Embed Size (px)

Citation preview

Case Studies in Community−Based Credit Systems for Low−IncomeHousing

Table of ContentsCase Studies in Community−Based Credit Systems for Low−Income Housing.........................................1

FOREWORD..........................................................................................................................................1I. COMMUNITY−BASED CREDIT SYSTEMS: AN OVERVIEW............................................................2

A. Introduction..................................................................................................................................2B. Types of institutions.....................................................................................................................3C. Mobilisation of funds for housing.................................................................................................4D. Allocation of funds for housing....................................................................................................5E. Management and Administration.................................................................................................6F. Types of Loans............................................................................................................................6G. Cost of Loans..............................................................................................................................8H. Linkages......................................................................................................................................9

II. URBAN THRIFT AND CREDIT COOPERATIVE SOCIETIES: A CASE STUDY OF COLOMBO, SRI LANKA......................................................................................................................10

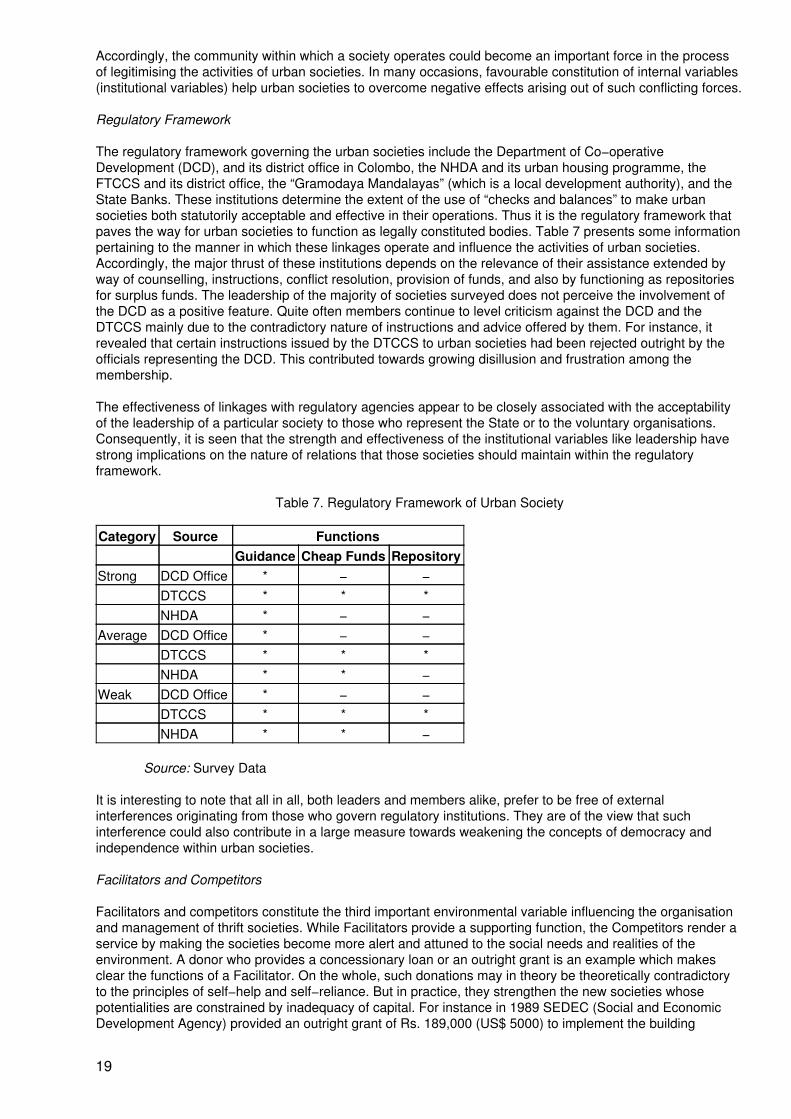

A. Background................................................................................................................................10B. Organisation and Management of Urban TCCSS: Evaluation of Performance.........................14C. Community Participation in Banking and Social Development Through Thrift Societies...........21D. Lessons learnt: Some Recommendations.................................................................................24

III. PUNERVAAS HABITAT AND LIVELIHOOD MOVEMENT, DELHI, INDIA.....................................29A. Background................................................................................................................................29B. The Case Study.........................................................................................................................30C. Lessons Learnt..........................................................................................................................36

IV. MUTUAL AID COOPERATIVE MOVEMENT IN URUGUAY..........................................................38A. Mutual Housing Cooperatives: What They Are and How They Work........................................38B. Advantages of cooperatives......................................................................................................40C. Conditions and replicability........................................................................................................41

V. THE HISTORY OF THE GROUP CREDIT COMPANY: CAPE TOWN, SOUTH AFRICA...............42A. Phase I − Research and Feasibility...........................................................................................42B. Phase II − Pilot...........................................................................................................................43C. Phase III − Expansion: One Region..........................................................................................45D. Phase IV − Multiple Regions.....................................................................................................46E. Phase V − Current Strategy.......................................................................................................51

VI. THE DANISH MODEL.....................................................................................................................52VII. CONCLUSIONS.............................................................................................................................54SELECTED BIBLIOGRAPHY...............................................................................................................55ENDNOTES..........................................................................................................................................56

i

ii

Case Studies in Community−Based Credit Systems for Low−IncomeHousing

UNITED NATIONS CENTRE FOR HUMAN SETTLEMENTS (Habitat)Nairobi, 1995

This document has been reproduced without formal editing

The designations employed and the presentation of the material in this publication do not imply the expressionof any opinion whatsoever on the part of the secretariat of the United Nations concerning the legal status ofany country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers orboundaries.

HS/337/95EISBN 92−1−131298−1

FOREWORD

For good reasons “Community Participation” and “Housing Finance” are two important activity areas ofUNCHS (Habitat). Experience has demonstrated time and again that each of the areas are absolutely crucialto the provision of shelter for the poor. Taken together they can make the difference between being housed orbeing homeless.

Community participation in the field of housing is not confined to finance. In fact, it permeates all kinds ofactivities in the community involved not only in the planning and building of houses but in many other activitiesrelated to the maintenance of structures and infrastructure. In addition it has some important spin−offs interms of learning to organise, manage and to solve problems. In this sense it becomes a valuable exercise indemocracy.

Most housing finance is not done by community groups with democratically elected leaders. But a lot of otherfinance is. Typically, it is in the form of “savings−and−credit societies” or groups with similar designations andfunctions. On the basis of members’ own savings they are known all over the world as providers of small,short−term loans for all kinds of domestic needs. To expand this kind of lending to bigger, longer−term loansfor housing seems obvious. However, as many case studies show, this is a very difficult step to take.

This publication aims to illustrate how some of these problems can be overcome. This is done through theselection of four cases from various parts of the world where conditions differ, but where the object is thesame: Access to housing finance for the poor. The problems encountered are similar, but the solutions are notalways the same. Local traditions, political climate, level of literacy, etc. are some of the many obstacles to thetransition from consumer credit to housing finance.

Some of the cases also show how vital linkages among members and the all important, yet very delicate,“peer pressure” operate to make community−based finance successful. Similarly, the larger organisationsdemonstrate how linkages to formal sector institutions are extremely important for expansion of their capitalbase and their lending activities. The distinction between formal and informal sectors is not always useful. Butin terms of housing finance the interface between them is a very useful concept to explore.

The report draws upon four case studies. One each from India, Sri Lanka, Uruguay and South Africa. Thestudies have not been reprinted in extenso because the aim was to highlight differences rather thansimilarities in problem solving.

Research on housing finance, undertaken by the UNCHS (Habitat), has over the past years focused onmobilization of finance, mortgage instruments and problems of lending for low−income housing. Theseresearch activities have led to a number of publications, including “Mobilization of Financial Resources for

1

Low−income Groups” (HS/167/89E), “Financing Human Settlements Development and Management inDeveloping Countries” (HS/174/89E) and “Case Studies of Innovative Housing finance Institutions”(HS/301/93E).

In contrast to past research which has focused on aspects related to formal finance mechanisms, thispublication presents some examples of informal financial systems. The aim is to contribute to the Centre’son−going activities related to poverty alleviation as well as to the forthcoming Second United NationsConference on Human Settlements (Habitat II). The four case studies show unequivocally thatcommunity−based finance systems can, indeed, become one of the most potent instruments in alleviatingpoverty.

I gratefully acknowledge the contribution of Dr. Niels O. Jorgensen in the preparation of this publication and ofthe case study authors: Sanat Kaul (India), Upali Vidanapathirana (Sri Lanka), Christine Glover (South Africa)and the Centro Cooperativista Uruguayo (Uruguay).

Wally N’DowAssistant Secretary−General

United Nations Centre for Human Settlements (Habitat)

Secretary−GeneralUnited Nations Conference on Human Settlements (Habitat II)

I. COMMUNITY−BASED CREDIT SYSTEMS: AN OVERVIEW

A. Introduction

Finance is one of the most important factors in the provision of housing everywhere, and for low incomefamilies in developing countries it is critical. Like most other families, who want to buy or build a house, theycannot pay for it out of their existing savings. They need access to credit in one form or another.

The formal housing finance systems play a major role in mobilising and allocating funds for housing also indeveloping countries. However, they often fail in providing credit on terms which meet the specialrequirements of those most in need, namely the poor. This situation is understandable from the point of viewof the formal institutions, because there is normally a large effective demand for housing finance fromborrowers who have little or no problem accepting the terms on which such finance is being offered.

It is too simplistic to view the problem of housing finance for the poor as merely a matter of reducing the costof houses through subsidies or the price of finance through lower interest rates. There are many otherconstraints − apart from affordability − to potential borrowers’ willingness to take up a loan. Some of theseconstraints are in areas such as: ownership rights, collateral requirements, unsteady income and cash−flows.

Informal or community−based credit systems have been able to break through some of these barriers whenproviding finance for consumer goods, cattle, seeds, school fees and a variety of other household needs. Insome countries they have also shown an ability to meet the need for low income housing to such an extentthat informal finance, comprising loans from friends, money−lenders and community−based institutions, nowaccounts for 80 per cent of shelter investments in developing countries.1 This fact gives encouragement to ourefforts of describing how such credit systems operate. To disseminate information about their activities shouldstimulate the creation of new user−friendly credit systems and the expansion and strengthening of existingones to the point where they become accepted as part of the formal financial system.

Community−based credit systems − which are an integral part of the so−called informal sector − consist of alarge variety of organisational arrangements ranging from the small locally−based savings and credit clubs tosome large city−based housing co−operatives to nationwide organisations such as the well known GrameenBank in Bangladesh. All of them have certain unique characteristics, but with one thing in common: to extendcredit to their members on the basis of their savings. The distinction between formal and informal is largely afalse dichotomy, but with respect to mobilisation and allocation of funds community−based organisationsdistinguish themselves from formal sector institutions in two important respect:

2

(1) The organisation is owned by its members in equal parts, thus being a democratic entityas opposed to a corporation or company.

(2) With a common bond between members they rely on them to run the organisation throughelected − sometimes paid − leaders and to enforce its rules especially with respect torepayment of loans.

Four case studies form the basis for this publication − two are from Asia, one from Africa and one from LatinAmerica. They are all different in certain respects, and they are used here to illustrate how poor familiesovercome the hurdles which prevent them from being borrowers in the formal housing finance market. Of thetwo cases from Asia one is from India and one from Sri Lanka. There is a case from South Africa while theUruguay case represents Latin America.

The reason for publishing yet another study on housing finance for low income groups is − apart from thesignificance of community−based credit systems − the importance of introducing new paradigms into thefrequently stale discussion of how to “solve” the housing problem in developing countries. Terms such as“housing needs”, “affordability” and “subsidies” have become standard phrases which most people accept asuniversal and virtually static concepts. The result is that the housing problem also becomes static and onewhich can only be tackled (not solved) by cutting costs and increasing subsidies. Instead, concepts such as“effective demand”, “user−value” and “willingness−to−pay” combine well with those long known to communityorganisations, such as “mutuality”, “responsibility” and “self−help”. Possible combinations of new theoreticalconcepts with old, practical approaches are described in the following section (B).

Chapter two is a case study of Urban Thrift and Credit Cooperative Societies in Colombo, Sri Lanka. They areformed within a clear legal framework and characterised by their separation from public sector interference.Membership tends to be from middle and lower−middle income groups where literacy and numeracy are thenorm. Investing in housing is not the only aim of these members, but in those cases members start savingwith their society. These savings will eventually pay for a large part of their house cost.

Chapter three first describes in detail the Indian “Punervaas Habitat and Livelihood Movement”, which is anApex organisation set up to assist housing co−operative societies − much like the National Co−operativeHousing Union in Kenya2 or Technical Service Organisations (TSO) in some Latin American countries. Aspecific example of how it operates is then explained in the case of the Ekta Vihar squatter settlement inDelhi.

In contrast to the Sri Lanka case, chapter four describes a case from Uruguay of state−supported Mutual AidCooperatives typical for many countries in Latin America. It is characterised by its simplicity and for being ableto cope with a high rate of inflation which otherwise discourages long−term savings. But its over−dependencyon the public sector, which by policy or simple directives can spell its demise, is a lesson to heed.

Chapter five is the story of the Group Credit Company in South Africa. While not exactly a success story, ithelps illustrate many of the typical things which can go wrong when trying to transform existing“savings−and−credit” societies (called Stockvels in S.A.) into a housing finance mechanism. The case historyhas been thoroughly analyzed and remedial action taken. It serves as a recipe for new groups who would liketo expand their lending activities from small, short−term consumer loans to large, long−term housing loans.

Finally, chapter six contains some observations on the Danish system of “Mortgage Societies” which hasflourished to the point where 98% of all family homes and many other types of properties are financed throughthem. In this case, what was once a typical community−based housing finance system has transformed itselfinto a very effective formal sector system. The advantages of this transformation will be explained for thebenefit of the inevitable long−term development of informal systems.

B. Types of institutions

The two principle aspects of housing finance are mobilisation and allocation of funds. Both of these functionsare fraught with problems. However, many formal sector institutions let the “market” solve some of them, suchas determining interest rates, others are legislated by the government, such as procedures for repossessions.Competition for savings is tough. Cost of operation is therefore a crucial factor in reducing “the margin” i.e. thedifference between the borrowing and lending rates of interest. Everything else being equal, the institutionwith the lowest margin can attract most business. In principal, this is how the private formal sector works.

3

Public sector institutions, on the other hand, are largely working without competition, because their fundscome from government allocations at below market interest rates, if any at all. Allocation of these funds areoften guided by government directives and are on terms, including rates of interest rates, which are morefavourable than in the private sector. It should be noted, however, that there are institutions wholly owned byGovernment which operate as private sector institutions. They can be ignored for the purpose of thispresentation or be grouped with the first category of institutions.

In terms of their objectives and mode of operation, community−based organisations fall between the formalprivate sector institutions and those in the public sector. Although firmly based in the private domain, theseorganisations mobilise and allocate funds according to criteria similar to what public sector institutions wereset up to follow. The difference being the “common bond” among members which tends to remove theimpersonal and bureaucratic administration of loans in public sector institutions.

C. Mobilisation of funds for housing

As pointed out above, competition for savings is tough − much keener than for loans. In theory there shouldbe no difference, but practice is different in most places, particularly in countries without a fully developedcapital market. There are several reasons for this phenomenon:

− the quality of savings is much more uniform than it is for loans. Savings can be small orlarge, short−or long term, but loans, in addition, have different degrees of risk. It is thereforesafe to assume that, in fact, there is keen competition for “first class” loans

− there is a strong reluctance by housing finance institutions to differentiate interest rates forloans with different kinds of risk or for large and small loans. This fact obviously tends tofavour large loans over small and “safe” loans over more risky ones

− in many countries, Government interferes directly in the capital market either by dictatingmaximum interest rates for certain kinds of loans, such as for housing, or by issuing tax freebonds. The result is that some housing finance institutions buy Government bonds, becausethey get a higher return on them than on housing loans after deduction of administrativeexpenses.

There are several other factors which influence the mobilisation of funds for housing, such as political stabilityand inflation, which are outside the scope of this study. But factors such as: security of funds, return oncapital, terms of savings, rate of loan recovery (because what is collected from existing loans is the mostimportant source of new loan funds). All of these and more will be addressed in turn. It is important to note,however, that if the allocation of resources is interfered with so that they do not seek the investments with thehighest return, less will be saved and the economic health of the whole country will suffer. Because of its highpolitical profile, housing is an investment good which suffers from a lot of − mostly well intended − interferencein terms of capital and land allocation and the supply of infrastructure. In addition inappropriate buildingstandards, complicated conveyancing and other legal and bureaucratic snags create the paradoxical situationwhere it is easier for the poor to mobilise funds for cars than for housing.

Community−based housing finance is in many ways better suited than formal sector institutions to overcomesome of the problems listed above. But some basic problems remain, of which some are common to allhousing finance systems, and others intrinsic to community−based organisations. For instance: selectingleaders, making decisions, to manage and run an administration, dealing with defaulters, etc. How theseproblems are tackled by groups of poor people is the focus of this study.

Whether formal or informal, the best incentive for people to save for housing is for them to see that they are,in the end, rewarded with a loan to buy or build a house. In most private, formal institutions this connection islost as seen from the savers perspective. In public sector institutions it rarely exists, if at all. This is anotherarea where group−based saving has a considerable advantage.

Various incentives to save have been described in numerous case studies. The prospect of a house is one ofthe strongest. An example of this is a Kenyan case3 where groups of people having been allocated servicedsites pooled their building materials loans in order to complete one house at a time, so the income from roomslet could help other members complete their houses in turn. But even more important are the cases wheremembers of the group are gainfully employed in the construction of houses for themselves and other

4

members. In this way they have not only the incentive to save, but a (new) source of income from which tosave.

Some of the more sophisticated savings−and−credit organisations with a record of success, such asJamaica’s Co−operative Credit Union League,4 have managed to link up with formal sector institutions as asource of funds. To be able to use the formal banking and/or Housing Finance sector as lenders of last resortis a natural way for the informal sector to be incorporated in the capital market. More will be said about thissource of funds in the subsection dealing with “linkages”.

D. Allocation of funds for housing

As pointed out above, repayment of loans is the most important source of funds in the long term. It is thereforeimperative that funds are allocated in such a way that they are repaid on time without undue hardship to theborrower. The orthodox approach to this by institutional lenders for housing has been to screen applicants onthe basis of “affordability” defined as a simple relationship between the required monthly payment, and theborrower’s income (usually 25% − 30%). Since these institutions use the “fixed annuity” method of repayment,they effectively bar most low income families from obtaining a loan.

There are, of course, other lending criteria:

− is the applicant’s income stable?− is the property in a “good” area and is it up to standard?− how old is the applicant, − old people need not apply?− can the applicant raise the deposit and all the other fees?− what will happen if the borrower looses his/her job!

From the point of view of a lender comfortably placed in a “sellers market” these are all very reasonableselection criteria. In fact, there is a strong incentive for such an institution to prefer few large loans to manysmall, since each loan costs about the same to process, which is yet another mark against the poor.

One mark for the poor, though seldom recognised in formal sector lending institutions, is that those with smallloans are less likely to default than large borrowers. In the same vein: Women are normally more reliableborrowers than men, and more likely to hang on to the house in times of hardship. This contrasts sharply withthe fact that in several developing countries women cannot own property and can, therefore, not obtain loans.Community groups recognise these facts and consider them when allocating their resources, as several of thecase studies show.

The rigid “affordability” criterion explained above along with an unrealistic repayment method are the maincauses for making poor people “defaulters before the event”. But if the lender operates in a seller’s markettheir is little incentive to innovate. Co−operatives have another perspective on these things, because theirmain objective is different: to help their members acquire a house. In this regard they not only rely on “peerpressure” for members to repay loans, they also try to ascertain what lending terms fit their members best. Afew examples will suffice:

For a poor, self−employed head of household with a fluctuating income, it is most impractical to have to repaya loan according to a fixed annuity schedule at the end of every month. Instead, a repayment schedule whichaims at a certain sum to have been repaid at the end of each year is much more acceptable.

If a member wants to conduct a business from the house or will want to lease some rooms to lodgers, itmakes no sense to restrict the size of the loan to what is justified by “present income”. “Future income” is therelevant criterion in this case. Moreover, the repayments should be lower in the early years of the loan thanlater on. This loan form is called a Graduated Repayment Mortgage or GRM.

Most poor members will have difficulties raising the required “down payment” or deposit on a house whichthey can otherwise demonstrate they can afford. In this case it makes sense to offer 100% loan, if the lendingcommittee agrees. Such a loan may have to be secured by extra collateral e.g. a guarantee from one or moremembers. In one of the case studies, all members are collectively responsible for all loans, in which case thequestion of guarantees does not arise.

5

One of the most controversial issues in community−based lending is the selection of members eligible forallocation of loans. The case studies will describe different selection criteria. There could be the “first come,first served” approach. Seniority of membership i.e. longest saving record, the “smallest loans first” or the“biggest savings first” criteria, or a combination of these. In the Latin American case, a point system of “needs”was established to determine preference in loan allocation.

Whichever selection criteria are chosen, the guiding principle is that allocation procedures satisfy the largestnumber of members in the long term, and that the allocation committee consists of members who are(s)elected on the basis of trust and credibility. In the case of the Delhi squatter cooperative, a conflict arosebetween the elected committee members and the traditional leader in the area. It was eventually resolved byappointing the traditional leader to the committee.

E. Management and Administration

All of the case studies highlight the severest problem for community−based organisations of all kinds: lack ofmanagement and administrative skills. This state of affairs is inevitable in organisations based to a largeextent − initially, at least − on volunteers. This fact, coupled with the inherent “democratic” decision making inall matters make for a very difficult management style. Exacerbating this problem is, more often than not, thelow education level of members.

In sharp contrast to formal sector institutions which theoretically select the most competent person to run theorganisation and pay dearly for the best experts in all aspects of their operations, we are dealing here withalmost the exact opposite situation. This has important consequences for efficiency and cost. Both of theseaspects of running a housing finance co−operative will be dealt with below and highlighted in the case studies.

The first thing members will notice and complain about in a newly formed organisation is if management failsor operates incompetently. In spite of the fact that they may have been directly involved in appointing thepeople in charge, it is typically the real reason for such organisations to collapse. It is difficult to avoid thissituation other than by securing the help of some professionals as in the South African case, or an NGOspecialising in such support activities, as in the Delhi case.

Administrative tasks can be simplified to such an extent that a competent manager can supervise a largenumber of people. Over the years, basic bookkeeping procedures and simple forms have been developed bynational and international NGOs for group savings−and−lending operations. Still, staff need training in usingthem.

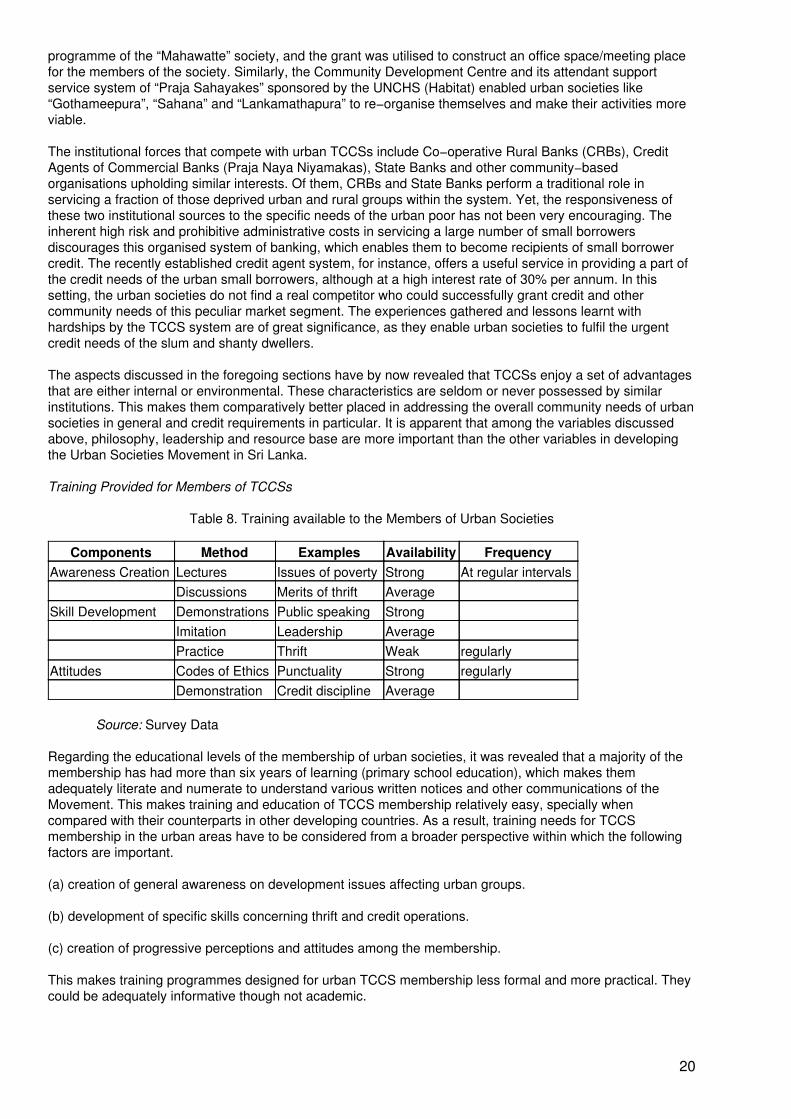

Training of staff is stressed in many case studies.5 This is an on−going activity which assists not only inintroducing new staff to their tasks, but which assures that existing staff is always kept abreast withdevelopments in the organisation and with new techniques and procedures. Training also serves the purposeof keeping staff − and committee members − informed about what goes on in the various departments, so thatthey can easily substitute for each other and, perhaps most importantly, be able to spot irregularities in theprocessing of savings and loans.

The above point cannot be made strongly enough, because fraud, theft, graft and pure incompetence aresome of the typical problems community−based savings and loan organisations have faced over the yearseverywhere. In some cases these problems are solved by “nipping them in the bud” and getting rid of theculprits. In other cases it goes on for some time and leads to the demise of the organisation with severelosses for members as a consequence.

F. Types of Loans

The success or failure of Community−based Housing Finance Institutions (CBHFI) can be very directlyinfluenced by the type of loans they give. For instance: Short−term credits are less risky than long−termhousing loans. The same can be said − with some qualification − for small and large loans. But the use towhich borrowers put their loans is perhaps the most critical aspect of lending. Apart from the pervasive peerpressure, a measure of “carrot and stick” incentives are useful in order to keep members actively engaged inthe activities of their savings−and−loan group and to keep the funds flowing. These incentives can take one ormore of several forms:

6

First, the prospect of getting a loan when a certain savings record has been achieved is themost common as well as the most effective.

Second, small loans initially, which are properly serviced, leads to increased creditworthinessand larger and/or longer loans.

Third, a default on a loan need not lead to permanent exclusion, but it should severely restrictaccess to a new loan for a limited period of time.

Fourth, if goods are purchased for the loan proceeds such goods must act as security alongwith other assets owned by the borrower.

Fifth, in the case of a house purchase, the loan must be secured by the property. If there is noformal title deed a written agreement to this effect is sufficient.

Sixth, mortgage insurance is obligatory in some groups, but could be optional if the housingproduced is collectively owned.

There is always the danger that when all members have acquired houses through loans from the group theycould − intentionally or accidentally − default collectively. If there were no external funds involved, only theirown savings are lost. However uneven individual losses may be, it is not as serious as when the group hasborrowed funds from other institutions. In such cases, depending on the arrangements, members should stillbe collectively responsible and the completed houses ultimately serve as security.

The above scenario was the fate of one of the best known cases in a developing country, namely the “GhanaRoof Loan Scheme”. As the name implies, loans were only granted for roofs, and no new loan could begranted if any of the existing loans were in arrears. Groups were formed on the basis of villages, and when allof the members had acquired their roof they intentionally defaulted. Since no external funds were involvedonly their savings were lost, and since they had all saved the same amount − though some had repaid morethan others − losses were shared. This type of arrangement is also known as a “terminating society” and iswell known from the early history of Building Societies − only in the Ghana case it terminated prematurely.

In modern times and with the groups saving for housing forming mostly in urban areas, the concept ofterminating societies has all but vanished. This is understandable because new members replace those whohave achieved their objective e.g. a house, and have paid off their loans or sold their house to anothermember. In fact, the more sophisticated mortgage societies never question the sale of a house, because thenew owner automatically becomes a member and takes over the existing loan. Exceptionally, the new owneropts to join another society and redeems the existing loan, but that usually involves extra costs and is onlydone, if the other society has more favourable lending terms.

Prevalent among housing finance societies in developed countries, but not limited to them, are such flexibletypes of lending terms as:

− no−deposit loans− graduated repayment loans− choices of variable or fixed interest loans− reversed mortgages− index loans

Among the more innovative loan types in CBHFIs in developing countries are:

− sweat−equity loans− repayment in kind− front−end interest loading− equity loans

A short description of each of these loan types follows:

No−deposit loans or 100% loans are given in circumstance where the borrower cannot find the deposit, butwhere other security than the house is available, e.g. guarantees from fellow members of a savings groupand/or an employer.

7

Graduated repayment loans means that instead of fixed monthly payments which are often incompatible withthe income profile of borrowers over time, the repayment schedule allows smaller payments initially. GRLs arealso known as “progressive annuities”6

Variable or fixed interest loans allows borrowers to opt for one or the other depending on their personalcircumstances and prevailing trends in the capital market. Most people prefer fixed interest rate loans,because there will be no changes in monthly repayments.

Reversed mortgages is a loan form created to serve older members who already have a house with amortgage loan they can no longer afford to service. Interest on the loan − and sometimes a monthly paymentto the borrower − is debited to the loan. The lender ends up holding a claim on the house at the borrower’sdeath which may be higher than the original loan sum, but calculated to be less than the value of the house atthat point in time.

Index loans are similar to GRMs in that repayments are adjusted according to an index of the inflation rate,such as the Consumer Price Index. This loan type resembles the “adjustable balance” loans well known inhigh−inflation countries in Latin America.

Sweat equity loans are given to poor families in the form of credits as the construction progresses and thehouse attains an increasing value. These loans − also known as construction loans − will therefore alsoacknowledge the owner’s own work as a substitute for a deposit. Repayment in kind can sometimes bearranged for a borrower in terms of work on a house of another member or on houses being developed by theCBHFI.

Front−end interest loading implies that interest on a loan is added to the borrowed amount from the start. Thisis similar to how Hire Purchase loans work. Poor families are familiar with them and expect their payment toreduce their indebtedness by the full amount of their payment. This need not result in exorbitant interest rates,if their group knows how to calculate them correctly.

Equity loans simply means that whatever is borrowed becomes equity capital at the original proportion of loanto house value. It stays that way until the owner reduces it by buying back “shares” according to an agreedtime schedule or by choice. Such loans carries little or no interest, since it is assumed that the propertyincreases in value over time.

G. Cost of Loans

It is said that “small is beautiful”, but another saying is just as true in the context of community−based housingfinance, namely “it is expensive to be poor”.

The beauty of being small informal organisations, as opposed to large formal and anonymous institutions, hasalready been described by pointing to the personal treatment and the collective concern for the individual. The“down side” of this personalised service is that this is an expensive way of doing business − even if committeemembers and others work for free and if losses on loans are reduced to a minimum.

The “cost” of housing finance in small groups and in large institutions alike can be measured by the interestrate differential (the difference between what savers receive and what borrowers pay). Although other chargesare often added on to this so that loans become even dearer, it simplifies the analysis to first look at theinterest differential. In savings and loans co−operatives it is common to keep the interest rate for loans doubleof what it is for savings.7 This may sound exorbitant, but that is not necessarily so. In fact, when it isconsidered that saving carries with it a right to borrow, then to save at a lower interest rate is worth more tomany than to get a few percentage points more in a formal institution, but with no such right.

A possible higher rate of interest for loans (though many groups prefer to keep the loan rate the same asformal institutions and the savings rate lower) demonstrates another important aspect of housing finance tolow−income groups: It is less a question of “affordability” than of “accessibility”. The main reason for this is thefact that many house−owners turn their premises into income earning assets, therefore not minding the higherprice of borrowing. A typical example of this scenario is the previously cited Kenyan case, where extra roomsare rented to lodgers at market prices which were higher than the loan repayment for those extra rooms. Inpractical terms, this meant that a given loan was affordable by even poorer families than would otherwisehave been the case.

8

A higher interest differential is also easier to accept for potential borrowers if there are no “extras”, which areso typical in formal private sector institutions. However, it is a fact that many small accounts are moreexpensive to administer than large ones. If the practical handling of savings and loans can be streamlined, forinstance by making collective payments of monthly dues (by employer), cost can be reduced significantly. Thesalary levels of staff is normally lower in community based housing finance, but the fact that they arenon−profit organisations accounts for substantial cost reductions.

In some cases − for instance the Delhi group − it was decided to build up a reserve fund, so that short arrearson loans could be covered without immediate recourse to members. Likewise, some groups decide to includecompulsory insurance in the loan arrangement in such a way that the interest rate differential covers thepremium. These are all collective expenses which members have agreed to or are obliged to pay. In othercases extra charges are optional, such as for having additional (mortgage, life, house) insurance.

As mentioned before, there are economies of scale in housing finance. So if groups want to expand thenumber of members, cost can usually be reduced. The risk is, of course, that the organisation becomesimpersonal and that “peer pressure” is eroded. This tendency need not be all negative. In some developedcountries, as in the case of the Scandinavian countries (see Chapter VI), the organisations have becomesomewhat impersonal, but collective responsibility is maintained and cost of administration has been reducedto the point where the interest differential is significantly lower than in large building societies.

H. Linkages

Informal institutions do not exist in a vacuum and it is important to know the social and economic environmentin which they operate. Needless to say, this environment varies a great deal from one country to another andwithin any given country. Still, there are many similarities and valuable lessons to be learnt by highlightingsome of the typical constellations.

Two kinds of linkages will be addressed:

(1) Membership linkages and (2) Financial linkages.

As regards membership linkages, it is the rule rather than the exception that groups form among individualswith a common bond. This is their strength, because it provides the all important peer pressure. In addition, itmakes communication easier and is more likely to produce leaders who are respected for their communityspirit and competence.

Common place of employment, church affiliation, tribal and ethnic origin, residential area, etc. are traditionalrecruitment bases. Linkages here are to other organisations, such as to the company, the church, burialsocieties, etc. which can be very helpful in terms of moral and practical support. The distinction between basicsavings−and−credit societies and those specialised in housing finance is important in this context, becauseloans are larger and of longer duration. Moreover, property is involved as security and therefore tyingmembers to a certain location.

There are many examples of employers being actively involved in assisting housing finance groups amongtheir staff with land, building materials, administrative services and general encouragement. If this is donewithout such strings attached as having to sell back houses to the employer or to another staff member, this isadvantageous. To attach conditions to who can live in the house or to whom it can be sold or rented is arestriction on normal legal rights of individuals and, in any case, extremely difficult to enforce.

Another crucial linkage for “primary” groups is to an Apex organisation. Such unions or leagues are found inmost countries with an informal savings−and−credit movement. They are useful in a number of ways: Theyprovide practical support with administrative tasks, such as membership books, loan application forms, ledgersheets, bye−laws, etc. Some also provide technical assistance, insurance and guarantees and periodicinspection visits. The bigger organisations become politically influential as lobbyists. But in all cases, they arevaluable sources of information and give status to small and newly formed groups. There is normally a fee tobe paid for this service, but it is worth it, if the Apex organisation is properly run by a democratically electedboard and a competent staff.

Financial linkages are rarer than those for membership, but equally important. As individuals, members ofprimary groups are unlikely to have access to loans from formal sector institutions. This, after all, was the

9

raison d’être for primary groups. Collectively, members represent more continuity and security which is whatformal lenders are looking for. Another attraction for institutional lenders is the ability of primary groups,possibly through their Apex organisation, to perform some of the administrative tasks, such as collection ofpayments and pursuance of arrears. The financial linkage can take different forms depending of thesophistication of the capital market and the track record of primary groups. A simple version is for the primarygroups to have a credit line in a commercial bank secured by its portfolio of loans. This is a usefularrangement, because members’ savings often run out before loans are repaid, thereby restricting the numberof new loans which can be approved. By pledging existing loans as collateral for extra funds, the group’smoney is not completely tied up in long−term loans. Apart from Commercial Banks and Housing FinanceInstitutions, the public sector is also a common lender to primary groups through government−owned banks orspecial funds for housing. There is no reason to make a distinction between public and private sectorinstitutions here, but in practice there can be considerable differences in lending terms and interest rates.There can also be differences in the way resources are allocated. On the positive side, public sectorinstitutions give preference to low−income housing. On the negative side, political preferences sometimesoverrule socio−economic considerations. But formal sector financial institutions are not the only ones knownfor extending loans to community−based housing finance organisations. Insurance Companies, PensionFunds and other institutional investors are known to look for secure, long−term investments. If these consist ofa portfolio of housing loans (mortgages) with more than half of the original loan sum already paid off, thenthey are considered a low−risk investment. If in addition the original lender continues to service these loans,then administrative costs are reduced, making them even more attractive to large investors. The mostadvanced approach to re−financing is the so−called “securitisation” of individual mortgages. This form ofmobilising funds for housing is characteristic for many developed countries (see the case of Denmark). Itworks as outlined above for institutional investors, but instead of selling a portfolio of individual mortgages inone lot, low−denominated shares in this portfolio, which is retained by the primary society, are sold to anyinterested party, including individual savers. These are very popular, because they are secure and yield ahigher rate of interest than is obtained on normal savings accounts.

One of the future linkages for developing countries will be to the international donor agencies. Increasingly,the bilateral agencies in particular will be looking towards viable NGOs for implementing developmentprojects. Experience has shown time and again that there is no shortage of external funds for developmentprojects. The problem of shortage is of viable projects. In this respect, low income housing has the potential ofbeing economically viable as well as socially desirable. An Apex organisation or a co−operative bank will bethe best suited intermediaries for donor funds. However, if these funds are given as loans, not grants, there isa foreign exchange risk which must be hedged against. This risk makes such funds more expensive than theyat first appear.

Over the years, some of the major development agencies have invested millions of dollars in low−incomehousing. The World Bank is the biggest source of funds in this regard. But its funds, unlike those of itssubsidiary, the International Finance Corporation, must go to public sector intermediaries. The second biggestsource, USAID, has a housing guarantee programme which acts as an incentive for financial institutions toinvest in low income housing. Unless borrowers default on their loans the guarantee is not called, and theforeign exchange risk is therefore reduced considerably. A third agency worth mentioning is theCommonwealth Development Corporation which has a long record of investing in equity capital of localhousing finance institutions.

II. URBAN THRIFT AND CREDIT COOPERATIVE SOCIETIES: A CASE STUDY OFCOLOMBO, SRI LANKA

A. Background

Thrift and Credit Co−operative Societies form the oldest type of co−operative institutions in Sri Lanka. Withtheir history dating back to the early parts of this century (1906), credit societies continued to sustain in manyparts of Sri Lanka even during their lean years of 1940’s and 1960’s. Around 1979, the Department ofCo−operative Development of Sri Lanka (DCD) introduced a set of changes to enhance its nationwidecoverage and further revamp the organisational structure of this movement. These changes includeconverting the efficiently run societies into rural banks by granting them limited liability status and morepowers to determine policies and procedures with regard to financial matters. The new policies have made a

10

significant effect on the outlook and status of credit societies; their numbers rapidly escalated, in servicing adiverse cross section of the underprivileged communities of Sri Lanka.

What is a Thrift Society?

As spelled out in the preamble of the Co−operative Credit Societies Ordinance No. 7 of 1911, the broadphilosophy of a Thrift Society (TCCS) encompasses thrift, self−help, and co−operation among agriculturalists,artisans and other persons of limited means.

A thrift society is an autonomous community based organisation (CBO) having a democratically institutedsystem of organisation. At its supreme level, the general membership formulates rules and by−laws and electleaders who are accountable to the membership. This makes Thrift Societies independent from state andpolitical interference.

The other cherished principles of the movement include the promotion of thrift habits, self help and voluntaryaction in order to upgrade self−reliance among its membership and eventually to enhance economic wellbeing of its members. Hence, a thrift society is a democratically instituted community−based organisation thatupholds broader principles of thrift, self help, and co−operation among its members with the intention ofuplifting their standard of living.

Organisational Structure of TCCSs

The organisational structure of a Thrift Society includes the general pattern on which the societies are built,and the relationships that have been established between various levels of the same structure of thismovement. It also covers the basis of ownership as it applies to these societies and also the manner in whichthey are steered and controlled.

Today Thrift Societies in Sri Lanka have a three−tier structure of operations. The Federation of Co−operativeThrift and Credit Societies Limited (FTCCS) which is the apex body of the TCCS movement was formed in1978. This body co−ordinates matters pertaining to overall management and well−being of the District Unionswhich form the secondary level of operations. While the FTCCS functions as the National level co−ordinatingbody, District Unions operate as the co−ordinating body at the district level. There are twenty seven (27)district Unions (DTCCS) established to perform this activity in all the 27 Co−operative districts in Sri Lanka.

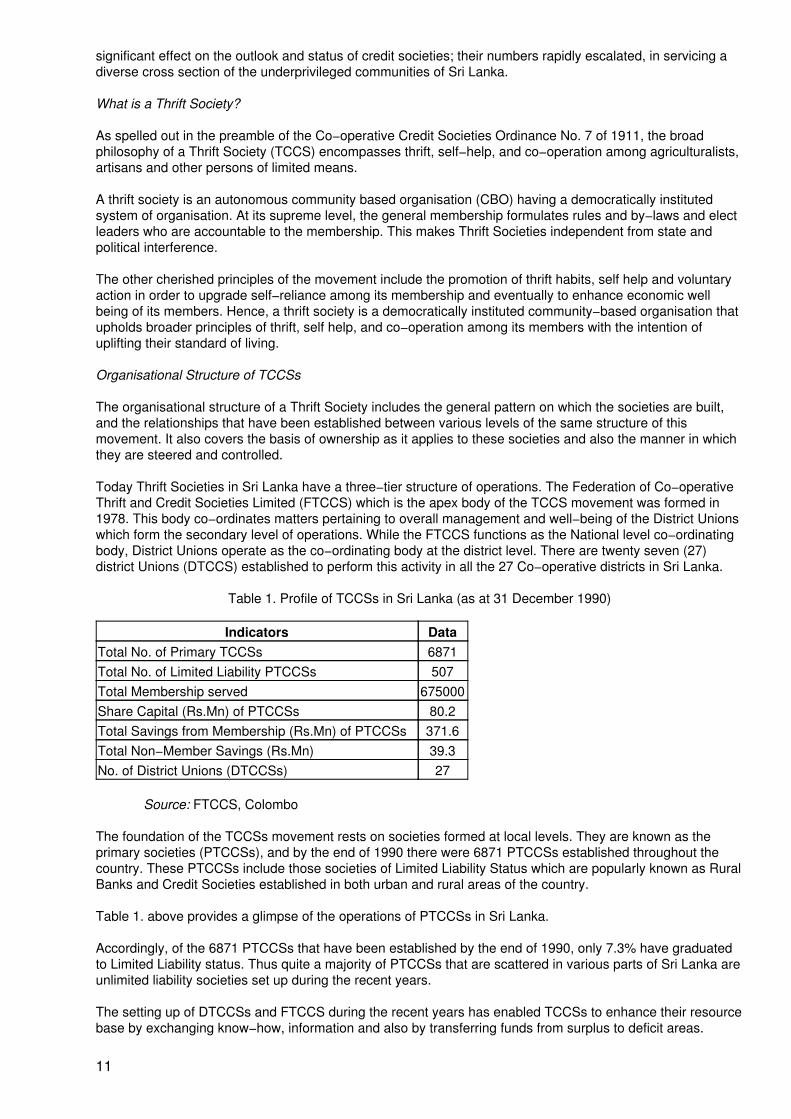

Table 1. Profile of TCCSs in Sri Lanka (as at 31 December 1990)

Indicators DataTotal No. of Primary TCCSs 6871Total No. of Limited Liability PTCCSs 507Total Membership served 675000Share Capital (Rs.Mn) of PTCCSs 80.2Total Savings from Membership (Rs.Mn) of PTCCSs 371.6Total Non−Member Savings (Rs.Mn) 39.3No. of District Unions (DTCCSs) 27

Source: FTCCS, Colombo

The foundation of the TCCSs movement rests on societies formed at local levels. They are known as theprimary societies (PTCCSs), and by the end of 1990 there were 6871 PTCCSs established throughout thecountry. These PTCCSs include those societies of Limited Liability Status which are popularly known as RuralBanks and Credit Societies established in both urban and rural areas of the country.

Table 1. above provides a glimpse of the operations of PTCCSs in Sri Lanka.

Accordingly, of the 6871 PTCCSs that have been established by the end of 1990, only 7.3% have graduatedto Limited Liability status. Thus quite a majority of PTCCSs that are scattered in various parts of Sri Lanka areunlimited liability societies set up during the recent years.

The setting up of DTCCSs and FTCCS during the recent years has enabled TCCSs to enhance their resourcebase by exchanging know−how, information and also by transferring funds from surplus to deficit areas.

11

Neither the Department of Co−operative Development (DCD) nor the Federation stipulates conditions todetermine the optimum size of operation for a Thrift Society. However, depending on the performance ofsocieties, those which are efficiently managed are transformed into banks or Limited Liability Societies. Thismakes the legal framework and the operational capacity of such banks superior to the unlimited societies.

How does a TCCS function?

Flexibility of those transformed societies are quite different from other unlimited societies. This makes thefunctioning of Limited Liability Societies unique, specially when compared with those unlimited societies. Thefollowing sections spell out the similarities and differences in the functioning of TCCSs.

A PTCCS, whether it be a Limited Liability Society or an Unlimited Liability Society is a democratic institutionespousing independence, self−help and voluntary action.

As a democratic institution, the general body forms the most important constituent of the TCCS structure fromwhich power and authority are derived. It is the general body that elects Office bearers including theleadership, and decides on by−laws and other rules. The leadership, and the appointed staff are accountableto the general body and therefore every society which functions properly makes it a point to have meetings ofthe general body once a month. Decisions taken by the Office bearers and various other Committees (e.g.Credit Committees, Women’s Development Committees etc.) are expected to be ratified by the General Bodyat its monthly meetings. This makes the general body the ultimate source of power and authority.

As discussed later those Limited liability Societies have their own offices and a team of appointed staffmembers who perform managerial functions which include the maintenance of accounts. However, in thecase of Unlimited Liability Societies, the overall management including maintenance of accounts and handlingof funds etc. are done by elected members on an honorary basis. Incidentally, almost all the Urban TCCSs inthe district of Colombo belong to this Unlimited category, and thus the majority of these societies do notmaintain offices with regular working hours.

Urban Housing Programme

Notwithstanding some of these success stories, mentioned in the preceding section, there have been fewother areas where TCCSs have not been able to make a successful impact on its membership. These includefacilities for the new irrigation settlements in the Dry Zone of Sri Lanka, and urban settlement developmentschemes in slums and shanties. Ironically, these two areas have been the lead projects in the overalldevelopment strategy of Sri Lanka during the past decade. Of them, the urban housing programme consistedof many facets. This programme included the construction of new flats, housing estates, model villages etc. aswell as improvement of existing slums and shanties.

The first phase of the housing programme was known as the One Hundred Thousand Houses (100,000)programme implemented during the period of 1978 − 1983. The second phase which started in 1984, wasknown as the One Million Houses Programme (MHP) in which the role of the State was changed from itsoriginal provider (or delivery agent) to a facilitator. The emphasis of housing was accordingly shifted from theconcept of constructing physical structures towards a holistic development activity. In theory this approachencompassed, shelter, housing, environment, infrastructure, and human development, leading eventually to abroader socio−economic development process for the beneficiaries.

Evolution of Urban TCCSs

The year 1985 marked another turning point in the history of TCCS movement. In this year Thrift Societies inKandy district joined the National Housing Development Authority in the process of disbursement of housingloans facilitating the One Million Houses Programme. Although this started as a pilot project it was picked upby the other districts, during the years that followed. As a direct response to this enhancement of scope, whichwas found very attractive by many, new societies sprang up in many parts of the country, primarily to obtaineligibility for housing loans.

Unlike the past societies, this new breed of societies did not confine themselves to rural areas alone. Manysocieties came to be established in the urban areas too. It is this scenario that induced the emergence ofmany of the urban TCCSs in the latter part of 1980s. This process which commenced towards late 1986 withinthe city limits of Colombo, showed marked improvement by the end of 1990, (See Table 2 below).

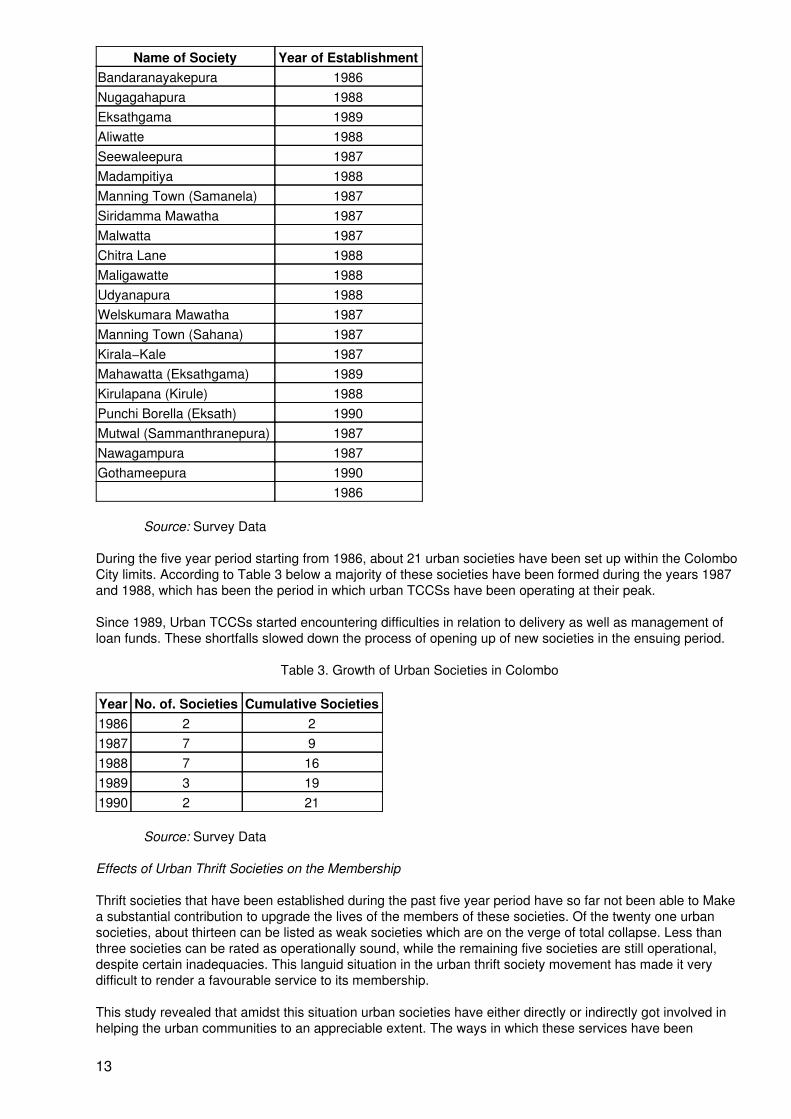

Table 2. Evolution of Urban Societies in Colombo

12

Name of Society Year of EstablishmentBandaranayakepura 1986Nugagahapura 1988Eksathgama 1989Aliwatte 1988Seewaleepura 1987Madampitiya 1988Manning Town (Samanela) 1987Siridamma Mawatha 1987Malwatta 1987Chitra Lane 1988Maligawatte 1988Udyanapura 1988Welskumara Mawatha 1987Manning Town (Sahana) 1987Kirala−Kale 1987Mahawatta (Eksathgama) 1989Kirulapana (Kirule) 1988Punchi Borella (Eksath) 1990Mutwal (Sammanthranepura) 1987Nawagampura 1987Gothameepura 1990

1986

Source: Survey Data

During the five year period starting from 1986, about 21 urban societies have been set up within the ColomboCity limits. According to Table 3 below a majority of these societies have been formed during the years 1987and 1988, which has been the period in which urban TCCSs have been operating at their peak.

Since 1989, Urban TCCSs started encountering difficulties in relation to delivery as well as management ofloan funds. These shortfalls slowed down the process of opening up of new societies in the ensuing period.

Table 3. Growth of Urban Societies in Colombo

Year No. of. Societies Cumulative Societies1986 2 21987 7 91988 7 161989 3 191990 2 21

Source: Survey Data

Effects of Urban Thrift Societies on the Membership

Thrift societies that have been established during the past five year period have so far not been able to Makea substantial contribution to upgrade the lives of the members of these societies. Of the twenty one urbansocieties, about thirteen can be listed as weak societies which are on the verge of total collapse. Less thanthree societies can be rated as operationally sound, while the remaining five societies are still operational,despite certain inadequacies. This languid situation in the urban thrift society movement has made it verydifficult to render a favourable service to its membership.

This study revealed that amidst this situation urban societies have either directly or indirectly got involved inhelping the urban communities to an appreciable extent. The ways in which these services have been

13

performed are manyfold. Urban Thrift societies in many places have been able to act as a harbinger in theprocess of mobilising self−help and co−operation among its members. A message concerning the benefits ofthrift and self reliance and the merits of democratic action has been conveyed to many of these members whohave still not rejected them, despite the inadequacies that prevail. It was also revealed that a majority of themembership of weak societies earnestly wanted to activate them, after rectifying their weaknesses.

Some of the more tangible benefits of the movement, according to a sample survey were as follows:

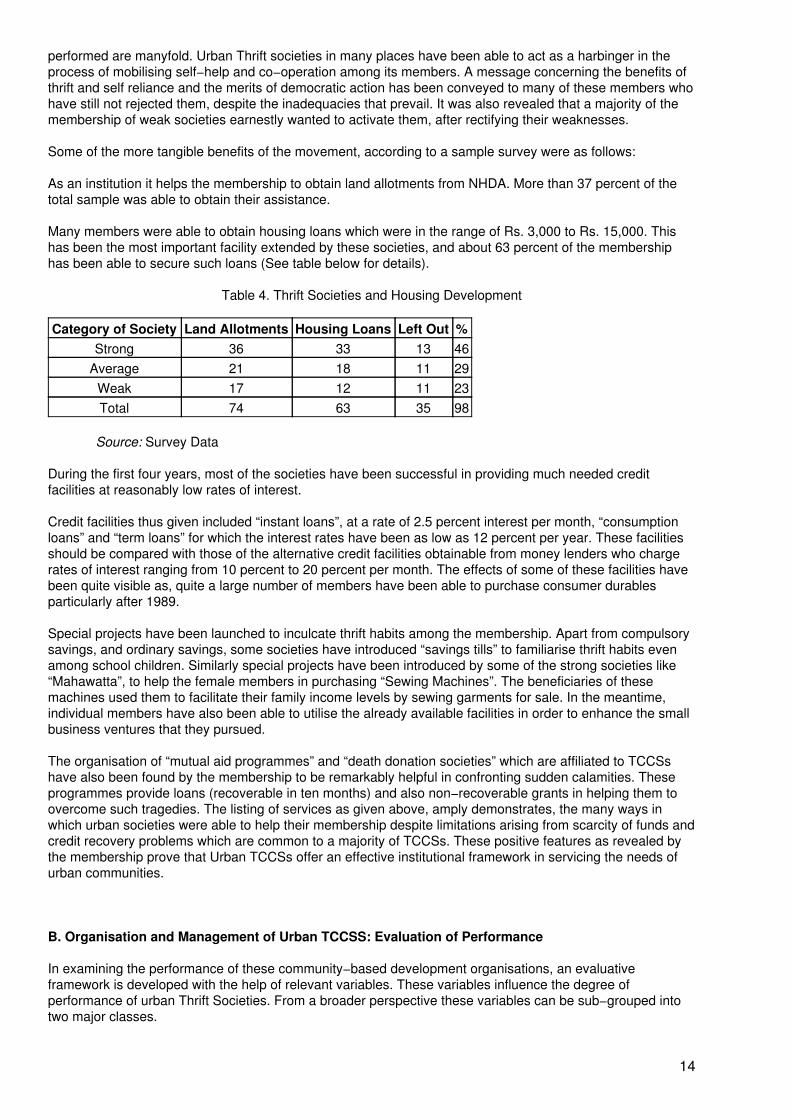

As an institution it helps the membership to obtain land allotments from NHDA. More than 37 percent of thetotal sample was able to obtain their assistance.

Many members were able to obtain housing loans which were in the range of Rs. 3,000 to Rs. 15,000. Thishas been the most important facility extended by these societies, and about 63 percent of the membershiphas been able to secure such loans (See table below for details).

Table 4. Thrift Societies and Housing Development

Category of Society Land Allotments Housing Loans Left Out %Strong 36 33 13 46

Average 21 18 11 29Weak 17 12 11 23Total 74 63 35 98

Source: Survey Data

During the first four years, most of the societies have been successful in providing much needed creditfacilities at reasonably low rates of interest.

Credit facilities thus given included “instant loans”, at a rate of 2.5 percent interest per month, “consumptionloans” and “term loans” for which the interest rates have been as low as 12 percent per year. These facilitiesshould be compared with those of the alternative credit facilities obtainable from money lenders who chargerates of interest ranging from 10 percent to 20 percent per month. The effects of some of these facilities havebeen quite visible as, quite a large number of members have been able to purchase consumer durablesparticularly after 1989.

Special projects have been launched to inculcate thrift habits among the membership. Apart from compulsorysavings, and ordinary savings, some societies have introduced “savings tills” to familiarise thrift habits evenamong school children. Similarly special projects have been introduced by some of the strong societies like“Mahawatta”, to help the female members in purchasing “Sewing Machines”. The beneficiaries of thesemachines used them to facilitate their family income levels by sewing garments for sale. In the meantime,individual members have also been able to utilise the already available facilities in order to enhance the smallbusiness ventures that they pursued.

The organisation of “mutual aid programmes” and “death donation societies” which are affiliated to TCCSshave also been found by the membership to be remarkably helpful in confronting sudden calamities. Theseprogrammes provide loans (recoverable in ten months) and also non−recoverable grants in helping them toovercome such tragedies. The listing of services as given above, amply demonstrates, the many ways inwhich urban societies were able to help their membership despite limitations arising from scarcity of funds andcredit recovery problems which are common to a majority of TCCSs. These positive features as revealed bythe membership prove that Urban TCCSs offer an effective institutional framework in servicing the needs ofurban communities.

B. Organisation and Management of Urban TCCSS: Evaluation of Performance

In examining the performance of these community−based development organisations, an evaluativeframework is developed with the help of relevant variables. These variables influence the degree ofperformance of urban Thrift Societies. From a broader perspective these variables can be sub−grouped intotwo major classes.

14

Institutional variables and environmental variables

Institutional variables refer to those internal forces which influence the success of TCCSs as they continue totransform urban societies. The study revealed that the following institutional variables are relevant inunderstanding the internal capabilities of urban societies.

1. Mission and Philosophy2. Leadership3. Membership4. Strategies employed5. Internal structure6. Resource Base

Environmental Variables are the external forces that influence the nature and the extent of interactions thaturban societies maintain with the world outside. The following forces are considered very important in thissphere:

1. Urban Community2. Regulatory Framework3. Facilitators and Competitors

Mission and Philosophy

This study found that the mission of urban societies is to provide more humane solutions to human problemsfaced by the low income groups living in housing estates, slums and shanties. As seen in the case of urbansocieties, the overall deterioration of socio−economic conditions that result in deprivation, poverty and lowincome is the most central crisis encountered by these communities. Urban societies are expected to initiatecommunity action to reverse this process and upgrade living standards of their membership.

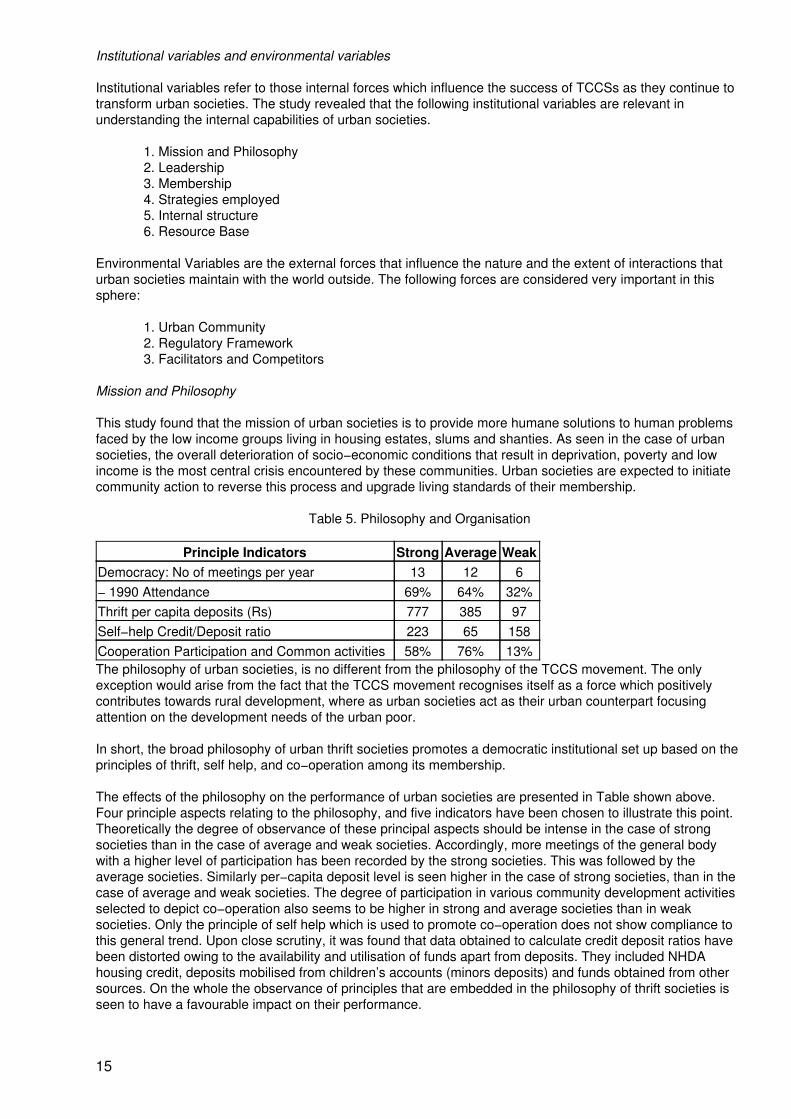

Table 5. Philosophy and Organisation

Principle Indicators Strong Average WeakDemocracy: No of meetings per year 13 12 6− 1990 Attendance 69% 64% 32%Thrift per capita deposits (Rs) 777 385 97Self−help Credit/Deposit ratio 223 65 158Cooperation Participation and Common activities 58% 76% 13%The philosophy of urban societies, is no different from the philosophy of the TCCS movement. The onlyexception would arise from the fact that the TCCS movement recognises itself as a force which positivelycontributes towards rural development, where as urban societies act as their urban counterpart focusingattention on the development needs of the urban poor.

In short, the broad philosophy of urban thrift societies promotes a democratic institutional set up based on theprinciples of thrift, self help, and co−operation among its membership.

The effects of the philosophy on the performance of urban societies are presented in Table shown above.Four principle aspects relating to the philosophy, and five indicators have been chosen to illustrate this point.Theoretically the degree of observance of these principal aspects should be intense in the case of strongsocieties than in the case of average and weak societies. Accordingly, more meetings of the general bodywith a higher level of participation has been recorded by the strong societies. This was followed by theaverage societies. Similarly per−capita deposit level is seen higher in the case of strong societies, than in thecase of average and weak societies. The degree of participation in various community development activitiesselected to depict co−operation also seems to be higher in strong and average societies than in weaksocieties. Only the principle of self help which is used to promote co−operation does not show compliance tothis general trend. Upon close scrutiny, it was found that data obtained to calculate credit deposit ratios havebeen distorted owing to the availability and utilisation of funds apart from deposits. They included NHDAhousing credit, deposits mobilised from children’s accounts (minors deposits) and funds obtained from othersources. On the whole the observance of principles that are embedded in the philosophy of thrift societies isseen to have a favourable impact on their performance.

15

Leadership

In the context of urban societies policy making is generally carried out by a team of persons or an individualrepresenting the leadership. They also translate policy into concrete action by taking initiatives of bothstrategic and operational importance. Such actions are meant to facilitate organisational relationships byproviding direction and guidelines. Accordingly, philosophy, leadership and strategy are seen to be stronglyinterrelated.

The general pattern of leadership in urban societies indicate a heavy concentration of power, authority andfunctions on a single person. In this respect, the degree of charisma of the president determines the destiny ofthe society. For instance, the controversy surrounding the arrest and imprisonment of the President of“Seewaleepura” society gave rise to its decline in 1990.

Leadership comprises the president and his Committee who are elected once a year by the generalmembership. The size of the Committee does not exceed seven persons. Although President often appearsas the most influential person, there are instances, where “back seat driving” by a powerful Committeemember becomes more prominent than the actions of the President designate.

Functioning as a leader of an urban thrift society appears to be on extremely difficult task. When electing aleader the membership is often mindful of a variety of qualities like integrity, experience social status,boldness, ability to make decisions, and ultimately the ability to communicate and implement decisions madeby the leadership. The story of a powerful urban society is quite often a story of a powerful leader. This hasbeen adequately reflected in the Mahawatta Society. In contrast, both “Samanala”, and “Bandaranaikepura”Societies have become failures mainly due to the shortfalls of their leadership. In the case ofBandaranaikepura, the society has been established so that some members could obtain eligibility to beelected into the “Pradeshiya Sabha” which is a statutory body set up to assist the divisional administration ofthe country.

In a stable society although the leadership performs only an honorary job, it is also expected to execute avariety of other routine and innovative operations. Those routine operations include conducting meetings,maintenance of accounts and other records, safe custody of petty cash, evaluation of credit limits etc. Theinnovative operations include settlement of conflicts within membership, between leadership and membershipand between the society and outside institutions. Such operations also include formulation of projects like the“Sewing Machine Scheme” or the “Till system”. Such innovative tasks were undertaken by the “Mahawatte”society, which received appreciation of the entire membership. Leadership thus, becomes one of the mostimportant organisational variables of Urban Thrift Societies.

Membership

The general body or the membership is yet another important variable that influences the level of performanceof an urban thrift society. The research revealed that a majority of the members of the six societies surveyedare poverty stricken. This makes the membership more homogeneous in terms of their economic standing.Yet, there are many differences that arise from other sources such as ethnicity, religion, birth place and moreimportantly the attitudes and expectations concerning this movement. In−depth discussions carried out by theresearch team revealed that the attitudes of members towards weak societies have been distinctly differentfrom the attitudes held concerning strong societies. In the case of weak societies, the membership generallyperceived thrift societies merely as a short−cut to obtain eligibility for loans, which they consider asgovernment doles which are further interpreted as pre−election bonuses. The expectations as a result havebeen to use these societies merely to obtain this particular eligibility. On the other hand, the membership ofstrong societies view their own societies as the only effective mode to overcome their present plight arisingfrom poverty and indebtedness. These differences in attitudes and expectations among members have beencreated partly by the leadership of the societies, and partly by other outside forces, which make themembership of these societies quite heterogeneous. It was found that a number of the members who wereinterviewed later realised their inadequacies and were willing to change, and allow room for counselling andeducation.

Strategies Employed

Aspects of goal setting, selecting a course of action, and its implementation demand a considerable time andeffort of the leadership of thrift societies. It should also be noted that there is a conspicuous absence of formalstrategies and programmes of action in many of the urban societies. Yet, leaders of those strong and effectivesocieties have their own ways of formulating goals and designing mechanisms through which they could

16

achieve results. For example, the goals of “Mahawatta” for the year 1990 had been to raise funds (deposits),expansion of membership and formulation of self−employment projects for unemployed youth and women.This society has been successful in expanding its membership to 273, thus opening 136 minors accounts.New Credit facilities have been implemented to finance self employment projects in the spheres of cottagelevel manufacturing of garments, and providing food preparations for the urban market. In contrast, strategyformulation is almost absent in societies where leadership has been ineffective.

Internal Structure

The internal structure of all the six societies have been similar in principle although differences exist when itcomes to their functioning. These differences that have a bearing on different categories of societies arise outof the degree of interactions that take place between the general body and the leadership. In more vibrantsocieties like “Mahawatta”, the general body is not only seemingly active but it also closely follows the stepstaken by the leadership. On the contrary, in the case of weak societies, the general body is very looselyformulated, resulting in limited interactions between the nominal leadership and its membership.

Resource Base

In general the resource base of urban societies includes not only the financial component (funds raisedthrough share capital, member and non member deposits, external assistance, profit reserves and fundscollected through other means) but also material and human components. Among these, the fixed capital(including buildings and equipment) and the quality and morale of the membership constitute a significantpart.

Financial set up of Thrift societies would mean its structure, (e.g. deposit mix giving interest rates and othercosts) composition, (e.g. how much of total funds are derived from share issues, deposits, and outsideassistance) and sources (from what sources these societies raise funds). These different aspects usuallyhave different outcomes pertaining to the effectiveness of societies. For instance, it is those combinations thatdetermine the volume of funds of the societies and also the extent of dependence on other organisations. Asociety that can manage on low operational costs and its own resources could be stronger and moreindependent in its operations than other societies without such ability.

Funds raised through membership shares constitute one of the most important sources of finance of newlyinstituted societies. This enables a society to have a share capital fund which is theoretically proportionate toits membership. In practice, members have the option of making the full share capital contribution of Rs.100/− at once, or in ten equal instalments. Consequently, at any given point of time, the share capital fundcould be equivalent to the sum of number of members into Rs. 100/− or less. From the point of view of themanagement of a society, this fund is an important source, though members consider it to be a deadinvestment. It is neither liquid (withdrawable at any time) nor interest bearing. In the history of the TCCSmovement, it is rarely that dividends have been paid to share holders even by the profitable societies.Consequently, many members perceive this fund to be an unrealistic source although it does serve a usefulpurpose.

The deposit mix of urban societies consists of three major types of deposits having different interest rates andmaturity patterns. They are (a) compulsory savings deposits (b) normal savings deposits and (c) specialsavings deposits. Of these, the compulsory savings deposit is an instrument designed to inculcate the thrifthabit as a regular and a consistent component of the lifestyle of its members. Each member is expected todeposit Rs. 5.00 per month and this makes the compulsory savings fund growing source of finance. This is aninterest bearing deposit which also makes the depositors eligible for credit facilities.

Normal savings deposits form the most important source of funds in the deposit mix of Urban TCCSs.Members can make contributions to this account at their own pace and by amounts convenient to them. Aswithdrawal of money from these deposits can be made on demand, the type is distinctly different fromcompulsory savings. These depositors are paid a comparatively high rate of interest. The final type which isknown as special deposit schemes consist of those innovative savings methods formulated by differentsocieties. Few examples would be the “till system”, and the children’s accounts etc. These accounts also bearinterest, although funds lying in these accounts are not withdrawable on demand.

The bulk of urban societies entertain non−member deposits for safe custody for which an interest is paid. Nonmembers can open ordinary savings account(s) or minors accounts, but they are not eligible for credit facilitiesfrom urban societies. Another major source of funds for Urban thrift societies is the assistance received fromoutside agencies. This can either be in the form of loans or in the form of grants. Some of the important

17

sources of outside financing consist of NHDA loans, funds available under the inter−lending programme of theDTCCS of Colombo, and other specific assistance coming from different donor agencies. Of these, the formertwo types are loans, while the latter could either be by way of grants or loans.

The NHDA housing loan scheme is the single most important type of outside assistance that has beenavailable for Urban societies during their formative years. In fact, quite a large number of these societies wereformed by members specifically to become eligible for NHDA sponsored loans. Under this scheme eacheligible member becomes a recipient of a loan of Rs. 10,000 to Rs. 15,000. In as much as this fund becamethe main reason for the birth of the majority of urban societies, it also became the principal reason for theirpresent plight.

The inter−lending facility of DTCCS is available for those societies which can formulate projects acceptable tothem. They also should possess a sound financial record. In the meantime, only a few societies have beenable to obtain grants from foreign donors who were willing to help them by way of absorbing a part of thefinancial burdens. For instance, “Mahawatte” society has been able to obtain sponsorship to meet the cost ofconstruction of its office complex. Finally, whatever profit that is made by those active and strong societies aretransferred to the society fund under profit reserves, which are added to the share capital fund.

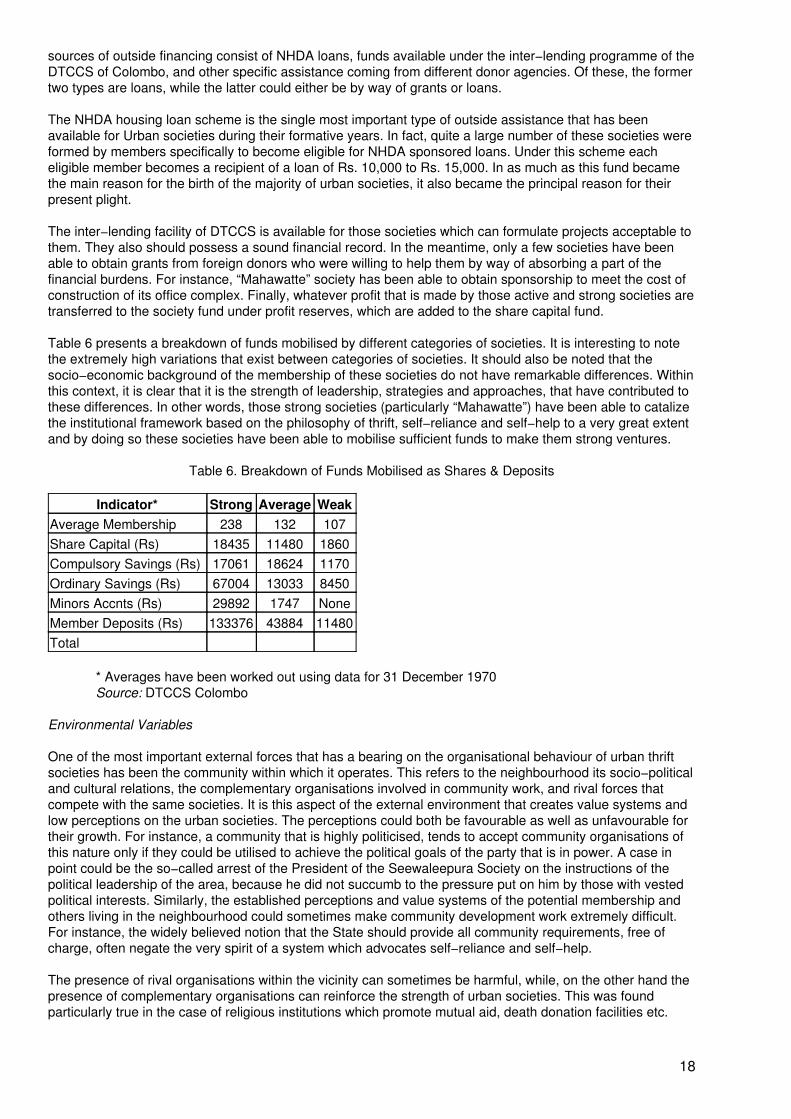

Table 6 presents a breakdown of funds mobilised by different categories of societies. It is interesting to notethe extremely high variations that exist between categories of societies. It should also be noted that thesocio−economic background of the membership of these societies do not have remarkable differences. Withinthis context, it is clear that it is the strength of leadership, strategies and approaches, that have contributed tothese differences. In other words, those strong societies (particularly “Mahawatte”) have been able to catalizethe institutional framework based on the philosophy of thrift, self−reliance and self−help to a very great extentand by doing so these societies have been able to mobilise sufficient funds to make them strong ventures.

Table 6. Breakdown of Funds Mobilised as Shares & Deposits

Indicator* Strong Average WeakAverage Membership 238 132 107Share Capital (Rs) 18435 11480 1860Compulsory Savings (Rs) 17061 18624 1170Ordinary Savings (Rs) 67004 13033 8450Minors Accnts (Rs) 29892 1747 NoneMember Deposits (Rs) 133376 43884 11480Total

* Averages have been worked out using data for 31 December 1970Source: DTCCS Colombo

Environmental Variables