Embed Size (px)

Citation preview

Cello

Gro

up p

lc Annual Rep

ort 2009

Annual ReportYear Ended 31 December 2009

Cello Group plc11-13 Charterhouse BuildingsLondon EC1M 7APtel: +44 (0)20 7812 8460www.cellogroup.co.uk

Company Registration No. 05120150

Page

Financial Highlights 1

Positioning and Strategy 2-3

Chairman’s Statement 4-9

Cello Research and Consulting 10-11

Tangible Group 12-13

Directors’ Report 14-17

Corporate Governance 18-19

Report of the Remuneration Committee 20-22

Independent Auditors’ Report 23

Consolidated Income Statement 24-25

Consolidated Statement of Comprehensive Income 25

Consolidated Balance Sheet 26

Consolidated Cash Flow Statement 27

Consolidated Statement of Changes in Equity 28

Consolidated Financial Statements – Accounting Policies 29-34

Notes to the Consolidated Financial Statements 35-68

Company Balance Sheet 69

Company Financial Statements – Accounting Policies 70

Notes to the Company Financial Statements 71-77

Notice of Annual General Meeting 78-83

Directors 84-85

Advisers 86

Group Directory 87-88

Contents

The Cello Annual Report 2009 is made from Naturalis Recycled Smooth paper, sourced from 50% FSC-certified recycled, 20% FSC virgin pulp and 30% mill broke. It is manufactured in Scotland.

1

Financial Highlights

• Like-for-like operating income £60.5m (2008: £65.4m)

• Research H2 2.6% growth

• Headline operating profit £5.9m (2008: £8.2m)

• Basic headline earnings per share 7.28p (2008: 13.08p)

• Full year dividend up 4% at 1.30p (2008: 1.25p)

• Strong cash management and generation held down net debt to £11.5m (2008: £9.9m), after cash earn out payments of £3.2m

• Banking facilities successfully renewed until 2013

• Solid second half performance in Research continues in 2010

• 6th largest UK research operation1 (2008: 9th) and 19th globally2 (2008: 21st)

• Good start to 2010 momentum in Q4 2009 continued into Q1 2010

• Robust pipelines of non-UK work in Research and Consulting

• Simon Dannatt appointed Managing Director, Cello USA

1source: Marketing Market Research Leagues September 20092source: Inside Research published August 2009

2

Against a very challenging backdrop in 2009,

Cello Group plc has continued to consolidate its

position in the specialist research and response

communications markets. Cello is now the 6th

largest research organisation domiciled in the

UK and the 19th largest globally. In Response we

remain number 6 in the UK. In both areas we

are the only business that is not part of a much

larger group.

Both research and response markets have

continued to evolve down the path of client sector

specialisation and Cello has benefitted from

structuring its offering along these lines. Healthcare

research and consulting has continued to develop

into our largest area of specialism, accounting

for approaching a third of our revenue. The

broader area of health in its various manifestations

accounts for a further 20% of our activities, and

has remained resilient during the downturn.

Cello’s business has been expanding most

rapidly in international markets, which account

for approaching half of our research revenues.

International revenue flows have shown resilience,

and pressure on gross margins in this area has

been more moderate than in domestic areas of

client activity. We are expanding our operations in

the US market, with a healthcare focus in particular,

and in due course will seek to grow our business in

Asia and the Far East.

The growing relevance of the internet to research

and response has continued unabated. We are

investing behind the growth of online research

communities, which are enjoying a rapid uptake

by clients, both in FMCG and healthcare markets.

Our Face brand has made particular headway in

this new evolving market under the banner of “co-

creation”. We continue to migrate our general data

collection capability online, as a complement to

our more traditional field force capability. Online

communications techniques are now core to the

daily activities of Tangible.

Our strategy as a Group remains to further

reinforce our positioning in research and response

during 2010 and beyond. In particular, we plan to

Positioning and Strategy

3

expand the international servicing capability of our

research business, with a focus on the US market

where we already have a profitable presence

in New York and San Francisco and a broad set

of client relationships, particularly in healthcare.

Asia is also a priority region for us where we have

strong client relationships on which we can readily

build. In the UK we continue to consolidate our

servicing capability so that we can compete more

effectively against our much larger rivals.

Operating Income by Industry Sector

Group Operating Board

Healthcare

5%

0

10%

15%

20%

25%

PublicSector

FinancialServices

Telecoms Leisure Charity Retail FMCG Food &Drink

Industrials Media Utilities Other

R & C 2009

R & C 2008

Tangible 2009

Tangible 2008

back row, L to R – John Rowley, Vincent Nolan, Richard Gilmore, Jane Shirley, Paul Walton, Stephen Highleyfront row, L to R – Andy Carolan, Mark Scott, Allan Rich, Mark Bentley, Owen Williams

4

Overview

2009 has been a demanding year for Cello with the

Group reporting headline operating profit of £5.9m

(2008: £8.2m) on operating income of £60.5m

(2008: £65.4m). However, the final quarter showed

clear signs of stabilisation and improving spend by

clients in the Group’s core areas of expertise.

The decline in income was not evenly spread

across the Group, nor across the year. A stronger

second half from Cello (Research) meant that

full year like-for-like income improved from the

half year decline of 10.4% to a full year decline

of 4.1% (H2 up by 2.6%). The rate of decline in

Tangible, the Group’s direct marketing arm also

improved slightly from 12.5% at the half year to a

full year decline of 11.7%.

These variations reflect the marked slowing in

H1 2009 of ad-hoc qualitative and quantitative

market research activity, which subsequently

recovered to more normal levels as clients

renewed their activity in the latter part of the year.

The rate of decline in certain parts of Tangible’s

business also slowed by year end.

As detailed in the interim results, the Group acted

rapidly to the market conditions by reducing

professional resource as well as property and

other administrative costs. Before discontinued

operations, the full year cost base for 2009 was

£4.3m lower than 2008 with a substantially

lower professional year end headcount of 760

(2008: 830). The Group has also taken action to

consolidate its property commitments and will exit

at least five leases over the next two years, reducing

annual property costs by a further £0.5m.

Cello continues to benefit from its client sector

focus and increasing orientation towards large

contracts. Performance remained particularly

strong in healthcare which now accounts for 38%

of operating income in Research (2008: 34%).

The fact that the top 20 Group clients remained

largely unchanged is a clear demonstration of the

Group’s ability to manage long term relationships.

They accounted for 38% of Cello’s total operating

income. At the same time the Group has achieved

significant new client wins.

In Cello (Research), the emphasis on international

activity has continued to yield good returns, with

overseas revenue now accounting for over 46%

of divisional revenue (2008: 42%). Overseas

revenue declined by 1.5%, at a significantly

slower rate of decline than UK domiciled income.

This has been achieved by continuing to target

multi-national client contracts which represent

higher growth opportunities outside the relatively

mature UK market.

Following continued strong operating cash

generation, net debt at year end was £11.5m

(2008: £9.9m) after £3.2m of earn out payments.

In March 2010, the Group secured new three year

debt facilities.

Financial Review

Total Group operating income was £60.5m

(2008: £65.4m). Headline profit before tax was

£5.1m (2008: £7.3m). The Group’s overall results

mask continued success in the core activities of

healthcare research, specialist FMCG research and

direct marketing. Within these areas, quantitative

research, where the Group has larger contract

sizes, has continued to prove particularly resilient.

The continued reduction in client activity in the

London-based financial services focused agency

and the business intelligence consulting business,

Chairman’s Statement

5

as well as weakness in parts of the charities activities

and in Tangible’s London communications market,

all impacted operating income. The Group headline

operating margin, before head office costs, was

12.4% (2008: 15.6%).

In all underperforming areas quick action was taken

to adjust the cost structure to an appropriate level,

resulting in an exceptional charge of £1.9m. This

charge relates to employee termination payments

and surplus space provisions. All of these were

deemed prudent actions to protect the medium

term profitability of the Group.

The net interest charge was £0.9m (2008: £0.9m).

The Group’s tax charge in the year was £0.2m

(2008: £1.0m). This reduction is as a result of

a decrease in headline operating profit; tax

deductible exceptional costs; deferred tax credits

occurring as a consequence of amortisation and

impairment of intangible assets, and recognition of

certain non-recurring tax credits from prior years.

Headline basic earnings per share were 7.28p

(2008: 13.08p) and headline fully diluted earnings

per share were 5.89p (2008: 8.41p). Fully diluted

earnings per share reflects the impact of the

anticipated future issuance of shares to vendors

of companies acquired by the Group under earn

out arrangements.

The Board is proposing a final dividend of 0.80p per

share, giving a total dividend per share for the year

ended 31 December 2009 of 1.30p (2008: 1.25p),

an increase of 4.0%. This dividend will be paid,

subject to shareholder approval, on 16 June 2010

to all shareholders on the register at 21 May 2010.

The Group’s net debt position at 31 December

2009 was £11.5m (2008: £9.9m), after earn out

payments of £3.2m. Operating cash flow of £5.2m

during the year represented an 87% conversion of

headline operating profit.

In March 2010, the Group renewed its banking

facility with The Royal Bank of Scotland. This new

66

facility consists of a £10.0m term loan and a

£7.0m Revolving Credit Facility. The facility expires

in March 2013. The multi-currency overdraft facility

of £2.0m was also renewed. Interest margin

is between 250pts and 325pts above LIBOR.

Increases in interest margins incurred under this

new facility are expected to be offset by ongoing

reduction in net debt through internally generated

cash during 2010 and beyond.

In April 2009, £7.8m of earn out liabilities were

settled, which is a very substantial part of the

Group’s outstanding earn out liabilities. These

were settled by £3.2m in cash and loan notes,

and £4.6m in shares issued at an average issue

price of 32.4p per share. Following a detailed

review of further liabilities, earn out commitments

now expected are £6.1m at 31 December 2009,

to be paid over the period from 2010 to 2013,

compared with £7.4m for the equivalent period

at 31 December 2008. The minimum cash or loan

note element of these liabilities is £2.8m. Shares

issued under these arrangements will be subject

to contractual trading lock-ins for up to three years

after their issue. The Board retains discretion to pay

a larger proportion of this in the form of loan notes

or cash.

Future earn out commitments including future

acquisition related employee expenses are

therefore expected to be as follows:

Year

Cash/Loan

notes

£m

Shares

£m

Total

£m

2010 1.4 1.1 2.5

2011 0.9 1.8 2.7

2012+ 0.5 0.4 0.9

Total 2.8 3.3 6.1

(continued)Chairman’s Statement

7

The Group incurs a number of non cash P&L

charges, detailed below. Deemed remuneration

of £0.2m (2008: £0.6m) and notional interest of

£0.1m (2008: £0.3m) have both dropped as a

large proportion of related earn outs have been

settled during the year. Impairment charges of

£8.4m, including £5.5m in the first half of the year,

relate to the write down in the carried balance sheet

value of Tangible Financial, SMT, TMI and Oomph

following their reduced performance in 2009, as

well as investment in a small research start-up which

failed to thrive.

2009

£’000

2008

£’000

Headline operating profit 5,943 8,168

Net interest payable (887) (891)

Headline profit before tax 5,056 7,277

Exceptional costs (1,949) (1,285)

Fair value gain/(loss) on

financial instruments

155 (444)

Deemed remuneration (163) (647)

Share option credit – 450

Impairment of investments (207) -

Impairment of intangibles (8,161) -

Amortisation of intangibles (455) (858)

Notional interest (104) (291)

Reported (loss)/profit before tax (5,828) 4,202

The Group examines the above financial indicators

and as such they can be considered to be key

performance indicators.

Divisional Review

Cello (Research)

The strong position of Cello in the international market

research industry enabled the Group to successfully

defend client revenues in a challenging and highly

competitive market. The Group has been able to

demonstrate greater scale and a broader range

of skills and services with clients as it competes for

larger contracts with existing and new clients.

In addition, the Group has continued to consolidate

our operations into shared facilities as leases come

up for renewal, enabling it to create clusters of

professional resource which are both more vibrant

and efficient. As a result of continued consolidation

in the market research sector, it has risen to become

the 6th largest research operation in the UK (2008:

9th), and 19th globally (2008: 21st).

Cello (Research) had a solid year given the

economic context, delivering a headline

operating profit of £5.6m (2008: £6.5m) from

operating income of £36.3m (2008: £37.9m).

With an employee base of 415 (2008: 460) and

revenue of £59.8m (2008: £64.9m), Cello ranks

firmly in the top ten of market research businesses

based in the UK and is the only business which is

not part of a much larger Group.

Operating margins were 15.4% (2008: 17.2%) as a

result of reduced profit performance in its business

intelligence business and in aspects of its public

sector market research activity which has come

under long anticipated pressure. The general hiatus

in market research activity which occurred in the

middle of 2009 has now been replaced by more

normal levels of client activity.

8

Healthcare research has shown particular resilience,

representing approximately 38% of operating

income in this division (2008: 36%). As well as

continued strength in the pharmaceutical core, the

Group has successfully extended into the growing

OTC and brand orientated market for drugs and

therapies, particularly in the USA.

The Group has continued to more closely integrate

its research and consulting capability and achieve

competitive advantage against the much larger

networks with which it is now directly competing.

The Group has also continued to consolidate its

field force and online data capture capacity to

improve utilisation levels and to position itself as

a competitive outsourcing solution for larger

research networks.

The research business has continued to grow

worldwide, with international work now accounting

for 46.4% of divisional activity (2008: 42.3%). The

Group plan to expand its US presence organically

in 2010, building on its successful existing operation

in New York. The Group has appointed Simon

Dannatt as Managing Director, Cello USA. Simon

was previously Chief Executive of Optimisa PLC.

Top clients during the year included GSK, Novartis, HP,

Tesco, EA Games and Nokia. All these clients are long

standing and reflect the first class blue chip nature of

the Group’s client base. Significant new client wins

in 2009 include; Sandoz, Mundipharma, Bupa, Kraft,

Kimberly Clark, L’Oreal, Boden, HP, Cadburys, Coors,

Nestle, Eurostar, Tesco Bank, Swiss Re and Bayer.

Tangible

Tangible (Response) had a more challenging

time than Cello (Research), delivering a headline

operating profit of £1.8m (2008: £3.7m) on

operating income of £24.2m (2008: £27.5m).

Headline operating margins in this business were

7.4% (2008: 13.5%), reflecting the continued

declines in financial services income, as well as a

challenging context for charities related work and

general agency activity in London.

The Edinburgh hub of Tangible had an excellent

year, as did the Cheltenham and London core

operations with their focus on direct marketing with

strong digital capability. The integration of online

capability with more traditional direct marketing

approaches has proved a successful strategy as

clients look to reduce risks. This is expected to put

the business in a good position to capitalise on the

recovery in client activity. The Groups pioneering

carbon footprinting tool for marketers, Footmark, has

successfully established its carbon management

offer with clients such as Unicef, Christian Aid, Lloyds

TSB and Cafod.

The Group continues to invest in developing digital

applications. Our online communities’ proposition,

trading as Face, continued to flourish as part of

the co-creation methodology which underpins our

unique client proposition.

Tangible remains the 6th largest UK direct marketing

company in the UK. Top clients of Tangible include

the Scottish Government, Coors, AGBarr, The Royal

British Legion and the British Heart Foundation.

Significant new client wins in 2009 include; Axiom,

Endsleigh Insurance, Shelter, Oxfam, Christian Aid,

Motability, Sony, HSBC GAM, EBRD, Baillie Gifford,

Platform, Energy Savings Trust, Tesco Bank, Scottish

Enterprise, BBC, Nandos, Which?, BT, Cancer

Research, Save the Children, Clorex, Nokia, Danone,

Aegon and Reckitt Benckiser.

(continued)Chairman’s Statement

9

Current Trading

The Group is optimistic that the higher levels of client

activity, particularly in the research sector, seen in

the last quarter of 2009 and in the early months

of 2010, will continue. Cello has strong revenue

pipelines in Research and Consulting and Tangible

has also seen a marked increase in levels of new

business activity.

At this early stage of the year, with its substantially

lower cost base, improved market position and

strong presence in healthcare research, the Group

is well positioned to benefit from more normal levels

of ongoing client activity and will materially benefit

from any upturn in the UK or internationally.

Allan Rich

Non-Executive Chairman

15 March 2010

10

Cello Research and Consulting

Cello Research and Consulting is now a significant

player in the global market research and advisory

sector, ranked 6th largest in the UK and 19th

globally. It is the only independent agency of this

scale that is not part of a larger holding company.

Cello derives competitive advantage from the

combination of its market research and consultant

capability, which allows it to deliver, clients strategic

direction, based on real world insight.

Our largest area of focus is the healthcare market

which accounts for 38% of divisional revenue.

FMCG, public sector, business to business and

technology applications account for a further 40% of

income. Whilst largely an ad-hoc business, the bulk

of revenues come from long term, blue chip client

relationships. There is an even balance between

quantitative and qualitative work.

We continue to invest in developing digital

applications. Our online communities research offer

through the Face brand has developed strongly.

The year saw good progress in the international

development of the business. International

work now accounts for 46% of divisional

income and we retain a physical presence in New

York, Chicago and San Francisco.

2010 will see continued implementation of a three

year strategy to establish Cello as the leading

research and consulting brand across a number

of identified priority ‘vertical’ industry sectors, most

notably healthcare, consumer products and

technology.

Healthcare: Insight Research Group,

MSI, Leapfrog

• Insight’s New York office experienced sustained

growth where bookings have nearly tripled from

those seen in 2008 and at higher margins than in

previous years.

• The number of online projects continues to rise,

with international work tripling since 2008 (nearly

a fifth of Insight’s business).

• There has been sustained growth and broadening

of our international client base which has risen

from 22 at the end of 2008 to more than 30

different healthcare focused clients in 2009.

• MSI had a strong year and continued to extend its

client base with significant new wins with Sandoz

and Mundipharma.

• MSI Marketing Sciences showed continued

rapid growth and now represents a significant

proportion of MSI business.

• Leapfrog’s health and wellbeing research offer

had a very strong year, with major projects for

GSK, SC Johnson, Kimberly Clark and Bayer.

FMCG and Retail: The Value Engineers, Leapfrog,

2CV, Rosenblatt, TMI

• The Value Engineers continued to perform

strongly in 2009 with new clients including

Advent International, Bupa, Kraft, and the return

of some previous clients such as Heineken and

Dairy Crest.

• Leapfrog continued to build on client relationships

with Carphone Warehouse, Cadbury, SC Johnson,

Bayer, Comic Relief and new clients, including

Kimberly Clark, L’Oreal, Boden, Laithwaites, ABRSM,

McCanns.

• Global business more than doubled, with many

multi-market projects across Australia, America,

the BRIC economies, Japan and Europe.

• 2CV’s focus on international, mission critical

product development and marketing evaluation

enabled it to perform strongly in 2009 with clients

such as COI, TfL and ITV.

• The 2CV US office established itself, winning a

major global tracking study with local technology

giant, HP, and increased activity from EA.

• During 2009 Rosenblatt consolidated its

relationship with Philips, the COI, the BBC and

Mitchells & Butlers, and formed new (or revived)

11

relationships with Cadbury, Coors Brewers, Digital

UK, Millie’s Cookies, Nestle/Cereal Partners, Turner

Broadcasting and Unilever.

• TMI worked with a wide range of clients including

Eurostar, BHS, The Home Office, Harley Medical

Group and the Dorchester Hotels Group.

Public Sector: RS Group, CELLO mruk research

• The RS Group’s public policy team successfully

increased its revenue with projects for both

Government Departments and the NHS.

• CELLO mruk research’s global business more than

doubled behind healthcare activity.

• The number of Government Framework contracts

won during the year increased by around 50%

to 34 contracts including Office of Fair Trading,

Central Office of Information, Competition

Commission, National Archives, Ofcom and the

Welsh Assembly.

Technology: RS Group, SMT, Kudos

• In RS’s core technology and logistics sectors there

were significant commissions from HP, Canon,

Brother and DHL, while its financial services division

delivered major new account wins including

Tesco Bank and Swiss Re.

• Significant investment in online research tools

has allowed the group to successfully market

both on qualitative and quantitative projects to

an increasing proportion of its customer base.

• 2009 saw SMT strengthen and build upon its

position in the utilities sector which contributed

over 50% of SMT’s revenue in 2009.

• Kudos saw an increase in revenue in the

pharma and wellbeing sectors, with health and

environmental strategy studies accounting for

15% of overall revenue in 2009.

12

Tangible Group

In 2009 tangible group made significant steps

toward organising itself into three hubs - London,

Edinburgh and Cheltenham. Shifting businesses into

shared offices reduces property and management

costs but also ensures better cross selling and

more effective use of senior, vocational staff. This

approach has been in place in Edinburgh since

2008, and 2009 saw that hub produce a record

profit and high levels of net profit margin compared

to industry norms. Overall the group’s emphasis

remains on results orientated and customer focused

marketing. Its strength in direct marketing has seen the

group reach 6th place in Marketing’s Direct League

table, making it the largest UK specific group.

The group has a significant client base in Financial

Services, Charities, Public Sector, FMCG/Drinks, Retail

and Utilities. Performance in 2009 was significantly

influenced by the downturn in Financial Services

and Charity marketing although these showed signs

of recovery towards the end of 2009.

tangible group is now organised around three

primary functions within the three hubs – insight,

marketing delivery and production.

Insight

Face, tangible data, Leithal Thinking.

• Face, continued to grow strongly with revenue

up by 50% on 2009 with client wins from Unilever,

Nokia, Clorox, SAB Miller, Danone and Reckitt

Benckiser in the US, Argentina, Mexico, Brazil,

China, Indonesia, Russia and Europe.

• Continued growth of our online communities

offering including the successful launch of

Mindbubble – a co-creation community for

women.

• The data division continues to provide cutting

edge analysis and research solutions and

segmentations, working closely with clients such

as British Gas, Help the Aged, and Business

Stream, as well as with new clients including

Tesco Bank, Which?, BT, Cancer Research UK,

Kidney Research UK, Save the Children.

• Clients such as VW/SEAT, Energy Saving Trust and

Calor continue to use Magellan, the proprietary

online marketing platform which supports on and

offline campaigns.

• The Leithal Thinking brand consultancy broke the

£1 million revenue mark with a number of wins

including Scottish Wildlife Trust, Kasteel Cru and

Historic Scotland.

Marketing Delivery

tangible, Leith, Farm, Blonde, Stripe

• Tangible’s increased emphasis on strategic

communications planning produced significant

new clients wins including Oxfam, Shelter,

Christian Aid (Present Aid), Beatson and Motability

in Charities, COI Energy Savings Trust, Scottish

Development International, Consumer Focus

Scotland, and Glasgow University roster in Public

Sector.

• Significant new financial client wins in 2009

included Tesco Bank, HSBC Global Asset

Management, European Bank for Reconstruction

and Development, Baillie Gifford and Platform.

• Tangible was awarded several industry awards

including a DMA award for Business to Consumer

Direct Marketing, a Silver for the Best Use of Direct

Mail in the Cream Awards and the Institute of

Fundraising Award for the Best use of Direct Mail.

• Tangible also received awards recognition from

Money Marketing – 2 x gold, 2 x silver and 1 x

bronze, and the Financial Services Forum (Most

Effective New Product, Service or Innovation –

MGM and tangible).

13

• 2009 saw a record operating profit performance

for Leith, driven by strong incremental growth in

existing clients and a number of new business

wins, predominantly in the public sector

(including Scottish Enterprise, See Me, Scottish

Natural Heritage and The Public Health Agency

for Northern Ireland).

• Farm strengthened its position on the Nestle

roster with wins from both the Confectionery and

Beverages divisions, as well as major projects with

the BBC, Nandos and Last Minute.com.

• New clients for Blonde included Nokia, Lloyds TSB,

Bank of Scotland Corporate, Rice Dream, Harrison

Parrot, SCO, Creative Scotland and AEGON.

• Stripe PR crowned a year of significant growth by

being awarded the IPR’s PR consultancy of the

year. They also cemented their position on the

Scottish Government roster with briefs for Alcohol

Awareness and Community and Road Safety.

Production

Brightsource, Magnetic

• Brightsource extended its track record of profit

growth for the 8th successive year. All top 15

clients increased their spend, compared with

2008, a reflection of the widening portfolio of

services. New clients for 2009 included Axiom,

Endsleigh Insurance and Shelter.

• Brightsource’s pioneering carbon footprinting

tool, Footmark, has successfully established the

carbon management offer with leading clients

such as Unicef, Christian Aid, Lloyds TSB, and

Cafod.

• Magnetic launched two new products – Standout

Covers and Proxi packs – the latter has been

picked up by Sony for worldwide use in their

Playstation 3 point of sale.

14

The directors present their report and the financial

statements of Cello Group plc for the year to 31

December 2009. To the best of their knowledge

the Directors’ Report includes a fair view of the

business and position of the Group, together with

a description of the principal risks and uncertainties

faced by the Group.

Principal Activities

The principal activity of the Group during the year

under review is that of research, consulting and

direct marketing.

Review of the Business and Future Developments

The results for the year ended 31 December 2009

are set out in the Group income statement on

pages 24 and 25. These show a loss attributable

to shareholders of £6,359,000. An interim dividend

of 0.50p per share was paid during the year and a

final dividend of 0.80p per share is proposed.

A review of the development and future prospects

of the business is given in the Chairman’s Statement

on pages 4 to 9. Key performance indicators are

also commented on within the Financial Review

section of the Chairman’s Statement.

Company law requires the Company to report on

principal risks and uncertainties facing the business,

which the directors believe to be as follows:

1. UK economy

The Group’s business is domiciled in the UK but 22%

of the Group’s revenues are from clients based

overseas. It is clear that the current economic

downturn has adversely affected the Group and

there is a risk that further economic downturn in

any of our markets will have an additional affect.

However, the mix of services we are offering is

proving resilient as the economy stabilises.

2. Loss of the Group’s key clients

Client relationships are crucial to the Group, and

the strength of them is key to its continued success.

The risk is mitigated by our client base being broadly

spread, but the loss of any large client would

require replacement. The Group’s client review

programmes help mitigate this risk.

3. Loss of key staff

The Group’s directors and staff are critical to the

servicing of existing business and the winning of new

accounts, departure of key staff could be a risk to

maintaining client service. With that risk in mind all

senior staff are subject to financial lock-ins and long-

term incentive arrangements, as well as being under

contractual non-compete and non-solicit clauses.

Directors

The following directors have held office since

1 January 2009:

Mark Scott

Mark Bentley

Paul Hamilton

Will David

Allan Rich

Chris Outram

Biographical details of the directors at the date of

this report are set out on pages 84 to 85.

Directors’ Report

15

Directors’ Interests in Shares and Options

Directors’ interests in the shares of the Company were as follows:

Number of ordinary

shares of 10p each

At 31 December 2009

Number of ordinary

shares of 10p each

At 31 December 2008

Mark Scott 724,010 714,010

Mark Bentley 15,000 15,000

Paul Hamilton 50,000 50,000

Will David 15,000 15,000

Allan Rich 444,595 415,184

Chris Outram 83,782 48,705

Under the rules of the Enterprise Management Incentive Scheme and the Unapproved Share Option

Scheme, the Executive Directors have been granted an interest in options over ordinary shares of 10p

each as follows:

At 1 January

2009 number of

ordinary shares of

10p each

Granted

in the year number of

ordinary shares of

10p each

Lapsed in

the year number of

ordinary shares of

10p each

At 31 December

2009 number of

ordinary shares of

10p each

Date from which

exercisable

Expiry date

Exercise price

(pence)

Mark Scott (1) 100,000 – – 100,000 Nov 2004 Nov 2014 100

Mark Scott (2) 200,000 – – 200,000 Nov 2004 Nov 2014 100

Mark Bentley (1) 81,633 – – 81,633 Jun 2008 Jun 2015 122.5

Mark Bentley (2) 81,633 – – 81,633 Jun 2008 Jun 2015 122.5

(1) Granted under the EMI Share Option Scheme

(2) Granted under the Unapproved Share Option Scheme

None of the options that have been granted were exercised in the year.

16

Share Capital

Changes to the Company’s share capital during

the year are given in note 22 to the consolidated

financial statements.

Treasury Shares

During the year the Company purchased 157,000

(0.29% of the issued share capital) ordinary shares

of 10p each for a total consideration of £53,000.

The total number of shares in treasury at 31

December 2009 was 237,000 (0.40% of the issued

share capital). The purpose of the acquisition was

to satisfy future earn out payments and/or option

awards.

Statement of Directors’ Responsibilities

The directors are responsible for preparing the

Directors’ Report and the financial statements in

accordance with applicable law and regulations.

Company law requires the directors to prepare

group and company financial statements for each

financial year. The directors are required by the AIM

rules of the London Stock Exchange to prepare

group financial statements in accordance with

International Financial Reporting Standards (“IFRS”)

as adopted by the European Union (“EU”) and

have elected under company law to prepare the

company financial statements in accordance with

United Kingdom Generally accepted Accounting

Practice (United Kingdom Accounting Standards

and applicable law).

The Group financial statements are required by law

and IFRS as adopted by the EU to present fairly the

financial position and performance of the Group,

the Companies Act 2006 provides in relation to

such financial statements that references in the

relevant part of that Act to financial statements

giving a true and fair view are references to their

achieving a fair presentation.

Under company law the directors must not approve

the financial statements unless they are satisfied

that they give a true and fair view of the state of

affairs of the Group and the Company and of the

profit or loss of the Group for that period.

In preparing each of the Group and Company

financial statements, the directors are required to:

a. Select suitable accounting policies and then

apply them consistently;

b. Make judgements and estimates that are

reasonable and prudent;

c. For the Group financial statements, state whether

they have been prepared in accordance with

IFRSs adopted by the EU; and for the Company

financial statements state whether applicable

UK accounting standards have been followed,

subject to any material departures disclosed and

explained in the Company financial statements;

d. Prepare the financial statements on the going

concern basis unless it is inappropriate to

presume that the Group and the Company will

continue in business.

Directors’ Report (continued)

Substantial Shareholdings

Other than the directors’ interests disclosed above, the Company is aware of the following shareholdings

of 3% or more in the issued share capital at 28 February 2010:

No. of shares %

Octopus Asset Management Limited 5,200,290 8.85

Richard Gilmore 3,214,144 5.47

Universities Superannuation Scheme 2,047,000 3.48

Paul Walton 1,869,680 3.18

17

The directors are responsible for keeping adequate

accounting records that are sufficient to show and

explain the Group’s and the Company’s transactions

and disclose with reasonable accuracy at any time

the financial position of the Company and enable

them to ensure that the financial statements

comply with the Companies Act 2006. They are

also responsible for safeguarding the assets of the

Group and hence for taking reasonable steps for

the prevention and detection of fraud and other

irregularities.

The directors are responsible for the maintenance and

integrity of the corporate and financial information

included on the Cello Group plc website.

Legislation in the United Kingdom governing

the preparation and dissemination of financial

statements may differ from legislation in other

jurisdictions.

Employees

It is the Company’s policy not to discriminate

between employees or potential employees on

any grounds. Full and fair consideration is given to

the recruitment, training and promotion of disabled

people and, should staff become disabled

during the course of their employment, efforts

are made to provide appropriate re-training. The

Company places enormous importance on the

contributions of its employees and aims to keep

them informed of developments in the Company

through a combination of meetings and electronic

communication.

Political and Charitable Contributions

During the year the Company made no political or

charitable donations.

Directors Third Party Indemnity Provisions

A qualifying Third Party Indemnity Provision was in

place for directors throughout the year.

Policy on Payment to Creditors

The Company agrees the terms and conditions

under which business transactions with suppliers are

conducted. It complies with these payment terms,

provided that it is satisfied that the supplier has

provided the goods or services in accordance with

agreed terms and conditions.

The effect of the Company’s payment policy is that

its trade creditors at the year end represent 48 days

(2008: 43 days).

Research and Development Activities

During the year the Group spent £141,000 (2008:

£119,000) on the development of new software

products which are expected to generate

economic benefits in the future. These amounts

were capitalised as intangible assets.

Statement as to Disclosure of Information to the

Auditors

The directors who were in office on the date of

approval of these financial statements have

confirmed that, as far as they are aware, there is

no relevant audit information of which the auditors

are unaware. Each of the directors has confirmed

that he, as far as he is aware, has taken all the

steps that he ought to have taken as a director

in order to make himself aware of any relevant

audit information and to establish that it has been

communicated to the auditor.

Auditors

A resolution to re-appoint Baker Tilly UK Audit LLP,

Chartered Accountants, as auditors will be proposed

at the forthcoming Annual General Meeting.

By order of the Board

Mark Bentley

Company Secretary

15 March 2010

18

Corporate Governance

The Board of Cello Group plc appreciates the value

of good corporate governance not only in the areas

of accountability and risk management but also as

a positive contribution to the business. The Board

considers that the Company, whilst trading on the

AIM Market, has adopted those requirements of the

Combined Code on Corporate Governance (the

“Code”) published in June 2006 as best applicable

to the Company given its current size.

Board Structure

The Board comprises two executive directors and

four non-executive directors. The roles of Chairman

and Chief Executive are separate. The Non-Executive

Directors are independent of management and

free from any business or other relationship with the

Company other than owning shares. The directors’

biographies appear on pages 84 to 85.

The Board is scheduled to meet at least six times

a year and additionally when necessary. At each

scheduled meeting of the Board, the Chief

Executive and Finance Director report on the

Group’s operations. The Board is satisfied that it is

provided with information in an appropriate form

and quality to enable it to discharge its duties. All

directors are subject to re-election by shareholders

at the first opportunity after their appointment. All

directors are required to retire by rotation and one

third of the Board is required to seek re-election

each year. The Chairman ensures that the directors

are permitted to take independent professional

advice as required.

All directors have access to the advice and services

of the Company Secretary, who is responsible to

the Board for ensuring that Board procedures are

followed and that applicable rules and regulations

are complied with.

The following committees of the Board have been

established to deal with specific aspects of the

Company’s affairs.

Audit Committee

The Audit Committee consists of three Non-Executive

Directors; Will David as Chairman, Paul Hamilton

and Allan Rich. The Committee considers matters

relating to the financial accounting controls, the

reporting of results, and the effectiveness and cost

of the audit. It aims to meet at least twice a year

with the Company’s auditors in attendance. Other

directors attend as required. The Company Secretary

provides secretarial support to the Committee. The

terms of reference of the Committee are available

on request.

In considering the effectiveness of the audit the

Audit Committee will also, where appropriate,

consider whether any flexibility over rotation of the

audit partner is appropriate in order to safeguard

the quality of the audit.

The Audit Committee is satisfied that the Group’s

auditors, Baker Tilly UK Audit LLP, have been objective

and independent of the Group. Associate firms of

Baker Tilly UK Audit LLP perform non-audit services for

the Group, but the Audit Committee is satisfied that

their objectivity is not impaired by such work.

Nomination Committee

The Nomination Committee consists of two

independent Non-Executive Directors; Paul

Hamilton and Will David. The Committee is chaired

by Paul Hamilton and meets as necessary. The

Committee is formally constituted with written terms

of reference and is responsible for reviewing and

making proposals to the Board on the appointment

of directors. The Company Secretary provides

secretarial support to the Committee. The terms

of reference of the Nominations Committee are

available on request.

Remuneration Committee

The Remuneration Committee is formally

constituted with written terms of reference and

makes recommendations to the Board with regard

to remuneration policy and related matters. The

Remuneration Committee consists solely of three

of the Independent Non-Executive Directors, Paul

Hamilton, who chairs the committee, Will David and

Chris Outram. However, the Chairman and the Chief

Executive attend as required and have the right to

address the Committee. The Committee aims to

19

meet at least twice a year. The terms of reference

of the Committee are available on request.

Further details of the Company’s policies on

remuneration, including details of directors’ share

options are given in the Report of the Remuneration

Committee on pages 20 to 22.

Shareholder Communications

The Company believes in maintaining good

communications with shareholders. The Chief

Executive and Finance Director meet analysts

and institutional shareholders regularly with a view

to ensuring that the strategies and objectives of

the Company are well understood. The Senior

Independent Director will not ordinarily attend

such meetings other than at the request of the

relevant shareholder. However, he is available to

shareholders if they have concerns which contact

through the Chairman, Chief Executive or the

Finance Director has failed to resolve or for which

such contact is inappropriate.

Going Concern

The directors have satisfied themselves that the

Company and Group have adequate resources to

continue in operational existence for the foreseeable

future, and for this reason the financial statements

continue to be prepared on a going concern basis.

Internal Control

The Board is responsible for ensuring that the

Group maintains a system of internal controls and

risk management, including suitable monitoring

procedures. The objective of the system is to

safeguard Group assets, ensure proper accounting

records are maintained and that the financial

information used within the business and for

publication is reliable. Any such system can only

provide reasonable, but not absolute, assurance

against material misstatement or loss.

Given the Group’s size and the nature of its business,

the Board does not consider it would be appropriate

to have its own internal audit function. An internal

audit function will be established as and when the

Group is of an appropriate size but meanwhile the

audit of internal financial controls forms part of the

responsibilities of the Group’s finance function.

All the day-to-day operational decisions are taken

initially by the executive directors or subsidiary

directors, in accordance with the Group’s strategy.

Where appropriate, the Board or subsidiary

directors approve such decisions. The executive or

subsidiary directors are also responsible for initiating

all transactions and authorising all payments, save

for those relating to their employment. As such, the

internal controls primarily comprise:

• the segregation of duties, such that the executive

directors have no involvement in the recording

of any financial data;

• the review of pertinent financial and other

information by the Board on a regular basis;

• the prior approval of all significant strategic

decisions;

• having a formal strategy for business activities.

The Environment

The activities of the Group do not have a high impact

on the environment. However, we aim to ensure that

where waste can be reduced, this is done efficiently,

by employing recycling where viable.

Employees

The Group employs nearly 800 employees, and we

place a great deal of emphasis on their training

and retention. Our central programme for rising

talent, “Cello Academy”, is now a well established

feature of our staff development initiatives.

On behalf of the Board

Mark Bentley

Company Secretary

15 March 2010

20

The directors have applied the principles of good

governance relating to directors’ remuneration as

described below:

Remuneration Committee

The Remuneration Committee is authorised on

behalf of the Board to determine the Company’s

remuneration policy on executive directors’

remuneration, including pension rights and share

option awards, and the terms of their service

contracts. The Committee aims to meet at least

twice a year and supervises the operation of share

schemes and other employee incentive schemes.

The remuneration and terms and conditions of

appointment of the Non-Executive Directors will

be set by the Board. No director shall participate

in discussions relating to his own remuneration.

The Remuneration Committee consists of three

of the independent Non-Executive Directors, Paul

Hamilton who chairs the committee, Will David and

Chris Outram.

Remuneration Policy

The policy of the Board is to provide executive

remuneration packages designed to attract,

motivate and retain directors of the calibre

necessary to maintain the Group’s position as a

market leader and to reward them for enhancing

shareholder value and return on investment. The

remuneration should also reflect the directors’

responsibilities and contain incentives to deliver the

Group’s objectives.

The main elements of the executive directors’

remuneration packages are as follows:

• basic salary;

• performance-related bonus – 50% of an

executive director’s bonus is based on earnings

per share growth targets set by the Remuneration

Committee at the beginning of the financial

year. The remaining 50% is paid at the discretion

of the Remuneration Committee;

• benefit package – car allowance and health

care insurance;

• share option incentives – details of share options

granted to the executive directors are shown on

page 15;

• contributions to directors’ individual defined

contribution pension schemes.

The Remuneration Committee reviews the

components of each executive director’s

remuneration package annually.

Report of the Remuneration Committee

Directors’ Remuneration

Salary/ Fees

£’000

Bonus £’000

Benefits

£’000

Total Emoluments

£’000

Pension

£’000

Total 2009 £’000

Total 2008 £’000

Kevin Steeds* – – – – – – 233

Mark Scott 195 45 9 249 29 278 296

Mark Bentley 145 28 6 179 22 201 204

Allan Rich 47 – – 47 – 47 25

Paul Hamilton 28 – – 28 – 28 30

Will David 25 – – 25 – 25 25

Chris Outram 23 – – 23 – 23 25

Total 463 73 15 551 51 602 838

*Deceased on 17 December 2008

21

Long Term Incentive Arrangements

In 2004, the Company established an EMI Share

Option plan to allow selected employees to share

in the success of the Group and promote motivation

and retention through the award of tax efficient

share options.

A summary of all the share option awards to directors

can be found in the directors’ report on page 15.

In 2004, the Company also established an

Unapproved Share Option plan for those individuals

not eligible to participate under the EMI Share Option

plan and for the award of additional options to the

recipients of awards under the EMI Share Option plan.

Vesting of the share options awarded to Mark Scott

in November 2004 under the EMI and Unapproved

Share Option Plans is not subject to performance

conditions but vesting of the share options granted

to Mark Bentley in June 2005 under these plans was

subject to performance conditions which have

been met.

On 13 March 2006 the Board adopted the Cello

Group plc Performance Share Plan 2006 (“PSP”).

However, no awards since made under the PSP

are now capable of vesting and the Remuneration

Committee has decided to make no further awards

under the PSP. To replace the PSP the Board has

adopted two new share option plans and a Joint

Ownership Share plan.

On 17 November 2009 the Board adopted the

Cello Group plc HM Revenue & Customs Approved

Share Option Plan 2009 (the “Approved Plan”) and

on 15 March 2010 adopted the Cello Group plc

Unapproved Option Plan 2010 (the “Unapproved

Plan”).

Under the Approved Plan and the Unapproved Plan

(the “Option Plans”) awards of options over shares

with a market value of no more than 150% of basic

salary may be made to any one individual in any

financial year. A higher percentage may be granted

in exceptional circumstances, as determined by the

Remuneration Committee. It is not currently intended

that main board directors will participate in the

Option Plans.

Options will generally be exercisable three years, but

not later than ten years, after the date of grant subject

to the extent to which performance conditions have

been achieved over the initial three year period after

the award is made and subject to the participant’s

continued employment with the Group.

Performance conditions will be tailored to each

participant according to his or her seniority and

responsibilities and will be based on performance

as measured against an appropriate combination

of Company, Division and Group targets and the

extent to which these are achieved or exceeded

over the performance period will determine the

proportion of each participant’s options which vest.

The Committee will review the Option Plans on a

regular basis and may amend the performance

conditions from time to time.

The Board are in the process of finalising a Joint

Ownership Share Plan 2010 (“JOSP”) under which it

is intended that awards will be made to the Group’s

most senior employees, including main board

executive directors.

Name Title Date of Appointment Notice period

Allan Rich Non-Executive Chairman 5 April 2005 3 months

Mark Scott Chief Executive 5 May 2004 12 months

Mark Bentley Finance Director 1 May 2005 12 months

Paul Hamilton Senior Non-Executive Director 8 October 2004 6 months

Will David Non-Executive Director 8 October 2004 6 months

Chris Outram Non-Executive Director 1 July 2007 3 months

22

Report of the Remuneration Committee (continued)

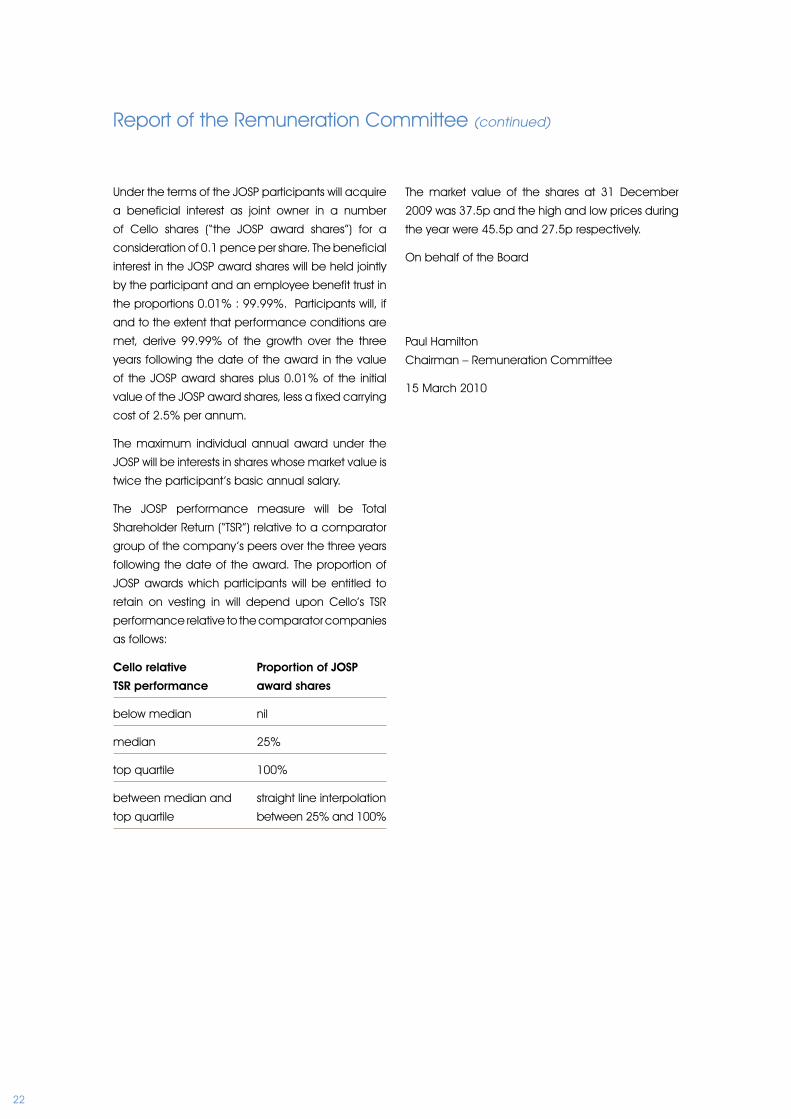

Under the terms of the JOSP participants will acquire

a beneficial interest as joint owner in a number

of Cello shares (“the JOSP award shares”) for a

consideration of 0.1 pence per share. The beneficial

interest in the JOSP award shares will be held jointly

by the participant and an employee benefit trust in

the proportions 0.01% : 99.99%. Participants will, if

and to the extent that performance conditions are

met, derive 99.99% of the growth over the three

years following the date of the award in the value

of the JOSP award shares plus 0.01% of the initial

value of the JOSP award shares, less a fixed carrying

cost of 2.5% per annum.

The maximum individual annual award under the

JOSP will be interests in shares whose market value is

twice the participant’s basic annual salary.

The JOSP performance measure will be Total

Shareholder Return (“TSR”) relative to a comparator

group of the company’s peers over the three years

following the date of the award. The proportion of

JOSP awards which participants will be entitled to

retain on vesting in will depend upon Cello’s TSR

performance relative to the comparator companies

as follows:

Cello relative Proportion of JOSP

TSR performance award shares

below median nil

median 25%

top quartile 100%

between median and straight line interpolation

top quartile between 25% and 100%

The market value of the shares at 31 December

2009 was 37.5p and the high and low prices during

the year were 45.5p and 27.5p respectively.

On behalf of the Board

Paul Hamilton

Chairman – Remuneration Committee

15 March 2010

23

We have audited the Group and parent company

financial statements (“the financial statements”) on

pages 24 to 77. The financial reporting framework

that has been applied in the preparation of the

Group financial statements is applicable law and

International Financial Reporting Standards (IFRSs)

as adopted by the European Union. The financial

reporting framework that has been applied in

the preparation of the parent company financial

statements is applicable law and United Kingdom

Accounting Standards (United Kingdom Generally

Accepted Accounting Practice).

This report is made solely to the company’s

members, as a body, in accordance with Chapter

3 of Part 16 of the Companies Act 2006. Our audit

work has been undertaken so that we might state

to the company’s members those matters we are

required to state to them in an auditor’s report and

for no other purpose. To the fullest extent permitted

by law, we do not accept or assume responsibility

to anyone other than the company and the

company’s members as a body, for our audit work,

for this report, or for the opinions we have formed.

Respective responsibilities of directors and

auditor

As more fully explained in the Statement of Directors’

Responsibilities, the directors are responsible for

the preparation of the financial statements and

for being satisfied that they give a true and fair

view. Our responsibility is to audit the financial

statements in accordance with applicable law and

International Standards on Auditing (UK and Ireland).

Those standards require us to comply with the

Auditing Practices Board’s (APB’s) Ethical Standards

for Auditors.

Scope of the audit of the financial statements

A description of the scope of an audit of financial

statements is provided on the APB’s website at

www.frc.org.uk/apb.scope/UKNP.

Opinion on the financial statements

In our opinion:

• the financial statements give a true and fair view

of the state of the Group’s and of the parent

company’s affairs as at 31 December 2009 and

of the Group’s loss for the year then ended;

• the Group financial statements have been

properly prepared in accordance with IFRSs as

adopted by the European Union;

• the parent company financial statements have

been properly prepared in accordance with

United Kingdom Generally Accepted Accounting

Practice; and

• the financial statements have been prepared

in accordance with the requirements of the

Companies Act 2006.

Opinion on other matters prescribed by the

Companies Act 2006

In our opinion the information given in the Directors’

Report for the financial year for which the financial

statements are prepared is consistent with the

financial statements.

Matters on which we are required to report

by exception

We have nothing to report in respect of the following

matters where the Companies Act 2006 requires us

to report to you if, in our opinion:

• adequate accounting records have not

been kept by the parent company, or returns

adequate for our audit have not been received

from branches not visited by us; or

• the parent company financial statements are

not in agreement with the accounting records

and returns; or

• certain disclosures of directors’ remuneration

specified by law are not made; or

• we have not received all the information and

explanations we require for our audit.

DAVID FENTON (Senior Statutory Auditor)

For and on behalf of

BAKER TILLY UK AUDIT LLP

Statutory Auditor

Chartered Accountants

2 Bloomsbury Street

London WC1B 3ST

15 March 2010

Independent Auditors’ Reportto the members of Cello Group plc

24

Consolidated Income Statement for the year ended 31 December 2009

Notes

Year ended 31 December 2009

£’000

Year ended 31 December 2008

£’000

Continuing operations

Revenue

Cost of sales

1 126,660

(66,201)

137,630

(72,269)

Operating income

Administration expenses

1

3a

60,459

(54,516)

65,361

(57,193)

Headline operating profit

Exceptional items

Amortisation of intangible assets

Acquisition related employee expenses

Share option credit

1

3a

10

18

23

5,943

(1,949)

(455)

(163)

–

8,168

(1,285)

(858)

(647)

450

Operating profit before impairment charges

Impairment of intangible assets

Impairment of goodwill

Impairment of available-for-sale investments

1

10

9

12

3,376

(778)

(7,383)

(207)

5,828

–

–

–

Operating (loss)/profit

Finance income

Finance cost of deferred consideration

Fair value gain/(loss) on derivative financial instruments

Other finance costs

3a

2

2

2

2

(4,992)

69

(104)

155

(956)

5,828

243

(291)

(444)

(1,134)

(Loss)/profit on continuing operations before taxation

Tax 5

(5,828)

(239)

4,202

(1,015)

(Loss)/profit on continuing operations after taxation

Loss from discontinued operations 6

(6,067)

(253)

3,187

(386)

(Loss)/profit for the year (6,320) 2,801

Attributable to:

Owners of the parent

Minority interest

(6,359)

39

2,761

40

(6,320) 2,801

25

Consolidated Income Statement (continued) for the year ended 31 December 2009

Notes

Year ended 31 December 2009

£’000

Year ended 31 December 2008

£’000

Basic (loss)/earnings per share

From continuing operations

From discontinued operations

8

8

(11.26)p

(0.47)p

7.35p

(0.90)p

(11.73)p 6.45p

Diluted (loss)/earnings per shareFrom continuing operationsFrom discontinued operations

88

(11.26)p(0.47)p

5.55p(0.68)p

(11.73)p 4.87p

Consolidated Statement of Comprehensive Income for the year ended 31 December 2009

Year ended 31 December 2009

£’000

Year ended 31 December 2008

£’000

(Loss)/profit for the year (6,320) 2,801

Other comprehensive income:

Exchange differences on translation of foreign operations

Deferred tax recognised direct in equity

12

–

(47)

222

Total other comprehensive income for the year 12 175

Total comprehensive income for the year (6,308) 2,976

26

Consolidated Balance Sheet 31 December 2009

Notes

31 December 2009 £’000

31 December 2008 £’000

Goodwill

Intangible assets

Property, plant and equipment

Available-for-sale investments

Deferred tax assets

9

10

11

12

21

67,926

1,174

2,515

20

962

76,291

2,266

3,103

227

1,080

Non-current assets

Trade and other receivables

Cash and cash equivalents

14

14

72,597

25,711

3,135

82,967

26,658

5,065

Current assets 28,846 31,723

Trade and other payables

Current tax liabilities

Borrowings

Consideration payable in respect of acquisitions

Obligations under finance leases

Derivative financial instruments

15

16

18

19

20

(25,419)

(568)

(14,529)

(2,472)

(68)

(289)

(26,633)

(708)

(1,053)

(7,980)

(68)

–

Current liabilities (43,345) (36,442)

Net current liabilities (14,499) (4,719)

Total assets less current liabilities

Borrowings

Provisions

Obligations under finance leases

Derivative financial instruments

Deferred tax liabilities

16

17

19

20

21

58,098

–

(3,315)

(65)

–

(292)

78,248

(13,750)

(6,453)

(86)

(444)

(616)

Non-current liabilities (3,672) (21,349)

Net assets 54,426 56,899

Equity

Share capital

Share premium

Retained earnings

Capital redemption reserve

Merger reserve

Share-based payment reserve

Foreign currency reserve

22 5,876

34,945

2,904

50

10,496

73

(35)

4,456

31,745

10,048

50

10,496

73

(47)

Equity attributable to equity holders of parent

Minority interest

54,309

117

56,821

78

Total equity 54,426 56,899

Approved and authorised for issue by the Board on 15 March 2010 and signed on its behalf by

Mark Scott Director

Mark Bentley Director

27

Consolidated Cash Flow Statement for the year ended 31 December 2009

Notes

Year ended 31 December

2009 £’000

Year ended 31 December

2008 £’000

Net cash inflow from operating activities before

taxation

Tax paid

24a 5,198

(591)

9,682

(1,911)

Net cash inflow from operating activities after taxation 4,607 7,771

Investing activities

Interest received

Purchase of property, plant and equipment

Sale of property, plant and equipment

Expenditure on intangible assets

Deferred consideration paid for subsidiary undertakings

69

(699)

39

(141)

(1,478)

243

(1,119)

66

(119)

(3,636)

Net cash outflow from investing activities (2,210) (4,565)

Financing activities

Dividends paid to equity holders of the parent

Repayment of borrowings

Repayment of loan notes

Drawdown of borrowings

Capital element of finance lease payments

Payment of finance lease interest

Interest paid

Purchase of own shares

(733)

(3,000)

(2,187)

2,600

(21)

(21)

(935)

(52)

(556)

(8,050)

(5,211)

10,050

(90)

(21)

(1,105)

(71)

Net cash outflow from financing (4,349) (5,054)

Movements in cash and cash equivalents

Net decrease in cash and cash equivalents

Exchange gains/(losses) on cash and bank overdrafts

Cash and cash equivalents at the beginning of the year

(1,952)

22

5,065

(1,848)

(73)

6,986

Cash and cash equivalents at end of the year 24b 3,135 5,065

28

Consolidated Statement of Changes in Equity for the year ended 31 December 2009

Share Capital

£’000

Share Premium

£’000

Capital Redemption

Reserve £’000

Merger Reserve

£’000

Share-based

Payment Reserve

£’000

Foreign Currency

Exchange Reserve

£’000

Retained Earnings

£’000

Total Attributable

to Owners of the Parent

£’000

Minority Interest

£’000

Total Equity £’000

At 1 January 2008 3,884 25,776 50 10,496 523 – 7,692 48,421 38 48,459

Profit for the year – – – – – – 2,761 2,761 40 2,801

Other comprehensive

income:

Currency translation

Deferred tax recognised

direct in equity

–

–

–

–

–

–

–

–

–

–

(47)

–

–

222

(47)

222

–

–

(47)

222

Total other comprehensive

income for the year

–

–

–

– – (47) 222 175 – 175

Total comprehensive income

for the year – – – – – (47) 2,983 2,936 40 2,976

Transactions with owners:

Shares issued

Own shares purchased

Debit for share-based

incentive schemes

Dividends

572

–

–

–

5,969

–

–

–

–

–

–

–

–

–

–

–

–

–

(450)

–

–

–

–

–

–

(71)

–

(556)

6,541

(71)

(450)

(556)

–

–

–

–

6,541

(71)

(450)

(556)

Total transactions with owners 572 5,969 – – (450) – (627) 5,464 – 5,464

At 1 January 2009 4,456 31,745 50 10,496 73 (47) 10,048 56,821 78 56,899

Loss for the year – – – – – – (6,359) (6,359) 39 (6,320)

Other comprehensive

income:

Currency translation – – – – – 12 – 12 – 12

Total comprehensive income

for the year

–

–

–

– – 12 (6,359) (6,347) 39 (6,308)

Transactions with owners:

Shares issued

Own shares purchased

Dividends

1,420

–

–

3,200

–

–

–

–

–

–

–

–

–

–

–

–

–

–

–

(52)

(733)

4,620

(52)

(733)

–

–

–

4,620

(52)

(733)

Total transactions with

owners 1,420 3,200 – – – – (785) 3,835 – 3,835

As at 31 December 2009 5,876 34,945 50 10,496 73 (35) 2,904 54,309 117 54,426

The merger reserve was created as a result of the placing of shares on 4 November 2004.

The capital redemption reserve arose from the purchase and cancellation of own share capital.

29

GENERAL INFORMATION

Cello Group plc is a company incorporated in the United Kingdom under the Companies Act 1985. The

Group’s operations consist principally of research, consulting and direct marketing.

These financial statements are presented in pounds sterling as this is the currency of the primary economic

environment in which the Group operates.

At the date of authorisation of these financial statements, the following standards and interpretations, which

are issued but not yet effective, have not been applied:

Effective for reporting

periods starting on or after

IFRIC 9 Reassessment of Embedded Derivatives – Amendment;

Embedded Derivatives

30 June 2009

IFRIC 14 Amendments – Prepayments of a Minimum Funding

Requirement

1 January 2011

IFRIC 17 Distributions of Non-cash Assets to Owners 1 July 2009

IFRIC 18 Transfers of Assets from Customers 1 July 2009

IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments 1 July 2010

Amendments to IFRSs arising from Annual Improvements Projects

Effective for reporting

periods starting on or after

IFRS 2 Share-based Payment 1 July 2009

IFRS 5 Non-current Assets Held for Sale and Discontinued

Operations

1 January 2010

IFRS 6 Exploration for and Evaluation of Mineral Resources

(consequential amendments from IAS 7)

1 January 2010

IFRS 8 Operating Segments 1 January 2010

IAS 1 Presentation of Financial Statements 1 January 2010

IAS 7 Statement of Cash Flows 1 January 2010

IAS 17 Leases 1 January 2010

IAS 36 Impairment of Assets 1 January 2010

IAS 38 Intangible Assets 1 July 2009

IAS 39 Financial Instruments: Recognition and Measurement 1 January 2010

IFRIC 9 Reassessment of Embedded Derivatives 1 July 2009

IFRIC 16 Hedges of a Net Investment in a Foreign Operation 1 July 2009

The directors anticipate that the adoption of these Standards and Interpretations as appropriate in future

periods will have no material impact on the financial statements of the Group when the relevant standards

come into effect for periods commencing after 1 January 2010.

Consolidated Financial Statements – Accounting Policies

30

SIGNIFICANT ACCOUNTING POLICIES

(1) Basis of accounting

The consolidated financial statements have been

prepared under the historical cost convention, as

modified by the revaluation of available-for-sale

investments and financial assets and liabilities

(including derivative instruments) at fair value

through profit and loss. The consolidated financial

statements have been prepared in accordance

with applicable International Financial Reporting

Standards as adopted by the European Union

(IFRS).

In preparing the consolidated financial statements

the Group has adopted the exemption in IFRS 1

not to restate business combinations prior to 1

December 2005.

The Group’s business activities, performance and

position are set out in the Chairman’s Statement

on pages 4 to 9 and an assessment of the risks

and uncertainties is set out in the Directors’ Report

on pages 14 to 17.

During the year the Group incurred a loss before

tax of £5.8m, although excluding non-recurring

exceptional costs and non-cash charges the

Group made a profit of £5.1m.

The Group had net current liabilities of £14.5m at

31 December 2009. This is due to the inclusion

in current liabilities of the borrowings under the

Group’s debt facilities, which were due to expire

on 31 December 2010, together with certain

earn out liabilities. Since the year end the Group

has entered into new debt facilities which total

£19.0m. £2.0m of these facilities are repayable

on 31 December 2010.

After reviewing the Group’s performance and

forecast future cashflows, the directors consider

the Group has adequate resources to continue in

operational existence for the foreseeable future.

The Group therefore continues to adopt the going

concern basis in preparing the Group’s Financial

Statements.

(2) Basis of consolidation

The Group’s financial statements consolidate the

financial statements of the Company and all of

its subsidiary undertakings. The results of subsidiary

undertakings acquired in the year are included in the

consolidated income statement from the effective

date of acquisition. On acquisition of a business all

of the assets and liabilities of that business that exist

at the date of acquisition are recorded at fair value.

Minority interests represent the portion of profit and or

loss and net assets in subsidiaries that is not held by