Embed Size (px)

Citation preview

LIABILITIES(Sources of Funds)

Long Term Liabilities / Fixed Liabilities

Short Term Liabilities / Current Liabilities

ASSETS(Application of Funds)

Long Term Assets / Fixed Assets

Short Term Assets/ Current Assets

Balance Sheet

Working Capital

Functions of Financial Management

• InvestmentLong –TermShort – Term

• Financing• Dividend Policy

Investment Function

• The long term investment function/decisions involves the acquisition of long term or fixed assets.

• The term long term investment is used interchangeably with Capital Budgeting, Capital Investment, Capital Project or Project Management

• Short term investment function/decisions involves working capital or management of current assets and current liabilities

Investment Function

Capital Investment decisions

Capital Budgeting /

Project Management

Working Capital

Investment decisions

Cash ManagementReceivables Management

Inventory Management

Graphically

Loan or Investment Strategic Plan

Loan Proposal Operational Start-up /Capital budgeting

Target Reader

External Internal

Existing Business

Start-up

Stag

e of

Dev

elop

men

t

Project Management / Capital Budgeting

MM

S –

Sem

II(F

inan

cial

Man

agem

ent)

What is a Project?

• A project is “a unique endeavor to produce a set of deliverables within clearly specified time, cost and quality constraints”.

• A project can be defined as initiative to achieve specific objectives, within a timescale, in a given context.

Cont…Projects are different from standard business operational activities as they: • Are unique in nature. They do not involve repetitive processes. Every

project undertaken is different from the last, whereas operational activities often involve undertaking repetitive (identical) processes

• Have a defined timescale. Projects have a clearly specified start and end date within which the deliverables must be produced to meet a specified customer requirement

• Have an approved budget. Projects are allocated a level of financial expenditure within which the deliverables must be produced to meet a specified customer requirement

• Have limited resources. At the start of a project an agreed amount of labor, equipment and materials is allocated to the project

• Involve an element of risk. Projects entail a level of uncertainty and therefore carry business risk.

• Achieve beneficial change. The purpose of a project, typically, is to improve an organization through the implementation of business change.

Objective of Project Management

• The main objective of project management is to optimize project cost, time and quality.

10

Should we build thisplant?

Importance of Capital Investments

Importance of Capital Investments

• Heavy substantial outlay• High degree of risk• Large anticipated benefits• High gestation period i.e. relative long term

period between initial outlay and anticipated return.

• Irreversible decision.

Types of Capital Investments• Mandatory investments e.g. pollution control

equipment's, medical dispensary, fire fighting equipment's, crèche in factory.

• Replacement projects.• Expansion projects e.g. increase the capacity,

widen the distribution network.• Diversification project e.g. producing new

product.• Research and development.• Strategic investment projects

Steps / PhasesPlanning

Analysis / Evaluation

Selection

Financing

Implementation and Execution

Follow Up and Review

Project formulation

Project Planning

• Generation of an idea• Selection of an idea• Converting the idea into a potential

investment opportunity• Assembling of investment proposals

Project Formulation

• Feasibility study– Preliminary Analysis,– Market,– Technical,– Financial,– Economic and Ecological

Evaluation Criteria

• Discounted Cash Flow (DCF) Criteria– Net Present Value (NPV)– Internal Rate of Return (IRR)– Profitability Index (PI)

• Non-discounted Cash Flow Criteria– Payback Period (PB)– Discounted Payback Period (DPB)– Accounting Rate of Return (ARR)

Methods

Discounted Cash Flow

Net Present Value

Internal Rate of Return

Profitability Index

Traditional

Pay Back Period

Average Rate of Return

NPV

• NPV = PVinflows – Pvoutflows

• If NPV ≥ 0, then accept the project; otherwise reject the project.

CF1 CF2 CFn (1+r)1 (1+r)2 (1+r)n

+ . . . ++ - I.I.NPV =

.

1 01

CFk

CFNPV tt

n

t

PI

• If PI ≥ 1, then accept the real investment project; otherwise, reject it.

Investment InitialPVPI InflowsCash

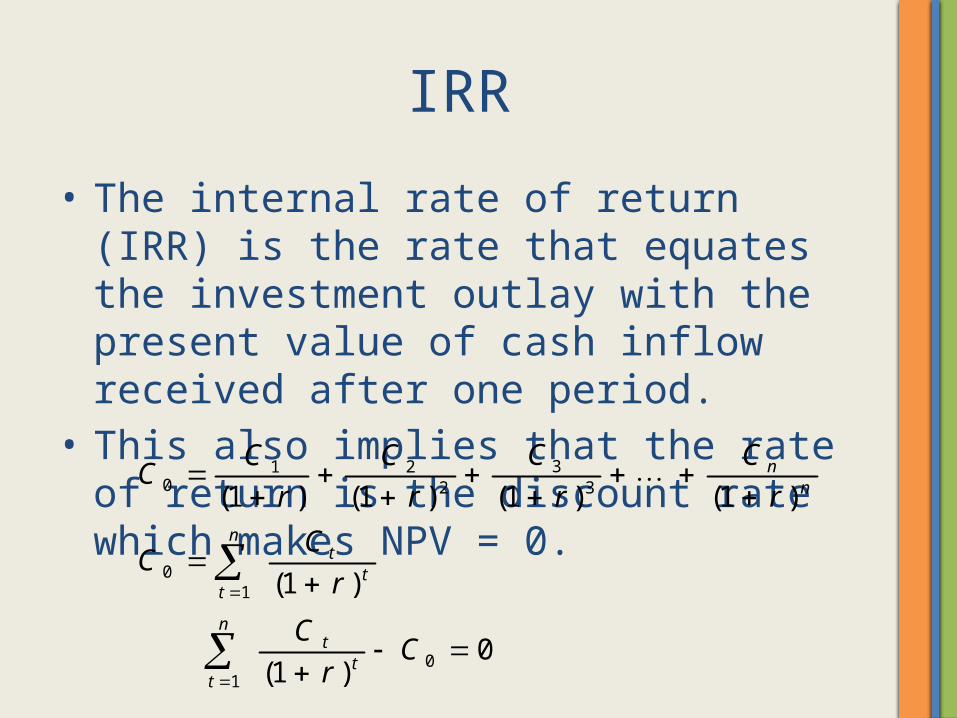

IRR

• The internal rate of return (IRR) is the rate that equates the investment outlay with the present value of cash inflow received after one period.

• This also implies that the rate of return is the discount rate which makes NPV = 0.

31 20 2 3

01

01

(1 ) (1 ) (1 ) (1 )

(1 )

0(1 )

nn

nt

tt

nt

tt

C CC CCr r r r

CC

r

CC

r

Payback

• Payback is the number of years required to recover the original cash outlay invested in a project.

• If the project generates constant annual cash inflows, the payback period can be computed by dividing cash outlay by the annual cash inflow. That is:

0Initial InvestmentPayback = = Annual Cash Inflow

CC

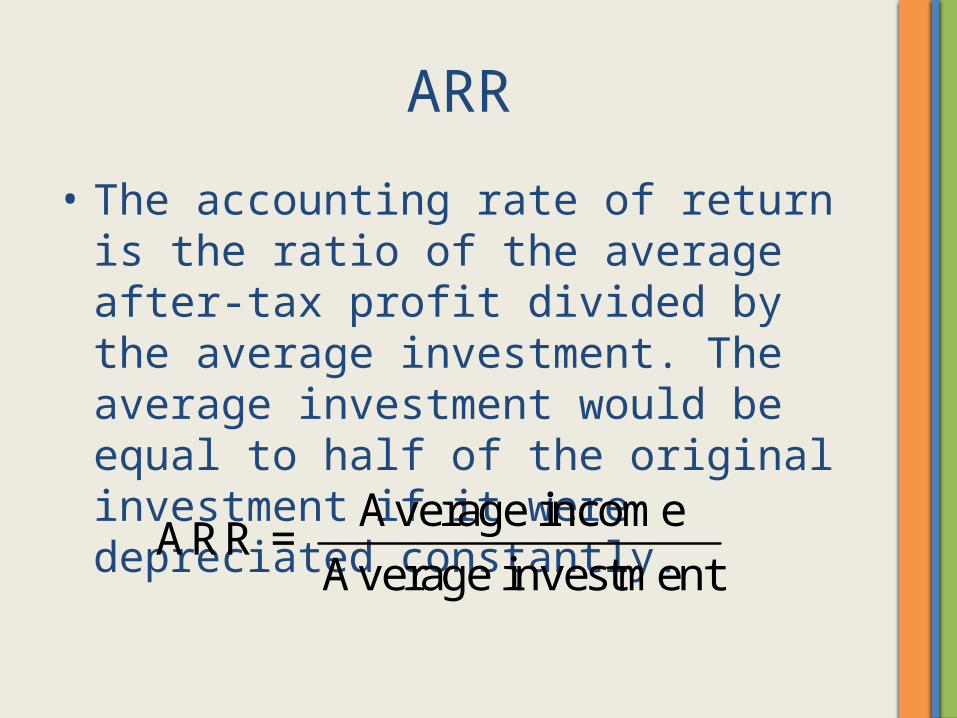

ARR

• The accounting rate of return is the ratio of the average after-tax profit divided by the average investment. The average investment would be equal to half of the original investment if it were depreciated constantly.

Average incomeARR = Average investment

Steps in Capital Budgeting

• Estimate cash flows (inflows & outflows).• Assess risk of cash flows.• Determine appropriate discount rate for

project.• Evaluate cash flows. (Find NPV or IRR etc.)• Make Accept/Reject Decision

Project Cost and Project Revenue

Components of Capital Cost of a Project (Initial Investment)

• Land• Land development• Buildings• Plant and Machinery• Electricals• Transport and erection charges• Know-how / consultancy fees• Miscellaneous assets• Preliminary and preoperative expenses• Provision for contingencies• Margin money for working capital

Operational Cashflow estimation

• Capacity Utilization• Life – Useful years• Projected Cashflow statement : Cash Inflow

– Cash Outflow

Projected Cashflow statement

SalesLess: Operating expense (Raw Material,

Labour charges, Overhead expenses)Less: Interest on LoansLess: DepreciationPBTLess: Provision for Income TaxesPAT

Cont…..

Cont….

PATAdd: DepreciationCashflows after tax (CFAT)Add: Salvage value of assets (if any)Add / Less: Tax benefit on short term capital loss / gainAdd: Recovery of working capital (if any)Free Cash Flows (FCF)Multiply: Discounting FactorPresent value of cash Inflows