Embed Size (px)

Citation preview

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Optimizing Social Security and Lifetime Income in Retirement

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

DisclosuresThis material is provided for overview or general informational purposes only. These concepts were derived under current tax and social security laws. Changes in the tax or social security laws may affect the information provided. This is not to be considered, or intended to be legal or tax advice. For answers to specific questions and before making any decisions, please consult a qualified attorney, tax advisor, or the Social Security Administration.

Not affiliated with or endorsed by the Social Security Administration, the Centers for Medicare & Medicaid Services, or any governmental agency.

HealthView and [insert agency] are not affiliates of American United Life Insurance Company® (AUL) and is not a OneAmerica company.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

PresentersJon P. LaFramboise, CLU®

Investment Advisor RepresentativeCentric Financial Group, LLC

Registered Representative of and securities offered through OneAmerica Securities, Inc., Member FINRA, SIPC, a Registered Investment Advisor, 4016 Townsfair Way, Suite 202, Columbus, OH 43219, 614-824-6100. Insurance Representative of American United Life Insurance Company® (AUL) and other insurance companies. Centric Financial Group, LLC. is not an affiliate of OneAmerica Securities or AUL and is not a broker dealer or Registered Investment Advisor .

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Agenda

• Retirement Facts

• Social Security Basics

• Filing Strategies and Recent Changes

• Wrap Up & Q&A

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Retirement Facts

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Retirement Concerns

7

Source: LIMRA

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Fast Facts

•Average Life Expectancy (if healthy)

•Average Length in Retirement

8789

20years

over

Source: HealthView, 2015 RETIREMENT HEALTH CARE COSTS DATA REPORT

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

The Retirement Income Stool

• Social Security • Personal Savings/

Retirement Accounts • Pension / Defined

Benefit

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Retirement ExpensesNon-discretionary expenses (things you MUST cover)

Food Taxes

Debt Transportation

Housing Health Care

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Retirement Expenses• Discretionary expense (things you may WANT to cover)

Legacy Hobbies

Travel Gadgets

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

What’s Discretionary?Contributions to a 529 for a grandchild?

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

What’s Discretionary?Contributions to a 529 for a grandchild?

Helping a child who has not made the best decisions?

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

What’s Discretionary?Contributions to a 529 for a grandchild?

Helping a child who has not made the best decisions?

That family vacation for kids and grandkids you always talked about?

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

What’s Discretionary?Contributions to a 529 for a grandchild?

Helping a child who has not made the best decisions?

That family vacation for kids and grandkids you always talked about?

Tithing?

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

What to Expect

• How will you generate lifetime income for 20-30+ years of retirement?

• Most retirees know how much money they have. Many don’t know how much income they can expect from that retirement

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

For use with financial professionals only. Not for public distribution.

Social Security Basics

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Test Your KnowledgeTest Your KnowledgeHow many years of earnings are included in Social Security benefit calculation?

What is the earliest age a person who is single, married or divorced is able to file for benefits?

If you are 62 or older, what is your FRA?

What percent of retirement benefit income do you lose by claiming Social Security at 62?

How much do benefits increase for waiting to claim past full retirement age (FRA)?

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Social Security Basics:How it Works

• While working, employees contribute 6.2% of earnings to Social Security• Up to $118,500 (maximum in 2016)• Paycheck deduction: “FICA”

• Employers match this amount• Self-employed workers pay 12.4% (6.2%x2)• Contributions are paid forward to current retirees

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

• Three elements govern Social Security benefits received:• Your earnings history• When you claim your benefit• When you pass away

• All three affect us, but we can only control two of them

Social Security Basics:How it Works

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Americans can qualify for benefits one of two ways:

1. On your own record:– Worked and contributed to Social Security for 40

quarters

2. On your spouse’s record:– Married to someone who worked and contributed to

Social Security for 40 quarters• May include an ex-spouse or late spouse

Social Security Basics:Who Is Entitled?

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Bob’s Social Security Benefit

• Bob made a pretty good living throughout his working life

• Typically earned above-average salary, just shy of the Social Security maximum earnings ($118,500 in 2016)

• To calculate Bob’s Social Security benefit:

– Adjust all of Bob’s annual earnings to 2016 dollars– Average the highest paying 35 years ($97,000)– Divide by 12 (months) to get Bob’s averaged adjusted monthly earnings

$8,083: Average Adjusted Monthly Earnings

Any individuals used in scenarios are fictitious and all numeric examples are hypothetical and were used for explanatory purposes only.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Bob’s Social Security Benefit (cont’d.)

• From that $8,083…• The first $856 is multiplied by 90%

• $856 x .90 = $770.40• Every dollar from $856 to $5,157 is multiplied by 32%

• $4,301 x .32 = $1,376.32• All remaining income from $5,158 up is multiplied by 15%

• $2,925 x .15 = $438.75

$770.40 + $1,376.32 + $438.75 = $2,585$2,585: Bob’s Primary Insurance Amount

(PIA)Any individuals used in scenarios are fictitious and all numeric examples are hypothetical and were used for explanatory purposes only.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

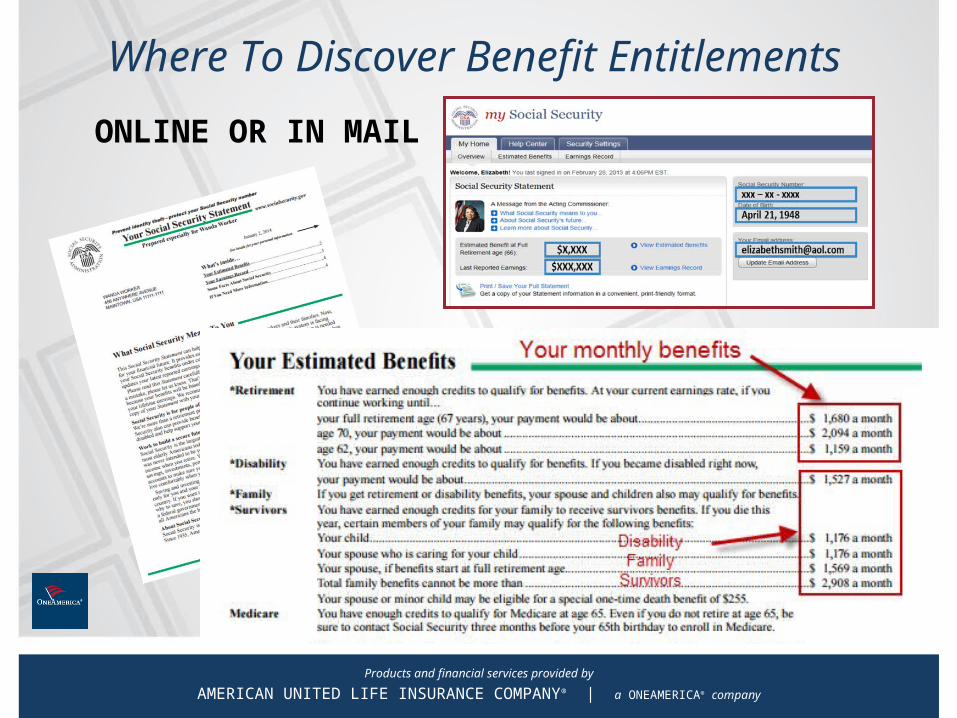

Where To Discover Benefit Entitlements

ONLINE OR IN MAIL

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Available Benefits

• Worker Benefit• Spousal Benefit• Ex-spousal Benefit• Widow/Widower/Survivor Benefit• Dependent Child Benefit• “Young Parent” Benefit• Disability Benefit

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Social Security Basics

Information Required to Determine Benefits:

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Social Security Basics: In the Report

Basic information and assumptions are used to generate results for you and your situation in each report

This report provides broad, general guidelines and strategies which may help you determine your Social Security income. This report isprovided for educational purposes only and you should not rely on it as the primary basis for your insurance, investment, financial, retirementor tax planning decisions.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

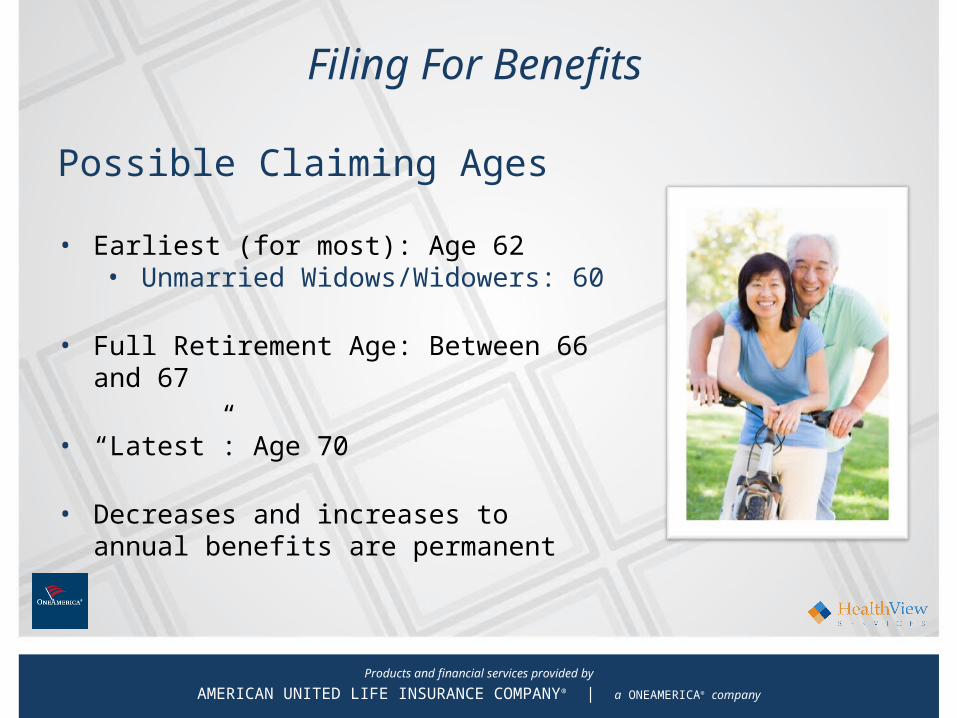

Filing For Benefits

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Filing For Benefits

Possible Claiming Ages

• Earliest (for most): Age 62• Unmarried Widows/Widowers: 60

• Full Retirement Age: Between 66 and 67

• “Latest”: Age 70

• Decreases and increases to annual benefits are permanent

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Full Retirement Age (FRA)

• Social Security Administration (SSA) uses the term “Full Retirement Age” or FRA– Based on individual’s year of birth

• At FRA, SSA recognizes you as qualified to collect “full” Social Security benefits

Year of Birth Full Retirement Age

1937 or earlier 65

1938 65 and 2 months

1939 65 and 4 months

1940 65 and 6 months

1941 65 and 8 months

1942 65 and 10 months

1943 to 1954 66

1955 66 and 2 months

1956 66 and 4 months

1957 66 and 6 months

1958 66 and 8 months

1959 66 and 10 months

1960 or later 67

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Full Retirement Age: In the Report

FRA details, as well as other helpful information, can be found within your personalized report

This report provides broad, general guidelines and strategies which may help you determine your Social Security income. This report isprovided for educational purposes only and you should not rely on it as the primary basis for your insurance, investment, financial, retirementor tax planning decisions.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

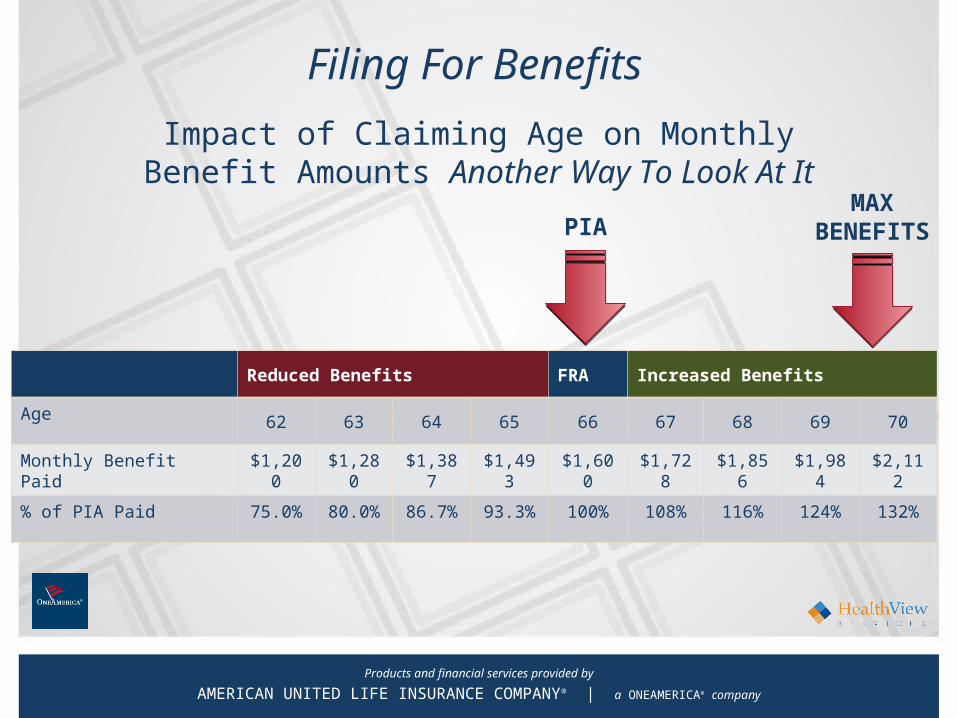

Filing For Benefits

Impact of Claiming Age on Monthly Benefit Amounts Another Way To Look At It

Reduced Benefits FRA Increased Benefits

Age 62 63 64 65 66 67 68 69 70

Monthly Benefit Paid $1,200

$1,280

$1,387

$1,493

$1,600 $1,728

$1,856

$1,984

$2,112

% of PIA Paid 75.0% 80.0% 86.7% 93.3% 100% 108% 116% 124% 132%

PIAMAX

BENEFITS

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Benefits of WaitingIncrease in benefits for clients with Full

Retirement Age (FRA) of 66/67

FRA: 66Age Benefit Increase

67 8%

68 16%

69 24%

70 32%

FRA: 67Age Benefit Increase

68 8%

69 16%

70 24%

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Filing For Benefits

• Mary:• 50 year old single

woman• PIA of $1,600• Life Expectancy: 89

• Optimal Claim Age: 70

The Impact of Life Expectancy

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

• Mary:• 50 year old single woman• PIA of $1,600• Life Expectancy: 74

• Optimal Claim Age: 62

Filing For Benefits

The Impact of Life Expectancy

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Filing For Benefits: In the Report

Year-by-year benefit projections show impact of life expectancy and “breakeven” point

This report provides broad, general guidelines and strategies which may help you determine your Social Security income. This report isprovided for educational purposes only and you should not rely on it as the primary basis for your insurance, investment, financial, retirementor tax planning decisions.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

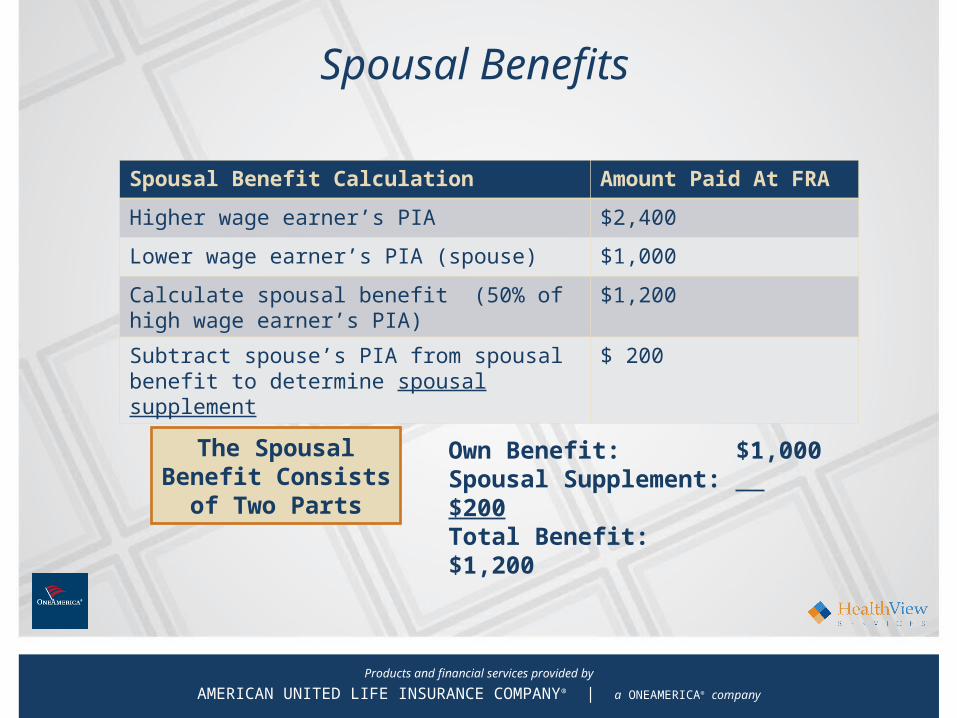

Spousal Benefit Calculation Amount Paid At FRA

Higher wage earner’s PIA $2,400

Lower wage earner’s PIA (spouse) $1,000

Calculate spousal benefit (50% of high wage earner’s PIA)

$1,200

Subtract spouse’s PIA from spousal benefit to determine spousal supplement

$ 200

The Spousal Benefit Consists

of Two Parts

Own Benefit: $1,000Spousal Supplement: $200Total Benefit: $1,200

Spousal Benefits

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Ex-Spousal Benefits

• Benefits are essentially the same as current spouse, if client meets below criteria:

• Unmarried*• Age 62 or older• Divorced at least two years• Marriage lasted 10 years or longer

*Can be married if remarriage took place at age 60 or later

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Widow/Widower/Survivor Benefits

• Can file for survivor benefits as young as age 60• No increase in benefits for delaying past

FRA

• Benefit is 100% of deceased spouse’s benefit• If spouse had claimed

• Benefit deceased was receiving • If spouse had not claimed

• PIA of deceased

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Filling the “Survivor Gap”

DELAY higher earner benefits as long as possible because higher earner covers two lives

1,6001,067 PIA PIA

Combined$2,667

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Filling the “Survivor Gap”

DELAY higher earner benefits as long as possible because higher earner covers two lives

1,6001,067 PIA PIA

Combined$2,667

$1,067 less

EVERY month

1,600

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Spousal Options After FRA: In the Report

All possible claiming options are reviewed, and the “Selected” and “Optimal” are highlighted

This report provides broad, general guidelines and strategies which may help you determine your Social Security income. This report isprovided for educational purposes only and you should not rely on it as the primary basis for your insurance, investment, financial, retirementor tax planning decisions.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Filing Strategies and Recent Changes

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Filing StrategiesFile For Benefits

Strategy: File For BenefitsWho Can Do It: Anyone eligible for Social Security benefitsWhen Can It Be Done: Anytime from 62 to 70What Happens: Client receives his or her benefit

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Before The Recent Budget Deal:

Strategy: File A Restricted Application

Who Can Do It: Any married person eligible for Social Security that has achieved his or her Full Retirement Age (FRA)

When Can It Be Done: Anytime from FRA to 70

What Happens: Client delays his or her own benefit, and instead receives 50% of his or her spouse’s benefit (includes divorcees)

Filing StrategiesFile Restricted

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Effective Immediately:

Strategy: File A Restricted Application

Who Can Do It: Any married person eligible for Social Security that has achieved his or her Full Retirement Age (FRA) who turned 62 by 2015

When Can It Be Done: Anytime from FRA to 70

What Happens: Client delays his or her own benefit, and instead receives 50% of his or her spouse’s benefit as long as spouse is receiving benefits

Filing StrategiesFile Restricted

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Other Factors to Consider

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Cost of Living Adjustment (COLA)

• Annual percentage increase in benefits• Helps offset increase in

retirement expenses

• Trustees’ projections:• 2016: 3.1% Increase• 2017 and beyond: 2.7% increase

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

COLA: In the Report

Benefit increases due to COLA are accounted for in all projections

This report provides broad, general guidelines and strategies which may help you determine your Social Security income. This report isprovided for educational purposes only and you should not rely on it as the primary basis for your insurance, investment, financial, retirementor tax planning decisions.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Child and “Young Parent” BenefitsA Family Affair

• Requirements:• Child under 18• Dependent child of

Social Security claimer• Benefits:

• 50% if parent is alive• 75% if parent is deceased

• Note: Unclaimed spouse of worker may be eligible for benefit (50%) if child under is 16

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

WEP And GPO

WEP and GPO may reduce or eliminate benefits based on public sector work and public pension

•WEP: Windfall Elimination Provision

•GPO: Government Pension Offset

•Benefit may decrease due to:• Years in public/private sectors• Pension value

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Rising Cost of Health Care• Rising cost of health care primary concern of:

– 82% of Baby Boomers– 72% of Gen X and Gen Y

Source: Massachusetts Financial Services (MSF), “MFS Investing Sentiment Insights Survey, 2014

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

The Medicare Alphabet

Part AHospitalization

Part BMedical Coverage

Part DDrug Coverage

MediGapSupplemental

Policy

Out-Of-Pocket CostsCopays, deductibles, etc.

Free*

Surcharges Paid by Social

Security deduction

Premiums, Surcharges

Paid Via Social Security

Not Paid Via Social Security

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Medicare Means Testing Brackets

Means Testing ThresholdsIncome Bracket Individuals Couples % Change in Cost

1st <$85,000 <$170,000

2nd $85,001-$107,000 $170,001-$214,000 37%

3rd $107,001-$133,500 $214,001-$267,000 93%

4th $133,501-$160,000 $267,001 - $320,000 149%

5th $160,000+ $320,000+ 204%

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Medicare Means: The Impact

Jane (Single 65 year old woman)

$186.42 – Monthly Medicare Part B and D Premiums

$135,000 - Annual Income

Because of her income, she is placed in the 3rd surcharge bracket (4th overall) – adding a 150% surcharge throughout retirement.

$476.92 – Actual cost of Medicare Part B($186.42 + $290.50 surcharge)

Both of these are deducted from Jane’s Social Security check.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Modified Adjusted Gross Income (MAGI)

Increases MAGI

•Social Security•Salary/Wages•Pension•RMDs•Dividends•Capital Gains•IRA Distributions

Does not Does not increase MAGIincrease MAGI

•Life Insurance•Non-Qualified Annuity*•Health Savings Account•Roth 401(k)•Longevity Insurance*•Reverse Mortgage

*To the extent that income is excluded, based on the exclusion ratio

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Managing Retirement Income Streams by Tax Asset Category

1. Pension and IRA income2. Interest income3. Dividend income4. Capital gain income5. Real estate, oil & gas income6. Annuity income7. Tax-exempt income8. Social Security income9. Roth IRA and life insurance income10.Loan cash flow11.Health Savings Account (HSA)

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Why is it important to manage tax-asset categories during

retirement?• Higher taxable income leads to:

– Higher marginal ordinary income tax brackets– Phase-out of personal exemptions– Phase-out of itemized deductions– 3.8% excise tax on income in excess of non-indexed thresholds

added by the Affordable Care Act– Income tax on Social Security benefit– Medicare Part B surcharges

All of these items increase the taxes that you will pay on your retirement income and Medicare.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

The Key• The key to managing tax asset category

income streams during retirement is to position in those categories before retirement

• Diversification can be not only based on time horizon, risk, and traditional measures, but also based on tax asset class

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Wrap Up & Moving Forward

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company 61

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$678,306

$737,850

$374,937$344,680

Lifetime Value of Lifetime Value of Social Security Social Security

Average Earner Couple$719,617

Max Earner Couple$1,416,156

“Today’s Dollars”

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Social Security Summary

• Significant form of retirement income for many Americans

• Earnings history, current age, claim age among most important variables

• Life expectancy can have major influence on optimal filing age

• Deferring Social Security benefits can allow you to have a larger safety net of inflation-adjusted lifetime income

• Important factors such as WEP/GPO, COLA, Medicare, and taxes should be considered

Note: When to begin Social Security is a very personal decision and beginning earlier may make sense for you, e.g., you are not in good health, have a family history of shorter than average life expectancy, etc.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Social Security Decision Making

• Social Security is not a decision meant to be made independently

• Other retirement factors and variables must be considered in conjunction with Social Security

– Desired retirement age– Life expectancy– Taxes– Medicare– Other retirement income

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Decision Making: In the Report

Customized Action Plan explains the “how” and “when” of filing

This report provides broad, general guidelines and strategies which may help you determine your Social Security income. This report isprovided for educational purposes only and you should not rely on it as the primary basis for your insurance, investment, financial, retirementor tax planning decisions.

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Optimizing Your Retirement Income Starts With:

Optimizing Social Security, Optimizing Retirement Income and Protecting

Against Longevity

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company

Thank You! Q&A Time

Products and financial services provided byAMERICAN UNITED LIFE INSURANCE COMPANY® | a ONEAMERICA® company