Embed Size (px)

Citation preview

Cashout Mergers

Chapter 10 Part 1

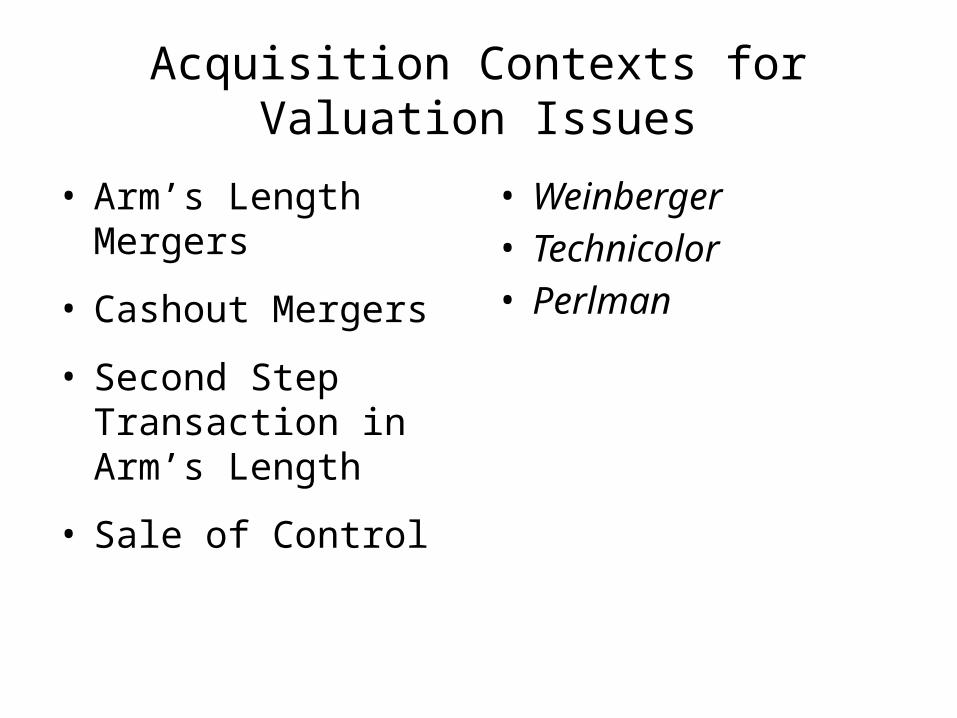

Acquisition Contexts for Valuation Issues

• Arm’s Length Mergers

• Cashout Mergers

• Second Step Transaction in Arm’s Length

• Sale of Control

• Weinberger• Technicolor• Perlman

Signal UOP deal• Signal had earlier divested a division, receiving hundreds of millions

in cash, so looking for an acquisition

• bought 50.5% of UOP, Inc at a large premium over market price.

• At the time it named Signal employees as half of the board members and a Signal employee left the firm to become CEO of the subsidiary.

• That deal had been completed at $21 a share at a time the UOP stock was selling for $14 per share.

• Two years later, having not fully invested the cash, Signal returns to UOP as a possible investment.

• Two Signal executives who were also UOP directors do a study of the possible merger and conclude it would be a good investment for Signal at a price up to $24/share.

Signal UOP negotiations

• There is some appearance of process (at least as compared to Van Gorkom).

• The two CEOs discuss price.

• The board retains an investment banker to provide a fairness opinion.

• Only the independent board members vote.

• Shareholder approval would have to occur by a majority of the minority and enough minority shareholders would have to vote so that the total number of shareholder votes exceeded two‐thirds.

• really isn’t much room to negotiate beyond what Signal wants to do?

Signal UOP questions

• Will this deal create new value?

• What is the basis for the legal challenge?

• How would you have advised Signal so that they would meet their fiduciary duty?

• Does Signal have to disclose its best price, that it is a good investment up to $24?

• What is the remedy?

Weinberger v. UOP: A Cashout Merger

• How was 251(a) met? What was the plan of merger?• How was 251(b) met? Approval by the boards• How was 251(c) met? Approval by shareholders• How was 262(b) met?

UOP SHs

UOPSignal

Should Exit Rights Vary with the Context?

• How did the majority’s transaction change what the minority had in each case?

• What did they have before? And now?• Why should the law protect them?

--against forced to go into a new business? -- against being forced out?

Loral Arco

A SHs

A AssetsL Stock L

Stock UOP SHs

UOPSignal

Weinberger: Risks to Minority

• Is there a risk of majority opportunism?

• Is the risk different than in an arm’s length merger?

• What protection might the law provide?

• Which remedy did the plaintiffs in Weinberger desire? Why?

Valuation in Cashout Context

• 262(h): “fair value exclusive of any element of value arising from…the merger…In determining such fair value, the Court shall take into account all relevant factors.”

• Tri-Continental :“The basic concept..is that the s/h is entitled to be paid for that which has been taken from him, viz, his proportionate interest in a going concern

What Does the Exclusion Mean?

• “Exclusive of any element of value arising from the accomplishment or expectation of the merger”

• “We take this to be a very narrow exception"

• “Elements of future value, including the nature of the enterprise…”

262(h) exclusion• DE Sup Ct makes a significant change in the Delaware appraisal

statute.

• The statute (§262(h)) specifies “the Court shall determine the fair value of the shares exclusive of any element of value arising from the accomplishment or expectation of the merger.”

• A later sentence of (h) provides “In determining such fair value, the Court shall take into account all relevant factors.”

• In putting those two sentences together, the Weinberger court finds the adding of “relevant” in one sentence effectively limits the reach of value arising from the merger so that the excluded term can only be a very narrow exception that would exclude speculative effects from the merger but not effects from the merger that are not speculative.

• Not so much statutory construction as reinterpreting statute to deal with new context

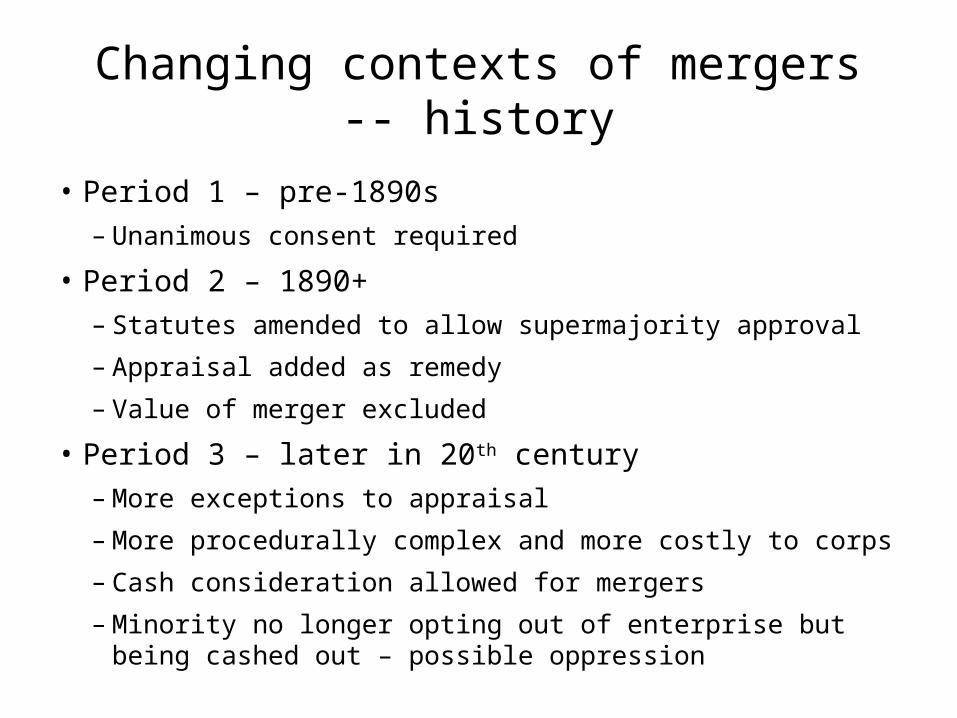

Changing contexts of mergers -- history

• Period 1 – pre-1890s– Unanimous consent required

• Period 2 – 1890+– Statutes amended to allow supermajority approval

– Appraisal added as remedy

– Value of merger excluded

• Period 3 – later in 20th century– More exceptions to appraisal

– More procedurally complex and more costly to corps

– Cash consideration allowed for mergers

– Minority no longer opting out of enterprise but being cashed out – possible oppression

Weinberger Valuation Issues

• Synergy• Minority Discount• Exclusivity– What other remedy might there be?– “We believe that [remedy] is, and hereafter should be, an

appraisal as hereinafter defined– “While a plaintiff’s monetary remedy ordinarily should be

confined to the more liberalized appraisal proceeding herein established,…

Fiduciary Duty in Cashouts

• What is the basis for Shareholder FD claim?

• How will the remedy be different than in appraisal? What is the court’s starting point when SH allege breach of FD?

• What moves the court off this starting point?

• What is the level of judicial review now?

Showing Entire Fairness in Weinberger

• “This conduct hardly meets the fiduciary standards applicable to such transactions.”

• How would you meet that standard? Does majority SH have to pay its top price? $24?

• RofR of 15.7% vs. 15.5% “This was a difference of only 2/10 of 1%, while it meant over $17MM to minority.”

Showing Entire Fairness

• What is the cause of the FD problem?• How might you eliminate that problem?– Board decision delegated to disinterested

members?– Shareholder decision delegated to disinterested

members?– How much disclosure is required?

Cede & Co. v. Technicolor

• Where is the value coming from in this transaction?

• How much?• Who should get it?• Do minority shareholders need protection?

The Technicolor Transaction

• What do we call it?

• Why did the planners pick this structure over alternatives?

• Is it different than Weinberger?

• Should the law’s protection be different?

• What are the plaintiffs seeking to accomplish?

M&F Technicolor

T SHs

T stock

$23 Macanfor

TM&F

Step One Step Two

Technicolor: Business History

Early 1980 Stagnation

May 1981 Kamerman Plan - 1 Hr Photo

$22.13

Sept. 1982 80% Income drop $8.37Oct. 4 Perelman offer $20Oct 27 CEOs agree $23Nov.30 Cash tender offer ends – Majorit

yDec. 3 MAF continues buying

shares83%

December Bd calls SH meetingJan 24 SH meeting: merger

approved

A Brief Review: Legal Protection for Minority Shareholders

• Fiduciary Duty– Judicial review of Director’s actions– Deference (BJR), Intermediate, Entire Fairness– Remedy: Rescissory damages or other equitable relief

• Appraisal– Fair value of the shares– The Weinberger reading of exclusion– Procedural Limitations

Technicolor: Litigation History

• January 1983: Merger & Lawsuit

• 1988 S Ct.: Ch. Ct should not have required election of remedies before trial

• 1990 Ch. Ct trial (47 days) of both claims; battle of experts ($13.14 vs. $62.75)=$21.60

• 1991 Ch Ct on FD: no harm no foul

• 1993 S. Ct remand: appraisal should not have been first; entire fairness as standard

Litigation History II

• Ch. Ct (1994) on FD-entire fairness met• 1995 S. Ct. affirms (contrast to Weinberger)• Ch. Ct (1995) on appraisal – $21.60 again – compound interest @ 10.32% pre-judgment; simple

interest @10.5% post-judgment– Excluding what?

• 1996 S. Ct. now reverses appraisal

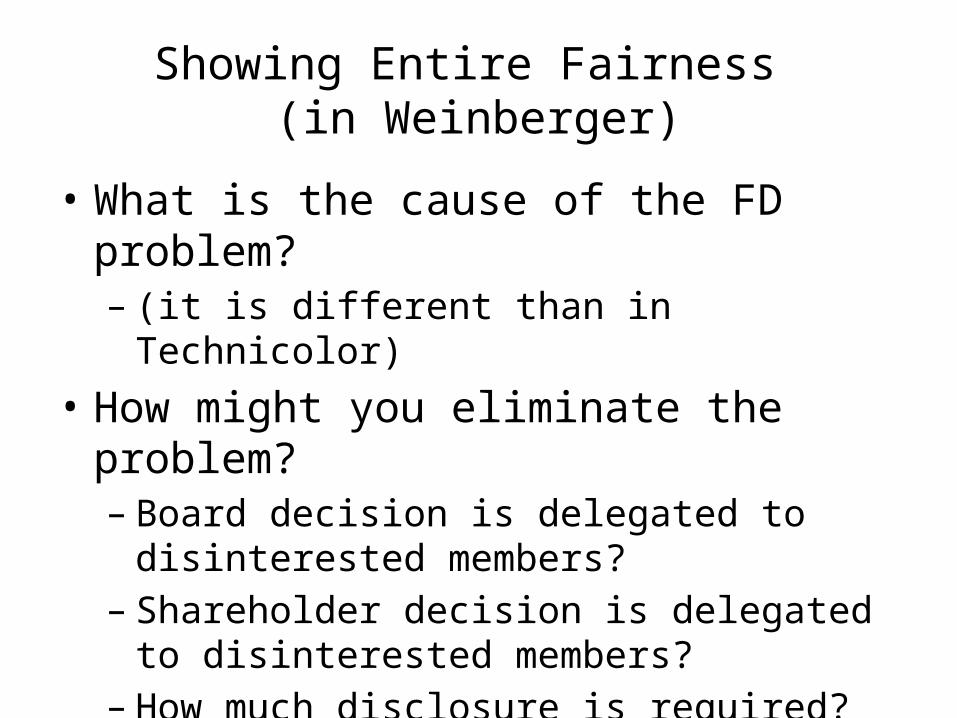

Showing Entire Fairness (in Weinberger)

• What is the cause of the FD problem?– (it is different than in Technicolor)

• How might you eliminate the problem?– Board decision is delegated to disinterested

members?– Shareholder decision is delegated to disinterested

members?– How much disclosure is required?

Appraisal• Fair price--What are we valuing?– In economic terms from last classes

• Is market price as relevant in Technicolor as Weinberger?– In legal terms

• On what day?• Exclusive of any value arising from merger• What economic category of merger gains might exclusion

leave out?• What drives Ch. Ct.?• Why does S.Ct. reverse?

• Procedural structure– what does it tell you about purpose?

Appraisal

• Merger date is after control change and asset restructuring is already underway

• What does the court’s opinion do in terms of allocating the gains from the transaction?

• As a shareholder, what incentive does it give you to change your behavior?

• As a bidder, what incentive does it give to change your behavior?

Technicolor appraisal

Tender offer

mergerSmart Perleman plan

Dumb Kamerman plan

Merger date/appraissal date

Cash flows anticipated

time

The Outcome for Plaintiff• Yet another appraisal

– Dec 2003 $23.33 corrected to $21.98– WACC (equity & debt) 19.89%– When do you get it?

• Time value of money; 7% interest after 1991– Costs?

• Compared to what?• The Last Appeal

– Praising the Chancellor and upholding his valuation choices– But 1990 decision’s WACC (15.28%) is the law of the case and pre-

judgment interest goes through remand– Per share value= $28.41 or $5.6 million for plaintiff– Interest = $46 million