Embed Size (px)

Citation preview

34 EMERGING MARKETS FINANCE AND TRADE

34

Emerging Markets Finance and Trade, vol. 43, no. 3,May–June 2007, pp. 34–57.© 2007 M.E. Sharpe, Inc. All rights reserved.ISSN 1540–496X/2007 $9.50 + 0.00.DOI 10.2753/REE1540-496X430303

THOMAS LAGOARDE-SEGOT AND BRIAN M. LUCEY

Capital Market Integration in theMiddle East and North Africa

Abstract: This paper studies capital market integration in Middle Eastern and North Afri-can (MENA) countries and its implications for international portfolio investment alloca-tion. Starting with four cointegration methodologies, we significantly reject the hypothesisof a stable, long-run bivariate relationship between each of these markets and the Euro-pean Monetary Union (EMU), the United States, and a regional benchmark. This indicatesthe existence of significant diversification opportunities for three categories of investors(EMU, world, and regional investors). A recursive analysis based on Barari (2004) sug-gests that recently, the MENA markets have started to move toward international financialintegration. Investigating the effect of selected financial, economic, and political events onsuch a process, we extend the methodology and find that the markets react heterogeneouslyto the different categories of shocks. They should therefore not be treated as a bloc forglobal allocation purposes. Finally, after adjusting the integration levels by relative marketcapitalization, Israel and Turkey are the most promising markets in the region, followed byEgypt, Jordan, and Morocco. Tunisia and Lebanon seem to be lagging behind.

Key words: MENA markets, portfolio diversification, stock market integration, time-varyingmethods.

The decreasing benefits stemming from international portfolio diversification arenow well documented, as recent empirical studies have highlighted growingcomovements across developed and emerging financial markets. Having under-gone capital market reforms, the Middle Eastern and North African (MENA) coun-

Thomas Lagoarde-Segot ([email protected]) is a Ph.D. candidate at the Institute for Inter-national Integration Studies, School of Business, Trinity College Dublin, and at the Centerof International Economics and Finance (CEFI), Université de la Mediterranée, France.Brian M. Lucey is a senior lecturer at the School of Business Studies and Institute forInternational Integration Studies, Trinity College, Dublin.

MAY–JUNE 2007 35

tries are starting to appear on the global financial stage. As a percentage of grossdomestic product (GDP), market capitalization is now higher in the region (36percent) than it is in Eastern Europe (26 percent) or Latin America (24 percent).However, equity–market linkages and their subsequent portfolio implications re-main largely underexplored.

A first category of studies was based on standard cointegration analysis withvector error correction (VEC) modeling of weekly closing prices taken in localcurrencies. Neaime (2002) investigated a mix of MENA and Gulf CooperationCouncil (GCC) countries—Egypt, Jordan, Morocco, Turkey, Bahrain, Kuwait, andSaudi Arabia—from 1990 to 2000. He found that, unlike the GCC markets, whichremained segmented, financial integration of the MENA markets seemed to go alongwith a strong sensitivity to unidirectional shocks flowing from the United Statesand United Kingdom. However, he found no evidence of intraregional financialintegration. This echoes Erdal and Gunduz (2001), who investigated the interde-pendence of the Istanbul Stock Exchange with the Group of Seven (G7) equitymarkets and the stock markets of Israel, Jordan, Egypt, and Morocco before andafter the Asian crisis. Based on Granger causality tests, they rejected the hypothesisof significant linkages among MENA markets. They also found one cointegratingvector between the Istanbul Stock Exchange and the G7 markets, but no lead–lagrelationship. Gunduz and Omran (2001) carried out a similar study, in which thehypothesis of common stochastic trends among the markets of Turkey, Israel, Egypt,Morocco, and Jordan was rejected over the period 1997–2000. This first generationof empirical investigations suggested overall that, though the MENA capital mar-kets still appear to be segmented from one another, they seem individually inte-grated to global markets through stable bivariate long-run relationships.

However, it is now acknowledged that a wide battery of econometric tests ismuch needed to assess the complex nature of the financial integration process(Kearney and Lucey 2004). Hence, a second series of papers started to look at inte-gration of the MENA markets from different perspectives. For instance, Girard et al.(2003) implemented a state-dependent multivariate generalized autoregressive con-ditional heteroskedasticity (GARCH) methodology and found, in contrast to previ-ous studies, that the MENA markets are still highly segmented and thus providediversification benefits to the global investor. Another paper by Girard and Ferreira(2004) conducted a daily spillover analysis suggesting an increased sensitivity tointraregional exogenous shocks, but not to interregional shocks, from 1990 to 2001.Finally, Alper and Yilmaz (2004) highlighted the presence of volatility spilloversfrom major financial centers to the Turkish stock market from 1992 to 2004.

This paper makes several contributions to this literature. First, we use standard-ized exchange-converted U.S. dollar equity indices rather than local prices. Thismight be preferable to using local prices for cross-markets analyses (Hassan et al.2003). We also use a daily time series to incorporate the information on marketinteractions contained in high-frequency series (Voronkova 2004). Second, our setof econometric methodologies is designed to apprehend various facets of financial

36 EMERGING MARKETS FINANCE AND TRADE

integration. Testing for the existence of bivariate cointegrating vectors between theMENA markets and other financial centers, we complement the usual Johansen (1988)framework with more recent approaches developed by Gregory and Hansen (1996),Harris et al. (2002), and Breitung (2002). We then capture the time-varying nature ofintegration with a new recursive methodology developed in Barari (2004), beforeextending it to assess the effect of selected financial, economic, and political events.To our knowledge, our paper is the first effort of this type. Finally, we adjust integra-tion scores by levels of relative market capitalization to discuss the implications ofthe financial liberalization process for the allocation of international portfolios.

Data and Methodology

Data

We obtained our data from Datastream International. There are several possiblesources for MENA data: Morgan Stanley Capital International (MSCI), the Inter-national Finance Corporation (IFC), and national indexes. Taking the point of viewof the international investor, our data set relies on the Standard and Poor’s (S&P)IFC index in U.S. dollars. We use daily indices ranging from January 1, 1998, toNovember 16, 2004, including the stock markets of Morocco, Tunisia, Egypt, Leba-non, Jordan, Turkey, and Israel. However, we use national indexes for Tunisia andLebanon, as these countries are not included in the S&P database. Accounting forthese countries’ trade structure, we investigate equity-market integration towardthe European Monetary Union (EMU), the extended Arabic region—that is, theMENA and Gulf countries—and the rest of the world. Regional benchmarks arealso taken from the S&P IFC database. For the world markets, we take the MSCIWorld Free Index, which also proxies the U.S. stock market. Finally, market capi-talization indexes are obtained from the Arab Monetary Fund for individual coun-tries and from MSCI for regional benchmarks.

Risk and Returns in the MENA Markets

Table 1 reports risks and returns information after transforming the series by loga-rithm difference.

The average daily rate of return for all countries in the sample (0.014 percent) islower than the EMU’s (0.037 percent) and the regional benchmark’s (0.036 per-cent), but higher than the rest of the world’s (0.009 percent). For measures of risk,the sample’s average standard deviation (1.44 percent) is also lower than the EMU’s(1.75 percent) but higher than that of the rest of the world (0.96 percent). The Jarque–Bera tests reject the hypothesis of normality in all markets. The world and the EMUare left-skewed. By contrast, the unconditional distribution of returns is right-skewedin Egypt, Jordan, Lebanon, and Morocco. The coefficients of left-skewed countries—Israel, Tunisia, and Turkey—are smaller than those of the benchmarks.

MAY–JUNE 2007 37

Tabl

e 1

Des

crip

tive

Sta

tistic

s

Sta

ndar

dJa

rque

–Je

nsen

Sha

rpe

Mar

ket

Mea

nM

edia

nM

axim

umM

inim

umde

viat

ion

Ske

wne

ssK

urto

sis

Ber

ara

tios

ratio

s

Egy

pt0.

0155

06.

819

–6.0

521.

322

0.19

96.

829

1108

.43

–0.0

21–0

.072

Isra

el0.

0356

06.

454

–7.7

171.

289

–0.1

96.

159

757.

15–0

.004

–0.0

69Jo

rdan

0.04

560

8.48

1–8

.344

0.87

90.

532

17.8

7516

,625

.67

–0.0

15–0

.109

Leba

non

–0.0

343

06.

417

–5.5

271.

128

0.42

17.

143

1,33

6.3

–0.0

28–0

.162

ME

NA

0.03

680.

083

5.05

4–7

.248

1–0

.991

9.85

83,

809.

66–0

.004

–0.0

68M

oroc

co–0

.001

50

5.02

9–3

.983

0.67

80.

792

12.4

636,

881.

71–0

.023

–0.1

91Tu

nisi

a0.

0455

015

.022

–16.

592

1.08

–1.5

9980

.659

451,

580.

7–0

.017

–0.1

09Tu

rkey

–0.0

079

022

.669

–27.

022

3.74

1–0

.009

8.49

92,

260.

53–0

.01

–0.0

4W

orld

00.

057

4.60

3–3

.985

0.96

7–0

.063

4.63

120

0.09

1—

–0.1

25E

MU

0.03

70.

0352

8.02

2–1

0.55

1.75

7–0

.437

5.92

469

6.55

–0.0

01–0

.052

Not

es:

Jens

en a

nd S

harp

e ra

tios

are

calc

ulat

ed u

sing

the

U.S

. T-b

ill m

onth

ly r

ate

as a

pro

xy f

or th

e ri

sk-f

ree

rate

. The

wor

ld m

arke

t is

the

refe

renc

e m

arke

t for

Jen

sen

ratio

s.

38 EMERGING MARKETS FINANCE AND TRADE

Market performances in most countries, as measured by Jensen (1969) andSharpe (1966) ratios, are lower than in the EMU, but higher than in the rest of theworld. Lebanon and Morocco are exceptions, possibly because the two countriesdisplay negative mean returns along with Turkey. On the other end of the spec-trum, we find the highest returns in Jordan and Tunisia (0.045 percent), followedby Israel (0.035 percent) and Egypt (0.015 percent).

Overall, the results suggest that the MENA stock markets are rather volatile andpromise relatively high returns, in accordance with the emerging markets litera-ture (Bekaert and Harvey 1995, 1997; Goetzmann et al. 2000).

Empirical Methodology

We adopt a three-step empirical methodology. First, we use a variety of bivariatecointegration techniques between the stock markets and international benchmarksto check whether the presence of a stable, long-run relationship offsets the benefitsstemming from international diversification. Second, we investigate the time-varyingnature of equity market integration through a recursive and event-based analysisof an extended version of the Akdogan (1995; 1997) financial integration score.Third, we adjust the latter by market capitalization ratios to assess the portfolioallocation implications of market integration.

Cointegration Analysis

The Johansen (1988) cointegration analysis is now a standard methodology, easilyimplemented as long as the investigated series have a unit root and are I(1) pro-cesses. However, recent advances in econometric theory have refined the conceptof cointegration further. To fully assess the presence of common stochastic pro-cesses in our sample, we thus complement the Johansen analysis with three alter-native techniques.

The first of these techniques is the Gregory and Hansen (1996) residual-basedcointegration analysis. Results of Monte Carlo experiments (Campos et al. 1996;Gregory and Hansen 1996) have shown that when parameters shift, standard testsfor cointegration may lose power and falsely signal the absence of equilibrium inthe system. The Gregory–Hansen (1996) test therefore assumes the null hypoth-esis of no cointegration against the alternative hypothesis of cointegration with asingle structural break of unknown timing. The timing of the structural changeunder the alternative hypothesis is estimated endogenously. Gregory and Hansen(1996) suggest three alternative models to accommodate changes in the param-eters of the cointegration vector under the alternative. First, a level shift modelallows for the change in the intercept only (C):

t t ty m m j a y1 1 2 2 2.! "+ + + + # (1)

MAY–JUNE 2007 39

The second model, accommodating a trend in data, also restricts shifts only tothe change in level with a trend (C/T):

t t t t ty m m j b a y

t n1 1 2 2

1,..., .!$ "= + + + + #

%=& (2)

The third and most general specification allows for changes in both the inter-cept and slope of the cointegrating vector:

t t t ty m m j b a y

t n1 1 2 1 1 2 t ta y j

1,..., .! !$ " "= + + + + + #

%=& (3)

Finally, the dummy variable that captures the structural change is representedas

[ ] [ ]t t n t n0, ; 1, .' ! = ( ! > ! (4)

where t (0,1) is a relative timing of the change point. The trimming interval isusually taken to be (0.15n, 0.08n), as Andrews (1993) recommends. Models (1)–(3) are estimated sequentially with the break point changing over the interval t(0.15n, 0.85n). A number of tests of unit roots under structural stability are avail-able. Nonstationarity of the obtained residuals, expected under the null hypoth-esis, is checked by augmented Dickey–Fuller (ADF) and Phillips–Perron (PP) tests.Setting the test statistics (denoted as ADF * (Za*, Zt*)) to the smallest value of theADF (Za, Zt) statistics in the sequence, we select the value that presents the stron-gest evidence against the null hypothesis of no cointegration.

The second technique is the stochastic cointegration analysis of Harris et al.(2002), based on the observation that bond and stock market prices are often toovolatile to be compatible with a I(0)/I(1) framework. The stochastic cointegrationprocedure therefore replaces the stationarity requirement of a first difference inindividual series with a looser condition that the series are free of I(1) stochastictrend terms. Accordingly, the approach induces a nonlinear form of hetero-skedasticity that fits those of the data by giving rise to volatile behavior, in both thefirst differences of individual series and the cointegrating error term. The proce-dure is based on nested hypotheses. First, it tests the null of stochastic cointegrationagainst the alternative of no cointegration. Then, within stochastic cointegration, ittests the null of stationary cointegration against the heteroskedastic alternative.The analysis thus begins with the following regression model:

t t ty k x1 "= )+ + *+ µ (5a)

t t t tt tu e q w w ," "= + + (5b)

40 EMERGING MARKETS FINANCE AND TRADE

where the regression error term µt is composed of a stationary term et, an inte-grated term q"wt, and a heteroskedastic component vt"wt. Testing the null hypoth-esis of stochastic cointegration against the alternative of no cointegration requirestesting whether q = 0 in (5b). The null hypothesis is composite and encompassesboth stationary and heteroskedastic cointegration. To eliminate nuisance param-eters from the distribution of the partial sum process {mt}, the test is based on thestatistic

TNC t t kt k

S 1 ,,= += µ µ- (6)

where the lag k is allowed to increase with T. The variable SNC is asymptoticallyN(0,1). Then, if stochastic cointegration is established, H0 can be decomposedinto the null of stationary cointegration against the heteroskedastic alternativeby considering

t t t tu e w ,"= ++ (7)

where under the null, V(+t) = 0.The N(0,1) distributed statistic is based on

THC tt

S t 21 .== µ- (8)

Our third cointegration approach is based on Bierens’s (1997) criticism of tra-ditional cointegration methodologies, which have the disadvantage of construct-ing test statistics that require specifying the short-run dynamics or estimatingnuisance parameters. We therefore also implement Breitung’s (2002) tests for non-parametric cointegration. The process is as follows. Let {yt}1

T be an observed timeseries that can be decomposed as yt = µt + x, where µt = E[y(t)] = ."dt is the deter-ministic component, modeled as a linear combination of a vector of nonrandomregressors dt. Typical components of dt are a constant, a time trend, or dummyvariables. Assuming a nonzero mean of the form dt = ."zt, yt is regressed on zt andthe residuals µ[t = yt – .{"zt are used to form the variance ratio statistic,

T

tt

T T

tt

T U1 2

1

2

1

ˆˆ ,

ˆ

,

=

=

/ =µ

-

-(9)

where U{t = µ1 + ... + µ [t. Critical values are then simulated to test the null that yt isI(1) against the alternative yt 0 I(0).

MAY–JUNE 2007 41

Time-Varying Linkages Analysis

For the time-varying evolution of stock market linkages, our methodology is basedon computing the individual countries’ contribution to global and regional system-atic risk. Following Akdogan (1997) and Barari (2004), we consider the followinginternational risk decomposition model:

i g IR R ,= )+ * +1 (10)

where Ri is the rate of return on the ith country, Rg is the global rate of return, * isthe beta of the ith country with respect to the global index, and 1I is the error term.The variance of the ith country’s portfolio can then be decomposed into

( ) ( ) ( )i g IR R2Var Var Var= * + 1 (11)

gi i

i i i

RR

R R R

2VarVar VarVar Var Var

* 1= + (12)

i ip q1 .= + (13)

In Equation (13), pi measures the country’s contribution to worldwide systemicrisk and is the proposed measure of market integration. To fit our study’s purpose,we extend this methodology to the following multivariate framework:

i g g iR U U R1 1 2 2 ,= )+ * + * + * +1 (14)

where U1 and U2 are residuals from the following regressions:

MENA gR R U1= )+* + (15a)

EMU gR R U2.=)+* + (15b)

The variance of Ri can then be decomposed as

( )i g gR U U R2 21 1 2 2Var Var Var Var= * + * + * (16a)

g gi

i i i i

RR U U

R R R R

22 21 1 2 2

VarVar Var VarVar Var Var Var

** *= + + (16b)

a b c d1 ,= + + + (17)

42 EMERGING MARKETS FINANCE AND TRADE

where a, b, and c measure integration with the EMU, the MENA, and the world,respectively, and d represents unsystematic risk. To observe the dynamics of eq-uity market integration, we compute each of the integration scores over incremen-tal time windows, adding eighty observations at each iteration until the end of thesample is reached. We also analyze the effect of financial events, trade liberaliza-tion, infrastructure privatization, and political shocks with a simple moving aver-age methodology. Using each event considered as a breaking point, we divide thedata set into two subperiods and observe the sign of the difference between thepost- and pre-event integration scores. A positive sign suggests integration; a nega-tive sign suggests segmentation. Financial events are the Turkish crisis and theimplementation of the EMU. January 1, 1999, corresponds to the birth of the euro.November 21, 2000, the selected date for the Turkish financial crisis, correspondsto a dramatic increase of the O/N interest rates that resulted in a liquidity crisis inthe Turkish banking system. Turning to trade liberalization, we adopt a de factoapproach, using the dates of implementation of the trade agreement as breakingpoints. In all countries, we considered the dates for which the Euro-MediterraneanAssociation Agreements entered into force, except for Tunisia, where it happenedat the very beginning of the sample (January 3, 1998, i.e., sixty observations), andTurkey, where it dates back to 1963. Considering that the Agadir Agreements,which created a free trade area between Egypt, Tunisia, Jordan, and Morocco,only entered into force in January 2006, we adopted a de jure approach based on apositive reaction from the European Commission one week after the initialing ofthese agreements. This is done to better capture market anticipations. Turning toinfrastructure privatization announcements, the selected dates coincide with thosepublished in the World Bank–European Commission “Private Participation on Medi-terranean Infrastructure” review. These dates vary for different countries. For Mo-rocco, it corresponds to the renewal of a privatization program launched in 1993and comprising most infrastructures sectors except electricity. For Lebanon, itcorresponds to the adoption of the May 2000 Privatization Law, which establisheda Higher Privatization Council and set the framework for the privatization of state-owned enterprises. For Turkey, it corresponds to the adoption of a strategic law forprivatizations in the telecommunications, airline, and electricity sectors. For Jor-dan, it corresponds to the adoption of the “economic priority program,” whichextended previous privatization of the water and energy sectors. For Egypt, it cor-responds to the adoption of the “new privatization strategy,” which officially aimedat attracting domestic and foreign funds for investment. For Tunisia, it correspondsto a series of twenty-six privatizations, mainly in the construction sector. For Is-rael, it corresponds to the privatization of the national airline El Al. Finally, politi-cal events include the beginning of the second Intifada in September 2000, the2001 World Trade Center attacks, and the invasion of Iraq in March 2003 (seeTable 2).

MAY–JUNE 2007 43

Portfolio Allocation Implications

Weak integration does not necessarily imply diversification opportunities if themarkets are thinly traded. Following Akdogan (1995; 1997), we therefore adjusteach score by the corresponding measure of country contribution to capitalizationin the benchmark area. The lower the contribution to systemic risk relative to com-pared market capitalization, the higher will be the diversification benefits. Thethree adjusted financial integration indicators below are therefore negatively pro-portional to diversification benefits:

Table 2

Moving Average Analysis: Selected Events

Financial events

January 1, 1999 EMU creationNovember 21, 2000 Turkish crisis

Trade liberalization

March 1, 2000 EuroMed, MoroccoJune 1, 2000 EuroMed, IsraelJanuary 6, 2001 EuroMed, EgyptJanuary 5, 2002 EuroMed, JordanJanuary 3, 2003 EuroMed, LebanonJanuary 16, 2003 Agadir agreements

Infrastructure privatization

December 31, 1998 MoroccoJanuary 5, 2000 LebanonDecember 14, 2000 TurkeyNovember 23, 2001 JordanDecember 16, 2001 EgyptJanuary 24, 2002 TunisiaJanuary 3, 2003 Israel

Political events

September 1, 2000 Second IntifadaSeptember 11, 2001 World Trade Center attacksMarch 17, 2003 Iraq invasion

44 EMERGING MARKETS FINANCE AND TRADE

i iEMU iEMUi EMU

U MCiadja W W

R MC

21 1VarVar

*= = (16a)

i iMENA iMENAi MENA

U MCiadjb W W

R MC

22 2VarVar

*= = (16b)

g gi iUS iUS

i US

R MCiadjc W W

R MC

2 Var.

Var

*= = (16c)

Results and Analysis

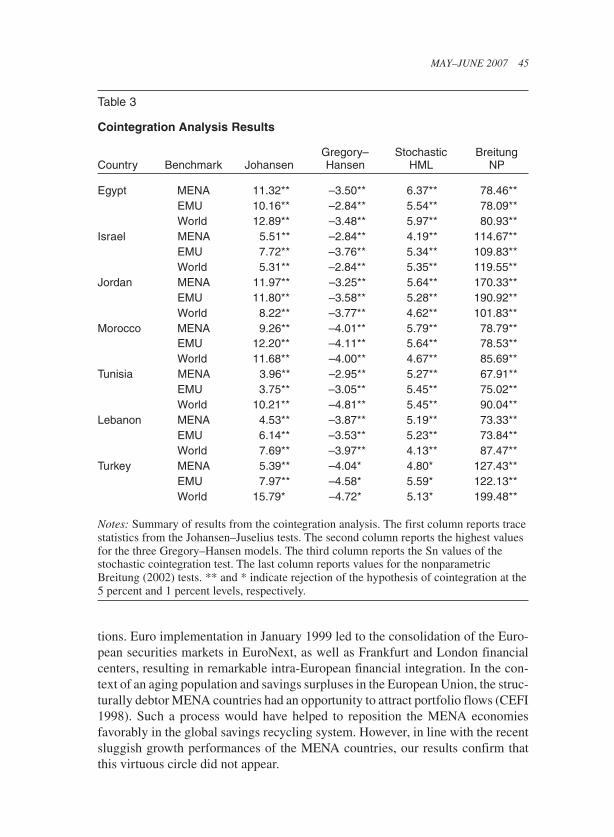

After the usual unit root analysis, all series are characterized as I(1) processes andwe proceed to our cointegration tests. The null hypothesis of cointegration withthe EMU, the world markets, and the local regional benchmark is significantlyrejected for all countries. By giving no evidence of a stable, long-run relationshipbetween the MENA stock markets and the various international benchmarks, theresults clearly indicate that the studied markets provide some potential for interna-tional diversification (see Table 3).

Turning to the dynamics of the linkages, the recursive analysis reveals that, thoughsegmentation from the MENA benchmark (see Figures 1–7) seems to increase formost countries—Egypt, Jordan, Morocco, Tunisia, and Lebanon—the process ofsegmentation in relation to the EMU is stabilized in Jordan (since 2000) and inTurkey and Tunisia (since 2001). The process of financial integration toward theEMU seems to have already begun for Israel and Lebanon (since 2001), Egypt (since2002), and Morocco (since 2003). Moreover, except for Jordan and Tunisia, ourplots display a growing integration to the world for most countries: Morocco, Leba-non, and Turkey (since 1999), and Egypt (since 2001). Compared to previous stud-ies investigating equity market integration in Asia, the finding reinforces the viewthat financial integration is primarily a global phenomenon (Chuah 2004). Regionalfinancial integration processes, such as those occurring between Eastern Europe andthe EMU (Voronkova 2004), are possible but conditioned on inserting the integra-tion agenda into a wider political project (Eichengreen and Pempel 2002).

In any case, without common stochastic processes, evidence favoring financialintegration does not threaten the benefits derived from international diversifica-tion in the MENA region. It should rather be seen as reflecting these markets’gradual maturation through intensified international linkages. The next step of theanalysis is therefore to shed light on the effect of selected financial, economic, andpolitical events on this emerging integration process (see Table 4).

The overall difference between post-EMU- and pre-EMU-integration MENAscores appears to be negative over the study period. This has significant implica-

MAY–JUNE 2007 45

Table 3

Cointegration Analysis Results

Gregory– Stochastic BreitungCountry Benchmark Johansen Hansen HML NP

Egypt MENA 11.32** –3.50** 6.37** 78.46**EMU 10.16** –2.84** 5.54** 78.09**World 12.89** –3.48** 5.97** 80.93**

Israel MENA 5.51** –2.84** 4.19** 114.67**EMU 7.72** –3.76** 5.34** 109.83**World 5.31** –2.84** 5.35** 119.55**

Jordan MENA 11.97** –3.25** 5.64** 170.33**EMU 11.80** –3.58** 5.28** 190.92**World 8.22** –3.77** 4.62** 101.83**

Morocco MENA 9.26** –4.01** 5.79** 78.79**EMU 12.20** –4.11** 5.64** 78.53**World 11.68** –4.00** 4.67** 85.69**

Tunisia MENA 3.96** –2.95** 5.27** 67.91**EMU 3.75** –3.05** 5.45** 75.02**World 10.21** –4.81** 5.45** 90.04**

Lebanon MENA 4.53** –3.87** 5.19** 73.33**EMU 6.14** –3.53** 5.23** 73.84**World 7.69** –3.97** 4.13** 87.47**

Turkey MENA 5.39** –4.04* 4.80* 127.43**EMU 7.97** –4.58* 5.59* 122.13**World 15.79* –4.72* 5.13* 199.48**

Notes: Summary of results from the cointegration analysis. The first column reports tracestatistics from the Johansen–Juselius tests. The second column reports the highest valuesfor the three Gregory–Hansen models. The third column reports the Sn values of thestochastic cointegration test. The last column reports values for the nonparametricBreitung (2002) tests. ** and * indicate rejection of the hypothesis of cointegration at the5 percent and 1 percent levels, respectively.

tions. Euro implementation in January 1999 led to the consolidation of the Euro-pean securities markets in EuroNext, as well as Frankfurt and London financialcenters, resulting in remarkable intra-European financial integration. In the con-text of an aging population and savings surpluses in the European Union, the struc-turally debtor MENA countries had an opportunity to attract portfolio flows (CEFI1998). Such a process would have helped to reposition the MENA economiesfavorably in the global savings recycling system. However, in line with the recentsluggish growth performances of the MENA countries, our results confirm thatthis virtuous circle did not appear.

46 EMERGING MARKETS FINANCE AND TRADE

Figure 1. Egypt—Recursive Analysis

Figure 2. Israel—Recursive Analysis

MAY–JUNE 2007 47

Figure 3. Jordan—Recursive Analysis

Figure 4. Morocco—Recursive Analysis

48 EMERGING MARKETS FINANCE AND TRADE

Figure 5. Tunisia—Recursive Analysis

Figure 6. Lebanon—Recursive Analysis

MAY–JUNE 2007 49

Figure 7. Turkey—Recursive Analysis

The 2000–2001 Turkish crisis was another major financial event. Starting inNovember 2000 with a liquidity crisis in the banking system, the crisis not onlydestabilized the Istanbul Stock Exchange from February 2001 onward, but alsoaggravated international perceptions of systemic risk, leading to negative anticipa-tions and trends in the global markets (Akyüz and Boratav 2003). Our resultssuggest that the crisis reinforced both intraregional and global linkages within theMENA capital markets. Defining financial contagion as an increase in shock sen-sibility in the aftermath of a foreign financial crisis (Forbes and Rigobon 2001),the latter result could constitute preliminary evidence of crisis vulnerability in theMENA region. This would be consistent with recent experience in the emergingmarkets of Latin America, East Asia, and Eastern Europe (Corsetti et al. 2005).Investigating crisis transmission mechanisms to the MENA markets might there-fore be necessary in the future.

Turning to the effect of regional economic integration, it appears that both theentry into force of trade liberalization agreements and the implementation of in-frastructure privatization programs have reinforced financial integration with theglobal market, but neither with the EMU nor with the MENA benchmark. Thisechoes recent work on Asian equity markets suggesting that financial integrationcan be affected by domestic policies and trade initiatives, but remains global innature (Chuah 2004; Vo 2005). It can also be connected to previous work in politi-cal economy that suggests that trade liberalization initiatives do not necessarilyresult in greater regional financial integration, unless some degree of political andinstitutional convergence has been reached (Park 2002).

50 EMERGING MARKETS FINANCE AND TRADE

Tabl

e 4

Mov

ing

Ave

rage

Ana

lysi

s

Egy

ptIs

rael

Jord

anM

oroc

coTu

nisi

aLe

bano

nTu

rkey

Pos

itive

Neg

ativ

e

Cre

atio

n of

the

EM

UE

MU

–0.9

2–1

.86

–2.8

40.

40–3

.31

–0.9

9–2

.30

16

ME

NA

–1.6

91.

29–1

.55

–0.6

7–2

.35

–2.6

2–0

.12

16

Wor

ld2.

830.

62–1

.00

1.35

–0.3

11.

363.

125

1Tu

rkis

h cr

isis

EM

U–1

.00

1.33

–0.1

40.

141.

611.

661.

095

1M

EN

A2.

560.

600.

541.

331.

171.

91–0

.06

51

Wor

ld2.

03–0

.48

–0.2

40.

81–1

.20

1.67

–0.8

13

4E

uroM

ed a

gree

men

tsE

MU

–1.3

3–0

.23

–1.7

30.

19N

A0.

54N

A3

2M

EN

A2.

990.

610.

230.

09N

A–2

.23

NA

41

Wor

ld2.

040.

222.

310.

82N

A–0

.41

NA

41

Aga

dir a

gree

men

tsE

MU

–0.4

1N

A–2

.10

–0.4

90.

19N

AN

A1

3M

EN

A1.

14N

A–0

.04

0.30

–0.6

4N

AN

A2

2W

orld

2.04

NA

2.23

0.55

1.52

NA

NA

40

Infr

astr

uctu

re p

rivat

izat

ion

EM

U–2

.68

–0.3

2–1

.38

0.44

1.37

1.72

1.13

43

ME

NA

2.46

–1.1

80.

95–0

.44

–0.2

70.

18–0

.08

34

Wor

ld2.

150.

881.

461.

371.

041.

99–0

.80

61

MAY–JUNE 2007 51

Intif

ada

EM

U0.

11–0

.21

–1.4

50.

160.

051.

56–0

.15

43

ME

NA

–1.2

20.

61–0

.90

0.10

1.79

–0.1

6–0

.37

34

Wor

ld2.

490.

21–1

.52

0.79

–0.0

92.

112.

705

2W

orld

Tra

de C

ente

r at

tack

sE

MU

–2.7

10.

92–1

.06

–0.7

11.

79–0

.26

0.32

34

ME

NA

3.18

–0.2

60.

901.

580.

462.

840.

086

1W

orld

2.25

0.35

1.36

1.14

0.39

1.33

–0.9

16

1In

vasi

on o

f Ira

qE

MU

–0.3

6–0

.33

–2.0

9–0

.50

0.29

–0.5

5–0

.63

16

ME

NA

1.17

–1.0

30.

010.

32–0

.39

2.21

–0.1

34

3W

orld

2.72

0.60

2.22

0.43

1.46

0.37

1.81

70

Not

es:

The

first

col

umn

repo

rts

the

even

ts a

nd th

e re

gion

al b

ench

mar

k un

der

anal

ysis

. In

colu

mns

2 to

8, f

or e

ach

coun

try,

we

repo

rt th

edi

ffer

ence

bet

wee

n po

stev

ent a

nd p

re-e

vent

inte

grat

ion

scor

es. T

hen,

for

each

eve

nt a

nd b

ench

mar

k, c

olum

ns 9

and

10

give

the

over

all n

umbe

rof

pos

itive

—th

at is

, int

egra

tion—

and

nega

tive—

that

is, s

egm

enta

tion—

resu

lts.

52 EMERGING MARKETS FINANCE AND TRADE

Finally, the successive increases of political risk in the region seem to have hadconflicting effects, as they led to integration with world and regional markets, butalso segmentation from the EMU. These results highlight the widely accepted co-existence of multiple perceptions of political risk among categories of investors.American Investment Market Research (2005, p. 12) characterizes emerging marketinvestments as “bets on emergence,” in which hardly measurable country-specificrisks go along with prospects of growth-driven, higher-than-average returns.

Overall, the moving average analysis suggests that the MENA markets are sen-sitive to financial, economic, and political events. However, this sensitivity seemsto take different forms. Investors should therefore avoid treating these marketshomogeneously for global allocation purposes. To further assess each country’sdiversification potential, we observe the adjusted integration scores from the pointof view of EMU, world, and MENA investors (see Tables 5–7). This permits us torank the MENA countries according to their expected diversification potential.Countries are ranked in a similar way for all three categories of investors. A headgroup of countries gathers Israel and Turkey. A second group consists of Egypt,Morocco, and Jordan. The third and least advantageous group consists of Tunisiaand Lebanon. Portfolio choice differences among investors are only minor: Tur-key seems preferable to Israel for MENA investors, and Tunisia to Lebanon forEMU investors.

Conclusion

This paper studied equity-market integration in the MENA countries with an em-phasis on international portfolio investment allocation. Using four cointegrationmethodologies, we significantly rejected the hypothesis of a stable, long-run bi-variate relation between each of these markets and the EMU, the United States,and a regional benchmark. This indicated the existence of significant diversifica-tion opportunities for the three categories of investors mentioned above. A time-varying analysis based on Barari (2004) suggested that the MENA markets haverecently started moving toward international financial integration. Extending thismethodology to capture the effects of financial, economic, and political events insuch a process, we found that these markets display heterogeneous reactions. Theyshould therefore not be treated as a bloc for global allocation purposes. Finally,adjusting these scores by market capitalization highlighted that Israel and Turkeyare the most appealing markets in the region, followed by Egypt, Jordan, andMorocco. Tunisia and Lebanon seem to be lagging behind. Future research couldinvestigate the actual performance of a MENA-inclusive portfolio based on profit-ability simulations, or extend the bivariate comovement analysis by including GCCcountries—Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and United Arab Emir-ates—on a longer time period, comparing results with local prices. We might alsoassess more robustly the nature of the shock transmission mechanisms within theregion, especially in the event of an international financial crisis.

MAY–JUNE 2007 53

Tabl

e 5

Inte

grat

ion

with

the

EM

U

Dat

eE

gypt

Isra

elJo

rdan

Mor

occo

Tuni

sia

Leba

non

Turk

ey

Apr

il 21

, 199

83.

505

1.87

14.

082

1.21

85.

844

1.74

81.

332

Aug

ust

11,

1998

1.22

01.

273

1.46

30.

661

6.30

31.

429

2.56

2D

ecem

ber

1, 1

998

2.05

33.

121

4.28

51.

603

3.92

02.

867

4.11

7M

arch

23,

199

92.

356

3.00

14.

179

1.67

02.

365

1.76

63.

713

July

13,

199

91.

772

2.50

93.

921

1.62

81.

738

1.09

73.

386

Nov

embe

r 2,

199

90.

966

2.13

73.

007

1.92

61.

681

0.66

42.

620

Febr

uary

22,

200

01.

056

1.68

42.

945

2.07

71.

287

0.65

92.

146

June

13,

200

01.

056

1.68

42.

945

2.07

71.

287

0.65

92.

146

Oct

ober

3, 2

000

1.63

20.

691

2.00

42.

064

0.38

10.

679

1.71

5Ja

nuar

y 23

, 200

12.

189

0.50

42.

237

2.34

70.

174

0.99

91.

231

May

15,

200

12.

868

0.50

82.

418

2.51

40.

114

1.65

11.

383

Sep

tem

ber

4, 2

001

3.27

50.

498

2.40

72.

456

0.11

12.

121

1.55

0D

ecem

ber

25, 2

001

3.01

60.

488

2.36

72.

187

0.10

62.

168

1.46

0A

pril

16, 2

002

1.42

20.

581

2.33

41.

664

0.15

91.

375

1.34

7A

ugus

t 6, 2

002

0.84

40.

652

2.42

31.

277

0.24

50.

959

1.10

4N

ovem

ber

26, 2

002

0.70

80.

721

2.39

51.

093

0.31

00.

843

1.10

2M

arch

18,

200

30.

657

0.74

32.

415

1.04

70.

338

0.82

91.

132

July

8, 2

003

0.62

00.

846

2.46

21.

083

0.39

30.

817

1.07

6O

ctob

er 2

8, 2

003

0.66

70.

951

2.34

71.

241

0.45

20.

867

1.10

4Fe

brua

ry 1

7, 2

004

0.76

31.

033

2.11

11.

438

0.51

20.

958

1.22

8Ju

ne 8

, 200

40.

894

1.13

02.

083

1.70

40.

590

1.10

51.

389

Sep

tem

ber

28, 2

004

0.94

61.

210

1.96

51.

821

0.64

51.

169

1.54

4N

ovem

ber

16, 2

004

0.97

11.

281

1.90

91.

923

0.68

01.

223

1.62

9

Mea

n1.

542

1.26

62.

639

1.68

31.

289

1.24

61.

827

Wi

0.00

60.

013

0.00

20.

003

0.00

10.

001

0.01

4A

djus

ted

244.

354

(3)

100.

023

(1)

1,64

6.96

7 (5

)56

4.71

5 (4

)2,

190.

690

(6)

2,39

4.55

8 (7

)12

6.33

8 (2

)

Not

es:

Wi c

orre

spon

ds to

eac

h co

untr

y-m

arke

t cap

italiz

atio

n re

lativ

e to

that

of

the

benc

hmar

k ar

ea. N

umbe

rs in

par

enth

eses

den

ote

coun

try

rank

.

54 EMERGING MARKETS FINANCE AND TRADE

Tabl

e 6

Inte

grat

ion

with

ME

NA

Dat

eE

gypt

Isra

elJo

rdan

Mor

occo

Tuni

sia

Leba

non

Turk

ey

Apr

il 21

, 199

80.

920

0.52

51.

545

0.48

73.

214

1.96

40.

672

Aug

ust

11,

1998

1.94

01.

746

1.77

20.

994

10.6

592.

985

0.77

3D

ecem

ber

1, 1

998

2.08

41.

057

2.26

61.

418

5.25

23.

269

0.29

1M

arch

23,

199

91.

812

1.49

72.

639

2.19

92.

562

2.56

60.

405

July

13,

199

91.

693

1.24

52.

653

2.17

91.

601

1.57

30.

426

Nov

embe

r 2,

199

91.

923

1.35

22.

716

1.95

20.

590

1.59

40.

538

Febr

uary

22,

200

02.

058

1.04

22.

620

2.05

80.

434

1.55

40.

458

June

13,

200

02.

058

1.04

22.

620

2.05

80.

434

1.55

40.

458

Oct

ober

3, 2

000

0.78

21.

043

0.97

61.

464

0.55

81.

066

0.36

7Ja

nuar

y 23

, 200

10.

342

1.35

50.

617

0.92

71.

009

0.67

40.

547

May

15,

200

10.

173

1.45

40.

517

0.76

81.

512

0.32

30.

466

Sep

tem

ber

4, 2

001

0.09

91.

603

0.52

60.

577

1.61

50.

194

0.36

3D

ecem

ber

25, 2

001

0.07

81.

640

0.51

90.

476

1.67

40.

152

0.31

3A

pril

16, 2

002

0.11

01.

452

0.50

80.

474

1.24

50.

197

0.33

1A

ugus

t 6, 2

002

0.10

81.

415

0.50

20.

406

1.21

00.

198

0.32

6N

ovem

ber

26, 2

002

0.10

41.

356

0.50

80.

357

1.15

70.

199

0.31

2M

arch

18,

200

30.

098

1.35

10.

516

0.33

81.

221

0.19

50.

310

July

8, 2

003

0.09

31.

446

0.51

80.

342

1.31

40.

193

0.29

2O

ctob

er 2

8, 2

003

0.09

71.

738

0.58

50.

426

1.63

30.

198

0.26

1Fe

brua

ry 1

7, 2

004

0.12

02.

044

0.77

20.

580

1.95

60.

214

0.25

7Ju

ne 8

, 200

40.

160

2.30

30.

909

0.79

12.

264

0.27

70.

254

Sep

tem

ber

28, 2

004

0.23

42.

359

1.07

91.

041

2.42

30.

404

0.27

0N

ovem

ber

16, 2

004

0.28

92.

334

1.16

11.

120

2.48

60.

465

0.28

4

Mea

n0.

755

1.49

61.

263

1.01

92.

088

0.95

70.

390

Wi

0.16

70.

397

0.05

10.

095

0.01

90.

016

0.43

8A

djus

ted

4.51

45 (

3)3.

763

(2)

24.8

01 (

5)10

.716

(4)

112.

447

(7)

59.8

10 (

6)0.

891

(1)

Not

es:

Wi

corr

espo

nds

to e

ach

coun

try-

mar

ket c

apita

lizat

ion

rela

tive

to th

at o

f th

e be

nchm

ark

area

. In

the

last

row

, num

bers

in p

aren

thes

es d

enot

e co

untr

yra

nk.

MAY–JUNE 2007 55

Tabl

e 7

Inte

grat

ion

with

the

Wor

ld

Dat

eE

gypt

Isra

elJo

rdan

Mor

occo

Tuni

sia

Leba

non

Turk

ey

Apr

il 21

, 199

82.

515

1.99

84.

886

2.60

27.

591

1.95

00.

251

Aug

ust

11,

1998

0.33

11.

962

1.94

62.

296

5.48

10.

837

0.53

7D

ecem

ber

1, 1

998

0.44

01.

213

1.31

20.

961

1.35

40.

895

0.84

9M

arch

23,

199

90.

400

0.75

41.

861

1.22

61.

573

0.31

40.

125

July

13,

199

90.

338

1.32

42.

139

1.21

11.

998

0.14

10.

327

Nov

embe

r 2,

199

90.

224

1.53

11.

830

1.41

62.

034

0.09

60.

525

Febr

uary

22,

200

00.

449

1.92

81.

941

1.70

62.

560

0.13

91.

713

June

13,

200

00.

449

1.92

81.

941

1.70

62.

560

0.13

91.

713

Oct

ober

3, 2

000

0.36

92.

365

0.87

51.

437

3.56

40.

138

3.05

5Ja

nuar

y 23

, 200

10.

247

2.32

60.

682

1.15

13.

448

0.12

53.

050

May

15,

200

10.

257

2.18

20.

685

1.10

52.

534

0.13

83.

378

Sep

tem

ber

4, 2

001

0.32

91.

918

0.74

11.

090

1.92

10.

176

3.99

7D

ecem

ber

25, 2

001

0.64

41.

673

0.82

01.

288

1.32

40.

343

4.98

8A

pril

16, 2

002

0.97

61.

597

0.80

41.

383

1.11

80.

473

4.77

0A

ugus

t 6, 2

002

1.43

91.

697

0.84

21.

576

1.04

00.

690

4.62

5N

ovem

ber

26, 2

002

1.87

11.

783

1.05

21.

856

1.01

60.

964

3.91

3M

arch

18,

200

32.

148

1.86

71.

233

2.00

41.

047

1.12

63.

397

July

8, 2

003

2.33

51.

770

1.20

22.

073

1.01

41.

231

3.33

6O

ctob

er 2

8, 2

003

2.41

81.

649

0.89

32.

090

0.96

61.

277

3.27

8Fe

brua

ry 1

7, 2

004

2.42

91.

532

0.65

52.

091

0.94

21.

271

3.23

0Ju

ne 8

, 200

42.

424

1.42

50.

534

2.07

30.

926

1.26

13.

213

Sep

tem

ber

28, 2

004

2.40

41.

360

0.46

22.

051

0.90

41.

257

3.18

5N

ovem

ber

16, 2

004

2.39

81.

353

0.43

52.

048

0.90

01.

257

3.18

0

Mea

n1.

210

1.70

21.

294

1.67

12.

079

0.70

62.

636

Wi

0.00

20.

004

0.00

00.

001

0.00

00.

000

0.00

4A

djus

ted

641.

830

(3)

450.

271

(1)

2,71

6.27

4 (5

)1,

885.

465

(4)

11,9

09.5

26 (

7)4,

653.

529

(6)

613.

111

(2)

Not

es:

Wi c

orre

spon

ds to

eac

h co

untr

y-m

arke

t cap

italiz

atio

n re

lativ

e to

that

of

the

benc

hmar

k ar

ea. N

umbe

rs in

par

enth

eses

den

ote

coun

try

rank

.

56 EMERGING MARKETS FINANCE AND TRADE

References

Akdogan, H. 1995. The Integration of International Capital Markets: Theory and Empiri-cal Evidence. Cheltenham, UK: Edward Elgar.

———. 1997. “International Security Selection Under Segmentation: Theory and Applica-tion.” Journal of Portfolio Management (Fall): 82–92.

Alper, C.E., and K. Yilmaz. 2004. “Volatility and Contagion: Evidence from the IstanbulStock Exchange.” Economic Systems 28, no. 4: 353–367.

American Investment Market Research. 2005. Investing in Emerging Markets. Charlottesville,VA: CFA Publications.

Andrews, D.W.K. 1993. “Tests for Parameter Instability and Structural Change with Un-known Change Point.” Econometrica 61, no. 4: 821–856.

Barari, M. 2004. “Equity Market Integration in Latin America: A Time Varying IntegrationScores Analysis.” International Review of Financial Analysis 13, no. 5: 649–658.

Bekaert, G., and C.R. Harvey. 1995. “Time-Varying World Market Integration.” Journal ofFinance 50, no. 2: 403–444.

———. 1997. “Emerging Equity Market Volatility.” Journal of Financial Economics 43,no. 1: 29–77.

Bierens, H.J. 1997. “Nonparametric Cointegration Analysis.” Journal of Econometrics 77,no. 2: 379–404.

Boratav, J., and Y. Akyüz. 2003. “The Making of the Turkish Financial Crisis.” World De-velopment 31, no. 9: 1549–1566.

Breitung, J. 2002. “Nonparametric Tests for Unit Roots and Cointegration.” Journal ofEconometrics 108, no. 2: 343–363.

Campos, J.; N.R. Ericcson; and D.F. Hendry. 1996. “Cointegration Tests in the Presence ofStructural Breaks.” Journal of Econometrics 70, no. 1: 187–220.

Centre d’Economie et de Finance Internationales (CEFI). 1998. L’euro et la Méditerranée.La Tour d’Aigues, France: Editions de l’Aube.

Chuah, H.L. 2004. “Are International Equity Market Co-movements Driven by Real orFinancial Integration?” Working paper, Department of Economics, Duke University,Durham, NC, July.

Corsetti, G.; M. Pericoli; and M. Sbracia. 2005. “Some Contagion, Some Interdependence,More Pitfalls in Tests of Financial Contagion.” Journal of International Money andFinance 4, no. 8: 1177–1199.

Eichengreen, B., and T.J. Pempel. 2002. “Why Has There Been Less Financial Integrationin East Asia Than in Europe?” Working paper, Institute of East Asian Studies and theInstitute of European Studies, Cornell University.

Erdal, F., and L. Gunduz. 2001. “An Empirical Investigation of the Interdependence ofIstanbul Stock Exchange with Selected Stock Markets.” Global Business and Technol-ogy Association International Conference Proceedings, Turkey, July (available at http://ozgur.beykent.edu.tr/~lokma/p_gbata.pdf).

Forbes, K.J., and R. Rigobon. 2001. “Measuring Contagion: Conceptual and EmpiricalIssues.” In International Financial Contagion: How It Spreads and How It Can beStopped, ed. S. Claessens and K.J. Forbes, pp. 43–66. Dordrecht: Kluwer Academic.

Girard, E., and E.J. Ferreira. 2004. “On the Evolution of Inter- and Intraregional Linkagesto Middle East and North African Capital Markets.” Quarterly Journal of Business &Economics 43, nos. 1–2 (Winter–Spring): 21–43.

Girard E.; M. Omran; and T. Zaher. 2003. “On Risk and Return in MENA Capital Markets.”International Journal of Business 8, no. 3: 285–314.

MAY–JUNE 2007 57

Goetzmann, W.; L. Li; and K.G. Rouwenhorst. 2000. “Long-Term Global Market Correla-tions.” Working Paper 00-60, Yale International Center for Finance, New Haven.

Gregory, A.W., and B.E. Hansen. 1996. “Residual-Based Tests for Cointegration in Modelswith Regime Shifts.” Journal of Econometrics 70, no. 1: 99–126.

Gunduz, L., and M. Omran. 2001. “Stochastic Trends and Stock Prices in Emerging Mar-kets: The Case of the Middle East and North Africa Region.” ISE Review 5, no. 17:1–23.

Harris, D., B. McCabe, and S. Leybourne. 2002. “Stochastic Cointegration: Estimation andInference.” Journal of Econometrics 111, no. 2: 363–384.

Hassan, M.H., C. Maroney, H. Monir El-Sadi, and A. Telfah. 2003. “Country Risk andStock Market Volatility, Predictability, and Diversification in the Middle East and Af-rica.” Economic Systems 27, no. 1: 63–82.

Jensen, M.C. 1969. “Risk: The Pricing of Capital and the Evaluation of Investment Portfo-lios.” Journal of Business 42, no. 2: 167–247.

Johansen, S. 1988. “Statistical Analysis of Cointegration Vectors.” Journal of EconomicDynamics and Control 12, nos. 2–3: 231–254.

Kearney, C., and B. Lucey. 2004. “International Equity Market Integration.” InternationalReview of Financial Analysis 13, no. 5: 571–583.

Neaime, S. 2002. “Liberalization and Financial Integration of MENA Stock Markets.” Pa-per presented at the 9th Economic Research Forum meeting, American University inSharja, UAE, October.

Park, Y.C. 2002. “Financial Liberalization and Economic Integration in East Asia.” KoreaUniversity, Department of Economics.

Sharpe, W.F. 1966: “Mutual Fund Performance.” Journal of Business 39, no. 1 (January):119–138.

Vo, X.V. 2005. “Determinants of International Financial Integration.” Working paper,Australasian Financial Research Group–University of Western Sydney, Australia.

Voronkova, S. 2004. “Equity Market Integration in Central European Emerging Markets: ACointegration Analysis with Shifting Regimes.” International Review of Financial Analy-sis 13, no. 5: 633–647.

To order reprints, call 1-800-352-2210; outside the United States, call 717-632-3535.