Embed Size (px)

Citation preview

CD Equisearch Pvt Ltd Feb 18, 2019

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

L.G.Balakrishnan & Brothers Ltd.

No. of shares (m) 31.4

Mkt cap (Rs crs/$m) 1213/170.2

Current price (Rs/$) 386/5.4

Price target (Rs/$) 544/7.6

52 W H/L (Rs.) 682/360

Book Value (Rs/$) 199/2.8

Beta 0.9

Daily volume (avg. monthly) 7070

P/BV (FY19e/20e) 1.9/1.7

EV/EBITDA (FY19e/20e) 5.8/4.9

P/E (FY19e/20e) 19.7/12.2/9.9

EPS growth (FY18/19e/20e) 21.9/16.4/22.9

OPM (FY18/19e/20e) 13.8/13.2/13.4

ROE (FY18/19e/20e) 16.3/16.7/17.9

ROCE(FY18/19e/20e) 14.5/15.2/16.7

D/E ratio (FY18/19e/20e) 0.2/0.2/0.1

BSE Code 500250

NSE Code LGBBROSLTD

Bloomberg LGBB IN

Reuters LGB.NS

Shareholding pattern %

Promoters 48.0

MFs / Banks / FIs 16.7

FPIs 0.6

Govt. Holding 0.0

Public & others 34.8

Total 100.0

As on Dec 31, 2018

Recommendation

BUY

Analyst

KISHAN GUPTA, CFA, FRM

Phone: + 91 (33) 4488 0043

E- mail: [email protected]

Consolidated (Rs crs)

FY16 FY17

FY18 FY19e FY20e

Income from operations 1205.30 1258.58 1418.00 1717.65 1985.86

Other Income 3.92 9.97 5.31 11.82 5.71

EBITDA (other income included) 141.60 171.90 200.86 238.32 271.40

Profit after MI & associate profit

63.37 69.94 85.28 99.31 122.03

EPS(Rs) 20.19 22.28 27.17 31.63 38.87

EPS growth (%) -3.9 10.4 21.9 16.4 22.9

Company Brief L G Balakrishnan (LGB) manufactures roller chains and undertakes metal

forming, including warm & cold forging, fine blanking and machined

parts.

Quarterly Highlights � Fortified by no smallish rise in revenues of metal forming business

(up 37.5%), overall revenues rose by a barely depressing 21.5% last

quarter. Belying historical trends, revenues of its flagship

transmission business has grown in high double digits for three

quarters in a row , galvanized by overall volume growth in excess of

20% in 9MFY19, thus reflecting gains in OEM market share.

Buoyancy in both fine products and machining business drove

recovery in metal forming business, whose revenues surge by a

gravity defying 32.4% in the first nine months of the current fiscal

compared to that in the same period a year ago.

� Margin stress in LGBs most distinguished transmission business

barely escaped attention in last two quarters (slid to 8.3% in Q3 from

9.9% in Q2), which unambiguously got reflected in its margins in

9MFY19 - 9.5% to 10.3% - thus eroding much of the volume gains

reported in dispatches to 2W OEMs. Yet metal forming business

margins hold up well , rising to all time high of 16% in Q2, before

normalizing in Q3 - still discernibly by over 300 bps in 9M to 12.3%.

� Near spectacular rise in post tax earnings in Q1 (nearly doubled then)

helped adjusted PAT - adjusted for exceptional gain of Rs 7.97 crs

arising from sale of land including to compulsory acquisition of land

of by Department of Highways - rose by 28% to Rs 73.15 crs compared

to Rs 57.17 crs in the nine months of the previous fiscal.

� The stock currently trades at 12.2x FY19e EPS of Rs 31.63 and 9.9x

FY20e EPS of Rs 38.87. Apart from higher capacities, the

commissioning of Chennai plant sometime early next fiscal would

strengthen its OEM engagement. Ample scope exists for capacity

ramp up at this plant as and when required. Amplified by modest

volume growth (in excess of 10% for both the bossiness) earnings are

projected to rise 16.4% on mid-teen growth in revenues. On balance

we maintain our buy rating on the stock with target of Rs 544

(previous target: Rs 662) based on 14x FY20e earnings.

2

2

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

[

Outlook & Recommendation

Two wheeler industry

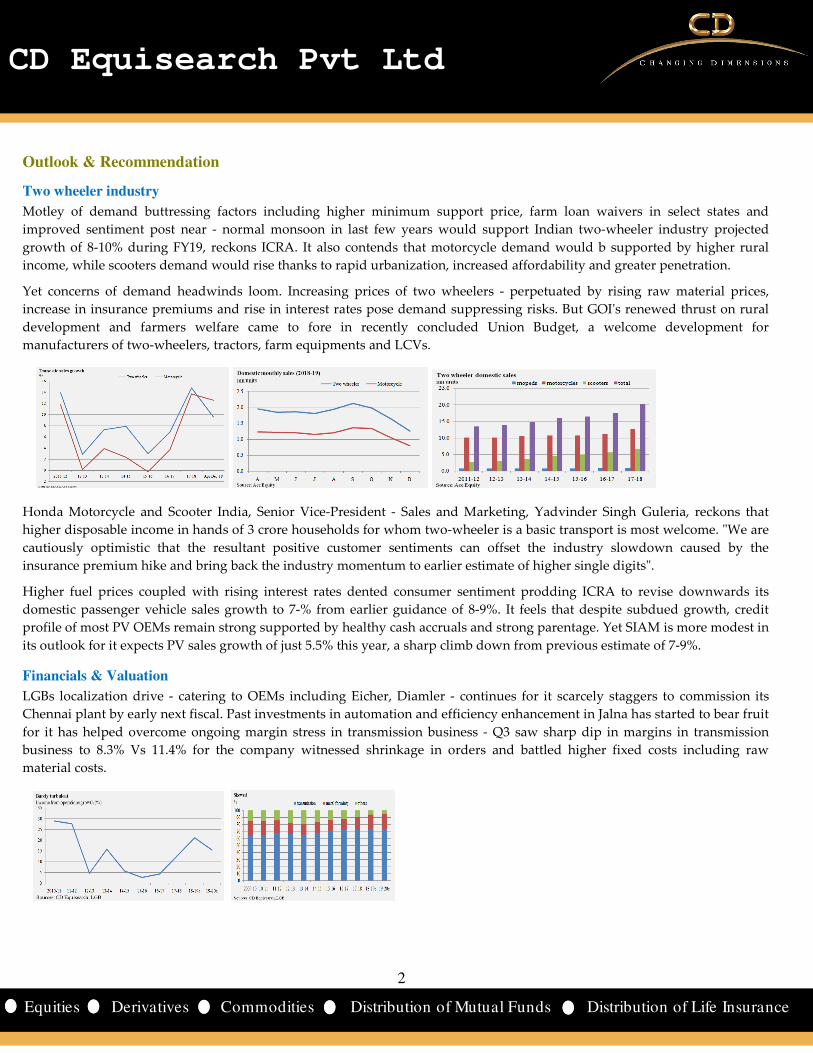

Motley of demand buttressing factors including higher minimum support price, farm loan waivers in select states and

improved sentiment post near - normal monsoon in last few years would support Indian two-wheeler industry projected

growth of 8-10% during FY19, reckons ICRA. It also contends that motorcycle demand would b supported by higher rural

income, while scooters demand would rise thanks to rapid urbanization, increased affordability and greater penetration.

Yet concerns of demand headwinds loom. Increasing prices of two wheelers - perpetuated by rising raw material prices,

increase in insurance premiums and rise in interest rates pose demand suppressing risks. But GOI's renewed thrust on rural

development and farmers welfare came to fore in recently concluded Union Budget, a welcome development for

manufacturers of two-wheelers, tractors, farm equipments and LCVs.

Honda Motorcycle and Scooter India, Senior Vice-President - Sales and Marketing, Yadvinder Singh Guleria, reckons that

higher disposable income in hands of 3 crore households for whom two-wheeler is a basic transport is most welcome. "We are

cautiously optimistic that the resultant positive customer sentiments can offset the industry slowdown caused by the

insurance premium hike and bring back the industry momentum to earlier estimate of higher single digits".

Higher fuel prices coupled with rising interest rates dented consumer sentiment prodding ICRA to revise downwards its

domestic passenger vehicle sales growth to 7-% from earlier guidance of 8-9%. It feels that despite subdued growth, credit

profile of most PV OEMs remain strong supported by healthy cash accruals and strong parentage. Yet SIAM is more modest in

its outlook for it expects PV sales growth of just 5.5% this year, a sharp climb down from previous estimate of 7-9%.

Financials & Valuation

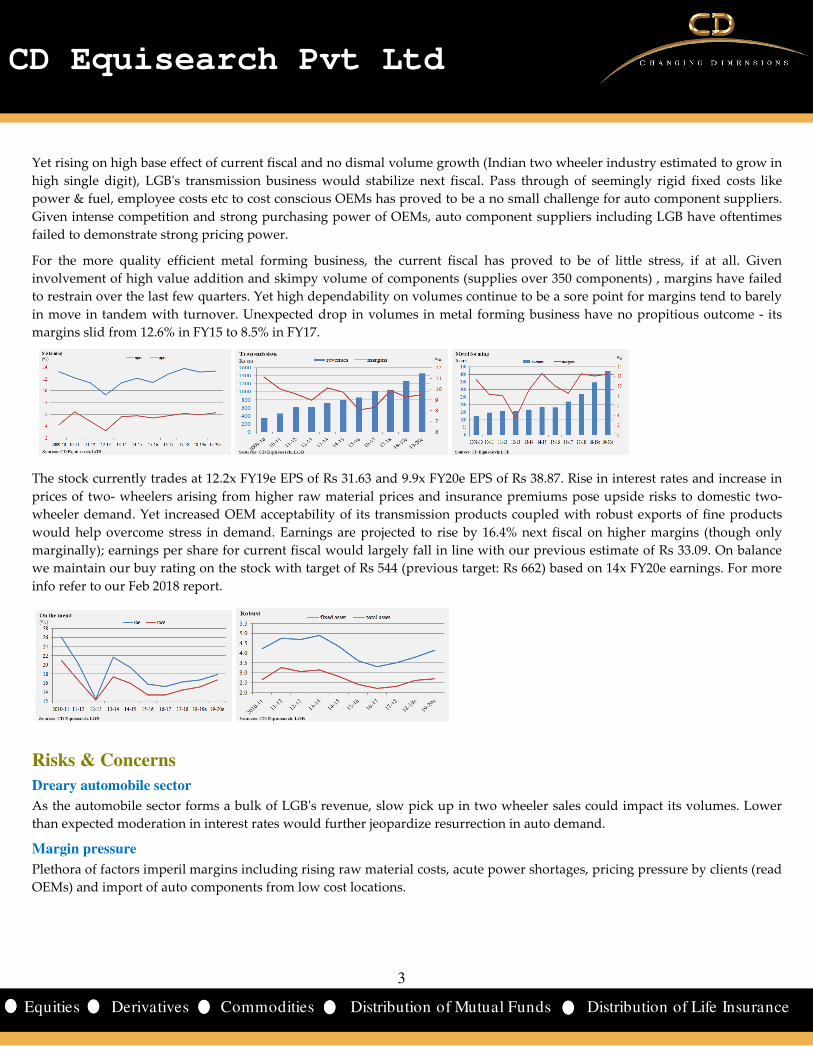

LGBs localization drive - catering to OEMs including Eicher, Diamler - continues for it scarcely staggers to commission its

Chennai plant by early next fiscal. Past investments in automation and efficiency enhancement in Jalna has started to bear fruit

for it has helped overcome ongoing margin stress in transmission business - Q3 saw sharp dip in margins in transmission

business to 8.3% Vs 11.4% for the company witnessed shrinkage in orders and battled higher fixed costs including raw

material costs.

3

3

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Yet rising on high base effect of current fiscal and no dismal volume growth (Indian two wheeler industry estimated to grow in

high single digit), LGB's transmission business would stabilize next fiscal. Pass through of seemingly rigid fixed costs like

power & fuel, employee costs etc to cost conscious OEMs has proved to be a no small challenge for auto component suppliers.

Given intense competition and strong purchasing power of OEMs, auto component suppliers including LGB have oftentimes

failed to demonstrate strong pricing power.

For the more quality efficient metal forming business, the current fiscal has proved to be of little stress, if at all. Given

involvement of high value addition and skimpy volume of components (supplies over 350 components) , margins have failed

to restrain over the last few quarters. Yet high dependability on volumes continue to be a sore point for margins tend to barely

in move in tandem with turnover. Unexpected drop in volumes in metal forming business have no propitious outcome - its

margins slid from 12.6% in FY15 to 8.5% in FY17.

The stock currently trades at 12.2x FY19e EPS of Rs 31.63 and 9.9x FY20e EPS of Rs 38.87. Rise in interest rates and increase in

prices of two- wheelers arising from higher raw material prices and insurance premiums pose upside risks to domestic two-

wheeler demand. Yet increased OEM acceptability of its transmission products coupled with robust exports of fine products

would help overcome stress in demand. Earnings are projected to rise by 16.4% next fiscal on higher margins (though only

marginally); earnings per share for current fiscal would largely fall in line with our previous estimate of Rs 33.09. On balance

we maintain our buy rating on the stock with target of Rs 544 (previous target: Rs 662) based on 14x FY20e earnings. For more

info refer to our Feb 2018 report.

Risks & Concerns

Dreary automobile sector

As the automobile sector forms a bulk of LGB's revenue, slow pick up in two wheeler sales could impact its volumes. Lower

than expected moderation in interest rates would further jeopardize resurrection in auto demand.

Margin pressure

Plethora of factors imperil margins including rising raw material costs, acute power shortages, pricing pressure by clients (read

OEMs) and import of auto components from low cost locations.

4

4

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Cross Sectional Analysis

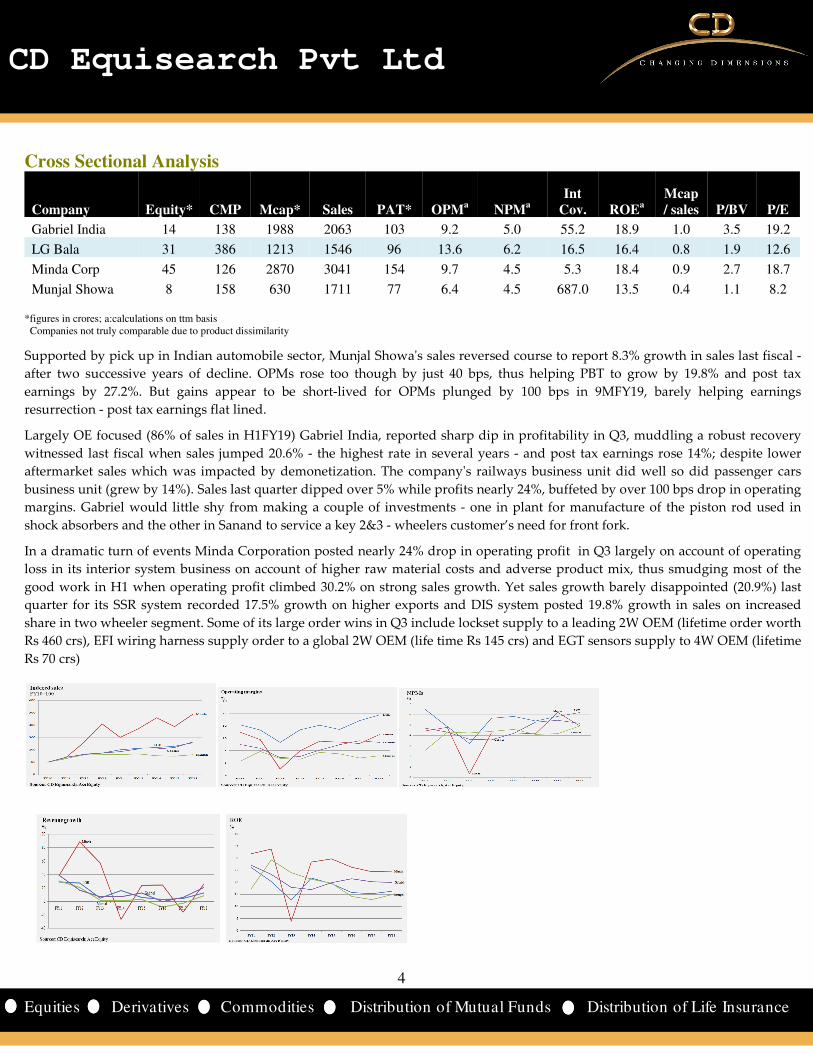

Company Equity* CMP Mcap* Sales PAT* OPMa NPMa Int

Cov. ROEa Mcap / sales P/BV P/E

Gabriel India 14 138 1988 2063 103 9.2 5.0 55.2 18.9 1.0 3.5 19.2

LG Bala 31 386 1213 1546 96 13.6 6.2 16.5 16.4 0.8 1.9 12.6

Minda Corp 45 126 2870 3041 154 9.7 4.5 5.3 18.4 0.9 2.7 18.7

Munjal Showa 8 158 630 1711 77 6.4 4.5 687.0 13.5 0.4 1.1 8.2 *figures in crores; a:calculations on ttm basis Companies not truly comparable due to product dissimilarity

Supported by pick up in Indian automobile sector, Munjal Showa's sales reversed course to report 8.3% growth in sales last fiscal -

after two successive years of decline. OPMs rose too though by just 40 bps, thus helping PBT to grow by 19.8% and post tax

earnings by 27.2%. But gains appear to be short-lived for OPMs plunged by 100 bps in 9MFY19, barely helping earnings

resurrection - post tax earnings flat lined.

Largely OE focused (86% of sales in H1FY19) Gabriel India, reported sharp dip in profitability in Q3, muddling a robust recovery

witnessed last fiscal when sales jumped 20.6% - the highest rate in several years - and post tax earnings rose 14%; despite lower

aftermarket sales which was impacted by demonetization. The company's railways business unit did well so did passenger cars

business unit (grew by 14%). Sales last quarter dipped over 5% while profits nearly 24%, buffeted by over 100 bps drop in operating

margins. Gabriel would little shy from making a couple of investments - one in plant for manufacture of the piston rod used in

shock absorbers and the other in Sanand to service a key 2&3 - wheelers customer’s need for front fork.

In a dramatic turn of events Minda Corporation posted nearly 24% drop in operating profit in Q3 largely on account of operating

loss in its interior system business on account of higher raw material costs and adverse product mix, thus smudging most of the

good work in H1 when operating profit climbed 30.2% on strong sales growth. Yet sales growth barely disappointed (20.9%) last

quarter for its SSR system recorded 17.5% growth on higher exports and DIS system posted 19.8% growth in sales on increased

share in two wheeler segment. Some of its large order wins in Q3 include lockset supply to a leading 2W OEM (lifetime order worth

Rs 460 crs), EFI wiring harness supply order to a global 2W OEM (life time Rs 145 crs) and EGT sensors supply to 4W OEM (lifetime

Rs 70 crs)

5

5

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Financials

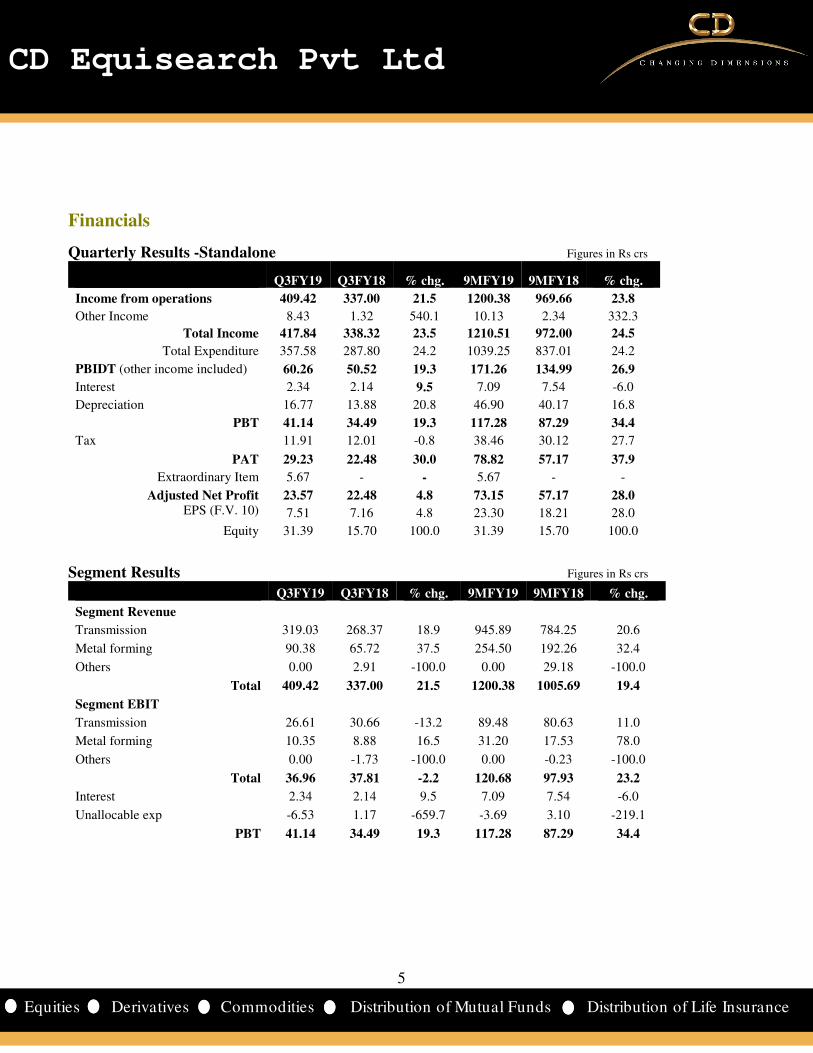

Quarterly Results -Standalone Figures in Rs crs

Q3FY19 Q3FY18 % chg. 9MFY19 9MFY18 % chg.

Income from operations 409.42 337.00 21.5 1200.38 969.66 23.8

Other Income 8.43 1.32 540.1 10.13 2.34 332.3

Total Income 417.84 338.32 23.5 1210.51 972.00 24.5

Total Expenditure 357.58 287.80 24.2 1039.25 837.01 24.2

PBIDT (other income included) 60.26 50.52 19.3 171.26 134.99 26.9

Interest 2.34 2.14 9.5 7.09 7.54 -6.0

Depreciation 16.77 13.88 20.8 46.90 40.17 16.8

PBT 41.14 34.49 19.3 117.28 87.29 34.4

Tax 11.91 12.01 -0.8 38.46 30.12 27.7

PAT 29.23 22.48 30.0 78.82 57.17 37.9

Extraordinary Item 5.67 - - 5.67 - -

Adjusted Net Profit 23.57 22.48 4.8 73.15 57.17 28.0 EPS (F.V. 10) 7.51 7.16 4.8 23.30 18.21 28.0

Equity 31.39 15.70 100.0 31.39 15.70 100.0

Segment Results Figures in Rs crs

Q3FY19 Q3FY18 % chg. 9MFY19 9MFY18 % chg.

Segment Revenue

Transmission 319.03 268.37 18.9 945.89 784.25 20.6

Metal forming 90.38 65.72 37.5 254.50 192.26 32.4

Others 0.00 2.91 -100.0 0.00 29.18 -100.0

Total 409.42 337.00 21.5 1200.38 1005.69 19.4

Segment EBIT

Transmission 26.61 30.66 -13.2 89.48 80.63 11.0

Metal forming 10.35 8.88 16.5 31.20 17.53 78.0

Others 0.00 -1.73 -100.0 0.00 -0.23 -100.0

Total 36.96 37.81 -2.2 120.68 97.93 23.2

Interest 2.34 2.14 9.5 7.09 7.54 -6.0

Unallocable exp -6.53 1.17 -659.7 -3.69 3.10 -219.1

PBT 41.14 34.49 19.3 117.28 87.29 34.4

6

6

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Financials

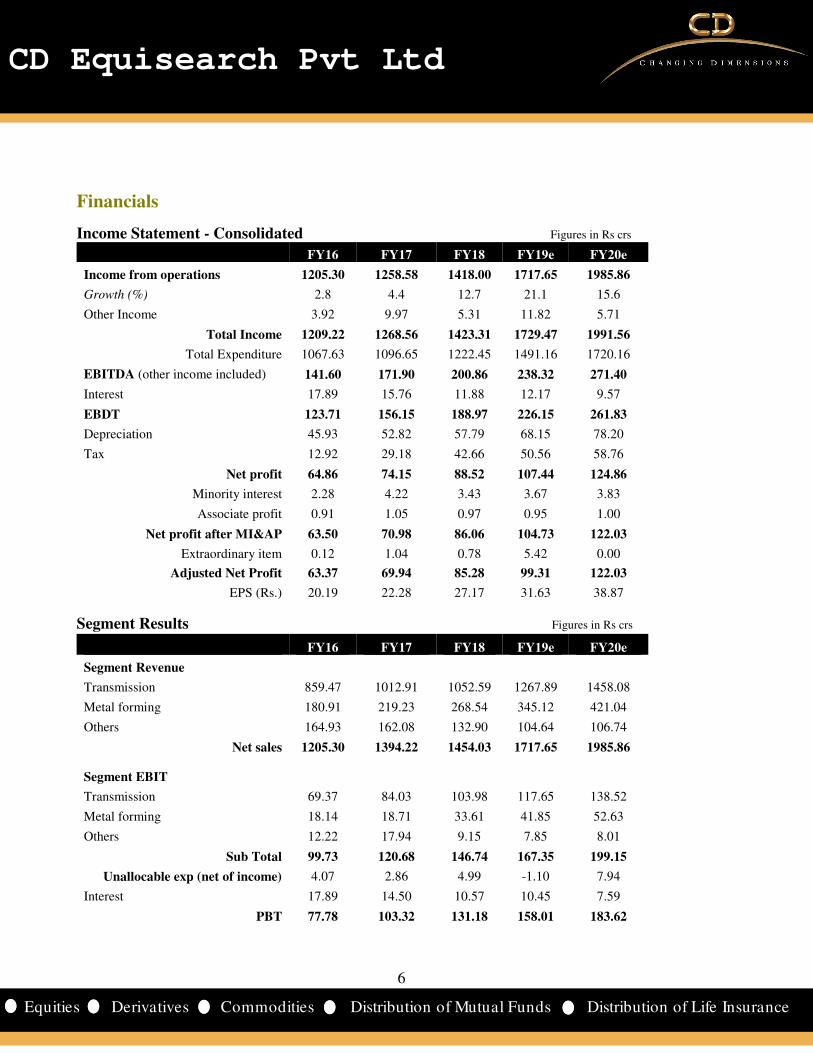

Income Statement - Consolidated Figures in Rs crs

FY16 FY17 FY18 FY19e FY20e

Income from operations 1205.30 1258.58 1418.00 1717.65 1985.86

Growth (%) 2.8 4.4 12.7 21.1 15.6

Other Income 3.92 9.97 5.31 11.82 5.71

Total Income 1209.22 1268.56 1423.31 1729.47 1991.56

Total Expenditure 1067.63 1096.65 1222.45 1491.16 1720.16

EBITDA (other income included) 141.60 171.90 200.86 238.32 271.40

Interest 17.89 15.76 11.88 12.17 9.57

EBDT 123.71 156.15 188.97 226.15 261.83

Depreciation 45.93 52.82 57.79 68.15 78.20

Tax 12.92 29.18 42.66 50.56 58.76

Net profit 64.86 74.15 88.52 107.44 124.86

Minority interest 2.28 4.22 3.43 3.67 3.83

Associate profit 0.91 1.05 0.97 0.95 1.00

Net profit after MI&AP 63.50 70.98 86.06 104.73 122.03

Extraordinary item 0.12 1.04 0.78 5.42 0.00

Adjusted Net Profit 63.37 69.94 85.28 99.31 122.03

EPS (Rs.) 20.19 22.28 27.17 31.63 38.87

Segment Results Figures in Rs crs

FY16 FY17 FY18 FY19e FY20e

Segment Revenue

Transmission 859.47 1012.91 1052.59 1267.89 1458.08

Metal forming 180.91 219.23 268.54 345.12 421.04

Others 164.93 162.08 132.90 104.64 106.74

Net sales 1205.30 1394.22 1454.03 1717.65 1985.86 Segment EBIT

Transmission 69.37 84.03 103.98 117.65 138.52

Metal forming 18.14 18.71 33.61 41.85 52.63

Others 12.22 17.94 9.15 7.85 8.01

Sub Total 99.73 120.68 146.74 167.35 199.15

Unallocable exp (net of income) 4.07 2.86 4.99 -1.10 7.94

Interest 17.89 14.50 10.57 10.45 7.59

PBT 77.78 103.32 131.18 158.01 183.62

7

7

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

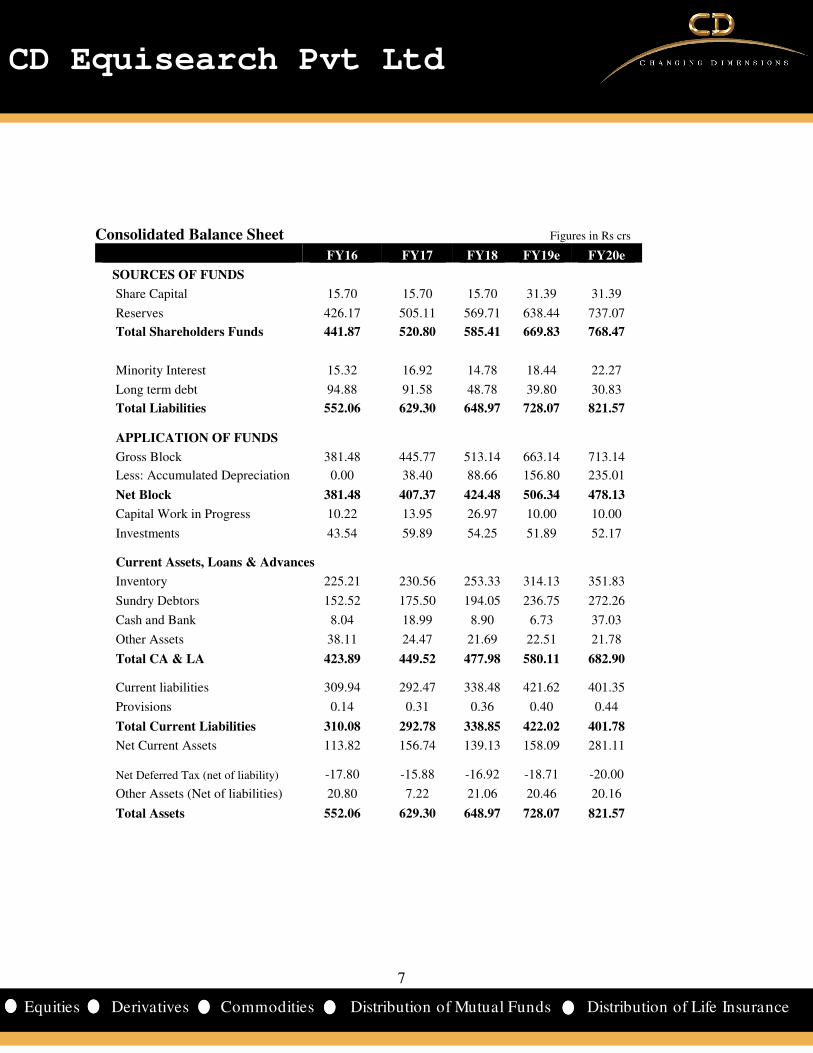

Consolidated Balance Sheet Figures in Rs crs

FY16 FY17 FY18 FY19e FY20e

SOURCES OF FUNDS

Share Capital 15.70 15.70 15.70 31.39 31.39

Reserves 426.17 505.11 569.71 638.44 737.07

Total Shareholders Funds 441.87 520.80 585.41 669.83 768.47

Minority Interest 15.32 16.92 14.78 18.44 22.27

Long term debt 94.88 91.58 48.78 39.80 30.83

Total Liabilities 552.06 629.30 648.97 728.07 821.57

APPLICATION OF FUNDS

Gross Block 381.48 445.77 513.14 663.14 713.14

Less: Accumulated Depreciation 0.00 38.40 88.66 156.80 235.01

Net Block 381.48 407.37 424.48 506.34 478.13

Capital Work in Progress 10.22 13.95 26.97 10.00 10.00

Investments 43.54 59.89 54.25 51.89 52.17

Current Assets, Loans & Advances

Inventory 225.21 230.56 253.33 314.13 351.83 Sundry Debtors 152.52 175.50 194.05 236.75 272.26 Cash and Bank 8.04 18.99 8.90 6.73 37.03 Other Assets 38.11 24.47 21.69 22.51 21.78 Total CA & LA 423.89 449.52 477.98 580.11 682.90

Current liabilities 309.94 292.47 338.48 421.62 401.35 Provisions 0.14 0.31 0.36 0.40 0.44 Total Current Liabilities 310.08 292.78 338.85 422.02 401.78 Net Current Assets 113.82 156.74 139.13 158.09 281.11

Net Deferred Tax (net of liability) -17.80 -15.88 -16.92 -18.71 -20.00 Other Assets (Net of liabilities) 20.80 7.22 21.06 20.46 20.16 Total Assets 552.06 629.30 648.97 728.07 821.57

8

8

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

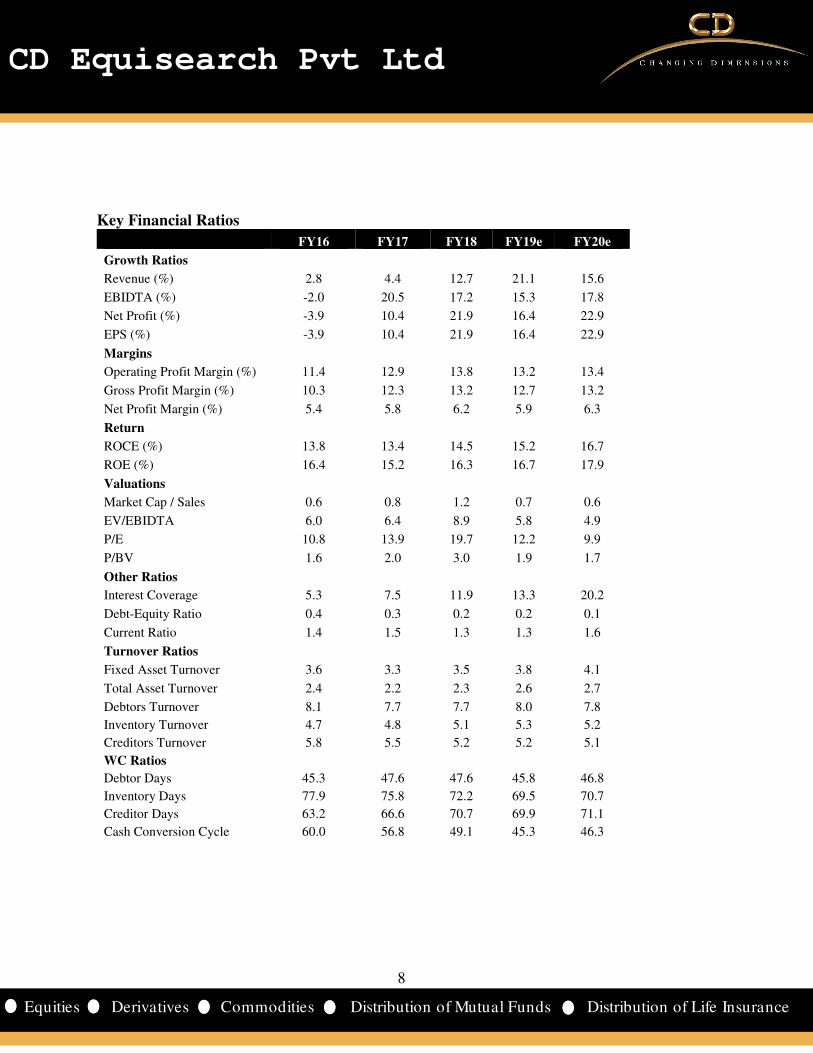

Key Financial Ratios

FY16 FY17 FY18 FY19e FY20e

Growth Ratios

Revenue (%) 2.8 4.4 12.7 21.1 15.6

EBIDTA (%) -2.0 20.5 17.2 15.3 17.8

Net Profit (%) -3.9 10.4 21.9 16.4 22.9

EPS (%) -3.9 10.4 21.9 16.4 22.9

Margins

Operating Profit Margin (%) 11.4 12.9 13.8 13.2 13.4

Gross Profit Margin (%) 10.3 12.3 13.2 12.7 13.2

Net Profit Margin (%) 5.4 5.8 6.2 5.9 6.3

Return

ROCE (%) 13.8 13.4 14.5 15.2 16.7

ROE (%) 16.4 15.2 16.3 16.7 17.9

Valuations

Market Cap / Sales 0.6 0.8 1.2 0.7 0.6

EV/EBIDTA 6.0 6.4 8.9 5.8 4.9

P/E 10.8 13.9 19.7 12.2 9.9

P/BV 1.6 2.0 3.0 1.9 1.7

Other Ratios

Interest Coverage 5.3 7.5 11.9 13.3 20.2

Debt-Equity Ratio 0.4 0.3 0.2 0.2 0.1

Current Ratio 1.4 1.5 1.3 1.3 1.6

Turnover Ratios

Fixed Asset Turnover 3.6 3.3 3.5 3.8 4.1

Total Asset Turnover 2.4 2.2 2.3 2.6 2.7

Debtors Turnover 8.1 7.7 7.7 8.0 7.8

Inventory Turnover 4.7 4.8 5.1 5.3 5.2

Creditors Turnover 5.8 5.5 5.2 5.2 5.1

WC Ratios

Debtor Days 45.3 47.6 47.6 45.8 46.8

Inventory Days 77.9 75.8 72.2 69.5 70.7

Creditor Days 63.2 66.6 70.7 69.9 71.1

Cash Conversion Cycle 60.0 56.8 49.1 45.3 46.3

9

9

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

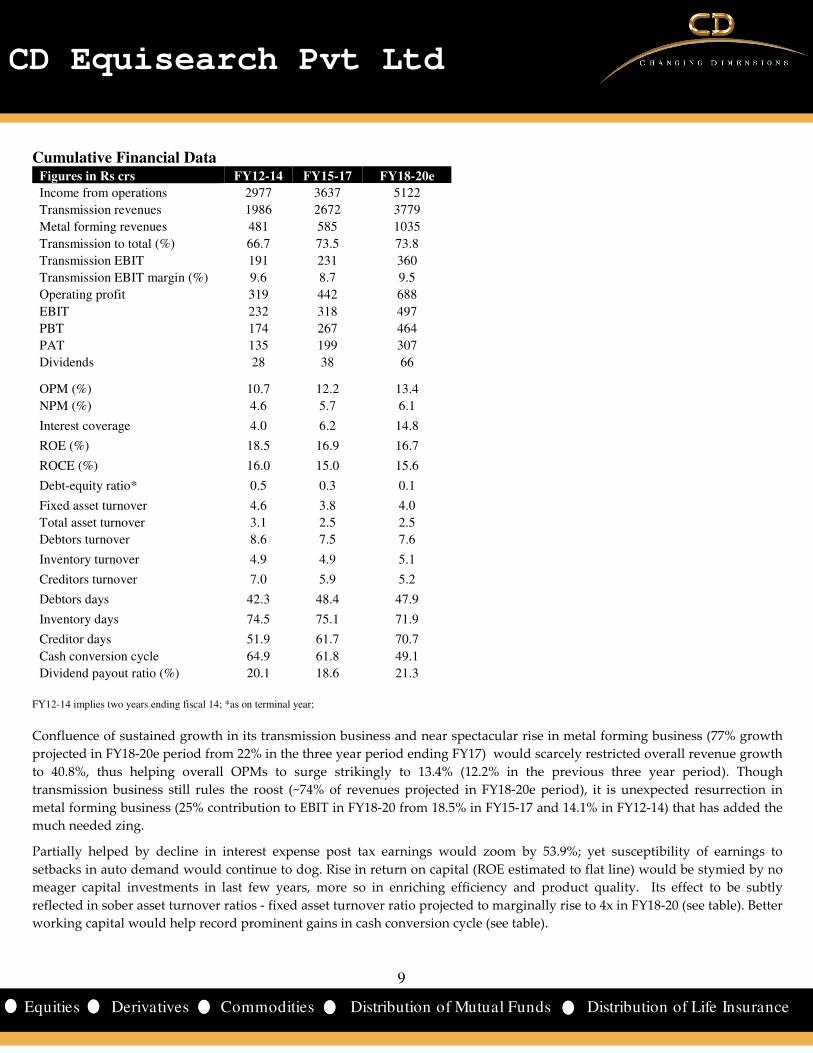

Cumulative Financial Data Figures in Rs crs FY12-14 FY15-17 FY18-20e

Income from operations 2977 3637 5122

Transmission revenues 1986 2672 3779

Metal forming revenues 481 585 1035

Transmission to total (%) 66.7 73.5 73.8

Transmission EBIT 191 231 360

Transmission EBIT margin (%) 9.6 8.7 9.5

Operating profit 319 442 688

EBIT 232 318 497

PBT 174 267 464

PAT 135 199 307

Dividends 28 38 66 OPM (%) 10.7 12.2 13.4

NPM (%) 4.6 5.7 6.1

Interest coverage 4.0 6.2 14.8

ROE (%) 18.5 16.9 16.7

ROCE (%) 16.0 15.0 15.6

Debt-equity ratio* 0.5 0.3 0.1

Fixed asset turnover 4.6 3.8 4.0

Total asset turnover 3.1 2.5 2.5

Debtors turnover 8.6 7.5 7.6

Inventory turnover 4.9 4.9 5.1

Creditors turnover 7.0 5.9 5.2

Debtors days 42.3 48.4 47.9

Inventory days 74.5 75.1 71.9

Creditor days 51.9 61.7 70.7

Cash conversion cycle 64.9 61.8 49.1

Dividend payout ratio (%) 20.1 18.6 21.3

FY12-14 implies two years ending fiscal 14; *as on terminal year;

Confluence of sustained growth in its transmission business and near spectacular rise in metal forming business (77% growth

projected in FY18-20e period from 22% in the three year period ending FY17) would scarcely restricted overall revenue growth

to 40.8%, thus helping overall OPMs to surge strikingly to 13.4% (12.2% in the previous three year period). Though

transmission business still rules the roost (~74% of revenues projected in FY18-20e period), it is unexpected resurrection in

metal forming business (25% contribution to EBIT in FY18-20 from 18.5% in FY15-17 and 14.1% in FY12-14) that has added the

much needed zing.

Partially helped by decline in interest expense post tax earnings would zoom by 53.9%; yet susceptibility of earnings to

setbacks in auto demand would continue to dog. Rise in return on capital (ROE estimated to flat line) would be stymied by no

meager capital investments in last few years, more so in enriching efficiency and product quality. Its effect to be subtly

reflected in sober asset turnover ratios - fixed asset turnover ratio projected to marginally rise to 4x in FY18-20 (see table). Better

working capital would help record prominent gains in cash conversion cycle (see table).

10

10

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

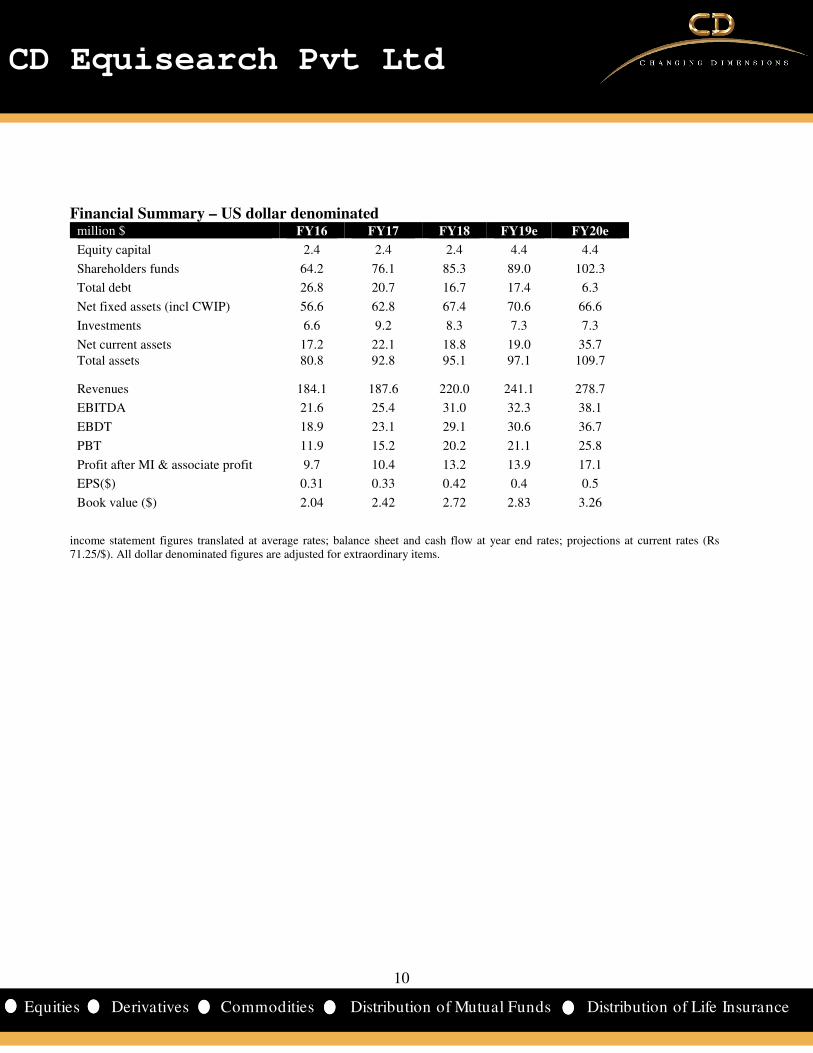

Financial Summary – US dollar denominated million $ FY16 FY17 FY18 FY19e FY20e

Equity capital 2.4 2.4 2.4 4.4 4.4

Shareholders funds 64.2 76.1 85.3 89.0 102.3

Total debt 26.8 20.7 16.7 17.4 6.3

Net fixed assets (incl CWIP) 56.6 62.8 67.4 70.6 66.6

Investments 6.6 9.2 8.3 7.3 7.3

Net current assets 17.2 22.1 18.8 19.0 35.7

Total assets 80.8 92.8 95.1 97.1 109.7

Revenues 184.1 187.6 220.0 241.1 278.7

EBITDA 21.6 25.4 31.0 32.3 38.1

EBDT 18.9 23.1 29.1 30.6 36.7

PBT 11.9 15.2 20.2 21.1 25.8

Profit after MI & associate profit 9.7 10.4 13.2 13.9 17.1

EPS($) 0.31 0.33 0.42 0.4 0.5

Book value ($) 2.04 2.42 2.72 2.83 3.26

income statement figures translated at average rates; balance sheet and cash flow at year end rates; projections at current rates (Rs 71.25/$). All dollar denominated figures are adjusted for extraordinary items.

11

11

CD Equisearch Pvt Ltd

Equities Derivatives Commodities Distribution of Mutual Funds Distribution of Life Insurance

Disclosure& Disclaimer CD Equisearch Private Limited (hereinafter referred to as ‘CD Equi’) is a Member registered with National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited (Formerly known as MCX Stock Exchange Limited). CD

Equi is also registered as Depository Participant with CDSL and AMFI registered Mutual Fund Advisor. The associates of CD Equi are

engaged in activities relating to NBFC-ND - Financing and Investment, Commodity Broking, Real Estate, etc.

CD Equi is registered under SEBI (Research Analysts) Regulations, 2014 with SEBI Registration no INH300002274. Further, CD Equi hereby

declares that –

• No disciplinary action has been taken against CD Equi by any of the regulatory authorities.

• CD Equi/its associates/research analysts do not have any financial interest/beneficial interest of more than one percent/material

conflict of interest in the subject company(s) (kindly disclose if otherwise).

• CD Equi/its associates/research analysts have not received any compensation from the subject company(s) during the past twelve

months.

• CD Equi/its research analysts has not served as an officer, director or employee of company covered by analysts and has not been

engaged in market making activity of the company covered by analysts.

This document is solely for the personal information of the recipient and must not be singularly used as the basis of any investment decision.

Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such

investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in

this document (including the merits and risks involved) and should consult their own advisors to determine the merits and risks of such an

investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading

volume, as opposed to focusing on a company's fundamentals and as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general

guidance only. CD Equi or any of its affiliates/group companies shall not be in any way responsible for any loss or damage that may arise to

any person from any inadvertent error in the information contained in this report. CD Equi has not independently verified all the information

contained within this document. Accordingly, we cannot testify nor make any representation or warranty, express or implied, to the accuracy,

contents or data contained within this document.

While, CD Equi endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory compliance or

other reasons that prevent us from doing so.

This document is being supplied to you solely for your information and its contents, information or data may not be reproduced, redistributed

or passed on, directly or indirectly. Neither, CD Equi nor its directors, employees or affiliates shall be liable for any loss or damage that may

arise from or in connection with the use of this information.

CD Equisearch Private Limited (CIN: U67120WB1995PTC071521)

Registered Office: 37, Shakespeare Sarani, 3rd Floor, Kolkata – 700 017; Phone: +91(33) 4488 0000; Fax: +91(33) 2289 2557 Corporate Office: 10,

Vasawani Mansion, 5th Floor, Dinshaw Wachha Road, Churchgate, Mumbai – 400 020. Phone: +91(22) 2283 0652/0653; Fax: +91(22) 2283, 2276

Website: www.cdequi.com; Email: [email protected]

buy: >20% accumulate: >10% to ≤20% hold: ≥-10% to ≤10% reduce: ≥-20% to <-10% sell: <-20%

Exchange Rates Used- Indicative

Rs/$ FY14 FY15 FY16 FY17 FY18

Average 60.5 61.15 65.46 67.09 64.45

Year end 60.1 62.59 66.33 64.84 65.04

All $ values mentioned in the write-up translated at the average rate of the respective quarter/ year as applicable. Projections converted at

current exchange rate. Cumulative dollar figure is the sum of respective yearly dollar value.