Embed Size (px)

Citation preview

________________________________

OFFICE OF CONTRACTS AND GRANTS

CAS & COMPLIANCE

2009 **This workbook was last updated in FY 2009, so there may have

been new regulations that are now in effect. **

1

NORTH CAROLINA STATE UNIVERSITY OFFICE OF CONTRACTS & GRANTS

TABLE OF CONTENTS

Page # POST AWARD ADMINISTRATIVE COMPLIANCE

Compliance Responsibilities 3-4 Pre-Audit Responsibilities 5 Sponsored Award Guidance 6

Definitions of Costs 7 Allowable Direct Costs 8

Unallowable Costs 9 Compliance Issues 10-11 Compliance Tools 12 COST ACCOUNTING STANDARDS

The Standards And Their Requirements 14 Cas Applicability 15 Roles And Responsibilities 16 Cost Allocation:

1. OMB “Unlike” Circumstances (Salaries & Benefits) 17 2. Specific Cost Allocation Issues 18-19 Judgement Process 20

Invalid Arguments 21 Written Justifications 22

Appendix

2

POST AWARD ADMINISTRATIVE

COMPLIANCE

3

COMPLIANCE RESPONSIBILITIES Contracts And Grants

The Office of Contracts and Grants, under the direction of the Associate Vice Chancellor of the Financial Services Division, is responsible to the University and to the funding agencies for the financial and post award administration of all contracts and grants awarded to North Carolina State University. This responsibility includes, but is not limited to: a. Establish, communicate and promote policies and procedures consistent with federal, state and sponsor regulations b. Provide assistance with proposal budget preparation if requested by the college c. Determine the propriety and reasonableness of costs d. Exercise budgetary control of contracts and grants funds e. Prepare and submit financial reports and invoices f. Make timely deposits of contract and grant receipts from sponsors and follow up with sponsors on delinquent payments g. Prepare timely G/L cash reconciliation h. Process prior approval requests when sponsor has delegated the authority or submit requests to other University offices or the sponsor when necessary i. Submit final financial reports, equipment inventories, and intangible asset disclosure statements to funding agencies j. Maintain an effective, auditable effort reporting system k. Monitor all payroll reallocation transactions l. Develop and negotiate the University's F&A cost rates m. Review and approve all special service facility rates n. Coordinate formal audits or interim reviews of contracts and grants by sponsoring agencies o. Provide support and guidance to college business offices for the effective administration and financial management of contracts and grants p. Perform annual subrecipient monitoring in accordance with OMB Circular A-133 and NCSU procedures q. Maintain the University's Cost Accounting Standards Disclosure Statement and submit changes to cost accounting practices as necessary.

4

COMPLIANCE RESPONSIBILITIES College/Unit

Certain compliance and pre-audit functions are the responsibility of the individual colleges and units as follows: a. Provide necessary training within the college for each employee. b. Ensure consistency in budgeting of direct costs vs. facilities and administrative (F&A) costs (pre-award phase). c. Ensure consistency in charging of direct vs. F&A costs (pre-audit function). d. Ensure budgets submitted to sponsoring agencies are in compliance with all applicable sponsor regulations. e. Conduct pre-audit reviews of all charges to sponsored awards to ensure that expenditures and subsequent adjustments to expenditures are reasonable, allowable, allocable, timely and non-personal and applied consistently in like circumstances. f. Ensure prior approvals for expenditures and activities are obtained when required. g. Ensure compliance with cost sharing commitments on sponsored projects. h. Establish internal procedures to ensure the timely processing of personnel actions and retroactive payroll adjustments which affect sponsored awards. i. Monitor and maintain the committed level of effort on sponsored projects. j. Ensure the conscientious completion, certification, and timely return of effort reports. k. Prevent budget overdrafts. l. Ensure all adjustments to expenditures are performed timely. m. Review subcontractor costs for reasonableness and compliance. n. Perform monthly reviews of charges to sponsored awards (Ledger 5 projects) appearing on Wolfpack Reports. o. Provide timely account close-out notices and timely processing of close-out adjustments. p. Ensure all technical reports are completed and submitted on a timely basis. r. Obtain and retain appropriate support documentation for financial transactions. This includes cost sharing documentation.

5

COMPLIANCE RESPONSIBILITIES

WHAT IS THE “PRE-AUDIT” FUNCTION?

The “pre-audit” function is a review process involving the accurate application of sponsored award costs in accordance with all applicable policies and procedures. This responsibility has been delegated to the College business offices/research offices. Some Colleges, based on their internal organization and structure have further delegated these responsibilities to individual departments. The “pre-audit” review process should at a minimum include the following: 1. A thorough review of all types of costs that will be or have been charged (in the

case of some internal billing processes) to sponsored award accounts. Does the budget support a line item for this charge/cost? Are there sufficient funds available to support this charge/cost? Is the charge “allowable” against the particular award? Has the charge been incurred within the project period? Are transfers of costs made in a timely manner? Is documentation sufficient to support the charge? 2. Review of all subcontractor costs/invoices (joint responsibility – PI and business

office) 3. Knowledge of when “Prior Approval” is necessary for post award administrative

changes. 4. Ability to provide adequate technical justifications on all prior approval requests

5. Prevention of account overdrafts (direct and F&A totals) 6. A thorough monthly reconciliation of the expenditure reports

6

SPONSORED AWARD GUIDANCE

SPONSORED AWARDS MUST BE IN COMPLIANCE WITH A VARIETY

OF REGULATORY DOCUMENTS The primary authoritative documents include: • Federal OMB Circular A-21, “Cost Principles for Educational Institutions” http://www.whitehouse.gov/omb/circulars/a021/a21_2004.html • Cost Accounting Standards (CAS) Can be referenced separately or as part of A-21 (Appendix A) • NCSU’s Disclosure Statement (DS-2) This is a document required by 48 CFR 9903 for Educational Institutions. It is a written description of our cost accounting practices and procedures. • Federal OMB Circular A-110, “Uniform Administrative Requirements for Grants and Agreements” http://www.whitehouse.gov/omb/circulars/a110/a110.html • Federal Demonstration Partnership Agreement (FDP IV) The Federal Demonstration Partnership is a cooperative initiative among 10 federal agencies and 98 institutional recipients of federal funds; its purpose is to reduce the administrative burdens associated with research grants and contracts. http://www.nsf.gov/awards/managing/fed_dem_part.jsp • NCSU PRRs (Policies, Regulations and Rules) http://www.ncsu.edu/policies/research/navigation.php • CFR (Code of Federal Regulations) http://www.gpoaccess.gov/cfr/index.html • FAR clauses (Federal Acquisition Regulation) http://www.arnet.gov/far/ • Specific Sponsor regulations and requirements • Individual agreement terms/conditions • Award budgets

DEFINITIONS OF COSTS

7

ALLOWABLE COSTS - these costs under the provisions of any pertinent law, regulation, or sponsored agreement, can be included in prices, cost reimbursements, or settlements of the sponsoring agency. These costs must meet specific criteria in order to be considered “allowable” on sponsored awards.

DIRECT COSTS - these costs are specifically identifiable with an

individual project. This identification can be made with relative ease and a high degree of accuracy.

FACILITIES & ADMINISTRATIVE (F&A/INDIRECT) COSTS - these costs are for general institutional expenses. These costs are incurred for a common objective and are included in the University’s facilities & administrative (indirect) cost proposal and rate agreement.

UNALLOWABLE COSTS - these costs under the provisions of any pertinent law, regulation, or sponsored agreement, can not be included in prices, cost reimbursements, or settlements of the sponsoring agency.

THE THEORY OF: ALLOCABILITY - the assignment of an item of cost to one or more sponsored awards/accounts, of which each award/account charged receives a realistic proportional benefit from the incurrence of the cost. There must be a correlation between the direct benefit received and the portion of the cost that is charged to each project/account.

ALLOWABLE DIRECT COSTS

8

MUST MEET EACH OF THESE CRITERIA:

Necessary: Must be needed to accomplish the approved goals and objectives of the project Reasonable: Must be prudent given the stated goals and objectives Timely: Must be charged to the project on a timely basis:

(ALL transfers and adjustments must be completed within 90 days of their original incurrence)

Non-Personal: Cannot be of a personal nature or result in a benefit not normally provided to employees

Consistent: Costs must be applied in the same manner in “like

circumstances”

9

UNALLOWABLE COSTS

SPECIFIC COSTS THAT ARE UNALLOWABLE CHARGES TO SPONSORED PROJECTS:

Advertising (Institutional) Goods/Services for Personal Use Alcoholic Beverages Insurance Against Defects Alumni Activities Legal Fees* Bad Debts Lobbying Costs Commencement & Convocation Expenses Losses/Cost Overruns on Sponsored Projects Contingency Provisions Memberships in Civic, Community Organizations, & Country Clubs Donations & Contributions Public Relations* Entertainment Selling & Marketing Costs Fines & Penalties Student Activity Costs* Trustees Expenses * Costs may be allowable if approved in advance, but are generally unallowable.

10

COMPLIANCE ISSUES FEDERAL REGULATORY CHECKLIST - This is a quick reference guide provided by The Office of Contracts and Grants to assist you with compliance issues on individual projects. It provides information related to prior approvals, restrictions, and level of approval. COST TRANSFERS - Costs should only be charged to sponsored awards if those costs directly relate to the goals and objectives of that project. The NCSU policy regarding the transfer of ALL charges requires that the transfer be made within 90 days of the original date of incurrence. In addition, the effort report should be re-certified within the appropriate time period (depends of where we are in the certification process) to assure that what was paid in labor distribution matches actual effort. This policy applies to all salary charges, both monthly and biweekly, and non-salary expenditures. The Director of the Office of Contracts and Grants must approve transfers of salary expenditures made later than 90 days. A written explanation, signed by the Dean, must be submitted for approval of the transfer. For transfers of non-salary expenditures, an adequate explanation should be documented on the appropriate journal entry. The justification “to move charges to correct account” is NOT an adequate justification.

A delay in the expected receipt of future funding IS NOT justification for making charges to another sponsored award, even if the projects are related. Request a “Pre-Award” account from SPARCS.

BUDGET OVERDRAFTS - The College and Principal Investigator are responsible for preventing budget overdrafts. Federal, State and Private Sponsors DO NOT permit the transfer of costs to other sponsored projects for the purpose of: • Eliminating overdrafts caused by expenditure overruns, • Avoiding restrictions, • Other reasons of convenience Cost overruns should be transferred within 90 days of occurrence or sooner if at closeout of the project. The Office of Contracts and Grants reserves the right to transfer these expenditures to the College’s or the Department’s operating budget if not transferred within the 90-day time frame. The College is responsible for all over-expenditures in the event that future funding is not received.

11

PURCHASES MADE IN THE LAST FEW MONTHS - Auditors, often question purchases made in the last few months of an award, especially the last three (3) months. Frequently, items or services purchased late in an award period are scrutinized to ensure that the costs can meet the criteria of “allowable direct” costs. These criteria include:

• Reasonableness, • Necessity/Purpose • Allocability

If the expenditure cannot meet these criteria, the cost may be considered an unallowable charge against the sponsored award. This is especially true with purchases of:

• Equipment • Supplies

as these types of costs are generally associated with the technical aspects of the project. Generally speaking, unless a no-cost extension is in progress, these types of costs should not be as frequent near the end of a project’s life. Journal Voucher entries processed near the end of an award period also present a concern. These are considered “red flags” to auditors as they represent the movement of costs between funding sources.

Purchases should not be made in an attempt to “spend-out” an account balance. Ensure that purchases made near the end of the project’s funding period can meet the definition of “allowable” and are required in order to meet the specific goals and objectives of the award being charged.

RECORD RETENTION -- All supporting documentation should be retained for at least THREE (3) years after the date of last financial transaction, depending on the specifics of the individual sponsored award. The Office of Contracts and Grants will provide the college a list of projects that have been destroyed in C&G. At this time you can destroy any college/departmental files. SUBCONTRACTORS – The college/department should ensure that proper internal controls are in place to address subcontractor invoices. The University is acting as the primary agency for these invoices and the college/department should verify dates, calculations, work performed, etc before approving for payment. SERVICE CENTER FACILITIES – Any service center facility or “recharge” facility that provides a good or service to a “ledger 5” project should have an approved use rate. The Office of Contracts and Grants approves these rates. See http://www.ncsu.edu/policies/research/contracts_grants/REG10.05.9.php for more information.

12

COMPLIANCE TOOLS New Award Meeting – Can be requested by College Business Offices for any award. Mostly used for awards for new faculty, agencies that are new to the college, awards with unusual terms and conditions… Federal Regulatory Checklist – provided for all federal and federal flow-through projects by the office of Contracts and Grants. These are award and agency specific. It is used to provide quick information pertaining to prior approval issues and other common terms and conditions. Mentoring across Departments/Colleges RAMP College Training Q&A Sessions – Available to anyone who would like to attend. Reminders go out using the RSC listserv. The dates are posted on the Contracts and Grants website. RSC – Research Support Council Networking

13

COST ACCOUNTING STANDARDS

14

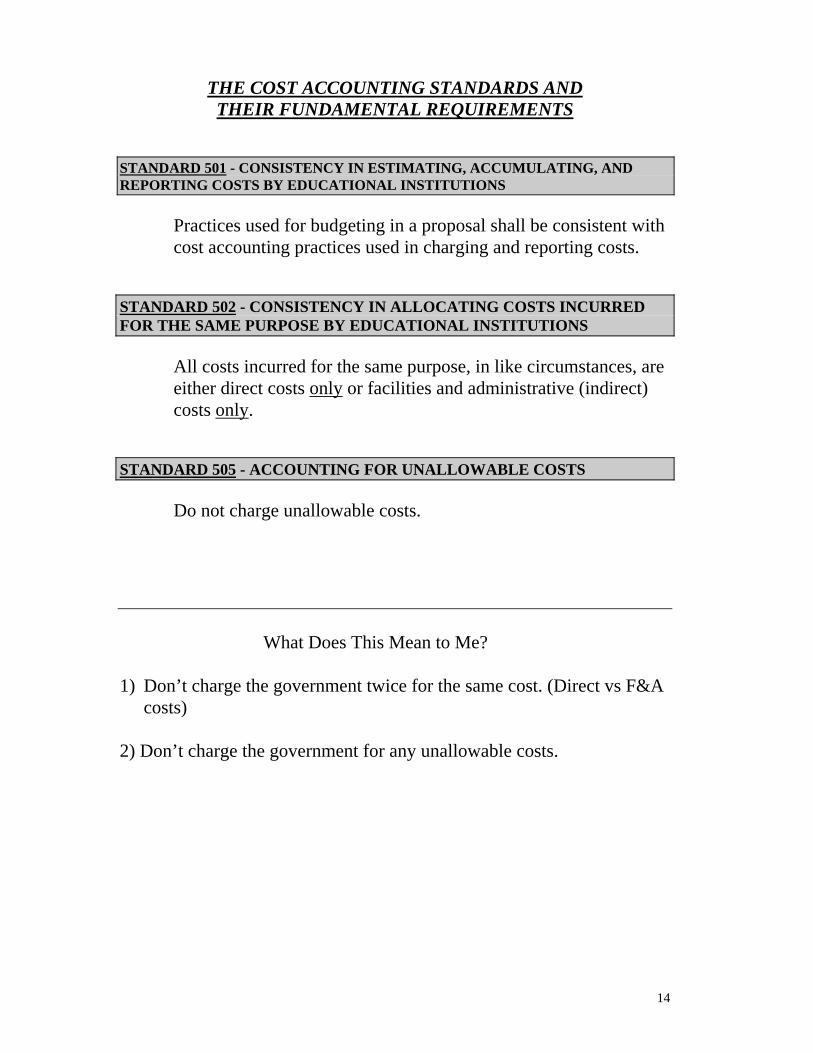

THE COST ACCOUNTING STANDARDS AND THEIR FUNDAMENTAL REQUIREMENTS

STANDARD 501 - CONSISTENCY IN ESTIMATING, ACCUMULATING, AND REPORTING COSTS BY EDUCATIONAL INSTITUTIONS

Practices used for budgeting in a proposal shall be consistent with cost accounting practices used in charging and reporting costs.

STANDARD 502 - CONSISTENCY IN ALLOCATING COSTS INCURRED FOR THE SAME PURPOSE BY EDUCATIONAL INSTITUTIONS

All costs incurred for the same purpose, in like circumstances, are either direct costs only or facilities and administrative (indirect) costs only.

STANDARD 505 - ACCOUNTING FOR UNALLOWABLE COSTS

Do not charge unallowable costs.

What Does This Mean to Me?

1) Don’t charge the government twice for the same cost. (Direct vs F&A costs)

2) Don’t charge the government for any unallowable costs.

15

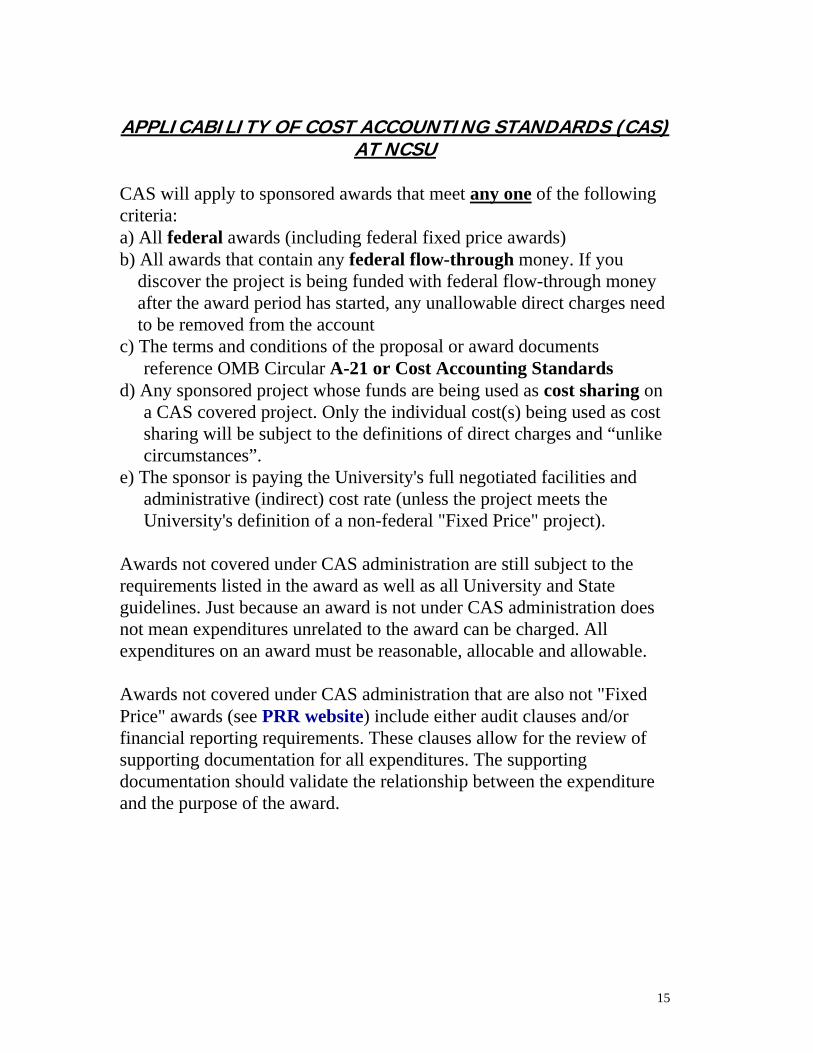

APPLICABILITY OF COST ACCOUNTING STANDARDS (CAS) AT NCSU

CAS will apply to sponsored awards that meet any one of the following criteria: a) All federal awards (including federal fixed price awards) b) All awards that contain any federal flow-through money. If you

discover the project is being funded with federal flow-through money after the award period has started, any unallowable direct charges need to be removed from the account

c) The terms and conditions of the proposal or award documents reference OMB Circular A-21 or Cost Accounting Standards

d) Any sponsored project whose funds are being used as cost sharing on a CAS covered project. Only the individual cost(s) being used as cost sharing will be subject to the definitions of direct charges and “unlike circumstances”.

e) The sponsor is paying the University's full negotiated facilities and administrative (indirect) cost rate (unless the project meets the University's definition of a non-federal "Fixed Price" project).

Awards not covered under CAS administration are still subject to the requirements listed in the award as well as all University and State guidelines. Just because an award is not under CAS administration does not mean expenditures unrelated to the award can be charged. All expenditures on an award must be reasonable, allocable and allowable. Awards not covered under CAS administration that are also not "Fixed Price" awards (see PRR website) include either audit clauses and/or financial reporting requirements. These clauses allow for the review of supporting documentation for all expenditures. The supporting documentation should validate the relationship between the expenditure and the purpose of the award.

16

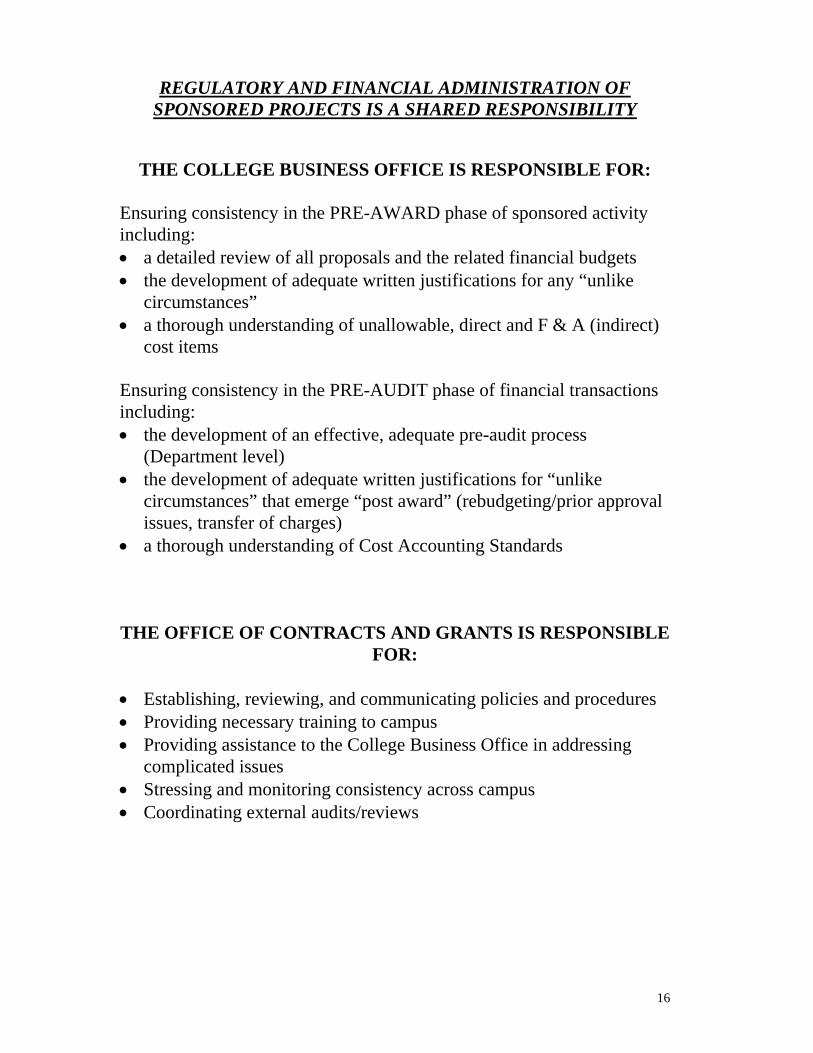

REGULATORY AND FINANCIAL ADMINISTRATION OF SPONSORED PROJECTS IS A SHARED RESPONSIBILITY

THE COLLEGE BUSINESS OFFICE IS RESPONSIBLE FOR: Ensuring consistency in the PRE-AWARD phase of sponsored activity including: • a detailed review of all proposals and the related financial budgets • the development of adequate written justifications for any “unlike

circumstances” • a thorough understanding of unallowable, direct and F & A (indirect)

cost items Ensuring consistency in the PRE-AUDIT phase of financial transactions including: • the development of an effective, adequate pre-audit process

(Department level) • the development of adequate written justifications for “unlike

circumstances” that emerge “post award” (rebudgeting/prior approval issues, transfer of charges)

• a thorough understanding of Cost Accounting Standards THE OFFICE OF CONTRACTS AND GRANTS IS RESPONSIBLE

FOR: • Establishing, reviewing, and communicating policies and procedures • Providing necessary training to campus • Providing assistance to the College Business Office in addressing

complicated issues • Stressing and monitoring consistency across campus • Coordinating external audits/reviews

17

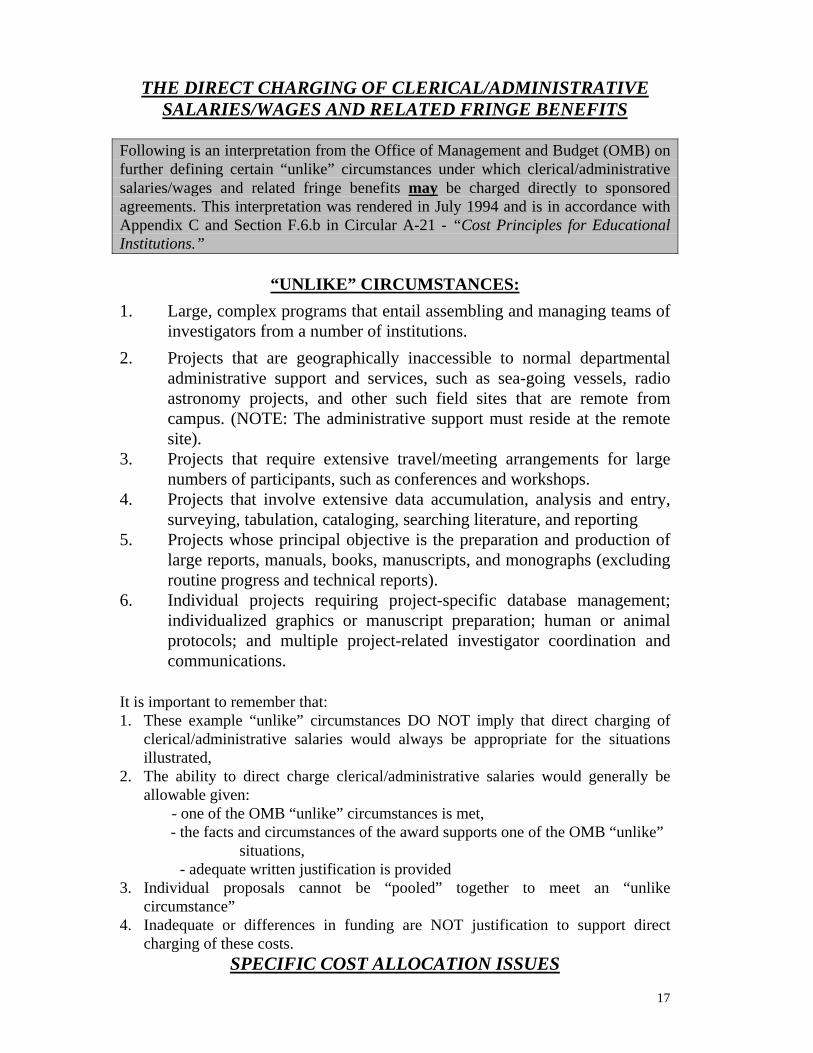

THE DIRECT CHARGING OF CLERICAL/ADMINISTRATIVE SALARIES/WAGES AND RELATED FRINGE BENEFITS

Following is an interpretation from the Office of Management and Budget (OMB) on further defining certain “unlike” circumstances under which clerical/administrative salaries/wages and related fringe benefits may be charged directly to sponsored agreements. This interpretation was rendered in July 1994 and is in accordance with Appendix C and Section F.6.b in Circular A-21 - “Cost Principles for Educational Institutions.”

“UNLIKE” CIRCUMSTANCES: 1. Large, complex programs that entail assembling and managing teams of

investigators from a number of institutions. 2. Projects that are geographically inaccessible to normal departmental

administrative support and services, such as sea-going vessels, radio astronomy projects, and other such field sites that are remote from campus. (NOTE: The administrative support must reside at the remote site).

3. Projects that require extensive travel/meeting arrangements for large numbers of participants, such as conferences and workshops.

4. Projects that involve extensive data accumulation, analysis and entry, surveying, tabulation, cataloging, searching literature, and reporting

5. Projects whose principal objective is the preparation and production of large reports, manuals, books, manuscripts, and monographs (excluding routine progress and technical reports).

6. Individual projects requiring project-specific database management; individualized graphics or manuscript preparation; human or animal protocols; and multiple project-related investigator coordination and communications.

It is important to remember that: 1. These example “unlike” circumstances DO NOT imply that direct charging of

clerical/administrative salaries would always be appropriate for the situations illustrated,

2. The ability to direct charge clerical/administrative salaries would generally be allowable given:

- one of the OMB “unlike” circumstances is met, - the facts and circumstances of the award supports one of the OMB “unlike”

situations, - adequate written justification is provided 3. Individual proposals cannot be “pooled” together to meet an “unlike

circumstance” 4. Inadequate or differences in funding are NOT justification to support direct

charging of these costs. SPECIFIC COST ALLOCATION ISSUES

18

GENERAL OFFICE SUPPLIES Costs include those incurred in support of routine administrative activities associated with instruction, public service, research and other institutional activities, (i.e., usb flash drives, paper, pencils, ink, toner cartridges, office furniture, external hard drives, staplers, note books, etc.). These items of cost are considered readily expendable and are treated as facilities and administrative costs covered by the negotiated F&A cost rate. The only exceptions are those wherein the purchase of the supplies is extensive in nature, can be specifically identified to the project, and meets the definition of a direct charge. The College should provide adequate written justification in the proposal narrative for the direct charging of costs in this category, explaining that the supplies were a direct benefit to the purpose of the project and can be specifically identified with the project. In addition, support documentation must be adequately detailed to pass an audit. Computers and Peripherals: The original purchase can either be charged as technical (direct) or general purpose (F&A) depending upon the ACTUAL usage of the items OR more likely, a combination of both (direct and F&A allocation). Replacement Parts: Are to be charged/allocated based on their current ACTUAL usage/benefit to various awards/accounts. Upgrades and Additions: Are to be charged based on the proportional benefits received to various awards/accounts. POSTAGE EXPENSES Postage expense incurred in support of routine administrative communication activities associated with instruction, public service, research, and other institutional activities should not be charged directly to sponsored accounts. The only exceptions are those cases where extensive postage expense is required in support of the goals and objectives of the sponsored award being charged. For example, if the purpose of your project were to survey 10,000 high school students to determine their attitudes on violence in the school system, the postage for the survey would be an allowable direct charge. The written justification should demonstrate that the postage provided a direct benefit to the purpose of the project, is extensive, and can be specifically identified with the project. In addition, support documentation must be adequately detailed to pass an audit. Mailing technical reports and other project deliverables are considered part of normal, routine business expenses and are therefore considered F&A costs. Postage expenses include US Mail, Federal Express, UPS, etc. The difference between postage (F&A) and freight (direct) is driven by the item(s) being sent not the means by which it is sent. MEMBERSHIPS AND SUBSCRIPTIONS Institutional memberships in professional organizations and subscriptions to technical periodicals are normally treated as an F&A cost. They may be charged direct only when related to a specific project and necessary for the successful completion of the goals and objectives of the project. Allocation, when applicable, should be able to be accomplished with relative ease and a high degree of accuracy.

19

Generally, individual memberships are unallowable. Individual memberships in civic or social organizations are expressly unallowable. An individual membership or subscription to a professional group or periodical may be allowed as a direct charge to a contract or grant only if the following can be demonstrated: 1. An institutional membership is not available or will not meet the needs of the project. 2. The cost has been justified (i.e. provides a direct benefit to the purpose of the project) in

the proposal or a justification is in the College file if the need arises after the project was awarded.

TELEPHONE AND VARIOUS OTHER COMMUNICATION EXPENSES Communication expenses incurred in support of routine administrative activities associated with instruction, public service, research and other institutional activities should not be charged directly against sponsored projects. Installation charges, monthly use charges, local access calls, pagers, etc. are considered F&A costs and should not be charged directly to sponsored accounts. The only exceptions are those relating to long distance calls, fax long distance charges, equipment charges (dedicated research/lab lines), and various other communication expenses specific to a project and incurred for the sole direct benefit of the project. Support documentation must be adequately detailed to pass an audit.

Cellular Phones – Per NCSU policy, individuals who require cellular telephone service to conduct University business must obtain approval from the dean or department head of their unit. Orders for cellular services and equipment must be placed through the University. The services paid for by the University are to be used in the conduct of University business. These phones and their charges would require an unlike circumstance in order to be charged to a sponsored award. Use of Personal Cellular Service for Business - Reimbursement of the employee for cellular telephone usage for business calls will be handled the same as making business calls away from the office. The employee may request reimbursement monthly. A copy of the cellular bill denoting business related calls must be submitted for reimbursement, with personal calls blacked out for privacy. No reimbursement will be made for the instrument, monthly fees, or the portion of "free" minutes. The employee should also provide information on how the call relates to the purpose of the project

How Do I Decide?

20

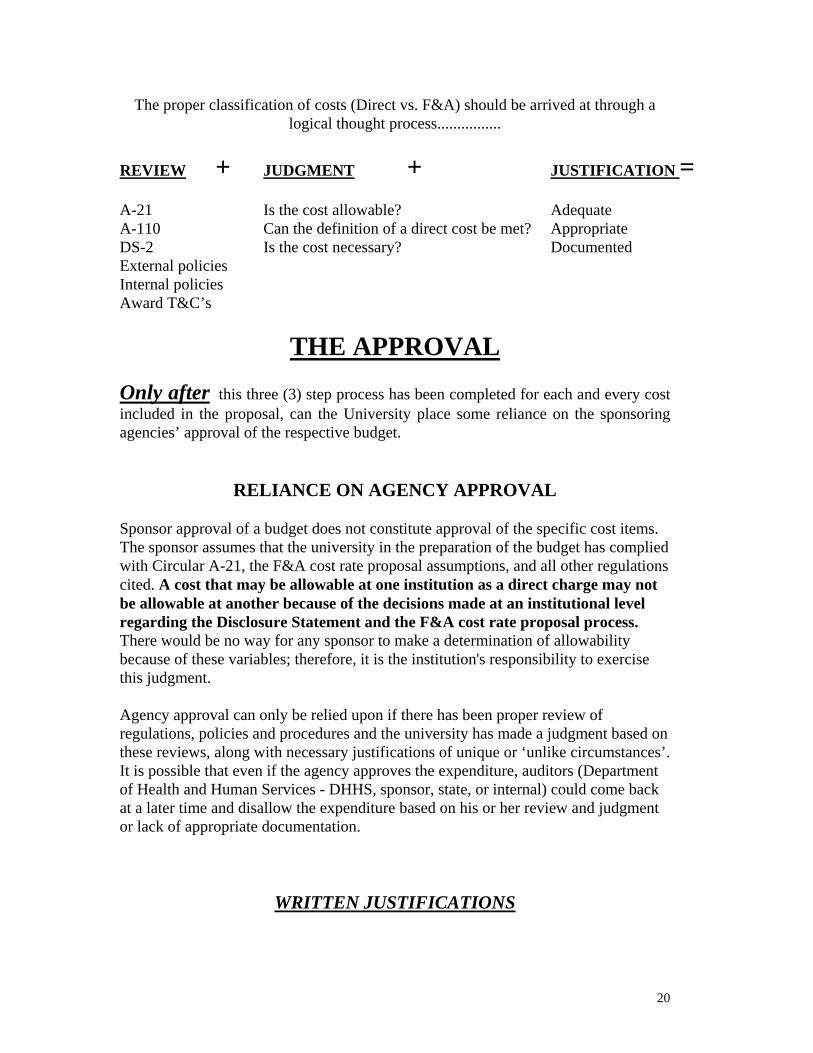

The proper classification of costs (Direct vs. F&A) should be arrived at through a

logical thought process................

REVIEW + JUDGMENT + JUSTIFICATION = A-21 Is the cost allowable? Adequate A-110 Can the definition of a direct cost be met? Appropriate DS-2 Is the cost necessary? Documented External policies Internal policies Award T&C’s

THE APPROVAL Only after this three (3) step process has been completed for each and every cost included in the proposal, can the University place some reliance on the sponsoring agencies’ approval of the respective budget.

RELIANCE ON AGENCY APPROVAL Sponsor approval of a budget does not constitute approval of the specific cost items. The sponsor assumes that the university in the preparation of the budget has complied with Circular A-21, the F&A cost rate proposal assumptions, and all other regulations cited. A cost that may be allowable at one institution as a direct charge may not be allowable at another because of the decisions made at an institutional level regarding the Disclosure Statement and the F&A cost rate proposal process. There would be no way for any sponsor to make a determination of allowability because of these variables; therefore, it is the institution's responsibility to exercise this judgment. Agency approval can only be relied upon if there has been proper review of regulations, policies and procedures and the university has made a judgment based on these reviews, along with necessary justifications of unique or ‘unlike circumstances’. It is possible that even if the agency approves the expenditure, auditors (Department of Health and Human Services - DHHS, sponsor, state, or internal) could come back at a later time and disallow the expenditure based on his or her review and judgment or lack of appropriate documentation.

WRITTEN JUSTIFICATIONS

21

In accordance with NCSU policies and procedures, the following cost items require detailed written budget justification on a “Narrative Budget Justification Page” or in the Proposal document (if required by the sponsoring agency).

• Clerical/Administrative Salaries • General Office Supplies (including computers) • Postage, Telephone calls, and Cell Phones • Memberships and Subscriptions

The justification must explain the purpose of the costs in sufficient detail to enable those responsible for reviewing the proposed budget to make a determination of whether the cost meets the definition of an ‘unlike circumstance’. It is important that written justifications quantify and fully explain the unique and extensive nature of the costs being considered for direct charging. These should be in writing and approved by the college business office. The “Narrative Budget Justification Page” should be retained by the College/Department with all other required pre-award documentation. In addition, written justifications should be obtained and retained by the College in instances of “Prior Approval” requests that involve the direct charging of costs that are normally considered as F&A. This information should be readily available to any auditor upon request. If a PAR is necessary, the written justification will need to be forwarded to the Office of Contracts and Grants as part of the request. All justifications should be detailed enough that a person could read only the justification and the abstract and feel comfortable with the decision that was made. Although one justification may suffice for all categories on a specific award, several justifications may be necessary depending on the award. Remember that each award must stand alone. A justification that works for one project may not be sufficient on another. This is especially important to remember when moving expenditures among projects.

22

Invalid Arguments For Unlike Circumstances

1. Insufficient Facilities and Administrative cost money from the

Sponsor to support the cost 2. Sponsor won’t pay any Facilities and Administrative costs 3. Sponsor approval without proper review by Institution 4. Sponsor is willing to pay the cost as direct 5. Cost represents a need versus being directly related to the

“purpose” of the award 6. Facilities and Administrative Costs earned are not made

available to the investigators

POVERTY IS NEVER AN EXCUSE!!!!!!!!!

23

APPENDIX

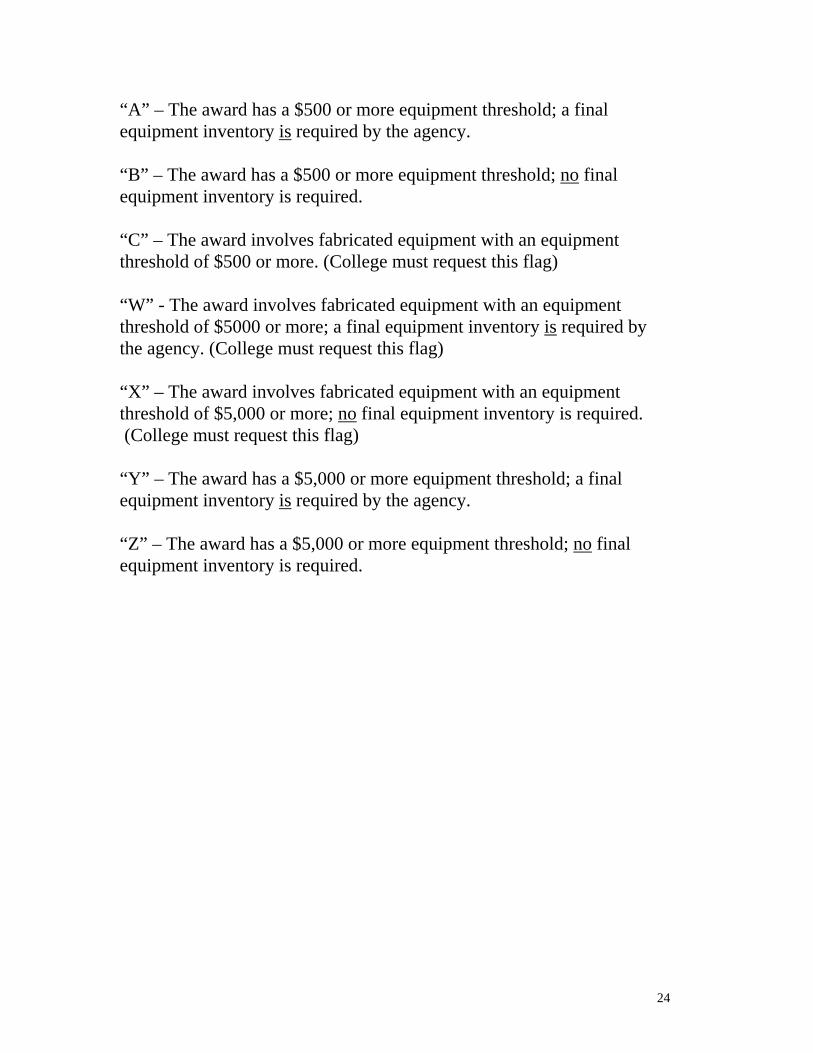

EQUIPMENT FLAG/INDICATORS IN PS

24

“A” – The award has a $500 or more equipment threshold; a final equipment inventory is required by the agency. “B” – The award has a $500 or more equipment threshold; no final equipment inventory is required. “C” – The award involves fabricated equipment with an equipment threshold of $500 or more. (College must request this flag) “W” - The award involves fabricated equipment with an equipment threshold of $5000 or more; a final equipment inventory is required by the agency. (College must request this flag) “X” – The award involves fabricated equipment with an equipment threshold of $5,000 or more; no final equipment inventory is required. (College must request this flag) “Y” – The award has a $5,000 or more equipment threshold; a final equipment inventory is required by the agency. “Z” – The award has a $5,000 or more equipment threshold; no final equipment inventory is required.

25

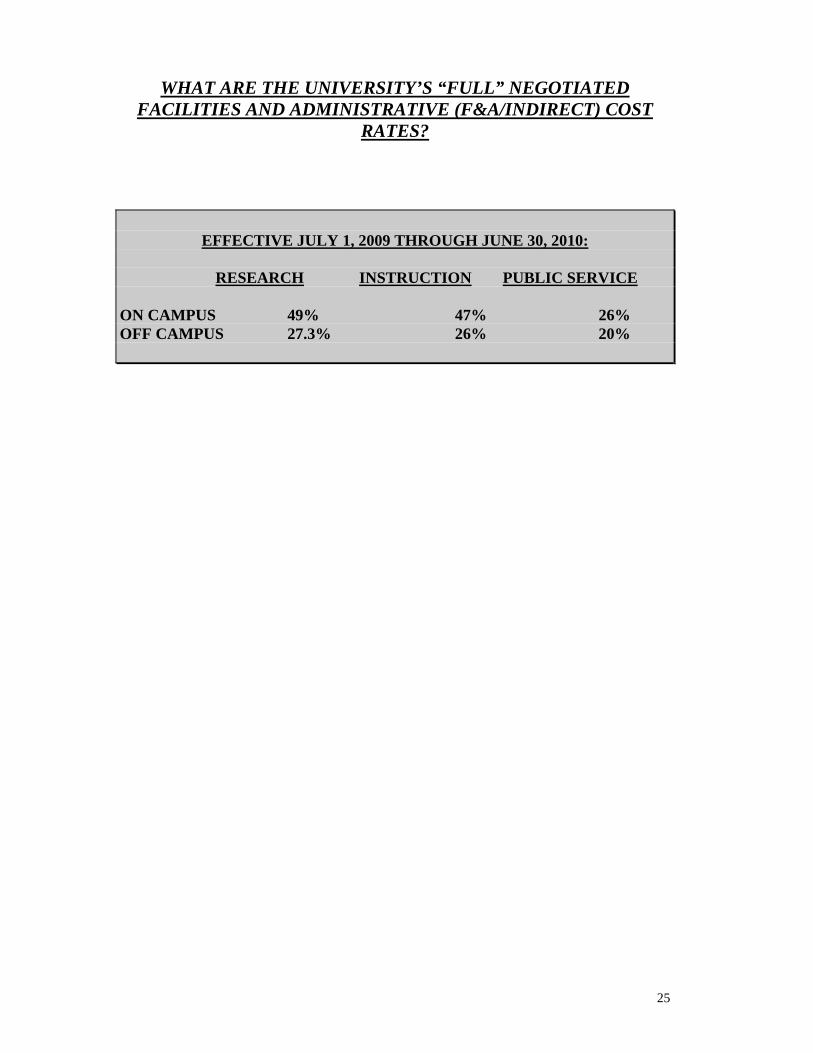

WHAT ARE THE UNIVERSITY’S “FULL” NEGOTIATED FACILITIES AND ADMINISTRATIVE (F&A/INDIRECT) COST

RATES?

EFFECTIVE JULY 1, 2009 THROUGH JUNE 30, 2010: RESEARCH INSTRUCTION PUBLIC SERVICE ON CAMPUS 49% 47% 26% OFF CAMPUS 27.3% 26% 20%