Embed Size (px)

Citation preview

BERENBERG EQUITY RESEARCH

Catalysts and metal recycling

Expectations are too high

Evgenia Molotova

Analyst

+44 20 3465 2664

Jaideep Pandya

Analyst

+44 20 3207 7890

John Klein

Analyst

+44 20 3207 7930

15 July 2013

Chemicals

Catalysts and metal recycling Chemicals

For our disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) and our disclaimer please see the end of this document. Please note that the use of this research report is subject to the conditions and restrictions set forth in the disclosures and the disclaimer at the end of this document.

Catalysts and metal recycling Chemicals

Table of contents

Catalysts and metal recycling: expectations are too high 4

Executive summary 5

Porter’s five forces analysis 8

Catalysts 10

Recycling 53

Umicore: Recycling at risk 85

Umicore: investment thesis 87

Valuation 126

Umicore: company overview 127

Financials 131

Johnson Matthey: Near-term expectations too high 135

Johnson Matthey: investment thesis 137

Johnson Matthey: company overview 156

Valuation 158

Financials 160

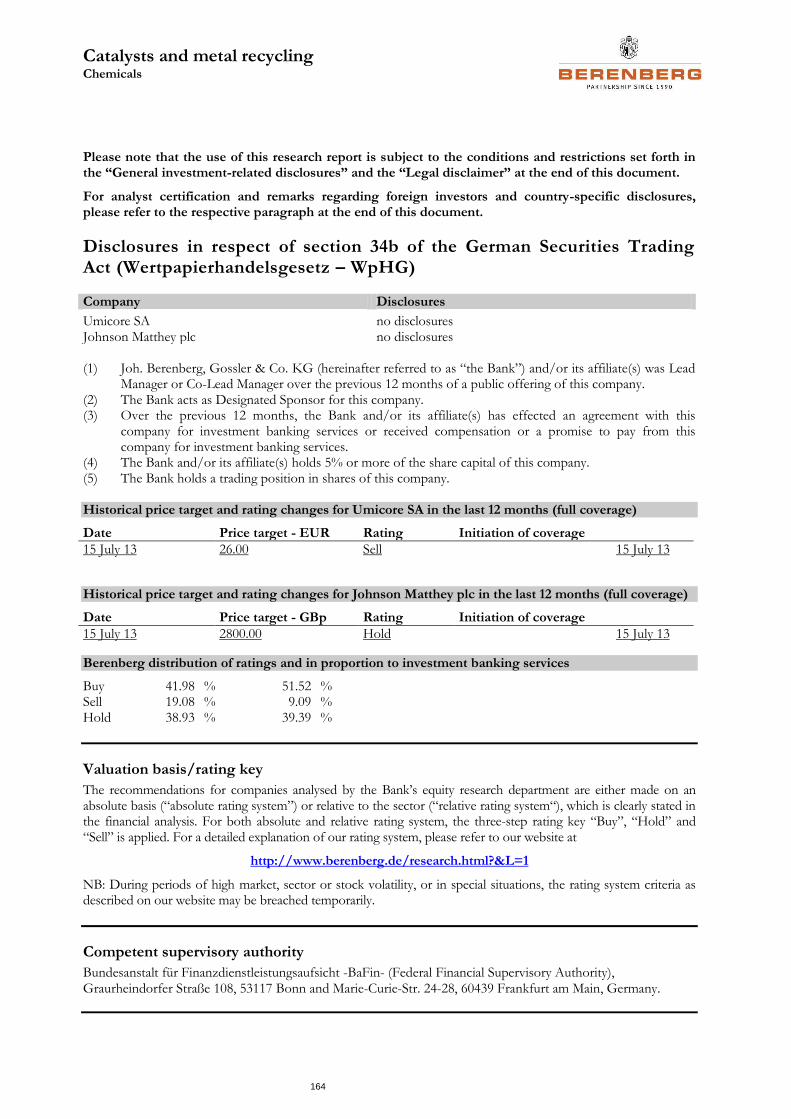

Disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) 164

Contacts: Investment Banking 167

Catalysts and metal recycling Chemicals

4

Expectations are too high

● With this note, we initiate coverage of Johnson Matthey and Umicore. We rate Johnson Matthey Hold with a price target of £28.00/share and Umicore Sell with a price target of €26/share.

● We have conducted an in-depth, bottom-up analysis of two industries: metal recycling, and automotive and process catalysts. We think that in both industries the market tends to rely on the forecasts of the main players and lacks visibility on key industry drivers, the stakeholders involved in the process and the risks associated with the industry. Medium-term, we are more positive on the prospects of the catalysts industry than we are on the recycling industry. Short-term, we have concerns for both industries.

● Johnson Matthey is the leading company in the area of automotive catalysts; it also has precious metals recycling and production capabilities. We think that in the long term Johnson Matthey is well positioned within the majority of the industries in which it is present; however, in the short term we see some risks to consensus numbers.

● In automotive catalysts, we think that the market is overestimating the effect of Euro VI legislation on the catalyst value per vehicle. We also think that the Chinese heavy-duty diesel (HDD) catalyst market will develop more slowly than consensus expects. Finally, short-term pre-buying of Euro V trucks ahead of Euro VI implementation could slow the penetration of Euro VI in 2013-14.

● Our expectations for Johnson Matthey’s Precious Metal Products division are also below consensus. The loss of the Anglo Platinum distribution contract will result in a £35m loss of EBIT. In our view, the market seems to believe that a similar contract can be signed with another precious metals producer, which will restore divisional profitability to the level of 2011. We view this as unrealistic.

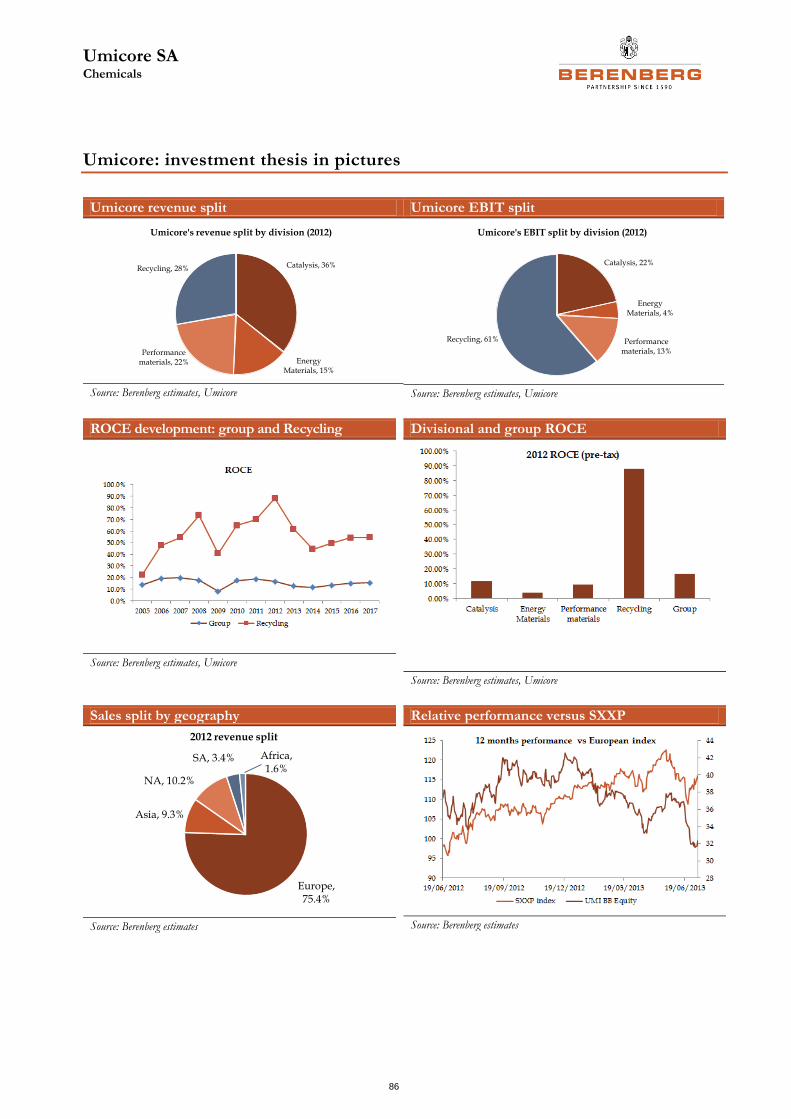

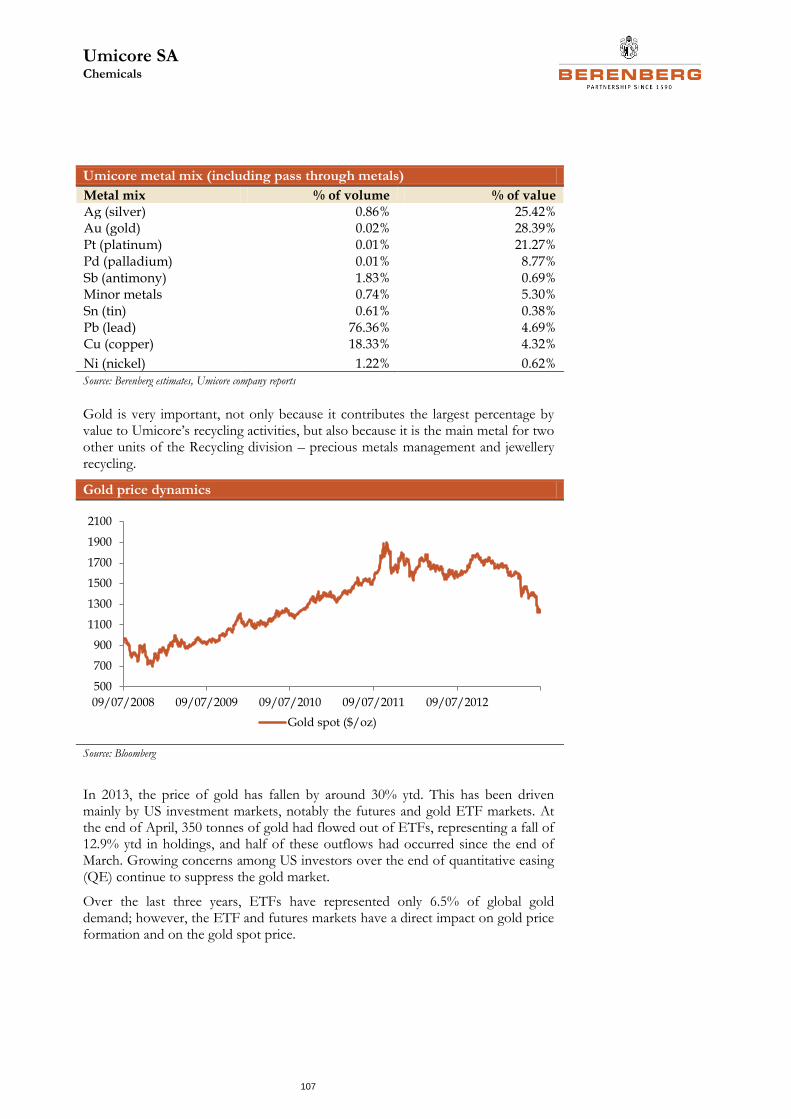

● Umicore is one of the leading companies in the areas of recycling and automotive catalysts. It has unique technical capabilities that allow it to recycle various feedstock streams and recover up to 20 metals. The recent underperformance of the stock reflects, in our view, market concerns about the short-term performance of the largest division – Recycling (c61% of group EBIT in 2012) – due to declining precious metal prices. We expect the competitive dynamics of the recycling industry to deteriorate significantly in the medium term.

● We expect a decrease in the availability of key recycling feedstocks: electronic scrap (e-scrap) and industrial residues. Contrary to market expectations, we do not expect e-scrap availability to increase in the medium term. On the other hand, recent capacity additions in e-scrap treatment have led to significant overcapacity in the market. Industrial residues – PGM-containing slimes of base metals (copper, lead, zinc) – were historically treated by Umicore. Recently, however, a number of metal refiners have invested in their own capacities. For instance, we believe the termination of the company’s supply agreement with Aurubis might lead to around a 10% fall in Umicore’s gold output. The company’s other divisions will not be able to compensate for the deterioration in Recycling.

● We are 9% below Bloomberg consensus for Johnson Matthey’s 2013 EPS and 12% below consensus for 2014 EPS. We are 8% below consensus for Umicore’s 2013 EPS; for 2014 we are 24% below consensus.

Umicore SA

Sell (initiation) Current price

EUR 33.26 Price target

EUR 26.00 11/07/2013 Brussels Close

Johnson Matthey plc

Hold (initiation) Current price

GBp 2,807 Price target

GBp 2,800 11/07/2013 London Close

Rating system: Absolute

15 July 2013

Evgenia Molotova Analyst +44 20 3465 2664 [email protected]

Jaideep Pandya Analyst +44 20 3207 7890 [email protected]

John Klein Analyst +44 20 3207 7930 [email protected]

Catalysts and metal recycling Chemicals

5

Executive summary

In this note, we analyse two industries in detail: catalysts (process and automotive) and metal recycling.

We think that in both industries the market tends to rely on the forecasts of the main players and lacks visibility on key industry drivers, the stakeholders involved in the process and the risks associated with the industry.

The process catalysts market is driven mostly by growth in the underlying customer industries. We have examined key trends in the refining, hydrogen, ammonia, methanol and alternative fuels industries in order to determine medium-term growth rates for process catalysts.

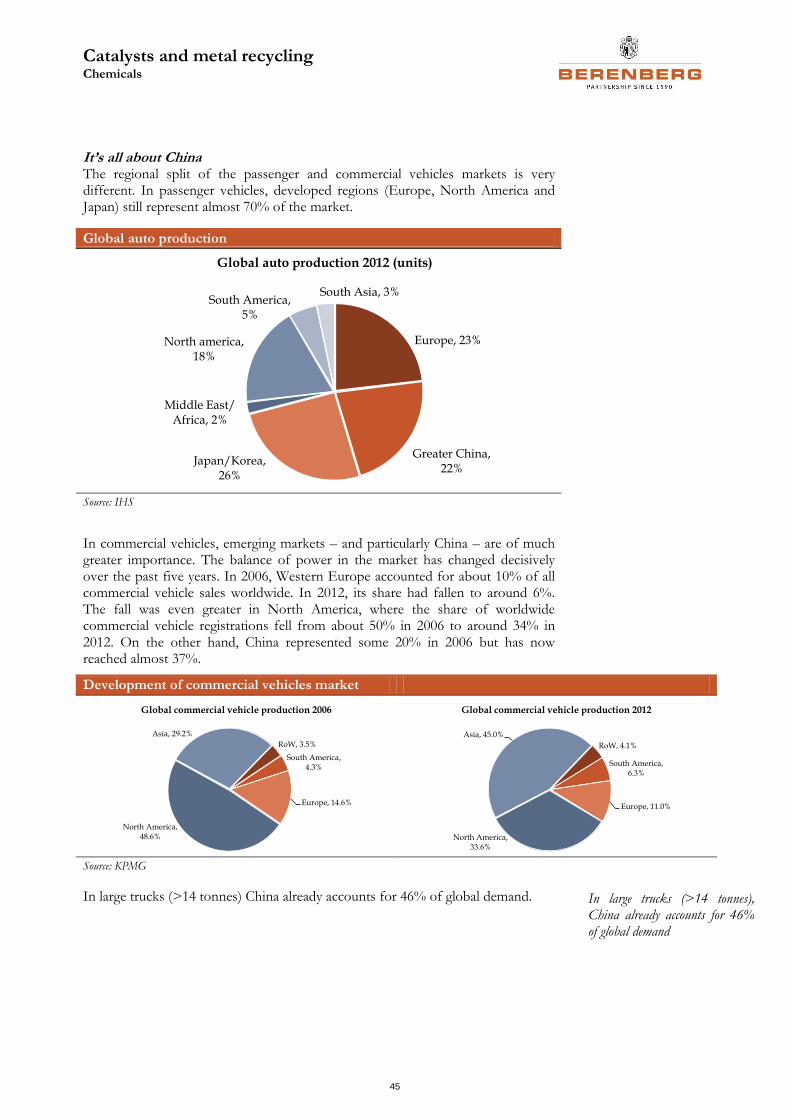

Legislative changes are driving industry growth in automotive catalysts. We have made a detailed analysis of future legislative changes globally and determined which catalytic technology is required to implement these changes. We also looked at how these technologies are translating into monetary value per vehicle. Lastly, we assessed the relationship between global automotive players and catalyst producers by determining key catalyst suppliers for each leading OEM producer in both passenger and commercial vehicles. Based on the market shares of auto manufacturers in different parts of the world, we estimated the market shares of leading catalyst producers in each region. This analysis allowed us to develop a more critical view on the prospects for both revenues and profits in the automotive catalyst industry.

The metal recycling universe within the chemicals sector is limited to two companies – Johnson Matthey and Umicore – and we believe financial markets tend to underestimate the industry’s complexity. We looked at the whole chain of different feedstock streams, from e-scrap to residues from metal refiners, and reached conclusions which differ substantially from current market perceptions. We think that the market underestimates capital intensity, competitive rivalry and supply dynamics; and we believe the fundamentals of the metal recycling industry will deteriorate in the medium term.

Process catalysts

The process catalysts segment is growing substantially faster than the underlying industries due to constant innovation, which helps client companies save money and allows catalyst companies to charge a premium for their products. Contrary to market perception, specialty process catalyst companies generate higher margins than automotive catalyst companies. For instance, we expect that Johnson Matthey’s process catalysts division will remain one of the key drivers of the company’s profitability.

Automotive catalysts market

We are more critical than the market regarding the future fundamentals of the automotive catalysts industry.

In light-duty vehicles (LDV), catalyst technology is mature. The market is highly consolidated, with three key players (BASF, Johnson Matthey and Umicore) controlling c90% of the total available market. Substantial revenue growth or a shift in market shares is only possible if there are legislative changes or if one of the players comes up with new, disruptive technology. We expect the European LDV catalyst market to increase in value by 2-2.3x within the next two years due to the introduction of the Euro VI standard. Thereafter, we expect growth to slow.

Catalysts and metal recycling Chemicals

6

As there are no considerable legislative changes in LDV until 2015, we expect average annual market growth to be 5-5.5%, still higher than global auto production growth. The maturity of the market in developed countries and the slowdown in legislative changes (as emissions control in these regions is already at a very high level) could lead to an erosion of catalyst producers’ pricing power.

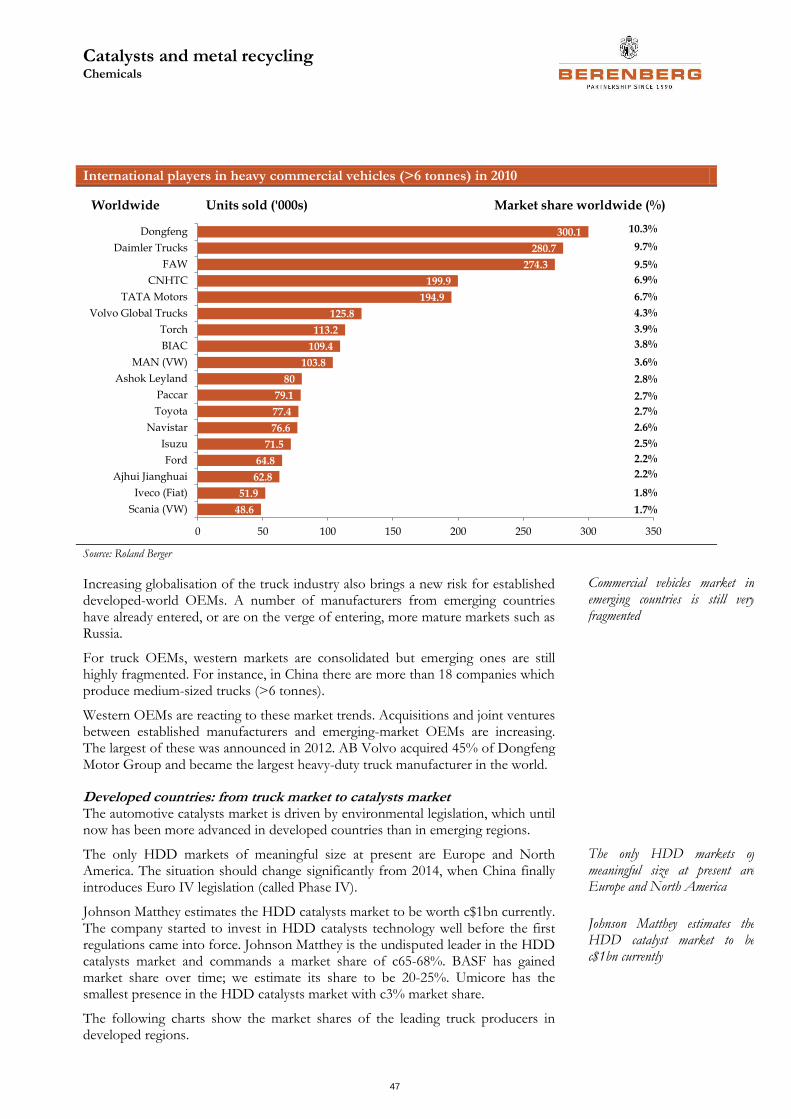

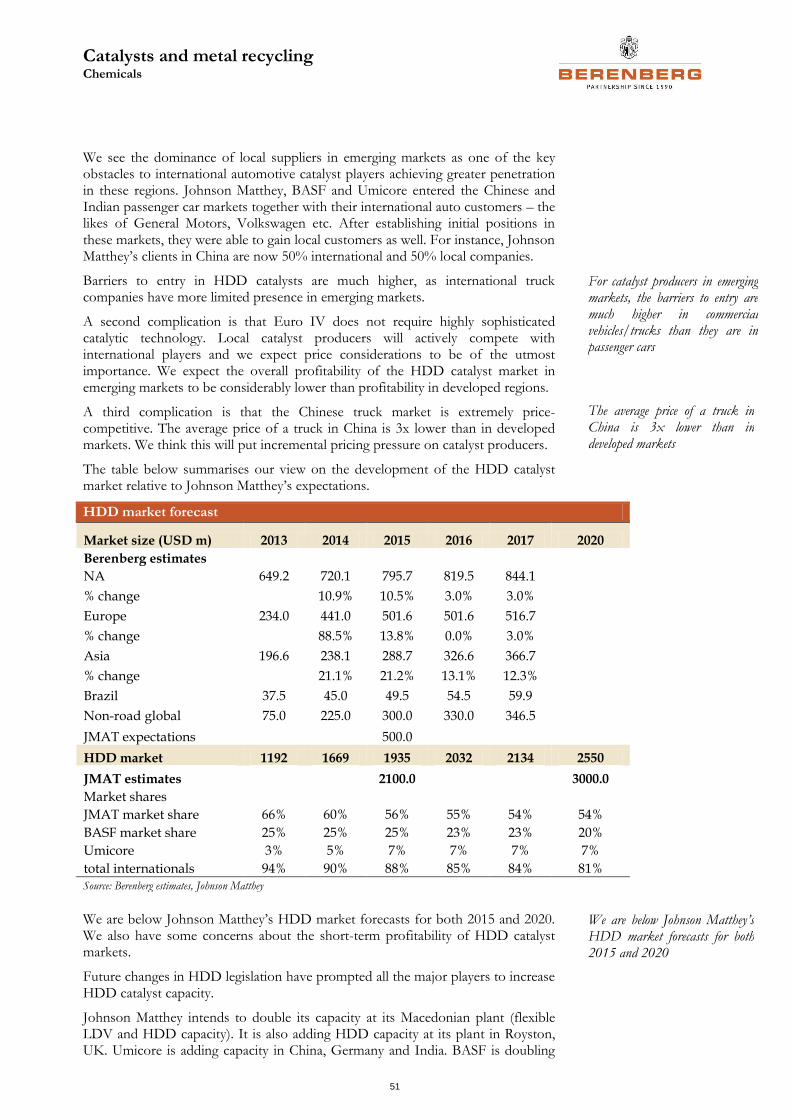

Less than a decade ago, the HDD catalyst market did not exist, but it is now growing very rapidly, driven mostly by the legislative changes discussed above. Johnson Matthey forecasts the HDD catalyst market to reach $2.1bn by 2015 and $3bn by 2020. We are more cautious and expect the HDD catalyst market to reach $1.9bn by 2015 and $2.5bn by 2020.

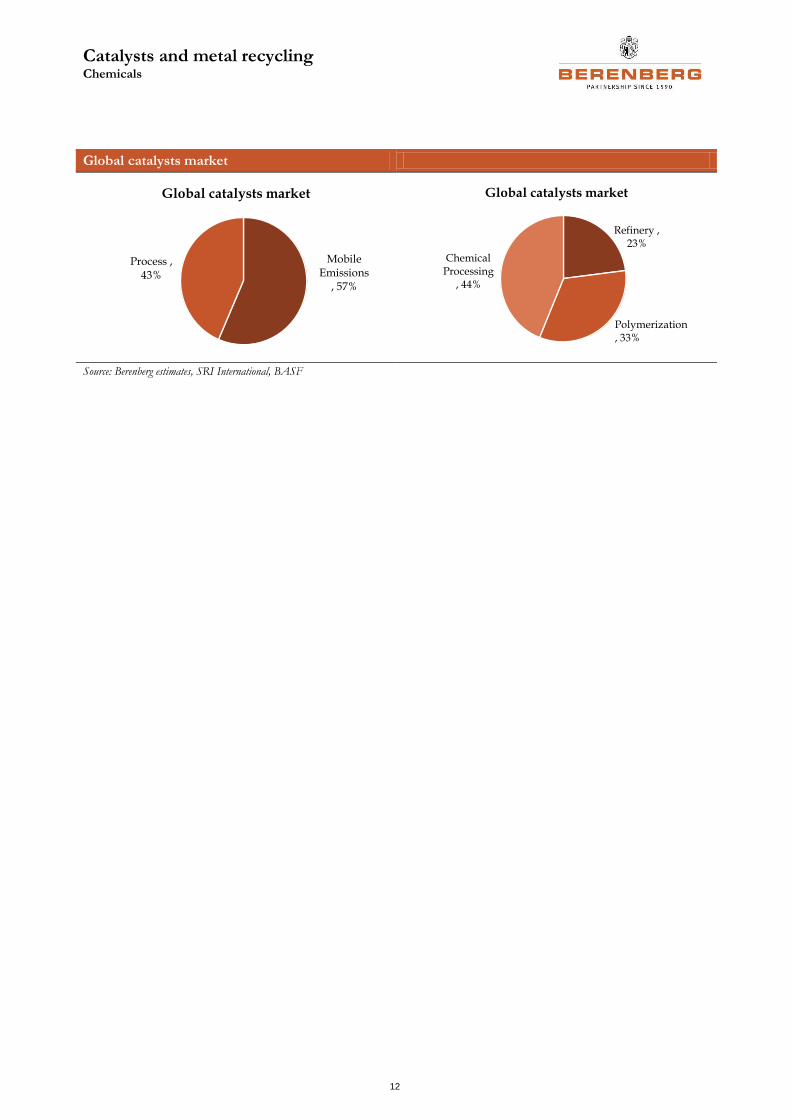

Short-term growth in the HDD market will be driven by the introduction of the Euro VI standard in Europe and Phase IV (similar to Euro IV) in China. Both are expected to come into force at the beginning of 2014. Based on our analysis, we expect the European HDD catalyst market to double due to this change in legislation.

We see the development of the Chinese market as more problematic. Low-sulphur fuel is necessary for Phase IV implementation and it is not yet clear whether this is available throughout the country. For the last four years, Chinese oil refineries have struggled with the capacity upgrades required for low-sulphur fuel production.

Phase IV does not require sophisticated technology, so the catalyst value per vehicle will be much less than it is in developed countries. Implementation will also attract local competitors to the market, so the catalyst majors’ market share will be smaller in China than in the developed world.

Lastly, it is not clear how the change in legislation will be enforced in China. In Europe or the US, faulty catalysts can result in significant fines for the auto manufacturer. In China, the stakeholders as well as the emissions measurement mechanisms are not clear. We think truck manufacturers will try to avoid additional investments in emissions control, should such an opportunity arise.

We also have certain concerns about the short-term profitability of the HDD catalyst market. Future changes in HDD legislation have prompted all the major players to increase capacity and we think that, in the next two years, the market will be unable to absorb all the capacity additions.

Metal recycling

We think that there are fundamental changes taking place in the recycling industry which will lead to a reduction in refining charges and precious metal yields for the leading player, Umicore. The company has developed a unique technological process which allows it to recover 20 precious and non-ferrous metals from various sources of secondary feedstock. Umicore’s metal extraction rates are much higher than those of its competitors, especially in cases where metal concentration in the feedstock is low.

So far, Umicore has been able to “cherry-pick” its feedstock in order to optimise the input metal mix and increase the metal yield of the output. However, we think that the availability of various platinum group metal (PGM) containing feedstocks will be severely reduced in the medium term.

E-scrap is one of the most important feedstocks for metal recycling, as it has the highest concentration of precious metals per tonne of scrap. The market – mistakenly, in our view – expects very strong growth in the availability of this type of feedstock. Based on our analysis, we expect the growth in e-scrap availability to be considerably lower than the market forecasts. The majority of the materials

Catalysts and metal recycling Chemicals

7

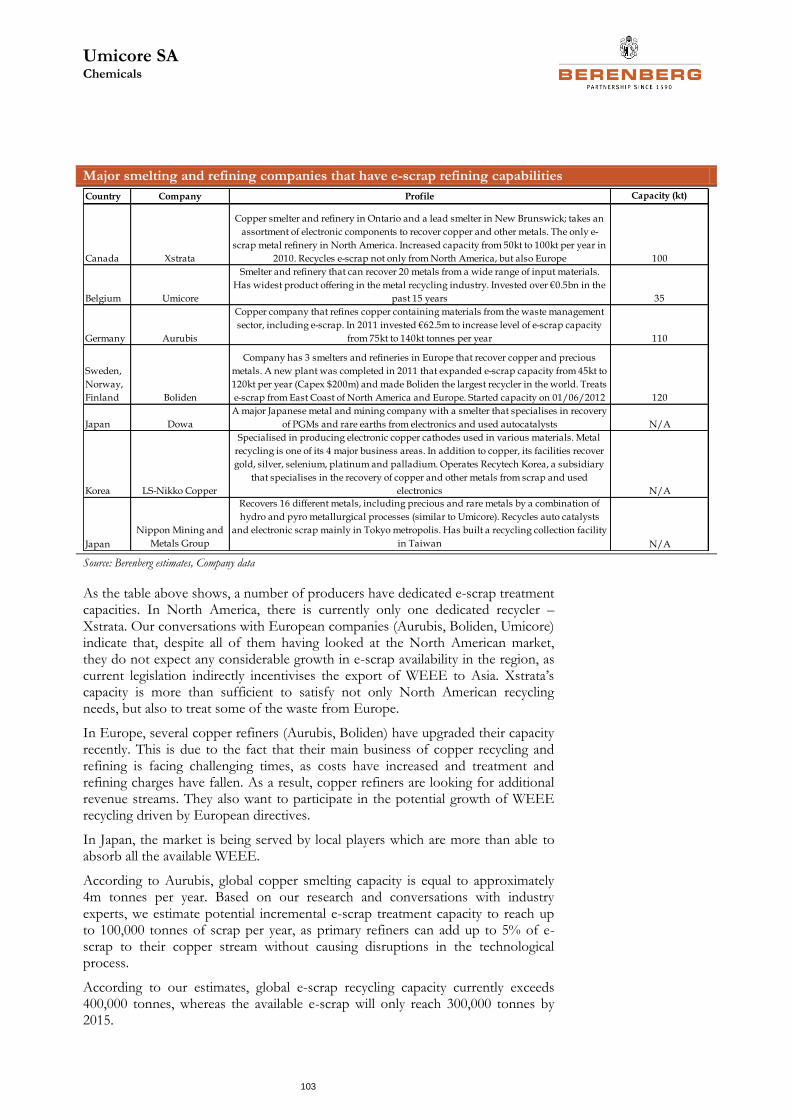

which are available and profitable to recycle are already being recycled (legally or illegally). Radical changes in legislation and changes in product design are required for further growth of the addressable market. On the other hand, capacity growth in e-scrap recycling is considerably outpacing the growth in scrap availability. According to our estimates, global e-scrap recycling capacity currently exceeds 400,000 tonnes, whereas the available e-scrap will only reach 300,000 tonnes by 2015.

We also think that the concentration of PGMs in industrial residues will decrease over time.

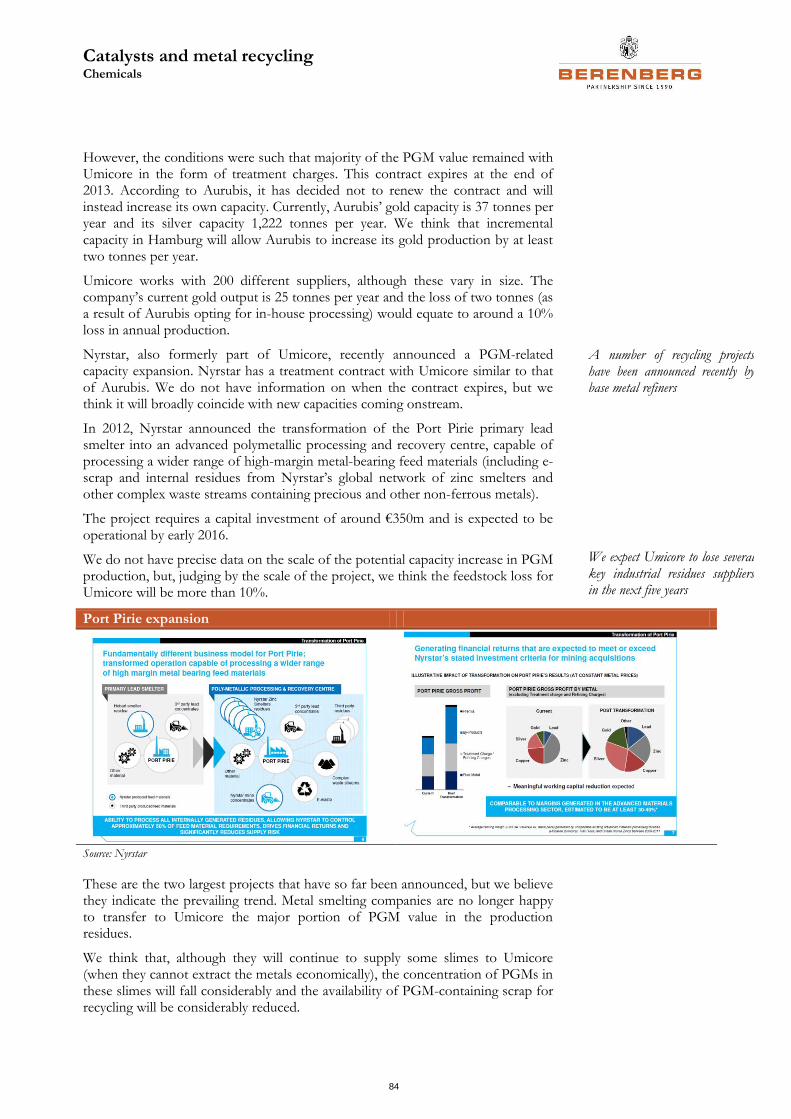

Concentrates which metal smelters use as feedstock contain precious and minor metals. In the past, base metal smelters used to outsource the treatment of their PGM-containing production slimes to the likes of Umicore. However, the recent decline in their main revenue streams (treatment charges, free metal sales and by-product sales) has forced them to look for incremental sources of revenue. A number of base metal refiners have made investments in recycling facilities. For instance, Aurubis has a long-term contract with Umicore which is coming to an end in 2013; Aurubis has decided not to renew it. Based on our calculations, the loss of this contract could result in the loss of 10% of Umicore’s gold feedstock. Nyrstar is another company which intends to end its contract with Umicore in 2015-16.

Recycling is a very capital-intensive business. We think that fixed costs represent up to 75% of total cash costs in recycling (excluding the cost of the metal, which is a pass-through). As a result, a recycler has to operate the smelter 24/7, even if the input mix is not optimal. As the metal mix deteriorates, the recycler begins to treat fewer precious metals and more base metals (lead, copper and zinc). As a result, revenues decline significantly, whereas costs remain broadly unchanged or even increase, as the recycler has to process higher volumes in order to reach the same precious metal yields.

We expect that the profitability and returns of Umicore – the leading player in the recycling industry – will fall in the medium term.

Catalysts and metal recycling Chemicals

8

Porter’s five forces analysis

Catalysis

The bargaining power of suppliers is limited. In precious-metals-based catalysts, metals represent a considerable portion of the catalyst price. However, precious metal costs are always a pass-through in the catalysts industry, so price fluctuations do not have an effect on catalyst producers’ profits. On the other hand, catalyst producers represent a major share of precious metals demand, so they have certain bargaining power with their suppliers. The cost of the substrate is also a pass-through, so similar relationships exist.

The bargaining power of customers is relatively low in the process catalyst industry and relatively high in the automotive catalyst industry. Process catalysts reduce the costs of the processes for which they are used. They are often critical to the production process and provide a competitive advantage to the technology owner. As a result, the bargaining power of customers in the process catalyst industry is not strong. Constant innovation and a high level of technological expertise allow catalyst producers to charge a premium for their products.

In the automotive catalyst industry, customers’ bargaining power is greater. Though catalysts are necessary to comply with strict environmental legislation, the technology is relatively mature and in the absence of legislative changes it is hard for the catalyst producers to come up with new solutions. The global automotive industry is highly consolidated and catalyst producers often work with the same client in different regions. The scale of cooperation gives additional bargaining power to the customers.

Competitive rivalry is lower in the process catalyst industry and higher in the automotive catalyst industry.

In the process catalyst industry, producers tend to specialise in certain types of technology, which limits competition. In the automotive catalyst industry, all three leading players have a high level of technical expertise. However, as the technology is relatively mature, they have to compete vigorously with each other.

The risk of substitution is low in both process and automotive catalysts. Catalysts are a critical part of the processes in which they participate.

The threat of new entrants is moderate in both industries. As demand for catalysts is very much technology-driven, new, disruptive technology is required in order to break through into the market.

Catalysts and metal recycling Chemicals

9

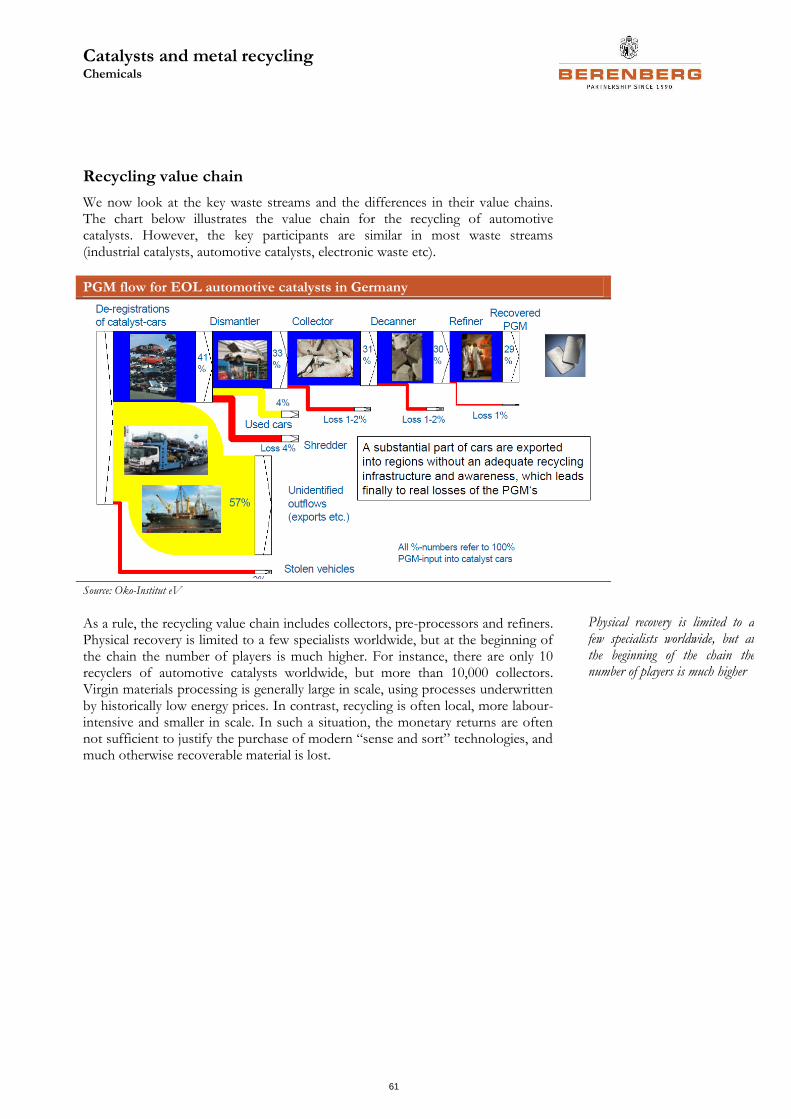

Recycling

The bargaining power of suppliers is limited, but increasing. In the majority of cases in the recycling industry, suppliers are also clients. The recycler obtains metal scrap from the client and returns extracted metal. Treatment charges are the key revenue stream for the recycler. In the past, the structure of the treatment charge allowed the recyclers to capture a large proportion of the underlying metal value. However, as recycling technology matures, more players are entering the market, with the suppliers themselves investing in metal treatment facilities. We think that these changes will affect the structure of treatment charges and reduce the value of the metal captured by the supplier.

The bargaining power of customers. See point above.

Competitive rivalry is increasing due to fundamental changes in the industry. We expect scrap availability to decline in the medium term. Recyclers will have to compete with their own suppliers for available feedstock material.

The risk of substitution is low. Metals can be either mined or recycled. Recycling feedstock has much higher metal concentrations than ore does. Recycling is therefore a much more cost-efficient method of metal production than mining.

The threat of new entrants is increasing. Scrap suppliers (mostly base metal refiners) are becoming increasingly involved in metal recycling, as they are reluctant to share a significant portion of the value of the recovered metal with the recycler.

Catalysts and metal recycling Chemicals

10

Catalysts

Catalysts are the “workhorses” of chemical transformations. Approximately 85-90% of the products of the chemicals industry and 20% of all industrial products are made via a catalytic process.

A catalyst accelerates a chemical reaction. Every catalytic reaction is a sequence of elementary steps in which reactant molecules bind to the catalyst, where they react, after which the product detaches from the catalyst, liberating the latter for the next cycle.

Catalysts are required in:

petroleum refining (which consists almost entirely of catalytic processes);

the production of bulk and fine chemicals in all branches of the chemicals industry (for instance, rubber, plastics, methanol etc);

the prevention of pollution by avoiding the formation of waste;

the abatement of pollution in end-of-pipe solutions (automotive and industrial exhausts); and

the production of pharmaceuticals.

A catalyst offers an alternative, energy-efficient mechanism to the non-catalytic reaction, thus enabling processes to be carried out under industrially-feasible conditions (in terms of pressure and temperature, for example). The chemicals industry would not exist without catalysts: they can help substantially decrease costs or develop new, unique product propositions, providing a competitive advantage to a company which owns certain catalytic technology.

Catalysts come in a multitude of forms, varying from atoms and molecules to large structures such as zeolites or enzymes. In addition, they may be employed in various surroundings: in liquids, in gases or on the surface of solids.

Catalytic reaction

Source: Concepts of Modern Catalysis and Kinetics (second edition); I Chorkendorff, JW Niemantsverdriet

Approximately 85-90% of the products of the chemicals industry and 20% of all industrial products are made via a catalytic process

Catalysts and metal recycling Chemicals

11

Catalysts: an integral part of chemicals production

Catalysts accelerate reactions and thus enable industrially-important reactions to be carried out efficiently under conditions that are attainable practically. Very often, catalytic routes can be designed such that raw materials are used efficiently and waste production is minimised. Consequently, the chemicals industry is largely based upon catalysis: roughly 85-90% of all products are made via catalytic processes and this percentage is increasing steadily.

In developed countries, demand growth is driven mostly by legislative changes, while economic growth is the major source in emerging and developing countries. While emissions standards and environmental norms are becoming stricter in developed countries, growth in vehicle production and fuel consumption as well as growth in chemicals production are the key drivers in emerging markets.

The table below describes the main types of catalyst and the companies which specialise in their production.

Key process catalyst types

Reaction Catalysts Company

Catalytic cracking of crude oil (FCC) Zeolites W.R. Grace, BASF, Albemarle, Criterion, Sud-

Chemie, JGC catalysts

Hydrotreating the crude oil Co-Mo, Ni-Mo, Ni-W

W.R. Grace Albermarle, Criterion, BASF

(Engelhard), Chevron Phillips, Criterion, Nikki-

Universal, Axens

Polymerization of olefinsCr, TiClx/MgCl1, Ziegler

catalysts

Albemarle, W.R. Grace, LyondellBasell, Air

Products, BASF, Dow, ExxonMobil, Evonik,

N.E. Chemcat, Nippon shokubai, Sud Chemie

Ethylene epoxidation to etylene oxide Ag Nippon Shokubai

Ammonia, Hydrogen, syngas and Methanol

productionPt-Rh, Fe, Cu-ZnO, Ni JMAT, Criterion, BASF, Sud chemie

Hydrogenation of vegetable oils, oleochemicals

and oxoalcoholsNi JMAT, BASF

Sulfuric acid V Nippon Shokubai

Oxidation of CO & hydrocarbons (car exhaust) Pt, PdJMAT, BASF, Umicore, Catalar, N.E. Chemcat,

Nippon Shokubai

Reduction of Nox (in exhaust) Rh, vanadium oxide JMAT, BASF, Umicore, Catalar

Coal to liquids, Gas to liquids Fischer-Tropsch Albermarle, BASF, JMAT, Criterion

Hydrogenation and oxidation Ni, Pt, Pd, Cu Johnson Matthey, BASF, Evonik, Sud Chemie

Silicon curing Pt BASF, W.R. Grace

Pharmaceuticals Chiral catalysts (Pd, Cu, Ni) JMAT, N.E. Chemcat, BASF

Petroleum desulfurization Ni, Co-Mo, Ni-MoNikki-Universal, Sud-chemie, Albermarle,

Axens, Criterion Source: Company data, Berenberg research

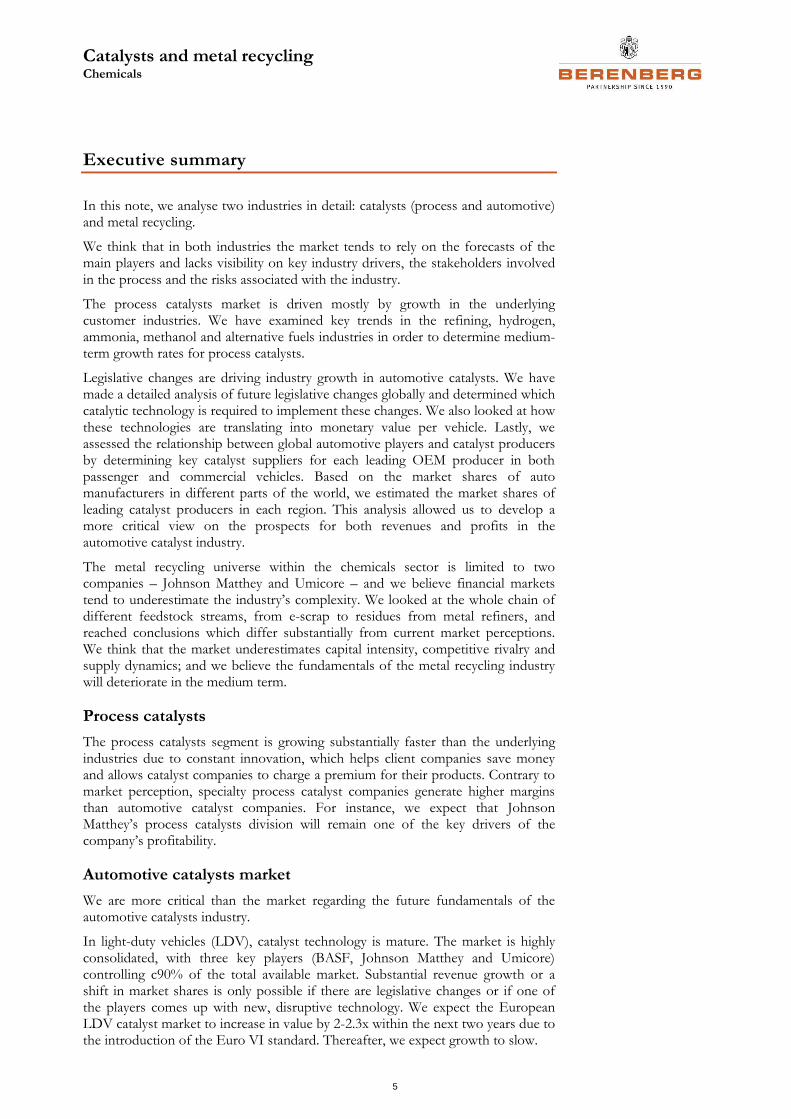

According to SRI International, the value of the mobile emissions catalysts market, including metals, is $16.9bn and the value of the process catalysts market is $13bn.

Catalysts reduce the costs of the processes for which they are used. They are often critical to the production process and provide a competitive advantage to the technology owner

Catalysts and metal recycling Chemicals

12

Global catalysts market

Mobile Emissions

, 57%

Process , 43%

Global catalysts market

Refinery , 23%

Chemical Processing

, 44%

Global catalysts market

Polymerization, 33%

Source: Berenberg estimates, SRI International, BASF

Catalysts and metal recycling Chemicals

13

Process catalysts

Catalysts for refineries represent approximately 23% of process catalysts, with catalytic cracking the largest segment within refining, followed by hydrotreating, reforming and hydrocracking.

Polymerisation catalysts represent 33% of the total market for process catalysts. Major market sub-segments include polyethylene, polypropylene, polyethylene terephthalate, polyvinyl chloride and polystyrene. Polyolefin catalysts are the largest category, accounting for a 60% share of the sub-segment.

The chemicals processing segment represents 44% of the process catalysts market and includes organic synthesis, oxidation/ammoxidation, hydrogen/ammonia/ methanol synthesis and hydrogenation/dehydrogenation. The markets for most of these chemicals have faced slow growth in the last five years. However, growth in the market for catalysts (ex-metals) has been 1.5-2x higher than that of the underlying chemicals due to the following trends:

the need to adapt to new feedstocks (for instance, renewable fuels require a different type of catalyst);

the use of higher-performing catalysts to achieve higher process yields – as well as to prolong catalyst life – favourably affects product mix;

gas-to-liquids and coal-to-liquids;

the development and commercialisation of chiral catalysts for selective hydrogenation to produce fine chemicals/pharmaceuticals for aroma and agrochemicals;

changes in legislation: stricter environmental requirements resulting in higher volumes of catalysts; and

a reduction in the quantity of high-value metals in the catalyst without sacrificing process yields.

We mentioned various players in the process catalysts market in the table above. There are several business models.

Captive manufacturers: as catalysts are critical for the production process, their technology is often highly proprietary in nature. The captive manufacture of catalysts is dominated by large chemicals manufacturers and petroleum refiners that possess both the sophisticated technology and the capital needed to finance expensive catalyst and process development programmes. Companies may also contract with catalyst manufacturers to produce the catalysts they need under secrecy agreements (for example, Exxon, BASF, Chevron, Albemarle etc).

Dedicated catalyst manufacturers, specialised in certain product groups (for example, Criterion).

Companies with divisions specialised in the manufacture of certain types of catalyst (for example, Johnson Matthey, Süd-Chemie).

The process catalysts segment is growing substantially faster than the underlying industries due to constant innovation, which helps client companies save money and allows catalyst producers to charge a premium for their products. R&D can range from 4% of sales for a company producing general-purpose catalysts to 10% of sales for a company which is highly specialised.

Technology-based M&A and technical alliances with client industries are quite common.

Refining catalysts have the largest share by volume, but the smallest by value. Chemical catalysts are highest in value

The market for chemical catalysts has grown 1.5-2x faster than the underlying chemicals markets

As catalysts are critical for the production process, their technology is often proprietary in nature

As innovation is one of the key growth drivers in the process catalysts industry, R&D can reach 10% of the producer’s sales

Catalysts and metal recycling Chemicals

14

The major players in the refinery catalysts business are global companies. Refinery catalysts are characterised by high volume but lower added-value. Customer loyalty is relatively low and competition among the various players is stiff.

In chemical catalysts, the level of specialisation and customer loyalty is higher as changing catalyst supplier is a lengthy and expensive process, which involves extensive testing. Adoption of the new products is normally driven by the improvement in process performance and not by price competition. Adoption is heavily dependent on the supplier’s reputation, depth of expertise and customer relationship. Catalyst companies usually do not reimburse their customers for the losses associated with off-spec products if the catalyst does not perform according to its specification. As potential losses for the customer can be considerable, reliability is one of the key factors during the choice of supplier and technological barriers to entry are high in the industry.

One of the key differences between automotive and process catalysts is the greater predictability of earnings in the case of process catalyst suppliers. Automotive catalysts are placed into the exhaust pipe of the vehicle at the moment of vehicle production and serve throughout the entire life of the vehicle. Process catalysts should be replaced regularly. For instance, Johnson Matthey states that the lifetime of the catalysts in its methanol, ammonia and hydrogen business is three years, after which replacement is required. As no incremental R&D costs are required for the replacement catalysts, replacement revenues are extremely important in terms of the overall profitability of process catalyst producers. They also provide good visibility on future earnings.

Process catalysts at Johnson Matthey

Johnson Matthey’s process catalysts business comprises various types of chemical catalysts. It includes base metal catalysts such as nickel, copper and cobalt for the production of syngas, ammonia, hydrogen, methanol, formaldehyde, oleo chemicals, oxo-alcohols, gas-to-liquids, coal-to-liquids and additives for refining. It also includes Davy Process Technology, which provides licences and know-how for the use of advanced process technologies related to the manufacture of oil and gas and petrochemicals.

In its Fine Chemicals division, Johnson Matthey manufactures base and precious metal catalysts for the fine chemicals and pharmaceuticals industries.

Johnson Matthey does not have direct exposure to high-volume but low-value refinery and hydrotreating catalysts, but concentrates instead on the higher-value, higher-margin field of process catalysts – catalysts for chemical processes. Not only do chemical catalysts often command a higher premium, but their markets have also demonstrated consistently high growth rates.

Johnson Matthey is not in the mainstream refinery catalysts business (such as fluid catalytic cracking – FCC – and hydroprocessing), but it has a leading position in the supply of hydrogen catalysts. Hydrogen is used by the refiners to remove sulphur and improve the quality of fuels. According to our estimates, Johnson Matthey commands a 35-40% market share in hydrogen catalysts (key competitors include Süd-Chemie, BASF and Chinese companies which sometimes satisfy local needs).

In November 2010, Johnson Matthey bought Intercat, a supplier of specialty additives to petroleum refining, further increasing its exposure to the petroleum refining industry. Johnson Matthey is also a major supplier of catalysts for the removal of impurities such as benzene from refinery streams, environmental catalysts for the destruction of volatile organic compounds and the removal of

As off-spec products resulting from faulty catalysts can cause substantial financial losses for the client, the technological barriers to entry in the industry are high

Automotive catalysts are not replaced during the lifetime of the vehicles. Process catalysts should be replaced regularly, which gives much better visibility to catalyst producers

Johnson Matthey makes catalysts for the production of syngas, ammonia, hydrogen and methanol

Catalysts and metal recycling Chemicals

15

organic impurities from caustic streams.

Johnson Matthey has a market share in catalysts for ammonia production of around 30% and in catalysts for methanol production of around 45%. Süd-Chemie is among its main competitors in these areas.

Recently, Johnson Matthey further increased its exposure to the methanol chain by acquiring Formox. The latter is a leading global provider of catalysts, plant designs and licences for the manufacture of formaldehyde. Currently, around 32% of the methanol produced globally is consumed in the production of formaldehyde. The main use of formaldehyde is as a component of resins, which are used in wood adhesives for plywood, particleboard and other reconstituted or engineered wood products. Formaldehyde is also used as a raw material for plastics, elastomers, paints, foams, polyurethane and automotive products. Formox developed a range of metal-oxide-based catalysts for the production of formaldehyde from methanol as well as licensing the technology.

Davy Process Technology increased its sales from £44m in 2009 to £100m in 2012. It won a consistently increasing number of contracts for methanol, oxo-alcohols, syngas and specialty chemicals plants, especially in China. The business is now seeing large chemicals and coal companies placing repeat orders for new plants.

Davy Process Technology growth

Source: Johnson Matthey Annual Report 2011-12

Johnson Matthey’s battery technologies business was formed after the acquisition of Axeon in 2012 and specialises in the design, development and manufacture of integrated battery systems. The business is focused on developing advanced technologies and materials to meet the requirements of high-performance battery applications, such as automotive, e-bikes and power tools.

As we stated above, growth in the chemical catalysts market is 1.5-2x higher than the growth in the underlying chemicals industries. In order to understand the growth outlook for Johnson Matthey’s Process Technologies division, we therefore look at various customer industries.

We expect the growth of Johnson Matthey’s process catalysts business to be 1.5-2x higher than the growth of the underlying industries

Catalysts and metal recycling Chemicals

16

Refining industry

Refinery catalyst production was traditionally a growth business, but in recent years the market has reached maturity in developed countries. Taking into account the wider macroeconomic climate, refinery infrastructure investment continues to face severe challenges in developed regions. Major growth is occurring in developing countries, especially in Asia and the Middle East. Among Asian countries, China is the largest consumer of catalysts, with high growth rates.

Currently, there is refining overcapacity in Europe and North America. In its Statistical Review of World Energy, BP confirmed that in 2010 production in non-OECD countries overtook that in OECD countries for the first time. China accounts for 85-90% of global refining capacity growth. PetroChina states that, while at present a net importer of crude oil, China is determined to become self-sufficient in refining. By 2015, Chinese oil companies aim to boost domestic capacity by 25% to 15mbpd. Growth in India is also expected to remain very strong, albeit the initial base is much smaller. At the 20th World Petroleum Congress, the Indian minister for petroleum and natural gas announced that his country would increase investment in refinery infrastructure. Current refinery capacity in India is 193m mta (metric tonnes annually); by 2014 the target is to raise this to 240m mta. The Indian government plans to reach domestic self-sufficiency by 2020. Brazilian consumption of petroleum products has more than doubled from 1998 to 2009, but refinery capacity stayed flat; Brazil is actively looking at enhancing downstream investment. Additionally, producers in Qatar and Saudi Arabia are targeting not only their respective local markets, but also Southeast Asian ones (for example, the Dow project in Saudi Arabia).

Global refinery capacity growth

-8%-6%-4%-2%0%2%4%6%8%

10%12%14%

1965

196

7

196

9

197

1

197

3

197

5

1977

197

9

198

1

198

3

198

5

198

7

198

9

199

1

199

3

199

5

199

7

1999

200

1

200

3

200

5

200

7

200

9

201

1

global growth OECD growth Non-OECD growth

Source: BP Statistical Review of World Energy 2013

In the last 10 years, global refinery capacity growth averaged 1% per year, with no overall growth in OECD countries and 2% growth in non-OECD countries. We expect global growth to slow in the next five years, as OECD countries will continue to struggle with overcapacity and cheaper alternative sources will take market share from oil (biofuels, natural gas liquids, liquids derived from gas and coal).

Hydrogen consumption growth

We expect hydrogen demand to grow at a much higher rate than refining capacity – 6-8% per year as demand increases, particularly in Asia. According to SRI

Refinery infrastructure investments continue to face severe challenges in developed jurisdictions. The major growth is occurring in developing countries, especially Asia and the Middle East

China accounts for 85-90% of global refining capacity growth

Catalysts and metal recycling Chemicals

17

International, China represents around 23% of global hydrogen consumption and we expect this will reach 30% by 2015.

Key drivers of growth in hydrogen consumption include:

tighter limits on the sulphur content in fuel;

the development of gas- and coal-to-liquids technologies; and

the use of methanol as a fuel.

Worldwide environmental regulations now mandate the production of cleaner fuels. Consequently, refiners are experiencing severe pressure from market forces that demand a change in the product mix, aside from quality (eg the production of low-sulphur fuel). On the regulatory side, stringent product specifications limit sulphur content and determine gasoline and diesel composition. Major technological challenges to refining include the achievement of “zero” or heavily-reduced sulphur content in all types of fuel in almost all countries around the world.

As the global refining industry moves towards cleaner fuels, refiners find themselves being squeezed in terms of hydrogen availability and octane requirements. Gasoline desulphurisation technology has thus advanced to limit hydrogen consumption.

On the diesel side of the clean fuels challenge, a significant increase in hydrogen consumption is forecast to obtain ultra-low-sulphur diesel (ULSD) from straight-run and cracked stocks containing refractory sulphur species.

Catalytic reforming is the technology of choice for the production of high-octane gasoline and is usually the main source of refinery hydrogen. Catalytic reforming and isomerisation continue to grow because of their role in removing lead from gasoline in the developing world. Hydroprocessing is probably growing the fastest, in response to the requirement for lower sulphur levels in gasoline and diesel. Johnson Matthey is one of the leaders in hydrogen catalysts for hydroprocessing, so we expect strong growth in this area to continue.

Gas-to-liquids and coal gasification projects all require extremely large quantities of hydrogen and will boost the size of the market considerably in the next five years.

A surge in hydrogen consumption is also expected as a result of growth in the manufacture of methanol. Substantial consumption of methanol as a direct fuel (ie as motor gasoline) is expected in countries such as China, Russia, South Africa, Venezuela and several Middle Eastern countries.

The main growth in hydrogen consumption is expected to come from China for two reasons: the country is experiencing the strongest growth in auto production as well as changes in environmental legislation.

Johnson Matthey is one of the leaders in hydrogen catalysts for hydroprocessing

The main growth in hydrogen consumption is expected to come from China for two reasons – highest growth in auto production and changes in environmental legislation

Catalysts and metal recycling Chemicals

18

China diesel fuel quality roadmap

Stage Standard Maximum sulphur

level (ppm) Date Standard

Issued Date standard Implemented

- GB 252-2000 2000 27 Oct 2000 1 Jan 2002

- GB/T 19147-2003 500 (voluntary) 23 May 2003 1 Oct 2003

China III GB 19147-2009 350 12 Jun 2009 Phased-in 1 Jan 2010-1 Jul 2011

China IV GB 19147-2013 50 7 Feb 2013 Phased-in by 31

Dec 2014

China V TBD 10 Before 1 Jun 2013 Phased-in by 31

Dec 2017

Source: The International Council on Clean Transportation

China was supposed to implement the China IV (Phase IV) fuel standard in January 2010; however, this was delayed until 2014. China has set a deadline for the Phase IV standard for gasoline to be adopted nationwide by January 2013, and that

for diesel to be adopted by the end of 2014. Delays in the implementation of emissions legislation are not unique to China. The other three BRIC countries (Brazil, Russia and India) have all seen similar delays. The reason for the delay in each case is a recurring theme: the lack of low-sulphur fuel. The successful implementation of advanced diesel after-treatment technologies relies on the availability of low-sulphur diesel. It was originally agreed that 350ppm-sulphur diesel should be made available nationwide in 2010. However, the implementation of low-sulphur fuel was delayed until summer 2011. Yet even now, after almost four years, we are not sure it is available nationwide.

The main issue lies in the costs associated with upgrading diesel refineries and the distribution of this type of diesel. Chinese diesel prices are regulated by the government and refiners were not certain that they would be able to recover the incremental costs. The additional cost is estimated at CNY150-250/mt ($24-40/mt) compared with Phase III gasoline, with the construction cost of a gasoline hydrogenation unit estimated at around CNY200m-300m.

However, as the transition deadline was finally approved in 2012, refineries were given a year to transition to the new legislation. Recently, Sinopec’s chairman, Fu Chengyu, said that the company would complete the upgrade of desulphurisation facilities at its refineries by the end of 2013, and start producing gasoline and diesel that meet the national Phase IV emissions standard from 2014.

Johnson Matthey has a very strong presence in Asia and good relationships with major industrial gas companies that supply hydrogen to petroleum refineries, so in our view it should experience very strong growth in hydrogen catalysts in the next three years.

We expect the use of hydrogen catalysts to grow at a faster rate than hydrogen consumption – 10-12% per year for the next three years.

Ammonia consumption growth

Johnson Matthey is one of the leading producers of the catalysts for ammonia production, along with Süd-Chemie. We are slightly less optimistic about developments in the market for ammonia, but still assume average annual growth of 5-6% for the catalysts.

According to Yara, global ammonia production grew at an average annual rate of 2.6% in 2001-11.

We expect the use of hydrogen catalysts to grow at a faster rate than hydrogen consumption – 10-12% per year for the next three years

China was supposed to implement the China IV fuel standard in January 2010; however, this was delayed until 2014 because of the lack of low-sulphur fuel

Johnson Matthey is one of the leading producers of the catalysts for ammonia production along with Süd-Chemie

Catalysts and metal recycling Chemicals

19

Global ammonia production growth

Million tonsTotal production

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

60

80

100

120

140

160

180

Source: Yara Fertiliser Industry Handbook, December 2012

We expect this trend to continue; however, we expect ammonia capacity additions to outpace supply and production growth. Capacity is expected to increase in China and in areas where the availability and cost of natural gas is lower, such as the Middle East, North Africa and North America. In 2013-15, the International Fertiliser Association expects global capacity ex-China to grow in line with demand (ie by around 3% per year); however, Chinese capacity is expected to grow by 8% per year. Beyond 2015, various North American capacities should come onstream; almost 8m tonnes pa of nitrogen capacity is expected to start up in 2015-18. However, rising construction costs can cause delays to these projects – Agrium recently postponed its $3bn greenfield nitrogen project and Yara postponed its capacity upgrade in Belle Plaine, Canada.

We expect global capacity growth in ammonia to reach 3.5% per year in the next five years and the production of ammonia catalysts to grow at 5-6%.

Methanol consumption growth

Süd-Chemie is one of Johnson Matthey’s key competitors in methanol catalysts. It not only manufactures catalysts for methanol production, but also has the also technology for converting methanol to propylene.

Methanol is a versatile liquid chemical produced primarily from natural gas (in China, from coal) and used as a chemical feedstock in the manufacture of a wide range of consumer and industrial products such as building materials, foams, resins and plastics. The fastest-growing markets for methanol are in the energy sector, which today represents one-third of methanol demand.

Methanol is used to produce methyl tertiary-butyl ether (MTBE), a gasoline component, and there are growing markets for using methanol in olefins production and energy applications such as direct blending into transportation fuels, dimethyl ether (DME) and biodiesel.

Demand for methanol is driven primarily by levels of industrial production, energy prices and the strength of the global economy.

Methanex expects methanol demand to grow at a 7.6% CAGR during 2012-16, driven mainly by energy applications.

We expect global capacity growth in ammonia to reach 3.5% in the next five years and ammonia catalysts to grow at 5-6%

Demand for methanol is driven primarily by levels of industrial production, energy prices and the strength of the global economy

Catalysts and metal recycling Chemicals

20

Uses and growth of methanol

Source: Methanex Investor Presentation, May 2013

China has now become the world’s leading consumer of methanol and should account for 80% of demand growth through at least 2016. China’s rapid increase in consumption is attributable to its expanding industrial markets, as well as soaring gasoline demand. Traditional, chemical derivative-based methanol demand in China has seen robust growth over the past decade on the back of China’s strong economic expansion, particularly in the industrial and construction sectors. However, future methanol consumption growth in China will likely be driven by the adoption of methanol as an alternative transportation fuel, among other emerging energy applications.

Methanol usage as a fuel

Source: Methanex Investor Presentation, May 2013

We expect the market for methanol catalysts to grow at 10-11% per year in the next five years. Johnson Matthey commands a 45% market share and is well positioned to capture this growth with Apico catalysts and technology.

China has now become the world’s leading consumer of methanol and should account for 80% of demand growth through at least 2016

We expect the market for methanol catalysts to grow at 10-11% per year over the next five years

Catalysts and metal recycling Chemicals

21

GTL, MTO, CTL etc

Gas-to-liquids (GTL) and coal-to-liquids (CTL) processing is an emerging area for catalysts. The growing requirements for ULSD fuel and the not-insignificant investment required by refiners to meet the new fuel specifications in Europe and elsewhere have pushed GTL technology to the forefront of development efforts. One key advantage of GTL processes is that they provide clean fuels. Companies such as Chevron, ExxonMobil, Sasol, Shell, Albemarle, BASF, Süd-Chemie and Johnson Matthey (via Davy Process Technology) are active in liquid fuel synthesis.

China is short of natural gas. As part of the country’s effort to reduce its dependence on crude oil and utilise cheaper feedstock costs, there are several coal-based projects under development in China. The majority of capacity expansion plans in petrochemicals announced beyond 2015 are China’s coal-to-olefins (CTO), methanol-to-olefins (MTO) and US-gas-based cracker projects.

However, we do expect certain difficulties in the development of these projects. Recent cost inflation has contributed to the cancellation or postponement of certain gas-based projects in North America; in China, MTO projects face multiple hurdles, such as lack of infrastructure, water consumption and high carbon emissions.

Johnson Matthey expects double-digit annual growth in these types of project in the next five years, but we are more cautious due to the challenges mentioned above – we think the growth will reach 7-8% per year.

Johnson Matthey is strongly positioned in the sector. Davy Process Technology (which Johnson Matthey acquired from Yukos for $71m in 2006 and which now has sales of $150m) provides licences and know-how to operate advanced process technologies related to oil and gas, MTO and CTL.

One key advantage of GTL processes is that they provide clean fuels

The majority of capacity expansion plans in petrochemicals announced beyond 2015 are China’s CTO, MTO and US-gas-based cracker projects

We think growth in GTL, MTO and CTL projects will reach 7-8% per year in the next five years

Catalysts and metal recycling Chemicals

22

Automotive catalysts

Emissions control catalysts represent c43% of the global catalysts market. We focus on emissions control catalysts for mobile sources, as stationary catalysts do not represent a large part of Johnson Matthey’s or Umicore’s business.

Technology

Emissions control catalysts for mobile sources are based on PGMs that convert vapour emissions into carbon dioxide, nitrogen and water. The catalyst can simultaneously oxidise carbon monoxide and hydrocarbons to carbon dioxide and water while reducing nitrogen oxides to nitrogen.

Automotive catalysts typically consist of a coating of PGMs on a substrate. The earlier oxidation catalysts used only platinum and palladium, but the newer three-way catalysts use various combinations of platinum, palladium and rhodium.

As an automotive catalyst serves throughout the life of the vehicle, its internal surface area is very large. In an average catalytic converter, the internal surface area of the substrate is equal to the size of a typical office and the internal area of the catalyst is equal to the size of three football fields.

During the manufacture of the catalytic convertor, ceramic monoliths are first treated with a wash that consists of alumina with additions of rare earth oxides to increase their surface area. The monoliths are subsequently coated with PGMs.

Structure and production process of automotive catalysts

Source: Johnson Matthey

The properties of automotive catalysts include the following.

Engine size and catalyst volume/weight are fairly proportional. Engine sizes, however, cover a wide range – from about 0.5 to six litres for passenger cars, to three to 18 litres for trucks and buses. An internal combustion engine, regardless of whether gasoline- or diesel-fuelled, requires a catalyst volume of about the same size as the engine.

Four-cylinder engines are equipped with one or two bricks, while large engines utilise more bricks.

Fuel specifications and emissions standards vary from region to region and may require different catalysts for the same auto platform.

Catalyst design, volume and precious metal content differ according to car manufacturer, region of application, engine type and year of production.

Emissions control catalysts represent c43% of the global catalysts market

Emissions control catalysts for mobile sources are based on PGMs that convert vapour emissions into carbon dioxide, nitrogen and water

For an average catalytic converter, the internal surface area of substrate is equal to the size of typical office and internal area of the catalyst is equal to the size of three football fields

Catalyst design, volume and precious metal content vary according to car manufacturer, region of application, engine type and year of production

Catalysts and metal recycling Chemicals

23

Key emissions categories

Carbon dioxide (CO2): an inevitable product of burning a fuel which contains carbon (as all petroleum products do). CO2 does not pollute the air we breathe, but is a main contributor to global warming and therefore has to be reduced.

Carbon monoxide (CO): produced when a carbon-based fuel is burned incompletely. In high concentrations it is poisonous and has to be controlled. It can be reduced by more efficient combustion in the engine (so that CO2 is produced instead of CO) and further reduced by oxidising after combustion, in a catalytic converter.

Hydrocarbons (HC): also known as volatile organic compounds (VOCs), these are really unburned fuel. They can be problematic for individuals with breathing difficulties and can contribute to photochemical smog in certain climatic conditions. They can be reduced by more efficient combustion in the engine and further reduced by oxidising after combustion, in a catalytic converter.

Oxides of nitrogen (NOx): produced when air (which is mainly a mixture of nitrogen and oxygen) is heated, as it is in an engine. NOx is a contributor to both photochemical smog and acid rain and can be an irritant to the lungs. Unlike CO and HC, it cannot be removed by oxidation. The opposite process – the removal of oxygen (known as reduction) – is necessary to convert it back to nitrogen and oxygen.

Particulate matter (PM): very small particles, mostly of unburned carbon.

Main chemical pathways catalysed by an after-treatment system

NO, NO2 N2

CO CO2

Hydrocarbons CO2, H2O

Particulate matter

(mainly carbon)

CO2

Source: Umicore

Why do diesel and gasoline automotive catalysts differ?

Gasoline The amounts of air and fuel burnt in a gasoline engine are usually in chemical balance, there being no excess of either.

Under these conditions, and at the quite high temperatures (350-750°C) of the gasoline exhaust gas, platinum and/or palladium oxidise the pollutants CO and HC, while rhodium catalyses the reduction of NOx (nitric oxide and nitrogen dioxide) to nitrogen.

Automotive companies therefore use catalysts containing platinum and rhodium, palladium and rhodium, or a mixture of all three to meet current gasoline vehicle emissions regulations. These catalytic converters are known as three-way catalysts because they efficiently and simultaneously convert the three pollutants to harmless gases.

Gasoline cars use platinum-, palladium- and rhodium-based three-way catalysts

Catalysts and metal recycling Chemicals

24

Three-way catalyst

Source: Umicore

Diesel By contrast, a diesel engine always operates with a large excess of air (the air-to-fuel ratio is 30:1) and has excess oxygen in its exhaust. An additional complication comes from the operating conditions of diesel engines, which result in low exhaust gas temperatures (120-350°C). Standard three-way catalysts cannot reduce NOx in such a system. Also, the large quantities of particulates emitted by diesel engines can foul existing gasoline-fuelled automobile catalysts, rendering them useless for reducing the levels of other components.

Only platinum- and palladium-based catalysts are able to deliver the required performance under these operating conditions. The low temperature of diesel engine exhaust gas also means diesel oxidation catalysts may have to contain higher loadings of metal than their gasoline equivalents to achieve the necessary conversions of HC and CO.

Catalytic technologies for diesel engines

A diesel oxidation catalyst (DOC) is the key technology for diesel engines. It is used to oxidise HC and CO in the exhaust stream to CO2 and water. All new diesel engines mounted in passenger cars, light-duty and heavy-duty trucks and buses in Europe and North America are now equipped with DOCs.

Improved engine control and combustion engineering can substantially reduce the formation of PM and reduce NOx emissions. These include the use of very high-pressure fuel pumps in sophisticated direct injection systems, which precisely control the volume of fuel injected into the cylinder and produce a finely-atomised spray. The delivery of fuel at very high pressure leads to a lower average combustion temperature that moderates the formation of NOx. To remove the remaining NOx from the exhaust, manufacturers utilise selective catalytic reduction (SCR).

A diesel engine operates with a large excess of air and a low exhaust gas temperature. Standard three-way catalysts cannot be used in diesel engines

A diesel oxidation catalyst is the key technology for diesel engines

Catalysts and metal recycling Chemicals

25

SCR

Source: Johnson Matthey

SCR was originally introduced in stationary power plants, but it is now fitted to most new heavy-duty (ie truck and bus) diesel engines in Europe and the US. In an SCR system, urea (for example, AdBlue, a trademark used by Yara) is sprayed from a separate tank into the exhaust stream ahead of the SCR catalyst. The nature of the diesel combustion process results in the formation of PM, or “soot”. The diesel particulate emissions problem is being addressed by the use of diesel particulate filters (DPFs).

DPF

Source: Turbopacs

Wall flow filters are the most common type of DPF. In these filters, PM is removed from the exhaust by using a honeycomb structure similar to an emissions catalyst substrate but with the channels blocked at alternate ends. The exhaust gas is thus forced to flow through the walls between the channels and the PM is deposited on the walls. Such filters are made of ceramic (cordierite, silicon carbide or aluminium titanate) materials. Diesel partial-flow filters normally use a metallic substrate. The metallic partial-flow filter uses a special perforated metal foil substrate with a metal “fleece” layer, so that the exhaust gas flow is diverted into adjacent channels and the particles are temporarily retained in the fleece before being burnt by a continuous reaction with the nitrogen dioxide (NO2) generated by an oxidation catalyst located upstream in the exhaust.

A catalysed diesel particulate filter (CDPF) or catalysed soot filter (CSF) may also be used. Traditional DPF systems consist of a filter material positioned in the exhaust designed to collect solid and liquid PM emissions while allowing the exhaust gases to pass through the ceramic walls. CDPFs are designed not only to

SCR was originally introduced in stationary power plants, but it is now fitted to most new heavy-duty diesel engines in Europe and in the US

The diesel particulate emissions problem is being addressed by the use of DPF

CDPFs are designed not only to achieve collection efficiencies of 90% or greater in terms of mass, but also to burn off the collected particulate matter into carbon dioxide and water

Catalysts and metal recycling Chemicals

26

achieve collection efficiencies of 90% or greater in terms of mass, but also to burn off the collected particulate matter into carbon dioxide and water.

CDPF

Source: Johnson Matthey

Johnson Matthey was the first to introduce and patent the CRT – continuously regenerating trap. It is now the most widely used DPF in the world. It involves the oxidation of nitric oxide (NO), which is already present in the exhaust gas, to NO2 over a platinum-based catalyst. The NO2 produced is a much more powerful oxidant than oxygen, and it starts to burn PM at temperatures as low as 250°C (the technology has already gone off-patent). It was a very successful product and allowed Johnson Matthey to gain considerable market share in diesel vehicle catalysts (both in light- and heavy-duty).

CRT

Source: Johnson Matthey

CCRT is catalysed CRT. The oxidation catalyst removes CO and HC and oxidises some of the NO in the exhaust gases to NO2. This NO2 then reacts with the PM trapped in the filter, producing NO and CO2. Some of the NO is then re-oxidised to NO2 in the filter, then reacts with more trapped PM. This enables the system to regenerate in applications with very low exhaust gas temperatures or low NOx:PM ratios in the exhaust gases.

Catalysts and metal recycling Chemicals

27

CCRT

Source: Johnson Matthey

Fuel properties

The quality of the fuel used can assist or degrade the performance of emissions control systems. Sulphur in gasoline (or petrol) and diesel fuel has a major negative impact on catalyst performance and in diesel also contributes to the mass of PM. Sulphur competes strongly against pollutants for space on the catalyst surface and thus limits the efficiency of catalyst systems to convert pollutants at any sulphur concentration. Sulphur is a naturally-occurring component of crude oil and is found in both gasoline and diesel. When these fuels are burned, sulphur is emitted as sulphur dioxide (SO2) or sulphate PM. SO2 has been recognised for decades as a major cause of the acid rain and air pollution that affect urban and industrial areas. More recently, it has been recognised that CO2 emissions contribute to the formation of secondary inorganic aerosol gases, fine particles that are harmful to human health.

Increasingly stringent controls on vehicle emissions led petroleum refiners to produce fuels which meet both reformulated gasoline and low-sulphur fuel mandates. These fuels, in combination with emissions control catalysts and engine developments, have enabled the transportation industry to manufacture products that meet government emissions targets.

Global legislation

Air pollution can cause a number of health problems, so various countries have taken policy actions in order to reduce it.

Regulatory authorities in the EU, US and Japan have been under pressure from engine and fuel manufacturers to harmonise worldwide emissions standards, in order to streamline engine development and emission-type approval/certification for the different markets. European standards for emissions control represent the most popular set of standards and are followed by many countries in various parts of the world. The majority of emerging economies are adopting the latest set of Euro emissions and fuel standards, while some smaller nations still comply with an older set of regulations.

The quality of the fuel used can assist or degrade the performance of emissions control systems

Increasingly stringent controls on vehicle emissions led petroleum refiners to produce fuels which meet both reformulated gasoline and low-sulphur fuel mandates

European standards for emissions control represent the most popular set of standards and are followed by many countries in various parts of the world

Catalysts and metal recycling Chemicals

28

Global emissions legislation

Source: Umicore

LDV legislation In most regions, standards apply to all vehicles, regardless of the fuel they use. Gasoline, diesel or alternative-fuel vehicles must therefore all meet the same emissions standards. These standards are defined in grams of regulated emission per mile or kilometre driven. Thus, for similar vehicles with different-sized engines, the vehicle with the larger engine must use more advanced and expensive emissions control technology than the vehicle with the smaller engine, in order to meet the emissions standard.

US

In general, the US has the most advanced regulation in the area of emissions control.

In LDVs, US legislators pay more attention to NOx emissions control than CO2. The chart below shows that US requirements allow for 220 grams of CO2 per kilometre (g/km) and European requirements are close to 120g/km. On the other hand, European NOx emissions standards are more relaxed (the US EPA Tier 2 NOx limit is 44mg/km). This is caused by the need to control NOx emissions without sacrificing the comparatively low fuel consumption of diesel engines.

Global CO2 emissions norms

Source: The International Council on Clean Transportation

In general, the US has the most advanced regulation in the area of emissions control

Catalysts and metal recycling Chemicals

29

Europe

Europe is the only region (except India) where the share of diesel as a fuel is high (it varies between 49% and 54%).

Since the Euro II stage, EU regulations have introduced different emissions limits for diesel and gasoline vehicles. Diesel engines must conform to more stringent CO standards but are allowed higher NOx levels. Gasoline vehicles had been exempt from PM standards through the Euro IV stage.

Euro V introduced PM mass emissions limits for gasoline cars (equal to that of diesel) and a 25% reduction in NOx emissions limits from 80mg/km to 60mg/km. The Euro V PM emissions standards require the use of particulate filters on all diesel cars (the use of filters on Euro IV cars was mostly voluntary).

The Euro VI standards, which will come into effect in 2014, will further tighten the NOx standards for diesel cars and light commercial vehicles by about 55% relative to the Euro V limits.

Japan

All passenger cars and light-duty trucks produced in Japan are equipped with three-way catalysts. New standards came into force in 2009 that added the regulation of PM for gasoline-powered vehicles and further reduced NOx and PM levels for diesel-powered vehicles.

China

Phase III of China’s emissions regulation was introduced in 2007; the requirements are similar to the Euro III legislation. China was supposed to implement the Phase IV (similar to Euro IV) fuel standard in January 2010; however, this was delayed until 2014. China set a January 2013 deadline for the Phase IV standard for

gasoline to be adopted nationwide, and that for diesel by the end of 2014. The reason for the delay is the lack of low-sulphur fuel. The successful implementation of advanced diesel after-treatment technologies relies on the availability of low-sulphur diesel. It was originally agreed that 350ppm-sulphur diesel should be made available nationwide in 2010.

The table below shows the current standards and prospective changes in legislation for LDVs in various regions.

Europe is the only region (except India) where the share of diesel as a fuel is high (it varies between 49% and 54%)

China set a deadline for the Phase IV (similar to Euro IV) standard for gasoline to be adopted nationwide by January 2013

Catalysts and metal recycling Chemicals

30

Summary of the fuel emissions standards for LDV

LDV (g/km) Time frame

CO HC NOx HC&NOx PM

Europe gasoline Now 1 0.1 0.06 0.005

Europe gasoline 2014 1 0.1 0.06 0.005

Europe diesel Now 0.5 0.18 0.23 0.005

Europe diesel 2014 0.5 0.08 0.17 0.005

Japan gasoline Now 1.92 0.08 0.08 0.007

Japan diesel Now 0.84 0.032 0.2 0.01

China gasoline 2014 1 0.1 0.08

China diesel 2014 0.63 0.06 0.33 0.04

US gasoline Now 2.8 0.14 0.07 0.01 Source: Delphi Worldwide Emissions Standards, 2012-13, Berenberg research

LDV emissions standards timeline

Source: Johnson Matthey

HDD legislation Currently, pollution measurement systems vary between countries; hence the units of measurement are different, which makes it difficult to reconcile the requirements on a global basis. The other particularity of this market is that most HDD vehicles worldwide are powered by diesel engines.

US

In the US, the federal regulations do not require that the entire HDD vehicle be certified as conforming to emissions standards. The regulations instead call for the engine to meet the emissions standards. The engine systems, including emission controls, are tested under prescribed engine dynamometer cycles. As a result, the standards are expressed in terms of grams per brake horsepower-hour (g/bhp-hr).

Most HDD vehicles globally are powered by diesel engines

Catalysts and metal recycling Chemicals

31

The US has the most progressive standards in HDD with the strictest requirements regarding HC and NOx emissions as well as levels of PM in the exhaust.

In August 2011, the Environmental Protection Agency (EPA) announced the Heavy-Duty National Program to reduce greenhouse gas emissions – primarily CO2 – and establish fuel consumption standards for medium- and heavy-duty vehicles.

Europe

Europe also addressed seriously the problem of pollution from HDD. European governments use grams per kilowatt-hour as a unit for emissions control measurements.

Over time, a series of standards has been developed. Euro III limits imposed in 2000 were met with the then-current generation of diesel engines, but Euro IV limits, mainly with respect to NOx and PM, required the adoption of catalytic control.

The Euro IV standard has been applied since 2005; Euro V has been mandatory from 2008. Euro VI emissions standards, comparable in stringency to the US 2010 standards, become effective from 2013 (new-type approvals) and 2014 (all registrations). To meet the stricter Euro IV and V regulations, vehicle manufacturers have employed after-treatment technologies such as SCR or exhaust gas recirculation (EGR). The majority of manufacturers in Europe have chosen to use SCR, as this method also allows improved fuel consumption. Euro V was the main reason for starting to use DPFs.

Under Euro VI, heavy-duty vehicles will have to be equipped with DPFs to meet not only particulate mass but also particle number limits.

Japan

In 1997, the Japanese government set new guidelines that require a drastic reduction in the emission of NOx and particulates from diesel-powered vehicles. New standards came into force in 2009 and further reduced NOx and PM levels for diesel-powered vehicles. Japan uses grams per kilometre as a unit for emissions control measurements.

China

Phase IV (similar to Euro IV) is now coming into force and should gradually be implemented by January 2014. China uses grams per kilometre as a unit for emissions control measurements.

Non-road vehicle legislation North America, Europe and Japan have also established standards that apply to non-road vehicles, locomotive and marine engines. These standards are grouped in tiers according to year of manufacture and engine power.

The table below shows current standards and prospective changes in legislation for HDD and non-road vehicles in different regions.

The US has the most progressive standards in HDD with the strictest requirements regarding HC and NOx emissions as well as levels of PM in the exhaust

According to the Euro VI standard all heavy-duty vehicles will have to be equipped with DPFs

North America, Europe and Japan have also established standards that apply to non-road vehicles, locomotive and marine engines

Catalysts and metal recycling Chemicals

32

Summary of fuel emissions standards for HDD

HDD Time frame

CO HC NOx HC&NOx PM Units

Europe Now 1.5 0.46 2 0.02 (gr/KWH) Europe 2014 1.5 0.13 0.4 0.01 (gr/KWH) Japan Now 2.95 0.23 0.9 0.013 gr/km China 2014 1.5 0.46 3.5 0.02 gr/km

US Now 1.55 0.13 0.2 0.14 0.01 gr/bhp-hr Source: Berenberg research

HDD and non-road emissions standards timeline

Source: Johnson Matthey

Value components of the catalyst

The price components of a catalytic converter are shown below.

Price components of a catalytic converter

Substrate, 20%

Chemicals, 20%

Handling, 10%

PGM, 50%

Source: Berenberg research

PGM costs and the costs of the substrate are a pass-through for the catalyst producer. The chemicals portion is where the added value lies; it is the actual catalytic technology, which represents the main part of the catalyst producer’s revenue stream.

PGM costs and the costs of the substrate are a pass-through for the catalyst producer

Catalysts and metal recycling Chemicals

33

Automotive catalysts do not increase the productivity of the process as process catalysts do; however, they are nevertheless critical for auto manufacturers. A catalyst is not a major cost factor, but even slight deficiencies in catalyst performance can cause serious damage to a company’s business. Non-compliance with environmental legislation, caused by the faulty catalyst, can result in substantial financial losses for an auto manufacturer. This is what allows catalyst companies to sustain their operating margin, which is among the highest in the automotive industry.

Operating margins in the auto industry

Sub-sector Average operating margin Auto manufacturers 4.50% Tyres 10% Trunks 8% Diversified 4.50% Catalysts 10% Source: Berenberg research. Diversified includes Lear, Visteon, Johnson Controls, Magna International

Monetary value of the catalyst depends on underlying technology

An internal combustion engine – regardless of whether gasoline- or diesel-fuelled – requires a catalyst volume of roughly the same size as the engine. This means that the monetary value of the catalyst also depends heavily on engine volume. Not only does the volume of PGMs required for the production of the catalyst increase with engine volume, but so does the amount that catalyst companies charge for their services (as normally the complexity of the catalyst also increases with engine volume).

Diesel catalysts require much more sophisticated technology; hence the value of the catalyst for diesel engines is higher than that for gasoline engines. According to Johnson Matthey, a diesel vehicle currently represents 5x the catalyst value of an equivalent gasoline vehicle.

LDVs (independent of legislation and region) require three-way catalysts.

A diesel engine requires different technology depending on the country’s regulation. The chart below illustrates the various technologies used in HDD vehicles.

A diesel vehicle currently represents 5x the catalyst value of an equivalent gasoline vehicle

A catalyst is not a major cost factor, but even slight deficiencies in catalyst performance can cause serious damage to an auto company’s business

Catalysts and metal recycling Chemicals

34

HDD on-/non-road catalyst systems

Source: Umicore

Euro III limits in 2000 were met with the then-current generation of diesel engines but Euro IV limits, mainly with respect to NOx and PM, required the adoption of catalytic control.

A three-way catalyst converts NOx, HC and CO in gasoline applications and contains platinum, palladium and rhodium. Rhodium is as a rule indispensable, while platinum and palladium can be mutually substituted. This substitution effect has led to a considerable increase in the use of palladium in the automotive applications (as palladium is less expensive than platinum). Light-vehicle engine volume varies from 0.7 to four litres, whereas a heavy-duty engine varies from three to eight litres. As a result of the smaller volume and less-favourable product mix, as well as the maturity of the technology, LDV catalysts are the least profitable category for catalyst companies. However, changes in legislation still affect the value of catalyst – for instance, with Euro VI adoption in 2014 we expect the value of gasoline catalysts to increase by c15-20%.

Platinum continues to be the metal of choice for diesel applications because of its higher activity in oxidation reactions under lean conditions.

A DOC oxidises CO and HC into CO2 and H2O; it contains platinum and palladium, although the ratio can vary depending on application.

SCR, which was introduced with Euro V legislation, converts NOX into nitrogen in diesel engines with the help of NH3; it does not require PGMs (ie is PGM-free). Euro V adoption also required a DPF, which traps PM in diesel engines. DPF contains platinum and palladium; the ratio can vary, depending on application.

CDPFs are more complex and require higher PGM content. They contain palladium and platinum. We think that Euro VI legislation will increase the value of the diesel catalyst market in Europe by 2-2.5x.

The relative monetary value of the different types of catalysts is shown in the chart below (CRT is a DPF, patented by Johnson Matthey; CCRT is a CDPF).

Platinum continues to be the metal of choice for diesel applications because of its higher activity in oxidation reactions under lean conditions

LDV catalysts are a less profitable category for the catalyst companies than HDD catalysts

We think that Euro VI legislation will increase the value of diesel catalyst market in Europe by 2-2.5x

Catalysts and metal recycling Chemicals

35

Catalytic technologies for diesel and their value

Source: Johnson Matthey

Catalyst pricing

The technological component is very high in automotive catalysts. The catalyst is not a major cost factor for the auto producer, but even slight deficiencies in catalyst performance can cause serious damage to a company’s business. Non-compliance with environmental legislation, caused by a faulty catalyst, can result in substantial financial losses. Faulty catalysts can also negatively affect fuel efficiency and the functioning of the whole power train.

This gives certain pricing power to the catalyst producers. New catalysts are normally introduced with changes in legislation and producers are able to charge premiums for their products. With time, technology becomes obsolete and competition increases, which pushes the price down.

Catalyst pricing

Source: Johnson Matthey

Catalyst companies therefore need continuous changes in environmental legislation in order to maintain their pricing power.

Catalyst companies need continuous changes in environmental legislation in order to maintain their pricing power

Catalysts and metal recycling Chemicals

36

Precious and rare-earth metals

As precious metals represent around 50% of the catalyst price and the value of the catalytic technology represents only 20%, automotive catalyst producers are not exposed to precious metal price volatility.