Embed Size (px)

Citation preview

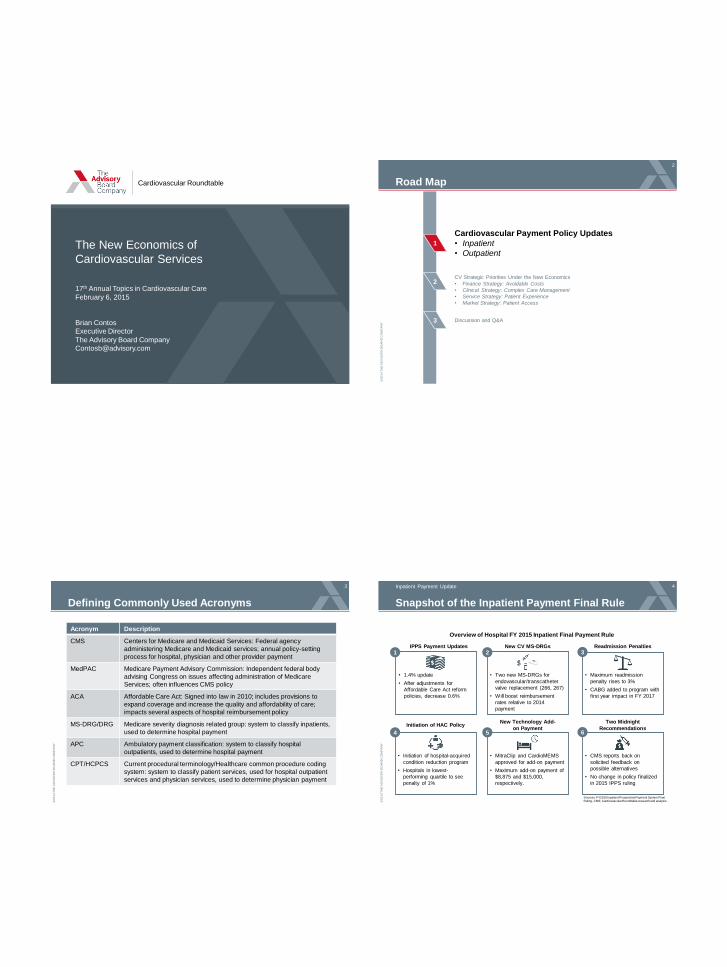

Cardiovascular Roundtable

The New Economics of

Cardiovascular Services

17th Annual Topics in Cardiovascular Care

February 6, 2015

Brian Contos

Executive Director

The Advisory Board Company

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Road Map

2

3

1

2

CV Strategic Priorities Under the New Economics

• Finance Strategy: Avoidable Costs

• Clinical Strategy: Complex Care Management

• Service Strategy: Patient Experience

• Market Strategy: Patient Access

Discussion and Q&A

Cardiovascular Payment Policy Updates

• Inpatient

• Outpatient

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Defining Commonly Used Acronyms

3

Acronym Description

CMS Centers for Medicare and Medicaid Services: Federal agency

administering Medicare and Medicaid services; annual policy-setting

process for hospital, physician and other provider payment

MedPAC Medicare Payment Advisory Commission: Independent federal body

advising Congress on issues affecting administration of Medicare

Services; often influences CMS policy

ACA Affordable Care Act: Signed into law in 2010; includes provisions to

expand coverage and increase the quality and affordability of care;

impacts several aspects of hospital reimbursement policy

MS-DRG/DRG Medicare severity diagnosis related group: system to classify inpatients,

used to determine hospital payment

APC Ambulatory payment classification: system to classify hospital

outpatients, used to determine hospital payment

CPT/HCPCS Current procedural terminology/Healthcare common procedure coding

system: system to classify patient services, used for hospital outpatient

services and physician services, used to determine physician payment

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Snapshot of the Inpatient Payment Final Rule

4

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

Inpatient Payment Update

z 1

z 2

z 3

z 4

z 5

z 6

IPPS Payment Updates Readmission Penalties

Initiation of HAC Policy New Technology Add-

on Payment

• Maximum readmission

penalty rises to 3%

• CABG added to program with

first year impact in FY 2017

• Initiation of hospital-acquired

condition reduction program

• Hospitals in lowest-

performing quartile to see

penalty of 1%

• MitraClip and CardioMEMS

approved for add-on payment

• Maximum add-on payment of

$8,875 and $15,000,

respectively.

New CV MS-DRGs

• Two new MS-DRGs for

endovascular/transcatheter

valve replacement (266, 267)

• Will boost reimbursement

rates relative to 2014

payment

Two Midnight

Recommendations

• CMS reports back on

solicited feedback on

possible alternatives

• No change in policy finalized

in 2015 IPPS ruling

• 1.4% update

• After adjustments for

Affordable Care Act reform

policies, decrease 0.6%

Overview of Hospital FY 2015 Inpatient Final Payment Rule

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

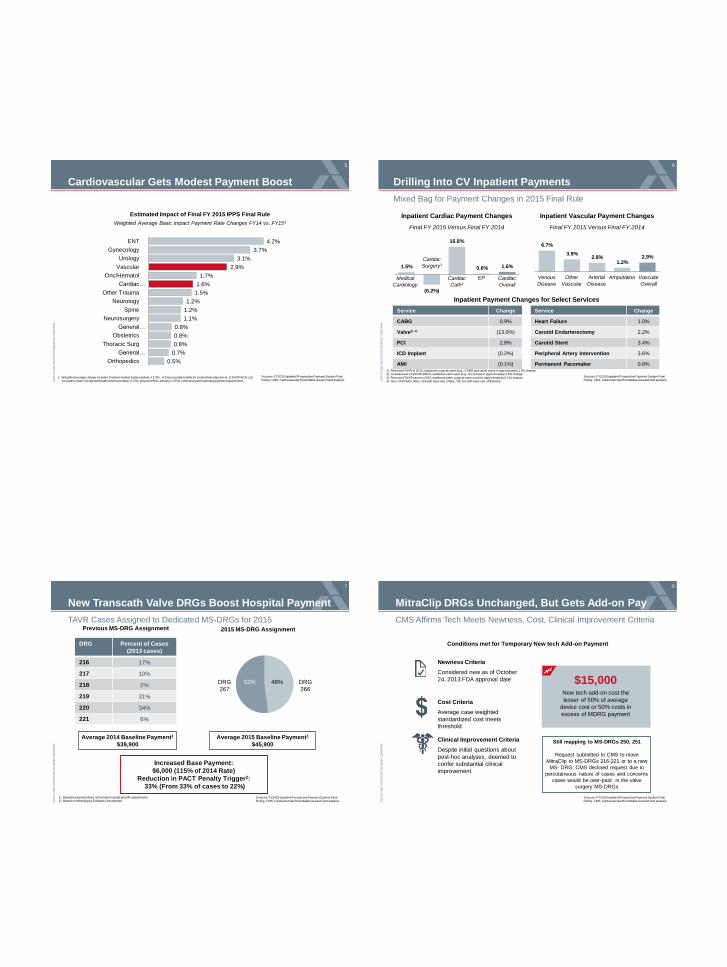

Cardiovascular Gets Modest Payment Boost

5

Estimated Impact of Final FY 2015 IPPS Final Rule

Weighted Average Basic Impact Payment Rate Changes FY14 vs. FY151

1. Weighted average change Includes: finalized market basket update (+2.9%, -0.5% proposed multifactor productivity adjustment,-0.2% PPACA cut), excludes impact of proposed readmissions penalty (-0.2%), proposed HAC penalty (-0.3%), other proposed operating payment adjustments

0.5%

0.7%

0.8%

0.8%

0.8%

1.1%

1.2%

1.2%

1.5%

1.6%

1.7%

2.9%

3.1%

3.7%

4.2%

Orthopedics

General…

Thoracic Surg

Obstetrics

General…

Neurosurgery

Spine

Neurology

Other Trauma

Cardiac…

Onc/Hematol

Vascular

Urology

Gynecology

ENT

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis. ©

20

14 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Drilling Into CV Inpatient Payments

6

Mixed Bag for Payment Changes in 2015 Final Rule

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

Service Change

CABG 0.9%

Valve3, 4 (13.0%)

PCI 2.8%

ICD Implant (0.2%)

AMI (0.1%)

Service Change

Heart Failure 1.0%

Carotid Endarterectomy 2.2%

Carotid Stent 3.4%

Peripheral Artery Intervention 3.6%

Permanent Pacemaker 0.8%

Inpatient Payment Changes for Select Services

1.5%

(6.2%)

16.8%

0.6% 1.6%

Inpatient Cardiac Payment Changes

Final FY 2015 Versus Final FY 2014

Cardiac

Surgery1

Cardiac

Cath2

EP Medical

Cardiology

Cardiac

Overall

6.7%

3.9% 2.8%

1.2% 2.9%

Amputation Other

Vascular

Arterial

Disease

Venous

Disease

Inpatient Vascular Payment Changes

Final FY 2015 Versus Final FY 2014

Vascular

Overall

1) Removed TAVR in 2015; traditional surgical cases (e.g., CABG and valve) result in approximately 1.0% change. 2) Includes new TAVR MS-DRGs; traditional cath cases (e.g., PCI) result in approximately 2.8% change.

3) Removed TAVR cases in 2015; traditional valve surgical cases result in approximately (0.1%) change. 4) New TAVR MS-DRGs: 266 with base rate of $52,743; 267 with base rate of $39,602.

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

New Transcath Valve DRGs Boost Hospital Payment

7

TAVR Cases Assigned to Dedicated MS-DRGs for 2015

1) Baseline payment does not include hospital-specific adjustments. 2) Based on Modeling by Edwards Lifesciences.

Previous MS-DRG Assignment

DRG Percent of Cases

(2013 cases)

216 17%

217 10%

218 2%

219 31%

220 34%

221 6%

52% 48% DRG

266

DRG

267

Increased Base Payment:

$6,000 (115% of 2014 Rate)

Reduction in PACT Penalty Trigger2:

33% (From 33% of cases to 22%)

Average 2014 Baseline Payment1

$39,900

Average 2015 Baseline Payment1

$45,900

2015 MS-DRG Assignment

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis. ©

20

14 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

MitraClip DRGs Unchanged, But Gets Add-on Pay

8

CMS Affirms Tech Meets Newness, Cost, Clinical Improvement Criteria

Conditions met for Temporary New tech Add-on Payment

Cost Criteria

Average case weighted

standardized cost meets

threshold

Newness Criteria

Considered new as of October

24, 2013 FDA approval date

Clinical Improvement Criteria

Despite initial questions about

post-hoc analyses, deemed to

confer substantial clinical

improvement

New tech add-on cost the

lesser of 50% of average

device cost or 50% costs in

excess of MDRG payment

$15,000

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

Still mapping to MS-DRGs 250, 251

Request submitted to CMS to move

MitraClip to MS-DRGs 216-221 or to a new

MS- DRG; CMS declined request due to

percutaneous nature of cases and concerns

cases would be over-paid in the valve

surgery MS-DRGs

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

10 10 21 27 30

44 45 55 57 59 59 57 63

Sta

rter

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

9

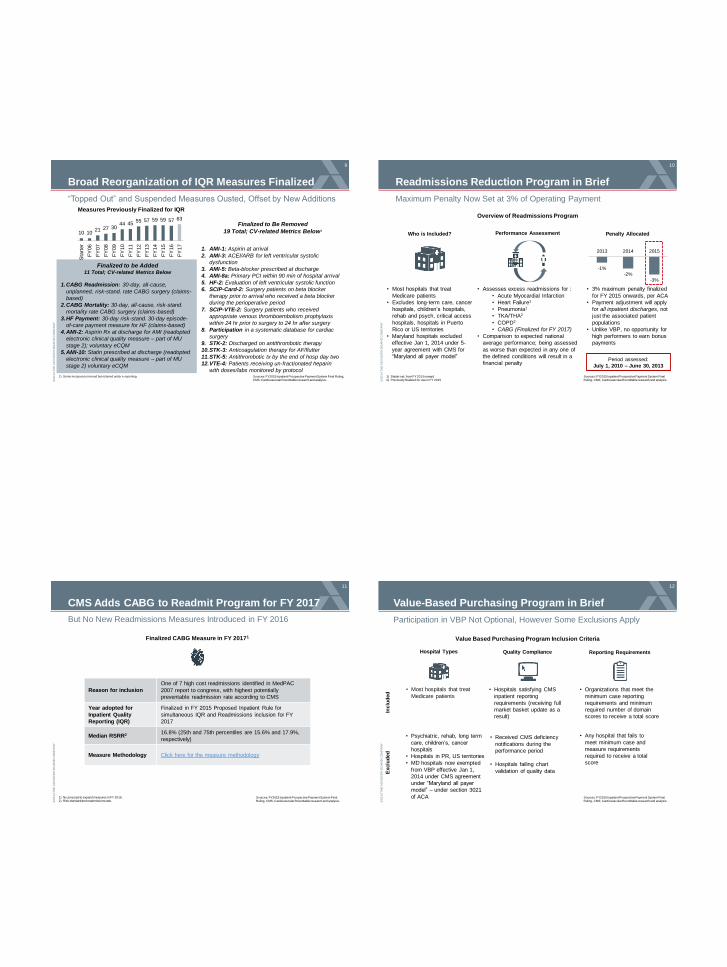

“Topped Out” and Suspended Measures Ousted, Offset by New Additions

1.CABG Readmission: 30-day, all-cause,

unplanned, risk-stand. rate CABG surgery (claims-

based)

2.CABG Mortality: 30-day, all-cause, risk-stand.

mortality rate CABG surgery (claims-based)

3.HF Payment: 30-day risk-stand. 30-day episode-

of-care payment measure for HF (claims-based)

4.AMI-2: Aspirin Rx at discharge for AMI (readopted

electronic clinical quality measure – part of MU

stage 2); voluntary eCQM

5.AMI-10: Statin prescribed at discharge (readopted

electronic clinical quality measure – part of MU

stage 2) voluntary eCQM

Finalized to be Added 11 Total; CV-related Metrics Below

Finalized to Be Removed

19 Total; CV-related Metrics Below1

Measures Previously Finalized for IQR

1. AMI-1: Aspirin at arrival

2. AMI-3: ACEI/ARB for left ventricular systolic

dysfunction

3. AMI-5: Beta-blocker prescribed at discharge

4. AMI-8a: Primary PCI within 90 min of hospital arrival

5. HF-2: Evaluation of left ventricular systolic function

6. SCIP-Card-2: Surgery patients on beta blocker

therapy prior to arrival who received a beta blocker

during the perioperative period

7. SCIP-VTE-2: Surgery patients who received

appropriate venous thromboembolism prophylaxis

within 24 hr prior to surgery to 24 hr after surgery

8. Participation in a systematic database for cardiac

surgery

9. STK-2: Discharged on antithrombotic therapy

10.STK-3: Anticoagulation therapy for AF/flutter

11.STK-5: Antithrombotic tx by the end of hosp day two

12.VTE-4: Patients receiving un-fractionated heparin

with doses/labs monitored by protocol Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

Broad Reorganization of IQR Measures Finalized

1) Some measures removed but retained under e-reporting. ©

20

14 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Readmissions Reduction Program in Brief

10

Maximum Penalty Now Set at 3% of Operating Payment

Who is Included? Performance Assessment Penalty Allocated

• Most hospitals that treat

Medicare patients

• Excludes long-term care, cancer

hospitals, children’s hospitals,

rehab and psych, critical access

hospitals, hospitals in Puerto

Rico or US territories

• Maryland hospitals excluded

effective Jan 1, 2014 under 5-

year agreement with CMS for

“Maryland all payer model”

• Assesses excess readmissions for :

• Acute Myocardial Infarction

• Heart Failure1

• Pneumonia1

• TKA/THA2

• COPD2

• CABG (Finalized for FY 2017)

• Comparison to expected national

average performance; being assessed

as worse than expected in any one of

the defined conditions will result in a

financial penalty

• 3% maximum penalty finalized

for FY 2015 onwards, per ACA

• Payment adjustment will apply

for all inpatient discharges, not

just the associated patient

populations

• Unlike VBP, no opportunity for

high performers to earn bonus

payments

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

Overview of Readmissions Program

1) Starter set, from FY 2013 onward 2) Previously finalized for use in FY 2015

-1%

-2%

-3%

2013 2014 2015

Period assessed:

July 1, 2010 – June 30, 2013

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

CMS Adds CABG to Readmit Program for FY 2017

11

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

1) No proposal to expand measures in FY 2016. 2) Risk standardized readmissions ratio.

Reason for inclusion

One of 7 high cost readmissions identified in MedPAC

2007 report to congress, with highest potentially

preventable readmission rate according to CMS

Year adopted for

Inpatient Quality

Reporting (IQR)

Finalized in FY 2015 Proposed Inpatient Rule for

simultaneous IQR and Readmissions inclusion for FY

2017

Median RSRR2 16.8% (25th and 75th percentiles are 15.6% and 17.9%,

respectively)

Measure Methodology Click here for the measure methodology

But No New Readmissions Measures Introduced in FY 2016

Finalized CABG Measure in FY 20171

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Value-Based Purchasing Program in Brief

12

Participation in VBP Not Optional, However Some Exclusions Apply

Value Based Purchasing Program Inclusion Criteria

• Most hospitals that treat

Medicare patients

• Hospitals satisfying CMS

inpatient reporting

requirements (receiving full

market basket update as a

result)

Hospital Types Quality Compliance

• Organizations that meet the

minimum case reporting

requirements and minimum

required number of domain

scores to receive a total score

Reporting Requirements

Inclu

ded

E

xclu

ded

• Psychiatric, rehab, long term

care, children’s, cancer

hospitals

• Hospitals in PR, US territories

• MD hospitals now exempted

from VBP effective Jan 1,

2014 under CMS agreement

under “Maryland all payer

model” – under section 3021

of ACA

• Any hospital that fails to

meet minimum case and

measure requirements

required to receive a total

score

• Received CMS deficiency

notifications during the

performance period

• Hospitals failing chart

validation of quality data

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

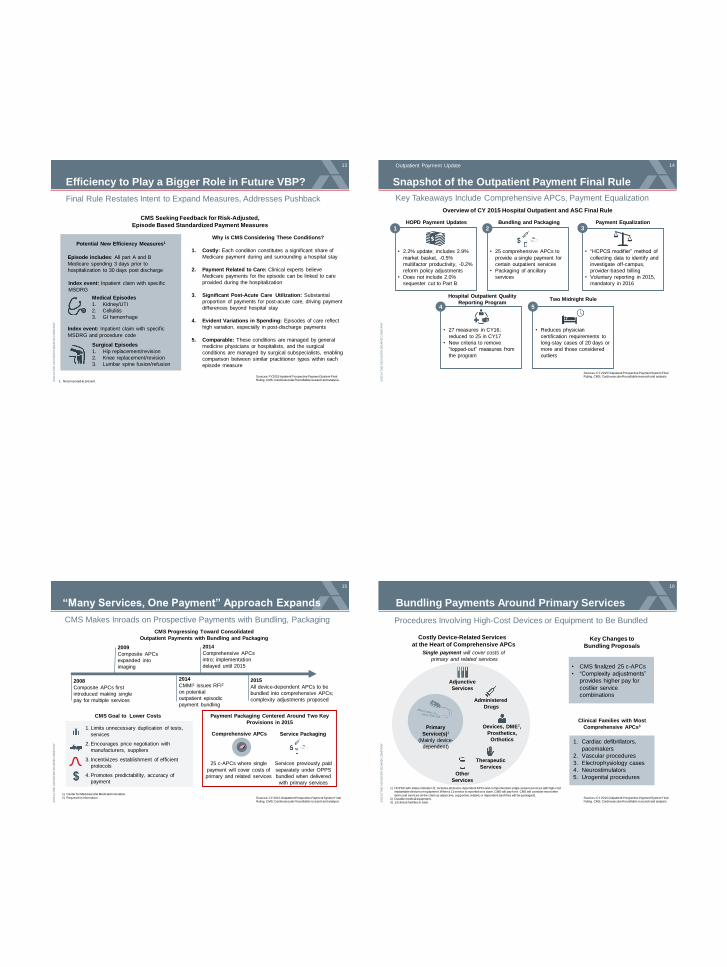

Efficiency to Play a Bigger Role in Future VBP?

13

1. Not proposed at present.

CMS Seeking Feedback for Risk-Adjusted,

Episode Based Standardized Payment Measures

Medical Episodes

1. Kidney/UTI

2. Cellulitis

3. GI hemorrhage

Surgical Episodes

1. Hip replacement/revision

2. Knee replacement/revision

3. Lumbar spine fusion/refusion

Potential New Efficiency Measures1

Index event: Inpatient claim with specific

MSDRG and procedure code

Why is CMS Considering These Conditions?

1. Costly: Each condition constitutes a significant share of

Medicare payment during and surrounding a hospital stay

2. Payment Related to Care: Clinical experts believe

Medicare payments for the episode can be linked to care

provided during the hospitalization

3. Significant Post-Acute Care Utilization: Substantial

proportion of payments for post-acute care, driving payment

differences beyond hospital stay

4. Evident Variations in Spending: Episodes of care reflect

high variation, especially in post-discharge payments

5. Comparable: These conditions are managed by general

medicine physicians or hospitalists, and the surgical

conditions are managed by surgical subspecialists, enabling

comparison between similar practitioner types within each

episode measure

Final Rule Restates Intent to Expand Measures, Addresses Pushback

Index event: Inpatient claim with specific

MSDRG

Episode includes: All part A and B

Medicare spending 3 days prior to

hospitalization to 30 days post discharge

Sources: FY2015 Inpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis. ©

20

14 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

14

Overview of CY 2015 Hospital Outpatient and ASC Final Rule

Snapshot of the Outpatient Payment Final Rule

z

• 2.2% update; includes 2.9%

market basket, -0.5%

multifactor productivity, -0.2%

reform policy adjustments

• Does not include 2.0%

sequester cut to Part B

1 z

2 z

3

z 4

z 5

HOPD Payment Updates Payment Equalization

Hospital Outpatient Quality

Reporting Program Two Midnight Rule

• “HCPCS modifier” method of

collecting data to identify and

investigate off-campus,

provider-based billing

• Voluntary reporting in 2015,

mandatory in 2016

• 27 measures in CY16;

reduced to 25 in CY17

• New criteria to remove

“topped-out” measures from

the program

• Reduces physician

certification requirements to

long-stay cases of 20 days or

more and those considered

outliers

Bundling and Packaging

• 25 comprehensive APCs to

provide a single payment for

certain outpatient services

• Packaging of ancillary

services

Key Takeaways Include Comprehensive APCs, Payment Equalization

Outpatient Payment Update

Sources: CY 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

“Many Services, One Payment” Approach Expands

CMS Makes Inroads on Prospective Payments with Bundling, Packaging

Sources: CY 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

1) Center for Medicare and Medicaid Innovation.

2) Request for information.

2008

Composite APCs first

introduced making single

pay for multiple services

2009

Composite APCs

expanded into

imaging

2014

Comprehensive APCs

intro; implementation

delayed until 2015

2015

All device-dependent APCs to be

bundled into comprehensive APCs;

complexity adjustments proposed

CMS Progressing Toward Consolidated

Outpatient Payments with Bundling and Packaging

Payment Packaging Centered Around Two Key

Provisions in 2015

CMS Goal to Lower Costs

25 c-APCs where single

payment will cover costs of

primary and related services

Comprehensive APCs

Services previously paid

separately under OPPS

bundled when delivered

with primary services

Service Packaging 1. Limits unnecessary duplication of tests,

services

2. Encourages price negotiation with

manufacturers, suppliers

3. Incentivizes establishment of efficient

protocols

4. Promotes predictability, accuracy of

payment

15

2014

CMMI1 issues RFI2

on potential

outpatient episodic

payment bundling

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Bundling Payments Around Primary Services

Procedures Involving High-Cost Devices or Equipment to Be Bundled

Sources: CY 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

1) HCPSC with status indicator J1; includes all device-dependent APCs and comprehensive single-session services with high-cost implantable devices or equipment. When a J1 service is reported on a claim, CMS will pay for it. CMS will consider most other

items and services on the claim as adjunctive, supportive, related, or dependent (and they will be packaged). 2) Durable medical equipment. 3) 13 clinical families in total.

• CMS finalized 25 c-APCs

• “Complexity adjustments”

provides higher pay for

costlier service

combinations

Adjunctive

Services

Therapeutic

Services

Other

Services

Administered

Drugs

Primary

Service(s)1

(Mainly device-

dependent)

Costly Device-Related Services

at the Heart of Comprehensive APCs

Single payment will cover costs of

primary and related services

16

1. Cardiac defibrillators,

pacemakers

2. Vascular procedures

3. Electrophysiology cases

4. Neurostimulators

5. Urogenital procedures

Clinical Families with Most

Comprehensive APCs3 Devices, DME2,

Prosthetics,

Orthotics

Key Changes to

Bundling Proposals

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

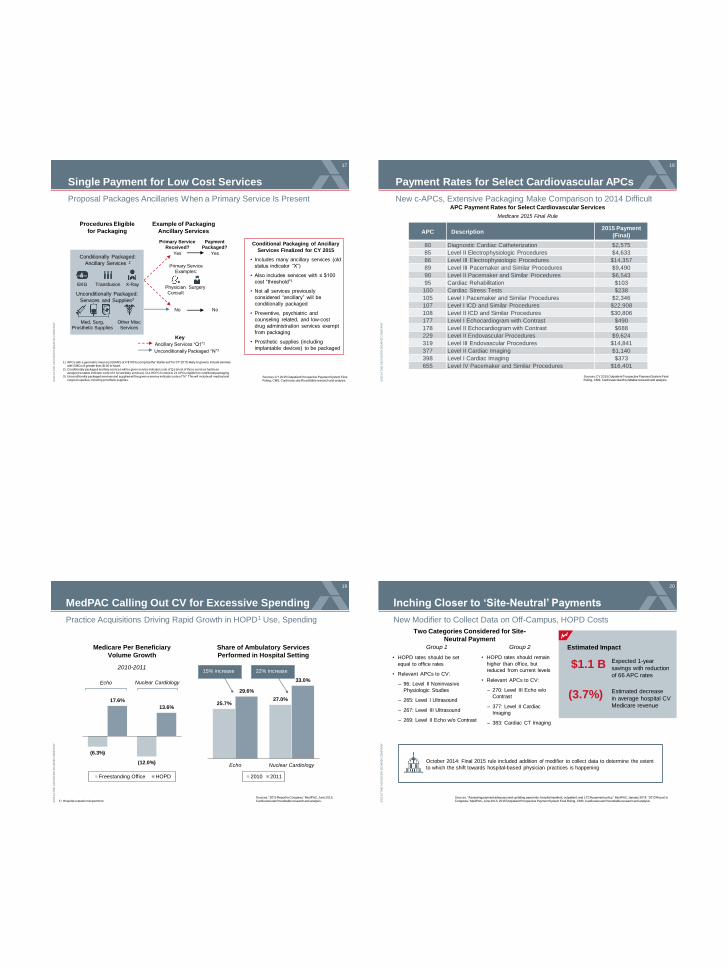

Single Payment for Low Cost Services

Proposal Packages Ancillaries When a Primary Service Is Present

Conditional Packaging of Ancillary

Services Finalized for CY 2015

• Includes many ancillary services (old

status indicator “X”)

• Also includes services with ≤ $100

cost “threshold”1

• Not all services previously

considered “ancillary” will be

conditionally packaged

• Preventive, psychiatric and

counseling related, and low-cost

drug administration services exempt

from packaging

• Prosthetic supplies (including

implantable devices) to be packaged

Example of Packaging

Ancillary Services

Procedures Eligible

for Packaging

Payment Packaged?

Primary Service Examples:

Conditionally Packaged:

Ancillary Services 2

1) APCs with a geometric mean cost (GMC) of ≤ $100 to comprise the “starter set” for CY 2015; likely to grow to include services with GMCs of greater than $100 in future.

2) Conditionally packaged ancillary services will be given service indicator code of Q1 (most of these services had been assigned a status indicator code of X for ancillary services). 511 HCPCS codes in 21 APCs eligible for conditional packaging.

3) Unconditionally packaged services and supplies will be given a service indicator code of “N.” This will include all medical and surgical supplies, including prosthetic supplies.

Sources: CY 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

17

EKG Transfusion X-Ray

Unconditionally Packaged:

Services and Supplies3

Primary Service Received?

Yes

No

Physician Consult

Surgery

Yes

No

Med, Surg, Prosthetic Supplies

Other Misc Services

Ancillary Services “Q1”2

Unconditionally Packaged “N”3

Key

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Payment Rates for Select Cardiovascular APCs

18

New c-APCs, Extensive Packaging Make Comparison to 2014 Difficult

Sources: CY 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

APC Payment Rates for Select Cardiovascular Services

Medicare 2015 Final Rule

APC Description 2015 Payment

(Final)

80 Diagnostic Cardiac Catheterization $2,575

85 Level II Electrophysiologic Procedures $4,633

86 Level III Electrophysiologic Procedures $14,357

89 Level III Pacemaker and Similar Procedures $9,490

90 Level II Pacemaker and Similar Procedures $6,543

95 Cardiac Rehabilitation $103

100 Cardiac Stress Tests $238

105 Level I Pacemaker and Similar Procedures $2,346

107 Level I ICD and Similar Procedures $22,908

108 Level II ICD and Similar Procedures $30,806

177 Level I Echocardiogram with Contrast $490

178 Level II Echocardiogram with Contrast $688

229 Level II Endovascular Procedures $9,624

319 Level III Endovascular Procedures $14,841

377 Level II Cardiac Imaging $1,140

398 Level I Cardiac Imaging $373

655 Level IV Pacemaker and Similar Procedures $16,401

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

MedPAC Calling Out CV for Excessive Spending

19

Practice Acquisitions Driving Rapid Growth in HOPD1 Use, Spending

Sources: “2013 Report to Congress,” MedPAC, June 2013; Cardiovascular Roundtable research and analysis. 1) Hospital outpatient department.

Medicare Per Beneficiary

Volume Growth

(6.3%)

(12.0%)

17.6%

13.6%

Freestanding Office HOPD

Echo Nuclear Cardiology

2010-2011

Share of Ambulatory Services

Performed in Hospital Setting

15% increase

25.7% 27.0%

29.6%

33.0%

Echo Nuclear Cardiology

2010 2011

22% increase

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Inching Closer to ‘Site-Neutral’ Payments

20

New Modifier to Collect Data on Off-Campus, HOPD Costs

Sources: “Assessing payment adequacy and updating payments: hospital inpatient, outpatient, and LTCH payment policy,” MedPAC, January 2014; “2013 Report to Congress,” MedPAC, June 2013; 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis

Two Categories Considered for Site-

Neutral Payment

Group 1 Group 2

• HOPD rates should be set

equal to office rates

• Relevant APCs to CV:

– 96: Level II Noninvasive

Physiologic Studies

– 265: Level I Ultrasound

– 267: Level III Ultrasound

– 269: Level II Echo w/o Contrast

Estimated Impact

$1.1 B Expected 1-year

savings with reduction

of 66 APC rates

(3.7%) Estimated decrease

in average hospital CV

Medicare revenue

• HOPD rates should remain

higher than office, but

reduced from current levels

• Relevant APCs to CV:

– 270: Level III Echo w/o

Contrast

– 377: Level II Cardiac

Imaging

– 383: Cardiac CT Imaging

October 2014: Final 2015 rule included addition of modifier to collect data to determine the extent

to which the shift towards hospital-based physician practices is happening

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

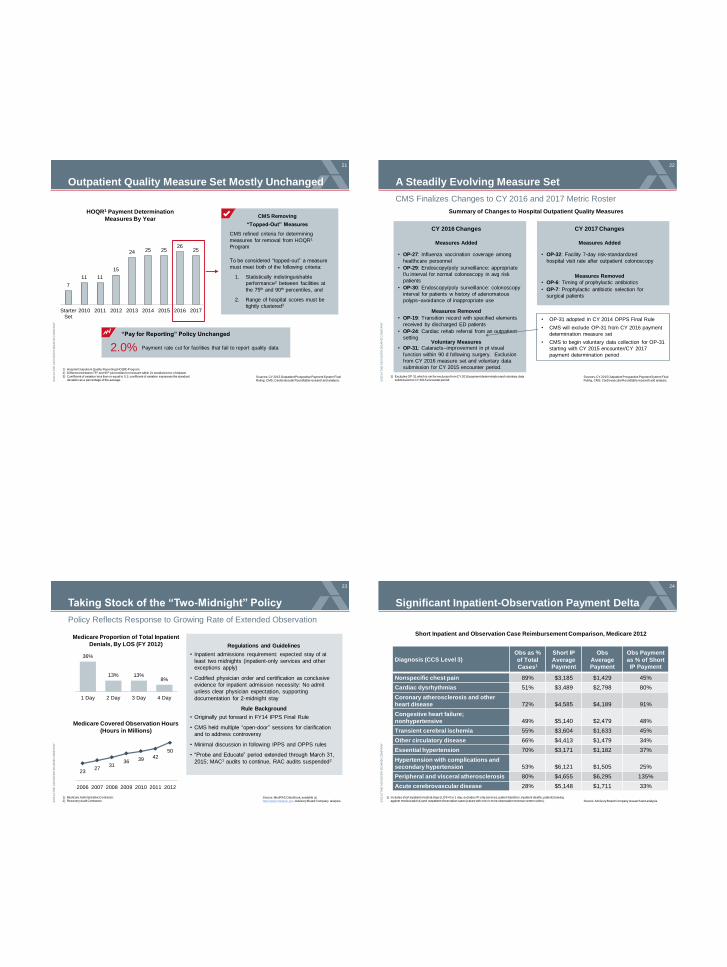

Outpatient Quality Measure Set Mostly Unchanged

21

Sources: CY 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

7

11 11

15

24 25 25 26

25

StarterSet

2010 2011 2012 2013 2014 2015 2016 2017

HOQR1 Payment Determination

Measures By Year

1) Hospital Outpatient Quality Reporting (HOQR) Program. 2) Difference between 75th and 90th percentiles for measure within 2x standard error of dataset.

3) Coefficient of variation less than or equal to 0.1; coefficient of variation expresses the standard deviation as a percentage of the average.

CMS Removing

“Topped-Out” Measures

CMS refined criteria for determining

measures for removal from HOQR1

Program

To be considered “topped-out” a measure

must meet both of the following criteria:

1. Statistically indistinguishable

performance2 between facilities at

the 75th and 90th percentiles, and

2. Range of hospital scores must be

tightly clustered3

Payment rate cut for facilities that fail to report quality data 2.0%

“Pay for Reporting” Policy Unchanged

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

A Steadily Evolving Measure Set

22

CMS Finalizes Changes to CY 2016 and 2017 Metric Roster

Sources: CY 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

Measures Added

• OP-27: Influenza vaccination coverage among

healthcare personnel

• OP-29: Endoscopy/poly surveillance: appropriate

f/u interval for normal colonoscopy in avg risk

patients

• OP-30: Endoscopy/poly surveillance: colonoscopy

interval for patients w history of adenomatous

polyps–avoidance of inappropriate use

Measures Removed

• OP-19: Transition record with specified elements

received by discharged ED patients

• OP-24: Cardiac rehab referral from an outpatient

setting Voluntary Measures

• OP-31: Cataracts–improvement in pt visual

function within 90 d following surgery. Exclusion

from CY 2016 measure set and voluntary data

submission for CY 2015 encounter period.

Measures Added

• OP-32: Facility 7-day risk-standardized

hospital visit rate after outpatient colonoscopy

Measures Removed

• OP-6: Timing of prophylactic antibiotics

• OP-7: Prophylactic antibiotic selection for

surgical patients

CY 2016 Changes CY 2017 Changes

• OP-31 adopted in CY 2014 OPPS Final Rule

• CMS will exclude OP-31 from CY 2016 payment

determination measure set

• CMS to begin voluntary data collection for OP-31

starting with CY 2015 encounter/CY 2017

payment determination period

1) Excludes OP-31 which is set for exclusion from CY 2016 payment determination and voluntary data submission for CY 2015 encounter period.

Summary of Changes to Hospital Outpatient Quality Measures

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Source: MedPAC Data Book, available at: http://www.medpac.gov; Advisory Board Company analysis.

36%

13% 13% 8%

1 Day 2 Day 3 Day 4 Day

Medicare Proportion of Total Inpatient

Denials, By LOS (FY 2012)

23 27

31 36 39 42

50

2006 2007 2008 2009 2010 2011 2012

Medicare Covered Observation Hours

(Hours in Millions)

Regulations and Guidelines

• Inpatient admissions requirement: expected stay of at

least two midnights (inpatient-only services and other

exceptions apply)

• Codified physician order and certification as conclusive

evidence for inpatient admission necessity: No admit

unless clear physician expectation, supporting

documentation for 2-midnight stay

Rule Background

• Originally put forward in FY14 IPPS Final Rule

• CMS held multiple “open-door” sessions for clarification

and to address controversy

• Minimal discussion in following IPPS and OPPS rules

• “Probe and Educate” period extended through March 31,

2015; MAC1 audits to continue, RAC audits suspended2

Taking Stock of the “Two-Midnight” Policy

Policy Reflects Response to Growing Rate of Extended Observation

23

1) Medicare Administrative Contractor. 2) Recovery Audit Contractor. ©

20

14 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Significant Inpatient-Observation Payment Delta

24

Source: Advisory Board Company research and analysis.

1) Includes short inpatient medical stays (LOS=0 or 1 day; excludes IP-only services, patient transfers, inpatient deaths, patients leaving against medical advice) and outpatient observation cases (cases with one or more observation revenue center codes).

Short Inpatient and Observation Case Reimbursement Comparison, Medicare 2012

Diagnosis (CCS Level 3) Obs as %

of Total

Cases1

Short IP

Average Payment

Obs

Average Payment

Obs Payment

as % of Short IP Payment

Nonspecific chest pain 89% $3,185 $1,429 45%

Cardiac dysrhythmias 51% $3,489 $2,798 80%

Coronary atherosclerosis and other

heart disease 72% $4,585 $4,189 91%

Congestive heart failure;

nonhypertensive 49% $5,140 $2,479 48%

Transient cerebral ischemia 55% $3,604 $1,633 45%

Other circulatory disease 66% $4,413 $1,479 34%

Essential hypertension 70% $3,171 $1,182 37%

Hypertension with complications and

secondary hypertension 53% $6,121 $1,505 25%

Peripheral and visceral atherosclerosis 80% $4,655 $6,295 135%

Acute cerebrovascular disease 28% $5,148 $1,711 33%

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

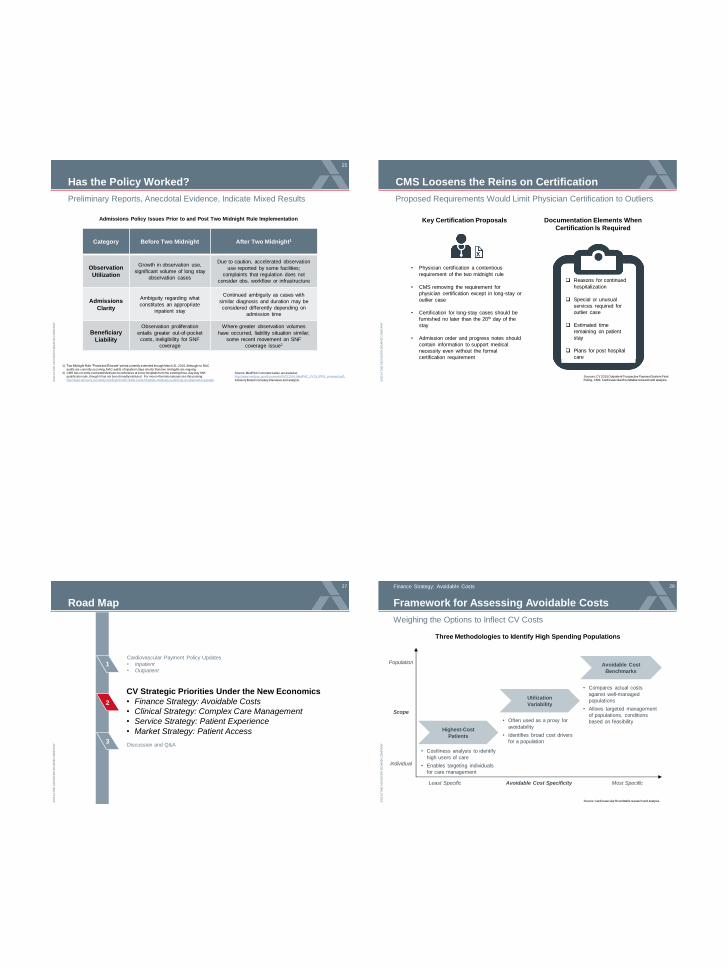

Has the Policy Worked?

Preliminary Reports, Anecdotal Evidence, Indicate Mixed Results

Source: MedPAC Comment Letter, accessed at: http://www.medpac.gov/documents/06132014_MedPAC_FY15_IPPS_comment.pdf;

Advisory Board Company interviews and analysis.

Category Before Two Midnight After Two Midnight1

Observation

Utilization

Growth in observation use,

significant volume of long stay

observation cases

Due to caution, accelerated observation

use reported by some facilities;

complaints that regulation does not

consider obs. workflow or infrastructure

Admissions

Clarity

Ambiguity regarding what

constitutes an appropriate

inpatient stay

Continued ambiguity as cases with

similar diagnosis and duration may be

considered differently depending on

admission time

Beneficiary

Liability

Observation proliferation

entails greater out-of-pocket

costs, ineligibility for SNF

coverage

Where greater observation volumes

have occurred, liability situation similar;

some recent movement on SNF

coverage issue2

Admissions Policy Issues Prior to and Post Two Midnight Rule Implementation

25

1) Two Midnight Rule “Probe and Educate” period currently extended through March 31, 2015. Although no RAC

audits are currently occurring, MAC audits of inpatient stays shorter than two midnights are ongoing. 2) CMS has recently exempted Medicare beneficiaries at some hospitals from the existing three-day stay SNF

qualification rule, though it has not been broadly instituted. For more information please see this posting: http://www.advisory.com/daily-briefing/2014/07/28/at-some-hospitals-medicare-is-ditching-an-observation-penalty. ©

20

14 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

CMS Loosens the Reins on Certification

Proposed Requirements Would Limit Physician Certification to Outliers

Sources: CY 2015 Outpatient Prospective Payment System Final Ruling, CMS; Cardiovascular Roundtable research and analysis.

Key Certification Proposals

• Physician certification a contentious

requirement of the two midnight rule

• CMS removing the requirement for

physician certification except in long-stay or

outlier case

• Certification for long-stay cases should be

furnished no later than the 20th day of the

stay

• Admission order and progress notes should

contain information to support medical

necessity even without the formal

certification requirement

Documentation Elements When

Certification Is Required

Reasons for continued

hospitalization

Special or unusual

services required for

outlier case

Estimated time

remaining on patient

stay

Plans for post hospital

care

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Road Map

2

3

1

27

CV Strategic Priorities Under the New Economics

• Finance Strategy: Avoidable Costs

• Clinical Strategy: Complex Care Management

• Service Strategy: Patient Experience

• Market Strategy: Patient Access

Discussion and Q&A

Cardiovascular Payment Policy Updates

• Inpatient

• Outpatient

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Framework for Assessing Avoidable Costs

28

Weighing the Options to Inflect CV Costs

Source: Cardiovascular Roundtable research and analysis.

Finance Strategy: Avoidable Costs

Three Methodologies to Identify High Spending Populations

Highest-Cost

Patients

Utilization

Variability

Avoidable Cost

Benchmarks

Population

• Costliness analysis to identify

high users of care

• Enables targeting individuals

for care management

• Often used as a proxy for

avoidability

• Identifies broad cost drivers

for a population

• Compares actual costs

against well-managed

populations

• Allows targeted management

of populations, conditions

based on feasibility

Individual

Most Specific Least Specific Avoidable Cost Specificity

Scope

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

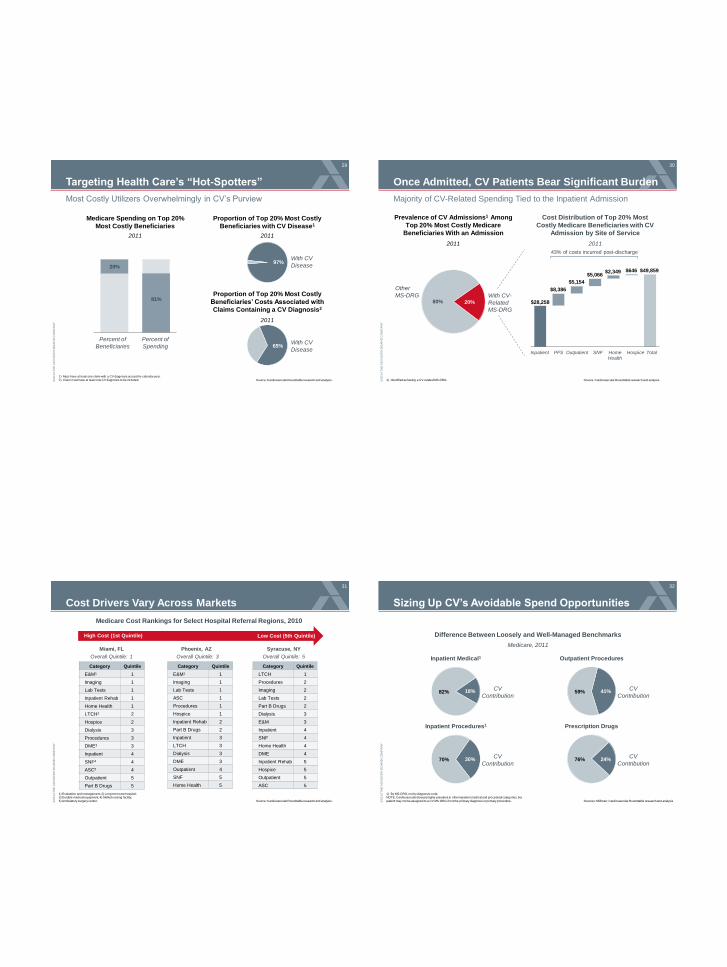

Targeting Health Care’s “Hot-Spotters”

29

Most Costly Utilizers Overwhelmingly in CV’s Purview

Source: Cardiovascular Roundtable research and analysis.

1) Must have at least one claim with a CV diagnosis across the calendar year. 2) Claim must have at least one CV diagnosis to be included.

20%

81%

Medicare Spending on Top 20%

Most Costly Beneficiaries

2011

Percent of

Beneficiaries

Percent of

Spending

Proportion of Top 20% Most Costly

Beneficiaries with CV Disease1

97% With CV

Disease

Proportion of Top 20% Most Costly

Beneficiaries’ Costs Associated with

Claims Containing a CV Diagnosis2

65%

2011

2011

With CV

Disease

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Once Admitted, CV Patients Bear Significant Burden

30

Majority of CV-Related Spending Tied to the Inpatient Admission

Source: Cardiovascular Roundtable research and analysis. 1) Identified as having a CV-related MS-DRG.

Prevalence of CV Admissions1 Among

Top 20% Most Costly Medicare

Beneficiaries With an Admission

2011

20% 80% With CV-

Related

MS-DRG

Other

MS-DRG

Cost Distribution of Top 20% Most

Costly Medicare Beneficiaries with CV

Admission by Site of Service

2011

Inpatient PFS Outpatient Home Health

Hospice Total SNF

43% of costs incurred post-discharge

$28,258

$8,386

$5,154

$5,066 $2,349 $646 $49,859

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Cost Drivers Vary Across Markets

31

Source: Cardiovascular Roundtable research and analysis.

1) Evaluation and management; 2) Long-term care hospital; 3) Durable medical equipment; 4) Skilled nursing facility;

5) Ambulatory surgery center.

Category Quintile

E&M1 1

Imaging 1

Lab Tests 1

Inpatient Rehab 1

Home Health 1

LTCH2 2

Hospice 2

Dialysis 3

Procedures 3

DME3 3

Inpatient 4

SNF4 4

ASC5 4

Outpatient 5

Part B Drugs 5

Category Quintile

E&M1 1

Imaging 1

Lab Tests 1

ASC 1

Procedures 1

Hospice 1

Inpatient Rehab 2

Part B Drugs 2

Inpatient 3

LTCH 3

Dialysis 3

DME 3

Outpatient 4

SNF 5

Home Health 5

Category Quintile

LTCH 1

Procedures 2

Imaging 2

Lab Tests 2

Part B Drugs 2

Dialysis 3

E&M 3

Inpatient 4

SNF 4

Home Health 4

DME 4

Inpatient Rehab 5

Hospice 5

Outpatient 5

ASC 5

Miami, FL Phoenix, AZ Syracuse, NY

Medicare Cost Rankings for Select Hospital Referral Regions, 2010

High Cost (1st Quintile) Low Cost (5th Quintile)

Overall Quintile: 1 Overall Quintile: 3 Overall Quintile: 5

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Sizing Up CV’s Avoidable Spend Opportunities

32

Sources: Milliman; Cardiovascular Roundtable research and analysis

1) By MS-DRG, not by diagnosis code. NOTE: Cardiovascular disease highly prevalent in other inpatient medical and procedural categories, but

patient may not be assigned to a CV MS-DRG if not the primary diagnosis or primary procedure.

18% 82%

Difference Between Loosely and Well-Managed Benchmarks

Medicare, 2011

Inpatient Medical1

CV

Contribution

30% 70%

Inpatient Procedures1

CV

Contribution

41% 59%

Outpatient Procedures

CV

Contribution

24% 76%

Prescription Drugs

CV

Contribution

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

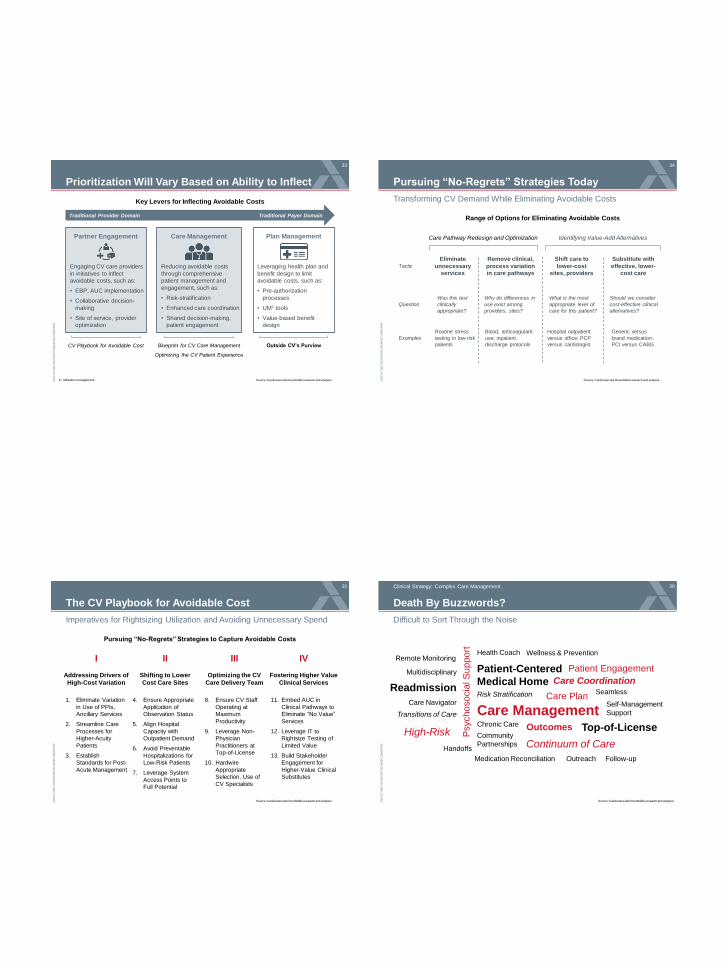

Prioritization Will Vary Based on Ability to Inflect

33

Source: Cardiovascular Roundtable research and analysis. 1) Utilization management.

Care Management

Reducing avoidable costs

through comprehensive

patient management and

engagement, such as:

• Risk-stratification

• Enhanced care coordination

• Shared decision-making,

patient engagement

Plan Management

Leveraging health plan and

benefit design to limit

avoidable costs, such as:

• Pre-authorization

processes

• UM1 tools

• Value-based benefit

design

Partner Engagement

Engaging CV care providers

in initiatives to inflect

avoidable costs, such as:

• EBP, AUC implementation

• Collaborative decision-

making

• Site of service, provider

optimization

Traditional Provider Domain Traditional Payer Domain

CV Playbook for Avoidable Cost Blueprint for CV Care Management

Optimizing the CV Patient Experience

Outside CV’s Purview

Key Levers for Inflecting Avoidable Costs

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Pursuing “No-Regrets” Strategies Today

34

Transforming CV Demand While Eliminating Avoidable Costs

Source: Cardiovascular Roundtable research and analysis.

Range of Options for Eliminating Avoidable Costs

Care Pathway Redesign and Optimization Identifying Value-Add Alternatives

Shift care to

lower-cost

sites, providers

What is the most

appropriate level of

care for this patient?

Hospital outpatient

versus office; PCP

versus cardiologist

Substitute with

effective, lower-

cost care

Should we consider

cost-effective clinical

alternatives?

Generic versus

brand medication;

PCI versus CABG

Eliminate

unnecessary

services

Was this test

clinically

appropriate?

Routine stress

testing in low-risk

patients

Remove clinical,

process variation

in care pathways

Blood, anticoagulant

use; inpatient

discharge protocols

Why do differences in

use exist among

providers, sites?

Tactic

Question

Examples

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

The CV Playbook for Avoidable Cost

35

Imperatives for Rightsizing Utilization and Avoiding Unnecessary Spend

Source: Cardiovascular Roundtable research and analysis.

Pursuing “No-Regrets” Strategies to Capture Avoidable Costs

1. Eliminate Variation

in Use of PPIs,

Ancillary Services

2. Streamline Care

Processes for

Higher-Acuity

Patients

3. Establish

Standards for Post-

Acute Management

Addressing Drivers of

High-Cost Variation

I

4. Ensure Appropriate

Application of

Observation Status

5. Align Hospital

Capacity with

Outpatient Demand

6. Avoid Preventable

Hospitalizations for

Low-Risk Patients

7. Leverage System

Access Points to

Full Potential

Shifting to Lower

Cost Care Sites

II

8. Ensure CV Staff

Operating at

Maximum

Productivity

9. Leverage Non-

Physician

Practitioners at

Top-of-License

10. Hardwire

Appropriate

Selection, Use of

CV Specialists

Optimizing the CV

Care Delivery Team

III

11. Embed AUC in

Clinical Pathways to

Eliminate “No Value”

Services

12. Leverage IT to

Rightsize Testing of

Limited Value

13. Build Stakeholder

Engagement for

Higher-Value Clinical

Substitutes

Fostering Higher Value

Clinical Services

IV

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Death By Buzzwords?

36

Difficult to Sort Through the Noise

Clinical Strategy: Complex Care Management

Readmission

High-Risk

Care Management

Patient-Centered

Medical Home Risk Stratification

Chronic Care

Care Plan Self-Management

Support

Psych

oso

cia

l S

up

po

rt

Community

Partnerships Continuum of Care

Care Navigator

Transitions of Care

Outcomes

Medication Reconciliation

Multidisciplinary

Remote Monitoring

Patient Engagement

Wellness & Prevention Health Coach

Seamless

Handoffs

Top-of-License

Care Coordination

Outreach Follow-up

Source: Cardiovascular Roundtable research and analysis.

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Complex Care Management Taking Center Stage

37

Receiving Increasing Attention from Payers, Regulators, and Providers

Source: McCall N, et al., “Evaluation of CMHCB Demonstration,” available at: www.cms.gov, accessed September 17, 2013; Anthem Blue Cross Blue Shield, available at: www.anthem.com, accessed September 17,

2013; 2014 Physician Fee Schedule Proposed Ruling, CMS; Cardiovascular Roundtable research and analysis.

1) Physician Fee Schedule. 2) Care Management for High-Cost Beneficiaries.

• 2014 PFS1 proposed rule

includes payment for

chronic care management

services for Medicare

beneficiaries with two or

more chronic conditions

• Payment for services

rendered over 90-day

period, would not require

in-person patient visit

CMS Payment

Policies

• Insurers building care

management programs

targeting highest-cost

beneficiaries

• Example: Anthem Blue

Cross’s ConditionCare,

ComplexCare programs

for chronic, complex

conditions including

HF, CAD

Private Payer

Involvement

• Several CMS, state-based

pilots, primarily focusing

on HF, CAD, diabetes

• Example: Medicare

CMHCB2 Demonstration

tests provider-based

intensive care

management to increase

quality, reduce cost

Nationwide

Demonstrations

Recent Initiatives Elevating the

Focus on Care Management

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Providers on the Hook for Long-Term Quality, Costs

38

Changing Payer Incentives Increasing Cross-Continuum Accountability

Source: Cardiovascular Roundtable research and analysis.

1) Acute Care Episode. 2) Shading indicates time period of accountability is

dependent on model selected within the initiative.

Pre-Acute Inpatient Acute Post-Acute

ACE1 Demonstration

Select Initiatives Expanding Responsibility Across the Continuum

Bundled Payments for Care Improvement Initiative2

Readmission Reduction Program

National Pilot Program on Payment Bundling

Value-Based Purchasing

Accountable Care Organizations/Shared Savings Programs

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Despite Best Efforts, Most

Hospitals Facing Penalties

Readmissions Still an Up-at-Night Issue

39

Comprehensive Approach to Readmission Reduction Often Elusive

Sources: Rau J, “Armed With Bigger Fines, Medicare to Punish 2,225 Hospitals For Excess Readmissions,” Kaiser Health News, accessed August 5, 2013; Bradley EH, et al., Journal of the American College of

Cardiology, 2012, 60: 607-614; Cardiovascular Roundtable Research and Analysis.

The First Area of Focus for CV

64% Percent of U.S. hospitals

facing payment penalty in

year two of HRRP

$227M Total readmissions fines

levied for 2013

3% 97%

Majority Not Implementing a Complete

Suite of Readmission Reduction Tactics

Percent of Hospitals Implementing

Top 10 Suggested Tactics

Implemented

All 10

Implemented

<10

Armed with Bigger Fines,

Medicare to Punish 2,225

Hospitals for Excess

Readmissions

Kaiser Health News,

August 2013

Hospitals put

in place only

4.8 practices

on average

n=537

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Toolkit Placing Readmission Reduction Tactics at Your Fingertips

Providing Intensive Transitional Care Support

Practice Description

Planning and

Operating a HF

Clinic

Roundtable Continuing to Support Your Efforts

40

Source: Cardiovascular Roundtable research and analysis.

Readmission Reduction Toolkit (Available Early 2014)

• Outlines best practice strategies, tools, and implementation guidance from

Cardiovascular Roundtable and Advisory Board research on reducing readmission

• Arranged by key sub-topics to support programs at each stage in the care pathway

• Provides tactical support for programs aiming to improve performance on 30-day

readmission rates in response to Medicare’s readmission reduction program

Coordinating with Post-Acute Care Services and Providers

Practice Description

Co-branded

Ultrafiltration

Services at PACs

Hospital partners with PAC nursing facility to provide co-

branded ultrafiltration services on site at the PAC; aim is to

reduce HF readmissions from the PAC, streamline care,

communication between the settings

Improving Patient Education and Activation During Hospitalization

Practice Description

Technology

Solutions for

Medication

Management

Transition Planning During the Inpatient Stay

Practice Description

Teach Back

Method

Reinforces patient’s comprehension of discharge instructions using

set questions to double-check patient understanding

Proactive PAC

Consults

Early Screen for Discharge Planning tool used at admission to identify

post-acute care needs, allow for earlier coordination with PAC team

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

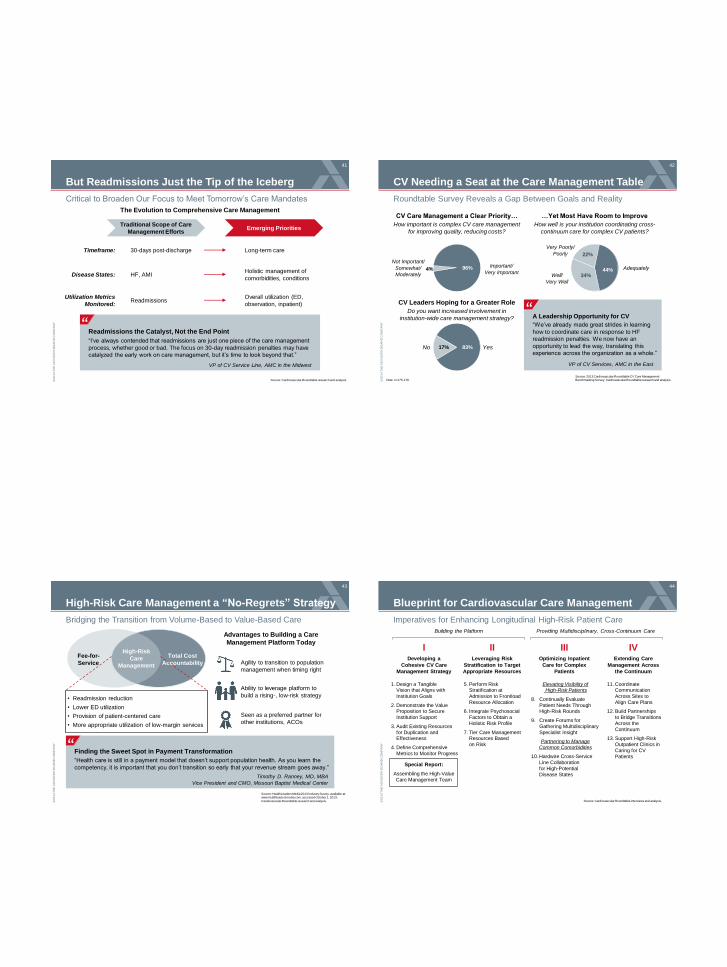

But Readmissions Just the Tip of the Iceberg

41

Critical to Broaden Our Focus to Meet Tomorrow’s Care Mandates

Source: Cardiovascular Roundtable research and analysis.

The Evolution to Comprehensive Care Management

Readmissions the Catalyst, Not the End Point

“I’ve always contended that readmissions are just one piece of the care management

process, whether good or bad. The focus on 30-day readmission penalties may have

catalyzed the early work on care management, but it’s time to look beyond that.”

VP of CV Service Line, AMC in the Midwest

”

Emerging Priorities Traditional Scope of Care

Management Efforts

Timeframe:

Disease States:

Utilization Metrics

Monitored:

30-days post-discharge Long-term care

HF, AMI Holistic management of

comorbidities, conditions

Readmissions Overall utilization (ED,

observation, inpatient)

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

CV Needing a Seat at the Care Management Table

42

Roundtable Survey Reveals a Gap Between Goals and Reality

Source: 2013 Cardiovascular Roundtable CV Care Management Benchmarking Survey; Cardiovascular Roundtable research and analysis. Note: n=175-179.

CV Care Management a Clear Priority…

How important is complex CV care management

for improving quality, reducing costs?

…Yet Most Have Room to Improve

How well is your institution coordinating cross-

continuum care for complex CV patients?

CV Leaders Hoping for a Greater Role

Do you want increased involvement in

institution-wide care management strategy? A Leadership Opportunity for CV

VP of CV Services, AMC in the East

”

22%

44% 34%

83% Yes

Very Poorly/

Poorly

Important/

Very Important 96%

“We’ve already made great strides in learning

how to coordinate care in response to HF

readmission penalties. We now have an

opportunity to lead the way, translating this

experience across the organization as a whole.”

Adequately

Well/

Very Well

17%

4%

Not Important/

Somewhat/

Moderately

No

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

High-Risk Care Management a “No-Regrets” Strategy

43

Bridging the Transition from Volume-Based to Value-Based Care

Source: HealthLeaders Media 2013 Industry Survey, available at: www.healthleadersmedia.com, accessed October 1, 2013;

Cardiovascular Roundtable research and analysis.

• Readmission reduction

• Lower ED utilization

• Provision of patient-centered care

• More appropriate utilization of low-margin services

Fee-for-

Service

High-Risk

Care

Management

Total Cost

Accountability Agility to transition to population

management when timing right

Ability to leverage platform to

build a rising-, low-risk strategy

Seen as a preferred partner for

other institutions, ACOs

Finding the Sweet Spot in Payment Transformation

“Health care is still in a payment model that doesn’t support population health. As you learn the

competency, it is important that you don’t transition so early that your revenue stream goes away.”

Timothy D. Ranney, MD, MBA

Vice President and CMO, Missouri Baptist Medical Center

”

Advantages to Building a Care

Management Platform Today

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Blueprint for Cardiovascular Care Management

44

Imperatives for Enhancing Longitudinal High-Risk Patient Care

Source: Cardiovascular Roundtable interviews and analysis.

Building the Platform Providing Multidisciplinary, Cross-Continuum Care

I II III IV Developing a

Cohesive CV Care

Management Strategy

Leveraging Risk

Stratification to Target

Appropriate Resources

Special Report:

Assembling the High-Value

Care Management Team

Optimizing Inpatient

Care for Complex

Patients

Extending Care

Management Across

the Continuum

1. Design a Tangible Vision that Aligns with

Institution Goals

2. Demonstrate the Value Proposition to Secure

Institution Support

3. Audit Existing Resources

for Duplication and Effectiveness

4. Define Comprehensive

Metrics to Monitor Progress

5. Perform Risk Stratification at

Admission to Frontload

Resource Allocation

6. Integrate Psychosocial

Factors to Obtain a

Holistic Risk Profile

7. Tier Care Management Resources Based

on Risk

Elevating Visibility of High-Risk Patients

8. Continually Evaluate

Patient Needs Through High-Risk Rounds

9. Create Forums for

Gathering Multidisciplinary

Specialist Insight

Partnering to Manage

Common Comorbidities

10. Hardwire Cross-Service

Line Collaboration

for High-Potential

Disease States

11. Coordinate Communication

Across Sites to

Align Care Plans

12. Build Partnerships

to Bridge Transitions

Across the

Continuum

13. Support High-Risk

Outpatient Clinics in

Caring for CV

Patients

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

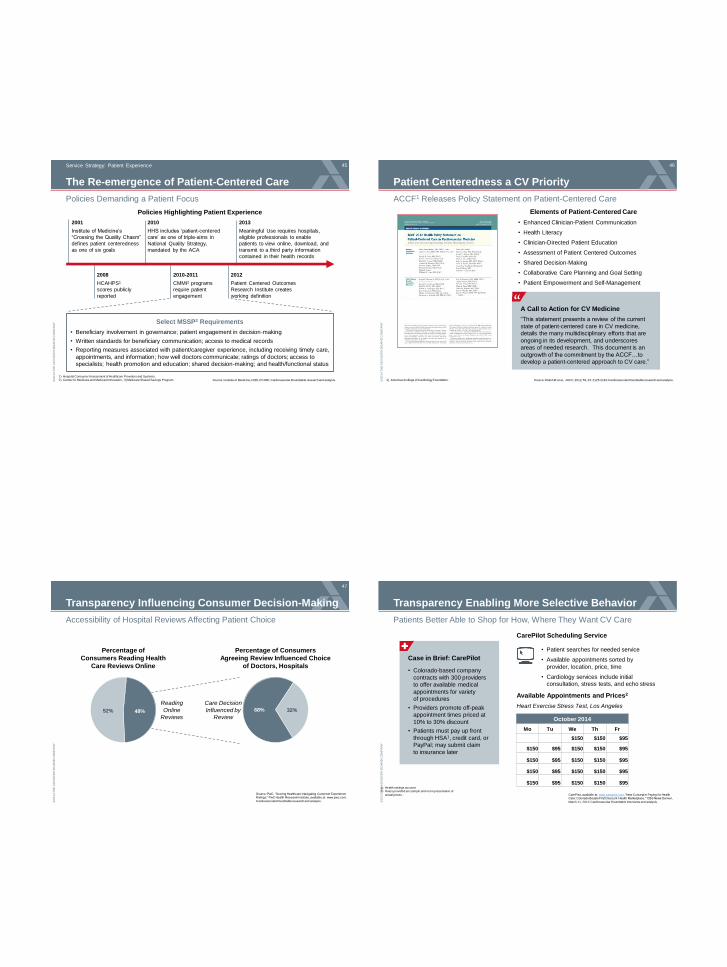

The Re-emergence of Patient-Centered Care

45

Policies Demanding a Patient Focus

Source: Institute of Medicine; CMS; PCORI; Cardiovascular Roundtable research and analysis.

Service Strategy: Patient Experience

1) Hospital Consumer Assessment of Healthcare Providers and Systems. 2) Center for Medicare and Medicaid Innovation.; 3) Medicare Shared Savings Program.

2001

Institute of Medicine’s

“Crossing the Quality Chasm”

defines patient centeredness

as one of six goals

2010

HHS includes ‘patient-centered

care’ as one of triple-aims in

National Quality Strategy,

mandated by the ACA

2013

Meaningful Use requires hospitals,

eligible professionals to enable

patients to view online, download, and

transmit to a third party information

contained in their health records

2010-2011

CMMI2 programs

require patient

engagement

Policies Highlighting Patient Experience

Select MSSP3 Requirements

• Beneficiary involvement in governance; patient engagement in decision-making

• Written standards for beneficiary communication; access to medical records

• Reporting measures associated with patient/caregiver experience, including receiving timely care,

appointments, and information; how well doctors communicate; ratings of doctors; access to

specialists; health promotion and education; shared decision-making; and health/functional status

2008

HCAHPS1

scores publicly

reported

2012

Patient Centered Outcomes

Research Institute creates

working definition

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Patient Centeredness a CV Priority

46

ACCF1 Releases Policy Statement on Patient-Centered Care

Source: Walsh M et al., JACC, 2012, 59, 23: 2125-2143; Cardiovascular Roundtable research and analysis. 1) American College of Cardiology Foundation.

A Call to Action for CV Medicine

“This statement presents a review of the current

state of patient-centered care in CV medicine,

details the many multidisciplinary efforts that are

ongoing in its development, and underscores

areas of needed research. This document is an

outgrowth of the commitment by the ACCF…to

develop a patient-centered approach to CV care.”

”

• Enhanced Clinician-Patient Communication

• Health Literacy

• Clinician-Directed Patient Education

• Assessment of Patient Centered Outcomes

• Shared Decision-Making

• Collaborative Care Planning and Goal Setting

• Patient Empowerment and Self-Management

Elements of Patient-Centered Care

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Transparency Influencing Consumer Decision-Making

47

Accessibility of Hospital Reviews Affecting Patient Choice

Source: PwC, “Scoring Healthcare: Navigating Customer Experience Ratings;” PwC Health Research Institute, available at: www.pwc.com;

Cardiovascular Roundtable research and analysis.

Percentage of Consumers

Agreeing Review Influenced Choice

of Doctors, Hospitals

48% 52% 68% 32%

Percentage of

Consumers Reading Health

Care Reviews Online

Reading

Online

Reviews

Care Decision

Influenced by

Review

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Patients Better Able to Shop for How, Where They Want CV Care

CarePilot, available at: www.carepilot.com, “New Concept in Paying for Health Care: Colorado Boasts First Discount ‘Health Marketplace,’” CBS News Denver,

March 11, 2012; Cardiovascular Roundtable interviews and analysis.

1) Health savings account. 2) Rates provided are sample and not representative of

actual prices.

Transparency Enabling More Selective Behavior

October 2014

Mo Tu We Th Fr

$150 $150 $95

$150 $95 $150 $150 $95

$150 $95 $150 $150 $95

$150 $95 $150 $150 $95

$150 $95 $150 $150 $95

Case in Brief: CarePilot

• Colorado-based company

contracts with 300 providers

to offer available medical

appointments for variety

of procedures

• Providers promote off-peak

appointment times priced at

10% to 30% discount

• Patients must pay up front

through HSA1, credit card, or

PayPal; may submit claim

to insurance later

• Patient searches for needed service

• Available appointments sorted by

provider, location, price, time

• Cardiology services include initial

consultation, stress tests, and echo stress

CarePilot Scheduling Service

Available Appointments and Prices2

Heart Exercise Stress Test, Los Angeles

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

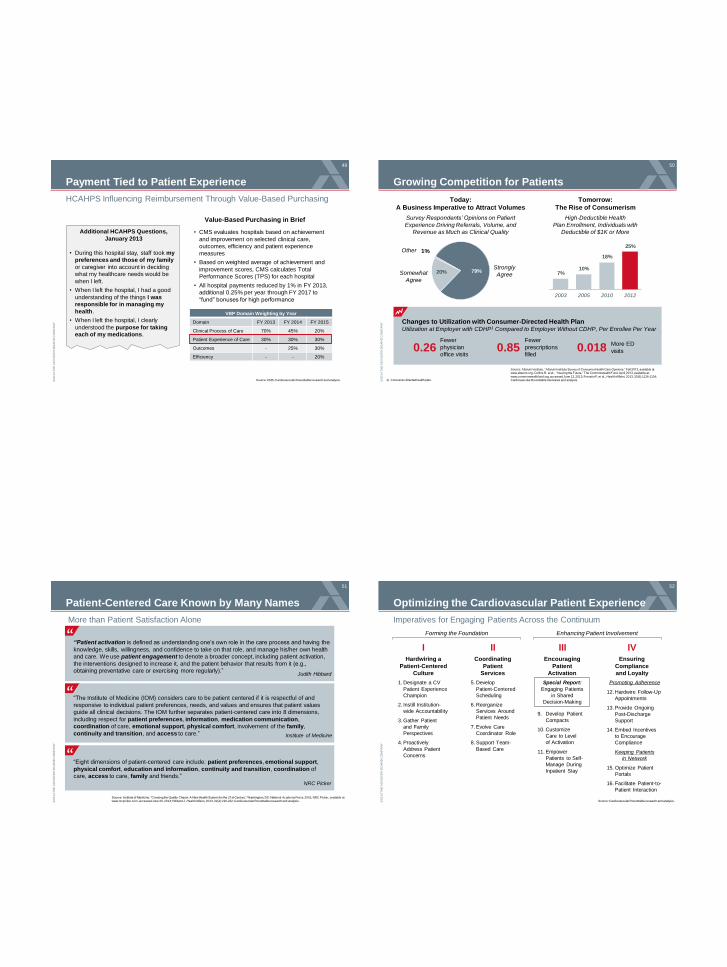

Payment Tied to Patient Experience

49

HCAHPS Influencing Reimbursement Through Value-Based Purchasing

Source: CMS; Cardiovascular Roundtable research and analysis.

Additional HCAHPS Questions,

January 2013

• During this hospital stay, staff took my

preferences and those of my family

or caregiver into account in deciding

what my healthcare needs would be

when I left.

• When I left the hospital, I had a good

understanding of the things I was

responsible for in managing my

health.

• When I left the hospital, I clearly

understood the purpose for taking

each of my medications.

VBP Domain Weighting by Year

Domain FY 2013 FY 2014 FY 2015

Clinical Process of Care 70% 45% 20%

Patient Experience of Care 30% 30% 30%

Outcomes - 25% 30%

Efficiency - - 20%

• CMS evaluates hospitals based on achievement

and improvement on selected clinical care,

outcomes, efficiency and patient experience

measures

• Based on weighted average of achievement and

improvement scores, CMS calculates Total

Performance Scores (TPS) for each hospital

• All hospital payments reduced by 1% in FY 2013,

additional 0.25% per year through FY 2017 to

“fund” bonuses for high performance

Value-Based Purchasing in Brief

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Growing Competition for Patients

50

Source: Altarum Institute, “Altarum Institute Survey of Consumer Health Care Opinions,” Fall 2012, available at: www.altarum.org; Collins R, et al., “Insuring the Future,” The Commonwealth Fund, April 2013, available at:

www.commonwealthfund.org, accessed June 12, 2013; Fronstin P, et al., Health Affairs, 2013, 32(6):1126-1134; Cardiovascular Roundtable interviews and analysis. 1) Consumer-directed health plan.

Today:

A Business Imperative to Attract Volumes

Tomorrow:

The Rise of Consumerism

Survey Respondents’ Opinions on Patient

Experience Driving Referrals, Volume, and

Revenue as Much as Clinical Quality

79% 20%

1%

Strongly

Agree Somewhat

Agree

High-Deductible Health

Plan Enrollment, Individuals with

Deductible of $1K or More

7% 10%

18%

25%

2003 2005 2010 2012

Other

Changes to Utilization with Consumer-Directed Health Plan Utilization at Employer with CDHP1 Compared to Employer Without CDHP, Per Enrollee Per Year

0.26 Fewer

physician

office visits 0.85 0.018

Fewer

prescriptions

filled

More ED

visits

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Patient-Centered Care Known by Many Names

51

More than Patient Satisfaction Alone

Source: Institute of Medicine. “Crossing the Quality Chasm: A New Health System for the 21st Century.” Washington, DC: National Academy Press, 2001; NRC Picker, available at: www.nrcpicker.com, accessed June 30, 2013; Hibbard J, Health Affairs, 2013, 32(2):216-222; Cardiovascular Roundtable research and analysis.

“Patient activation is defined as understanding one’s own role in the care process and having the

knowledge, skills, willingness, and confidence to take on that role, and manage his/her own health

and care. We use patient engagement to denote a broader concept, including patient activation,

the interventions designed to increase it, and the patient behavior that results from it (e.g.,

obtaining preventative care or exercising more regularly).” Judith Hibbard

“The Institute of Medicine (IOM) considers care to be patient centered if it is respectful of and

responsive to individual patient preferences, needs, and values and ensures that patient values

guide all clinical decisions. The IOM further separates patient-centered care into 8 dimensions,

including respect for patient preferences, information, medication communication,

coordination of care, emotional support, physical comfort, involvement of the family,

continuity and transition, and access to care.” Institute of Medicine

“Eight dimensions of patient-centered care include: patient preferences, emotional support,

physical comfort, education and information, continuity and transition, coordination of

care, access to care, family and friends.”

NRC Picker

”

”

”

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Optimizing the Cardiovascular Patient Experience

52

Imperatives for Engaging Patients Across the Continuum

Source: Cardiovascular Roundtable research and analysis.

I II III IV Hardwiring a

Patient-Centered

Culture

Coordinating

Patient

Services

Special Report:

Engaging Patients

in Shared

Decision-Making

Encouraging

Patient

Activation

Ensuring

Compliance

and Loyalty

1. Designate a CV

Patient Experience

Champion

2. Instill Institution-

wide Accountability

3. Gather Patient

and Family

Perspectives

4. Proactively

Address Patient

Concerns

5. Develop

Patient-Centered

Scheduling

6. Reorganize

Services Around

Patient Needs

7. Evolve Care

Coordinator Role

8. Support Team-

Based Care

9. Develop Patient

Compacts

10. Customize

Care to Level

of Activation

11. Empower

Patients to Self-

Manage During

Inpatient Stay

Forming the Foundation Enhancing Patient Involvement

Promoting Adherence

12. Hardwire Follow-Up

Appointments

13. Provide Ongoing

Post-Discharge

Support

14. Embed Incentives

to Encourage

Compliance

Keeping Patients

in Network

15. Optimize Patient

Portals

16. Facilitate Patient-to-

Patient Interaction

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

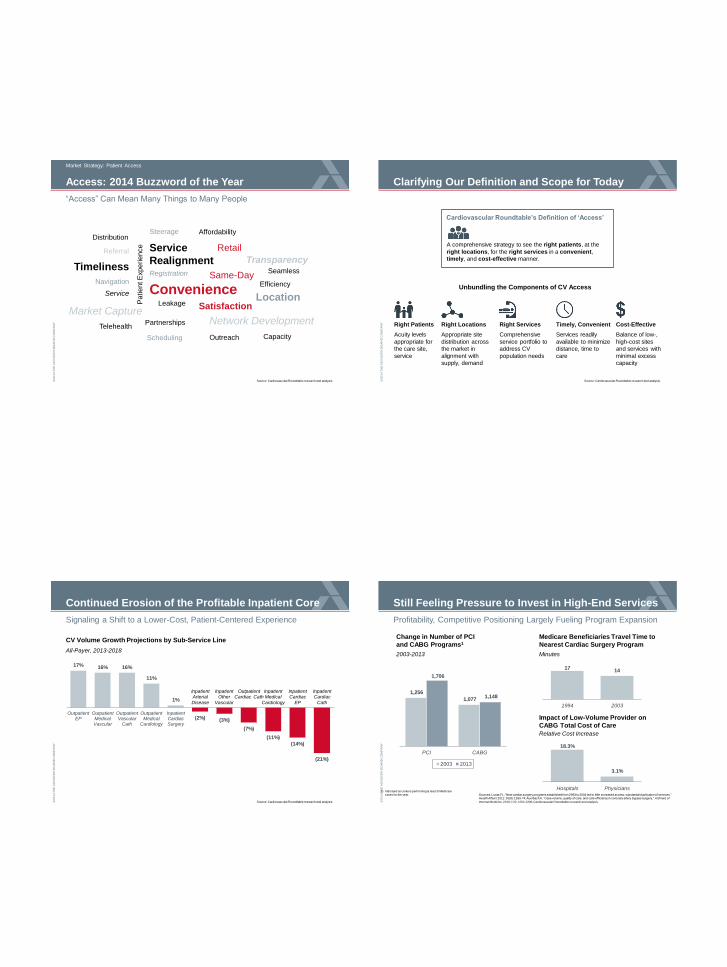

“Access” Can Mean Many Things to Many People

Market Strategy: Patient Access

Access: 2014 Buzzword of the Year

Source: Cardiovascular Roundtable research and analysis.

Timeliness

Market Capture

Convenience

Service

Realignment Registration

Leakage

Same-Day Efficiency

Partnerships Network Development

Navigation

Service

Satisfaction

Scheduling

Referral

Distribution

Retail

Affordability Steerage

Seamless

Telehealth

Location

Transparency

Outreach Capacity

Pa

tie

nt E

xp

erie

nce

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Source: Cardiovascular Roundtable research and analysis.

Clarifying Our Definition and Scope for Today

Cardiovascular Roundtable’s Definition of ‘Access’

A comprehensive strategy to see the right patients, at the

right locations, for the right services in a convenient,

timely, and cost-effective manner.

Unbundling the Components of CV Access

Right Patients

Acuity levels

appropriate for

the care site,

service

Right Locations

Appropriate site

distribution across

the market in

alignment with

supply, demand

Right Services

Comprehensive

service portfolio to

address CV

population needs

Timely, Convenient

Services readily

available to minimize

distance, time to

care

Cost-Effective

Balance of low-,

high-cost sites

and services with

minimal excess

capacity

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Signaling a Shift to a Lower-Cost, Patient-Centered Experience

Continued Erosion of the Profitable Inpatient Core

17% 16% 16%

11%

1%

(2%) (3%)

(7%)

(11%)

(14%)

(21%)

OutpatientEP

OutpatientMedicalVascular

OutpatientVascular

Cath

OutpatientMedical

Cardiology

InpatientCardiacSurgery

CV Volume Growth Projections by Sub-Service Line

All-Payer, 2013-2018

Inpatient Arterial

Disease

Inpatient Other

Vascular

Outpatient Cardiac Cath

Inpatient Medical

Cardiology

Inpatient Cardiac

EP

Inpatient Cardiac

Cath

Source: Cardiovascular Roundtable research and analysis. ©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Profitability, Competitive Positioning Largely Fueling Program Expansion

Sources: Lucas FL, “New cardiac surgery programs established from 2993 to 2004 led to little increased access, substantial duplication of services,” Health Affairs 2011: 30(8): 1569-74; Auerbach A, “Case volume, quality of care, and care efficiency in coronary artery bypass surgery,” Archives of

Internal Medicine, 2010; 170: 1202-1208; Cardiovascular Roundtable research and analysis.

Still Feeling Pressure to Invest in High-End Services

Change in Number of PCI

and CABG Programs1

2003-2013

1,256

1,077

1,706

1,148

PCI CABG

2003 2013

Medicare Beneficiaries Travel Time to

Nearest Cardiac Surgery Program

17 14

1994 2003

Impact of Low-Volume Provider on

CABG Total Cost of Care

18.3%

3.1%

Hospitals Physicians

Minutes

Relative Cost Increase

1) Indicated as centers performing at least 5 Medicare cases for the year.

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

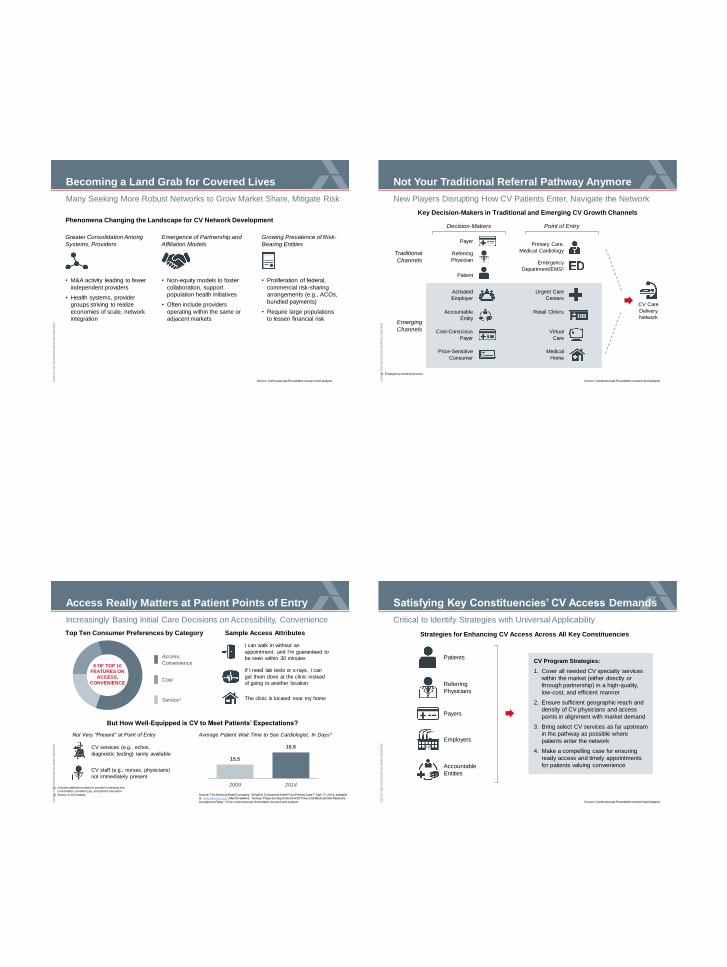

Many Seeking More Robust Networks to Grow Market Share, Mitigate Risk

Source: Cardiovascular Roundtable research and analysis.

Becoming a Land Grab for Covered Lives

Phenomena Changing the Landscape for CV Network Development

Greater Consolidation Among

Systems, Providers

Emergence of Partnership and

Affiliation Models

Growing Prevalence of Risk-

Bearing Entities

• M&A activity leading to fewer

independent providers

• Health systems, provider

groups striving to realize

economies of scale, network

integration

• Non-equity models to foster

collaboration, support

population health initiatives

• Often include providers

operating within the same or

adjacent markets

• Proliferation of federal,

commercial risk-sharing

arrangements (e.g., ACOs,

bundled payments)

• Require large populations

to lessen financial risk

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

New Players Disrupting How CV Patients Enter, Navigate the Network

Source: Cardiovascular Roundtable research and analysis.

Not Your Traditional Referral Pathway Anymore

Traditional

Channels

Key Decision-Makers in Traditional and Emerging CV Growth Channels

Payer

Emerging

Channels

Patient

Decision-Makers

Emergency

Department/EMS1

Point of Entry

Primary Care,

Medical Cardiology

Retail Clinics

Urgent Care

Centers

Virtual

Care

Price-Sensitive

Consumer

Activated

Employer

Medical

Home

Accountable

Entity

Cost-Conscious

Payer

CV Care

Delivery

Network

1) Emergency medical services.

Referring

Physician

©2

01

4 T

HE

AD

VIS

OR

Y B

OA

RD

CO

MP

AN

Y

Increasingly Basing Initial Care Decisions on Accessibility, Convenience

Source: The Advisory Board Company, “What Do Consumers Want From Primary Care?” April 17, 2014, available at: www.advisory.com; Merritt Hawkins, “Survey: Physician Appointment Wait Times and Medicaid and Medicare

Acceptance Rates,” 2014; Cardiovascular Roundtable research and analysis.

1) Includes attributes related to provider continuity and coordination, provider type, and patient education.

2) Survey of 15 markets.

Access Really Matters at Patient Points of Entry

Cost

Service1

Access,

Convenience

Top Ten Consumer Preferences by Category

6 OF TOP 10 FEATURES ON

ACCESS,

CONVENIENCE

I can walk in without an

appointment, and I’m guaranteed to

be seen within 30 minutes

If I need lab tests or x-rays, I can

get them done at the clinic instead

of going to another location

The clinic is located near my home

Sample Access Attributes

But How Well-Equipped is CV to Meet Patients’ Expectations?