Embed Size (px)

DESCRIPTION

This report, the first in a series analyzing middle-market equity capital formation, provides insight into the topics influencing middle-market businesses access to capital.

Citation preview

May 2014A CohnReznick LLP Report

Perspectives on Middle-Market Equity Capital

IPO On-Ramp Accelerates Capital Formation While Small Issuers Continue to Stall

game chang • ernoun: a newly introduced element or factor that significantly changes an existing mindset, situation, or activity

A CohnReznick Report 3

Today’s Financing Environment: A “Risk On” Posture...............................1

Legislation Opens the Capital Spigot........................................................3

Analysis of Capital Formation in 2014―What Have We Discovered?.......7

Preparing to Take Advantage of Equity Markets....................................15

What’s Next?..............................................................................................17

Contributors and Upcoming Events.........................................................18

Appendix....................................................................................................19

About CohnReznick’s Capital Markets Group........................................30

Table of Contents

Preface

In this report―the fi rst in a series analyzing middle-market equity capital formation―CohnReznick demonstrates the positive impact the Jumpstart Our Business Startups (JOBS) Act has had on middle-market businesses (defi ned in this report as those businesses with market capitalization of $100 million to $1 billion) in the fi rst quarter of 2014.

It is clear that economic and regulatory forces are enhancing the potential for middle-market companies to access capital. Equity capital markets had robust activity in the fi rst quarter, as issuers rushed to take advantage of the lower hurdles offered by the JOBS Act and the continued strength of the broader market. We anticipate the high levels of middle-market fi nancing activity to continue apace throughout 2014 as there is evident investor appetite both for IPOs and for seasoned issuers.

Unfortunately, our analysis of Q1 transactions reveals a continued dearth of small IPOs (under $50 million in proceeds). The lack of capital market participation in this sector threatens future middle-market growth and demonstrates that legislators and regulators have more work to do. We expect to see a steady stream of pro-equity capital formation legislation from Congress and enactments by the U.S. Securities and Exchange Commission to address this concern and further fuel middle-market growth.

For these reasons, CohnReznick is optimistic in our outlook for equity capital formation over the next 12 months. The window of opportunity for middle-market companies considering an IPO or follow-on transaction has cracked open, and with additional legislative and regulatory action expected, soon it will open wide enough to be a game changer for middle-market growth.

.

Dom EspositoPartner, National Practiceand Growth Director

“The window of opportunity for middle-market companies considering an IPO or follow-on transaction has cracked open, and with additional legislative and regulatory action expected, soon it will opened wide enough to be a game changer for middle-market growth.”

A CohnReznick Report 1

Today’s Financing Environment: A “Risk On” Posture

CohnReznick believes the financing environment will remain opportune for middle-market business owners. In the equity markets, the Federal Reserve, whose policies have contributed demonstrably to the stock market’s rally over the past few years, bears close watching. Even if the Fed’s liquidity taps tighten, we believe the market will benefit from continued regulatory and legislative reform (as detailed below) designed to facilitate capital formation for small and middle-market companies.

• Debt Markets Attractive but Trading Lower – Interest rates may tick up in response to modestly better growth, but they will remain low compared to historical norms, continuing the attractive market for borrowers. While an improved economy typically leads to an increased appetite to lend to smaller and middle-market companies, there is a massive deleveraging of the banking system underway in the wake of the Credit Crisis and the Dodd Frank Act. Banking regulations that raise reserve requirements will result in a drive to increase equity on the balance sheets of lending institutions. This, in turn, decreases the amount of capital that banks can earmark for investment. What does this mean for middle-market companies? CohnReznick expects the regulations may continue to limit the supply of debt capital, particularly for smaller companies.

• Capital Shift into Stocks Drives Equity Capital Formation – As interest rates tick up, bond portfolios will be marked down. Against this backdrop, investors may shift assets into stocks. This would help propel the equity new issue market forward. In addition, as economic conditions improve, appetite for risk-taking should also improve, which bodes well for the equities of small and middle-market companies.

Perspectives on Middle-Market Equity Capital ― May 20142

Today’s Financing Environment: A “Risk On” Posture

What does CohnReznick think?In this positive financing environment, management and investors may be going on the offensive in a “risk on” posture. Why? They are more concerned about being left behind than about the consequences if things go wrong. This bodes well for capital formation, growth, business conditions, and gradually tightening monetary policy.

The key risk to the scenario stated above, however, will be geopolitical instability including: the potential for worsening hostilities between Russia and the Ukraine; the possibility of deflation in Western Europe; a continued softening of growth rates in Asia, especially China; and the unpredictability of the Middle East.

We’re reminded of the cliché: “In the land of the blind, the one-eyed man is king.” While we do face our share of domestic challenges, the United States may be an island of stability in an ocean of global uncertainty for the next 12 months.

• Higher Commodity Prices in U.S. Dollar Terms – An improving economy will lead to an increased demand for commodities and real estate. Commodity prices may be driven up further due to expected appreciation in the U.S. dollar, as interest rates in the U.S. rise relative to other countries around the globe that are experiencing slackening demand.

• Merger & Acquisition Activity Higher – M&A activity is highly correlated to stock market performance and economic growth. In down-market cycles, many pundits expect M&A to increase because acquisition prices decline, but, in fact, the reverse is true. Acquirers undertake strategic acquisitions when stock prices are strong and their own buying power is increased. In the current environment, M&A backlog is building as corporations enjoy better business conditions, and managements are focused on growth planning and strategic acquisitions. Middle-market companies will be both buyers and sellers, becoming acquisition targets of larger cap competitors and mining smaller companies to enter new markets and increase vertical integration.

A CohnReznick Report 3

Legislation Opens the Capital Spigot

The original JOBS Act―an “omnibus bill” that rolled together six separate pro-capital formation bills into one―was informed, in large part, by the research of this report’s principal authors (see contributors, pg 18), whose ideas were adopted by the Congressional representatives behind the various bills. We attribute the dual decline in the small IPO market and in the number of publicly listed companies to the shift from telephone-quoted markets to electronic markets in 1998, and not to the Sarbanes-Oxley Act as popularly diagnosed. This abrupt change in market structure undermined the economic incentives sustaining interest and profitability in the market making of small cap stocks.

CohnReznick believes the JOBS Act was the single most important piece of pro-capital formation legislation in a generation―and activity in the first quarter of 2014 reflects that there may be a harbinger of a secular shift in financial markets. The JOBS Act has not only caused Congress to be more aware of the issues impacting equity capital availability and led to bipartisan collaboration to find market-driven solutions to spur growth and innovation; it has unleashed a revolution of services to support equity capital formation for small and middle-market businesses. How? The following JOBS Act provisions are currently enabling the capital formation needs of middle-market businesses or will do so in the near future:

Perspectives on Middle-Market Equity Capital ― May 20144

Legislation Opens the Capital Spigot

Testing the IPO Waters: Emerging Growth Companies

Significance: Makes it more attractive for private companies to access the public markets by allowing them to decrease the up-front costs of going public and to cut the risk of an IPO failure by allowing them to pre-market their shares.

Title I of the JOBS Act enables companies to continue to market their shares by meeting and communicating with institutional investors. Previously, most attorneys would counsel clients to shut down their marketing at least six months before filing a registration statement with the SEC. For many companies this resulted in a year-long blackout. It isn’t surprising that more than 80% of the companies qualifying for Emerging Growth Company status (revenues less than $1 billion) are availing themselves of Title I provisions, taking advantage of such benefits as confidential filings and delaying compliance with Section 404(b) of Sarbanes Oxley. It has been a clear success.

Are there notable industries impacted? For companies that have complicated stories―especially technology-intensive stories such as those found in the biotechnology industry―the ability to “test the waters” must seem like “just what the doctor ordered.” Institutional investors simply could not get comfortable in making a multimillion dollar investment based on only one 45-minute meeting with management on the IPO roadshow. Now, management teams have the opportunity to develop real relationships with institutional investors over time which can have significant benefits as it leads to:

• Offsetting market risk and the risk of a failed transaction by building a better book of investor demand;

• Higher proceeds and lower cost of capital; and

• Better aftermarket stock price performance.

In his recent OpEd in The Wall Street Journal entitled, “Hey, Washington, the JOBS Act You Passed is Working,” AOL co-founder Steve Case, stated that “the self-executing IPO on-ramp is starting to make a real difference. IPOs are up 70% this year [and]…Technology-company IPOs are forecast to hit their highest level in more than a decade.”

“It is exciting that healthcare, pharmaceutical, and biotechnology companies have embraced Title 1 of the JOBS Act to reduce the inherent risks involved in accessing the IPO marketplace. The fact that more than 80% of the companies that qualify for EGC status are using some provision of Title 1 speaks louder than words.”― Alex Castelli, Partner, Technology and Life Sciences Industry Practice Leader

A CohnReznick Report 5

Tick Size Pilot Program

Significance: Improves aftermarket support of small-cap and middle-market companies by increasing tick sizes (the increment in which a security can be quoted).

What would higher tick sizes achieve? Aftermarket support for small and mid-capitalization stocks is weaker than in the ‘80s and ‘90s because the shift to trading-oriented computerized stock markets made aftermarket support for small public companies unprofitable. CohnReznick believes that higher minimum tick sizes may induce market makers to become more active in committing capital, sales, trading, and research resources to support smaller capitalization stocks. In turn, this could lead to an increase in capital allocated by institutional investors to small and middle-market public companies which would raise prices and improve (lower) the cost of capital experienced by their management, investors and boards of directors.

Equity Crowdfunding

Significance: Title II of the JOBS Act is improving access to capital for start-ups and early stage companies by enhancing “accredited crowdfunding” efforts. Title III, currently awaiting SEC rulemaking, will further accelerate the pace of capital formation by allowing for “non-accredited crowdfunding.”

Title II of the JOBS Act repealed the prohibition against general solicitation of accredited investors. It enables corporations to issue press releases about private placements and to speak on television and at conferences about the placement. As a result, equity crowdfunding platforms such as Crowdfunder, Angel’s List, EarlyShares.com, Microventures, Fundersclub, and CircleUp have helped equip firms to raise funds in larger amounts than they otherwise would have raised before Title II took effect. Title III is on the horizon. “If Americans allocate just 1% of their investable assets into Title III equity crowdfunding, it will be a $300 billion market,” says Heather Schwarz-Lopes, CSO and Co-Founder of EarlyShares. “Equity crowdfunding will be a tremendous capital raising tool for entrepreneurs and small business owners, since it will enable them to give their entire networks the chance to become owners in their ventures.”

Perspectives on Middle-Market Equity Capital ― May 20146

Legislation Opens the Capital Spigot

Regulation A+

Significance: Makes it less costly and less risky for small and middle-market companies to access public capital in amounts up to $50 million over any 12 month period by increasing the upper bound of proceeds from $5 million and by removing costly state-by-state (“Blue Sky”) registration requirements.

Originally passed in the wake of the Great Depression to stimulate job growth, Regulation A allowed corporations to raise up to $5 million in equity from public investors exempt from registration with the SEC. Title IV of the JOBS Act seeks to reform this flawed, and thus seldom used, method of raising capital and bring it into the 21st Century.

What does CohnReznick think?If the SEC creates adequate incentives for liquidity providers in the aftermarket (higher tick sizes or quoted markets), we believe the number of IPOs― especially those of smaller and middle-market companies― would grow dramatically over the next five to ten years, resulting in significant job growth for the U.S. economy.

The first step toward modernization is that Congress has mandated that Regulation A’s upper bound be increased from $5 million to a more practical $50 million in proceeds over any 12 month period (there is a CPI escalator intended to make sure that this limit is adjusted for inflation). It requires the publication of audited financial statements and prohibits so-called “Bad Actors.”

One of the primary reasons the prior version of Reg. A was rarely used by corporate issuers is because there was no exemption from state (“Blue Sky”) registration. State-by-state registration, especially for small amounts of money, likely made Reg. A an impractical alternative to the traditional Reg. D private placement to accredited (non-public) investors that had no dollar limit. The second step toward modernizing Reg. A is to pre-empt state-by-state Blue Sky registration―a path the SEC is clearly traveling. To be maximally effective, however, the SEC must maintain access for all investors, including the retail public; eliminate any resell restrictions; and provide exchange listing options that do not trigger a full blown registration process.

A CohnReznick Report 7

Analysis of Capital Formation in 2014 ―What Have We Discovered?

Overview

Equity capital markets activity was robust in the first quarter, with 74 IPOs compared to only 42 IPOs in Q1 2013. In addition Q1 2014 results reflected that there were 278 follow-on offerings completed. Technology, healthcare, and the financial services sectors topped the industry list with the greatest IPO activity. Stripping out the financial vehicles, there were 66 corporate IPOs and 233 corporate follow-on offerings. CohnReznick’s focus in this report is on the middle- market, defined throughout this report as businesses with a market capitalization of $100 million to $1 billion. Within this space, there were 47 IPOs and 101 follow-ons, demonstrating strong growth over the prior year’s period and over the previous quarter.

One point of concern is the continued deficiency in the number of small IPOs (under $50 million in proceeds)―a disturbing trend that has continued unabated since the market structure changes in 1998 (see Figure 1). Only 12 of the 66 corporate IPOs in the first quarter raised less than $50 million.

“The JOBS Act has made it less complicated for growing technology companies to utilize IPOs as an attractive and realistic strategy to raise capital. As the United States economy continues to strengthen, middle- market technology companies with their eye on raising capital in 2014, should find plenty of options.”

― Alex Castelli, Partner, Technology and Life Sciences Industry Practice Leader

Perspectives on Middle-Market Equity Capital ― May 20148

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 Q1:2014

Order Handling RulesRegulation ATS

Sarbanes-OxleyRegulation NMS

Decimalization

Transactionsraising at least$50 million

Transactionsraising less than$50 million

Analysis of Capital Formation in 2014 ―What Have We Discovered?

What doesCohnReznick think?CohnReznick believes that transactions at the small end of the market will continue to languish until the JOBS Act provisions described above are fully implemented by the SEC. Why? The economics that supported small and mid-cap infrastructure were destroyed by regulatory changes that began in 1998. That year, Reg ATS instituted regulations designed to protect investors from concerns arising from increased use of alternative trading systems such as electronic communication networks. Stocks used to trade at a tick size of 25 cents or 12.5 cents until 1998, when Reg ATS took effect. At that time, brokers could make money by supporting small and mid cap stocks, and providing research coverage. Today, with tick sizes are one cent, brokers cannot make money in those stocks, so they suffer in their efforts to raise capital.

Figure 1. Small IPOs Remain Largely Absent Despite Increased Overall Equity Financing Activity

A CohnReznick Report 9

Analyzing Q1 IPO Results

Healthcare IPOs led the way in the fi rst quarter, accounting for more than half (24 out of 47) of middle-market issuances with more than twice the number of deals seen in the fourth quarter of 2013 (see Figure 2). CohnReznick observes that the healthcare industry’s success is, in part, due to that sector’s stocks trading well. Therefore, this uptick in investor demand presented an opportunityfor other healthcare companies to go public. We expect that any continued broad market strength would see the rate of healthcare issuance continue apace. Any meaningful progress with Regulation A+ would also be a boon for healthcare fi nance, particularly for the small and mid-cap life sciences sector.

Figure 2. Healthcare IPOs Accounted for More Than Half of Middle-Market New Issues in the First Quarter

50

45

40

35

30

25

20

15

10

5

0Q1: 2013 Q2: 2013 Q3: 2013 Q4: 2013 Q1: 2014

Commercial Real EstateConstructionFinancial ServicesHealthcare

HospitalityIndustrialLife SciencesManufacturingEnergy

Professional ServicesRetailTechnology/TelecomTransportation

Perspectives on Middle-Market Equity Capital ― May 201410

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%Q1: 2013

Below Filing Range

Q2: 2013 Q3: 2013 Q4: 2013 Q1: 2014

Within Filing Range Above Filing Range

42.9%

21.4%30.3% 33.3% 32.3%

25.5%

35.7%

54.5%42.4%

51.6%55.3%

15.2% 24.2% 16.1% 19.1%

What About IPO Pricing?

Investment banks generally did a commendable job in pricing IPOs, executing nearly 75% of middle-market issues at or above the original fi ling range (see Figure 3). While it was the best executionby investment banks since the fi rst quarter of 2013, it still leaves one quarter of issuers disappointed in their IPO price.

We believe that this under-pricing phenomenon can be dramatically reduced as more issuers take the lead in building relationships with investors early and not merely waiting for their bankers and the IPO roadshow. In fact, CohnReznick recommends that company management and their Boards of Directors, as fi duciaries, do everything possible to build those relationships, thereby increasing demand and creating leverage for more favorable pricing on middle-market transactions.

Figure 3. 75% of Middle-Market IPOs Priced At or Above the Initial Filing Range

Analysis of Capital Formation in 2014 ―What Have We Discovered?

“No one knows how long the window of opportunity for IPOs and follow-on transactions will remain open. In that regard, if you’re a middle-market decision maker and an IPO or follow-on is part of your strategic plan, the best strategy may be to prepare yourself for the transaaction and move forward when the timing is most advantageous.”

― Mark Spelker, Partner, National Director of SEC Services

A CohnReznick Report 11

Figure 3. 75% of Middle-Market IPOs Priced At or Above the Initial Filing Range

Middle-Market IPOs – How Did They Fare in the Aftermarket?

IPOs traded well in the aftermarket in the fi rst quarter, buoyed in part by the strength in the overall market (see Figure 4). While the results were modestly lower than the fourth quarter of 2013, we believe the demand for new and innovative companies remains strong, in addition to demand for IPOs as an asset class. What does this mean for middle-market businesses? CohnReznick believes it is another positive signal about the health of the equity market and points to the market’s support of innovation. This is particularly good news for industries like healthcare that are capital intensive and rely on equity investment to thrive. There is clear demand for high quality companies, particularly those in fi elds that are fostering innovation such as healthcare.

Were it not for the market structure changes in the late 1990s, CohnReznick believes the market today would be experiencing signifi cantly higher trading activity than we are currently seeing. We remain optimistic that the SEC will move forward in formally adopting the remaining titles of the JOBS Act and restore the markets to the vibrancy they once enjoyed.

50%

40%

30%

20%

10%

Q1: 2013 Q2: 2013 Q3: 2013 Q4: 2013 Q1: 2014

1 Day

1 Week

2 Weeks

1 Month

Figure 4. Middle Market IPOs Traded Well in the Aftermarket in the First Quarter

Perspectives on Middle-Market Equity Capital ― May 201412

Analysis of Capital Formation in 2014 ―What Have We Discovered?

Were There Clear Industry Winners in Follow-On Offerings?

CohnReznick also saw brisk activity in the secondary market in the fi rst quarter, with 101 transactions by middle-market corporate issuers (see Figure 5). As with the IPO market, healthcare issues were prominent among follow-on offerings, accounting for 30% of all transactions. Issuers clearly took advantage of near record-highs in the market to raise additional capital in the quarter, and we could see similar levels of activity throughout the year with the backdrop of a favorable broad market. What do these results mean for the middle-market in general? The Q1 results for follow-on offerings are a sign that investors are willing to fund future growth, knowing that further funding may be required as investors appear optimistic about the market’s ability to support innovation and growth.

Notably, we saw a signifi cant increase in life sciences follow-ons, with 17 deals in the fi rst quarter of 2014, compared to only three deals in the prior year’s period and 11 deals in the previous quarter. CohnReznick believes that raising capital through follow-on offerings is a strategic opportunity. Middle-market businesses may want to take advantage of escalating stock prices to sell more equity or provide shareholders with an opportunity to cash out. As illustrated in Figure 5, it was clear that follow-on equity deals got done.

120

100

80

60

40

20

0Q1: 2013 Q2: 2013 Q3: 2013 Q4: 2013 Q1: 2014Q1: 2013

AgribusinessConstructionEnergyFinancial ServicesHealthcare

IndustrialLife SciencesManufacturingProfessional ServicesRetail

Professional ServicesRetailTechnology/TelecomTransportation

Figure 5. Healthcare Companies Also Dominated the Secondary Market for Sub $2 Billion Equity Issuance

“Middle-marketcompanies naturally fi nd it easier to invest in renewable energy projects when they have suffi cient capital to do so. As the number of IPOs and follow-on transactions increase, the renewable energy space is likely to experience an uptick in overall business activity.”

― Anton Cohen, Partner, Renewable Energy Industry Practice Co-National Director

A CohnReznick Report 13

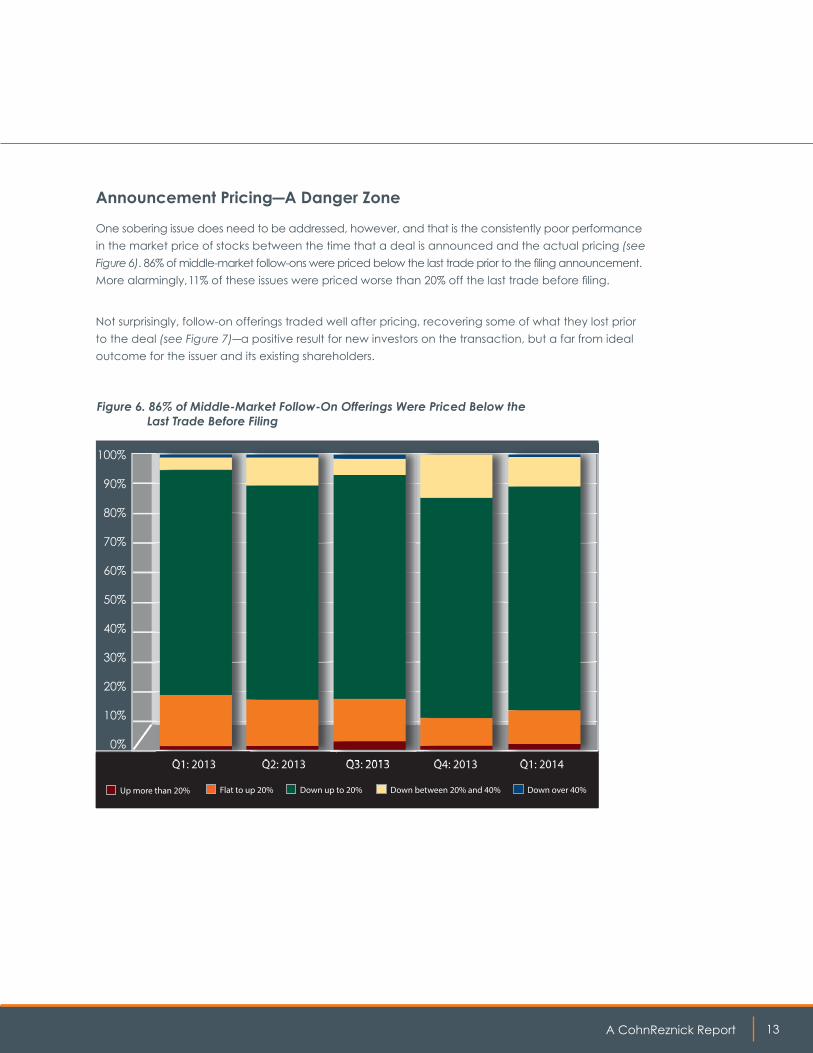

Announcement Pricing―A Danger Zone

One sobering issue does need to be addressed, however, and that is the consistently poor performance in the market price of stocks between the time that a deal is announced and the actual pricing (see Figure 6). 86% of middle-market follow-ons were priced below the last trade prior to the fi ling announcement. More alarmingly, 11% of these issues were priced worse than 20% off the last trade before fi ling.

Not surprisingly, follow-on offerings traded well after pricing, recovering some of what they lost prior to the deal (see Figure 7)―a positive result for new investors on the transaction, but a far from ideal outcome for the issuer and its existing shareholders.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%Q1: 2013 Q2: 2013 Q3: 2013 Q4: 2013 Q1: 2014

Flat to up 20% Down up to 20% Down between 20% and 40% Down over 40%

Q1: 2013 Q2: 2013 Q3: 2013 Q4: 2013 Q1: 2014

Up more than 20%

Figure 6. 86% of Middle-Market Follow-On Offerings Were Priced Below the Last Trade Before Filing

Perspectives on Middle-Market Equity Capital ― May 201414

11%

10%

9%

8%

7%

6%

5%

4%

3%

2%

Q1: 2013 Q2: 2013 Q3: 2013 Q4: 2013 Q1: 2014

1 Day

1 Week

2 Weeks

1 Month

Figure 7. Sub $2 Billion Follow-Ons Traded Well After Pricing, Regaining Ground Lost Since Filing

What doesCohnReznick think? Issuers would be well-advised to improve their knowledge of their existing and potential shareholder bases, and their capacity to place new shares quickly and effi ciently with a minimum of information leakage. CohnReznick believes that issuers who rely solely on their investment banks for this have been sorely disappointed―86% of them certainly. We would recommend that issuers leverage service providers that can help target institutions most effi ciently, especially those institutions that “traditional Wall Street” may ignore.

Analysis of Capital Formation in 2014 ―What Have We Discovered?

“The real estate industry benefi ts when middle- market companies gain access to additional sources of capital like IPOs and follow-ons. There is a positive correlation between the level of activity in the capital markets and the level of activity in the real estate industry. Middle-market companies who are successful in raising capital will invest in improving their facilities and adding locations, both of which drive transactions in real estate.”

― David Kessler, Partner, Commercial Real Estate Industry Practice National Director

One of the key reasons for such poor stock price performance leading up to a deal is the information leakage that occurs between the announcement of a deal and pricing. In recent years, we have seen fewer and fewer follow-on transactions become fully marketed, with more accelerated book-builds and overnight deals becoming commonplace. Even with the absence or severe restrictions in marketing, however, the evidence of information leakage is clear.

A CohnReznick Report 15

Preparing to Take Advantage of Equity Markets

With pro-equity capital formation legislation coming from Congress, indications the JOBS Act is fueling equity financing, and a positive outlook for the equity markets, now is an ideal time for middle-market companies looking for an equity infusion to ready their companies to go public.

“Going public” isn’t for everyone, however. There is greater oversight and public scrutiny, pressure to achieve short-term results, and greater exposure to liabilities for officers and directors. These changes are significant, so CohnReznick advises companies looking at a future IPO to begin acting like a public company prior to filing. Doing so can help the organization avoid costly delays and increase the attractiveness of the company to underwriters and investors.

While every company should develop a plan that is tailored for their organization to take advantage of the IPO On-Ramp, CohnReznick advises companies to consider the following initiatives as part of their planning:

Analyze and Update Your Board of Directors:As a public company, you’ll need to comply with tougher rules regarding the composition and responsibilities of your board and its committees. Although the JOBS Act provides for a longer transition to Sarbanes Oxley (SOX) compliance, eventually your audit, compensation, and nominating committees must be comprised of independent outside directors with at least one member of the audit committee being a “financial expert.” CohnReznick advises clients to begin evaluating current and desired board competencies. Board members experienced in public companies can be critical sources of insight in readying for an IPO.

Perspectives on Middle-Market Equity Capital ― May 201416

Preparing to Take Advantage of Equity Markets

Evaluate and Strengthen Internal Controls:With the enactment of the JOBS Act, going public has fewer regulatory hurdles, including delaying compliance with Section 404(b) of Sarbanes Oxley. That does not mean, however, that you can afford to ignore internal controls as part of your preparation process. No one wants to be on a “road show” drumming up interest in an offering and not be able to answer questions about adequacy of controls. In May 2013, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) released its 2013 Internal Control-Integrated Framework that provides an updated framework to help organizations design and implement internal controls and that clarifies the requirements for determining what constitutes effective internal control. Evaluate your company’s internal controls against this framework and have an action plan that demonstrates to underwriters that you will be prepared to withstand regulatory scrutiny and issue quarterly SEC filings (10-Q) that state that the company’s financial information is materially accurate and that its internal control over financial reporting and disclosure controls and procedures are adequate.

Get Audited Financial Statements:The SEC requires Public Company Accounting Oversight Board (PCAOB) audited financial statements prepared in accordance with U.S. generally accepted accounting principles (US – GAAP). You may be required to submit separate audited financial statements for acquired companies. Obtaining audited financial statements for previous years can be difficult and costly―especially if your documentation isn’t up-to-par―potentially delaying the IPO process.

Assess Your Management Team:The quality and depth of your management team is one of the most important factors for underwriters and investors. Senior executives should be experienced professionals who understand your industry and are prepared for the enhanced accountability, formality, and discipline associated with a public company. In particular, the organization’s CFO and other financial executives need to have the experience and training necessary to deal with public company accounting and financial systems.

Get Your House in Order:There are a variety of housekeeping issues you should address to prepare for an IPO.

• Develop a public and investor relations program to tell your “story” to underwriters, potential investors, and shareholders, and to further enhance brand reputation and name recognition.

• Review contracts, pending litigation, and third-party related transactions, and mitigate any issues that could disrupt the IPO process.

• Revise compensation agreements, if necessary, to ensure they are fair and in-line with best practices and market expectations.

• Review articles of incorporation, bylaws, stock ownership, and other corporate records to ensure public company suitability.

A CohnReznick Report 17

What’s Next?

Today, as was the case a few years ago, there is an overriding need for U.S. economic policy to grow the economy and create jobs. Legislators correctly concluded that the growth of middle- market and entrepreneurial companies was being hampered by regulatory red-tape that made it cost prohibitive for many companies to access equity markets and secure needed capital.

The JOBS Act was passed including IPO on-ramp provisions designed to make it easier for middle-market companies to secure growth capital. Our report shows initial evidence that the JOBS Act is beginning to make an impact in enhancing capital formation.

CohnReznick’s analysis shows an increase in the number of IPO transactions, highlights participation by industry in those transactions, and demonstrates that middle-market IPOs traded well in the aftermarket during the first quarter of 2014.

We caution, however, that the job of legislators and regulators is not finished. Small IPOs languished and will continue to do so until additional action is taken. We expect to see further pro-equity capital formation legislation from Congress and enactments by the U.S. Securities and Exchange Commission.

We conclude that the window of opportunity for middle-market companies considering an IPO or follow-on transaction, now cracked open, will soon be opened wide enough to be a game changer for middle-market growth.

Perspectives on Middle-Market Equity Capital ― May 201418

Contributors and Upcoming Events

Contributors to This ReportCohnReznick has an agreement with IssuWorks, Inc. that enables CohnReznick to utilize their services and resources to assist clients with their capital needs. IssuWorks provides services and technologies that improve capital formation, distribution, and aftermarket results for companies, investors, and investment banks. The primary contributors from IssuWorks were:

David Weild IV – IssuWorks Founder, Chairman, and Chief Executive Offi cerDavid has co-authored studies that document the long-term decline in equity capital formation and has testifi ed in Congress and at the CFTC-SEC Joint Panel on Emerging Regulatory Issues. He is a former Vice-Chairman of NASDAQ and a frequent resource to the media on issues relevant to the capital markets.

Edward H. Kim – IssuWorks Chief Operating Offi cerEd has over 25 years of capital markets, fi nance, product development, and operations experience. He was formerly Managing Director of Financial Communications at Stern and Company, a Senior Vice President at NASDAQ, and the Chief Administrative Offi cer of a publicly held software company.

CohnReznick has also formed a Capital Markets Advisory Consortium to provide clients and business associates with direct access to a group of boutique investment bankers across the United States who are known for their market knowledge and specifi c industry expertise.

CohnReznick’s Fourth Annual Liquidity and Capital Raising National ForumCohnReznick is committed to providing the owners/operators of middle-market companies with critical insights on liquidity and capital formation. We are pleased to announce that our Fourth Annual Liquidity and Capital Raising National Forum will take place in fi ve cities this Fall to better accommodate an expanding group of attendees.

Designed for the key decision makers―CEOs, CFOs, and Presidents―this event offers an outstanding networking venue that enables attendees to connect, exchange ideas, and develop relationships. Some of the country’s top M&A and capital markets experts and CEOs will be on hand to share their insights, advice, and experiences. We hope you can join us for this not-to-be-missed forum.

Registration opens this summer at www.cohnreznick.com.

LOS ANGELESNOV.

20Four Seasons

BOSTONOCT.

24MandarinOriental

NEW YORKSEPT.

23 St. Regis

BALTIMORENOV.

05Four Seasons

ATLANTAOCT.

30Ritz-CarltonBuckhead

A CohnReznick Report 19

Appendix

Number of IPOs By Investment Bank

Q1: 2013 Q2: 2013 Q3: 2013 Q4: 2013 Q1: 2014

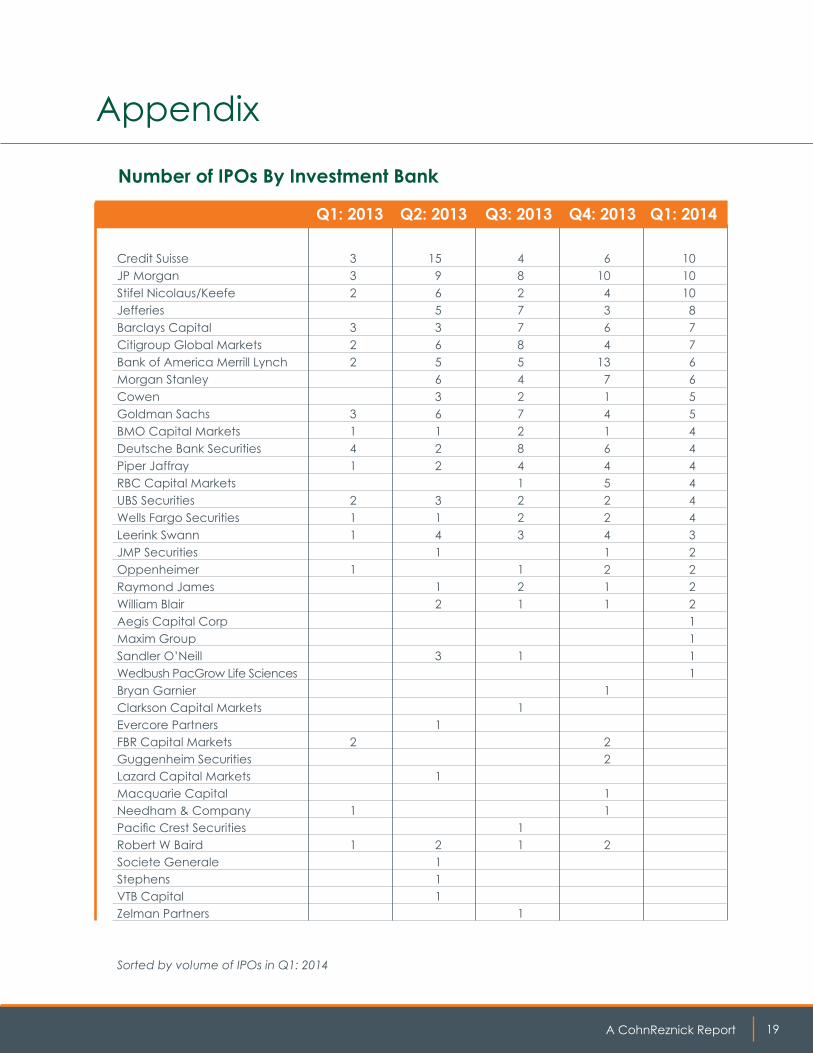

Credit Suisse 3 15 4 6 10JP Morgan 3 9 8 10 10Stifel Nicolaus/Keefe 2 6 2 4 10Jefferies 5 7 3 8Barclays Capital 3 3 7 6 7Citigroup Global Markets 2 6 8 4 7Bank of America Merrill Lynch 2 5 5 13 6Morgan Stanley 6 4 7 6Cowen 3 2 1 5Goldman Sachs 3 6 7 4 5BMO Capital Markets 1 1 2 1 4Deutsche Bank Securities 4 2 8 6 4Piper Jaffray 1 2 4 4 4RBC Capital Markets 1 5 4UBS Securities 2 3 2 2 4Wells Fargo Securities 1 1 2 2 4Leerink Swann 1 4 3 4 3JMP Securities 1 1 2Oppenheimer 1 1 2 2Raymond James 1 2 1 2William Blair 2 1 1 2Aegis Capital Corp 1Maxim Group 1Sandler O’Neill 3 1 1Wedbush PacGrow Life Sciences 1Bryan Garnier 1 Clarkson Capital Markets 1 Evercore Partners 1FBR Capital Markets 2 2Guggenheim Securities 2Lazard Capital Markets 1Macquarie Capital 1Needham & Company 1 1Pacific Crest Securities 1Robert W Baird 1 2 1 2Societe Generale 1Stephens 1VTB Capital 1Zelman Partners 1

Sorted by volume of IPOs in Q1: 2014

Perspectives on Middle-Market Equity Capital ― May 201420

Continental Building Products Inc

189,416,500 Construction “Citigroup Global Markets Inc; Credit Suisse Securities (USA) LLC; Barclays Capital Inc; Deutsche Bank Securities Inc; RBC Capital Markets”

New Home Company Inc

98,828,125 Construction “Citigroup Global Markets Inc; JP Morgan Securities LLC; Credit Suisse Securities (USA) LLC”

Installed Building Products Inc

94,242,500 Construction “Deutsche Bank Securities Inc; UBS Securities LLC”

Talmer Bancorp Inc

232,555,544 Financial Services “Keefe, Bruyette & Woods, a Stifel Company.; JP Morgan Securities LLC”

Square 1 Financial Inc

119,669,274 Financial Services “Sandler O’Neill & Partners; Keefe, Bruyette & Woods, a Stifel Company.”

CM Finance Inc 114,999,990 Financial Services “Raymond James & Associates Inc; Keefe, Bruyette & Woods, a Stifel Company.; Oppenheimer & Co Inc”

TPG Specialty Lending Inc

112,000,000 Financial Services “JP Morgan Securities LLC; Bank of America Merrill Lynch; Goldman Sachs; Citigroup Global Markets Inc; Wells Fargo Securities LLC; Barclays Capital Inc”

Versartis Inc 144,900,000 Healthcare “Morgan Stanley & Co LLC; Citigroup Global Markets Inc”

Ultragenyx Pharmaceutical Inc

139,112,883 Healthcare “JP Morgan Securities LLC; Morgan Stanley & Co LLC”

Middle Market IPOs in Q1: 2014

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

A CohnReznick Report 21

Middle Market IPOs in Q1: 2014 (continued)

Akebia Therapeutics Inc

114,954,000 Healthcare “Morgan Stanley & Co LLC; Credit Suisse Securities (USA) LLC; UBS Securities LLC”

Revance Therapeutics Inc

110,400,000 Healthcare “Cowen & Co LLC; Piper Jaffray & Co”

Dicerna Pharmaceuticals Inc

103,500,000 Healthcare “Jefferies LLC; Leerink Swann LLC; Stifel Nicolaus & Co Inc”

Auspex Pharmaceuticals Inc

96,600,000 Healthcare “Stifel Nicolaus & Co Inc; BMO Capital Markets”

Concert Pharmaceuticals Inc

93,095,660 Healthcare “UBS Securities LLC; Wells Fargo Securities LLC”

UniQure BV 91,800,000 Healthcare “Jefferies LLC; Leerink Swann LLC”

Lumenis Ltd 84,232,224 Healthcare “Goldman Sachs; Credit Suisse Securities (USA) LLC; Jefferies LLC”

Achaogen Inc 82,800,000 Healthcare “Credit Suisse Securities (USA) LLC; Cowen & Co LLC”

MediWound Ltd 80,500,000 Healthcare “Credit Suisse Securities (USA) LLC; Jefferies LLC; BMO Capital Markets”

Flexion Therapeutics Inc

74,750,000 Healthcare “BMO Capital Markets; Wells Fargo Securities LLC”

Inogen Inc 70,588,208 Healthcare JP Morgan Securities LLC

Trevena Inc 66,643,143 Healthcare “Barclays Capital Inc; Jefferies LLC”

Genocea Biosciences Inc

66,000,000 Healthcare “Citigroup Global Markets Inc; Cowen & Co LLC”

Cara Therapeutics Inc

63,250,000 Healthcare “Stifel Nicolaus & Co Inc; Piper Jaffray & Co”

Egalet Corp 57,960,000 Healthcare “Stifel Nicolaus & Co Inc; JMP Securities LLC”

Aquinox Pharmaceuticals Inc

53,130,000 Healthcare “Jefferies LLC; Cowen & Co LLC”

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

Perspectives on Middle-Market Equity Capital ― May 201422

Eagle Pharmaceuticals Inc

51,750,000 Healthcare “Piper Jaffray & Co; William Blair & Co LLC”

Celladon Corp 50,600,000 Healthcare Barclays Capital Inc

Argos Therapeutics Inc

49,829,800 Healthcare “Piper Jaffray & Co; Stifel Nicolaus & Co Inc; JMP Securities LLC”

Galmed Pharmaceuticals Ltd

44,050,635 Healthcare Maxim Group LLC

Dipexium Pharmaceuticals

37,950,000 Healthcare Oppenheimer & Co Inc

NephroGenex Inc 37,200,000 Healthcare Aegis Capital Corp

Intrawest Resorts Holdings Inc

215,625,000 Hospitality “Goldman Sachs; Credit Suisse Securities (USA) LLC; Deutsche Bank Securities Inc; Bank of America Merrill Lynch”

GlycoMimetics Inc

64,400,000 Life Sciences “Jefferies LLC; Barclays Capital Inc”

Applied Genetic Technologies Corp

57,500,004 Life Sciences “BMO Capital Markets; Wedbush PacGrow Life Sciences”

Eleven Biotherapeutics Inc

57,500,000 Life Sciences “Citigroup Global Markets Inc; Cowen & Co LLC; Leerink Swann LLC”

2U Inc 119,275,000 Professional Services “Goldman Sachs; Credit Suisse Securities (USA) LLC”

Care.com Inc 104,592,500 Professional Services “Morgan Stanley & Co LLC; Bank of America Merrill Lynch; JP Morgan Securities LLC”

Everyday Health Inc

100,100,000 Professional Services “JP Morgan Securities LLC; Credit Suisse Securities (USA) LLC; Citigroup Global Markets Inc”

A10 Networks Inc 187,500,000 Technology/Telecom “Morgan Stanley & Co LLC; Bank of America Merrill Lynch; JP Morgan Securities LLC; RBC Capital Markets”

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

Middle Market IPOs in Q1: 2014 (continued)

A CohnReznick Report 23

Paylocity Holding Corp

137,729,750 Technology/Telecom “Deutsche Bank Securities Inc; Bank of America Merrill Lynch; William Blair & Co LLC”

Varonis Systems Inc

121,440,000 Technology/Telecom “Morgan Stanley & Co LLC; Barclays Capital Inc; Jefferies LLC; RBC Capital Markets”

Q2 Holdings Inc 116,025,013 Technology/Telecom “JP Morgan Securities LLC; Stifel Nicolaus & Co Inc”

Amber Road Inc 110,503,887 Technology/Telecom Stifel Nicolaus & Co Inc

Borderfree Inc 92,000,000 Technology/Telecom “Credit Suisse Securities (USA) LLC; RBC Capital Markets”

Aerohive Networks Inc

75,000,000 Technology/Telecom “Goldman Sachs; Bank of America Merrill Lynch”

CHC Group Ltd 310,000,000 Transportation “JP Morgan Securities LLC; Barclays Capital Inc; UBS Securities LLC”

Malibu Boats Inc 112,589,540 Transportation “Raymond James & Associates Inc; Wells Fargo Securities LLC”

Stock Building Supply Holdings Inc

124,237,425 Construction “Goldman Sachs; Barclays Capital Inc; Citigroup Global Markets Inc”

William Lyon Homes Inc

62,675,000 Construction “JP Morgan Securities LLC; Citigroup Global Markets Inc; Credit Suisse Securities (USA) LLC”

GeoPark Ltd 97,997,900 Energy “JP Morgan Securities LLC; BTG Pactual; Itau BBA USA Securities Inc”

American Eagle Energy Corp

83,490,000 Energy Johnson Rice & Co

Synthesis Energy Systems Inc

15,000,001 Energy TR Winston & Co Inc

Waterstone Financial Inc

253,000,000 Financial Services Sandler O’Neill & Partners

MoneyGram International Inc

151,800,000 Financial Services “Bank of America Merrill Lynch; Wells Fargo Securities LLC; Goldman Sachs; JP Morgan Securities LLC”

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

Middle Market IPOs in Q1: 2014 (continued)

Perspectives on Middle-Market Equity Capital ― May 201424

Middle Market Follow-On Offerings in Q1: 2014

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

PennyMac Financial Services Inc

100,815,000 Financial Services Citigroup Global Markets Inc

Arlington Asset Investment Corp

83,912,500 Financial Services "Barclays Capital Inc; Credit Suisse Securities (USA) LLC; RBC Capital Markets"

Enzymotec Ltd 151,303,180 Healthcare "Bank of America Merrill Lynch; Jefferies LLC"

Epizyme Inc 151,122,465 Healthcare "Citigroup Global Markets Inc; Cowen & Co LLC; Leerink Partners LLC"

Aratana Therapeutics Inc

142,025,000 Healthcare “Jefferies LLC; Barclays Capital Inc; William Blair & Co LLC”

Receptos Inc 117,403,500 Healthcare “Credit Suisse Securities (USA) LLC; Leerink Swann LLC; BMO Capital Markets”

Endocyte Inc 108,675,000 Healthcare “Credit Suisse Securities (USA) LLC; Citigroup Global Markets Inc”

Flamel Technologies SA

105,300,000 Healthcare JMP Securities LLC

GW Pharmaceuticals plc

101,061,900 Healthcare “Morgan Stanley & Co LLC; Cowen & Co LLC”

Tornier NV 98,656,250 Healthcare Bank of America Merrill Lynch

AtriCure Inc 94,084,375 Healthcare Piper Jaffray & Co

Derma Sciences Inc

86,250,000 Healthcare “Piper Jaffray & Co; Canaccord Genuity Inc”

Ampio Pharmaceuticals Inc

68,425,000 Healthcare “Citigroup Global Markets Inc; Jefferies LLC”

Inovio Pharmaceuticals Inc

63,251,610 Healthcare “Piper Jaffray & Co; Stifel Nicolaus & Co Inc”

NanoString Technologies Inc

61,399,983 Healthcare “JP Morgan Securities LLC; Morgan Stanley & Co LLC”

Tekmira Pharmaceuticals Corp

60,562,500 Healthcare Leerink Partners LLC

A CohnReznick Report 25

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

OvaScience Inc 55,186,300 Healthcare Leerink Partners LLC

ANI Pharmaceuticals Inc

49,999,993 Healthcare “Oppenheimer & Co Inc; Roth Capital Partners”

Tonix Pharmaceuticals Holding Corp

43,478,250 Healthcare Roth Capital Partners

Sunesis Pharmaceuticals Inc

43,012,500 Healthcare "Cowen & Co LLC; Cantor Fitzgerald & Co"

Progenics Pharmaceuticals Inc

40,250,000 Healthcare Jefferies LLC

Idera Pharmaceuticals Inc

40,104,752 Healthcare "Piper Jaffray & Co; Cowen & Co LLC"

Alimera Sciences Inc

37,500,000 Healthcare Cowen & Co LLC

Omeros Corp 35,000,009 Healthcare Cowen & Co LLC

Cytokinetics Inc 35,000,000 Healthcare Cowen & Co LLC

iCAD Inc 30,360,000 Healthcare Craig-Hallum Group

Neptune Technologies & Bioressources Inc

28,750,000 Healthcare "Roth Capital Partners; Euro Pacific Canada Inc"

Biota Pharmaceuticals Inc

28,749,736 Healthcare Guggenheim Securities LLC

Cardiome Pharma Corp

27,377,259 Healthcare Canaccord Genuity Corp

Rexahn Pharmaceuticals Inc

20,002,500 Healthcare Roth Capital Partners

TG Therapeutics Inc

18,135,848 Healthcare Ladenburg Thalmann & Co Inc

BioLife Solutions Inc

15,480,000 Healthcare Ladenburg Thalmann & Co Inc

IsoRay Inc 14,675,180 Healthcare Maxim Group LLC

Primero Mining Corp

202,280,519 Industrial Canaccord Genuity Corp

Middle Market Follow-On Offerings in Q1: 2014 (continued)

Perspectives on Middle-Market Equity Capital ― May 201426

Solazyme Inc 63,250,000 Industrial “Goldman Sachs; Morgan Stanley & Co LLC”

Noranda Aluminum Holding Corp

47,500,000 Industrial Morgan Stanley & Co LLC

SilverCrest Mines Inc

18,269,757 Industrial Dundee Securities Ltd

United Insurance Holdings Corp

57,500,000 Insurance "Raymond James; Wells Fargo Securities LLC"

PTC Therapeutics Inc

126,499,993 Life Sciences "JP Morgan Securities LLC; Credit Suisse Securities (USA) LLC"

Arrowhead Research Corp

119,858,750 Life Sciences "Jefferies LLC; Barclays Capital Inc; Deutsche Bank Securities Inc"

Intra-Cellular Therapies Inc

107,485,000 Life Sciences "Leerink Partners LLC; Cowen & Co LLC"

Geron Corp 103,500,000 Life Sciences Bank of America Merrill Lynch

CytRx Corp 85,962,500 Life Sciences Jefferies LLC

XenoPort Inc 82,800,000 Life Sciences Credit Suisse Securities (USA) LLC

Prothena Corp plc

82,738,578 Life Sciences "Bank of America Merrill Lynch; Citigroup Global Markets Inc"

Compugen Ltd 72,450,000 Life Sciences Jefferies LLC

Agenus Inc 60,037,200 Life Sciences William Blair & Co LLC

Ignyta Inc 55,190,513 Life Sciences Leerink Partners LLC

Oxygen Biotherapeutics Inc

51,999,993 Life Sciences "Ladenburg Thalmann & Co Inc; MTS Securities LLC"

Five Prime Therapeutics Inc

43,125,000 Life Sciences "Jefferies LLC; BMO Capital Markets; Wells Fargo Securities LLC"

Retrophin Inc 39,999,997 Life Sciences Jefferies LLC

Athersys Inc 20,500,000 Life Sciences Maxim Group LLC

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

Middle Market Follow-On Offerings in Q1: 2014 (continued)

A CohnReznick Report 27

Bio-Path Holdings Inc

9,999,999 Life Sciences Maxim Group LLC

pSivida Corp 6,987,000 Life Sciences Northland Securities Inc

Mercer International

57,557,500 Manufacturing Credit Suisse Securities (USA) LLC

Quantum Fuel Systems Technologies Worldwide Inc

16,620,375 Manufacturing Craig-Hallum Capital Group

Kandi Technologies Group Inc

11,053,440 Manufacturing FT Global Capital Inc

MakeMyTrip Ltd 145,475,000 Professional Services "Citigroup Global Markets Inc; JPMorgan; Deutsche Bank Securities Inc"

China Distance Education Holdings Ltd

84,000,000 Professional Services "Morgan Stanley & Co LLC; Credit Suisse Securities (USA) LLC"

Marchex Inc 59,997,000 Professional Services "Deutsche Bank Securities Inc; RBC Capital Markets; Piper Jaffray & Co"

NanoViricides Inc 20,000,001 Professional Services "Chardan Capital Markets LLC; Midtown Partners & Co LLC"

Roundy's Inc 71,196,923 Retail "Credit Suisse Securities (USA) LLC; JP Morgan Securities LLC; Bank of America Merrill Lynch; BMO Capital Markets"

American Apparel Inc

30,500,000 Retail Roth Capital Partners

Sonus Networks Inc

145,525,680 Technology/Telecom Goldman Sachs

Montage Technology Group Ltd

129,202,500 Technology/Telecom "Deutsche Bank Securities Inc; Barclays Capital Inc; Stifel Nicolaus & Co Inc"

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

Middle Market Follow-On Offerings in Q1: 2014 (continued)

Perspectives on Middle-Market Equity Capital ― May 201428

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

E2open Inc 116,513,925 Technology/Telecom "Bank of America Merrill Lynch; Pacific Crest Securities LLC"

Applied Optoelectronics Inc

83,662,500 Technology/Telecom "Raymond James & Associates Inc; Piper Jaffray & Co"

China Mobile Games & Entertainment Group Ltd

82,608,000 Technology/Telecom "Credit Suisse Securities (USA) LLC; Barclays Capital Inc; Jefferies LLC; Nomura Securities International Inc"

SciQuest Inc 80,250,000 Technology/Telecom "JP Morgan Securities LLC; Stifel Nicolaus & Co Inc"

Magic Software Enterprises Ltd

58,650,000 Technology/Telecom "Barclays Capital Inc; William Blair & Co LLC"

Datawatch Corp 57,520,125 Technology/Telecom "Canaccord Genuity Inc; William Blair & Co LLC"

Orbcomm Inc 38,898,750 Technology/Telecom Raymond James & Associates Inc

Rubicon Technology Inc

37,375,000 Technology/Telecom Canaccord Genuity Inc

Mattson Technology Inc

34,500,288 Technology/Telecom "Needham & Company LLC; Cowen & Co LLC"

AudioCodes Ltd 32,200,000 Technology/Telecom "William Blair & Co LLC; Needham & Company LLC"

Cinedigm Digital Cinema Corp

31,671,000 Technology/Telecom Piper Jaffray & Co

FuelCell Energy Inc

31,625,000 Technology/Telecom Stifel Nicolaus & Co Inc

Plug Power Inc 30,000,000 Technology/Telecom Cowen & Co LLC

Rubicon Technology Inc

28,222,500 Technology/Telecom Canaccord Genuity Inc

Plug Power Inc 22,400,006 Technology/Telecom Cowen & Co LLC

Mandalay Digital Group Inc

20,015,175 Technology/Telecom Ladenburg Thalmann & Co Inc

RadiSys Corp 19,380,000 Technology/Telecom Needham & Company LLC

SciQuest Inc 16,813,281 Technology/Telecom UBS Securities LLC

Middle Market Follow-On Offerings in Q1: 2014 (continued)

A CohnReznick Report 29

ISSUER PROCEEDS INDUSTRY BOOKRUNNERS

WidePoint Corp 12,500,001 Technology/Telecom B Riley & Co Inc

DHT Holdings Inc 227,250,000 Transportation "RS Platou Markets AS; DnB Markets"

Ardmore Shipping Corp

108,675,000 Transportation "Morgan Stanley & Co LLC; Wells Fargo Securities LLC; Clarkson Capital Markets"

Tsakos Energy Navigation Ltd

86,416,750 Transportation "Morgan Stanley & Co LLC; UBS Securities LLC; Wells Fargo Securities LLC"

Navios Maritime Acquisition Corp

57,557,500 Transportation "Citigroup Global Markets Inc; RS Platou Markets AS; Deutsche Bank Securities Inc"

Paragon Shipping Inc

42,406,250 Transportation Jefferies LLC

StealthGas Inc 32,999,998 Transportation Global Hunter Securities LLC

Middle Market Follow-On Offerings in Q1: 2014 (continued)

Perspectives on Middle-Market Equity Capital ― May 201430

About CohnReznick’s Capital Markets Group

Utilizing comprehensive resources and deep industry expertise, the professionals of CohnReznick’s Capital Markets Group understand the goals of both middle-market companies and investors to deliver timely and appropriate solutions and opinions. We understand the challenges and opportunities of the Capital Markets and possess the forward thinking technical skills and experience necessary to address the needs of clients, investment bankers, investment advisors, attorneys, lenders, investors, managements, audit committees, and the U.S. Securities and Exchange Commission and other regulatory authorities.

• Mark Spelker, CPA, Partner, National Director of SEC Services• Steven Schenkel, CPA, Partner, Chief Risk Officer• Dom Esposito, CPA, Partner, National Practice and Growth Director• George Gallinger, Principal, CohnReznick Advisory Group − Governance, Risk, and Compliance

National Director• Jeremy Swan, Principal, CohnReznick Advisory Group• Alex Castelli, CPA, Partner, Technology and Life Sciences Industry Practice Leader• David Kessler, CPA, Partner, Commercial Real Estate Industry Practice National Director• Tim Kemper, CPA, Regional Managing Partner-South/Central, Renewable Energy Industry Practice

Co-National Director• Anton Cohen, CPA, Partner, Renewable Energy Industry Practice Co-National Director• Richard Schurig, CPA, Partner, Retail and Consumer Products Industry Practice Leader

CohnReznick’s Capital Market Group provides a range of relevant capabilities including:

• Auditor of Record: The professionals at CohnReznick’s Capital Markets Group provide knowledge and valued assurance services to CEOs, CFOs, and audit committees for privately held companies seeking an auditor of record for an anticipated public filing, mid-sized publicly held companies seeking a change from their existing auditor of record, and privately held companies seeking assistance in preparing for a capital market event.

• IPO Readiness Assessment: Our readiness assessment will determine where a company is now, where it needs to be to position itself for a successful IPO, and what it will take to get there.

• Corporate Governance Services: Having helped hundreds of pre- and post-IPO companies comply with the demands of SOX and exchange requirements, we understand the ROI of proper planning.

• CFO Services: We assist busy CFOs and CAOs by providing strategic, operational, financial, and accounting support, adding value to their core financial operations.

• Information Technology Services: Our IT Governance and Security and IT Infrastructure Design and Implementation teams work seamlessly to assess, design, recommend, and implement systems.

A CohnReznick Report 31

CohnReznick Advantage for Capital Markets Industry Insights, Optimized Solutions

• Partners immersed in supporting public companies and capital markets transactions who understand your business drivers.

• Support from industry specialists to offer comprehensive industry-specific solutions and insights.• Engagement teams utilize the Firm’s broad resources to provide innovative solutions and

breakthrough ideas.

Transformative Advice

• Timely, relevant views about critical economic, business, legislative, tax, and global news and emerging trends in the Capital Markets.

• Thought leadership reports, alerts, conferences, and events delivered in the context of what these issues mean to public companies, companies considering a public filing, the Capital Markets and your business.

Responsive Culture

• Our partners are empowered and entrepreneurial decision makers. • They draw on our depth of knowledge and expertise to provide faster, smarter, more efficient service.

Capital Markets Dexterity

• Preparation, valuation, structuring, and facilitation of Capital Markets transactions, and introductions to capital sources.

• Assistance with acquisitions, identification/dispositions, liquidity events, and other capital-raising needs.

Proactive, Resourceful Service

• A true partner-led service model ensures direct access and active partner management.• Accountability and expectations are developed to meet your needs and documented in the

CohnReznick Client Service Plan.

National and Global Reach

• With 26 offices, we seamlessly and cost-efficiently serve clients on a regional, national, and international basis.

• Companies with international interests in 100+ countries are served through our membership in Nexia International, a global network of independent accountancy, tax, and business advisors.

About CohnReznick LLPWith origins dating back to 1919, CohnReznick LLP is the 10th largest accounting, tax, and advisory firm in the United States, combining the resources and technical expertise of a national firm with the hands-on, entrepreneurial approach that today’s dynamic business environment demands. CohnReznick serves a large number of diverse industries and offers specialized services for Fortune 1000 companies, owner-managed firms, international enterprises, government agencies, not-for-profit organizations, and other key market sectors. Headquartered in New York, NY, CohnReznick serves its clients with more than 280 partners, 2,500 employees, and 26 offices. The Firm is a member of Nexia International, a global network of independent accountancy, tax, and business advisors.

1212 Avenue of the Americas New York, NY 10036 212-297-0400

www.cohnreznick.comCohnReznick is an independent member of Nexia International

CohnReznick LLP © 2014This has been prepared for information purposes and general guidance only and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is made as to the accuracy or completeness of the information contained in this publication, and CohnReznick, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you and anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

Circular 230 Notice: In compliance with U.S. Treasury Regulations, the information included herein (or in any attachment) is not intended or written to be used, and it cannot be used by any taxpayer for the purpose of i) avoiding penalties the IRS and others may impose on the taxpayer or ii) promoting, marketing or recommending to another party any tax related matters.

![Archaeology and State Formation in the Middle East.ppt Repaired]](https://img.pdfslide.us/doc/110x75/542080817bef0a9c458b4578/archaeology-and-state-formation-in-the-middle-eastppt-repaired.jpg)