Embed Size (px)

Citation preview

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 1 of 35 Page ID #:307

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 2 of 35 Page ID #:308

Violations of the Federal Securities Laws against Gulf Resources, Inc., (“Gulf

Resources” or the “Company”) alleges the following based upon personal

knowledge as to himself and his own acts, and information and belief as to all other

matters, based upon, inter alia, the investigation conducted by and through his

attorneys, which included, among other things, a review of the Defendant’s public

documents, conference calls and announcements made by the Defendants, United

States Securities and Exchange Commission (“SEC”) filings, Chinese State

Administration of Industry and Commerce (“SAIC”) filings, wire and press releases

published by and regarding Gulf Resources, securities analysts’ reports and

advisories about the Company, and information readily obtainable on the Internet.

Plaintiff believes that substantial evidentiary support will exist for the allegations

set forth herein after a reasonable opportunity for discovery.

NATURE OF THE ACTION

1. This is a federal securities class action on behalf of a class consisting

of all persons other than Defendants who purchased common stock of Gulf

Resources during the period between March 16, 2009 and April 26, 2011,

inclusively (the “Class Period”). Plaintiff seeks to recover damages caused by

Defendants’ violations of the Securities Exchange Act of 1934 (the “Exchange

Act”).

2. Throughout the class period, Defendants made false and misleading

statements about the Company’s financial performance.

3. Gulf Resources overstated its revenue and income for fiscal 2009 by a

multiple of 10x or $100 million and overstated revenue by a multiple of 1,000x or

$30 million.

4. Defendants kept two sets of books, one filed with the SEC and

provided to U.S. investors that paints a picture of a thriving company with over

$110 million of revenue and $30.5 million of net income in fiscal 2009. Another,

1 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 3 of 35 Page ID #:309

set of books, filed with Chinese regulators, show the Company barely keeping its

head above water, with $10.5 million of revenue and $38,000 of net income.

5. For fiscal 2008, Gulf similarly overstated its revenue by $82.7 million.

Instead of earning $87.5 million of revenue, it really earned $4.8 million of

revenue. And rather than earning a profit of $22.4 million as it reported for 2008,

Gulf really earned a net loss of over $127,000.

6. Maintaining two materially different sets of financial records is the

classic hallmark of accounting fraud.

7. Gulf’s chairman, Ming Yang, owns and runs the Haoyuan Group an

industrial holding company (“Haoyuan”). 1 Haoyuan Group holds a significant

equity interest in Gulf Resources (approximately 11.9%) according to Gulf’s public

statements.

8. Yang failed to disclose that Haoyuan’s two principal subsidiaries are

active direct competitors of Gulf Resources. Undisclosed to shareholders, Gulf’s

chairman has been simultaneously operating Haoyuan and utilizing the resources

and assets of Gulf Resources for the benefit of Haoyuan.

9. Defendants also failed to disclose material related party transactions in

violation of generally accepted accounting principles (“GAAP”) rendering Gulf’s

financial statements false and misleading under SEC regulations.

10. Gulf’s second biggest customer is Shouguang City Rongyuan

Chemical Company Limited (“Rongyuan”). Defendants failed to disclose that the

Haoyan Group, which is owned by Gulf’s Chairman Ming Yang, is a 74% owner of

Rongyuan. Ya Fei Ji, a Gulf Director, owned 18% of Rongyuan. 2

1 Several Chinese websites, including two governmental websites, indicate that Ming Yang is also the Chairman of Board of Haoyuan Group. http://gh.weifang.gov.cn/Article.asp?ArticleId=1217 http://sgqyjxh.com/xiehuizuzhi/huiyuanmingdan.htm 2 Based on review of SAIC filings. Ming Yang and Ya Fei Ji transferred their ownership in Rongyuan to what appears to be “straw men” in January 2010,

2 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

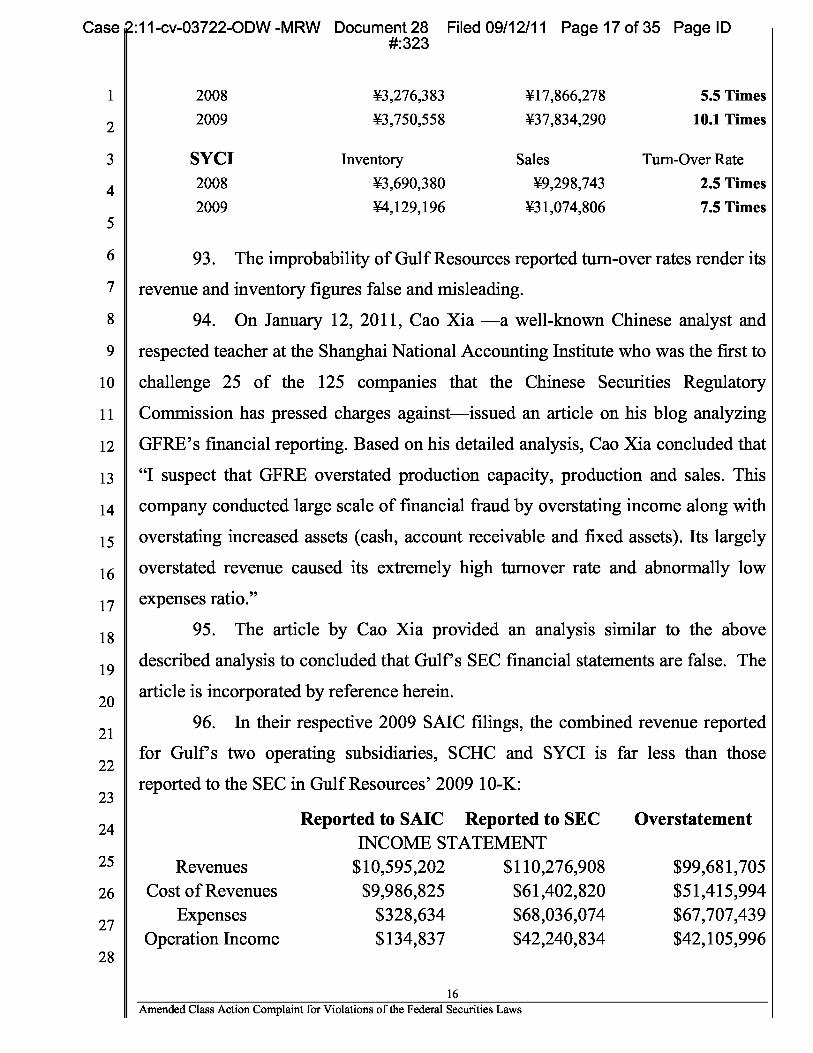

7

8

9

10

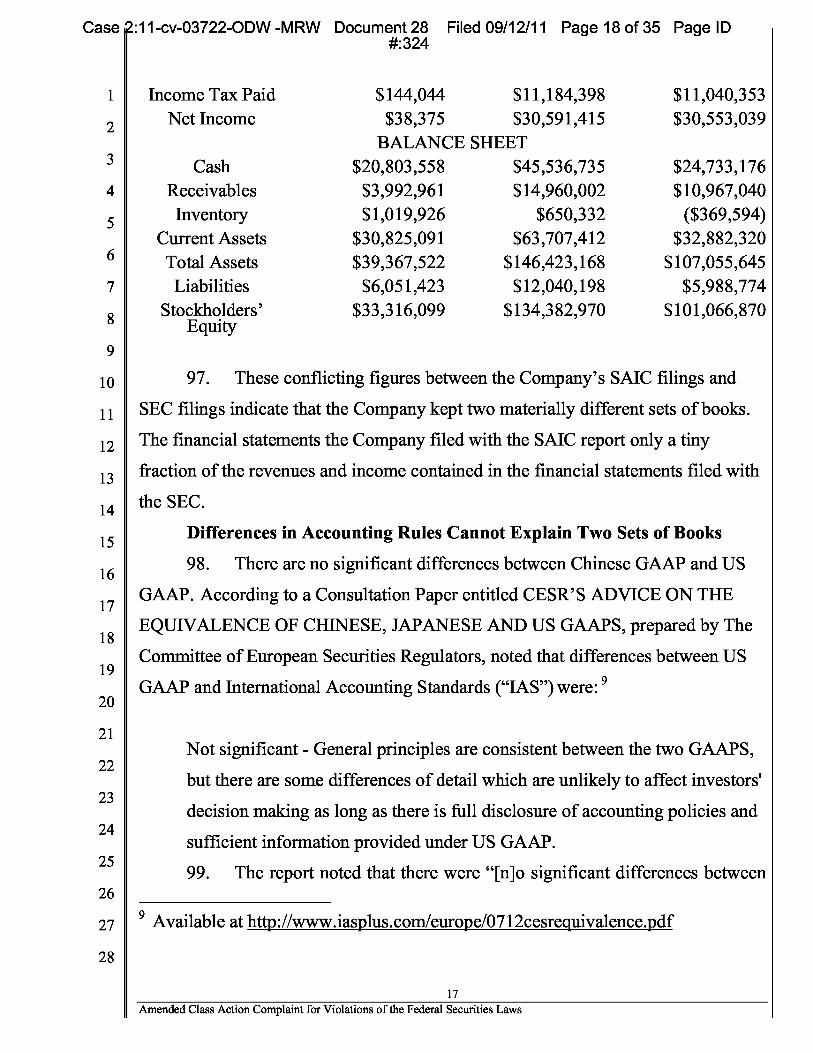

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 4 of 35 Page ID #:310

11. This means that the more than $20 million of sales revenue Gulf

earned from Rongyuan in fiscal 2008 and 2009 are undisclosed related party

transactions in violation of GAAP and SEC regulations.

12. Defendants also failed to disclose in its fiscal 2009 annual report that

Shouguang Hongye Trading Company Limited (“Hongye”) was one of its three

principal suppliers. Hongye is a related party, owned and controlled by Haoyan

Group, Ming Yang, his wife and their son.

13. The Company also concealed its Chief Executive Officer’s sordid past

as Chief Financial Officer of China Finance, Inc., a company behind a series of

well-known stock frauds involving reverse mergers of Chinese companies going

public in U.S. capital markets.

14. China Finance brought a large number of small-cap Chinese

companies to the United States markets in exchange for equity in these companies,

which China Finance sold at a profit before the companies were exposed as

fraudulent.

15. On April 26, 2011, a report was issued publicly by Glaucus Research

which asserted that the Company had materially overstated its revenue and net

income, engaged in undisclosed related party transactions, concealed its CEO’s

past, and as a result of all of these actions, had defrauded shareholders.

16. In particular, the report claimed that (1) $20 million of sales to

Rongyuan were undisclosed related party transactions; (2) Chinese regulatory

filings showed that the Company’s had materially overstated its revenue and

income; (3) Gulf’s Chairman Yang secretly used the assets of Gulf to operate two

businesses that he owned that directly compete with Gulf’s two operating

subsidiaries; and (4) the Company’s CEO had concealed a sordid past in China

Finance, a company that took fraudulent small-cap Chinese companies public in US

according to Rongyuan’s SAIC filings. The straw man that received Ming Yang’s 74% ownership in Rongyuan was a 28 year old woman named Cuiping Liu.

3 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 5 of 35 Page ID #:311

markets via reverse mergers.

17. The public allegations of fraud in the Glaucus report caused the

Company’s stock price to fall $1.16 per share or over 30% on heavy trading

volume, causing substantial financial damages to investors.

JURISDICTION AND VENUE

18. The claims asserted herein arise under and pursuant to Sections 10(b)

and 20(a) of the Exchange Act, (15 U.S.C. §78j(b) and 78t(a)), and Rule 10b-5

promulgated thereunder (17 C.F.R. §240.10b-5).

19. This Court has jurisdiction over the subject matter of this action

pursuant to §27 of the Exchange Act (15 U.S.C. §78aa) and 28 U.S.C. § 1331.

20. Venue is proper in this Judicial District pursuant to §27 of the

Exchange Act, 15 U.S.C. § 78aa and 28 U.S.C. § 1391(b)-(d).

21. In connection with the acts, conduct and other wrongs alleged in this

Complaint, the Defendants, directly or indirectly, used the means and

instrumentalities of interstate commerce, including but not limited to, the United

States mails, interstate telephone communications and the facilities of the

NASDAQ and the OTC:BB.

PARTIES

22. Plaintiffs Zachary Lewy, Sampson Daruvalla, William, Spiegelberg

and Ioannis Zoumas purchased Gulf Resources securities on the NASDAQ at

artificially inflated prices during the Class Period and have been damaged thereby.

Plaintiffs’ PSLRA certifications previously filed with the Court are incorporated by

reference herein.

23. Defendant Gulf Resources is a Delaware Corporation with its principal

executive offices located at Cheming Industrial Park, Shouguang City, Shangdong,

Peoples’ Republic of China (“PRC”).

24. Gulf Resources’ operations are conducted through its two operating

subsidiaries, Shouguang City Haoyuan Chemical Company Limited (“SCHC”) and

4 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 6 of 35 Page ID #:312

Shouguang Yuxing Chemical Industry Co., Limited (“SYCI”). Both companies are

organized under the laws of the PRC. SCHC manufactures and sells bromide and

crude salt, and SYCI manufactures industrial chemical products used in oil and gas

field exploration, oil field drilling, wastewater processing, papermaking chemical

agents, and inorganic chemicals.

25. All of Gulf’s revenue and income is generated by its two operating

subsidiaries SYCI and SCHC.

26. At all relevant times herein, the Company’s common stock was

actively traded on the NASDAQ under the ticker “GFRE” or on the OTC BB under

the ticker “GFRE”.

27. Defendant Ming Yang (“Yang”) was, at all relevant times, Chairman

of Gulf Resource’s Board of Directors.

28. Yang was simultaneously legal representative of SCHC and SYCI at

all relevant times. 3 As the legal representative of SCHC and SYCI, Yang was

required to sign the subsidiaries’ audited financial statements filed with the SAIC

annually. Yang therefore had actual knowledge that Gulf materially overstated its

revenue and income.

29. In a Proxy Statement filed with the SEC on October 10, 2009, the

Company stated that as of July 29, 2009, Defendant Yang held 14,793,259 shares.

The breakdown of shares was 6,481,526.5 shares owned by Defendant Yang's wife,

1,674,800 shares owned by Defendant Yang's son, and 4,124,732.5 shares owned

by a company of which Defendant Yang was the controlling shareholder, with the

remainder (2,512,200 shares) held by Defendant Yang himself. In a proxy

statement filed with the SEC on April 30, 2010, the Company indicated that as of

"April 28, 2009" [sic -- 2010], Defendant Yang held 13,391,454 shares. The proxy

3 Based on SAIC filings of SCHC and SYCI. Ming Yang was also the Chairman of SCHC during the Class Period according to SCHC’s filings with Chinese tax authorities.

5 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 7 of 35 Page ID #:313

statement indicated that Defendant Yang's wife only held 5,079,721 shares,

meaning that she had sold 1,401,805.5 shares, or approximately 25% of her

holdings (and approximately 10% of Defendant Yang's holdings). Defendant Yang

never filed the required report on Form 4 with the SEC to announce the sale.

Moreover, according to a lock-up agreement dated May 10, 2009, Defendant Yang,

his wife, and the other officers and directors of Gulf Resources agreed not to sell

their shares in a public transaction until March 9, 2011 -- making Defendant Yang's

wife's sale all the more suspicious.

30. In that time period, Gulf shares traded between $8.52/share and

$14.74/share, meaning that Ming Yang, his wife and son, made between $11 and

$20 million.

31. Defendant Xiaobin Liu (“Liu”) was at all relevant times Gulf

Resources’ Chief Executive Officer and one of its Directors.

32. Defendant Min Li (“Li”) was at all relevant times Gulf Resources’

Chief Financial Officer.

33. Defendants Li, Liu, and Yang are collectively referred to as the

“Individual Defendants.”

34. Gulf Resources, Liu, Li, and Yang are collectively referred to herein as

the “Defendants.”

35. Defendants’ fraudulent scheme: (i) deceived the investing public

regarding Gulf Resources’ business, operations, management and the intrinsic value

of Gulf Resources’ common stock; and (ii) caused plaintiff and other members of

the Class to purchase Gulf Resources securities at artificially inflated prices.

36. During the Class Period, the Defendant Yang and Gulf Resources and

its subsidiaries and affiliates were privy to non-public information concerning the

Company’s business, finances, products, markets, and present and future business

prospects, via access to internal corporate documents, conversations and

connections. Because of possession of such information, the Defendants knew or

6 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 8 of 35 Page ID #:314

recklessly disregarded the fact that the adverse facts specified herein had not been

disclosed to, and were being concealed from, the investing public.

37. Individual Defendants’ had direct access to and reviewed the adverse

undisclosed information about the Company’s business, operations, and financial

statements.

38. Throughout the Class Period, the Defendants were able to control the

content of the various SEC filings, press releases and other public statements

pertaining to the Company during the Class Period. The Defendants had access to

the documentation of filings alleged herein to be misleading prior to or shortly after

their issuance and/or had the ability and/or opportunity to prevent their issuance or

to cause them to be corrected. Accordingly, the Defendants are responsible for the

accuracy of the public reports and press releases detailed herein, and are therefore

primarily liable for the representations contained therein.

SUBSTANTIVE ALLEGATIONS

39. The Class Period begins on March 16, 2009, when Gulf Resources

filed with the SEC its annual report on Form 10-K for FY 2008.

40. The Class Period and ends on April 26, 2011, when the Glaucus

Research Group issued a thoroughly-researched report indicating that Gulf

Resources had overstated its revenue and income, engaged in undisclosed related

party transactions, concealed the Chairman’s use of Gulf’s assets to further his

competing businesses and concealed CEO Liu’s checkered role in connection with

several well-publicized stock fraud schemes. 4

4 Glaucus Research Group describes itself as a research firm dedicated to helping capital markets investors navigate treacherous financial waters in search of great investment opportunities. Glaucus stated that the April 26, 2011 report was a result of Glaucus Research Group’s thorough investigation, including personal visits to each of Gulf Resources’ factories, interviews with government officials in China, and reviews of Gulf Resources’ public filings and other documents.

7 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 9 of 35 Page ID #:315

1 I. False And Misleading Financial Statements

The False 2008 10-K

41. On March 16, 2009, the Company issued its annual report on SEC

form 10-K for fiscal year ended December 31, 2008 (“2008 10-K”).

42. The 2008 10-K falsely reported that Gulf earned consolidated revenue

of $87.5 million and $22.4 million of net income for fiscal year 2008.

43. Plaintiffs’ counsel obtained financial statements filed by Gulf’s two

subsidiaries (SYCI and SCHC) with both the PRC State Administration for

Industry and Commerce (“SAIC”) 5 and PRC State Administration of Taxation

(“SAT”) 6 .

44. The financial statements that Gulf’s two operating subsidiaries filed

with the Chinese regulators, the SAIC and SAT, showed Gulf really earned only a

fraction of the revenue and income it reported in its 2008 10-K.

45. The financial statements filed with the SAIC and SAT indicate the true

financial performance of Gulf Resources because:

• Under PRC law, penalties for filing false SAIC filings include fines and revocation of the entity’s business license;

• If an entity’s business license is revoked, the People’s Bank of China requires all bank accounts of that entity be closed;

• Without a business license the entity cannot legally conduct any business.

• The financial statements Gulf Resources filed in the PRC with the SAIC are required to be audited by Chinese CPA firms in conformance with Chinese GAAP.

5 The SAIC (State Administration for Industry and Commerce) is the Chinese government body that regulates industry and commerce in China. It is primarily responsible for business registrations, issuing and renewing business licenses and acts as the government supervisor of corporations. All Chinese companies are required to file audited financial statements with the Chinese government annually or bi-annually.

6 The SAT (State Administration of Taxation) is PRC equivalent of the Internal Revenue Service in the U.S.

8 Amended Class Action Complaint for Violations of the Federal Securities Laws

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 10 of 35 Page ID #:316

• Under PRC law, filing false tax documents is a crime subject to severe criminal and civil penalties, including imprisonment;

• Chinese GAAP are substantially the same as U.S. GAAP. In particular for revenue recognition for sales of product U.S. GAAP, Chinese GAAP and Gulf’s stated revenue recognitions policy are the same.

46. The 2008 10-K overstated revenue by $82.7 million. Gulf really

earned revenue of only $4.8 million in fiscal 2008.

47. In the 2008 10-K Gulf overstated net income by $22.5 million.

Indeed, Gulf actually lost over $127,000, rather than earning $22.4 million of profit

as it falsely claimed in its 2008 10-K.

The 2008 10-K Fails to Disclose the Related Party Nature of Gulf’s

Business

48. The 2008 10-K stated that Rongyuan was Gulf’s second biggest

customer for its chemical business purchasing $6.7 million of product from Gulf.

49. The 2008 10-K also failed to report that Rongyuan, from which it

reported revenue of $6.7 million in fiscal 2008 was secretly owned and controlled

by Gulf’s Chairman Ming Yang in violation of GAAP and SEC regulations that

require disclosure of all material related party transactions.

50. The 2008 10-K stated that its Chairman was owned Haoyan Group

which owned 11.9% of Gulf’s outstanding stock. However, Defendants failed to

disclose that Haoyuan’s two principal subsidiaries are active direct competitors of

Gulf Resources. Gulf’s chairman has been simultaneously operating Haoyuan and

utilizing the resources and assets of Gulf Resources for the benefit of Haoyuan.

51. SEC regulation S-K required Gulf to disclose its officers and directors

employment history in the 2008 10-K. In describing the past employment of Gulf

CEO Xiaobin Liu, the 2008 10-K purported to list his previous employment. The

2008 10-K failed to disclose that Liu served as the Chief Financial Officer for

China Finance, the notorious promoter of Chinese stock frauds.

The 2008 10-K’s False SOX Certifications

9 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 11 of 35 Page ID #:317

52. Defendants Li, Liu, and Yang signed the false and misleading 2008

10-K. Defendants Li and Liu signed the accompanying Sarbanes-Oxley Act of

2002 (“SOX”) certifications, attesting to the accuracy of the Company’s financial

statements.

The False 2009 10-K

53. On March 2, 2010, the Company issued its annual report for fiscal

2009 on Form 10-K (“2009 10-K”) containing false and misleading financial

statements.

54. The 2009 10-K falsely states that Gulf had earned revenue of $110.7

million and net income of $30.6 million.

55. In truth, audited financial statements filed by Gulf’s two operating

subsidiaries, SCHC and SYCI, with Chinese regulators (SAIC, SAT) show that

Gulf really earned only $10.6 million of revenue and $38 thousand of net income

for fiscal 2009.

56. Thus, Defendants overstated Gulf’s 2009 revenue by $100 million and

its net income by $30.5 million.

The 200910-K Fails to Disclose the Related Party Nature of Gulf’s

Business

57. The 2009 10-K stated that Rongyuan was Gulf’s second biggest

customer for its chemical business purchasing $11.44 million of product from Gulf

in 2009 and $6.7 million of product from Gulf in 2008.

58. The 2009 10-K failed to report that Rongyuan, from which it reported

revenue of $11.44 million in 2009 and $6.7 million in fiscal 2008 was secretly

owned and controlled by Gulf’s Chairman Ming Yang in violation of GAAP and

SEC regulations that require disclosure of all material related party transactions.

59. The Company’s 2009 10-K and 2010 10-K, however, failed to disclose

that its top customer Rongyuan was a related party.

60. The 2009 10-K reported that Hongye was one of Gulf’s three largest

10 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 12 of 35 Page ID #:318

suppliers of raw materials. However, it failed to disclose that Hongye is owned and

controlled by Haoyan Group, Yang, his wife and their son. 7

61. Several Chinese yellow page websites show Hongye Trading is a

subsidiary of Haoyuan Group. Wenxiang Yu- Mingyang's wife is the legal

representative of Hongye Trading.

62. Wenxiang Yu-Mingyang's wife is listed as the contact person of

Hongye Trading.

63. The 2009 10-K stated that its Chairman s owned Haoyan Group, which

owned 11.9% of Gulf’s outstanding stock. However, Defendants failed to disclose

that Haoyuan’s two principal subsidiaries are active direct competitors of Gulf

Resources. Gulf’s chairman has been simultaneously operating Haoyuan and

utilizing the resources and assets of Gulf Resources for the benefit of Haoyuan. The

Company’s 2009 10-K and 2010 10-K, however, failed to disclose that its top

customer Rongyuan was a related party.

64. SEC regulations required Gulf to disclose its officers and directors

employment history in the 2009 10-K. In describing the past employment of Gulf

CEO Xiaobin Liu, the 2009 10-K purported to list his previous employment. The

2008 10-K failed to disclose that Liu served as the Chief Financial Officer for

China Finance, the notorious promoter of Chinese stock frauds.

The 2009 10-K’s False SOX Certifications

65. Defendants Li and Liu signed the false and misleading 2009 10-K, as

well as the accompanying SOX certifications, attesting to the accuracy of the

Company’s financial statements.

The False 2010 10-K

66. On March 16, 2011, the Company issued its annual report for fiscal

7 Gulf’s 2010 10-K reports that Hongye, onf of Gulf’s principal suppliers in 2010 is a related party but contradicts the 2009 10-K in stating that Gulf did not purchase any materials from Hongye in 2009.

11 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 13 of 35 Page ID #:319

2010 on Form 10-K (“2010 10-K”) containing false and misleading financial

statements.

67. The 2010 10-K was false and misleading for the same reasons as the

2009 10-K was false and misleading described above.

68. The 2010 10-K overstated Gulf’s 2009 revenue by $100 million and its

net income by $30.5 million.

The 2010 10-K Fails to Disclose the Related Party Nature of Gulf’s

Business

69. The 2010 10-K also failed to disclose that Rongyuan, Gulf’s second

biggest customer in 2008 and 2009, generating $20 million of revenue for Gulf in

2008 and 2009, was secretly owned and controlled by Gulf’s Chairman Yang, until

January 2010 when he transferred his interest to a straw man.

70. The 2010 10-K also failed to disclose that Chairman Yang operated

two businesses that directly competed with Gulf’s operating subsidiaries, SCHC

and SYCI.

71. The 2010 10-K also failed to disclose that Gulf’s CEO Xiaobin Liu

was the Chief Financial Officer for China Finance, the notorious stock promoter of

several similarly fraudulent Chinese reverse merger scams.

The 2010 10-K’s False SOX Certifications

72. Defendants Li, Liu, and Yang signed the false and misleading 2010

10-K. Defendants Li and Liu also signed the accompanying SOX certifications,

attesting to the accuracy of the Company’s financial statements.

Gulf’s False Interim Quarterly Reports and SOX Certifications During

the Class Period

73. All of Gulf’s quarterly reports on form 10-Q filed with the SEC during

the Class Period are also false and misleading for all of the same reasons described

above. The fraudulent quarterly reports are as follows:

a) Filed May 11, 2009, for the first quarter ended March 31, 2009;

12 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 14 of 35 Page ID #:320

b) Filed August 10, 2009, for the second quarter June 30, 2009;

c) Filed November 9, 2009, for the third quarter ended September 30, 2009;

d) Filed May 11, 2010, for the first quarter ended March 31, 2010;

e) Filed August 16, 2010, for the second quarter ended June 30, 2010; and

f) Filed November 15, 2010, for the third quarter ended September 30, 2010.

74. Defendants Li and Liu signed all of the above-listed false and

misleading quarterly reports on form 10-Q, as well as their accompanying SOX

certifications, falsely attesting to the accuracy of the Company’s financial

statements.

Additional Evidence that Gulf’s 2008, 2009 and 2010 10-K’s

Overstated Revenue and Income

Bromine Production Doesn’t Add Up

75. In its 2008 10-K, 2009 10-K, and 2010 10-K, Gulf Resources

repeatedly boasted that “[a]ccording to figures published by the China Crude Salt

Association, we are one of the largest manufacturers of bromine in China, as

measured by production output.”

76. These statements were false when made.

77. According to a December 2010 report issued by CCM International

Ltd., 8 neither Gulf Resources nor its subsidiaries are listed among the top 30

bromine producers in China.

78. According to the CCM report “there are around 100 producers of

bromine, [and] 30 main producers have controlled most of [the] production lines

8 CCM stands for China Chemicals Market a company dedicated to providing high quality business and corporate Market Data and Primary Intelligence across agriculture, biotechnologies, life sciences, renewable energies, printing and packaging, and specialty chemicals. (See Who Is CCM , available at http://www.cnchemicals.com/ About/AboutUs.shtml (last visited Sep. 5, 2011).) The December 2010 report was a result of thorough research efforts, including over 250 calls with industry participants.

13 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 15 of 35 Page ID #:321

with output accounting for 93.6% of the total in China in 2009.”

79. The CCM report states that the annual output of bromine in China was

157,000 tons in 2010 and 107,665 in 2009. The report further identifies the top five

producers, each of which produced less than 20,000 tons of bromine per year:

2009` 2010 Shandong Haihua Group Co. Ltd. 15,000 20,000 Souguang Fukang Pharmaceutical Co. Ltd. Shandong Yuyuan Group Co. Ltd 10,000 15,000 Weifang Longwei Industrial Co. Ltd. 10,000 15,000 Shandong Futong Chemical Co. Ltd. 9,000 10,000

80. These output figures stated in the CCM report render the production

figures in Gulf Resources’ Form 10-Ks highly improbable.

81. In its 2008 10-K, 2009 10-K, and 2010 10-K, Gulf Resources reported

bromine production of 17,648 tons in 2007, 28,673 in 2008, 34,930 in 2009, and

34,672 in 2010.

82. These figures, if they were true, would have placed Gulf Resources at

the very top of the top 30 producers list in the CCM report and would have made

Gulf Resources responsible for over 40% of China’s bromine production in 2010.

83. An investigation conducted by market analysts could not locate China

Crude Salt Association, the entity that Gulf relies on for its claims to being one of

China’s largest producers of bromine.

84. Accordingly, the statements in the 2008 10-K, 2009 10-K, and 2010

10-K regarding its bromine production were false when made. And provide further

evidence that Gulf overstated its revenue and income in its annual reports for fiscal

2008, 2009 and 2010.

85. Based on the inventory and sales figures reported in Gulf Resources’

2008 10-K, 2009 10-K, and 2010 10-K, the Company turned its inventory between

59 and 209 times each year:

14 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

12,000 20,000

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 16 of 35 Page ID #:322

1 Inventory Sales Turn-Over Rate

2008 $418,259 $87,488,334 209 Times 2009 $650,332 $110,276,908 169.5 Times 2010 $2,679,899 $158,335,023 59 Times

Financial Metrics Don’t Add Up

86. Moreover, based on the revenue and earnings before interest, taxes,

depreciation and amortization (“EBITDA”) figures reported in the 2010 10-K, Gulf

Resources’ profit margin is over 50%.

87. An interview with a bromine industry expert reveals that Great Lakes

Chemical, the largest methyl bromide supplier in the United States, operates under

a inventory-sales turn-over rate of five times and a profit margin of below 10%.

88. Similarly, an analysis of the public filings of Shandong Haihua Group

Company Ltd., one of the “principal competitors” identified in Gulf Resources

Form 10-Ks, operates under a inventory-sales turn-over rate of seven times and a

profit margin of below 20%.

89. Compared against the figures reported by Great Lakes and Shandong

Haihua, the inventory and sales figures stated in Gulf Resources’ 2008 10-K, 2009

10-K, and 2010 10-K are improbable.

90. Accordingly, the inventory and sales figures stated in Gulf Resources’

2008 10-K, 2009 10-K, and 2010 10-K were false when made.

Regulatory Filings with the PRC Don’t Add Up

91. Moreover, Gulf Resources’ subsidiaries, SCHC and SYCI, in their

filings with Chinese regulators reported much lower turn-over rates that are more in

line with those reported by Great Lakes and Shandong Haihua.

92. In their respective filings with the SAIC in China, both SCHC and

SYCI reported sales and inventory figures that indicate a turn-over rate of under

10.1 times or less in 2008 and 2009:

SCHC Inventory Sales Turn-Over Rate

15 Amended Class Action Complaint for Violations of the Federal Securities Laws

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 17 of 35 Page ID #:323

2008 ¥3,276,383 ¥17,866,278 5.5 Times

2009 ¥3,750,558 ¥37,834,290 10.1 Times

SYCI Inventory Sales Turn-Over Rate

2008 ¥3,690,380 ¥9,298,743 2.5 Times

2009 ¥4,129,196 ¥31,074,806 7.5 Times

93. The improbability of Gulf Resources reported turn-over rates render its

revenue and inventory figures false and misleading.

94. On January 12, 2011, Cao Xia —a well-known Chinese analyst and

respected teacher at the Shanghai National Accounting Institute who was the first to

challenge 25 of the 125 companies that the Chinese Securities Regulatory

Commission has pressed charges against—issued an article on his blog analyzing

GFRE’s financial reporting. Based on his detailed analysis, Cao Xia concluded that

“I suspect that GFRE overstated production capacity, production and sales. This

company conducted large scale of financial fraud by overstating income along with

overstating increased assets (cash, account receivable and fixed assets). Its largely

overstated revenue caused its extremely high turnover rate and abnormally low

expenses ratio.”

95. The article by Cao Xia provided an analysis similar to the above

described analysis to concluded that Gulf’s SEC financial statements are false. The

article is incorporated by reference herein.

96. In their respective 2009 SAIC filings, the combined revenue reported

for Gulf’s two operating subsidiaries, SCHC and SYCI is far less than those

reported to the SEC in Gulf Resources’ 2009 10-K:

Reported to SAIC Reported to SEC INCOME STATEMENT

Overstatement

Revenues $10,595,202 $110,276,908 $99,681,705 Cost of Revenues $9,986,825 $61,402,820 $51,415,994

Expenses $328,634 $68,036,074 $67,707,439 Operation Income $134,837 $42,240,834 $42,105,996

16 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 18 of 35 Page ID #:324

Income Tax Paid $144,044 $11,184,398 $11,040,353 Net Income $38,375 $30,591,415 $30,553,039

BALANCE SHEET Cash $20,803,558 $45,536,735 $24,733,176

Receivables $3,992,961 $14,960,002 $10,967,040 Inventory $1,019,926 $650,332 ($369,594)

Current Assets $30,825,091 $63,707,412 $32,882,320 Total Assets $39,367,522 $146,423,168 $107,055,645 Liabilities $6,051,423 $12,040,198 $5,988,774

Stockholders’ $33,316,099 $134,382,970 $101,066,870 Equity

97. These conflicting figures between the Company’s SAIC filings and

SEC filings indicate that the Company kept two materially different sets of books.

The financial statements the Company filed with the SAIC report only a tiny

fraction of the revenues and income contained in the financial statements filed with

the SEC.

Differences in Accounting Rules Cannot Explain Two Sets of Books

98. There are no significant differences between Chinese GAAP and US

GAAP. According to a Consultation Paper entitled CESR’S ADVICE ON THE

EQUIVALENCE OF CHINESE, JAPANESE AND US GAAPS, prepared by The

Committee of European Securities Regulators, noted that differences between US

GAAP and International Accounting Standards (“IAS”) were: 9

Not significant - General principles are consistent between the two GAAPS,

but there are some differences of detail which are unlikely to affect investors'

decision making as long as there is full disclosure of accounting policies and

sufficient information provided under US GAAP.

99. The report noted that there were “[n]o significant differences between

9 Available at http://www.iasplus.com/europe/0712cesrequivalence.pdf

17 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 19 of 35 Page ID #:325

ASBE 14, the China GAAP standard for revenue recognition, and IAS 18, the IAS

equivalent.” See Id. pg 35.

100. Gulf’s 2010 10-K states “We recognize revenue, net of value added

tax, when persuasive evidence of an arrangement exists, delivery of the goods has

occurred, customer acceptance has been obtained, which means the significant risks

and ownership have been transferred to the customer, the price is fixed or

determinable and collectability is reasonably assured. The Chinese accounting

standard governing revenue recognition, ASBE 14, is similar. 10 It states:

Chapter II Revenue from Selling Goods

Article 4 No revenue from selling goods may be recognized unless the

following conditions are met simultaneously:

(1) The significant risks and rewards of ownership of the goods have been

transferred to the buyer by the enterprise;

(2) The enterprise retains neither continuous management right that usually

keeps relation with the ownership nor effective control over the sold goods;

(3) The relevant amount of revenue can be measured in a reliable way;

(4) The relevant economic benefits may flow into the enterprise; and

(5) The relevant costs incurred or to be incurred can be measured in a reliable

way.

101. Accordingly, there are no significant differences between US GAAP

and Chinese GAAP for recognizing revenue for the sale of goods in Gulf’s case.

And differences between U.S. GAAP and Chinese GAAP are not the cause of the

huge differences in revenue and income between Gulf’s SEC filed financial

statements and its China filed SAIC and SAT financial statements. Fraud is the

only plausible explanation for the differences.

10 Accounting Standards for Enterprises No. 14 – Revenues; Promulgation date: 02-15-2006; Effective date:01-01-2007; Department: China Ministry of Finance; Subject: Accounting.

18 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 20 of 35 Page ID #:326

II. Related Party Transactions are Violations of GAAP Rendering the Financial Statements False and Misleading

102. Generally Accepted Accounting Principles (“GAAP”), Statement of

Financial Accounting Standards (“SFAS”), and SEC regulations required the

Company to disclose all material related party transactions.

103. SFAS No. 57 and No. 850 provide that a public company’s “[f]inancial

statements shall include disclosures of material related party transactions.” SFAS

No. 57 ¶ 2; 850-10-50-1.

104. “Related party transactions” include those between “an enterprise and

its principal owners, management, or members of their immediate families” and

those between a company and its “affiliates.” SFAS No. 57 ¶ 1; 850-10-05-3.

“Affiliate” includes any company that is under common control or management

with the public company. SFAS No. 57 ¶ 24(a, b); 850-10-20.

105. Disclosures of related party transactions shall include

• the nature of the relationship involved;

• a description of the transactions for each period for which income statements are presented and such other information necessary to an understanding of the effects of the transactions on the financial statements;

• the dollar amount of transactions for each of the periods for which income statements are presented; and

• amounts due from or to related parties as of the date of each balance sheet presented and, if not otherwise apparent, the terms and manner of settlement. SFAS No. 57 ¶ 2; 850-10-50-1.

106. Defendant Yang, the Company’s former CEO and current Chairman of

its Board, is also Chairman of the Board and founder of Haoyuan Group.

107. The 2008 and 2009 10-Ks stated that Gulf Resources’ second largest

customer for 208 and 2009 Rongyuan.

108. The 2010 10-K stated that Gulf Resources’ largest customer was

19 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 21 of 35 Page ID #:327

Rongyuan, accounting for 13.2% of its bromine revenue and 24.3 of its crude salt

revenue. Rongyuan accounted for 10.6% of Gulf Resources’ total 2010 revenue.

109. Rongyuan has the same phone number, fax number, and address, as

Haoyuan.

110. Rongyuan’s SAIC filings show that Yang owned 74% and Gulf

Director Ya Fei Ji owned 18% of Rongyuan from 2006 to at least January 2010.

111. Further, Chinese regulatory filings show that Rongyuan has the same

address as Haoyuan.

112. Rongyuan’s Web site has the name “Haoyuan” in the URL address.

113. Therefore, Rongyuan is operated as a subsidiary of Haoyuan.

114. Under GAAP rules, Rongyuan is a related party to Gulf Resources.

CHAIRMAN YANG CONCEALED THAT HIS COMPANIES COMPETE

WITH GULF RESOURCES

115. Ming Yang is the chairman and founder of Gulf Resources.

116. Shandong Haoyuan Industry Group Ltd. (“Haoyuan Group”) is a

privately-owned Chinese conglomerate, owned by Ming Yang and his wife

Wenxiang Yu. Several Chinese websites, including two governmental websites,

indicate that Ming Yang is also the Chairman of Board of Haoyuan Group. 11

117. Haoyuan Group is a competitor of SYCI. As of May 18, 2011 when

our investigator obtained their SAIC filings, those filings show the two companies

share very similar business scope.

Haoyuan Group SYCI

Production and sales of plastic

woven bags, petroleum machinery

parts and labor protective

appliance; oilfield drilling

Production and sales of chemical products,

plastic woven bags, petroleum machinery

parts, oil field additives, paper production

chemical additives, plastic products and

11 http://gh.weifang.gov.cn/Article.asp?ArticleId=1217 http://sgqyjxh.com/xiehuizuzhi/huiyuanmingdan.htm

20 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 22 of 35 Page ID #:328

technology services; oil field waste anti-corrosion insulation projects.

water treatment; anti-corrosion

insulation projects.

118. In addition, Haoyuan Group owns a subsidiary which is also in

chemical manufacturing business- Shouguang City Shengbang Chemical Company

Limited. 12

119. Gulf did not disclose that its chairman and his family own a competing

business.

120. GFRE uses Haoyuan Group’s address in its SEC filings.

121. In its SEC filings, Gulf’s address of principal executive offices and zip

code is 99 Wenchang Road, Chenming Industrial Park, Shouguang City, Shandong,

China 262714. But this address does not belong to either one of Gulf Resources'

two operating subsidiaries – SCHC and SYSC. Instead, it belongs to Haoyuan

Group. Since its registration in March 2006, Haoyuan Group has been using the

same address in its SAIC filings.

CEO Xiaobin Liu Concealed his Role at Disgraced China Finance

122. The Company’s Chief Executive Officer was Defendant Liu.

Defendant Liu’s biography omitted the position he had been Chief Financial Officer

of China Finance as late as 2004.

123. According to its SEC filings, China Finance “provid[ed] financial

support and services [...] to privately-owned small and medium sized enterprises in

China when they seek access to capital or to be acquired by a United States

reporting company [in a reverse merger]”.

124. China Finance would be compensated for its services through equity

ownership of these companies.

125. Many of these companies were later determined to be fraudulent, or to

12 Haoyuan Group’s website shows that Shouguang City Shengbang Chemical Company Limited is one of its subsidiaries.

21 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 23 of 35 Page ID #:329

have such serious undisclosed weaknesses in internal controls that their shares were

nearly valueless. Accordingly, the stock price for the common stock of many of

these companies collapsed after allegations of fraud – that is, when trading in the

companies’ shares was not permanently halted altogether.

126. China Finance would customarily dispose of the equity it held in these

fraudulent companies at elevated prices before the fraud was discovered.

127. China Finance provided financing to Gulf Resources in exchange for

6% of the equity in Gulf Resources. Seven days after China Finance’s investment,

Defendant Liu was installed as Gulf Resources’ Chief Executive Officer. Had

Defendant Liu disclosed his past affiliation with China Finance, it would have been

apparent that he was installed to provide favorable treatment to China Finance.

128. The Company failure to disclose Defendant Liu’s ties to China

Finance renders each of its SOX certifications false because the certifications

requires disclosure of “all significant deficiencies and material weaknesses in the

design or operation of internal control over financial reporting which are reasonably

likely to adversely affect the registrant’s ability to record, process, summarize and

report financial information” and “any fraud.”

III. Auditors Run for the Exits

129. Between 2007 and 2010, the Company dismissed two auditors.

130. In February 2010 – less than three weeks before the filing of the 2009

10-K – the Company dismissed Morison Cogen, LLP (“MCO”) under suspicious

circumstances.

131. A year before the dismissal, MCO warned investors about the

possibility of fraud at the Company. In the 2008 10-K, MCO identified two

“material weaknesses” in the effectiveness of the Company’s internal controls:

a. Insufficient complement of accounting personnel with the appropriate level of accounting knowledge, experience and training in the application of accounting principles generally accepted in the United States

22 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 24 of 35 Page ID #:330

commensurate with financial statement reporting requirements.

b. Inability to timely and properly recognize issuance of share-based compensation

132. BDO Limited, the Hong Kong member of the BDO International

network, completed the Company’s audit in less than three weeks, an unusually

short period of time for a newly hired accountant with little familiarity with the

Company’s books, records, and accounting practices.

133. In September 2010, the Company retained Deloitte Touche &

Tohmatsu (“DTT”) to investigate and report on the Company’s internal controls.

134. The Company kept the findings of DTT’s investigation secret.

135. After receiving DTT’s findings, Richard Khaleel, an independent

director and a member of the audit committee of the Board, resigned. Khaleel is the

sole director who is a United States citizen and subject to the jurisdiction of the

United States.

IV. The SEC Has Warned Of Chinese Reverse Merger Companies (“RCMs”) Like Gulf Resources

136. Chinese reverse mergers have been a magnet for disreputable stock

promoters, leading the SEC to issue warnings about investing in companies like

Gulf Resources.

137. Shielded by the geographic distance of thousands of miles and

operating under a regulatory framework that is a world apart from the SEC’s

oversight, RCMs have few incentives to provide complete and accurate disclosures

to American investors. An August 28, 2010 article in Barron’s by Bill Alpert and

Leslie P. Norton entitled, “Beware This Chinese Export,” discusses the enforcement

problems that American regulators face when dealing with Chinese companies that

trade on U.S. exchanges through RCMs. The article states that “[t]he SEC’s

enforcement staff can’t subpoena evidence of any fraudulent activities in China,

and Chinese regulators have little incentive to monitor shares sold only in the U.S.”

23 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 25 of 35 Page ID #:331

138. U.S. regulators have finally begun to take notice of the manipulation

and fraud endemic in RCMs. The SEC has recently established a task force to

investigate investors’ claims regarding the impropriety and fraud of RCMs trading

on the U.S. markets. SEC Commissioner Luis A. Aguilar (the “Commissioner”)

discussed Chinese reverse mergers and the process of “backdoor registration,”

stating:

In the world of backdoor registrations to gain entry into the U.S. public market, the use by Chinese companies has raised some unique issues, even compared to mergers by U.S. companies. Two important ones are:

• First, there appear to be systematic concerns with the quality of the auditing and financial reporting; and

• Second, even though these companies are registered here in the U.S., there are limitations on the ability to enforce the securities laws, and for investors to recover their losses when disclosures are found to be untrue, or even fraudulent.

I am worried by the systematic concerns surrounding the quality of the financial reporting by these companies. In particular, according to a recent report by the staff of the Public Company Accounting Oversight Board (PCAOB), U.S. auditing firms may be issuing audit opinions on the financials, but not engaging in any of their own work. Instead, the U.S. firm may be issuing an opinion based almost entirely on work performed by Chinese audit firms. If this is true, it could appear that the U.S. audit firms are simply selling their name and PCAOB-registered status because they are not engaging in independent activity to confirm that the work they are relying on is of high quality. This is significant for a lot of reasons, including that the PCAOB has been prevented from inspecting audit firms in China

139. On June 9, 2011, the SEC issued an Investor Bulletin warning

investors about investing in companies that enter U.S. markets through RCM “...

there have been instances of fraud and other abuses involving reverse merger

companies.” “Given the potential risks, investors should be especially careful when

considering investing in the stock of reverse merger companies,” said Lori J.

Schock, Director of the SEC’s Office of Investor Education and Advocacy.

24 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 26 of 35 Page ID #:332

Applicability of Presumption of Reliance:

Fraud-on-the-Market Doctrine

140. At all relevant times, the market for Gulf Resources common stock

was an efficient market for the following reasons, among others:

(a) The Company’s stock met the requirements for listing, and

was listed and actively traded on a national exchange in a

highly efficient and automated market;

(b) More than 2% of Gulf Resources’ outstanding shares were

traded in the public markets on a weekly basis providing a

strong presumption of an efficient market in Gulf Resources

shares;

(c) As a regulated issuer, Gulf Resources filed periodic public

reports with the SEC;

(d) Gulf Resources regularly communicated with public investors

via established market communication mechanisms, including

through regular disseminations of press releases on the

national circuits of major newswire services and through

other wide-ranging public disclosures, such as

communications with the financial press and other similar

reporting services;

(e) Gulf met the requirements for filing an S-3 registration

statement during the Class Period;

(f) Gulf Resources was followed by several securities analysts

employed by major brokerage firms who wrote reports that

were distributed to the sales force and certain customers of

25 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 27 of 35 Page ID #:333

their respective brokerage firms during the Class Period. Each

of these reports was publicly available and entered the public

marketplace; and

141. As a result of the foregoing, the market for the Company’s common

stock promptly digested current information regarding Gulf Resources from all

publicly available sources and reflected such information in Gulf Resources’ stock

price. Under these circumstances, all purchasers of the Company’s common stock

during the Class Period suffered similar injury through their purchase of Gulf

Resources’ common stock at artificially inflated prices, and a presumption of

reliance applies.

PLAINTIFF’S CLASS ACTION ALLEGATIONS

142. Plaintiff brings this action as a class action pursuant to Federal Rules

of Civil Procedure 23(a) and (b)(3) on behalf of a Class, consisting of all persons

who purchased common stock of Gulf Resources during the Class Period and who

were damaged thereby. Excluded from the Class are the officers and directors of

the Company at all relevant times, members of their immediate families and their

legal representatives, heirs, successors or assigns and any entity in which

Defendants have or had a controlling interest.

143. The members of the Class are so numerous that joinder of all members

is impracticable. Throughout the Class Period, the Company’s common stock was

actively traded on the NASDAQ or OTC:BB. While the exact number of Class

members is unknown to Plaintiff at this time, and can only be ascertained through

appropriate discovery, Plaintiff believes that there are at least hundreds of members

in the proposed Class. Members of the Class may be identified from records

maintained by Gulf Resources or its transfer agent, and may be notified of the

pendency of this action by mail using a form of notice customarily used in

securities class actions.

26 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 28 of 35 Page ID #:334

144. Plaintiff’s claims are typical of the claims of the members of the Class,

as all members of the Class are similarly affected by Defendants’ wrongful conduct

in violation of federal law that is complained of herein.

145. Plaintiff will fairly and adequately protect the interests of the members

of the Class and has retained counsel competent and experienced in class and

securities litigation.

146. Common questions of law and fact exist as to all members of the Class

and predominate over any questions solely affecting individual members of the

Class. Among the questions of law and fact common to the Class are:

(a) whether the federal securities laws were violated by Defendants

acts as alleged herein;

(b) whether statements made by the Defendants to the investing public

during the Class Period misrepresented material facts about the

business, operations, and management of Gulf Resources; and

(c) to what extent the members of the Class have sustained damages,

and the proper measure of damages.

147. A class action is superior to all other available methods for the fair and

efficient adjudication of this controversy since joinder of all members is

impracticable. Furthermore, as the damages suffered by individual Class members

may be relatively small, the expense and burden of individual litigation make it

impossible for members of the Class to redress individually the wrongs done to

them. There will be no difficulty in the management of this action as a class action.

FIRST CLAIM

Violation of Section 10(b) of

The Exchange Act and Rule 10b-5

Promulgated Thereunder Against All Defendants

27 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 29 of 35 Page ID #:335

148. Plaintiff repeats and realleges each and every allegation contained

above as if fully set forth herein.

149. During the Class Period, Defendants carried out a plan, scheme and

course of conduct which was intended to and, throughout the Class Period, did: (1)

deceive the investing public, including Plaintiff and other Class members, as

alleged herein; and (2) cause Plaintiff and other members of the Class to purchase

Gulf Resources’ securities at artificially inflated prices. In furtherance of this

unlawful scheme, plan and course of conduct, Defendants took the actions set forth

herein.

150. Defendants (a) employed devices, schemes, and artifices to defraud;

(b) made untrue statements of material fact and/or omitted to state material facts

necessary to make the statements not misleading; and (c) engaged in acts, practices,

and a course of business that operated as a fraud and deceit upon the purchasers of

the Company’s securities in an effort to maintain artificially high market prices for

Gulf Resources’ securities in violation of Section 10(b) of the Exchange Act and

Rule 10b-5 thereunder.

151. Defendants, directly and indirectly, by the use, means or

instrumentalities of interstate commerce and/or of the mails, engaged and

participated in a continuous course of conduct to conceal adverse material

information about the business, operations and future prospects of Gulf Resources

as specified herein.

152. These Defendants employed devices, schemes, and artifices to defraud

while in possession of material adverse non-public information, and engaged in

acts, practices, and a course of conduct as alleged herein in an effort to assure

investors of Gulf Resources’ value and performance and continued substantial

growth, which included the making of, or participation in the making of, untrue

statements of material facts and omitting to state material facts necessary in order to

make the statements made about Gulf Resources and its business operations and

28 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 30 of 35 Page ID #:336

future prospects in the light of the circumstances under which they were made, not

misleading, as set forth more particularly herein, and engaged in transactions,

practices and a course of business that operated as a fraud and deceit upon the

purchasers of Gulf Resources’ securities during the Class Period.

153. Defendants had actual knowledge of the misrepresentations and

omissions of material facts set forth herein, or acted with reckless disregard for the

truth in that they failed to ascertain and to disclose such facts, even though such

facts were available. Such material misrepresentations and/or omissions were done

knowingly or recklessly and for the purpose and effect of concealing Gulf

Resources’ operating condition and future business prospects from the investing

public and supporting the artificially inflated price of its securities. As

demonstrated by overstatements and misstatements of the Company’s financial

condition throughout the Class Period, if the Defendants did not have actual

knowledge of the misrepresentations and omissions alleged, they were reckless in

failing to obtain such knowledge by deliberately refraining from taking those steps

necessary to discover whether those statements were false or misleading.

154. Gulf Resources is liable for the acts of the Individual Defendants and

its employees under the doctrine of respondeat superior and common law

principles of agency as all of the wrongful acts complained of herein were carried

out within the scope of their employment with authorization.

155. The scienter of the Individual Defendants and other employees and

agents of the Company is similarly imputed to Gulf Resources under respondeat

superior and agency principles.

156. As a result of the dissemination of the materially false and misleading

information and failure to disclose material facts, as set forth above, the market

price of Gulf Resources’ securities was artificially inflated during the Class Period.

In ignorance of the fact that market prices of Gulf Resources’ publicly-traded

securities were artificially inflated, and relying directly or indirectly on the false

29 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 31 of 35 Page ID #:337

and misleading statements made by the Defendants, or upon the integrity of the

market in which the common stock trades, and/or on the absence of material

adverse information that was known to or recklessly disregarded by the Defendants,

but not disclosed in public statements by the Defendants during the Class Period,

Plaintiff and the other members of the Class acquired Gulf Resources common

stock during the Class Period at artificially high prices, and were, or will be,

damaged thereby.

157. At the time of said misrepresentations and omissions, Plaintiff and

other members of the Class were ignorant of their falsity, and believed them to be

true. Had Plaintiff and the other members of the Class and the marketplace known

the truth regarding Gulf Resources’ financial results, which was not disclosed by

the Defendants, Plaintiff and other members of the Class would not have purchased

or otherwise acquired their Gulf Resources securities, or, if they had acquired such

securities during the Class Period, they would not have done so at the artificially

inflated prices that they paid.

158. As a direct and proximate result of the Defendants’ wrongful conduct,

Plaintiff and other members of the Class suffered damages in connection with their

purchases of Gulf Resources’ securities during the Class Period.

159. This action was filed within two years of discovery of the fraud and

within five years of Plaintiffs’ purchases of securities giving rise to the cause of

action.

FIRST CLAIM Violation of Section 20(a) of The Exchange Act

Against the Individual Defendants

160. Plaintiffs repeat and reallege each and every allegation contained

above as if fully set forth herein.

161. This Second Claim is asserted against each of the Individual

Defendants.

30 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 32 of 35 Page ID #:338

162. The Individual Defendants, acted as controlling persons of Gulf

Resources within the meaning of Section 20(a) of the Exchange Act as alleged

herein. By virtue of their high-level positions as Chairman, CEO and CFO, agency,

and their stock ownership and contractual rights, participation in and/or awareness

of the Company’s operations and/or intimate knowledge of aspects of the

Company’s revenues and earnings and dissemination of information to the

investing public, the Individual Defendants had the power to influence and control,

and did influence and control, directly or indirectly, the decision-making of the

Company, including the content and dissemination of the various statements that

Plaintiffs contend are false and misleading. The Individual Defendants were

provided with or had unlimited access to copies of the Company’s reports, press

releases, public filings and other statements alleged by Plaintiffs to be misleading

prior to and/or shortly after these statements were issued, and had the ability to

prevent the issuance of the statements or to cause the statements to be corrected.

163. In particular, each of these Defendants had direct and supervisory

involvement in the day-to-day operations of the Company and, therefore, is

presumed to have had the power to control or influence the particular transactions

giving rise to the securities violations as alleged herein, and exercised the same.

164. As set forth above, Gulf Resources and the Individual Defendants each

violated Section 10(b) and Rule 10b-5 by their acts and omissions as alleged in this

Complaint.

165. By virtue of their positions as controlling persons, the Individual

Defendants are liable pursuant to Section 20(a) of the Exchange Act as they

culpably participated in the fraud alleged herein. As a direct and proximate result of

Defendants’ wrongful conduct, Plaintiffs and other members of the Class suffered

damages in connection with their purchases of the Company’s common stock

during the Class Period.

166. This action was filed within two years of discovery of the fraud and

31 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 33 of 35 Page ID #:339

within five years of Plaintiffs’ purchases of securities giving rise to the cause of

action.

WHEREFORE , Plaintiff prays for relief and judgment, as follows:

(a) Determining that this action is a proper class action, designating

Plaintiff as Lead Plaintiff and certifying Plaintiff as a class representative under

Rule 23 of the Federal Rules of Civil Procedure and Plaintiff’s counsel as Lead

Counsel;

(b) Awarding compensatory damages in favor of Plaintiff and the

other Class members against all Defendants, jointly and severally, for all damages

sustained as a result of Defendants’ wrongdoing, in an amount to be proven at trial,

including interest thereon;

(c) Awarding plaintiff and the Class their reasonable costs and

expenses incurred in this action; and

(d) Such other and further relief as the Court may deem just and

proper.

JURY TRIAL DEMANDED

Plaintiff hereby demands a trial by jury.

Dated: September 12, 2011 Respectfully submitted,

THE ROSEN LAW FIRM, P.A.

Laurence M. Rosen, Esq. (LR 5733) THE ROSEN LAW FIRM, P.A. 355 South Grand Avenue, Suite 2450 Los Angeles, CA 90071

32 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 34 of 35 Page ID #:340

Telephone: (213) 785-2610 Facsimile: (213) 226-4684 Email: [email protected]

and

Francis A. Bottini, Jr., Esq. (SBN 175783) Chapin Fitzgerald Sullivan & Bottini LLP 550 West C Street, Suite 2000 San Diego, CA 92101 Telephone: (619) 241-4810 Facsimile: (619) 955-5318 Email: [email protected]

Lead Counsel for Plaintiffs and the Class

33 Amended Class Action Complaint for Violations of the Federal Securities Laws

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Case 2:11-cv-03722-ODW -MRW Document 28 Filed 09/12/11 Page 35 of 35 Page ID #:341

![ADMISSIONS GUIDELINE FOR INTERNATIONAL …...50 Yonsei-ro, Seodaemun-gu, Seoul, South Korea 03722 Korean [03722] 서울특별시 서대문구 연세로 50 새천년관 510 호 Office](https://img.pdfslide.us/doc/110x75/5f59f42bd7603c52cc756ef5/admissions-guideline-for-international-50-yonsei-ro-seodaemun-gu-seoul-south.jpg)