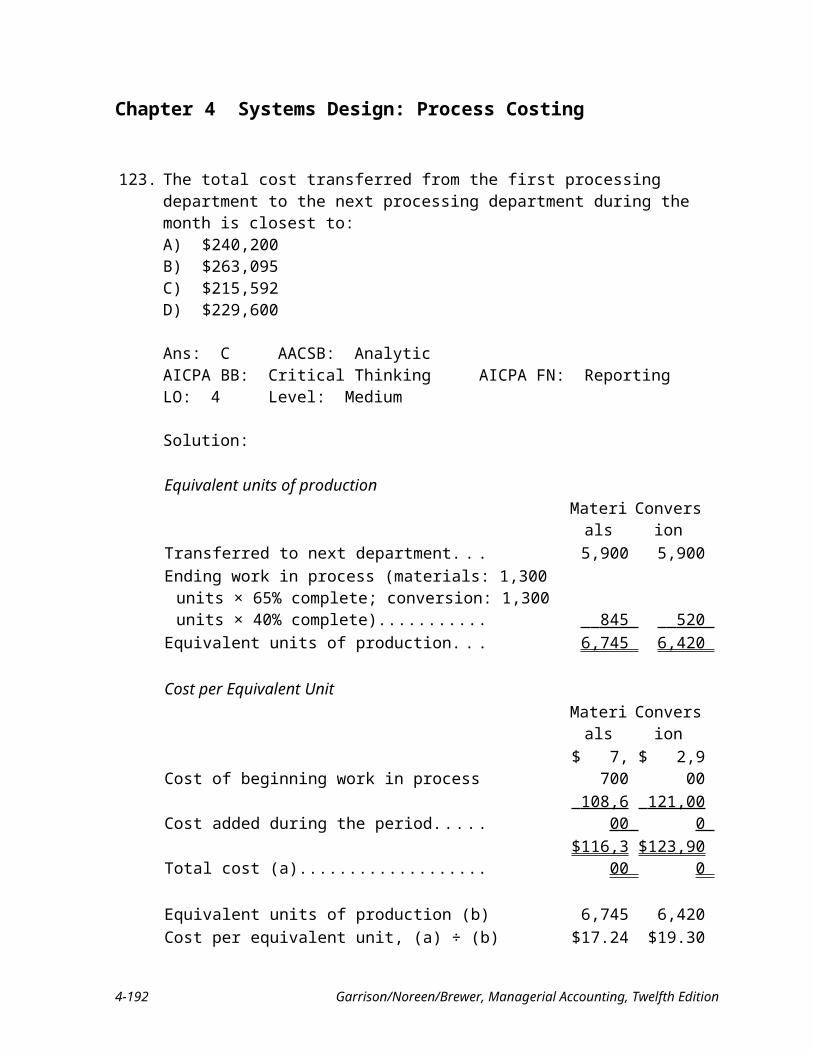

Equivalent units of productionMaterials

Transferred to next department........................................... 97,000 Ending work in process (materials: 15,000 units × 100%

complete)......................................................................... 15,000 Equivalent units of production........................................... 112,000

Cost per Equivalent UnitMaterials

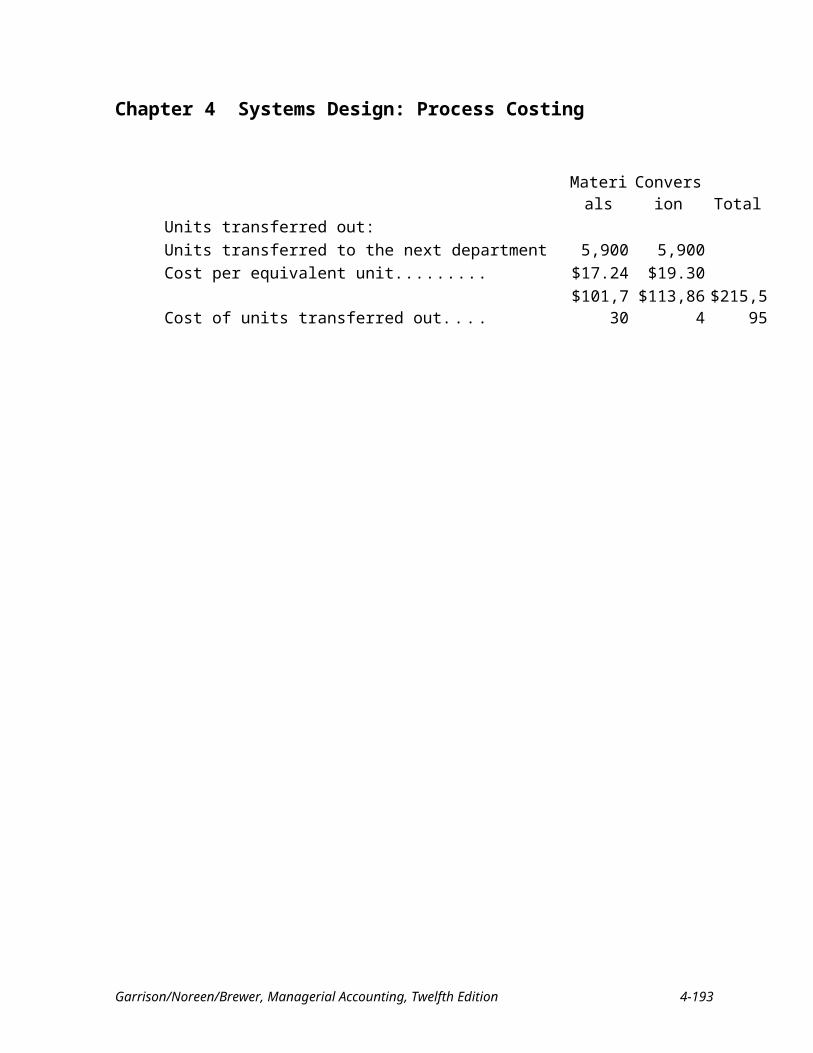

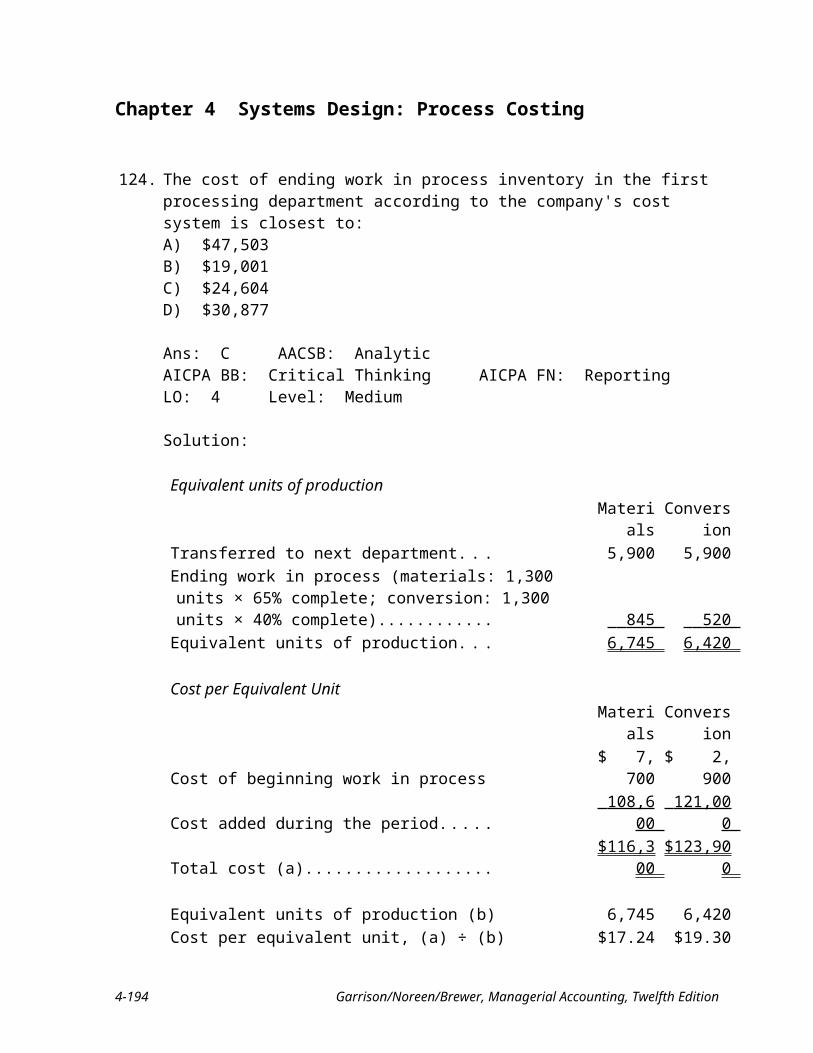

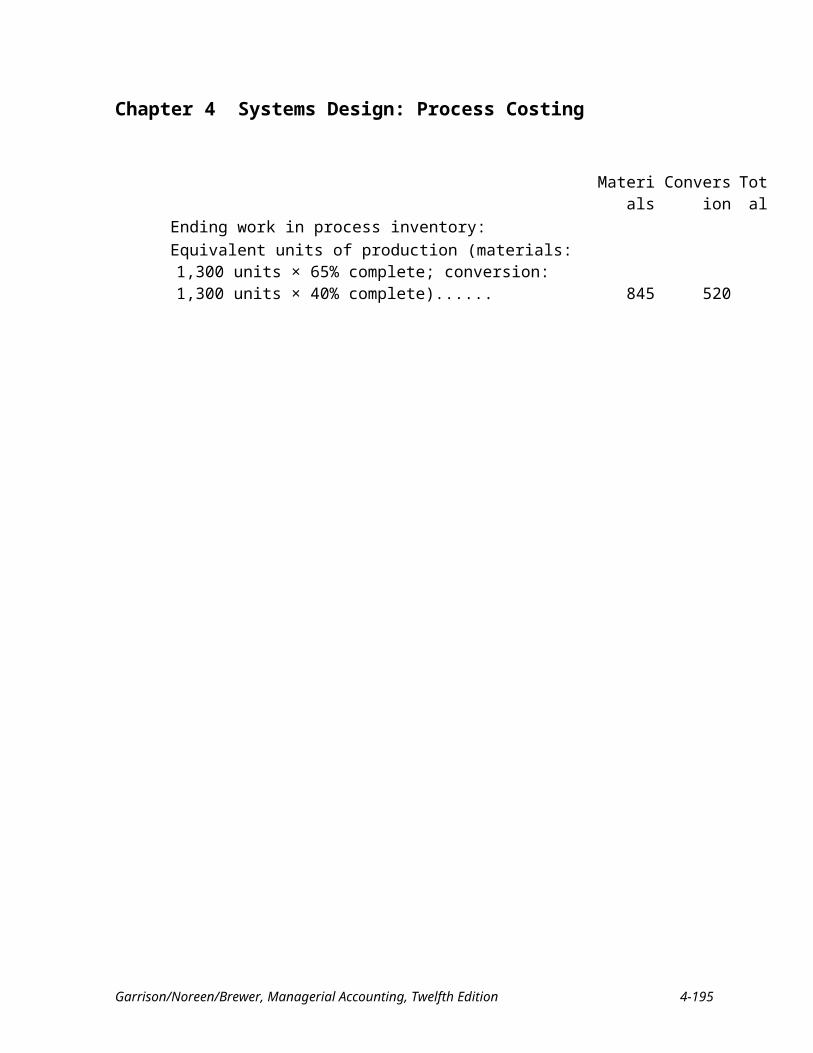

Cost of beginning work in process..................................... $11,000 Cost added during the period.............................................. 46,120 Total cost (a)....................................................................... $57,120

Equivalent units of production (b)...................................... 112,000 Cost per equivalent unit, (a) ÷ (b)....................................... $0.51

MaterialsEnding work in process inventory:Equivalent units of production (materials: 15,000 units ×

100% complete; conversion: 15,000 units × % complete)......................................................................... 15,000

Cost per equivalent unit...................................................... $0.51 Cost of ending work in process inventory.......................... $7,650

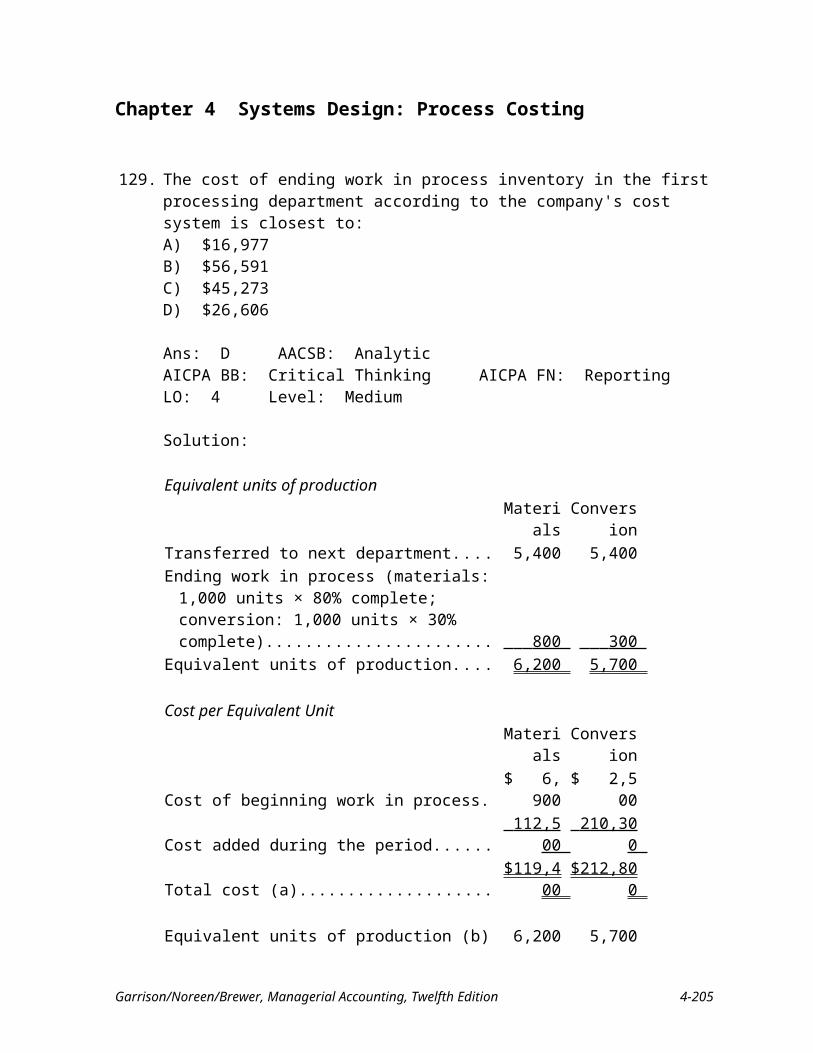

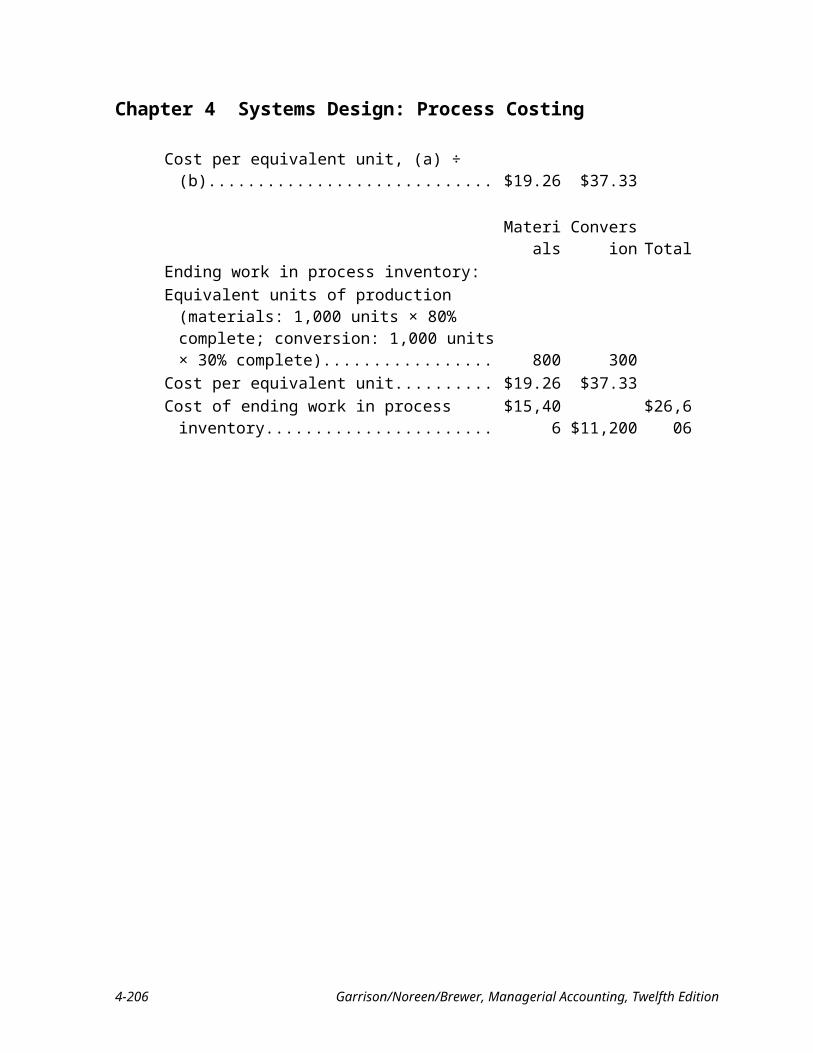

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-17

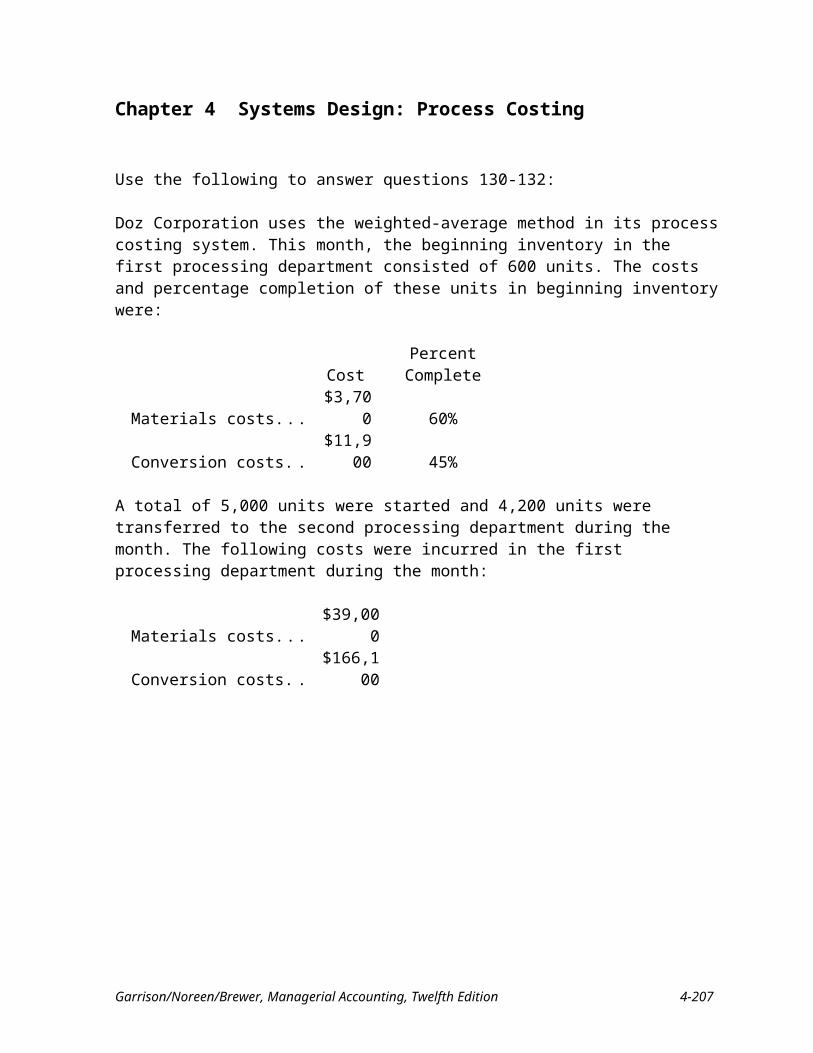

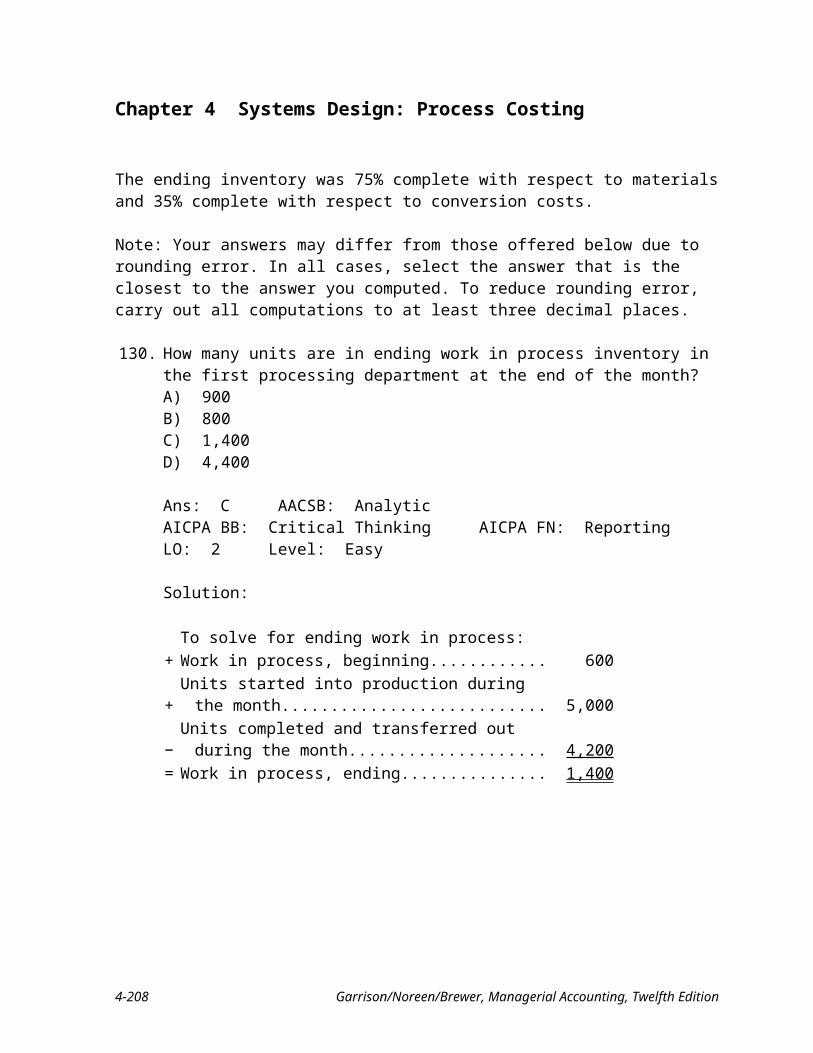

Chapter 4 Systems Design: Process Costing

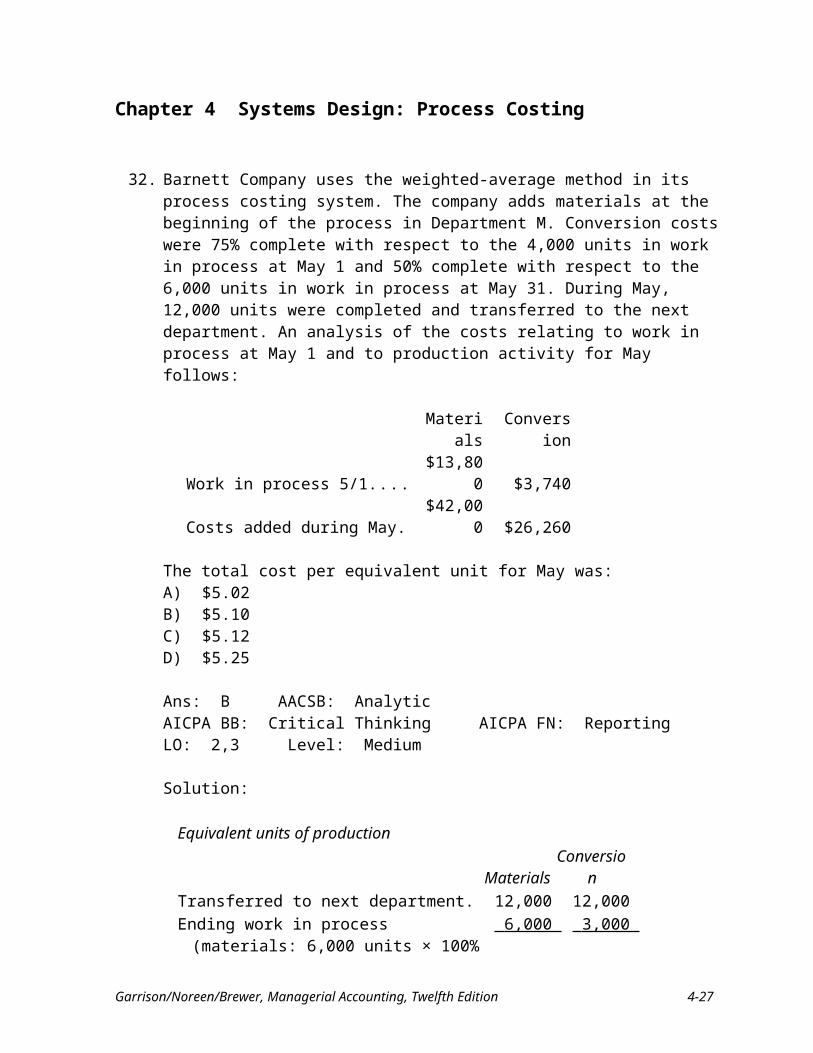

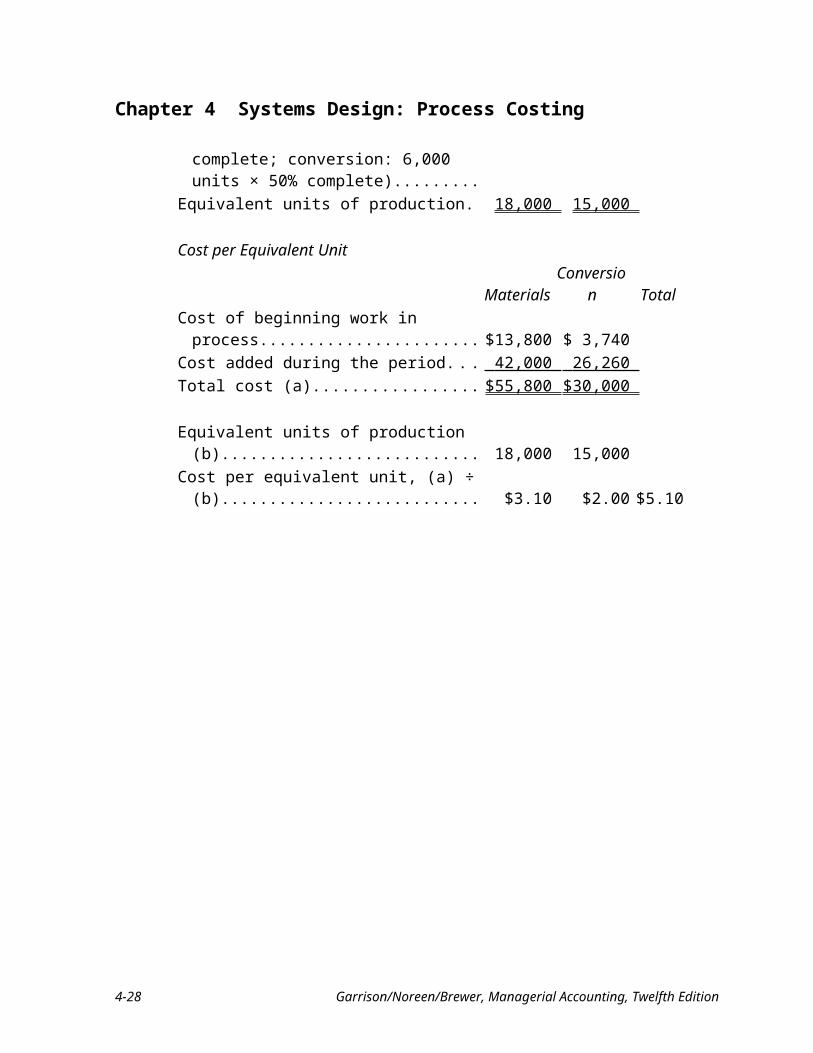

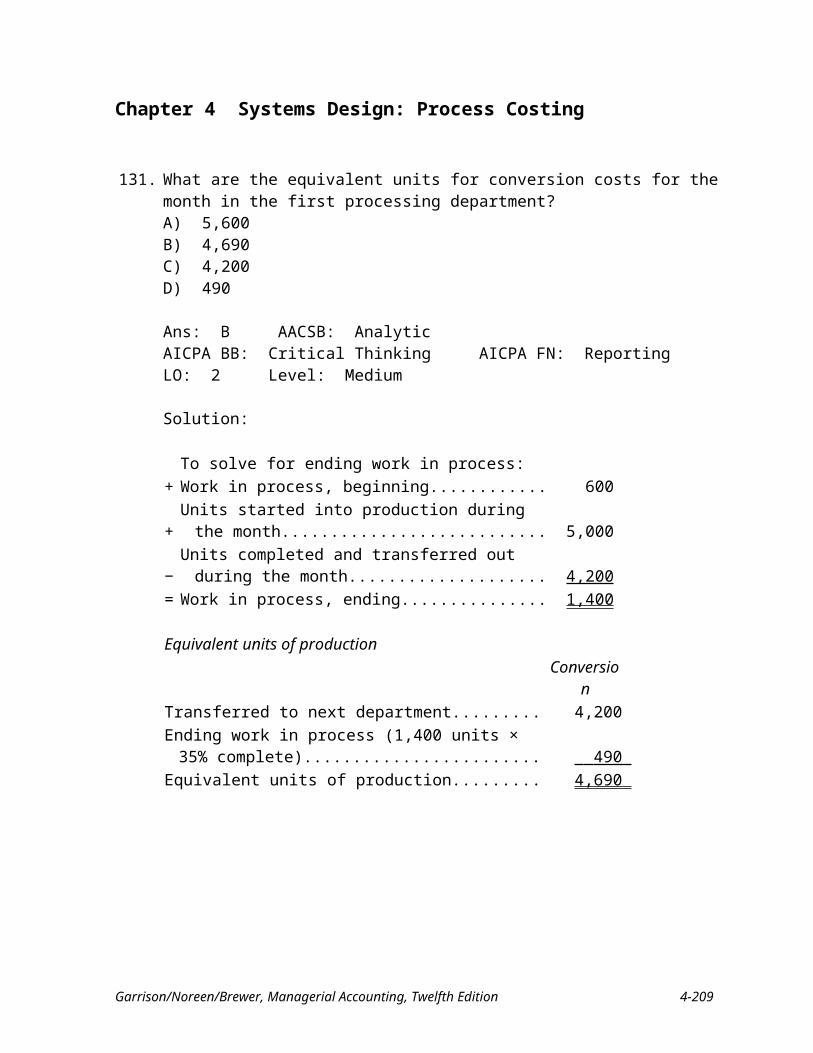

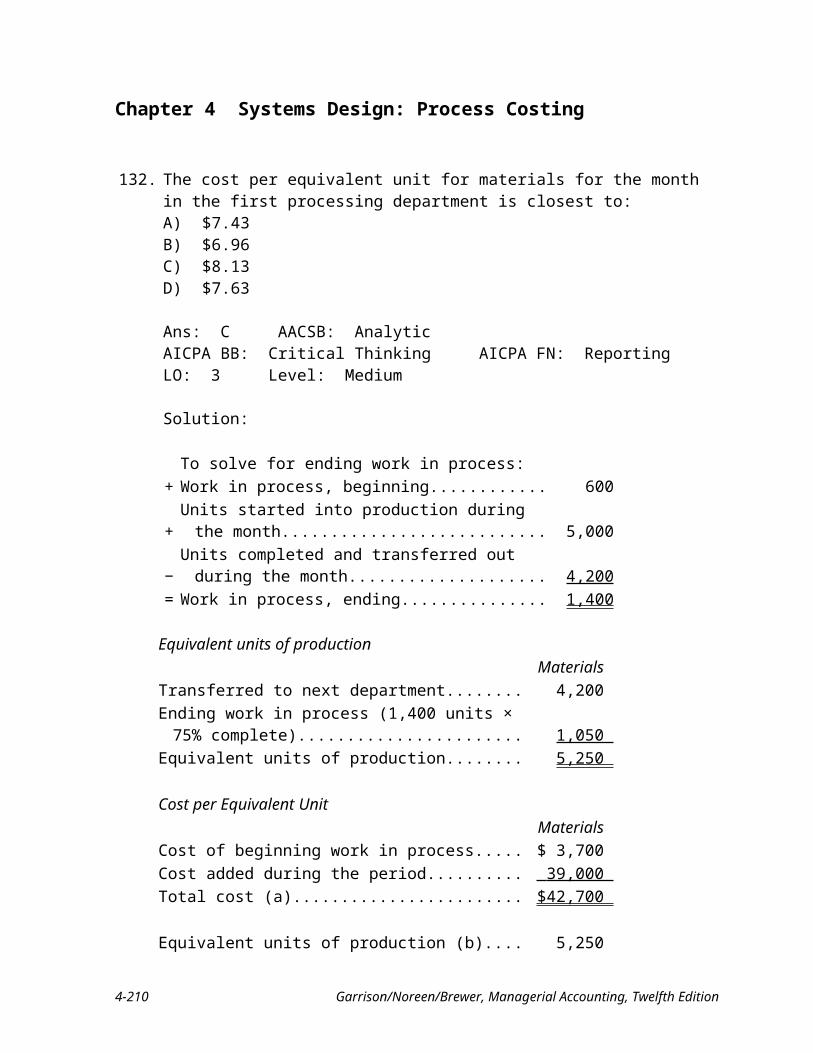

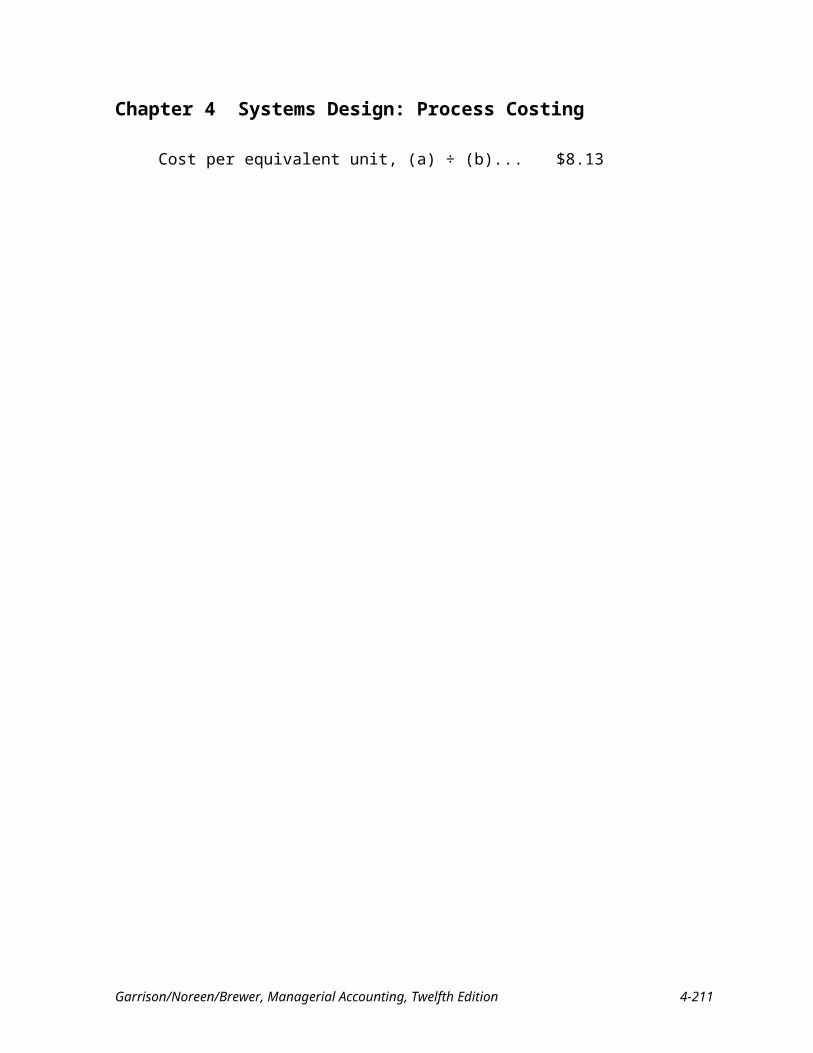

32. Barnett Company uses the weighted-average method in its process costing system. The company adds materials at the beginning of the process in Department M. Conversion costs were 75% complete with respect to the 4,000 units in work in process at May 1 and 50% complete with respect to the 6,000 units in work in process at May 31. During May, 12,000 units were completed and transferred to the next department. An analysis of the costs relating to work in process at May 1 and to production activity for May follows:

Materials ConversionWork in process 5/1....................... $13,800 $3,740Costs added during May................ $42,000 $26,260

The total cost per equivalent unit for May was:A) $5.02B) $5.10C) $5.12D) $5.25

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,3 Level: Medium

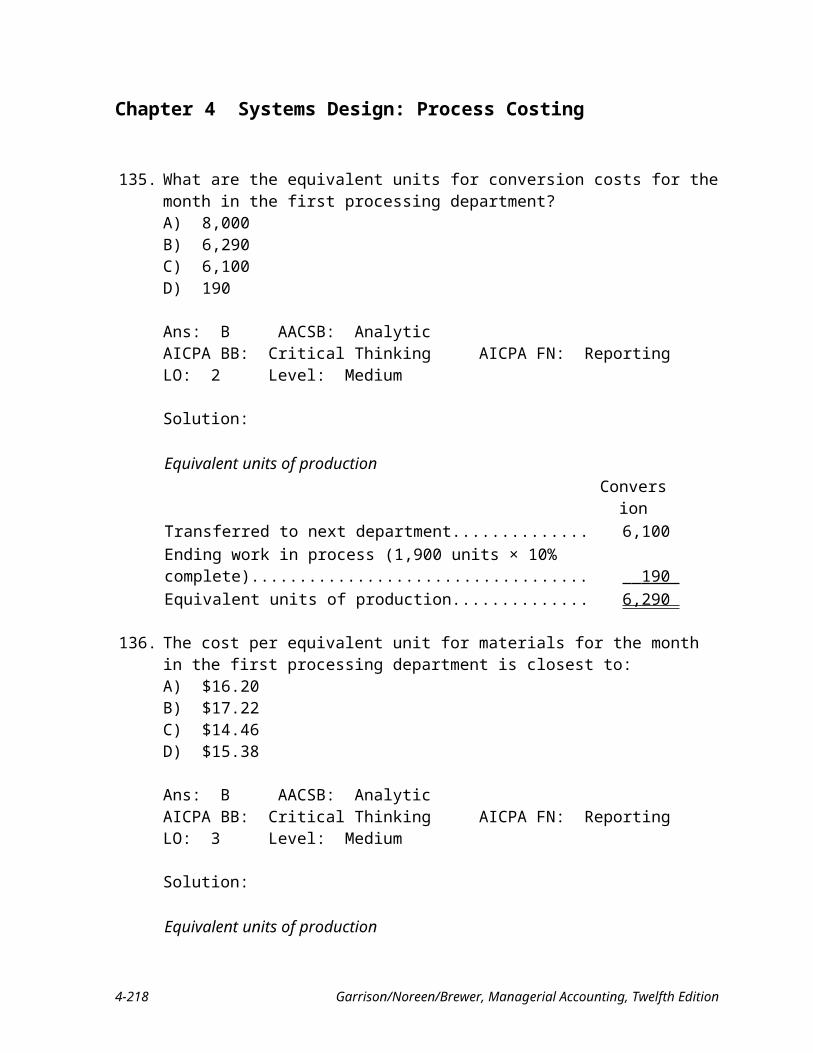

Solution:

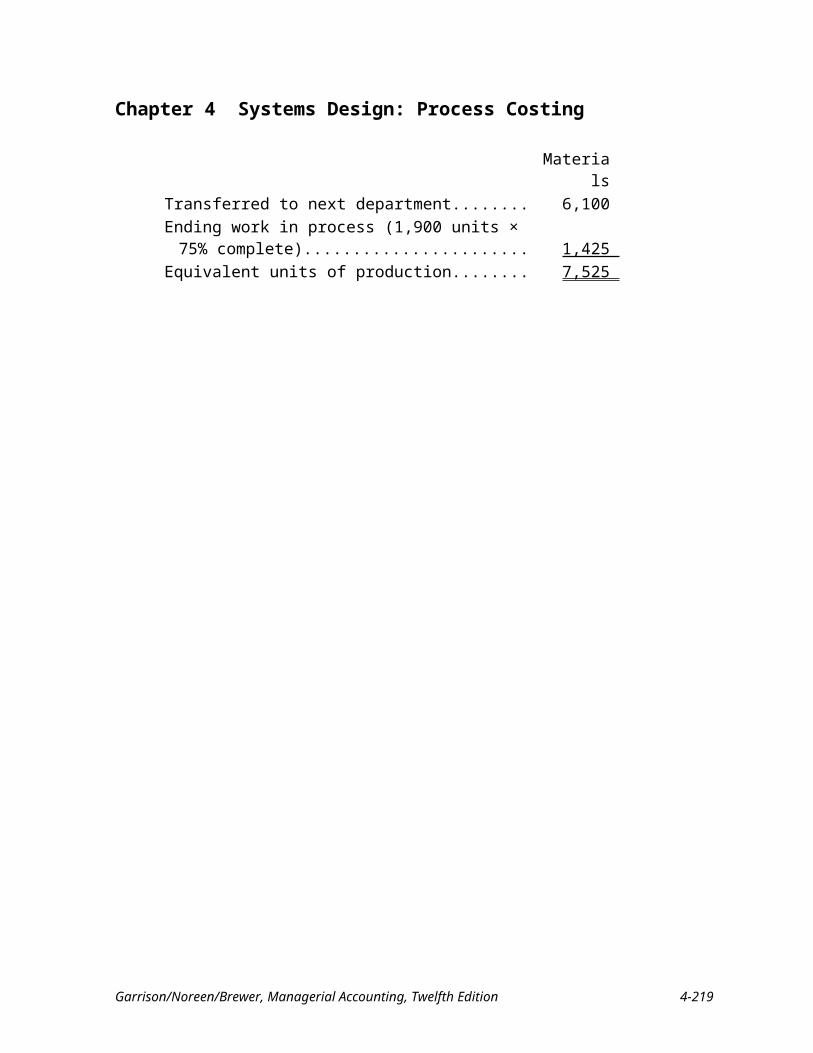

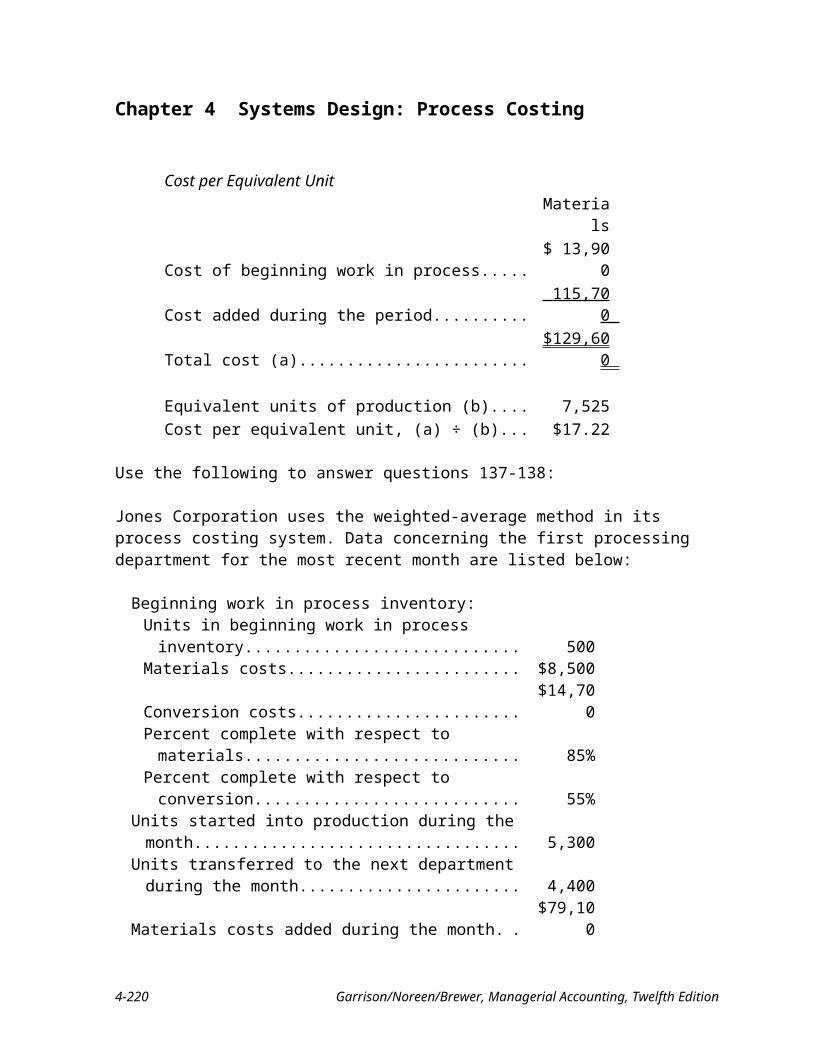

Equivalent units of productionMaterials Conversion

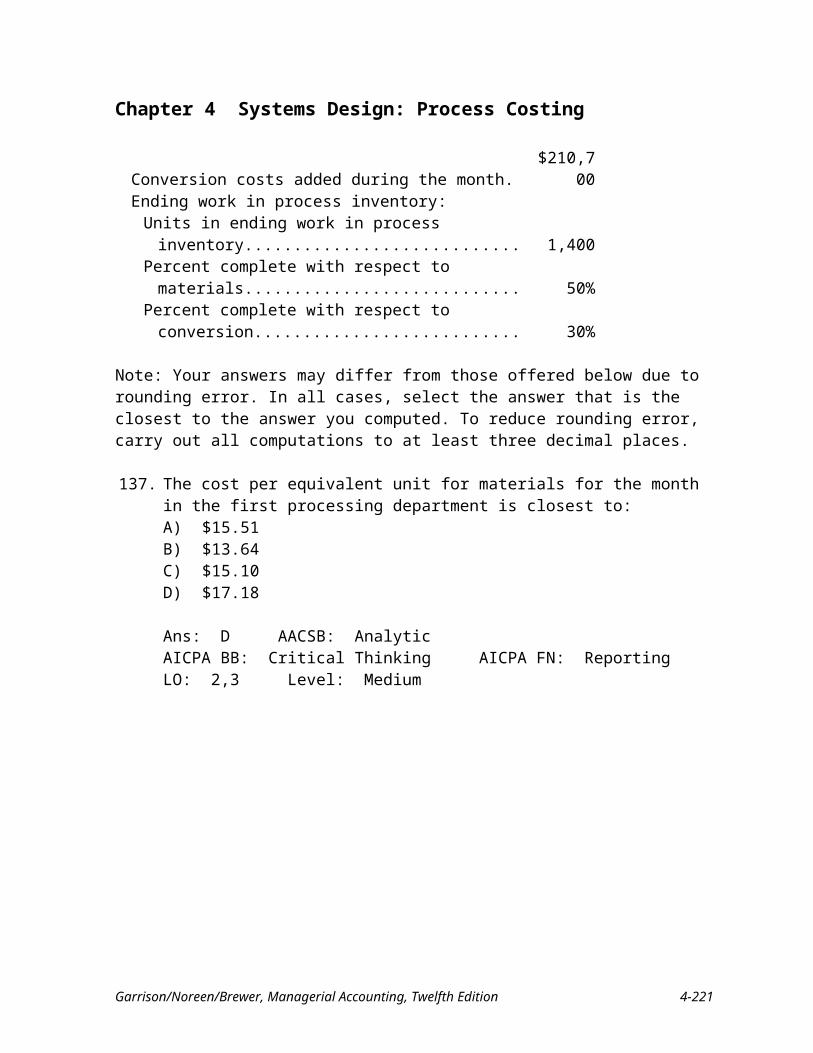

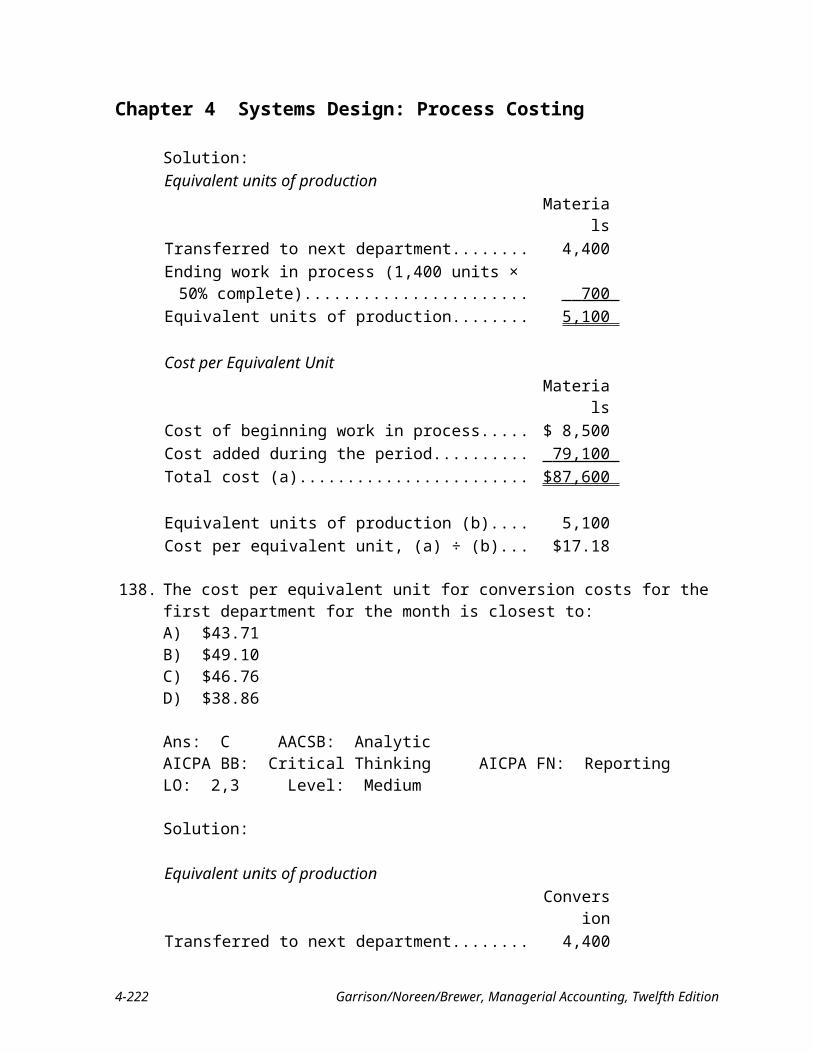

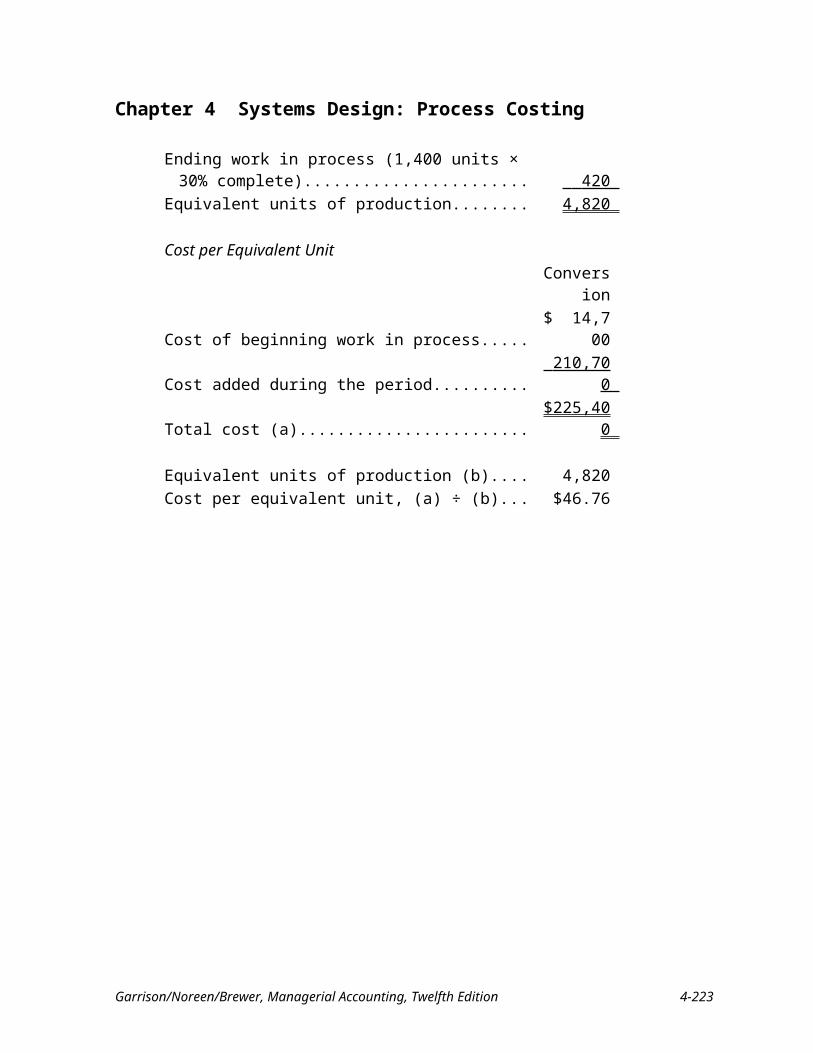

Transferred to next department.......................... 12,000 12,000 Ending work in process (materials: 6,000 units

× 100% complete; conversion: 6,000 units × 50% complete)............................................... 6,000 3,000

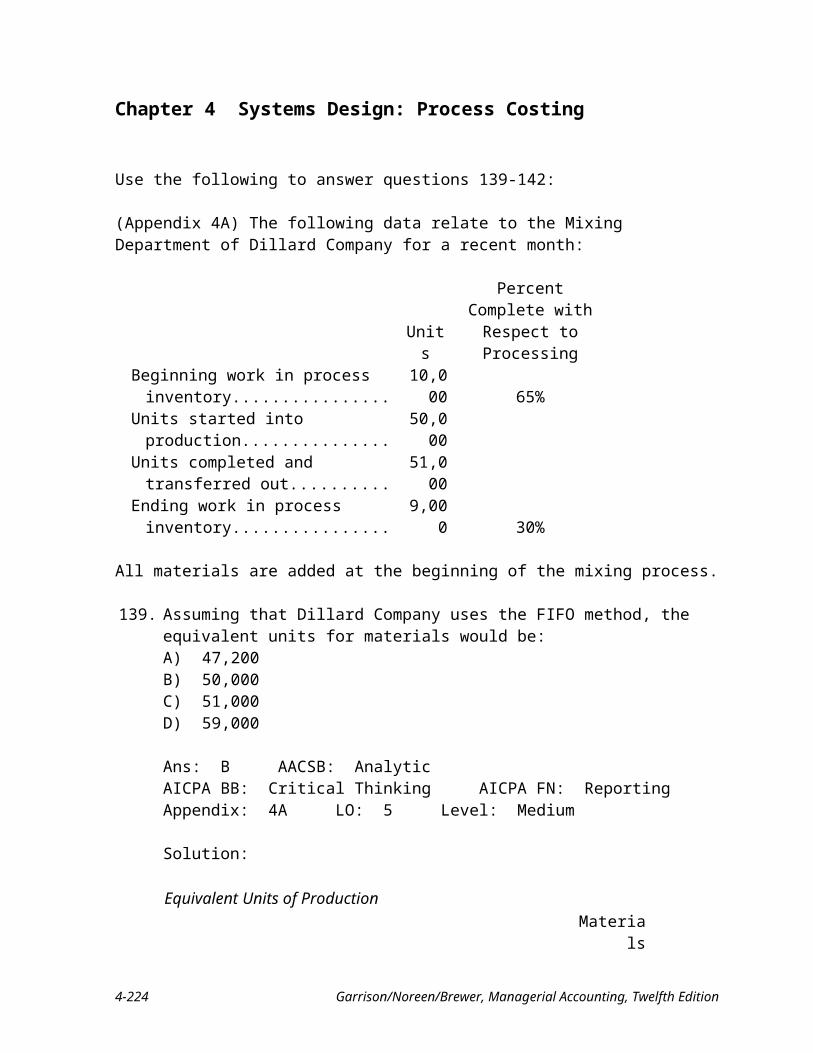

Equivalent units of production........................... 18,000 15,000

Cost per Equivalent UnitMaterials Conversion Total

Cost of beginning work in process.................... $13,800 $ 3,740 Cost added during the period............................. 42,000 26,260 Total cost (a)...................................................... $55,800 $30,000

Equivalent units of production (b)..................... 18,000 15,000 Cost per equivalent unit, (a) ÷ (b)...................... $3.10 $2.00 $5.10

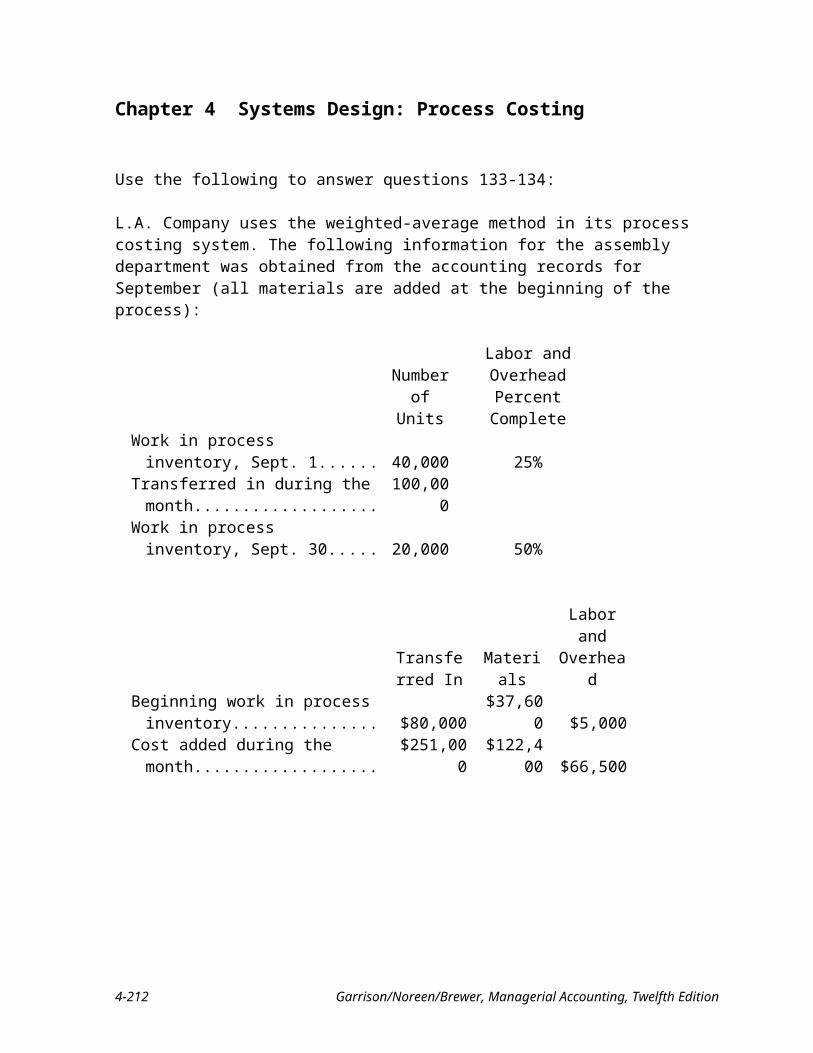

4-18 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

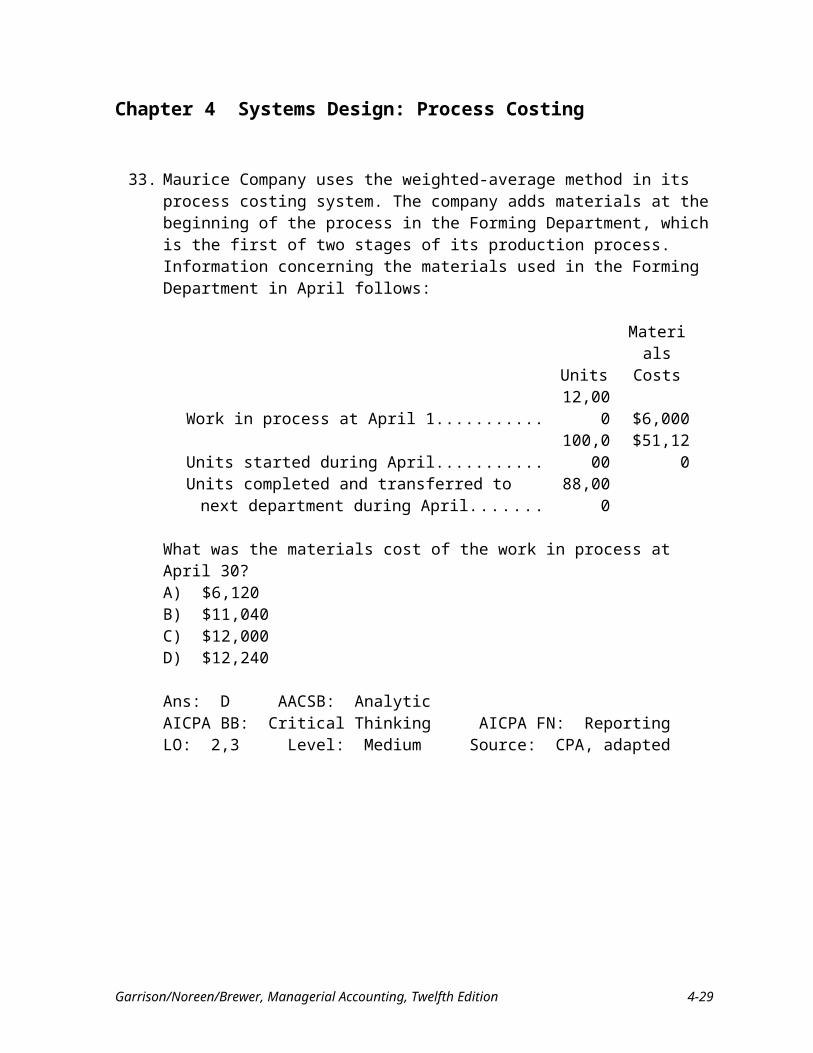

33. Maurice Company uses the weighted-average method in its process costing system. The company adds materials at the beginning of the process in the Forming Department, which is the first of two stages of its production process. Information concerning the materials used in the Forming Department in April follows:

UnitsMaterials

CostsWork in process at April 1............................................... 12,000 $6,000Units started during April................................................ 100,000 $51,120Units completed and transferred to next department

during April.................................................................. 88,000

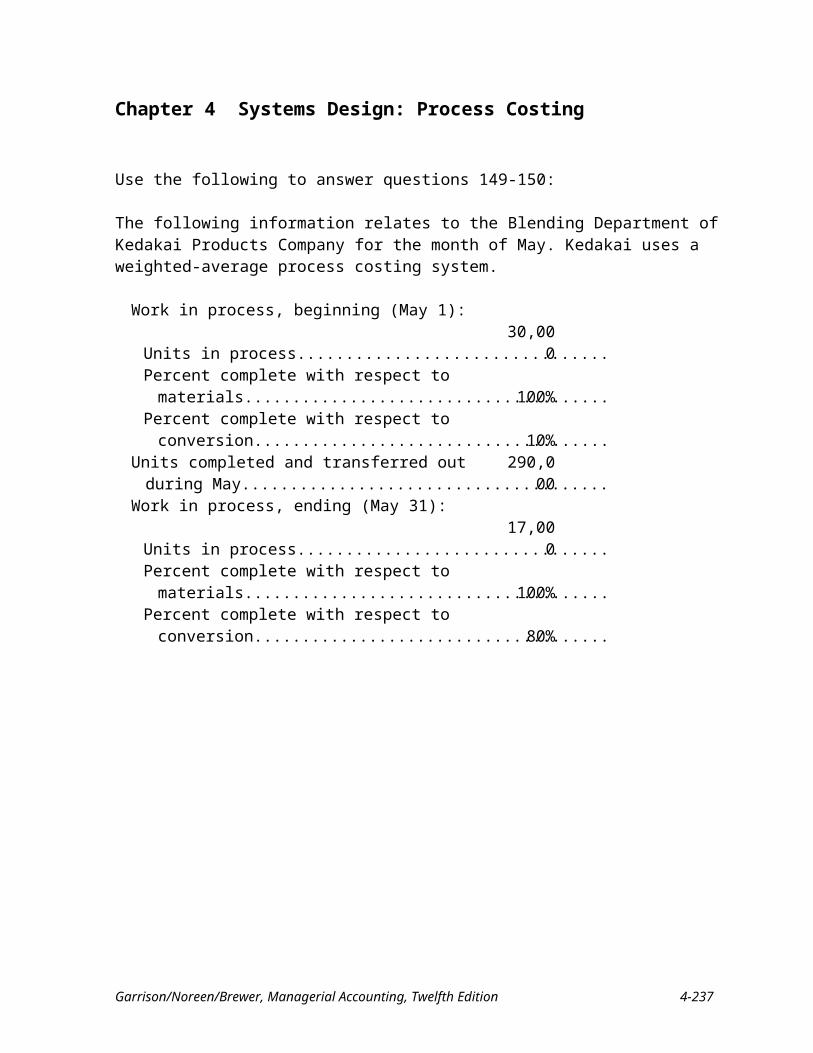

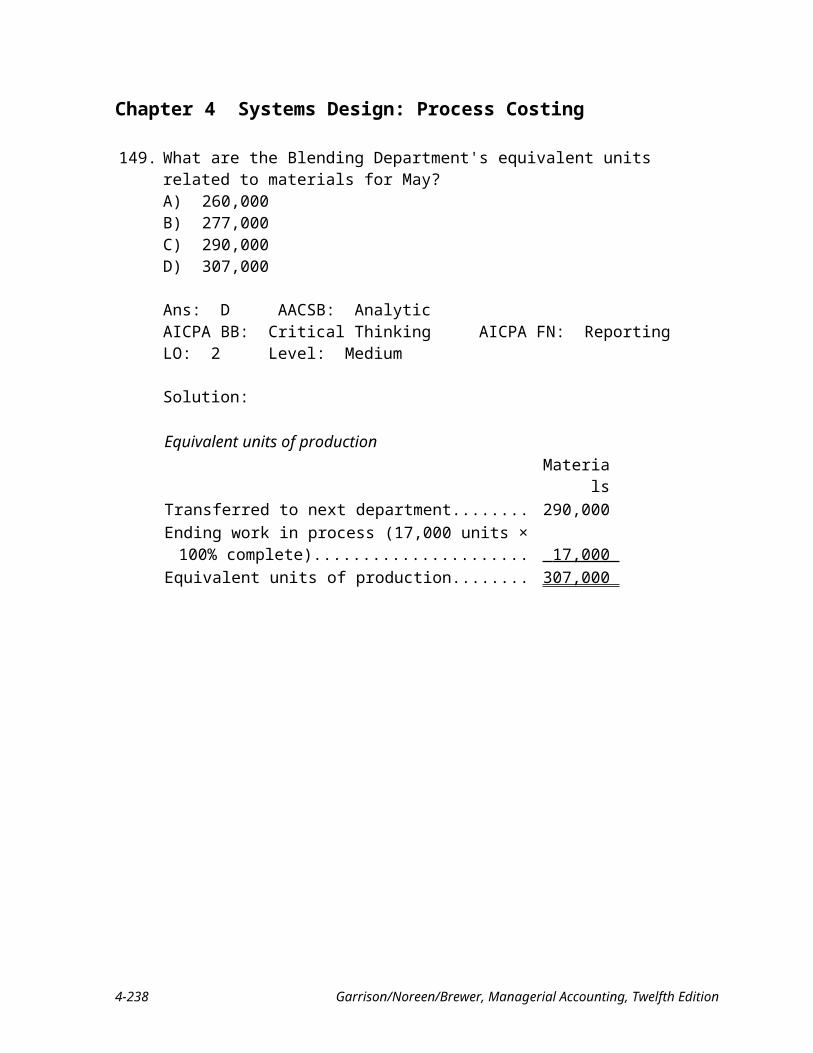

What was the materials cost of the work in process at April 30?A) $6,120B) $11,040C) $12,000D) $12,240

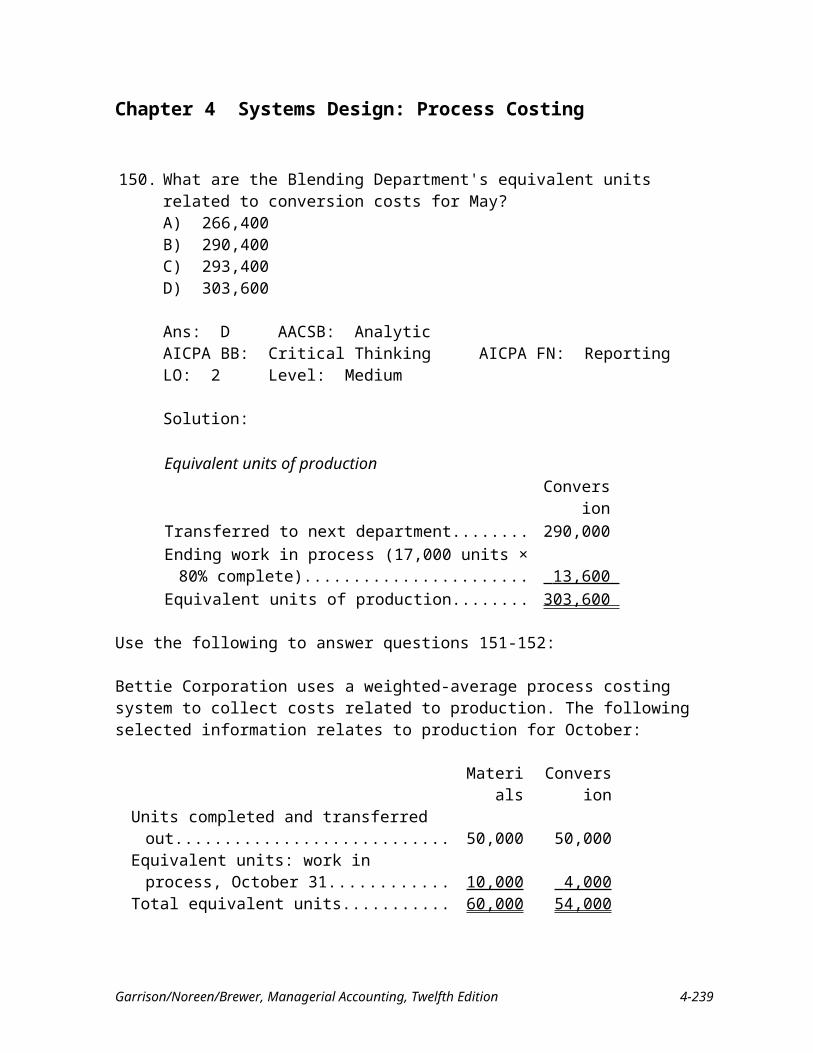

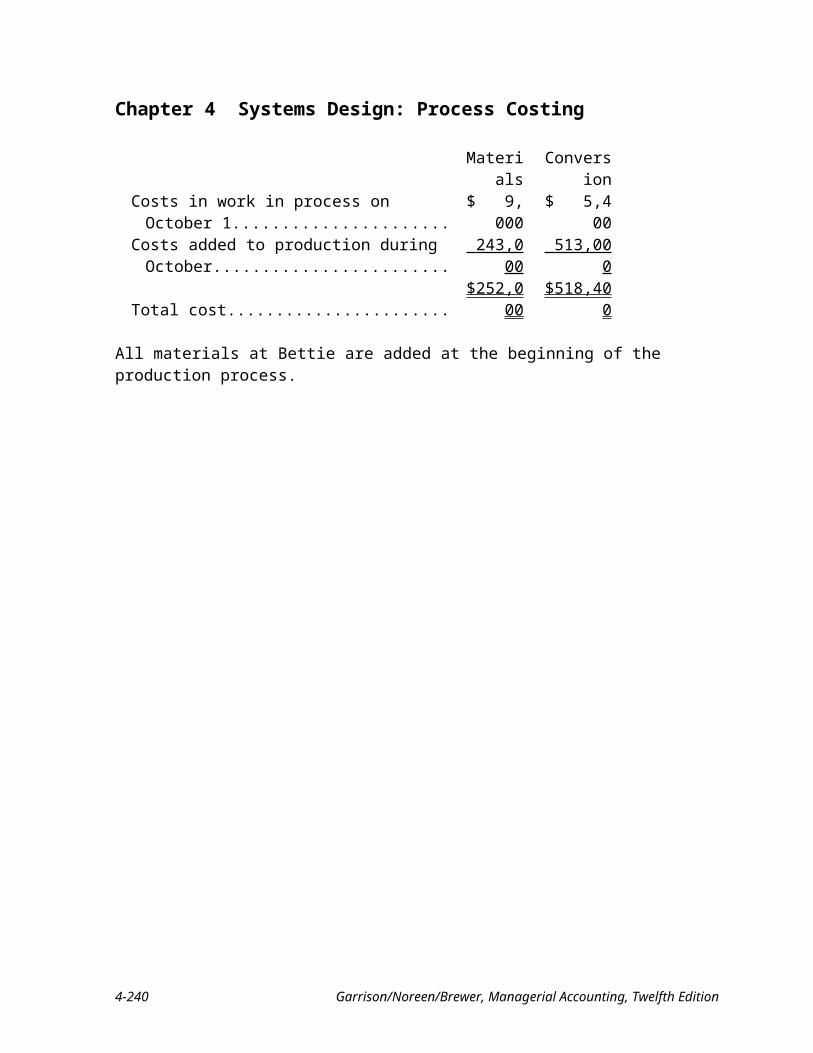

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,3 Level: Medium Source: CPA, adapted

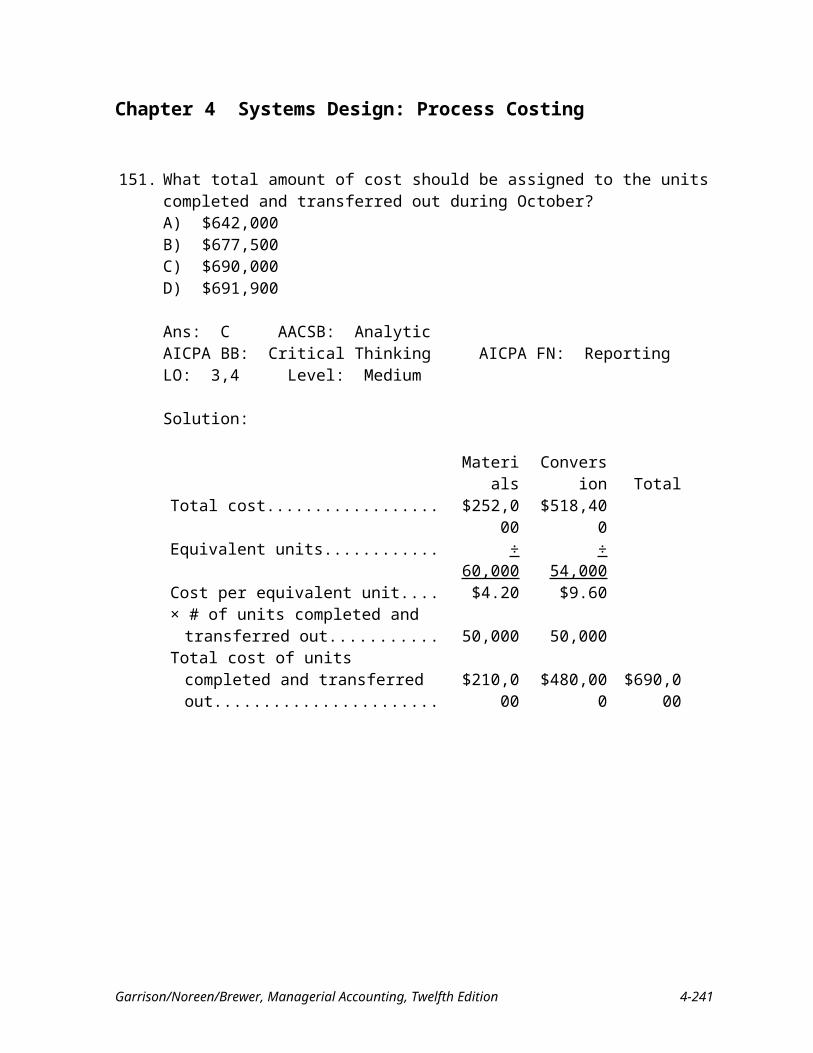

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-19

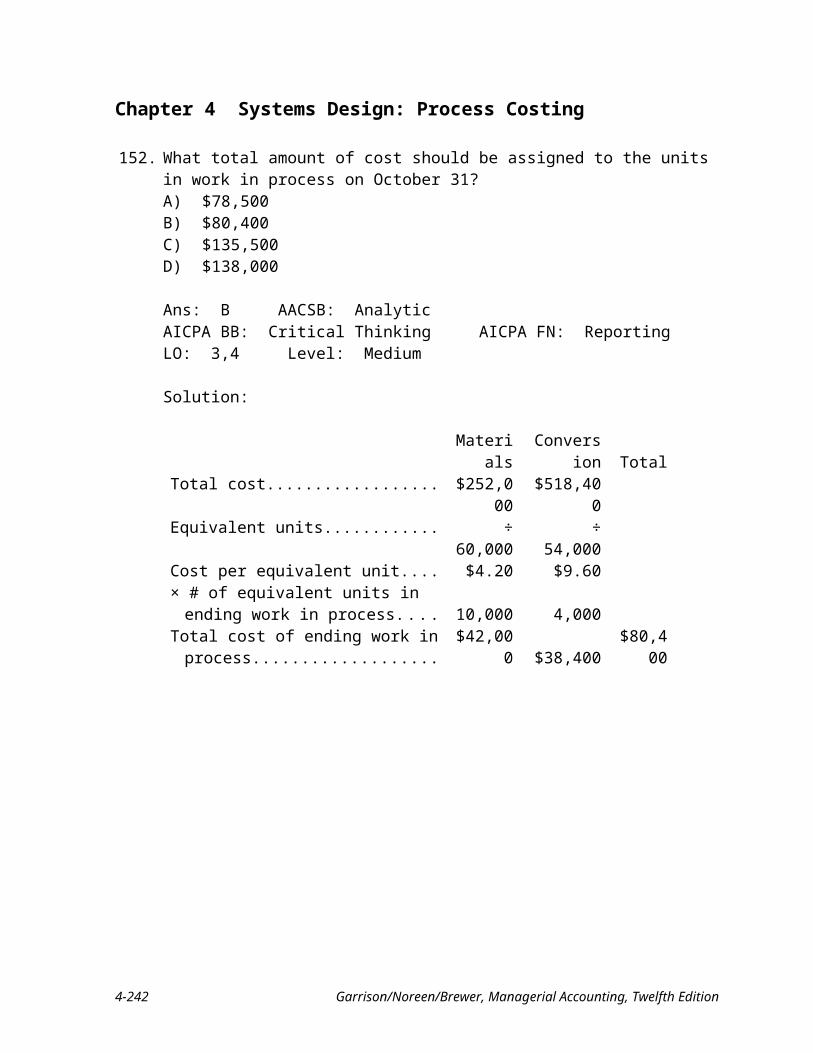

Chapter 4 Systems Design: Process Costing

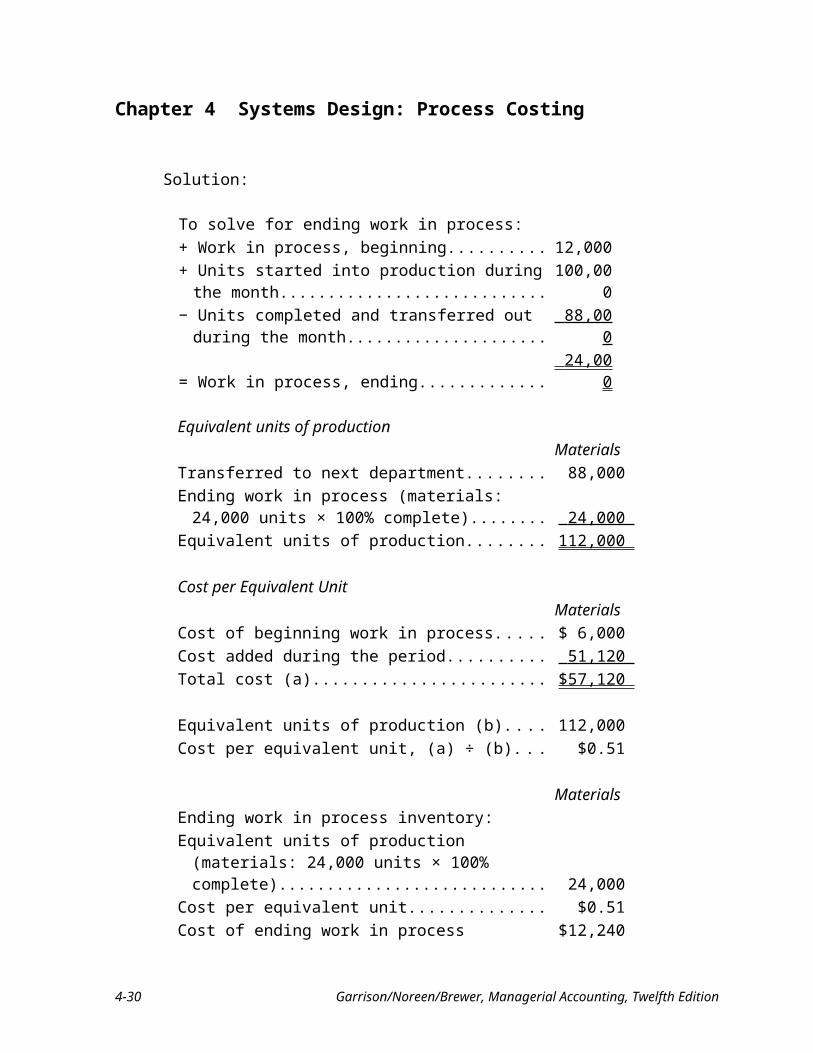

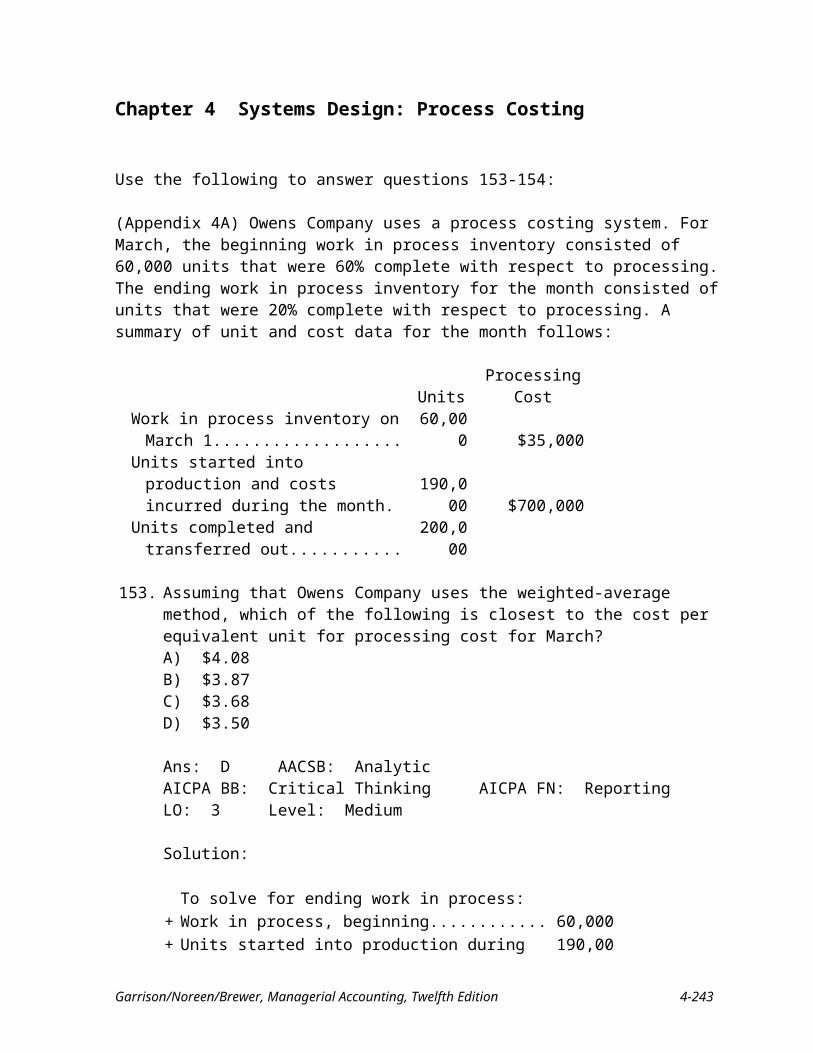

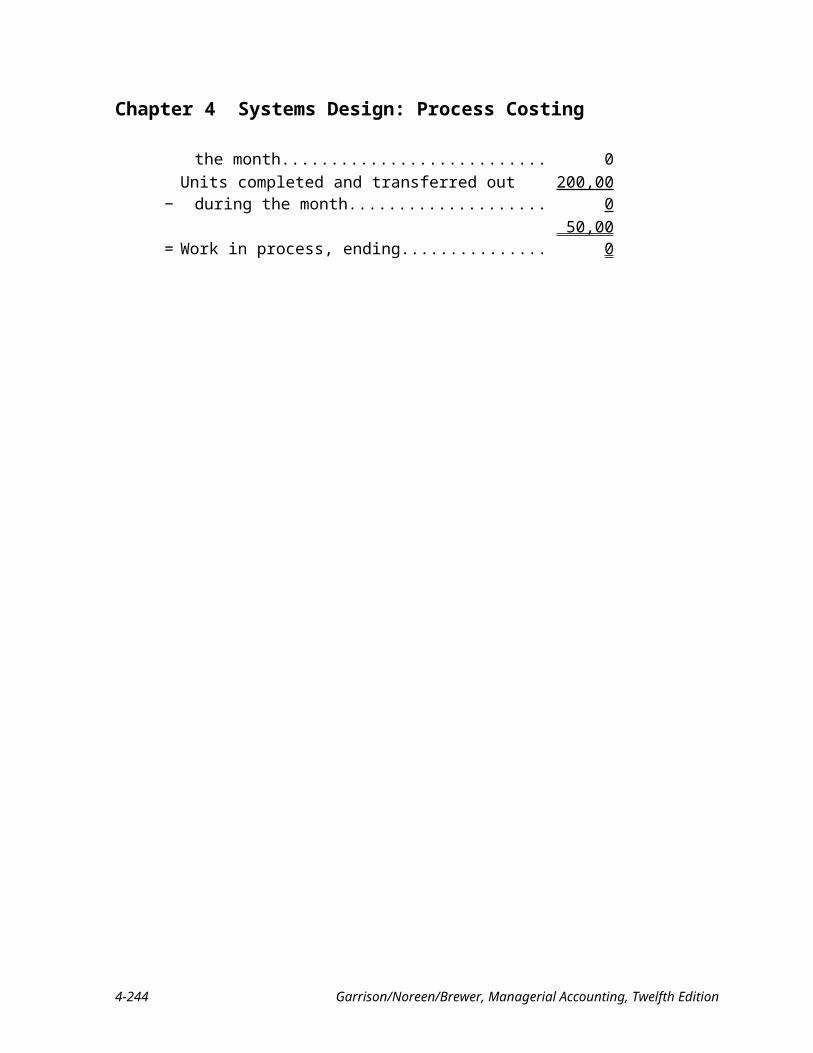

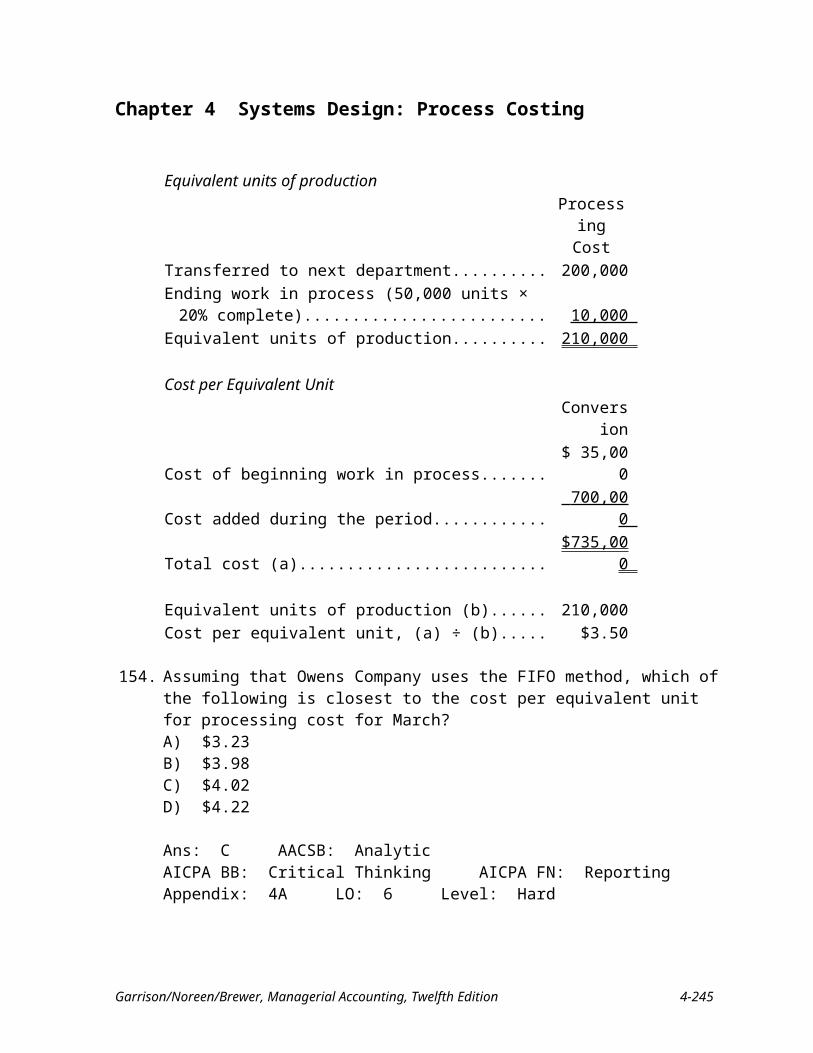

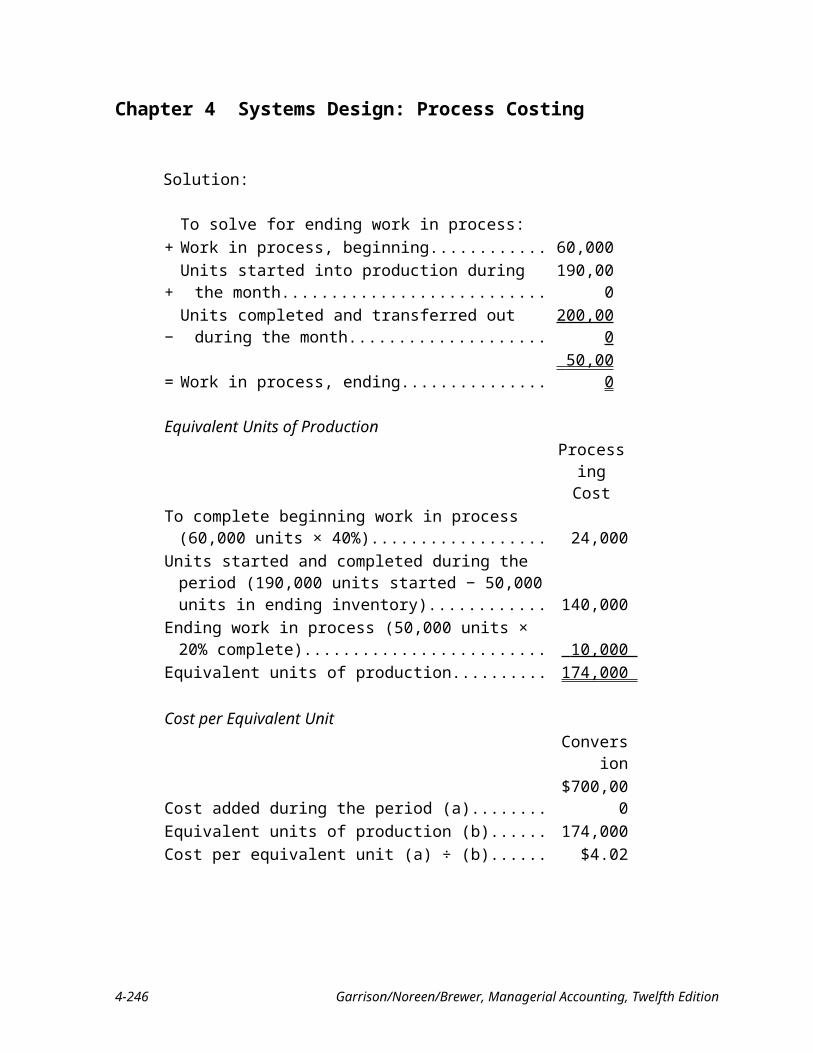

Solution:

To solve for ending work in process:+ Work in process, beginning............................................ 12,000+ Units started into production during the month.............. 100,000− Units completed and transferred out during the month... 88,000 = Work in process, ending.................................................. 24,000

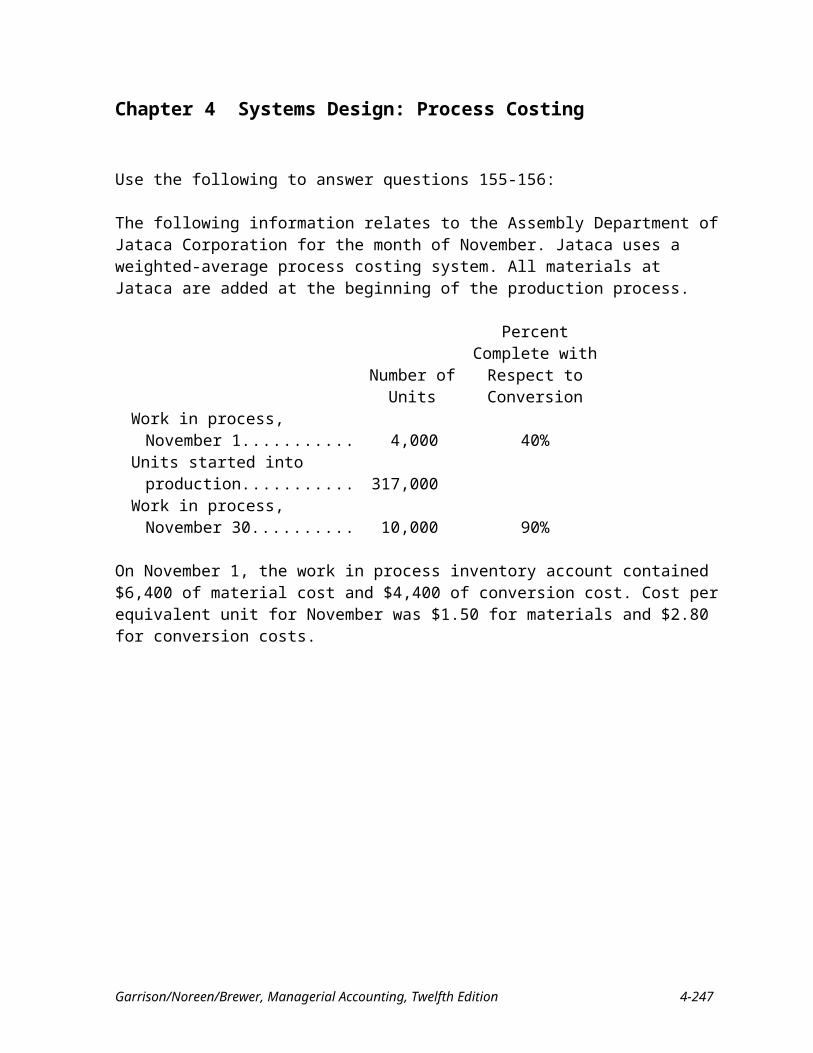

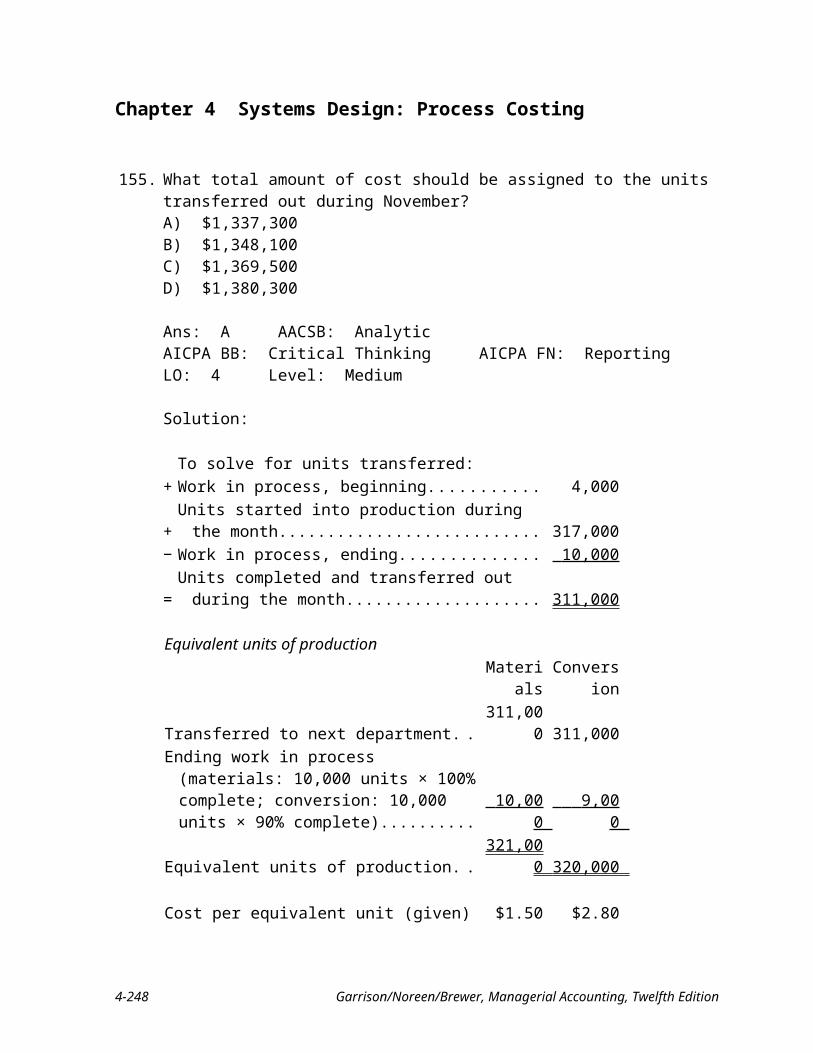

Equivalent units of productionMaterials

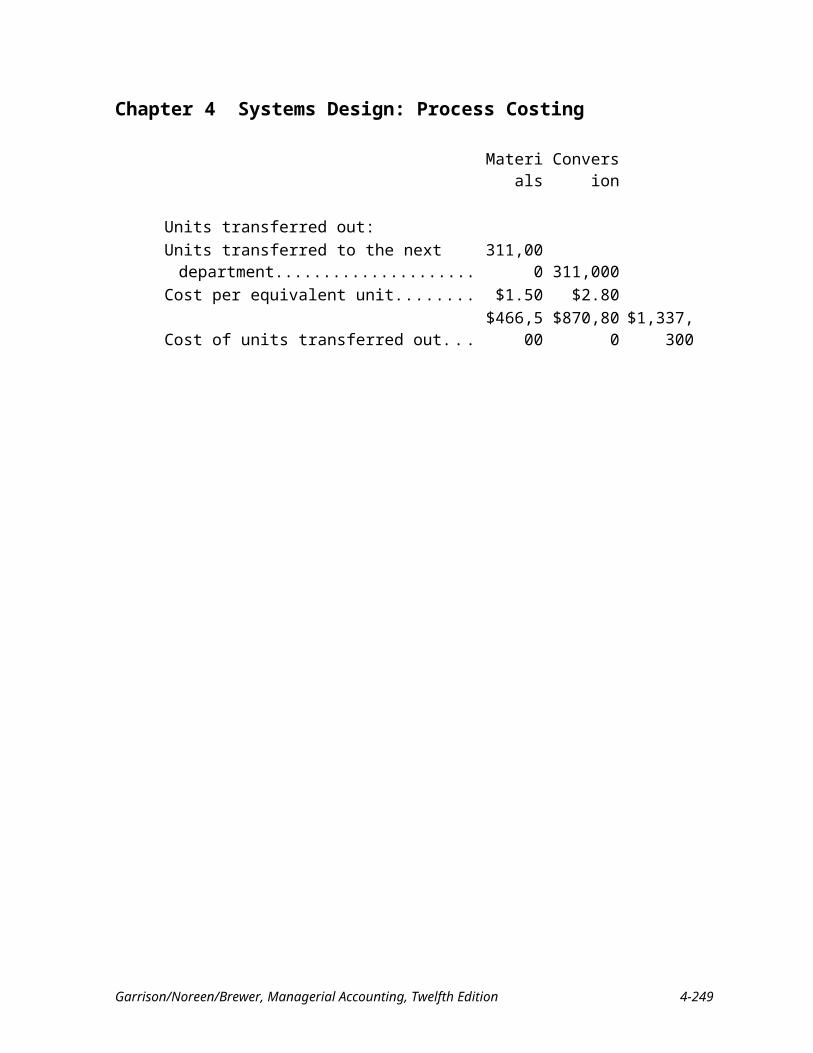

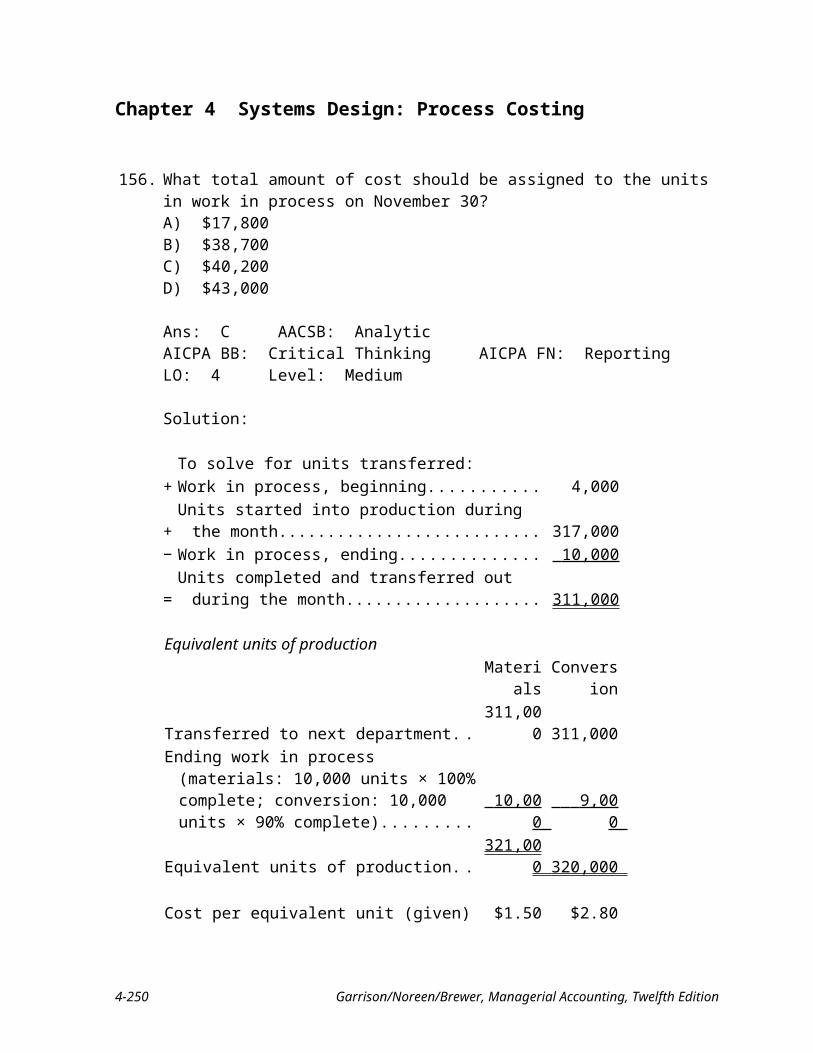

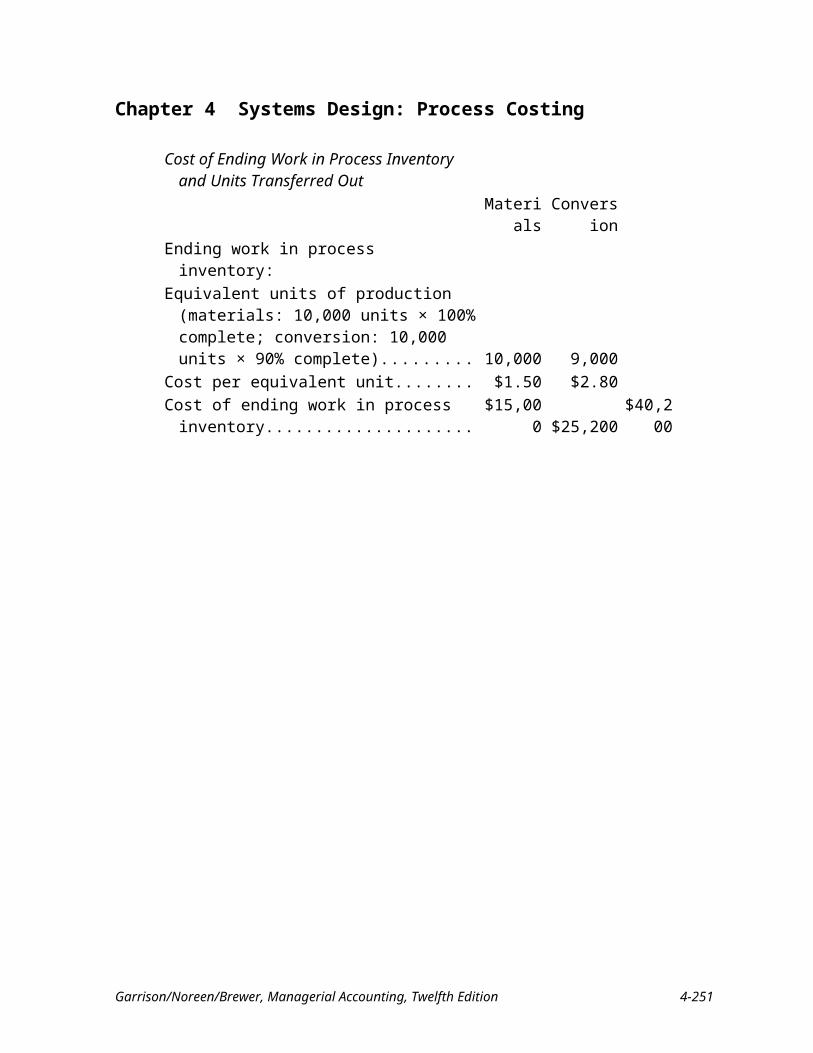

Transferred to next department........................................... 88,000 Ending work in process (materials: 24,000 units × 100%

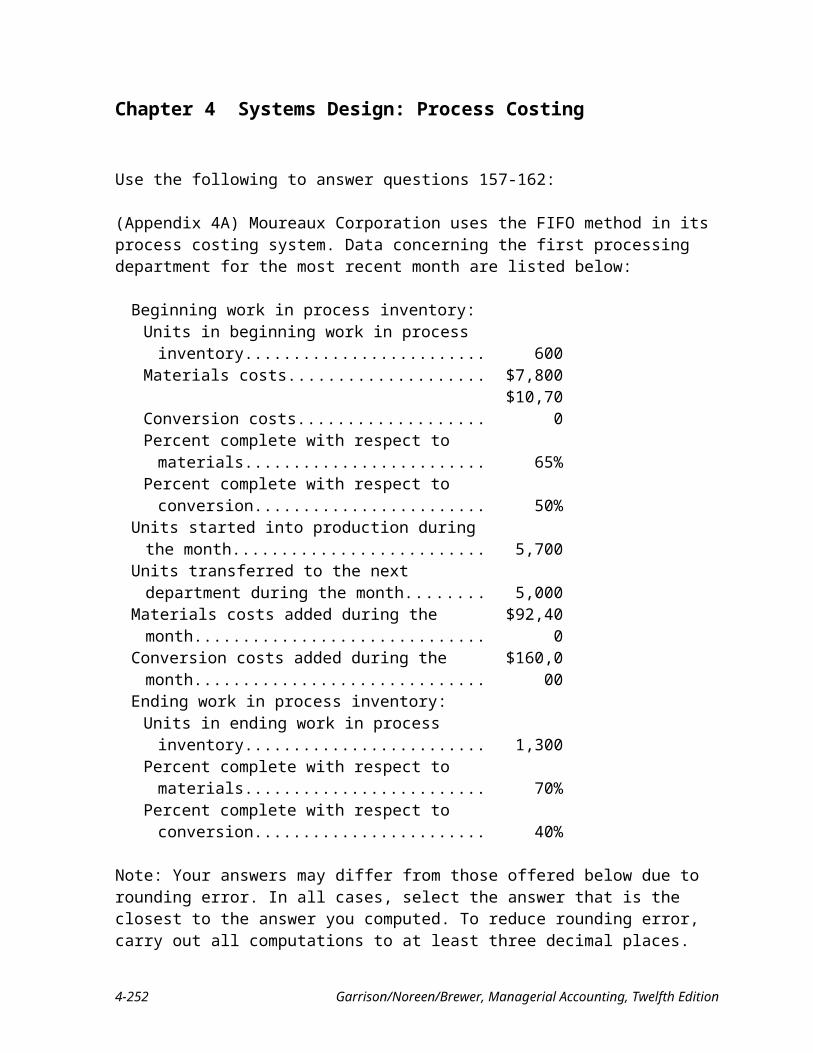

complete)......................................................................... 24,000 Equivalent units of production........................................... 112,000

Cost per Equivalent UnitMaterials

Cost of beginning work in process..................................... $ 6,000 Cost added during the period.............................................. 51,120 Total cost (a)....................................................................... $57,120

Equivalent units of production (b)...................................... 112,000 Cost per equivalent unit, (a) ÷ (b)....................................... $0.51

MaterialsEnding work in process inventory:Equivalent units of production (materials: 24,000 units ×

100% complete).............................................................. 24,000 Cost per equivalent unit...................................................... $0.51 Cost of ending work in process inventory.......................... $12,240

4-20 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

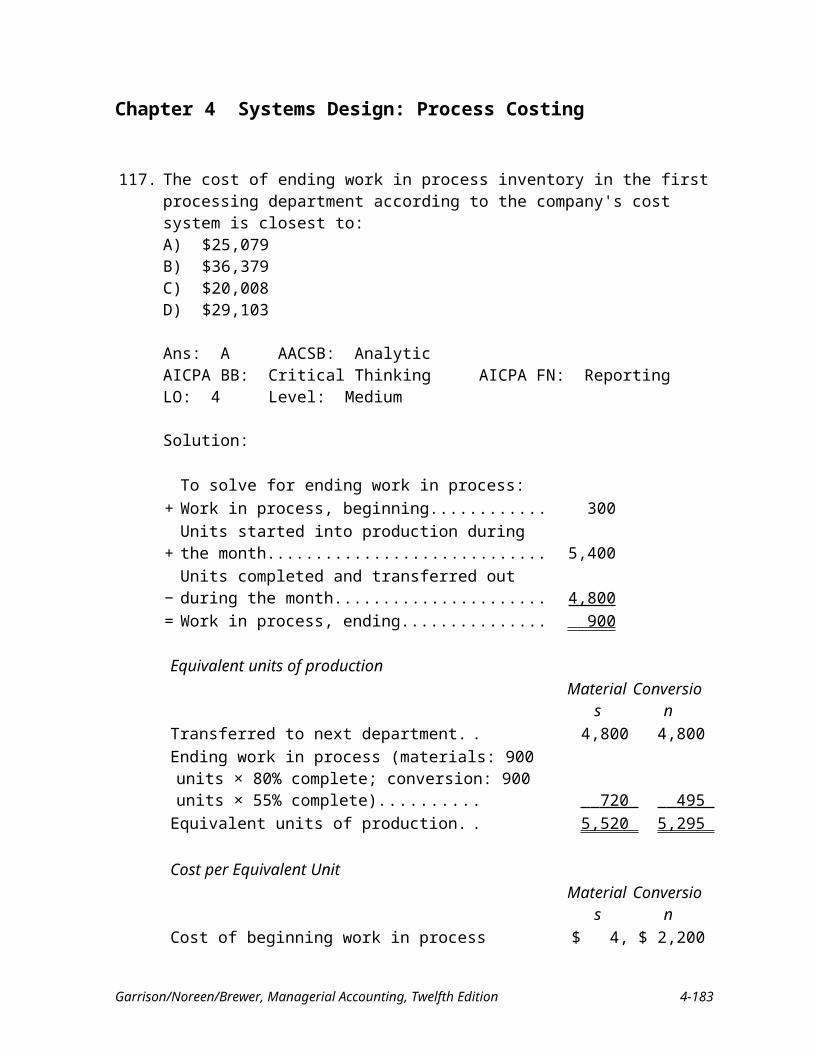

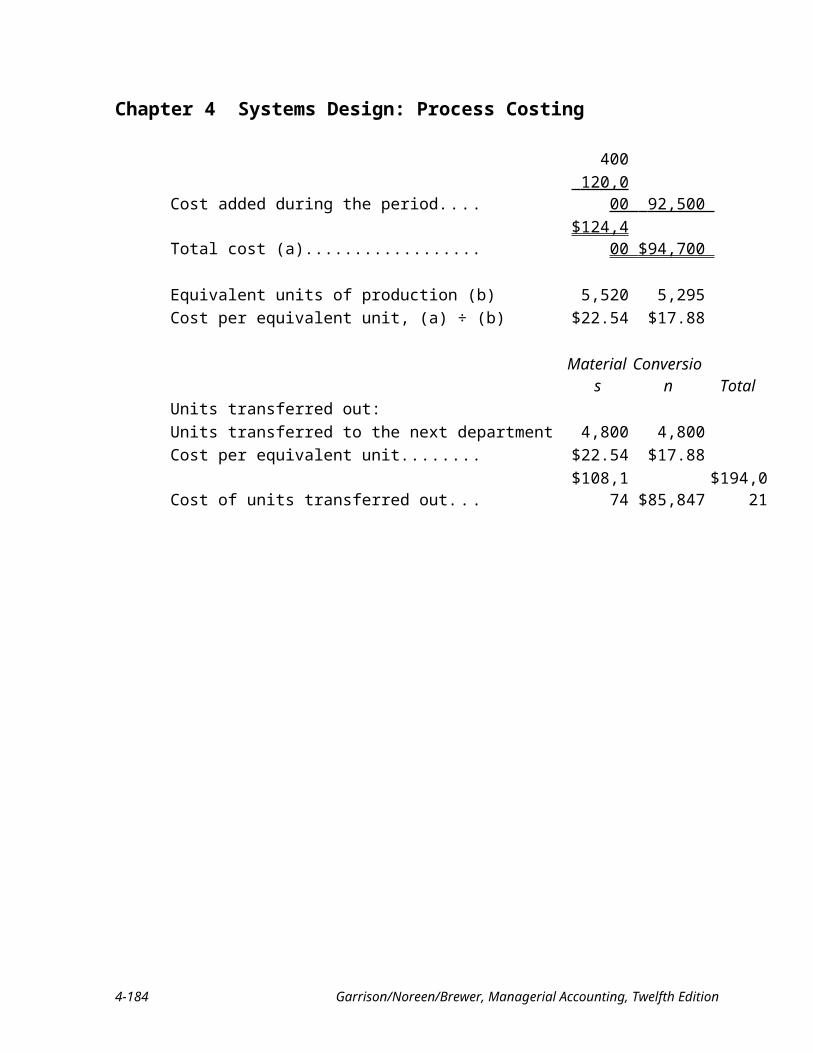

Chapter 4 Systems Design: Process Costing

34. Destry Company uses the weighted-average method in its process costing system. The first processing department, the Welding Department, started the month with 10,000 units in its beginning work in process inventory that were 30% complete with respect to conversion costs. The conversion cost in this beginning work in process inventory was $19,200. An additional 60,000 units were started into production during the month. There were 19,000 units in the ending work in process inventory of the Welding Department that were 70% complete with respect to conversion costs. A total of $380,060 in conversion costs were incurred in the department during the month.

What would be the cost per equivalent unit for conversion costs for the month? (Round off to three decimal places.)A) $6.400B) $6.334C) $6.209D) $4.811

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,3 Level: Medium

Solution:

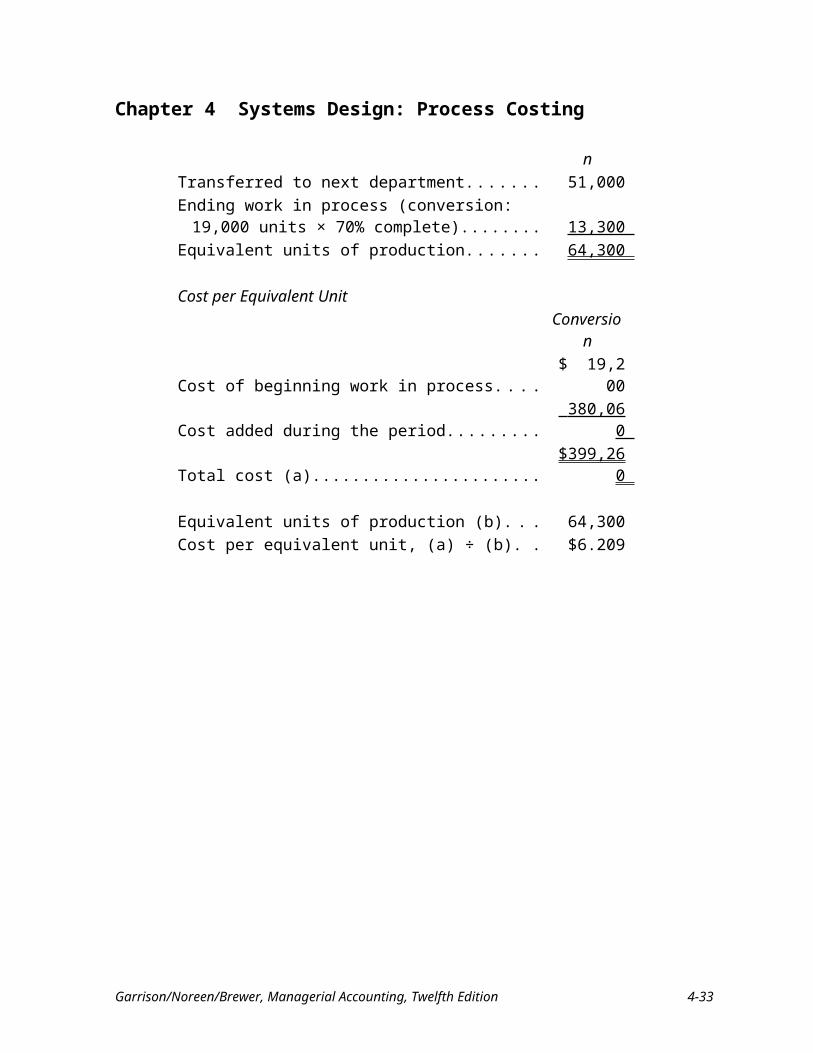

To solve for units transferred:+ Work in process, beginning.................................................. 10,000+ Units started into production during the month.................... 60,000− Work in process, ending....................................................... 19,000= Units completed and transferred out during the month........ 51,000

Equivalent units of productionConversion

Transferred to next department......................................... 51,000 Ending work in process (conversion: 19,000 units × 70%

complete)....................................................................... 13,300 Equivalent units of production.......................................... 64,300

Cost per Equivalent UnitConversion

Cost of beginning work in process.................................... $ 19,200 Cost added during the period............................................ 380,060 Total cost (a)..................................................................... $399,260

Equivalent units of production (b).................................... 64,300 Cost per equivalent unit, (a) ÷ (b)..................................... $6.209

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-21

Chapter 4 Systems Design: Process Costing

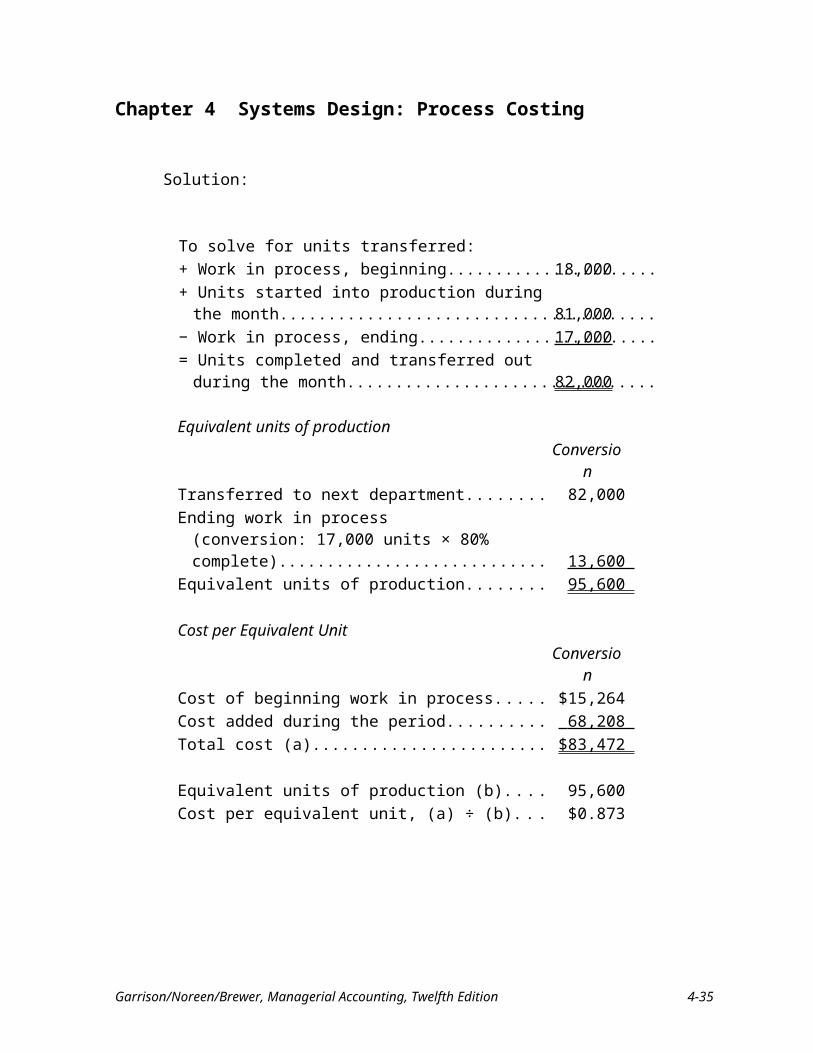

35. Limber Company uses the weighted-average method in its process costing system. Operating data for the first processing department for the month of June appear below:

Units

Percent Complete with

Respect to Conversion

Beginning work in process inventory........ 18,000 80%Started into production during June........... 81,000Ending work in process inventory............. 17,000 80%

According to the company's records, the conversion cost in beginning work in process inventory was $15,264 at the beginning of June. Additional conversion costs of $68,208 were incurred in the department during the month.What was the cost per equivalent unit for conversion costs for the month? (Round off to three decimal places.)A) $0.873B) $0.696C) $0.842D) $1.060

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,3 Level: Medium

4-22 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

Solution:

To solve for units transferred:+ Work in process, beginning........................................................................18,000+ Units started into production during the month..........................................81,000− Work in process, ending.............................................................................17,000= Units completed and transferred out during the month..............................82,000

Equivalent units of productionConversion

Transferred to next department........................................... 82,000 Ending work in process

(conversion: 17,000 units × 80% complete)................... 13,600 Equivalent units of production........................................... 95,600

Cost per Equivalent UnitConversion

Cost of beginning work in process..................................... $15,264 Cost added during the period.............................................. 68,208 Total cost (a)....................................................................... $83,472

Equivalent units of production (b)...................................... 95,600 Cost per equivalent unit, (a) ÷ (b)....................................... $0.873

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-23

Chapter 4 Systems Design: Process Costing

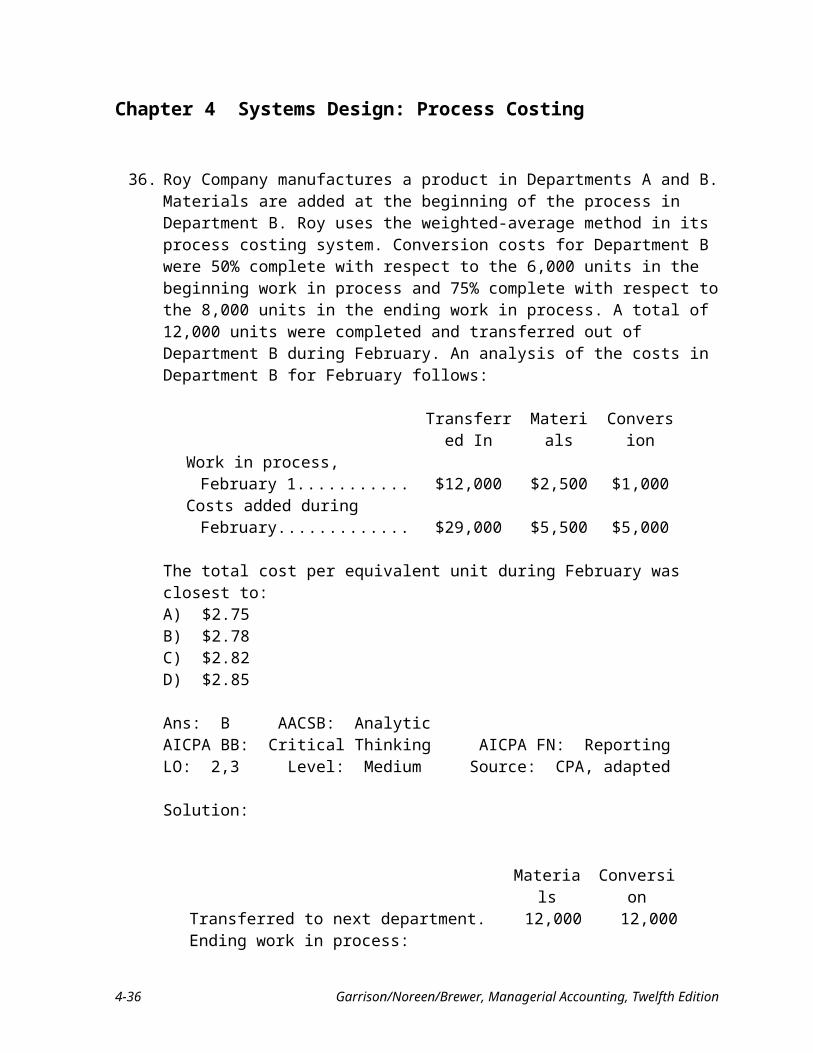

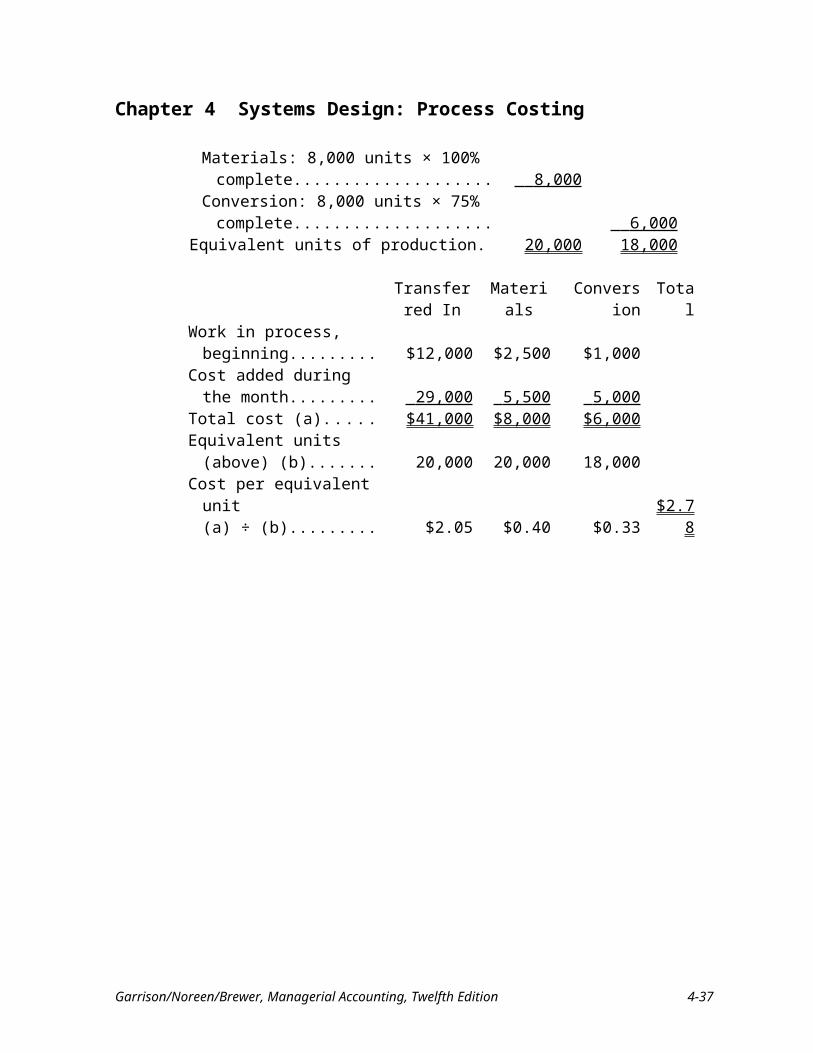

36. Roy Company manufactures a product in Departments A and B. Materials are added at the beginning of the process in Department B. Roy uses the weighted-average method in its process costing system. Conversion costs for Department B were 50% complete with respect to the 6,000 units in the beginning work in process and 75% complete with respect to the 8,000 units in the ending work in process. A total of 12,000 units were completed and transferred out of Department B during February. An analysis of the costs in Department B for February follows:

Transferred In Materials ConversionWork in process, February 1.......... $12,000 $2,500 $1,000Costs added during February......... $29,000 $5,500 $5,000

The total cost per equivalent unit during February was closest to:A) $2.75B) $2.78C) $2.82D) $2.85

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,3 Level: Medium Source: CPA, adapted

Solution:

Materials ConversionTransferred to next department.......................... 12,000 12,000Ending work in process:

Materials: 8,000 units × 100% complete........ 8,000 Conversion: 8,000 units × 75% complete....... 6,000

Equivalent units of production........................... 20,000 18,000

Transferred In Materials Conversion Total

Work in process, beginning... $12,000 $2,500 $1,000Cost added during the month 29,000 5,500 5,000 Total cost (a).......................... $41,000 $8,000 $6,000Equivalent units (above) (b). . 20,000 20,000 18,000Cost per equivalent unit

(a) ÷ (b).............................. $2.05 $0.40 $0.33 $2.78

4-24 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

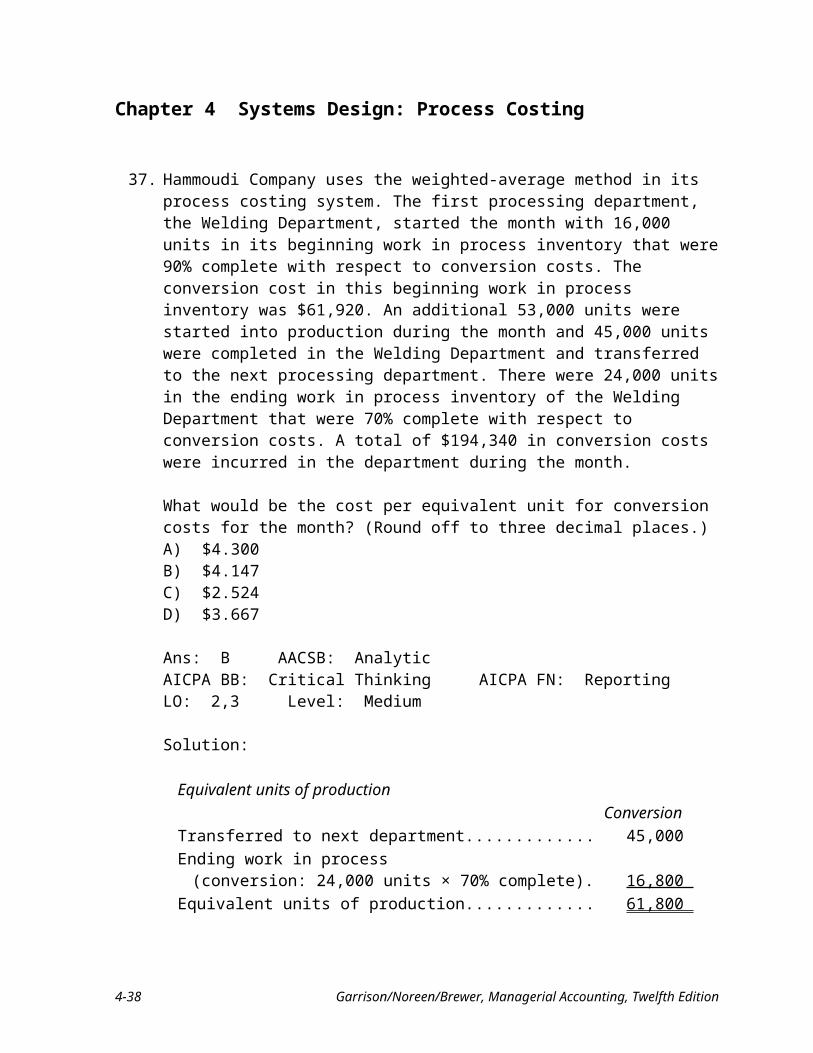

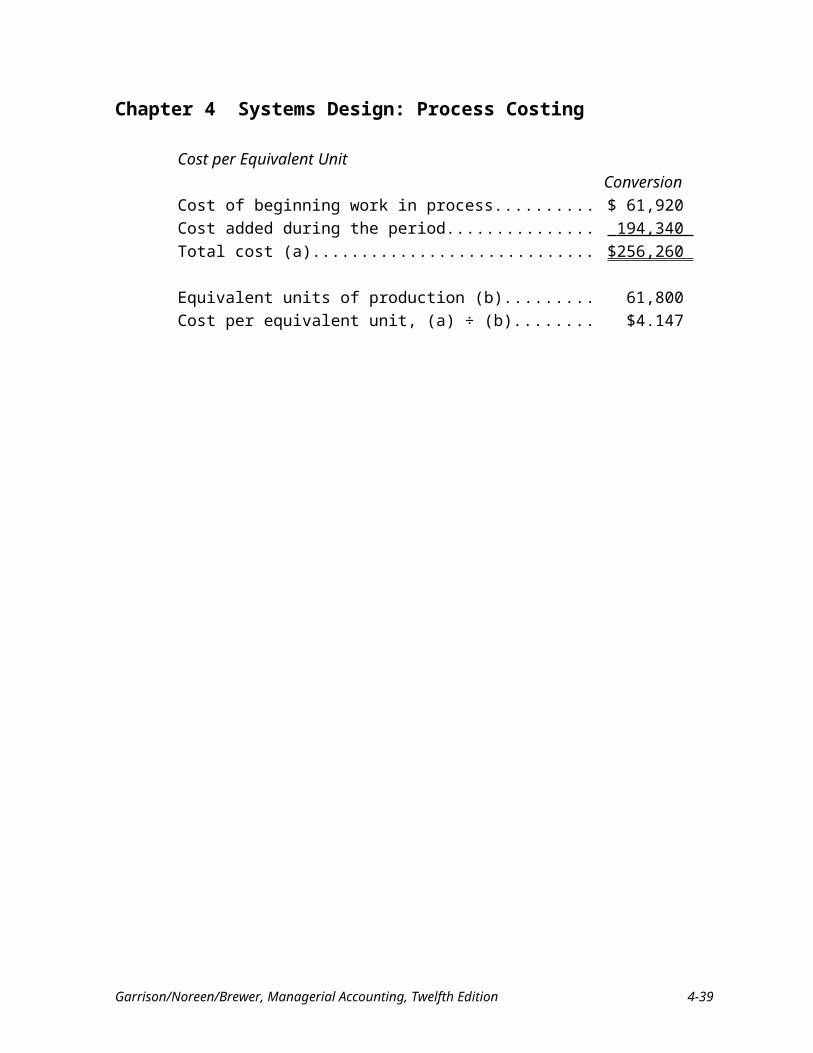

37. Hammoudi Company uses the weighted-average method in its process costing system. The first processing department, the Welding Department, started the month with 16,000 units in its beginning work in process inventory that were 90% complete with respect to conversion costs. The conversion cost in this beginning work in process inventory was $61,920. An additional 53,000 units were started into production during the month and 45,000 units were completed in the Welding Department and transferred to the next processing department. There were 24,000 units in the ending work in process inventory of the Welding Department that were 70% complete with respect to conversion costs. A total of $194,340 in conversion costs were incurred in the department during the month.

What would be the cost per equivalent unit for conversion costs for the month? (Round off to three decimal places.)A) $4.300B) $4.147C) $2.524D) $3.667

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,3 Level: Medium

Solution:

Equivalent units of productionConversion

Transferred to next department....................................................... 45,000 Ending work in process

(conversion: 24,000 units × 70% complete)............................... 16,800 Equivalent units of production....................................................... 61,800

Cost per Equivalent UnitConversion

Cost of beginning work in process................................................. $ 61,920 Cost added during the period.......................................................... 194,340 Total cost (a)................................................................................... $256,260

Equivalent units of production (b).................................................. 61,800 Cost per equivalent unit, (a) ÷ (b)................................................... $4.147

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-25

Chapter 4 Systems Design: Process Costing

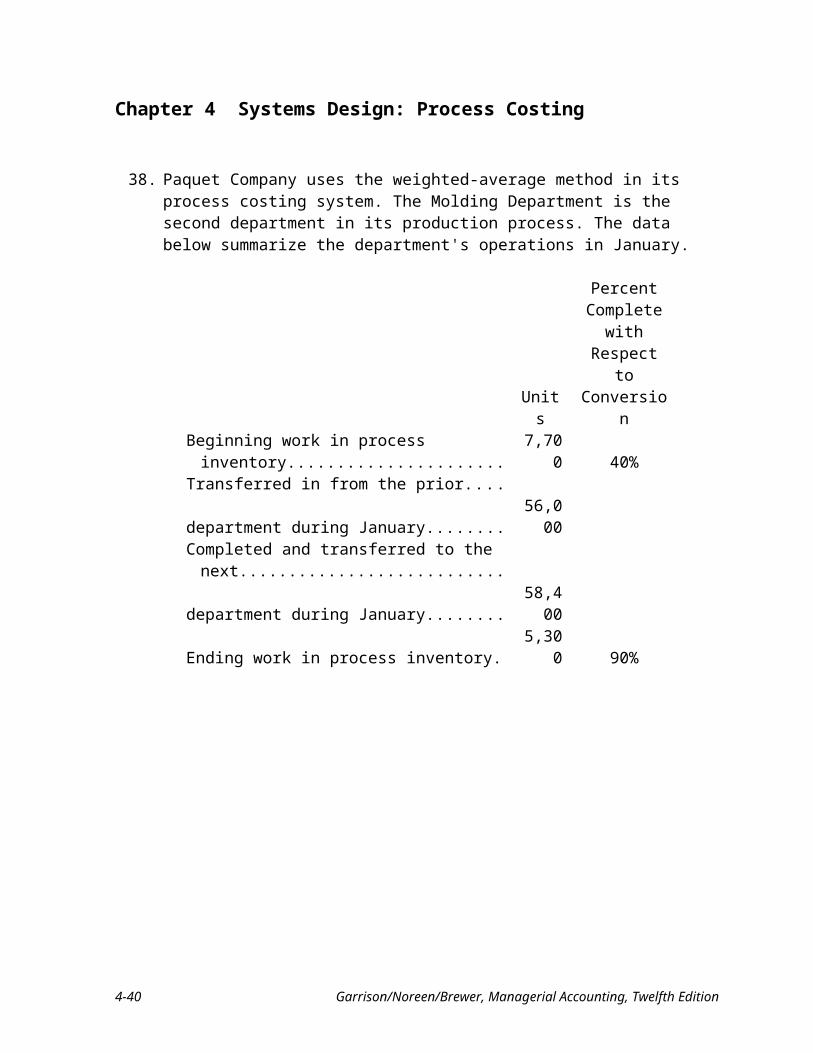

38. Paquet Company uses the weighted-average method in its process costing system. The Molding Department is the second department in its production process. The data below summarize the department's operations in January.

Units

Percent Complete with

Respect to Conversion

Beginning work in process inventory.................... 7,700 40%Transferred in from the prior.................................department during January..................................... 56,000Completed and transferred to the next...................department during January..................................... 58,400Ending work in process inventory......................... 5,300 90%

The accounting records indicate that the conversion cost that had been assigned to beginning work in process inventory was $16,940 and a total of $347,320 in conversion costs were incurred in the department during January.

What was the cost per equivalent unit for conversion costs for January in the Molding Department? (Round off to three decimal places.)A) $5.500B) $5.666C) $5.766D) $6.202

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,3 Level: Medium

Solution:Units transferred out..................................................................... 58,400Add: equivalent units in the ending inventory (5300 × 90%

complete)................................................................................... 4,770 Equivalent units of production...................................................... 63,170

Cost in the beginning inventory.................................................... $ 16,940Cost added during the month........................................................ 347,320 Total cost....................................................................................... $364,260

$364,260 ÷ 63,170 units = $5.766 per unit

4-26 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

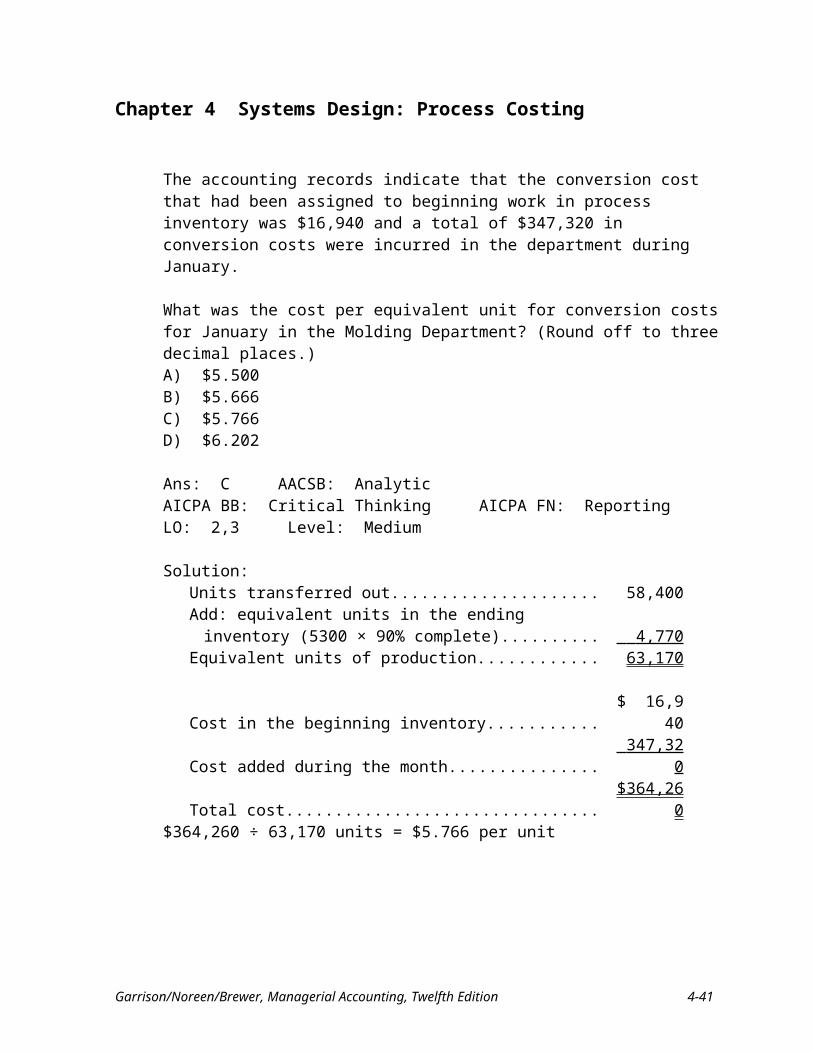

39. Jimmy Company uses the weighted-average method in its process costing system. The ending work in process inventory consists of 9,000 units. The ending work in process inventory is 100% complete with respect to materials and 70% complete with respect to labor and overhead. If the cost per equivalent unit for the period is $3.75 for material and $1.25 for labor and overhead, what is the balance of the ending work in process inventory account?A) $41,625B) $33,750C) $45,000D) $31,500

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2,4 Level: Medium

Solution:

Ending work in process:Materials: 9,000 units × 100% complete.... 9,000Conversion: 9,000 units × 70% complete... 6,300

Ending work in process: Materials Conversion TotalEquivalent units of production............ 9,000 6,300Cost per equivalent unit...................... $3.75 $1.25Cost of ending work in process........... $33,750 $7,875 $41,625

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-27

Chapter 4 Systems Design: Process Costing

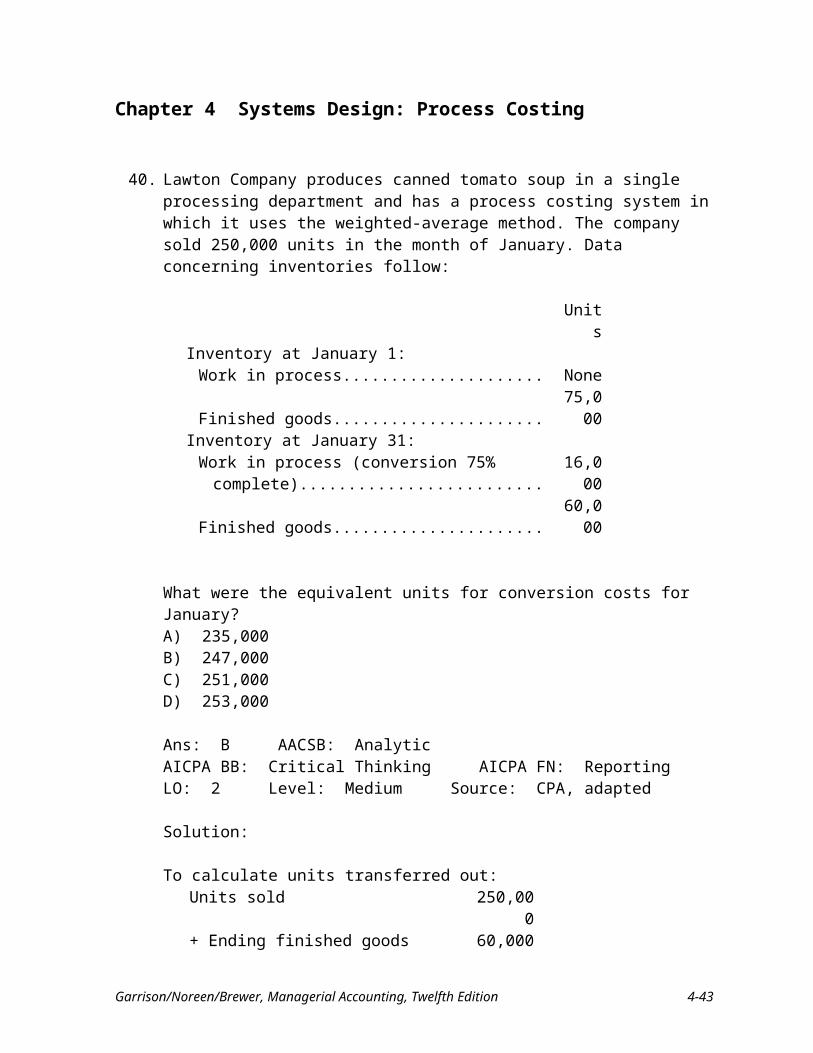

40. Lawton Company produces canned tomato soup in a single processing department and has a process costing system in which it uses the weighted-average method. The company sold 250,000 units in the month of January. Data concerning inventories follow:

Units Inventory at January 1:

Work in process............................................................ NoneFinished goods.............................................................. 75,000

Inventory at January 31:Work in process (conversion 75% complete)............... 16,000Finished goods.............................................................. 60,000

What were the equivalent units for conversion costs for January?A) 235,000B) 247,000C) 251,000D) 253,000

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Medium Source: CPA, adapted

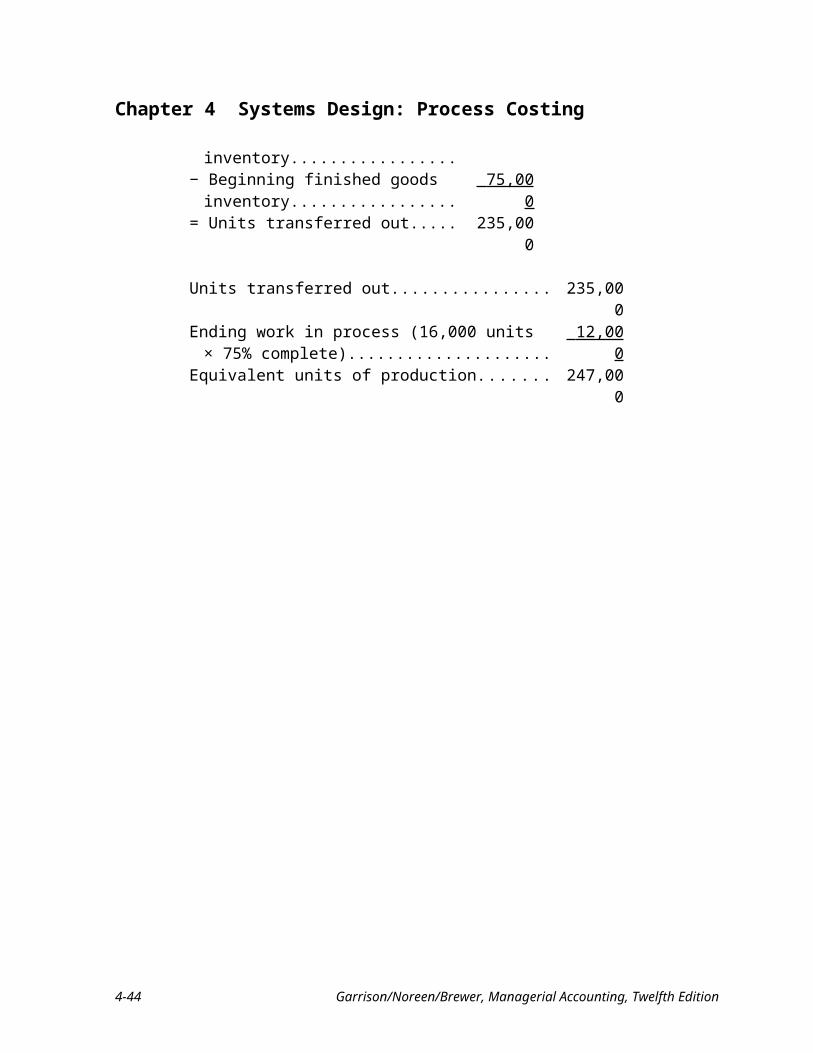

Solution:

To calculate units transferred out:Units sold 250,000+ Ending finished goods inventory........... 60,000− Beginning finished goods inventory...... 75,000 = Units transferred out.............................. 235,000

Units transferred out......................................................... 235,000Ending work in process (16,000 units × 75% complete).. 12,000 Equivalent units of production.......................................... 247,000

4-28 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

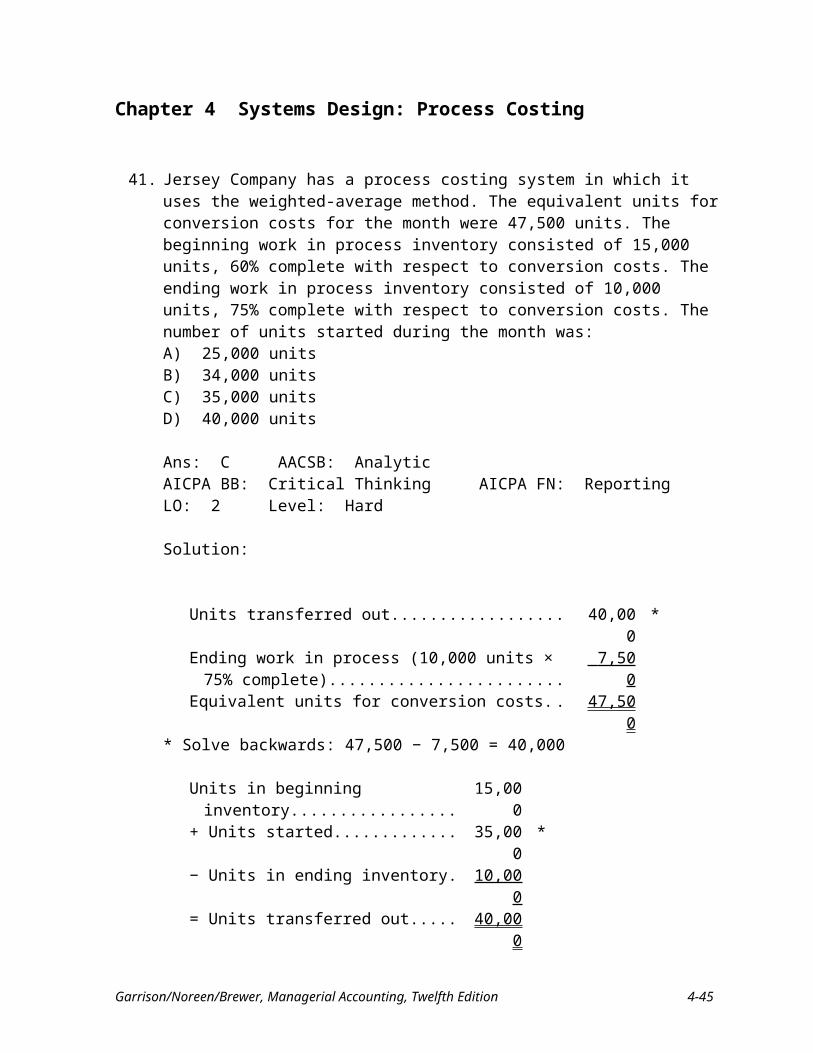

41. Jersey Company has a process costing system in which it uses the weighted-average method. The equivalent units for conversion costs for the month were 47,500 units. The beginning work in process inventory consisted of 15,000 units, 60% complete with respect to conversion costs. The ending work in process inventory consisted of 10,000 units, 75% complete with respect to conversion costs. The number of units started during the month was:A) 25,000 unitsB) 34,000 unitsC) 35,000 unitsD) 40,000 units

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Hard

Solution:

Units transferred out............................................................. 40,000 *Ending work in process (10,000 units × 75% complete)..... 7,500 Equivalent units for conversion costs.................................. 47,500

* Solve backwards: 47,500 − 7,500 = 40,000

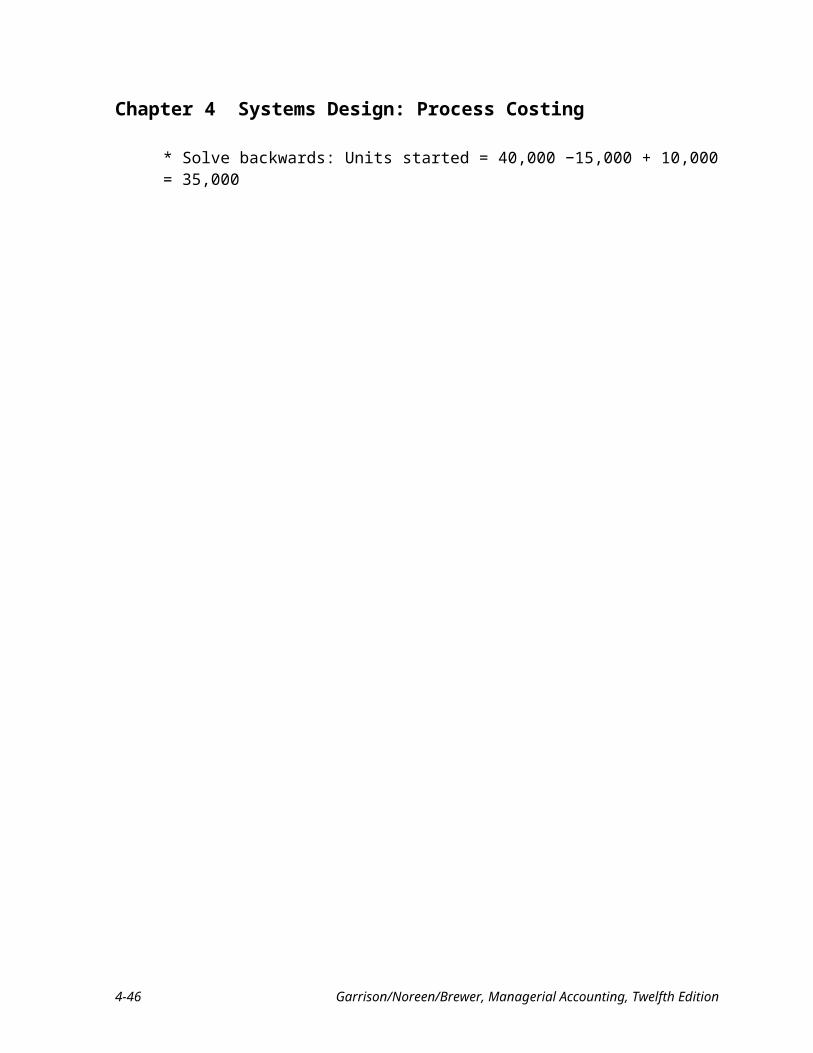

Units in beginning inventory..................... 15,000+ Units started........................................... 35,000 *− Units in ending inventory...................... 10,000= Units transferred out.............................. 40,000

* Solve backwards: Units started = 40,000 −15,000 + 10,000 = 35,000

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-29

Chapter 4 Systems Design: Process Costing

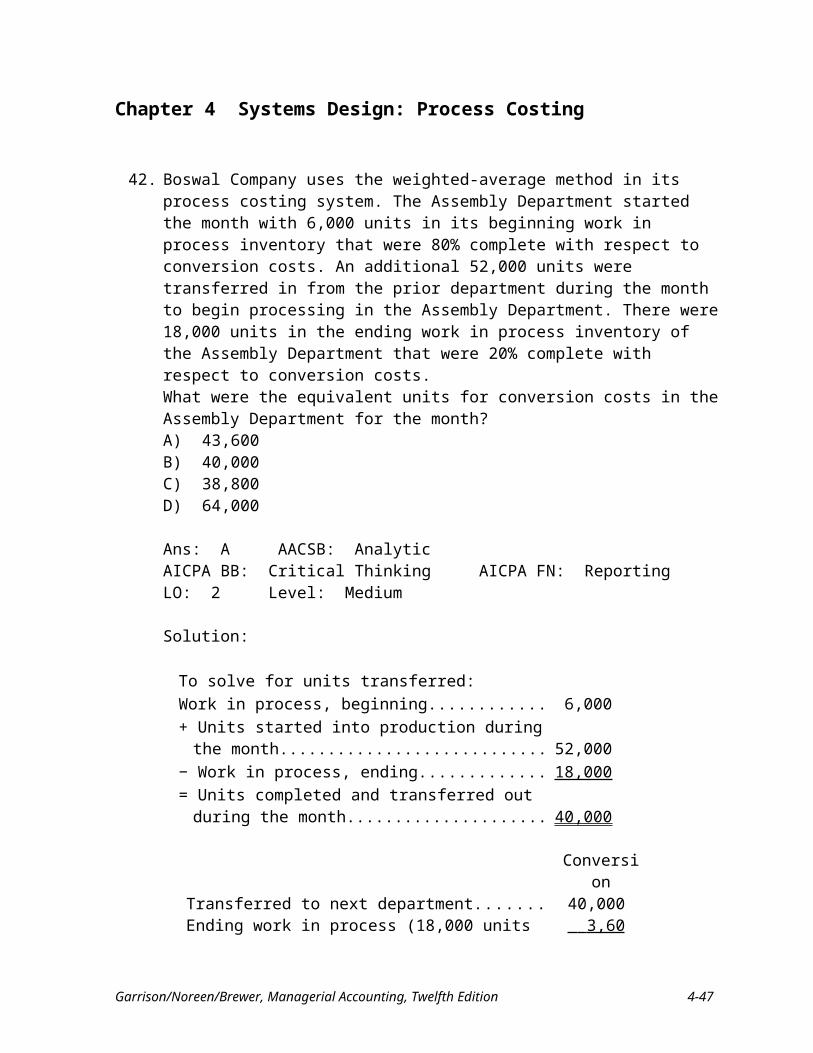

42. Boswal Company uses the weighted-average method in its process costing system. The Assembly Department started the month with 6,000 units in its beginning work in process inventory that were 80% complete with respect to conversion costs. An additional 52,000 units were transferred in from the prior department during the month to begin processing in the Assembly Department. There were 18,000 units in the ending work in process inventory of the Assembly Department that were 20% complete with respect to conversion costs.What were the equivalent units for conversion costs in the Assembly Department for the month?A) 43,600B) 40,000C) 38,800D) 64,000

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Medium

Solution:

To solve for units transferred:Work in process, beginning................................................ 6,000+ Units started into production during the month.............. 52,000− Work in process, ending.................................................. 18,000= Units completed and transferred out during the month... 40,000

ConversionTransferred to next department........................................ 40,000Ending work in process (18,000 units × 20% complete). 3,600 Equivalent units of production......................................... 43,600

4-30 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

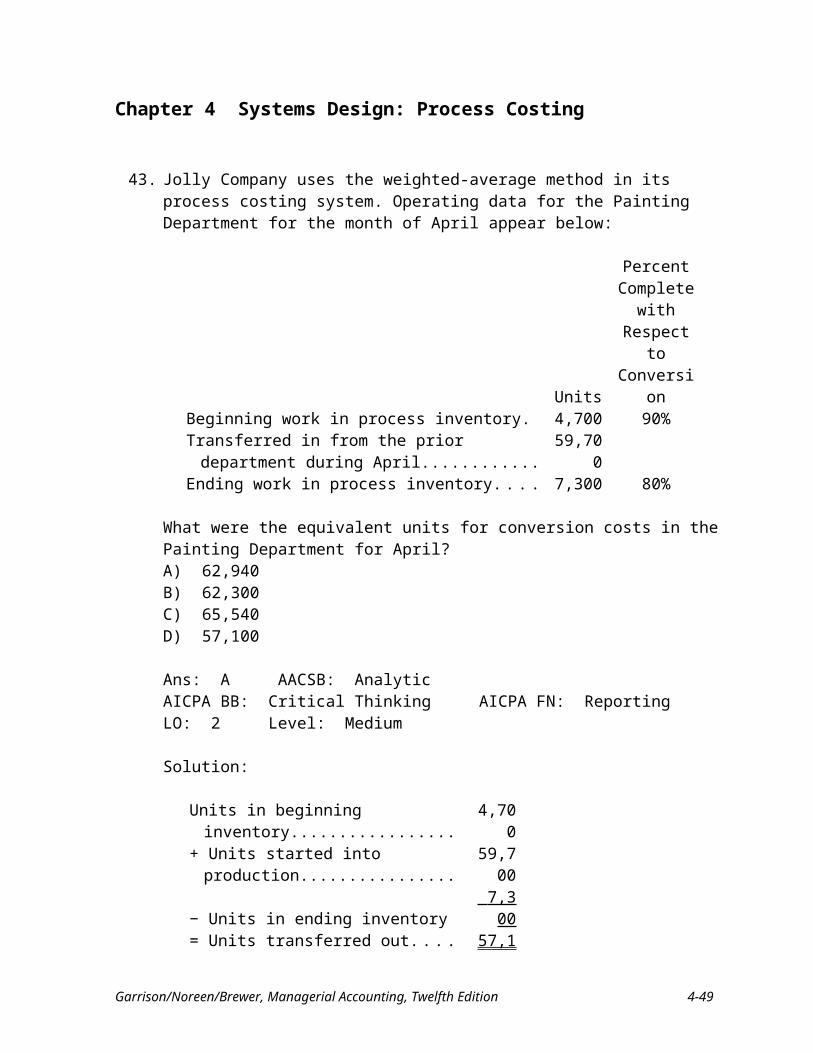

43. Jolly Company uses the weighted-average method in its process costing system. Operating data for the Painting Department for the month of April appear below:

Units

Percent Complete

with Respect to Conversion

Beginning work in process inventory............................. 4,700 90%Transferred in from the prior department during April. . 59,700Ending work in process inventory.................................. 7,300 80%

What were the equivalent units for conversion costs in the Painting Department for April?A) 62,940B) 62,300C) 65,540D) 57,100

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Medium

Solution:

Units in beginning inventory.................... 4,700+ Units started into production................. 59,700− Units in ending inventory...................... 7,300 = Units transferred out.............................. 57,100

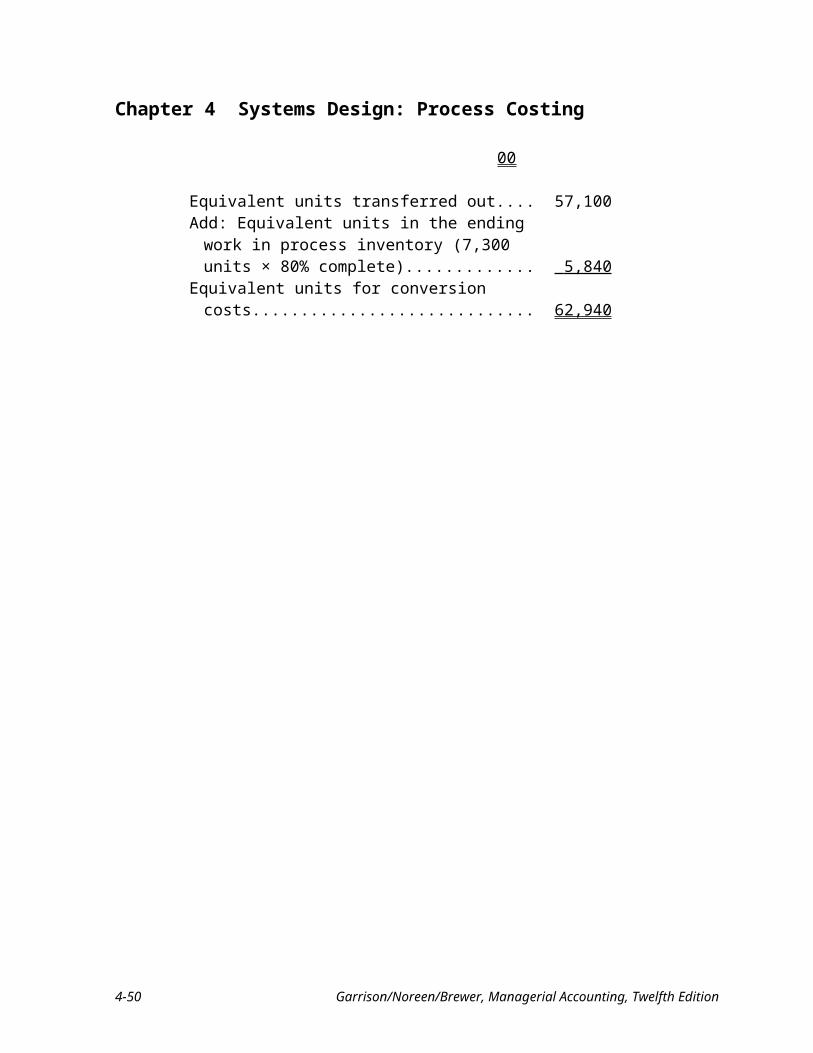

Equivalent units transferred out.................................... 57,100Add: Equivalent units in the ending work in process

inventory (7,300 units × 80% complete)................... 5,840 Equivalent units for conversion costs........................... 62,940

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-31

Chapter 4 Systems Design: Process Costing

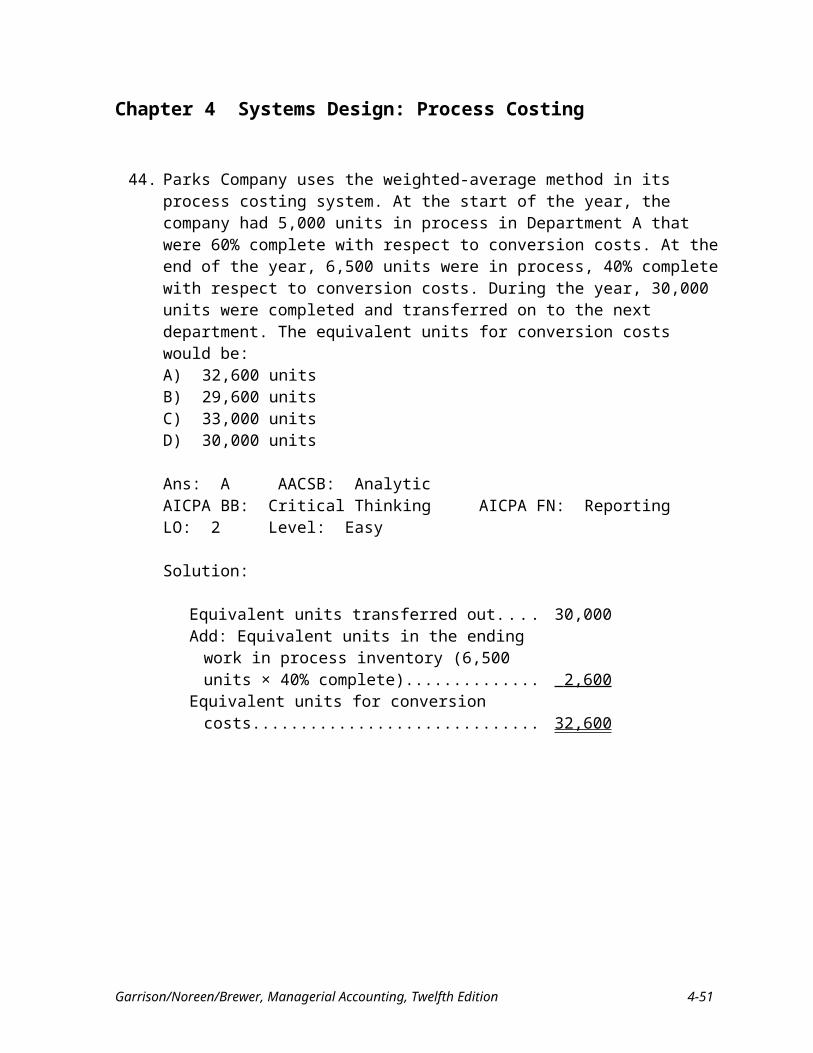

44. Parks Company uses the weighted-average method in its process costing system. At the start of the year, the company had 5,000 units in process in Department A that were 60% complete with respect to conversion costs. At the end of the year, 6,500 units were in process, 40% complete with respect to conversion costs. During the year, 30,000 units were completed and transferred on to the next department. The equivalent units for conversion costs would be:A) 32,600 unitsB) 29,600 unitsC) 33,000 unitsD) 30,000 units

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Easy

Solution:

Equivalent units transferred out..................................... 30,000Add: Equivalent units in the ending work in process

inventory (6,500 units × 40% complete).................... 2,600 Equivalent units for conversion costs............................ 32,600

4-32 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

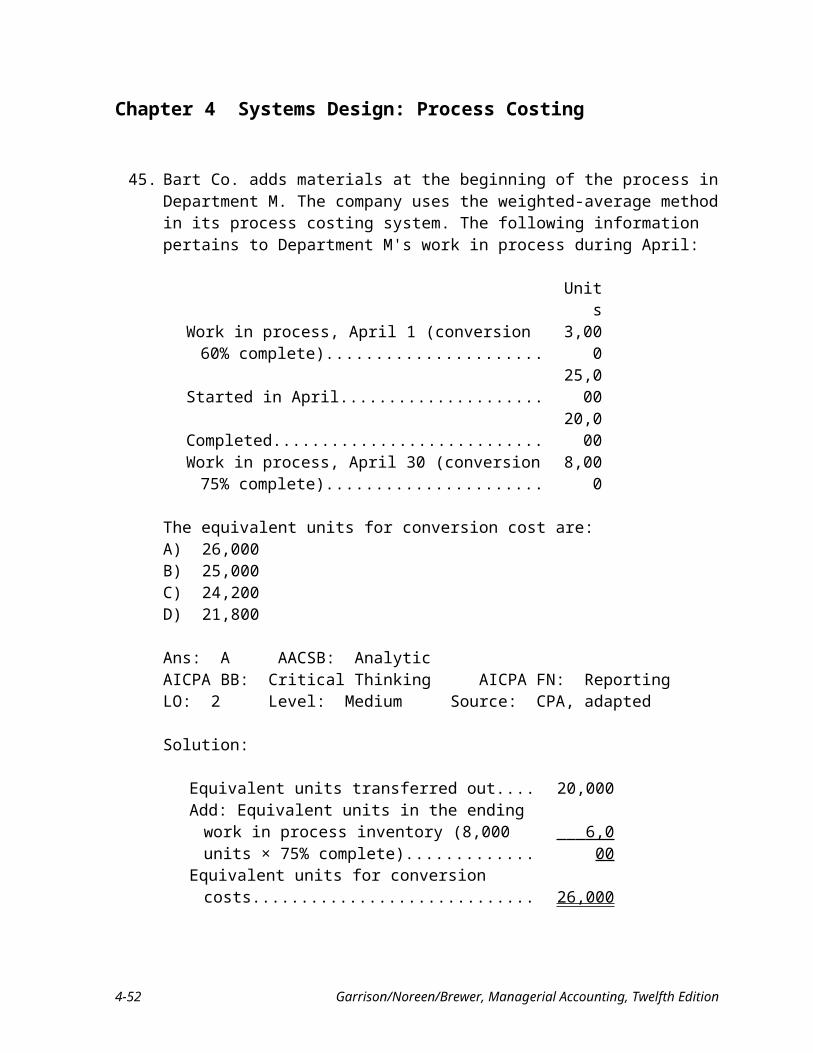

45. Bart Co. adds materials at the beginning of the process in Department M. The company uses the weighted-average method in its process costing system. The following information pertains to Department M's work in process during April:

UnitsWork in process, April 1 (conversion 60% complete).... 3,000Started in April................................................................ 25,000Completed........................................................................ 20,000Work in process, April 30 (conversion 75% complete). . 8,000

The equivalent units for conversion cost are:A) 26,000B) 25,000C) 24,200D) 21,800

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Medium Source: CPA, adapted

Solution:

Equivalent units transferred out.................................... 20,000Add: Equivalent units in the ending work in process

inventory (8,000 units × 75% complete)................... 6,000 Equivalent units for conversion costs........................... 26,000

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-33

Chapter 4 Systems Design: Process Costing

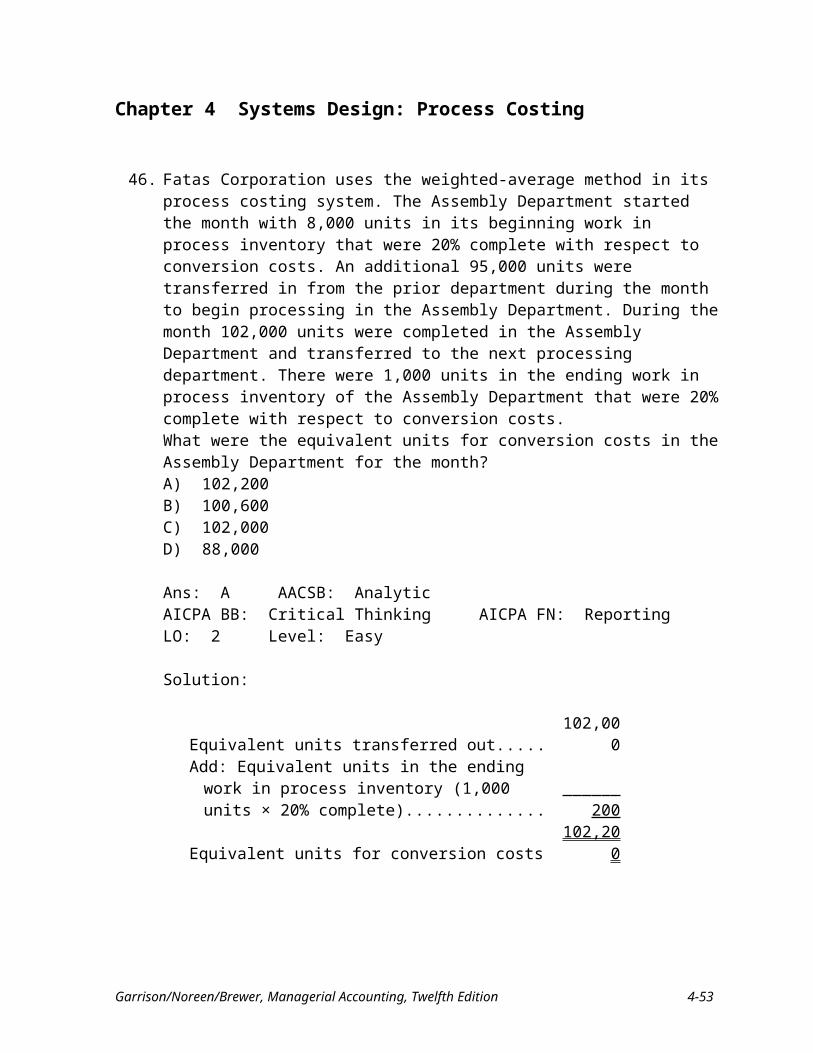

46. Fatas Corporation uses the weighted-average method in its process costing system. The Assembly Department started the month with 8,000 units in its beginning work in process inventory that were 20% complete with respect to conversion costs. An additional 95,000 units were transferred in from the prior department during the month to begin processing in the Assembly Department. During the month 102,000 units were completed in the Assembly Department and transferred to the next processing department. There were 1,000 units in the ending work in process inventory of the Assembly Department that were 20% complete with respect to conversion costs.What were the equivalent units for conversion costs in the Assembly Department for the month?A) 102,200B) 100,600C) 102,000D) 88,000

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Easy

Solution:

Equivalent units transferred out...................................... 102,000Add: Equivalent units in the ending work in process

inventory (1,000 units × 20% complete)..................... 200 Equivalent units for conversion costs.............................. 102,200

4-34 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

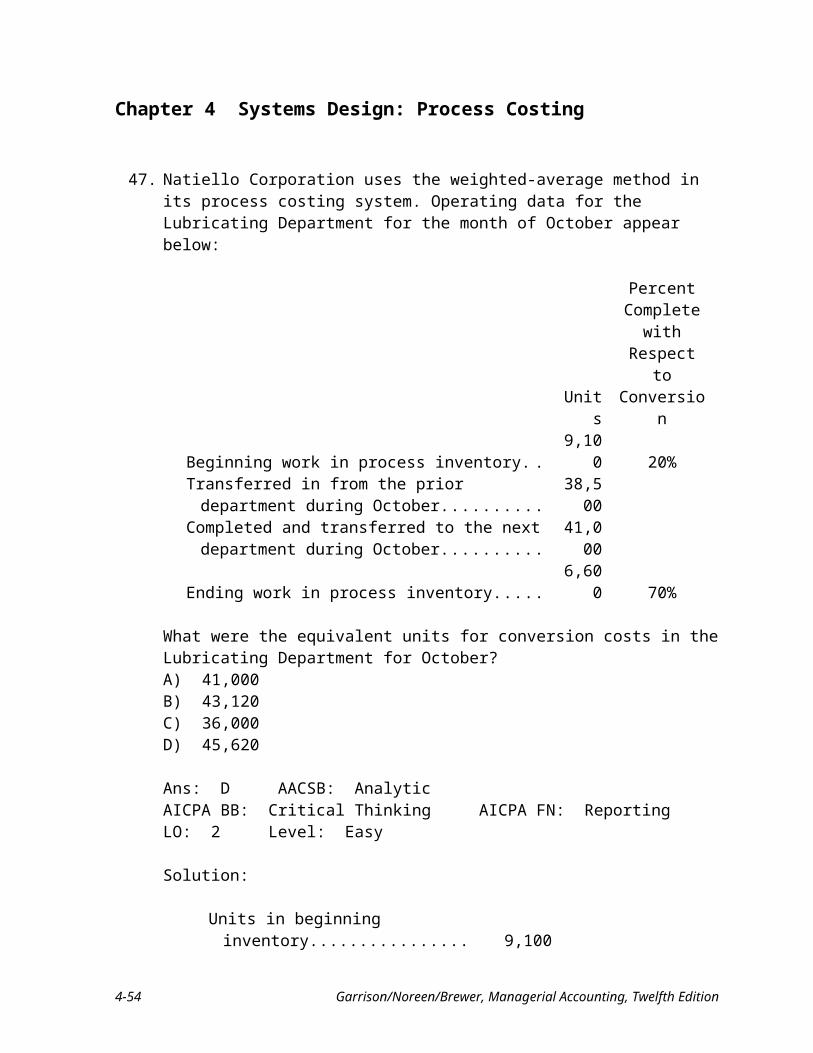

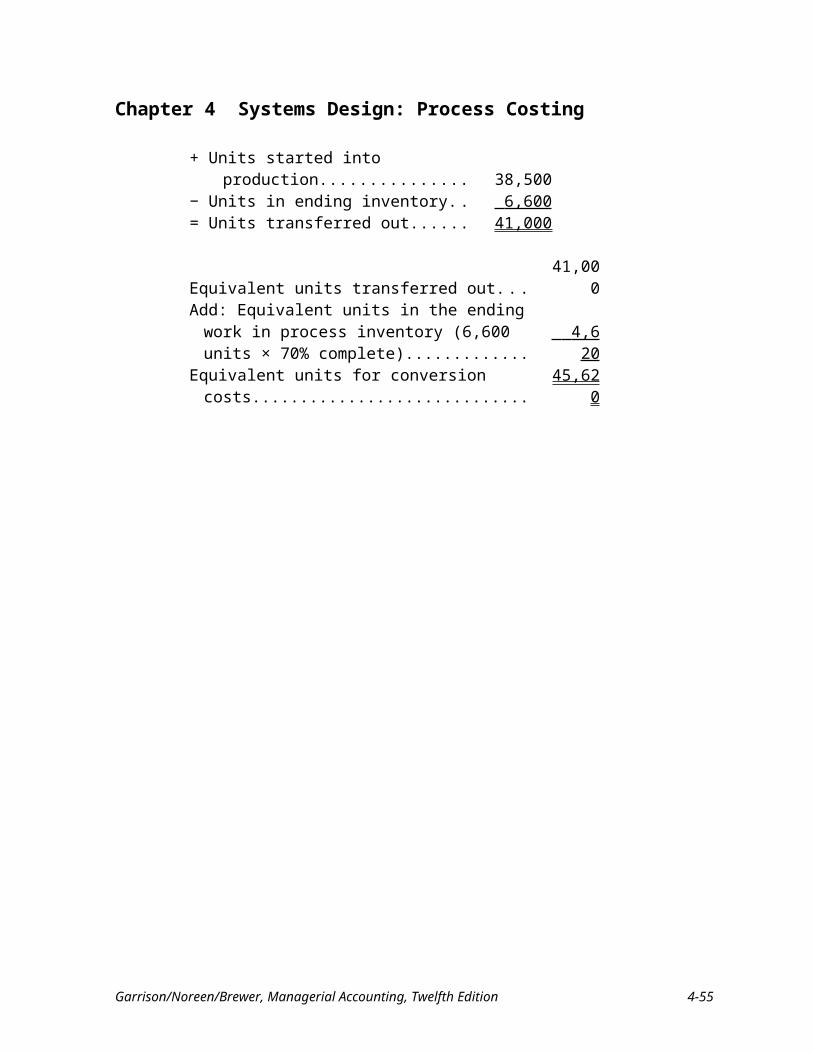

47. Natiello Corporation uses the weighted-average method in its process costing system. Operating data for the Lubricating Department for the month of October appear below:

Units

Percent Complete

with Respect to Conversion

Beginning work in process inventory.............................. 9,100 20%Transferred in from the prior department during

October......................................................................... 38,500Completed and transferred to the next department

during October............................................................. 41,000Ending work in process inventory................................... 6,600 70%

What were the equivalent units for conversion costs in the Lubricating Department for October?A) 41,000B) 43,120C) 36,000D) 45,620

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Easy

Solution:

Units in beginning inventory................... 9,100+ Units started into production................... 38,500− Units in ending inventory........................ 6,600 = Units transferred out................................ 41,000

Equivalent units transferred out.................................. 41,000Add: Equivalent units in the ending work in process

inventory (6,600 units × 70% complete)................. 4,620 Equivalent units for conversion costs......................... 45,620

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-35

Chapter 4 Systems Design: Process Costing

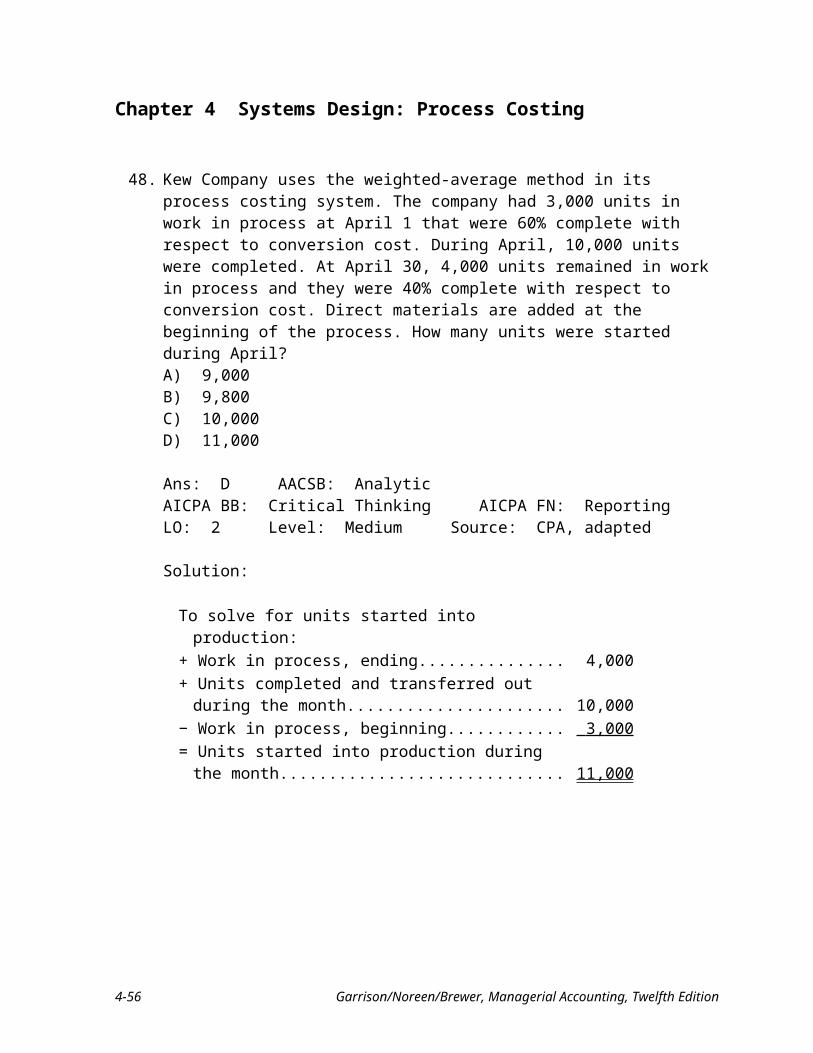

48. Kew Company uses the weighted-average method in its process costing system. The company had 3,000 units in work in process at April 1 that were 60% complete with respect to conversion cost. During April, 10,000 units were completed. At April 30, 4,000 units remained in work in process and they were 40% complete with respect to conversion cost. Direct materials are added at the beginning of the process. How many units were started during April?A) 9,000B) 9,800C) 10,000D) 11,000

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 2 Level: Medium Source: CPA, adapted

Solution:

To solve for units started into production:+ Work in process, ending...................................................... 4,000+ Units completed and transferred out during the month....... 10,000− Work in process, beginning................................................. 3,000 = Units started into production during the month................... 11,000

4-36 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

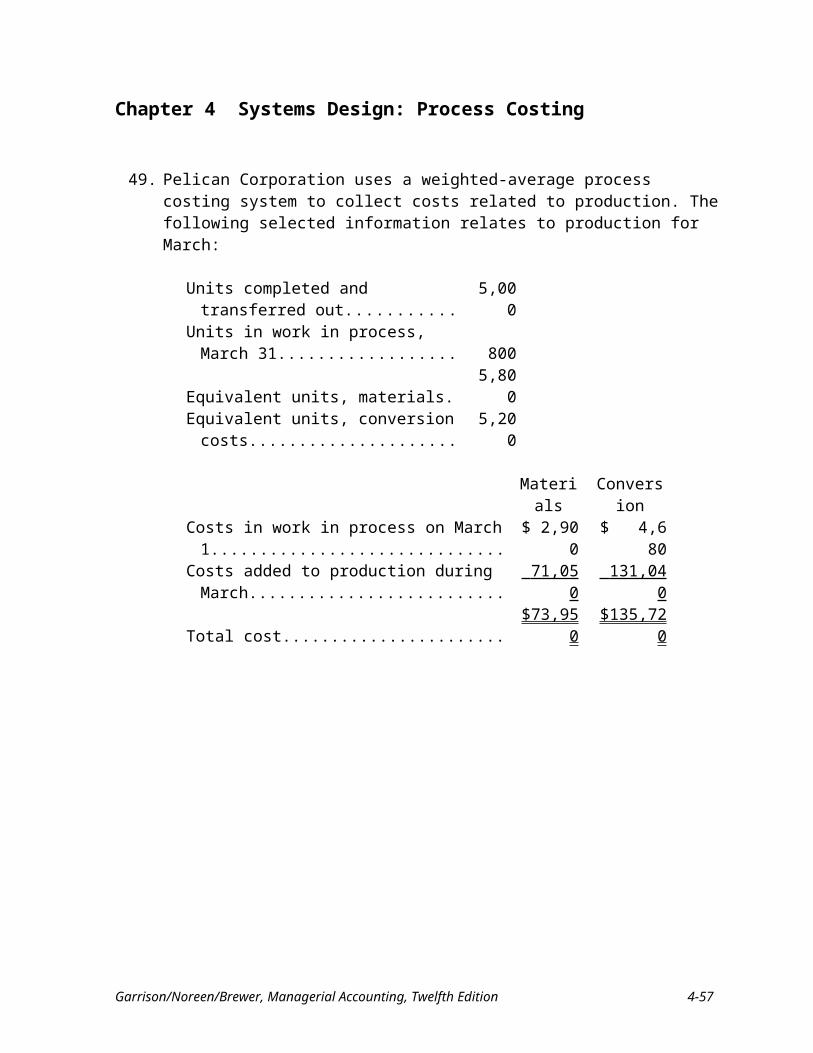

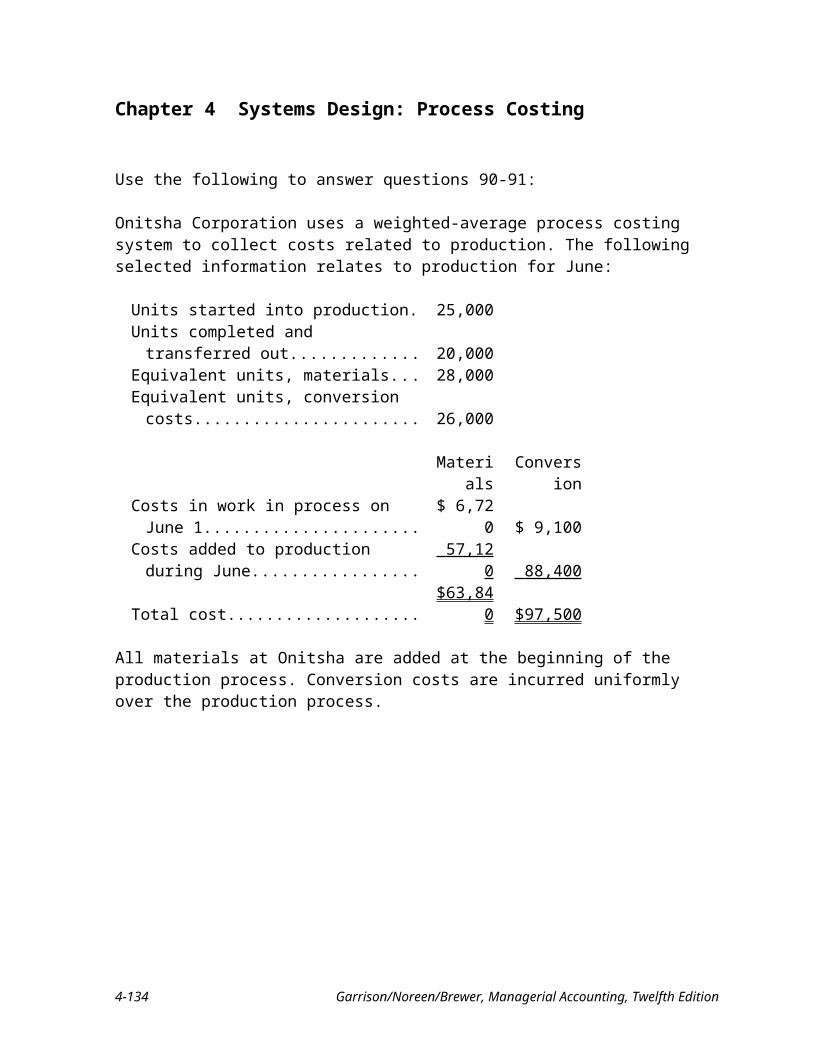

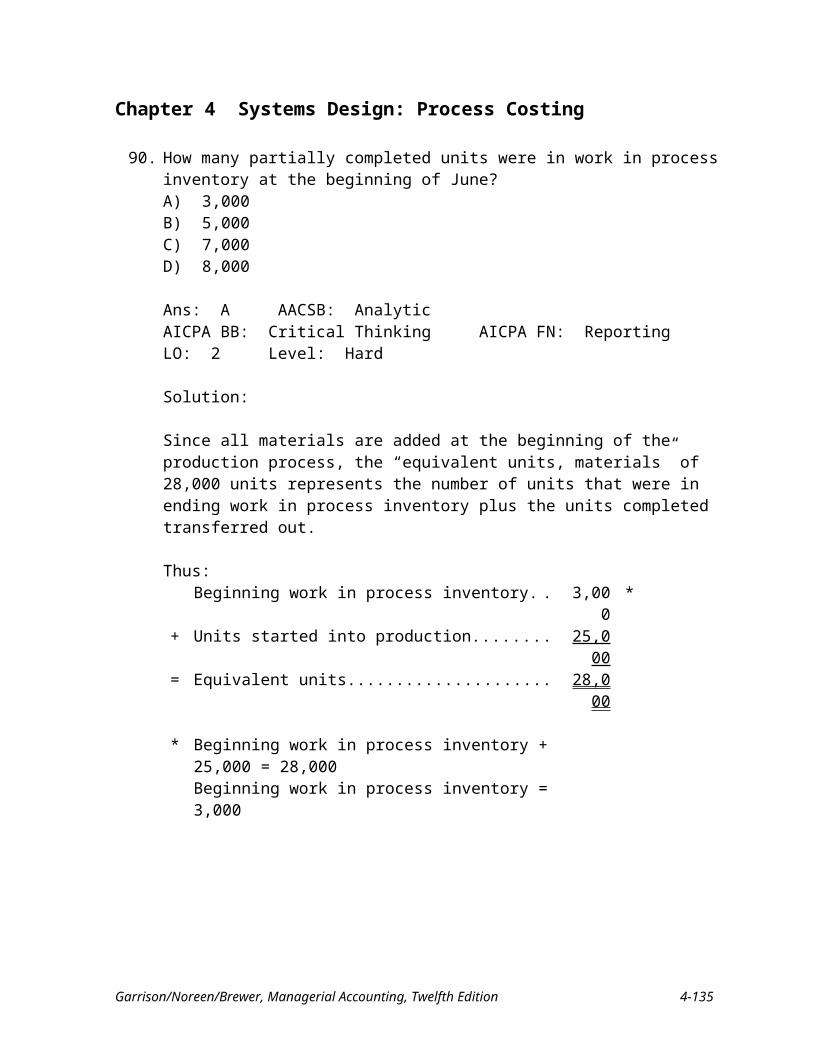

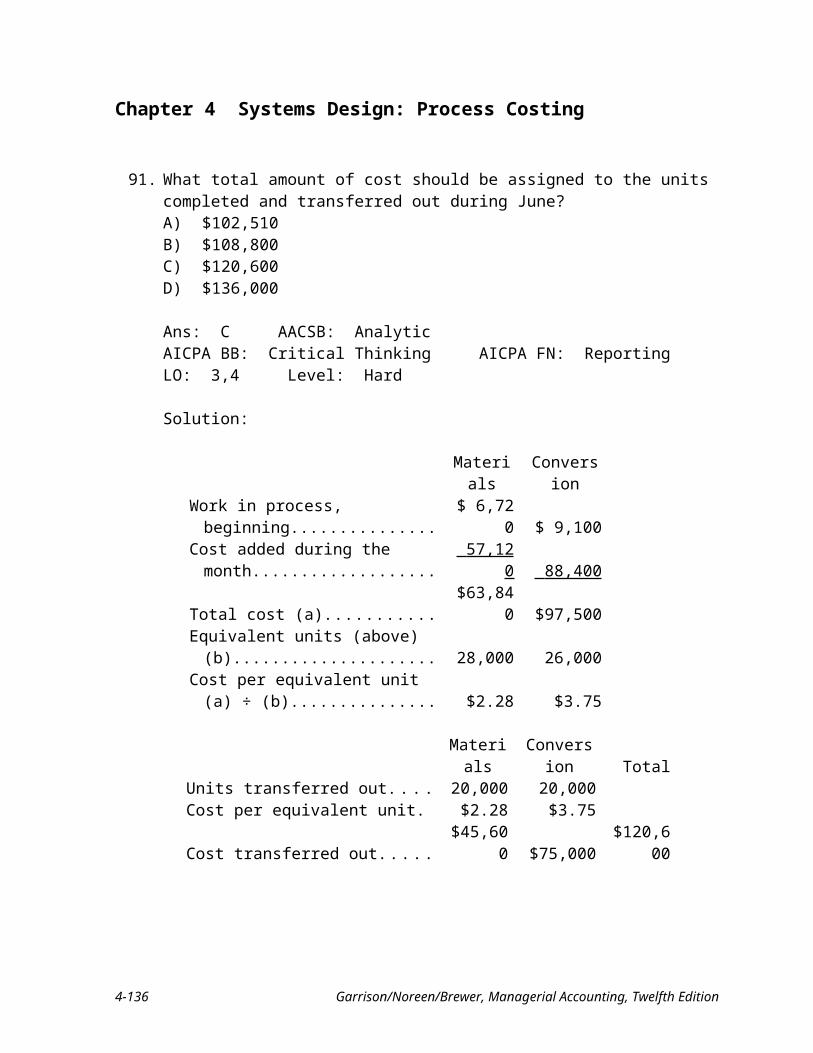

49. Pelican Corporation uses a weighted-average process costing system to collect costs related to production. The following selected information relates to production for March:

Units completed and transferred out.......... 5,000Units in work in process, March 31........... 800Equivalent units, materials......................... 5,800Equivalent units, conversion costs............. 5,200

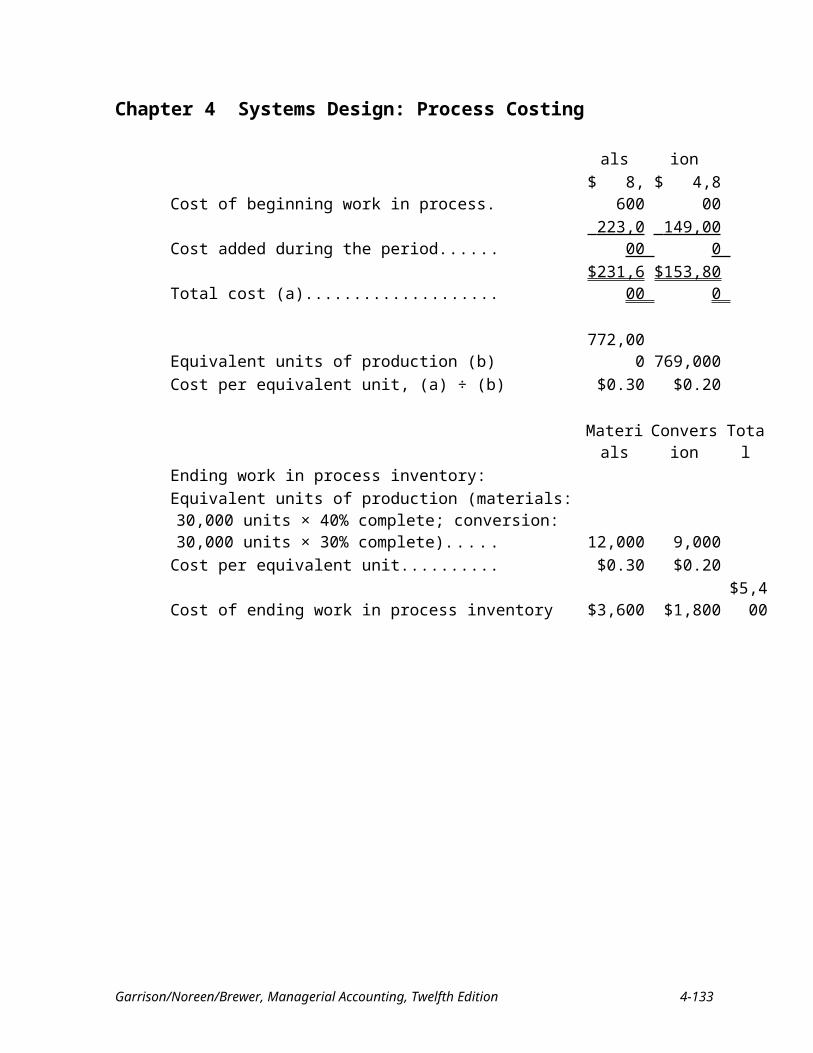

Materials ConversionCosts in work in process on March 1..................... $ 2,900 $ 4,680Costs added to production during March............... 71,050 131,040 Total cost................................................................ $73,950 $135,720

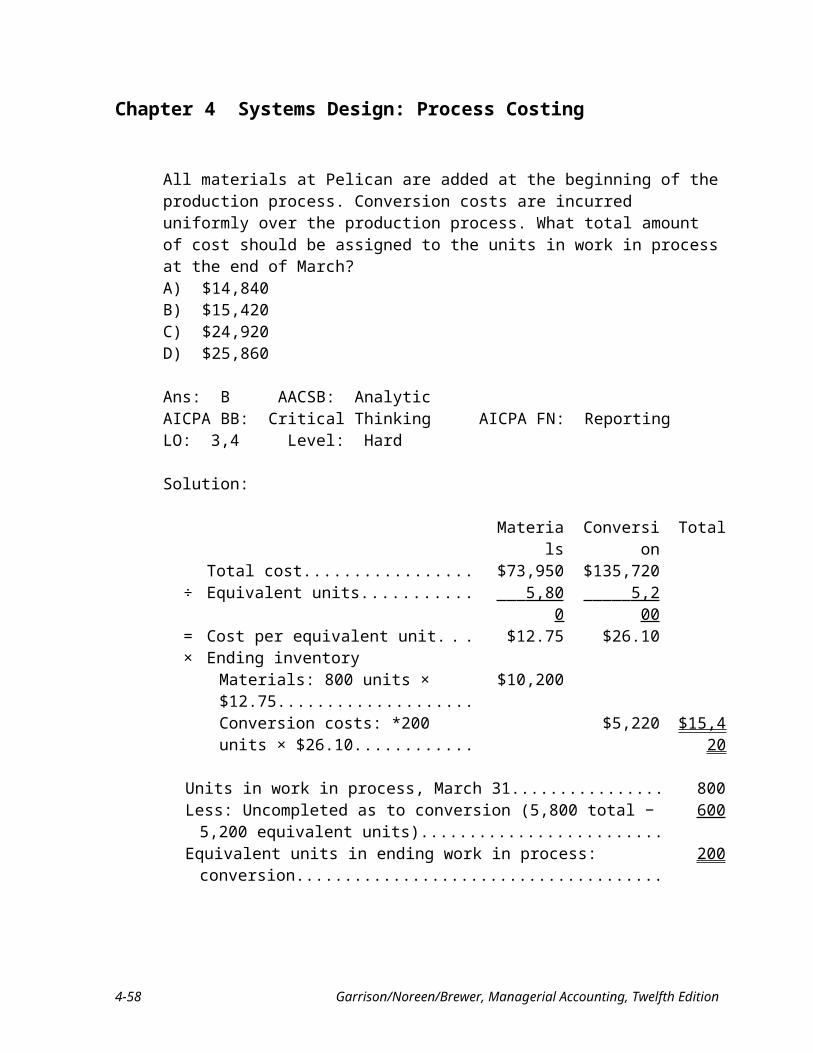

All materials at Pelican are added at the beginning of the production process. Conversion costs are incurred uniformly over the production process. What total amount of cost should be assigned to the units in work in process at the end of March?A) $14,840B) $15,420C) $24,920D) $25,860

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 3,4 Level: Hard

Solution:

Materials Conversion TotalTotal cost................................................... $73,950 $135,720

÷ Equivalent units........................................ 5,800 5,200 = Cost per equivalent unit............................ $12.75 $26.10× Ending inventory

Materials: 800 units × $12.75................ $10,200Conversion costs: *200 units × $26.10.. $5,220 $15,420

Units in work in process, March 31............................................................... 800Less: Uncompleted as to conversion (5,800 total − 5,200 equivalent units). 600Equivalent units in ending work in process: conversion............................... 200

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-37

Chapter 4 Systems Design: Process Costing

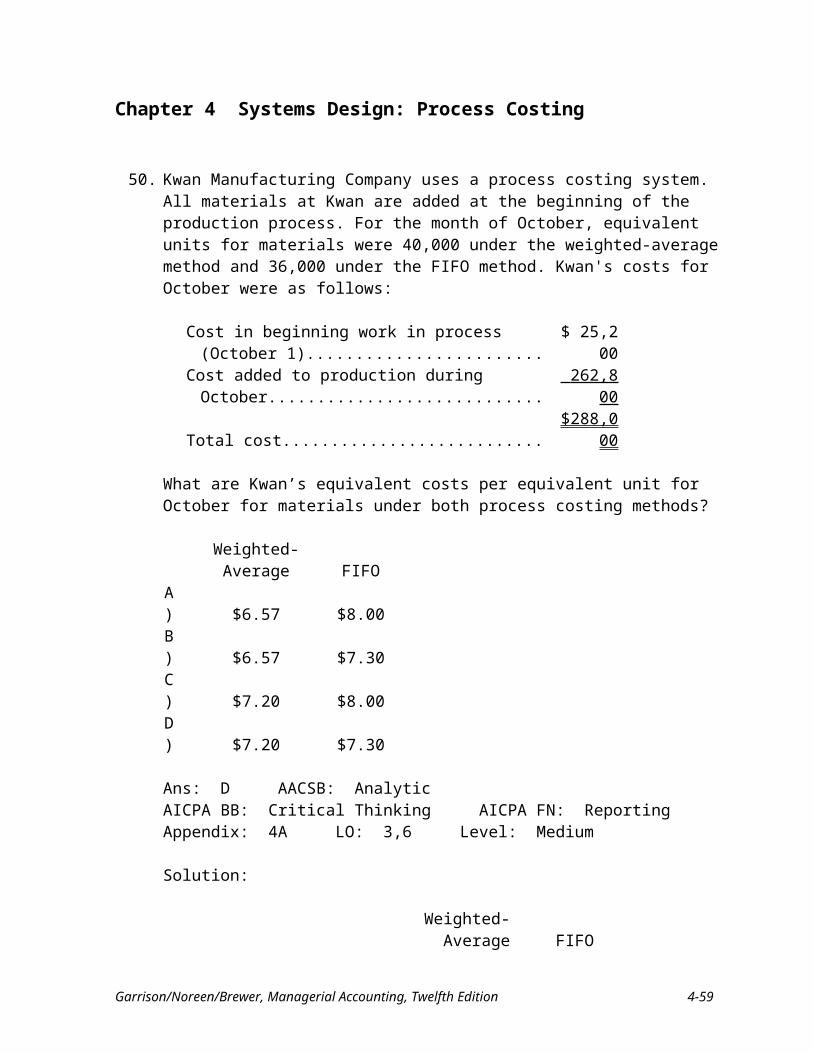

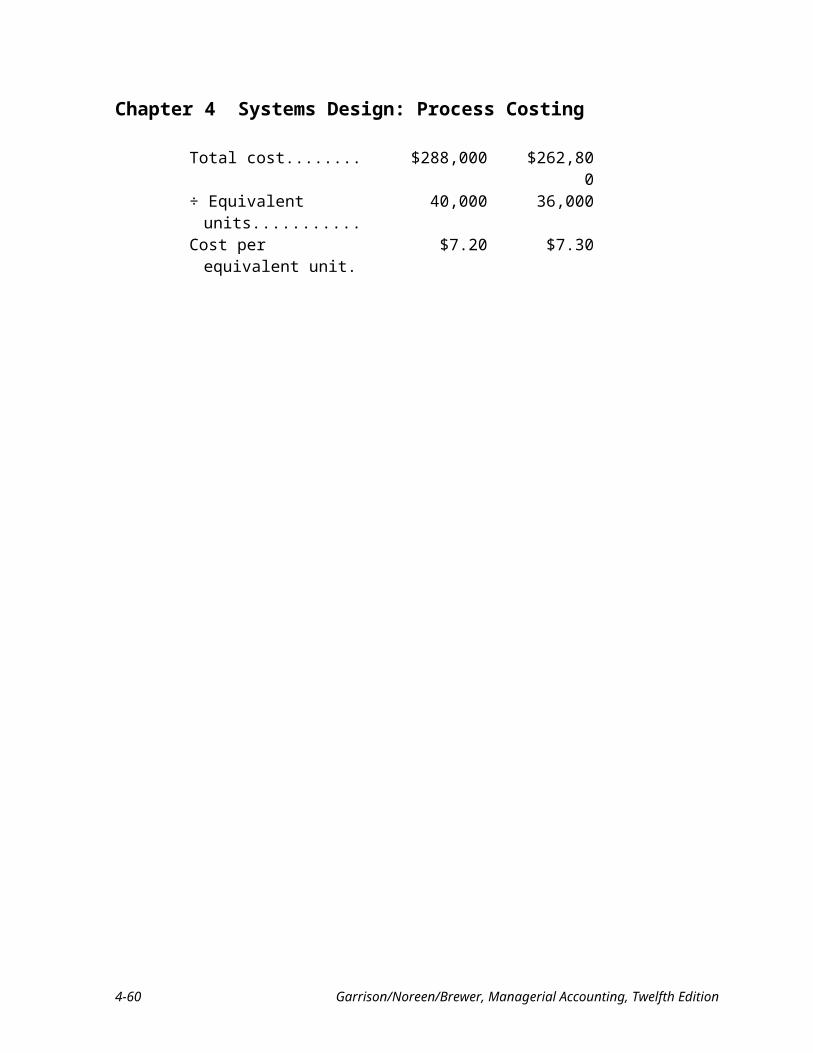

50. Kwan Manufacturing Company uses a process costing system. All materials at Kwan are added at the beginning of the production process. For the month of October, equivalent units for materials were 40,000 under the weighted-average method and 36,000 under the FIFO method. Kwan's costs for October were as follows:

Cost in beginning work in process (October 1)............... $ 25,200Cost added to production during October........................ 262,800 Total cost......................................................................... $288,000

What are Kwan’s equivalent costs per equivalent unit for October for materials under both process costing methods?

Weighted-Average FIFOA) $6.57 $8.00B) $6.57 $7.30C) $7.20 $8.00D) $7.20 $7.30

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 3,6 Level: Medium

Solution:

Weighted-Average FIFOTotal cost........................... $288,000 $262,800÷ Equivalent units............. 40,000 36,000Cost per equivalent unit.... $7.20 $7.30

4-38 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

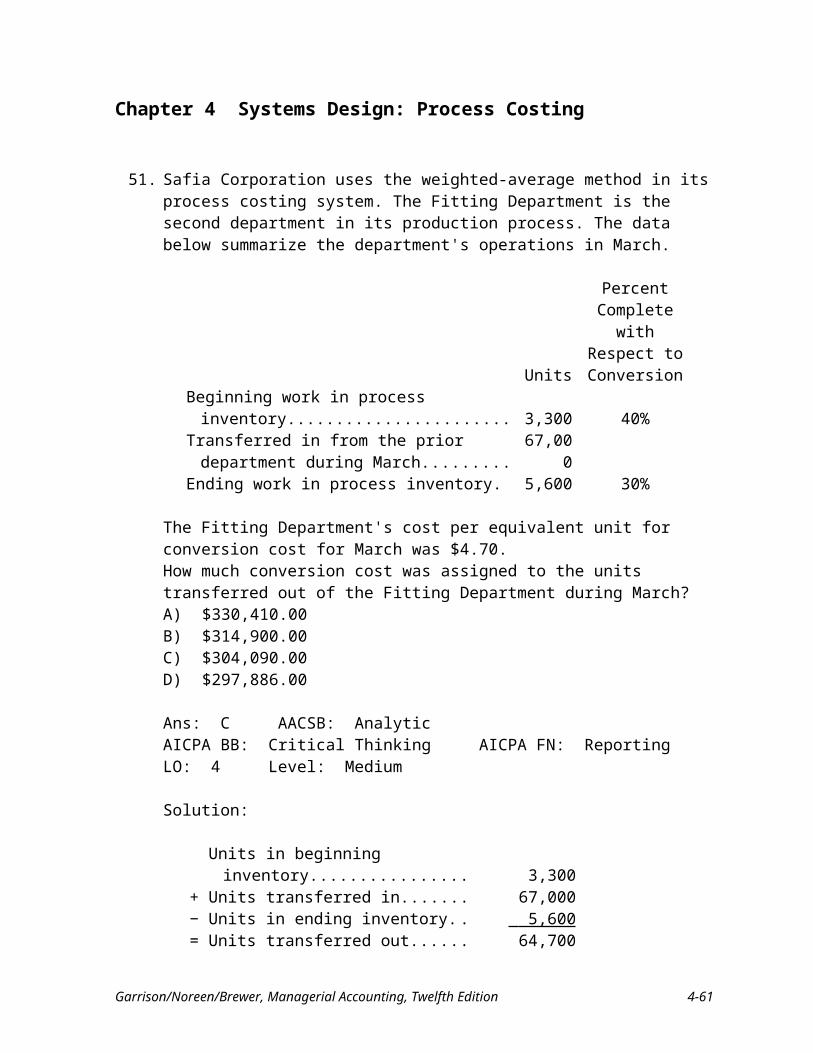

51. Safia Corporation uses the weighted-average method in its process costing system. The Fitting Department is the second department in its production process. The data below summarize the department's operations in March.

Units

Percent Complete with

Respect to Conversion

Beginning work in process inventory...................... 3,300 40%Transferred in from the prior department during

March................................................................... 67,000Ending work in process inventory........................... 5,600 30%

The Fitting Department's cost per equivalent unit for conversion cost for March was $4.70.How much conversion cost was assigned to the units transferred out of the Fitting Department during March?A) $330,410.00B) $314,900.00C) $304,090.00D) $297,886.00

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Medium

Solution:

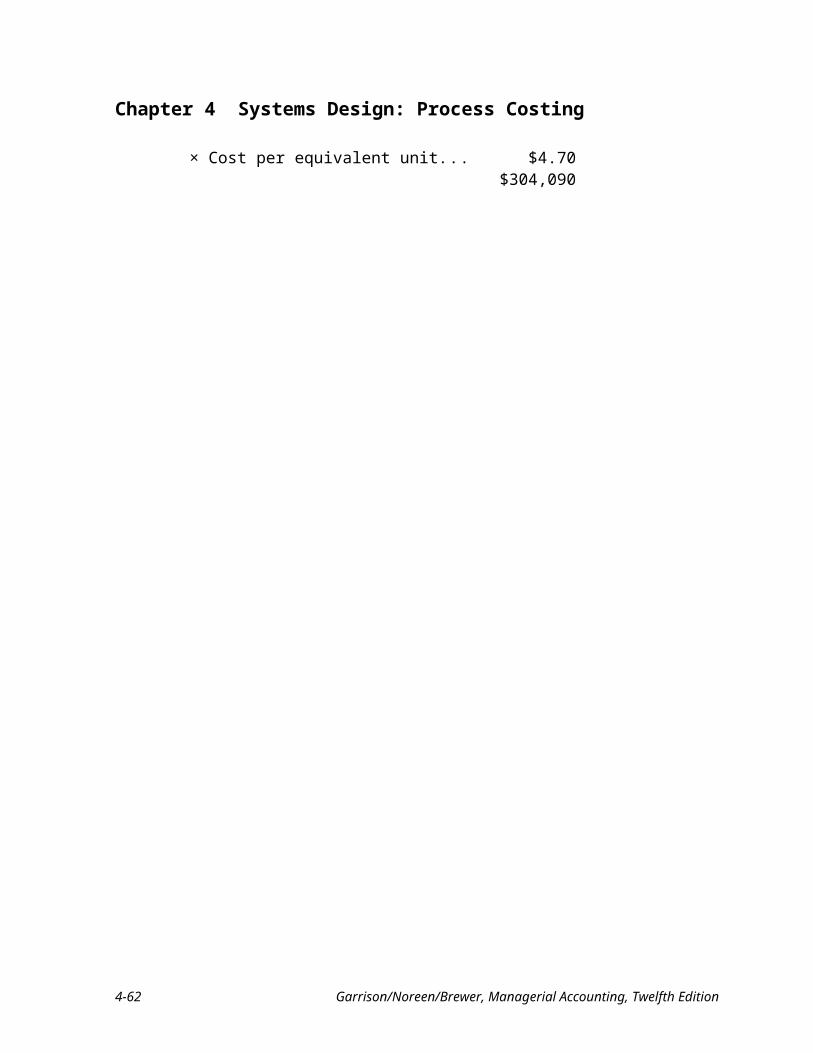

Units in beginning inventory................... 3,300+ Units transferred in.................................. 67,000− Units in ending inventory........................ 5,600 = Units transferred out................................ 64,700× Cost per equivalent unit........................... $4.70

$304,090

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-39

Chapter 4 Systems Design: Process Costing

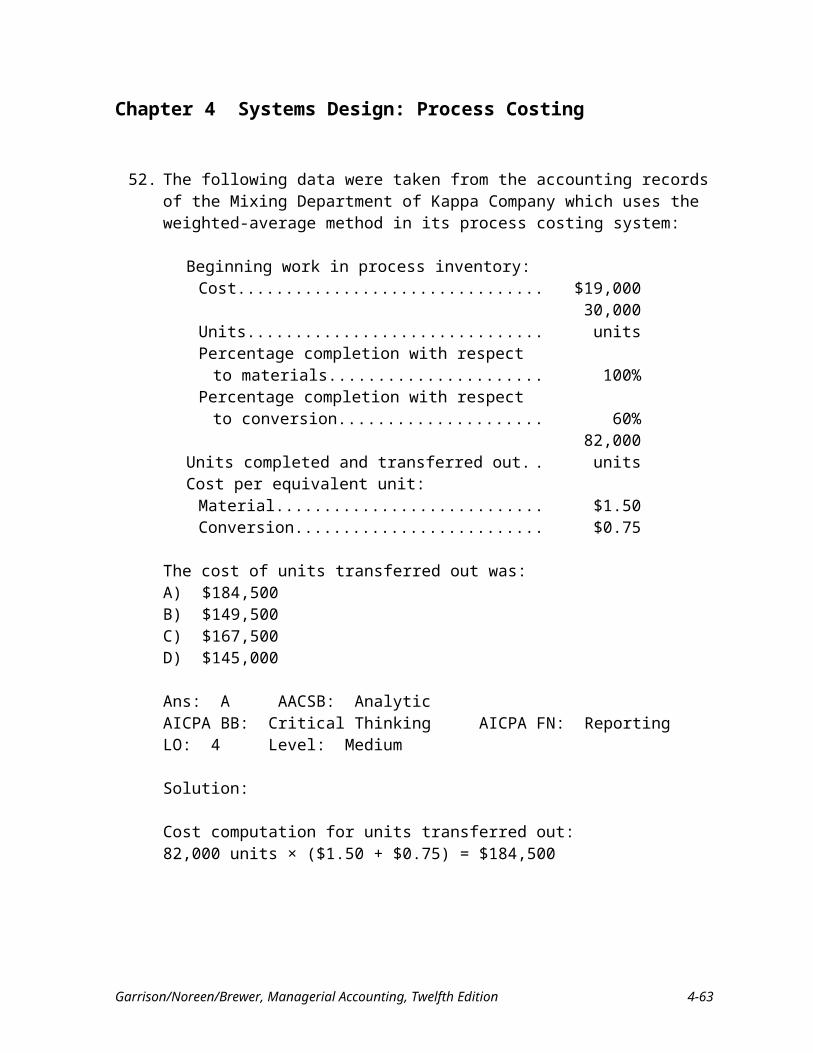

52. The following data were taken from the accounting records of the Mixing Department of Kappa Company which uses the weighted-average method in its process costing system:

Beginning work in process inventory:Cost............................................................................... $19,000Units............................................................................. 30,000 unitsPercentage completion with respect to materials......... 100%Percentage completion with respect to conversion...... 60%

Units completed and transferred out................................ 82,000 unitsCost per equivalent unit:

Material......................................................................... $1.50Conversion.................................................................... $0.75

The cost of units transferred out was:A) $184,500B) $149,500C) $167,500D) $145,000

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Medium

Solution:

Cost computation for units transferred out:82,000 units × ($1.50 + $0.75) = $184,500

4-40 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

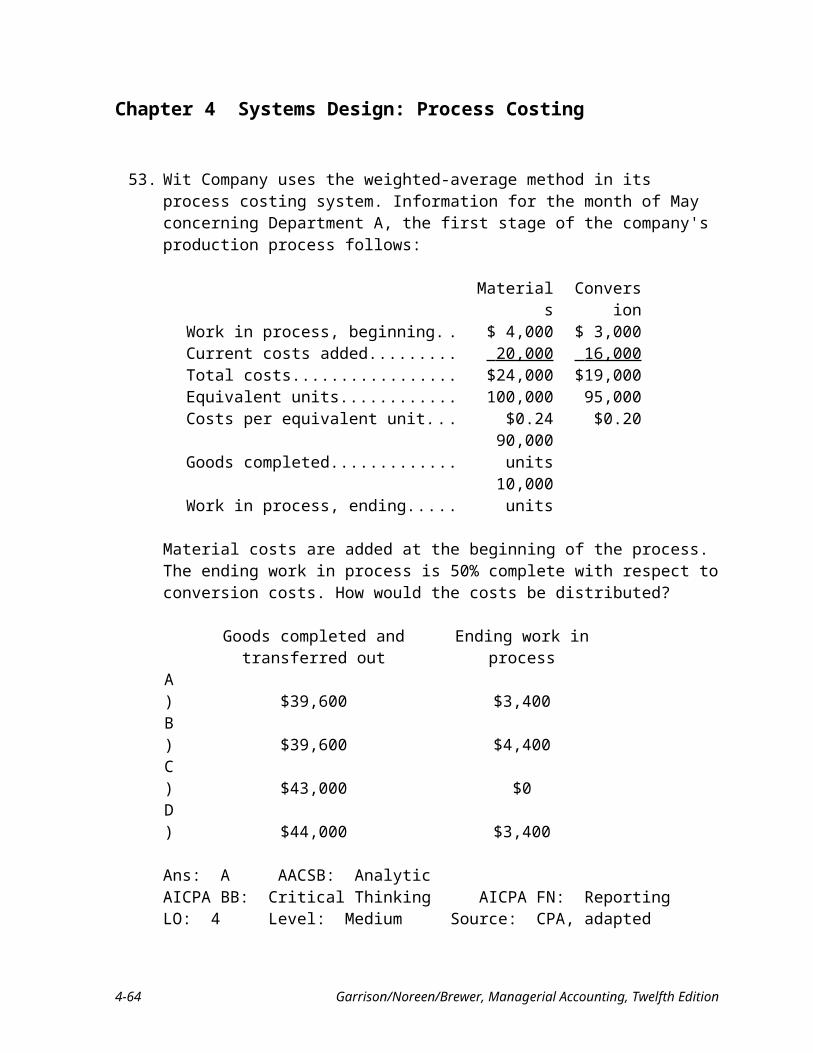

53. Wit Company uses the weighted-average method in its process costing system. Information for the month of May concerning Department A, the first stage of the company's production process follows:

Materials ConversionWork in process, beginning....................... $ 4,000 $ 3,000Current costs added.................................... 20,000 16,000 Total costs.................................................. $24,000 $19,000Equivalent units......................................... 100,000 95,000Costs per equivalent unit............................ $0.24 $0.20Goods completed....................................... 90,000 unitsWork in process, ending............................ 10,000 units

Material costs are added at the beginning of the process. The ending work in process is 50% complete with respect to conversion costs. How would the costs be distributed?

Goods completed and transferred out Ending work in processA) $39,600 $3,400B) $39,600 $4,400C) $43,000 $0D) $44,000 $3,400

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Medium Source: CPA, adapted

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-41

Chapter 4 Systems Design: Process Costing

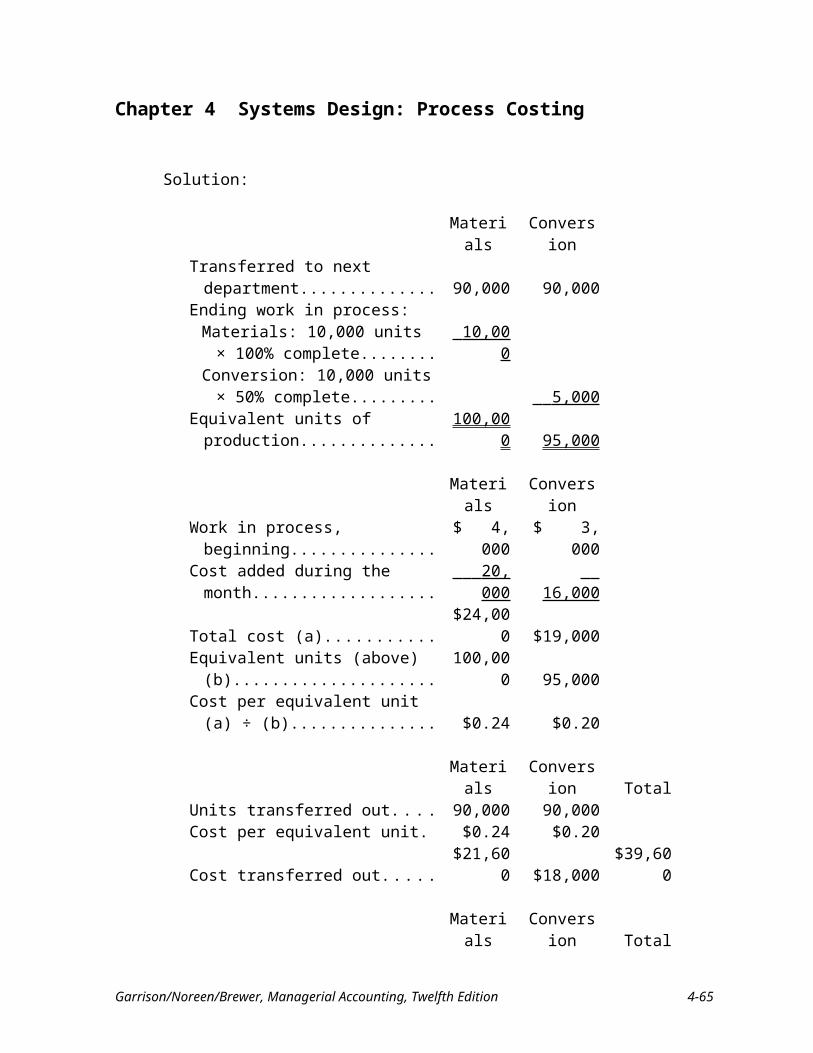

Solution:

Materials ConversionTransferred to next department............ 90,000 90,000Ending work in process:

Materials: 10,000 units × 100% complete........................................ 10,000

Conversion: 10,000 units × 50% complete........................................ 5,000

Equivalent units of production............. 100,000 95,000

Materials ConversionWork in process, beginning................. $ 4,000 $ 3,000Cost added during the month............... 20,000 16,000 Total cost (a)........................................ $24,000 $19,000Equivalent units (above) (b)................. 100,000 95,000Cost per equivalent unit (a) ÷ (b)......... $0.24 $0.20

Materials Conversion TotalUnits transferred out............................ 90,000 90,000Cost per equivalent unit....................... $0.24 $0.20Cost transferred out.............................. $21,600 $18,000 $39,600

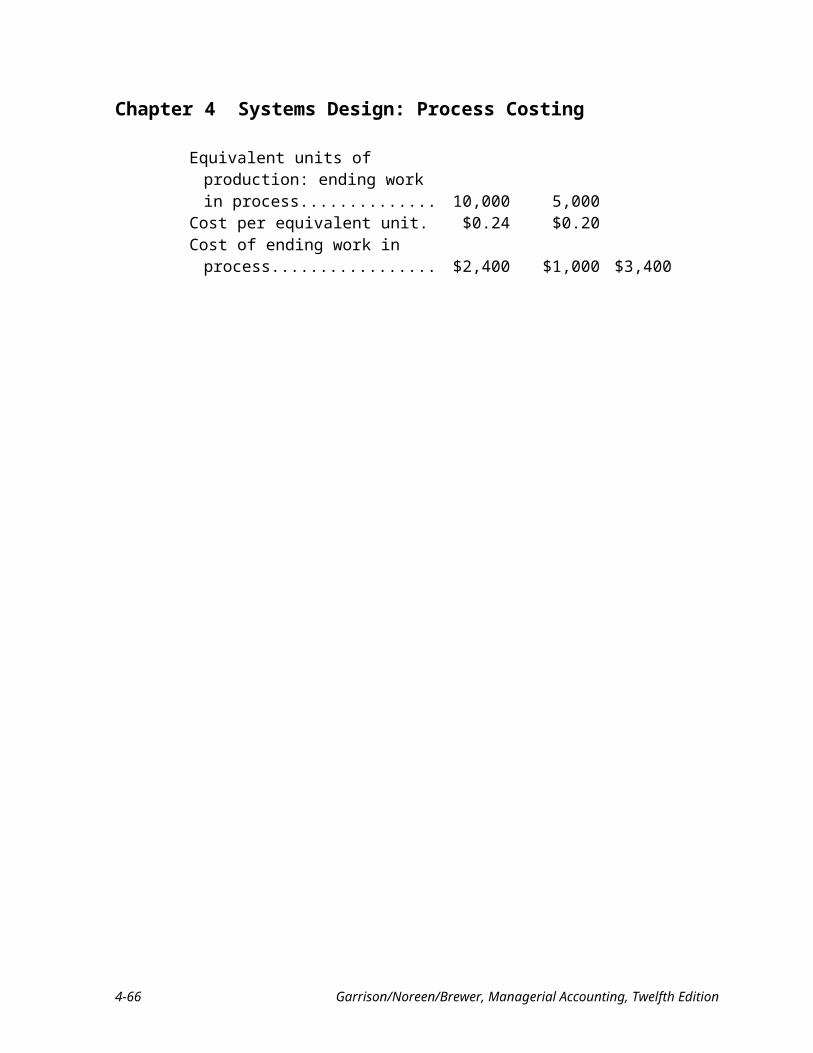

Materials Conversion TotalEquivalent units of production:

ending work in process..................... 10,000 5,000Cost per equivalent unit....................... $0.24 $0.20Cost of ending work in process............ $2,400 $1,000 $3,400

4-42 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

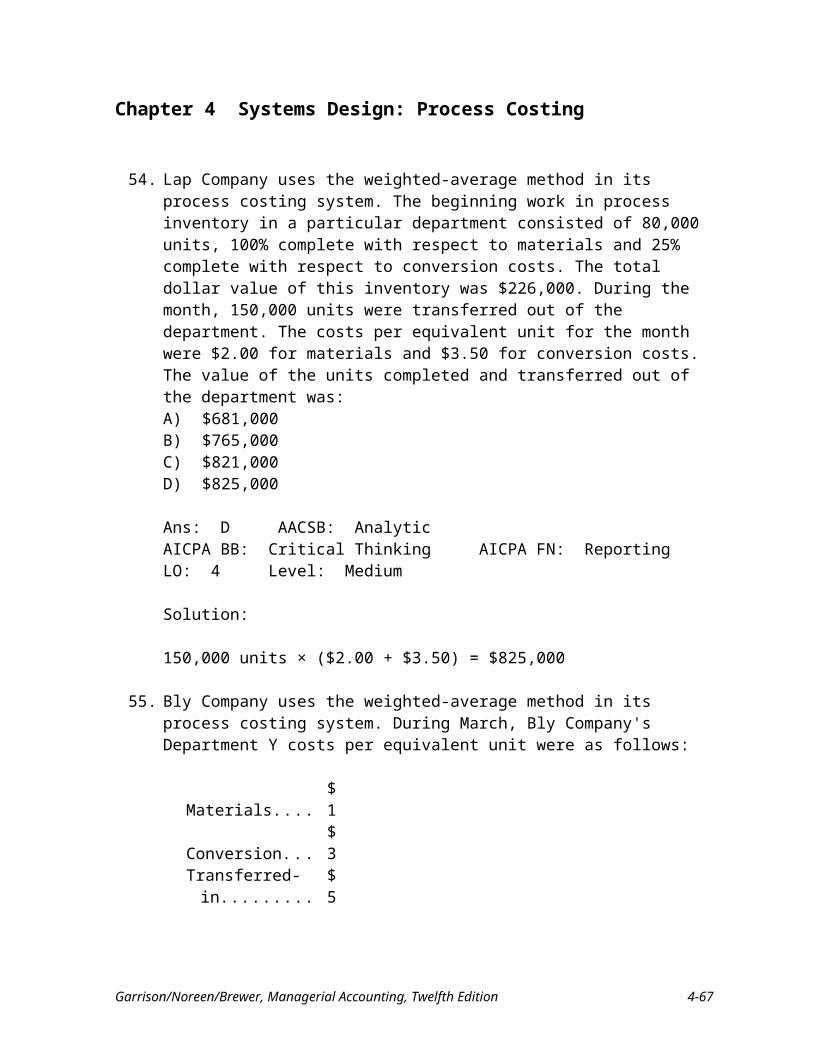

54. Lap Company uses the weighted-average method in its process costing system. The beginning work in process inventory in a particular department consisted of 80,000 units, 100% complete with respect to materials and 25% complete with respect to conversion costs. The total dollar value of this inventory was $226,000. During the month, 150,000 units were transferred out of the department. The costs per equivalent unit for the month were $2.00 for materials and $3.50 for conversion costs. The value of the units completed and transferred out of the department was:A) $681,000B) $765,000C) $821,000D) $825,000

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Medium

Solution:

150,000 units × ($2.00 + $3.50) = $825,000

55. Bly Company uses the weighted-average method in its process costing system. During March, Bly Company's Department Y costs per equivalent unit were as follows:

Materials................ $1Conversion............. $3Transferred-in........ $5

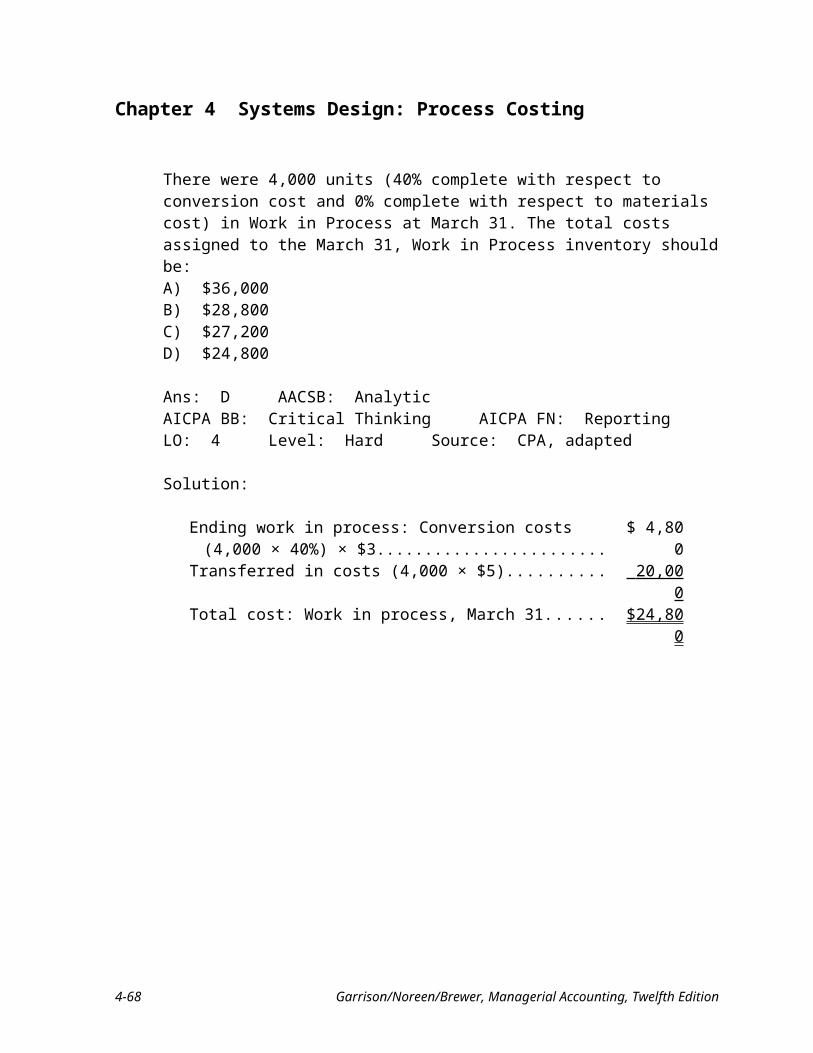

There were 4,000 units (40% complete with respect to conversion cost and 0% complete with respect to materials cost) in Work in Process at March 31. The total costs assigned to the March 31, Work in Process inventory should be:A) $36,000B) $28,800C) $27,200D) $24,800

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Hard Source: CPA, adapted

Solution:

Ending work in process: Conversion costs (4,000 × 40%) × $3.... $ 4,800Transferred in costs (4,000 × $5).................................................... 20,000 Total cost: Work in process, March 31........................................... $24,800

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-43

Chapter 4 Systems Design: Process Costing

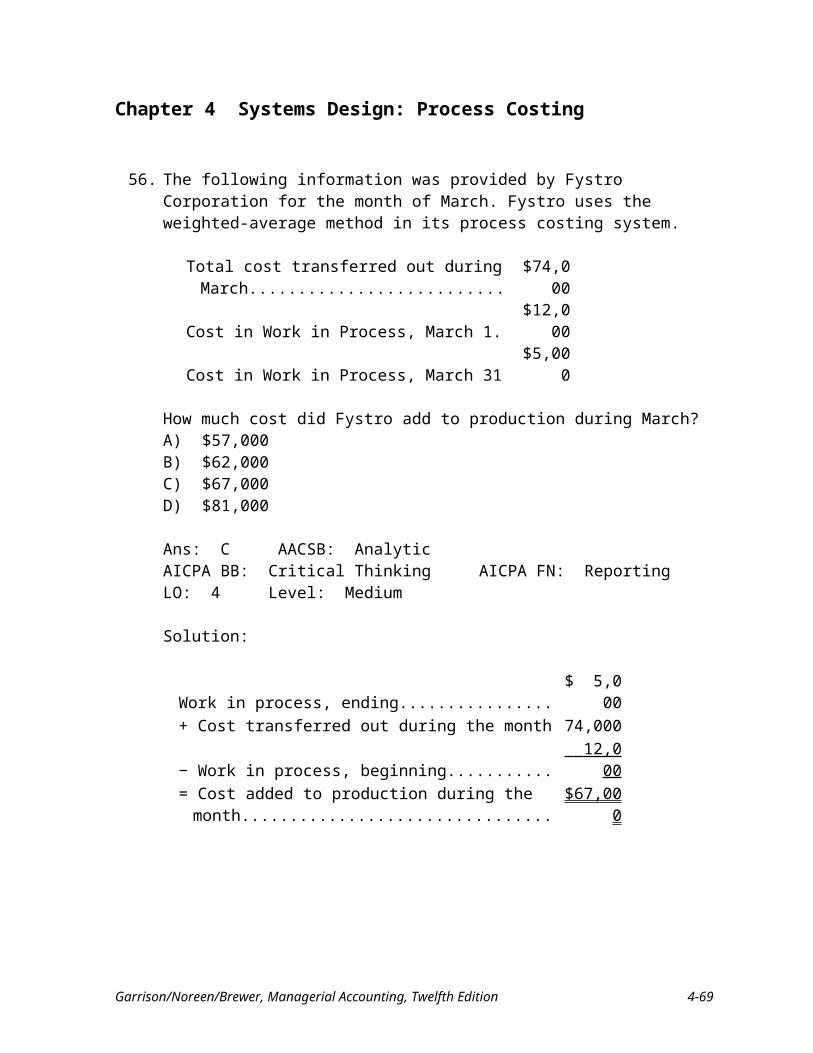

56. The following information was provided by Fystro Corporation for the month of March. Fystro uses the weighted-average method in its process costing system.

Total cost transferred out during March................ $74,000Cost in Work in Process, March 1......................... $12,000Cost in Work in Process, March 31....................... $5,000

How much cost did Fystro add to production during March?A) $57,000B) $62,000C) $67,000D) $81,000

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Medium

Solution:

Work in process, ending...................................................... $ 5,000+ Cost transferred out during the month.............................. 74,000− Work in process, beginning.............................................. 12,000 = Cost added to production during the month..................... $67,000

4-44 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

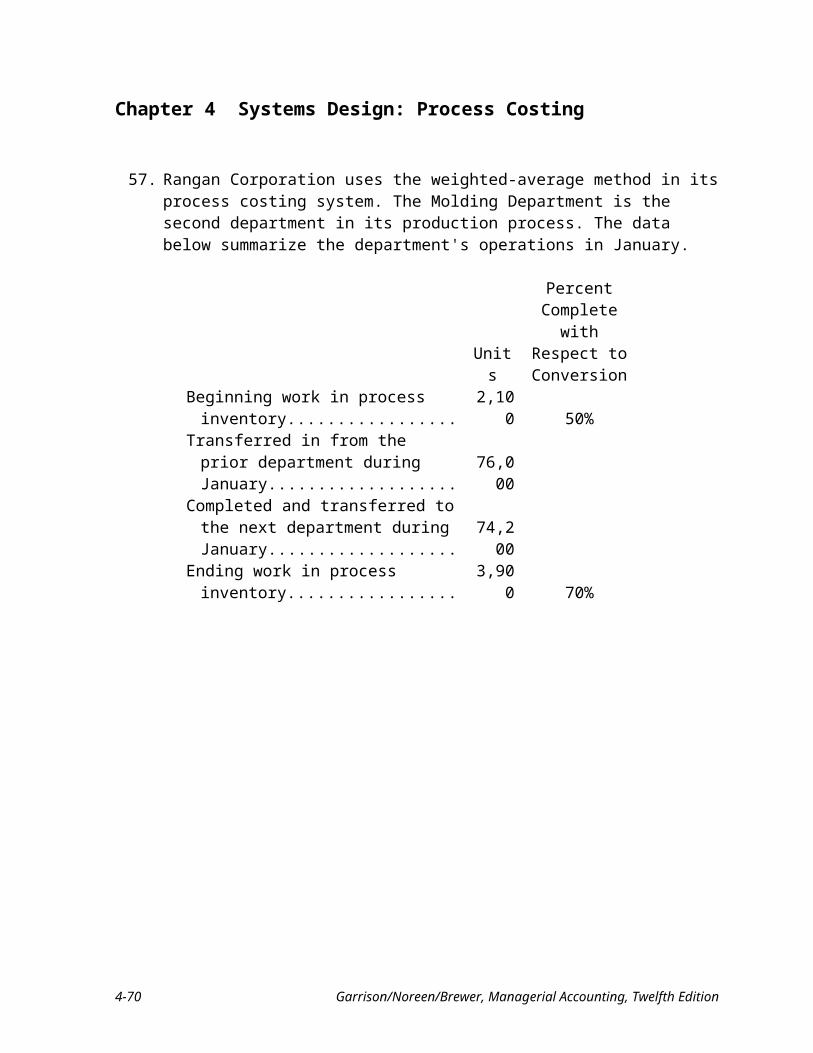

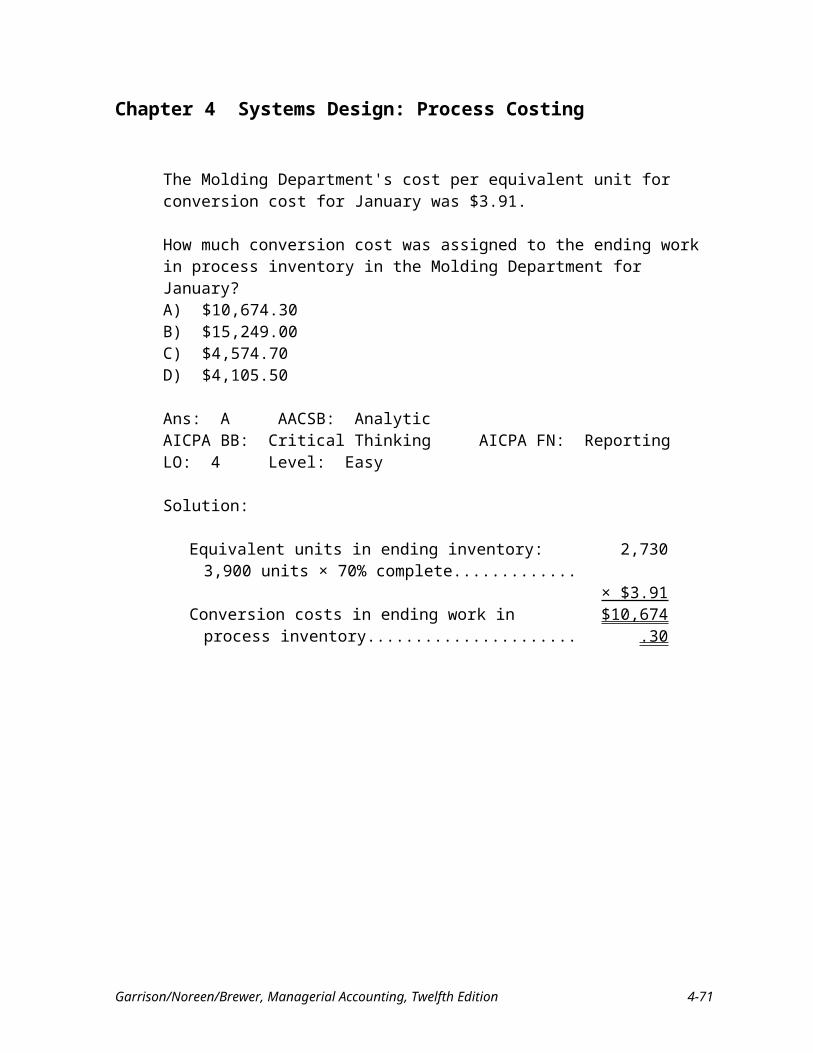

57. Rangan Corporation uses the weighted-average method in its process costing system. The Molding Department is the second department in its production process. The data below summarize the department's operations in January.

Units

Percent Complete with

Respect to Conversion

Beginning work in process inventory........ 2,100 50%Transferred in from the prior department

during January........................................ 76,000Completed and transferred to the next

department during January..................... 74,200Ending work in process inventory............. 3,900 70%

The Molding Department's cost per equivalent unit for conversion cost for January was $3.91.

How much conversion cost was assigned to the ending work in process inventory in the Molding Department for January?A) $10,674.30B) $15,249.00C) $4,574.70D) $4,105.50

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting LO: 4 Level: Easy

Solution:

Equivalent units in ending inventory: 3,900 units × 70% complete..............................................................................

2,730

× $3.91Conversion costs in ending work in process inventory........... $10,674.30

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-45

Chapter 4 Systems Design: Process Costing

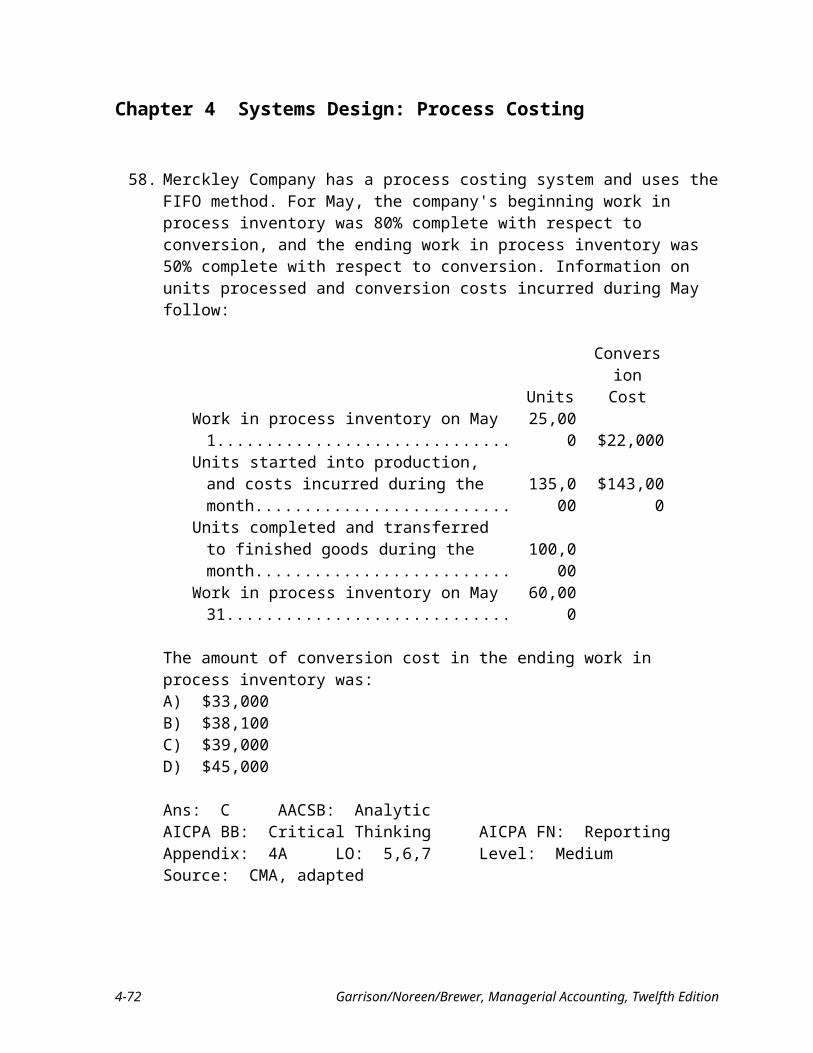

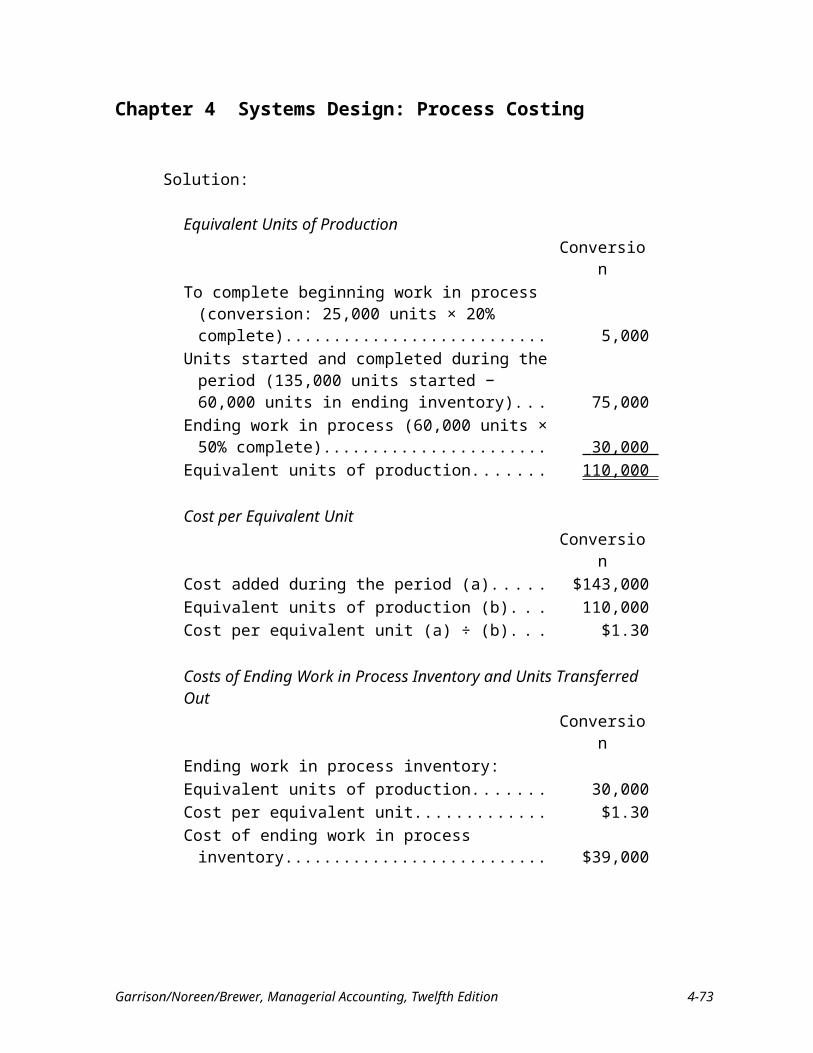

58. Merckley Company has a process costing system and uses the FIFO method. For May, the company's beginning work in process inventory was 80% complete with respect to conversion, and the ending work in process inventory was 50% complete with respect to conversion. Information on units processed and conversion costs incurred during May follow:

UnitsConversion

CostWork in process inventory on May 1..................... 25,000 $22,000Units started into production, and costs incurred

during the month................................................ 135,000 $143,000Units completed and transferred to finished

goods during the month...................................... 100,000Work in process inventory on May 31................... 60,000

The amount of conversion cost in the ending work in process inventory was:A) $33,000B) $38,100C) $39,000D) $45,000

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5,6,7 Level: Medium Source: CMA, adapted

4-46 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

Solution:

Equivalent Units of ProductionConversion

To complete beginning work in process (conversion: 25,000 units × 20% complete)....................................... 5,000

Units started and completed during the period (135,000 units started − 60,000 units in ending inventory).......... 75,000

Ending work in process (60,000 units × 50% complete). . 30,000 Equivalent units of production.......................................... 110,000

Cost per Equivalent UnitConversion

Cost added during the period (a)....................................... $143,000 Equivalent units of production (b).................................... 110,000 Cost per equivalent unit (a) ÷ (b)...................................... $1.30

Costs of Ending Work in Process Inventory and Units Transferred OutConversion

Ending work in process inventory:Equivalent units of production.......................................... 30,000 Cost per equivalent unit.................................................... $1.30 Cost of ending work in process inventory........................ $39,000

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-47

Chapter 4 Systems Design: Process Costing

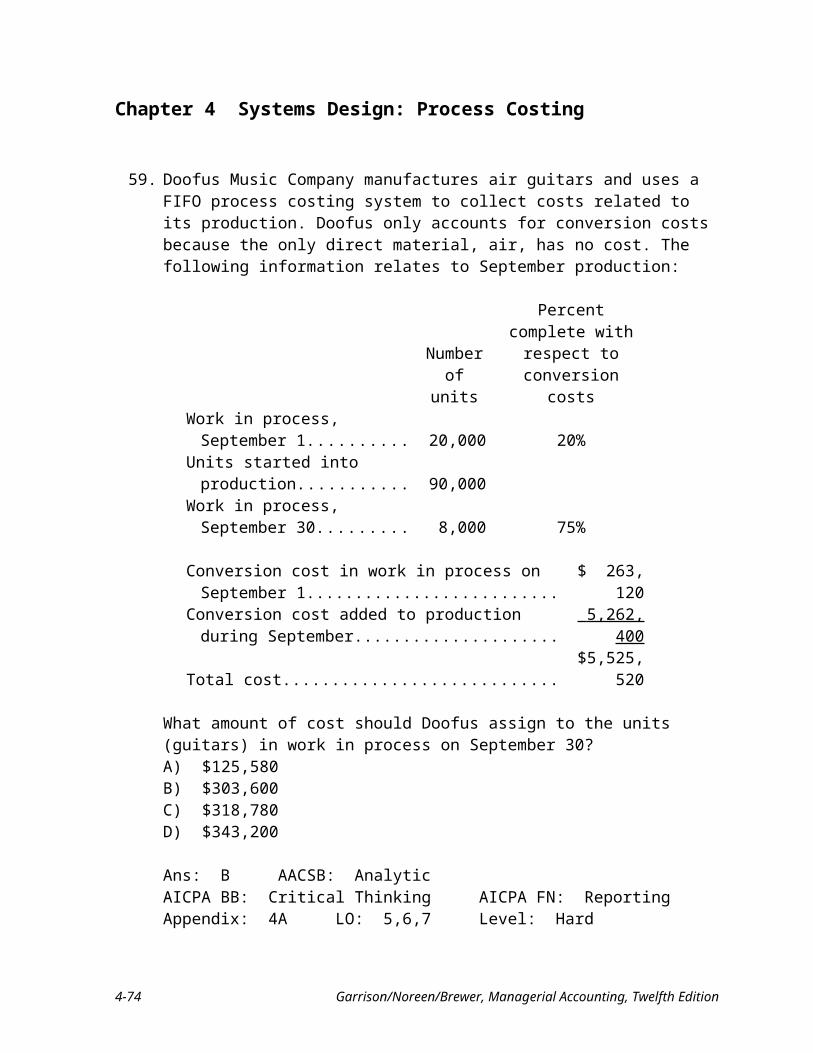

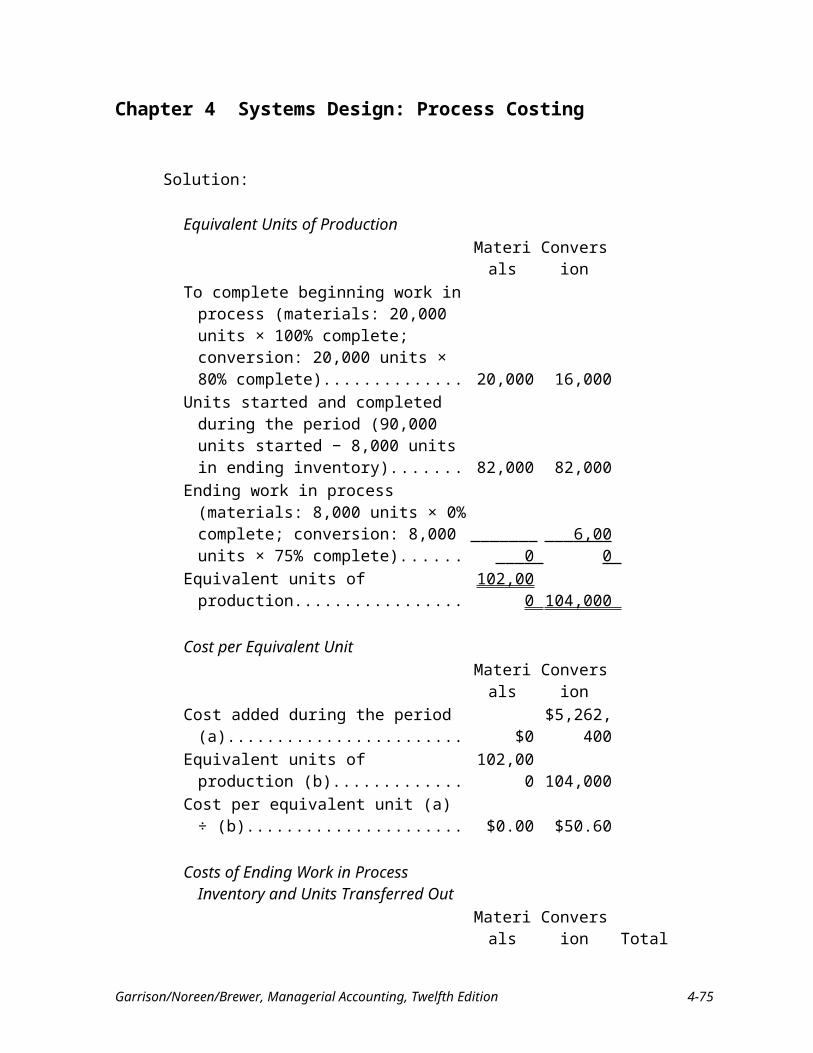

59. Doofus Music Company manufactures air guitars and uses a FIFO process costing system to collect costs related to its production. Doofus only accounts for conversion costs because the only direct material, air, has no cost. The following information relates to September production:

Number of units

Percent complete with respect to

conversion costsWork in process, September 1....... 20,000 20%Units started into production.......... 90,000Work in process, September 30..... 8,000 75%

Conversion cost in work in process on September 1........... $ 263,120Conversion cost added to production during September..... 5,262,400 Total cost............................................................................. $5,525,520

What amount of cost should Doofus assign to the units (guitars) in work in process on September 30?A) $125,580B) $303,600C) $318,780D) $343,200

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5,6,7 Level: Hard

4-48 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

Solution:

Equivalent Units of ProductionMaterials Conversion

To complete beginning work in process (materials: 20,000 units × 100% complete; conversion: 20,000 units × 80% complete).......................................... 20,000 16,000

Units started and completed during the period (90,000 units started − 8,000 units in ending inventory)................................. 82,000 82,000

Ending work in process (materials: 8,000 units × 0% complete; conversion: 8,000 units × 75% complete).............................. 0 6,000

Equivalent units of production..................... 102,000 104,000

Cost per Equivalent UnitMaterials Conversion

Cost added during the period (a).................. $0 $5,262,400 Equivalent units of production (b)............... 102,000 104,000 Cost per equivalent unit (a) ÷ (b)................. $0.00 $50.60

Costs of Ending Work in Process Inventory and Units Transferred Out

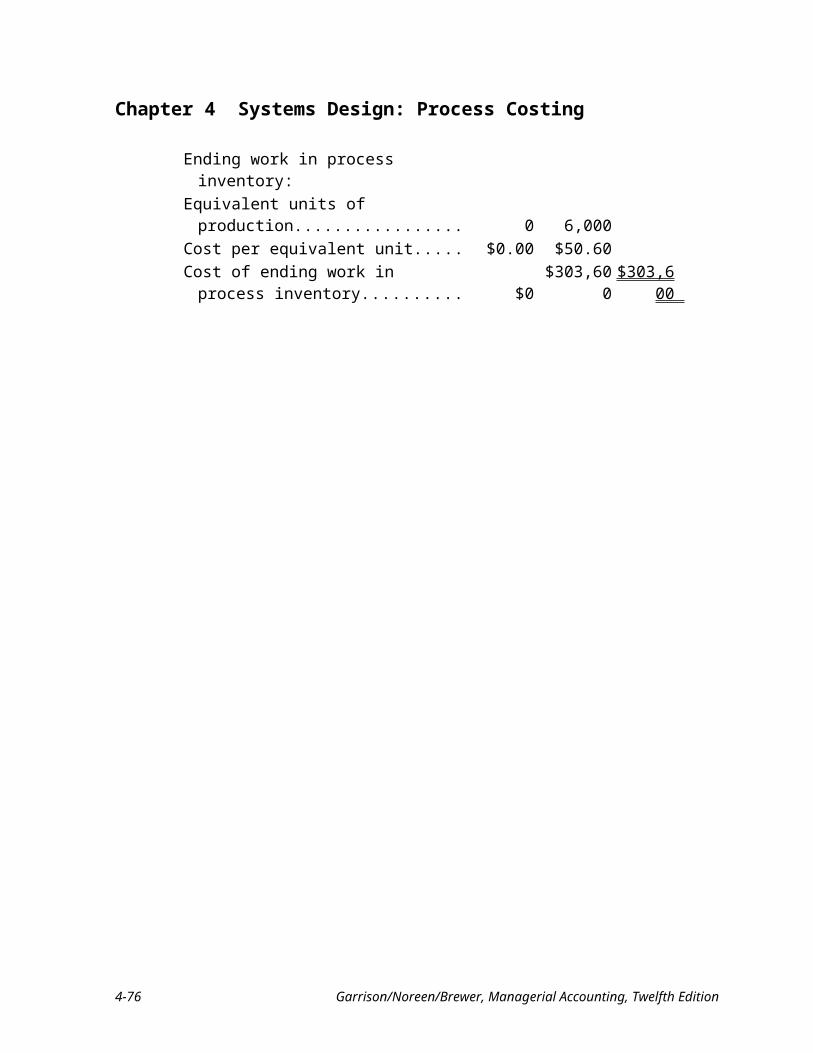

Materials Conversion TotalEnding work in process inventory:Equivalent units of production..................... 0 6,000 Cost per equivalent unit............................... $0.00 $50.60 Cost of ending work in process inventory.... $0 $303,600 $303,600

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-49

Chapter 4 Systems Design: Process Costing

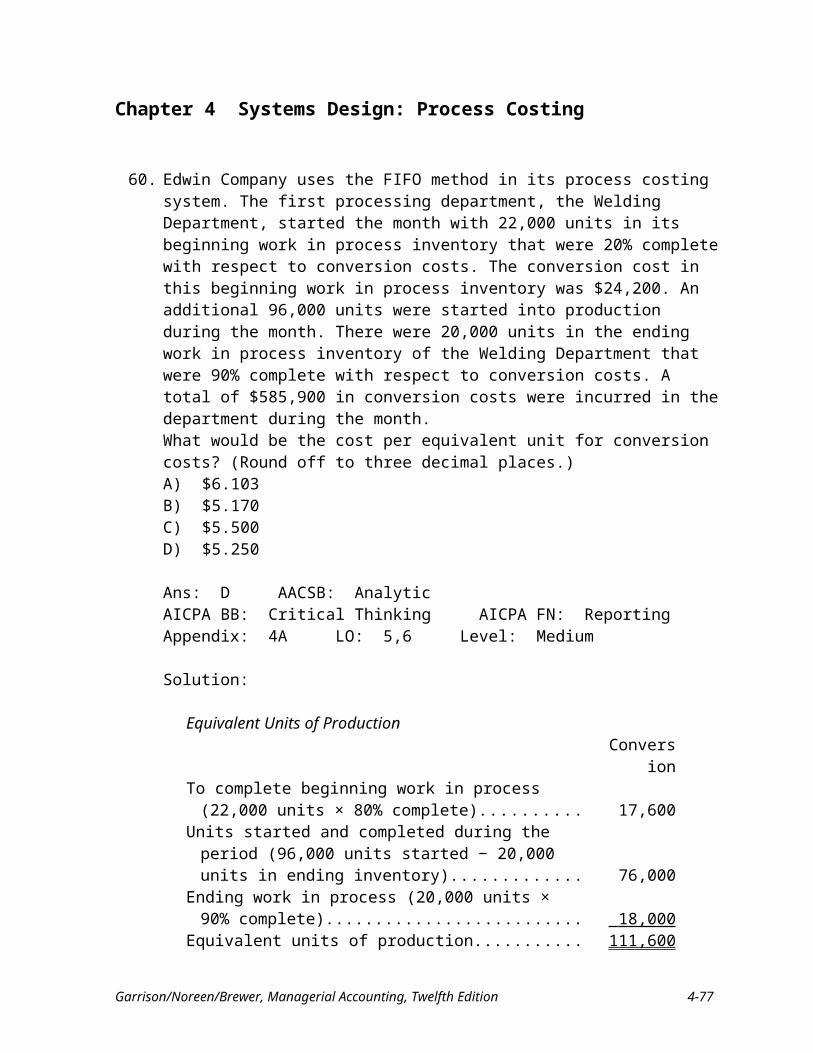

60. Edwin Company uses the FIFO method in its process costing system. The first processing department, the Welding Department, started the month with 22,000 units in its beginning work in process inventory that were 20% complete with respect to conversion costs. The conversion cost in this beginning work in process inventory was $24,200. An additional 96,000 units were started into production during the month. There were 20,000 units in the ending work in process inventory of the Welding Department that were 90% complete with respect to conversion costs. A total of $585,900 in conversion costs were incurred in the department during the month.What would be the cost per equivalent unit for conversion costs? (Round off to three decimal places.)A) $6.103B) $5.170C) $5.500D) $5.250

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5,6 Level: Medium

Solution:

Equivalent Units of ProductionConversion

To complete beginning work in process (22,000 units × 80% complete)............................................................................... 17,600

Units started and completed during the period (96,000 units started − 20,000 units in ending inventory)........................... 76,000

Ending work in process (20,000 units × 90% complete).......... 18,000 Equivalent units of production.................................................. 111,600

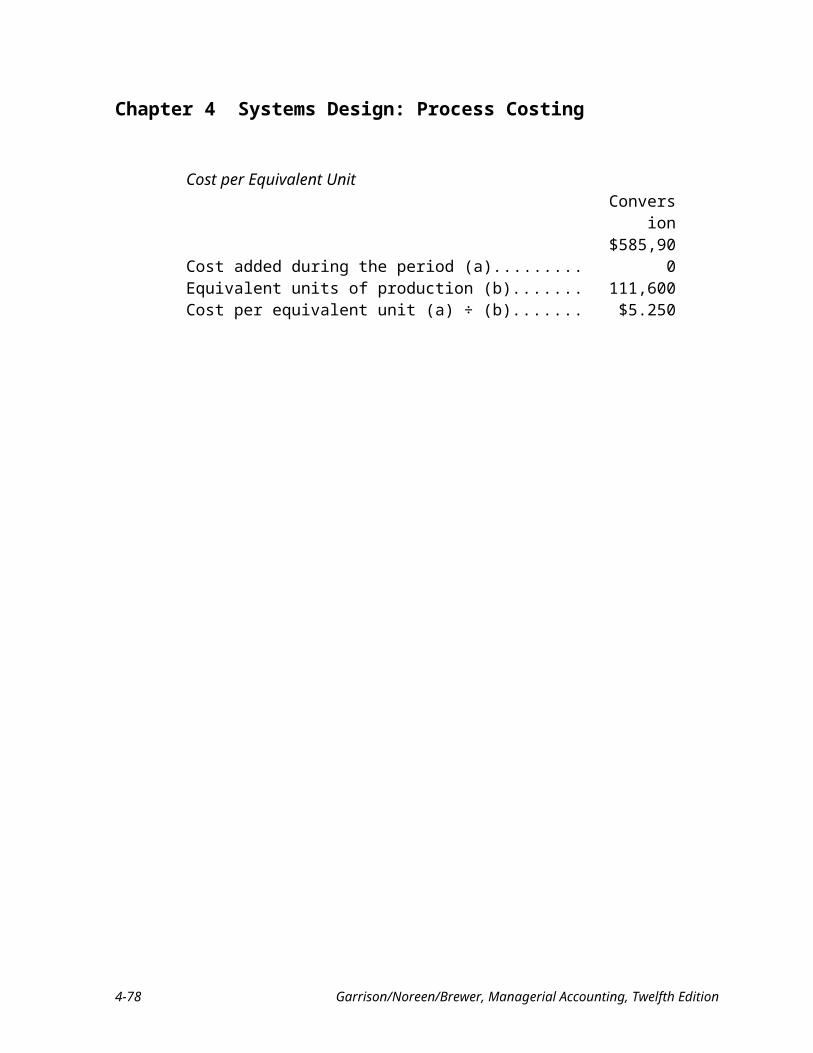

Cost per Equivalent UnitConversion

Cost added during the period (a)............................................... $585,900Equivalent units of production (b)............................................. 111,600Cost per equivalent unit (a) ÷ (b).............................................. $5.250

4-50 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

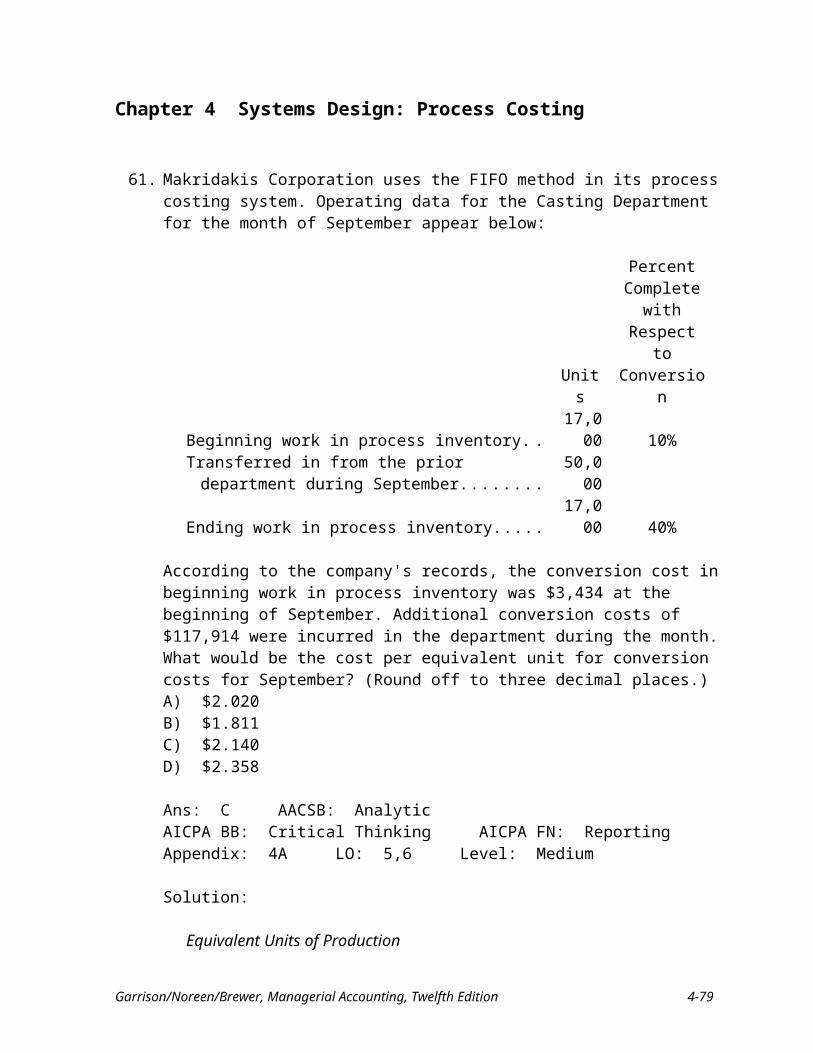

61. Makridakis Corporation uses the FIFO method in its process costing system. Operating data for the Casting Department for the month of September appear below:

Units

Percent Complete

with Respect to Conversion

Beginning work in process inventory.............................. 17,000 10%Transferred in from the prior department during

September..................................................................... 50,000Ending work in process inventory................................... 17,000 40%

According to the company's records, the conversion cost in beginning work in process inventory was $3,434 at the beginning of September. Additional conversion costs of $117,914 were incurred in the department during the month.What would be the cost per equivalent unit for conversion costs for September? (Round off to three decimal places.)A) $2.020B) $1.811C) $2.140D) $2.358

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5,6 Level: Medium

Solution:

Equivalent Units of ProductionConversion

To complete beginning work in process (17,000 units × 90% complete)............................................................. 15,300

Units started and completed during the period (50,000 units started − 17,000 units in ending inventory)........ 33,000

Ending work in process (17,000 units × 40% complete) 6,800 Equivalent units of production........................................ 55,100

Cost per Equivalent UnitConversion

Cost added during the period (a)..................................... $117,914Equivalent units of production (b).................................. 55,100Cost per equivalent unit (a) ÷ (b).................................... $2.140

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-51

Chapter 4 Systems Design: Process Costing

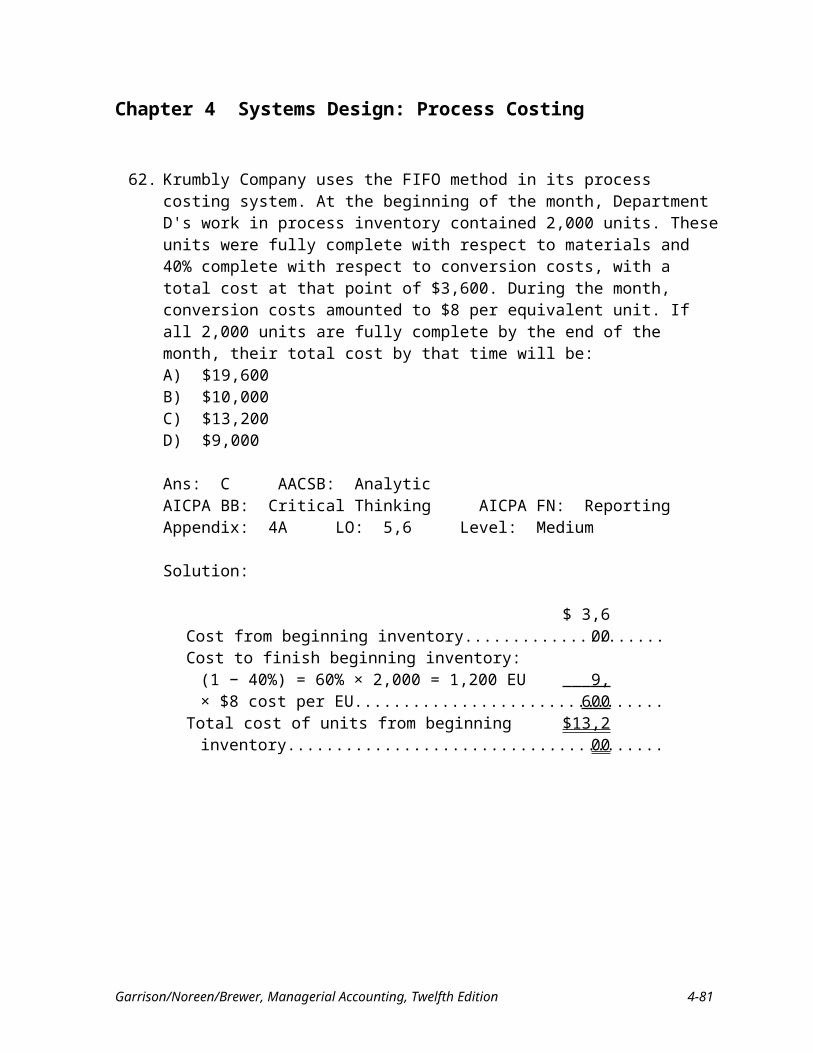

62. Krumbly Company uses the FIFO method in its process costing system. At the beginning of the month, Department D's work in process inventory contained 2,000 units. These units were fully complete with respect to materials and 40% complete with respect to conversion costs, with a total cost at that point of $3,600. During the month, conversion costs amounted to $8 per equivalent unit. If all 2,000 units are fully complete by the end of the month, their total cost by that time will be:A) $19,600B) $10,000C) $13,200D) $9,000

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5,6 Level: Medium

Solution:

Cost from beginning inventory......................................................................$ 3,600Cost to finish beginning inventory: (1 − 40%) = 60% ×

2,000 = 1,200 EU × $8 cost per EU........................................................... 9,600 Total cost of units from beginning inventory................................................$13,200

4-52 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

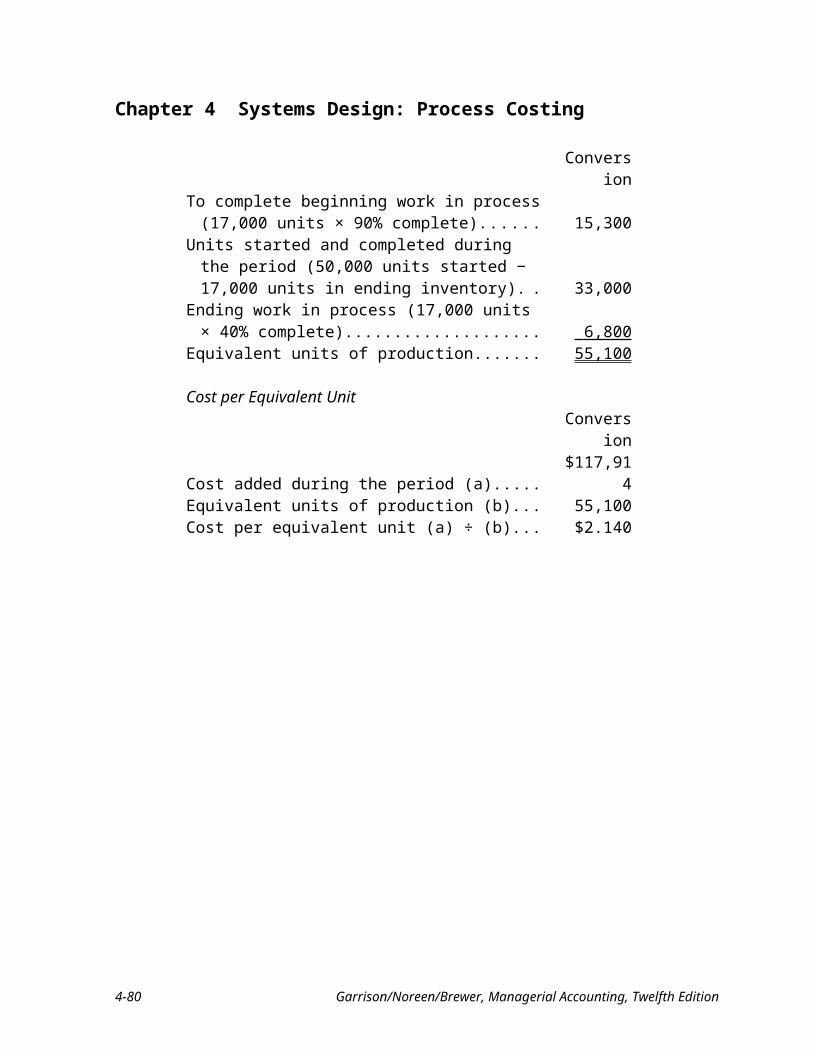

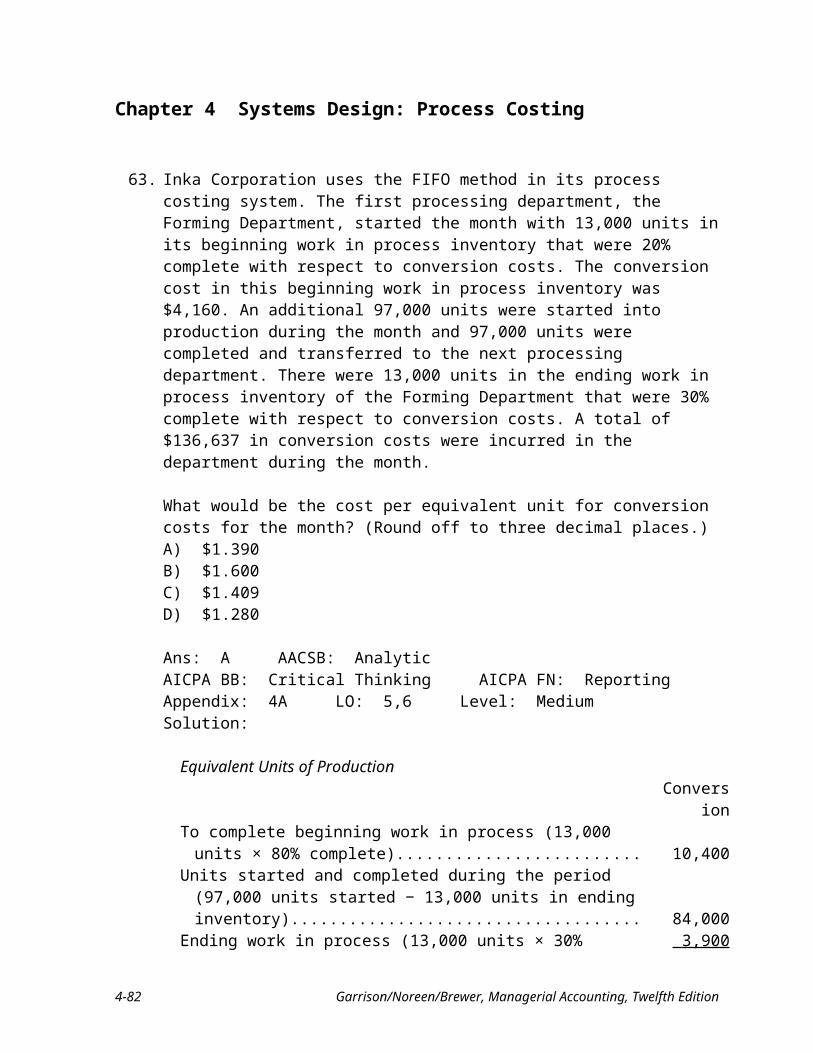

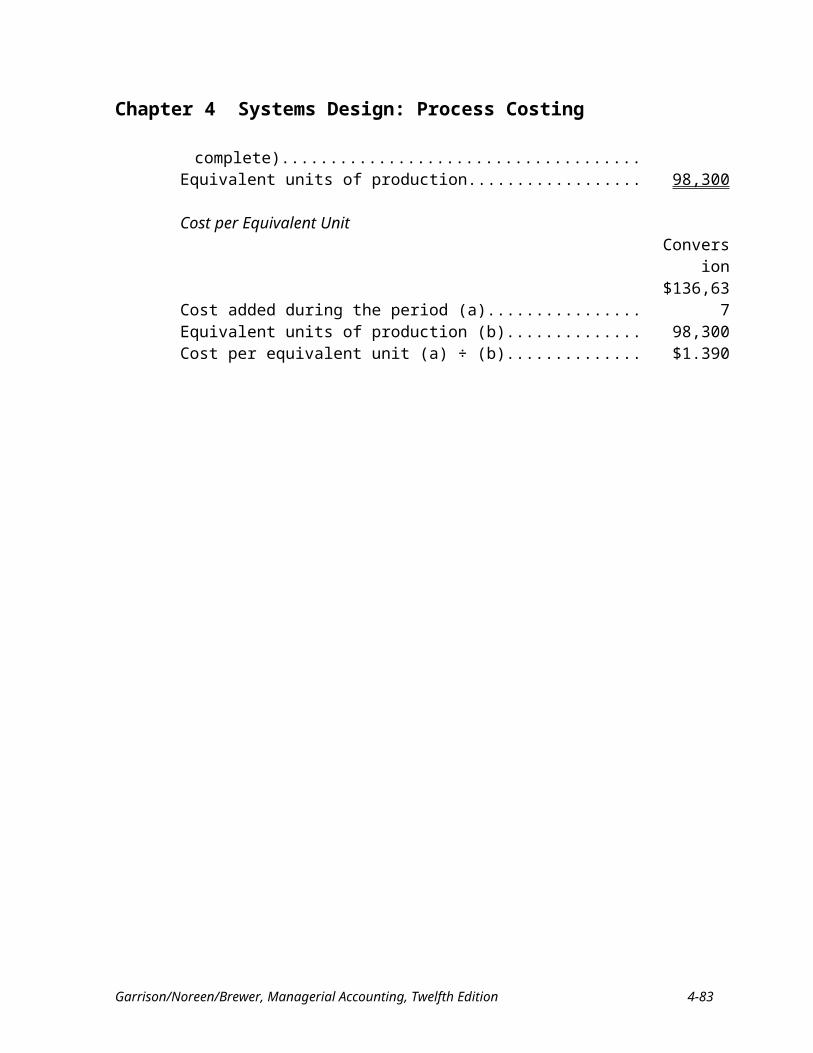

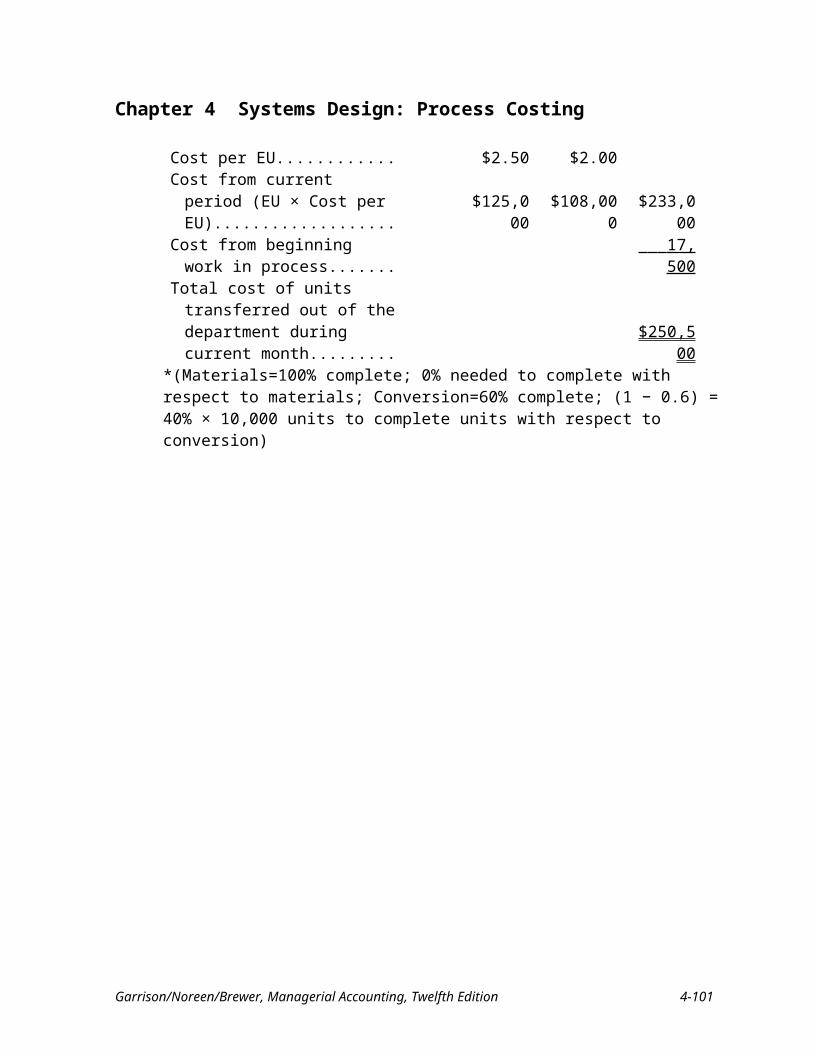

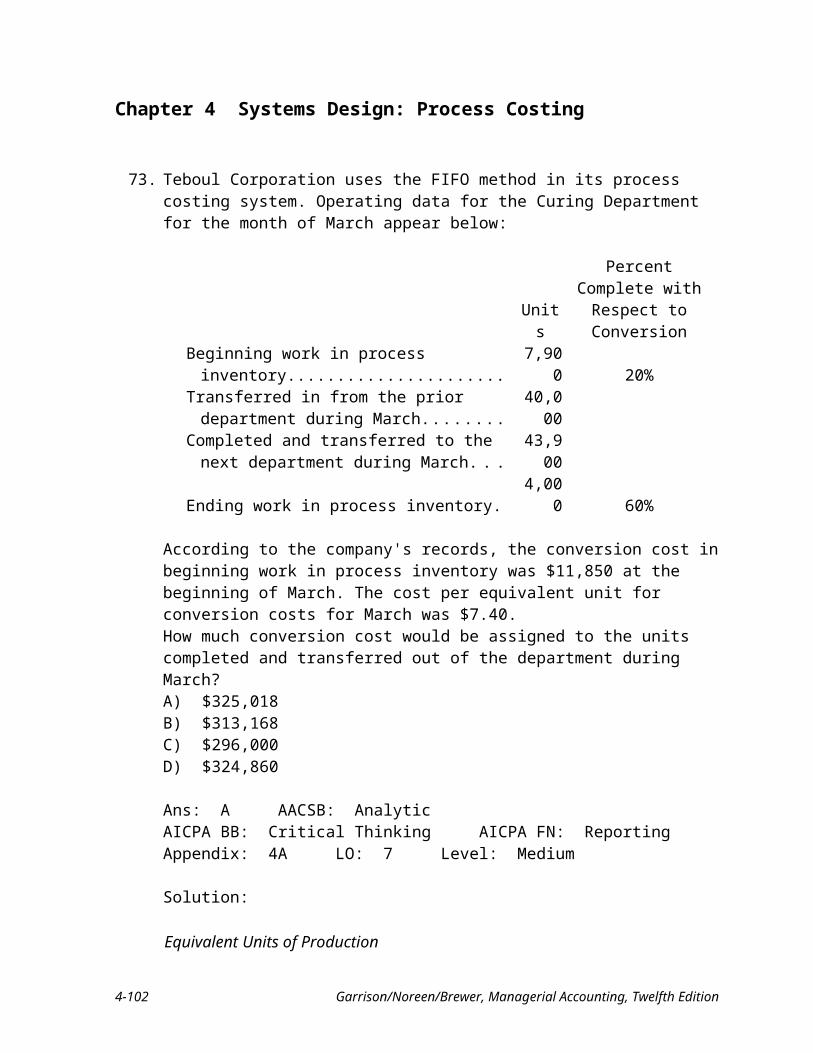

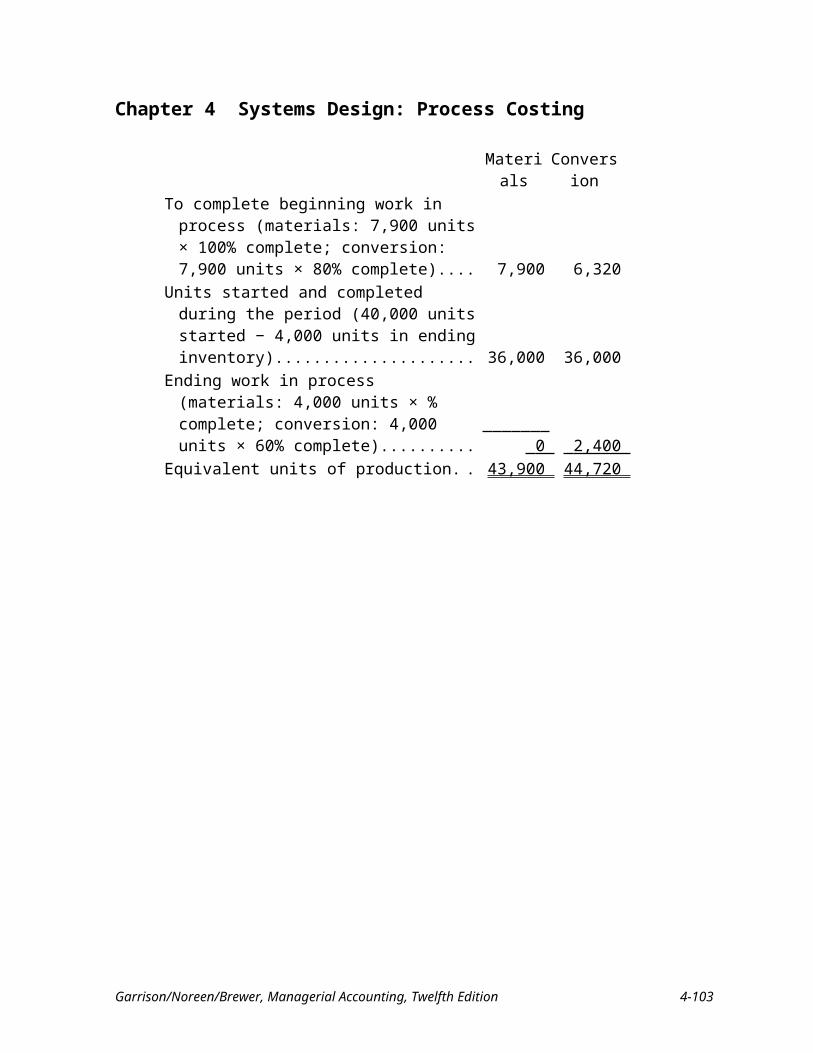

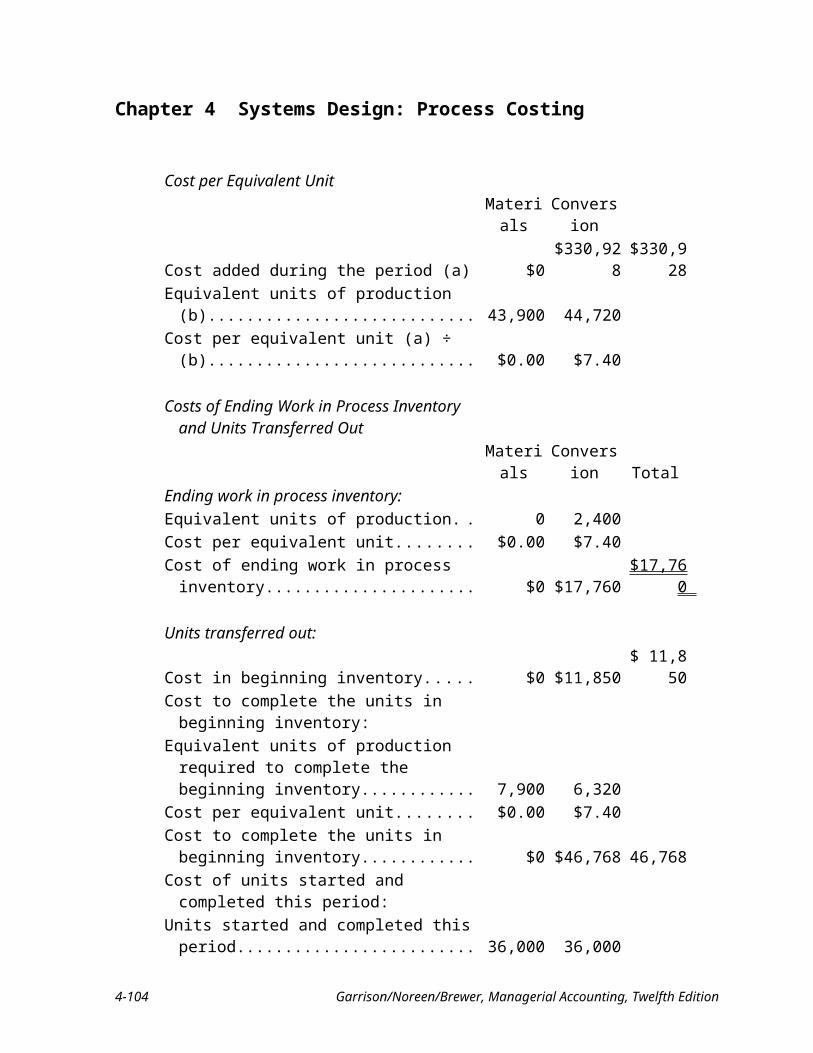

63. Inka Corporation uses the FIFO method in its process costing system. The first processing department, the Forming Department, started the month with 13,000 units in its beginning work in process inventory that were 20% complete with respect to conversion costs. The conversion cost in this beginning work in process inventory was $4,160. An additional 97,000 units were started into production during the month and 97,000 units were completed and transferred to the next processing department. There were 13,000 units in the ending work in process inventory of the Forming Department that were 30% complete with respect to conversion costs. A total of $136,637 in conversion costs were incurred in the department during the month.

What would be the cost per equivalent unit for conversion costs for the month? (Round off to three decimal places.)A) $1.390B) $1.600C) $1.409D) $1.280

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5,6 Level: MediumSolution:

Equivalent Units of ProductionConversion

To complete beginning work in process (13,000 units × 80% complete). 10,400Units started and completed during the period (97,000 units started −

13,000 units in ending inventory).......................................................... 84,000Ending work in process (13,000 units × 30% complete)........................... 3,900 Equivalent units of production................................................................... 98,300

Cost per Equivalent UnitConversion

Cost added during the period (a)............................................................... $136,637Equivalent units of production (b)............................................................. 98,300Cost per equivalent unit (a) ÷ (b)............................................................... $1.390

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-53

Chapter 4 Systems Design: Process Costing

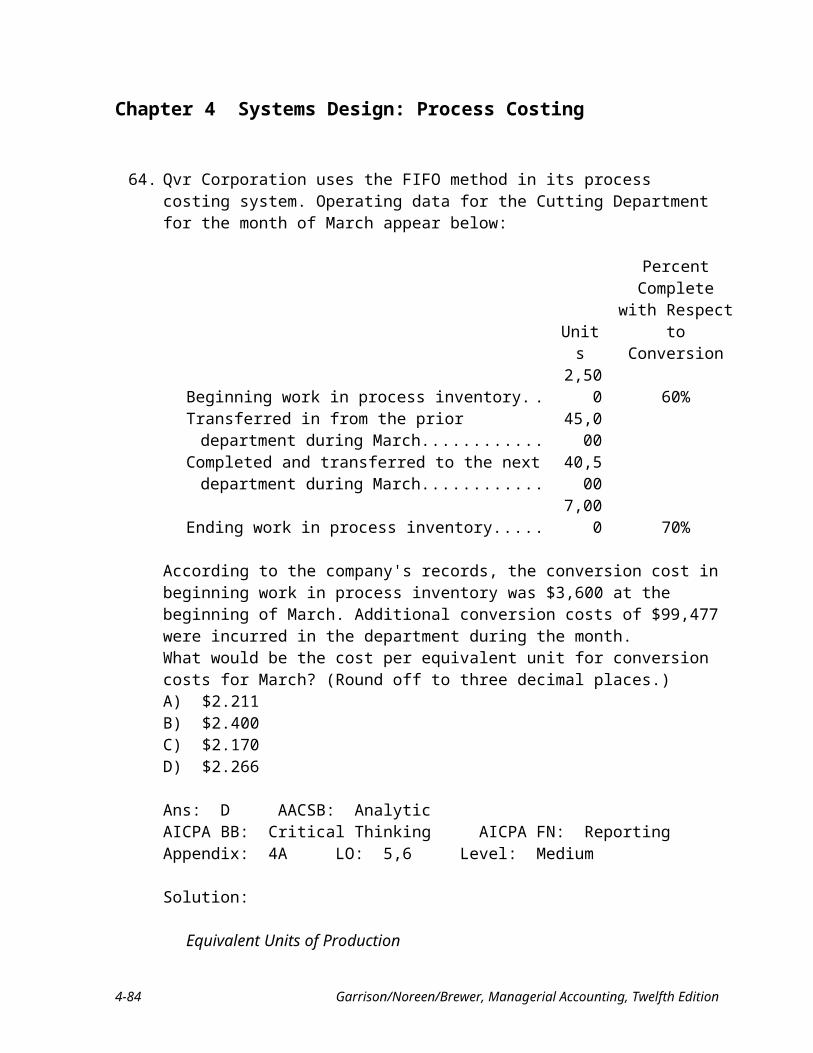

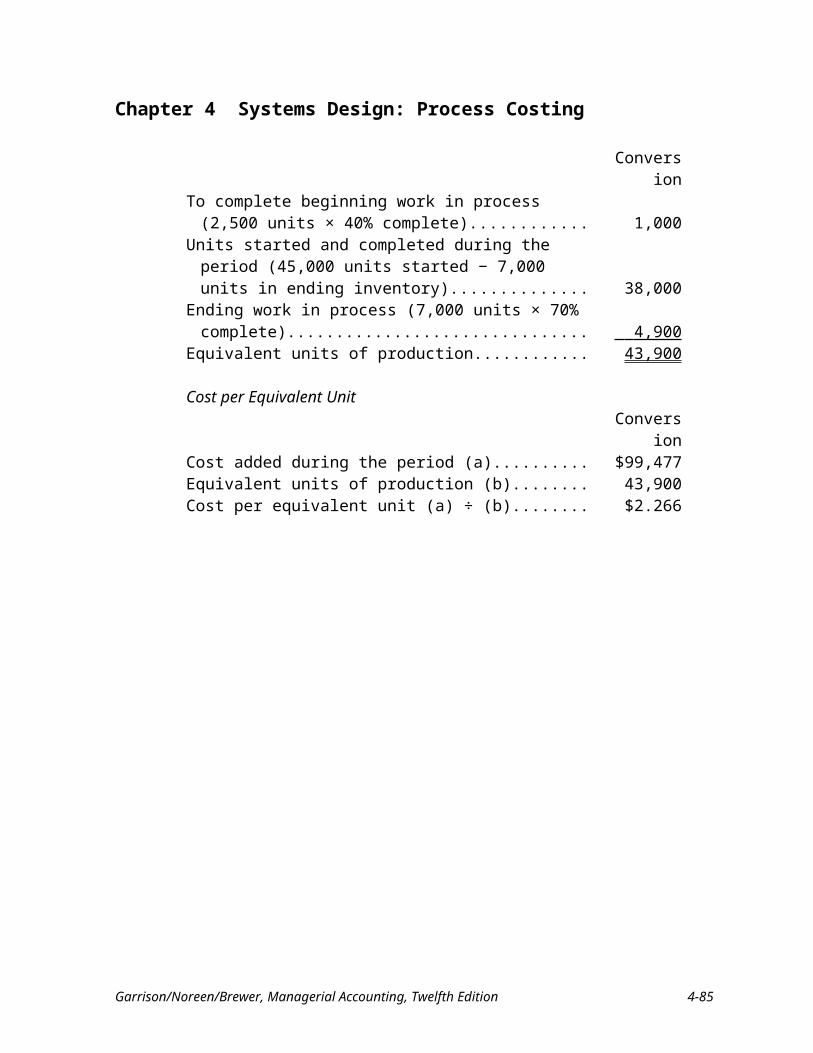

64. Qvr Corporation uses the FIFO method in its process costing system. Operating data for the Cutting Department for the month of March appear below:

Units

Percent Complete with Respect to

ConversionBeginning work in process inventory.............................. 2,500 60%Transferred in from the prior department during March. 45,000Completed and transferred to the next department

during March................................................................ 40,500Ending work in process inventory................................... 7,000 70%

According to the company's records, the conversion cost in beginning work in process inventory was $3,600 at the beginning of March. Additional conversion costs of $99,477 were incurred in the department during the month.What would be the cost per equivalent unit for conversion costs for March? (Round off to three decimal places.)A) $2.211B) $2.400C) $2.170D) $2.266

Ans: D AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5,6 Level: Medium

Solution:

Equivalent Units of ProductionConversion

To complete beginning work in process (2,500 units × 40% complete)................................................................................. 1,000

Units started and completed during the period (45,000 units started − 7,000 units in ending inventory)............................... 38,000

Ending work in process (7,000 units × 70% complete).............. 4,900 Equivalent units of production.................................................... 43,900

Cost per Equivalent UnitConversion

Cost added during the period (a)................................................. $99,477Equivalent units of production (b).............................................. 43,900Cost per equivalent unit (a) ÷ (b)................................................ $2.266

4-54 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

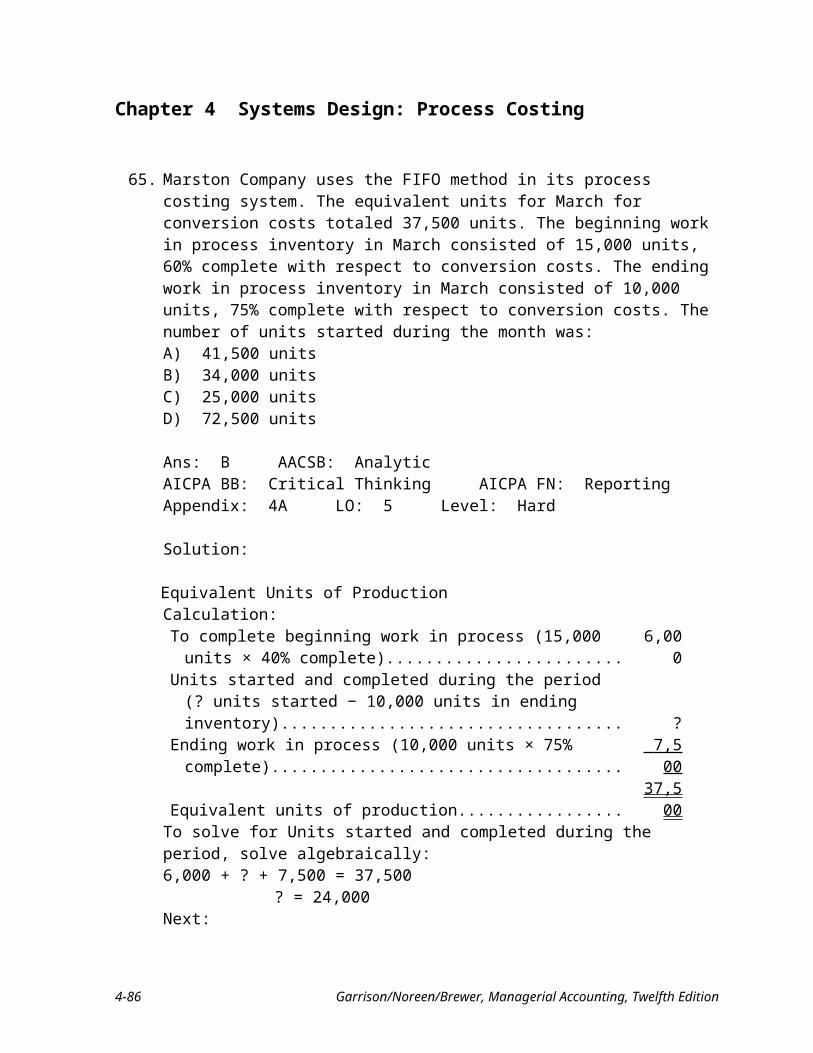

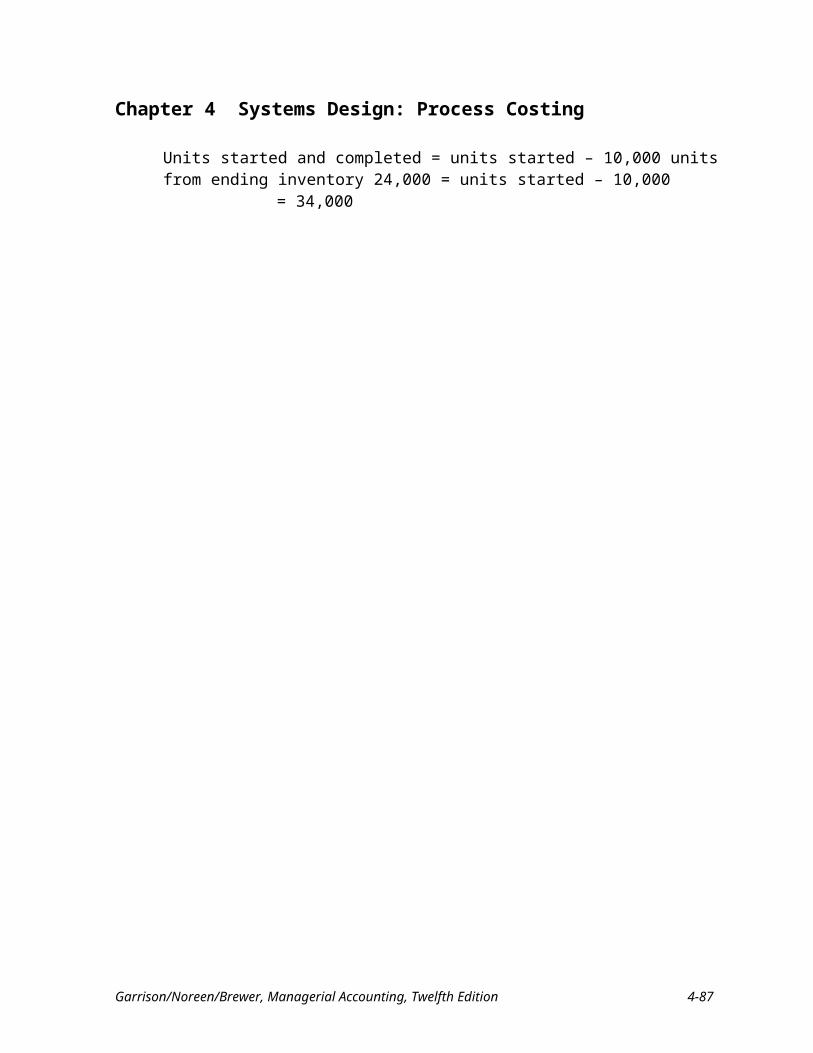

65. Marston Company uses the FIFO method in its process costing system. The equivalent units for March for conversion costs totaled 37,500 units. The beginning work in process inventory in March consisted of 15,000 units, 60% complete with respect to conversion costs. The ending work in process inventory in March consisted of 10,000 units, 75% complete with respect to conversion costs. The number of units started during the month was:A) 41,500 unitsB) 34,000 unitsC) 25,000 unitsD) 72,500 units

Ans: B AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5 Level: Hard

Solution:

Equivalent Units of Production Calculation:To complete beginning work in process (15,000 units × 40%

complete).............................................................................................. 6,000Units started and completed during the period (? units started − 10,000

units in ending inventory).................................................................... ?Ending work in process (10,000 units × 75% complete)......................... 7,500 Equivalent units of production................................................................ 37,500

To solve for Units started and completed during the period, solve algebraically:6,000 + ? + 7,500 = 37,500

? = 24,000Next:Units started and completed = units started – 10,000 units from ending inventory 24,000 = units started – 10,000

= 34,000

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-55

Chapter 4 Systems Design: Process Costing

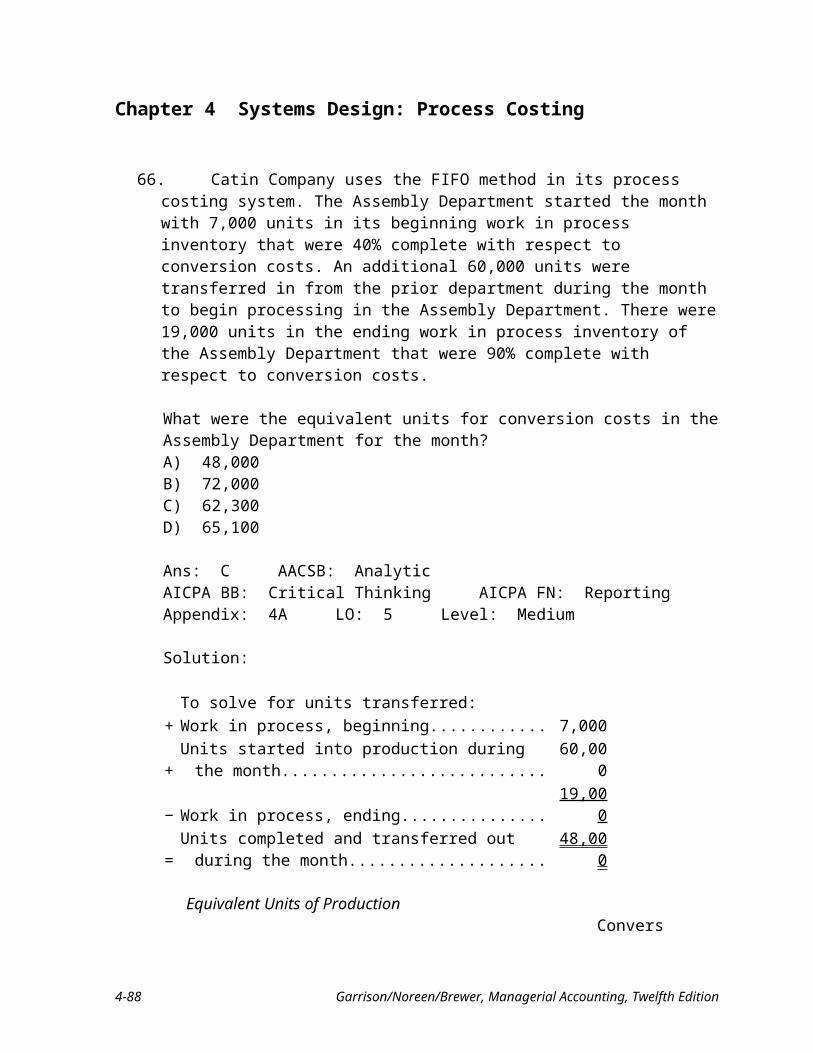

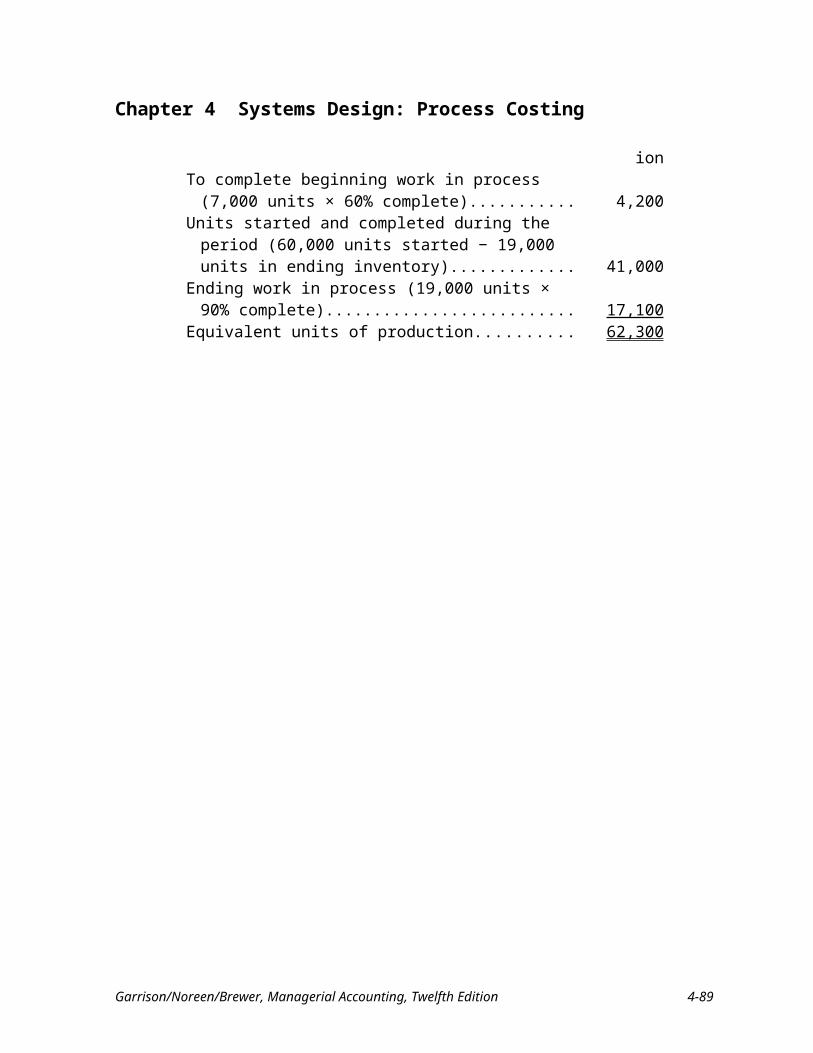

66. Catin Company uses the FIFO method in its process costing system. The Assembly Department started the month with 7,000 units in its beginning work in process inventory that were 40% complete with respect to conversion costs. An additional 60,000 units were transferred in from the prior department during the month to begin processing in the Assembly Department. There were 19,000 units in the ending work in process inventory of the Assembly Department that were 90% complete with respect to conversion costs.

What were the equivalent units for conversion costs in the Assembly Department for the month?A) 48,000B) 72,000C) 62,300D) 65,100

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5 Level: Medium

Solution:

To solve for units transferred:+ Work in process, beginning............................................... 7,000+ Units started into production during the month................. 60,000− Work in process, ending.................................................... 19,000= Units completed and transferred out during the month..... 48,000

Equivalent Units of ProductionConversion

To complete beginning work in process (7,000 units × 60% complete).............................................................................. 4,200

Units started and completed during the period (60,000 units started − 19,000 units in ending inventory)......................... 41,000

Ending work in process (19,000 units × 90% complete)......... 17,100Equivalent units of production................................................. 62,300

4-56 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Chapter 4 Systems Design: Process Costing

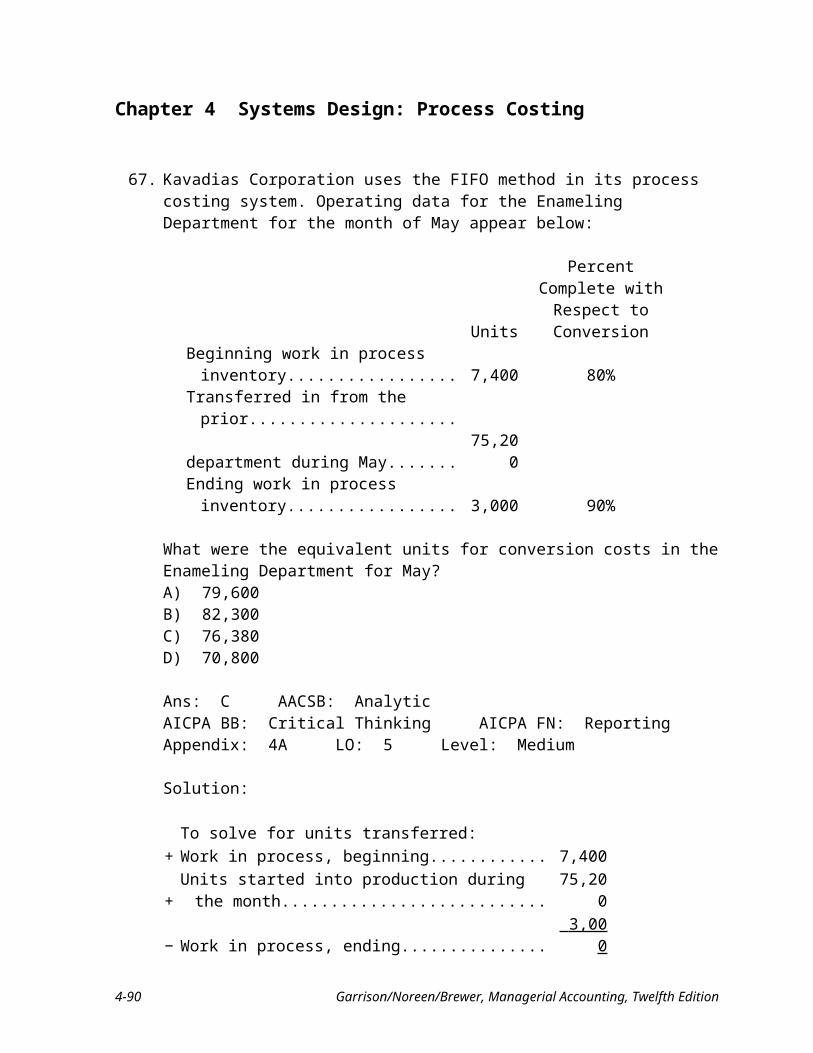

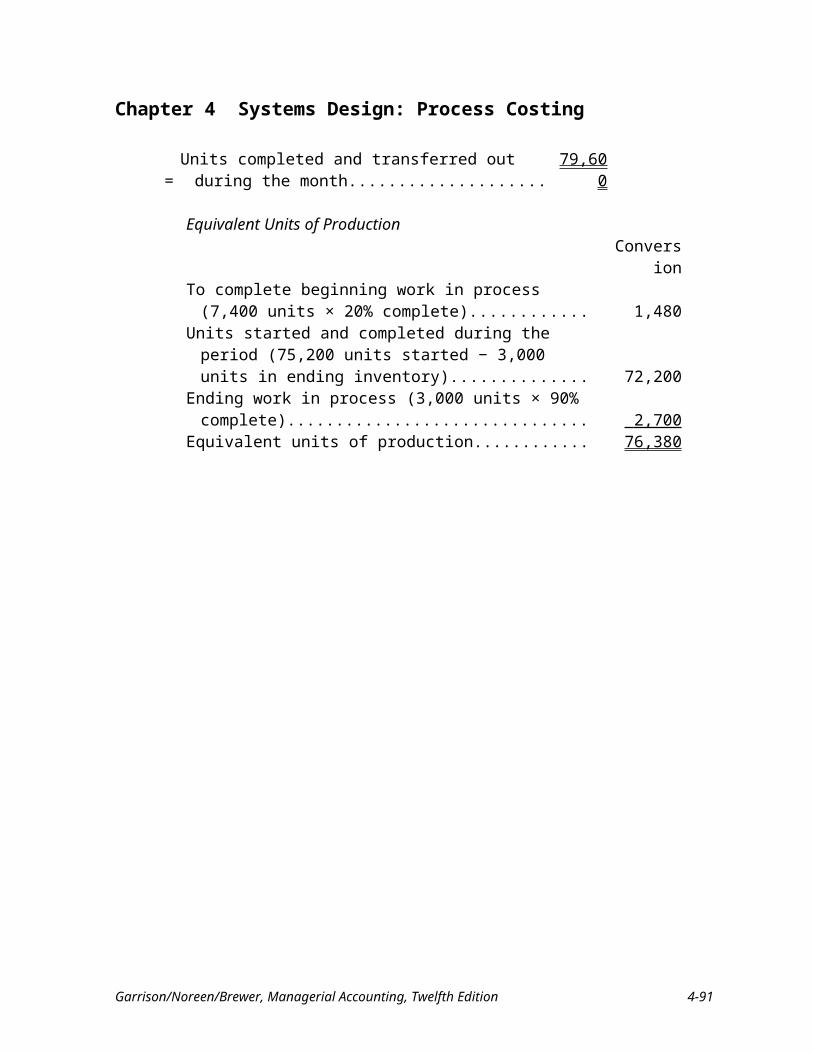

67. Kavadias Corporation uses the FIFO method in its process costing system. Operating data for the Enameling Department for the month of May appear below:

Units

Percent Complete with Respect to

ConversionBeginning work in process inventory........ 7,400 80%Transferred in from the prior.....................department during May.............................. 75,200Ending work in process inventory............. 3,000 90%

What were the equivalent units for conversion costs in the Enameling Department for May?A) 79,600B) 82,300C) 76,380D) 70,800

Ans: C AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5 Level: Medium

Solution:

To solve for units transferred:+ Work in process, beginning............................................... 7,400+ Units started into production during the month................. 75,200− Work in process, ending.................................................... 3,000 = Units completed and transferred out during the month..... 79,600

Equivalent Units of ProductionConversion

To complete beginning work in process (7,400 units × 20% complete)................................................................................. 1,480

Units started and completed during the period (75,200 units started − 3,000 units in ending inventory)............................... 72,200

Ending work in process (3,000 units × 90% complete).............. 2,700 Equivalent units of production.................................................... 76,380

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-57

Chapter 4 Systems Design: Process Costing

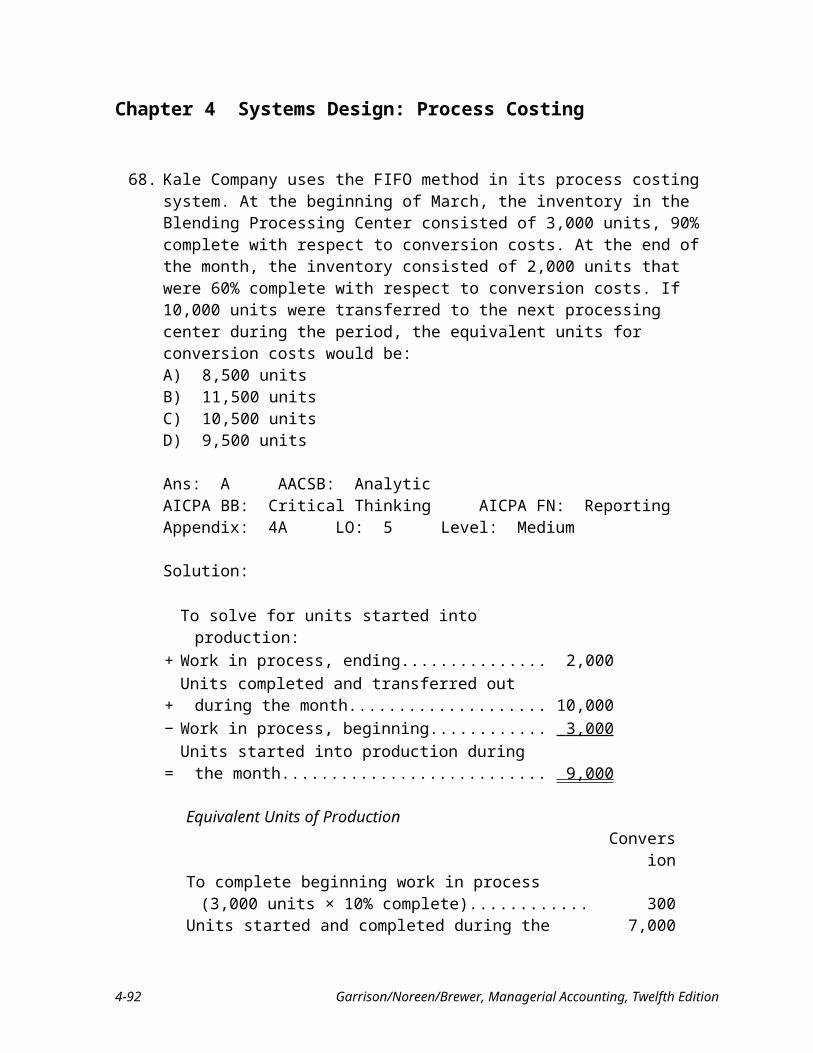

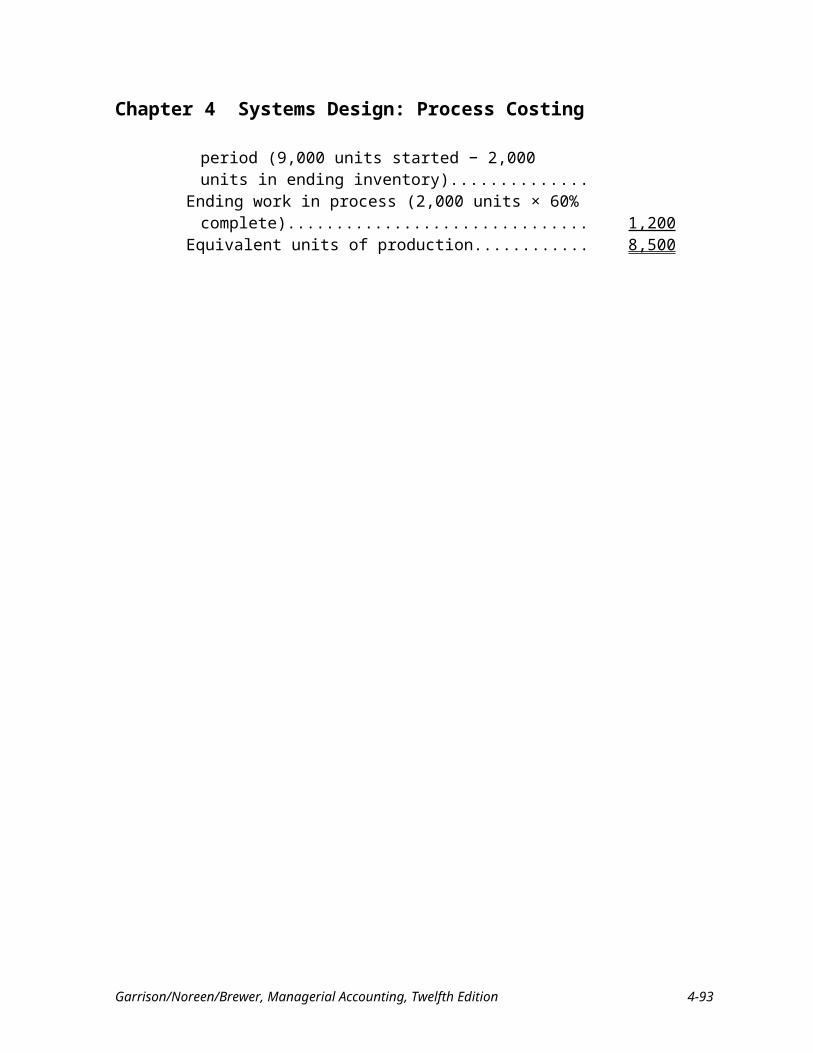

68. Kale Company uses the FIFO method in its process costing system. At the beginning of March, the inventory in the Blending Processing Center consisted of 3,000 units, 90% complete with respect to conversion costs. At the end of the month, the inventory consisted of 2,000 units that were 60% complete with respect to conversion costs. If 10,000 units were transferred to the next processing center during the period, the equivalent units for conversion costs would be:A) 8,500 unitsB) 11,500 unitsC) 10,500 unitsD) 9,500 units

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5 Level: Medium

Solution:

To solve for units started into production:+ Work in process, ending.................................................... 2,000+ Units completed and transferred out during the month..... 10,000− Work in process, beginning............................................... 3,000 = Units started into production during the month................. 9,000

Equivalent Units of ProductionConversion

To complete beginning work in process (3,000 units × 10% complete)................................................................................. 300

Units started and completed during the period (9,000 units started − 2,000 units in ending inventory)............................... 7,000

Ending work in process (2,000 units × 60% complete).............. 1,200Equivalent units of production.................................................... 8,500

4-58 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

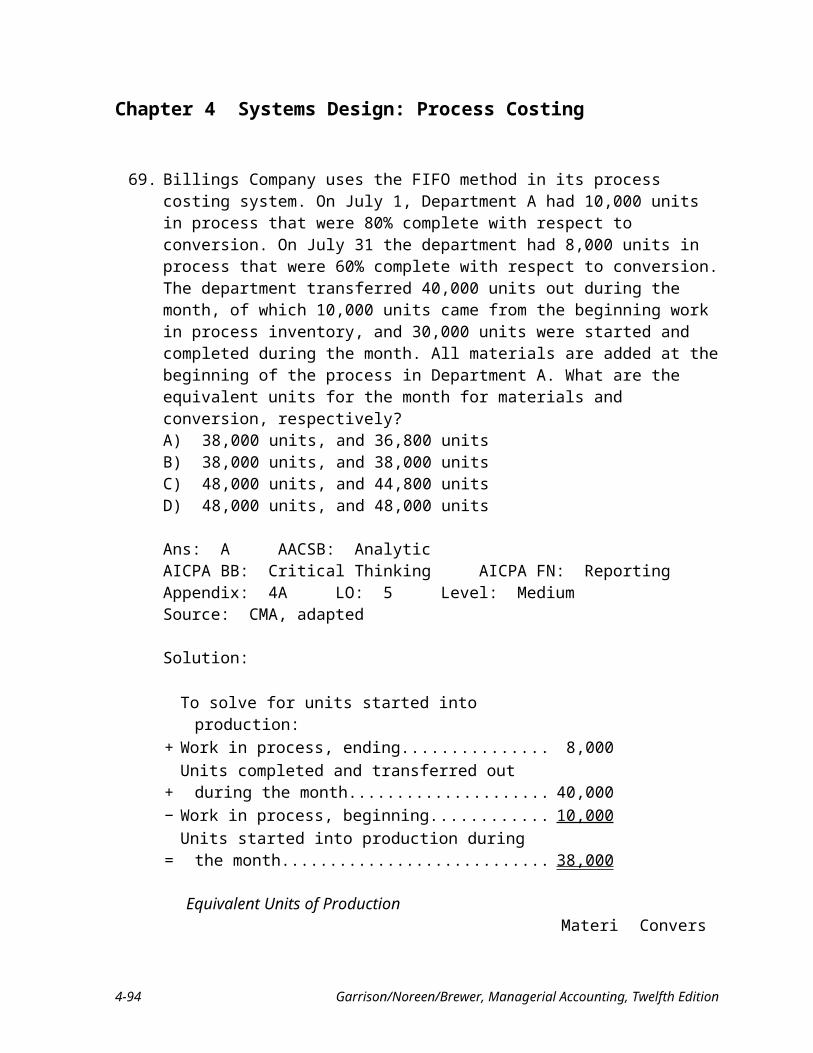

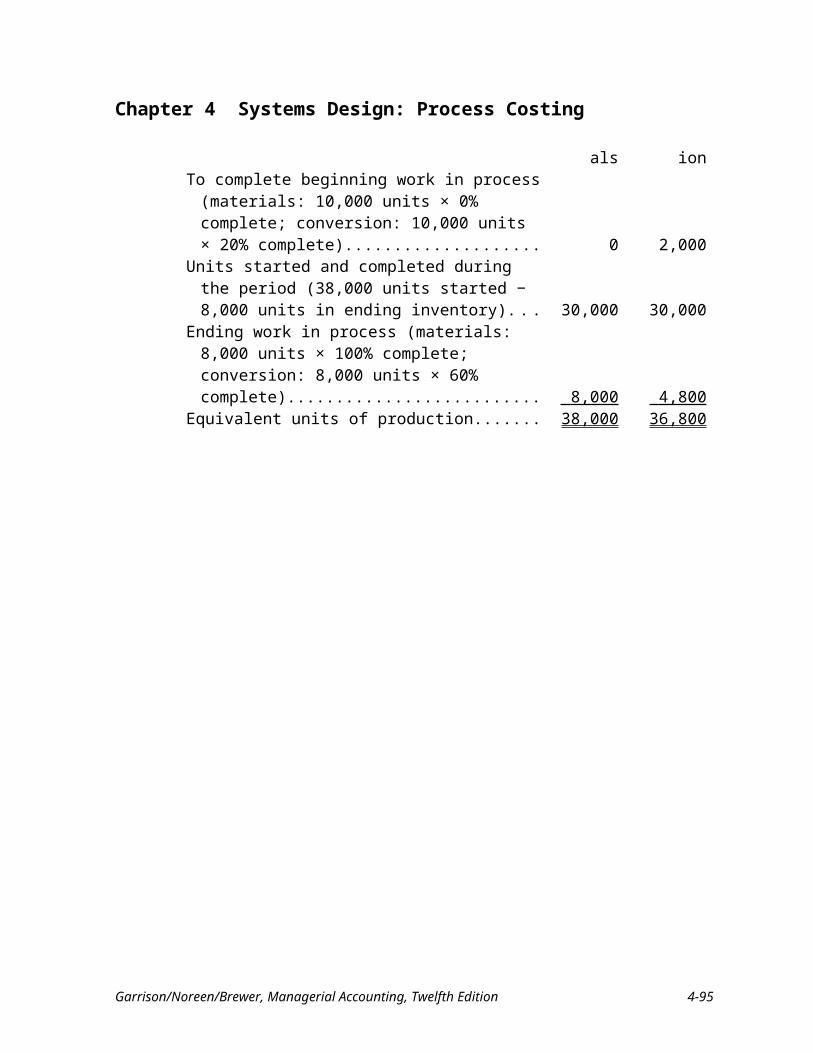

Chapter 4 Systems Design: Process Costing

69. Billings Company uses the FIFO method in its process costing system. On July 1, Department A had 10,000 units in process that were 80% complete with respect to conversion. On July 31 the department had 8,000 units in process that were 60% complete with respect to conversion. The department transferred 40,000 units out during the month, of which 10,000 units came from the beginning work in process inventory, and 30,000 units were started and completed during the month. All materials are added at the beginning of the process in Department A. What are the equivalent units for the month for materials and conversion, respectively?A) 38,000 units, and 36,800 unitsB) 38,000 units, and 38,000 unitsC) 48,000 units, and 44,800 unitsD) 48,000 units, and 48,000 units

Ans: A AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Reporting Appendix: 4A LO: 5 Level: Medium Source: CMA, adapted

Solution:

To solve for units started into production:+ Work in process, ending..................................................... 8,000+ Units completed and transferred out during the month...... 40,000− Work in process, beginning................................................ 10,000= Units started into production during the month.................. 38,000

Equivalent Units of ProductionMaterials Conversion

To complete beginning work in process (materials: 10,000 units × 0% complete; conversion: 10,000 units × 20% complete)................................................. 0 2,000

Units started and completed during the period (38,000 units started − 8,000 units in ending inventory).......... 30,000 30,000

Ending work in process (materials: 8,000 units × 100% complete; conversion: 8,000 units × 60% complete). . 8,000 4,800

Equivalent units of production........................................ 38,000 36,800

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 4-59

Chapter 4 Systems Design: Process Costing