Embed Size (px)

Citation preview

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 144

Capital InsightsHelping businesses raise invest preserve and optimize capital

SAPrsquos Werner Brandt on smartMampA organic growth andclear capital management

Makingthe market

The top 10 acquirers

India open for business

Asset managementthe dawn of a new era

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 244

Capital Insights from the Transaction Advisory Services practice at EY

For EYMarketing Director Leor Franks(lfranksukeycom)

Program Director Nathaniel Hass(nhassukeycom)Consultant Editor Richard HallCompliance Editor Jwala PoovakattCreative Manager Laura HodgesCreative Executive Jess CowleyDesign Consultant David HaleSenior Digital Designer Christophe MenardDeployment Executive Angela Singgih

For RemarkEditor Nick CheekAssistant Editor Sean LightbownHead of Design Jenisa PatelDesigner Anna ChouProduction Managers Daniela SchichorDavid SwettenhamEMEA Director Simon Elliott

Capital Insights is published on behalf of

EY by Remark the publishing

and events division of Mergermarket Ltd

80 Strand London WC2R 0RL UK

wwwmergermarketgroupcomevents-publications

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance tax transactionand advisory services The insights and qualityservices we deliver help build trust and condence

in the capital markets and in economies the worldover We develop outstanding leaders who team todeliver on our promises to all of our stakeholdersIn so doing we play a critical role in building a betterworking world for our people for our clients and forour communities

EY refers to the global organization and mayrefer to one or more of the member rms of EY

Global Limited each of which is a separate legalentity EY Global Limited a UK company limited byguarantee does not provide services to clients Formore information about our organization please

visit eycom

About EYs Transaction Advisory Services How organizations manage their capital agendatoday will dene their competitive position

tomorrow We work with our clients to helpthem make better and more informed decisionsabout how they strategically manage capitaland transactions in a changing world Whetheryoursquore preserving optimizing raising or investingcapital EYrsquos Transaction Advisory Services bringtogether a unique combination of skills insightand experience to deliver tailored advice attunedto your needs mdash helping you drive competitiveadvantage and increased shareholder returnsthrough improved decision-making across allaspects of your capital agenda

copy 2013 EYGM Limited

All Rights Reserved

EYG no DE 0433

ED 1013

This material has been prepared for general

informational purposes only and is not intended to be

relied upon as accounting tax or other professional

advice Please refer to your advisors for specic advice

The opinions of third parties set out in this publication

are not necessarily the opinions of the global

EY organization or its member rms Moreover

they should be viewed in the context of the time

they were expressed

wwweycomServicesTransactions

ContributorsCapital Insights would like to thank the following

business leaders for their contribution to this issue

A l l d a t a i n C a p i t a l I n s i g h t s i s c o r r e c t a t 1 J u l y 2 0 1 3 u n l e s s o t h e r w i s e s t a t e d

copy P

a u l H e a r t f e l d

Helping businesses raise invest

preserve and optimize capital

P r e s e r v

i n g O

p t i m i z

i n g

R a i s

i n g

I n v e s

t i n g

Gunjan Bagla

Author Doing

Business in 21st

Century India

James M Loree

President and

COO

Stanley Black amp

Decker

Wolf-Dieter

Starp

Head of Global

MampA

BASF

Hugh Young

Managing

Director

Aberdeen Asset

Management Asia

Alix Stewart

Head of UK

Corporate

Bonds

Schroders

Mike Teng

CEO

Corporate

Turnaround

Centre

Bill Bohstedt

Vice President mdash

MampA Arthur J

Gallagher amp Co

Cedric Collange

Senior Vice

President for

MampA Schneider

Electric

Rob Conn

Founder

Innova Capital

Elizabeth

Corley

CEO Allianz

Global Investors

Arvind Dham

Chairman

Amtek Auto

Group

Barry Donlon

Managing

Director DCM

EMEA

UBS

Yves Doz

Professor

of Strategic

Management

INSEAD

Ed Dymott

Head of

Business

Development

Fidelity

Anna Faelten

Deputy Director

MARC

Cass Business

School

Campbell

Fleming

CEO

Threadneedle

Investments

Ehud Ronn

Professor of

Finance

University of

Texas at Austin

Prashant Mara

Head of India

Practice

Osborne Clarke

Chetan Modi

EMEA Head

of Leverage

Finance

Moodys

Brian May

Finance Director

Bunzl

Massimo Tosato

Global Head of

Distribution

Schroders

Adrian MuttonCEO

Sannam S4

Angad PaulCEO

Caparo

Piers

Prichard-Jones

CorporatePartner

Freshelds

Brendon Moran

Co-head

CorporateOriginations

Socieacuteteacute Geacuteneacuterale

Werner Brandt

CFO SAP

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 344

For more insights visit wwwcapitalinsightsinfo where you can find our latest

thought leadership including our market-leading Capital Confidence Barometer

Joachim Spi

Transaction Advisory Services Leader EMEI

(Europe Middle East India and Africa) at E

If you have any feedback or questions please email joachimcapitalinsightsinf

American golfing great Jack Nicklaus once said ldquoConfidence is

the most important single factor in this gamerdquo The same notion

rings true for MampA And thankfully it appears that confidence in

dealmaking is returning to the boardroom

In EYrsquos latest Capital Confidence Barometer (CCB) released in

April 72 of respondents said they expected global deal volumes to

improve over the next year Overall economic confidence has improved

significantly 87 of those surveyed in the CCB view the global economy

as either stable or improving up from 69 in October 2012

As self-belief grows business leadersrsquo focus shifts back to investing

So in this issue of Capital Insights we explore how companies can get

the very best from their deals

MampA is a three-act story First pinpointing the right locations

Second doing the deal Third ensuring that post-merger integration

plans are ready early And we have key insights for every stage

On page 30 we explore why companies need to take a more targeted

approach when entering rapid-growth markets Elsewhere corporates

both inside and outside India provide insights into how to get the best ou

of deals in Asias third-largest economy (page 24) And on page 20 we

investigate how to pull off a successful post-merger integration planThese issues are brought together in our in-depth and exclusive

interview with SAPrsquos CFO Werner Brandt He tells us how brave

acquisitions and a strong integration policy have helped SAP become

Europersquos most successful technology company (page 14) In another

exclusive story (page 8) we reveal the top 10 acquirers of the last five

years and analyze what other corporates can learn

Itrsquos good news that confidence is making a comeback but it needs

to be allied to a strong deal rationale proper preparation and a clear

growth strategy For those not only looking to do deals but also to raise

preserve invest and optimize capital I hope that this issue of EYs

Capital Insights will help give you the tools to go with your appetite

Confidence breeds success

wwwcapitalinsightsinfo | Issue 7 | Q3 2013 |

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 444

14SAP

Features8 Transaction insights The top 10

In a special edition of ldquoTransaction insightsrdquowe reveal the top 10 acquirers since 2008and discuss MampA with some of the worldrsquosmost acquisitive corporates

14 Cover story Making the market

SAP CFO Werner Brandt reveals howintelligent deals innovation and clear capitalmanagement have helped the Europeantechnology giant to thrive

20 Put the pieces togetherIt may not grab the headlines quite like a dealannouncement but post-merger integrationis vital to MampA success We identify the topfactors behind uniting companies correctly

24 India IncAs one of the worldrsquos leading emerging

economies the Asian giant is a key target forthose looking to grow But what do companiesneed to know before investing in India

30 Taking aimCorporates from developed economies areincreasingly looking to emerging nations forgrowth But how can companies target thesemarkets effectively

34 The big issuanceCorporate bond markets are boomingBut as a source of capital is their growth

in popularity sustainable or will governmentaction change the funding cycle again

38 Taking care of businessAsset management emerged relativelyunscathed from the nancial crisis But

the industry must push for innovation andmanage regulation to reach its full potential

8Top 10 acquirers

WINNER 2012

EY is proud to be the FinancialTimesMergermarket EuropeanAccountancy Firm of The Year

1EY mdash recognized by Mergermarket as

top of the European league tables for

accountancy advice on transactions

in calendar year 2012

As run on 7 January 2013

C o r b i s L y n s e y A d d a r i o V I I

copy P

a u l H e a r t f e l d

G e t t y I m a g e s Z e n S e k i z a w a

Capital Insights from the Transaction Advisory Services practice at EY

Capital InsightsHelping businesses raise invest preserve and optimize capital

Q 3 2 0 1 3

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 544

On the web or on the moveCapital Insights is available online and on your mobiledevice To access extra content and download the appvisit wwwcapitalinsightsinfo

Regulars06 HeadlinesThe latest news in the world ofcorporate fnance and what it means

for your business

07 Deal dynamicsEYrsquos Paumlr-Ola Hansson explains howcompanies can establish a successfulplatform in brand-new countries

29 The PE perspectiveEYrsquos Sachin Date discusses how privateequity needs to work hard to attractlimited partnersrsquo capital

42 Moellerrsquos cornerMampA Professor Scott Moeller reveals thesigns that show a deal is in trouble andhow corporates can mitigate the risks

43 Further insightsFind out about exclusive content

available on the Capital Insights website

(wwwcapitalinsightsinfo) and new

apps Plus details on three EY thought

leadership reports on rapid-growth

markets private equity and working

capital management

30MampA targeting

India 24

Corporate bonds34

G e t t y I m a g e s W e s t e n d 6 1

D o r l i n g K i n d e r s l e y

wwwcapitalinsightsinfo | Issue 7 | Q3 2013 |

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 644

Capital Insights from the Transaction Advisory Services practice at EYCapital Insights from the Transaction Advisory Services practice at EY

HeadlinesEmerging bonds boomEmerging market corporates are set to overtake

their developed peers in terms of debt

Standard and Poorrsquos (SampP) figures show that

Chinarsquos corporates could owe US$138t by the

end of 2014 more than the US$137t set to be

owed by the US This figure could reach US$18t

by 2017 mdash over a third of the US$53t that SampP

expects global companies will need in terms

of debt and refinancing And in May Brazilrsquos

Petrobas (pictured below) sold US$11b-worth

of bonds on a single day mdash the largest bond issue

by an emerging market company ever With

investors hungry for returns corporates in rapid-

growth economies are in an ideal position to tap

the market For more on bonds see page 34

Safety first for fundsAsset managers are playing safe when it comes

to distributing their investorsrsquo capital The BofA

Merrill Lynch Fund Manager Survey for June

revealed that fund managers are focusing more

on the US and Japan whereas by contrast

emerging markets are being shunned Global

emerging market equity allocations are at their

lowest since 2008 according to the survey

with a net 9 underweight in that area Opti-

mism in Europe is returning however with 6

of asset allocators overweight in that area mdash a

14 percentage point swing from Mayrsquos survey

Managers should be wary of balancing the

need to safeguard funds with the imperative

to generate returns For more on the asset

management sector see page 38

Time to bet on India India could be in store for a deal boom as inter-

national corporates look to tap the countryrsquosincreasingly prosperous population Consumer

spending growth in India is expected to average

89 in the next five years according to market

researcher Euromonitor On the back of this

foreign company bids for Indian food drink

cosmetic and household goods businesses

reached a record US$56b in the year to

15 May according to Bloomberg Examples in-

clude Unileverrsquos offer to raise its majority stake

in Hindustan Unilever Corporates continuing

the search for new growth areas would do well

to keep an eye on this Asian tiger For more onIndia see page 24

Confidence is coming back Corporate executives are getting ready to invest

their capital again In EYrsquos latest Global Capital

Confidence Barometer (GCCB) mdash a survey of

almost 1600 senior executives from around

the world mdash 40 now feel their organizationrsquos

focus lies in investing over the next year up

from 32 year on year Additionally 51 feel

the economy is improving up from 22 in

October 2012 And despite lower-than-normal

MampA volumes 72 expect global deal numbers

to improve while almost a third expect to do

a deal themselves within the next 12 months

These levels of confidence are a boost for

economies worldwide as well as for companies

looking to divest assets For more on the

GCCB visit wwwcapitalinsightsinfogccb

tc

GettyImagesManpreetRomanaStringe

r

crGettyImagesKrzysztofDydynski

The changing face of risk The risks involved in cross-border MampA

transactions are changing Law firm Baker

amp Mckenziersquos Opportunities in High-Growth

Markets Trends in Cross-Border MampA report

shows that concerns over cultural barriers

are diminishing as globalization presses on

with issues over corporate compliance (46

of respondents) as the top legal or regulatory

challenge Corruption is not so high with 29

of those surveyed considering it a main issue

Only accounting or business fraud (20) is

seen as less of a threat Additionally 50

believe that pre-transaction integration plan-

ning is the biggest factor in mitigating deal-

execution risk As challenges change in cross-

border deal-making corporates competing on

foreign soil need to be aware of the changing

deal climates in these new regions

The consumer evolutionThe consumer sector is undergoing a deal-

making revolution in response to a changing

economic climate EYrsquos Consumer products deals

quarterly Q1 2013 shows that there were 347

announced consumer deals in the first three

months of this year a 9 increase on deals from

Q4 2012 Acquisitions by private equity groups

in the consumer industry fell however from 60

to 55 over the same period The US still makes

up the bulk of the sectorrsquos deal activity making

up eight of the sectorrsquos top 10 deals by value

mdash the June 2013 buyout of Heinz by private

equity firm 3G and conglomerate Berkshire

Hathaway being a prime example and the largest

deal in Q1 2013 However corporates should

keep an eye on rapidly expanding consumer

markets outside their borders as well For more

on targeting emerging markets see page 30

P r e s e r v

i n g O p t i m

i z i n g

R a i s

i n g

I n v e s

t i n g

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 744

Paumlr-Ola Hansson is EMEIA Markets Leade

Transaction Advisory Services EYFor further insight please ema

par-olacapitalinsightsinf

Deal dynamics

Paumlr-Ola Hansson

The search for growth will leadmany corporates to boldly go

where they have not gone before

In regional terms this means

moving beyond developed markets and

into rapid-growth markets (RGMs) such

as Turkey Vietnam and Chile EYrsquos Rapid-

Growth Markets Forecast published in April

expects growth in the RGMs to accelerate

from 47 in 2012 to 6 in 2014

However entering a market where your

business has no previous presence requires

corporates to make several vital decisions

When looking to penetrate new marketscorporates must decide whether to create

alliances with local firms or build the

business alone This depends on the region

sector and nature of the business

For companies in highly regulated

sectors finding a strong local partner is

often vital for establishing a business For

instance in the financial services sector

Germanyrsquos Allianz acquired Turkish insurer

Yapi Kredi for euro684m (US$894m) in March

Board member Oliver Baumlte noted that ldquothis

transaction fits perfectly into Allianzrsquos

strategy to use bolt-on acquisitions to

strengthen its position in growth marketsrdquoFor more on finding the right JV partner

visit wwwcapitalinsightsinfojvs

On the other hand some companies

choose to take a more organic approach

This has been the case for Swedenrsquos IKEA

Its plans to open 25 stores in India were

approved by the Indian Government in May

As a privately owned company IKEA

is able to take a long-term approach to

investment in a new market As Juvencio copy P a u l H e a r t f e l d

As companies strive for growth they will ndthemselves heading into uncharted watersJust how do they establish a platform for success

unknown

Maeztu IKEArsquos India Chief Executive saidldquoWe will never compromise on a good

location So even if it takes five years to

[find] it is no problemrdquo

However many listed firms canrsquot wait

that long They have reporting requirements

and responsibilities to shareholders Itrsquos

more difficult for them to think long term

Whether a company enters organically

or via a partnership another issue is finding

the right model to monitor the organization

The key argument here is centralization

versus localization Corporate development

officers who have no corporatedevelopment function in new regions

need to redefine how they work That can

mean moving decision-making power from

headquarters to where the business is

growing A prime example of this came in

September 2012 when human resources

consultancy Aon Hewitt opened a new

office in Indonesia as part of its regional

expansion strategy At the time Edouard

Merette CEO of Aon Hewitt Consulting

in Asia Pacific said ldquoThe fast-growing

economy of Indonesia offers Aon Hewitt

an important business opportunity as

we continuously develop and affirm ourpresence throughout Southeast Asiardquo

There is also increasing pressure for

corporate social responsibility Companies

need to take environmental concerns into

account and engage in the communities

and cultures they enter

Clear strategy regional accessibility

and cultural accountability are the three

key drivers when seeking growth in a brave

new world

A step into the

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 844

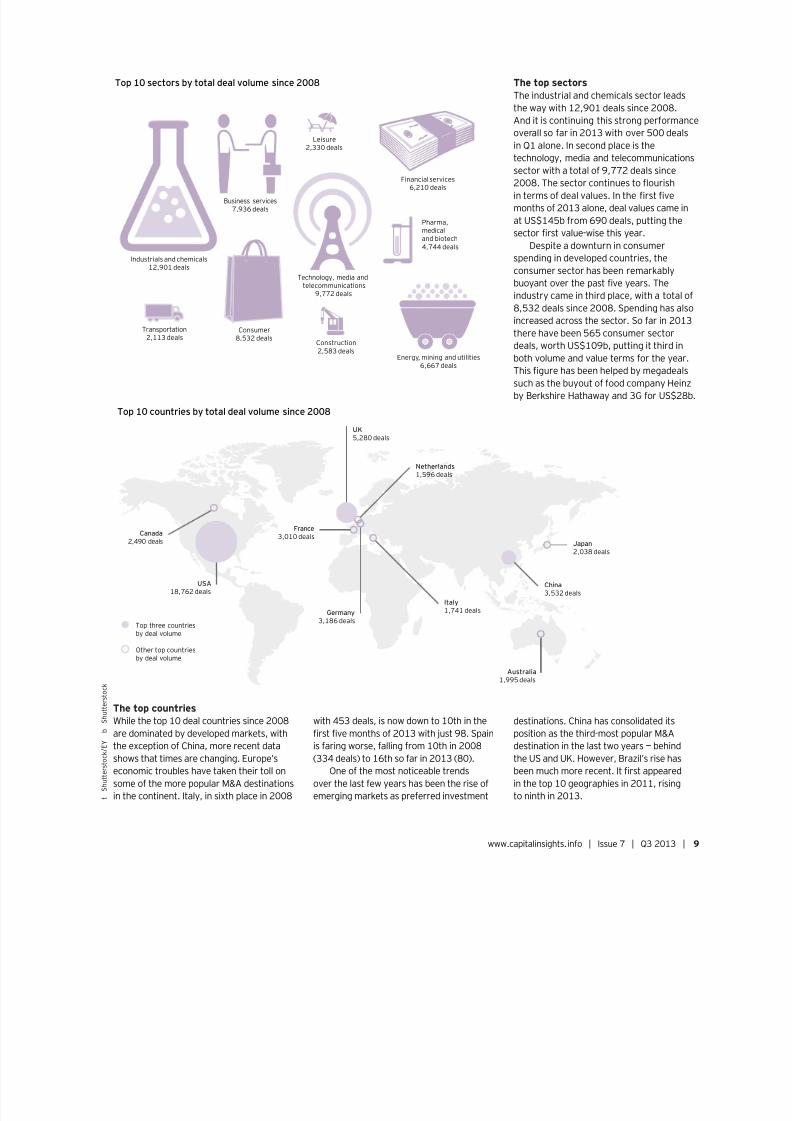

TransactioninsightsKey facts and gures from the world of MampA This issue the top 10corporate acquirers by volume of the last ve years Plus the biggestdeal sectors and countries since 2008

Acquisitions are key drivers behind corporate

development and growth But which companies

have been buying the most and what insights can

other acquisitive corporates gain from the broadexperience of those who are most active These

are the questions Capital Insights asks and with

data supplied by Mergermarket looks to answer In

addition we reveal the top 10 sectors and regions

by deal volume since 2008 (see figures page 9)

The breakdown of the top 10 shows a mixture of

sectors regions and corporate sizes mdash proving that

growth via acquisition is not just limited to giants

such as Google and IBM With that in mind on page

10 we talk exclusively to corporate leaders from

three of the top 10 mdash Capita Arthur J Gallagher

amp Co and Bunzl mdash to discover more about their

growth strategies their rationale for deals and

some of the challenges they face and how theyhave overcome these

Meanwhile a breakdown of the top 10 sectors

(top page 9) since 2008 shows that the industrials

and chemicals sector has seen the most deals

followed unsurprisingly by the technology media

and telecommunications industry In terms of

regions (bottom page 9) it is interesting to note

that while developed economies dominate China

is in third place and Brazil India and South Korea sit

just outside the top 10

Methodology

bull The data for the top 10 has been

gathered from the Mergermarket

database of MampA transactions

bull The table shows deals conducted

by top-level companies across

the world from January 2008

to April 2013

bull The data only includes deals by

the parent company recorded on

the Mergermarket database It

does not include private equity

deals joint ventures lapsed or

subsidiary deals As a result deal

volumes may differ from those

expressed by the corporates

themselves

bull For further Mergermarket

deal criteria please visit www

mergermarketcompdfdeal_

criteriapdf

Big dealersThe table right showsthe top 10 acquirers since2008 by deal volumeaccording to MergermarketWe have chosen this periodto show which companieshave been most acquisitive

post financial crisisThe table shows the

deal landscape of the pastfive years and the top 10 isnot just limited to corporategiants While some suchas tech companies Googleand IBM are predictableserial acquirers due to thesectorrsquos history of big namessnapping up smaller start-ups others are from sectorswhich are traditionally lessacquisitive For instanceArthur J Gallagher amp Coand Bunzl are from theinsurance and distributionindustries respectively

In terms of geographythe US can boast fourcorporates in the top 10while Europe and Japanhave three apiece

Top 10 acquirers 2008mdash2013

Company Country Sector Deal volume

1 Google US Technology 50

2 IBM US Technology 49

3 Capita UK Outsourcing 43

4 Mitsui amp Co Japan Trading house 41

5 Marubeni Japan Trading house 40

6 Mitsubishi Japan Trading house 39

7 International Finance

CorporationUS Financial services 39

8 Arthur J Gallagher amp Co US Financial services 37

9 Assa Abloy Sweden Security 32

10 Bunzl UK Distribution 31

Capital Insights from the Transaction Advisory Services practice at EY

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 944

t

S h u t t e r s t o c k E Y

b

S h u t t e r s t o c k

The top sectorsThe industrial and chemicals sector leads

the way with 12901 deals since 2008

And it is continuing this strong performanc

overall so far in 2013 with over 500 deals

in Q1 alone In second place is the

technology media and telecommunications

sector with a total of 9772 deals since2008 The sector continues to flourish

in terms of deal values In the first five

months of 2013 alone deal values came in

at US$145b from 690 deals putting the

sector first value-wise this year

Despite a downturn in consumer

spending in developed countries the

consumer sector has been remarkably

buoyant over the past five years The

industry came in third place with a total of

8532 deals since 2008 Spending has also

increased across the sector So far in 2013

there have been 565 consumer sectordeals worth US$109b putting it third in

both volume and value terms for the year

This figure has been helped by megadeals

such as the buyout of food company Heinz

by Berkshire Hathaway and 3G for US$28b

The top countriesWhile the top 10 deal countries since 2008

are dominated by developed markets with

the exception of China more recent data

shows that times are changing Europersquos

economic troubles have taken their toll on

some of the more popular MampA destinations

in the continent Italy in sixth place in 2008

USA

18762 deals

Germany

3186 deals

Australia

1995 deals

UK

5280 deals

Top three countries

by deal volume

Netherlands

1596 deals

Italy

1741 deals

China

3532 deals

Japan

2038 deals

Other top countries

by deal volume

Top 10 countries by total deal volume since 2008

Canada

2490 deals

France

3010 deals

Transportation

2113 deals

Technology media and

telecommunications

9772 deals

Industrials and chemicals

12901 deals

Financial services

6210 deals

Energy mining and utilities

6667 deals

Consumer8532 deals

Leisure

2330 deals

Pharma

medical

and biotech

4744 deals

Business services

7936 deals

Construction

2583 deals

Top 10 sectors by total deal volume since 2008

with 453 deals is now down to 10th in the

first five months of 2013 with just 98 Spain

is faring worse falling from 10th in 2008

(334 deals) to 16th so far in 2013 (80)

One of the most noticeable trends

over the last few years has been the rise of

emerging markets as preferred investment

destinations China has consolidated its

position as the third-most popular MampA

destination in the last two years mdash behind

the US and UK However Brazilrsquos rise has

been much more recent It first appeared

in the top 10 geographies in 2011 rising

to ninth in 2013

wwwcapitalinsightsinfo | Issue 7 | Q3 2013 |

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1044

The last five years have been

turbulent for the MampA market

This period culminated with

a peak at the end of 2012

The yearrsquos final quarter saw the highest

MampA values since 2008 (US$737b from

3565 deals) according to Mergermarket

There has been a slowdown this year with

the 2789 deals in Q2 2013 comparing

unfavorably with Q2 2012rsquos 3327

However the number of megadeals takingplace such as Liberty Globalrsquos US$219b

buyout of Virgin Media combined with rising

confidence among corporates means that

there is room for increased optimism

EYrsquos Capital Confidence Barometer

(CCB) published in April shows that 72 of

respondents expected volumes to rise over

the next year Half are also more confident

about the number of opportunities available

compared with 37 in October 2012

Against this background of renewed confidence

we have looked back at the top 10 acquirers by volume

over the last half decade to uncover why they have been so

acquisitive and what other corporates can learn from their

deal strategies

Deal hungrySince 2008 those in the top 10 have done more than 400

deals between them The reasons why they have chosen

MampA for growth are as varied as the sectors they represent

Bill Bohstedt Vice President mdash MampA for US property andcasualty mergers at insurance broker Arthur J Gallagher

amp Co (AJG) believes that the rationale for acquisitions is

about finding the perfect partner to grow the business

ldquoThat was really our core vision for MampA growth finding

good merger partners who fit into our culture and wanting

to keep growing By coming together with us we grow better

together than we could if we were separaterdquo says Bohstedt

A similar sentiment is echoed by Ian West Director

of MampA for Capita the UK outsourcing group ldquoSmall

to medium-sized acquisitions that take us into new

The way

The top acquirers tell us about the strategieschallenges and keys to a successful deal

forward

GettyImagesZenSekizawa

Capital Insights from the Transaction Advisory Services practice at EY

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1144

complementary areas and strengthen our

capabilities and scale have always played

a key role in Capitarsquos growthrdquo says West

Google has also stated that acquisitions

are about finding a perfect synergy between

bidder and target ldquoThe important thing

I look for is alignment between what the

entrepreneur wants to do with their product

and their company and what Google wants

to dordquo said David Lawee Googlersquos Vice

President of Corporate Development in

an interview in 2012 ldquoIf there is perfect

alignment then it has a very high chanceof success If there is not then we should

not be doing itrdquo

For IBM second in the table one of the

key drivers is innovation ldquoSmall companies

are started around a great idea to change

the worldrdquo said Steve Mills IBMrsquos Senior Vice

President and Group Executive for Software

and Systems at an information and analytics

forum last October ldquoBig companies through

acquisitions and RampD are also driving some

part of that innovation agendardquo

Breaking new groundAccording to Bunzlrsquos Finance Director Brian

May the companyrsquos acquisition rationale is

twofold to consolidate the business as well

as to break into new territories

Since 2008 the UK distribution giant

has spent an average of pound167m (US$257m)

per year on acquisitions ldquoWersquore in a

fragmented marketplacerdquo says May ldquoWe

are an acquisitive company the only one

consolidating in our industry mdash one that is

mainly comprised of family-run businessesrdquo

Bunzl has targeted South America mdash in

particular Brazil mdash as a key area for growth

Over the past five years the company hasundertaken a targeted acquisition strategy

to build the business there As recently as

March it bought medical supply business

Labor Import based in Sao Paulo

ldquoWe identified Brazil a market of 200m

people as a place with the scale and size of

GDP that makes it interesting for us Having

then researched the market we found there

existed suitable acquisition candidates

Brazil has the need for distribution whereas

in the other BRICs there isnrsquot that level of development

in our marketrdquo says May

The three Japanese trading houses in the list mdash Mitsui

amp Co Marubeni and Mitsubishi mdash have also made overseas

acquisitions something of a priority in recent years A good

example of this has been Marubenirsquos US$26b acquisition of

US grain trader Gavilon in June this year

When the deal was first announced in May 2012 the

company stated in its annual report that ldquoThis will further

raise Marubenirsquos global profile in grain trading More

importantly it will make it possible to address expanding

demand for grains in China and other emerging countriesrdquo

Swedish lock maker Assa Abloy has also usedacquisitions to break into emerging markets mdash in particular

China where it bought two companies Shandong Guoqiang

and Sahne Metal in 2012 Speaking at the beginning of the

year Chief Executive Johan Molin stated in an interview that

the volume of deals was a

result of having to compete

in emerging markets

ldquoAs people [in emerging

markets] get wealthier they

will spend more money on

door openingrdquo he said

ldquoThere are often very low-

quality doors in emerging marketsrdquo

Family values and volumeTaking the acquisition route to growth is often going to

be fraught with challenges For the high-volume acquirers

interviewed by Capital Insights the three key issues

identified were the type of companies on offer the volume of

businesses available and the valuations that the targets set

Doing deals in Bunzlrsquos sector often involves dealing with

family businesses This brings challenges for many firms

particularly when operating in emerging markets

ldquoWhen dealing with family businesses you need to

engage and build a greater level of trust We have separate

management teams and their heads will form relationships

with businesses we would ultimately like to buy Familiesdonrsquot want their business consumed and their identity

changed significantlyrdquo says May

ldquoThe deals often come when they need more investment

But we do relatively little with the front office The customer

relationships and supplier relationships we leave with the

families who we usually tie in to stay In the main it is what

they want as well as they have often reached the point

where to go to the next level is beyond their own resourcesrdquo

Itrsquos not only the types of businesses that pose issues

There is also the dilemma of getting a decent volume of

On the webFor more on how EYrsquos Capital Confdence Barometer affects CFOs readThe CFO Perspective mdash at a glance at wwwcapitalinsightsinfoccbcfo

Our challenge is to cast ournet as wide as possibleand get managementspreading the messageBill Bohstedt VP mdash MampA Arthur J Gallagher amp Co

wwwcapitalinsightsinfo | Issue 7 | Q3 2013 | 1

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1244

businesses In the case of Bunzl ensuring

they have a good supply-line can sometimes

be the issue ldquoThere are the ongoing

challenges of getting a good supply of

businesses Overcoming this is all about

getting the right timing and building trust in

advancerdquo he says

For AJG the opposite is true Thereare around 38000 independent insurance

agencies in the US And the challenge is to

reach out to as many as possible in an effort

to find the most suitable partners

ldquo[To overcome] this issue we have to

have as many management people meeting

these merger partners in their areas and

at events and starting a dialoguerdquo says

Bohstedt ldquoBecause when they get ready to

sell we want them to know who we are and

consider us as a potential partner

A new perspectiveEYrsquos Pip McCrostie on what is needed to lift MampA activityfrom its lowest levels since the nancial crisis

ldquoIf we havenrsquot had that dialogue they may decide tomerge with one of our competitors Our challenge is to cast

our net as wide as possible and get management spreading

the message about the benefits of joining usrdquo

However arguably the main issue that many buyers face

is the valuation gap between themselves and their targets

In Aprilrsquos CCB 44 of respondents expected valuations to

increase over the next 12 months compared with only 31

in October 2012 For Ian West at Capita the solution is

disarmingly simple mdash stick to your guns

ldquoBeing disciplined around pricing is a critical factor for

doing the number of deals we do and for generating the

value that these acquisitions will ultimately createrdquo West

says ldquoThe biggest challenge is the temptation to becomelsquobusy foolsrsquo by chasing deals where pricing will always be

too high Itrsquos important to know when to leave well alone

or to walk awayrdquo

The high-volume acquirers all point to three key

messages when it comes to successful deals mdash find the right

partner agree on the right price and get the post-merger

integration (PMI) right (for more on this see the PMI

feature on page 20) And they should know With over

400 deals mdash many more if you include subsidiary and

joint venture deals mdash between them in the last five years

theyrsquove had the practice

What is your expectation for global MampAdeal volumesin the next 12 months

Decline

Remain the same

Improve

Return tohistoric highs

3

69

23

5

12

3

45

Itrsquos a tough time for MampA

However as wersquove seen markets

can change quickly If there is to

be an upswing in MampA this year

and beyond the following five

changes need to happen

Greater economic stability and

confidence in growth Therehas been more stability around

macroeconomic issues such as

the Eurozone but investors want

to see this translating into an

outlook for growth

Long-term stability in equity

markets This would provide

a more robust longer-term

view on valuations

and prices

Clarification on

QE unwinding The

complex impact of

the withdrawal of

QE and its influence

on the economy and equityindices is critical to better

understanding growth prospects

and asset prices

Greater shareholder influence

on investments Many large

corporates have big cash

piles Shareholders may want

that money to be utilized and

Pip McCrostie

is Global Vice ChairTransaction AdvisoryServices EY

inorganic growth could be part

of that equation

Bold movers Three-quarters of

big corporates expect MampA to rise

yet less than a third intend to do

a deal The lsquoyou firstrsquo sentiment

could turn into lsquome toorsquo if bold

moves are made and competitors

are seen to be establishing an

advantage via MampA

Source EY Capital Confdence Barometer

G e t t y I m a g e s A i r R a b b i t

Capital Insights from the Transaction Advisory Services practice at EY

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1344

EY expertsSteve Krouskos

(SK) is Deputy

Leader GlobalTransaction Advi-

sory Services EY

Charles Honnywill(CH) is EuropeanHead of Sell Side

Services Trans-action Advisory

Services EY

M983078A The art of

The top 10 acquirers have shown that sector region orindeed size is no barrier to acquisition activity Two EYexperts give their views on the results

What are your thoughts on the top 10

SK Itrsquos a varied list I wasnrsquot surprised by the

variation in there as there has been no over-

riding theme driving the market I also wasnrsquot

surprised by the three Japanese companies

CH I am a little surprised that there were

two UK-based businesses but not so much by

the Japanese ones I think we are seeing the

beginning of a huge outflow of capital from

Japan There arenrsquot enough good-quality

businesses in Japan to invest in for growth

Will tech firms continue to be as active

SK I think tech will be one of the more

active sectors maybe not with headline

deals but more mid-sized acquisitions Itrsquos

driven by rapid change in the sector such as

the evolution to cloud big data and mobile

applications There is a lot of disruption in

the sector and companies are placing a wide

array of bets to solidify their position

CH They will continue to acquire

high-quality services that they donrsquot have

acquiring in lieu of in-house RampD Butfor the bulk of what they need to do to

grow their businesses which is customer

acquisition and growing share of spend

they will continue to do that organically

What drives firms to be so acquisitive

CH First a number of them will need to

infill services that they cannot readily build

internally IT companies in particular need

to buy services that consumers will findattractive The second reason is that some

of these deals have been defensive mdash beating

competitors by building market share Finally

a number of these organizations have capital

and need to deploy it in new markets

SK Itrsquos hard to find a single theme A lot

of these are simply unique opportunistic

companies in search of growth In the early

portion of the last five years there were

more consolidating deals to capture cost

efficiencies But as we move forward deals

are more about access to new marketsproducts and trying to control supply chains

Which sectors will be most acquisitive

over the next 12 months

SK If you look at our most recent CCB

I think sectors standing out are automotive

life sciences technology and oil and gas

CH Therersquos also likely to be some big deals

in sectors such as defense In mining therersquos

lots for sale but few buyers The volume

will be seen in health carelife sciences and

business services Within all sectors demandfor acquisitions that enable growth will be

the highest

Which countries will be most acquisitive

in the next 12 months

SK In terms of outbound deals Japanese

companies are cash rich and looking for

opportunities to deploy capital Chinese

and US companies will also be active These

companies will look increasingly to emergingmarkets and not just the BRICs but places

like Indonesia Africa and Colombia

CH I agree The Japanese will continue to

acquire looking toward the more developed

part of the Eurozone There will be more

acquisitions out of China it will be looking fo

high-quality assets to diversify away from th

Chinese mainland The other big area is the

US I believe that their businesses will move

capital from Europe to the Americas

After a slow start to 2013 what willkickstart the MampA market

CH I do think wersquoll see an uptick and will be

quite surprised by it Confidence is returning

because the imminent disasters feared from

the fiscal cliff the collapse of the Eurozone

and the issues with Cyprus have not come

to pass Available capital on balance sheets

and the debt available to those with the righ

credit rating will create the impetus

SK I expect some small improvements in

the second half of the year Companies have

cash and access to credit However I donrsquotsee one major event that will spark the

market Corporates are still concerned with

making mistakes but confidence will return

gradually as they get more comfortable

that there wonrsquot be a catastrophic event

That said I think this market offers a great

window of opportunity

For further insight please email

editorcapitalinsightsinfo

wwwcapitalinsightsinfo | Issue 7 | Q3 2013 | 1

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1444

Making themarketSAP CFO Werner Brandttells Capital Insights howsmart MampA innovativethinking and a clear capitalagenda have helped thecompany to expand itsposition as a global leader

Capital Insights from the Transaction Advisory Services practice at EY

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1544

W hen it comes to growing

a business in the ultra-

competitive technology

market companies that

want to succeed need to focus on the future

and then deliver it now

The sector is developing at a rapid rate

Global spending on information technology

(IT) products and services will grow 41 this

year to US$38t according to analyst firm

Gartner Only forward-thinking corporates

with a clear strategy will reap the rewards

This is borne out in a report from late2012 by research group International Data

Corporation which predicted that from

2013 through to 2020 technologies built

on mobile computing cloud services social

networking and big data analytics would drive

around 90 of all the growth in the IT market

This statistic highlights what Germanyrsquos

SAP the biggest technology company in

Europe and the worldrsquos largest vendor of

business applications decided to do some

years ago ldquoSAPrsquos success mdash 13 quarters

of double-digit growth in a row mdash is based

on the strategy that we laid out in 2010rdquosays CFO Werner Brandt ldquoIn addition to our

core business of applications and analytics

we chose to focus on three major areas

which will help us to double our addressable

market from US$100b to over US$200b by

2015 These areas are in-memory database

technology mobile and the cloudrdquo

Strategic moves into these three

categories alongside the continued focus

on the core businesses have helped SAP to

become one of the most valuable companies on the German

DAX index And itrsquos the only European name in the top 10

global high-tech businesses ldquoNow we are number nine but

our ambition is to rise higher in the marketrdquo says Brandt

SAP risingGrowth is the guiding principle at SAP and it is the priority

for the CFO when it comes to allocating capital ldquoAt SAP we

generate a very strong cash flowrdquo says Brandt ldquoAnd we use

cash for acquisitions to support the implementation of our

strategy The second allocation is for paying dividends to our

shareholders and the third usage is share buyback But in

the first instance we use cash to grow the businessrdquoSAPrsquos growth story is based around a mixture of a strong

MampA strategy and maximizing the potential of its existing

products in its five key market categories mdash applications

analytics cloud mobile and database technologies

In terms of organic growth the key weapon in SAPrsquos

arsenal is HANA a database evolving

into an application platform that provides

information on a real-time basis and

can analyze massive quantities of data

10000 times faster than traditional

databases It is the fastest-growing

product in the companyrsquos history

ldquoTo the end of Q1 2013 we haveaccumulated HANA revenue of euro640m (US$856m)rdquo

he says ldquoAnd through the huge potential of application

data being analyzed at high speed there will be a paradigm

shift for enterprise intelligence and an opportunity for

far greater growthrdquo

HANA is now being used by more than 1500 corporate

customers around the world in all industries ranging from

financial services to sports For example in February the

US National Basketball Association (NBA) announced that it

would be using HANA software to give fans unprecedented

access to nearly 70 years of statistical data HANA was

chosen by the NBA due to its speed flexibility and ability to

allow unlimited searches unlike more conventional products

ldquoHANA is one of our key organic growth drivers We need tostay focused and do everything we can to position HANA in the

right way so that it is adopted by all our customersrdquo he says

While HANA is driving organic growth SAP has made

some bold MampA moves in key areas of the business such as

cloud computing and mobile technology

High up in the cloudsThe cloud has long been seen as fundamental to the future

of the industry Indeed the cloud services market is forecast

to grow 185 this year to US$131b worldwide according

wwwcapitalinsightsinfo | Issue 7 | Q3 2013 | 1

Preserving

Investing

Optimizing

Raising

We use cash foracquisitions to supportthe implementationof our strategy

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1644

to Gartner SAP first

entered the market

with a homegrown

product some years

ago ldquoWe initially focused on a complete

solution in the cloud via a product calledBusiness by Design However we learned

that the cloud market was not ready for such

a comprehensive approachrdquo says the CFO

ldquoSo we decided that we would invest via the

acquisition of more focused cloud solutionsrdquo

SAP bought the cloud software company

SuccessFactors in February 2012 for

US$34b and followed this up in October

2012 with the acquisition of business-to-

business trading network Ariba for US$43b

ldquoIn the cloud business these acquisitions

were bold But today we are number two in

the market and closing the gap to numberone For this year we already expect total

cloud revenue to approach US$13b We are

among the fastest-growing cloud companies

worldwiderdquo says Brandt

These acquisitions took SAPrsquos cloud

business to another level and meant it could

provide a uniquely broad offering ldquoWe are

driving the adoption of the cloud holistically

while other cloud players focus on specific

products for individual lines of businessrdquo he

says ldquoWe have offerings around all business

aspects whether related to money people

suppliers or customers and in addition we

provide a full suite in the cloud Our complete offering and

the seamless integration into on-premise solutions make us

unique and provide triple-digit growthrdquo

SAP used the same targeted approach in the mobile

space In May 2010 it acquired the mobile software provider

Sybase for US$58b ldquoIt was clear that the world was going

mobile and we had to push ourselves into that business

Therefore we bought a company that was a leader in mobilerdquo

says Brandt ldquoSybase also had great database technology

experience which fitted perfectly into HANArsquos organic

development and added significant value for usrdquo

SAP is not just making big money moves such as the

SuccessFactors and Sybase deals It is also looking at smallertuck-in acquisitions such as online ticket provider Ticket-Web

which it bought in January and insurance software provider

Camilion purchased in May to complete the portfolio

Target practiceHowever given that many of SAPrsquos acquisitions were not

on the market how does SAP target these companies

ldquoWe look to acquire when we see a business that will give

us the chance to accelerate our growth strategy in our five

market categoriesrdquo says Brandt ldquoAnd more often than not

if you want to do this you have to get the number one in a

given industry mdash and these are normally not for sale

ldquoFor example we aimed to be a leader in the cloud sowe bought SuccessFactors which was and is the leader in

human capital management [HCM] the fastest-growing cloud

segment SuccessFactors really brought the cloud DNA to

SAP and today we have 29m users using our cloud HCM

solutions Then later we bought Ariba because it was number

one in supplier relationship management and had the biggest

enterprise network in the world for business Ariba manages

a transaction volume of nearly US$500b each yearrdquo

In addition to both companiesrsquo fast-growing status Brandt

outlines two other key factors in the acquisition process ldquoYou

have to ensure that you get a company that has the right

cultural fit and which will accelerate the implementation of

your strategyrdquo he says

1 9 7 2 1 9 8 81 9 8 6 1 9 9 0

SAP becomes a publicly traded

company International subsidiaries open

in Denmark Sweden Italy and the US

SAP opens its first

international subsidiary

in Austria

Company started under the name SAP Systemanalyse

und Programmentwicklung (System Analysis and

Program Development)

SAP acquires a 50 holding in German

software company Steeb and takes

over software firm CAS outright

copy P a u l H e a r t f e l d

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1744

In some cases these companies are

already working with SAP In the ever-

evolving technology industry in particular

itrsquos often worthwhile keeping an eye on

smaller partners who have industry-specific

knowledge This helps both partners to grow

and heads off potential future rivalries

ldquoIn our industry we are working in

an eco-system comprising thousands of

partners These include hardware technology

and implementation partners Sometimes

the solutions provided by our partners

become so attractive to our customers thatwe decide to buy these companies and build

up a new business This was the case with

Camilionrdquo says Brandt

Getting togetherA deal whether transformational or tuck-in

can be judged both by figures mdash turnover

and margin mdash and by the success of the

post-merger integration (PMI) As Brandt

puts it ldquoIf you invest almost US$8b in two

companies then you have to ensure that you

get the integration rightrdquo

For larger acquisitions such asSuccessFactors Ariba or Sybase SAP uses

a bespoke PMI model ldquoIf you look at our

history of integrating companiesrdquo says

Brandt ldquowe always use the tailor-made

approach to effectively integrate these

acquired companiesrdquo

In practice this means that SAP

approaches different acquisitions from very

different angles according to the CFO

ldquoWith the Sybase acquisition we had

acquired a business that was new to us So

we decided to bring together only the market

activities of both companies in order to

capture the potential growth

and combine the solution

offeringrdquo he says ldquoWe kept

the rest separate and then

after two years having learnt

about the database business

we integrated Sybase fully

from a development and

back-office perspectiverdquo

With Business Objects

a business intelligence

software company that

SAP acquired in 2008 forUS$48b the company used

another integration model

ldquoWhile Sybase was more

a partial integration over

time with Business Objects

we had bought a company

operating in the same field

We were blending the power

of our applications with

analytical applications so

we decided to fully integrate

right from the beginning

This also helped increaseefficiencyrdquo says Brandt

For the cloud

businesses SAP used yet

another approach which

the CFO refers to as a

ldquoreverse integrationrdquo In

this case the company took

its existing cloud business

and integrated it with the

acquired SuccessFactors

business to create a new

SAP cloud unit Brandt feels

that this approach has been

1 9 9 1 1 99 4 1 9 9 4 1 9 9 8

SAP acquires

a 52 stake in

DACOS Software

SAP is listed on th

New York Stoc

Exchang

SAP concludes a cooperative

agreement with the largest Russian

software company ZPS

SAPrsquos global expansion continues

as it opens its 19th international

subsidiary in Mexico

Lessons learned

1

24567 8

3

Werner Brandt explains SAPrsquos

tenets for successful growth

When it comes to organic growth you need

to stay focused on the product or service and

maximize its opportunities

Offer a complete product and services portfolio

The combination of five different market categories

is what makes SAP different from its competitors

Keep an eye on smaller partners who have an

attractive offering They can help the larger partner

to grow and head off potential future rivalries

With acquisitions always look for companies that

accelerate the implementation of your strategy and

have a good cultural fit

Ensure that you have a tailor-made integration

scenario for each acquisition and that each shares

one objective to capture top-line growth

When integrating companies ensure thatthe innovation capability of the target company

is preserved

When investing in a country build tight links with

that country SAP is not just there to sell but to

co-innovate to train people and bring them closer to IT

Wherever possible companies need to make

the market rather than react to what is going

on within it

1

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1844

extremely successful ldquoAfter you acquire abusiness what you normally see is a dip in

revenue for the acquired companyrdquo he says

ldquoBut if you look at SuccessFactors we grew

in triple digits from the first quarter on The

same holds true for Aribardquo

When it comes to smaller acquisitions

such as Camilion and Ticket-Web SAP has

a more standardized integration concept

ldquoFrom a back-office perspective it takes us

60 to 90 days maximum to fully integrate

and we also create a clear combination

from a go-to-market and a development

perspectiverdquo says BrandtWhy the difference between integration

models According to the CFO itrsquos a simple

matter of size and complexity

ldquoWith smaller companies we

usually buy a piece of technology

that we want to bring into the

market or a small solution that

helps us to accelerate in a given

environment or within a given

industry There is no need to

keep it separaterdquo he says

Acquisitions of any size have

a number of risks Yet Brandt

1 9 9 9 20052003 2007

SAP opens its ninth development

location outside Walldorf mdash in China

SAP announces a series of acquisitions

including strategy management provider Pilot

Software Yusa Wicom and MaXware

SAP invests nearly 15 of the yearrsquos

euro51b (US$68b) in revenue into

research and development

SAP buys several smaller companies including

retail providers Triversity and Khimetrics

feels that SAPrsquos bespoke approach helps to mitigate two key

post-merger issues mdash staff retention and innovation leakage

from the acquired company

ldquoThe first objective of an acquisition is to realize the

top-line synergies We do not buy for efficiency on the

bottom line we buy to grow And itrsquos very important that

you do everything to ensure that the growth of the acquired

company is not diminished This has a lot to do with people

The retention aspect is a very important onerdquo he says

ldquoOn the development side you have to ensure that the

innovation power within the given company is preserved

that it can develop on its own and is not diminished by the

big development organization that is SAP This is one reasonwhy we did the reverse integration of our cloud business into

SuccessFactors and then built the new SAP cloud businessrdquo

Get involvedThe company is not only looking to grow in its mature markets

such as Germany and the US it is also seeking expansion

across emerging markets in particular China Brazil and the

Middle East and North Africa (MENA) region And just as it

does with acquisitions and integration SAP takes a holistic

approach to its regional focus

ldquoIf we look at China we have more than 4000

employees there mdash 2000 of which are developers Itrsquos

not just a country where we want to sell software butalso a country where we have a huge and well-accepted

development organizationrdquo he says ldquoWe decided in 2011

that we would invest heavily in China mdash US$2b until 2015

We have increased our presence recently by hiring more than

1000 people mdash two-thirds on the sales side and one-third on

development We also decided to move our head of global

customer support to Beijingrdquo

This idea of becoming fully involved in a region to

maximize growth opportunities equally extends to both Brazil

and MENA ldquoIn Brazil four years ago we decided to take the

same approach of not only selling but also developingrdquo says

Brandt ldquoThis started with a development center for Latin

America in Satildeo Leopoldo We have about 500 people there

Being CFOWerner Brandt discusses

how his role works in SAP

There are different shades betweenthe roles of the CFO There is the

business partner role and there is the

stewardship role The business partner role helps the

company to grow and ensures that all the processes are

set up in a way that constantly improves efficiency

The stewardship role ensures that the company

fulfils all of its obligations from a governance

perspective mdash be that related to financial reporting or

adherence to business codes of conduct and compliance

copy S

A P A G

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 1944

2008 2010 2 0 1 2 2 01 2

SAP announces plans to buy Sybase for US$58b

Software revenues of euro15b (US$2b) in Q4 helps

SAP to its best quarter in history

SAP acquires clou

software provide

Ariba for US$45

SAP completes the acquisition

of Business Objects

SAP acquires cloud

application provider

SuccessFactors

and are doubling our capacity by setting

up a second facility This is an area that

has one of the most prominent universities

in Brazil We are attached to this university

and can attract young talent to SAPrdquo

In MENA SAP has taken a similar

approach ldquoWe have invested in training

and development centers expanded our

customer base and hired young professionals

We have done a lot in order to capture growth

in these countriesrdquo he says

Saving the dayWhile deals get the headlines and moves to

exotic emerging locations provide a level of

pioneering glamor to a business they could

not happen without the work that goes on

behind the scenes improving efficiency and

working capital management

In terms of enhancing efficiency SAP has

invested heavily in its shared service center

(SSC) infrastructure Finance transactions

are managed out of four service centers in

EMEA the Americas and Asia Pacific Many

of the companyrsquos transactional processes

are integrated into a SSC already and SAP ismoving more and more processes on top of

purchase-to-pay order-to-cash and record-to-

report to SSCs

When it comes to the day-to-day level of

improving working capital the CFO ensures

that the two complementary angles mdash day

sales outstanding (DSO) and day payments

outstanding (DPO) mdash are very closely

monitored in order to optimize cash flow to

fund acquisitions and further growth

ldquoWe have reduced DSO from 70 to 60

days over the last four years and have a

clear focus on being close to the payment

behavior of our customersrdquo says

Brandt ldquoWe use a new HANA-

based solution that enables each

manager to look into receivables

around the world via their

mobile devices

ldquoThis starts with the global

view and then you can dig down

into a country and really go

into a specific account to seehow the customerrsquos payment

behavior developed over time

Our internal solutions help our people understand and solve

disputes with customers quickly so they can payrdquo

On the payables side Brandt feels that the best way to

optimize the process is to look at a better way of collaborating

with suppliers This helps to get the best terms and conditions

after which he feels the company needs to pay on the agreed

day ldquoI donrsquot think itrsquos the right approach not to pay on time in

order to get better cash flowrdquo he says ldquoItrsquos better to discuss

and see that you have the optimal financial supply chain in

place in order to maximize your cash flowrdquo

Unique combinationSAPrsquos success story is a lesson in how a strong acquisition

and regional strategy a pinpoint focus on maximizing the

potential of existing products and services and solid capital

management can lead to substantial growth Yet Werner

Brandt feels that there is one final factor that gives SAP

an edge over its competitors a complete offering with

customers having mobile access to all solutions no matter

whether they are deployed on premise or in the cloud

ldquoIf you look at what we offer and the combination of the

five different market categories this makes SAP uniquerdquo

says Brandt ldquoI would argue that we make the market

instead of reacting to itrdquo

The CFO

Werner Brandt

Age 59

Appointed CFO at SAP 2001

Educated University of Nuremberg-Erlangen Technical University of

Darmstadt

Previous positions Prior to becoming CFO atSAP Werner was the CFO and Labor Director

of German-American health care companyFresenius Medical Care AG From 1992 to 1999

he was VP of European operations at health carecompany Baxter Deutschland responsible for its

financial operations in Europe

SAPFounded 1972

Employees 65000

Countries 130

Market capitalization US$74b(as of H1 2013)

copy SAP AG Reto Klar

1

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 2044

together

Put the pieces Deals that look goodon the surface can oftenfall apart due to poorintegration processesHow can corporatesovercome this challenge

and make the pieces t

Capital Insights from the Transaction Advisory Services practice at EY

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 2144

Key insightsbull Early planning is

vital for the successof a post-merger

integration teamsneed to be set up early

preferably during the

due diligence phase

bull Companies needto work out quickly

whether the objectiveof the deal is a full or

partial integration ofthe two businesses

bull Due diligence shouldgo beyond the financial

legal and regulatoryissues and into the

organizational andcultural areas

bull One key to success is

communication withall stakeholders

especially managementand employees

bull Integration is not ashort-term activity

but a process thatcontinues over a long

period and mustbe managed actively

and monitored

The post-merger integration (PMI) phase of an MampA

deal will never grab the headlines like the deal itself

Yet in many ways successful PMI of one company

into another is the only way to evaluate a deal

Bad integration is certainly seen as a key reason for a deal

failing A 2011 survey by insurance consultants Aon Hewitt

revealed that a longer than anticipated integration process

(41 of those surveyed) and cultural integration issues (33)were identified by organizations as the top two reasons for

deal failure So how can corporates overcome these hurdles

Early birdsEYrsquos EMEIA Operational Transaction Services Leader Max

Habeck strongly believes that early preparation is the key for

an effective PMI process ldquoBetter planning leads to successrdquo

he says ldquoSuccess is based on having a good understanding

of what you are buying and why you are buying and on

effective operational due diligence That should shape

realistic expectations of synergies Early mistakes here can

create big problems later You need clarity on the degree of

integration you are seeking You need to clearly match top-down and bottom-up viewsrdquo

Schneider Electric the multinational electricity

management company that has pulled off a string of

successful acquisitions in the past decade mdash including the

purchase of full ownership of Russiarsquos Electroshield TM

Samara in March this year mdash has made early planning a key

part of the integration process

ldquoThe integration model to be used is something we

discuss at a very early stage when we consider acquiring a

companyrdquo says Cedric Collange Schneider Electricrsquos Senior

Vice President for Mergers and Acquisitions ldquoIf you look at

this at the acquisition stage it is too laterdquo

German chemical company BASF has experience as a

successful integrator One year after its December 2010acquisition of nutritional supplier Cognis Samy Jandali Vice

President of Nutrition and Health in North America said

he had been ldquovery impressedrdquo with the integration of the

two firmsrsquo differing expertise areas This was backed up by

2011rsquos Q1 figures which showed BASFrsquos reported sales of

performance products up 39 which included a significant

contribution from Cognis It was fully integrated by 2012

Dr Wolf-Dieter Starp BASFrsquos Head of Global MampA says

that the company benefits from thorough preparation ldquoFor

successful PMI planning for the integration has to

start during the due diligence phaserdquo

he explains ldquoCritical issues are identified

through a number of analyses using

external consultants where necessary

These include a wide variety of issues such

as the complexity of the business the age

and condition of production plants and

taxes Both cost and growth synergies areidentified in the due diligence phase mdash and

then regularly measured to see if they are

being achieved in the integration phaserdquo

Having the correct teams and

procedures in place early on in the lifespan

of an acquistion isnrsquot the only factor that

determines a smooth transaction process

As a company with extensive experience

of acquisitions BASF has learnt that

itrsquos beneficial to announce the targetrsquos

organizational structure and management

as soon as possible as well

ldquoTimely and regular communication iscrucialrdquo says Starp ldquoThe new and current

employees need to know where the journey

is going and what the next steps arerdquo

Samy Walleyo EYrsquos Operational

Transaction Services Markets Leader for

Southern Germany Switzerland and Austria

agrees ldquoCompanies need to plan in advance

yet often they set up integration teams just

a couple of weeks before deals close That is

far too laterdquo he says

Tailoring integrationAs well as starting early in the process

companies need to work out quicklywhether the objective of the deal is a full or

partial integration of the two businesses

ldquoThe level of integration depends on your

motivationrdquo says Habeck ldquoIf you are buying

innovation and skills it may be unwise to

integrate those into a large corporationrdquo

Therefore large corporates should

consider whether giving the company some

autonomy rather than fully assimilating it

into the business will yield better results

wwwcapitalinsightsinfo | Issue 7 | Q3 2013 | 2

Optimizing

Investing

8142019 Capital Inside

httpslidepdfcomreaderfullcapital-inside 2244

What do you believe are the principal

factors needed to ensure successful

post-merger integration

Source NetjetsMergermarketDoing the Deal 2013

Having a clear andactionable post-mergerintegration plan 46

Understandingthe strategic fit

of the target withinyour business 65 Cultural understanding 46

Retainingtalentedstaff 54

60of respondents

identified culture as

a key challenge during

the integration process

according to a survey

by Mercer

The key is to communicatewith stakeholdersespecially managementand employees

Cedric Collange Senior VP MampA Schneider Electric

Schneider Electric has three types of integration model

according to Collange ldquoThese are full integration light

integration and no integration mdash where the competencies in

the acquired company are very different from our own and we

want to learn from them rather than to integraterdquo he says

In the ldquono integrationrdquo model Collange explains there

will still be back-office integration bringing the acquired

company into Schneiderrsquos financial systems and reporting

An example of this was the acquisition of Brazilian

low-voltage product producer Steck in 2011 Steck-

manufactured products were at a lower end of the market

than Schneider Therefore Steck was set up as a separate

brand with a separate structure ldquoThere is some integrationof the back office with reporting and financial controls but

otherwise it was not suitable for integrationrdquo says Collange

For the ldquolight integration modelrdquo Collange explains

that the company needs time to understand the acquired

business and learn its culture ldquoThis means that we might

integrate after one or two years

depending on what we findrdquo

he says ldquoIn these cases you

have to make sure that the key

people are comfortable before

you push for full integration It

is more important to keep them

than to achieve full integrationWe would rather wait before we

fully integrate to make sure we

understand the differences in the acquired companyrdquo

Internet giant Yahoo also took this tailored approach in

its US$11b acquisition of social networking website Tumblr

in May 2013 In its media release the company said that

ldquoper our promise not to screw uprdquo Tumblr ldquowill continue

to be defined and developed separatelyrdquo under current CEO

David Karprsquos leadership

However for creating fiscal synergies other issues

must be considered says Habeck ldquoIf you are seeking to

lower your cost base or extend productive capacity then

questions have to be asked whether the existing operations

are scalable about regulatory constraints the practicalchallenges involved in integration and the level of investment

that will be requiredrdquo

Companies must also consider their IT systems

ldquoIT compatibility is a big question mark in some executivesrsquo

mindsrdquo he adds ldquoItrsquos not just about pulling levers to change

systemsrdquo Indeed according to EYrsquos IT as a driver of MampA

success survey only 21 of corporates and 11 of private

equity firms always undertake IT due diligence prior to

signing deals Yet IT incompatibility can destroy the

prospect of achieving synergies

Capital of cultureWalleyo says that the importance of

thorough due diligence which goes beyond

the financial legal and regulatory issues

and into the organizational and cultural

areas cannot be overestimated ldquoItrsquos not

only about culture between countries

but also between companies and within

countries for example between north and

south Italyrdquo he explains

This is borne out in the 2011 study

from Aon Hewitt It found that over 70 of

corporates believed that the top impactsof unsuccessful cultural integration include

decreased employee engagement loss of

key talent and reduced productivity

ldquoThere is no magic recipe for due

diligence there will always be something

that takes you by