Embed Size (px)

Citation preview

2015

C A P S T O N E T U R B I N E

A N N U A LR E P O R T

10938_2015 Capstone AR_Cover.indd 3 6/24/15 11:00 AM

2 | Capstone Turbine Corporation 2015 Annual Report | 2

08 | Capstone Turbine Corporation

02 LETTER TO STOCKHOLDERS

06 VERTICAL CHANNEL DISTRIBUTION

08 MARKET AND GEOGRAPHIC DIVERSIFICATION

10 GLOBAL MARKET SEGMENTS

11 MEGAWATTS SHIPPED AND GLOBAL HIGHLIGHTS

14 BROAD SUITE OF PRODUCTS

16 AFTERMARKET SERVICES

18 FUTURE GROWTH

20 FINANCIAL AND OPERATING SUMMARY

21 KEY FINANCIAL FIGURES

CONTENTS

10938_2015 Capstone Annual Report_23June_R1.indd 2 6/26/15 5:10 PM

2 | Capstone Turbine Corporation 2015 Annual Report | 2

DEAR FELLOW STOCKHOLDERS

In fiscal 2015, Capstone continued to make significant progress in strengthening our company by further diversifying our business, growing and maturing our distribution network, improving our

product reliability, implementing cost savings and expanding into promising new geographies. The operational improvements to our cost structure that we implemented over the past several years resulted in flat gross margins year over year despite the 13 percent decline in top line revenue. Additionally, gross margin was impacted by a non-cash reserve for slow moving inventory and certain direct material costs were recorded without the associated revenue as of March 31, 2015. Gross margin has been in the double digits since the third quarter of 2013, or 10 consecutive quarters. However, our operational progress has been eclipsed by the challenging macroeconomic headwinds that have confronted us over the last year. The dramatic downturn of the oil markets, a substantially stronger U.S. dollar making our products more expensive overseas and ongoing geopolitical tensions in Russia, North Africa and the Middle East were all factors that have negatively impacted our business.

Despite these challenging global and economic market dynamics, we have pushed onward and adapted in ways that have undoubtedly built a more resilient Capstone today and for the future. By improving our supply chain and making strategic management adjustments, we have significantly reduced operational costs within the organization. Additionally, as our installed base of microturbines continues to grow, it will drive more predictable and recurring revenue from our service business. This will help to accelerate the overall market acceptance of our product solutions and fuel new business development.

VERTICAL CHANNEL DISTRIBUTION

Our most valuable and intangible asset is our worldwide distribution network that we have proudly developed from the ground up. We have built this robust distribution network through education, training and empowerment. In addition, our flexibility in working with our distributors in a more challenging environment has further strengthened our relationships and fostered a mutual bond of loyalty built on trust and teamwork. Capstone is building long-term sustainable growth potential within our

network of 88 distributors and 9 OEM partners. This gives Capstone the global presence and manpower of approximately 740 employees collectively spread out across 152 locations around the world. Each one of our distributors is a strategically placed independent partner out on the front lines marketing and selling Capstone products and services. We look to a promising future as our existing distributors mature and succeed. As we continue to bring on new distributors in our expanding geographies, we expect to capture an increasing share of the worldwide distributed generation market.

10938_2015 Capstone Annual Report_23June.indd 2 6/24/15 11:21 AM

3 | Capstone Turbine Corporation 2015 Annual Report | 4

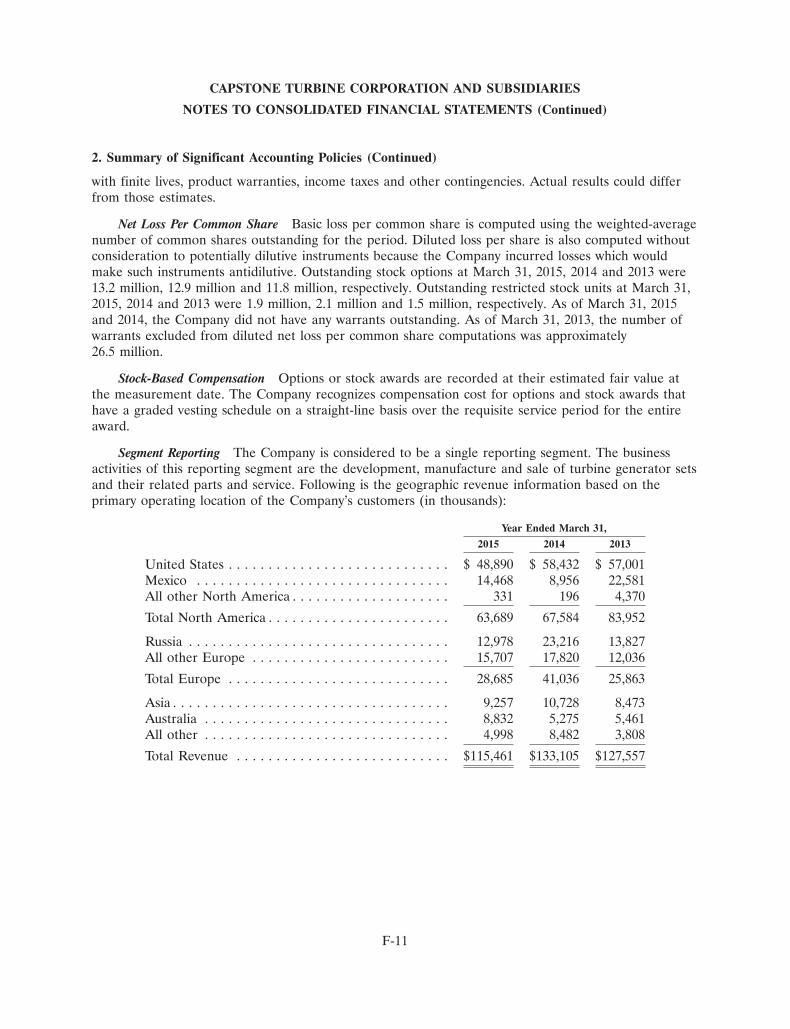

MARKET AND GEOGRAPHIC DIVERSIFICATION

Recognition of the Capstone brand and interest in our microturbine products continues to grow in all six of our major vertical markets – oil, gas and other natural resources, energy efficiency, renewable energy, critical power supply, marine and transportation. Demand for clean-and-green power generation technology continues to flourish worldwide and we estimate the global market opportunity for microturbine technology to be valued at approximately $15 billion, with Capstone’s potential market share at $1.5 billion.

Capstone is expanding its market share in a challenging oil, gas and other natural resources market. In Mexico, we are capitalizing on the opportunities that resulted from the Mexican energy reform, which has established reduced electricity and gas prices. One of our Mexican distributors, Industrias Energetícas, secured two of the largest orders in Capstone's history in participation with the Los Ramones pipeline project in eastern Mexico. With this type of success, Mexico is poised to be one of our top markets throughout fiscal 2016. Furthermore, we have seen strong demand for flare gas reduction in the Middle East and Africa. We see positive growth going forward in these markets as our distribution network matures in new regions and we expect to capitalize on these opportunities, offsetting business that may be down in other markets next year.

We have seen an increase in combined heat and power (CHP) projects around the world. In particular, we have experienced strong traction

in Australia, Mexico, Germany, Italy and Brazil. In the United States, the CHP market is growing in several states including New York, New Jersey, Pennsylvania, California, Alaska and Hawaii. Despite the slowdown in oil production in Russia, one of our distributors, BPC Engineering, is pursuing growth in the sales of CHP and combined cooling, heat and power (CCHP) plants within the Russian manufacturing sector and in neighboring Kazakhstan and Belarus. Although Europe remains economically constrained, we are encouraged by the strengthening demand for CHP applications in a number of other countries including Germany, Italy, Austria, Switzerland, Finland, Poland and the United Kingdom.

With oil, gas and other natural resources serving as one of Capstone’s larger market segments in the United States, shale plays have become a major focus going into fiscal 2016. Capstone microturbines provide shale oil and gas operations with ultra-low emission, low maintenance and reliable solutions that operate more efficiently and for longer periods of time than typical reciprocating engine generators. This helps to solidify Capstone’s position as the preferred option for new and repeat oil and gas customers.

Capstone continues to search the globe for opportunities in new markets and recently found success in developing power projects from palm oil production in Malaysia and propane-based CHP in the Caribbean. These new markets showcase tremendous opportunities for us. Palm oil is a multi-billion dollar industry Capstone can most certainly

10938_2015 Capstone Annual Report_23June.indd 3 6/24/15 11:21 AM

3 | Capstone Turbine Corporation 2015 Annual Report | 4

Gary D. SimonChairman of the Board

Darren R. JamisonPresident and Chief Executive Officer

capitalize on. In addition, the Caribbean utility rates are extremely high, making CHP a very attractive alternative.

AFTERMARKET SERVICE

The recent design enhancements to our flagship C200 and C1000 series products combined with the improvements we made to our aftermarket service business have led to reduced warranty expenses and higher Factory Protection Plan (FPP) contribution margins. Our FPP backlog grew to approximately $61.2 million by March 31, 2015 — a new record for Capstone. Our market-leading FPP also better aligns our service offering with our customer requirements. Approximately 20 percent of our units in the field are currently operating under a FPP, leaving plenty of opportunity to both expand and further scale our aftermarket services business. Overall, our aftermarket services carry higher margins, which we expect to increase as a percentage of total revenue as our global fleet continues to grow each year.

FUTURE GROWTH

The headwinds we faced in fiscal 2015 led us to flatten our organization. By streamlining our internal operations, we can better foster innovation and creativity, focus on product robustness and broaden our aftermarket services. These actions will lower operating costs and result in an estimated $2 million

in annual savings after severance costs. Our long-term outlook for the future of Capstone remains positive as we continue to expand and mature our worldwide distribution network, drive accelerated growth through new emerging markets, deliver ongoing product enhancements and develop new and improved microturbine products and services.

Without question the economic challenges we encountered this past year made it a difficult one, pushing out our anticipated achievement of EBITDA breakeven. While we are disappointed in this outcome, we have focused on adapting quickly and executing better under these new circumstances.

Today, Capstone is stronger, leaner, more flexible and better positioned for growth than ever before. Our team is extremely motivated and driven by the highest standards of open communication, creativity, collaboration, adaptability and accountability, keeping customer satisfaction and stockholder value at the center of all our business decisions. We would like to thank our stockholders, customers, employees, distributors and suppliers for your continued support, confidence and patience as we continue on our mission to deliver world-class clean energy solutions. We look forward to reporting on our progress over the next year.

10938_2015 Capstone Annual Report_23June.indd 4 6/24/15 11:21 AM

5 | Capstone Turbine Corporation 2015 Annual Report | 6

10938_2015 Capstone Annual Report_23June.indd 5 6/24/15 11:21 AM

5 | Capstone Turbine Corporation 2015 Annual Report | 6

Capstone’s global distribution network is constantly expanding and evolving to better serve our customers. As we continue to penetrate markets in new and developing regions, Capstone and our distributors are working harder than ever to raise brand awareness and drive a more robust sales pipeline. With integrated marketing efforts, a more advanced applications training program and the increased availability of parts and services, we remain on track to further mature our global distribution network.

GROWING CHANNEL TO MARKET

152 88 9 740LOCATIONS DISTRIBUTORS OEMs DISTRIBUTOR EMPLOYEES

Through trust and innovation, we have established our distributor network as one of our top competitive advantages. Our 88 distributors and 9 OEM partners provide a vital link between Capstone and our customer base, by collaborating with us to provide the highest-quality products, services and customer experience possible. Our refined distribution network extends our workforce presence to approximately 740 employees across 152 locations around the world. Through this network we are able to penetrate geographies and market segments more efficiently by leveraging the local expertise of each region. Capstone was successful in signing 10 new distribution partners over the last year in new and emerging market regions. With a focus on

expanding our global reach, Capstone signed contracts with new distributors in France, Jordan, Kuwait, The Netherlands, Republic of Moldova, Saudi Arabia, Trinidad and Tobago, Turkey and the United States. Success in new geographies and vertical markets is critical for company growth as it further diversifies and strengthens our global distribution.

Capstone only invests in distribution partners that are committed to align strategically with our business in order to accelerate channel optimization. Once a distribution partner is signed, we stand shoulder-to-shoulder with them in order to grow our global presence and deliver the best industry-leading power generation solutions.

VERTICAL CHANNEL DISTRIBUTION

10938_2015 Capstone Annual Report_23June.indd 6 6/24/15 11:21 AM

7 | Capstone Turbine Corporation 2015 Annual Report | 8

10938_2015 Capstone Annual Report_23June.indd 7 6/24/15 11:21 AM

7 | Capstone Turbine Corporation 2015 Annual Report | 8

OIL, GAS AND OTHER NATURAL RESOURCES

Over the past year, the precipitous drop in global oil prices and other macroeconomic challenges faced within the oil and gas industry have all affected the rate at which customers are adopting Capstone products. Despite a shift in oil and gas production worldwide, the advantages Capstone solutions has over its competitors have led to follow-on orders for traditional oil and gas applications and further expansion into the flare gas market.

Producers of oil, gas and other natural resources are continually looking for energy systems that reduce operational costs while being both reliable and easy to maintain. Capstone microturbines are the proven solution for oil and gas operations worldwide as many of the operations are off-the-grid or in remote locations.

ENERGY EFFICIENCY

High energy demand and unpredictable fluctuations in energy costs have led companies across the United States, Europe and Australia to seek out more efficient energy solutions. We have significantly grown our installed microturbine fleet within the CHP and CCHP markets by diversifying in key regions. Capstone had a 39 percent increase

in revenue from the energy efficiency market to $39 million in fiscal 2015 from $28 million in fiscal 2014.

We expect this high demand for CHP and CCHP applications to grow exponentially in other regions including Asia Pacific, Europe, Russia and South America. With CHP efficiency levels exceeding 80 percent, the cost benefits achieved by owning a Capstone microturbine outweigh those of our competitors.

RENEWABLE ENERGY

As an important part of our commitment to improving the efficiency of the world’s energy infrastructure and reducing global emissions, Capstone microturbines can be configured to operate on numerous types of biogases to produce renewable energy. Capstone continues to prove its ability to produce renewable energy by securing projects in Lithuania, Malaysia and the United States. These customers can now operate knowing that their carbon footprint is smaller and reliance on the local utility is lower. With their high reliability, low operating costs and low emissions, Capstone microturbines represent a smart power generation solution that can easily integrate with leading-edge green waste conversion technologies.

The global demand for alternative energy technologies is steadily growing across all six of our vertical markets. As we strengthen Capstone’s global presence through a maturing distributor network and improved supply chain, the value and benefits of owning a Capstone microturbine continues to define the standard for power generation solutions.

MARKET AND GEOGRAPHIC DIVERSIFICATION

FY14

$28M

FY15

$39M

Capstone EnergyEfficiency Market

$340Mpotential market capture

of renewable energy

10938_2015 Capstone Annual Report_23June.indd 8 6/24/15 11:22 AM

9 | Capstone Turbine Corporation 2015 Annual Report | 10

CRITICAL POWER SUPPLY

Businesses such as hospitals and data centers demand the highest level of energy reliability. These facilities cannot suffer even a momentary lapse in power without potentially devastating effects. To meet the needs of these customers, Capstone has developed two solutions that deliver the dependability and security they require. The Capstone UPSource and the hybrid uninterruptible power supply (HUPS) both provide primary and emergency power for critical loads. These integrated solutions can also be deployed in a high efficiency CHP configuration, providing heating and/or cooling to the facility and further reducing operating costs.

TRANSPORTATION

Capstone microturbines operate in conjunction with mobile onboard battery packs to provide electrical power as needed for hybrid electric vehicle (HEV) applications. There are many benefits to implementing Capstone’s technology into HEVs, including low noise, no

vibration and ultra-low emissions. Capstone stands ready to help propel the transportation market into the future as our microturbines provide an overall lower environmental footprint than any other onboard power source.

MARINE

Capstone microturbines can be deployed in a number of marine applications, from workboats to luxury yachts, providing onboard power to ancillary equipment and living quarters. In a CHP configuration, microturbines can increase the overall efficiency of a vessel by providing space heating, hot water and cold water. With the ability to run on liquid fuel or liquefied natural gas (LNG), microturbines can serve as an onboard range extender or drive the electrical propulsion system. With many added benefits including reduced fuel consumption, lower emissions, higher reliability, longer maintenance intervals and minimal vibration, Capstone microturbines provide a superior alternative for powering the marine industry.

54267

301

112

734

4,144

3,750

274343

8,511

CUMULATIVE UNITS SHIPPEDCUMULATIVE MEGAWATTS SHIPPED

C600|C800|C1000C200C65C30

average cost of one minute of data center downtime

$7,900

10938_2015 Capstone Annual Report_23June.indd 9 6/24/15 11:22 AM

9 | Capstone Turbine Corporation 2015 Annual Report | 10

Capture and utilize thermal energy from the clean exhaust in CHP and CCHP

applications for Hotels, Large Residential Complexes, Retail Buildings and

Office Buildings.

Cleanly and efficiently operate on biogas and other waste products to create

high-efficiency renewable power and heat for Farm Digesters, Landfills, Food Waste

and Solid Waste Management.

Generate on-site power for all phases of oil and gas production in both onshore

and offshore applications including Drilling Operations, Flare Gas Reduction,

Gas Compression, Mining and Water Conversion.

Operate in conjunction with battery packs to provide onboard battery charging and vehicle range extension to Commercial

Trucks, Heavy-duty Vehicles, Supercars, Transit Buses and Delivery Vehicles.

Mission critical businesses have an uninterruptible power source with the

world’s only microturbine-powered UPS solution for Data Centers, Hospitals,

Telecom and Power Rentals.

Provide onboard auxiliary power, vessel range extension and utilize thermal

energy for onboard heating and cooling for Cargo Ships, Commercial Vessels, Luxury

Yachts and Work Boats.

Potential Market $100MPotential Market $90MPotential Market $250M

Potential Market $340MPotential Market $440MPotential Market $310M

Energy Efficiency Renewable EnergyOil, Gas and OtherNatural Resources

TransportationCritical Power Supply Marine

GLOBAL MARKET SEGMENTS

10938_2015 Capstone Annual Report_23June.indd 10 6/24/15 11:22 AM

11 | Capstone Turbine Corporation 2015 Annual Report | 12

GLOBAL HIGHLIGHTS FY15

91MWMEGAWATTS SHIPPED FY15

13 C800 microturbines and 16 C30 microturbines to power two major phases of the Los Ramones pipeline project in Northeastern Mexico.

Natural-gas-fueled C600 microturbines installed at three compressor stations in the Marcellus and Utica Shale plays.

A 14MW order for multiple CHP projects in Mexico to help boost the energy efficiency of the country’s manufacturing sector.

A C1000 provides electricity, heating and cooling to help a business district in Medellín, Colombia meet its growing energy needs.

Capstone’s first project in El Salvador with a propane-fueled C200 microturbine (CCHP) for a plastics manufacturing plant in San Salvador.

A natural-gas-fueled C1000 microturbine to upgrade a cancer treatment center in New York City.

A 1MW order to upgrade a Southern California water recycling plant in Irvine using biogas produced on-site.

A propane-fueled Capstone C1000 deployed in a CCHP configuration will provide 24/7 prime power for an exclusive resort in the U.S. Virgin Islands.

North AmericaEurope

South America

47MW12MW

2MW

Energy Efficiency

Renewable Energy

Critical Power Supply

Oil, Gas and Other Natural Resources

10938_2015 Capstone Annual Report_23June_R1.indd 11 6/26/15 5:10 PM

11 | Capstone Turbine Corporation 2015 Annual Report | 12

Capstone’s first project in El Salvador with a propane-fueled C200 microturbine (CCHP) for a plastics manufacturing plant in San Salvador.

A natural-gas-fueled C1000 microturbine to upgrade a cancer treatment center in New York City.

A 1MW order to upgrade a Southern California water recycling plant in Irvine using biogas produced on-site.

A propane-fueled Capstone C1000 deployed in a CCHP configuration will provide 24/7 prime power for exclusive resort in U.S. Virgin Islands.

A natural-gas-fueled C600 microturbine to power a popular Russian rubber footwear manufacturing facility in Astrakhan.

Capstone’s first project in Oman with two natural-gas-fueled C65 microturbines for an oil and gas pipeline supply company.

One of the first Italian food retailers to implement Capstone technology with a methane-fueled C800 microturbine (CCHP) in Fiano Romano.

Two C1000’s installed on an offshore platform in Africa will run on flare gas to power artificial lift equipment (electrical submersible pumps) that is used to increase oil production.

Two orders totaling 3MW to provide power to palm oil processing plants in Malaysia using biogas-fueled microturbines.

A 5.5MW (CHP) order to upgrade two Russian sports centers in Sochi and in Kislovodsk.

A 1.4MW (CCHP) order to upgrade a building in a major Australian business center in Sydney.

Capstone natural gas C1000 in a CHP configuration will provide 1MW of clean power and heat to a new Metro-City residential high-rise in Masan, South Korea.

Asia

Australia

Russia

Africa

Middle East

7MW

5MW

16MW

2MW

<1MW

10938_2015 Capstone Annual Report_23June.indd 12 6/24/15 11:22 AM

13 | Capstone Turbine Corporation 2015 Annual Report | 14

10938_2015 Capstone Annual Report_23June.indd 13 6/24/15 11:22 AM

13 | Capstone Turbine Corporation 2015 Annual Report | 14

Features Benefits

Patented air bearing technology No lubricants or coolants needed

Clean waste heat Thermal energy for CHP and CCHP

Remote monitoring View performance and diagnostics 24/7

Capstone offers a comprehensive lineup of clean-and-green microturbines that are scalable from 30kW to 30MW and can operate on a variety of gaseous or liquid fuels. Capstone microturbines are the ideal solution for today’s distributed generation needs. Reliable power when and where you need it. Clean and simple.

BROAD SUITE OF PRODUCTS

Only one moving part Longer service intervals, low operating cost

High power density Compact footprint, small modular design

Stand alone or grid connect Multiple applications and industries

Wide fuel range Operates on gaseous, renewable and liquid fuels

COMPETITIVE ADVANTAGES

Advanced combustion controls Low emissions, no exhaust aftertreatment

10938_2015 Capstone Annual Report_23June.indd 14 6/24/15 11:22 AM

15 | Capstone Turbine Corporation 2015 Annual Report | 16

10938_2015 Capstone Annual Report_23June.indd 15 6/24/15 11:22 AM

15 | Capstone Turbine Corporation 2015 Annual Report | 16

Capstone’s global network of distribution partners provide on-site problem diagnosis and repairs any day of the year, ensuring minimal downtime for our customers’ operations.

Capstone provides factory and on-site training to certify all personnel that are allowed to perform service on our microturbines. Certified individuals are called authorized service providers (ASPs) and must be employed by a distributor in order to perform work pursuant to a Capstone FPP.

We are actively working with our ASPs to strengthen our service offerings and fine tune our FPP to provide higher availability and reliability through a more comprehensive service package. The success of Capstone hinges on both distributor and customer satisfaction. A greater focus on service has led our team to develop and implement a mutually agreeable, definable and actionable plan to advance the business and grow Capstone’s global presence.

Capstone has increased the emphasis on regional teams composed of representatives from our Sales and Marketing, Applications and Customer Service groups. These teams provide improved communication methods and better escalation processes that translate to a superior customer experience. The overarching goals, which stretch across the entire organization, are to maximize revenue

growth and heighten support for both our customers and distribution partners. Capstone prides itself on being the world’s leading clean technology manufacturer of microturbine energy systems. With this increased focus on aftermarket support around the world, Capstone is committed to providing the best customer service and product support.

We at Capstone understand the critical nature of reliable power generation. Capstone microturbines have approximately 60 million cumulative operating hours in the field and the installed base continues to grow. Manufacturing a reliable product is the first step to ensuring a customer’s needs are met and a working relationship is established. The next step is properly managing that relationship by providing the very best service and support in a timely manner.

Customers from each of our market segments, from oil and gas producers to food manufacturers, rely on our product expertise to guide them towards the return on their investment. We will continue to take the quality of our service business to the next level by working closely with our customers as they pursue their energy goals.

One of our top priorities going into fiscal 2016 is to further strengthen our aftermarket service business to better align with the needs of our customers.

AFTERMARKET SERVICES

FY14

$47.2M

FY15

$61.2M

FPP Backlog+30% from FY14

cumulative operating hours,15% increase from FY14

60M

10938_2015 Capstone Annual Report_23June.indd 16 6/24/15 11:22 AM

17 | Capstone Turbine Corporation 2015 Annual Report | 18

10938_2015 Capstone Annual Report_23June.indd 17 6/24/15 11:22 AM

17 | Capstone Turbine Corporation 2015 Annual Report | 18

Over the last year, Capstone has identified and successively targeted market segments that are experiencing significant growth. Shortly after signing a new Middle East and Africa distributor, Micro Turbine Power (M.T.P.), Capstone secured two major flare reduction projects in the region. With consistent onshore and offshore oil production in the Middle East and Africa, we anticipate substantial new business opportunities in these areas. Capstone is committed to expanding our global presence, especially in the developing regions of the world.

Capstone is also targeting new and emerging markets. For example, Malaysia has seen a surge in the demand and subsequent extraction of crude palm oil, making it the second largest palm oil producer in the world. Palm oil production plants require continuous power for around-the-clock manufacturing and Capstone microturbines are able to use the waste from the oil extraction process as a sustainable fuel for power generation. We are excited to be pursuing an industry conservatively estimated to be greater than $40 billion globally and one that is expected to double by 2020.

Our company has made improvements both internally and cooperatively with our distribution partners. Our flattened organizational approach will ensure that we create a more efficient management structure

to further capitalize on worldwide opportunities through increased collaboration and open communication. We will expand our global distributor network as a platform for long-term sustainable growth. The expansion of our distributor network provides Capstone a competitive advantage and will include new distributors being signed on as independent partners, as well as the goal of having our distributors increase their sales force by collectively adding 100 new sales positions to their staff during fiscal year 2016.

There have been new levels of excitement, dedication, teamwork and cross-functional cooperation within Capstone and across our greater distributor and OEM networks. By improving the quality and structure of our operations across our entire organization, Capstone will continue to lead the way in clean-and-green microturbine energy systems.

Our market-leading FPP closely aligns our service offering with customer requirements and we believe it is virtually unmatched in the industry. We look to accelerate our aftermarket service business to better leverage growth and improve overall margins.

We are more confident than ever that once the current economic challenges subside, we will emerge better positioned for global growth than ever before.

The future for Capstone is brighter than ever. Even with the global and economic challenges we faced over the past year, there are vast opportunities across all six of our vertical markets and in new and developing regions.

FUTURE GROWTH

10

$40 billion

distributors added in FY15

palm oil industry

10938_2015 Capstone Annual Report_23June_R1.indd 18 6/26/15 5:10 PM

19 | Capstone Turbine Corporation 2015 Annual Report | 20

10938_2015 Capstone Annual Report_23June.indd 19 6/24/15 11:22 AM

19 | Capstone Turbine Corporation 2015 Annual Report | 20

During fiscal 2015, our revenue was impacted by a weakness in the oil and gas market, stronger U.S. dollar and a challenging Russian economy. However, we did experience an increase in our Australian and South American markets by $3.6 million and $0.8 million, respectively, as the result of our continued efforts to improve our distribution channels in these developing regions. Capstone continues to invest in its aftermarket service business, creating both a market-leading FPP business and lower warranty expenses. Fiscal 2015 was the first year in which our FPP business generated both a higher percentage of revenue and a record level FPP backlog of $61.2 million. As a result of these efforts, we continue to create a more efficient business.

FINANCIAL AND OPERATING SUMMARY

OPERATING LEVERAGE

FY15FY14FY13FY12FY11FY10

$115.5$127.6

$133.1

$109.4

$81.9

$61.6

$14.7 $14.5$14.6$14.8$13.4$13.5

• Capstone’s product backlog as of March 31, 2015 was $165.7 million, down 3 percent year over year. On a unit basis we had 787 units, or 182.8 megawatts, in total backlog.

• Accessories, parts and service revenue increased

7 percent, to $26.1 million compared to fiscal 2014. The growing installed base of equipment is increasing demand for aftermarket parts and services, overhauls and upgrades.

• FPP backlog increased 30 percent compared to fiscal 2014, demonstrating our growing installed base around the world and affirming the market’s acceptance of our FPP offering.

• Warranty expense decreased 10 percent to $3.5

million compared to fiscal 2014. We are seeing improved product reliability, which decreases warranty and maintenance costs associated with our fixed price FPP contracts.

RESULTS AND HIGHLIGHTS

Revenue(Dollars in Millions)

Production Laborand Overhead(Dollars in Millions)

$24.3M

FY14 FY15

$26.1M

Accessories, Parts & Service

decrease in warranty expense in FY15

10%

10938_2015 Capstone Annual Report_23June_R1.indd 20 6/26/15 5:10 PM

KEY FINANCIAL FIGURESDollars in millions except gross margin, shares outstanding, loss per share, megawatts, and units shipped.

FY15 FY14 FY13 FY12 FY11 FY15 Y/Y

Revenue $115.5 $133.1 $127.6 $109.4 $81.9 (13%)

Gross Margin (Loss) % 16% 16% 11% 5% (1%) 0bps

Research and Development $9.7 $9.0 $9.0 $8.2 $7.0 8%

Selling, General, and Administrative(1) $39.5 $28.0 $27.4 $28.9 $26.2 41%

Loss from Operations ($30.9) ($15.3) ($22.0) ($31.7) ($33.7) 102%

Weighted Average Shares Outstanding (in millions) 328.0 307.1 302.2 266.9 245.9 7%

Loss per Share ($0.10) ($0.05) ($0.07) ($0.07) ($0.16) 100%

Stock-Based Compensation Expense $2.2 $2.1 $1.6 $1.7 $2.4 5%

Depreciation and Amortization $1.7 $2.3 $2.8 $3.4 $3.8 (26%)

Capital Expenditures $1.6 $1.2 $1.2 $1.4 $1.0 33%

Cash and Cash Equivalents $32.2 $27.9 $38.8 $50.0 $33.5 15%(1) The company recorded bad debt expense of approximetly $10.1 million, $0.2 million, $0.3 million, $2.3 million and $0.2 million for the years ended March 31, 2015, 2014, 2013, 2012 and 2011 respectively.

See also Notes to our Condensed Consolidated Financial Statements.

Supplemental Data (Unaudited)

New Orders $84.5 $131.5 $112.6 $122.5 $86.5 (36%)

New Orders in Megawatts 86 135.3 107.2 136.3 91.9 (36%)

Microturbine Units Shipped 620 671 628 627 611 (8%)

Megawatts Shipped 91.4 109.9 103.2 96.1 69.7 (17%)

Total Backlog $165.7 $171.6 $148.9 $139.0 $106.4 (3%)

FY11 FY12 FY13 FY14 FY15

106.4

139.0148.9

171.6165.7

Total Backlog(In Millions)

81.9

109.4

127.6133.1

115.5

FY11 FY12 FY13 FY14 FY15

Revenue(In Millions)

FY11 FY12 FY13 FY14 FY15

5%

11%

16% 16%

(1%)

Gross Margin (Loss)

21 | Capstone Turbine Corporation

10938_2015 Capstone Annual Report_23June_R1.indd 21 6/26/15 5:10 PM

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K(Mark One)

� ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGEACT OF 1934

For the fiscal year ended March 31, 2015

or

� TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIESEXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-15957

CAPSTONE TURBINE CORPORATION(Exact name of registrant as specified in its charter)

Delaware 95-4180883(State or other jurisdiction of (I.R.S. Employerincorporation or organization) Identification No.)

21211 Nordhoff Street, 91311Chatsworth, California (Zip Code)

(Address of principal executive offices)(818) 734-5300

(Registrant’s telephone number, including area code)Securities registered pursuant to Section 12(b) of the Act:

Title of each class Name of exchange on which registered

Common Stock, par value $.001 per share NASDAQ Global MarketSeries A Preferred Stock Purchase Rights

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the SecuritiesAct. Yes � No �

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of theAct. Yes � No �

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) ofthe Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant wasrequired to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes � No �

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, ifany, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 ofthis chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and postsuch files). Yes � No �

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not containedherein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statementsincorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. �

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer,or a smaller reporting company. See the definitions of ‘‘large accelerated filer,’’ ‘‘accelerated filer’’ and ‘‘smaller reportingcompany’’ in Rule 12b-2 of the Exchange Act.

Large accelerated filer � Accelerated filer � Non-accelerated filer � Smaller reporting company �(Do not check if a

smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the ExchangeAct). Yes � No �

The aggregate market value of the shares of Common Stock of the registrant held by non-affiliates on September 30,2014 was approximately $353.3 million.

As of June 8, 2015, there were 330,689,556 shares of the registrant’s Common Stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement relating to the registrant’s 2015 annual meeting of stockholders areincorporated by reference into Part III of this report to the extent described therein.

CAPSTONE TURBINE CORPORATION

FORM 10-K

TABLE OF CONTENTS

Page

PART IItem 1. Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Item 1A. Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Item 1B. Unresolved Staff Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Item 2. Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Item 3. Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Item 4. Mine Safety Disclosures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

PART IIItem 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Item 6. Selected Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34Item 7. Management’s Discussion and Analysis of Financial Condition and Results of

Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35Item 7A. Quantitative and Qualitative Disclosures About Market Risk . . . . . . . . . . . . . . . . . . 53Item 8. Financial Statements and Supplementary Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53Item 9. Changes in and Disagreements with Accountants on Accounting and Financial

Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53Item 9A. Controls and Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53Item 9B. Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

PART IIIItem 10. Directors, Executive Officers and Corporate Governance . . . . . . . . . . . . . . . . . . . . . 56Item 11. Executive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56Item 12. Security Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57Item 13. Certain Relationships and Related Transactions, and Director Independence . . . . . . . 57Item 14. Principal Accounting Firm Fees and Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

PART IVItem 15. Exhibits and Financial Statement Schedules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

PART I

Item 1. Business.

Overview

Capstone Turbine Corporation (‘‘Capstone’’ or the ‘‘Company’’) develops, manufactures, marketsand services microturbine technology solutions for use in stationary distributed power generationapplications, including cogeneration (combined heat and power (‘‘CHP’’), integrated combined heatand power (‘‘ICHP’’), and combined cooling, heat and power (‘‘CCHP’’)), renewable energy, naturalresources and critical power supply. In addition, our microturbines can be used as battery charginggenerators for hybrid electric vehicle applications. Microturbines allow customers to produce poweron-site in parallel with the electric grid or stand alone when no utility grid is available. Severaltechnologies are used to provide ‘‘on-site power generation’’ (also called ‘‘distributed generation’’) suchas reciprocating engines, solar power, wind powered systems and fuel cells. For customers who do nothave access to the electric utility grid, microturbines provide clean, on-site power with fewer scheduledmaintenance intervals and greater fuel flexibility than competing technologies. For customers withaccess to the electric grid, microturbines provide an additional source of continuous duty power,thereby providing additional reliability and potential cost savings. With our stand-alone feature,customers can produce their own energy in the event of a power outage and can use microturbines astheir primary source of power for extended periods. Because our microturbines also produce clean,usable heat energy, they provide economic advantages to customers who can benefit from the use ofhot water, chilled water, air conditioning and heating. Our microturbines are sold, installed andserviced primarily through our global distribution network. Together we offer new and remanufacturedparts as well as a comprehensive Factory Protection Plan (‘‘FPP’’). Successful implementation ofmicroturbines relies on the quality of the microturbine, marketability for appropriate applications, andthe quality of the installation and support.

We believe we were the first company to offer a commercially available power source usingmicroturbine technology. Capstone offers microturbines designed for commercial, industrial and utilityusers with product offerings ranging from 30 kilowatts (‘‘kW’’) to one megawatt in electric poweroutput. Our 30 kW (‘‘C30’’) microturbine can produce enough electricity to power a small conveniencestore. The 65 kW (‘‘C65’’) microturbine can produce enough heat to provide hot water to a 100-roomhotel while also providing about one-third of its electrical requirements. Our 200 kW (‘‘C200’’)microturbine is well suited for larger hotels, office buildings and wastewater treatment plants, amongothers. By packaging the C200 microturbine power modules into an International Organization forStandardization (‘‘ISO’’) sized container, Capstone has created a family of microturbine offerings from600 kW up to one megawatt in a compact footprint. Our 1000 kW (‘‘C1000 Series’’) microturbines arewell suited for utility substations, larger commercial and industrial facilities and remote oil and gasapplications. Our microturbines combine patented air-bearing technology, advanced combustiontechnology and sophisticated power electronics to form efficient and ultra-low emission electricity andcooling and heat production systems. Because of our air-bearing technology, our microturbines do notrequire liquid lubricants. This means they do not require routine maintenance to change and dispose ofoil or other liquid lubricants, as do the most common competing products. Capstone microturbines canbe fueled by various sources, including natural gas, propane, sour gas, renewable fuels such as landfillor digester gas, kerosene, diesel and biodiesel. The C65 and C200 microturbines are available withintegrated heat exchangers, making them easy to engineer and install in applications where hot water isused. Our products produce exceptionally clean power. Our natural gas-fueled C65 andC200 microturbines were certified by the California Air Resources Board (‘‘CARB’’) as meeting itsstringent 2007 emissions requirements—the same emissions standard used to certify fuel cells and thesame emissions levels as a state-of-the-art central power plant. Our C65 Landfill and Digester Gassystems were certified in January 2008 by CARB as meeting 2008 waste gas emissions requirements forlandfill and digester gas applications. Our C200 Landfill and Digester Gas systems were certified in

2

November 2010 by CARB as meeting 2008 waste gas emissions requirements for landfill and digestergas applications.

On February 1, 2010, we acquired the 100 kW (‘‘TA100’’) microturbine product line from CalnetixPower Solutions, Inc. (‘‘CPS’’). The TA100 microturbine is most similar to the Capstone product designcompared to other microturbine products in the industry.

We sell complete microturbine units, subassemblies, components and various accessories. We alsoremanufacture microturbine engines and provide after-market parts and services. Our microturbines aresold primarily through distributors and Original Equipment Manufacturers (‘‘OEMs’’). Distributorspurchase our products for sale to end users and also provide application engineering and installationsupport. Distributors are also required to provide a variety of additional services, including engineeringthe applications in which the microturbines will be used, installation support of the products at the endusers’ sites, commissioning the installed applications and providing post-commissioning service. Ourdistributors perform as value-added resellers. OEMs integrate Capstone’s products into their ownproduct solutions.

To assure proper installation of Capstone microturbine systems, we have instituted a FactoryTrained Installer (‘‘FTI’’) training and certification program. Personnel from our distributors andOEMs, as well as design engineering firms, contractors and end users attend this FTI training. We offerto assist all customers by reviewing their installation designs to confirm that the technical requirementsfor proper operation have been met, such as electrical interconnections, load requirements, fuel typeand pressure, cooling air flow and turbine exhaust routing. As part of the microturbine commissioningprocess, we also receive a checklist to confirm that the final installation adheres to Capstone technicalrequirements before we accept any warranty obligations. This is aimed at providing the end user with aproper installation that will operate as expected for the life of the equipment.

Through our global distribution network, we offer a comprehensive FPP for a fixed annual fee toperform regularly scheduled and unscheduled maintenance as needed. Capstone provides factory andon-site training to certify all personnel that are allowed to perform service on our microturbines.Individuals who are certified are called Authorized Service Providers (‘‘ASPs’’), and must be employedby a distributor in order to perform work pursuant to a Capstone FPP. The majority of our distributorsprovide these services.

This Annual Report on Form 10-K (this ‘‘Form 10-K’’) refers to Capstone’s fiscal years endingMarch 31 as its ‘‘Fiscal’’ years.

Our Products

We began commercial sales of our C30 products in 1998, targeting the emerging distributedgeneration industry that was being driven by fundamental changes in power requirements. InSeptember 2000, we shipped the first commercial unit of our 60 kW microturbine (‘‘C60’’), which wasreplaced by the C65 model during the quarter ended March 31, 2006. We began shipping theC60 ICHP solution in 2003. The first commercial C200 microturbine was shipped on August 28, 2008.Our C1000 Series product was developed based on Capstone’s C200 microturbine engine. TheC1000 Series product can be configured into 1,000 kW, 800 kW and 600 kW solutions in a singleISO-sized container. The first commercial shipment of our C1000 Series product was on December 29,2008. We began shipping TA100 microturbines in March 2010.

During Fiscal 2015, we booked total orders of $84.5 million for 587 units, or 86.0 megawatts,compared to $131.5 million for 675 units, or 135.3 megawatts, during Fiscal 2014. We shipped 620 unitswith an aggregate of 91.4 megawatts, generating revenue of $90.4 million compared to 671 units withan aggregate of 109.9 megawatts, generating revenue of $108.8 million during Fiscal 2014. Total backlogas of March 31, 2015 decreased $5.9 million, or 3%, to $165.7 million from $171.6 million at March 31,

3

2014. As of March 31, 2015, we had 787 units, or 182.8 megawatts, in total backlog compared to820 units, or 188.2 megawatts, at the same date last year. The decrease in backlog was primarily theresult of the downturn of the oil markets, a substantially stronger U.S. dollar making our productsmore expensive overseas and on-going geopolitical tensions in Russia, North Africa and the MiddleEast. The timing of the backlog is based on the requirement date indicated by our customers. However,based on historical experience, management expects that a significant portion of our backlog may notbe shipped within the next twelve months. The timing of shipments is subject to change based onseveral variables (including customer deposits, payments, availability of credit and customer deliveryschedule changes), most of which are not in our control and can affect the timing of our revenue.

The following table summarizes our backlog:

As of March 31,

2015 2014

Megawatts Units Megawatts Units

C30 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.9 97 3.0 101C65 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32.6 502 33.8 520TA100 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1.9 19 1.9 19C200 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.4 12 3.4 17C600 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7.2 12 9.0 15C800 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9.8 12 8.8 11C1000 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125.0 125 127.0 127Waste heat recovery generator . . . . . . . . . . . . . . . . . . . . . . . . . 1.0 8 1.3 10

Total Backlog . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182.8 787 188.2 820

Capstone microturbines are compact, lightweight and environmentally friendly generators ofelectricity and heat compared to competing technologies. They operate on the same principle as a jetengine with the added capability of using a variety of commercially available fuels. For example, ourmicroturbines can operate on low British Thermal Unit (‘‘BTU’’) gas, which is gas with lower energycontent, and can also operate on gas with a high amount of sulfur, known in the industry as sour gas.Examples of these fuel sources include methane from facilities such as wastewater treatment plants,landfills and anaerobic digesters.

Our microturbines incorporate four major design features:

• advanced combustion technology;

• patented air-bearing technology;

• digital power electronics; and

• remote monitoring capability.

Our advanced combustion technology allows Capstone microturbines to achieve low emissions witha design geared towards manufacturability. These low emission levels not only provide anenvironmentally friendly product, but also eliminate permitting requirements in several municipalitiesfor continuously operated onsite power generation. The air-bearing system allows the microturbine’ssingle moving assembly to produce power without the need for typical petroleum-based lubrication.Air-bearings use a high-pressure field of air rather than petroleum lubricants. This improves reliabilityand reduces maintenance such as oil changes. The electronic controls manage critical functions andmonitor operations of the microturbine. For instance, our electronics control the microturbine’s speed,temperature and fuel flow and communicate with external networks and building management systems.The power electronics coordinate with the grid when the units are operated in a grid-connect modeand with the onboard battery when equipped for stand-alone mode. All control functions are

4

performed digitally. Performance is optimized, resulting in lower emissions, higher reliability and highefficiency over a variable power range.

The electrical output of our units can be paralleled in multiple unit configurations through ourAdvanced Power Server product and a digital communications cable to serve larger installationsrequiring electrical loads up to ten megawatts.

Our products can operate:

• connected to the electric utility grid as a current source;

• on a stand-alone basis as a voltage source;

• multipacked to support larger loads as a ‘‘virtual single’’ unit; and

• in dual mode, where the microturbine operates connected to the electric utility grid or operatesindependently.

We also offer C65 and C200 ICHP systems. These systems combine the standard C65 andC200 microturbine unit with a heat recovery module that provides electricity and heats water.

Our family of products is offered in the following configurations:

C30 C65 TA100 C200 C1000 Series

Grid Dual Grid Dual Grid Dual Grid Dual Grid DualFuel Types Connect Mode Connect Mode Connect Mode Connect Mode Connect Mode

Low pressure natural gas . . . . X X X X X X X X X XHigh pressure natural gas . . . . X X X X X X X X X XCompressed natural gas . . . . . X X X X X X X X X XLandfill gas . . . . . . . . . . . . . . X X X XDigester gas . . . . . . . . . . . . . . X X X XGaseous propane . . . . . . . . . . X X X X X X X XHigh pressure sour gas . . . . . . X X X X X X X XDiesel . . . . . . . . . . . . . . . . . . X X X X X X X XKerosene . . . . . . . . . . . . . . . . X X X X

We offer various accessories for our products including rotary gas compressors with digitalcontrols, heat recovery modules for CHP applications, dual mode controllers that allow automatictransition between grid connect and stand-alone modes, batteries with digital controls for stand-aloneor dual-mode operations, power servers for large multipacked installations, protocol converters forInternet access, packaging options and miscellaneous parts such as frames, exhaust ducting andinstallation hardware. We also sell microturbine components and subassemblies.

Our electronic controls manage microturbines using Capstone’s proprietary software and advancedalgorithms. The controls:

• start the turbogenerator and manage its load;

• coordinate the functioning of the microturbine with the grid;

• manage the speed, fuel flow and exhaust temperature of the microturbine;

• convert the variable frequency, up to a maximum of 1,600 Hertz and variable voltage powerproduced by the generator into a usable output of either 50 or 60 Hertz AC for stationaryapplications or DC for hybrid electric vehicle applications; and

• provide digital communications to externally maintain and control the equipment.

5

In addition, our proprietary Capstone Remote Monitoring Software (‘‘CRMS’’) allows end users toremotely operate and manage the microturbine. Unlike the technology of other power sources thatrequire on-site monitoring and maintenance, the CRMS allows end users to remotely and efficientlymonitor their microturbine systems. This remote capability can provide end users with powergeneration flexibility and cost savings.

The C30 microturbines were initially designed to operate connected to an electric utility grid andto use a high pressure natural gas fuel source. We have expanded our microturbine’s functionality tooperate with different fuels. The combustor system remains the same for all fuels except for the fuelinjectors, which currently vary between liquid and gaseous fuels. The Capstone microturbine’s multi-fuelcapability provides significant competitive advantages with respect to some of our selected verticalmarkets.

Our C65 grid-connect and stand-alone microturbine power systems are listed by UnderwritersLaboratories (‘‘UL’’) as meeting the UL 2200 stationary engine generator standards and the UL 1741utility interconnection requirements. Our products are manufactured by processes that areISO 9001:2008 and ISO 14001:2004 certified.

In 2002, the California Energy Commission certified our C30 and C60 microturbines as the firstproducts to comply with the requirements of its ‘‘Rule 21’’ grid interconnection standard. This standardstreamlines the process for connecting distributed generation systems to the grid in California. Thebenefits of achieving this standard include avoiding both costly external equipment procurementrequirements and extensive site-by-site and utility-by-utility analysis. Our protective relay functionalityhas also been recognized by the State of New York, which has pre-cleared our microturbines forconnection to New York’s electric utility grid.

Our C60 microturbine was the first combustion power generation product to be certified by theCARB as meeting its stringent distributed generation emissions standards that went into effect in 2003.Our C65 microturbine now meets the even more stringent CARB 2007 standard for natural gas.

The TA100 microturbine offers a digital communication interface which can be connected to anexternal controller (not sold by Capstone) to provide multiple unit and dual mode dispatchingfunctionality. An external synchronization board is provided to parallel the electrical output in multipleunit configurations for stand-alone operation.

We are the first microturbine manufacturer to achieve UL Class I, Division 2 certification foroperation in hazardous-area oil and gas applications. These specially packaged systems are applied inoil and gas production areas with potentially explosive environments. In September 2009, we receivedUL certification for our C200 grid-connect and stand-alone microturbine as meeting the UL 2200stationary engine generator standards and the UL 1741 utility interconnection requirements. In June2010, we received UL certification for our C1000 Series grid-connect and stand-alone microturbine asmeeting the UL 2200 stationary engine generator standards and the UL 1741 utility interconnectionrequirements.

Applications

Worldwide, stationary power generation applications vary from huge central stationary generatingfacilities up to 1,000 MW to back-up generators as small as 2 kW. Historically, power generation inmost developed countries such as the United States has been part of a regulated utility system. Anumber of developments related primarily to the deregulation of the utility industry as well assignificant technology advances have broadened the range of power supply choices available to all typesof customers.

Capstone products serve multiple vertical markets worldwide. Within the markets served, we focuson vertical markets that we have identified as having the greatest near-term potential. In the markets

6

we are focusing on, which are energy efficiency, renewable energy, natural resources, critical powersupply, transportation and marine, we have identified specific targeted vertical market segments.

Energy Efficiency—CHP/CCHP

Energy efficiency maximizes the use of energy produced by the microturbines, reduces emissionscompared with traditional power generation and enhances the economic advantage to customers.Energy efficiency uses both the heat and electric energy produced in the power generation process.Using the heat and electricity created from a single combustion process increases the efficiency of thesystem from approximately 30% to 75% or more. The increased operating efficiency reduces overallgreenhouse gas emissions compared with traditional independent sources such as power generation andlocal thermal generation and, through displacement of other separate systems, can reduce operatingcosts. Our microturbines’ emissions of commonly found air pollutants (‘‘criteria pollutants’’), such asnitrogen oxides (‘‘NOx’’), carbon monoxide (‘‘CO’’) and volatile organic compounds (‘‘VOCs’’), arelower than those from the on-site boilers that our CHP system displaces, meaning that local emissionsof these pollutants are actually reduced when a Capstone energy efficiency CHP system is installed.This high CHP efficiency also means more efficient use of fuel and can reduce net utility costs for endusers. The most common uses of heat energy include space heating and air conditioning, heating andcooling water, as well as drying and other applications. For example, we have used the heat generatedby the microturbines to supply hot water solutions for hotels, office buildings and retail, commercialand industrial customers. When our microturbine exhaust drives an absorption chiller, the chillerproduces chilled water for air conditioning and other uses.

There are energy efficiency markets for CHP and CCHP applications worldwide. A U.S.Department of Energy (‘‘DOE’’) report cited the total technical potential for the energy efficiency CHPat commercial, institutional and industrial sites in the United States to be over 130 gigawatts. Manygovernments have encouraged more efficient use of the power generation process to reduce pollution,lower dependence on fossil fuels and control the cost of locally produced goods. To access thesemarkets, we have entered into agreements with distributors which have engineered energy efficiencyCHP packages that utilize the hot exhaust air of the microturbine for heating water and also use thehot exhaust to run an absorption chiller for air conditioning. We also offer our own integrated energyefficiency CHP and CCHP product for the C65, C200 and C1000 Series products.

Renewable Energy

Our microturbines can use renewable methane gases from landfills, wastewater treatment facilitiesand other biogas applications such as food processing and agricultural waste, referred to as greenwaste, and cow, pig and chicken manure. They can burn these renewable waste gases with minimalemissions, thereby, in some cases, avoiding the imposition of penalties incurred for pollution whilesimultaneously producing electricity from this ‘‘free’’ renewable fuel for use at the site or in thesurrounding areas. The microturbines have demonstrated effectiveness in these applications andoutperform conventional combustion engines in a number of situations, including when the gas containsa high amount of sulfur.

Capstone released for sale the C65 stand-alone digester product in the renewable energy marketsegment in 2007. This product is targeted at remote villages in third-world countries with wastewatertreatment facilities that offer a valuable source of fuel which can be converted to electricity. A jointapplications and engineering team evaluated the performance of the existing C65 digester gas system toensure that the combustion system would be stable from 0 to 100% power output. Minor controlschanges were implemented to increase stability at low power levels. The ability to convert this low BTUfuel to electricity along with the high reliability and low maintenance features of this product make itwell suited for this market.

7

Natural Resources—Oil, Natural Gas, Shale Gas & Mining

On a worldwide basis, there are thousands of locations where the drilling, production, compressionand transportation of natural resources and other extraction and production processes create fuelbyproducts, which traditionally have been released or burned into the atmosphere. Our microturbinesare installed in the natural resource market to be used in oil and gas exploration, production,compression and transmission sites both onshore and offshore as a highly reliable critical source ofpower generation. In addition, our microturbines can use flare gas as a fuel to provide prime power.Typically these oil and gas or mining operations have no electric utility grid and rely solely onCapstone’s microturbine for reliable low emission power supply.

Many major oil and gas companies are exploring large shale reserves, or plays, in the UnitedStates. In mid-2010 Capstone sold its first microturbines into the U.S. shale gas market in the EagleFord and Marcellus shale plays. The addressable market for Capstone microturbines in this industry issignificant. The shale gas market for microturbines is expected to grow substantially as demand fornatural gas continues to rise and the U.S. Environmental Protection Agency (‘‘EPA’’), the Departmentof the Interior and other federal and state agencies work to reduce emissions of methane, volatileorganic compounds and hazardous air pollutants associated with natural gas development. Capstone hasbeen invited to participate in numerous Natural Gas STAR workshops in the United States and foreignmarkets to demonstrate the emissions reductions our technology can provide.

The C200 product is offered for sale configured to meet Class 1 Zone 2 hazardous locationrequirements for the oil and gas market. Hazardous location requirements are met through packageventilation changes for purging and pressurizing package air to avoid potential flammable mixtures aswell as controls for emergency disconnect of fuel and electrical sources. The package is upgraded tostainless steel construction to withstand the corrosive offshore environments where these units areinstalled. Oil and gas customers prefer the low maintenance and high reliability attributes offered byour turbines to ensure continued production. Capstone also offers C30 and C65 microturbine productsin similar configurations.

Critical Power Supply

Because of the potentially catastrophic consequences of even momentary system failure, certainpower users such as high technology, health care and information systems facilities require particularlyhigh levels of reliability in their power service. To meet these customer requirements, traditionalsolutions utilize Uninterruptible Power Supplies (‘‘UPS’’) to protect critical loads from momentarypower disturbances along with backup diesel generators for extended outages. Capstone offers analternative solution that can both meet customer reliability requirements and reduce operating costs.

Capstone has developed the world’s only microturbine powered UPS solutions that offer clean,IT-grade power and can completely displace the need for traditional UPS and backup diesel generators.We offer two microturbine-powered UPS solutions. The Capstone UPSource microturbine-poweredUPS solution provides prime or emergency power solutions. Capstone’s Hybrid UPS microturbinepowered solution provides power when dispatched in high efficiency, standard UPS and emergencypower solutions. Both critical power supply products offer 99.999999% availability in an n+1configuration when the product has at least one independent backup. Our microturbine-powered UPSsolutions are UL listed. These integrated solutions are ideal for new construction or facility expansionand are typically installed with absorption chillers or other heat recovery systems to obtain highefficiency and reduce operating costs compared with traditional solutions.

Dual mode units operating in a prime power configuration can support a 150% overload for10 seconds during transient conditions. Dual mode units operating in grid parallel mode can providecustomers a back-up power system with an economic return. These systems offer high onsite energyefficiency when combined with a heat exchanger (CHP) to create hot water or with a chiller (CCHP)

8

for air conditioning at these facilities. This configuration, when combined with the Capstone DualMode Controller, can transition from the grid parallel mode to prime power mode in less than tenseconds. Capstone microturbines can also be installed along with a rotary UPS to provide a completeline-interactive continuous power solution. In this case, the microturbines remain in grid connect modewhile the rotary UPS stabilizes the utility voltage and provides a seamless transfer from operationconnected to the grid to operation isolated from the grid.

Transportation

Our technology is also used in hybrid electric vehicle (‘‘HEV’’) applications. Our customers haveapplied our products in hybrid electric vehicles such as transit buses and trucks. In these applicationsthe microturbine acts as an onboard battery charger to recharge the battery system as needed. Thebenefits of microturbine hybrids include extended range, fuel economy gains, quieter operation,reduced emissions and higher reliability compared with traditional internal combustion engines. Internalcombustion diesel engine manufacturers have been challenged for the last several years to developtechnology improvements, prior to aftertreatment that reduce emissions to levels specified by the EPAand CARB 2007 and 2010 standards. Many manufacturers are incorporating aftertreatment thatincreases upfront equipment costs, vehicle weight and life cycle costs and may reduce overall engineefficiency.

Marine

Our technology is also used in marine applications. Our customers have applied our products inthe commercial vessel and luxury yacht markets. The most immediate market for our marine productsis for use as a ship auxiliary engine. In this application, the microturbines provide power to the vessel’selectrical loads and, in some cases, the vessel is able to utilize the exhaust energy to increase theoverall efficiency of the application, reducing overall fuel consumption and emissions. The otherapplication is similar to our HEV application where the vessel is driven by an electric propulsionsystem and the microturbine serves as an on board range extender. Our marine customers use both ourliquid fueled and natural gas products. Liquefied natural gas (‘‘LNG’’) is in its early stages as a marinefuel, and the number of vessels powered by LNG is forecasted to double every two years over the nextdecade. Vessel owners can receive the same benefits as users of stationary Capstone products: lowemissions with no aftertreatment, long maintenance intervals, high reliability, low noise and novibration.

Sales, Marketing and Distribution

We primarily sell our microturbine product, parts and service through distributors. Our world-widedistribution network is our most valuable intangible asset that we have proudly developed from theground up. Each one of our distributors is a strategically placed independent partner of Capstonemarketing and selling the Capstone products and services on our behalf. Our typical terms of saleinclude shipment of the products with title, care, custody and control transferring at our dock, paymentdue anywhere from in advance of shipment to 90 days from shipment, and warranty periods ofapproximately 15 to 18 months from shipment. We typically do not have customer acceptanceprovisions in our agreements.

North America

We have distribution agreements with a number of companies throughout North America for theresale of our products. Many of these distributors serve multiple markets in their select geographicregions. The primary markets served in this region have been energy efficiency, renewable energy,natural resources, critical power and mobile products. The energy efficiency and natural resourcesvertical markets are expected to grow as a result of an increased domestic production of hydrocarbons,the low downstream price of natural gas and public and regulatory acceptance of distributedgeneration.

9

Recent energy reform in Mexico has opened new market opportunities by allowing competitionand enabling power generation companies to sell directly to consumers instead of only to the state-owned Federal Electricity Commission. Capstone’s strategy in Mexico is to leverage our distributionnetwork in Mexico across various market verticals.

In developing our sales opportunities we have identified the need to address various requirementspresent in our target localities. These requirements include electric grid interconnection standards, gasutility connection requirements, emissions standards, building and fire safety codes and variousinspections and approvals. The costs and scheduling ramifications of these various approvals, inconjunction with normal bidding process requirements and construction delays, can be significant to thecompletion of an installation. Our goal is to work with the applicable regulating entities to establishcompliant standards for the installation of our microturbines so that the costs and installation timelinesare minimized for our customers. Management believes that we can create market advantages for ourproducts through enhancing the ease of deploying our distributed generation solutions.

Asia and Australia

Our sales and marketing strategy in Asia and Australia has been to develop and strengthendistributor relationships throughout these continents.

Our target markets in Asia and Australia are energy efficiency, renewable energy and naturalresources. Our historical sales in Southeast Asia and Australia have primarily been in the CHP, CCHPand the oil and gas market. Other areas in Asia and the Pacific Rim offer attractive opportunities aswell. China is expected to see growth in the oil and gas market, while biogas recovery is showing signsof growth in Southeast Asia.

Middle East and Africa

Our target market in the Middle East and Africa is primarily oil and gas. Flare gas to powerprojects are a particularly attractive market opportunity given the volume of gas being flared and theacute and chronic need for stable power in the region. Management has targeted distributors andcustomers involved in the capture and use of flare gas in the oil and gas market. However, thegeopolitical environment in this region is still volatile, which can impact our sales.

Europe and Russia

To address the European market, including Russia, we are strengthening our relationships withexisting and new distributors and have increased Capstone local sales and service support. We have anoffice in Europe for the purpose of working with our distributors there on a daily basis to realizegrowth opportunities. We have established a spare parts distribution center in Europe to make partsreadily available to our distributors. Europe has a history of extensive use of distributed generationtechnologies. During Fiscal 2015, the pace of economic recovery in Europe was slow and demandremained soft with a decrease in revenue of 30%, primarily from Russia, compared to Fiscal 2014.Further, the continuation or escalation of the current geopolitical instability in Russia and Ukrainecould continue to negatively impact our operations, sales, and future growth prospects in that region.For more information, see ‘‘Risk Factors’’ beginning on Page 14 of this Form 10-K.

South America

South America constitutes a diverse group of markets that vary greatly in potential capture forCapstone based on a number of factors including availability of oil and gas production andtransmission, energy pricing and political and investment climate. While Capstone has distributors innearly all South American countries, management is focused on what we consider to be the topmarkets, such as Colombia, Brazil, Chile and Ecuador. Our target markets in South America are

10

energy efficiency, renewable energy and natural resources. Our historical sales in South America haveprimarily been in the natural resources market.

Revenue

For geographic and segment revenue information, please see Note 2—Summary of SignificantAccounting Policies—Segment Reporting in the ‘‘Notes to Consolidated Financial Statements.’’

Customers

Sales to Horizon Power Systems (‘‘Horizon’’), one of the Company’s domestic distributors,accounted for 17%, 12% and 27% of our revenue for the years ended March 31, 2015, 2014 and 2013,respectively. Sales to BPC Engineering (‘‘BPC’’), one of the Company’s Russian distributors, accountedfor 11%, 17% and 11% of our revenue for the years ended March 31, 2015, 2014 and 2013,respectively. Sales to E-Finity Distributed Generation, LLC (‘‘E-Finity), one of the Company’s domesticdistributors, accounted for 19% of our revenue for the year ended March 31, 2014. Additionally,Optimal Group Australia Pty Ltd (‘‘Optimal’’), one of the Company’s Australian distributors, accountedfor 17% of net accounts receivable as of March 31, 2015. BPC, Electro Mecanique Industries (‘‘EMI’’),one of the Company’s distributors in the Middle East and Africa, and E-Finity accounted for 26%,18% and 16%, respectively, of net accounts receivable as of March 31, 2014.

During the three months ended March 31, 2015, we recorded approximately $7.1 million withrespect to the accounts receivable allowance from BPC. We determined that the collectability of thisaccounts receivable balance was not reasonably assured based on BPC’s recent payment history andbecause the impact of the steep decline of the Russian ruble could continue to negatively impact itsability to pay its outstanding accounts receivable balance. Also during the three months endedSeptember 30, 2014, we recorded approximately $2.6 million with respect to the accounts receivableallowance from EMI. We determined that the collectability of this accounts receivable balance was notreasonably assured based on EMI’s payment history. The Company recorded bad debt expense ofapproximately $10.1 million, $0.2 million and $0.3 million for the years ended March 31, 2015, 2014and 2013, respectively.

Competition

The market for our products is highly competitive. Our microturbines compete with existingtechnologies such as reciprocating engines and may also compete with emerging distributed generationtechnologies, including solar power, wind-powered systems, fuel cells and other microturbines. Manypotential customers rely on the utility grid for their electrical power. Many of our distributedgeneration competitors are large, well-established companies that derive competitive advantages fromproduction economies of scale, worldwide presence, brand recognition and greater resources which theycan devote to product development or promotion.