Embed Size (px)

Citation preview

OVERVIEW WHAT’S INSIDE

OVERVIEW

OUR MAIN INVESTMENT IDEA Johnson Matthey plc (revisited)

INVESTMENT INSIGHTS

WHAT HAPPENED? Market & Sector analysis

HINDESIGHT DIVIDEND UK PORTFOLIO # 1 (SEPTEMBER 2017)

APPENDIX I THE WAY WE THINK

APPENDIX II HOW WE THINK

Inside this edition of the UK Dividend Letter you’ll find:

1

4

10

14

15

16

17

AUGUST 2017ISSUE 34 - SEPTEMBER 2017 WWW.HINDESIGHTLETTERS.COM

An old colleague of mine, who used to work at UBS (the name for the merged banks of Union

Bank of Switzerland and Swiss Bank Corporation), sent me the photos below from an article written last year in ‘Business Insider’. The left-hand one is taken in 2008, when their offices in Stamford, Connecticut were filled to the rafters, despite being the size of two American football fields, and the right hand-one is taken last year. Of course, the party line will be that ‘some’ of the investment bankers have been relocated to other offices, but the reality is that many have been relocated home. Clearly, this doesn’t represent the staffing levels of compliance and regulatory police. Despite being completely non-revenue producing, it is currently the only growth area in banking. Unfortunately, ridiculous monetary policies with zero interest rates are keeping equity and bond valuations at nosebleed levels, and the level of transactional activity has fallen off a cliff. Hence, the demise of trading floors. The few souls left today are no longer

Dirty Harry

"Personnel Is For Assholes"

2 HINDESIGHT Dividend UK Letter

Masters of the Universe but bored young robots and grumpy old wizened veterans, forced to spend over twelve hours a day in the office ‘complying’, watched over by the fun police teams in compliance and human resources. All the powers of the Third Reich’s Gestapo, but none of the humour. When did the Personnel department become Human Resources exactly? Was it when Clint Eastwood told us his view of Personnel?

It is not just the finance professionals, the scapegoats of the last great crisis, who are feeling life is nowhere near as good as it used to be. Many people I find these days consider themselves to be overworked, overpoliced and underpaid.

A typical story would be a recent conversation with a 35-year-old acquaintance, a senior fashion designer who tells me her standard week is a five-day week, 12 hours a day in the office, as well as two hours travelling between one part of London and another. But, in order to ‘produce’ enough output, she has to not only put in extra hours most nights, but also some time at the weekends. With an estimated 75-hour work week, not including the 10 hours travelling on crowded public transport, the salary of £30,000 a year is barely the minimum wage. That ‘schedule’ doesn’t leave much energetic time for a personal life and no excess money for savings.

So, I find this chart below rather difficult to believe. I am possibly misjudging the amount of people in this statistic who are still on 9-5 public sector worker hours or Southern Rail employees.

Or, more likely, these extra hours put in by fashion designers or bankers or teachers are just not recorded because overtime is not actually paid and some random box-ticker has interpreted this, as per their contract, which probably states a regular five-day week with lunch hours and sick pay etc.

Obviously, there is a flip side to the impoverished worker, this being the employer. Not only are wages being contained, despite full employment, but workers are ‘giving’ their free time to their employers in unrecorded and unpaid hours, effectively enslaving them. It's a win-win for the companies. Of course, we have made great strides in the headlines of labour’s rights. Children are no longer employed in coalmines, we now have maternity/paternity paid leave, as well as closing gender pay inequality, but labour is being quietly downtrodden.

To put the final nail in the coffin in the UK, real wages are falling due to rising inflation. While all the academics are happy to agree that the current rise in retail prices is ‘temporary’ because of Brexit currency declines and oil base

THE COMPANY

Mark Mahaffey

Ben Davies

Aalok Sathe

HindeSight Publishing which runs HindeSight Letters is a unique blend of financial market professionals – investment managers, analysts and a financial editorial team of notable pedigree. The co-founders of Hinde Capital, Ben Davies and Mark Mahaffey, a successful alternative investment management company joined forces with the financial journalist David Stevenson best known for his regular columns in the FT Weekend, Money Week and numerous other global media titles to deliver something different in the financial newsletters segment – simply put it’s a reliable newsletter version of a managed fund.

Our writers actually run money, not just write about it, so they are the right mix of book smarts and street smarts. Truly a team of individuals that make up a formidable pool of knowledge, wherever the investing landscape shifts to. Source: Pantheon Macroeconomics

Source: Hinde Capital / Bloomberg

CONTRIBUTORS

CO-FOUNDER & CFO OF HINDE CAPITAL

CO-FOUNDER & CEO OF HINDE CAPITAL

ANALYST

A picture says it all – a sad state of affairs

ISSUE 34 - SEP 2017 3

effects, the average private sector worker is getting shafted big time.

I have always looked at socialist leaning countries, like France or the Nordic countries, in the belief that they were underselling themselves in available productivity, taking all of August ‘en grandes vacances’ and no emails read or answered outside of office time, but I certainly don’t believe in employers ‘stealing’ hours off their employees, in the vague pretence that it’s the norm and you have to do so ‘to get on’ in the rat race. Sweden has experimented in the last few years with reducing people’s hours to six hours a day to see what the benefits and pitfalls are of such a system. The jury is still out on productivity and the health of employees, with

the increased leisure time measured against the cost.Writers over the years have worried about how increased technology would threaten the human being’s ability to cope with ever-increasing free time. Unfortunately, this prediction seems to be getting further away than ever, but I am ever hopeful. Maybe there should be a move to re-establish more union power again, but this time for all working levels to push back against the evil employer, and not just the lower working classes.

But if official productivity is flatlining, even with all of the ‘stolen’ unpaid hours to keep profit margins high, employers and companies and their earnings might be in for a very harsh lesson if the worker revolts in the near future!Source: Hinde Capital / Bloomberg

Source: Hinde Capital / Bloomberg

Source: ONS / BBC

4 HINDESIGHT Dividend UK Letter

In our original recommendation, which is reprinted further below, our thesis focused on three main issues:

• Worries over global growth, China Slowdown• Challenging commodity market conditions• Volkswagen investigation

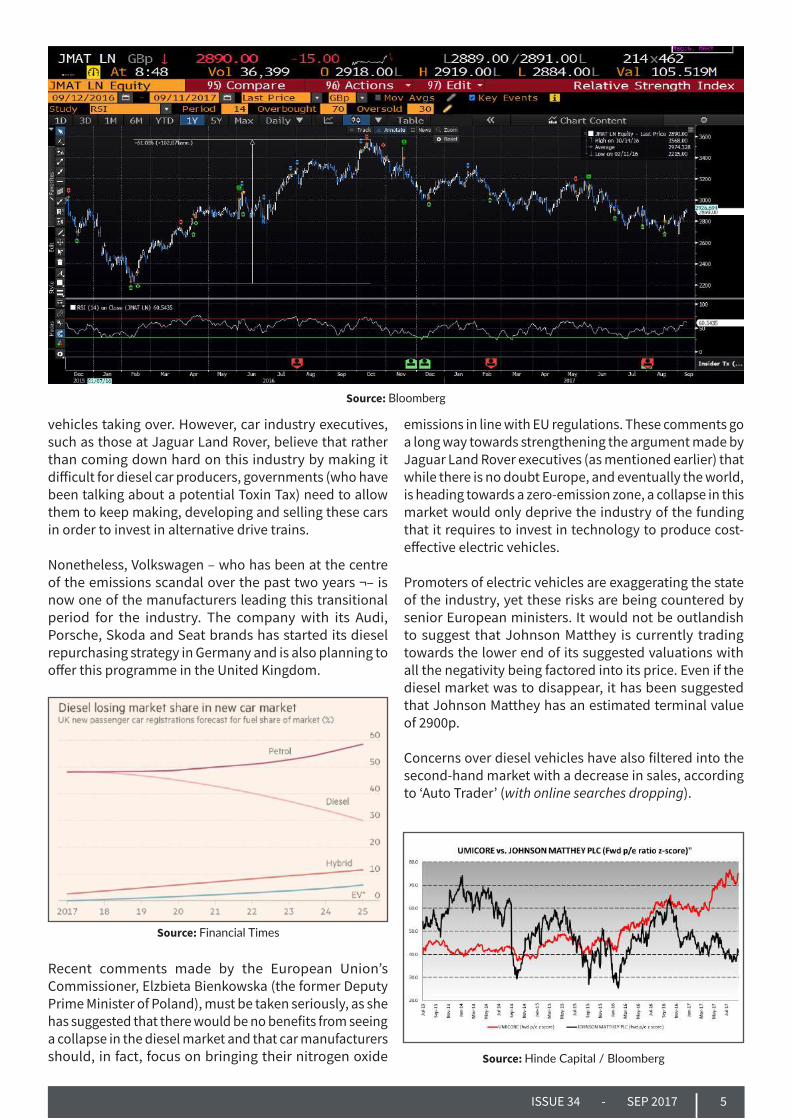

It was, in fact, these factors above that helped the stock to rally higher, as we saw a recovery in commodity prices and the sentiment around China stabilised, enabling the market to move higher. After we took profit, the stock carried on rising and eventually traded well above 3400p. With the stock having gained over 60% relative to its February 2016 lows, many sell-side analysts started to turn negative on the chemical producers future prospects. In October 2016, Johnson Matthey received a raft of negative downgrades that saw its share price change momentum and trade lower. Over the last 12 months, Johnson Matthey has fallen over 10%, and since October 2016, the chemical specialist is down over 20%. In that same period of time, the firm’s closest competitor Umicore, which also specialises in the chemicals and catalyst industry, has had a significant up trade.

Demise of the Diesel Market

A large part of the negativity that surrounds this specialist chemical producer has come from the downbeat sentiment there is towards the longevity of the diesel car market. With Johnson Matthey being one of the largest providers of catalytic converters around the world, the firm’s share price has not fared well since the news broke and created jitters across its investor base. On the surface, this anxiety seems to be well justified, with rumours suggesting that a number of German carmakers are hoping to start programs that entice customers to trade in traditional vehicles in return for their electric alternatives.

It is definitely a far cry from the time, not so long ago, when the government was incentivising customers to buy diesel cars because they were emitting around 20% less CO2 compared to their petrol counterparts. Unfortunately, it was later discovered that diesel engines, and particularly the older ones, tend to emit nitrogen oxide and other pollutants that create roadside air contamination and potential respiratory conditions.

No one is under any illusions that the market will eventually see diesel cars being phased out and electric

INVESTMENT IDEA #1JOHNSON MATTHEY PLC (REVISITED)

BY MARK MAHAFFEY

We first recommended Johnson Matthey (JMAT: LSE) on 4th of November 2015 at a price of 2631p when the FTSE100 was 6655. This stock was held for over 8 months with our team taking profit at 3175p in July 2016. During the time that it was held, Johnson Matthey rose 31.82% and 34.53%, in absolute and relative terms respectively. From an income perspective, Johnson Matthey paid 222.44p in dividend over the period that it was held in the HindeSight Dividend Portfolio.

CO-FOUNDER & CFO OF HINDE CAPITAL

Price (£)Turnover (£mm)Net Income (£mm)Market Cap (£mm)Fwd P/E RatioDividend Yield (%)Payout Ratio (%)Total Debt to Total Equity (%)FCF to Market Cap (%)ROIC (%)

2,865.012,031.0386.05,631.812.92.95%-48.0%--

JOHNSON MATTHEY PLC

ISSUE 34 - SEP 2017 5

vehicles taking over. However, car industry executives, such as those at Jaguar Land Rover, believe that rather than coming down hard on this industry by making it difficult for diesel car producers, governments (who have been talking about a potential Toxin Tax) need to allow them to keep making, developing and selling these cars in order to invest in alternative drive trains. Nonetheless, Volkswagen – who has been at the centre of the emissions scandal over the past two years ¬– is now one of the manufacturers leading this transitional period for the industry. The company with its Audi, Porsche, Skoda and Seat brands has started its diesel repurchasing strategy in Germany and is also planning to offer this programme in the United Kingdom.

Recent comments made by the European Union’s Commissioner, Elzbieta Bienkowska (the former Deputy Prime Minister of Poland), must be taken seriously, as she has suggested that there would be no benefits from seeing a collapse in the diesel market and that car manufacturers should, in fact, focus on bringing their nitrogen oxide

emissions in line with EU regulations. These comments go a long way towards strengthening the argument made by Jaguar Land Rover executives (as mentioned earlier) that while there is no doubt Europe, and eventually the world, is heading towards a zero-emission zone, a collapse in this market would only deprive the industry of the funding that it requires to invest in technology to produce cost-effective electric vehicles.

Promoters of electric vehicles are exaggerating the state of the industry, yet these risks are being countered by senior European ministers. It would not be outlandish to suggest that Johnson Matthey is currently trading towards the lower end of its suggested valuations with all the negativity being factored into its price. Even if the diesel market was to disappear, it has been suggested that Johnson Matthey has an estimated terminal value of 2900p.

Concerns over diesel vehicles have also filtered into the second-hand market with a decrease in sales, according to ‘Auto Trader’ (with online searches dropping).

Source: Hinde Capital / Bloomberg

Source: Financial Times

Source: Bloomberg

6 HINDESIGHT Dividend UK Letter

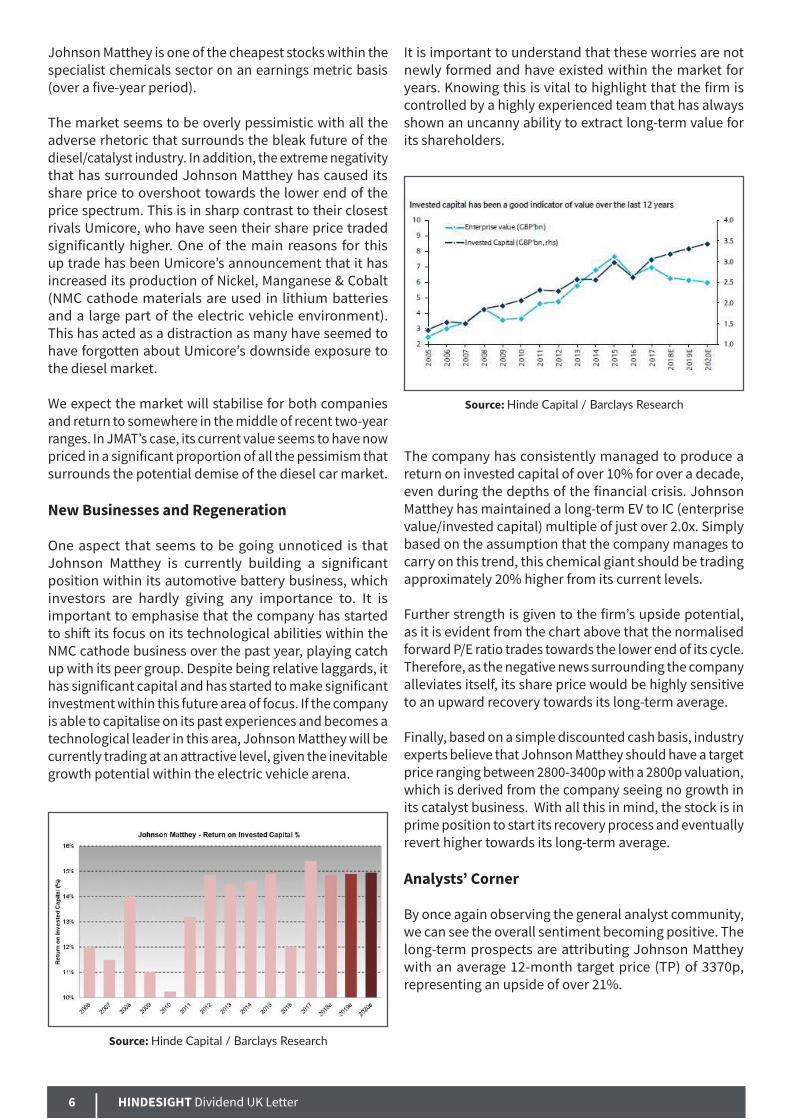

Johnson Matthey is one of the cheapest stocks within the specialist chemicals sector on an earnings metric basis (over a five-year period).

The market seems to be overly pessimistic with all the adverse rhetoric that surrounds the bleak future of the diesel/catalyst industry. In addition, the extreme negativity that has surrounded Johnson Matthey has caused its share price to overshoot towards the lower end of the price spectrum. This is in sharp contrast to their closest rivals Umicore, who have seen their share price traded significantly higher. One of the main reasons for this up trade has been Umicore’s announcement that it has increased its production of Nickel, Manganese & Cobalt (NMC cathode materials are used in lithium batteries and a large part of the electric vehicle environment). This has acted as a distraction as many have seemed to have forgotten about Umicore’s downside exposure to the diesel market.

We expect the market will stabilise for both companies and return to somewhere in the middle of recent two-year ranges. In JMAT’s case, its current value seems to have now priced in a significant proportion of all the pessimism that surrounds the potential demise of the diesel car market.

New Businesses and Regeneration

One aspect that seems to be going unnoticed is that Johnson Matthey is currently building a significant position within its automotive battery business, which investors are hardly giving any importance to. It is important to emphasise that the company has started to shift its focus on its technological abilities within the NMC cathode business over the past year, playing catch up with its peer group. Despite being relative laggards, it has significant capital and has started to make significant investment within this future area of focus. If the company is able to capitalise on its past experiences and becomes a technological leader in this area, Johnson Matthey will be currently trading at an attractive level, given the inevitable growth potential within the electric vehicle arena.

It is important to understand that these worries are not newly formed and have existed within the market for years. Knowing this is vital to highlight that the firm is controlled by a highly experienced team that has always shown an uncanny ability to extract long-term value for its shareholders.

The company has consistently managed to produce a return on invested capital of over 10% for over a decade, even during the depths of the financial crisis. Johnson Matthey has maintained a long-term EV to IC (enterprise value/invested capital) multiple of just over 2.0x. Simply based on the assumption that the company manages to carry on this trend, this chemical giant should be trading approximately 20% higher from its current levels.

Further strength is given to the firm’s upside potential, as it is evident from the chart above that the normalised forward P/E ratio trades towards the lower end of its cycle. Therefore, as the negative news surrounding the company alleviates itself, its share price would be highly sensitive to an upward recovery towards its long-term average.

Finally, based on a simple discounted cash basis, industry experts believe that Johnson Matthey should have a target price ranging between 2800-3400p with a 2800p valuation, which is derived from the company seeing no growth in its catalyst business. With all this in mind, the stock is in prime position to start its recovery process and eventually revert higher towards its long-term average.

Analysts’ Corner

By once again observing the general analyst community, we can see the overall sentiment becoming positive. The long-term prospects are attributing Johnson Matthey with an average 12-month target price (TP) of 3370p, representing an upside of over 21%.

Source: Hinde Capital / Barclays Research

Source: Hinde Capital / Barclays Research

ISSUE 34 - SEP 2017 7

Summary

Johnson Matthey has had a significant down trade over the past 12 months due to global fears within the market over the potential downfall of the diesel car market. These worries have seen the stock trade down 20%. With the industry openly accepting that the diesel market will eventually cease to exist, the speed of this decline has been exaggerated, with the European Union suggesting that there are no benefits to be seen from the immediate collapse of this particular market. With all this negativity being baked into the firm’s share price and significant investment being committed to the future battery industry, the long-term prospects are starting to look highly positive. We would suggest starting to build a position in Johnson Matthey, as the fundamental and technical analysis is suggesting that the company is trading to the lower end of its cycle.

8 HINDESIGHT Dividend UK Letter

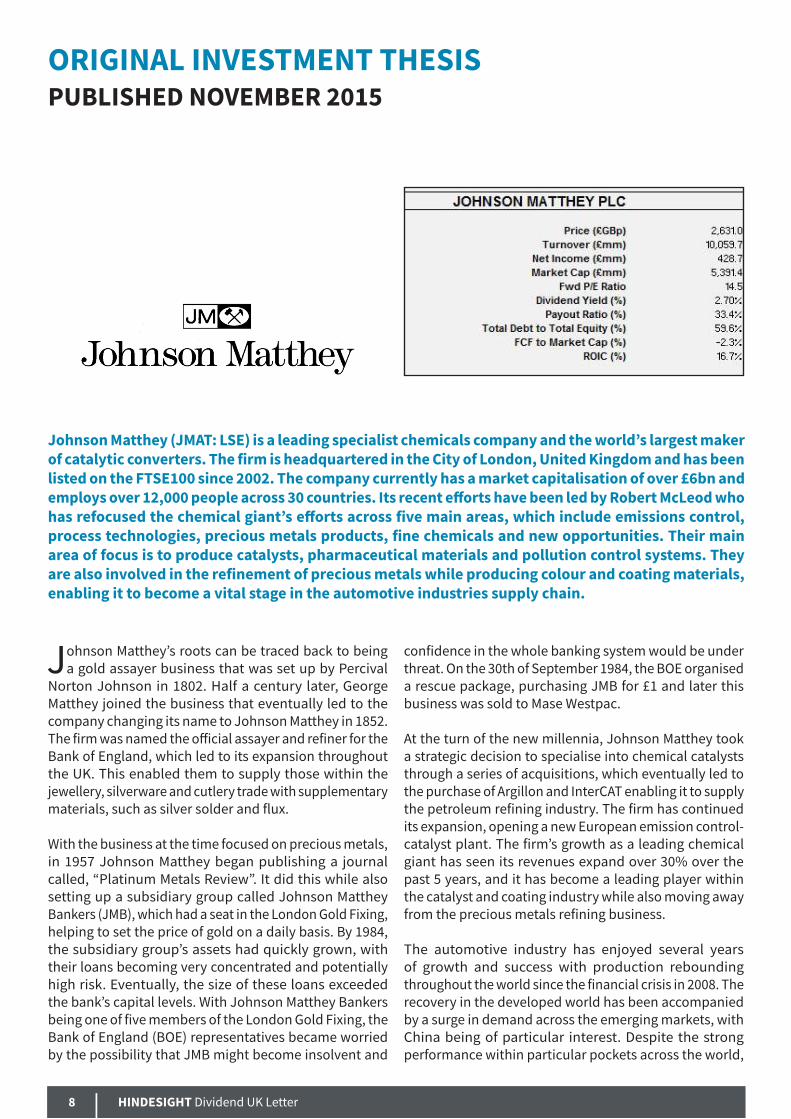

ORIGINAL INVESTMENT THESIS PUBLISHED NOVEMBER 2015

Johnson Matthey’s roots can be traced back to being a gold assayer business that was set up by Percival

Norton Johnson in 1802. Half a century later, George Matthey joined the business that eventually led to the company changing its name to Johnson Matthey in 1852. The firm was named the official assayer and refiner for the Bank of England, which led to its expansion throughout the UK. This enabled them to supply those within the jewellery, silverware and cutlery trade with supplementary materials, such as silver solder and flux.

With the business at the time focused on precious metals, in 1957 Johnson Matthey began publishing a journal called, “Platinum Metals Review”. It did this while also setting up a subsidiary group called Johnson Matthey Bankers (JMB), which had a seat in the London Gold Fixing, helping to set the price of gold on a daily basis. By 1984, the subsidiary group’s assets had quickly grown, with their loans becoming very concentrated and potentially high risk. Eventually, the size of these loans exceeded the bank’s capital levels. With Johnson Matthey Bankers being one of five members of the London Gold Fixing, the Bank of England (BOE) representatives became worried by the possibility that JMB might become insolvent and

confidence in the whole banking system would be under threat. On the 30th of September 1984, the BOE organised a rescue package, purchasing JMB for £1 and later this business was sold to Mase Westpac.

At the turn of the new millennia, Johnson Matthey took a strategic decision to specialise into chemical catalysts through a series of acquisitions, which eventually led to the purchase of Argillon and InterCAT enabling it to supply the petroleum refining industry. The firm has continued its expansion, opening a new European emission control-catalyst plant. The firm’s growth as a leading chemical giant has seen its revenues expand over 30% over the past 5 years, and it has become a leading player within the catalyst and coating industry while also moving away from the precious metals refining business.

The automotive industry has enjoyed several years of growth and success with production rebounding throughout the world since the financial crisis in 2008. The recovery in the developed world has been accompanied by a surge in demand across the emerging markets, with China being of particular interest. Despite the strong performance within particular pockets across the world,

Johnson Matthey (JMAT: LSE) is a leading specialist chemicals company and the world’s largest maker of catalytic converters. The firm is headquartered in the City of London, United Kingdom and has been listed on the FTSE100 since 2002. The company currently has a market capitalisation of over £6bn and employs over 12,000 people across 30 countries. Its recent efforts have been led by Robert McLeod who has refocused the chemical giant’s efforts across five main areas, which include emissions control, process technologies, precious metals products, fine chemicals and new opportunities. Their main area of focus is to produce catalysts, pharmaceutical materials and pollution control systems. They are also involved in the refinement of precious metals while producing colour and coating materials, enabling it to become a vital stage in the automotive industries supply chain.

ISSUE 34 - SEP 2017 9

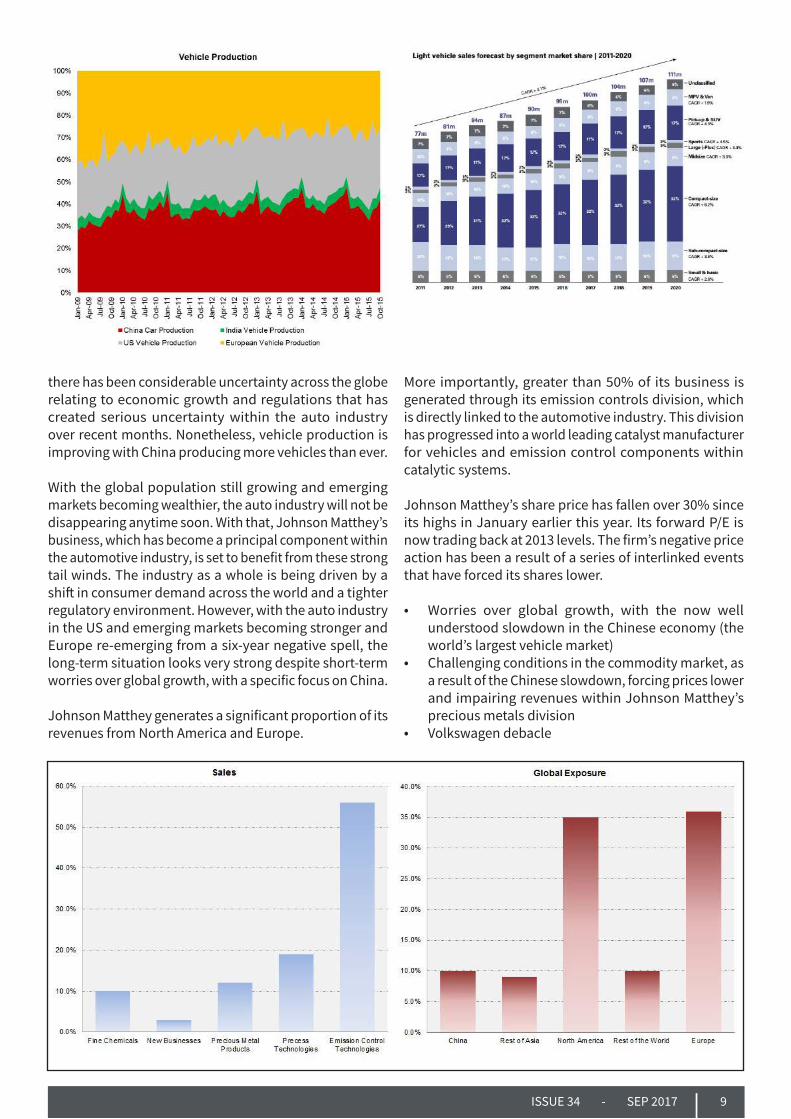

there has been considerable uncertainty across the globe relating to economic growth and regulations that has created serious uncertainty within the auto industry over recent months. Nonetheless, vehicle production is improving with China producing more vehicles than ever. With the global population still growing and emerging markets becoming wealthier, the auto industry will not be disappearing anytime soon. With that, Johnson Matthey’s business, which has become a principal component within the automotive industry, is set to benefit from these strong tail winds. The industry as a whole is being driven by a shift in consumer demand across the world and a tighter regulatory environment. However, with the auto industry in the US and emerging markets becoming stronger and Europe re-emerging from a six-year negative spell, the long-term situation looks very strong despite short-term worries over global growth, with a specific focus on China.

Johnson Matthey generates a significant proportion of its revenues from North America and Europe.

More importantly, greater than 50% of its business is generated through its emission controls division, which is directly linked to the automotive industry. This division has progressed into a world leading catalyst manufacturer for vehicles and emission control components within catalytic systems.

Johnson Matthey’s share price has fallen over 30% since its highs in January earlier this year. Its forward P/E is now trading back at 2013 levels. The firm’s negative price action has been a result of a series of interlinked events that have forced its shares lower. • Worries over global growth, with the now well

understood slowdown in the Chinese economy (the world’s largest vehicle market)

• Challenging conditions in the commodity market, as a result of the Chinese slowdown, forcing prices lower and impairing revenues within Johnson Matthey’s precious metals division

• Volkswagen debacle

10 HINDESIGHT Dividend UK Letter

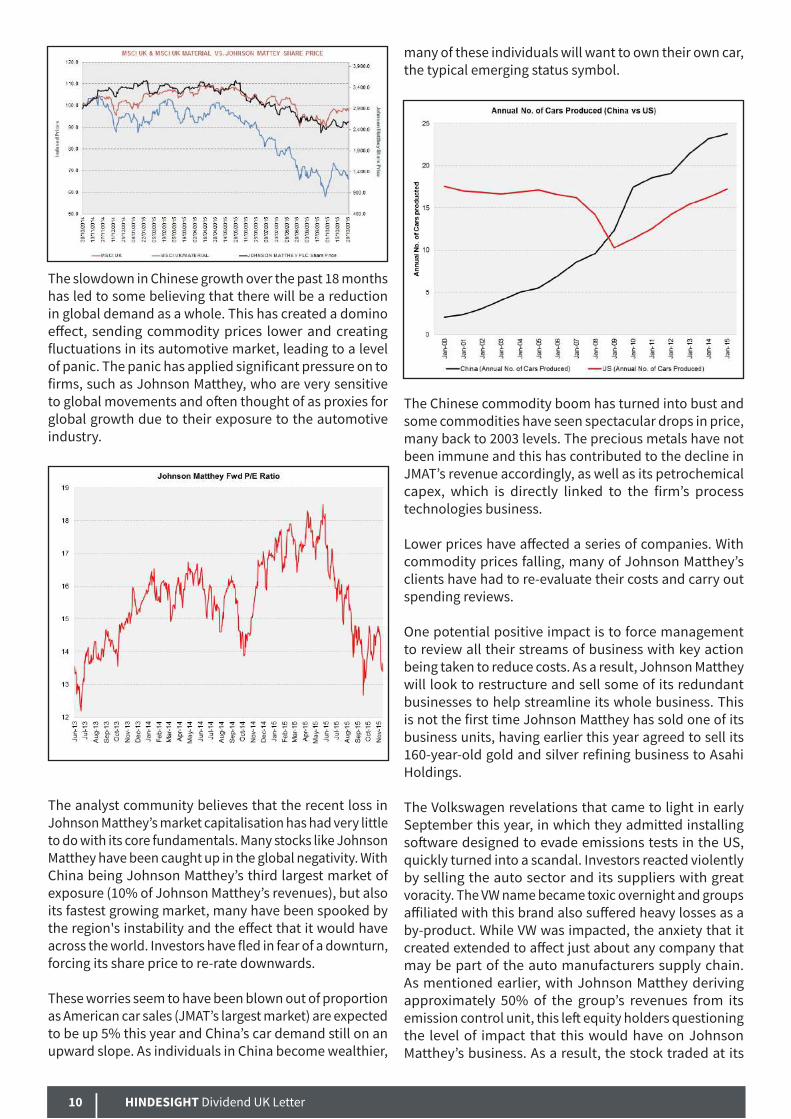

The slowdown in Chinese growth over the past 18 months has led to some believing that there will be a reduction in global demand as a whole. This has created a domino effect, sending commodity prices lower and creating fluctuations in its automotive market, leading to a level of panic. The panic has applied significant pressure on to firms, such as Johnson Matthey, who are very sensitive to global movements and often thought of as proxies for global growth due to their exposure to the automotive industry.

The analyst community believes that the recent loss in Johnson Matthey’s market capitalisation has had very little to do with its core fundamentals. Many stocks like Johnson Matthey have been caught up in the global negativity. With China being Johnson Matthey’s third largest market of exposure (10% of Johnson Matthey’s revenues), but also its fastest growing market, many have been spooked by the region's instability and the effect that it would have across the world. Investors have fled in fear of a downturn, forcing its share price to re-rate downwards.

These worries seem to have been blown out of proportion as American car sales (JMAT’s largest market) are expected to be up 5% this year and China’s car demand still on an upward slope. As individuals in China become wealthier,

many of these individuals will want to own their own car, the typical emerging status symbol.

The Chinese commodity boom has turned into bust and some commodities have seen spectacular drops in price, many back to 2003 levels. The precious metals have not been immune and this has contributed to the decline in JMAT’s revenue accordingly, as well as its petrochemical capex, which is directly linked to the firm’s process technologies business.

Lower prices have affected a series of companies. With commodity prices falling, many of Johnson Matthey’s clients have had to re-evaluate their costs and carry out spending reviews.

One potential positive impact is to force management to review all their streams of business with key action being taken to reduce costs. As a result, Johnson Matthey will look to restructure and sell some of its redundant businesses to help streamline its whole business. This is not the first time Johnson Matthey has sold one of its business units, having earlier this year agreed to sell its 160-year-old gold and silver refining business to Asahi Holdings.

The Volkswagen revelations that came to light in early September this year, in which they admitted installing software designed to evade emissions tests in the US, quickly turned into a scandal. Investors reacted violently by selling the auto sector and its suppliers with great voracity. The VW name became toxic overnight and groups affiliated with this brand also suffered heavy losses as a by-product. While VW was impacted, the anxiety that it created extended to affect just about any company that may be part of the auto manufacturers supply chain. As mentioned earlier, with Johnson Matthey deriving approximately 50% of the group’s revenues from its emission control unit, this left equity holders questioning the level of impact that this would have on Johnson Matthey’s business. As a result, the stock traded at its

ISSUE 34 - SEP 2017 11

lowest price for over two years.

Fortunately for the likes of Johnson Matthey, many believe this will not affect car sales and, in turn, their own business. The global population is still rising and people still need to commute in their own personal vehicles. Academics from the Institute of Mechanical Engineers suggested that the price action Johnson Matthey had demonstrated was just a “knee-jerk” response to the VW crisis. This is likely to be a turning point for its share price as the automotive industry will demand even higher quality testing and emissions catalysts. As car manufacturers are forced to adhere to more stringent emissions standards, this will create even greater demand for Johnson Matthey’s components. The level of quality catalysts that auto manufacturers will be required to implement will only be produced by one of a few fabricators, with Johnson Matthey being one of them. With sentiment in Europe and America becoming more positive, and China and India set to adopt more rigorous emission rules, Johnson Matthey is due to benefit from these tailwinds.

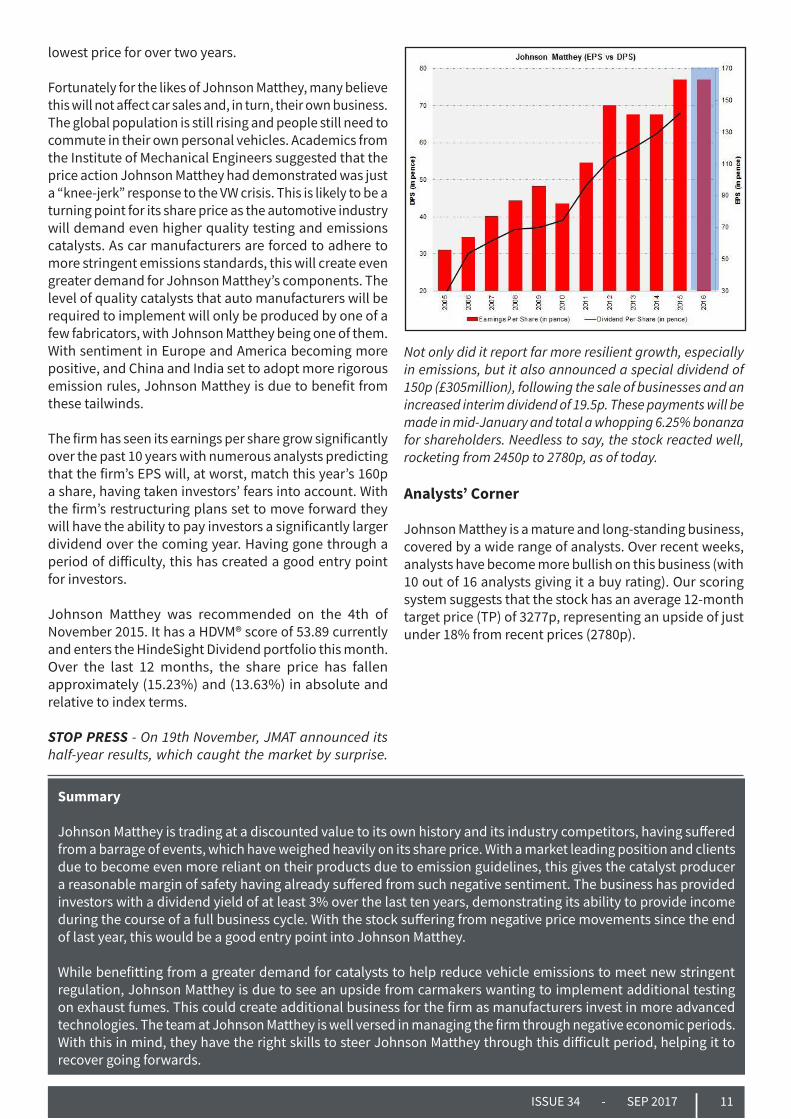

The firm has seen its earnings per share grow significantly over the past 10 years with numerous analysts predicting that the firm’s EPS will, at worst, match this year’s 160p a share, having taken investors’ fears into account. With the firm’s restructuring plans set to move forward they will have the ability to pay investors a significantly larger dividend over the coming year. Having gone through a period of difficulty, this has created a good entry point for investors. Johnson Matthey was recommended on the 4th of November 2015. It has a HDVM® score of 53.89 currently and enters the HindeSight Dividend portfolio this month. Over the last 12 months, the share price has fallen approximately (15.23%) and (13.63%) in absolute and relative to index terms.

STOP PRESS - On 19th November, JMAT announced its half-year results, which caught the market by surprise.

Not only did it report far more resilient growth, especially in emissions, but it also announced a special dividend of 150p (£305million), following the sale of businesses and an increased interim dividend of 19.5p. These payments will be made in mid-January and total a whopping 6.25% bonanza for shareholders. Needless to say, the stock reacted well, rocketing from 2450p to 2780p, as of today.

Analysts’ Corner

Johnson Matthey is a mature and long-standing business, covered by a wide range of analysts. Over recent weeks, analysts have become more bullish on this business (with 10 out of 16 analysts giving it a buy rating). Our scoring system suggests that the stock has an average 12-month target price (TP) of 3277p, representing an upside of just under 18% from recent prices (2780p).

Summary

Johnson Matthey is trading at a discounted value to its own history and its industry competitors, having suffered from a barrage of events, which have weighed heavily on its share price. With a market leading position and clients due to become even more reliant on their products due to emission guidelines, this gives the catalyst producer a reasonable margin of safety having already suffered from such negative sentiment. The business has provided investors with a dividend yield of at least 3% over the last ten years, demonstrating its ability to provide income during the course of a full business cycle. With the stock suffering from negative price movements since the end of last year, this would be a good entry point into Johnson Matthey.

While benefitting from a greater demand for catalysts to help reduce vehicle emissions to meet new stringent regulation, Johnson Matthey is due to see an upside from carmakers wanting to implement additional testing on exhaust fumes. This could create additional business for the firm as manufacturers invest in more advanced technologies. The team at Johnson Matthey is well versed in managing the firm through negative economic periods. With this in mind, they have the right skills to steer Johnson Matthey through this difficult period, helping it to recover going forwards.

12 HINDESIGHT Dividend UK Letter

INVESTMENT INSIGHTS

However, all the actual indices, the FTSE 100, FTSE 250 and FTSE 350 are up, 3.2%, 8.6% and 4.1% respectively. Clearly, there must be some companies doing very well. Regular readers will know that I believe stock valuations are very overpriced currently, but before we argue that this is just a case of the half-full, half-empty glass, we should understand that the observation is just typically what the technical analysts of the stock markets call ‘breadth’. Breadth can be measured in many ways, but the eventual analysis should focus on whether the ratio of stocks going up, versus down, signals a potential strong or weak market in the future. Declining breadth, where the number of companies making new highs versus lows, is usually a sign of wider spread weakness ahead.

We know that in the UK stock indices, just like the SP500 in the US, there are some huge companies potentially ‘holding’ up the index, which is not a particularly good sign, especially if these companies are not seeing strong earnings. In the UK, for example, the huge size of Unilever, at almost 5% weighting of the index, means that the stellar 40% stock price rise this year is responsible alone for an index move of 2%, over half the actual 3.2% year to date rise in the FTSE 100. In the US, we have the well-known FANGs stocks – Facebook, Amazon, Netflix and Google ¬– almost dictating daily SP500 movements with their high market capitalisation weightings.

Neither a huge difference in returns across companies in

Headlines like these have become far too regular of late. In fact, when we ran some statistics for how many companies’ share prices in the FTSE 350 had seen more than 15% declines from their early 2017 highs and are still down, 180 companies were below the red line. That’s over 50% of the index, with some of them down 80%. No wonder even the legendary Neil Woodford’s fund is falling fast.

ISSUE 34 - SEP 2017 13

the preceding periods, nor a small number of very large companies driving the index returns, is a great sign of a stable and strong market.

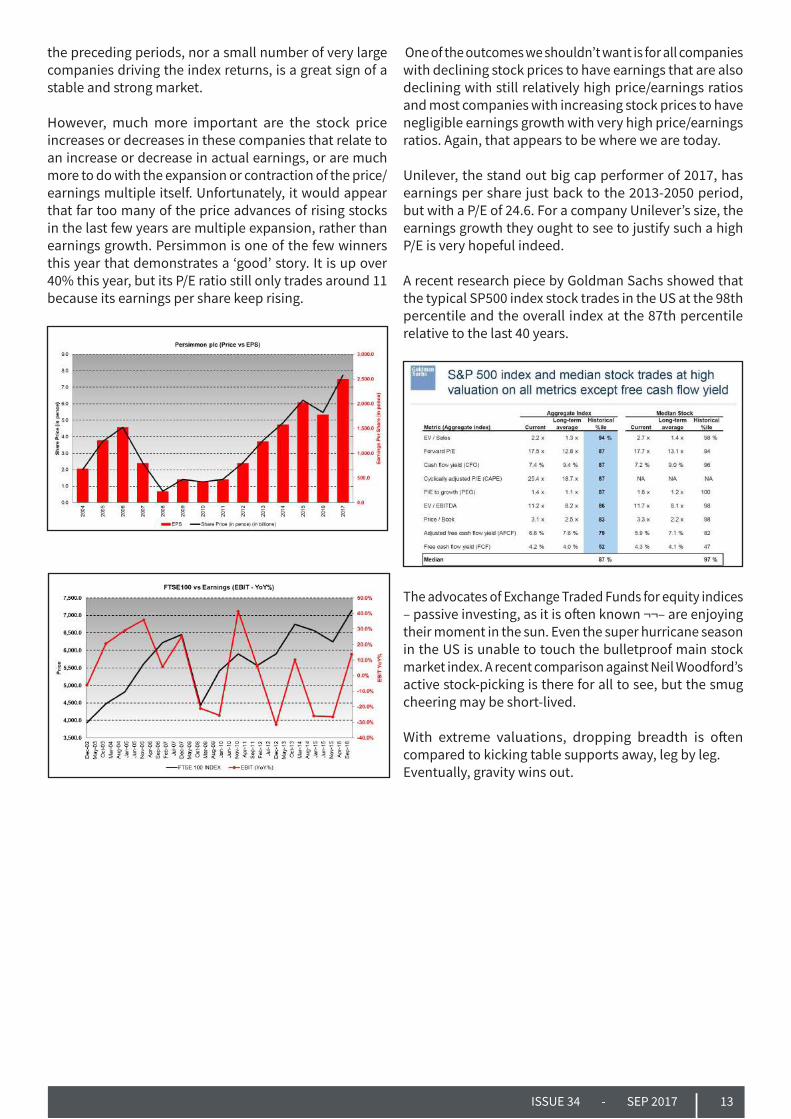

However, much more important are the stock price increases or decreases in these companies that relate to an increase or decrease in actual earnings, or are much more to do with the expansion or contraction of the price/earnings multiple itself. Unfortunately, it would appear that far too many of the price advances of rising stocks in the last few years are multiple expansion, rather than earnings growth. Persimmon is one of the few winners this year that demonstrates a ‘good’ story. It is up over 40% this year, but its P/E ratio still only trades around 11 because its earnings per share keep rising.

One of the outcomes we shouldn’t want is for all companies with declining stock prices to have earnings that are also declining with still relatively high price/earnings ratios and most companies with increasing stock prices to have negligible earnings growth with very high price/earnings ratios. Again, that appears to be where we are today.

Unilever, the stand out big cap performer of 2017, has earnings per share just back to the 2013-2050 period, but with a P/E of 24.6. For a company Unilever’s size, the earnings growth they ought to see to justify such a high P/E is very hopeful indeed.

A recent research piece by Goldman Sachs showed that the typical SP500 index stock trades in the US at the 98th percentile and the overall index at the 87th percentile relative to the last 40 years.

The advocates of Exchange Traded Funds for equity indices – passive investing, as it is often known ¬¬– are enjoying their moment in the sun. Even the super hurricane season in the US is unable to touch the bulletproof main stock market index. A recent comparison against Neil Woodford’s active stock-picking is there for all to see, but the smug cheering may be short-lived.

With extreme valuations, dropping breadth is often compared to kicking table supports away, leg by leg.Eventually, gravity wins out.

14 HINDESIGHT Dividend UK Letter

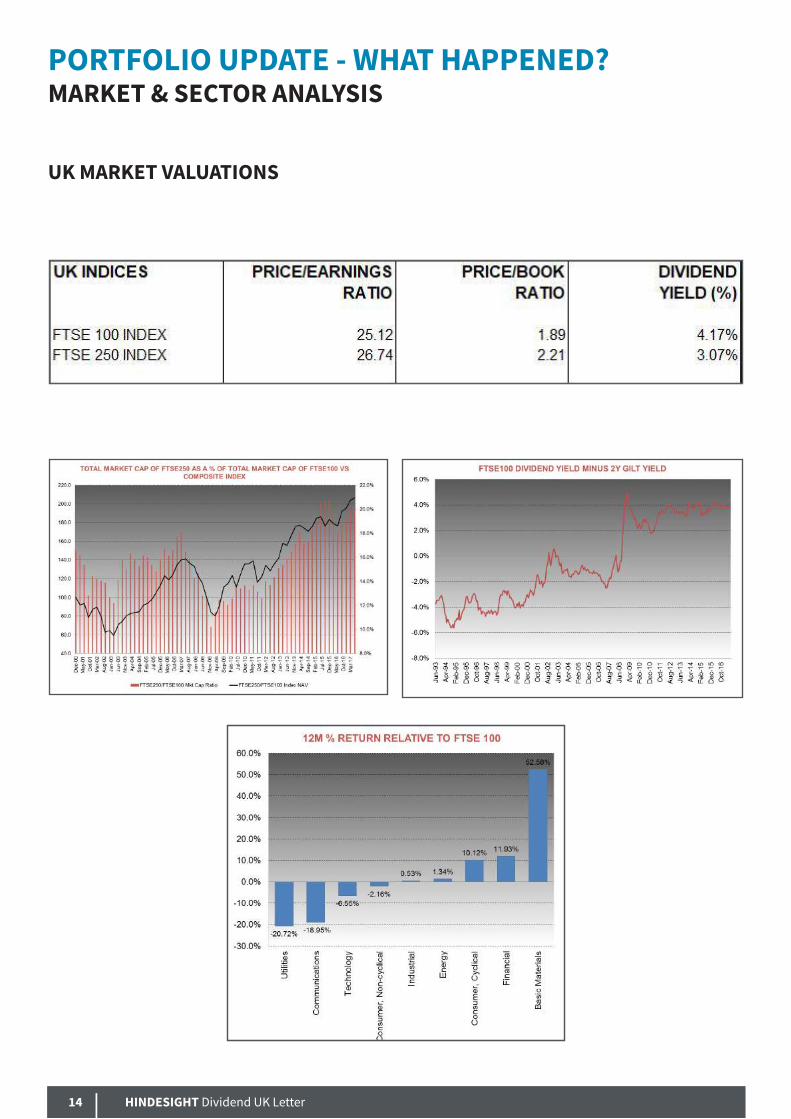

UK MARKET VALUATIONS

PORTFOLIO UPDATE - WHAT HAPPENED?MARKET & SECTOR ANALYSIS

ISSUE 34 - SEP 2017 15

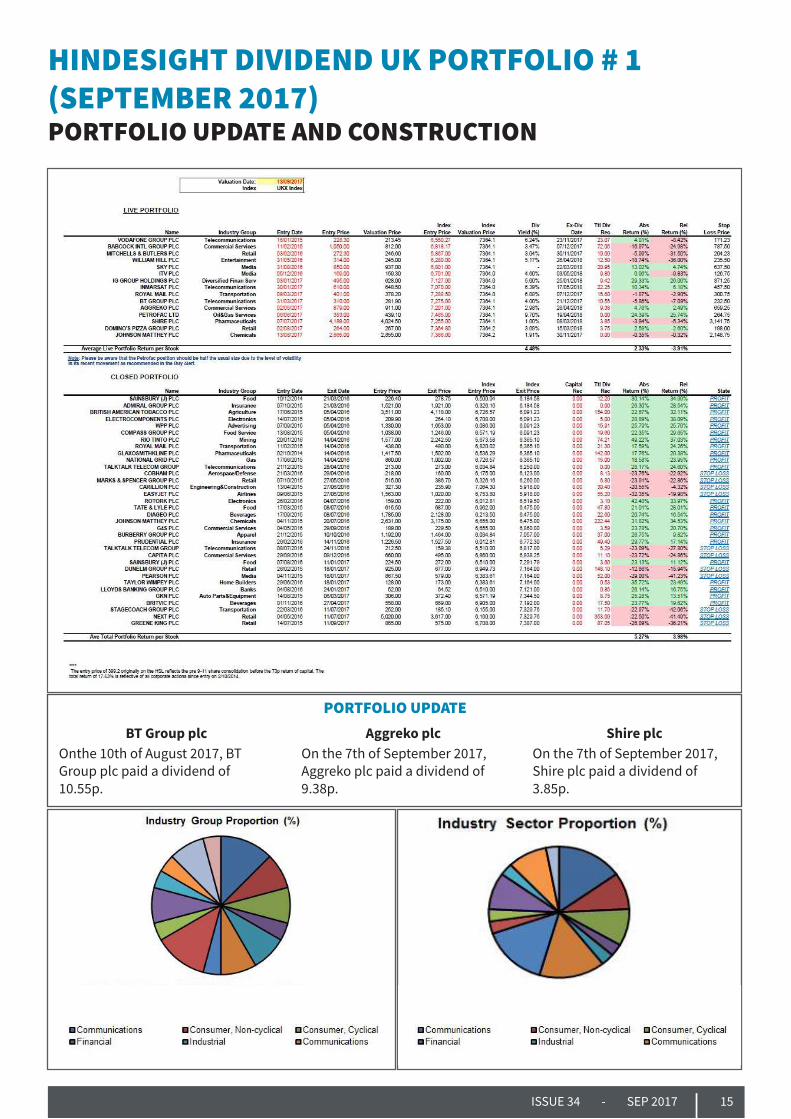

HINDESIGHT DIVIDEND UK PORTFOLIO # 1 (SEPTEMBER 2017)PORTFOLIO UPDATE AND CONSTRUCTION

BT Group plc Onthe 10th of August 2017, BT Group plc paid a dividend of 10.55p.

Aggreko plcOn the 7th of September 2017, Aggreko plc paid a dividend of 9.38p.

Shire plcOn the 7th of September 2017, Shire plc paid a dividend of 3.85p.

PORTFOLIO UPDATE

16 HINDESIGHT Dividend UK Letter

We passionately believe that dividends really,really matter. William Thorndike in his fascinating book

'The Outsiders- Eight Unconventional CEOs and Their Radically RationalBlueprint for Success' examined one of the most impor tant aspects of running a business a CEO must undertake: Capital Allocation. He summarised how a CEO deploys capitalin order to best utilise cash flow generated from his or her business operations. Essentially,CEOs have 5 ways of deploying capital:

• Investing in existing operations• Acquiring other businesses• Repaying debt• Repurchasing their own stock (buybacks)• Paying dividends

Dividend payments are a crucial operation in creating stakeholder wealth. It is this aspect of a business that we are so fixated by - the propensity for a company to produce and continue to grow dividends so that we may accrue wealth over a generation. But as readers will know we can't just grab stocks with the highest yield for fear that this signals some cash flow or even solvency issues for the firm. So it is with this very real threat in mind we explore only well-capitalised FTSE 350 companies.

This letter's purpose is to help inform readers on dividend investing so that they can construct a portfolio of sound UK dividend stocks based on our recommendations. Our prerequisite is that any stocks selected for this let ter

must be liquid,well-capitalised with a strong free cash flow and a progressive dividend policy.

Our System

• Every month we will provide a write up of 3 to 4 stocks untilwe create a portfolio of 25 UK dividend stocks. This will be the HindeSight UK Dividend Portfolio #1

• You wiII bealerted by subscriber email intra-month when these stocks become a buy. Timing is critical to the strategy, not only buying quality stocks but buying them at the right time

• Theentry points willthen be recorded in the next month ly in the HindeSight UK Dividend Portfolio section and the stock(s) wr itten up in full

• We will run our winners but tend to rotate every 6 months depending on specific criteria which would elevate cheaper companies into the portfolio relative to stocks that had performed

• The basis for stock and portfolio selection is derived from our quantitative systematic methodology which screens these companies using the Hinde Dividend Value Matrix, (HDVMdl), a proprietary stock-rating system

• In the section on ETPs we will highlight our invest ment philosophy and the investment process behind our stock selections. This is the b*is of our dynamic risk and money management in our portfolio con struction for you. You can also read the stand-alone Hinde Dividend Value Strategy document to see the methodology behind our stock selection.

APPENDIX I

THE WAY WE THINK

ISSUE 34 - SEP 2017 17

“We have met the enemy, and he is us.” Walt Kelly

Our key to long-term performance investing is premised on the following:

• Systematic rule-based strategy• Systematic risk and money management• Occam’s razor, aka ‘K.I.S.S.’, Keep It Simple Stupid• Consistency• Discipline

All our investment ideas are rule-based methodologies driven by systematic and quantitative models.

Hinde Dividend Value Strategy

Hinde Dividend Value Strategy seeks to generate a total return from an actively managed basket of UK dividend-paying stocks. The strategy selects 20 highly liquid, mid-to-large capitalised stocks on an equally-weighted basis, which offer the highest total return potential. The 50%

Hedge version of the strategy would then be subject to a strategic Beta Hedge*, which is designed to cover 50% of the value of the UK stock basket at all times.

The 50% hedge is maintained using UK equity benchmark indices to reduce exposure to overall market volatility, but without reducing overall total returns to the market over the long run. The Hinde Dividend Value Strategy (100% Hedge) would deploy a full beta hedge at all times.

Hinde Dividend Value Matrix ®

The strategy employs a quantitative, systematic methodology, whereby FTSE 100 and FTSE 250 constituent stocks are screened using the Hinde Dividend Value Matrix®, a proprietary stock-rating system. We use the same system to select stocks for any of our strategies, long-only, 50% Hedge or 100% Hedge. The only difference is clearly the extent of the hedge on the exposure to the overall market.

APPENDIX II

HOW WE THINK

18 HINDESIGHT Dividend UK Letter

The basic premise of the strategy is to accelerate returns by selecting relatively high yielding stocks that offer the highest potential for capital revaluation. The dynamic rotation of stocks each quarter enables us to sell stocks where the capital revaluation and dividend has been captured, and use this additional capital to invest in more undervalued quality companies. If successful, this cycle of capture and re-investment offers the chance to significantly improve the total return generated by the Dynamic Portfolio.

The basis of the stock selection process is the Hinde Dividend Value Matrix®, which is a derived process that looks at 3 crucial variables:

* Beta is the stock’s sensitivity to market movements, e.g. if a share has a beta of 1.5 its price tends to move by 1.5% for each 1% move in the index

1. Dividend Screen

The top ranking stocks will be those offering a relatively high dividend. A composite of the following criteria comprises the Dividend Rank:

• Relative Dividend Yield• Dividend Capture• Payout ratios

The Relative Dividend Yield assesses if a company pays a higher dividend than the Index it derives from (the FTSE 100 or FTSE 250). The Dividend Capture criteria explain how quickly and how much of the dividend is paid at any point in time. The Payout Ratio gives a snapshot of whether a company will be able to maintain and grow its dividend. It helps us to assess how much of a company’s revenue, profit or cash flow is paid out in dividends.

The lower the amount of dividends paid out as a percentage of profits, the healthier future dividend potential will be. History is for once a good guide as to whether companies will continue to pay and grow their dividends. A stock with an excessively high yield relative to its sector or the overall market is invariably showing signs of heightened risk to its dividend sustainability and often the viability of the company itself. The screen incorporates a limit on yield dispersions from the overall market.

The strategy is emphatically not a yield chaser. It is the Performance and Value screens that are used to assess the total return potential of a stock by analysis of how undervalued it is relative to its fundamentals, sector and overall market index.

2. Performance Screen

The top ranking stocks have the poorest relative

performance to their index over multiple time horizons.

A composite rank of the following criteria provides the Performance Rank:

• Stock relative performance ranked over multiple time periods

• Average of time periods taken to select rank of stocks

3. Value Screen

The top ranking stocks by key fundamental criteria show stable fundamentals and exhibit upside momentum growth potential. The following are some of the criteria that provide the Value Rank:

• Value - Price to Book (intangible book adjustment), Free Cash Flow metrics

• Quality - Return on Investment and Earnings metrics

• Financial Stability - Debt levels, Coverage and Payout ratios

• Volatility - Stock variance, Dividend variance

• Momentum - Sales Growth, Cash flow metrics

• Liquidity - Minimum market capitalisation relative to index, Shares outstanding

Implementing the Hinde Dividend Value Matrix ®

The FTSE 100 and FTSE 250 stocks are ranked using the Dividend, Performance and Value screens. An equally-weighted composite rank is then taken of these 3 ranks, which provides a final ranking from which a selection of 20 stocks is made for the portfolio.

The stocks with the highest ranking are compiled for the FTSE 100 and the FTSE 250. The top 10 from each index are then taken, subject to diversification rules, which entail that normally only 1 stock per sector per index can be invested in. For example, if the top 10 stocks are all mining companies, the selection process would take the first of these and then move on to select the next top stock from another sector. As long as a stock has the highest score in its sector, the fact that it has appeared in the final ranking means it is already eligible for investment. In exceptional circumstances, it may be that more than one stock has to be selected from an individual sector.

ISSUE 34 - SEP 2017 19

DISCLAIMER

This newsletter is intended to give general advice only on the importance of dividends within the equity space. The investments mentioned are not necessarily suitable for any individual, and you should use this information in conjunction with other advice and research to determine its suitability for your own circumstances and risk preferences. The value of all securities and investments, and the income from them, can fall as well as rise. Your investments may be subject to sudden and large falls in value and you may get back nothing at all. You should not buy any of the securities or other investments mentioned with money you cannot afford to lose. In some cases there may be significant charges which may reduce the value of your investment. You run an extra risk of losing money when you buy shares in certain securities where there is a big difference between the buying price and the selling price. If you have to sell them immediately, you may get back much less than you paid for them. The price may change quickly, particularly if the securities have an element of gearing. In the case of investment trusts and certain other funds, they may use or propose to use the borrowing of money to increase holdings of investments or invest in other securities with a similar strategy and as a result movements in the price of the securities may be more volatile than the movements in the price of underlying investments. Some investments may involve a high degree of ‘gearing’ or ‘leverage’. This means that a small movement in the price of the underlying asset may have a disproportionately dramatic effect on your investment. A relatively small adverse movement in the price of the underlying asset can result in the loss of the whole of your original investment. Changes in rates of exchange may have an adverse effect on the value or price of the investment in sterling terms, and you should be aware they may be additional dealing, transaction and custody charges for certain instruments traded in a currency other than sterling. Some investments may not be quoted on a recognised investment exchange and as a result you may find them to be ‘illiquid’. You may not be able to trade your illiquid investments, and in certain circumstances it may be difficult or impossible to sell or realise the investment. Investment in any of the assets mentioned may have tax consequences and on these you should consult your tax adviser. The opinions of the authors and/or interviewees of/in each article are their own, and are not necessarily those of the publisher. We have taken all reasonable care to ensure that all statements of fact and opinion contained in this publication are fair and accurate in all material respects. All data is from sources we consider reliable but its accuracy cannot be guaranteed. Investors should seek appropriate professional advice if any points are unclear. Ben Davies and Mark Mahaffey the editors of this newsletter, are responsible for the research ideas contained within. They or any of the contributors or other associates of the publisher may have a beneficial interest in any of the investments mentioned in this newsletter.

Disclosures of holdings: None relevant to any content discussed within this issue of the newsletter

This score is derived from 3 inputs that have been obtained from all the external analysts at leading institutions who are covering the stock:

1. The 12 month target price in relation to current price

2. The number of analysts covering the stock

3. The recommendation analysis, e.g. STRONG SELL, SELL, UNDERPERFORM or HOLD

This score is used to observe the other analysts’ view of the stock and is helpful when understanding the methodology that other analysts use to determine their 12-month target price. We ultimately get a blend of price targets that is based on different valuation metrics.

EAS Score Output:

1. The combined score will vary from 30-702. A stock with a lowest score of 30 shows the majority

of analysts not only have a full sell/underweight recommendation, but also a low 12-month target

price in relation to current price.3. A stock with the highest score of 70 shows the majority

of analysts not only have a full buy/overweight recommendation, but also a high 12-month target price in relation to current price.

Note:

On a standalone basis, the EAS score must be viewed in the following context:

• Equity analysts issue far more positive recommendations than negative

• If all analysts are overwhelmingly bearish or bullish, then this can signal a contrarian position be held, but this is determinate on the where the stock is valued.

However, in conjunction with the HDVM ®, we have found the score to be useful when it is high or momentum is turning higher, as this suggests that the stock offers deep value.

EXTERNAL ANALYST SCORE (EAS)