Embed Size (px)

Citation preview

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

CASM WORKSHOPBlack- Scholes and Beyond: Pricing Equity

DerivativesMay 16 -18 2014 @ LUMS

Day 1: LECTURE 1OPTIONS

Seema NandaTata Institute of Fundamental Research

Centre for Applicable MathematicsBangalore, India

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Financial Derivative

●What is a financial derivative (aka Contingent Claim)?

Ans: A derivative is a financial instrument whose value depends on the values of other underlying assets such as a stock, a bond, an interest rate etc

● Example 1 : forward contract (simplest derivative)

A forward contract is an agreement to buy or sell an asset at an agreed price (delivery price) at a certain future date. Two parties are involved:One takes a long position i.e. agrees to buy the underlying asset at agreed price and on agreed date. The other takes a short position and agrees to sell the asset on the same date and same price.

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Forward Contract

● Value of forward contract to both parties is ZERO on date of writing the contract. Forward Price is chosen this way.

● Contract is settled at maturity

● At maturity Short position holder delivers asset to Long position holder in return for cash payment = delivery price

As time passes forward price is likely to change. Fwd price = delivery price only at start of contract. Delivery price is contractual so remains the same.

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Forward Contract -example

An investor takes a long position in a forward contract on May 18, 1996 to buy 1 million pounds in 90 days at an exchange rate of $1.80/pound.

Foreign Exchange quotes on May 8, 1996Spot $1.8330 day forward $1.7990 day forward $1.80

What would happen if spot rate at 90 days becomes $1.82?(Spot rate is rate quoted for immediate settlement)

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Forward Contract

Problem 1

Draw a graph representing the payoff Vs underlying asset price for the long position.

Draw a graph representing the payoff Vs asset price for the short position

EXAMPLES of FINANCIAL INSTRUMENTS

Futures and Forwards contracts

Common Stock

Bond

Options

Swaps

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Stocks and Bonds

A business can raise money for its operations in two ways:

●Borrow it from individuals or banks (sell bonds)●Sell an ownership interest i.e sell shares/stocks in the business to interested parties

Bond: a financial instrument issued by a borrower that obligates the issuer to make specified payments to the bond holder over a specified period. A coupon bond obligates the issuer to make coupon (interest) payments over the life of the bond, and then repay the face value at maturity.

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Stocks and Bonds

Common Stock: Equities issued as ownership shares in a publicly held company. Shareholders have voting rights and may receive dividends in proportion to their ownership.

QuestionWhich one is riskier from the investor's perspective? a stock or a bond for the same company?

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Risk-Return Trade-off

● Risk is the chance that an actual return will be different than expected. Risk means you have the possibility of losing some, or even all, of the original investment.

● Technically, this is measured by standard deviation of the return

● The risk/return tradeoff tells us that the higher risk gives us the possibility of higher returns. There are no guarantees.

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Some definitions

RISK:

RISK FREE INVESTMENT :

PORTFOLIO

Gives a guaranteed return (called the risk-free rate of return) with no chance of a default. T-bill rates are considered a proxy for risk-free rate.

Specific and Non-specific. Specific is associated with a Single asset. Non-specific is related to whole market

A collection of investments.

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Present Value/discounting

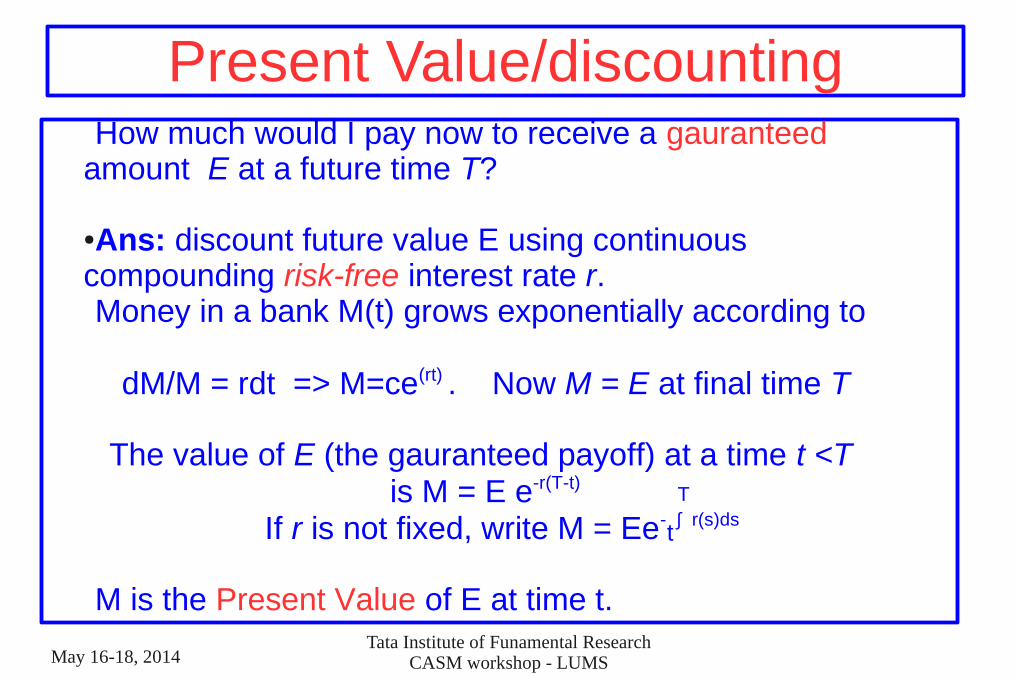

How much would I pay now to receive a gauranteed amount E at a future time T?

●Ans: discount future value E using continuous compounding risk-free interest rate r. Money in a bank M(t) grows exponentially according to

dM/M = rdt => M=ce(rt) . Now M = E at final time T

The value of E (the gauranteed payoff) at a time t <T is M = E e-r(T-t)

If r is not fixed, write M = Ee- ∫ r(s)ds

M is the Present Value of E at time t.

T

t

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

ARBITRAGE

Example: Stock XYZ is traded in NY at $172 and simultaneoulsy in London at ₤100. Exchange rate is $1.75/₤. Simultaneously buying 100 shares in NY and selling them in

London gives the following net result:

100 x [(₤100x 1.75) – $172] = 100X $3 = $300

If instead the shares were traded at $176 in NY, buy in London and sell in NY to get: (100 x $176) – (₤100x 100 x$1.75) = $100.

Arbitrage is the locking in of a riskless profit by simultaneously entering into two or more transactions

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

OPTIONS

Options are derivatives on stocks, currencies, bonds, stock indices, commodities and futures contracts.

Call Option: is a contract which gives the holder (buyer) the right to buy the underlying asset by a certain date (expiration date) at a fixed price (expiration or strike price)

Put Option: gives the holder (buyer) the right to sell the underlying asset by a certain date at a fixed price (expiration or strike price).

There is a cost associated with each optionAmerican Options can be exercised at any time up to the exp. dateEuropean Option can only be exercised on expiration date

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

OPTIONS

Problem 2

Describe a Call Option on a stock from the point of view of the seller (writer)

Describe a Put Option from the point of view of a seller.

In this lecture assume that Options are on stocks. We only analyse European options.

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Example – CALL OPTION

Consider a long position in a call option on IBM shares with a strike at $175 expiring June, 2014. The cost is $2.00 per option. On Aug 30, 2014 IBM shares are at $177.

●Draw the payoff diagram of this position

●Draw a payoff diagram for the short position

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Example – PUT OPTION

Consider an IBM put contract at $160 strike, expiring June 2014. This option costs the buyer $3.85 on Nov 4, 2013. ●Draw the payoff diagram of this position

●Draw a payoff diagram for the short position

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Example Put Option

Collecting $3.85 as the premium represents a 2.4% return against the $160 commitment, or a 3.8% annualized rate of return.

QUESTIONWhat % would the stock have to drop for the

put to be exercised? Spot price of IBM is $179.

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

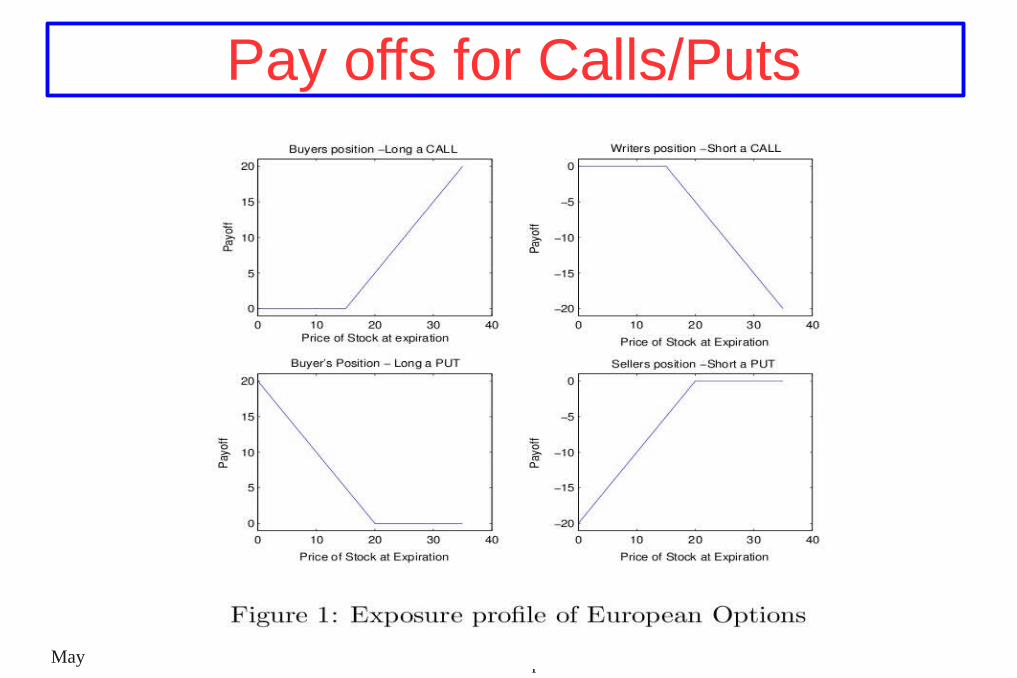

Pay offs for Calls/Puts

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

OPTIONS

Fill in the blanks

Purchaser of a Call Option is hoping that the stock price will ____________

Writer of a Put Option is hoping that the stock price will ________

Purchaser of a Put Option is hoping that the stock price will _________

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

OPTIONSWhy are options used?

- for hedging - for speculation

Speculator will typically buy an option

Hedger will typically write (sell) an option

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Hedging Hedging is the investing in an asset to reduce risk of the overall portfolio.Example: A portfolio contains a put option and a stock. What happens to the value of this portfolio as stock price falls?

stock price declines => the put price goes up.

If portfolio has only puts, value increases as stock price declines.

If it has only stocks, value decreases.

In between there is a ratio of put options and stocks where the portfolio is instantaneously risk-free.

Hedging is risk reduction by taking advantage of such correlations.

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

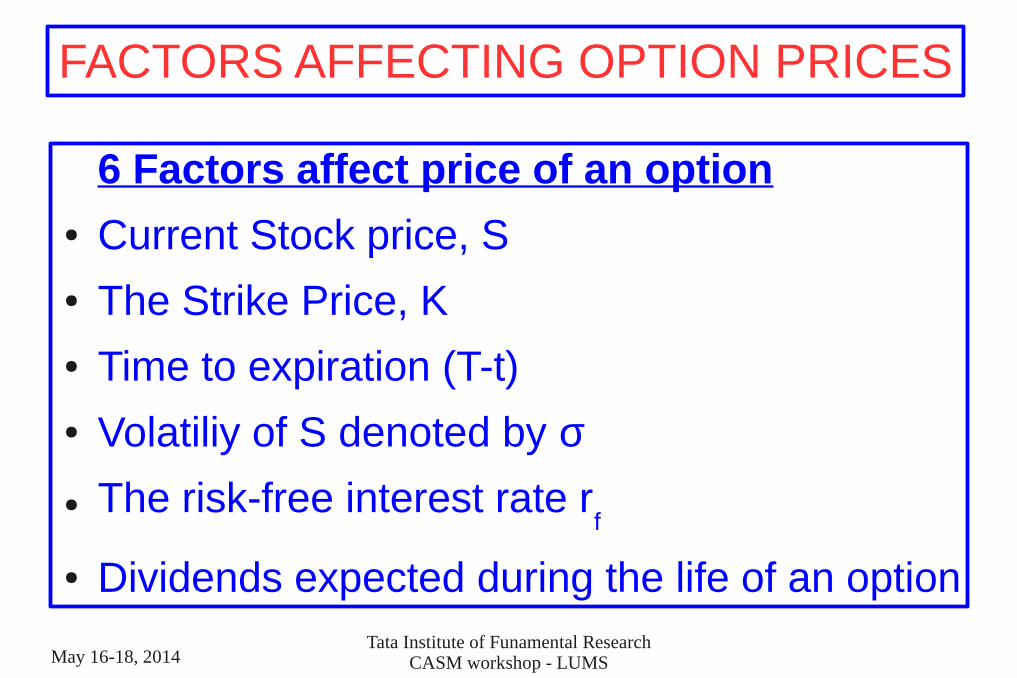

6 Factors affect price of an option● Current Stock price, S● The Strike Price, K● Time to expiration (T-t)● Volatiliy of S denoted by σ

● The risk-free interest rate rf

● Dividends expected during the life of an option

FACTORS AFFECTING OPTION PRICES

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

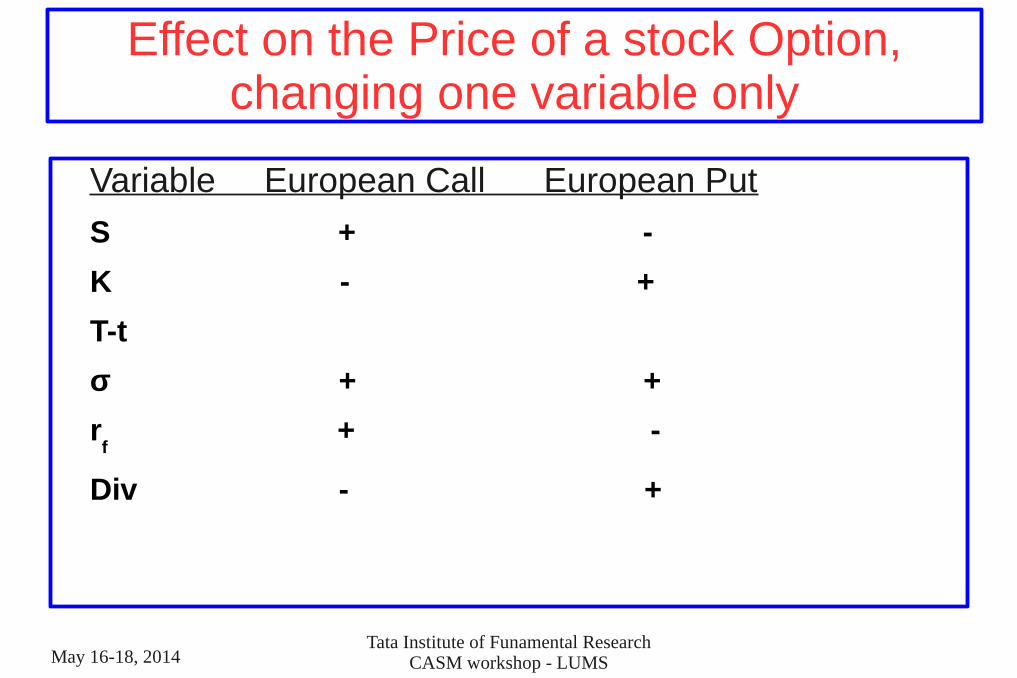

Effect on the Price of a stock Option, changing one variable only

Variable European Call European Put

S + -

K - +

T-t

σ + +

rf

+ -

Div - +

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

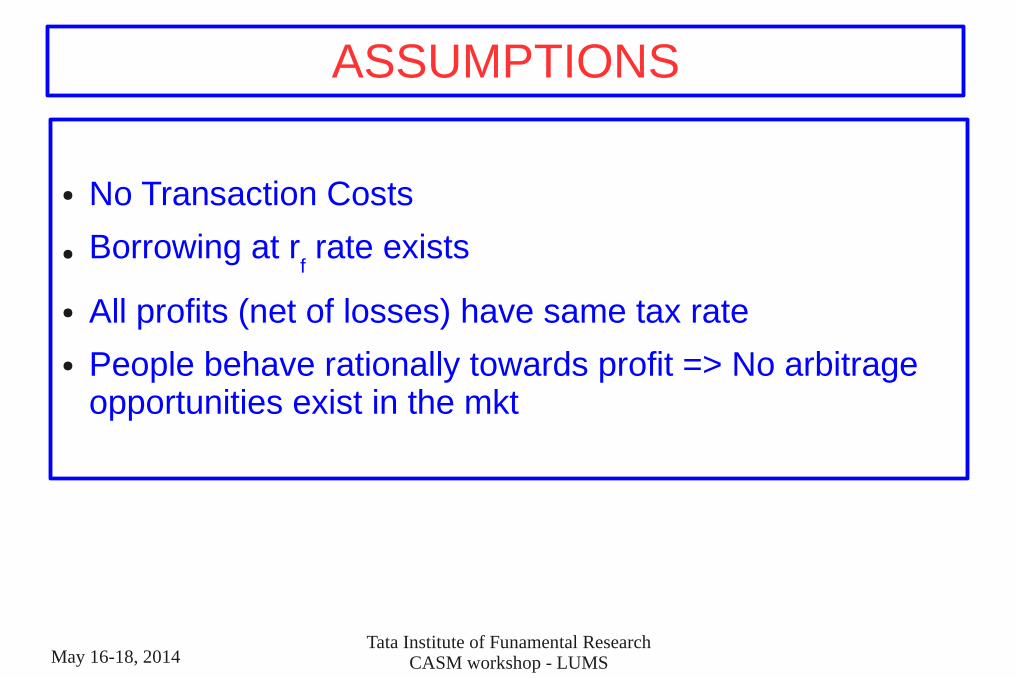

ASSUMPTIONS

● No Transaction Costs

● Borrowing at rf rate exists

● All profits (net of losses) have same tax rate

● People behave rationally towards profit => No arbitrage opportunities exist in the mkt

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

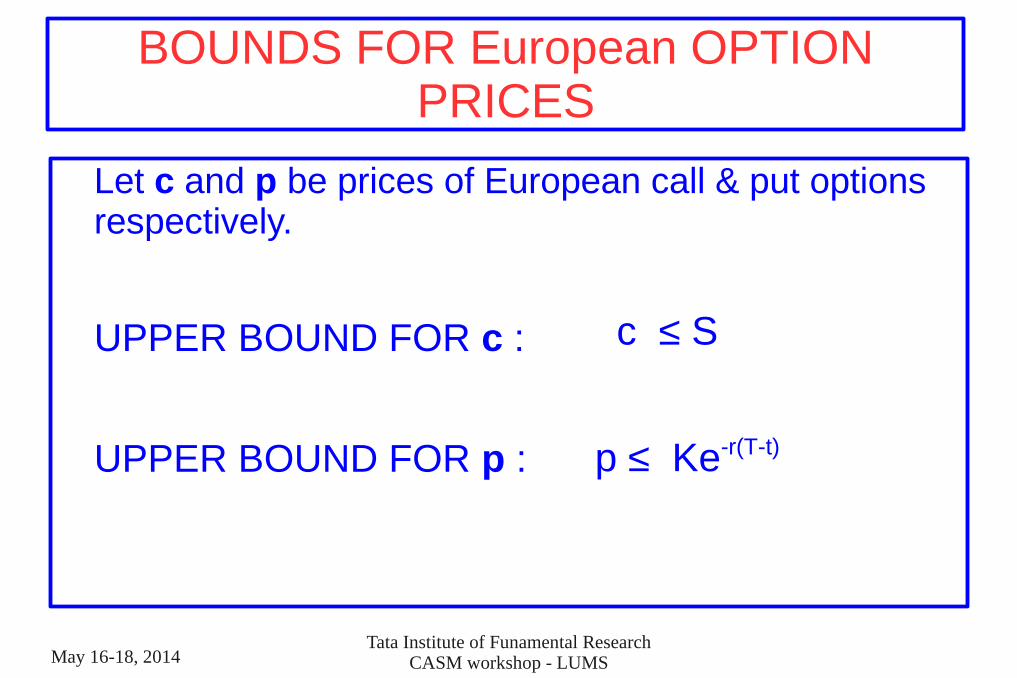

BOUNDS FOR European OPTION PRICES

Let c and p be prices of European call & put options respectively.

UPPER BOUND FOR c :

UPPER BOUND FOR p :

c ≤ S

p ≤ Ke-r(T-t)

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

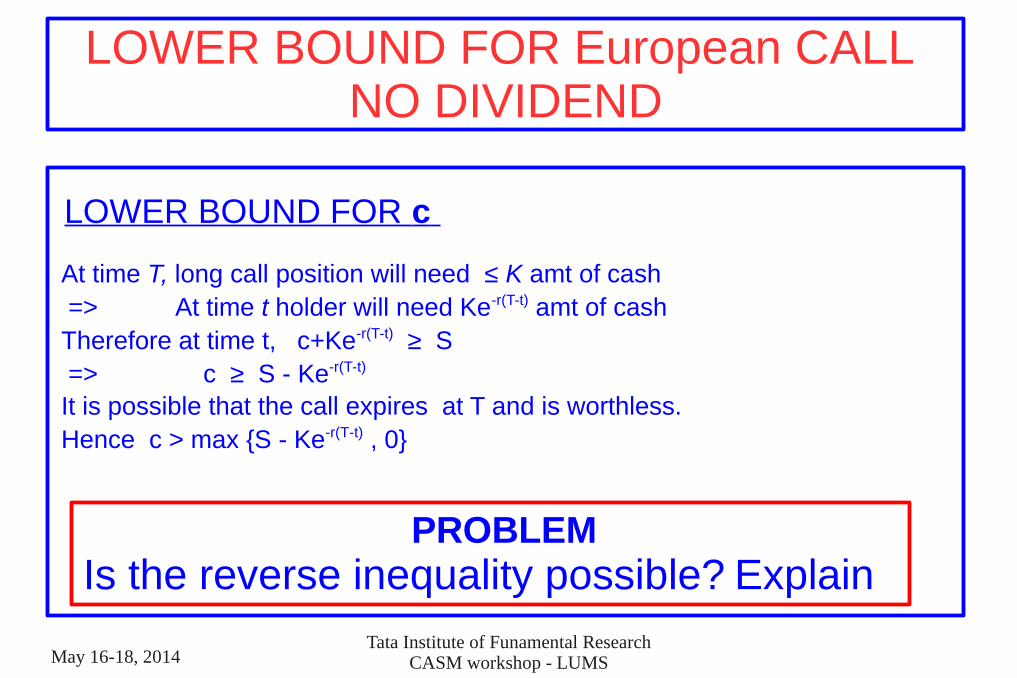

LOWER BOUND FOR European CALL NO DIVIDEND

LOWER BOUND FOR c

At time T, long call position will need ≤ K amt of cash => At time t holder will need Ke-r(T-t) amt of cashTherefore at time t, c+Ke-r(T-t) ≥ S => c ≥ S - Ke-r(T-t)

It is possible that the call expires at T and is worthless.Hence c > max {S - Ke-r(T-t) , 0}

PROBLEMIs the reverse inequality possible? Explain

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

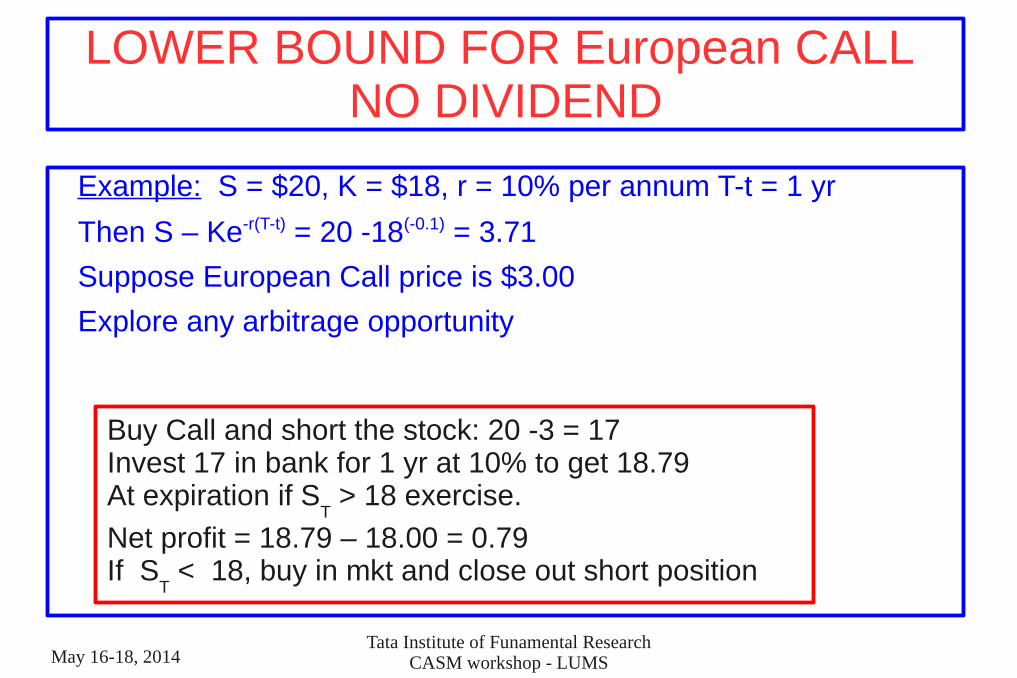

LOWER BOUND FOR European CALL NO DIVIDEND

Example: S = $20, K = $18, r = 10% per annum T-t = 1 yr

Then S – Ke-r(T-t) = 20 -18(-0.1) = 3.71

Suppose European Call price is $3.00

Explore any arbitrage opportunity

Buy Call and short the stock: 20 -3 = 17Invest 17 in bank for 1 yr at 10% to get 18.79At expiration if S

T > 18 exercise.

Net profit = 18.79 – 18.00 = 0.79If S

T < 18, buy in mkt and close out short position

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

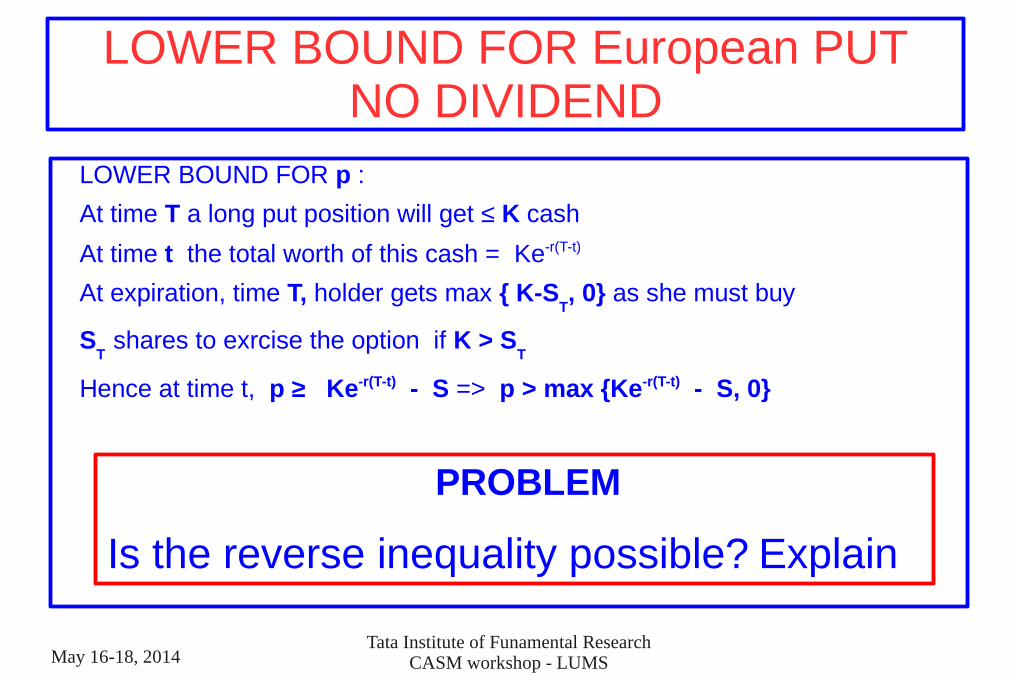

LOWER BOUND FOR European PUTNO DIVIDEND

LOWER BOUND FOR p :

At time T a long put position will get ≤ K cash

At time t the total worth of this cash = Ke-r(T-t)

At expiration, time T, holder gets max { K-ST, 0} as she must buy

ST

shares to exrcise the option if K > ST

Hence at time t, p ≥ Ke-r(T-t) - S => p > max {Ke-r(T-t) - S, 0}

PROBLEM

Is the reverse inequality possible? Explain

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

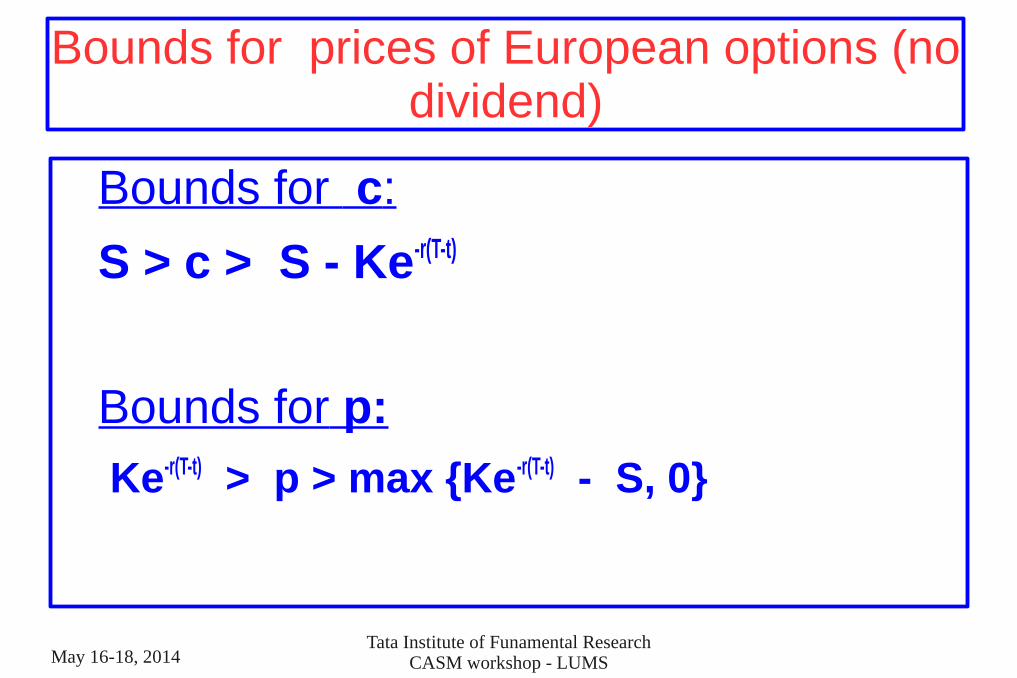

Bounds for prices of European options (no dividend)

Bounds for c:

S > c > S - Ke-r(T-t)

Bounds for p:

Ke-r(T-t) > p > max {Ke-r(T-t) - S, 0}

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

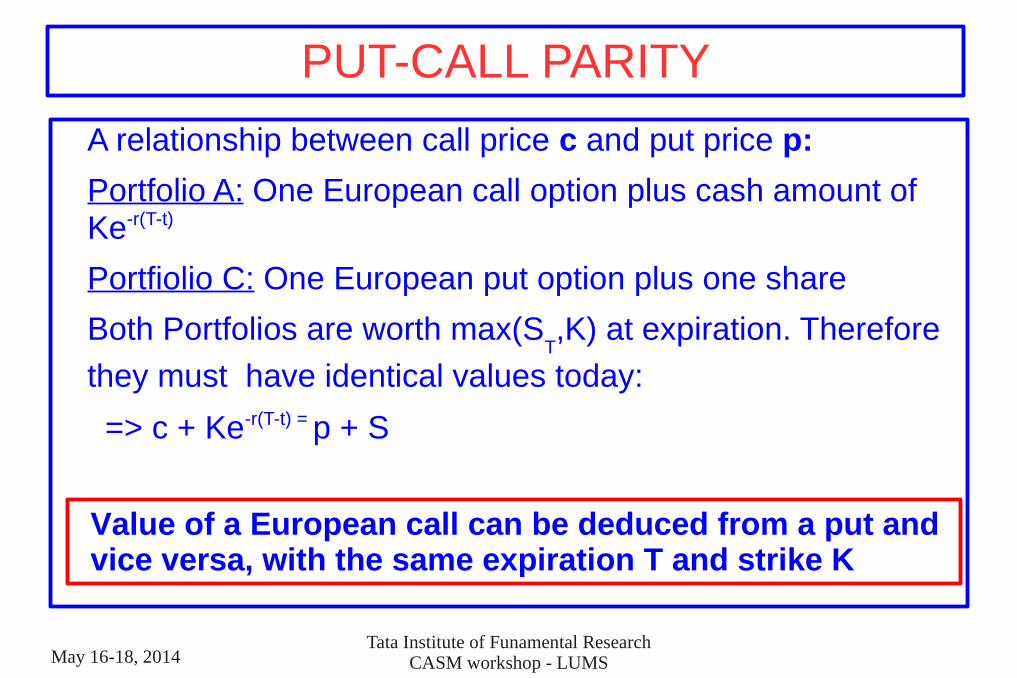

PUT-CALL PARITY

A relationship between call price c and put price p:

Portfolio A: One European call option plus cash amount of Ke-r(T-t)

Portfiolio C: One European put option plus one share

Both Portfolios are worth max(ST,K) at expiration. Therefore

they must have identical values today:

=> c + Ke-r(T-t) = p + S

Value of a European call can be deduced from a put and vice versa, with the same expiration T and strike K

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

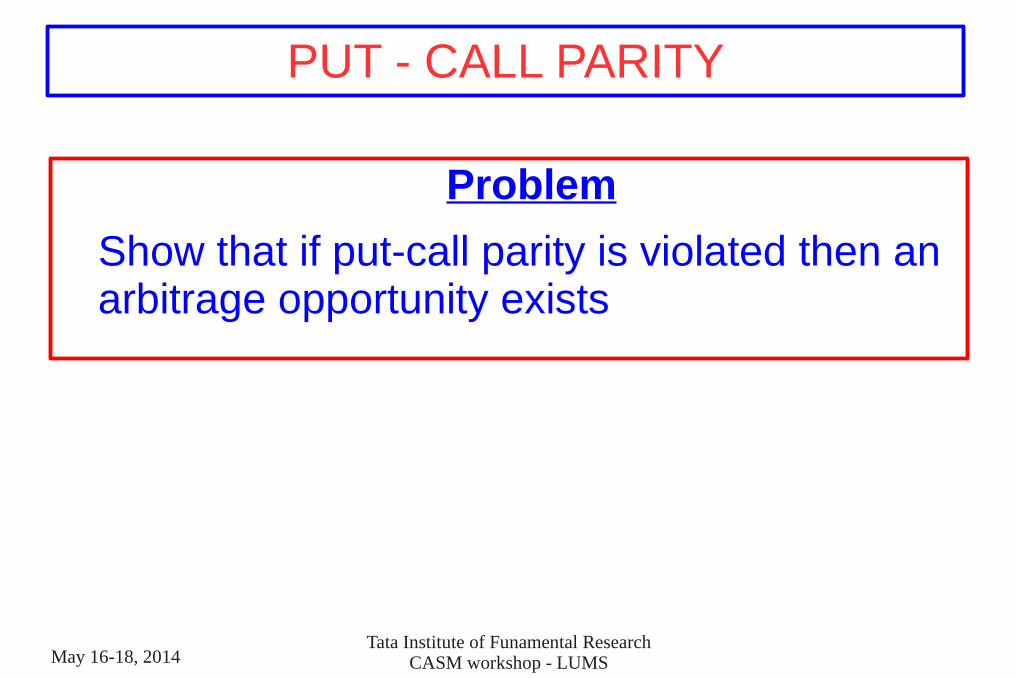

PUT - CALL PARITY

Problem

Show that if put-call parity is violated then an arbitrage opportunity exists

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

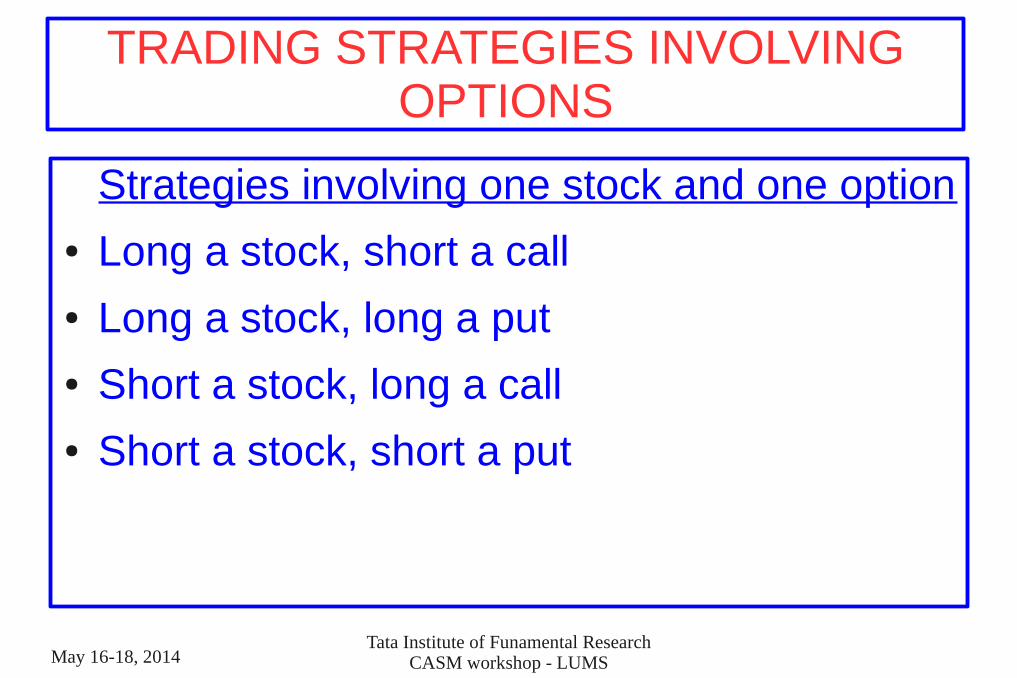

TRADING STRATEGIES INVOLVING OPTIONS

Strategies involving one stock and one option● Long a stock, short a call● Long a stock, long a put● Short a stock, long a call● Short a stock, short a put

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

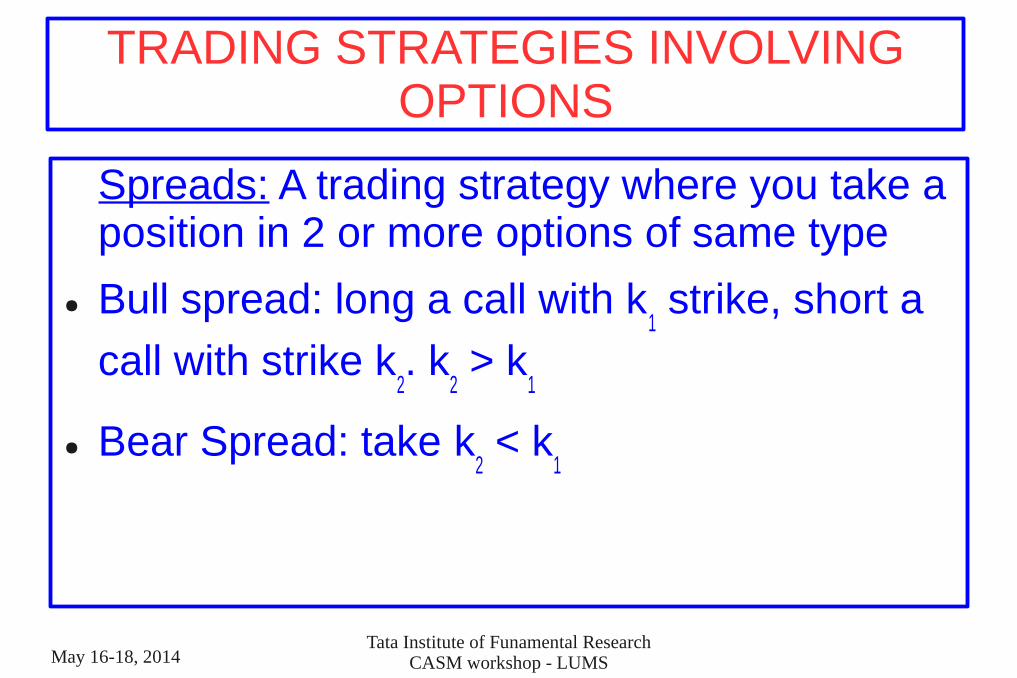

TRADING STRATEGIES INVOLVING OPTIONS

Spreads: A trading strategy where you take a position in 2 or more options of same type

● Bull spread: long a call with k1 strike, short a

call with strike k2. k

2 > k

1

● Bear Spread: take k2 < k

1

May 16-18, 2014Tata Institute of Funamental Research

CASM workshop - LUMS

Home work

Do the problems handed out