Embed Size (px)

Citation preview

CAPITAL BUDGETINGCAPITAL BUDGETING

Capital budgeting is finance terminology for the process of deciding whether or not to undertake an investment project. There are two standard concepts used in capital budgeting:

1. Net present value (NPV) and2. Internal rate of return (IRR).

The NPV Rule for Judging Investments and Projects

Suppose you are considering a project that has cash flows CF0, CF1, CF2, . . . , CFN. Suppose that the appropriate discount rate for this project is r. Then the NPV of the project is:

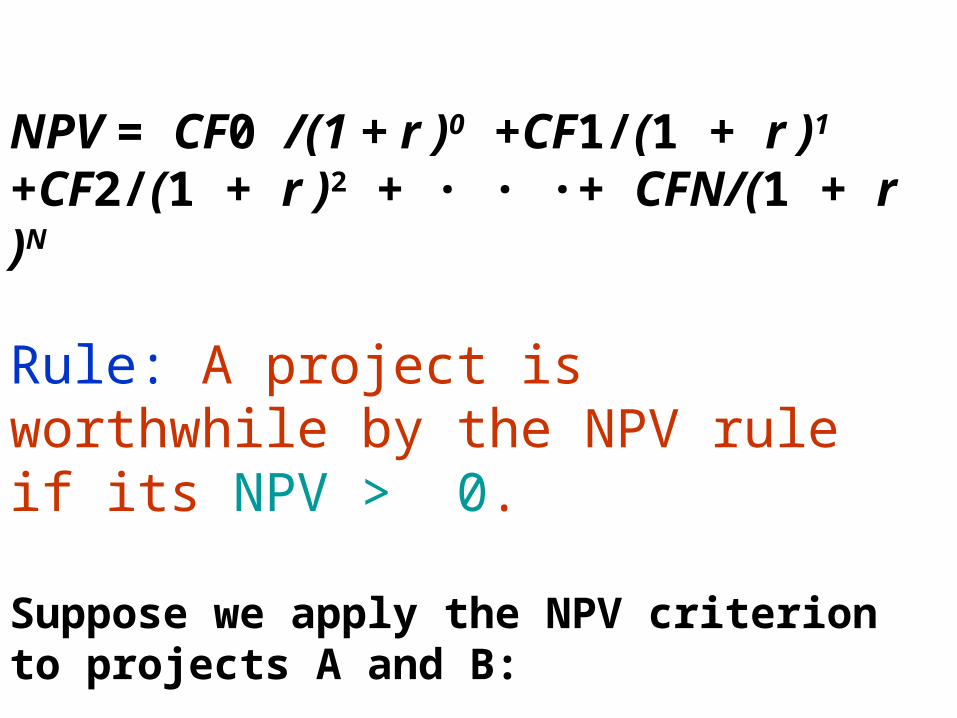

NPV = CF0 /(1 + r )0 +CF1/(1 + r )1 +CF2/(1 + r )2 + · · ·+ CFN/(1 + r )N

Rule: A project is worthwhile by the NPV rule if its NPV > 0.

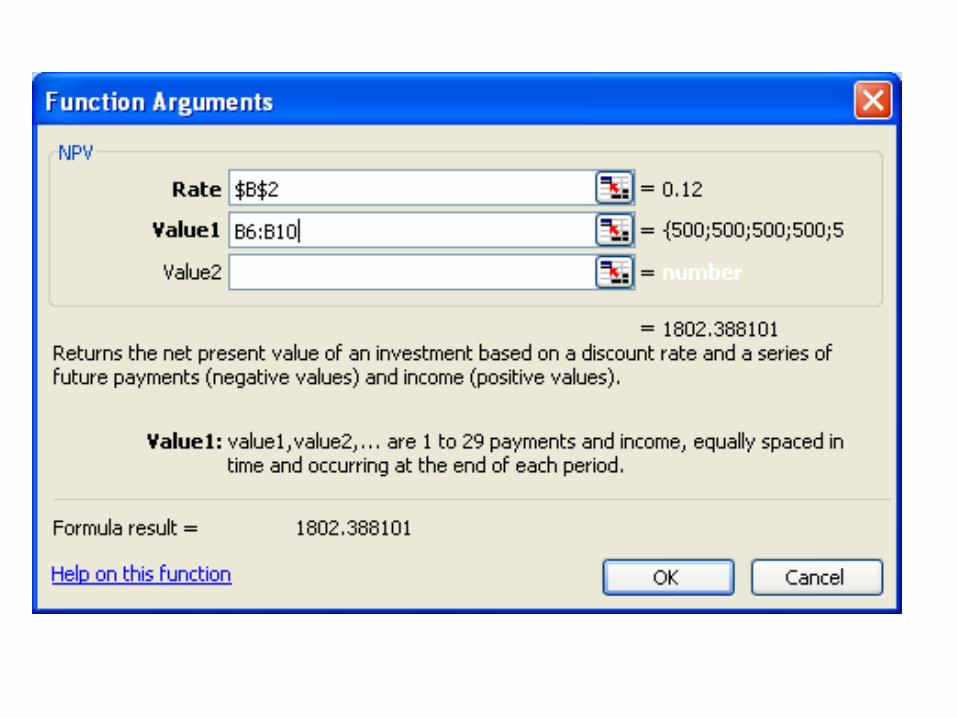

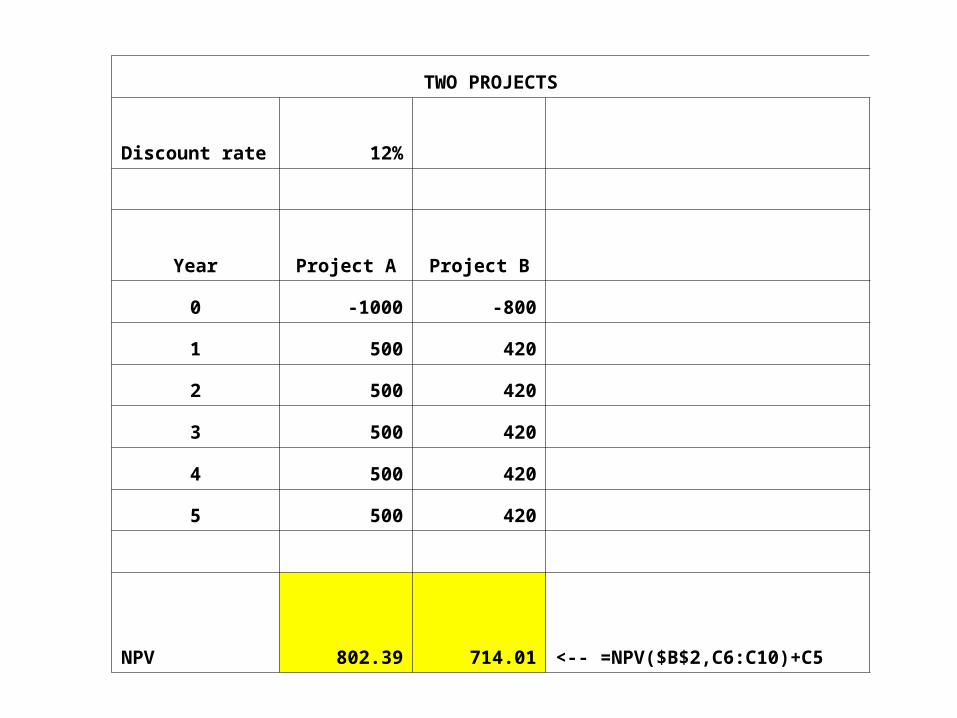

Suppose we apply the NPV criterion to projects A and B:

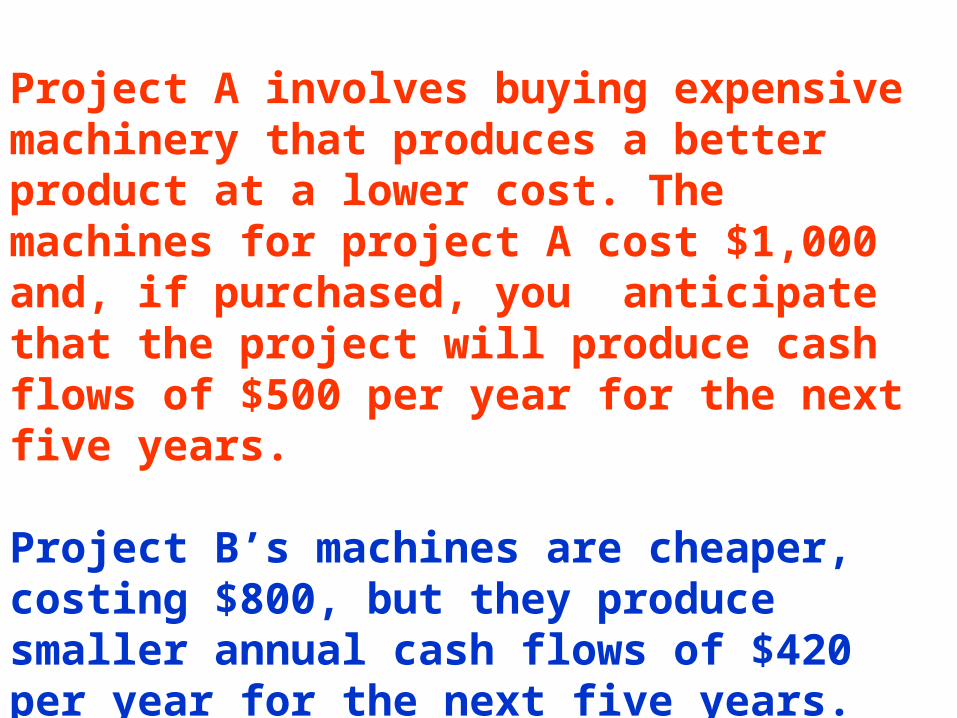

Project A involves buying expensive machinery that produces a better product at a lower cost. The machines for project A cost $1,000 and, if purchased, you anticipate that the project will produce cash flows of $500 per year for the next five years.

Project B’s machines are cheaper, costing $800, but they produce smaller annual cash flows of $420 per year for the next five years. We’ll assume that the correct discount rate is 12%.

TWO PROJECTS

Discount rate 12%

Year Project A Project B

0 -1000 -800

1 500 420

2 500 420

3 500 420

4 500 420

5 500 420

NPV 802.39 714.01 <-- =NPV($B$2,C6:C10)+C5

Both projects are worthwhile, since each has a positive NPV. If we have to choose between the two projects, then

project A is preferred to

project B because it has the higher NPV.

The IRR Rule for Judging Investments

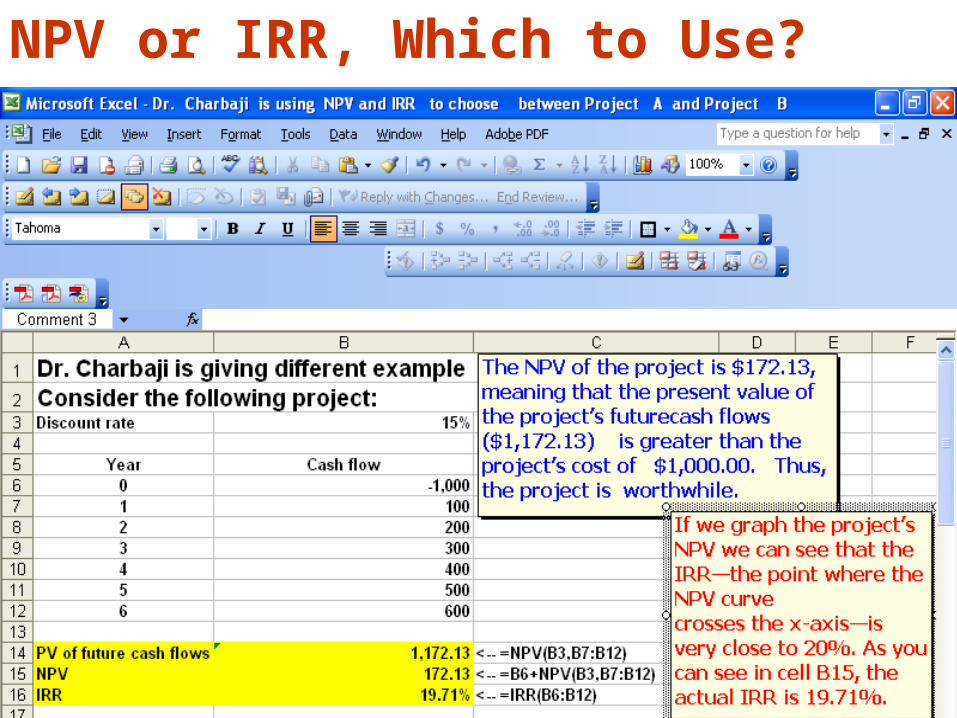

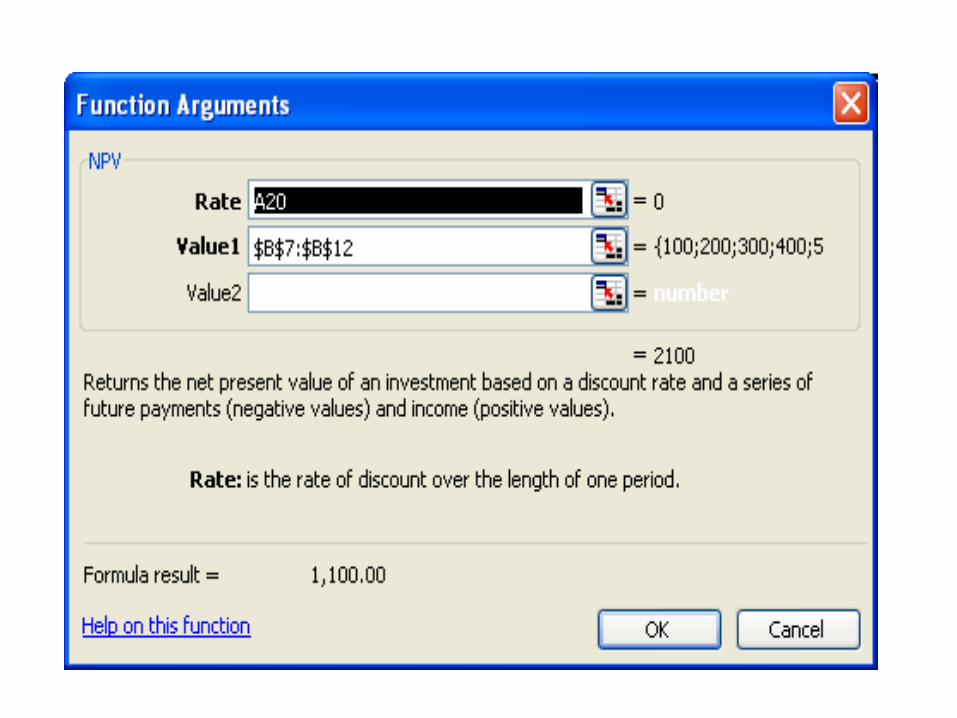

An alternative to using the NPV criterion for capital budgeting is to use the internal rate of return (IRR). IRR is defined as the discount rate for which the NPV equals zero.

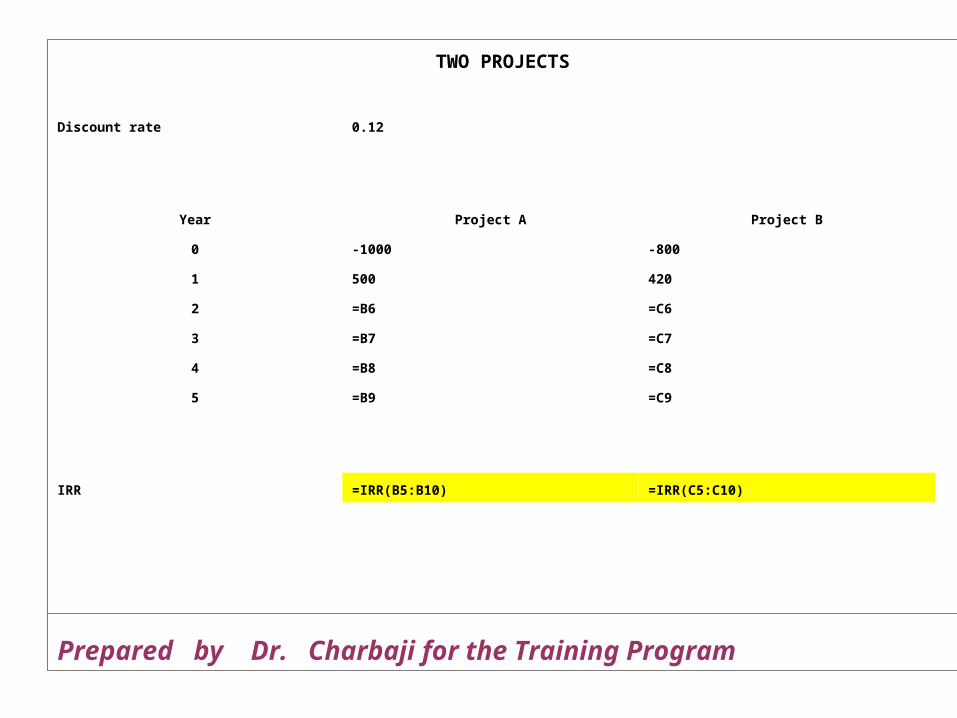

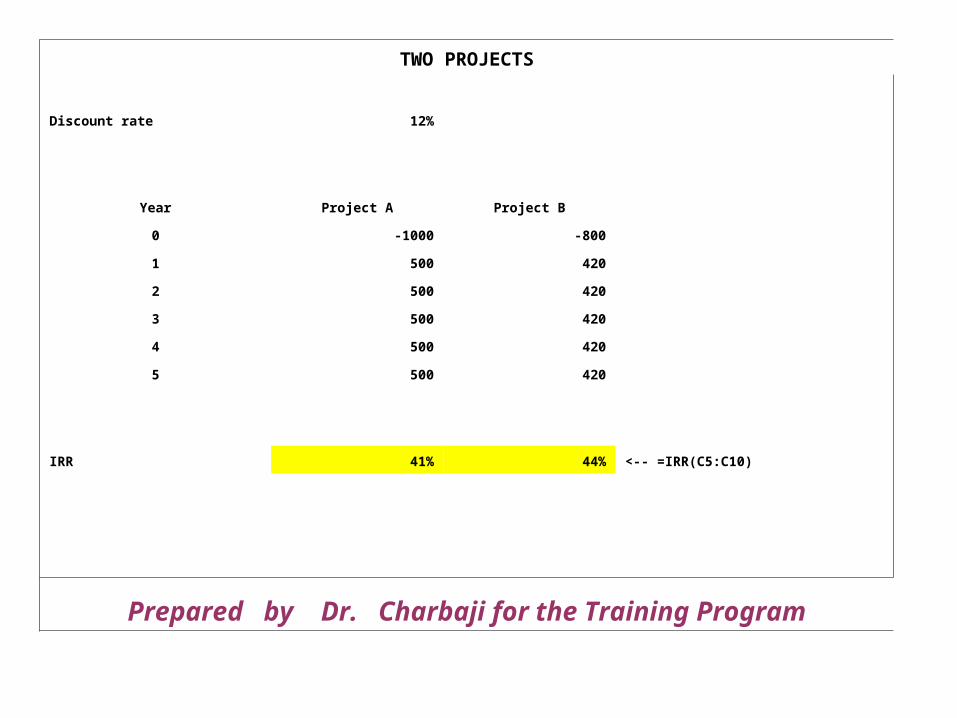

TWO PROJECTS

Discount rate 0.12

Year Project A Project B

0 -1000 -800

1 500 420

2 =B6 =C6

3 =B7 =C7

4 =B8 =C8

5 =B9 =C9

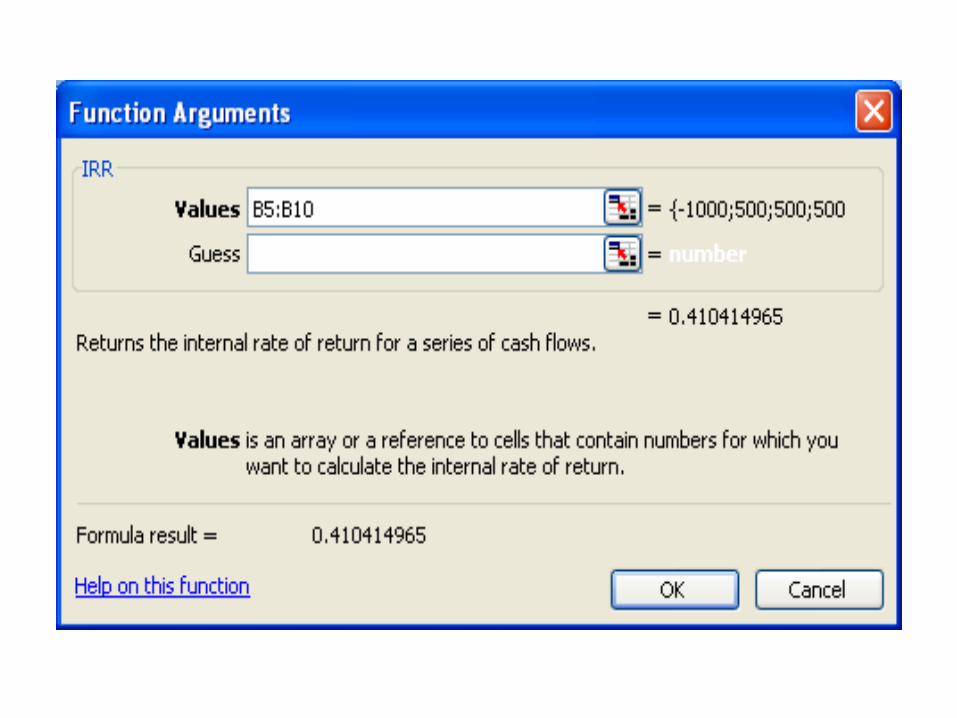

IRR =IRR(B5:B10) =IRR(C5:C10)

Prepared by Dr. Charbaji for the Training Program

TWO PROJECTS

Discount rate 12%

Year Project A Project B

0 -1000 -800

1 500 420

2 500 420

3 500 420

4 500 420

5 500 420

IRR 41% 44% <-- =IRR(C5:C10)

Prepared by Dr. Charbaji for the Training Program

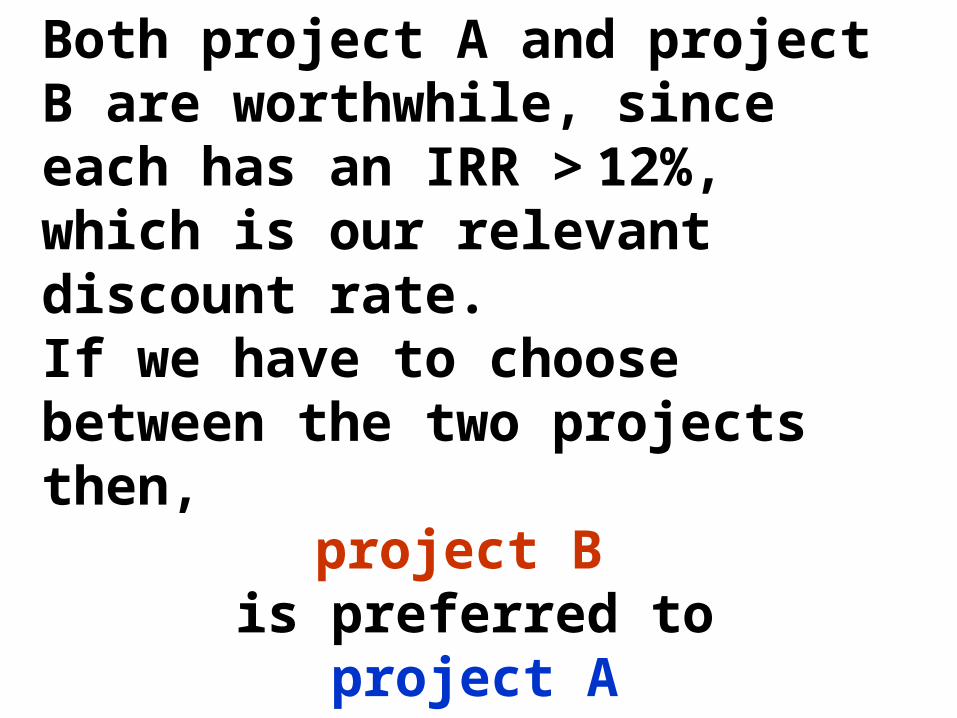

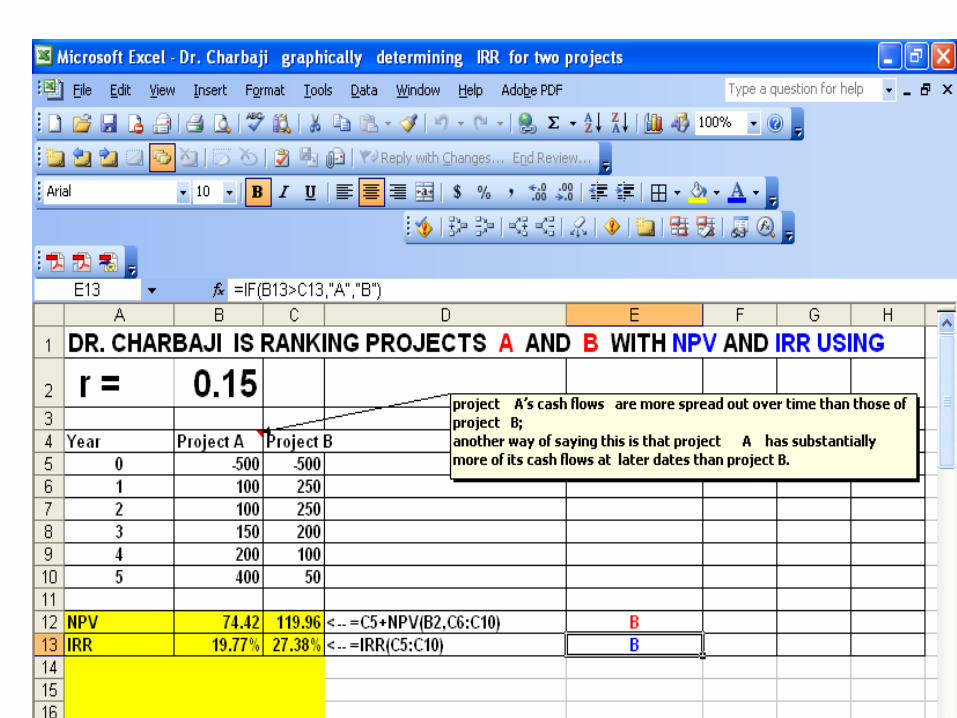

Both project A and project B are worthwhile, since each has an IRR > 12%, which is our relevant discount rate. If we have to choose between the two projects then,

project B is preferred to

project A because it has a higher IRR.

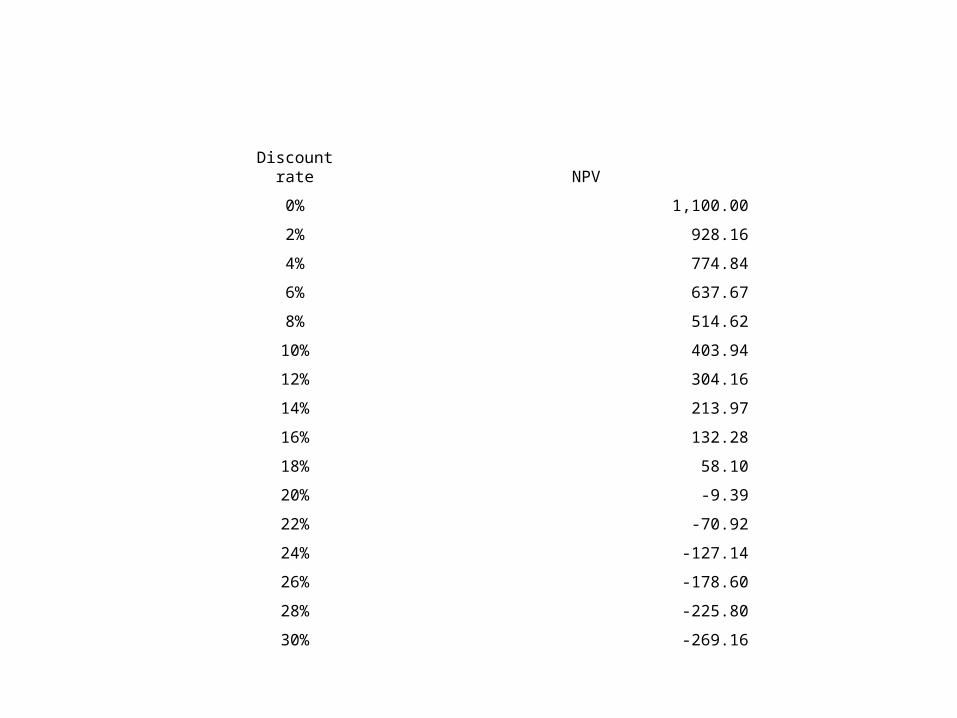

NPV or IRR, Which to Use?

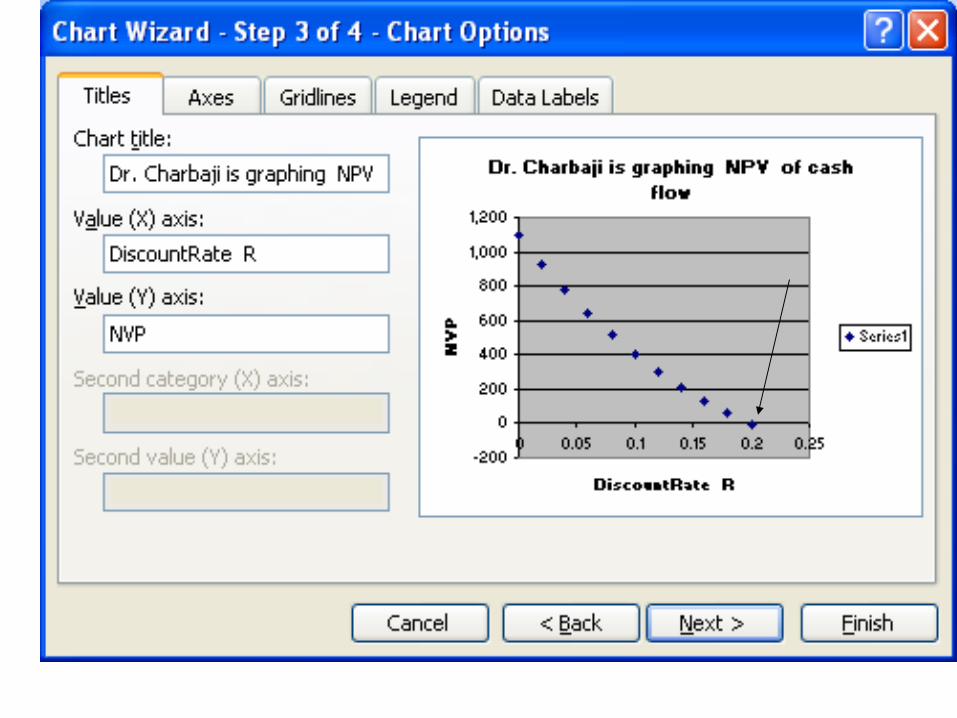

Discountrate NPV

0% 1,100.00

2% 928.16

4% 774.84

6% 637.67

8% 514.62

10% 403.94

12% 304.16

14% 213.97

16% 132.28

18% 58.10

20% -9.39

22% -70.92

24% -127.14

26% -178.60

28% -225.80

30% -269.16

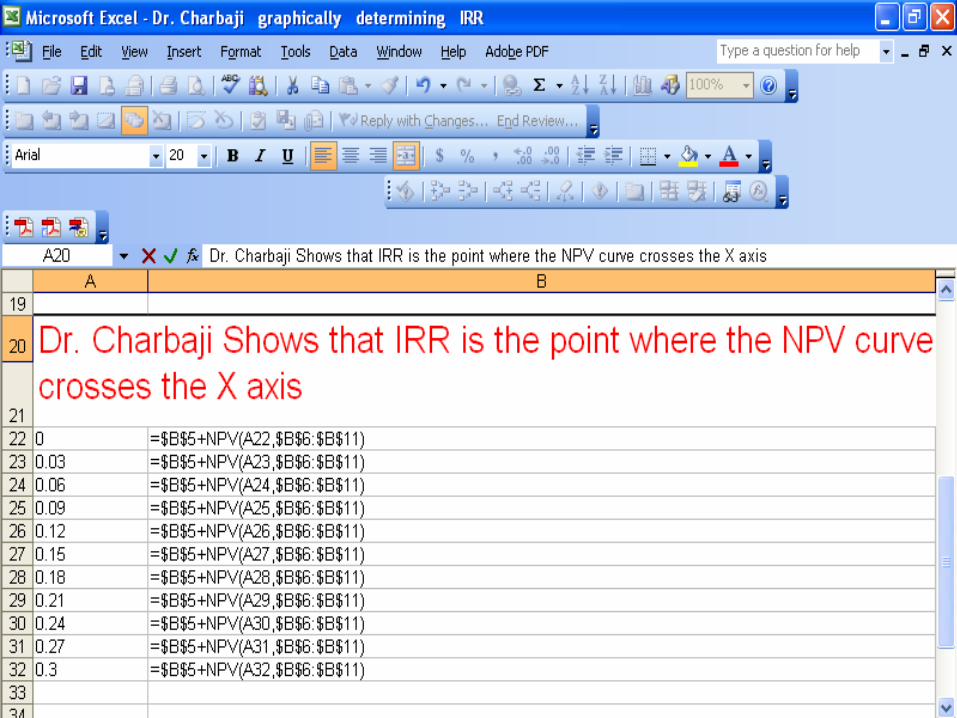

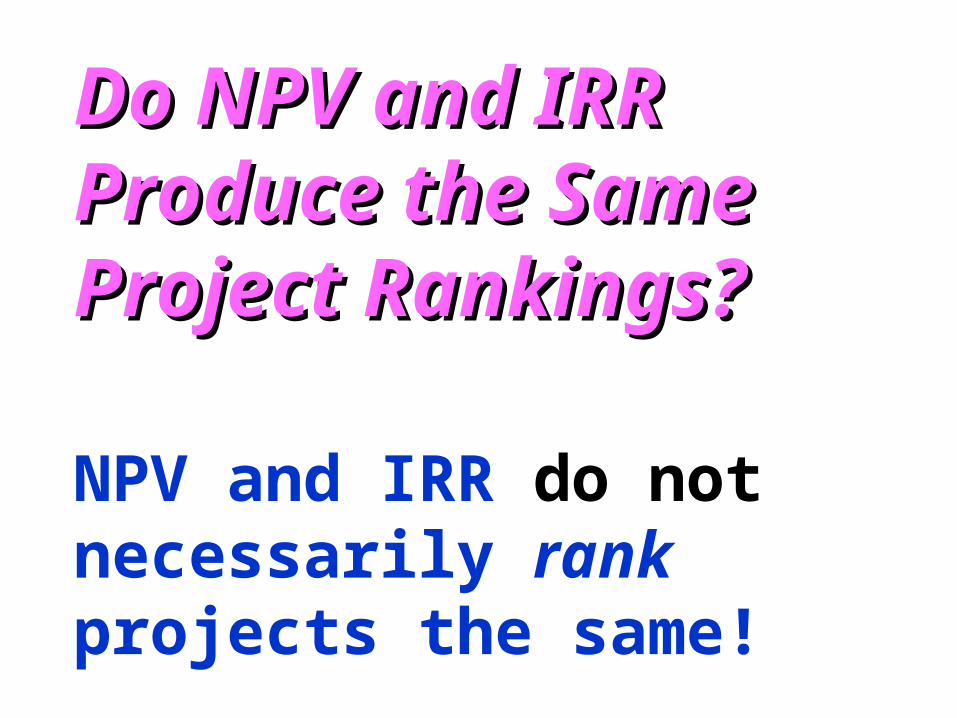

Do NPV and IRRDo NPV and IRRProduce the Same Produce the Same Project Rankings?Project Rankings?

NPV and IRR do not necessarily rank projects the same!

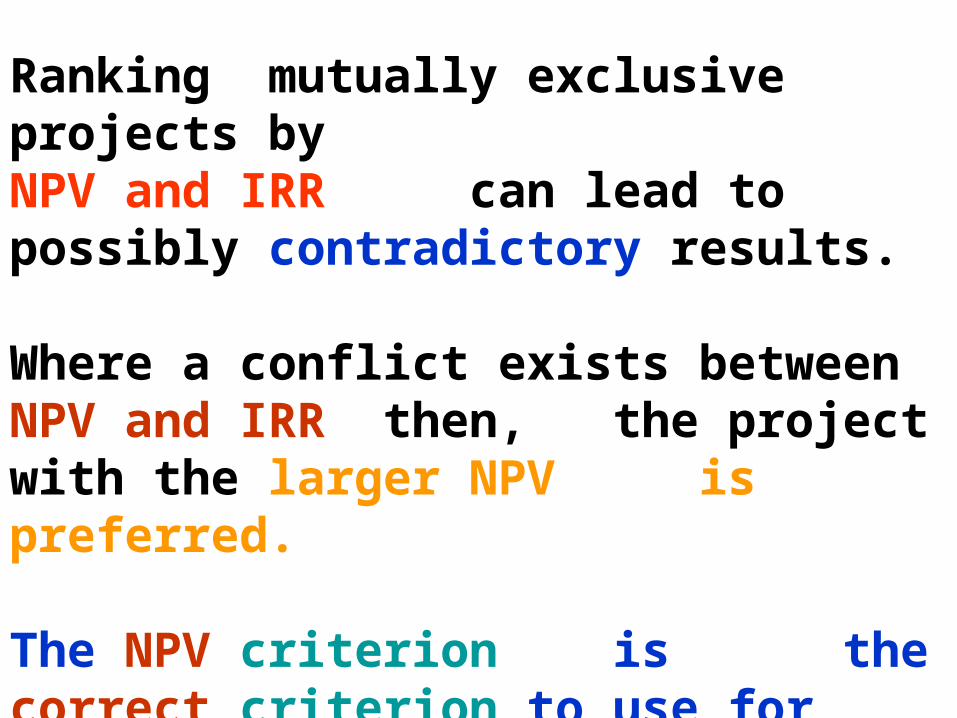

Ranking mutually exclusive projects by NPV and IRR can lead to possibly contradictory results.

Where a conflict exists between NPV and IRR then, the project with the larger NPV is preferred.

The NPV criterion is the correct criterion to use for capital budgeting.

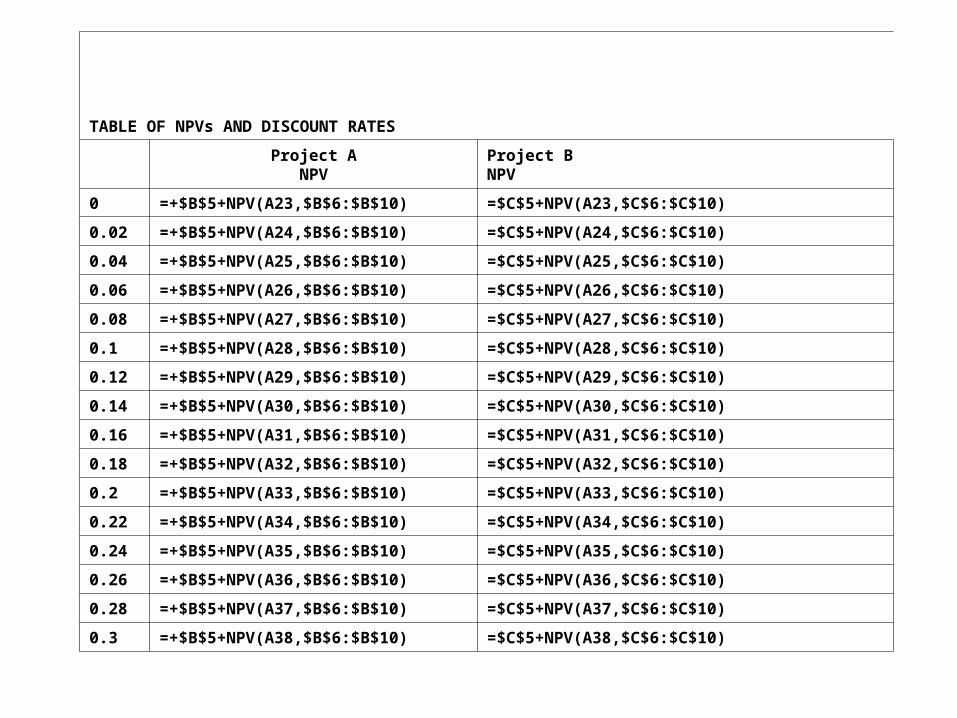

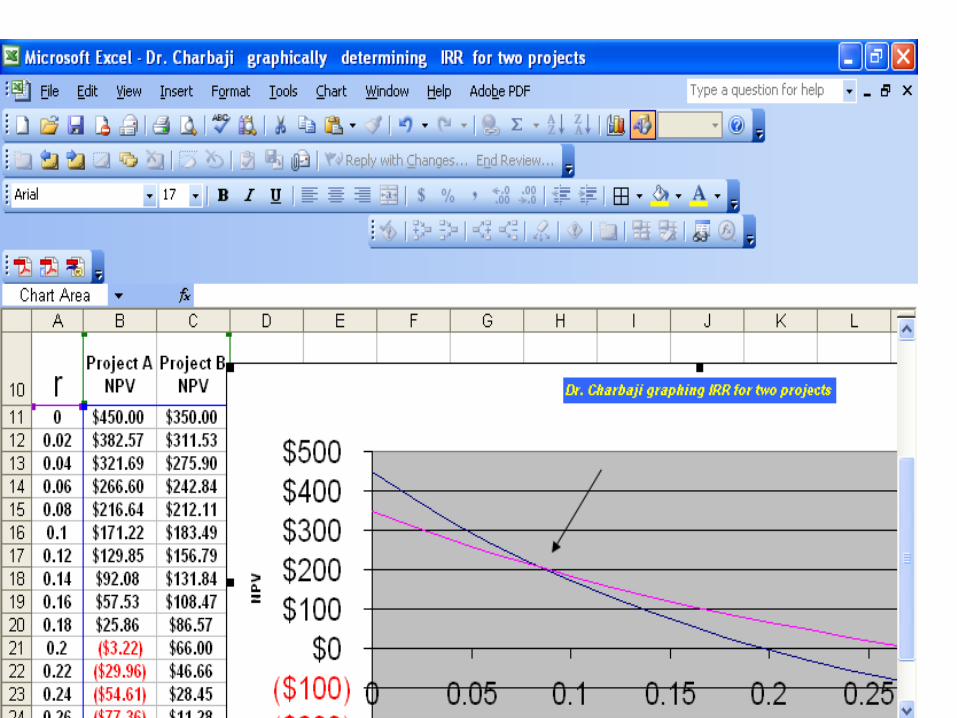

TABLE OF NPVs AND DISCOUNT RATES

Project A

NPVProject BNPV

0 =+$B$5+NPV(A23,$B$6:$B$10) =$C$5+NPV(A23,$C$6:$C$10)

0.02 =+$B$5+NPV(A24,$B$6:$B$10) =$C$5+NPV(A24,$C$6:$C$10)

0.04 =+$B$5+NPV(A25,$B$6:$B$10) =$C$5+NPV(A25,$C$6:$C$10)

0.06 =+$B$5+NPV(A26,$B$6:$B$10) =$C$5+NPV(A26,$C$6:$C$10)

0.08 =+$B$5+NPV(A27,$B$6:$B$10) =$C$5+NPV(A27,$C$6:$C$10)

0.1 =+$B$5+NPV(A28,$B$6:$B$10) =$C$5+NPV(A28,$C$6:$C$10)

0.12 =+$B$5+NPV(A29,$B$6:$B$10) =$C$5+NPV(A29,$C$6:$C$10)

0.14 =+$B$5+NPV(A30,$B$6:$B$10) =$C$5+NPV(A30,$C$6:$C$10)

0.16 =+$B$5+NPV(A31,$B$6:$B$10) =$C$5+NPV(A31,$C$6:$C$10)

0.18 =+$B$5+NPV(A32,$B$6:$B$10) =$C$5+NPV(A32,$C$6:$C$10)

0.2 =+$B$5+NPV(A33,$B$6:$B$10) =$C$5+NPV(A33,$C$6:$C$10)

0.22 =+$B$5+NPV(A34,$B$6:$B$10) =$C$5+NPV(A34,$C$6:$C$10)

0.24 =+$B$5+NPV(A35,$B$6:$B$10) =$C$5+NPV(A35,$C$6:$C$10)

0.26 =+$B$5+NPV(A36,$B$6:$B$10) =$C$5+NPV(A36,$C$6:$C$10)

0.28 =+$B$5+NPV(A37,$B$6:$B$10) =$C$5+NPV(A37,$C$6:$C$10)

0.3 =+$B$5+NPV(A38,$B$6:$B$10) =$C$5+NPV(A38,$C$6:$C$10)

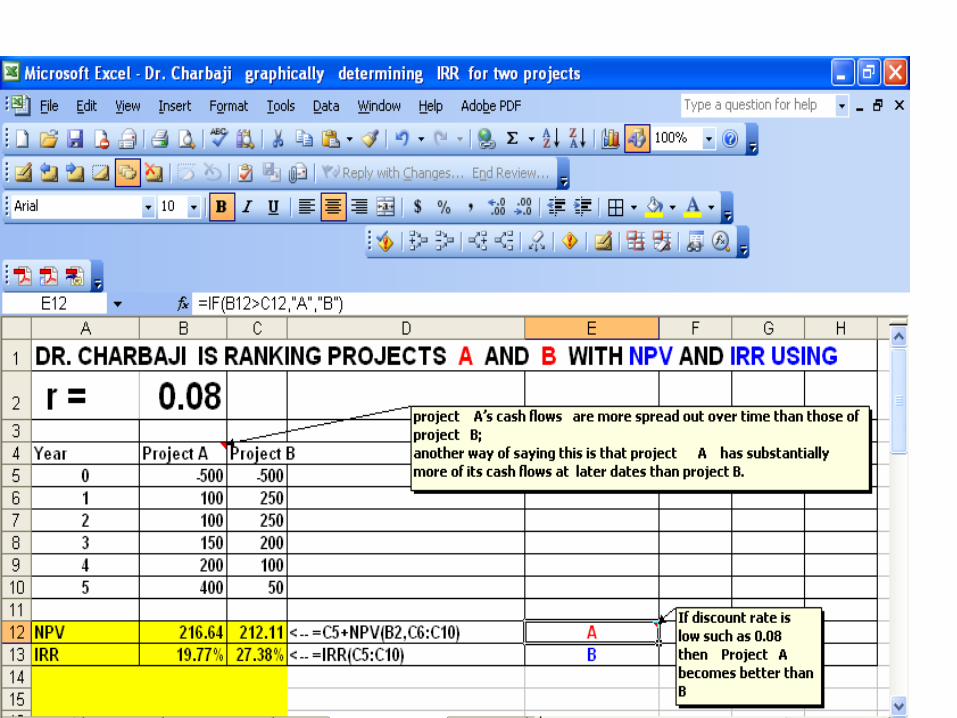

•When the discount rate is low, project A has a higher NPV than project B.•But when the discount rate is high, project B has a higher NPV. •There is a crossover point that marks the disagreement/agreement range.

• Project A’s NPV is more sensitive to changes in the discount rate than project B’s NPV. The reason for this is that project A has substantially more of its cash flows at later dates than project B.

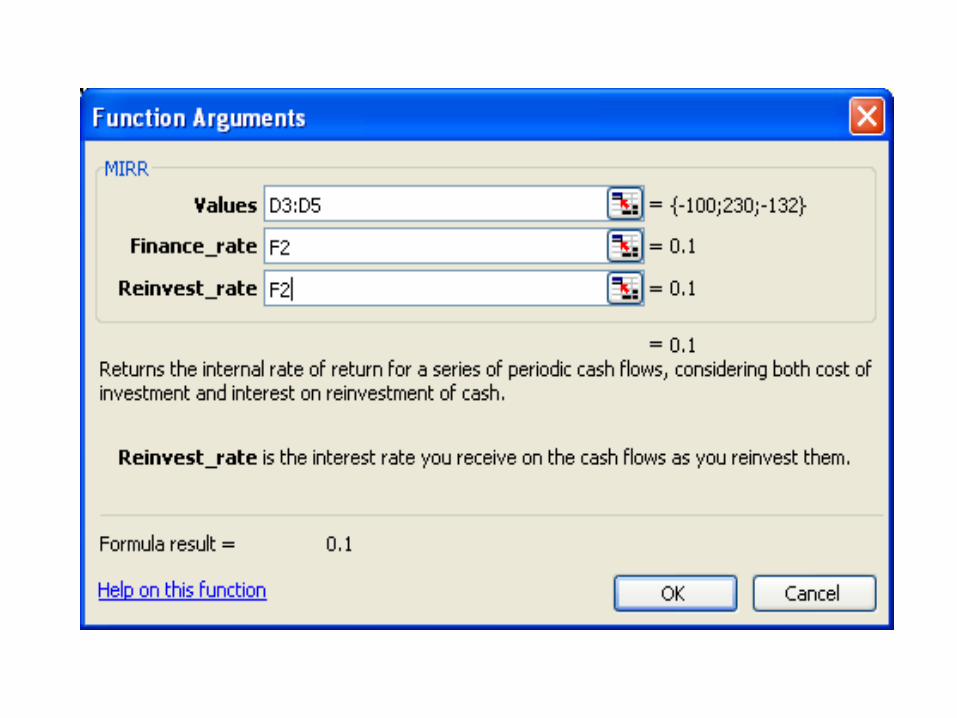

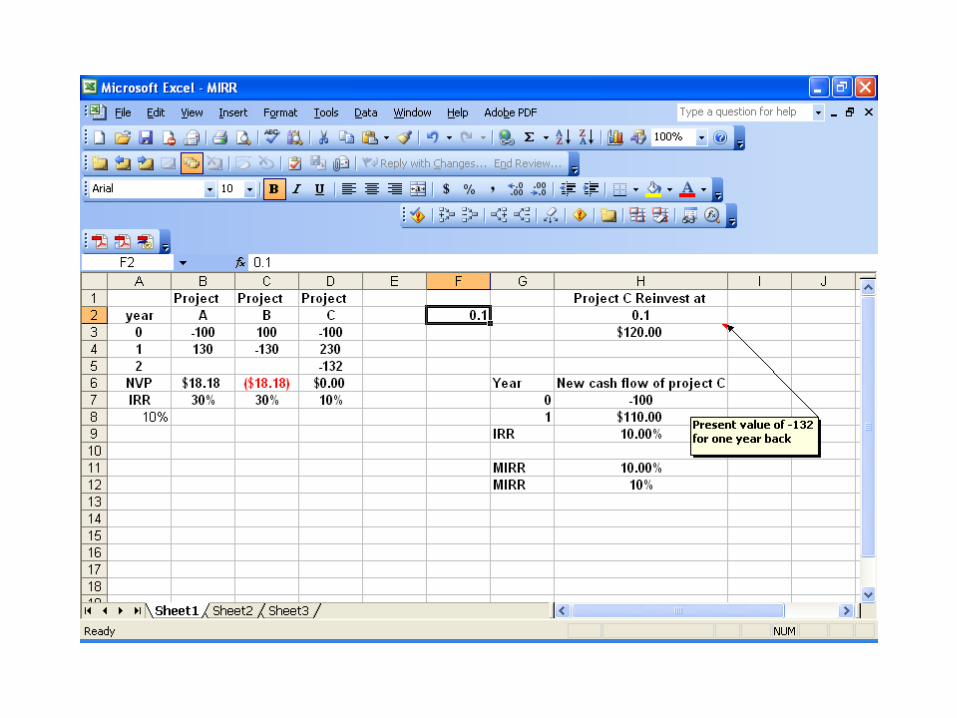

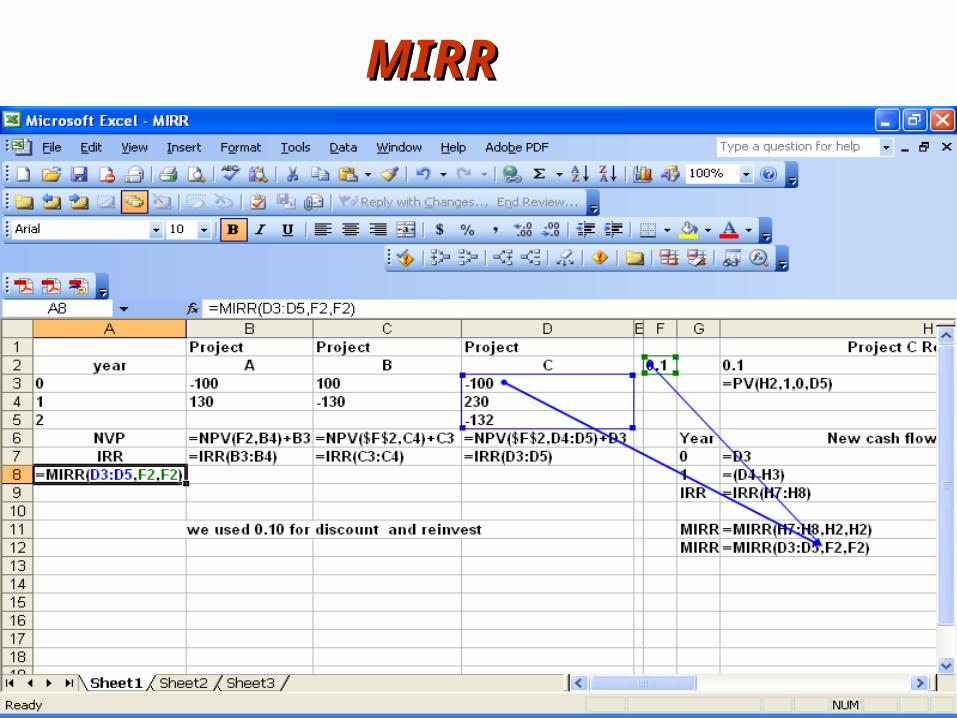

The Modified Internal Rate of The Modified Internal Rate of ReturnReturn

MIRRMIRR avoids the problem of avoids the problem of

multiple IRRsmultiple IRRs

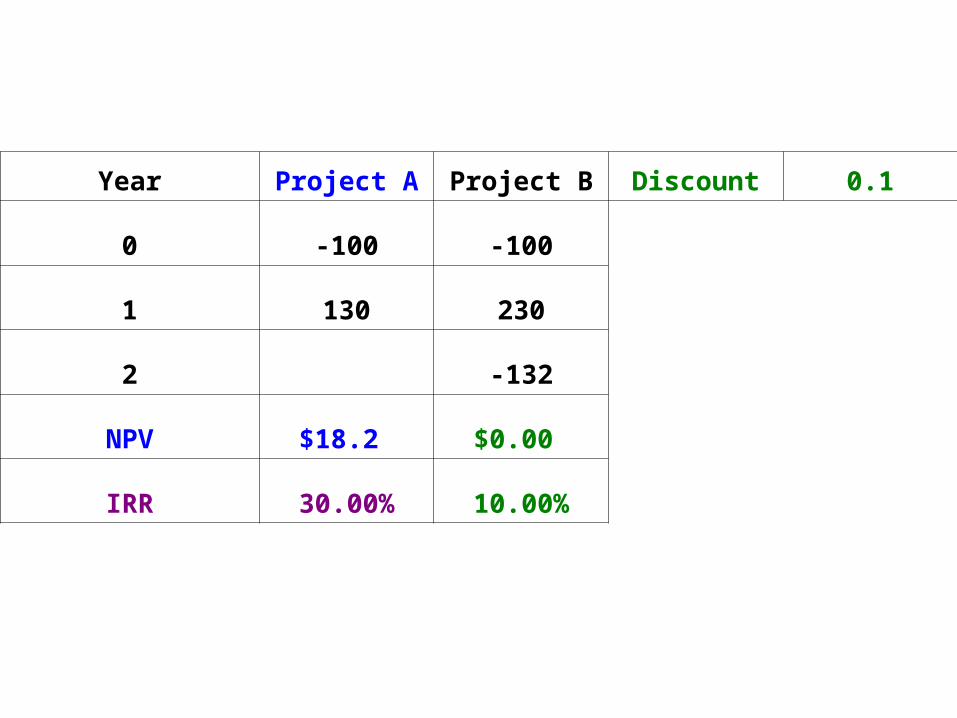

Year Project A Project B Discount 0.1

0 -100 -100

1 130 230

2 -132

NPV $18.2 $0.00

IRR 30.00% 10.00%

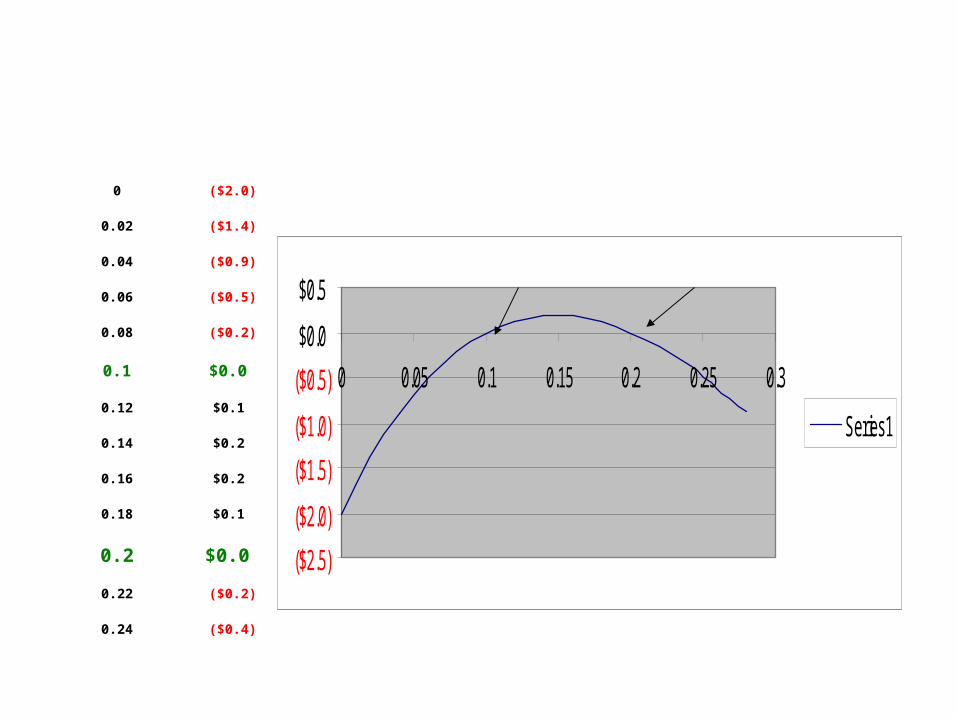

0 ($2.0)

0.02 ($1.4)

0.04 ($0.9)

0.06 ($0.5)

0.08 ($0.2)

0.1 $0.0

0.12 $0.1

0.14 $0.2

0.16 $0.2

0.18 $0.1

0.2 $0.0

0.22 ($0.2)

0.24 ($0.4)

($2.5)

($2.0)

($1.5)

($1.0)

($0.5)

$0.0

$0.5

0 0.05 0.1 0.15 0.2 0.25 0.3

Series1

MIRRMIRR