Embed Size (px)

Citation preview

Change of Time Methods

in

Quantitative Finance

Anatoliy SwishchukUniversity of Calgary

Department of Mathematics & Statistic2500 University Drive NW

Calgary, AB,Canada T2N 1N4

Preface

”Time changes everything except something within us, which is alwayssurprised, by change”, -Thomas Hardy.

The present book is devoted to the history of change of time methods(CTM), connection of CTM with stochastic volatilities and finance, and manyapplications of CTM. A reader may consider this book as a brief introductionto the theory of CTM and as a handbook that can be used to apply tomany real life problems. As Winston Churchill once said, ’...I only readfor pleasure or for profit,’ similarly, someone may read the present book forpleasure, someone for profit (but see disclaimer below!) and many for both.The author’s intension was to satisfy all the readers who like change of timemethods, stochastic volatilities and finance. There is one book that the mostclose to the present book-’Change of Time and Change of Measure’ by O.Barndorff-Nielsen and A. Shiryaev (Springer, 2010). The difference betweenthe present book and the latter book is that the present book focuses moreon applications and presents some novel models, e.g., the delayed versionof Heston model, that not covered by the monograph of Barndorff-Nielsenand Shiryaev. For some extent, someone may consider the present book as auseful complement to the latter monograph. I hope that the present book willattract a wide audience from graduate students and quants to researchers inmathematical finance, and also to practicioners in finance and energy areas.

Anatoliy SwishchukUniversity of CalgaryCalgary, Alberta, CanadaAugust 2015

Disclaimer

We make no warranties that the approaches contained in this book are free oferror or that they will meet your requirements for any particular application.They should not be relied on for solving a problem, using these approaches,whose incorrect solution could result in loss of money or property. If you douse the approaches, it is at your own risk. The author and publisher disclaimall liability for direct or consequencial damages resulting from your use of theapproaches.

Dedication

To my late parents

Achowledgements

I would like to thank very much to many of my colleagues and graduatestudents, with whom I duscussed or obtained some results presented in thebook, and also to all the participants of the ’Lunch at the Lab’ finance semi-nar at our Department of Mathematics and Statistics, University of Calgary,where all the results were first presented and tested.

Many thanks go to my family, wife Mariya, son Victor and daughter Julia(who found and recommended the picture in the Preface), whose continuoussupport encouraged me on writing and creating.

Chapter 1: Introduction to the Change of Time

Methods: History, Stochastic Volatility, Fi-

nance

”Both Aristotle and Newton believed in absolute time...Time was completelyseparate from and independent of space...However, we have had to change ourideas about space and time...”-Stephen Hawking ’A Brief History of Time’

1 Introduction to the Change of Time Meth-

ods

In this Chapter, we consider a history for the change of time methods (CTM),connection of CTM with finance and stochastic volatilities.

Let (Ω,F ,Ft, P ) be a filtered probability space, t ≥ 0. We shall frequentlyuse in this book the notion of: 1) Brownian motion Bt (or Wiener processWt): a process with independent Gaussian (normal) increments and con-tinuous trajectories (A. Einstein (1905) used it when analysing the chaoticmotion of particles in a liquid); 2) stochastic differential equation dXt =a(Xt, t)dt + σ(Xt, t)dBt (describing diffusion process Xt with drift a anddiffusion σ) with local Lipschitz and linear growth conditions for the coeffi-cients a and σ; 3) martingale Mt (stochastic model for fair game), meaningE|Mt| < +∞ and E(Mt|Fs) = Ms, s ≤ t, where Mt is a stochastic process onthe above mentioned filtered probability space; 4) Levy process Lt (processthat contains deterministic drift, diffusion and jumps) (i.e., stochasticallycontinuous process with stationary and independent increments) (see, e.g.,Jacod & Shiryaev (1987), Applebaum (2003)).

The main idea of change of time method is to find a simple representationfor a stochastic process with a complicated structure, using some simpleprocess and change of time process. For example, if we consider a Brownianmotion Bt (or Levy process Lt) as a simple process and Xt as a complicatedprocess, that satisfies the following stochastic differential equation dXt =a(Xt, t)dt + σ(Xt, t)dBt (or dXt = a(Xt, t)dt + σ(Xt, t)dLt) on the latterfiltered probability space, then the question is: can we represent Xt in thefollowing form

Xt = BTt , (or Xt = LTt)

where Tt is a change of time process? In many cases, the answer is ’yes’.In this book, we shall show you those cases and many applications of them.In general, the procedure of change of time means that we proceed from old(or physical, calendar) time t to a new (operational, business) time t′ witht′ = Tt in a such way to be able to construct our initial complicated processXt (old one) through a simple process Xt (new one) that satisfies the relationXt = XTt . If we define t = T ′

t , then Xt′ = XT ′t, t′ > 0.

1

1.1 A Brief History of Change of Time Method

To the best of the author’s knowledge, Wolfgang Doeblin (see Doeblin W.(1940), Levy (1955), Lindvall (1991) and also Bru and Yor (2002) for details)was the first one who introduced change of time method into the theory ofstochastic processes. He took the martingale point of view in his analysisof the paths of an inhomogeneous real-valued diffusion Xt, t ≥ 0, startingfrom x, with drift coefficient a(x, t) and diffusion coefficient σ(x, t). If wedefine Yt := Xt − x−

∫ t0a(Xs, s)ds and ht :=

∫ t0σ2(Xs, s)ds, then he proved

first that Yt and Y 2t − ht are martingales without mentioning the notion

of martingale (see Doeblin (1940)). Secondly, Doeblin introduced the timechange θ(τ) := inft : mt > τ, τ > 0 and showed that B(τ) := Yθ(τ) isa Brownian motion. In fact, he proved that there exists a Brownian motionB(s), s ≥ 0, such that Yt := B(ht). All in all, Doeblin has obtained therepresentation of Xt as

Xt = x+B(ht) +

∫ t

0

a(Xs, s)ds. (1)

Of course, at that time the general notion of martingale did not exist (seefor more details Bru and Yor (2002)). The notion of positive martingale andits denomination (which Doeblin does not use) are due to Ville, in his 1939thesis (see Ville (1939)) (martingale property was also used by Levy underanother name, ’condition C’, since 1934). A several years later, K. Ito (1942a,1942b (see also Ito (1951a, 1951b)) presented Xt in the form of stochasticdifferential equation

Xt = x+

∫ t

0

a(Xs, s)ds+

∫ t

0

σ(Xs, s)dB(s), (2)

where B(s) is a Brownian motion. If we compare Doeblin’s and Ito’s repre-sentaions (1) and (2), then we can obtain∫ t

0

σ(Xs, s)ds = B(ht). (3)

The latter result (3) would be understood, of course, in a general settingmany years later with the Dambis (1965) and Dubins-Schwartz (1965) rep-resentation of a continuouus martingale Mt as

Mt = B(< M >t), (4)

where B(u) is a Browinian motion and < . > is the quadratic variation. Theidea of associating with a diffusion Xt a compensated process Yt which followsthe trajectories of a standard Brownian motion is presented in the works ofLevy on additive processes (see Levy (1934, 1937, 1948)) and in the seminalpaper of Kolmogorov (1931). However, as Bru and Yor (2002) mentioned,”Doeblin’s method goes much further and the change of time which he adopts

2

seems to be original.It is usually attributed to Volkonskii (1958); see e.g.Dynkin (1965); Williams (1979). In any case, there does not seem to bemuch use for random time-changes in the study of diffusion before the endof the fifties”. Though, we would like to mention that Bochner (1949) alsoused the notion of ’change of time’, namely, time-changed Brownian motion,before the beginning of fifties.

Girsanov (1960) used change of time method to find a nontrivial weaksolution to the following stochastic differential equation dXt = |Xt|αdBt,where X0 = 0, Bt is a Brownian motion and 0 < α < 1/2.

It worth to mention here that the change of time method is closely asso-ciated with the embedding problem: to embed a process X(t) in Brownianmotion is to find a Brownian motion (or Wiener process) B(t) and an in-creasing family of stopping times Tt such that B(Tt) has the same jointdistribution as X(t). Skorokhod (1965) first treated the embedding problem,showing that the sum of any sequence of independent random variables withmean zero and finite variation could be embedded in Brownian motion usingstopping times. See also Monroe (1972).

Dambis (1965), Dubins & Schwartz (1965) independently showed thatevery continuous martingale could be embedded in Brownian motion (inthe sense of (4) above). Feller (1936, 1966) introduced subordinated pro-cess X(Tt) for a Markov process X(t) with Tt a process having indepen-dent increments. Tt was called ’randomized operational time’. Huff (1969)showed that every process of pathwise bounded variation could be embed-ded in Brownian motion. Knight (1971) discovered a multivariate extensionof the Dambis (1965) and Dubins & Schwartz (1965) result. Monroe (1972)proved that every right continuous martingale could be embedded in a Brow-nian motion. Meyer (1971) and Papangelou (1972) independently discoveredKnight’s (1971) result for point processes.

Clark (1973) introduced change of time method into financial economics.Monroe (1978) proved that a process can be embedded in Brownian motionif and only if this process is a local semimartingale. Johnson (1979) intro-duced a time-changed stochastic volatility model in continuous time. Ikeda& Watanabe (1981) introduced and studied the change of time to find thesolutions of stochastic differential equations. Rosinski & Woyczynski (1986)considered time changes for integrals over a stable Levy processes. Levyprocesses can also be used as a time change for other Levy processes (sub-ordinators). Johnson & Shanno (1987) studied pricing of options using atime-changed stochastic volatility model.

Madan & Seneta (1990) introduced variance gamma process (i.e., Brown-ian motion with drift time changed by a gamma process). Kallsen & Shiryaev(2001) showed that the Rosinski-Woyczynski-Kallenberg result can not be ex-tended to any other Levy processes other than the symmetric α-stable pro-cesses.Kallenberg (1992) considered time change representations for stableintegrals. Geman, Madan & Yor (2001) considered time changes (’businesstimes’) for Levy processes .

3

Barndorff-Nielsen, Nicolato & Shephard (2002) studied the relationshipbetween subordination and stochastic volatility models using a change of time(they called it the Tt-’chronometer’). Carr, Geman, Madan, Yor (2003) usedsubordinated processes to construct stochastic volatility for Levy processes,(Tt being ’business time’).

Carr, Geman, Madan & Yor (2003) also used a change of time to introducestochastic volatility into a Levy model to achieve leverage effect and a long-term skew.

Swishchuk (2004) applied change of time method for pricing varinace,volatility, covariance and correlation swaps for Heston model. Change oftime method was applied to option pricing for mean-reverting models inenergy markets in Swishchuk (2008b). Pricing of Levy-based interest ratederivatives based on change of time method was considered in Swishchuk(2008a). An overview of change of time method in mathematical finance andits applications was presented in Swishchuk (2007). Applications of changeof time method to multi-factor Levy-based model for pricing of financial anaenergy derivatives was considered in Swishchuk (2009).

The book ’Option Prices as Probabilities’ by C. Profeta, B. Roynette andM. Yor (Springer, 2010) is also relies on time change methods.

The recent book ’Change of Time and Change of Measure’ by Barndorff-Nielsen and Shiryaev (2010) states the main ideas and results of the stochastictheory of ’change of time and change of measure’.

1.2 Change of Time Method and Stochastic Volatility

The volatility is a measure for variation of price St of a financial instrumentover time t ≥ 0. We use the symbol σ for volatility and it corresponds tostandard deviation which quantifies the amount of variation or dispersionof a set of data values St. Of course, σ can be positive constant, positivedeterministic function of time σ(t) or a stochastic process σ(t, ω), ω ∈ Ω, e.g.,that satisfies some stochastic differential equation. The model for volatilitythat initiated the stochastic volatility model was implied volatility model:this volatility σ ≡ σ(K,T ) can be derived from the Black-Scholes formulafor the European call option price and demonstrates the smile effect, e.g.,dependency of volatility from strike price K and maturity T (see Fouque,Papanicolaou and Sircar (2000)). This smile effect tells us that the Balck-Scholes model with a constant volatility is not adequate to statistical andprobabilitical structures of observable prices St. Merton (1973) was the firstone who replaced the constant volatility σ by a deterministic function σ =σ(t), t ≥ 0. In such models there is no smile effect across strike, howeversmile effect appears for different maturiries. Another way to obtain smileeffect with nonstochastic volatility is to add to the deterministic volatilityσ(t) one more variable, namely, phase one, S : σ ≡ σ(t, S) (see Dupire(1994)). We can go further and assume that volatility depends not onlyfrom t and S, but also on all proceding values Su, u ≤ t, i.e., the volatility

4

σ(t, Su;u ≤ t)) depends on all past observed prices, or volatility dependson its own past values. The latter case will be considered in Chapter 8.Besides smile effect, mean reversion (i.e., returning of the volatility to themean) is another important property of stochastic volatility. That’s why mostof modern models of stochastic volatility are assumed that the volatility isgenerated by another source of randomness than initial Brownian motion Bt,say by process Yt, which correlates with Bt, and this process follows somemean-reversion process, say, Ornstein-Uhlenbeck or CIR process (see Contand Tankov (2004)).

The connection of change of time with stochastic volatility can be de-scribed by the following representation: Xt = XT (t) =

∫ t0σ(s, ω)dXs, where

Xt is a given process, σ(t, ω) is a stochastic volatility, Xt is a simple initialprocess and T (t) is a change of time process. In many cases in finance, theprocess Xt is a Brownian motion or Levy process. In general case, the processXt is a semimartingale, meaning Xt = X0 +At+Mt, where At is a process ofbounded variation and Mt is a local martingale (see, e.g., Barndorff-Nielsenand Shiryaev (2010)).

The most typical example of this connection between change of timeand stochastic volatility is the following one. Let Mt =

∫ t0σ(s, ω)dBs, t ≥

0, where Bs is a Brownian motion, σ(s, ω) is a positive process such that∫ t0σ2sds < +∞. Then Mt can be presented in the following way:

Mt = BTt ,

where Tt :=∫σ2sds, Bt := MTt

, and Tt = infs :∫ s0σ2udu ≥ t. We note that

Bt := MTtis a Brownian motion with respect to the filtration Ft := FTt .

Another interesting example associated with the α-stable processes Lαs , 0 <α ≤ 2 (see Applebaum (2003)). LetXt =

∫ t0σ(s, ω)dLαs , T (t) :=

∫ t0|σ(s, ω)|αds <

+∞, and Tt = infs ≥ 0 : Ts > t. Then

Lαt := XTt, t ≥ 0,

is an α-stable process. The proof follows from the Doob optional samplingtheorem and the characteristic property of semimartingales (see Jacod &Shiryaev (1987)). We note that processXt can be represented through changeof time in the following way:

Xt = LαTt .

We shall use this approach in Chapters 6 and 7 for Levy-based and multi-factor financial models.

It is worth to mention that the only change of time process Tt that re-tains the Gaussian property of the time changed Brownian motion BTt isdetrministic one.

The probability literature has demonstrated that stochastic volatilitymodels and their time-changed Brownian motion relatives are fundamental(see Shephard (2005a, 2005b)).

5

1.3 Change of Time Method and Finance

The change of time method in finance is related directly to the notion ofvolatility, the measure for variation of price of a financial instrument (stock,etc.) over time t ≥ 0. Often the change of time is called an ’operational time’(the term first coined by Felller (1966)) or ’business time’ (Carr, Madan &Yor (2001)). This time measures the intensity of the variations/fluctuationsof the prices in the financial markets. The notion of change of time is veryimportant in finance because many prices in the financial markets can beexpressed in the form of Brownian motion with the changed time, called theoperational or business time.

The role of Brownian motion in finance is also hard to underestimate:besides its important role in probability and stochastic processes (centrallimit theorem, functional limit theorem and so-called time-changed Brownianmotion processes), it was the main component in modeling of the dynamicsof financial asset prices St, t ≥ 0. We would like to mention Bachelier model(1900) St = S0 +µt+σBt and Samuelson model (1965) log St

S0= µt+σBt for

asset prices St, where Bt is a Brownian motion. Another important processin finance is Poisson process, antipode to Brownian motion, which was firstused by Lundberg (1903) to model the dynamics of the capital of insurancecompanies.

Both Brownian motion and Poisson process are main components in con-structing more general class of processes in finance and insurance, Levy pro-cesses (see Levy (1934, 1935, 1937, 1954), Applebaum (2003)). To go fur-ther, we mention that even more general processes recently have been usedto construct many financial and insurance model, namely, processes with in-dependent increments and semimartingales (see Shiryaev (2008)). The latterprocesses are not necessarily homogeneus as in the case of Levy processes.As we can see later, we can obtain these kind of processes in finance if weconsider Bachelier (1903) and Samuelson (1965) models, mentioned above, inchange of time mode, namely, St = S0+µT (t)+σBTt and log St

S0= µTt+σBTt ,

respectively, where Tt is a change time process. Another important examplein finance can be constructed if we take gamma process Tt and a Brown-ian motion B(t), independent of each other, and then form a new processG(t) such that G(t) = µt + βTt + BTt . This process is called the variancegamma process (or VG process) (see Madan & Seneta (1990)). To catchthe leverage and clustering effects, other models of stock prices in financecan be obtained using, for example, exponential Levy models that includeboth stochastic volatility and change of time, and also the models based onfractional Brownian motion (see Barndorff-Nielsen and Shiryaev (2010)).

Many stochastic differential equations, that practicioners use in finance,can be solved using chnage of time method as well. One of such equations isOrnstein-Uhlenbeck equation (see Ornstein & Uhlenbeck (1930)) (we presentthis equation in general form):

dXt = (a(t)− b(t)Xt)dt+ c(t)dW (t),

6

where W (t) is a Wiener process (or Brownian motion) and a, b, c are deter-ministic functions of time t ≥ 0. The solution of this equation is:

Xt = exp(−∫ t

0

b(s)ds)[X0+

∫ t

0

a(s) exp(

∫ s

0

b(u)du)ds+

∫ t

0

c(s) exp(

∫ s

0

b(u)du)dWs].

The solution of this equation can also be presented in the following form,using chnage of time method (see Swishchuk (2007) and Ikeda & Watanabe(1981)):

Xt = exp(−∫ t

0

b(s)ds)[X0 +

∫ t

0

a(s) exp(

∫ s

0

b(u)du)ds+BTt ],

where Tt =∫ t0(c(s)) exp(

∫ s0b(u)du))2ds-change of time process, and Bt is a

new Brownian motion. The latter Brownian motion can be obtained fromthe previous one, W (t), by the following formulae:

Bt :=

∫ Tt

0

c(s) exp(

∫ s

0

b(u)du)dW (s),

where Tt = infs : Ts > t, where Tt is defined above.We shall use this approach in the next Chapter 2 to find the solutions of

many stochastic differential equations.

2 Structure of the Book

Chapter 2 is devoted to the general theory of change of time method andmany approaches in this field.

Chapter 3 gives yet one more derivation (among many others) of Black-Scholes option pricing formula using change of time method. In this chapterwe also present a brief introduction to the option pricing theory.

Chapter 4 models and prices variance, volatility, covariance and corre-lation swaps for classical Heston model of a stock price. We also give anumerical example based on S&P60 Canada Index.

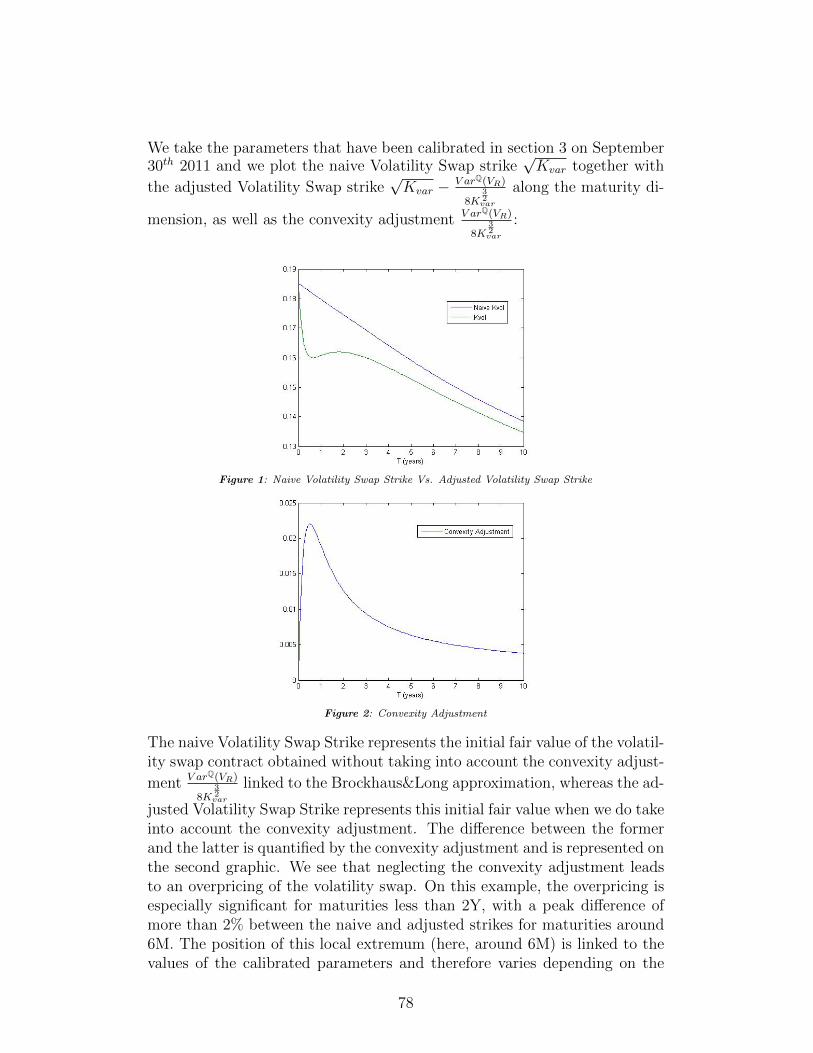

Chapter 5 introduces a new delayed Heston model for pricing of varianceand volatility swaps, and also for hedging volatility swaps using varianceswaps. We use here change of time method as well, and also calibrate all theparameters based on real data. This model improves the market volatilitysurface fitting by 44% compare with classical Heston model.

Chapters 6 introduces multi-factor Levy-based financial and energy mod-els. Change of time method is used to price many financial and energyderivatives.

Chapter 7 deals with explicit option pricing formula for a mean-revertingasset in energy markets using change of time method. We also present herea numerical example for AECO natural gas index.

7

Finally, Chapter 8 deals with variance and volatility swpas in energymarkets using CTM as well.

All chapters contain their own list of References.Warning!: We note that we use throughout the book two notations for

the change of time process, namely, Tt and φt, with respect to Barndorff-Nielsen and Shiryaev’s and Ikeda and Wananabe’s books. For example, inChapters 1,2 and 7 we use Tt and in Chapters 3-5 and 8 we use φt.

3 References

Applebaum, D. Levy Processes and Stochastic Calculus, Cambridge Uni-versity Press, 2003.

Bachelier, L. Theorie de la speculation. Ann. Ecole Norm. Sup. 17,(1900), 21-86.

Barndorff-Nielsen, O.E., Nicolato, E. and Shephard, N. Some recent de-velopment in stochastic volatility modeling, Quantitative Finance, 2, 11-23,2002.

Barndorff-Nielsen, O. E. and Shiryaev, A. N. Change of Time and Changeof Measure. World Scientific. Singapore, 2010, 305 p..

Bochner, S. Diffusion equation and stochastic processes. Proc. Nat.Acad. Sci. USA, 85, 369-370, 1949.

Bru, B. and Yor, M. Comments on the life and mathematical legacy ofWolfgang Doeblin. Finance and Stochastics, 6, 3-47 (2002).

Carr, P., Geman, H., Madan, D. and Yor, M. Stochastic volatility for Levyprocesses.// Mathematical Finance, vol. 13, No. 3 (July 2003), 345-382.

Clark, P. A subordinated stochastic process model with fixed variance forspeculative prices, Econometrica, 41, 135-156, 1973.

Cont, R. and Tankov, P. Financial Modeling with Jump Processes, Chap-man & Hall/CRC Fin. Math. Series, 2004.

Dambis, K.E. On the decomposition of continuous submartingales, The-ory Probabability and its Appl., 10, 4091-410, 1965.

Doeblin, W. Sur l’equation de Kolmogoroff. Pli cachete depose le 26fevrier 1940, ouvert le 18 mai 2000. C.R. Acad. Sci. Paris, Series I, 331,1031-1187 (2000).

Dubins, L. and Schwartz, G. On continuous martingales, Proc. Nat.Acad. Sciences, USA, 53, 913-916, 1965.

Dupire, B. Pricing with a smile. Risk, 7,1, 18-20 (1994).Dynkin, E. B. Markov Processes. vol. 2. Berlin-Heidelberg-New York:

Springer, 1965.Einstein, A. Uber die von der molekularkinetischen Theorie der Warme

geforderte Bewegung von in rehunden Flussigkeiten suspendierten Teilchen,Ann. Phys. (4) 17, 549-560 (1905).

8

Feller, W. Zur der stochastischen prozesse (Existenz-und Eindeutigkeitssatze).Math. Ann., 113, 113-160 (1936).

Feller, W. Introduction to Probability Theory and its Applications, v. II,Wiley & Sons, 1966.

Fouque, J.-P., Papanicolaou, G. and Sircar, K. R. Derivatives in FinancialMarkets with Stochastic Volatilities. Springer-Verlag, 2000.

Geman, H., Madan, D. and Yor, M. Time changes for Levy processes,Math. Finance, 11, 79-96 (2001).

Girsanov, I. On transforming a certain class of stochastic processes by ab-solutely continuous subtitution of measures. Theory Probab. Appl., 5(1960),3, 285-301.

Heston, S. A closed-form solution for options with stochastic volatilitywith applications to bond and currency options, Review of Financial Studies,6, 327-343, 1993.

Huff, B. The loose subordination of differential processes to Brownianmotion, Ann. Math. Statist., 40, 1603-1609.

Ikeda, N. Watanabe, S. Stochastic Differential Equations and DiffusionProcesses. North-Holland/Kodansha Ltd., Tokyo, 1981.

Ito, K. Differential equations determining a Markoff proces.. J. Pan-JapanMath. Colloq. 1077, 1352-1400 (in Japanese) (1942a).

Ito, K. On stochastic processes (I) (Infinitely divisible laws of probability).Japan J. Math. 18, 261-301 (1942b)

Ito, K. On stochastic differential equations. Mem. Amer. Math. Soc., 4(1951a).

Ito, K. On a formula concerning stochastic differentials. Nagoya Math.J., 3, 55-65 (1951b).

Jacod, J. and Shiryaev, A. Limit Theorems for Stochastic Processes.Springer-Verlag, 1987.

Johnson, H. Option pricing when the variance rate is changing. Workingpaper, University of california, Los Angeles, 1979.

Johnson, H. and Shanno, D. Option pricing when the variance is changing,J. Financial Quant. Anal., 22, 143-152 (1987).

Kallenberg, O. Some time change representations of stable integrals, viapredictable transformations of local martingales. Stochastic Processes andTheir Applications, 40 (1992), 199-223.

Kallsen, J. and Shiryaev, A. Time change representation of stochasticintegrals, Theory Probab. Appl., vol. 46, N. 3, 522-528, 2002.

Khinchin A. Y. Asymptotische gesetze der Warsheinlichkeitsrechnung.Berlin-Heidelberg-New York: Springer, 1933 (Ergebnisse der Mathematikund ihrer Grenzgebiete, vol. 2, no. 4) (Reprint, New York: Chelsea, 1948).

Knight, F. A reduction of continuous, square-integrable martingales toBrownian motion, in: H. Dinges, ed., Martingales, Lecture Notes in Math.No. 190 (Springer, Berlin, 1971) pp. 19-31.

Kolmogorov A. N. Uber die analytischen methoden in der Wahrschein-lichkeitsrechnung. Math. Ann., 104, 149-160 (1931).

9

Levy, P. Sur les integrals dont les elements sont des variables aleatoiresindependentes. Ann. J. Sc. Norm. Sup. Pisa S. 2 (3), 337-366 (1934), 4,217-218 (1935).

Levy, P. Theorie de l’addition des variables aleatoires, Paris: Gauthier-Villars, 1937 (2nd edn. ibid, 1954).

Levy, P. Processus Stochastiques et Mouvement Brownian, 2nd ed., Gauthier-Villars, Paris, 1948 (2nd edn. ibid, 1954).

Levy, P. Wolfgang Doeblin (V. Doblin)(1915-1940). Rev. Histoire Sci.107-115 (1955).

Lindvall, T. W. Doeblin 1915-1940. Ann. Prob., 19, 929-934 (1991).Lundberg, F. Approximerad Framstallning Sannolikhetsfunktionen. II.

Aterforrsakering av Kolletivrisker. Akad. Afhandling. (Almqvist&Wiksell,Uppsala), (1903)

Madan, D. and Seneta, E. The variance gamma (VG) model for sharemarket returns, J. Business 63, 511-524, (1990).

Merton, R. Theory of rational option pricing. Bell J. Econ. and Man-agement Sci., 4, 141-183 (1973).

Meyer, P. A. Demonstration simplifiee d’un theoreme de Knight, in: Sem-inaire de Probabilites V, Lecture Notes in Math. No. 191 (Springer, Berlin,1971) pp. 191-195.

Monroe, I. On embedding right continuous martingales in Brownian mo-tion, Ann. Math. Statist., 43, 1293-1311, 1972.

Monroe, I. Processes that can be embedded in Brownian motion, TheAnnals of Probab., 6, No. 1, 42-56, 1978.

Ornstein, L. and G.Uhlenbeck. On the theory of Brownian motion. Phys-ical Review, 36 (1930), 823-841.

Papangelou, F. Integrability of expected increments of point processesand a related random change of scale, Trans. Amer. Math. Soc., 165 (1972)486-506.

Profeta, B., Roynette, B. and Yor, M. Option Prices as Probabilities.Springer-Verlag, Berlin-Hedelberg, 2010.

Rosinski, J. and Woyczinski, W. On Ito stochastic integration with re-spect to p-stable motion: Inner clock, intagrability of sample paths, doubleand multiple integrals, Ann. Probab., 14 (1986), 271-286

Samuelson, P. Rational theory of warrant pricing. Industrial ManagementRev., 6, (1965), 13-31.

Shephard, N. Stochastic Volatility: Selected Readings. Oxford: OxfordUniversity Press, 2005a.

Shephard, N. Stochastic Volatility. Working paper, Oxford: Oxford Uni-versity Press, 2005b.

Shiryaev, A. Essentials of Stochastic Finance, World Scientific, 2008.Skorokhod, A. Random Processes with Independent Increments, Nauka,

Moscow, 1964. (English translation: Kluwer AP, 1991).Skorokhod, A. Studies in the Theory of Random Processes, Addison-

Wesley, Reading, 1965.

10

Swishchuk, A. Modelling and valuing of variance and volatility swaps forfinancial markets with stochastic volatilites, Wilmott Magazine, TechnicalArticle, N0. 2, September, 2004, 64-72.

Swishchuk, A. Change of time method in mathematical finance, Canad.Appl. Math. Quart., vol. 15, No. 3, 2007, 299-336.

Swishchuk, A. Levy-based interest rate derivatives: change of time andPIDEs, Canad. Appl. Math. Quart., v. 16. No. 2, 2008a.

Swishchuk, A. Explicit option pricing formula for a mean-reverting assetin energy market, J. of Numer. Appl. Math., Vol. 1(96), 2008b, 216-233.

Swishchuk, A. Multi-factor Levy models for pricing of financial and energyderivatives, Canad. Appl. Math. Quart., v. 17, N0. 4, 2009.

Ville, J. Etude critique de la notion de collectif, These sci. math. Paris,(fascicule III de la Collection de monographies des probabilites, publiee sousla direction de M. Emile Borel). Paris: Gautier-Villars, 1939.

Volkonskii, V. A. Random substitution of time in strong Markov pro-cesses. Teor. Veroyatnost. i Primenen., 3, 332-350 (1958).

Williams, D. Diffusion, Markov Processes and Martingales I. Fiundations.New York, Wiley, 1979.

11

Chapter 2: Change of Time Methods: Defini-

tions, Theory and Applications

’It is always more easy to discover and proclaim general principles than toapply them’,-Winston Churchill.

1 Change of Time Methods: Definitions, Prop-

erties and Theory

In this Chapter, we consider a general theory of change of time method.One of probabilistic methods which is useful in solving stochastic differentialequations (SDEs) arising in finance is the change of time method. In thisIntroduction we give definition of CT, describe CTM in martingale, semi-martingale and the SDEs settings. We also point out the association ofCTM with subordinators and stochastic volatilities. Applications of CTMsuch as Black-Scholes formula, option pricing formula for a mean-revertingasset, variance and volatility swap prices for Heston and delayed Heston mod-els, and variance and volatility swap prices in energy markets are describedas well.

1.1 Change of Time Process: Definition and Proper-ties

Let (Ω,F ,Ft, P ) be a filtered probability space with a sample space Ω, σ-algebra F of subsets of Ω and probability measure P. The filtration Ft, t ≥0, is a nondecreasing right-continuous family of sub-σ-algebras of F .

Definition of Change of Time Process. A time change process is aright-continuous increasing [0,+∞]-valued and Ft-adapted process (Tt)t∈R+

such that limt→+∞ = +∞. Tt is also a stopping time for any t ∈ R+.By Ft := FTt we define the time-changed filtration (Ft)t∈R+ . The inverse

time change (Tt)t∈R+ is defined as Tt := infs ∈ R+ : Ts > t. We note

that Tt is increasing process and limt→+∞ Tt = +∞. Furthermore, Tt is anFt-stopping time. Let Xt be an Ft-adapted process and define XTt

. Then

XTtis Ft-adapted process and this process is called the time change of Xt

by Tt.One of the examples of change of time is the following. Let At be an Ft-

adapted, increasing, right-continuous random process with A0 = 0. Define

Tt = infs : As > t, t ≥ 0.

Then the process Tt is a change of time process. We call At as the processgenerating the change of time Tt. We note that the process Tt (see abovedefinition) coincides with At in this case. It means that changes of time

12

processes Tt and Tt are mutually inverse processes: someone may constructTt using Tt,

Tt = infs : Ts > t,or, may construct Tt using Tt :

Tt = infs : Ts > t.We also note that

TTt = t and TTt = t.

We would like to also mention the change of time in Lebesque-Stiltjes inte-grals, which is well-known from calculus. If we take At, A0 = 0, as a deter-ministic increasing continuous function, f(t) as a nonnegative Borel functionon [0,+∞), and put

At = infs : As > t,then we have ∫ Aa

0

f(t)dAt =

∫ a

0

f(At)dt, a > 0.

We note that At =∫s : As > t and AAt

= t. The latter expression can bewritten in the symmetric form as well:∫ Aa

0

f(t)dAt =

∫ a

0

f(At)dt, a > 0.

There are many stochastic generalizations of the last two relationships for thecase of A and f being some stochastic processes. One of them is the folllowingone: let f(t, ω) be a progressively measurable nonegative stochastic process,and let Bt(ω) be an Ft-measurable right-continuous process with boundedvariation. Then ∫ Ta

0

f(t, ω)dBt(ω) =

∫ a

0

f(Tt, ω)dBTt(ω),

where Tt is the inverse change of time process. For example, if f(t, ω) =F (T (t)), where Tt = At, and At is a continuous and strictly increasing processgenerating the change of time Tt (see above), then∫ Ta

0

F (Tt)dBt(ω) =

∫ a

0

F (t)dBTt(ω).

Of course, if Bt = t, then∫ Ta

0

F (Tt)dt =

∫ a

0

F (t)dTt,

and, if Bt = Tt, then ∫ Ta

0

F (Tt)dTt =

∫ a

0

F (t)dt.

See Ikeda and Watanabe (1981) and Barndorff-Nielsen and Shiryaev (2010)for more details.

13

1.2 CTM: Martingale and Semimartingale Settings

The general theory of time changes for martingale and semimartingale the-ories is well known (see Ikeda and Watanabe (1981)). We will give a briefoverview of those results.

The following result on martingales and change of time process belongsto Dambis (1965) and Dubins and Schwartz (1965): Suppose Mt is squareintegrable local continuous martingale such that limt→+∞ < M > (t) = +∞a.s., and define Tt := infu :< M >u> t and Ft = FTt . Then the time

changed process B(t) := MTtis an Ft-Brownian motion. Also, Mt = B(<

M >t). Thus, Mt can be presented by an Ft-Brownian motion B(t) andan Ft-stopping time < M >t . Here, < · > defines predictable quadraticvariation. One of the examples of this result was considered in section 1.2. fora continuous local martingale Mt =

∫ t0σs(ω)dB(s), where Bt is a Brownian

motion and σt(ω) is a positive process such that∫ t0σ2s(ω)ds < +∞. In tis

case, Tt = infs :∫ s0σ2u(ω)du ≥ t and Tt =

∫ t0σ2s(ω)ds.

This result was generalized by Knight (1971) for d-dimensional case: LetM i

t be square integrable local continuous martingales, i = 1, 2, ..., d, suchthat < M i,M j >t= 0 if i 6= j and limt→+∞ < M i >t= +∞ a.s. If T it =

infu :< M i >u> t, then ~B(t) = (B1(t), B2(t), ..., Bd(t)) is a d-dimensionalBrownian motion, where Bi(t) = M i

T it

, i = 1, 2, ..., d.

One of the main properties of semimartingale Xt with respect to the CTMis the following (see Liptser and Shiryaev (1989)): If Xt is a semimartingalewith respect to a filtration Ft, then the changed time process XTt

is also a

semimartingale with respect to the filtration Ft (see sec. 1.1).If we have the triplet of predictable characteristics (Bt, Ct, ν) for a semi-

martingale Xt, then the triplet of the time changed semimartingale XTtis

determined as (BTt, CTt , IGνTt) (see Kallsen and Shiryaev (2001)).

The connection of semimartingales, Brownian motions and CTM is de-scribed by the Monroe result (see Monroe (1978)): if Xt is a semimartingale,then there exists a filtered probability space with Brownian motion Bt anda change of time Tt on it such that distribution of Xt coincides with thedistribution of BTt , namely,

Xt =law BTt . (1)

Let us consider now a counting process Nt with respect to the filtrationFt and with the continuous compensator At such that Nt = At +Mt, whereMt is a local martingale. Here, < M >= A. Let us then define time changeas Tt = infs :< M >s> t. If we suppose that < M >+∞= +∞, then thefollowing process

Nt := NTt

is a standard Poisson process with the intensity parameter λ = 1. We notethat the initial counting process Nt can be expressed in the following way:

Nt = NTt ,

14

where Tt =< M >t . We note that here Mt = MTt , where Mt = Nt − t is aPoisson martingale (see Liptser and Shiryaev (2001) for more detauls).

Suppose that we have a nondecreasing Levy process Xt and a Brownianmotion Bt independent of Xt. Then we can find a change of timne Tt suchthat

Xt = BTt (2)

holds with probability one. This change of time Tt can be found as

Tt = infs : Bs = Xt.

We mention that a semimartingale Xt can be presented in the form (1) withcontinuous change of time Tt if and only if the process Xt is a continuouslocal martingale (see Huff (1969) and Cherny and Shiryaev (2002) for moredetails).

1.3 CTM: Subordinators and Stochastic Volatility

We note, that if the process Tt (see sec. 1.1) is a Levy process, then Tt iscalled subordinator. Feller (1966) introduced a subordinated process Xτt fora Markov process Xt and τt a process with independent increments. τt wascalled a ‘randomized operational time‘. Increasing Levy processes can alsobe used as a time change for other Levy processes (see Applebaum (2004),Barndorf-Nielsen et al. (2001), Barndorf-Nielsen et al. (2003), Bertoin(1996), Cont et al. (2004) and Schoutens (2003)). Levy processes of this kindare called subordinators. They are very important ingredients for buildingLevy based models in finance (see Cont et al. (2004) and Schoutens (2003)).If St is a subordinator, then its trajectories are almost surely increasing, andSt can be interpreted as a ‘time deformation‘ and used to ‘time change‘ otherLevy processes. Roughly, if (Xt)t≥0 is a Levy process and (St)t≥0 is a sub-ordinator independent of Xt, then the process (Yt)t≥0 defined by Yt := XSt

is a Levy process (see Cont et al. (2004)). This time scale has the finan-cial interpretation of business time (see Geman et. al. (2001)), that is, theintegrated rate of information arrival. Using subordinator St and a Brow-nian motion Bt that is independent of Stwe can construct many stochasticprocesses Xt = BSt . For example: for Cauchy process St = infs : Bs > t,where Bs is a standard Brownian motion independent of Bt; for generalizedhyperbolic Levy processes St is generated by the nonnegative infinitely divis-ible random variable having generalized inverse Gaussian distribution (thenormal inverse Gaussian and hyperbolic Levy processes are particular casesof the generalized hyperbolic Levy processes).

The time change method was used to introduce stochastic volatility into aLevy model to achieve the leverage effect and a long-term skew (see Carr et.al. (2003)). In the Bates (1996) model the leverage effect and long-term skewwere achieved using correlated sources of randomness in the price process and

15

the instantaneous volatility. The sources of randomness are thus required tobe Brownian motions. In the Barndorff-Nielsen et al. (2001, 2002) model theleverage effect and long-term skew are generated using the same jumps in theprice and volatility without a requirement for the sources of randomness to beBrownian motions. Another way to achieve the leverage effect and long-termskew is to make the volatility govern the time scale of the Levy process drivingjumps in the price. Carr et al. (2003) suggested the introduction of stochasticvolatility into an exponential-Levy model via a time change. The genericmodel here is St = exp(Xt) = exp(Yvt), where vt :=

∫ t0σ2sds. The volatility

process should be positive and mean-reverting (i.e., an Ornstein-Uhlenbeckor Cox-Ingersoll-Ross processes). Barndorff-Nielsen et al.(2003) reviewed andplaced in the context some of their recent work on stochastic volatility modelsincluding the relationship between subordination and stochastic volatility.

In general setting, the connection between stochastic volatility and changeof time can be described in the following way. Let Xt =

∫ t0HsdBs, where

Hs is the adapted process such that∫ t0H2sds < +∞,

∫ +∞0

H2sds = +∞, and

Bt is a Brownian motion. Then the process Bt := XTt, where Tt = infs :<

X >s> t, is a Brownian motion. Moreover, the process Xt has the followingrepresentation Xt = BTt , where Tt =< X >t=

∫ t0H2sds.

In the case of α-stable processes Y αt instead of Brownian motion Bt in the

integral Xt =∫ t0HsdY

αs , we have similar result for Tt =

∫ t0|Hs|αds < +∞

and∫ +∞0|Hs|αds = +∞. If we set Tt = infs : Ts >> t, then Y α

t = XTtis

an α-stable process and Xt = Y αTt.

The main difference between the change of time method and the sub-ordinator method is that in the former case the change of time process Ttdepends on the process Xt, but in the latter case, the subordinator St andLevy process Xt are independent.

1.4 CTM: Stochastic Differential Equations (SDEs) Set-ting

1.4.1 General Result

We consider the following generalization of the previous results to the SDEof the following form (without a drift)

(2.1) dX(t) = α(t,X(t))dW (t),

where W (t) is a Brownian motion and α(t,X) is a continuous and measurableby t and X function on [0,+∞)×R.

The reason to consider this equation is the following one: if we solve theequation, then we can solve and more general equation with a drift β(t,X)by drift transformation method or Girsanov transformation (see Ikeda andWatanabe (1981), Chapter 4, Section 4]).

16

Theorem 2.1. (Ikeda and Watanabe (1981), Chapter IV, Theorem 4.3)Let W (t) be an one-dimensional Ft-Wiener process with W (0) = 0, given ona probability space (Ω,F , (Ft)t≥0, P ) and let X(0) be an F0-adopted randomvariable. Define a continuous process V = V (t) by the equality

(2.2) V (t) = X(0) + W (t).

Let φt be the change of time process (see Section 2.3):

(2.3) Tt =

∫ t

0

α−2(Ts, X(0) + W (s))ds.

If

(2.4) X(t) := V (Tt) = X(0) + W (Tt)

and Ft := FTt , then there exists Ft-adopted Wiener process W = W (t) such

that (X(t),W (t)) is a solution of (1) on probability space (Ω,F , Ft, P ). Here,Tt is the inverse process to Tt in (2.3).

Proof of this Theorem may be found in Ikeda and Watanabe (1981),Chapter IV, Theorem 4.3.

We note that in this case,

(2.5) M(t) := W (Tt)

is a martingale with quadratic variation

(2.6) < M > (t) = Tt =

∫ Tt

0

α2(Ts, X)dTs =

∫ t

0

α(s,X)2ds,

and Tt satisfies the equation

(2.7) Tt =

∫ t

0

α2(s,X(0) + W (Ts))ds.

We also remark, that

(2.8) W (t) =

∫ t

0

α−1(s,X(s))dW (Ts) =

∫ t

0

α−1(s,X(s))dM(s)

and

X(t) = X(0) +

∫ t

0

α(s,X)dW (s).

17

1.4.2 Corollary.

The solution of the following SDE

(2.9) dX(t) = a(X(t))dW (t)

may be presented in the following form

X(t) = X(0) + W (Tt),

where a(X) is a continuous measurable function, W (t) is an one-dimensionalFt-Wiener process with W (0) = 0, given on a probability space (Ω,F , (Ft)t≥0, P )and let X(0) is an F0-adopted random variable. In this case,

(2.10) Tt =

∫ t

0

a−2(X(0) + W (s))ds,

and

(2.11) Tt =

∫ t

0

a2(X(0) + W (Ts))ds.

(See Ikeda and Watanabe (1981), Chapter IV, Example 4.2).We note that

M(t) := W (Tt)

is a martingale with quadratic variation

< M > (t) = Tt =

∫ Tt

0

a2(X)dTs =

∫ t

0

a(X)2ds.

We also remark, that

W (t) =

∫ t

0

a−1(X(s))dW (Ts) =

∫ t

0

a−1(X(0) + W (Ts)))dW (Ts)

and

X(t) = X(0) +

∫ t

0

a(X(s))dW (s).

1.4.3 One-factor Diffusion Models and their Solutions Using CTM

In this section, we introduce well-known one-factor diffusion models (usedin finance) described by SDEs and driven by a Brownian motion (so-calledGaussian models).

For one-factor Gaussian models we define the following well-known pro-cesses:

1. The Geometric Brownian Motion: dS(t) = µS(t)dt+ σS(t)dW (t);

18

2. The Continuous-Time GARCH Process: dS(t) = µ(b − S(t))dt +σS(t)dW (t);

3. The Ornstein-Uhlenbeck (1930) Process: dS(t) = −µS(t)dt+σdW (t);4. The Vasicek (1977) Process: dS(t) = µ(b− S(t))dt+ σdW (t);5. The Cox-Ingersoll-Ross (1985) Process: dS(t) = k(θ − S(t))dt +

γ√S(t)dW (t);6. The Ho and Lee (1986) Process: dS(t) = θ(t)dt+ σdW (t);7. The Hull and White (1990) Process: dS(t) = (a(t) − b(t)S(t))dt +

σ(t)dW (t);8. The Heath, Jarrow and Morton (1987) Process: Define the forward in-

terest rate f(t, s), for t ≤ s, characterized by the following equality P (t, u) =exp[−

∫ utf(t, s)ds] for any maturity u. f(t, s) represents the instantaneous

interest rate at time s as ‘anticipated‘ by the market at time t. It is naturalto set f(t, t) = r(t). The process f(t, u)0≤t≤u satisfies an equation

f(t, u) = f(0, u) +

∫ t

0

a(v, u)dv +

∫ t

0

b(f(v, u))dW (v),

where the processes a and b are continuous. We note that the last SDEmay be written in the following form: df(t, u) = b(f(t, u))(

∫ utb(f(t, s)))ds+

b(f(t, u))dW (t), where W (t) = W (t)−∫ t0q(s)ds and

q(t) =∫ utb(f(t, s))ds− a(t,u)

b(f(t,u)).

We use the change of time method to get the solutions of the above-mentioned SDEs.

W (t) below is an standard Brownian motion, and W (t) is a (Tt)t∈R+-

adapted standard Brownian motion on (Ω,F , (Ft)t∈R+ , P ). We use Tt and Ttnotations instead of φt and φ−1t , for time change and inverse time change,respectively.

1. The Geometric Brownian Motion: dS(t) = µS(t)dt + σS(t)dW (t).Solution S(t) = eµt[S(0) + W (Tt)], where Tt = σ2

∫ t0[S(0) + W (Ts)]

2ds.2. The Continuous-Time GARCH Process: dS(t) = µ(b − S(t))dt +

σS(t)dW (t). Solution S(t) = e−µt(S(0)−b+W (Tt))+b, where Tt = σ2∫ t0[S(0)−

b+ W (Ts) + eµsb)2ds.3. The Ornstein-Uhlenbeck Process: dS(t) = −µS(t)dt + σdW (t), Solu-

tion S(t) = e−µt[S(0) + W (Tt)], where Tt = σ2∫ t0(eµs[S(0) + W (Ts)])

2ds.4. The Vasicek Process: dS(t) = µ(b−S(t))dt+σdW (t), solution S(t) =

e−µt[S(0)− b+ W (Tt)], where Tt = σ2∫ t0(eµs[S(0)− b+ W (Ts)] + b)2ds.

5. The Cox-Ingersoll-Ross Process: dS2(t) = k(θ−S2(t))dt+γS(t)dW (t),solution S2(t) = e−kt[S2

0 − θ2 + W (Tt)] + θ2, where Tt = γ−2∫ t0[ekTs(S2

0 − θ2 +

W (s)) + θ2e2kTs ]−1ds.6. The Ho and Lee Process: dS(t) = θ(t)dt + σdW (t). Solution S(t) =

S(0) + W (σ2t) +∫ t0θ(s)ds.

7. The Hull and White Process: dS(t) = (a(t)− b(t)S(t))dt+σ(t)dW (t).

Solution S(t) = exp[−∫ t0b(s)ds][S(0)−a(s)

b(s)+W (Tt)], where Tt =

∫ t0σ2(s)[S(0)−

a(s)b(s)

+ W (Ts) + exp[∫ s0b(u)du]a(s)

b(s)]2ds.

19

8. The Heath, Jarrow and Morton Process: f(t, u) = f(0, u)+∫ t0a(v, u)dv+∫ t

0b(f(v, u))dW (v). Solution f(t, u) = f(0, u) + W (Tt) +

∫ t0a(v, u)dv, where

Tt =∫ t0b2(f(0, u) + W (Ts) +

∫ s0a(v, u)dv)ds.

2 Applications of CTM: Overview

In this section we give an overview on applications of change of time methodsin quantitative finance. These applications include: yet one more derivationof Black-Scholes formula; derivation of option pricing formula for a mean-reverting asset in energy finance; pricing of variance, volatility, covarianceand correlation swaps for Heston model; pricing of variance and volatilityswaps in energy markets; pricing of variance and volatility swaps and hedgingof volatility swaps for delayed Heston model.

2.1 Black-Scholes Formula by Change of Time Method

In the early 1970’s, Black and Scholes (1973) made a major breakthrough byderiving pricing formula for vanilla option written on the stock. Their modeland its extensions assume that the probability distribution of the underlyingcash flow at any given future time is lognormal.

There are at least three proofs of their result, including PDE and mar-tingale approaches (see Wilmott et al (1995), Elliott and Kopp (1999)).

One of the aim of this application is to give yet one more derivation ofBlack-Scholes result by change of time method.

2.2 Variance and Volatility Swaps by Change of TimeMethod: Heston Model

Volatility swaps are forward contracts on future realized stock volatility, vari-ance swaps are similar contract on variance, the square of the future volatility,both these instruments provide an easy way for investors to gain exposure tothe future level of volatility.

A stock’s volatility is the simplest measure of its risk less or uncertainty.Formally, the volatility σR is the annualized standard deviation of the stock’sreturns during the period of interest, where the subscript ’R’ denotes theobserved or ’realized’ volatility.

The easy way to trade volatility is to use volatility swaps, sometimescalled realized volatility forward contracts, because they provide pure expo-sure to volatility(and only to volatility).

Demeterfi, K., Derman, E., Kamal, M., and Zou, J. (1999) explained theproperties and the theory of both variance and volatility swaps. They derived

20

an analytical formula for theoretical fair value in the presence of realisticvolatility skews, and pointed out that volatility swaps can be replicated bydynamically trading the more straightforward variance swap.

Javaheri A, Wilmott, P. and Haug, E. G. (2002) discussed the valuationand hedging of a GARCH(1,1) stochastic volatility model. They used ageneral and exible PDE approach to determine the first two moments of therealized variance in a continuous or discrete context. Then they approximatethe expected realized volatility via a convexity adjustment.

Brockhaus and Long (2000) provided an analytical approximation forthe valuation of volatility swaps and analyzed other options with volatilityexposure.

Working paper by Theoret, Zabre and Rostan (2002) presented an analyt-ical solution for pricing of volatility swaps, proposed by Javaheri, Wilmottand Haug (2002). They priced the volatility swaps within framework ofGARCH(1,1) stochastic volatility model and applied the analytical solutionto price a swap on volatility of the S&P60 Canada Index (5-year historicalperiod: 1997− 2002).

Although options market participants talk of volatility, it is variance, orvolatility squared, that has more fundamental significance (see Demeterfi,K., Derman, E., Kamal, M., and Zou, J. (1999)).

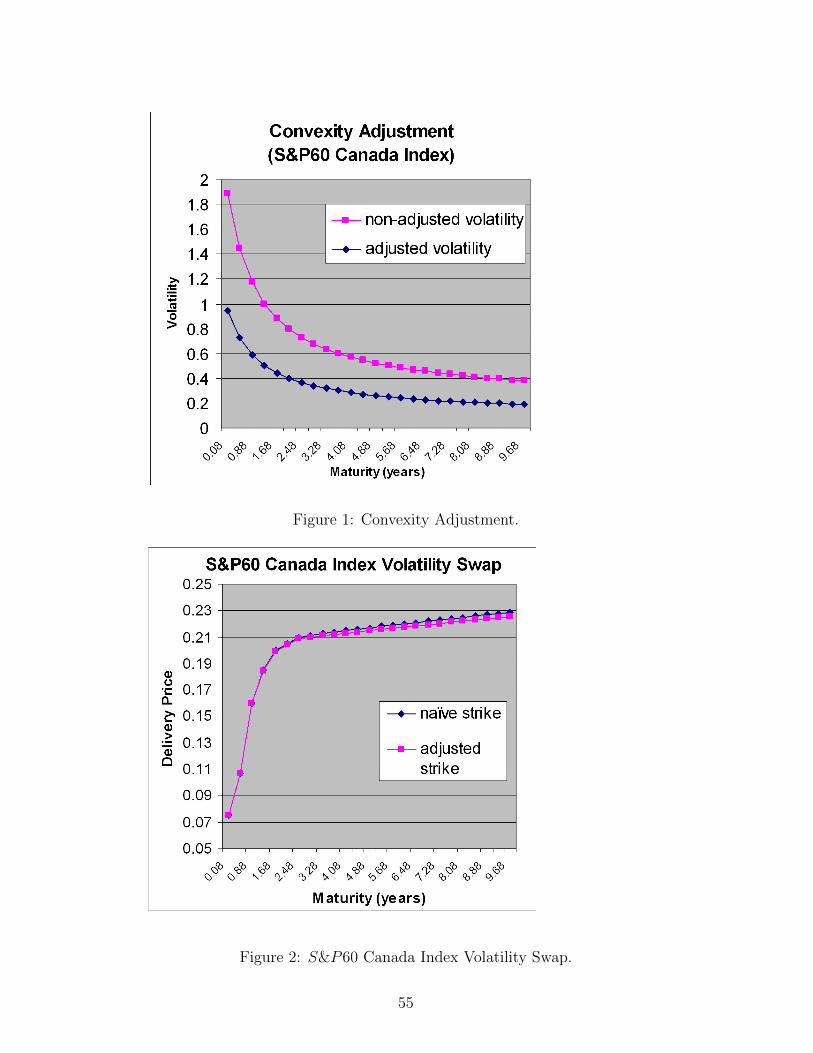

Modeling and pricing of variance, volatility, covariance and correlationswaps for Heston model have been considered in Swishchuk (2004). In thispaper, a new probabilistic approach, change of time method, was proposedto study variance and volatility swaps for financial markets with underlyingasset and variance that follow the Heston (1993) model. We also studiedcovariance and correlation swaps for the financial markets. As an application,we provided a numerical example using S&P60 Canada Index to price swapon the volatility.

Variance swaps for financial markets with underlying asset and stochas-tic volatilities with delay were modelled and priced in the paper Swishchuk(2005a). We found some analytical close forms for expectation and varianceof the realized continuously sampled variance for stochastic volatility withdelay both in stationary regime and in general case. The key features of thestochastic volatility model with delay are the following: i) continuous-timeanalogue of discrete-time GARCH model; ii) mean-reversion; iii) containsthe same source of randomness as stock price; iv) market is complete; v)incorporates the expectation of log-return. As applications, we provided twonumerical examples using S&P60 Canada Index (1998-2002) and S&P500Index (1990-1993) to price variance swaps with delay. Varinace swaps forstochastic volatility with delay is very similar to variance swaps for stochas-tic volatility in Heston model (see Swishchuk (2004)), but simplier to modeland to price it.

Variance swaps for multi-factor stochastic volatility models with delayhave been studied in Swishchuk (2006).

Pricing of variance swaps in Markov-modulated Brownian markets was

21

considered in Elliott and Swishchuk (2005, 2007).One of the aim of this application is to value variance and volatility swaps

for Heston (1993) model using change of time method.Remark 1.1. A extensive reviews of the literature on stochastic volatility

is given in Shephard (2005a, 2005b). A detailed introduction to variance andvolatility swaps, including a history and market products, may be found inCarr and Madan (1998) and Demeterfi et al (1999). The pricing of a range ofvolatility derivatives, including volatility and variance swaps and swaptions,is studied in Howison et al (2004). This paper also contains a lot of volatilitymodels, including those with jumps. Volatility model with jumps was firstconsidered in Naik (1993). Parameter estimation in a stochastic drift hiddenMarkov model with a cap and with applications to the theory of energyfinance and interest rate modeling is studied in Hernandez et al (2005).

Remark 1.2. The fact that stochastic volatility models, such the Hestonmodel and others, are able to fit skews and smiles, while simultaneouslyproviding sensible Greeks, have made these models a popular choice in thepricing of options and swaps. Some ideas of how to calculate the Greeks forvolatility contracts may be found in Howison et al (2004).

Remark 1.3. We note, that the change of time method was used inSwishchuk and Kalemanova (2000) to study stochastic stability of interestrates with and without jumps, in Swishchuk (2004) to model and to pricevariance and volatility swaps for Heston model and in Swishchuk (2005) toprice European call option for commodity prices that follow mean-revertingmodel.

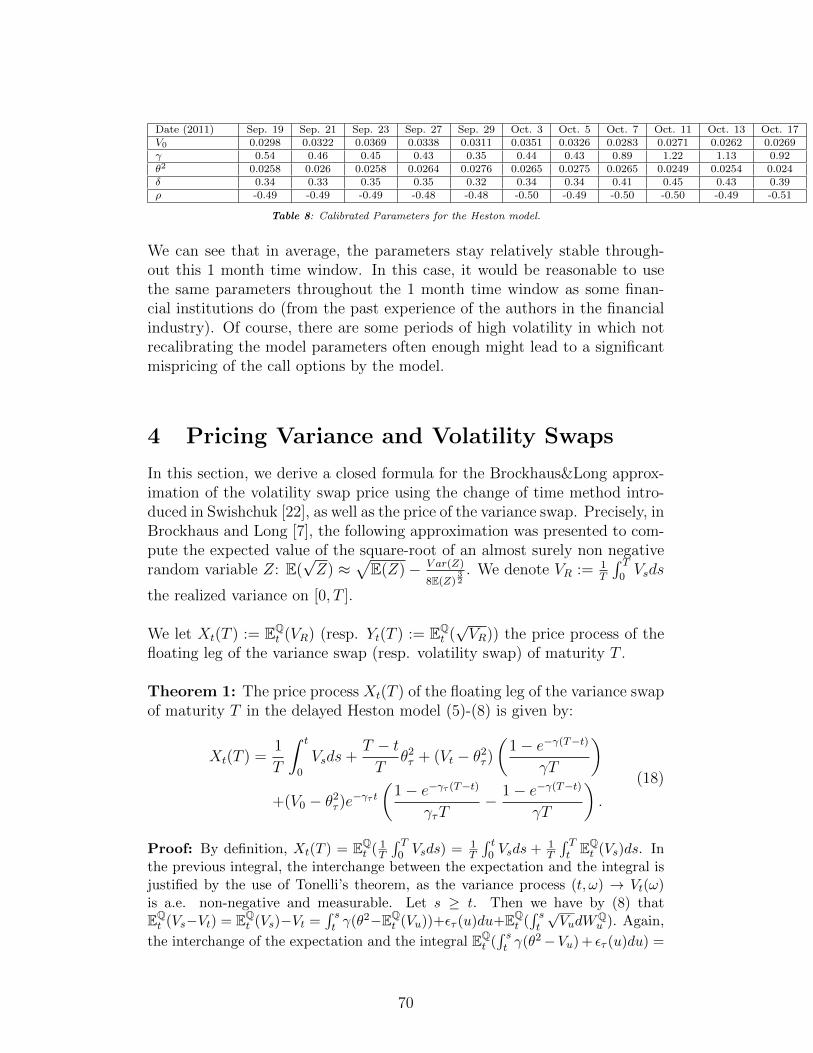

2.3 Change of Time Method: Delayed Heston Model

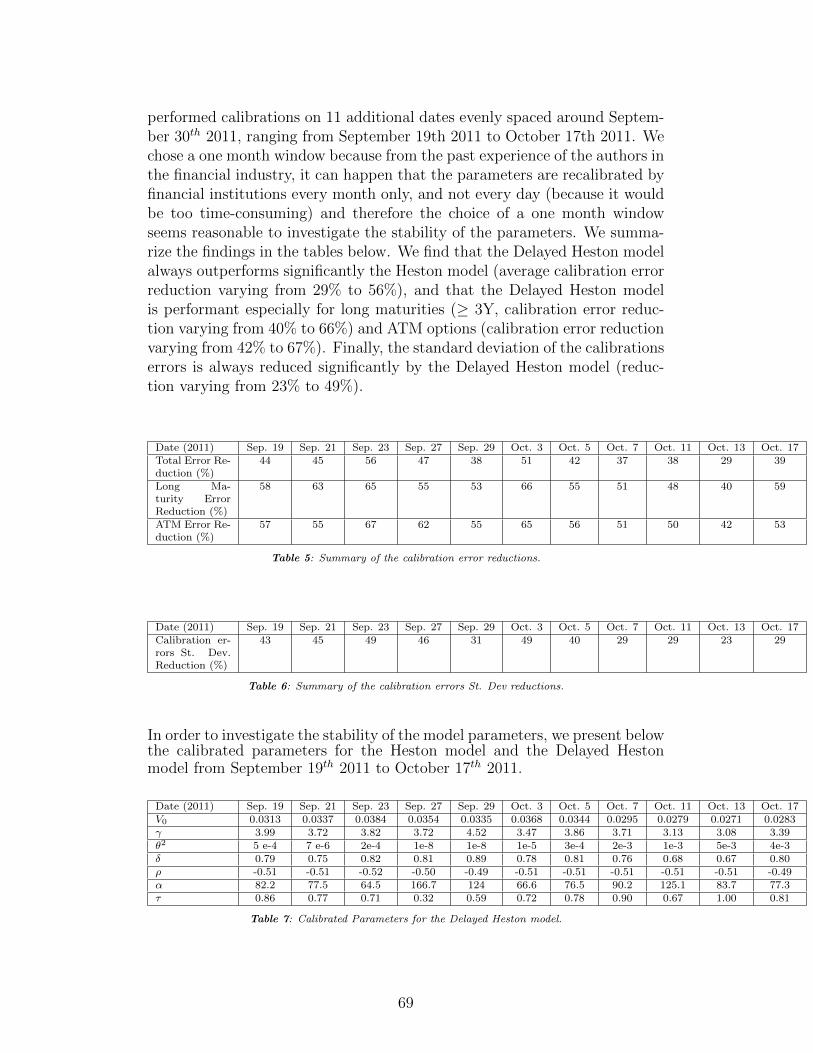

Heston model (Heston (1993)) is one of the most popular stochastic volatilitymodels in the industry as semi-closed formulas for vanilla option prices areavailable, few (five) parameters need to be calibrated, and it accounts for themean-reverting feature of the volatility.One might be willing, in the variance diffusion, to take into account notonly its current state but also its past history over some interval [t − τ, t],where τ > 0 is a constant and is called the delay. Starting from the discrete-time GARCH(1,1) model (Bollerslev (1986)), a first attempt was made inthis direction in Kazmerchuk et al. (2005), where a non-Markov delayedcontinuous-time GARCH model was proposed We present a variance driftadjusted version of the Heston model which leads to a significant improve-ment of the market volatility surface fitting by 44% (compared to Heston).The numerical example we performed with recent market data shows a sig-nificant reduction of the average absolute calibration error 1 (calibration on

1The average absolute calibration error is defined to be the average of the absolutevalues of the differences between market and model implied Black & Scholes volatilities.

22

12 dates ranging from Sep. 19th to Oct. 17th 2011 for the FOREX un-derlying EURUSD). Our model has two additional parameters compared tothe Heston model, can be implemented very easily and was initially intro-duced for volatility derivatives pricing purpose. The main idea behind ourmodel is to take into account some past history of the variance process in its(risk-neutral) diffusion. Using a change of time method for continuous localmartingales, we derive a closed formula for the Brockhaus&Long approxi-mation of the volatility swap price in this model. We also consider dynamichedging of volatility swaps using a portfolio of variance swaps.

One of the aim of this application is to get varinace and volatility swapprices using change of time method and to get hedge ration for volatility swapsin the delayed Heston model model.

2.4 Change of Time Method: Multi-factor Levy-basedModels for Pricing of Financial and Energy Deriva-tives

We also introduce one-factor and multi-factor α-stable Levy-based models toprice financial and energy derivatives. These models include, in particular,as one-factor models, the Levy-based geometric motion model, the Ornstein-Uhlenbeck (1930), the Vasicek (1977), the Cox-Ingersoll-Ross (1985), thecontinuous-time GARCH, the Ho-Lee (1986), the Hull-White (1990) andthe Heath-Jarrrow-Morton (1992) models, and, as multi-factor models, var-ious combinations of the previous models. For example, we introduce newmulti-factor models such as the Levy-based Heston model, the Levy-basedSABR/LIBOR market models, and Levy-based Schwartz-Smith and Schwartzmodels. Using the change of time method for SDEs driven by α-stable Levyprocesses we present the solutions of these equations in simple and com-pact forms. We then apply this method to price many financial and energyderivatives such as variance swaps, options, forward and futures contracts.

One of the aim of this application is to consider various applications of thechange of time method for Levy-based SDEs arising in financial and energymarkets: swap and option pricing, interest derivatives pricing and forwardand futures contracts pricing.

2.5 Mean-Reverting Asset Model by Change of TimeMethod: Option Pricing Formula

Some commodity prices, like oil and gas, exhibit the mean reversion, unlikestock price. It means that they tend over time to return to some long-termmean. This mean-reverting model is a one-factor version of the two-factormodel made popular in the context of energy modeling by Pilipovic (1997).

23

Black’s model (1976) and Schwartz’s model (1997) have become a standardapproach to the problem of pricing options on commodities. These modelshave the advantage of mathematical convenience, in that they give rise toclosed-form solutions for some types of option (see Wilmott (2000)).

Bos, Ware and Pavlov (2002) presented a method for evaluation of theprice of a European option based on St using a semi-spectral method. Theydid not have the convenience of a closed-form solution, however, they shownthat values for certain types of option may nevertheless be found extremelyefficiently. They used the following partial differential equation (see, forexample, Wilmott, Howison and Dewynne (1995))

C ′t +R(S, t)C ′S + σ2S2C ′′SS/2 = rC

for option prices C(S, t), where R(S, t) depends only on S and t, and corre-sponds to the drift induced by the risk-neutral measure, and r is the risk-freeinterest rate. Simplifying this equation to the singular diffusion equationthey were able to calculate numerically the solution.

The working paper Swishchuk (2005b) presents explicit expression for aEuropean option price, C(S, t), for mean-reverting asset St, using change oftime method under both physical and risk-neutral measures.

We note, that recent book by Geman (2005) covers hard and soft com-modities (energy, agriculture and metals) and analysis economic and geopo-litical issues in commodities markets, commodity price and volume risk,stochastic modeling of commodity spot prices and forward curves, real op-tions valuation and hedging of physical assets in the energy industry.

One of the aim of this application is to obtain explicit expression for aEuropean call option price on mean-reverting model of commodity asset usingchange of time method. As we can see, if mean-reverting level equals to zerothen the option pricing formula coincides with Black-Scholes result.

2.6 Variance and Volatility Swaps by Change of TimeMethod: Energy Markets

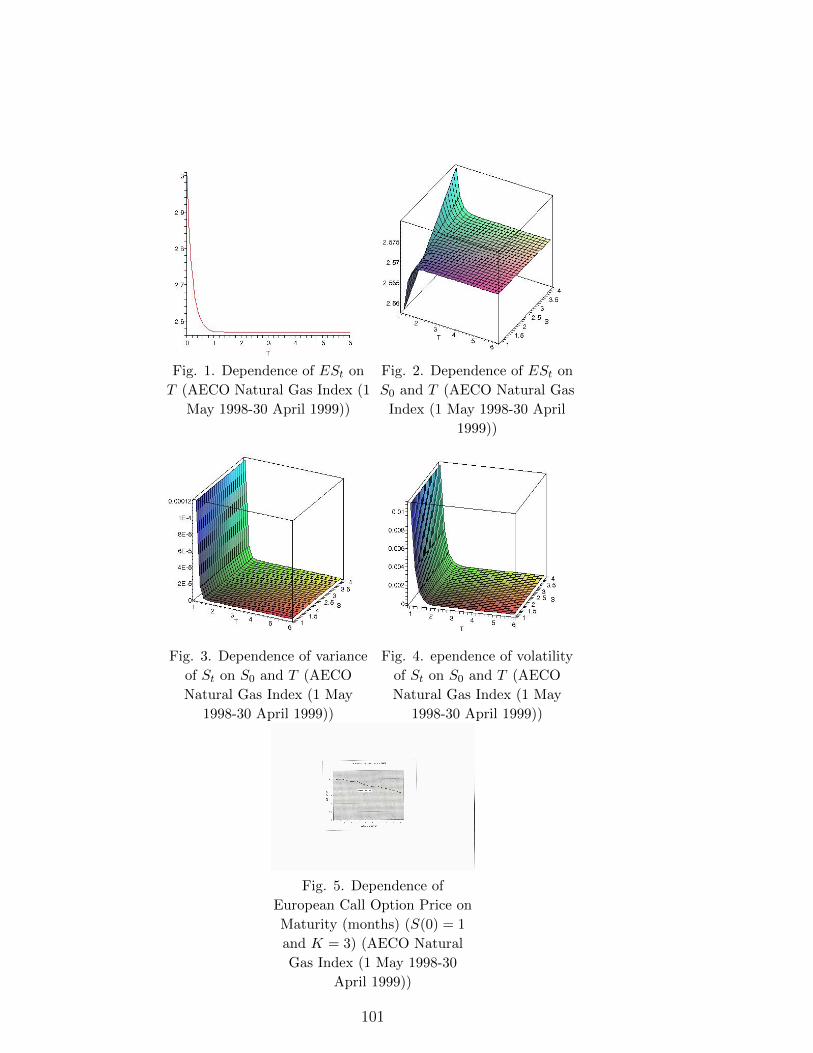

One of applications of CTM is devoted to the pricing of variance and volatil-ity swaps in energy market. We found explicit variance swap formula andclosed form volatility swap formula (using change of time) for energy as-set with stochastic volatility that follows continuous-time mean-revertingGARCH (1,1) model. Numerical example is presented for AECO NaturalGas Index (1 May 1998-30 April 1999). Variance swaps are quite common incommodity, e.g., in energy market, and they are commonly traded. We con-sider Ornstein-Uhlenbeck process for commodity asset with stochastic volatil-ity following continuous-time GARCH model or Pilipovic (1998) one-factormodel. The classical stochastic process for the spot dynamics of commodityprices is given by the Schwartz’ model (1997). It is defined as the exponential

24

of an Ornstein-Uhlenbeck (OU) process, and has become the standard modelfor energy prices possessing mean-reverting features.

In this book, we consider a risky asset in energy market with stochasticvolatility following a mean-reverting stochastic process satisfying the follow-ing SDE (continuous-time GARCH(1,1) model):

dσ2(t) = a(L− σ2(t))dt+ γσ2(t)dWt,

where a is a speed of mean reversion, L is the mean reverting level (orequilibrium level), γ is the volatility of volatility σ(t), Wt is a standard Wienerprocess. Using a change of time method we find an explicit solution of thisequation and using this solution we are able to find the variance and volatilityswaps pricing formula under the physical measure. Then, using the sameargument, we find the option pricing formula under risk-neutral measure. Weapplied Brockhaus-Long (2000) approximation to find the value of volatil;ityswap. A numerical example for the AECO Natural Gas Index for the period1 May 1998 to 30 April 1999 is presented.

Commodities are emerging as an asset class in their own. The range ofproducts offered to investors range from exchange traded funds (ETFs) tosophisticated products including principal protected structured notes on indi-vidual commodities or baskets of commodities and commodity range-accrualor varinace swap. More and more institutional investors are including com-modities in their asset allocation mix and hedge funds are also increasinglyactive players in commodities. Example: Amaranth Advisors lost USD 6billion during September 2006 from trading natural gas futures contracts,leading to the fund’s demise. Concurrent with these developments, a num-ber of recent papers have examined the risk and return characteristics of in-vestments in individual commodity futures or commodity indices composedof baskets of commodity futures. However, since all but the most plain-vanilla investments contain an exposure to volatility, it is equally importantfor investors to understand the risk and return characteristics of commodityvolatilities.

The focusing on energy commodities derives from two reasons: 1) en-ergy is the most important commodity sector, and crude oil and natural gasconstitute the largest components of the two most widely tracked commod-ity indices: the Standard & Poors Goldman Sachs Commodity Index (S&PGSCI) and the Dow Jones-AIG Commodity Index (DJ-AIGCI); 2) existenceof a liquid options market: crude oil and natural gas indeed have the deepestand most liquid options marketss among all commodities. The idea is to usevariance (or volatility) swaps on futures contracts. At maturity, a varianceswap pays off the difference between the realized variance of the futures con-tract over the life of the swap and the fixed variance swap rate. And sincea variance swap has zero net market value at initiation, absence of arbitrageimplies that the fixed variance swap rate equals to conditional risk-neutralexpectation of the realized variance over the life of swap. Therefore, e.g., the

25

time-series average of the payoff and/or excess return on a variance swap isa measure of the variance risk premium.

Variance risk premia in energy commodities, crude oil and natural gas, hasbeen considered by A. Trolle and E. Schwartz (2009). The same methodologyas in Trolle & Schwartz (2009) was used by Carr & Wu (2009) in their studyof equity variance risk premia. The idea was to use variance swaps on futurescontracts. The study in Trolle & Schwartz (2009) is based on daily data fromJanuary 2, 1996 until November 30, 2006-a total of 2750 business days. Thesource of the data is NYMEX. Trolle & Schwartz (2009) found that: 1) theaverage variance risk premia are negative for both energy commodities butmore strongly statistically significant for crude oil than for natural gas; 2)the natural gas variance risk premium (defined in dollars terms or in returnterms) is higher during the cold months of the year (seasonality and peaksfor natural gas variance during the cold months of the year); 3) energy riskpremia in dollar terms are time-varying and correlated with the level of thevariance swap rate. In contrast, energy variance risk premia in return terms,paerticularly in the case of natural gas, are much less correlated with thevarinace swap rate.

The S&P GSCI is comprised of 24 commodities with the weight of eachcommodity determined by their relative levels of world production over thepast five years. The DJ-AIGCI is comprised of 19 commodities with theweight of each component detrmined by liquidity and world production val-ues, with liquidity being the dominant factor. Crude oil and natural gas arethe largest components in both indices. In 2007, their weight were 51.30%and 6.71%, respectively, in the S&P GSCI and 13.88% and 11.03%, respec-tively, in the DJ-AIGCI. The Chicago Board Optiopns Exchange (CBOE)recently introduced a Crude Oil Volatility Index (ticker symbol OVX). Thisindex also measures the conditional risk-neutral expectation of crude oil vari-ance, but is computed from a cross-section of listed options on the UnitedStates Oil Fund (USO), which tracks the price of WTI as closely as possi-ble. The CBOE Crude Oil ETF Volatility Index (’Oil VIX’, Ticker - OVX)measures the market’s expectation of 30-day volatility of crude oil pricesby applying the VIX methodology to United States Oil Fund, LP (Ticker -USO) options spanning a wide range of strike prices. We have to notice thatcrude oil and natural gas trade in units of 1,000 barrels and 10,000 Britishthermal units (mmBtu), respectivel. Price are quoted as US dollars andcents per barrel or mmBtu. The continuous-time GARCH model has alsobeen exploited by Javaheri, Wilmott and Haug (2002) to calculate volatilityswap for S&P500 index. They used PDE approach and mentioned (page 8,sec. 3.3) that ’it would be interesting to use an alternative method to calcu-late F (v, t) and the other above quantities’. This paper exactly contains thealternative method, namely, ’change of time method’, to get varinace andvolatility swaps. The change of time method was also applied by Swishchuk(2004) for pricing variance, volatility, covariance and correlation swaps forHeston model. The first paper on pricing of commodity contracts was pub-

26

lished by Black (1976).One of the aim of this application is to get variance and volatility swap

prices for Heston model using change of time method.

References

Applebaum, D. (2004): Levy Processes and Stochastic Calculus, Cam-bridge University Press.

Barnhoff-Nielsen, O.E. and Shephard, N. (2001): Modelling byLevy processes for financial econometrics, in Levy Processes-Theory and Ap-plications, Birkhauser.

Barndorff-Nielsen O.E., Mikosch, T. and Resnick, S. (eds.) (2001):Levy Processes: Theory and Applications, Birkhauser.

Barndorff-Nielsen O.E., Mikosch, T. and Resnick, S. (eds.) (2001):Levy Processes: Theory and Applications, Birkhauser, pp. 283-718.

Barnhoff-Nielsen, O.E. and Shephard, N. (2002): Econometric anal-ysis of realized volatility andits use in estimating stochastic volatility models,J. R. Statistic Soc. B, 64, pp. 253-280.

Barnhoff-Nielsen, O.E., Nicolato, E. and Shephard, N. (2002):Some recent development in stochastic volatility modeling, Quantitative Fi-nance, 2, 11-23.

Barnhoff-Nielsen, O.E. and Shiryaev A. (2009): Change of Timeand Change of Measure. World Scientific.

Bates, D. (1996): Jumps and stochastic volatility: the exchange rate pro-cesses implicit in Deutschemark options. Rev. Fin. Studies, 9, pp. 69-107.

Bertoin, J. (1996): Levy Processes, Cambridge University Press.

Black, F. and Scholes, M. (1973): The pricing of options and corporateliabilities, J. Political Economy 81, 637-54.

Black, F. (1076): The pricing of commodity contarcts, J. Financial Eco-nomics, 3, 167-179.

Bochner, S. (1949): Diffusion equation and stochastic processes. Proc.Nat. Acad. Sci. USA, 85, 369-370.

Bollerslev, T. (1986): Generalized autoregressive conditional heteroscedas-ticity. Journal of Economics, 31: 307-27.

Bos, L.P., Ware, A. F. and Pavlov, B. S. (2002): On a semi-spectralmethod for pricing an option on a mean-reverting asset, Quantitative Fi-nance, Volume 2, 337-345.

27

Brockhaus, O. and Long, D. (2000): Volatility swaps made simple,RISK, January, 92-96.

Carr, P. and Madan, D. (1998): Towards a Theory of Volatility Trading.In the book: Volatility, Risk book publications,http://www.math.nyu.edu/research/carrp/papers/.

Carr, P., Geman, H., Madan, D. and Yor, M. (2003): Stochasticvolatility for Levy processes, Mathem. Finance, 13, pp. 345-382.

P. Carr and L. Wu (2009): Variance risk premia, Review of FinancialStudies 22, 1311-1341.

Chesney, M. and Scott, L. (1989): Pricing European Currency Op-tions: A comparison of modifeied Black-Scholes model and a random variancemodel, J. Finan. Quantit. Anal. 24, No3, 267-284.

Cherny, A. and Shiryaev, A. (2002): Change of time and change ofmeasure for Levy processes. Lecture Notes 13, Aarhus University, Aarhus,46p.

Clark, P. (1973): A subordinated stochastic process model with fixedvariance for speculative prices, Econometrica, 41, 135-156.

Cont, R. and Tankov, P. (2004): Financial Modeling with Jump Pro-cesses, Chapman & Hall/CRC Fin. Math. Series.

Cox, J., Ingersoll, J. and Ross, S. (1985): A theory of the termstructure of interest rates, Econometrica 53, 385-407.

Dambis, K.E. (1965): On the decomposition of continuous submartingales,Theory Probabability and its Appl., 10, 4091-410.

Dubins and Schwartz (1965): On continuous martingales, Proc. Nat.Acad. Sciences, USA, 53, 913-916.

Demeterfi, K., Derman, E., Kamal, M. and Zou, J. (1999): A guideto volatility and variance swaps, The Journal of Derivatives, Summer, 9-32.

Elliott, R. (1982): Stochastic Calculus and Applications, Springer-Verlag,New York.

Elliott, R. and Kopp, P. (1999): Mathematics of Financial Markets,Springer-Verlag, New York.

Elliott, R. and Swishchuk, A. (2005): Pricing options and volatilityswaps in Markov-modulated Brownian and Fractional Brownian markets,RJE 2005 Conference, Calgary, AB, Canada, July 24-27, 2005, 35p.

Elliott, R. and Swishchuk, A. (2007): Pricing options and variance

28

swaps in Markov-modulated Brownian markets, In: Hidden Markov Mod-els in Finance, Springer, International Series in Operations Research andManagement Science, Eds.: Elliott, R. and Mamon, R.

Feller, W. (1966): Introduction to Probability Theory and its Applica-tions, v. II, Wiley & Sons.

Geman, H., Madan, D. and Yor, M. (2001): Time changes for Levyprocesses, Mathem. Finance, 11, pp. 79-96.

Geman, H., Madan, D. and Yor, M. (2001): Asset prices are Brownianmotion: only in business time, in Quantitative Analysis in Financial Markets,Avellaneda, M., ed., World Scientific: River Edge, NJ, pp. 103-146.

Geman, H. (2005): Commodities and Commodity Derivatives: Modellingand Pricing for Agricaltural, Metals and Energy, Wiley.

D. Heath, R.Jarrow and A.Morton: Bond pricing and the term struc-ture of the interest rates: A new mathodology. Econometrica, 60, 1 (1992),pp. 77-105.

Hernandez,J., Sounders, D. and Seco, L. (2005): Parameter Esti-mations in a Stochastic Drift Hidden Markov Model with a Cap, submittedto SIAM.

Heston, S. (1993): A closed-form solution for options with stochasticvolatility with applications to bond and currency options, Review of Finan-cial Studies, 6, 327-343

Ho T.S.Y. and Lee S.-B.: Term structure movements and pricing interestrate contigent claim. J. of Finance, 41 (December 1986), pp. 1011-1029.

Hobson, D. and Rogers, L. (1998): Complete models with stochasticvolatility, Math. Finance 8, no.1, 27-48.

Howison, S., Rafailidis, A. and Rasmussen, H. (2004): On the Pric-ing and Hedging of Volatility Derivatives, Applied Math. Finance J., p.1-31.

Huff, B. (1969): The loose subordination of differential processes to Brow-nian motion, Ann. Math. Statist., 40, 1603-1609.

Hull, J., and White, A. (1987): The pricing of options on assets withstochastic volatilities, J. Finance 42, 281-300.

Ikeda, N. and Watanabe, S. (1981): Stochastic Differential Equationsand Diffusion Processes, North-Holland/Kodansha Ltd., Tokyo.

Kallsen, J. and Shiryaev, A. (2001): Time change representation ofstochastic integrals. Theory Probab. Appl. 46, 3, 522-528.

Kazmerchuk, Y., Swishchuk, A. and Wu, J. (2005): A continuous-

29

time GARCH model for stochastic volatility with delay. Canadian AppliedMathematics Quarterly, 13, 2: 123-149.

Knight, F. (1971) A reduction of continuous, square-integrable martin-gales to Brownian motion, in: H. Dinges, ed., Martingales, Lecture Notes inMath. No. 190 (Springer, Berlin) pp. 19-31.

Javaheri, A., Wilmott, P. and Haug, E. (2002): GARCH and volatil-ity swaps, Wilmott Technical Article, January, 17p.

Lamperton, D. and Lapeyre, B. (1996): Introduction to StochasticCalculus Applied to Finance, Chapmann & Hall.

Liptser R. and Shiryaev A. (1989): Theory of Martingales. Kluwer,Dordrecht.

Liptser R. and Shiryaev A. (2001): Statistics of Random Processes.Vol. I: General Theory; Vol. II: Applications, 2nd edn. Springer-Verlag,Berlin.

Madan, D. and Seneta, E. (1990): The variance gamma (VG) modelfor share market returns, Journal of Business 63, No. 4, 511-524.

Merton, R. (1973): Theory of rational option pricing, Bell Journal ofEconomic Management Science 4, 141-183.

Monroe, I. (1972): On embedding right continuous martingales in Brow-nian motion, Ann. Math. Statist., 43, 1293-1311.

Monroe, I. (1978): Processes that can be embedded in Brownian motion,The Annals of Probab., 6, No. 1, 42-56.

Naik, V. (1993): Option Valuation and Hedging Strategies with Jumps inthe Volatility of Asset Returns, Journal of Finance, 48, 1969-84.

Øksendal, B. (1998): Stochastic Differential Equations: An Introductionwith Applications. NY: Springer.

Pilipovic, D. (1997): Valuing and Managing Energy Derivatives, NewYork, McGraw-Hill.

Price Pseudo-Variance, Pseudo-Covariance, Pseudo-Volatility, and Pseudo-Correlation Swaps-In Analytical Closed-Forms, Proceedings of the Sixth PIMSIndustrial Problems Solving Workshop, PIMS IPSW 6, University of BritishColumbia, Vancouver, Canada, May 27-31, 2002, pp. 45-55. Editor: J.Macki, University of Alberta, June 2002. (Joint report: Raymond Cheng,Stephen Lawi, Anatoliy Swishchuk, Andrei Badescu, HammoudaBen Mekki, Asrat Fikre Gashaw, Yuanyuan Hua, Marat Moly-boga, Tereza Neocleous, Yuri Petrachenko).

30

Schoutens, W. (2003): Levy Processes in Finance: Pricing Derivatives,Wiley.

Shephard, N. (2005a): Stochastic Volatility: Selected Readings. Oxford:Oxford University Press.

Shephard, N. (2005b): Stochastic Volatility. Working paper, Univresityof Oxford, Oxford.

Skorokhod, A. (1965): Studies in the Theory of Random Processes,Addison-Wesley, Reading.

Schwartz, E. (1997): The stochastic behaviour of commodity prices: im-plications for pricing and hedging, J. Finance, 52, 923-973.

Swishchuk, A. and Kalemanova, A. (2000): Stochastic stability ofinterest rates with jumps. Theory probab. & Mathem statist., TBiMC Sci.Publ., v.61, Kiev, Ukraine.

Swishchuk, A. (2004): Modeling and valuing of variance and volatilityswaps for financial markets with stochastic volatilities, Wilmott Magazine,Technical Article No2, September Issue, 64-72.

Swishchuk, A. (2005a): Modelling and Pricing of Variance Swaps forStochastic Volatilities with Delay, Wilmott Magazine, Technical Article, Septem-ber Issue (to appear).

Swishchuk, A. (2008): Explicit option pricing formula for mean-revertingmodel, J. Numer. Appl. Math., Vol. 1(96), 2008, pp.216-233.

Swishchuk, A. (2006): Modelling and pricing of variance swaps for multi-factor stochastic volatilities with delay, Canadian Applied Math. Quarterly,14, No. 4, Winter.

Theoret, R., Zabre, L. and Rostan, P. (2002): Pricing volatilityswaps: empirical testing with Canadian data. Working paper, Centre deRecherche en Gestion, Document 17-2002, July 2002.

Trolle, A. and Schwartz, E. (2010): Variance risk premia in energycommodities, J. of Derivatives, Spring, v. 17, No. 3, 15-32.

Wilmott, P., Howison, S. and Dewynne, J. (1995): Option Pricing:Mathematical Models and Computations. Oxford: Oxford Financial Press.

Wilmott, P., Howison, S. and Dewynne, J. (1995): The Mathematicsof Financial Derivatives, Cambridge, Cambridge University Press.

Wilmott, P. (2000): Paul Wilmott on Quantitative Finance, New York,Wiley.

Winkel, M. (2001): The recovery problem for time-changed Levy pro-

31

cesses, Res. Report, 2001-37, MaPhySto, October.

32

Chapter 3: Change of Time Method (CTM)

and Black-Scholes Formula

’It is said that there is no such thing as a free lunch. But the universe is theultimate free lunch’,-Alan Guth (MIT).

1 Introduction to Option Pricing and Black-

Scholes Formula