Embed Size (px)

Citation preview

Certain issuesin

Capital Gains

Agenda

2

S.No Overview

1. Arrangement of sections

2. Provision to Computation of Capital Gains & Key issues

3. Specific provisions relating to certain transactions

4. Union budget amendments

5. International tax

Arrangement of sections

1 Arrangement of sections

Important issues in Capital Gains

3

Arrangement of Sections

1 Arrangement of sections

4

• Section 45 - Charging section

• Section 46 – Capital gains on distribution of assets by companies in liquidation

• Section 46A - Capital gains on buyback of shares

• Section 47 – Transactions not regarded as transfer (exceptions)

• Section 47A - Withdrawal of exemption in certain cases

• Section 48 - Mode of computation

• Section 49 - Cost with reference to certain modes of acquisition

• Section 50 - Special provision for computation of capital gains in case of depreciable assets

• Section 50B - Slump Sale

• Section 50C - Defines full value of consideration in certain cases

• Section 50D - Fair market value deemed to be full value of consideration in certain cases

• Section 51 - Advance money received

• Section 54 to 54GA - Exemptions of capital gains in certain cases

• Section 55 - Cost of Acquisition/ Cost of improvement

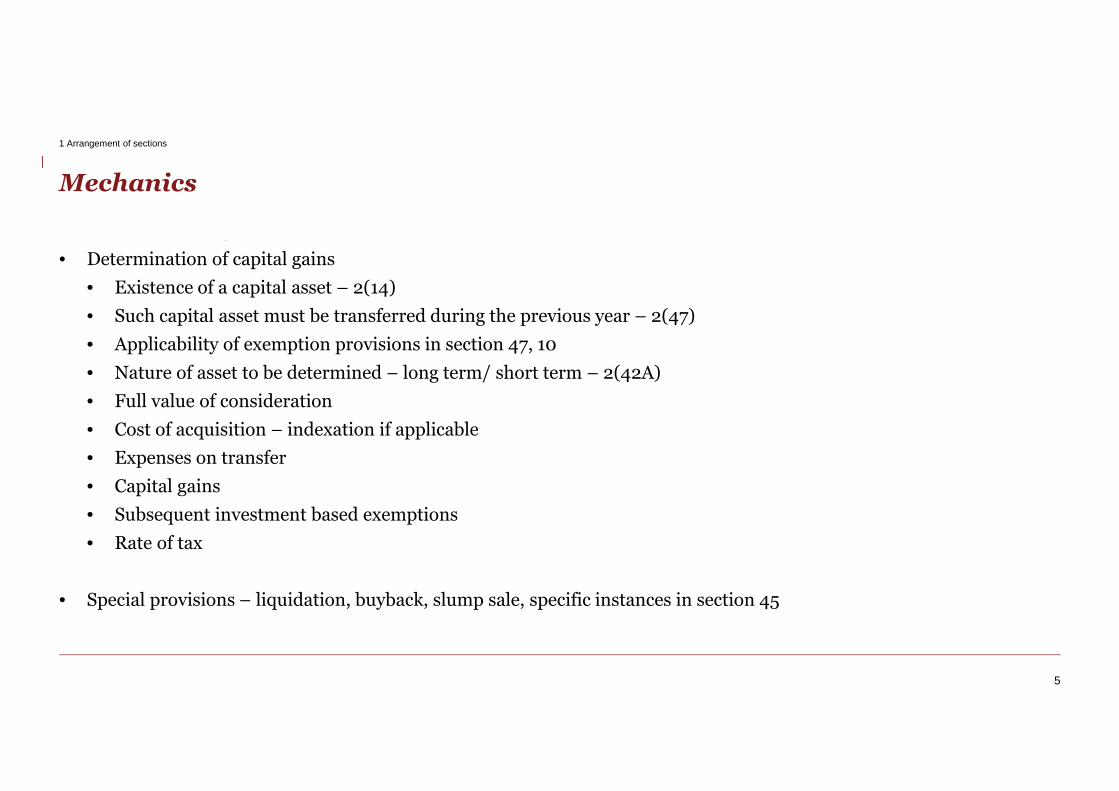

• Determination of capital gains

• Existence of a capital asset – 2(14)

• Such capital asset must be transferred during the previous year – 2(47)

• Applicability of exemption provisions in section 47, 10

• Nature of asset to be determined – long term/ short term – 2(42A)

• Full value of consideration

• Cost of acquisition – indexation if applicable

• Expenses on transfer

• Capital gains

• Subsequent investment based exemptions

• Rate of tax

• Special provisions – liquidation, buyback, slump sale, specific instances in section 45

Mechanics

1 Arrangement of sections

5

Provision to Computation ofCapital Gains & Key issues

2 Provision to Computation of Capital Gains & Key issues

Important issues in Capital Gains

5

Computation Provisions

2 Provision to Computation of Capital Gains & Key issues

6

• Provision explained – Section 48

- Full value of consideration received or accruing as a result of transfer of capital asset

- To be reduced by i) expenditure incurred wholly & exclusively in connection with transfer and ii) Cost of Acquisition andCost of Improvement

- “Indexed Cost of acquisition” and “Indexed Cost of Improvement” to be used in case of long term capital gain arising fromtransfer of long term capital.

• Key issues

- Taxability of contingent consideration - Ajay Guliya 209 Taxmann 295, Hemal Raju Shete 68 taxmann.com 319

- Indexation benefit for assets covered in section 49(1). – Manjula J Shah 16 Taxman 42

- Benefit of indexation for preference shares carrying fixed rate of dividend – Enam Securities Pvt Ltd. 345 ITR 64

- Taxability of consideration received in kind/where consideration received is not ascertainable – Section 50D.

- Taxability of Capital gains in case where the Computation section fails

Capital Gains on Sale of Depreciable Assets – Section 50

2 Provision to Computation of Capital Gains & Key issues

7

• Provision explained

• Key issues

- Tax rates for gain arising on sale of depreciable assets – LTCG/ STCG. – Smita Conducters 41 taxmann.com514

- Applicability of section 50 to assets on which depreciation was never claimed. - Santosh Structural & Alloys Ltd.20 taxmann.com 501

Consideration Block cease to exist Block exists

Exceeds (WDV+ actual cost of assetacquired during the year+ expenses ontransfer)

Short-term capital gain Short-term capital gain.

WDV of block becomes zero

Is less than (WDV+ actual cost of assetacquired during the year+ expenses ontransfer)

Short-term capital loss Balance left shall be WDV at theend of the year

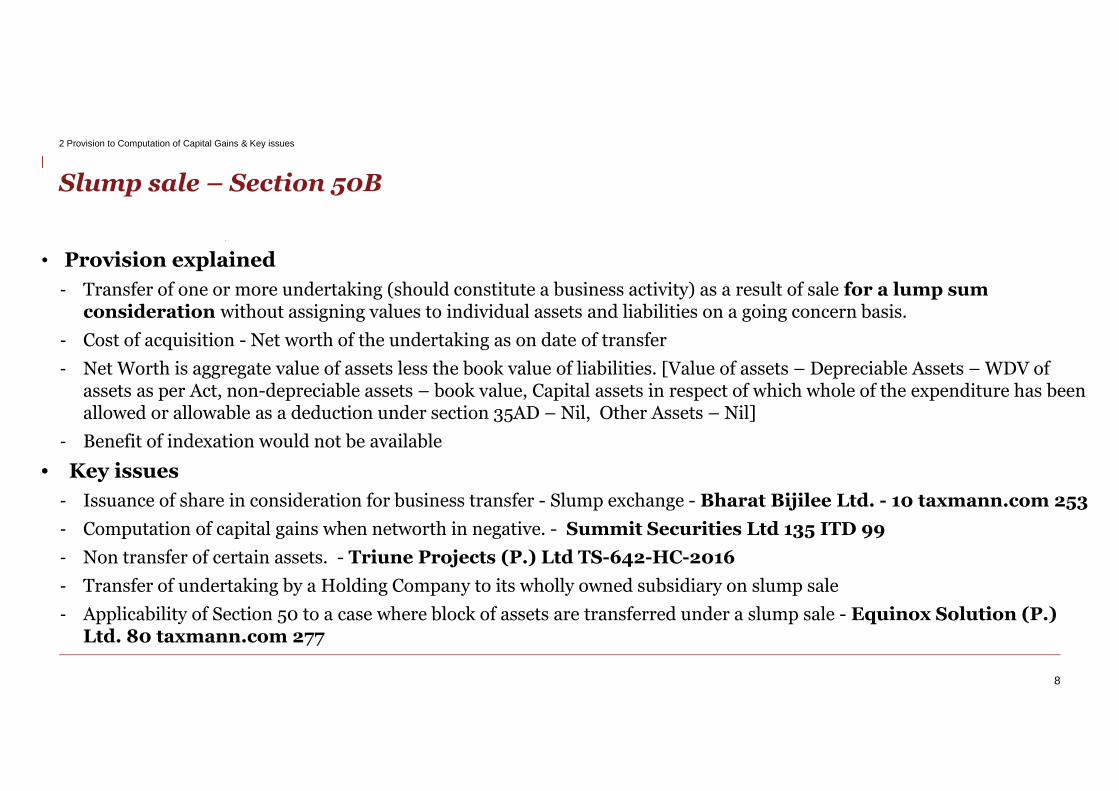

Slump sale – Section 50B

2 Provision to Computation of Capital Gains & Key issues

8

• Provision explained

- Transfer of one or more undertaking (should constitute a business activity) as a result of sale for a lump sumconsideration without assigning values to individual assets and liabilities on a going concern basis.

- Cost of acquisition - Net worth of the undertaking as on date of transfer

- Net Worth is aggregate value of assets less the book value of liabilities. [Value of assets – Depreciable Assets – WDV ofassets as per Act, non-depreciable assets – book value, Capital assets in respect of which whole of the expenditure has beenallowed or allowable as a deduction under section 35AD – Nil, Other Assets – Nil]

- Benefit of indexation would not be available

• Key issues

- Issuance of share in consideration for business transfer - Slump exchange - Bharat Bijilee Ltd. - 10 taxmann.com 253

- Computation of capital gains when networth in negative. - Summit Securities Ltd 135 ITD 99

- Non transfer of certain assets. - Triune Projects (P.) Ltd TS-642-HC-2016

- Transfer of undertaking by a Holding Company to its wholly owned subsidiary on slump sale

- Applicability of Section 50 to a case where block of assets are transferred under a slump sale - Equinox Solution (P.)Ltd. 80 taxmann.com 277

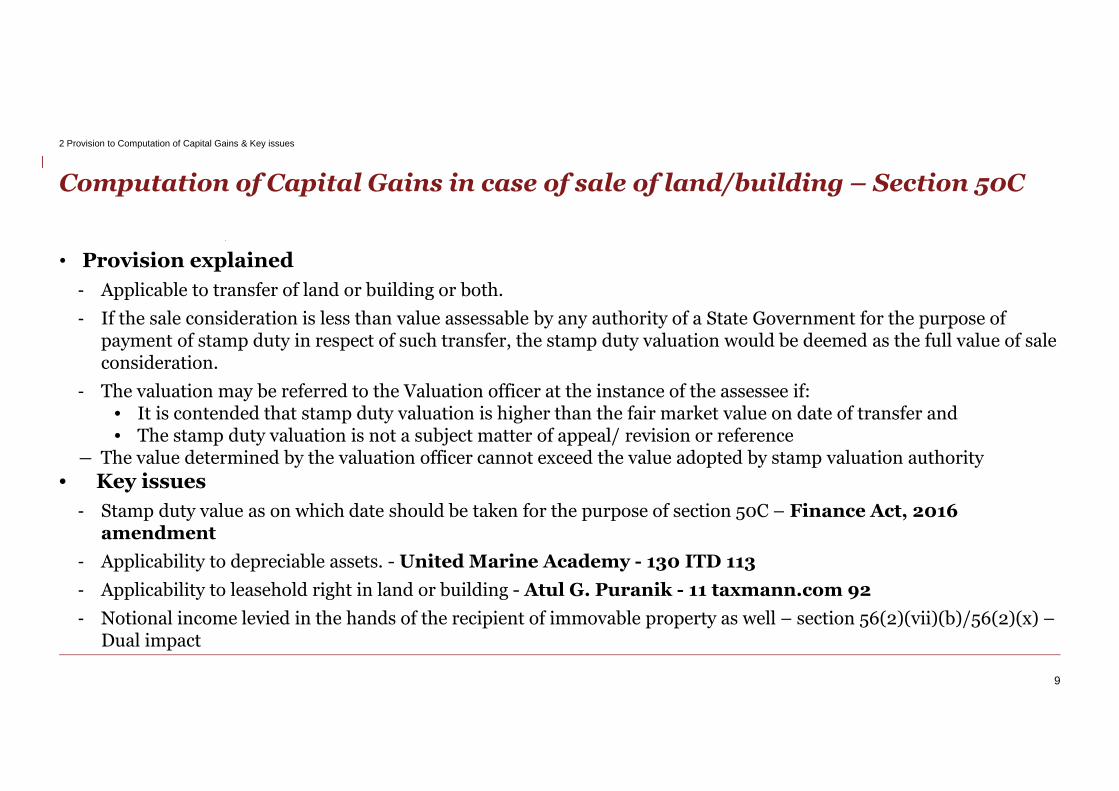

• Provision explained

- Applicable to transfer of land or building or both.

- If the sale consideration is less than value assessable by any authority of a State Government for the purpose ofpayment of stamp duty in respect of such transfer, the stamp duty valuation would be deemed as the full value of saleconsideration.

- The valuation may be referred to the Valuation officer at the instance of the assessee if:• It is contended that stamp duty valuation is higher than the fair market value on date of transfer and• The stamp duty valuation is not a subject matter of appeal/ revision or reference

― The value determined by the valuation officer cannot exceed the value adopted by stamp valuation authority

• Key issues

- Stamp duty value as on which date should be taken for the purpose of section 50C – Finance Act, 2016amendment

- Applicability to depreciable assets. - United Marine Academy - 130 ITD 113

- Applicability to leasehold right in land or building - Atul G. Puranik - 11 taxmann.com 92

- Notional income levied in the hands of the recipient of immovable property as well – section 56(2)(vii)(b)/56(2)(x) –Dual impact

Computation of Capital Gains in case of sale of land/building – Section 50C

2 Provision to Computation of Capital Gains & Key issues

9

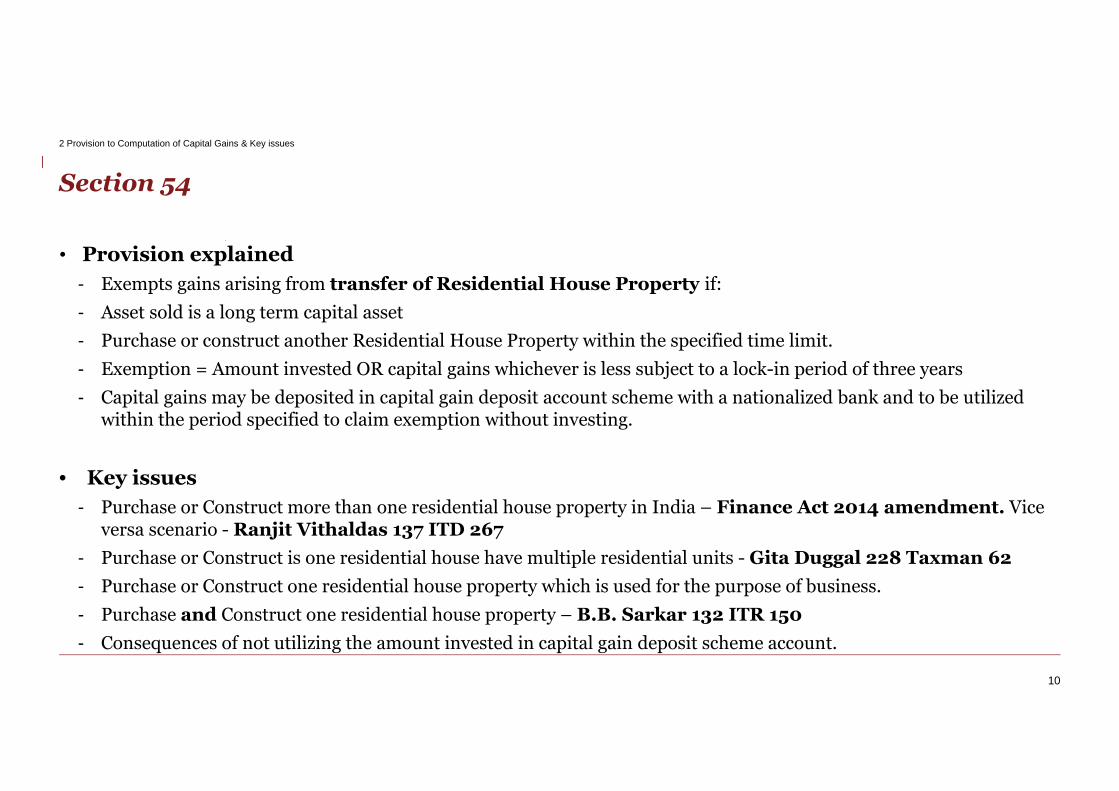

Section 54

2 Provision to Computation of Capital Gains & Key issues

10

• Provision explained

- Exempts gains arising from transfer of Residential House Property if:

- Asset sold is a long term capital asset

- Purchase or construct another Residential House Property within the specified time limit.

- Exemption = Amount invested OR capital gains whichever is less subject to a lock-in period of three years

- Capital gains may be deposited in capital gain deposit account scheme with a nationalized bank and to be utilizedwithin the period specified to claim exemption without investing.

• Key issues

- Purchase or Construct more than one residential house property in India – Finance Act 2014 amendment. Viceversa scenario - Ranjit Vithaldas 137 ITD 267

- Purchase or Construct is one residential house have multiple residential units - Gita Duggal 228 Taxman 62

- Purchase or Construct one residential house property which is used for the purpose of business.

- Purchase and Construct one residential house property – B.B. Sarkar 132 ITR 150

- Consequences of not utilizing the amount invested in capital gain deposit scheme account.

Section 54F

2 Provision to Computation of Capital Gains & Key issues

11

• Provision explained

- Exempts gains arising from transfer of long term capital asset (other than a residential house property) if:

- Purchase or construct one Residential House Property in India within the specified time limit.

- Transferor does not hold more than one residential house property other than the new residential houseproperty for a period of 3 years from date of transfer of original asset.

- Exemption = Amount invested * [capital gains/net sale consideration] subject to a lock-in period of threeyears

- Capital gains may be deposited in capital gain deposit account scheme with a nationalized bank and to be utilizedwithin the period specified.

• Key issues

- Claim of exemption under section 54 & 54F in respect of same capital gain - Venkata Ramana Umareddy 155 TTJ234

- Purchase of new residential house as◦ joint owner and; - Ravindra Kumar Arora – 342 ITR 38◦ In name of wife - Kamal Wahal 351 ITR 1

54EC

2 Provision to Computation of Capital Gains & Key issues

12

• Provision explained

- Available to any person for transfer of long term capital asset.

- Investment within 6 months in bonds of specified bonds which are redeemable after 3 years.

- Specified bonds should not be sold within 3 years of acquisition, otherwise will be treated as a long term capital gain.

- Exemption = Amount Invested OR Capital Gains whichever is Less.

- Capital gain deposit account scheme – Not Applicable

• Key issues

- Claim of exemption when amount invested is > 50 lakhs – Second Proviso to section 54EC

- Claim of exemption when the amount is invested in specified bonds within 6 months from date of transfer of stock intrade under section 45(2) - Circular No.791, dated 2-6-2000

- Bonds to be purchased within 6 months from date of receipt of consideration - Mahesh NemichandraGaneshwade 21 taxmann.com 136

- Claim of exemption in respect capital gains arising on transfer of depreciation asset. – Rajiv Shukla 334 ITR 138

- Bonds may be issued after a period of 6 months from date of transfer. – Hindustan Unilever Ltd – 325 ITR 102

Partnership related

2 Provision to Computation of Capital Gains & Key issues

13

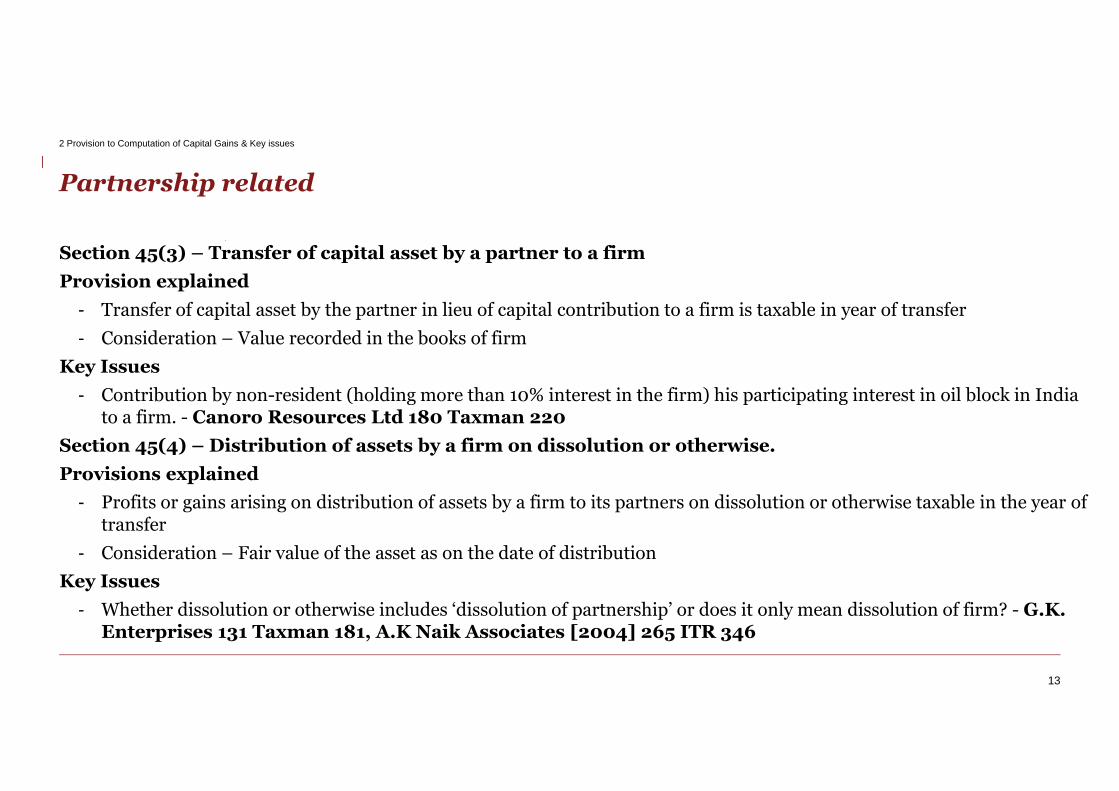

Section 45(3) – Transfer of capital asset by a partner to a firm

Provision explained

- Transfer of capital asset by the partner in lieu of capital contribution to a firm is taxable in year of transfer

- Consideration – Value recorded in the books of firm

Key Issues

- Contribution by non-resident (holding more than 10% interest in the firm) his participating interest in oil block in Indiato a firm. - Canoro Resources Ltd 180 Taxman 220

Section 45(4) – Distribution of assets by a firm on dissolution or otherwise.

Provisions explained

- Profits or gains arising on distribution of assets by a firm to its partners on dissolution or otherwise taxable in the year oftransfer

- Consideration – Fair value of the asset as on the date of distribution

Key Issues

- Whether dissolution or otherwise includes ‘dissolution of partnership’ or does it only mean dissolution of firm? - G.K.Enterprises 131 Taxman 181, A.K Naik Associates [2004] 265 ITR 346

MAT Provisions & Capital Gains

2 Provision to Computation of Capital Gains & Key issues

14

• Provision explained

- MAT regime is applicable to every “company” as defined in the Act, unless specifically exempted

- MAT provisions shall apply when tax payable on total income is less than 18.5% of adjusted book profits

- Non Obstante Provision - Provisions of section 115JB shall override all the other provisions of the Act

- “Book Profit” shall be determined by making adjustments to net profit as per P/L Account prepared in accordancewith Part II of Schedule VI to Companies Act, 1956

• Key issues

- Applicability of MAT on gain arising on sale of long term capital asset being listed shares exempt under section10(38).

- Applicability of MAT provisions on capital receipts not falling within income definition. - Shivalik Venture (P.)Ltd. 70 SOT 92

- Availability of indexation benefit to capital gains under section 10(38) for MAT purposes. - Karnataka StateIndustrial Infrastructure Development Corporation Ltd 54 ITR(T) 425

Specific provisions relatingto certain transactions

3 Specific provisions relating to certain transactions

Important issues in Capital Gains

15

• Provisions explained:

• Company - Distribution of assets by a Company at the time of liquidation would not be regarded as transfer – 46(1)

• Shareholder – Full value of consideration on transfer of shares held in company would be – 46(2)

Money received plus market value of other assets received

Less Amount assessed as dividend under section 2(22)(c)

• Issues:

Whether exemption under section 47 be claimed?

Whether distribution of capital asset would only be covered? - N. Bagavathy Ammal (SC)

Determination of consideration when there is no distribution; Full value of consideration must be taken as Nil (or)the provision is not applicable

Liquidation of a Company

3 Specific provisions relating to certain transactions

16

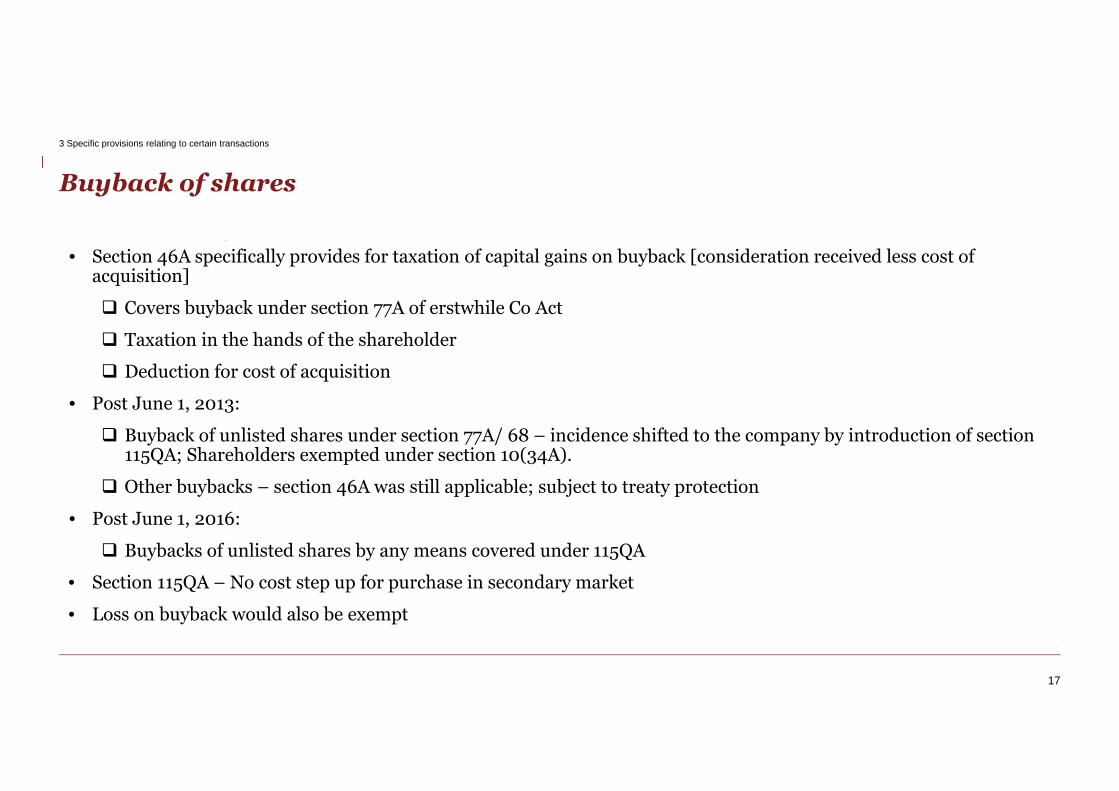

• Section 46A specifically provides for taxation of capital gains on buyback [consideration received less cost ofacquisition]

Covers buyback under section 77A of erstwhile Co Act

Taxation in the hands of the shareholder

Deduction for cost of acquisition

• Post June 1, 2013:

Buyback of unlisted shares under section 77A/ 68 – incidence shifted to the company by introduction of section115QA; Shareholders exempted under section 10(34A).

Other buybacks – section 46A was still applicable; subject to treaty protection

• Post June 1, 2016:

Buybacks of unlisted shares by any means covered under 115QA

• Section 115QA – No cost step up for purchase in secondary market

• Loss on buyback would also be exempt

Buyback of shares

3 Specific provisions relating to certain transactions

17

• Provisions explained:

Gift of a capital asset is non-taxable transfer – 47(iii)

• Issues:

Possibility of corporate gifting?

Applicability of section 50D?

Deemed consideration under the new law – section 50CA

Recipient based taxation – Section 56(2)(x)

Period of holding and cost of acquisition for the donee – Section 2(42A) and 49 refers to original acquisition

Applicability of transfer pricing provisions

Gift of shares

3 Specific provisions relating to certain transactions

18

• Illustrative manner of capital reduction

Reduction of paid up value of shares, in cases where shares are not fully paid up

Cancellation of paid up capital – cancellation of shares or amount paid

Pay off the paid up share capital

• Dividend under section 2(22)(d) to the extent of accumulated profits, whether capitalised or not

• Capital gains chargeable to tax under section 45?

Reduction by change in face value without change in shareholding - Bennett Coleman & Co. Ltd [2011] 12 ITR(T) 97(Mum) (SB)

Payment of consideration for reduction of capital - Kartikeya V. Sarabhai [1997] 228 ITR 163 (SC)

Reduction of amount considered as dividend u/s 2(22)(d) – provision similar to section 46(2) absent - G.Narasimhan [1999] 236 ITR 327 (SC)

Capital reduction

3 Specific provisions relating to certain transactions

19

• Transfer of capital assets by Transferor Company in a non-tax neutral merger

Specific exemption under section 47(vi) – would not be applicable

Absence of flow of consideration to the Transferor company

Non-existence of Transferor company

Statutory vesting of assets and liabilities

• Transfer of capital assets by firm / LLP to company in a non-tax neutral conversion – breach of section 47(xiii)

Implications on subsequent non-satisfaction of conditions

Can the argument for non-tax neutral merger be taken?

Conversion of Company to LLP?

Conversion of a firm to LLP?

Entity restructuring related

3 Specific provisions relating to certain transactions

20

Union budgetamendments

4 Union budget amendments

Important issues in Capital Gains

21

• Introduction of new provision for JDA taxation – section 45(5A):

- Applicable to individuals and HUF

- CG arising on transfer of land/ building/ both pursuant to JDA

- Deferred to obtaining certificate of completion of the project from competent authority– partly/ wholly

- Consideration = stamp value as on date of the certificate of land / building / both in the project + Cash received

- If assessee’s share transferred before obtained completion certificate – sec 45(5A) would be inapplicable – normalprovisions would apply

• Key issues

− Only registered agreements are covered

− CG incidence is postponed; not the date of transfer – time period for investment exemption?

− Determination of consideration

Joint development agreement related

4 Union budget amendments

22

• Section 50CA - Provision explained

- Applicable to all Assessees on sale of unquoted shares – shares quoted in recognised stock exchange based on currenttransactions in ordinary course is excluded

- If consideration received or accruing is less than fair market value (FMV), FMV would be deemed as the full value ofsale consideration

• Draft rule notified for computation of FMV – book value adjusted for specific assets

• Key issues:

- Applicability to all assessees, including unrelated parties

- Interplay with 56(2)(x) – possibility of double taxation

- Existence of consideration, a prerequisite?

- Applicability of TP provisions, other deeming provisions?

Deemed consideration

4 Union budget amendments

23

• Anti-abuse provision

• Capital gains exemption on transfer of listed equity shares to be available for shares acquired after October 2004 only ifSTT was paid on acquisition

- Exceptions for genuine transactions proposed

• Draft rules for the above purpose introduced:

− Acquisition of infrequently traded equity shares listed in recognised stock exchange through preferential issue

− Listed equity shares purchased through off the market transactions – block deals

− Acquisition of equity shares between delisting and listing

LTCG on listed equity shares

4 Union budget amendments

24

• Exemption for conversion of preference shares into equity shares; Cost of acquisition and period of holding of equityshares linked to original purchase of preference shares

- Earlier there was divergent views and jurisprudence on the issue

- Conversion of equity to preference not covered

• NR to NR transfer of Rupee Denominated Bonds - exempted

• Base year for indexation of cost of acquisition shifted from 1981 to 2001

• 10 percent beneficial rate for non residents on sale of shares of a private company made applicable retrospectively fromFY 2012-13

• Period of holding for long term capital gains for land and building reduced to 24 months from 36 months

Others

4 Union budget amendments

25

International tax

5 International tax

Important issues in Capital Gains

26

• Treaties with Mauritius, Singapore, Korea and Cyprus renegotiated:

Investments in shares made from the above jurisdictions till March 31, 2017 grandfathered

W.r.t investments in shares made after March 31, 2017 (from Mauritius and Singapore):

Transfers till March 31, 2019 - Taxable in India at 50 percent of the normal rates, subject to satisfaction of LoBconditions

Transfers after March 31, 2019 – Taxable in India at normal rates

• Key issues:

Shares received after March 31, 2017 from convertible instruments acquired before March 31, 2017

Applicability of bonus and rights shares

Indirect transfers

Treaty amendments - shares

5 International tax

27

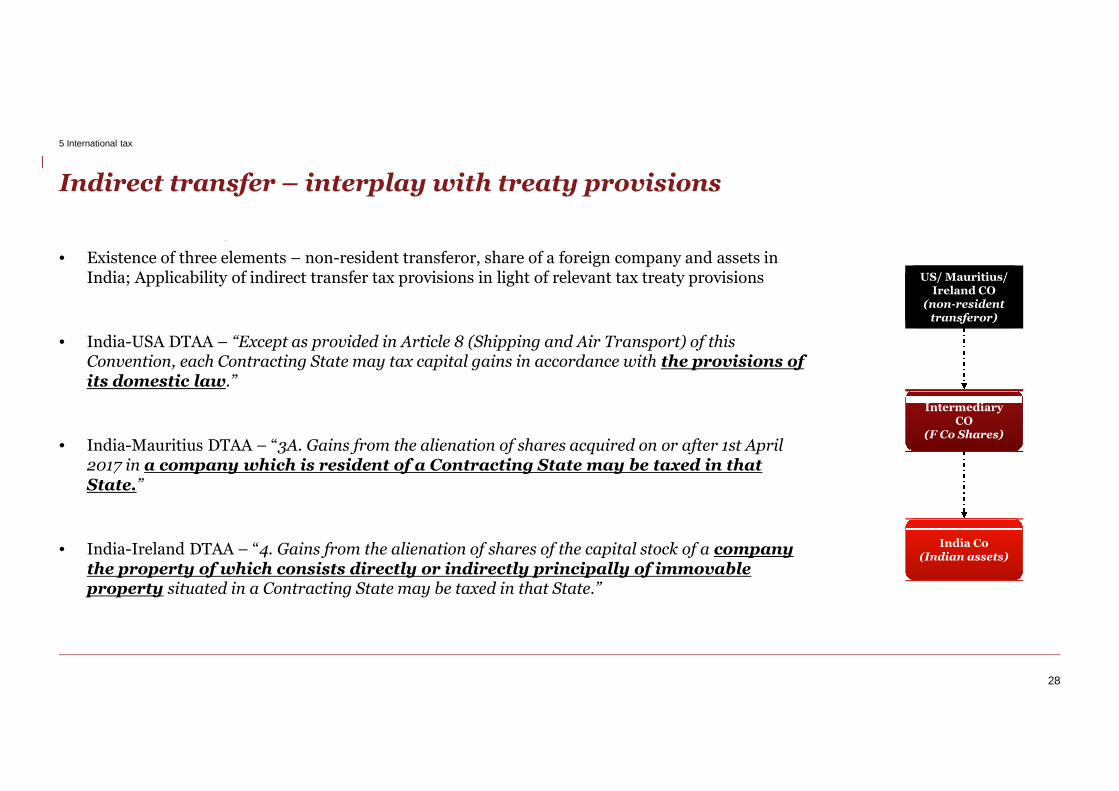

• Existence of three elements – non-resident transferor, share of a foreign company and assets inIndia; Applicability of indirect transfer tax provisions in light of relevant tax treaty provisions

• India-USA DTAA – “Except as provided in Article 8 (Shipping and Air Transport) of thisConvention, each Contracting State may tax capital gains in accordance with the provisions ofits domestic law.”

• India-Mauritius DTAA – “3A. Gains from the alienation of shares acquired on or after 1st April2017 in a company which is resident of a Contracting State may be taxed in thatState.”

• India-Ireland DTAA – “4. Gains from the alienation of shares of the capital stock of a companythe property of which consists directly or indirectly principally of immovableproperty situated in a Contracting State may be taxed in that State.”

Indirect transfer – interplay with treaty provisions

5 International tax

28

US/ Mauritius/Ireland CO

(non-residenttransferor)

IntermediaryCO

(F Co Shares)

India Co(Indian assets)

Thank You

![Capital Gains [Income Tax]](https://img.pdfslide.us/doc/110x75/5695cfd31a28ab9b028fba58/capital-gains-income-tax.jpg)