Embed Size (px)

Citation preview

Challenges in Market and Counterparty Risk Management

How to solve the critical issues? Solutions that can help.

ZADAR, 14 May 2011

Reinhard Keider; Head of Risk Architecture and Risk Methodologies in Bank Austria

Don´t ever try to understand everything,

some things will just never make sense.

2

I guess some of you might agree with this saying.

Despite this I will try to

1)Make my brief presentation understandable

2)And hopefully it make sense to you.

….so let´s start !

3

4

AGENDA

Part 1: Market Risk Management

Part 2: Counterparty Credit Risk

Part 3: New regulatory framework (Basel 2.5/3)

5

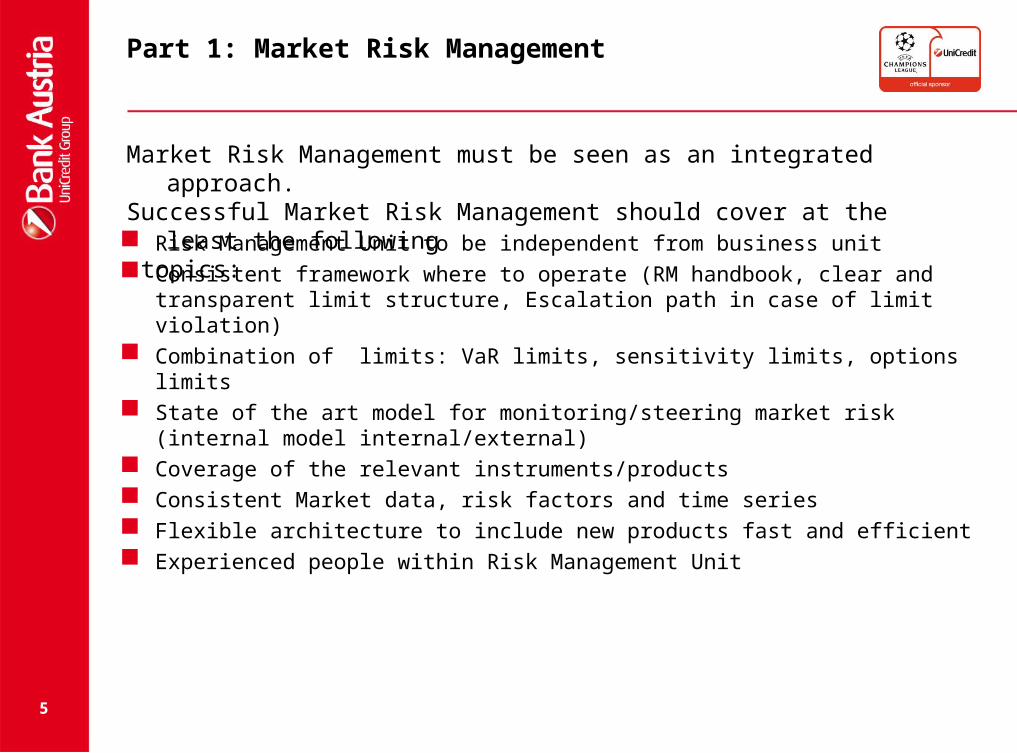

Part 1: Market Risk Management

Risk Management Unit to be independent from business unit Consistent framework where to operate (RM handbook, clear and

transparent limit structure, Escalation path in case of limit violation) Combination of limits: VaR limits, sensitivity limits, options limits State of the art model for monitoring/steering market risk (internal model

internal/external) Coverage of the relevant instruments/products Consistent Market data, risk factors and time series Flexible architecture to include new products fast and efficient Experienced people within Risk Management Unit

Market Risk Management must be seen as an integrated approach. Successful Market Risk Management should cover at the least the following topics:

6

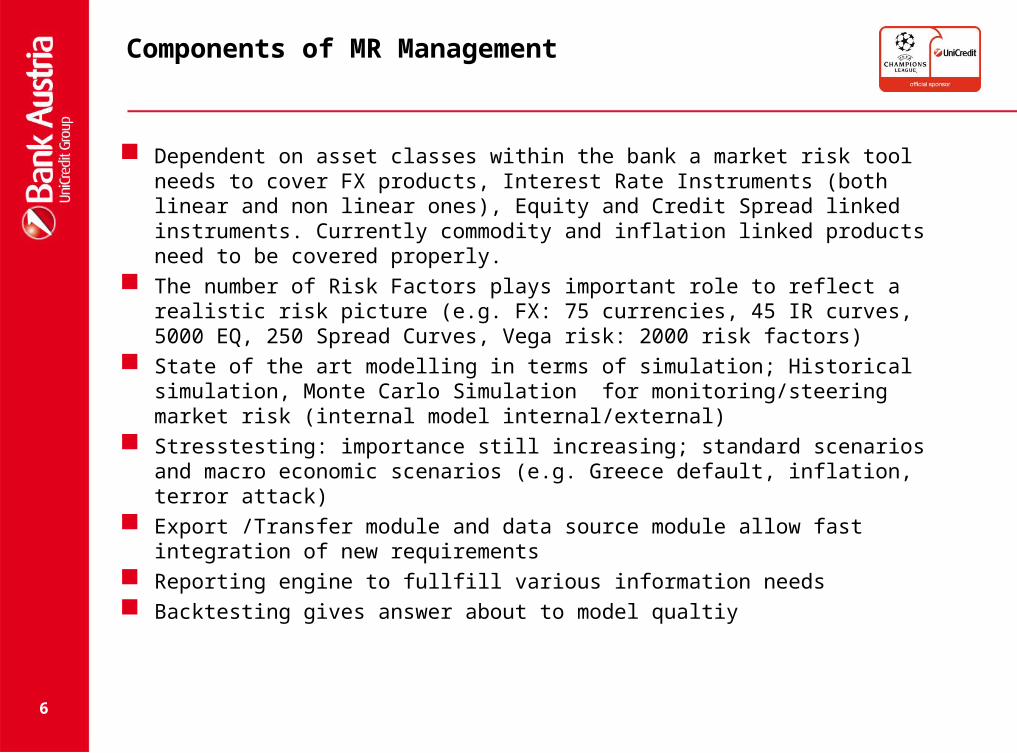

Components of MR Management

Dependent on asset classes within the bank a market risk tool needs to cover FX products, Interest Rate Instruments (both linear and non linear ones), Equity and Credit Spread linked instruments. Currently commodity and inflation linked products need to be covered properly.

The number of Risk Factors plays important role to reflect a realistic risk picture (e.g. FX: 75 currencies, 45 IR curves, 5000 EQ, 250 Spread Curves, Vega risk: 2000 risk factors)

State of the art modelling in terms of simulation; Historical simulation, Monte Carlo Simulation for monitoring/steering market risk (internal model internal/external)

Stresstesting: importance still increasing; standard scenarios and macro economic scenarios (e.g. Greece default, inflation, terror attack)

Export /Transfer module and data source module allow fast integration of new requirements

Reporting engine to fullfill various information needs Backtesting gives answer about to model qualtiy

7

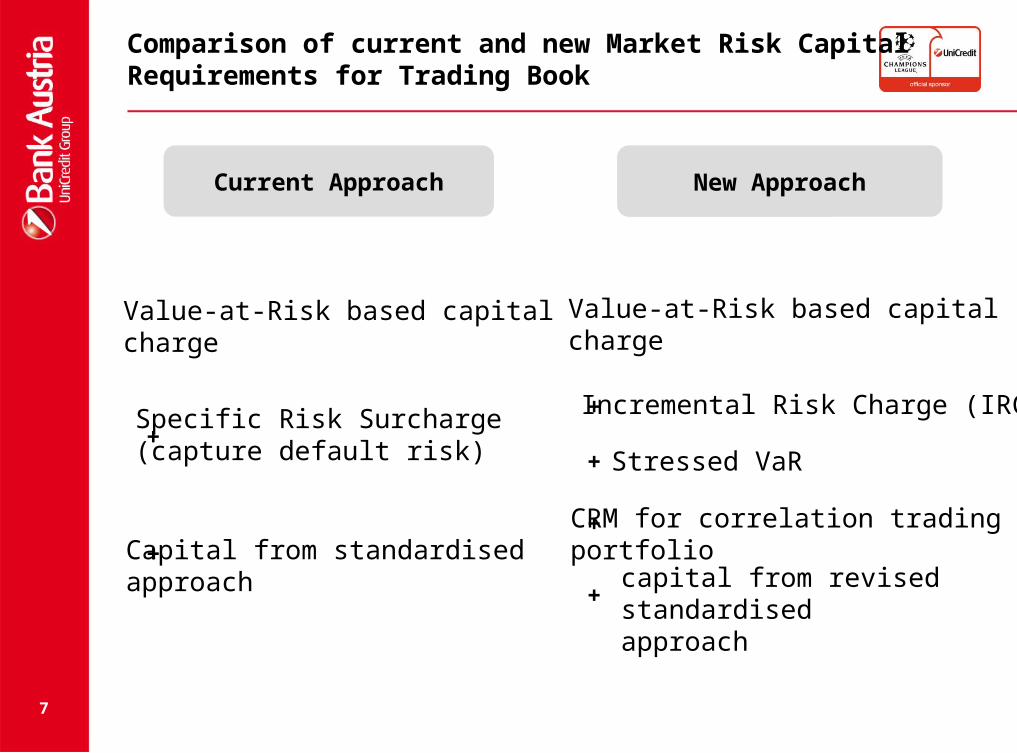

Comparison of current and new Market Risk Capital Requirements for Trading Book

+

Current Approach New Approach

Value-at-Risk based capitalcharge

Value-at-Risk based capitalcharge

Specific Risk Surcharge(capture default risk)

+ Capital from standardisedapproach

+

+ Stressed VaR

Incremental Risk Charge (IRC)

+

+

CRM for correlation tradingportfolio

capital from revised standardised approach

8

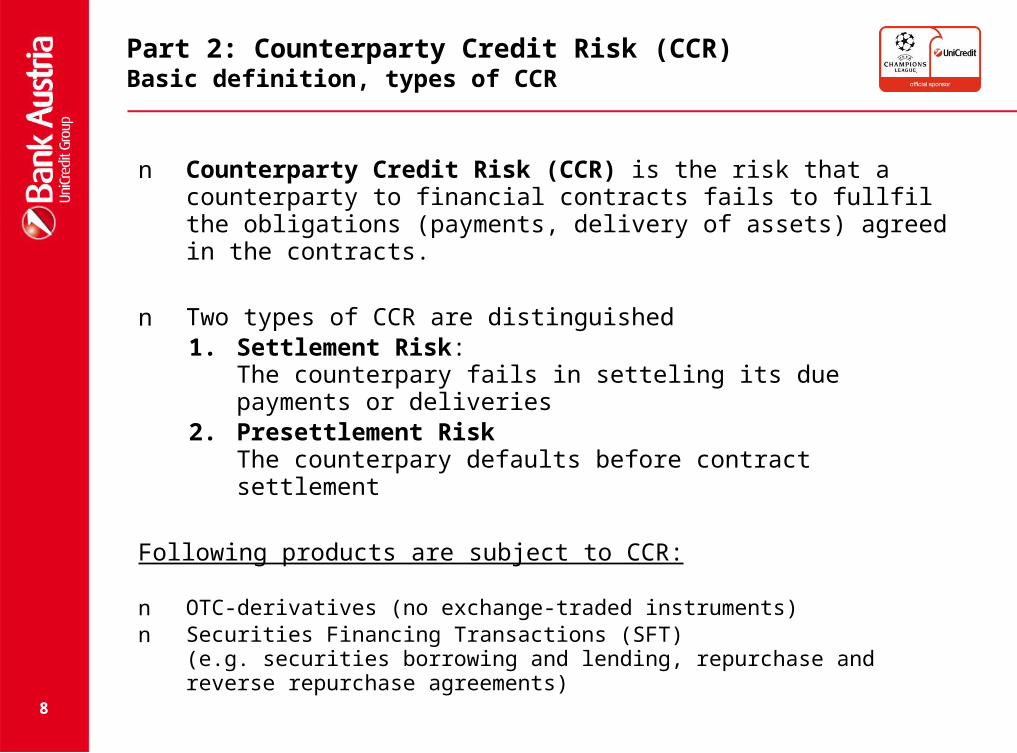

Part 2: Counterparty Credit Risk (CCR)Basic definition, types of CCR

n Counterparty Credit Risk (CCR) is the risk that a counterparty to financial contracts fails to fullfil the obligations (payments, delivery of assets) agreed in the contracts.

n Two types of CCR are distinguished1. Settlement Risk:

The counterpary fails in setteling its due payments or deliveries2. Presettlement Risk

The counterpary defaults before contract settlement

Following products are subject to CCR:

n OTC-derivatives (no exchange-traded instruments)n Securities Financing Transactions (SFT)

(e.g. securities borrowing and lending, repurchase and reverse repurchase agreements)

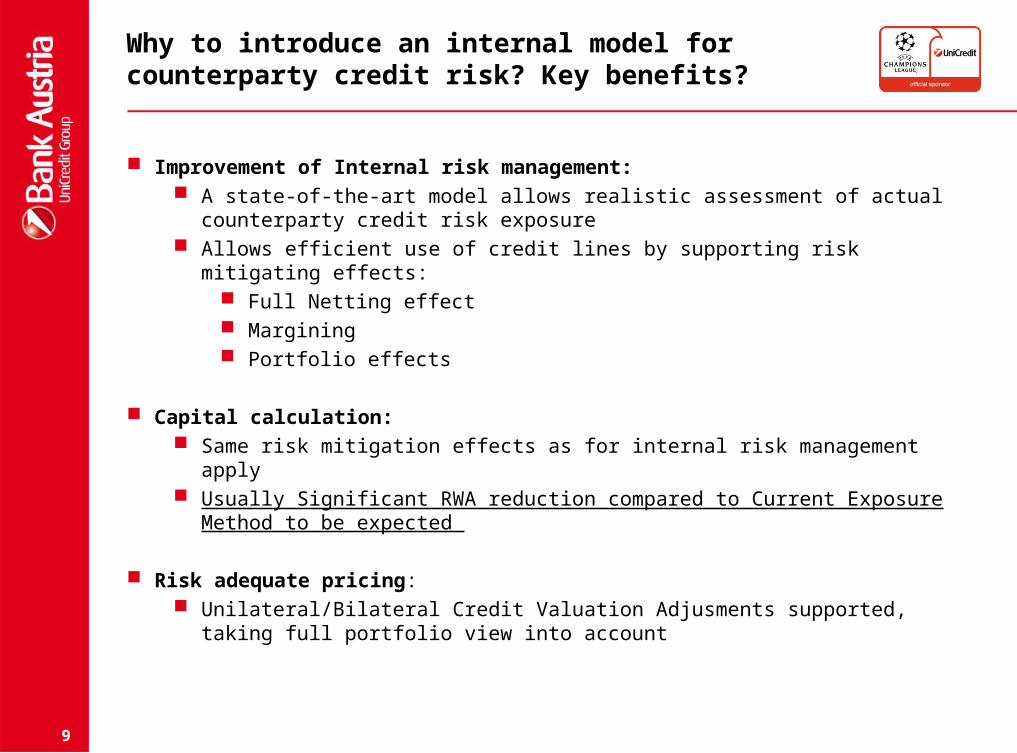

Why to introduce an internal model for counterparty credit risk? Key benefits?

Improvement of Internal risk management: A state-of-the-art model allows realistic assessment of actual counterparty credit

risk exposure Allows efficient use of credit lines by supporting risk mitigating effects:

Full Netting effect Margining Portfolio effects

Capital calculation: Same risk mitigation effects as for internal risk management apply Usually Significant RWA reduction compared to Current Exposure Method to be

expected

Risk adequate pricing: Unilateral/Bilateral Credit Valuation Adjusments supported, taking full portfolio

view into account

9

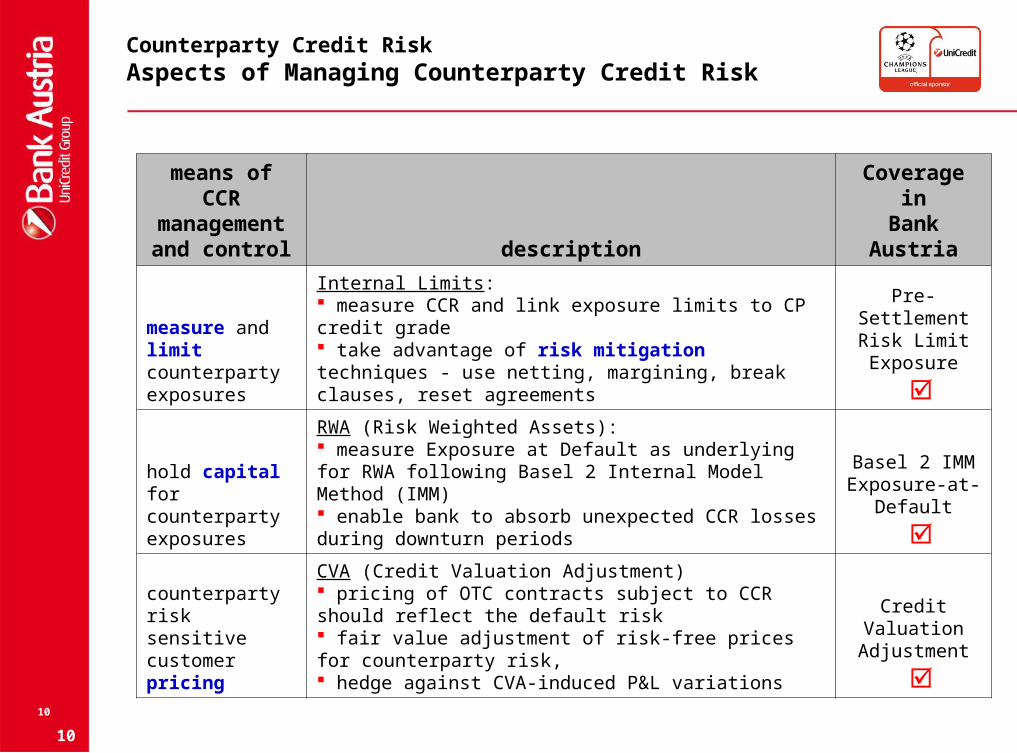

Counterparty Credit Risk Aspects of Managing Counterparty Credit Risk

means of CCR management and control description

Coverage inBank Austria

measure and limit counterparty exposures

Internal Limits: measure CCR and link exposure limits to CP credit grade take advantage of risk mitigation techniques - use netting, margining, break clauses, reset agreements

Pre-Settlement Risk Limit Exposure

hold capital for counterparty exposures

RWA (Risk Weighted Assets): measure Exposure at Default as underlying for RWA following Basel 2 Internal Model Method (IMM) enable bank to absorb unexpected CCR losses during downturn periods

Basel 2 IMM Exposure-at-

Default

counterparty risk sensitive customer pricing

CVA (Credit Valuation Adjustment) pricing of OTC contracts subject to CCR should reflect the default risk fair value adjustment of risk-free prices for counterparty risk, hedge against CVA-induced P&L variations

Credit Valuation Adjustment

10

10

11

Quantitative measures for CCR Exposure measure and purpose

Exposure Measure purpose of application

Current Positive Exposure (CPE)equal to the current replacement cost of a transaction

Potential Future Exposure (PFE)

maximum exposure estimated to occur on a future date at a high confidence level used for counterparty credit limit

Expected Positive Exposure (EPE)

• credit equivalent input for risk capital calculation (regulatory and economic)• input for cost calculation• EPE profile input for Credit Value Adjustment (CVA)• closely related to EE (Expected Exposure)

Internal Counterparty Risk Model

Model overview and components

12

Scenario engine Instrument price distributions Output

Market data

Spot rates

Yield curves

Volatilities

etc.

Product valuation models

Vanilla options (Black Scholes)

Exotic (accrual, extendable)

Barrier (standard, double)

Swaption, cap/floor

etc.

Transaction data

Swap rate

Reference rate

Settlement frequency

Maturity

etc.

Counterparty data

Legal agreements

Netting data

Collateral data

Country

etc.

Aggregation

USD interest rates

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0 2 4 6 8 10 12

Time

US

D in

tere

st r

ate

s (

%)

Value of swap (% of notional)

0 2 4 6 8 10

Reduction)

Exp

osu

re

Limit

EE

PFE

TimeTime

-10

-5

0

5

10

15

20

0 1 2 3 4 5

-10

-5

0

5

10

15

20

0 1 2 3 4 5

Risk Management

Limit monitoring

Capital requirements

Credit Valuation Adjustment

Reporting

Stresstesting

ValidationMarket data pre-processing

13

Part 3: Basel 2.5 and Basel 3

Challenges to the Banking industry in front of

new Basel regulations

Chapter Title - Chapter Section Title

14

Current situation (Basel II)

• VaR based Trading book capital charge calculated using 99% quantile of 10 day loss

Common assumption: • Losses from issuer defaults in trading book positions negligible since – Mainly high rated issuers in trading book – Positions are sold in case of downgrading

Financial crisis:• Losses >> trading book capital charge occurred (e.g. Lehman Brothers)• Particularly positions subject to credit spread risk (cds, cdo,bonds,…) • Significant part of the losses not caused by actual defaults but by rating migrations

15

Regulatory Response

Basel Committee proposed changes to the capital requirements for the trading book: (mainly for internal model)

• Incremental risk charge (IRC), specific risk

• Stressed value-at-risk, general risk

• Comprehensive risk measure for correlation trading activities

• For remaining securitization products the capital charges of the banking book apply

Implementation date: 31 Dez. 2011

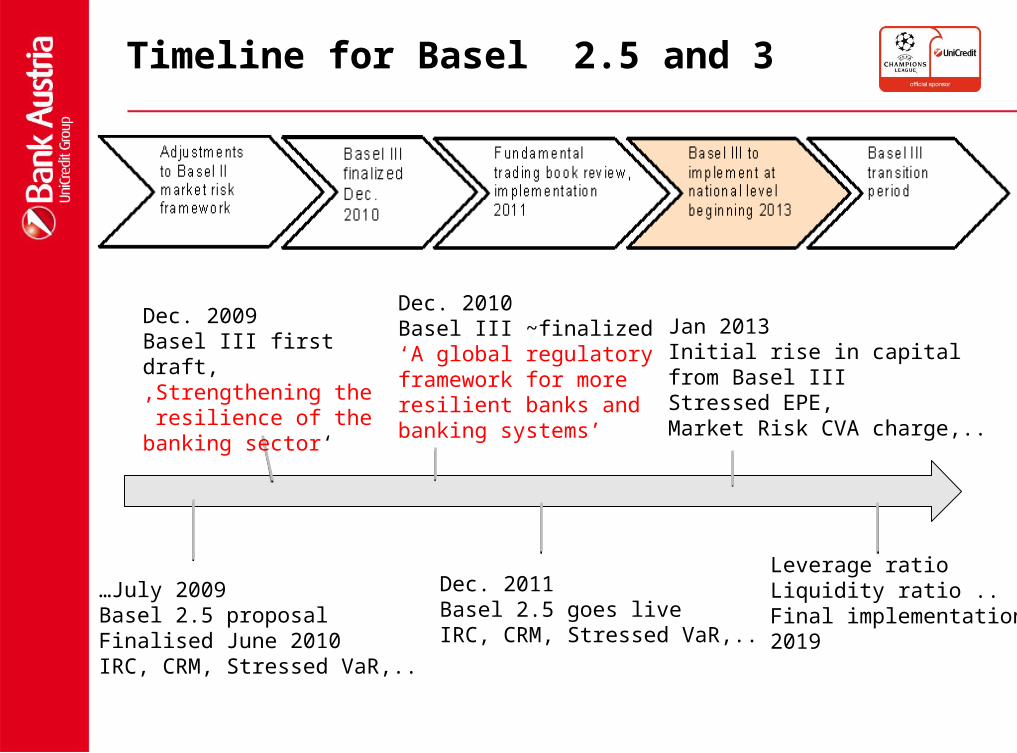

Timeline for Basel 2.5 and 3

…July 2009Basel 2.5 proposalFinalised June 2010IRC, CRM, Stressed VaR,..

Dec. 2010Basel III ~finalized‘A global regulatory framework for more resilient banks and banking systems’

Dec. 2011Basel 2.5 goes liveIRC, CRM, Stressed VaR,..

Leverage ratioLiquidity ratio ..Final implementation2019

Jan 2013Initial rise in capitalfrom Basel IIIStressed EPE,Market Risk CVA charge,..

Dec. 2009Basel III first draft,‚Strengthening the resilience of the banking sector‘

17

Basel Reform Programme: Focus on Counterparty Credit Risk - Overview

A. Capital Base B. Counterparty Risk C. Leverage Ratio D. Procyclicality

Raise quality, consistency and transparency of bank's

capital base

Strengthen risk coverage, amending July 2009's

trading book and securitization reforms by

adding capital requirements for

counterparty credit risk

Introduce a "leverage ratio" as a supplementary

measure to the Basel II framework with in order to

build up excessive leverage in the banking

system

Promote measures for building up capital buffers in good times that can be

drawn upon in stress periods

E. Liquidity Standard

Promote measures for building up capital buffers in good times that can be

drawn upon in stress periods

Determine capital requirement for counterparty credit risk using effective EPE calculation for a period of stress (similar to 2009' proposal regarding market risk stressed VaR) and

Introduce captial charge for mark-to-market losses (ie credit value adjustment losses = CVA risk) associated with deterioation in the credit worthiness (not necessarily default) of counterparties

Strengthen standards for collateral management and initial margining. Eg banks with large and illiquid derivative exposures will have to apply longer margining periods.

Banks with exposure to central counterparties (of those are meeting some CPSS/IOSCO "strict criteria" only) will qualify for a zero percent risk weight.

Include "wrong-way risk" (cases where the exposure rises when the credit quality of the counterparty deteriorates) into Pillar 1 requirements, enhance stress test requirements, revise model validation standards and issue supervisory guidance for sound backtesting practices of CCR.

EXAMPLES

Additional Market Risk Capital ChargeCredit Valuation Adjustment: Cover MtM of unexpected counterparty risk losses

In addition to the existing capital charge for unexpected losses arising from counterparty defaults (Counterparty Credit Risk RWA) a stand-alone capital charge has been proposed to cover the market risk of potential MtM losses due to spread driven increase of unilateral credit value adjustments (CVA) of OTC portfolios.

Unilateral CVA: Adjustment of the risk-free mark-to-model prices of OTC derivatives for the credit risk of the counterparty (= expected loss).

Calculation of the new CVA capital charge by evaluating the unexpected losses of a portfolio composed of bond-equivalents each describing the OTC exposure to a counterparty and associated hedges.

Applying the applicable regulatory market risk charge (IMOD) to the bond-equivalents (i.e. 99% VaR: general + specific risk including stressed VaR but not IRC).

Liquidation horizon = 10 days recognises hedges: eligible, single-name CDS / CCDS or other hedging instrument directly

referencing the counterparty Central Counterparties (CCP) and Securities finance transactions (SFT) are excluded CVAs already recognised by the bank as an incurred write-down, can be used to reduce the

Counterparty Default Risk capital charge (no “double counting”)

18

Now it´s up to you to decide:

1)Was the presentation understandable ?

2)Does it make sense ?

….in any case: it is the end!

19

Many thanks for your attention !

20