Embed Size (px)

Citation preview

ltDI March 2000

Centre for Development Economics

Nonparametric Bootstrap Tests for Neglected Nonlinearity ill Time Series Regression Models

Arnall Ullab Centre for Development Economics

amp Department of Economics University of California

Riverside CA 92521 ullahmailucredu

Tae-Hwy Lee Department of Economics

University of California Riverside CA 92521 taeleemailucredll

Working Paper No 77

Abstract

A unified framework for various nonparametric kemel regression estimators is presented based on which we consider two non parametric tests for neglected nonlinearity in time series regression models One of them is the goodness-of-fit test of Cai Fan and Yao (2000) and another is the nonparametric conditional moment test by Li and Wang (1998) and Zheng (1996) Bootstrap procedures are used for these tests and their perfomlance is examined via monte carlo experiments especially with conditionally heteroskedastic errors

Key Words nonparametric test nonlinearity time series functional-coefficient model conditional moment test naive bootstrap wild bootstrap conditional heteroskedasticity GARCH monte carlo

HL Classification C 12 C22

We would like to thank Zongwu Cai Jianqing Fan and Qj Li for programs and discussion Lee thanks UC Regentss Faculty Fellowship and Faculty Development Awards and Ullah thanks the Academic Senate of UCR for the research support

1 Introduction II

Much research in empirical and theoretical econometrics has been centered around the esti~

mation and testing of vario~ flmctions such as regression functions (eg conditional mean

and variance) and density functions A traditional approach to studying these functions has

been to fist impose a parametric functional form and then proceed with the estimation and

testing of interest A major disadvantage of this approach is that the econometric analysis

may not be robust to the slight data inconsistency with the particular parametric specific~

tion and this may lead to erroneous conclusions In view of these problems in the last five

decades a vast amount of literature has appeared on the nonparametric and semi parametric

approaches to econometrics eg see the books by Hardle (1990) Fan and Gijbels (1996)

and Pagan and Ullah (1999) The basic point in the nonpararuetric approach to econometrics

is to realize that in many instances one is attempting to estimate an expectation of one

variable y conditional upon others x This identification directs attention to the need to

be able to estimate the conditional mean of y given x from the data Yt and Xt t = 1 In

A nonparametric estimate of this conditional mean simply follows as a weighted average

Lt w(Xt x)Yt where w(Xt x) are a set of weights that depend upon the distance of Xt from

the point x at which the condi tional expectation is to be evaluated

Based on these nonparametric estimation techniques of the conditional expectations in

recent years a rich literature has evolved on the consistent model specification tests in econoshy

metrics For example various test statistics for testing a parametric functional form have

been proposed by Bierens (1982) UUah (1985) Robinson (1989) Eubank and Spiegelman

(1990) Yatchew (1992) Tooldridge (1992) Gozalo (1993) Hardle and Mammen (1993)

Hong and White (1995) Zheng (1996) Bierens and Ploberger (1997) and Li and Wang

(1998) Also see UUah and Vinod (1993) Whang and Andrews (1993) Delgado and Stenshy

gos (1994) Lewbel (1993 1995) AIt-Sahalia et al (1994) Fan and Li (1996) Lavergne and

Vuong (1996) and Linton and Gozalo (1997) for testing problems related to insignificance of

regressors non-nested hypothesis semi parametric versus nonparametric regression models

among others 110st of these tests especially the test for a parametric specification are

developed under the following goodness of fit measures (i) compare the expected values

of the squared error under the null and alternative hypotheses (eg Ullah (1985) type F

statistic) (ii) calculate the expected value of the squared distance between the null and

1

s

oJternaUve rnodel spc1ificatic)l1s (eg Hlirdle poundlud M~unmen (1993) Ullah and Vinod (1993)

Ait~SahEllia (1994)) and (iii) calculate the expected value of the product of the error lUlder

the null with the model specffied under the aHernative (eg conditional moment tests of

BiercnS (1982) Zhang (1996) Fan and Li (1996) and Li and Wang (1998) All these three

alternative goodness of fit measures are equal to zero lWder the null hypothesis of correct

specification For details see Pagan and Ul1ah (1999)

We note here that the asymptotic as well as the simulation based finite sample proper~

ties of the most of the above mentioned test statistics have been extensively analyzed for

the cross sectional models with independent data However not much is known about the

asymptotic as well as the small sample performance of these test statistics for the case of

time series models with weak dependent data although see the recent works of Chen and

Fan (1999) Hjellvik and Tj0stheim (1995 1998) Hjellvik et al (1999) Kreiss et al (1998)

Berg and Li (1998) and a very important contribution by Li (1999) where he develops the

asymptotic theory results of Li-Wang-Zheng (LWZ) test under the goodness of fit measure

(iii) The modest goal of this paper is to conduct an extensive monte carlo study to analyze

the size and power properties of two kernel based tests for time series models One of them

is the bootstrap version of Ullahtype goodness of fit test (i) due to Cai Fan and Yao (2000

henceforth CFY) and another is the nonparametric conditional moment goodness of fit test

(iii) of LWZ We examine the bootstrap performances of these two goodness of fit tests beshy

cause of the asymptotic validity results of using bootstrap methods for these statistics due to

CFY (2000) and Berg and Li (1998) Berg and Li (1998) also support the better performance

of LWZ over the Hardle and Mammen (1993) type tests considered for time series data in

Hjellvik and Tj0stheim (1995 1998) Hjellvik et al (1999) and Kreiss et al (1998) For the

purpose of our simulation study we consider the testing of linearity against a large class of

nonlinear time series models which include threshold autoregressive bilinear exponential

autoregressive models smooth transition autoregressive models GARCH models and var~

ious nonlinear autoregressive and moving average models Both naive bootstrap and wild

bootstrap procedures are used for our analysis We also compare the bootstrap results with

the results using the asymptotic distribution for LWZ test

The plan of the paper is as follows In Section 2 we present the nonparametric kernel

regression estimators and the tests of CFY and LWZ based on them Then in Section 3 we

2

pr

2

2

is

the monte carlo results Finally Section 4 gives conclusions

Nonparametric regression and specification testing

Nonparametric regression

UtI Xtl t 1 I n be stochastic processes where Yt is a scalar and Xt = (Xtll Xtk)

a 1 x k vector which may contain the lagged valu~ of Yt Consider the regression model

(1)

where m(xc) E (YtIXt) is the true but unknown regression fllhction and Ut is the error term

that E(Utlxt = 0 and Var(UtXt) == (72

If m(xc) == g(Xt 6) is a correctly specified family of parametric regression functions then

== g(Xt 6) +Ut is a correct model and in this case one can construct a consistent least

squares (LS) estimator of m(Xt given by g(x 6) where 6is the LS estimator of the parameter

6 This 6is obtained by minimizing

(2)

with respect to 6 For example if 9(XtO) = Xto is linear we can obtain the LS estimator of

0 as

6= (XX)-lXy (3)

and the predicted residuals il t = Yt - m(xt) where X is an n x (k + 1) matrix generated by

X t = (1 Xt) and

(4)

In general l if the parametric regression gXto) is incorrect or the form of m(Xt) is unknovvn

then 9(Xt1 b) may not be a consistent estimator of m(Xt)

For this case an alternative approach to estimate the unknown m(xc) is to use the

consistent nonparametric kernel regression estimator which is essentially a local constant LS

(LeLS) estimator To obtain this estimator take Taylor series expansion of m(Xt around I

so that

Yt - m(Xt) +Ut (5)

- m(x) +tt

3

(9)

wht

wit

LC

0(1

derivative of m(x) at Xt x ThcpLCLS estimator can then be derived by minimizing

n n

2 vlKtt = 2(Yt - m(xraquo2Ktz (6) t-I 1

with respect to constant m(x) where K tz = K(xI1) is a decreasing function of the distanCeS

of the regressor vector Xt from the point x = (Xb X) and h -+ 0 as n -t oc is the

window width (smoothing parameter) which determines how rapidly the weights decrease as

the clistance of Xt from x increases The LCLS estimator so estimated is

bull( ) _ l~1 YtKtx _ (OK( ))-1degK( ) (7)m x - K - I X I I X Y4t=l tr

where K(x) is the n x n diagonal matrix with the diagonal elements (Klr Knx) and i is

an n x 1 cohunn vector of unit elements The estimator m(x) is due to Nadaraya (1964) and

Watson (1964) (NW) who derived this in an alternative way Generally ih(x) is calculated

at the data points Xt in which case we can write the leave-one out estimator as

_ () E~=1tFt Yt Ktt (8)m x = n 4t=1tt Ktt

where Ktt = Kec~Xt) The assumption that h -tO as n -+ 00 gives Xt - x = O(h) -t 0

and hence EVt -t 0 as n -t 00 Thus the estimator m(x) will be consistent under certain

smoothing conditions on h K and m(x) In small samples however EVt f 0 so m(x) will be

a biased estimator see Pagan and Ullah (1999) for details on asymptotic and small sample

properties

An estimator which has a better small sample bias and hence the mean square error

(MSE) behavior is the local linear LS (LLLS) estimator due to Stone (1977) and Cleveland

(1979) also see Fan and Gijbels (1996) and Ruppert and Wand (1994) for their properties

In the LLLS estimator we take first order Taylor-Series expansion of m(xt) around x so that

Yt - m(xt) +Ut = m(x) + (Xt - x)m(l)(x) +Vt

- a(x) + XtB(x) + Vt

- Xto(x) +Vt

4

estin

and

to 1)

Obv

j

witl

h= the

esti

coe

1

(6)

nreg

the

(7)

Us

(8)

~ 0

un be

Ie

[o(x) t3(x)] with Q(x) = m(x) x3(x) and f3(x) = m(l)(x) The LLLS

estimator of 6(x) is then o~ned by minimizing

n n

Lv~KtJ = 2(Yt Xt6(X))2Ktt (10) t~l t~l

and it is given by

6(x) = (XK(X)X)-l XK(x)y (11)

The LL~S estimator of a(x) and f3(x) can be calculated as amp(x) = [1 0)6(x) and ~(x) ==

[0 1)6(x) This gives

~(X) = [1 x]8(x) = amp(x) + x[3(x) (12)

Obviously when X = i 8(x) reduces to the NWs LeL8 estimator m(x)

An estimator of the LLL8 is the local polynomial L8 (LPL8) estimators see Fan and

Gijbels (1996) In fact one can obtain the local estimators of a general nonlinear model

g(Xtlj) by minimizing n

L[Yt - g(Xtl o(x))fKt1 (13) =1

with respect to o(x) For g(xto(x)) = Xto(x) we get the LLL8 in (11) Further when

h = 00 Ktx = K(O) is a constant so that the minimization of K(O) ElYt - g(xt o(x))]2 is

the same as the minimization of ElYt - g(x 0(x))]2 that is the LL8 becomes the global L8

estimator given by (3)

The LLL8 estimator in (11) can also be interpreted as the estimator of the functional

coefficient (varying coefficient) linear regression model

Yt - m(xt) + Ut (14)

- Xto(x) + Ut

where o(Xt) is approximated locally by a conStant o(Xt) ~ o(x) The minimization of E uKtx

with respect to 6(x) then gives the LLL8 estimator in (11) which can be interpreted as the

LC varying coefficient estimator An extension of this is to consider the linear approximation

o(Xt) ~ o(x) + D(x)(xt - xY where D(x) = 8~~t) evaluated at Xt = x In this case

Yt - m(Xt) + Ut = Xto(Xt) + Ut (15)

Xto(x) + XtD(x)(xt - x) + Ut

5

(20)

(21)

N

S

= X8(x) +X 0 (Xt - x)vecD(x) + Ut

= ~8(x) +Ut

wbere Xt = tXt Xt 0 (Xt - x)] cmiddot(x) = [c(x) (vecD(x))) and 0 represents the Hadamard

product The LL varying coeffident or LPLS estimator of c(xcan then be obtained by

minimizing n

(16)L[Yt - Xc(x)fK e= 1

with respect to c(x) as

r (x) = (X K(x)X)-l X Kx)y (17)

- From this 8(x) = II 0]8 (x) and hence

- shy1 (x) = [1 x 0]8 (x) = Il xJ6(x) (18)

The above idea can be extended to the situations where et = (Xt Zt) such that

(19)

where the coefficients are varying with respect to only a subset of et Zt is 1 x l and et is

1 X P P = k + l Examples of these include random coefficient model (Raj and UUah 198L

Granger and Teriisvirta 1993) exponential autoregressive model (Haggan and Ozaki 1981)

and threshold autoregressive model (Tong 1990) also see Section 3 To estimate C(Zt) we can

again do a local constant approximation C(Zt) ~ c(z) and then minimize E[Yt - Xc(z)]2K tz

with respect to c(z) where K tz = KCt) This gives the LC varying coefficient estimator

8(z) = (XK(Z)X)-l XK(z)y

where K(z) is a diagonal matrix of Ktz t = 1 n

CFY (2000) consider a local linear approximation b(zt) ~ 6(z) + D(z)(zt - z) The LL

varying coefficient estimator of CFY is then obtained by minimizing

n n

L[Yt - X tC(Zt)]2 K tz - LIYt - Xtc(z) - (Xt 0 (Zt - z))vecD(z)]2Ktz t=1 t=1

n

- 2)Yt - X6(z)j2Ktz t==l

6

witl

Me

WI

ing

2

Cc

rut

In

etl

T

d

Y

i)

)

)

5

1

with respect to 6(z) [6(z (1JecD(z))j where Xi ~ [X Xt ) (Zt - z)] Thls gives

-I6 (z) = (XK(Z)x u -lXu K(z)y (22)

- and 6(z) = [10]6 (z) Hence

(23)

When z = x (20) and (22) reduce to the LLLS estimator bex) in (11) and the LL vary~

ing coefficient estimator 6 (x) in (17) respectively For the asymptotic properties of these

varying coefficient estimators see CFY (2000)

22 Nonparametric tests for functional forms

Consider the problem of testing a specified parametric model against a nonparametric (NP)

alternative

Ho E(ytleurot = g(ee 6)

HI E(ytleuro) = m(eurot)

In particular if we are to test for neglected nonlinearity in the regression models set 9 (et 16) = eurot8 Then under HOI the process yd is linear in mean conditional on eurot

(24)

The alternative of interest is the negation of the null that is

(25)

When the alternative is true a linear m09-e1 is said to suffer from neglected nonlinearity

Note that eurot = (Xt Zt) = Xt when zt = Xt

Using the nonparametric estimation technique to construct consistent model specification

tests was first suggested by UUah (1985) The idea is to compare the parametric residual

sum of squares (RSSP ) E ur ilt = Yt - g(euro 6) with the nonparametric RSS (RSS~P) L u-

where Ut = Yt ~ m (eurot) The test statistic is

(26)

7

~--- -----~--~~--------------------~-------

or simply TI (RSSP -- RSSNP) We reject the null hypothesis when T is large ViiT has a

degenerate distribuUon under ltlo- Yatchew (1992) avoids this degeneracy by splitting sample

of n into 711 and n2 and calculating L u based on nl observations and r u based OJ) n2

observations Lee (1992) l)es density weighted residuals and compares EWtu with LU Fan and Li (1995) uses different normalizing factor and show the asymptotic normality of

nhP 2T

Another way is to use the bootstrap method as suggested by CFY (2000) The bootstrap

allows the implementation of (26) and it involves the following steps to evaluate p-values of

the test

1 Generate the bootstrap residuals u from the centered NP residuals (iit -11) where

11= n-1 Lilt and define V == et 6+u

2 Construct the bootstrap sample v et f=l and calculate the bootstrap fest statistic

T using for the sake of simplicity the same h used in estimation with the original

sample

3 Repeat the above two steps B times and use the empirical distribution of T as the

null distribution of T Reject the null hypothesis Ho when T is greater than the upper

a point of the conditional distribution of T given Vt ettl The p-value of the test

is simply the relative frequency of the event Tmiddot 2 T in the bootstrap resamples

Kreiss et al (1998) provide more detailed r~asons why the bootstrap works in general

non parametric regression setting They proved that asymptotically the conditional distrishy

bution of the bootstrap test statistic is indeed the distribution of the test statistic under

the null hypothesis As mentioned by CFY (2000) it may be proved that the similar result

holds for T as long as 6converges to f at the rate n-12 We use both naive bootstrap (Efron

1979) and wild bootstrap (Wu 1986 Liu 1988) The wild bootstrap method preserves the

conditional heteroskedasticity in the original residuals For wild bootstrap see also Shao

and Th (1995 p 292) Hardle (1990 p 247) or Li and Wang (1998 p 150)

An intuitive and simple test of the parametric specification follows from the combined

regression

8

p

v

k

v

l (

las a

nple paramotric specification is tmen the conditional moment test for mu(et) = E(utlet) 0

n n2 which is identical to testing

E[uE(ucled(et) = 0 (28)

y of where f(et) is the density of e A sample estimator of the left hand side of (28) is

Lrap (29)

s of

lere where E(Utlet) = Etl utKed EtirH Kt t from (8) and j(et) = (nhPt 1 2t1ft Ktt is the

kernel density estimator Ktt = K((h(I) The asymptotic test statistic is then given by

2 Lstic L nhP r N(O 1) (30) vw

nal where w 2(n(n - 1)hP)-1 Et Etlt-t ft~UIKft is a consistent estimator of the asymptotic

variance of nhP 2 L see Zheng (1996) Fan and Li (1996) Li and Wang (1998) Fan and the Ullah (1999) and Rahman and Ullah (1999) for details Also see Pagan and Ullah (1999

per eh 3) and Ullah (1999) for the relationship of this test statistic with other nonparametric est specification tests Based on the asymptotic results of Fan and Li (1996 1997 1999) and Li

(1999) for dependent data Berg and Li (1998) establish the asymptotic validity of using the

wild bootstrap method for L for time-series ral

rishy3 Monte carlo

ler

llt In this section we examine the finite sample properties of T and L especially with the on empirical null distributions being generated by the bootstrap method Asymptotic critical he values are also used for L To generate data we use the following models all of which ao have been used in the related literature Most of them are univariate while there are some

multivariate situations There are six blocks The error term Ct below is iid N (0 1) unless

otherwise is indicated The models will be referred by the name shown in parentheses in

bold 7)

9

BLOCK 1 (I~gte White and Granger 1993)

Linear (AR)

Linear AR with GARCH (AR)

Vt - O6Yt_l + pound

ht - E(cIYt-l) = (1 - a - (3) +Qe-l + (3ht- 1

Bilinear (BL)

Threshold Autoregressive (TAR)

Yt - 09Yt-l + et IYt-11 ~ 1

- -O3Yt-l + et IYt-IIgt 1

Sign Nonlinear Autoregressive (SGN)

Yt = sign(Yt-l) +et

where sign(x) = 1 if xgt 00 if x = 0 and -1 if x lt O

Rational Nonlinear Autoregressive (NAR)

071Vt-l Yt = I 2 +CtYt-l +

BLOCK 2 (Lee White and Granger 1993)

MA() (Ml)

Heteroskedastic MA(2) (M2)

Note that 112 is linear in conditional mean as the forecastable part of M2 is linear and the

final term introduces heteroskedasticity

No

Ali

Bil

BL

Squ

Eq

ThE

BLi

fron

Lin~

Que

10

Nonlinear MA (M3) til

y = It - O3et_l + O2Ct-2 + OAet-lct-2 - O25e~_2

AR(2) (M4)

Bilinear AR (M5)

Bilinear ARMA (M6)

Vt = OAY-l - O3Vt-2 + O5Vt-middotlet-l + O8et-l + Et

BLOCK 3 (Lee White and Granger 1993)

Square (SQ)

Exponential (EXP)

These are bivariate models where Xt = O6Xt-l +et Ctt rv N(O 52)and Ctt Et are independent

BLOCK 4 (Zheng 1996)

Five models with Xt = (X71 Xt2) are considered in this block Let Un and Ut2 be drawn

from IN(O 1) Two regressors Xtl and Xt2 are defined as Xu = Utl and Xt2 = (Uti +udJ2middot

Linear (ZI)

Yt = 1 + Xtl + Xt2 + et

Linear with conditionally heuroskedastic error (ZI)

11 - 1 + Xu + Xt2 + et

h- _ E(elx~) = (1 + X~l + X2)3

the Quadratic (Z2)

Yt = 1 + Xu + Xt2 + Xu X t2 + Et

11

Concave (Z3)

II lt = (1 + Xu + Xt2)13 + Et

Convex (Z4)

BLOCK 5 (Cai Fan and Yao 1999)

Exponential AR (EXPAR)

Yt - al(Yt-dYt-l + a2(Yt-dYt-2 +et

al (Yt-l) - 0138 + (0316 + 0982Y_I) exp( -389Y~I)

a2(Yt-l) - -0437 - (0659 + 1260Yt_1) exp(-389Y_I)

e IV 1N(O 022 )

Threshold AR (TAR)

Yt - al (Yt-2)Yt-1 + a2(Yt-2)Yt-2 + et

a1 (Yt-2) - 04(Yt-2 ~ 1) - 08(Yt-2 gt 6)

a2(Yt-2) - -06(Yt-2 ~ 1) + 02(Yt-2 gt 1)

et 1N(O 1)IV

BLOCK 6 (Terasvirta Lin and Granger 1993)

Logistic smooth transition AR (LSTAR)

Yt - 18Yt-l - 106Yt-2 + (002 - 09Yt-l +O795Yt-2)F(Yt-1) + et

F(Yt-l) - [1 + exp -100(Yt-l - O02)t1

et rv IN(OO022 )

Exponential smooth transition AR (ESTAR)

Yt - 18Yt-1 - 106Yt-2 + (-09Yt-1 +0795Yt-2)F(Yt-l) + et

F(Yt-1) - [1 - exp-4000Y_1t1

I3t rv 1N(O 0012 )

12

T

inion

for B

F( Let T1

sutrS(

then 1

mb~

squar

where

and 6t Epane

(with I

for BIc

FOI

an 1 x

param4

for BIo

values

will be

Teslt

methoc

bootstr

with 30

Tao

are line

To estimate (3) and Ut

ntDlrIIUiII111IU set used are et Yt-l for Block 11 et Block 3 and et (xu X(2) for Block 4

For T as suggested by CFY (2000)

es of lengths n

m bnsed on the estimated models That is to choose h minimizing the average of the mean

rtf the linear model Iltld (23) and Ut for the NP model the

(Yl Yt-2) for Blocks 2 5 and 6 et = Xt

we select h using out-of-sample cross~vaUdatlon

m andQ be two positive integers such that n gt mQThe basic idea is first to use Q

- qm (q = 1 Q) to estimate the coefficient functions Oq(Zt and

to compute the one-step forecast errors of the next segment of the time series of length

Q

AMS(h) 2AMSq(h) (31) q=l

1 n-~+m -

AMSq(h) = m L [Yt - X t 5q(Zt)]2 (32) t=n-qm+l

-and 5q() are computed from the sample Yt et~tn We use m = [Oln) Q = 4 and the

Epanechiniko kernel K() = ~(l - z2)1(lzl lt 1) We use a scalar threshold variable Zt

(with l = 1) for all models Zt = Yt-l for Blocks 12 and 6 Zt = Xt for Block 3 and z = Xlt

for Block 4 For Block 5 Zt = Yt--l for EXPAR and Zt = Yt-2 for TAR

For L as in Li and Wang (1998 p 154) we use a standard normal kernel Note that et is an 1 x p vector and p = 1 for Blocks 13 and p = 2 for Blocks 2 4 5 6 Thus the smoothing

parameter h is chosen as hi - cain-l5 (i = 1) for Blocks 1 and 3 and hi = win-16 (i = 12)

for Blocks 2 middott 56 where ai is the sample standard deviation of i-th element of e The three

values of c = 05 1 and 2 are used and the corresponding estimated rejection probability

will be denoteurod as Le In computing L hP shown in (29) and (30) is replaced with Df=l hi

Test statistics are denoted as Ti and L~ with the superscripts i = A B W referring to the

methods of obtaining the null distributions of the test statistics asymptotics (i = A) naive

bootstrap (i = B) and wild bootstrap (i = W) Monte carlo experiments are conducted

with 300 bootstrap resamples and 300 monte carlo replications

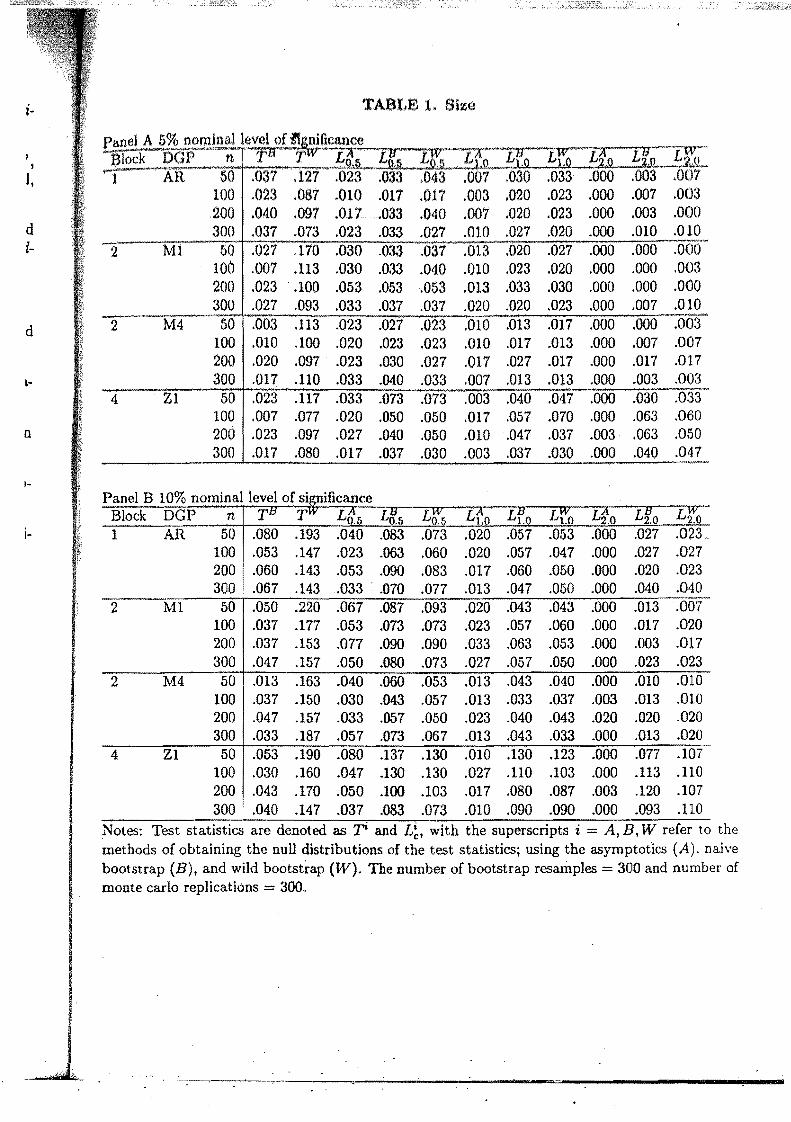

TaBle 1 gives the estimated size of the tests for the data generating processes (DGP) which

are linear in conditional mean Table 1 reports the cases with the conditional homoskedastic

13

(~rrors The 95 confidence interval of the estimated size is (0025 0075) at 5 nOmlnal

level of significance and (0066~134) at 10 nominal level of significance since if the true

size is 8 (eg s 1$ 005010) the estimated size follows the asymptotic normal distribution

with mean s and variance 8(1 - s) 300 with 300 monte carlo replications Due to the long

(~mputing time for each Simulation only 300 replications are conducted and thus it must be

noted that the confidence intervals are rather wide The naive bootstrap CFY test TB tends

to under-reject the null while rW with wild bootstrap method tends to overMreject the nulL

The size is often worse with n 50 which may be due to an estimation of the bootstrap

DGP (23) to generate the bootstrap residuals tL in the very small samples While the two

bootstrap procedures work differently for the CFY test (TB and T W ) they are very similar

for the LWZ test (L and L~) Both bootstrap tests L and L~ are generally better than

the asymptotic test pound~ Both bootstrap procedures work very well especially with c = 05

pound05 is better than pound10 which is better than pound20 The size of L is quite sensitive to the choice

of c and the bandwidth h

Davidson and MacKinnon (1999) show that the size distortion of a bootstrap test is at

least of the order n-1 2 smaller than that of the corresponding asymptotic test A further

refinement beyond n-12 of the order n-1 2 can be obtained when an asymptotically pivotal

statistic (whose limiting distribution is independent of unknown nuisance parameters) is used

for testing Since L is asymptotically normal under the null the bootstrap tests LB and LW

are more accurate than the asymptotic test LA by a full order of n-1bull See Hall (1992) for

further discussion based on Edgeworth expansions on the extent of the refinements in other

contexts

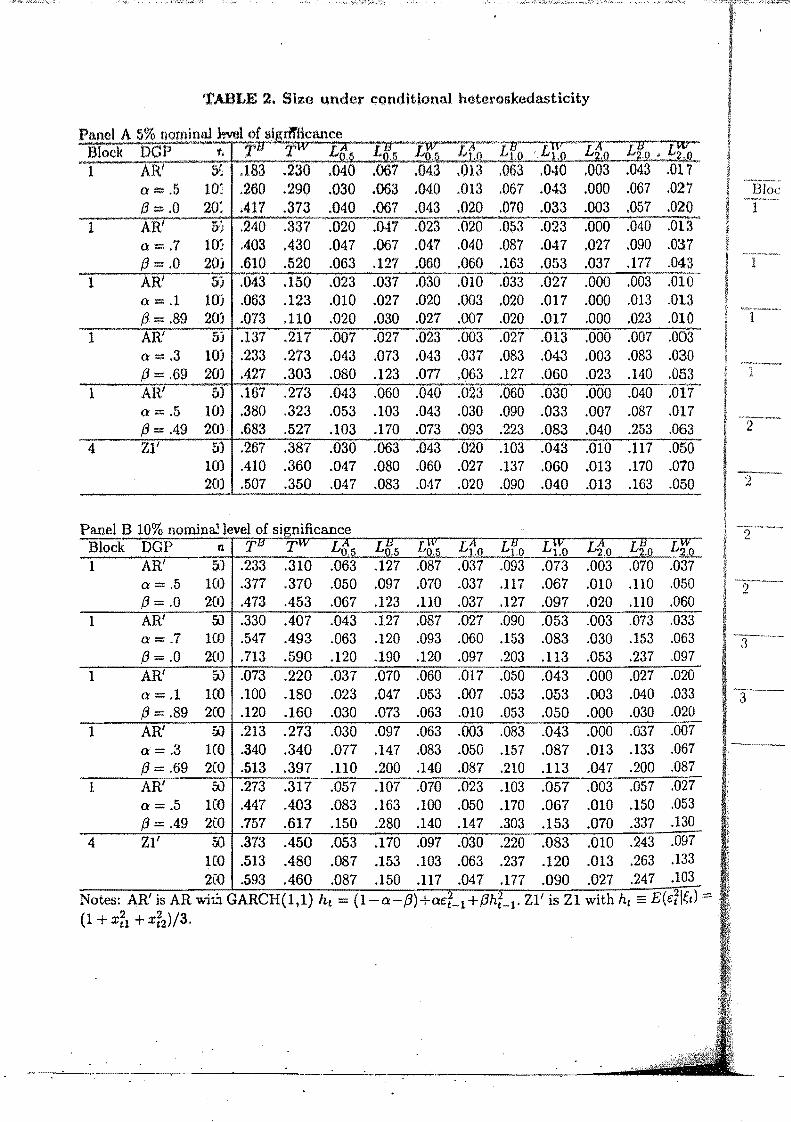

Table 2 gives the estimated size of the tests for the data generating processes (DGP)

which are linear in conditional mean with conditional heteroskedastic errors For AR we

consider GARCH errors with five different parameter values (0 3) = (0500) (0700)

(01089) (03069) and (05049) The condition for the existence of the unconditional

fourth moment is 302 + 20f3 + 132 lt 1 (Bollerslev 1986) Accordingly the condition is

a lt 0577 if 13 = 0 (3 lt 0890 if a 01 13 lt 0606 if 0 = 03 and f3 lt 0207 if a = 05

Thus for a given values of f3 or a + 13 the series becomes more leptokurtic as 0 increases

Table 2 shows that with 3 = 0 fixed the size distortion is larger with the larger ( With

a + f3 = 099 fixed the size distortion is larger also as 0 increases The size distortion

14

general

does nc

Gen

will ha

resultin

(asympl

moment

will the

presenc(

expectal

linear in

Table 2

which is

Two heterosk

to L wh(

removed

bootstra

here Th

has the (

On tl

conditio

As the ai

model (2

the CFY

distortiOI

the wild 1

attemptmiddot

is cor

unat true

tion

long

t be

~nds

lull

Lrap

two

tilar

han

05

oice

sat

her

)tal

sed

LW

for

her

we

0)

nal

I is

15

ies

ith

Ion

gets worse as n increases nlls is most apparent with LB as the naive bootstrap

not preserve the conditionl11 hettgtroskedasticity in resampling

Generally as discussed in Lee et al (1993 p 288) the conditional heteroskedastidty

have one of two effects either it will cause the size of a test to be incorrect while still

ting in a test statistic bmmded in probability under the null or it will directly lead

) to rejection despite linearity in mean The test statistic L is a conditional

liiIlomem test based on the fact that E(utled = 0 under the null hypothesis (24) which

then imply equation (28) for L As this moment condition will hold even under the

I~nresence of the conditional heteroskedasticity (which can be shown by the law of iterated

1I1exoeCtatlollS) L should not have power to reject the null for the DGPs AR and ZI which are

iII~lVlt_ in conditional mean with conditionally heteroskedastic errors However the results in

2 show that the size of L~ is adversely affected by the conditional heteroskedasticity

is more serious with a larger sample size

Two remedies may be considered olle may either (1) remove the effect of the conditional

or (2) remove the conditional heteroskedasticity itself The first is relevant

to L whose size is adversely affected The effect of the conditional heteroskedasticity can be

removed using a heteroskedasticity-consistent covariance matrix estimator or using the ild

bootstrap that preserves the heteroskedasticity in resampling We use the wild bootstrap

here The results in Table 2 show that the LVZ test with the wild bootstrap L generally

has the adequate size for the both nGPs AR and ZI

On the other hand T is not a conditional moment test as it is not based on any moment

condition T is constructed to compare the two residual sums of squares RSSP and RSSxP

Ai the alternative model to compute RSSNP is estimated by the functional coefficient (Fe)

model (23) if the FC model absorbs some of the conditional heteroskedasticity the size of

the CFY test T will be incorrect which we may observe in Table 2 Note that the size

distortion generally tends to get more severe as n increasf5 especially for AR The use of

the wild bootstrap reduces the size distortion but only by small margin In this case one may

attempt the second remedy by remOing the conditional heteroskedasticity itself whenever

one is confidently able to specify the form of the conditional heteroskedasticity However use

of misspecified conditional variance model in the procedure will again adversely affect the size

of the test Furthermore if the alternative is true the fitted conditional heteroskedasticity

15

model can absorb some or even much of the neglected nonlinearity in conditional mean

model Conceivably this could java adverse impact on the power of T Consideration of the

second remedy together with the wild bootstrap could raise issu~ that take us well bey()nd

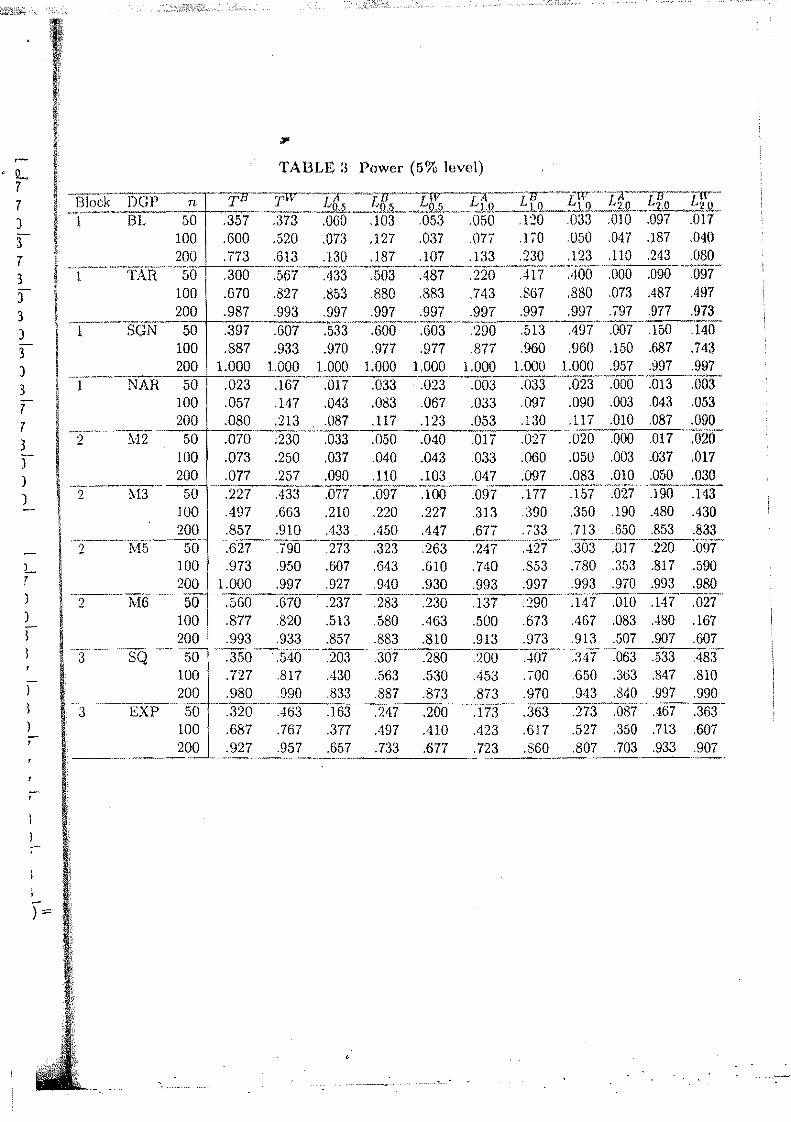

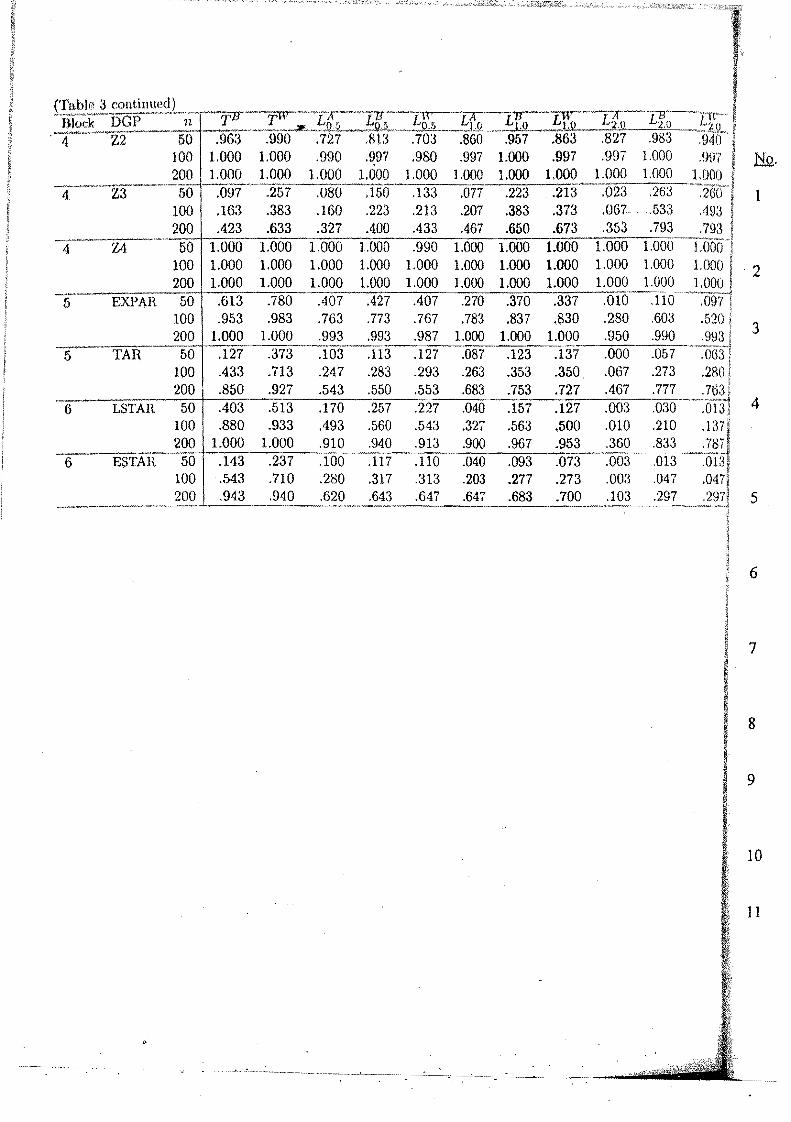

the scope of the pretmnt study and their investigation is left for other work Be Table 3 presents the power of the tests T and L at 5 leveL The results at 1 and

10 levels are available but not presented to save space As the r~ults obtained can be Bie considerably influenced by the choice of nonlinear models we try to include as many different

types of nonlinear models as possible Neither T nor L is urufonnly superior to the other Bie

T has good p~wer for BL and ESTAR and has power comparable to L in other cases

Bol

4 Conclusions Cai

We have presented a unified framework for various non parametric kernel regression estimashy

tors based on which we have considered two non parametric tests for neglected nonlinearity

in regression models Both naive bootstrap and wild bootstrap are used to generate the erit Che

ical values together with the asymptotic distributions TB with the naive bootstrap tends

to under-reject the null while rW with wild bootstrap method tends to over-reject the null

The bootstrap LWZ tests LB anq LW are better than the asymptotic test LA When the

errors are conditionally heteroskedastic the wild bootstrap for the LWZ test corrects the size Davi

distortion However the use of the wild bootstrap for TW does not correct the size problem

This difference of the two statistics is due to the different construction of the test statistics Delg L is constructed based on a moment condition implying linearity in conditional mean while

T is constructed to detect any possible forecast improvement via a nonparametric model over Eubc a linear model Hence L can be robustified to the presence of conditional heteroskedasticy

in testing for the linearity in conditional mean while T will have power to detect neglected Fannonline-Mity in conditional mean as well as the conditional heteroskedasticity

Fan (

Fan

shy

Fan S

16

c

poundan

the

ond

and

1 be

rent

her

mashy

rity

ritshy

~nds

lUll

the

size

em

ics

hile

)ver

ticy

ted

ferences

AitySahalia y Bickel t PJ iStoker TM (1994) HGoodnesgof~Fit Tests for Regreampion Using Kernel Modelsl

Princeton UC Berkeley and MIT Submitted to Econometrica

Berg M Douglas and Dingding Li (1998) A Consistent Bootstrap Test for Time Series Regression Models I University of Guelph

Bierens HJ (1982) Consistent Model Specification Tests Journal 0 Economet1ic8 20 105-134

Bierens HJ and W Ploberger (1997) Asymptotic Theoryof Integrated Conditional Moment Tests I Econometrica 65 1129-1151

Bollerslev Tim (1986) Generalized Autoregressive Conditional Heteroskedasticity JOUih

nal 0 Econometrics 31 307-327

Cai Zongwu Jianqing Fan and Qiwei Yao (2000) Functional-coefficient Regression Modshyels for Nonlinear Time Series Forthcoming Journal 0 the American Statistical As~ sociation

Chen X and Y Fan (1999) Consistent Hypothesis Testing in Semi parametric and Nonshyparametric Models for Econometric Time Series Journal of Econometrics 91(2) 373-401

Cleveland WS (1979) Robust Locally Weighted Regression and Smoothing Scatter Plots Journal 0 American Statistical Association 74 829-836

Davidson Russell and James G MacKinnon (1999) The Size Distortion of Bootstrap Tests Econometric Theory 15(3) 361-376

Delgado MA and T Stengos (1994) Semiparametric Testing of Non-nested Econometric Models Review 0 Economic Studies 75 345-367

Eubank R L and C H Spiegelman (1990) Testing the Goodness-of-Fit of t~e Linear Models via Nonparametric Regression Techniques Journal of the American Statistical Association 85 387-392

Fan J and L Gijbels (1996) Local Polynomial Modelling and Its Applications Chapman and Hall London

Fan Y (1998) Goodness of Fit Tests Based on Kernel Density Estimation with Fixed Smoothing Parameters Econometric Theo i1J 14 604-621

Fan Y and Q Li (1995) Consistent 110del Specification Tests Omitted Variables and Semiparametrie Ftmctional Forms Manuscript University of Windsor

Fan Y and Q Li (1996) Consistent Model Specification Tests Omitted Variables and Semiparametric Functional Forms Econometrica 64 865-890

17

Fan Y and Q Li (1997) A Consistent Nonparametric Test for Linearity for AR(p) Lee TModels EconornicJ Letters 55 53~59

fII HI Fan Y and Q Li (1999) IICentral Limit Theorem for Degenerate U~Statistics of AbQJ() te

lutely Regular Processes with Applications to Model Specification Tests forthcoming Lewbei Journal of Nonparametric Statistics to

Fan Y and A Ullah (1999) Asymptotic Normality of a Combined Regression Estimator Lewbel forthcoming Journal of Multivariate Analysis S11

Gozalo PL (1993) A Consistent Model Specifiration Test for Nonparametric Estimation Li Qi i of Regression Function Models Econometric Theory 9 451-477 Jo

Granger Clive VJ and Timo Terasvirta (1993) Modelling Nonlinear Economic Relation~ Li Qi ( ships Oxford University Press New York sio

Haggan V and T Ozaki (1981) Modeling Nonlinear Vibrations Using an Amplitud~ Linton dependent Autoregressive Time Series Model Biometrika 68 189middot196

Liu R Hall Peter (1992) The Bootstrap and Edgeworth Expansion Springer-Verlag 16

HardIe W (1990) Applied N onparametric Regression New York Cambridge University Nadara Press cat

Hardle W and E Mammen (1993) Comparing tonparametric versus Parametric RegTE$shy Pagansion Fits~ Annals of Statistics 21 192amp1947 PrE

Hjellvik V and D Tj0stheim (1995) Nonparametric Tests of Lineari ty for Time Series Rahmar Biometrika 82 351-368 Ref

Hjellvik V and D Tj0stheim (1998) Nonparametric Statistics for Testing of Linearity Raj B and Serial Independence Journal of Nonparametric Statistics 6 223-251 Lon

Hjellvik V Q Yao and D Tj0stheim (1999) Linearity Testing Using Local Polynomial Robinso Approximation Journal of Statistical Planning and Inference forthcoming for

Hong Yongmiao and Halbert White (1995) Consistent Specification Testing via Nonparashy Ruppertmetric Series Regression Econometrica 63 1133-1160 sion

Kreiss JeIlS-Peter rvlichael H Neumann and Qiwei Yao (1998) Bootstrap Tests for Simshy Shao J ple Structures in Nonparametric Time Series Regression University of Kent at Canshyterbury Stone C

645 Lavergne P and Q Vuong (1996) Nonparametric Selection of Regressors the Nonnested

Case Econometrica 64 207-219 Terasvirl Net

Lee Byung-Joo (1992) A Heteroskedasticity Test Robust to Conditional Mean Misspecishyfication Econometrica 60 159-171 Tong H

axi(

18

lR(p)

0000shyIlling

ltor

ation

tionshy

udeshy

rsity

~res-

ies

Lfity

nial

u-ashy

lIDshy

anshy

ted

~i-

Tae--Hwy Halbert White and Clive WJ Granger (1993L Testing for Neglected Non linearity in Time Series Models A Comparison of Neural Network Methods and Al temotive Tests Journal~f Econometric 56 269-290

bull I A (1993) Consistent Tests with Nonparametric Components with an Application

to Chinese Production Data Brandeis University

I A (1995) Consistent Nonparametric Testing with an Application to Testing Slutsky Synunetri Journal of Econometrics 67 379-401

Li Qi (1999) Consistent Model Specification Tests for Time Series Econometric Models Journal of Econometrics 92(1) 101-147

Li Qi and S Wang (1998) A Simple Consistent Bootstrap Test for a Parametric Regres~ sion Function Journal of Econometrics 87 145middot165

Linton O and P Gozalo (1997) Consistent Testing of Additive Models

Liu RY (1988) Bootstrap Procedures under Some Non-iid Models Annals of Statistics 16 1697-1708

Nadaraya EA (1964) On Estimating Regression I Theon) of Probability and its Appli~ cations 9 141-142

Pagan AR and A Ullah (1999) Nonparametric Econometrics Cambridge University Press

Rahman M and A Ullah (1999) Improved Combined Parametric and Nonparametric Regressions Estimation and Hypothesis Testing UC Riverside

Raj B and A Ullah (1981) Econometrics A Varying Coefficients Approach Croom Helm London

Robinson PM (1989) Hypothesis Testing in Semiparametric and Nonparametric Models for Econometric Time Series Review of Economic Studies 56 511-534

Ruppert D and lLP Wand (1994) Multivariate Locally Weighted Least Squares Regresshysion Annals of Statistics 22 1346-1370

Shao J and D Tu (1995) The Jackknife and Bootstrap Springer

Stone CJ (1977) Consistent Nonparametric Regression Annals of Statistics 5 595shy645

Teriisvirta Timo Chieurom-Fu Lin and Clive VJ Granger (1993) Power of the Neural Network Linearity Test Journal of Time Series Analysis 14 209-220

Tong H (1990) Nonlinear Time Series A Dynamic System Approach Clarendon Press Oxford

19

GUall Arnan (1985) IISpecification Analysis of Econometric Models Journal of Quant$ tative Economics 1j 187209

tJllah A (1999) Nonparametric Kernel Methods of Estimation and Hypothesis Testing I

forthcoming Companion in Econometric Theory B Baltagi (ad) Basil Blackwell UK

Ullah A and H D Vinod (1993) General Nonparametric Regression Estimation and Testing in Econometrics j in G S Maddala C R Roo and H D Vinod (OOs) Handshybook of Statistics Vol 11 Amsterdam Elseiver Publishing Co 85~116

Vatson GS (1964) Smooth Regression Analysis Sankhya Series A 26 359-372

11ang YJ and DWK Andrews (1993) Testing of Specification for Parametric and Semiparametric Models Journal of Econometrics 57 277-318

Vooldridge JM (1992) A Test for FUnctional Form Against Nonparametric Alternashytives) Econometric Theory 8 452-475

Vu CFJ (1986) Jackknife Bootstrap and Other Resampling Methods in Regression Analysis Annals of Statistics 141261-1350

Yatchew A J (1992) Nonparametric Regression Tests Based on Least Squares Econoshymetric Theory 8 435-45 L

Zheng John Xu (1996) A Consistent Test of FUnctional Form via Nonparametric Estishymation Techniques Journal of Econometrics 75 263-289

Par ru 1

4

Pal B

2

4

Nc mE bo mlt

20

TABLE 1 Silts

n LL 50 037 121 bull 23 033 043 7 030 000 007

100 1

023 087 010 017 017 003 020 000 003 200 040 097 017 033 040 007 020 000 000

d 300 037 073 023 033 027 0lD 027 000 010-ishy 027 170 030 033 037 013 020 027 000 000 100

2 Ml 50 007 113 030 033 040 010 023 020 000 003

200 023 100 053 053 053 013 033 030 000 000 300 027 093 033 037 037 020 020 023 000 007 0lD

2 M4 50 003 113 023 027 023 0lD 013 017 000 000 003d 100 0lD 100 020 023 023 010 017 013 000 007 007 200 020 097 023 030 027 017 027 017 000 017 017 300 017 110 033 040 03a 007 013 013 000 003 003

4 Zl 50 Lshy

023 117 033 073 073 003 040 047 000 030 033 100 007 077 020 050 050 017 057 070 000 063 060

n 200 023 097 027 040 050 0lD 047 037 003middot 063 050 300 017 080 017 037 030 003 037 030 000 040 047

1shy

Panel B 10 nominal level of significance TB TWBlock DGP n LCs Lls Ltr Lto Lfo Lro L~o Lyeno Lro

ishy 080 193 040 083 073 020 057 053 000 027 023 100

1 AR 50 053 147 023 063 060 020 057 047 000 027 027

200 060 143 053 090 083 017 060 050 000 020 023 300 067 143 033 070 077 013 047 050 000 040 040

2 Ml 50 050 220 067 087 093 020 043 043 000 013 007 100 037 177 053 073 073 023 057 060 000 017 020 200 037 153 077 090 090 033 063 053 000 003 017 300 047 157 050 080 073 027 057 050 000 023 023

2 M4 50 013 163 040 060 053 013 043 040 000 010 0lD 100 037 150 030 043 057 013 033 037 003 013 010 200 047 157 033 057 050 023 040 043 020 020 020 300 033 187 057 073 067 013 043 033 000 013 020

4 Zl 50 053 190 080 137 130 010 130 123 000 077 107 100 030 160 047 130 130 027 110 103 000 113 110 200 043 170 050 100 103 017 080 087 003 120 107 300 040 147 037 083 073 0lD 090 090 000 093 110

Notes Test statistics are denoted as T and L~ with the superscripts i = A B W refer to the methods of obtaining the null distributions of the test statistics using the asymptotics (A) naive bootstrap (B) and wild bootstrap (W) The number of bootstrap resarnples = 300 and number of monte carlo replications = 300

TABLE 2 Size under conditional heteroskedastidty

L L L L L 1 ARt 183 230 043 013 063 043 017

a ==5 260 290 040 013 067 067 027

t3 0 417 373 043 020 070 057 020

1 ARt 51 240 337 023 020 053 023 040 013 a= 7 to1 403 430 047 040 087 047 090 037 3 ==0 2m 610 520 127 060 060 163 053 177 043

1 ARt 5) 043 150 023 037 030 010 033 027 003 010 a ==1 1m 063 123 010 027 020 003 020 017 013 013 3= 89 20) 073 110 020 030 027 007 020 017 000 023 010

1 AR 5j 137 217 007 027 023 003 027 013 000 007 003 a ==3 10) 233 273 043 073 043 037 083 043 003 083 030 t3 69 20) 427 303 080 123 077 063 127 060 023 140 053

1 ARt 5) 167 273 043 060 040 023 060 030 000 040 017 a 5 to) 380 323 053 103 043 030 090 033 007 087 017 3 49 20) 683 527 103 170 073 093 223 083 040 253 063

4 ZIt 5) 267 387 030 063 043 020 103 043 010 117 050 100 410 360 047 080 060 027 137 060 013 170 070 200 507 350 047 083 047 020 090 040 013 163 050

P I B 10lt1lt 1 If fiane o nOffilna eve 0 slgm cance ~

~r~L~c

1

I bull shyNotes AR s AR WlU GARCH(ll) h t = (l-a-3)+atF-l +t3h_l Z1 IS Zl WIth ht = E(etl~t) - middot (1 + Xl + x2)3

Block DGP n

1 ARt 5J a= 5 1(1)

3 =0 200 1 ARt 5J

a= 7 100 3 ==0 2(1) ARt1 5J a= 1 100 3 = 89 2(0

1 ARt W a= 3 1(0

3 = 69 2(0 ARt1 W a= 5 1(0

3 = 49 2(0

4 Zl ro 1(0 2[Q

TlJ TW L~5 Lffs Lbs L~o Lro Li~o LfJo Lyeno L~o 233 310 063 127 087 037 093 073 003 070 037 377 370 050 097 070 037 117 067 0lD 1l0 050 473 453 067 123 110 037 127 097 020 110 060 330 407 043 127 087 027 090 053 003 073 033 547 493 063 120 093 060 153 083 030 153 063 713 590 120 190 120 097 203 113 053 237 097 073 220 037 070 060 017 050 043 000 027 020 100 180 023 047 053 007 053 053 003 040 033 120 160 030 073 063 0lD 053 050 000 030 020 213 273 030 097 063 003 083 043 000 037 007 340 340 077 147 083 050 157 087 013 133 067 513 397 110 200 140 087 210 113 047 200 087 273 317 057 lD7 070 023 103 057 003 057 027 447 403 083 163 100 050 170 067 010 150 053 757 617 150 280 140 147 303 153 070 337 130

373 450 053 170 097 030 220 083 010 243 097

513 480 087 153 103 063 237 120 013 263 133

593 460 087 150 117 047 177 090 027 247 103 t 2

rshy

Dshy7 7 )

3 7 3

100J 2003

) 1 SGN 50 1003 200)

NAR 503 1007 2007

503 100) 200)

2 13 50) 100 200

M5 50

L 100 7 200 ) 2 M6 50 ) 100

200 SQ 50

100 200 50

100 t 200

I shy

I -)==

TABLE 3 Power (5 lv(~l)

520 073 127 037 077 170 050 047 187 040 773 613 130 187 107 133 230 123 110 243 080 -300 567 433 503 487 220 417 400 000 090 097 670 827 853 880 883 743 867 880 073 487 497 987 993 997 997 997 997 997 997 797 977 973 397 607 533 600 603 290 513 497 007 150 140 887 933 970 977 977 877 960 960 150 687 743

1000 LOOO 1000 l000 1000 1000 1000 1000 957 997 997 023 167 017 033 023 003 033 023 000 013 003 057 147 043 083 067 033 097 090 003 043 053 080 213 087 117 123 053 130 117 0lD 087 090 070 230 033 050 040 Oli 027 020 000 017 020 073 250 037 040 043 033 t)60 050 003 037 017 077 257 090 110 103 047 097 083 010 050 030 227 133 077 097 100 097 177 157 027 190 143 A91 663 210 220 227 313 390 350 190 480 430 857 910 433 450 447 677 i33 713 650 853 833 627 790 273 323 263 247 427 303 017 220 097 973 950 607 643 610 740 853 780 353 817 590

1000 997 927 940 930 993 997 993 970 993 980 560 670 237 283 230 137 290 147 010 147 027 877 820 513 580 463 500 673 467 083 480 167 993 933 857 883 810 913 973 913 507 907 607 350 540 203 307 280 200 107 347 063 533 483 727 817 430 563 530 453 700 650 363 847 810 980 990 833 887 873 873 970 943 840 997 990 320 163 163 247 200 173 363 273 087 467 363 687 767 377 497 410 423 617 527 350 713 607 927 957 657 733 677 723 860 807 703 933 907

1000 1000

077 223 21 263 100 223 207 383 373 067 533

200 400 467 650 673 353 793

50 1000 1 1000 1000 1000 100 1000 1000 1000 1000 1000 1000 1000 1000 200 1000 1000 1000 1000 1000 1000 1000 1000

EXPAR 50 780 4 010 110 100 953 983 763 767 783 837 830 280 603 520 200 1000 1000 993 987 1000 1000 1000 950 990 993

5 TAR 50 1 7 373 1 127 087 123 137 057 063 100 433 713 247 293 263 353 350 067 273 280 200 850 927 543 550 553 683 753 727 467 777 763

l[Q

I

2

3

46 LSTAR 50 0403 513 170 257 227 040 157 003 030 100 880 933 493 560 543 327 563 500 010 210 200 1000 1000 910 940 913 900 967 953 360 833

6 143 237 117 110 040 093 073 013 100 543 710 280 317 313 203 277 273 003 047 200 943 940 620 643 647 647 683 700 103 297 5

6

7

8

9

10

11

rwshy2amp 940 997 000 260 493 793

L

l000 l000 097 520 993 063 280 763 013

tQ

1

2

3

4

5

6

7

8

9

10

11

CENTRE FOR DEVELOPMENT ECONOMICS

Kaushik Basu Arghya Ghosh Tridip Ray

MN Murty Ranjan Ray

V Bhaskar Mushtaq Khan

VBhaskar

Bishnupriya Gupta

Kaushik Basu

Partha Sen

Partha Sen

Partha Sen Arghya Ghosh Abheek Bannan

VBhaskar

V Bhaskar

WORKING PAPER SEI~IES

The Baby and The ijoXlYAUllh Managerial Incentives and Government Intervention (January 1994) Review Qf Development ECQnomiSG~h 1927

Optimal Taxation and Resource Transfers in a Federal Nation (February 1994)

Privatization and Employment A Study of The Jute Industry in Bangladesh (March 1994) American Economic Review Mm9n 1995 pp 267-273

Distributive Justice and The Control of Global Warming (March 1994) The North the South and the Enyironment V Bhaskar and Andrew Glyn (Ed) Earthscan Pul2Hcation London Februruy 1995

The Great Depression and Brazils Capital Goods Sector A Re~examination (April 1994) Revista Brasileria de Economia 1997

Where There Is No Economist Some Institutional and Legal Prerequisites of Economic Reform in India (May 1994)

An Example of Welfare Reducing Tariff Under Monopolistic Competition (May 1994) Reveiw of International Economics (forthcoming)

Environmental Policies and North-South Trade A Selected Survey of the Issues (May 1994)

The Possibility of Welfare Gains with Capital Inflows in A Small Tariff-Ridden Economy (June 1994)

Sustaining Inter-Generational Altruism when Social Memory is Bounded (June 1994)

Repeated Games with Almost Perfect Monitoring by Privately Observed Signals (June 1994)

shy

12 S Nandeibam Coalitional Power Structure in Stochastic Social Choice Functions with An Unrestricted Preference Domain (June 1994) JQUID1l QfEl(9]Omic TOft0rt Vol 68 No t Januaa 12921 12121 212M2~~

13 Kaushik Basu The Axiomatic Structure of Knowledge And Perception (July 1994)

14 Kaushik Basu Bargaining with Set-Valued Disagreement (JlJly 1994) Social Choice and Welfare 19962 (Vol 13 1m 61-74)

15 S Nandeibam A Note on Randomized Social Choice and Random Dictatorships (July 1994) Journal of Economic Theoa Vol 66 No2 August 1995 1m 581-589

16 Mrinal Datta Labour Markets As Social Institutions in India (July Chaudhuri 1994)

17 S Nandeibam Moral Hazard in a Principal-Agent(s) Team (July 1994) Economic Design Vol 1 1995 pp 227-250

18 D Jayaraj Caste Discrimination in the Distribution of Consumption S Subramanian Expenditure in India Theory and Evidence (August

1994)

19 K Ghosh Debt Financing with Limited Liability and Quantity Dastidar Competition (August 1994)

20 Kaushik Basu Industrial Organization Theory and Developing Economies (August 1994) Indian Industry Policies and Performance D Mookherjee (ed) Oxford University Press 1995

21 Partha Sen Immiserizing Growth m a Model of Trade with Monopolisitic Competition (August 1994) The Review of International Economics (forthcoming)

22 K Ghosh Comparing Coumot and Bertrand in a Homogeneous Dastidar Product Market (September 1994)

23 K Sundaram On Measuring Shelter Deprivation in India (September SD Tendulkar 1994)

24 Sunil Kanwar Are Production Risk and Labour Market Risk Covariant (October 1994)

~

25

26

27

28

29

30

31

32

33

34

35

36

37

38

hoice

ption

gt94) Z1l

dom Imic

Tuly

94)

ion ust

ity

ng es rd

th

IS

f

AuthQr(]

Partha Sen

26 Ranjan Ray

Wietze Lise27

28 Jean Dreze Anne-C Guio Mamta Murthi

29 Jean Dreze Jackie Loh

30 Partha Sen

31 SJ Turnovsky Partha Sen

32 K Krishnamurty V Pandit

33 Jean Dreze P V Srinivasan

34 Ajit Mishra

35 Sunil Kanwar

Jean Dnze36 PV Srinivasan

Sunil Kanwar 37

Partha Sen 38

Welfare~Improving Debt Policy Undct Monopolistic Competition (November 1994)

The Reform and Design of Commodity Taxes in the presence of Tax Evasion with Illustrative Evidence from India (December 1994)

Preservation of the Commons by Pooling Resources Modelled as a Repeated Game (January 1995)

Demographic Outcomes Economic Development and Womens Agency (May 1995) Population smd Revelopment Review December 1995

Literacy in India and China (May 1995) Economic jJnd Politigal Weekly 1995

Fiscal Policy 10 a Dynamic Open-Economy New-Keynesian Model (June 1995)

Investment in a Two-Sector Dependent Economy (June 1995) The Journal of Jayanese md International Economics Vol 9 No 1 March 1995

Indias Trade Flows Alternative Policy Scenarios 1995shy2000 (June 1995) Indian Economic Review Vol 31 No1 1996

Widowhood and Poverty in Rural India Some Inferences from Household Survey Data (July 1995) Journal of Develoyment Economics 1997

Hierarchies Enforcement

Incentives and Collusion (January 1996)

10 a Model of

Does the Dog wag the Tail or the Tail the Dog Co integration of Indian Agriculture with NonshyAgriculture (February 1996)

Poverty 10 India Regional Estimates 1987-8 (February 1996)

The Demand for Labour 10 Risky Agriculture (April 1996)

Dynamic Efficiency 10 a Two-Sector Overlapping Generations Model (May 1996)

- -~----- --------~~ -----------~---shy

39 Parthn Sen

40 Pami Dua Stephen M Mi11er David J Smyth

41 Pami Dua David J Smyth

42 Aditya Bhattacharjea

43 M Datta-Chaudhuri

44 Suresh D Tendulkar T A Bhavani

45 Partha Sen

46

47 Pami Dua Roy Batchelor

48 V Pandit B Mukherji

49 Ashwini Deshpande

50 Rinki Sarkar

51 Sudhir A Shah

52 V Pandit

53 Rinki Sarkar

Asset Bubbles in a Monopolisticmiddot Competitive Maem Model (June 1996)

Using Leading Indicators to Forecast US Home Sales in a Bayesian VAR Framework (October 1996)

The Determinants of Consumers Perceptions of Buying Conditions for Houses (November 1996)

Optimal Taxation ofa Foreign Monopolist with Unknown Costs (January 1997)

Legacies of the Independence Movement to the Political Economy of Independent India (April 1997)

Policy on Modern Small Scale Industries A Case of Government Failure (May 1997)

Terms of Trade and Welfare for a Developing Economy with an Imperfectly Competitive Sector (May 1997)

Tariffs and Welfare in an Imperfectly Competitive Overlapping Generations Model (JUle 1997)

Conswner Confidence and the Probability of Recession A Markov Switching Model (July 1997)

Prices Profits and Resource Mobilisation in a Capacity Constrained Mixed Economy (August 1997)

Loan Pushing and Triadic Relations (September 1997)

Depicting the Cost Structure of an Urban Bus Transit Firm (September 1997)

Existence and Optimality of Mediation Schemes for Games with Communication (November 1997)

A Note on Data Relating to Prices in India (November 1997)

Cost Function Analysis for Transportation Modes A Survey of Selective Literature (December 1997)

5

5

5

19

ro

In

n

f

54

55

56

57

58

59

60

61

62

63

64

65

66

67

Rlnld SarkaI

Aditya Bhattacharjea

Bishwanath Golda Badal Mukherji

Smita Misra

TA Bhavani Suresh D Tendulkar

Partha Sen

Ranjan Ray JV Meenakshi

Brinda Viswanathan

Pami Dua Aneesa 1 Rashid

Pami Dua Tapas Mishra

Sumit Joshi Sanjeev Goyal

Abhijit Banerji

Jean Dreze Reetika Khera

Sumit Joshi

Economic Characteristics of the Urban Bus Transit Industry A Comparative Analysis of Three Regulated Metropolitan Bus Corporations in India (February 1998)

Was Alexander Hamilton Right Limit~pricing Foreign Monopoly and Infant~industry Protection (February 1998)

Pollution Abatement Cost Function Methodological and Estimation Issues (March 1998)

Economies of Scale in Water Pollution Abatement A Case of Small-Scale Factories in an Industrial Estate in India (April 1998)

Determinants of Firm-level Export Performance A Case Study of Indian Textile Garments and Apparel Industry (May 1998)

Non-Uniqueness In The First Generation Balance of Payments Crisis Models (December 1998)

State-Level Food Demand in India Some Evidence on Rank~Three Demand Systems (December 1998)

Structural Breaks in Consumption Patterns India 1952shy1991 (December 1998)

Foreign Direct Investment and Economic Activity in India (March 1999)

Presence of Persistence in Industrial Production The Case of India (April 1999)

Collaboration and Competition in Networks (May 1999)

Sequencing Strategically Wage Negotiations Under Oligopoly (May 1999)

Crime Gender and Society in India Some Clues from Homicide Data (June 1999)

The Stochastic Turnpike Property without Uniformity in Convex Aggregate Growth Models (June 1999)

J wam

68

69

70

71

72

73

74

75

76

77

JV M eenakshi Ranjan Ray

Jean Drezc Gceta GandhishyKingdon

Mausumi Das

Chander Kant

KN Murty

Pami Dua Anirvan Banerj i

V Pandit

A Banerji

Jean Dreze Mamta Murthi

Aman Ullah Tae-Hwy Lee

Impact of Household Size Family Composition and Socio Economic Characteristics on Poverty in Rural India (July 1999)

School Participation in Rural India (September 1999)

Optimal Growth with Variable Rate of Time Preference (December 1999)

Local Ownership Requirements and Total Tax Collections (January 2000)

Effects ofChanges in Household Size Consumer Taste amp Preferences on Demand Pattern in India (January 2000)

An Index of Coincident Economic Indicators for the Indian Economy (January 2000)

Macroeconometric Policy Modeling for India A Review of Some Analytical Issues (February 2000)

Selling Jointly Owned Assets via Bilateral Bargaining Procedures (March 2000)

Fertility Education and Development Further Evidence from India (March 2000)

Nonparametric Bootstrap Tests for Neglected Nonlinearity in Time Series Regression Models (March 2000)

1 Introduction II

Much research in empirical and theoretical econometrics has been centered around the esti~

mation and testing of vario~ flmctions such as regression functions (eg conditional mean

and variance) and density functions A traditional approach to studying these functions has

been to fist impose a parametric functional form and then proceed with the estimation and

testing of interest A major disadvantage of this approach is that the econometric analysis

may not be robust to the slight data inconsistency with the particular parametric specific~

tion and this may lead to erroneous conclusions In view of these problems in the last five

decades a vast amount of literature has appeared on the nonparametric and semi parametric

approaches to econometrics eg see the books by Hardle (1990) Fan and Gijbels (1996)

and Pagan and Ullah (1999) The basic point in the nonpararuetric approach to econometrics

is to realize that in many instances one is attempting to estimate an expectation of one

variable y conditional upon others x This identification directs attention to the need to

be able to estimate the conditional mean of y given x from the data Yt and Xt t = 1 In

A nonparametric estimate of this conditional mean simply follows as a weighted average

Lt w(Xt x)Yt where w(Xt x) are a set of weights that depend upon the distance of Xt from

the point x at which the condi tional expectation is to be evaluated

Based on these nonparametric estimation techniques of the conditional expectations in

recent years a rich literature has evolved on the consistent model specification tests in econoshy

metrics For example various test statistics for testing a parametric functional form have

been proposed by Bierens (1982) UUah (1985) Robinson (1989) Eubank and Spiegelman

(1990) Yatchew (1992) Tooldridge (1992) Gozalo (1993) Hardle and Mammen (1993)

Hong and White (1995) Zheng (1996) Bierens and Ploberger (1997) and Li and Wang

(1998) Also see UUah and Vinod (1993) Whang and Andrews (1993) Delgado and Stenshy

gos (1994) Lewbel (1993 1995) AIt-Sahalia et al (1994) Fan and Li (1996) Lavergne and

Vuong (1996) and Linton and Gozalo (1997) for testing problems related to insignificance of

regressors non-nested hypothesis semi parametric versus nonparametric regression models

among others 110st of these tests especially the test for a parametric specification are

developed under the following goodness of fit measures (i) compare the expected values

of the squared error under the null and alternative hypotheses (eg Ullah (1985) type F

statistic) (ii) calculate the expected value of the squared distance between the null and

1

s

oJternaUve rnodel spc1ificatic)l1s (eg Hlirdle poundlud M~unmen (1993) Ullah and Vinod (1993)

Ait~SahEllia (1994)) and (iii) calculate the expected value of the product of the error lUlder

the null with the model specffied under the aHernative (eg conditional moment tests of

BiercnS (1982) Zhang (1996) Fan and Li (1996) and Li and Wang (1998) All these three

alternative goodness of fit measures are equal to zero lWder the null hypothesis of correct

specification For details see Pagan and Ul1ah (1999)

We note here that the asymptotic as well as the simulation based finite sample proper~

ties of the most of the above mentioned test statistics have been extensively analyzed for

the cross sectional models with independent data However not much is known about the

asymptotic as well as the small sample performance of these test statistics for the case of

time series models with weak dependent data although see the recent works of Chen and

Fan (1999) Hjellvik and Tj0stheim (1995 1998) Hjellvik et al (1999) Kreiss et al (1998)

Berg and Li (1998) and a very important contribution by Li (1999) where he develops the

asymptotic theory results of Li-Wang-Zheng (LWZ) test under the goodness of fit measure

(iii) The modest goal of this paper is to conduct an extensive monte carlo study to analyze

the size and power properties of two kernel based tests for time series models One of them

is the bootstrap version of Ullahtype goodness of fit test (i) due to Cai Fan and Yao (2000

henceforth CFY) and another is the nonparametric conditional moment goodness of fit test

(iii) of LWZ We examine the bootstrap performances of these two goodness of fit tests beshy

cause of the asymptotic validity results of using bootstrap methods for these statistics due to

CFY (2000) and Berg and Li (1998) Berg and Li (1998) also support the better performance

of LWZ over the Hardle and Mammen (1993) type tests considered for time series data in

Hjellvik and Tj0stheim (1995 1998) Hjellvik et al (1999) and Kreiss et al (1998) For the

purpose of our simulation study we consider the testing of linearity against a large class of

nonlinear time series models which include threshold autoregressive bilinear exponential

autoregressive models smooth transition autoregressive models GARCH models and var~

ious nonlinear autoregressive and moving average models Both naive bootstrap and wild

bootstrap procedures are used for our analysis We also compare the bootstrap results with

the results using the asymptotic distribution for LWZ test

The plan of the paper is as follows In Section 2 we present the nonparametric kernel

regression estimators and the tests of CFY and LWZ based on them Then in Section 3 we

2

pr

2

2

is

the monte carlo results Finally Section 4 gives conclusions

Nonparametric regression and specification testing

Nonparametric regression

UtI Xtl t 1 I n be stochastic processes where Yt is a scalar and Xt = (Xtll Xtk)

a 1 x k vector which may contain the lagged valu~ of Yt Consider the regression model

(1)

where m(xc) E (YtIXt) is the true but unknown regression fllhction and Ut is the error term

that E(Utlxt = 0 and Var(UtXt) == (72

If m(xc) == g(Xt 6) is a correctly specified family of parametric regression functions then

== g(Xt 6) +Ut is a correct model and in this case one can construct a consistent least

squares (LS) estimator of m(Xt given by g(x 6) where 6is the LS estimator of the parameter

6 This 6is obtained by minimizing

(2)

with respect to 6 For example if 9(XtO) = Xto is linear we can obtain the LS estimator of

0 as

6= (XX)-lXy (3)

and the predicted residuals il t = Yt - m(xt) where X is an n x (k + 1) matrix generated by

X t = (1 Xt) and

(4)

In general l if the parametric regression gXto) is incorrect or the form of m(Xt) is unknovvn

then 9(Xt1 b) may not be a consistent estimator of m(Xt)

For this case an alternative approach to estimate the unknown m(xc) is to use the

consistent nonparametric kernel regression estimator which is essentially a local constant LS

(LeLS) estimator To obtain this estimator take Taylor series expansion of m(Xt around I

so that

Yt - m(Xt) +Ut (5)

- m(x) +tt

3

(9)

wht

wit

LC

0(1

derivative of m(x) at Xt x ThcpLCLS estimator can then be derived by minimizing

n n

2 vlKtt = 2(Yt - m(xraquo2Ktz (6) t-I 1

with respect to constant m(x) where K tz = K(xI1) is a decreasing function of the distanCeS

of the regressor vector Xt from the point x = (Xb X) and h -+ 0 as n -t oc is the

window width (smoothing parameter) which determines how rapidly the weights decrease as

the clistance of Xt from x increases The LCLS estimator so estimated is

bull( ) _ l~1 YtKtx _ (OK( ))-1degK( ) (7)m x - K - I X I I X Y4t=l tr

where K(x) is the n x n diagonal matrix with the diagonal elements (Klr Knx) and i is

an n x 1 cohunn vector of unit elements The estimator m(x) is due to Nadaraya (1964) and

Watson (1964) (NW) who derived this in an alternative way Generally ih(x) is calculated

at the data points Xt in which case we can write the leave-one out estimator as

_ () E~=1tFt Yt Ktt (8)m x = n 4t=1tt Ktt

where Ktt = Kec~Xt) The assumption that h -tO as n -+ 00 gives Xt - x = O(h) -t 0

and hence EVt -t 0 as n -t 00 Thus the estimator m(x) will be consistent under certain

smoothing conditions on h K and m(x) In small samples however EVt f 0 so m(x) will be

a biased estimator see Pagan and Ullah (1999) for details on asymptotic and small sample

properties

An estimator which has a better small sample bias and hence the mean square error

(MSE) behavior is the local linear LS (LLLS) estimator due to Stone (1977) and Cleveland

(1979) also see Fan and Gijbels (1996) and Ruppert and Wand (1994) for their properties

In the LLLS estimator we take first order Taylor-Series expansion of m(xt) around x so that

Yt - m(xt) +Ut = m(x) + (Xt - x)m(l)(x) +Vt

- a(x) + XtB(x) + Vt

- Xto(x) +Vt

4

estin

and

to 1)

Obv

j

witl

h= the

esti

coe

1

(6)

nreg

the

(7)

Us

(8)

~ 0

un be

Ie

[o(x) t3(x)] with Q(x) = m(x) x3(x) and f3(x) = m(l)(x) The LLLS

estimator of 6(x) is then o~ned by minimizing

n n

Lv~KtJ = 2(Yt Xt6(X))2Ktt (10) t~l t~l

and it is given by

6(x) = (XK(X)X)-l XK(x)y (11)

The LL~S estimator of a(x) and f3(x) can be calculated as amp(x) = [1 0)6(x) and ~(x) ==

[0 1)6(x) This gives

~(X) = [1 x]8(x) = amp(x) + x[3(x) (12)

Obviously when X = i 8(x) reduces to the NWs LeL8 estimator m(x)

An estimator of the LLL8 is the local polynomial L8 (LPL8) estimators see Fan and

Gijbels (1996) In fact one can obtain the local estimators of a general nonlinear model

g(Xtlj) by minimizing n

L[Yt - g(Xtl o(x))fKt1 (13) =1

with respect to o(x) For g(xto(x)) = Xto(x) we get the LLL8 in (11) Further when

h = 00 Ktx = K(O) is a constant so that the minimization of K(O) ElYt - g(xt o(x))]2 is

the same as the minimization of ElYt - g(x 0(x))]2 that is the LL8 becomes the global L8

estimator given by (3)

The LLL8 estimator in (11) can also be interpreted as the estimator of the functional

coefficient (varying coefficient) linear regression model

Yt - m(xt) + Ut (14)

- Xto(x) + Ut

where o(Xt) is approximated locally by a conStant o(Xt) ~ o(x) The minimization of E uKtx

with respect to 6(x) then gives the LLL8 estimator in (11) which can be interpreted as the

LC varying coefficient estimator An extension of this is to consider the linear approximation

o(Xt) ~ o(x) + D(x)(xt - xY where D(x) = 8~~t) evaluated at Xt = x In this case

Yt - m(Xt) + Ut = Xto(Xt) + Ut (15)

Xto(x) + XtD(x)(xt - x) + Ut

5

(20)

(21)

N

S

= X8(x) +X 0 (Xt - x)vecD(x) + Ut

= ~8(x) +Ut

wbere Xt = tXt Xt 0 (Xt - x)] cmiddot(x) = [c(x) (vecD(x))) and 0 represents the Hadamard

product The LL varying coeffident or LPLS estimator of c(xcan then be obtained by

minimizing n

(16)L[Yt - Xc(x)fK e= 1

with respect to c(x) as

r (x) = (X K(x)X)-l X Kx)y (17)

- From this 8(x) = II 0]8 (x) and hence

- shy1 (x) = [1 x 0]8 (x) = Il xJ6(x) (18)

The above idea can be extended to the situations where et = (Xt Zt) such that

(19)

where the coefficients are varying with respect to only a subset of et Zt is 1 x l and et is

1 X P P = k + l Examples of these include random coefficient model (Raj and UUah 198L

Granger and Teriisvirta 1993) exponential autoregressive model (Haggan and Ozaki 1981)

and threshold autoregressive model (Tong 1990) also see Section 3 To estimate C(Zt) we can

again do a local constant approximation C(Zt) ~ c(z) and then minimize E[Yt - Xc(z)]2K tz

with respect to c(z) where K tz = KCt) This gives the LC varying coefficient estimator

8(z) = (XK(Z)X)-l XK(z)y

where K(z) is a diagonal matrix of Ktz t = 1 n

CFY (2000) consider a local linear approximation b(zt) ~ 6(z) + D(z)(zt - z) The LL

varying coefficient estimator of CFY is then obtained by minimizing

n n

L[Yt - X tC(Zt)]2 K tz - LIYt - Xtc(z) - (Xt 0 (Zt - z))vecD(z)]2Ktz t=1 t=1

n

- 2)Yt - X6(z)j2Ktz t==l

6

witl

Me

WI

ing

2

Cc

rut

In

etl

T

d

Y

i)

)

)

5

1

with respect to 6(z) [6(z (1JecD(z))j where Xi ~ [X Xt ) (Zt - z)] Thls gives

-I6 (z) = (XK(Z)x u -lXu K(z)y (22)

- and 6(z) = [10]6 (z) Hence

(23)

When z = x (20) and (22) reduce to the LLLS estimator bex) in (11) and the LL vary~

ing coefficient estimator 6 (x) in (17) respectively For the asymptotic properties of these

varying coefficient estimators see CFY (2000)

22 Nonparametric tests for functional forms

Consider the problem of testing a specified parametric model against a nonparametric (NP)

alternative

Ho E(ytleurot = g(ee 6)

HI E(ytleuro) = m(eurot)

In particular if we are to test for neglected nonlinearity in the regression models set 9 (et 16) = eurot8 Then under HOI the process yd is linear in mean conditional on eurot

(24)

The alternative of interest is the negation of the null that is

(25)

When the alternative is true a linear m09-e1 is said to suffer from neglected nonlinearity

Note that eurot = (Xt Zt) = Xt when zt = Xt

Using the nonparametric estimation technique to construct consistent model specification

tests was first suggested by UUah (1985) The idea is to compare the parametric residual

sum of squares (RSSP ) E ur ilt = Yt - g(euro 6) with the nonparametric RSS (RSS~P) L u-

where Ut = Yt ~ m (eurot) The test statistic is

(26)

7

~--- -----~--~~--------------------~-------

or simply TI (RSSP -- RSSNP) We reject the null hypothesis when T is large ViiT has a

degenerate distribuUon under ltlo- Yatchew (1992) avoids this degeneracy by splitting sample

of n into 711 and n2 and calculating L u based on nl observations and r u based OJ) n2

observations Lee (1992) l)es density weighted residuals and compares EWtu with LU Fan and Li (1995) uses different normalizing factor and show the asymptotic normality of

nhP 2T

Another way is to use the bootstrap method as suggested by CFY (2000) The bootstrap

allows the implementation of (26) and it involves the following steps to evaluate p-values of

the test

1 Generate the bootstrap residuals u from the centered NP residuals (iit -11) where

11= n-1 Lilt and define V == et 6+u

2 Construct the bootstrap sample v et f=l and calculate the bootstrap fest statistic

T using for the sake of simplicity the same h used in estimation with the original

sample

3 Repeat the above two steps B times and use the empirical distribution of T as the

null distribution of T Reject the null hypothesis Ho when T is greater than the upper

a point of the conditional distribution of T given Vt ettl The p-value of the test

is simply the relative frequency of the event Tmiddot 2 T in the bootstrap resamples

Kreiss et al (1998) provide more detailed r~asons why the bootstrap works in general

non parametric regression setting They proved that asymptotically the conditional distrishy

bution of the bootstrap test statistic is indeed the distribution of the test statistic under

the null hypothesis As mentioned by CFY (2000) it may be proved that the similar result

holds for T as long as 6converges to f at the rate n-12 We use both naive bootstrap (Efron

1979) and wild bootstrap (Wu 1986 Liu 1988) The wild bootstrap method preserves the

conditional heteroskedasticity in the original residuals For wild bootstrap see also Shao

and Th (1995 p 292) Hardle (1990 p 247) or Li and Wang (1998 p 150)

An intuitive and simple test of the parametric specification follows from the combined

regression

8

p

v

k

v

l (

las a

nple paramotric specification is tmen the conditional moment test for mu(et) = E(utlet) 0

n n2 which is identical to testing

E[uE(ucled(et) = 0 (28)

y of where f(et) is the density of e A sample estimator of the left hand side of (28) is

Lrap (29)

s of

lere where E(Utlet) = Etl utKed EtirH Kt t from (8) and j(et) = (nhPt 1 2t1ft Ktt is the

kernel density estimator Ktt = K((h(I) The asymptotic test statistic is then given by

2 Lstic L nhP r N(O 1) (30) vw

nal where w 2(n(n - 1)hP)-1 Et Etlt-t ft~UIKft is a consistent estimator of the asymptotic

variance of nhP 2 L see Zheng (1996) Fan and Li (1996) Li and Wang (1998) Fan and the Ullah (1999) and Rahman and Ullah (1999) for details Also see Pagan and Ullah (1999

per eh 3) and Ullah (1999) for the relationship of this test statistic with other nonparametric est specification tests Based on the asymptotic results of Fan and Li (1996 1997 1999) and Li

(1999) for dependent data Berg and Li (1998) establish the asymptotic validity of using the

wild bootstrap method for L for time-series ral

rishy3 Monte carlo

ler

llt In this section we examine the finite sample properties of T and L especially with the on empirical null distributions being generated by the bootstrap method Asymptotic critical he values are also used for L To generate data we use the following models all of which ao have been used in the related literature Most of them are univariate while there are some

multivariate situations There are six blocks The error term Ct below is iid N (0 1) unless

otherwise is indicated The models will be referred by the name shown in parentheses in

bold 7)

9

BLOCK 1 (I~gte White and Granger 1993)

Linear (AR)

Linear AR with GARCH (AR)

Vt - O6Yt_l + pound

ht - E(cIYt-l) = (1 - a - (3) +Qe-l + (3ht- 1

Bilinear (BL)

Threshold Autoregressive (TAR)

Yt - 09Yt-l + et IYt-11 ~ 1

- -O3Yt-l + et IYt-IIgt 1

Sign Nonlinear Autoregressive (SGN)

Yt = sign(Yt-l) +et

where sign(x) = 1 if xgt 00 if x = 0 and -1 if x lt O

Rational Nonlinear Autoregressive (NAR)

071Vt-l Yt = I 2 +CtYt-l +

BLOCK 2 (Lee White and Granger 1993)

MA() (Ml)

Heteroskedastic MA(2) (M2)

Note that 112 is linear in conditional mean as the forecastable part of M2 is linear and the

final term introduces heteroskedasticity

No

Ali

Bil

BL

Squ

Eq

ThE

BLi

fron

Lin~

Que

10

Nonlinear MA (M3) til

y = It - O3et_l + O2Ct-2 + OAet-lct-2 - O25e~_2

AR(2) (M4)

Bilinear AR (M5)

Bilinear ARMA (M6)

Vt = OAY-l - O3Vt-2 + O5Vt-middotlet-l + O8et-l + Et

BLOCK 3 (Lee White and Granger 1993)

Square (SQ)

Exponential (EXP)

These are bivariate models where Xt = O6Xt-l +et Ctt rv N(O 52)and Ctt Et are independent

BLOCK 4 (Zheng 1996)

Five models with Xt = (X71 Xt2) are considered in this block Let Un and Ut2 be drawn

from IN(O 1) Two regressors Xtl and Xt2 are defined as Xu = Utl and Xt2 = (Uti +udJ2middot

Linear (ZI)

Yt = 1 + Xtl + Xt2 + et

Linear with conditionally heuroskedastic error (ZI)

11 - 1 + Xu + Xt2 + et

h- _ E(elx~) = (1 + X~l + X2)3

the Quadratic (Z2)

Yt = 1 + Xu + Xt2 + Xu X t2 + Et

11

Concave (Z3)

II lt = (1 + Xu + Xt2)13 + Et

Convex (Z4)

BLOCK 5 (Cai Fan and Yao 1999)

Exponential AR (EXPAR)

Yt - al(Yt-dYt-l + a2(Yt-dYt-2 +et

al (Yt-l) - 0138 + (0316 + 0982Y_I) exp( -389Y~I)

a2(Yt-l) - -0437 - (0659 + 1260Yt_1) exp(-389Y_I)

e IV 1N(O 022 )