Embed Size (px)

Citation preview

CFA Institute Research Challenge Hosted by

Local Challenge CFA Society, Bahrain Bahrain Polytechnic

1

0.15

0.16

0.17

0.18

0.19

0.2

0.21

Zain Bahrain B.S.C. Stock Price Movements Key Highlights

We issued a Hold recommendation on Zain Bahrain B.S.C (Closed) based on the target price of BD 0.178, which could imply a -1.1% expected rate of return from its closing price of BD 0.180 as of December 31, 2015. Zain BH is one of the leading telecommunication operators in the Kingdom of Bahrain. It has an average daily trading volume of 20,000 shares. The recommendation is driven by the following factors:

Negative Growth Drivers: Zain BH has been seeing fluctuations in revenues since 2009. Many

factors have contributed to the change in the company’s performance, mainly economic factors surrounding the Bahraini and the regional economy which has led revenues to drop from BD 93 million in 2009 to BD 71 million in 2015, showing a -5% growth in revenues.

Deteriorating financial performance and positioning: The financial performance analysis of Zain BH highlights lower potential for growth in a penetrated market, with a weak economic outlook and a heavily competitive market. These difficulties are incorporated in declining return on assets and return on capital employed.

Valuation results: An absolute valuation model – discounted cash flow analysis – and relative valuation model using the comparable company multiples approach have been used to estimate the target price of Zain BH. Using a forecast of future financial statements for the next 5 years, the target price for Zain BH is estimated to be at BD 0.178.

Main risk issues to Zain BH: Zain BH is facing multiple risk factors such as control on strategic decisions from MTC group, unfavorable global macro indicators, and a strong competition in a saturated market.

Recent Press Release

Zain Bahrain Announces Rise in Profits By 16.7% During Q3 2015 (19/10/2015) – Zain BH has

announced a 16.7% increase in profits for the nine-month period ended 30 September 2015 to reach BD 3.412 million ($9.026 million) compared to BD 2.924 million ($7.735 million) for the corresponding period in 2014. In addition, Zain BH have recorded a 7.6% decrease in revenues as of September 2015 for the same period from the previous year of 2014 as a result of the defaulted payment by customers.

Zain Bahrain Reflects on Year-end Achievements (05/01/2016) - Zain Bahrain has been rewarded with the ISO 27001:2013 Certification which makes them the first operator in the Middle East to be rewarded with that certificate for their performance in 2015. They have also been awarded with the ‘Middle East Customer Experience Program’ of the year 2015.

Telecommunication Sector, Service Industry

Bahrain Bourse Date: 31/12/2015 Current Price: BD 0.180 at (31/12/15) Recommendation: Hold Ticker - BB: ZAINBH USD 1.00: BD 0.377 Target Price: BD 0.178

Market Profile – Dec 2015

Closing Price BD 0.180

Annual Dividends BD 0.005

52-Week High/Low BD 0.185 – BD 0.162

YTD Change % 2.94%

Average Daily Volume 20,000

Shares Outstanding 368 M

Market Cap 62.560 M

EPS 0.013

EV / EBITDA 15.88x

EV / Sales 0.83x

Source: Bahrain Bourse

Valuation Method

Price Weight

DCF BD 0.175 50%

Multiples BD 0.182 50%

Target Price 0.178

Source: Team Estimates

Key Financials & Ratios 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Total Revenue (in BD’000) 73,533 78,081 71,804 72,050 70,033 68,072 66,166 64,313 Net Profit 13,047 6,409 5,403 4,142 4,581 3,856 3,408 2,355 Gross profit margin 79% 80% 84% 78% 80% 81% 83% 83% Net Profit margin 7% 6% 6% 6% 5% 4% 3% 2% Return on Capital Employed 9% 6% 6% 5% 4% 2% 1% 0%

ARPU (in BD) 0.101 0.091 0.088 0.085 0.080 0.078 0.076 0.073

Current Ratio 0.72 0.71 0.79 0.65 0.70 0.62 0.62 0.70 Total Asset Turnover 0.78 0.65 0.65 0.63 0.60 0.54 0.50 0.47 Account Receivable Turnover 3.85 3.43 3.35 3.20 3.10 2.99 2.88 2.77 Interest Coverage Ratio 17.83 6.28 7.15 5.91 5.10 3.68 2.88 2.03 Net Debt/EBITDA 1.74 1.83 1.59 1.81 1.85 2.19 2.20 2.30 Debt to Equity 1.02 0.88 0.84 0.78 0.76 0.91 0.89 0.88 Dividend Payout Ratio 1.18 1.37 0.80 0.29 0.31 0.42 0.54 0.88

Source: Team Estimates

Key Ratios Dec

2015

Dividend per share BD 0.005

Price to book value 1.23x

Price to earnings ratio 15.38x

Dividend Payout ratio 44.42%

Dividend Yield 2.50%

Return on Equity 6.95%

Return on Assets 3.70%

Equity to total assets 53.20%

Liabilities to total equity

0.88x

Source: Bahrain Bourse

This report is published for educational purposes only by

students competing in The CFA Institute Research

Challenge

BD

Source: Bahrain Bourse

Target Price = BD 0.178

2

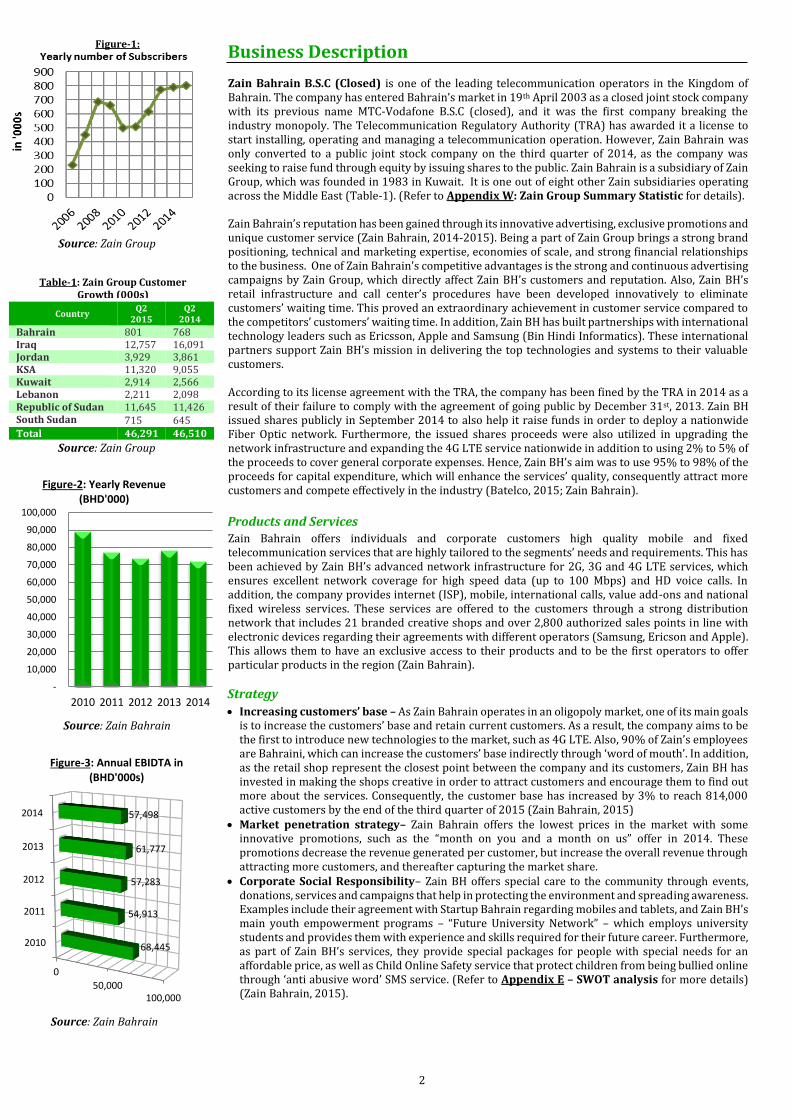

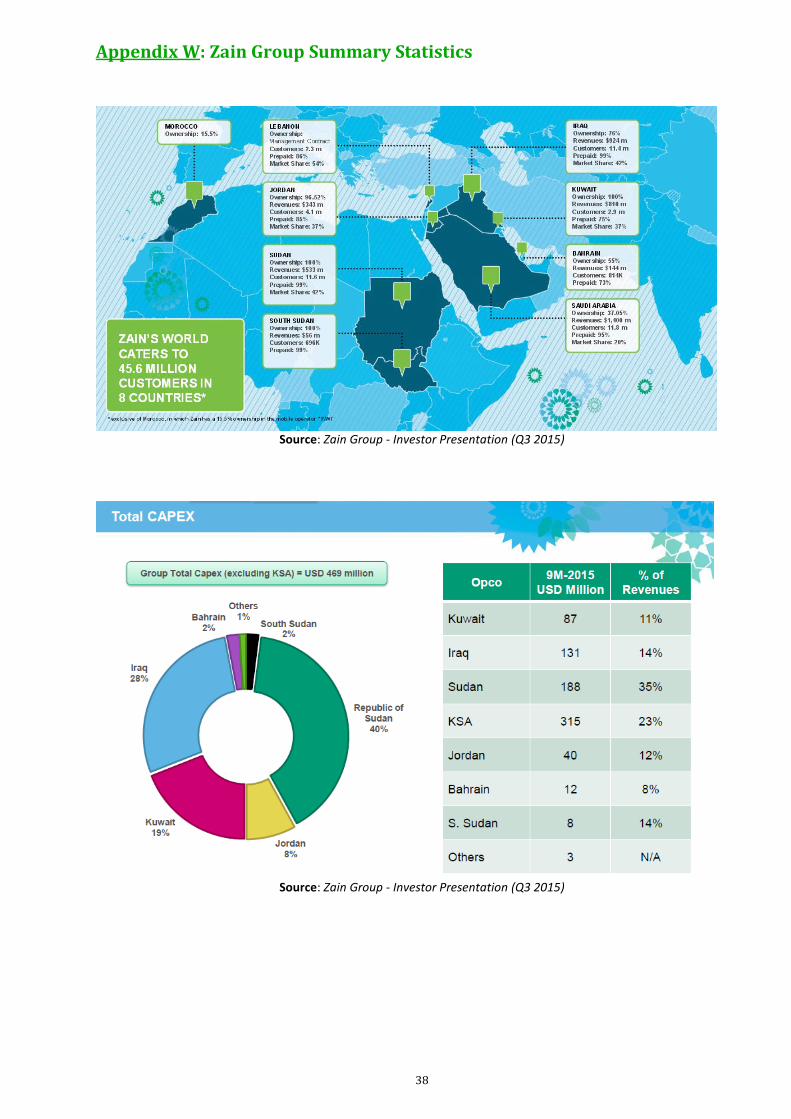

Business Description Zain Bahrain B.S.C (Closed) is one of the leading telecommunication operators in the Kingdom of Bahrain. The company has entered Bahrain’s market in 19th April 2003 as a closed joint stock company with its previous name MTC-Vodafone B.S.C (closed), and it was the first company breaking the industry monopoly. The Telecommunication Regulatory Authority (TRA) has awarded it a license to start installing, operating and managing a telecommunication operation. However, Zain Bahrain was only converted to a public joint stock company on the third quarter of 2014, as the company was seeking to raise fund through equity by issuing shares to the public. Zain Bahrain is a subsidiary of Zain Group, which was founded in 1983 in Kuwait. It is one out of eight other Zain subsidiaries operating across the Middle East (Table-1). (Refer to Appendix W: Zain Group Summary Statistic for details). Zain Bahrain’s reputation has been gained through its innovative advertising, exclusive promotions and unique customer service (Zain Bahrain, 2014-2015). Being a part of Zain Group brings a strong brand positioning, technical and marketing expertise, economies of scale, and strong financial relationships to the business. One of Zain Bahrain’s competitive advantages is the strong and continuous advertising campaigns by Zain Group, which directly affect Zain BH’s customers and reputation. Also, Zain BH’s retail infrastructure and call center’s procedures have been developed innovatively to eliminate customers’ waiting time. This proved an extraordinary achievement in customer service compared to the competitors’ customers’ waiting time. In addition, Zain BH has built partnerships with international technology leaders such as Ericsson, Apple and Samsung (Bin Hindi Informatics). These international partners support Zain BH’s mission in delivering the top technologies and systems to their valuable customers. According to its license agreement with the TRA, the company has been fined by the TRA in 2014 as a result of their failure to comply with the agreement of going public by December 31st, 2013. Zain BH issued shares publicly in September 2014 to also help it raise funds in order to deploy a nationwide Fiber Optic network. Furthermore, the issued shares proceeds were also utilized in upgrading the network infrastructure and expanding the 4G LTE service nationwide in addition to using 2% to 5% of the proceeds to cover general corporate expenses. Hence, Zain BH’s aim was to use 95% to 98% of the proceeds for capital expenditure, which will enhance the services’ quality, consequently attract more customers and compete effectively in the industry (Batelco, 2015; Zain Bahrain).

Products and Services Zain Bahrain offers individuals and corporate customers high quality mobile and fixed telecommunication services that are highly tailored to the segments’ needs and requirements. This has been achieved by Zain BH’s advanced network infrastructure for 2G, 3G and 4G LTE services, which ensures excellent network coverage for high speed data (up to 100 Mbps) and HD voice calls. In addition, the company provides internet (ISP), mobile, international calls, value add-ons and national fixed wireless services. These services are offered to the customers through a strong distribution network that includes 21 branded creative shops and over 2,800 authorized sales points in line with electronic devices regarding their agreements with different operators (Samsung, Ericson and Apple). This allows them to have an exclusive access to their products and to be the first operators to offer particular products in the region (Zain Bahrain).

Strategy

Increasing customers’ base – As Zain Bahrain operates in an oligopoly market, one of its main goals is to increase the customers’ base and retain current customers. As a result, the company aims to be the first to introduce new technologies to the market, such as 4G LTE. Also, 90% of Zain’s employees are Bahraini, which can increase the customers’ base indirectly through ‘word of mouth’. In addition, as the retail shop represent the closest point between the company and its customers, Zain BH has invested in making the shops creative in order to attract customers and encourage them to find out more about the services. Consequently, the customer base has increased by 3% to reach 814,000 active customers by the end of the third quarter of 2015 (Zain Bahrain, 2015)

Market penetration strategy– Zain Bahrain offers the lowest prices in the market with some innovative promotions, such as the “month on you and a month on us” offer in 2014. These promotions decrease the revenue generated per customer, but increase the overall revenue through attracting more customers, and thereafter capturing the market share.

Corporate Social Responsibility– Zain BH offers special care to the community through events, donations, services and campaigns that help in protecting the environment and spreading awareness. Examples include their agreement with Startup Bahrain regarding mobiles and tablets, and Zain BH’s main youth empowerment programs – “Future University Network” – which employs university students and provides them with experience and skills required for their future career. Furthermore, as part of Zain BH’s services, they provide special packages for people with special needs for an affordable price, as well as Child Online Safety service that protect children from being bullied online through ‘anti abusive word’ SMS service. (Refer to Appendix E – SWOT analysis for more details) (Zain Bahrain, 2015).

Country Q2

2015 Q2

2014

Bahrain 801 768 Iraq 12,757 16,091 Jordan 3,929 3,861 KSA 11,320 9,055 Kuwait 2,914 2,566 Lebanon 2,211 2,098 Republic of Sudan 11,645 11,426 South Sudan 715 645 Total 46,291 46,510

Source: Zain Group

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2010 2011 2012 2013 2014

Figure-2: Yearly Revenue (BHD'000)

Source: Zain Bahrain

0

50,000100,000

2010

2011

2012

2013

2014

68,445

54,913

57,283

61,777

57,498

Figure-3: Annual EBIDTA in (BHD'000s)

Source: Zain Bahrain

Table-1: Zain Group Customer Growth (000s)

Source: Zain Group

Figure-1:

3

Management and Governance

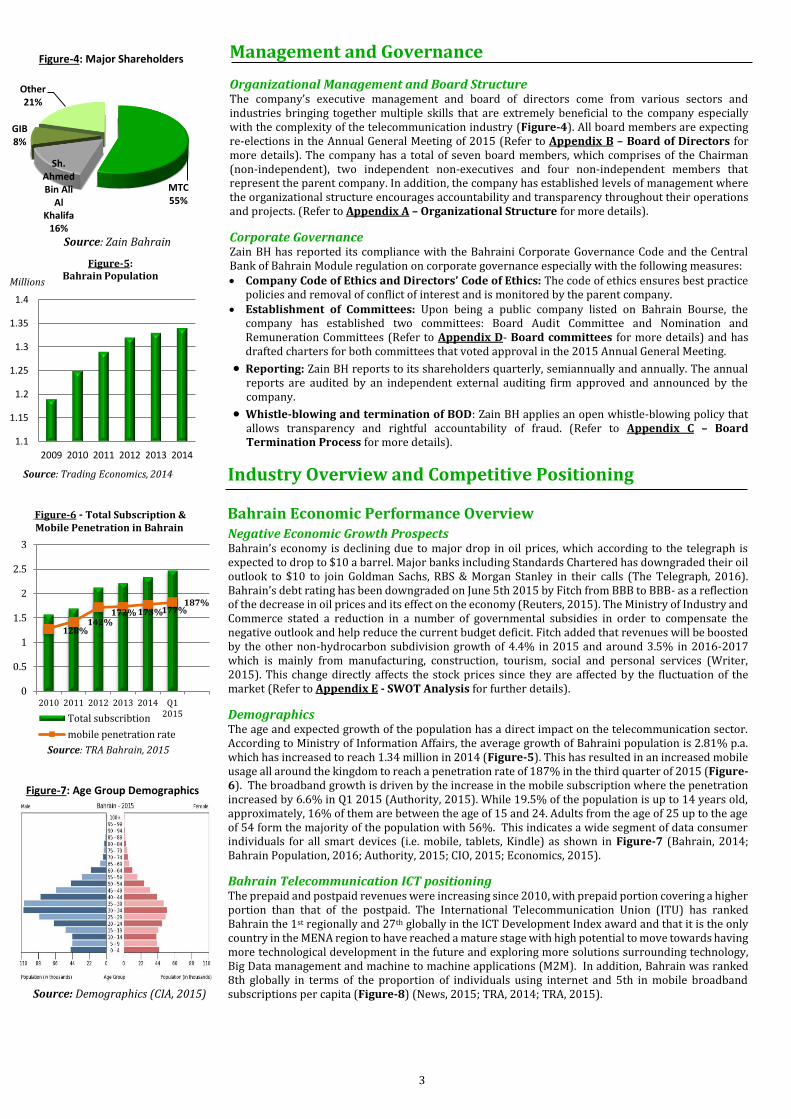

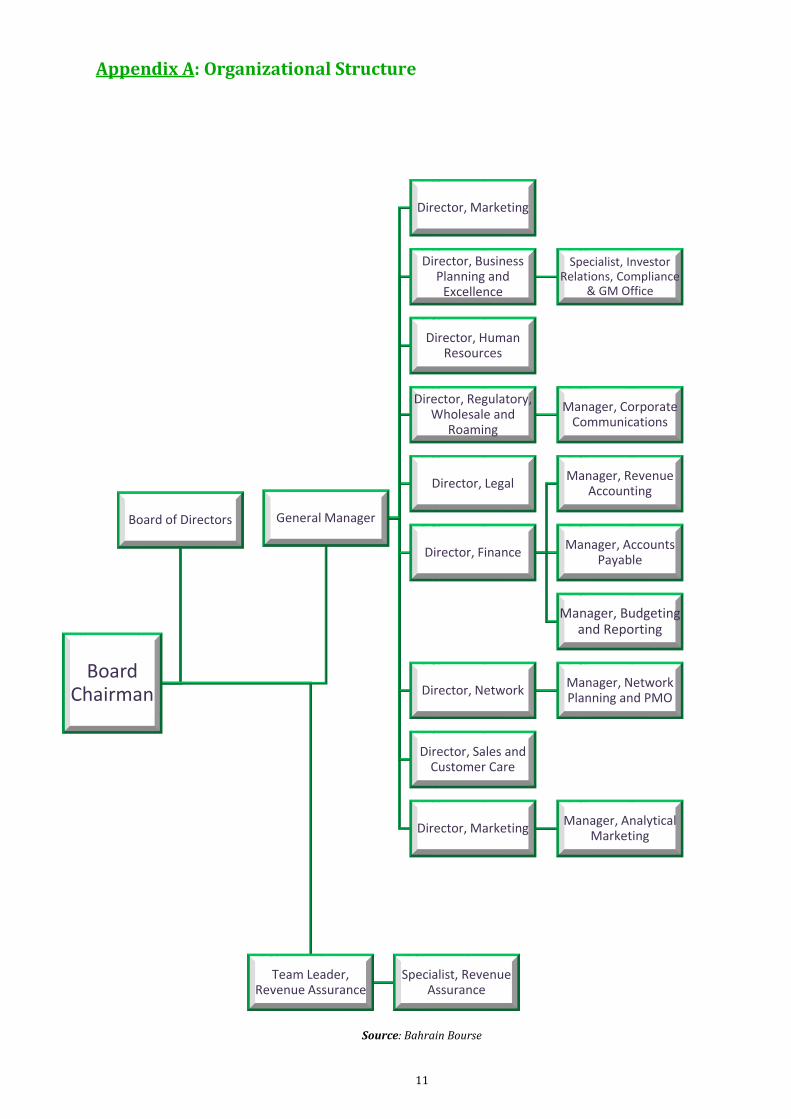

Organizational Management and Board Structure The company’s executive management and board of directors come from various sectors and industries bringing together multiple skills that are extremely beneficial to the company especially with the complexity of the telecommunication industry (Figure-4). All board members are expecting re-elections in the Annual General Meeting of 2015 (Refer to Appendix B – Board of Directors for more details). The company has a total of seven board members, which comprises of the Chairman (non-independent), two independent non-executives and four non-independent members that represent the parent company. In addition, the company has established levels of management where the organizational structure encourages accountability and transparency throughout their operations and projects. (Refer to Appendix A – Organizational Structure for more details).

Corporate Governance Zain BH has reported its compliance with the Bahraini Corporate Governance Code and the Central Bank of Bahrain Module regulation on corporate governance especially with the following measures: Company Code of Ethics and Directors’ Code of Ethics: The code of ethics ensures best practice

policies and removal of conflict of interest and is monitored by the parent company. Establishment of Committees: Upon being a public company listed on Bahrain Bourse, the

company has established two committees: Board Audit Committee and Nomination and Remuneration Committees (Refer to Appendix D- Board committees for more details) and has drafted charters for both committees that voted approval in the 2015 Annual General Meeting.

Reporting: Zain BH reports to its shareholders quarterly, semiannually and annually. The annual reports are audited by an independent external auditing firm approved and announced by the company.

Whistle-blowing and termination of BOD: Zain BH applies an open whistle-blowing policy that allows transparency and rightful accountability of fraud. (Refer to Appendix C – Board Termination Process for more details).

Industry Overview and Competitive Positioning Bahrain Economic Performance Overview

Negative Economic Growth Prospects Bahrain’s economy is declining due to major drop in oil prices, which according to the telegraph is expected to drop to $10 a barrel. Major banks including Standards Chartered has downgraded their oil outlook to $10 to join Goldman Sachs, RBS & Morgan Stanley in their calls (The Telegraph, 2016). Bahrain’s debt rating has been downgraded on June 5th 2015 by Fitch from BBB to BBB- as a reflection of the decrease in oil prices and its effect on the economy (Reuters, 2015). The Ministry of Industry and Commerce stated a reduction in a number of governmental subsidies in order to compensate the negative outlook and help reduce the current budget deficit. Fitch added that revenues will be boosted by the other non-hydrocarbon subdivision growth of 4.4% in 2015 and around 3.5% in 2016-2017 which is mainly from manufacturing, construction, tourism, social and personal services (Writer, 2015). This change directly affects the stock prices since they are affected by the fluctuation of the market (Refer to Appendix E - SWOT Analysis for further details).

Demographics The age and expected growth of the population has a direct impact on the telecommunication sector. According to Ministry of Information Affairs, the average growth of Bahraini population is 2.81% p.a. which has increased to reach 1.34 million in 2014 (Figure-5). This has resulted in an increased mobile usage all around the kingdom to reach a penetration rate of 187% in the third quarter of 2015 (Figure-6). The broadband growth is driven by the increase in the mobile subscription where the penetration increased by 6.6% in Q1 2015 (Authority, 2015). While 19.5% of the population is up to 14 years old, approximately, 16% of them are between the age of 15 and 24. Adults from the age of 25 up to the age of 54 form the majority of the population with 56%. This indicates a wide segment of data consumer individuals for all smart devices (i.e. mobile, tablets, Kindle) as shown in Figure-7 (Bahrain, 2014; Bahrain Population, 2016; Authority, 2015; CIO, 2015; Economics, 2015).

Bahrain Telecommunication ICT positioning The prepaid and postpaid revenues were increasing since 2010, with prepaid portion covering a higher portion than that of the postpaid. The International Telecommunication Union (ITU) has ranked Bahrain the 1st regionally and 27th globally in the ICT Development Index award and that it is the only country in the MENA region to have reached a mature stage with high potential to move towards having more technological development in the future and exploring more solutions surrounding technology, Big Data management and machine to machine applications (M2M). In addition, Bahrain was ranked 8th globally in terms of the proportion of individuals using internet and 5th in mobile broadband subscriptions per capita (Figure-8) (News, 2015; TRA, 2014; TRA, 2015).

MTC 55%

Sh. Ahmed Bin Ali

Al Khalifa

16%

GIB 8%

Other 21%

Figure-4: Major Shareholders

Source: Zain Bahrain

Source: Demographics (CIA, 2015)

Figure-7: Age Group Demographics

Source: TRA Bahrain, 2015

128%142%

172% 173%177%187%

0

0.5

1

1.5

2

2.5

3

2010 2011 2012 2013 2014 Q12015Total subscribtion

mobile penetration rate

Figure-6 - Total Subscription & Mobile Penetration in Bahrain

1.1

1.15

1.2

1.25

1.3

1.35

1.4

2009 2010 2011 2012 2013 2014

Figure-5:Bahrain Population

Millions

Source: Trading Economics, 2014

4

External Influencers Affecting the Telecommunication Market There are several external factors that could have significant effects on the telecommunication market which includes the following: Political Issues: The Bahraini market faces occasional political unrest that increases the data

consumption due to increased news exchange and communication. Subsidy Cuts: The reduction of governmental subsidies and increase in fuel prices by 60% could

decrease consumer spending and lead to lower demand on telecommunication services. Regulatory Considerations: The TRA regulations enforce price reduction in certain telecom

services that may cost the companies a partial loss of their revenues in the short run. Companies will also have to invest in more environment-friendly devices while regulating the radiations level. Despite the short-term cost, those regulations are found to have long-term benefits for the company and assist in retaining their clients.

Consumer Preferences: The recent TRA report shows that customers’ are shifting their preference to postpaid services over prepaid service and this may require Zain BH to promote fixed-amount installments-based packages that suite with the clients’ needs. Prepaid packages are used currently by Zain BH, VIVA and Batelco. The cost is BD 1 per week. (Refer to Table-M1 in Appendix M – Market analysis and Appendix F - PESTEL Analysis for a more detailed analysis.)

Competitive Positioning

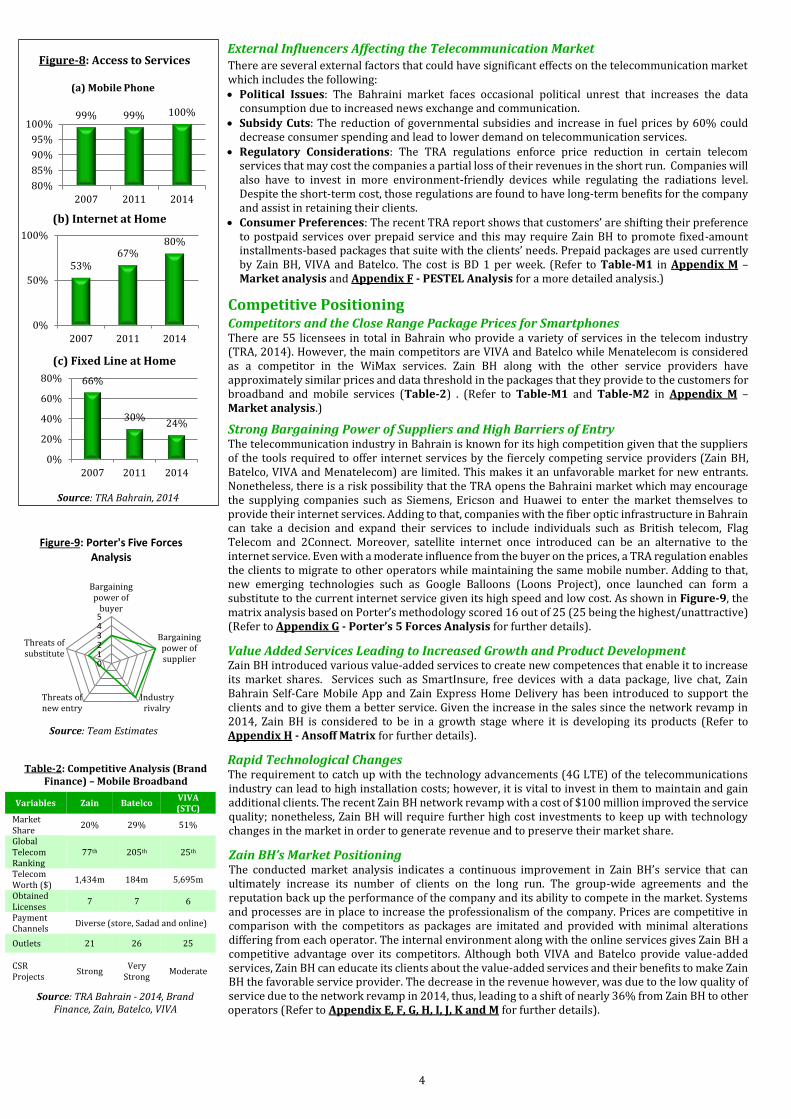

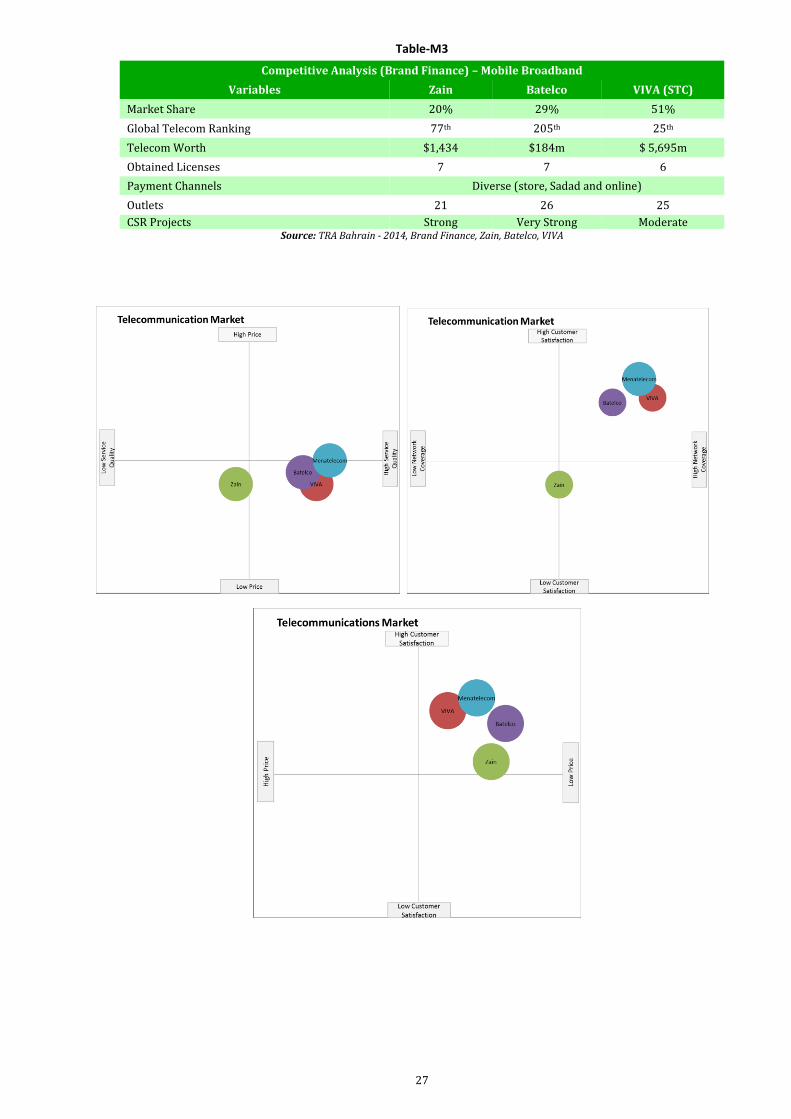

Competitors and the Close Range Package Prices for Smartphones There are 55 licensees in total in Bahrain who provide a variety of services in the telecom industry (TRA, 2014). However, the main competitors are VIVA and Batelco while Menatelecom is considered as a competitor in the WiMax services. Zain BH along with the other service providers have approximately similar prices and data threshold in the packages that they provide to the customers for broadband and mobile services (Table-2) . (Refer to Table-M1 and Table-M2 in Appendix M – Market analysis.)

Strong Bargaining Power of Suppliers and High Barriers of Entry The telecommunication industry in Bahrain is known for its high competition given that the suppliers of the tools required to offer internet services by the fiercely competing service providers (Zain BH, Batelco, VIVA and Menatelecom) are limited. This makes it an unfavorable market for new entrants. Nonetheless, there is a risk possibility that the TRA opens the Bahraini market which may encourage the supplying companies such as Siemens, Ericson and Huawei to enter the market themselves to provide their internet services. Adding to that, companies with the fiber optic infrastructure in Bahrain can take a decision and expand their services to include individuals such as British telecom, Flag Telecom and 2Connect. Moreover, satellite internet once introduced can be an alternative to the internet service. Even with a moderate influence from the buyer on the prices, a TRA regulation enables the clients to migrate to other operators while maintaining the same mobile number. Adding to that, new emerging technologies such as Google Balloons (Loons Project), once launched can form a substitute to the current internet service given its high speed and low cost. As shown in Figure-9, the matrix analysis based on Porter’s methodology scored 16 out of 25 (25 being the highest/unattractive) (Refer to Appendix G - Porter’s 5 Forces Analysis for further details).

Value Added Services Leading to Increased Growth and Product Development Zain BH introduced various value-added services to create new competences that enable it to increase its market shares. Services such as SmartInsure, free devices with a data package, live chat, Zain Bahrain Self-Care Mobile App and Zain Express Home Delivery has been introduced to support the clients and to give them a better service. Given the increase in the sales since the network revamp in 2014, Zain BH is considered to be in a growth stage where it is developing its products (Refer to Appendix H - Ansoff Matrix for further details).

Rapid Technological Changes The requirement to catch up with the technology advancements (4G LTE) of the telecommunications industry can lead to high installation costs; however, it is vital to invest in them to maintain and gain additional clients. The recent Zain BH network revamp with a cost of $100 million improved the service quality; nonetheless, Zain BH will require further high cost investments to keep up with technology changes in the market in order to generate revenue and to preserve their market share.

Zain BH’s Market Positioning The conducted market analysis indicates a continuous improvement in Zain BH’s service that can ultimately increase its number of clients on the long run. The group-wide agreements and the reputation back up the performance of the company and its ability to compete in the market. Systems and processes are in place to increase the professionalism of the company. Prices are competitive in comparison with the competitors as packages are imitated and provided with minimal alterations differing from each operator. The internal environment along with the online services gives Zain BH a competitive advantage over its competitors. Although both VIVA and Batelco provide value-added services, Zain BH can educate its clients about the value-added services and their benefits to make Zain BH the favorable service provider. The decrease in the revenue however, was due to the low quality of service due to the network revamp in 2014, thus, leading to a shift of nearly 36% from Zain BH to other operators (Refer to Appendix E, F, G, H, I, J, K and M for further details).

Variables Zain Batelco VIVA (STC)

Market Share

20% 29% 51%

Global Telecom Ranking

77th 205th 25th

Telecom Worth ($)

1,434m 184m 5,695m

Obtained Licenses

7 7 6

Payment Channels

Diverse (store, Sadad and online)

Outlets 21 26 25

CSR Projects

Strong Very

Strong Moderate

Table-2: Competitive Analysis (Brand Finance) – Mobile Broadband

Source: TRA Bahrain - 2014, Brand Finance, Zain, Batelco, VIVA

012345

Bargainingpower of

buyer

Bargainingpower ofsupplier

Industryrivalry

Threats ofnew entry

Threats ofsubstitute

Figure-9: Porter's Five Forces Analysis

Source: Team Estimates

Source: TRA Bahrain, 2014

99% 99% 100%

80%

85%

90%

95%

100%

2007 2011 2014

(a) Mobile Phone

53%67%

80%

0%

50%

100%

2007 2011 2014

(b) Internet at Home

66%

30%24%

0%

20%

40%

60%

80%

2007 2011 2014

(c) Fixed Line at Home

Figure-8: Access to Services

5

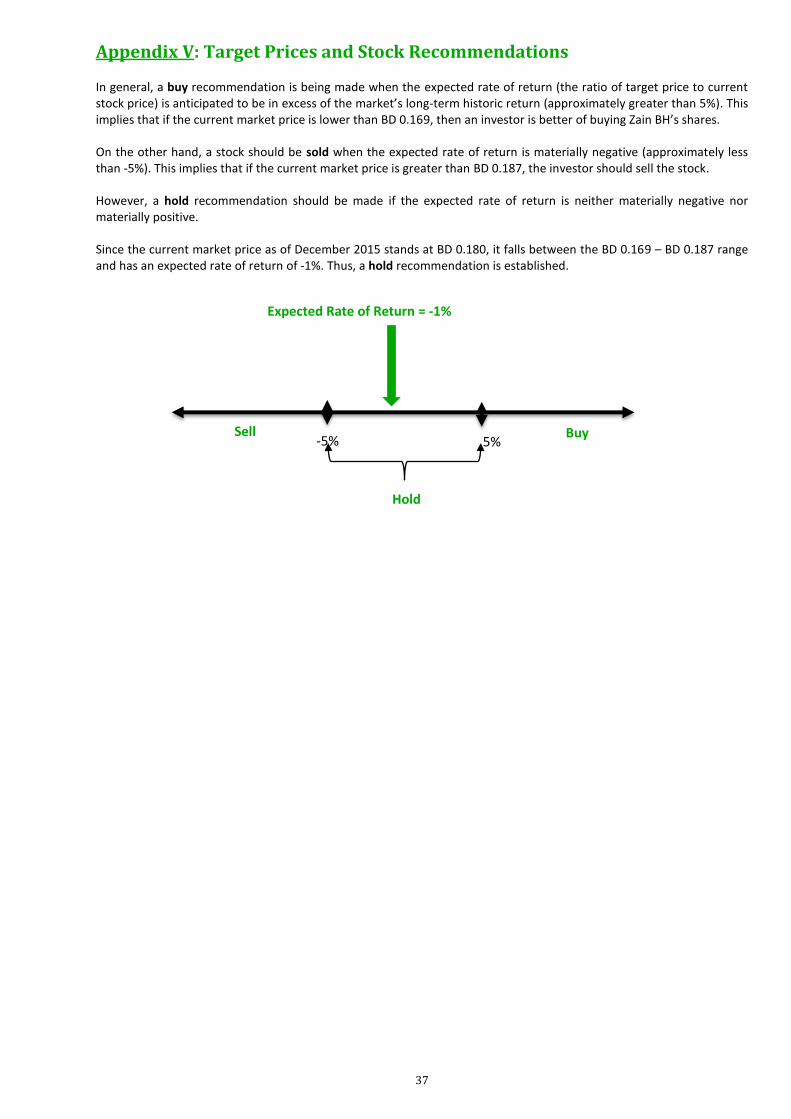

Investment Summary For Zain BH, we issue a Hold recommendation as the target price of BD 0.178 is only slightly lower than the market price of BD 0.180 as of December 2015 (Appendix V – Target Prices and Stock Recommendations). This implies a -1.1% expected rate of return from its closing price, which in absolute terms is not materially large. This recommendation is supported by the information mentioned herein.

Valuation Methods The target price is derived by combining two methods, namely the discounted cash flow model (DCF) and the multiples approach using comparable. For the DCF analysis, cash flows has been forecasted and discounted to arrive at a target price of BD 0.175. For the multiples approach, several multiples using regional peer group in the telecommunication industry with comparable attributes has been selected to arrive at a target price of BD 0.182. Calculating an average of the two methods implies a target price of BD 0.178. Equal weights have been applied to each method as there is no reason as to why a specific treatment should be giving to any of the two methods (Table-3).

Weakening Economic Outlook The 2015 developments in the Bahraini market and the regional changes due to the severe decrease in oil prices has affected Zain BH and its competitors. Consumer spending is expected to decrease due to inflation of necessity prices, especially octane fuel price which has increased in early 2016. Government reforms and budget cuts in government spending, salaries and economic development show less confidence in investing in the Bahraini market, especially for 2016. The oil prices are expected to decrease further to $10 per barrel which will continuously affect the Bahraini economy and Zain BH. The Bahraini decision of following the US interest rates hike will also impose negative possibilities on the market and the economic future (Figure-10).

Highly Penetrated Market Zain BH is competing with several communication companies with a 187% penetration rate of the Bahraini telecommunication sector, reducing the ability of Zain BH to acquire market share easily. They should thus increase their focus on quality of services provided rather than the existence of the service. With customers shifting away from Zain BH and the fluctuation in customer base since 2009 with slow growth due to poor quality and assumed higher prices, it has become difficult for Zain BH to generate more profits. As a telecommunication operator, it is extremely difficult to operate within a highly penetrated market especially that Zain BH is operating in a relatively small populated country. The company should thus strive for developments in technology to advance over competitors.

Lack of Growth Potential Zain BH is a subsidiary of a parent company, Zain Group. This imposes great limitations on growth across borders and growth to other services. Zain BH is one of the smallest and least profit generating subsidiary contributing to the parent company, as its customer base is only 814,000 customers out of 46 million total customers of all subsidiaries of the group. The company has not been showing significant growth in customer base, in fact, it has been reported by TRA that many customer only shift to Zain BH to acquire smart phone devices, then leaving the company for its competitors.

Decline in Voice Revenues Although data revenues are expected to increase, the massive decrease in voice revenues will not be compensated; as more and more users are shifting towards internet and Voice-over-Internet-Protocol (VoIP) for calls or texting, the sales generated from voice and SMS will see a dramatic decrease. The forecasted revenue decline in 2016-2020 is affected by the decline in voice. Despite that Zain BH’s has showed great efforts in campaigns for its data services, the data growth remains stable and insignificant to overcome issues arising from loss in voice revenue.

Bahraini Market Competitive Advantage The competition is high in the market between the internet service providers in Bahrain. The prices offered by the service providers (Batelco, VIVA and Zain BH) are relatively close to each other. More customers are recently preferring prepaid services as they favor having a fixed payment rather than an open bill at the end of the month. The customers choose the provider based on the service quality and thus high speed internet and value added services determine which provider to choose. Zain BH only holds 20% of the market which is relatively low in comparison to 29% for Batelco and 51% for VIVA (Figure-12). Given the similar packages that are provided with the same price, it is unlikely that the customers will favor Zain BH over the other telecom providers especially that Zain BH had a reputation of not delivering high speed internet to the clients, and thus, it is hard to attract more clients in the short-run.

Zain BH Share Prices and Stock Analysis Zain BH’s stocks were being sold at around BD 0.200 when they initially went public in 2014. The shares then increased slightly after being publicly offered to reach a cap of BD 0.204. However, market events

Valuation Method

Price Weight

DCF BD 0.175 50%

Multiples BD 0.182 50%

Target Price 0.178

Source: Team Estimates

20%

29%

51%

Figure-12: Market Share

Zain BH Batelco VIVA

Source: Team Estimates

0 100 200

2013

2014

2015

2016E

2017E

2018E

2019E

2020E

Figure-11: Average Revenue Per User

Source: Zain BH, Team Estimates

Source: TRA Bahrain, 2014

Table-3: Estimation of Target Price

5

4.5

54

5

3.5

012345

Technological Changes

Governmental Taxes

MarketPrices

NetworkOverload

FierceCompetition

TRARegulations

Figure-10: SWOT Analysis -Threats

6

have caused the stock price to fluctuate since then, and the company faced a decrease in their prices with the biggest drop encountered on November 16th 2015 leading it to reach BD 0.162 per share. This was a reflection of the decreasing share prices in Bahrain Bourse as a result of the news relating to the decrease in oil prices, which reflected badly not only on Zain BH, but on the region as a whole. Zain BH stocks have decreased by -88% over one year and stands at BD 0.180 on 31st December 2015. The stock has an average trading volume of 20,000 shares (Bahrain Bourse, 2015). (Refer to Appendix-K: Stock Price Analysis for more details)

Financial Analysis

Overview The financial ratio analysis chart above sheds the light on Zain BH’s future prospects, revealing the historical and future expected trend in profitability, liquidity, efficiency and solvency ratios. The starting point of the analysis has been pushed backward to 2009 in order to gain a full image of the declining financial trend (Figure-14). Thus, the financial analysis of Zain BH is conducted using data from the years 2009 to 2015, the reason being that the previous years has faced several political and financial crisis and thus a longer period can better capture a whole business cycle.

Financial Ratio 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

Profitability

Gross profit margin 79% 80% 84% 78% 80% 81% 83% 83%

Net Profit margin 7% 6% 6% 6% 5% 4% 3% 2%

Return on Capital Employed 9% 6% 6% 5% 4% 2% 1% 0%

EBITDA Margin 38% 38% 39% 37% 39% 40% 42% 42%

Return on Asset 20% 13% 14% 11% 10% 5% 3% 0%

ARPU (BD) 0.101 0.091 0.088 0.085 0.080 0.078 0.076 0.073

Liquidity

Current Ratio 0.72 0.71 0.79 0.65 0.70 0.62 0.62 0.70

Acid test ratio 0.64 0.65 0.73 0.59 0.61 0.52 0.48 0.50

Efficiency

Total Asset Turnover 0.78 0.65 0.65 0.63 0.60 0.54 0.50 0.47

Inventory Turnover 7.14 5.61 5.30 6.92 4.76 3.06 1.84 1.22

Account Receivable Turnover 3.85 3.43 3.35 3.20 3.10 2.99 2.88 2.77

Solvency

Debt to Assets 0.51 0.47 0.46 0.44 0.43 0.48 0.47 0.47

Interest Coverage Ratio 17.83 6.28 7.15 5.91 5.10 3.68 2.88 2.03

Net Debt/EBITDA 1.74 1.83 1.59 1.81 1.85 2.19 2.20 2.30

Debt to Equity 1.02 0.88 0.84 0.78 0.76 0.91 0.89 0.88

Shareholder Ratios

Dividend Payout Ratio 1.18 1.37 0.80 0.29 0.31 0.42 0.54 0.88 Source: Zain Bahrain

Figure-13: Zain BH’s Stock Price Movement

Net Profit

2009 27917

2010 21872

2011 13,047

2012 6,409

2013 5,403

2014 4,142

2015 4,581

Figure-14: Net Income in BD

7

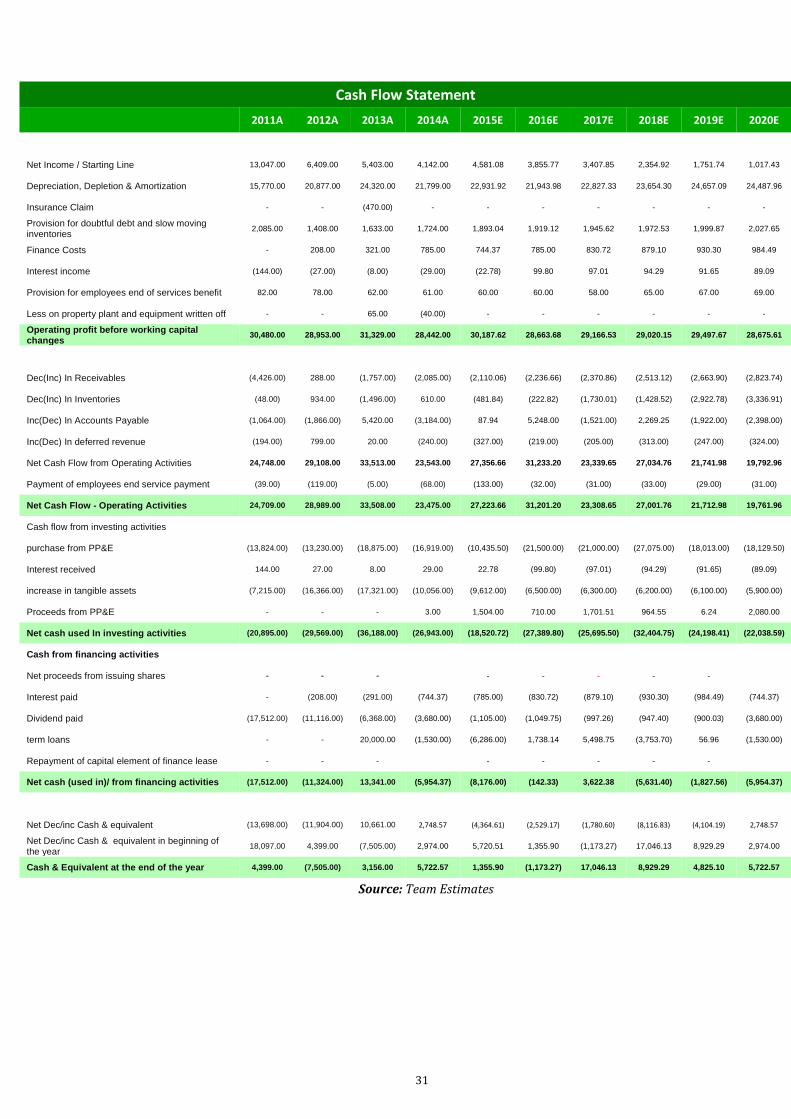

Unfavorable Oil Prices and Declining Government Spending Weakens Sales Revenue The fall in oil prices in the global market affects Bahrain’s economy negatively. In addition, the uplifting of a number of governmental subsidies and the decrease in GDP has led to fluctuations in goods’ prices since July 2015. In particular, the new government’s announcement of removing subsidies on meat led to its increase of 125.8% since October 2015. This results in a decrease in customers spending and is considered to directly affect the revenue of Zain BH. Hence, gradual decrease in revenues is built into the forecasts for the next five years, as well as the decrease in Zain BH’s profitability ratios. The fall in subscriber base is also assumed to be due to the reduction in the purchasing power of customers. This fall of revenues are estimated in the forecasted year of 2016 at BD 71 million down by 10% to reach BD 62 million in 2020 (Trading Economics, 2015; The National Business, 2015).

Hiking Interest Rate Limits Financing Options Flexibility The continuous increase in interest rate is expected to affect Zain BH’s ability and opportunity to finance its operations and upgrade its services through debt. In the forecasted period of 2018, Zain BH is expected to take a loan of BD 20 million (See Appendix U – Financial Forecast of Working Loans) for expanding and upgrading its network towers to keep up with the latest technology and be competitive in the market. However, the high interest rate will result in increased cost of debt, which will affect management’s future decision when examining investment opportunities and negatively impact the NOI of the company. Moreover, this might push Zain BH to seek additional funding through equity, as a more secured option. However, due to high amount of overdraft that Zain BH is utilizing, it is estimated that the debt to equity ratio for the forecasted years of 2016-2020 will rise from 0.78 in 2016 to 0.88 in 2020 as per the forecasted financial statements.

Penetrated Market Forces Zain BH to Upgrade Business Products The Bahrain telecommunication market is very competitive, resulting in a penetration rate of 187% as of Q3 2015. Considering the aggressive nature of this industry, Zain BH needs to focus on increasing its customers’ base and thus, like other industry players, Zain BH will have to retain its customers and increase their market share via attracting customers from the other operators through attractive offers and the diversification of their services. An example of that is Zain BH’s current involvement in the new agreement of the Radio Dot system which aims at providing improved voice clarity. Thus, rather than relying on mobile phone as the main revenue source, Zain BH is expected to get involved in several new agreements in the future. Consequently, an upgrade to network service and SAP service in 2020 has been considered in the preparation of the forecast (Bahrain Bourse, 2015).

DuPont Analysis – ROE Decomposition By analyzing the historical data of Zain BH, it is observed that the company has exhibited a declining trend in its return on equity (ROE) which stood at 35% in 2010 to reach 7.61% by 2015. This gradual decline in ROE is directly related to the gradual decline in the net profit margin throughout the period of 2009-2015. For the forecasted period, the ROE falls down to reach 1% as of 2020. Similar to the historical period, the main driver behind this decline is the fall in the net profit margin. Several macroeconomic factors such as decreasing oil prices, increasing competition and reduction in customer purchasing power is expected to lead to a fall in revenues. Without a similar reduction in costs, the company’s forecasted net profit falls year-on-year. Hence, Zain BH is assumed to be able to generate less profit for every unit of revenue. The second driver appears to be the equity multiplier or financial leverage, which is the ratio of total assets to total equity. Thus the forecasted increase in equity without a subsequent increase in the total assets impacts the ROE negatively.

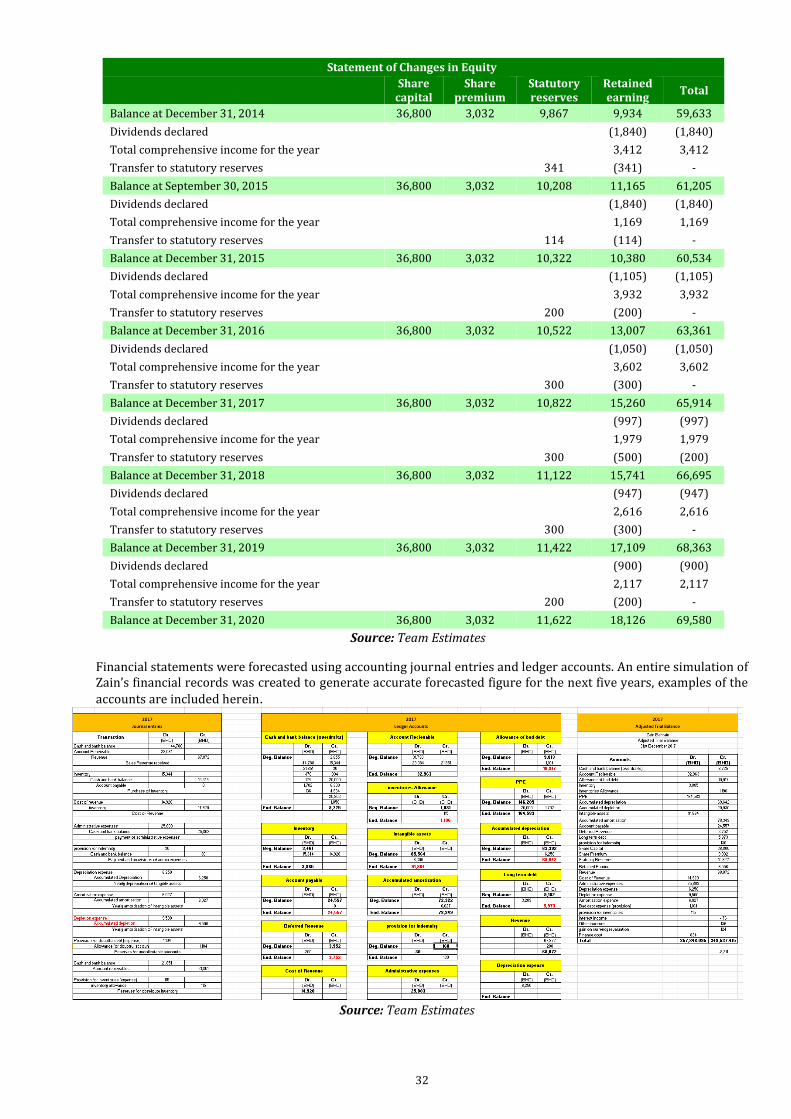

Cash Generating Capabilities During the historical period from 2011-2015, it can be observed that Zain BH had the highest CFO in 2013 (BD 33.5m) after a constant yearly growth of around 16.5% from 2011, which highlights the economy’s recovery from the political instability effect and the well-organized investment strategies by Zain BH. In particular, Zain BH encountered a huge ending cash flow decline of 271% in 2012, resulting in a net cash outflow and forcing it to take loans worth BD 20m in the following year, where the funds were invested in upgrading PPE and intangible assets to recover the CFO by 36% compared to 2011 (Figure-18). In addition, the CFO decreased by 30% in 2014 due to the TRA law that allowed customers to shift the service provider without changing the SIM number, thus affecting Zain BH’s negatively. On the other hand, it was assumed that from 2015, Zain BH will start paying back its debt resulting in cash outflow to 2020. Furthermore, although the economic crisis started in 2015, Zain BH will be mostly affected in 2017 by a 25% reduction in CFO. Yet, the NCF has increased in this period due to management decisions of being less reliant on cash, control investments spending and postpone some investments to the following year. Additionally, the CFO will only increase from BD 4.825 million to BD 5.722 million in 2020, due to low investments that may affect its position in the competitive market.

DuPont Analysis 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

Net Profit margin 7% 6% 6% 6% 5% 4% 3% 2%

Total Asset Turnover 73% 64% 65% 62% 59% 52% 49% 47%

Equity Multiplier 202% 188% 184% 178% 176% 191% 189% 188%

ROE 10% 7% 8% 6% 5% 4% 3% 1%

Source: Zain Bahrain, Team Estimates

Source: Zain Bahrain, Team Estimates

34% 41%51% 47% 46% 44%

66% 59%49% 53% 54% 56%

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014 2015

Figure-16: Debt/Equity

Equity

Debt

DEBT to Equity

Figure-17: DuPont Analysis

Source: Zain Bahrain, Team Estimates

(25,000)

(15,000)

(5,000)

5,000

15,000

25,000

35,000

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Figure-18: Cash Flow Trend

Net Cash flows

Cash flow from Financing Activities

Cash flow from Investing Activities

Cash flow from Operation Activities

6400

5280

1840

10501050 997 947 900

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000Figure-15: Dividends Payout

8

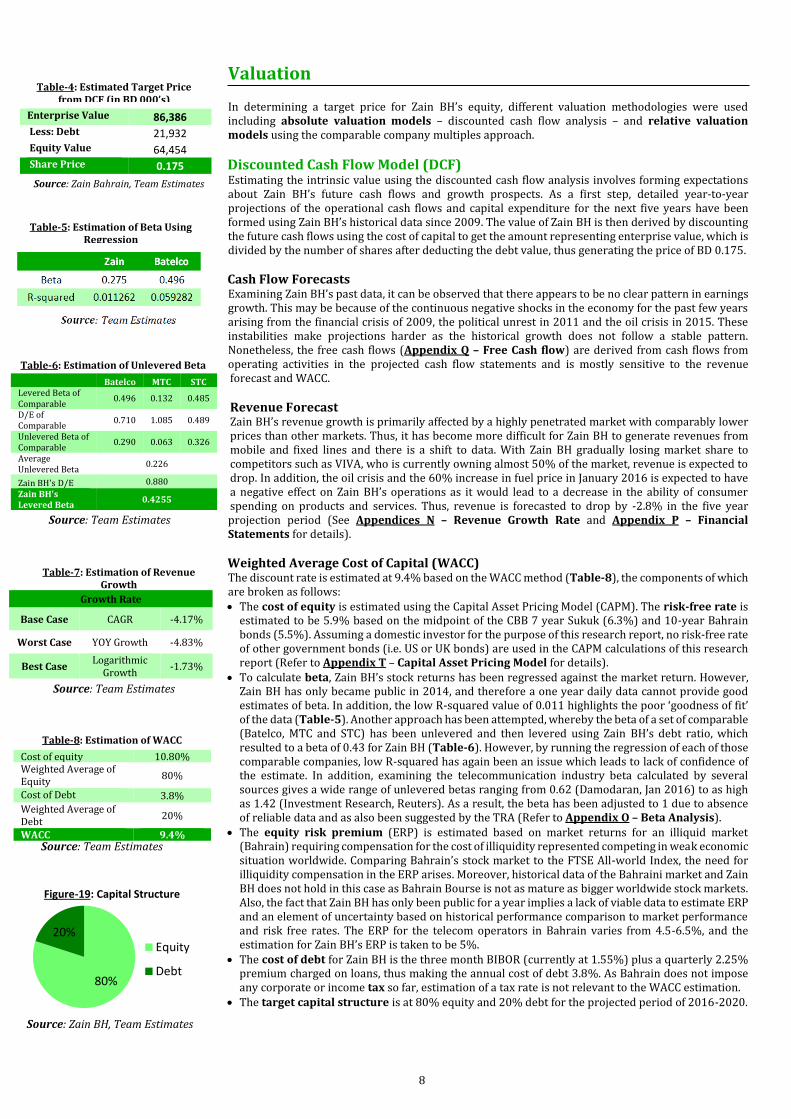

Valuation

In determining a target price for Zain BH’s equity, different valuation methodologies were used including absolute valuation models – discounted cash flow analysis – and relative valuation models using the comparable company multiples approach.

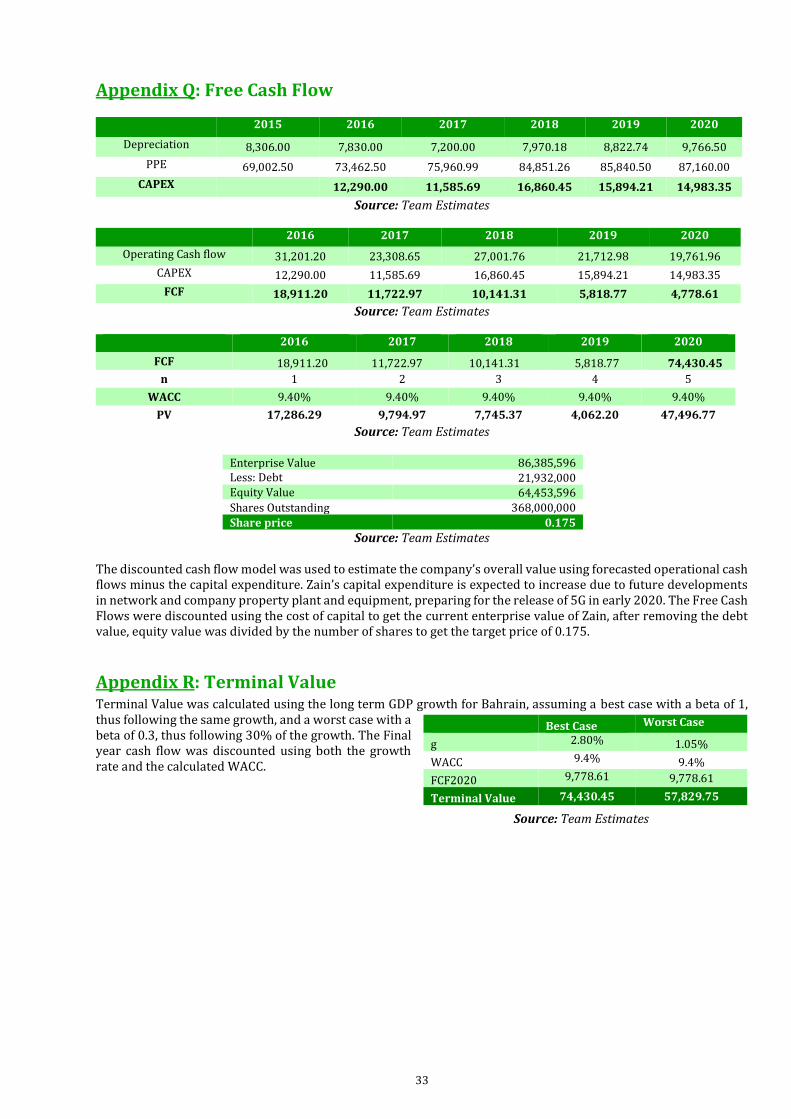

Discounted Cash Flow Model (DCF) Estimating the intrinsic value using the discounted cash flow analysis involves forming expectations about Zain BH’s future cash flows and growth prospects. As a first step, detailed year-to-year projections of the operational cash flows and capital expenditure for the next five years have been formed using Zain BH’s historical data since 2009. The value of Zain BH is then derived by discounting the future cash flows using the cost of capital to get the amount representing enterprise value, which is divided by the number of shares after deducting the debt value, thus generating the price of BD 0.175.

Cash Flow Forecasts Examining Zain BH’s past data, it can be observed that there appears to be no clear pattern in earnings growth. This may be because of the continuous negative shocks in the economy for the past few years arising from the financial crisis of 2009, the political unrest in 2011 and the oil crisis in 2015. These instabilities make projections harder as the historical growth does not follow a stable pattern. Nonetheless, the free cash flows (Appendix Q – Free Cash flow) are derived from cash flows from operating activities in the projected cash flow statements and is mostly sensitive to the revenue forecast and WACC.

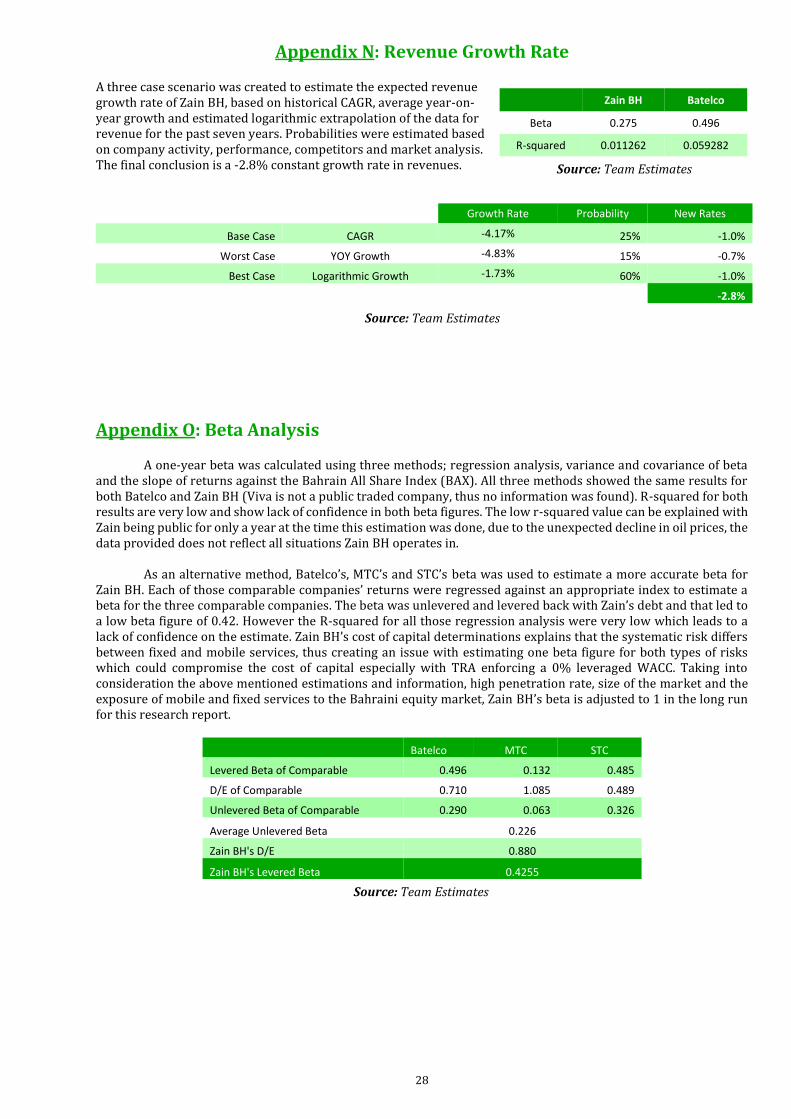

Revenue Forecast Zain BH’s revenue growth is primarily affected by a highly penetrated market with comparably lower prices than other markets. Thus, it has become more difficult for Zain BH to generate revenues from mobile and fixed lines and there is a shift to data. With Zain BH gradually losing market share to competitors such as VIVA, who is currently owning almost 50% of the market, revenue is expected to drop. In addition, the oil crisis and the 60% increase in fuel price in January 2016 is expected to have a negative effect on Zain BH’s operations as it would lead to a decrease in the ability of consumer spending on products and services. Thus, revenue is forecasted to drop by -2.8% in the five year projection period (See Appendices N – Revenue Growth Rate and Appendix P – Financial Statements for details).

Weighted Average Cost of Capital (WACC) The discount rate is estimated at 9.4% based on the WACC method (Table-8), the components of which are broken as follows: The cost of equity is estimated using the Capital Asset Pricing Model (CAPM). The risk-free rate is

estimated to be 5.9% based on the midpoint of the CBB 7 year Sukuk (6.3%) and 10-year Bahrain bonds (5.5%). Assuming a domestic investor for the purpose of this research report, no risk-free rate of other government bonds (i.e. US or UK bonds) are used in the CAPM calculations of this research report (Refer to Appendix T – Capital Asset Pricing Model for details).

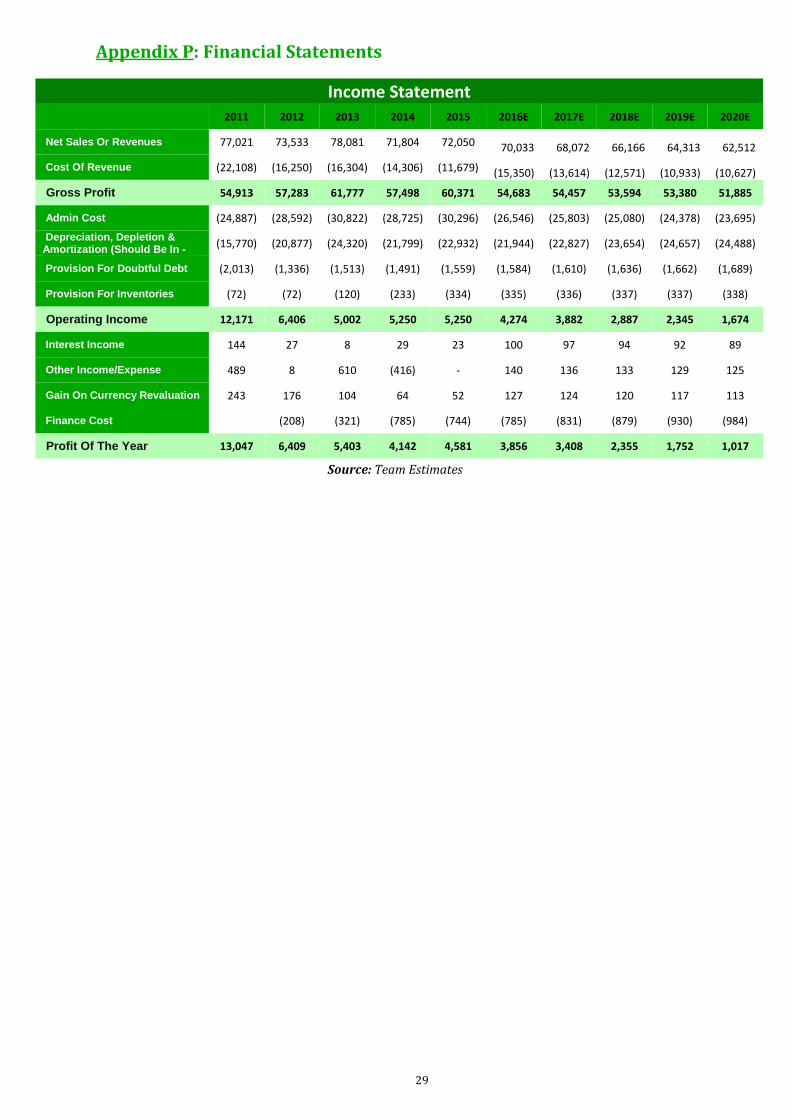

To calculate beta, Zain BH’s stock returns has been regressed against the market return. However, Zain BH has only became public in 2014, and therefore a one year daily data cannot provide good estimates of beta. In addition, the low R-squared value of 0.011 highlights the poor ‘goodness of fit’ of the data (Table-5). Another approach has been attempted, whereby the beta of a set of comparable (Batelco, MTC and STC) has been unlevered and then levered using Zain BH’s debt ratio, which resulted to a beta of 0.43 for Zain BH (Table-6). However, by running the regression of each of those comparable companies, low R-squared has again been an issue which leads to lack of confidence of the estimate. In addition, examining the telecommunication industry beta calculated by several sources gives a wide range of unlevered betas ranging from 0.62 (Damodaran, Jan 2016) to as high as 1.42 (Investment Research, Reuters). As a result, the beta has been adjusted to 1 due to absence of reliable data and as also been suggested by the TRA (Refer to Appendix O – Beta Analysis).

The equity risk premium (ERP) is estimated based on market returns for an illiquid market (Bahrain) requiring compensation for the cost of illiquidity represented competing in weak economic situation worldwide. Comparing Bahrain’s stock market to the FTSE All-world Index, the need for illiquidity compensation in the ERP arises. Moreover, historical data of the Bahraini market and Zain BH does not hold in this case as Bahrain Bourse is not as mature as bigger worldwide stock markets. Also, the fact that Zain BH has only been public for a year implies a lack of viable data to estimate ERP and an element of uncertainty based on historical performance comparison to market performance and risk free rates. The ERP for the telecom operators in Bahrain varies from 4.5-6.5%, and the estimation for Zain BH’s ERP is taken to be 5%.

The cost of debt for Zain BH is the three month BIBOR (currently at 1.55%) plus a quarterly 2.25% premium charged on loans, thus making the annual cost of debt 3.8%. As Bahrain does not impose any corporate or income tax so far, estimation of a tax rate is not relevant to the WACC estimation.

The target capital structure is at 80% equity and 20% debt for the projected period of 2016-2020.

Enterprise Value 86,386 Less: Debt 21,932 Equity Value 64,454 Share Price 0.175

Batelco MTC STC Levered Beta of Comparable

0.496 0.132 0.485

D/E of Comparable

0.710 1.085 0.489

Unlevered Beta of Comparable

0.290 0.063 0.326

Average Unlevered Beta

0.226

Zain BH's D/E 0.880

Zain BH's Levered Beta

0.4255

Growth Rate

Base Case CAGR -4.17%

Worst Case YOY Growth -4.83%

Best Case Logarithmic

Growth -1.73%

Cost of equity 10.80% Weighted Average of Equity

80%

Cost of Debt 3.8%

Weighted Average of Debt

20%

WACC 9.4%

Table-4: Estimated Target Price from DCF (in BD 000’s)

Table-8: Estimation of WACC

80%

20%

Figure-19: Capital Structure

Equity

Debt

Table-5: Estimation of Beta Using Regression

Table-6: Estimation of Unlevered Beta

Table-7: Estimation of Revenue Growth

Source: Zain BH, Team Estimates

Source: Team Estimates

Source: Team Estimates

Source: Zain Bahrain, Team Estimates

Source: Team Estimates

9

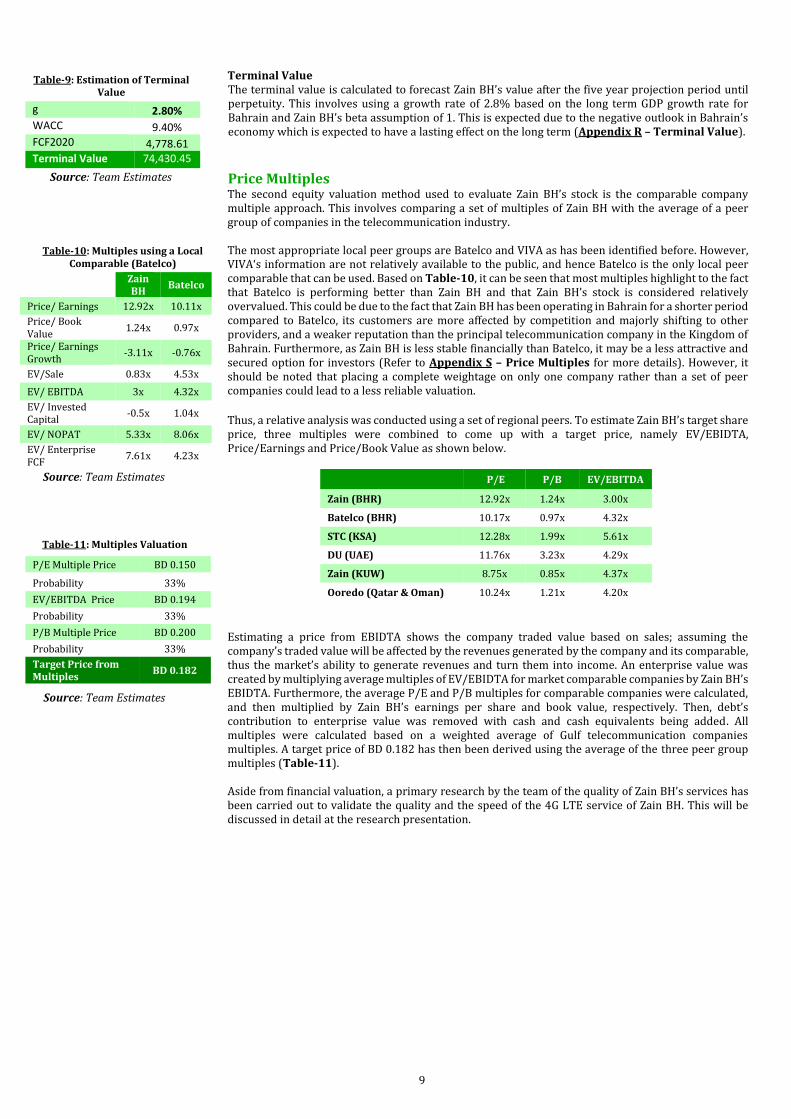

Terminal Value The terminal value is calculated to forecast Zain BH’s value after the five year projection period until perpetuity. This involves using a growth rate of 2.8% based on the long term GDP growth rate for Bahrain and Zain BH’s beta assumption of 1. This is expected due to the negative outlook in Bahrain’s economy which is expected to have a lasting effect on the long term (Appendix R – Terminal Value).

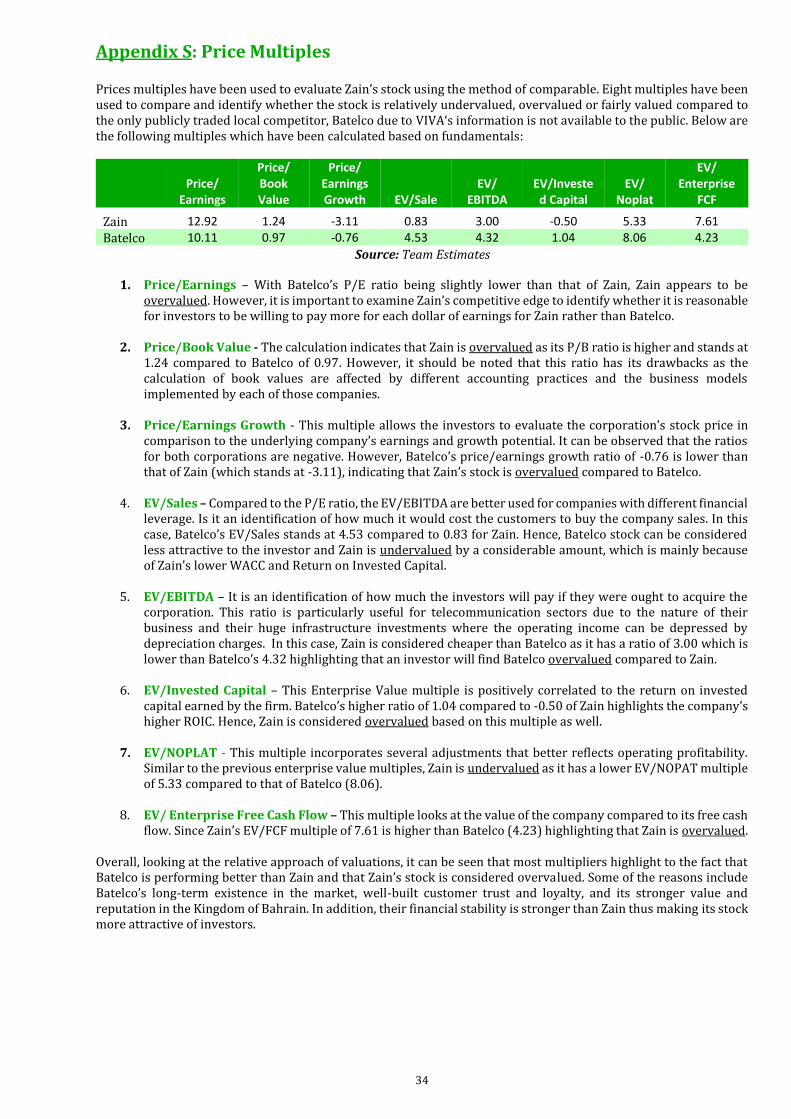

Price Multiples The second equity valuation method used to evaluate Zain BH’s stock is the comparable company multiple approach. This involves comparing a set of multiples of Zain BH with the average of a peer group of companies in the telecommunication industry. The most appropriate local peer groups are Batelco and VIVA as has been identified before. However, VIVA‘s information are not relatively available to the public, and hence Batelco is the only local peer comparable that can be used. Based on Table-10, it can be seen that most multiples highlight to the fact that Batelco is performing better than Zain BH and that Zain BH’s stock is considered relatively overvalued. This could be due to the fact that Zain BH has been operating in Bahrain for a shorter period compared to Batelco, its customers are more affected by competition and majorly shifting to other providers, and a weaker reputation than the principal telecommunication company in the Kingdom of Bahrain. Furthermore, as Zain BH is less stable financially than Batelco, it may be a less attractive and secured option for investors (Refer to Appendix S – Price Multiples for more details). However, it should be noted that placing a complete weightage on only one company rather than a set of peer companies could lead to a less reliable valuation.

Thus, a relative analysis was conducted using a set of regional peers. To estimate Zain BH’s target share price, three multiples were combined to come up with a target price, namely EV/EBIDTA, Price/Earnings and Price/Book Value as shown below.

P/E P/B EV/EBITDA

Zain (BHR) 12.92x 1.24x 3.00x

Batelco (BHR) 10.17x 0.97x 4.32x

STC (KSA) 12.28x 1.99x 5.61x

DU (UAE) 11.76x 3.23x 4.29x

Zain (KUW) 8.75x 0.85x 4.37x

Ooredo (Qatar & Oman) 10.24x 1.21x 4.20x

Estimating a price from EBIDTA shows the company traded value based on sales; assuming the company’s traded value will be affected by the revenues generated by the company and its comparable, thus the market’s ability to generate revenues and turn them into income. An enterprise value was created by multiplying average multiples of EV/EBIDTA for market comparable companies by Zain BH’s EBIDTA. Furthermore, the average P/E and P/B multiples for comparable companies were calculated, and then multiplied by Zain BH’s earnings per share and book value, respectively. Then, debt’s contribution to enterprise value was removed with cash and cash equivalents being added. All multiples were calculated based on a weighted average of Gulf telecommunication companies multiples. A target price of BD 0.182 has then been derived using the average of the three peer group multiples (Table-11). Aside from financial valuation, a primary research by the team of the quality of Zain BH’s services has been carried out to validate the quality and the speed of the 4G LTE service of Zain BH. This will be discussed in detail at the research presentation.

g 2.80% WACC 9.40% FCF2020 4,778.61 Terminal Value 74,430.45

Zain BH

Batelco

Price/ Earnings 12.92x 10.11x

Price/ Book Value

1.24x 0.97x

Price/ Earnings Growth

-3.11x -0.76x

EV/Sale 0.83x 4.53x

EV/ EBITDA 3x 4.32x

EV/ Invested Capital

-0.5x 1.04x

EV/ NOPAT 5.33x 8.06x

EV/ Enterprise FCF

7.61x 4.23x

P/E Multiple Price BD 0.150

Probability 33%

EV/EBITDA Price BD 0.194

Probability 33%

P/B Multiple Price BD 0.200

Probability 33%

Target Price from Multiples

BD 0.182

Table-9: Estimation of Terminal Value

Source: Team Estimates

Table-11: Multiples Valuation

Source: Team Estimates

Table-10: Multiples using a Local Comparable (Batelco)

Source: Team Estimates

10

Investment Risks Regulatory Risk Compliance with TRA’s WACC covenant (RR) In order to comply with the Telecommunication Regulatory Authority, Zain BH needs to control its WACC at 9.5% and use 100% equity financing as imposed by the authority. Zain BH currently fails to comply as it announced that its WACC stands between 11-12% and that it is using debt financing. This will lead to Zain BH facing sanctions, penalties or license issues with the regulator. Zain BH also faces regulatory risks due from price reduction enforcements and other imposed regulations which may for example require it to invest in more environment-friendly devices.

Market Risk Competition in a highly saturated market and interest rate hike (MR) Zain BH’s growth in a very saturated market has become very difficult, with its subscriber growth decreasing from 25% in 2013 to 1.6% in 2015-Q2. The Bahraini telecommunication market penetration rate stands at 187% with only 2.6 million subscribers. Thus, further expansion and growth will be very difficult especially that Zain BH’s 6-year CAGR is at -4%. Expected growth in data consumption will be faced with decrease in voice revenues which comprise 42% of total telecommunication sector revenues

(TRA) especially with expected decrease in consumer spending due to governmental budget cuts. Moreover, Bahrain is facing an upcoming increase in CBB’s interest rates, following the Fed’s interest rate increase, as the Bahraini Dinar is pegged to the US Dollar; this puts Zain BH and the country at risk of high inflation rates.

Economic Risk Unfavorable Global Macro Indicators (ER) The oil price decrease from $115 in August 2014 to $38 in November 2015 can affect Zain BH in multiple ways as the government has started budget cuts, decrease in spending, and inflation in prices of basic necessities which could lead to a decrease in consumer spending on telecommunications and other services thus decreasing demand on the company’s service line. Furthermore, many petrochemical companies have shut down operations which will lead to loss in fixed lines and business services also loss of expat’s demand on mobile services as they will be leaving the country. This also puts Zain BH at risk of probable taxes or fees imposed by the government to cover budget deficits. If oil prices remain decreasing, it could lead to a potential stock market loss/crash.

Liquidity Risk A highly costly sector (LR) Zain BH reported spending $100million on LTE infrastructure and licensing in 2014, and decreasing current and quick ratios over the past five years. This means that the company is lacking cash on hand which can affect its shareholder’s return and dividend payment and it ability to meet immediate funding needs. With continuous development and licensing in daily operations, Zain BH will compromise its WACC structure and ratio.

Operational Risk Information Security in the telecommunication industry (OR) Providing safety for consumer data in a highly developed technological era is essential to maintain subscriber base. Zain BH lacks public information security data communicated with subscribers regularly to maintain safety. Moreover, any breach in security of subscriber’s information will compromise the entire subscriber base especially in a very social media affected society that has become mainly dependent on data and is uneducated regarding safety measures.

Other Risk Independence of board and Relationship with Parent Company (TR) Zain Bahrain’s Board of Directors has only 2 independent members out of a total of 7 members. Out of which, 4 are representatives of Zain Group based on a management agreement signed between both companies. This means the company lacks shareholder control in strategic decisions as most strategic verdicts are decided by the parent company. Furthermore, Zain BH only compromises 1.7% of the total group subscribers, which means that the group’s risk tolerance towards Zain BH can differ from shareholder’s risk culture thus creating a conflict of interest and decisions within the company board.

Value-at-Risk Historical and Linear VaR Based on historical prices and returns, the VaR value shows that, at a 99% confidence level, the maximum loss for a 1-day holding period is BD 0.004. This figure is not insignificant considering that the stock price was originally priced at BD 0.200. This means that the worst expected loss from a 1-day holding period is 2%. VaR was calculated based on daily prices for 2014 (Table-12).

Average 0.0001

Standard Deviation

0.0010

Alpha 0.0500

Z-Square (99%) (2.3300)

Linear VaR (99%)

(0.004)

Figure-20: Risk Matrix

Source: Team Estimates

Figure-21: Oil Prices 2015

Source: Infome.com

Source: Team Estimates

Table-12: Value-At-Risk

11

Appendix A: Organizational Structure

Board Chairman

General Manager

Director, Marketing

Director, Business Planning and

Excellence

Specialist, Investor Relations, Compliance

& GM Office

Director, Human Resources

Director, Regulatory, Wholesale and

Roaming

Manager, Corporate Communications

Director, Legal

Director, Finance

Manager, Revenue Accounting

Manager, Accounts Payable

Manager, Budgeting and Reporting

Director, NetworkManager, Network Planning and PMO

Director, Sales and Customer Care

Director, MarketingManager, Analytical

Marketing

Team Leader, Revenue Assurance

Specialist, Revenue Assurance

Board of Directors

Source: Bahrain Bourse

12

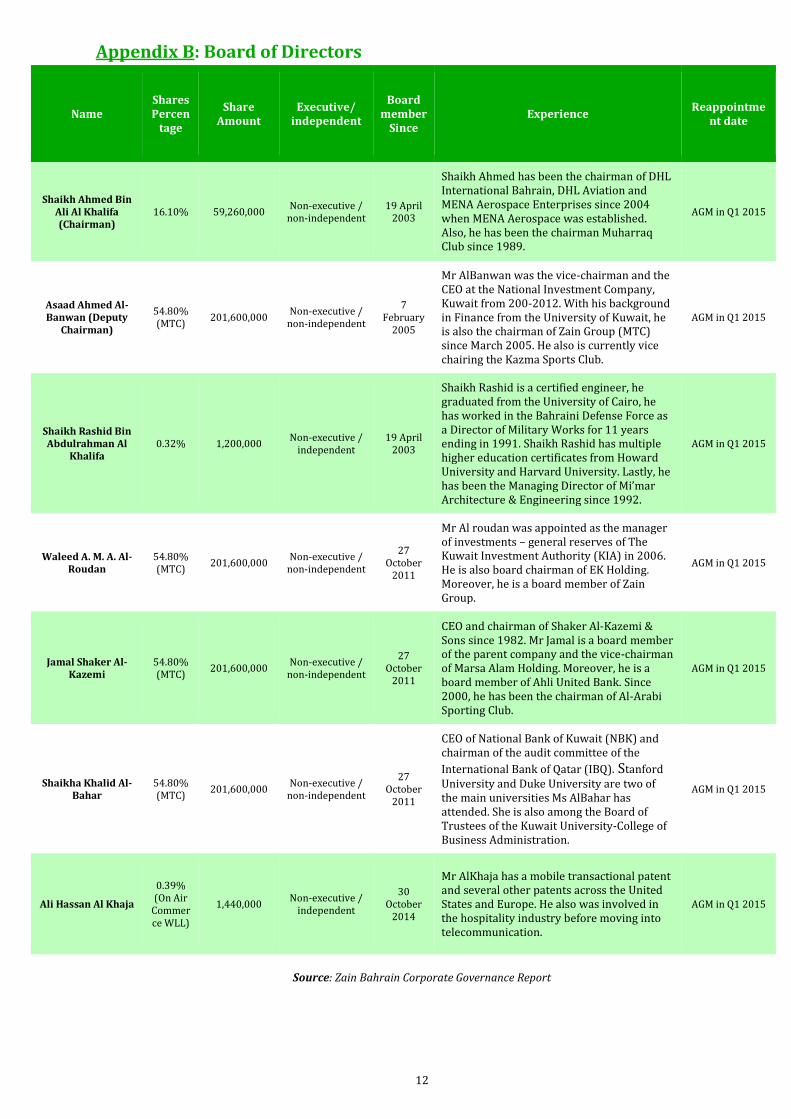

Appendix B: Board of Directors

Name Shares Percen

tage

Share Amount

Executive/ independent

Board member

Since Experience

Reappointment date

Shaikh Ahmed Bin Ali Al Khalifa (Chairman)

16.10% 59,260,000 Non-executive / non-independent

19 April 2003

Shaikh Ahmed has been the chairman of DHL International Bahrain, DHL Aviation and MENA Aerospace Enterprises since 2004 when MENA Aerospace was established. Also, he has been the chairman Muharraq Club since 1989.

AGM in Q1 2015

Asaad Ahmed Al-Banwan (Deputy

Chairman) 54.80% (MTC) 201,600,000 Non-executive /

non-independent 7

February 2005

Mr AlBanwan was the vice-chairman and the CEO at the National Investment Company, Kuwait from 200-2012. With his background in Finance from the University of Kuwait, he is also the chairman of Zain Group (MTC) since March 2005. He also is currently vice chairing the Kazma Sports Club.

AGM in Q1 2015

Shaikh Rashid Bin Abdulrahman Al

Khalifa 0.32% 1,200,000 Non-executive /

independent 19 April

2003

Shaikh Rashid is a certified engineer, he graduated from the University of Cairo, he has worked in the Bahraini Defense Force as a Director of Military Works for 11 years ending in 1991. Shaikh Rashid has multiple higher education certificates from Howard University and Harvard University. Lastly, he has been the Managing Director of Mi’mar Architecture & Engineering since 1992.

AGM in Q1 2015

Waleed A. M. A. Al-Roudan

54.80% (MTC) 201,600,000 Non-executive /

non-independent 27

October 2011

Mr Al roudan was appointed as the manager of investments – general reserves of The Kuwait Investment Authority (KIA) in 2006. He is also board chairman of EK Holding. Moreover, he is a board member of Zain Group.

AGM in Q1 2015

Jamal Shaker Al-Kazemi

54.80% (MTC) 201,600,000 Non-executive /

non-independent 27

October 2011

CEO and chairman of Shaker Al-Kazemi & Sons since 1982. Mr Jamal is a board member of the parent company and the vice-chairman of Marsa Alam Holding. Moreover, he is a board member of Ahli United Bank. Since 2000, he has been the chairman of Al-Arabi Sporting Club.

AGM in Q1 2015

Shaikha Khalid Al-Bahar

54.80% (MTC) 201,600,000 Non-executive /

non-independent 27

October 2011

CEO of National Bank of Kuwait (NBK) and chairman of the audit committee of the

International Bank of Qatar (IBQ). Stanford University and Duke University are two of the main universities Ms AlBahar has attended. She is also among the Board of Trustees of the Kuwait University-College of Business Administration.

AGM in Q1 2015

Ali Hassan Al Khaja 0.39% (On Air

Commerce WLL)

1,440,000 Non-executive / independent

30 October

2014

Mr AlKhaja has a mobile transactional patent and several other patents across the United States and Europe. He also was involved in the hospitality industry before moving into telecommunication.

AGM in Q1 2015

Source: Zain Bahrain Corporate Governance Report

13

Appendix C: Board Termination Process

Appendix D: Board Committees

Committee Responsibilities Yearly Meetings

Board Audit Committee (BAC)

Reviewing accounting and finance policies and internal control procedures.

Appointing external auditors and supervising the financial statements reviewing and audit process externally and internally.

Review company law and regulations compliance. Review the control systems of information and telecom

technology.

At least four times a year.

Nomination and Remuneration

Committees NRC

Recommending potential board members to the current board.

Recommending potential candidates for board committees. Review and monitor compliance of board members with the

code of conduct and overseeing remuneration issues. Review and evaluate performance of board members and

successful committees.

At least twice a year.

Source: Zain Bahrain Corporate Governance Report

Board Termination process

Termination of directorship can take effect in the cases set out below:

•”If a Director does not have the appropriate legal qualifications or has been sentenced for an act, a fraud or a crime affecting

his honor or integrity;

• If a Director is appointed or elected in a manner contrary to the provisions of the law;

• If a Director abuses his membership to carry on a competitive business to the Company or causes damages to the Company;

or

• If the Shareholder appointing the member removes him.

• Termination of a member of the Board or indeed the whole Board can also be effected by a General Assembly in accordance

with Article 178 of the Commercial Companies Law of Bahrain.”

Source: Zain Bahrain Corporate Governance Report

14

Appendix E: SWOT Analysis

STRENGTHS:

1. Partnership and suppliers: Zain BH partnered with companies from diversified industries to provide a variety of telecom services that not only deliver tangible benefits but intangible ones too. Zain BH continues to add unique blend of services in order

to increasing the data consumption, loyalty, retention of their current and potential customers through partnership with unexpected companies. With every partnership, Zain BH delivers a message that touch on an emotional aspect and a personal need of a specific target market from its target market pool. Although the partnerships are unexpected, they are in line with their vision and slogan “A Wonderful World”. For instance, the very recent Zain group-wide gaming partnership with Zeptolab (the developer of “Cut the Rope” game) gives Zain BH access to over 750 million game downloaders where the game will display Zain BH brand in all of the countries that Zain Group operates in, and according to Zain, this agreement “offers their customers the latest and most exciting products and services as it transforms to become a digital lifestyle provider” (Zain Bahrain, n.d.). In the same context, Zain BH has partnered with Polytechnic's Annual ICT Exhibition as their CSR’s strategic approach focuses on education and empowering youth. Thus, this partnership intends to “nurture the young talents and to develop the next generation of talents”. Adding to that, Zain BH has supported the start-up boot camp since its first edition. Start-up Bahrain is the kingdom’s first independent digital publication for the start-ups corporation and entrepreneurs, by this partnership, Zain BH will provide them with products and services that are tailored to fit the needs of entrepreneurs with mobiles, broadband and enterprise services with the aim to empower youth and foster innovation and entrepreneurship in the Kingdom. On another level, Zain BH partnered with Uber which is a modern transporting company that is evolving the way the world moves. From this group-wide agreement, Uber platform users who use Zain BH will receive a discounted and a preferential service. Moreover, the Uber driver partners will receive a superior network quality and will enable a mobile payment for the Uber service too. This partnership also includes but is not limited to having Wifi in vehicles for Zain customers in the future in addition to having discounted services for the transportation services provided by Uber. Those benefits would encourage not only Zain BH users to try Uber service, but for Uber users to switch to Zain BH if they are aware of such services. Touching on the needs of the diversified and multi-cultural community that Bahrain has through an agreement with an exchange company (NAFEX), where people transferring money will be able to benefit from special telecom services provided by Zain BH (for Zain users), a set of innovative services that enable the expatriate customers to effectively communicate with their friends and family. Another agreement was with Apple and Samsung Bin Hindi informatics in order to have a complete support with regards to the new devices that are released in the market. This agreement ensures no shortage in the new devices for Zain BH customers as most of the shifted customers from Zain BH to other operators have stated that the reason behind that shifting is that they have purchased a phone from Zain BH. This means that the operator succeeded in securing the devices for those customers due to this agreement that they have. They are authorized also to give prices offers for their customers and limited packages in order to have a competitive edge. Zain Bahrain was the first to launch the iPhone 6 and iPhone 6 plus and the leading operator in the GCC to launch Samsung integrated mobility “IM ZONE” in their headquarters store at Seef mall department where a variety of Samsung products are available for sale. Tie-up with local corporation who are looking to play a dynamic role in strengthen the country economics such as Fakhro Electronics via strengthening the business and giving them the advantage of maintaining and providing high security, cost effective internal network with the best quality service from world class brands that are known for their communication solutions such as AVAYA and CISCO. In 2015, Zain BH renewed its main sponsorship of the Capital Club event program and to be the telecoms partner. This is in line with Zain’ s strategy in reaching out to a wider range of corporate decision making partners in providing strong and powerful services for them and technological advantages for the corporations around Bahrain. A partnership with Bahrain Bay took place with Zain BH to provide advanced voice and data services that is delivered to each commercial unit via a fiber optic network making this contract a mixed-use development with cutting-edge ICT solutions for all commercial, retail and residential communities. Easy access for topping up credit and bills payment through mobile applications, Zain’ s website and 650 Sadad kiosks that are available in major supermarkets, 15 of those kiosks are available at Zain BH branches.

15

In early 2015, Zain BH expanded its existing partner market agreement with Vodafone to deliver machine-to-machine services to enterprise and government sectors across the region. This group-wide agreement shall enhance the service as the waiting time will be limited. Adding to that, the cost of having many customer service officers can be avoided once it is automated and it operating effectively.

2. Advanced Network Infrastructure: Over $100 Million invested to revamp in the current network towers to enhance the quality of the 4G / LTE service provided. The focus is to enhance the capacity for providing the best customer experience against tremendously increasing data usage and thus, drawing more individuals to switch to Zain BH’s network.

3. Complaints Management System:

In 2014 Zain BH launched a new program called Astellia. This program helps them to study their customer’s satisfaction regardless of the mobile type, the data package, the location and the timing of the use in order to enhance their performance. This lead to a 50% decrease in the number of complaints, a 30% increase in positive feedback and the increase in the percentage of conflict resolution by 10%. Data is collected through Transactional-Net Promoter Score (T-NPS) which ensures its objectivity (Zain Bahrain, 2014).

4. Licenses and diversified portfolio:

They have made Bahrain the leading in technological sector regionally and globally by being the first to initiate the 3G, 3.5G and the WIMAX coverage in line with the radio coverage expansion up to 30% in the kingdom (Zain Bahrain, 2014). In addition, Zain BH has 7 different licenses from the telecommunication Regulatory Authority which means that they have a wide variety of services.

5. Prospectus Competitive Strengths: According to Zain BH IPO prospectus, Zain BH has a strong brand positioning and recognition in addition to the strong relationship that Zain BH has with its parent company. This means that Zain BH can benefit from the experience of its management team. Adding to that, Zain BH has a strong distribution network and a Culture of New Innovative Products and Services.

WEAKNESS:

1. Directed Awareness from customer service employees: Zain BH advertisements usually feature the theme of the campaign rather than certain information that would attract the users to purchase the packages. General statements such as “Addicted to Data” in the Big Gigs Family does not feature the fact that the network is now upgraded or that the service now is much better than it used to be in the past. Random poster with a new character would not indicate that there are packages that are tailored to the needs of each of the family members. It is true that the website and application include more details about the packages, nonetheless, if such details were not addressed and executed efficiently in posters or in online landing pages, most people would not bother to look at it and thus, no sales will take place. Application use is limited due to low level of awareness about its availability. Employees at the point of sell (customer service) do not inform to the current or the new customers about a mobile application as it will be an easy way to change packages, top up their credit, access their information and packages without the need of standing in long queues either in branches or waiting for a longtime to be served on the mobile phone.

2. Network Coverage: In 2014, the TRA report stated that the 4G/LTE coverage based on governmental location of Zain BH is only 96.2 % compared to that of its competitor VIVA 99.7%. Batelco’s percentage was behind 91%. Many locations as demonstrated in the report are IN coverage but many of them are NOK in comparison with VIVA’s diagram which shows IN coverage and OK for the 4G services. 3. Service quality and Prices: Given the close variance in prices, the customers judge the provider based on the provided services and its quality. Nonetheless, when customers do not put into account the fact that the network has been revamped, and that the quality is now enhanced, they will chose another service provider and thus, Zain BH will lose a customer. Adding to that, when the perception is already negative towards the service and a client with a negative experience exploits something negative about the service after the revamp, other potential customers will be hesitant to try the service.

16

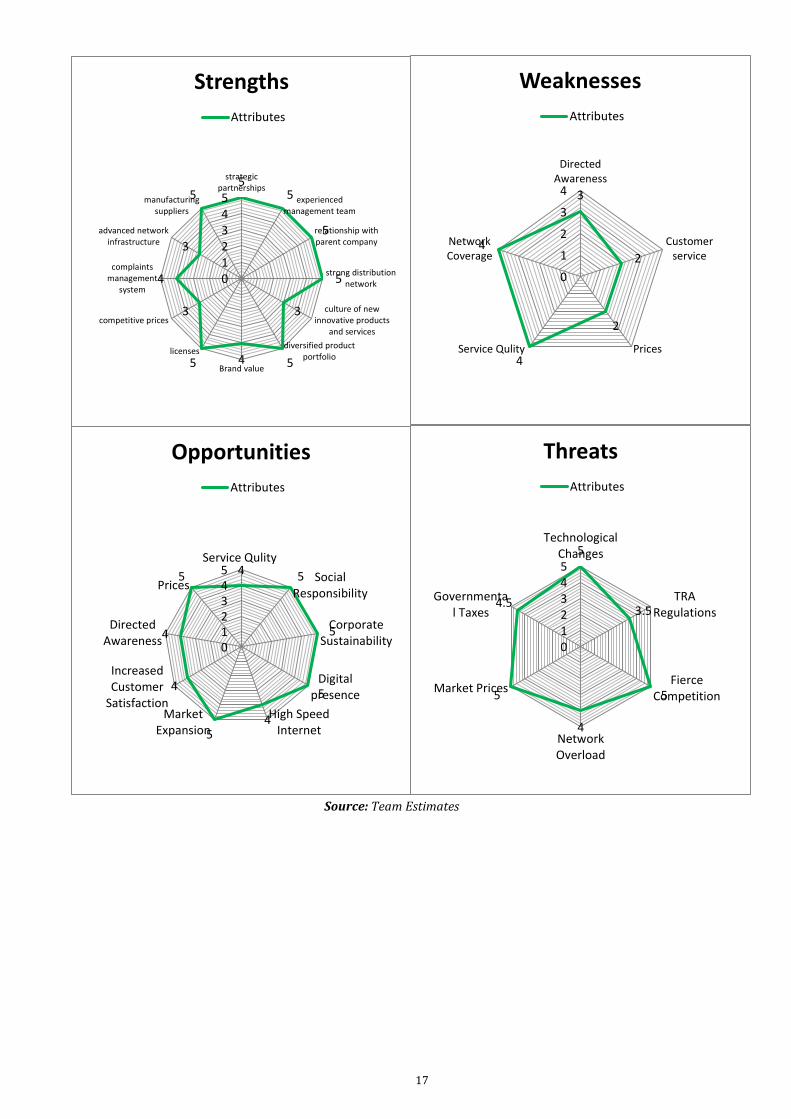

OPPORTUNITIES:

1. Customers Satisfaction: Having Astellia as enables Zain BH to have a better understanding of their customers’ needs and thus, address it appropriately. Since time of use and location can be identified, Zain BH has the opportunity to alter the strength of its network depending on the density of the population in that particular area or even based on the data consumption. This would give Zain BH more credibility as they will tackle the issues and reduce it by far more than 20% if implemented correctly and efficiently (Zain Bahrain, 2014). This service can also be promoted as an efficient tool to solve connection issues in order to attract more customers towards Zain services even though this system is also implemented in Batelco, which is a Zain’ s competitor (Batelco Bahrain, 2014; Zain Bahrain, 2014).

2. Market Expansion: Given the recent revamp in the network towers, Zain BH can utilize its valuable partnerships with various sectors to retain customers and to gain more customers from the other telecommunication providers. The benefits and the discounts that they can enjoy only if they are Zain BH customers. These benefits can be combined in a marketing campaign and spread in the community as people’s nature goes towards getting more services for less prices.

3. Internet speed: Preparation to promote and provide 5G services and fiber optic high speed internet services before the other operators in the form of cost efficient packages to entice the users.

4. Digital Presence: Zain BH is transforming itself to become a digital lifestyle services provider. This means

that the company is flexible with the modern style of life and is capable of adapting with the needs of the market while providing high speed internet service that suites the modern lifestyle of the community communications habits.

5. Service quality and price: If Zain BH managed to maintain a high service quality, it will be able to retain

and gain more clients from the market especially that the prices are approximately the same.

6. CSSR: Zain BH can utilize their CSSR programs to increase the sales and focus of the CSSR’s that can make their reputation even better and bring in more customers and thus, revenue to the company.

THREATS:

1. Technological Changes: Continuous need for rapid upgrades that cost time and money. Revamping the towers costs were over $100 million and were 17% of the revenues. Drastic technology changes require significant CAPEX needs while revenues are not matching to proceed with such investments.

2. Governmental Taxes: Governments view telecom revenue as a key source of revenue which makes them impose additional taxes on telecom operators and consumers. This reduces the revenue of the operator that also limits their ability to technology upgrades.

3. Market Prices: Competing rivals are reducing the profit margin to increase their market share of the customers. This is forces the companies into an unhealthy competition that affects the ability of all of the involved companies. The user however will be the only beneficiary from such a competition.

4. Network Overload: Increasing demand on broadband services causes occasional congestion in peak times especially in high populated areas where businesses operate. This reduces the efficiency of the provided service and thus, leads to customers altering the service provider.

5. Fierce Competitors: Menatelecom is considered as a major competitor for Zain BH since it is the only

operators alongside with Zain BH in the market to have access to WiMAX. Zain BH’s WiMAX awareness amongst its users is 77% while the users are only 4% in comparison to 88% of awareness in Menatelecom with 6% users. Another reason is that Menatelecom is promoting the availability of iPhone 6S which indicates a possible entrance in the mobile internet services (Zain Bahrain, 2015; Mena telecom, 2015).

6. TRA Regulations: The ability to shift from one operator to another by paying a BD 5 fees while carrying the same number from one operator to another is a threat and an opportunity in the same time as Zain BH can obtain more customers from other operators. This however can be eliminated by addressing the needs of the clients and working proactively to reduce the change of them leaving to other operators. Satisfied customers stay loyal and refer friends to the business too

17

55

3

4

3

5 4 5

3

5

5

5

012345

strategicpartnerships

manufacturingsuppliers

advanced networkinfrastructure

complaintsmanagement

system

competitive prices

licenses

Brand value

diversified productportfolio

culture of newinnovative products

and services

strong distributionnetwork

relationship withparent company

experiencedmanagement team

Strengths

Attributes

3

4

4

2

2

0

1

2

3

4

DirectedAwareness

NetworkCoverage

Service Qulity Prices

Customerservice

Weaknesses

Attributes

45

4

4

54

5

5

5

012345

Service Qulity

Prices

DirectedAwareness

IncreasedCustomer

SatisfactionMarket

ExpansionHigh Speed

Internet

Digitalpresence

CorporateSustainability

SocialResponsibility

Opportunities

Attributes

5

4.5

5

4

5

3.5

012345

TechnologicalChanges

Governmental Taxes

Market Prices

NetworkOverload

FierceCompetition

TRARegulations

Threats

Attributes

Source: Team Estimates

18

Appendix F: PESTEL Analysis

Factors Analysis

Po

liti

cal

& L

eg

al

Low tax environment

with no income taxes.

Occasional Political unrests

TRA regulations

Customers have high purchasing power and thus, the willingness to spend is also high. Nonetheless, the spending is mainly found in VIVA as it’s dominating 51% of the market followed by Batelco 29% and finally Zain BH with 20% only from the market share. This indicates other possible problems (quality of service/ prices “money value”). The TRA regulates the operations of the telecom companies and ensure that the companies are acting legally, ethically and professionally in all telecom and business aspects such as the price range and the speed. A 2011 regulation enabled users to switch operators while keeping the same number. This lead to a switch between operators. A 2014 TRA survey indicated that the reason behind the switch was attractive promotions, good prices, and service satisfaction. Adding to that, the TRA has stated that effective April 2016, roaming prices in the GCC will be lowered for voice, SMS and mobile data. This can encourage more users to use data roaming; nonetheless, this also means a reduced profit margin for the telecom companies.

Eco

no

mic

al

Fitch downgrading

Bahrain to “BBB-“ Governmental subsidies Connection purchasing

habits

Oil Prices

Bahrain’s economy has been downgraded which explains the governmental reduction in spending and the elimination of subsidies on various goods/services in the year 2015 and more in the year 2016 as the oil prices are in continuous decline. More than half of the Bahraini population is foreigners who will incur additional living costs that may lead them to decrease their spending on new mobile phones which may reduce sales. Promotions however and better packages on devices installments may stabilize the purchasing habit. In 2014, 65% of Zain BH’s customer’s connection purchasing habit was for postpaid whereas in Bahrain, the postpaid connection forms 73% of the connection type purchases in 2014. Furthermore, the agency recorded that the rent of the office prices in 2014 has declined to 6% in accordance to their analysis of the diplomatic and financial harbor area and stabilized in 2015 and there were no decreases in the prices so far as for 20th December, 2015. In case of the retail sector it is growing especially due to the Saudi tourists in the weekends to benefit from the expending in the retail Sector in Bahrain.

So

cia

l a

nd

Te

chn

olo

gic

al

High speed data is a must

to engage with the modern community activities.

Free communication

provided by the telecom operator encourages others (friends/ family) to switch to the same operator.