Embed Size (px)

Citation preview

© Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Candor Research

Expert Analysis & Insight

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

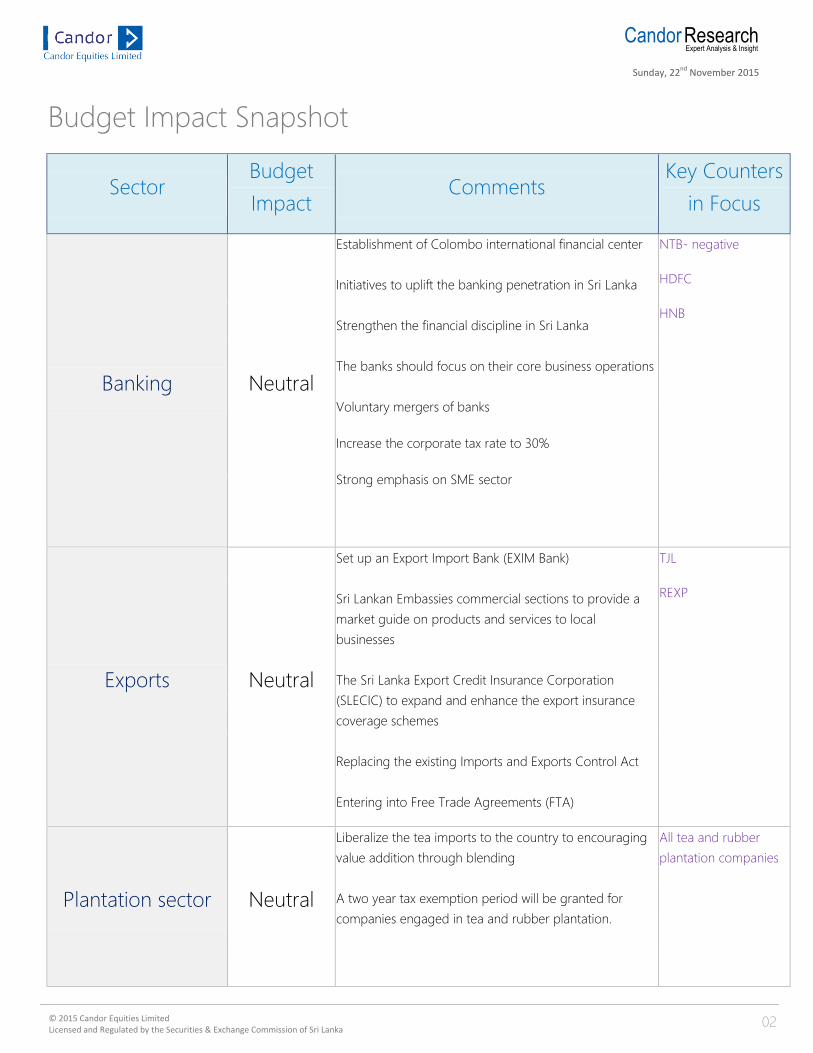

Budget Impact Snapshot

Sector Budget

Impact Comments

Key Counters

in Focus

Banking Neutral

Establishment of Colombo international financial center

Initiatives to uplift the banking penetration in Sri Lanka

Strengthen the financial discipline in Sri Lanka

The banks should focus on their core business operations

Voluntary mergers of banks

Increase the corporate tax rate to 30%

Strong emphasis on SME sector

NTB- negative

HDFCNB

HNBNTB- negative

NDB

SAMP

SEYB

UBC

HDFC

Exports Neutral

Set up an Export Import Bank (EXIM Bank)

Sri Lankan Embassies commercial sections to provide a

market guide on products and services to local

businesses

The Sri Lanka Export Credit Insurance Corporation

(SLECIC) to expand and enhance the export insurance

coverage schemes

Replacing the existing Imports and Exports Control Act

Entering into Free Trade Agreements (FTA)

TJL

REXP

Plantation sector Neutral

Liberalize the tea imports to the country to encouraging

value addition through blending

A two year tax exemption period will be granted for

companies engaged in tea and rubber plantation.

All tea and rubber

plantation companies

02

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

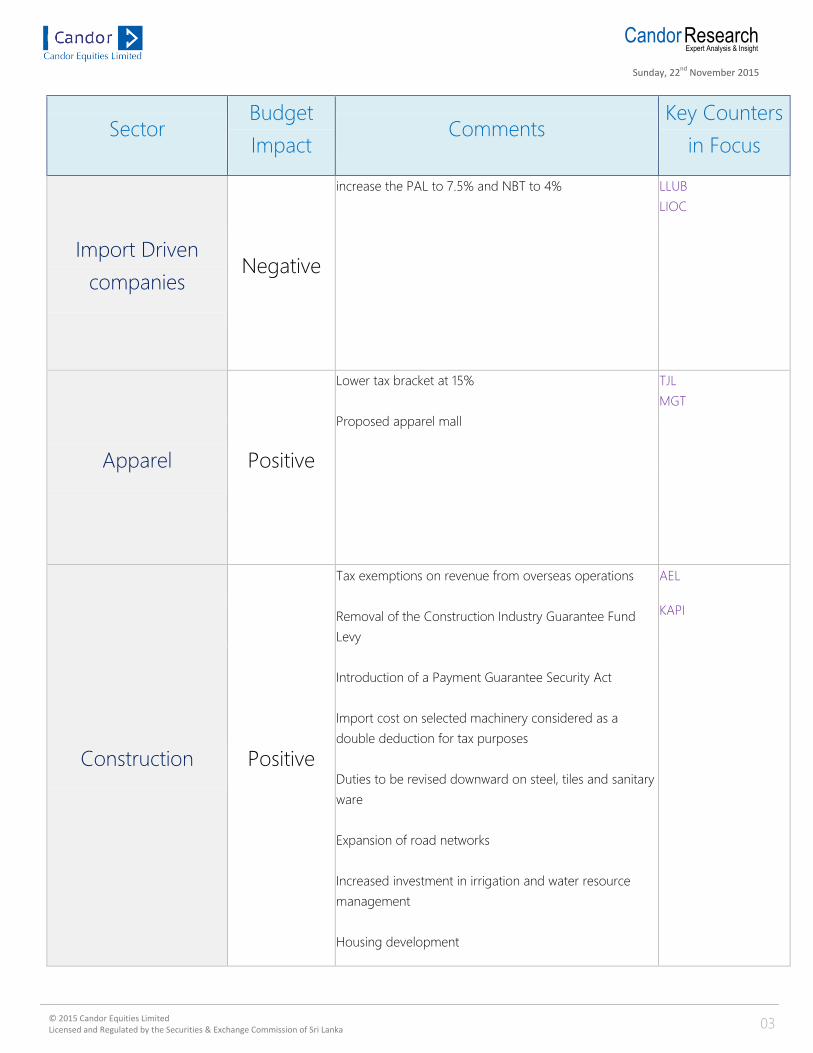

Sector Budget

Impact Comments

Key Counters

in Focus

Import Driven

companies Negative

increase the PAL to 7.5% and NBT to 4% LLUB

LIOC

Apparel Positive

Lower tax bracket at 15%

Proposed apparel mall

TJL

MGT

Construction Positive

Tax exemptions on revenue from overseas operations

Removal of the Construction Industry Guarantee Fund

Levy

Introduction of a Payment Guarantee Security Act

Import cost on selected machinery considered as a

double deduction for tax purposes

Duties to be revised downward on steel, tiles and sanitary

ware

Expansion of road networks

Increased investment in irrigation and water resource

management

Housing development

AEL

KAPI

03

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

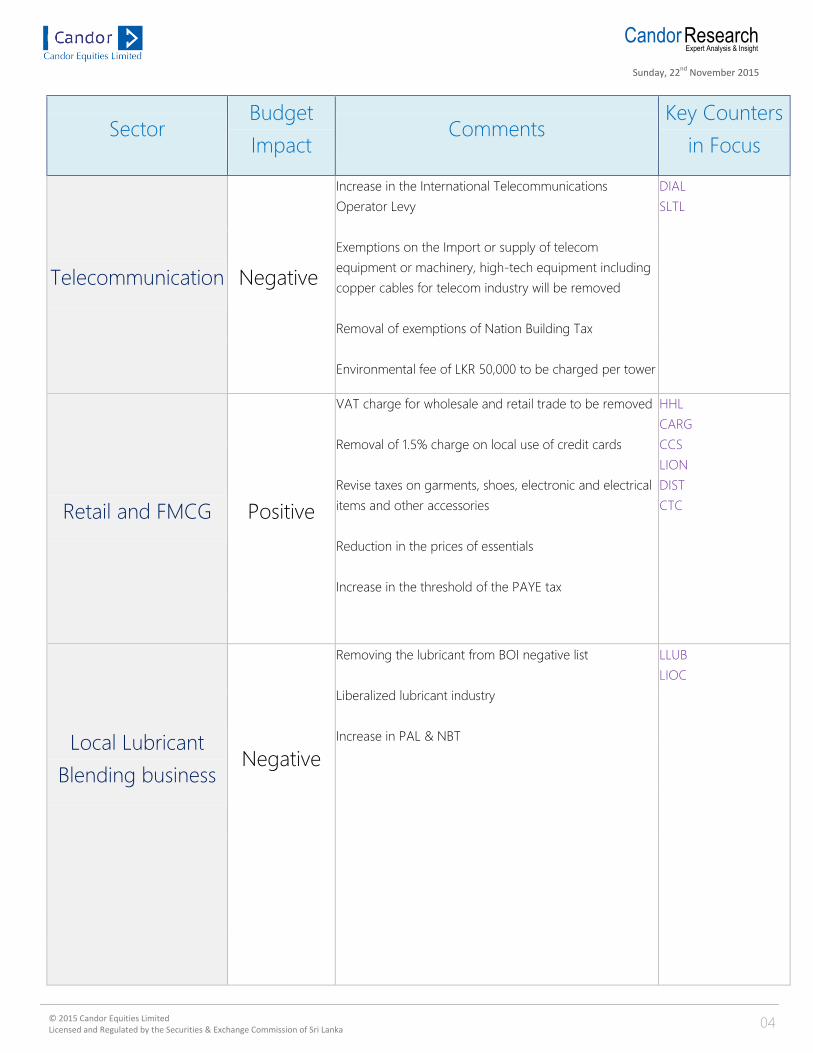

Sector Budget

Impact Comments

Key Counters

in Focus

Telecommunication Negative

Increase in the International Telecommunications

Operator Levy

Exemptions on the Import or supply of telecom

equipment or machinery, high-tech equipment including

copper cables for telecom industry will be removed

Removal of exemptions of Nation Building Tax

Environmental fee of LKR 50,000 to be charged per tower

DIAL

SLTL

Retail and FMCG Positive

VAT charge for wholesale and retail trade to be removed

Removal of 1.5% charge on local use of credit cards

Revise taxes on garments, shoes, electronic and electrical

items and other accessories

Reduction in the prices of essentials

Increase in the threshold of the PAYE tax

HHL

CARG

CCS

LION

DIST

CTC

Local Lubricant

Blending business Negative

Removing the lubricant from BOI negative list

Liberalized lubricant industry

Increase in PAL & NBT

LLUB

LIOC

04

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Sector Budget

Impact Comments

Key Counters

in Focus

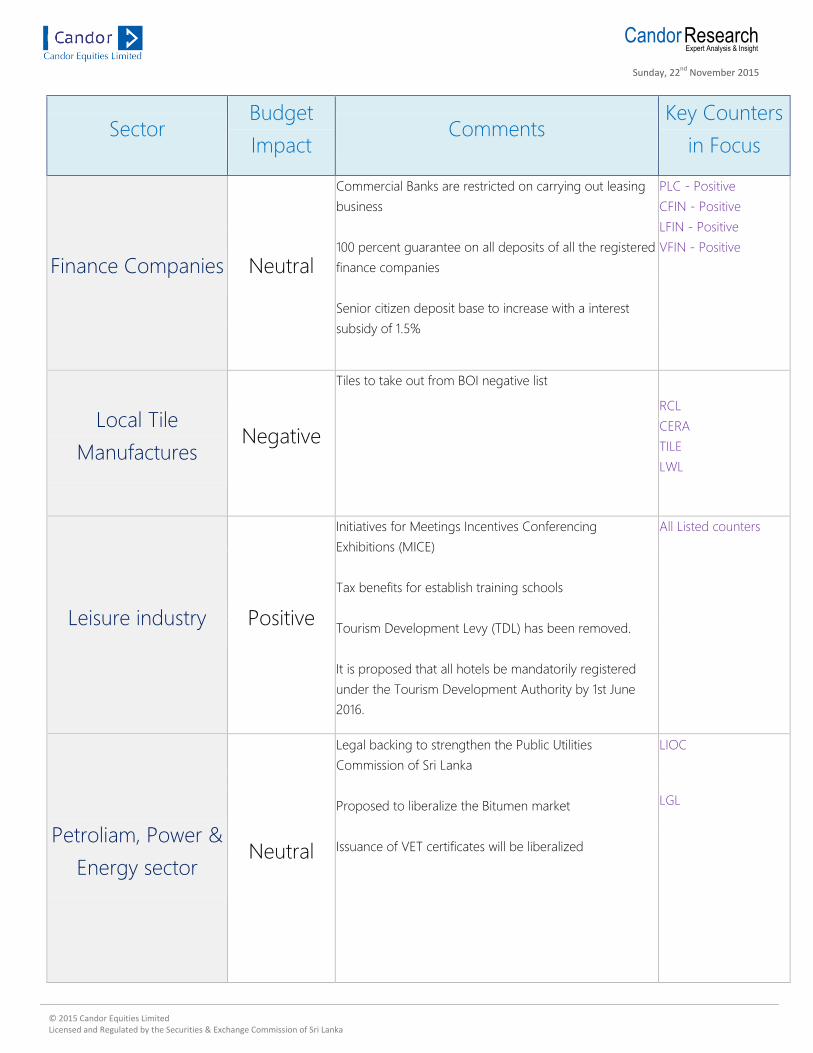

Finance Companies Neutral

Commercial Banks are restricted on carrying out leasing

business

100 percent guarantee on all deposits of all the registered

finance companies

Senior citizen deposit base to increase with a interest

subsidy of 1.5%

PLC - Positive

CFIN - Positive

LFIN - Positive

VFIN - Positive

Local Tile

Manufactures Negative

Tiles to take out from BOI negative list

RCL

CERA

TILE

LWL

Leisure industry Positive

Initiatives for Meetings Incentives Conferencing

Exhibitions (MICE)

Tax benefits for establish training schools

Tourism Development Levy (TDL) has been removed.

It is proposed that all hotels be mandatorily registered

under the Tourism Development Authority by 1st June

2016.

All Listed counters

Petroliam, Power &

Energy sector Neutral

Legal backing to strengthen the Public Utilities

Commission of Sri Lanka

Proposed to liberalize the Bitumen market

Issuance of VET certificates will be liberalized

LIOC

LGL

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Sector Budget

Impact Comments

Key Counters

in Focus

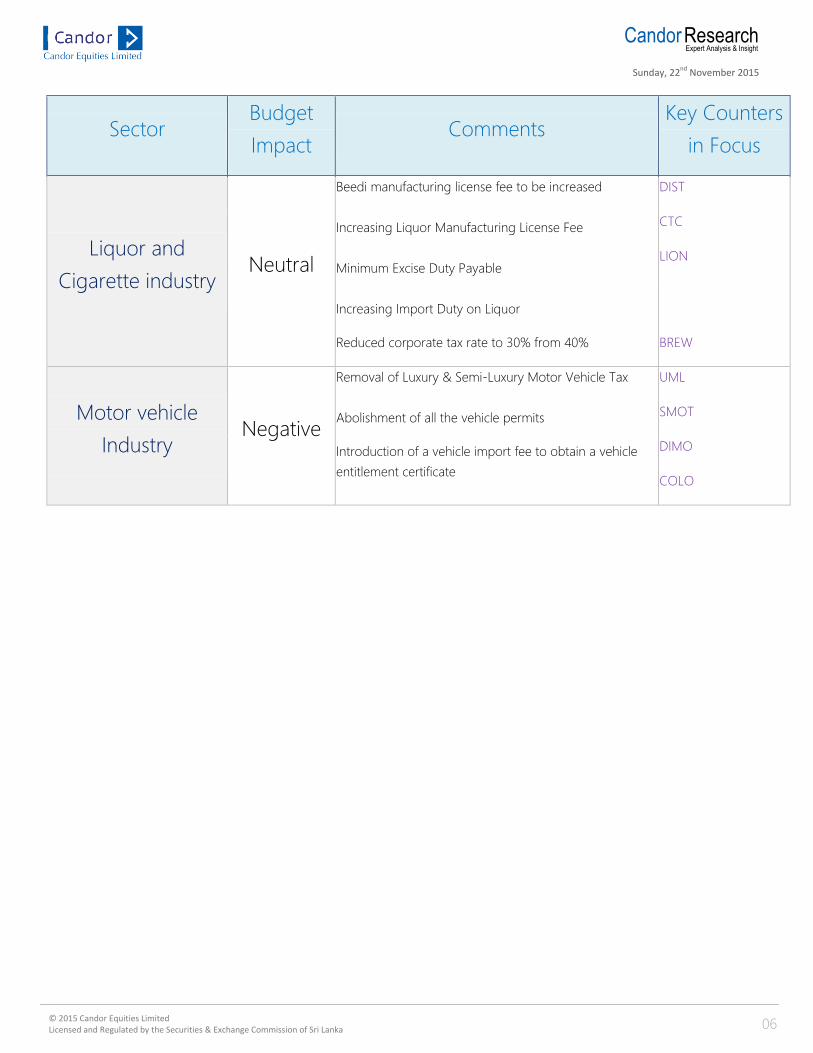

Liquor and

Cigarette industry Neutral

Beedi manufacturing license fee to be increased

Increasing Liquor Manufacturing License Fee

Minimum Excise Duty Payable

Increasing Import Duty on Liquor

Reduced corporate tax rate to 30% from 40%

DIST

CTC

LION

BREW

Motor vehicle

Industry Negative

Removal of Luxury & Semi-Luxury Motor Vehicle Tax

Abolishment of all the vehicle permits

Introduction of a vehicle import fee to obtain a vehicle

entitlement certificate

UML

SMOT

DIMO

COLO

06

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

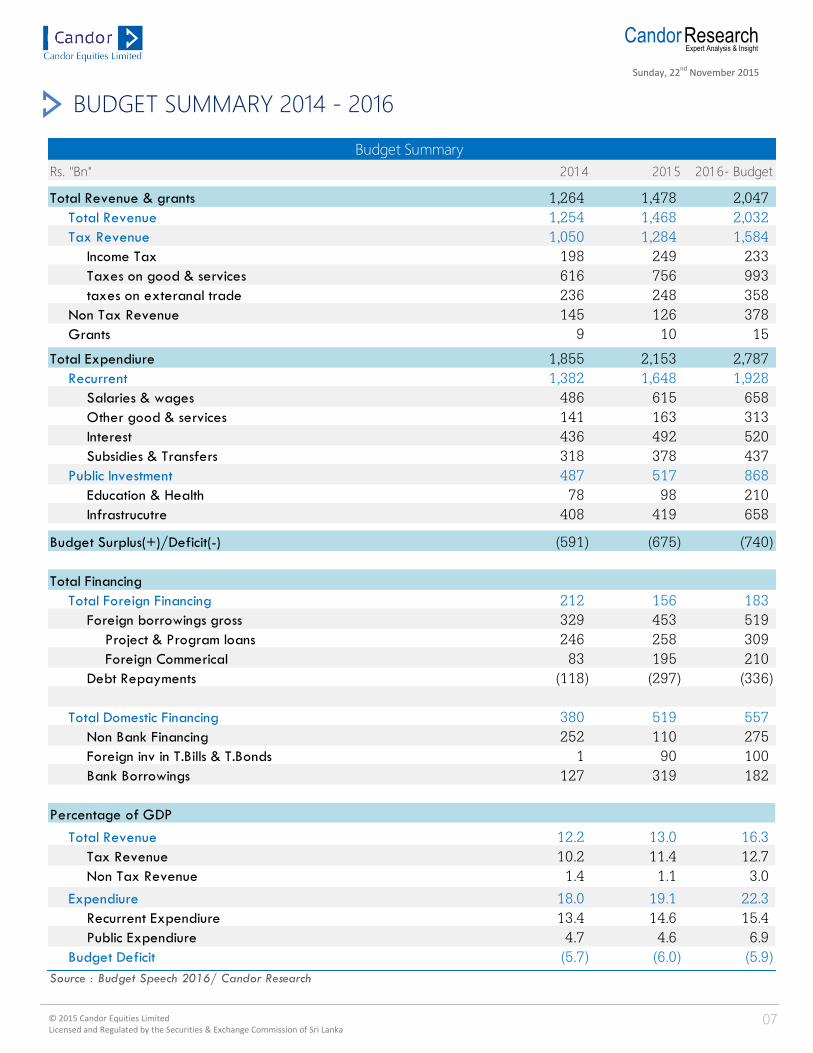

BUDGET SUMMARY 2014 - 2016

Rs. "Bn" 201 4 201 5 201 6- Budget

Total Revenue & grants 1,264 1,478 2,047

Total Revenue 1,254 1,468 2,032

Tax Revenue 1,050 1,284 1,584

Income Tax 198 249 233

Taxes on good & services 616 756 993

taxes on exteranal trade 236 248 358

Non Tax Revenue 145 126 378

Grants 9 10 15

Total Expendiure 1,855 2,153 2,787

Recurrent 1,382 1,648 1,928

Salaries & wages 486 615 658

Other good & services 141 163 313

Interest 436 492 520

Subsidies & Transfers 318 378 437

Public Investment 487 517 868

Education & Health 78 98 210

Infrastrucutre 408 419 658

Budget Surplus(+)/Deficit(-) (591) (675) (740)

Total Financing

Total Foreign Financing 212 156 183

Foreign borrowings gross 329 453 519

Project & Program loans 246 258 309

Foreign Commerical 83 195 210

Debt Repayments (118) (297) (336)

Total Domestic Financing 380 519 557

Non Bank Financing 252 110 275

Foreign inv in T.Bills & T.Bonds 1 90 100

Bank Borrowings 127 319 182

Percentage of GDP

Total Revenue 12.2 13.0 16.3

Tax Revenue 10.2 11.4 12.7

Non Tax Revenue 1.4 1.1 3.0

Expendiure 18.0 19.1 22.3

Recurrent Expendiure 13.4 14.6 15.4

Public Expendiure 4.7 4.6 6.9

Budget Deficit (5.7) (6.0) (5.9)

Source : Budget Speech 2016/ Candor Research

Budget Summary

07

Candor2Research

Expert Analysis & Insight

Tuesday, 5 January 2016

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Capital Markets – Growth stimulus through exciting proposals

The Hon. Minister of Finance emphasized during his budget speech with regard to Capital Markets, that Market

capitalization currently stands at Rs. 2.8 Trillion, and with all the measures proposed it is expected to reach market

capitalization Rs. 5 Trillion. This expectation with regard to the Capital Markets seems attainable through the

following proposed new initiatives and incentives which were outlined during the budget speech;

Demutualization of the Colombo Stock Exchange

The Hon. Finance Minister emphasized to conclude the demutualization process of the CSE during 2016.

This is to ensure greater transparency, better use of technology and to achieve lower trading costs. Further,

demutualization results in more flexible governance structure fostering decisive action in response to

changes in the business environment. Also, it leads to greater investor participation in the

governance of the exchange. Currently, a key issue with regard to the capital markets is the lack of investor

participation especially domestically. Therefore, we believe this milestone will help to overcome this

challenge in the long run.

Proposal to abolish SIA (Securities Investment Account), and to allow the foreign investors to route money

through any bank account existing in the banking system.

Currently foreign investments (including share capital and loans) should be brought into Sri Lanka through

the Securities Investment Account (SIA). It is proposed to allow investors to bring in money to Sri Lanka

through any bank account existing in the formal banking system. This creates more flexibility and space for

FDIs (Foreign Direct Investments) into the Capital markets. Currently, this structure is established within the

Unit Trust Investment space, and along with the complete abolishment of the SIA will open more investment

space into Equity & Debt instruments.

Introduce Real Estate Investment Trusts (REITs)

One of the key bottlenecks to establish REITs within the Sri Lankan Capital markets context was the Stamp

duty on real estate assets. This has been addressed through the exemption of Stamp duty charges on

transfer of real estate assets to a Listed REIT (subject to conditions). This will provide capital to real estate

and infrastructure development and to enable small investors to directly benefit from the growth of the real

estate sector. Furthermore, due to the abolishment of the Land lease tax and ownership restriction for

foreigners, we can expect the demand of local property markets increase gradually. Therefore, this opens

great investment return opportunities through the introduction of REITS within the expected scenario.

Proposal to establish an SME Board

The budget indicated more focus and incentives for the growth and promotion of the SME sector. This has

been also integrated with the Capital markets through the proposal of establishing an SME board in the CSE

BROADER MACRO IMPLICATIONS

08

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

in addition to the current Main & Dirisavi boards. This is facilitated through less stringent compliances for the

SME listing to enable the SME sector to raise capital through the SME board. Further, this will also provide a

comfortable exit strategy for the Venture Capital firms that have invested in SMEs. Further, Venture Capital

funds are given 50% tax off for 5 years for equity investments in the SME sector.

Proposals to encourage and improve Foreign participation in the Capital markets

In addition to the benefits derived from the abolishment of the SIA, the following proposals were also

introduced to encourage foreign investments;

It is proposed to exempt dividend income on investments made by non-citizens or foreign

companies in listed shares through inward remittances. The withholding tax of 10% on dividends will

not apply to such dividend income.

Repeal of the existing Exchange Controls Act and introduce a new Act named ‘Foreign Exchange

Management Act’ will be introduced to facilitate foreign investments. The Inland Revenue Act will

also be amended to accommodate such investments (where necessary) and to exempt income tax

on foreign currency inflows.

Removal of Share transaction levy

Share transaction levy of 0.3% to be removed, which will reduce the overall transaction cost and encourage

more volume in investments in listed securities. Therefore, we believe the standard transaction cost may fall

below 1%.

Tax Concessions on new listings

Local companies listing in the CSE would receive tax concessions for 2 years whilst the concessions would be

extended to 3 years if listed on a foreign Stock Exchange

The minimum amount of dividend to be distributed by quoted companies was increased to 15% of

distributable profits.

Proposals on Debt securities

To facilitate the expansion of the corporate debt securities market, it is proposed to waive the income tax

and withholding tax applicable to those activities into 2016. Further it is also proposed to set up a Bond

Clearing House primarily for transactions in government securities which could then be extended to other

instruments including the corporate debt securities known as debt exchanges. The Bond Clearing house will

be established by the Central Bank. Once the Bond Clearing House is fully operationalized, it is proposed to

be governed by an independent Board of Directors.

Proposal to establish a Commodities exchange

Finance Minister proposed to establish a Commodity exchange to accommodate & facilitate the exchange of

commodities which are a significant part of our export economy (tea, rubber, coconut). This can be

considered as an effective Market development considering the expected prospects from other initiatives

proposed within Capital market context in order to boost overall market participation in the long run.

09

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Investment promotions – Strong Emphasis coupled with integrated strategies

The key entities of Board of Investment (BOI), Export Development Board (EDB) and the Sri Lanka Tourism

Development Authority (SLTDA) will be restructured. These entities begin key institutions in the investment

promotions aspect will have an impact in the attraction of investments, exports and the tourism industry.

The government has identified thrust areas which have the potential for investments over USD 2 billion in the

areas of manufacturing, energy, agriculture, technology, etc.

In the pursuit of the above investment attractions and other investments specific proposals include;

Removal of taxes on leased land to foreigners and the removal of restrictions on ownership on identified

investments imposed through the Land (Restrictions on Alienation) Act. These will provide stimulus to the

attraction of foreign investments particularly to investors seeking to invest in real estate assets.

Introduction of an investor friendly Foreign Exchange Management Bill (FEMB). The exchange rate being a

key consideration in the attraction of FDI’s, this will be a notable incentive to the attraction of foreign

investments.

The proposal to remove taxes on dividends from investments (applicable on inward remittances) in listed

companies made by non-citizens and foreign companies will further entice foreign investments into the

country.

The Agency for Development is expected to ensure that application for foreign investment is completed

within the period of 50 days will contribute positively to the ease of doing business.

Investment promotion in lagging areas through tax concessions of 50% for a period of five years (for a

company providing 500 employment opportunities) and up to 8 years (for a company providing 800

employment opportunities) where the minimum investment is over USD 10 million will also be an

encouraging tool for investments.

Profits, from expansion and modernization by investing in machineries based on job creation will also receive

a half tax rate for 3 year. This too will be an encouraging factor for companies looking to expand its

business.

The review and revision of the Underperforming Enterprises and Underutilized Assets Act No 43 of 2011

would also augur positively for the investor confidence.

The extension of tax incentives to mixed development projects under the Strategic Development Project Act

will also contribute to business confidence. The proposed new investment act can also be expected to

complement the business confidence.

10

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Promoting Exports – Long road ahead, yet satisfying

Strengthening the commercial sections of Sri Lankan diplomatic missions abroad to play an essential role

in export promotions will enable a more effective and an efficient process of identifying and responding

to export market requirements within the country’s capabilities.

The formation of a high level body which possesses the ability to make policy decisions and clear

bottlenecks will contribute positively to ensuring the successful implementation and monitoring of the

export strategy of the country. This would pave the way for an effective mechanism to take remedial

action in the event of any deviation or other external dynamics. The high level body will be empowered

by the establishment of the Export Development Council of Ministers (EDCM) chaired by his Excellency

the President and the Honorable Prime Minister and other relevant ministers, the initiative will

complement the achievement of targets.

The proposed establishment of the Export Import Bank (EXIM bank) will facilitate the initiatives to identify

the new opportunities. Coupled with smooth policy making and addressing bottlenecks in the export

process will allow for a more efficient function.

Management of Export Processing Zones (EPZ’s), existing and proposed to be vested with the private

sector management companies with skills. The necessities to attract and retain investments in the zones

will be addressed by these initiatives.

The proposed expansion of support of the Sri Lanka Export Credit Insurance Corporation (SLECIC) to

exporters will also enable exporters to access new markets.

Other incentives under export promotions include incentives for spice and other industries such as the

export cess on pepper, clove and nutmeg to be removed, unutilized government land to be utilized to

grow spices such as cinnamon, pepper, cardamom, etc.

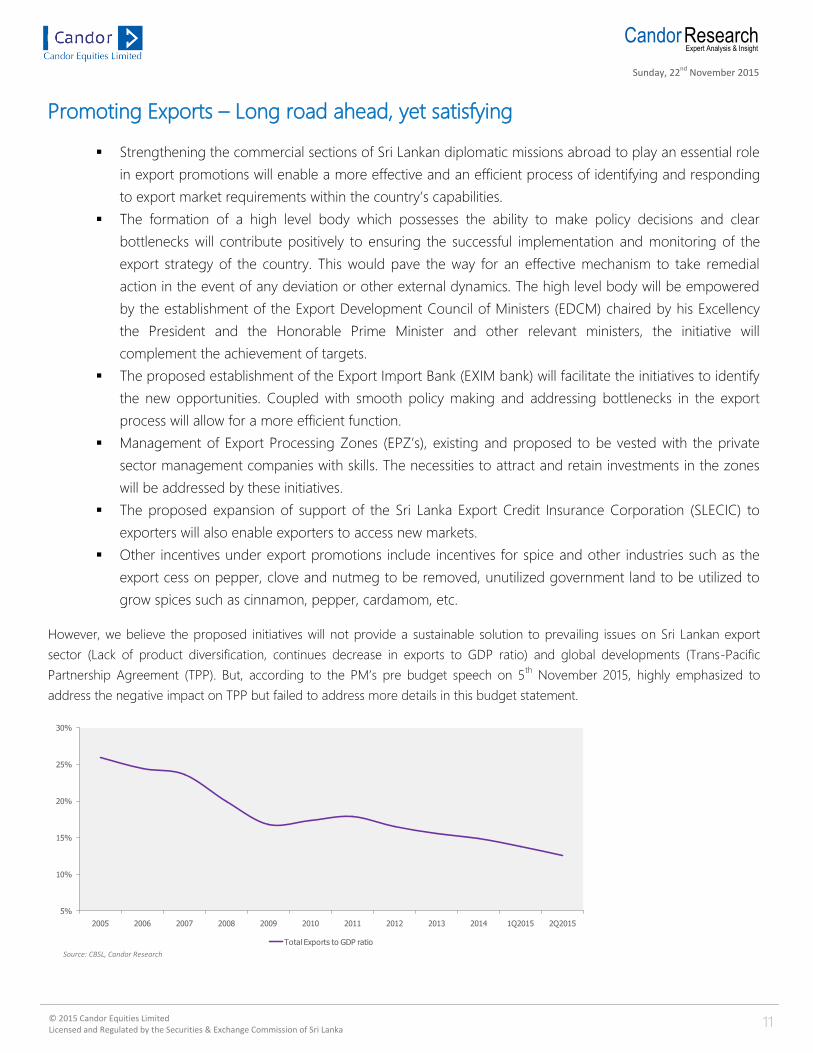

However, we believe the proposed initiatives will not provide a sustainable solution to prevailing issues on Sri Lankan export

sector (Lack of product diversification, continues decrease in exports to GDP ratio) and global developments (Trans-Pacific

Partnership Agreement (TPP). But, according to the PM’s pre budget speech on 5th November 2015, highly emphasized to

address the negative impact on TPP but failed to address more details in this budget statement.

5%

10%

15%

20%

25%

30%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q2015 2Q2015

Total Exports to GDP ratio

Source: CBSL, Candor Research

11

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Import Substitution – A balanced approach

With the policy makers striving to address the broader macro challengers, is looking to address the import

substitution challenge. This has been a challenge due to Sri Lanka being a net importer with total value of imports

standing at USD 19.42bn (including oil imports) in contrast to the USD 11.13bn exports for year 2014. The policy

makers however in the Budget 2016 has liberalized the Lubricant and bitumen market and the removal of tiles,

sanitary ware and steel from the BOI negative list and downward revision of duties will encourage more imports.

Further, reducing import duties electronics, branded garments and foot ware. Sri Lanka has a high propensity to

import which is further evident with the 44% increase in consumer goods post interim budget for the first half of

2015 to USD 2.3Bn. The policy makers have introduced controlled prices for 13 essential food items, however

increasing the PAL to 7.5% and NBT to 4% will still pose a significant cost increase to importers. Therefore there will

be some deterrent to import. However in hindsight it seems a more import friendly policies through the budget

2016, but with increase in fees indirect taxes will increase the revenue to government coffers.

The effectiveness of the government’s revenue generating proposals

The government strategy in tax revenue has seen a change, the revenue from fees and charges have been increased

with the policy makers targeting LKR 75Bn through such schemes. Further Ports and Airports Development Levy

(PAL) is expected to bring in LKR 30Bn and the increase in NBT a further LKR 90Bn. There for it is evident that

indirect taxes and fees are mobilized to bring in the extra revenue required. This is amides the direct corporate taxes

been revised with a standard rate of 15% on most entities and a higher rate of 30% to industries such as banking

and financial services, liquor, tobacco, trading and betting & gaming. The annual PAYE tax threshold is increased to

LKR 2.4Mn from LKR 750,000 p.a, and above the limit is to be charged at a 15% flat rate. This will result in disposable

incomes increasing specially amongst the middle income category, which is the largest consumer market. This

encourages the population to spend and government revenue will be through the indirect taxes where the extra

income through tax savings will be absorbed through encouraging consumption. This is progressive as it will not

hamper the current consumption momentum.

Policies are groomed to absorb anticipated global shocks

Recently we have witnessed a continuous foreign outflow from the government security market amidst the

expectation of US interest rate hike. On YTD basis massive LKR 153.8Bn worth of foreign investments existed from

the government security market whilst creating an immense pressure on the local currency. Thus, we believe the

favorable initiatives on foreign direct investment and foreign investments (share capital) are required in order to

endure against the prevailing global market developments (Fed rate hike, Euro zone recovery etc.). Because, due to

the recoveries in advanced economies it is possible to see foreign investments to such economies from emerging

markets considering their robust risk ratings. Furthermore, we believe the proposal to abolish the exchange control

act will be a move to liberalize the Sri Lankan capital account. But, the GOSL should establish a comprehensive

mechanism for this; otherwise Sri Lanka would be a destination to launder money. Hence, a clear methodology is

12

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

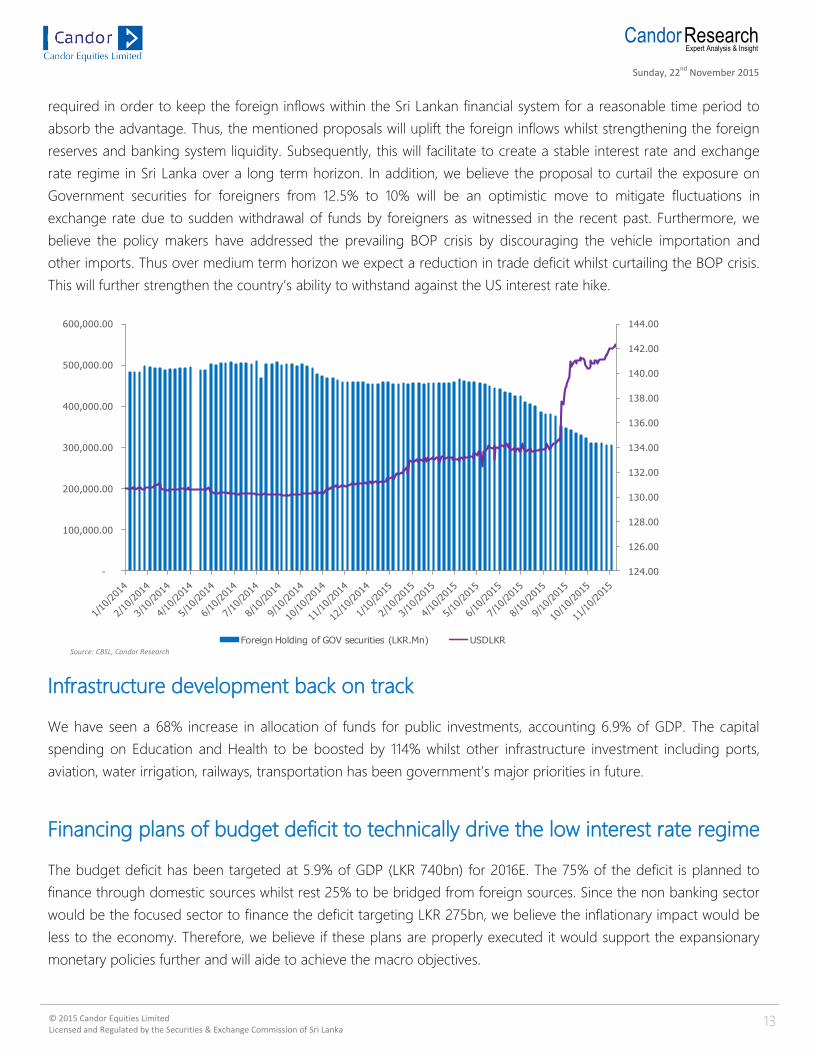

required in order to keep the foreign inflows within the Sri Lankan financial system for a reasonable time period to

absorb the advantage. Thus, the mentioned proposals will uplift the foreign inflows whilst strengthening the foreign

reserves and banking system liquidity. Subsequently, this will facilitate to create a stable interest rate and exchange

rate regime in Sri Lanka over a long term horizon. In addition, we believe the proposal to curtail the exposure on

Government securities for foreigners from 12.5% to 10% will be an optimistic move to mitigate fluctuations in

exchange rate due to sudden withdrawal of funds by foreigners as witnessed in the recent past. Furthermore, we

believe the policy makers have addressed the prevailing BOP crisis by discouraging the vehicle importation and

other imports. Thus over medium term horizon we expect a reduction in trade deficit whilst curtailing the BOP crisis.

This will further strengthen the country’s ability to withstand against the US interest rate hike.

Infrastructure development back on track

We have seen a 68% increase in allocation of funds for public investments, accounting 6.9% of GDP. The capital

spending on Education and Health to be boosted by 114% whilst other infrastructure investment including ports,

aviation, water irrigation, railways, transportation has been government’s major priorities in future.

Financing plans of budget deficit to technically drive the low interest rate regime

The budget deficit has been targeted at 5.9% of GDP (LKR 740bn) for 2016E. The 75% of the deficit is planned to

finance through domestic sources whilst rest 25% to be bridged from foreign sources. Since the non banking sector

would be the focused sector to finance the deficit targeting LKR 275bn, we believe the inflationary impact would be

less to the economy. Therefore, we believe if these plans are properly executed it would support the expansionary

monetary policies further and will aide to achieve the macro objectives.

124.00

126.00

128.00

130.00

132.00

134.00

136.00

138.00

140.00

142.00

144.00

-

100,000.00

200,000.00

300,000.00

400,000.00

500,000.00

600,000.00

Foreign Holding of GOV securities (LKR.Mn) USDLKRSource: CBSL, Candor Research

13

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Disposable Income & increasing indirect tax burden

While personal income remaining unchanged, the government has taken initiatives to introduce personal tax

concessions to improve the overall disposable income amidst the growing indirect tax burden. The following

proposals were identified with regard to this commentary;

Profits and income accruing to any individual in excess of LKR 2.4 Mn per annum, is to be taxed at a flat rate

of 15%.This applies to employees under the PAYE scheme and self employed persons. At present whose

annual income is over Rs. 750,000 is liable for PAYE.

The prevailing withholding tax rate of 2.5% on interest income accruing to an individual will be removed and

such income will be considered as part of the taxable income of an individual.

Interest income accruing to senior citizens will continue to be exempt from tax. At present the 15% interest

rate offered to senior citizens is limited to Rs. 1 Million and only to citizens above 60 years. This benefit is to

be expanded to citizens above 55 years of age and the 15% interest rate to be applicable on deposits up to

Rs. 1.5 Million.

Further, the removal of stamp duty on credit cards for local purchases can also be considered as a positive

impact on the overall disposable incomes. Presently stamp duty is levied at 1.5% for local purchases using a

credit card.

14

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Apparel

The manufacturing sector will benefit from the exclusions of the higher tax rate of 30% for the sector. As

such the sector will be liable to pay income taxes at the lower rate of 15%. Textured Jersey Lanka PLC

and Hayleys Fabric PLC will benefit from the lower rates.

The proposed apparel mall will also be beneficial to the apparel sector as the government, having

recognized the competence of the sector players in branding, where the manufacturers and potential

buyers are intermediated for increased business possibility.

Construction

Tax exemptions on construction companies revenue from overseas markets to be entirely exempt from

taxes will encourage companies with the competence, expertise, experience and relationships to venture

into foreign markets. Access Engineering PLC who has had numerous foreign investments will be able to

bear fruit from this proposal.

The removal of the Construction Industry Guarantee Fund Levy to be beneficial for small and medium

scale contractors will create a more level playing field and a healthy level of competition.

The introduction of a Payment Guarantee Security Act will bode well for the sector players to manage

cash flows.

Import cost on machinery for purifying sea sand in the deep sea to be considered as a double deduction

for tax purposes.

Duties to be revised downward on steel, tiles and sanitary ware to address short supply and high prices

of building materials. The property development sector will particularly see a positive impact from this

proposal. Overseas Realty (Ceylon) PLC, MTD Walkers and Access Engineering PLC (recent venture into

property development) will see a positive influence.

Expansion of road networks (expressways, marine drive, bridge construction, etc.) will benefit the

construction sector. Access Engineering and MTD Walkers would be among the listed entities to be vying

for these opportunities.

The proposal to further allocate LKR 1 billion (in addition to the currently allocated LKR 2 billion) for

irrigation and water resource management will provide opportunity for Access Engineering PLC.

The Governments proposals to develop housing will benefit MTD Walkers PLC.

Any foreign contractor entering into Sri Lanka to undertake construction work should enter into joint

venture agreement with local contractors.

BUSINESS IMPACT

15

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Telecommunications

Increase in the International Telecommunications Operator Levy. Proposal to increase the levy from USD

9 cents to USD 12 cents and 6 cents be credited to the consolidated fund (compared to the previous 3

cents).

The exemptions on the Import or supply of telecom equipment or machinery, high-tech equipment

including copper cables for telecom industry will be removed.

The Removal of exemptions of Nation Building Tax on Telecommunication services will adversely affect

the margins of the Telecommunication sector companies.

Environmental fee of LKR 50,000 to be charged per tower.

The above mentioned proposals will have a direct impact on the Telecom counters of Dialog Axiata PLC

and Sri Lanka Telecom PLC.

Retail and FMCG

VAT charge for wholesale and retail trade to be removed.

The removal of the present duty of 1.5% on local usage of credit cards will be removed. This will be

beneficial for consumers thus allowing for spending capacity. All retail and FMCG counters can be

expected to benefit.

The proposal to revise taxes on garments, shoes, electronic and electrical items and other

accessories will bode positively for the retail and FMCG counters.

Reduction in the prices of essentials will also have a positive sentiment to the consumers and offer

benefits to the retail and FMCG counters.

The increase in the threshold of the PAYE tax will also allow for increased disposable income thus

allowing a positive impetus to the retail and FMCG sectors.

Hemas Holdings PLC, Cargills Ceylon PLC, Ceylon Cold Stores PLC, Lion Breweries Ceylon PLC,

Distilleries Company of Ceylon PLC and Ceylon Tobacco Company PLC are among the counters

which can be expected to benefit.

Leisure industry

The tourist industry remains a growth industry and continues to have the focus of the policy makers. In line with the

policy makers growth policies to the industry the existing 1% Tourism development levy has been removed. Further,

recognizing the major potential for MICE policies were brought forward to establish a MICE triangle (BMICH, Nelum

Pokuna Theater and New Town Hall) that will better cater to this growing segment. The MICE is a growing global

market the government therefore to further push this segment has proposed Public Private Partnership to construct

a exhibition center near the parliament. Further keeping to the tourism development drive the policy makers have

introduced provisions of tax reductions for setting up theme parks. Further, concessions were granted for setting up

businesses for training in hospitality management for youth. This is to encourage the industry to train and educate

due to the expected lack of available skilled labor for the industry. The entire tourism industry stands to gain

16

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

provided the policies gain momentum. With the targeting of high end tourism import duty was removed from

caravan carriages, speed boats, mini cruise boats, yachts and surfing equipments.

Petroleum, Power & Energy sector

The government has provided legal backing to strengthen the Public Utilities Commission of Sri Lanka (PUCSL) to

include Ceylon Petroleum Corporation (CPC) and National Water Supply and Drainage Board (NWSDB) to enable

and formulate a more cost effective and transparent pricing mechanism. This could be the early steps in building the

much needed legal and operational fame work for the much anticipated formula pricing for energy related products.

This will be a positive move for LIOC.

The policymakers to further reduce the burden of the people have reduced LKR 150.00 per 12.5Kg cylinder of LPG.

This will reduce the retail price of a 12.5Kg LPG cylinder to LKR 1,396.00. This will directly impact Laugfs Gas PLC

(LGL.N) margins, however this will be managed due to the low LPG prices prevailing in the global market and

improving LPG consumption levels in the island due to penetration levels increasing and disposable incomes rising.

The liberalization of the Vehicle Emission Testing (VET) certificate issuance will break the duopoly of the industry

currently secured by Clean Co Lanka Limited and Laugfs Eco Sri. Laugfs Gas PLC (LGL.N) will be affected through this

due to new players entering the market which will dilute the company market share due to the risk of new players

entering the market.

Liquor and Cigarette industry

With the introduction of the new two tear tax base, corporate tax will reduce the from 40% to 30% for, Distilleries

Company of Sri Lanka PLC (DIST.N), Lion Brewery Ceylon PLC (LION.N), Ceylon Beverage Holdings PLC (BREW.N)

and Ceylon Tobacco Company PLC (CTC.N). However, annual manufacturing license fee for a distillery are to be

increased to LKR 150Mn instead of a per bottle license fee. The excise Duty of Rs.250 million per month from liquor

manufacturers who are having distilleries and Rs.50 million per month from persons engaged only in liquor

manufacturing based on the minimum quantity of liquor required to be manufactured. The liquor industry is

burdened with fees and taxes in spite of the reduction in corporate taxes. However with the eradication of the illicit

market coupled with inelastic demand for the product will naturalize this effect in the long run.

Motor vehicle Industry

The major impact to the industry will be the abolition of vehicle permits granted under every different scheme. This

was a significant market for all motor sector companies, who will see a universal negative effect forming due to this.

Introducing Unit Rate of Excise Duty for Motor Cars based on size measured in cubic centimeters. Further,

introduction of a vehicle import fee to obtain a Vehicle Entitlement Certificate for each vehicle. Within this segment

too the policy maker strategy has been to include fee base revenue collection. However the increase in NBT and PAL

will too have a significant impact on the cost of import of motor vehicles over all. Therefore the overall motor sector

will be negatively affected with expected number of units sold reducing.

17

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

Banking Sector

Colombo international financial center

The government has proposed to establish a Colombo international financial center, a specific zone that will be built

in line with the Dubai International Financial Centre in order to cater the growing local and SAARC region

opportunities. We believe the abolishment of Exchange control act coupled with FDI favorable polices will be

positively impacted on the proposed financial center. However, establishment of separate legislative system and

regulatory authority in lines with the Dubai International Financial Centre will have practical challenges in

implementing the said proposal.

Initiatives to uplift the banking penetration in Sri Lanka

In order to improve the banking penetration, the government has proposed for all banks to expand the branch

network by 15% by opening branches in lagging areas. But, this would have a negative impact on large players such

as COMB (239 Branches), HNB (249 Branches) and SAMP (220 Branches) which have already expanded to the

lagging areas while maintaining a high side cost to income ratio. However, the emerging players including NDB,

NTB, UBC etc will not have a significant impact from the proposed initiative as they are constantly focusing on

branch expansions. In addition, the proposal to open bank accounts for employees would positively impact on the

banking sector, as banks are aggressively focused on the salaries accounts due to the healthy credit quality.

Furthermore, the initiative to abolish the 2.5% withholding tax on deposits will improve the banking sector deposits

base.

Strengthen the financial discipline in Sri Lanka

In order to strengthen the financial discipline in Sri Lanka the government has proposed charges on cash

withdrawals and expands the Credit Information Bureau (CRIB). We believe the charges on cash withdrawals will

have an immediate negative impact on the banking sector. But, over long term horizon a shift towards electronic

cash transportation will limit the negative impact. In addition, this will provide a positive impetus on the banking

sector fee based income as well.

Dubai International Financial Centre (DIFC) - Key Features

Legislative system consistent with English Common law

The Dubai Financial Services Authority (DFSA), which grants licenses and regulates the activities of all banking

and financial institutions in DIFC

The DIFC Courts is the entity responsible for the independent administration and enforcement of justice in

DIFC

100% foreign ownership

Zero percent tax rate on income and profits (guaranteed for a period of 50 years)

No exchange controls (free capital convertibility)

An independent common law judicial system

18

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

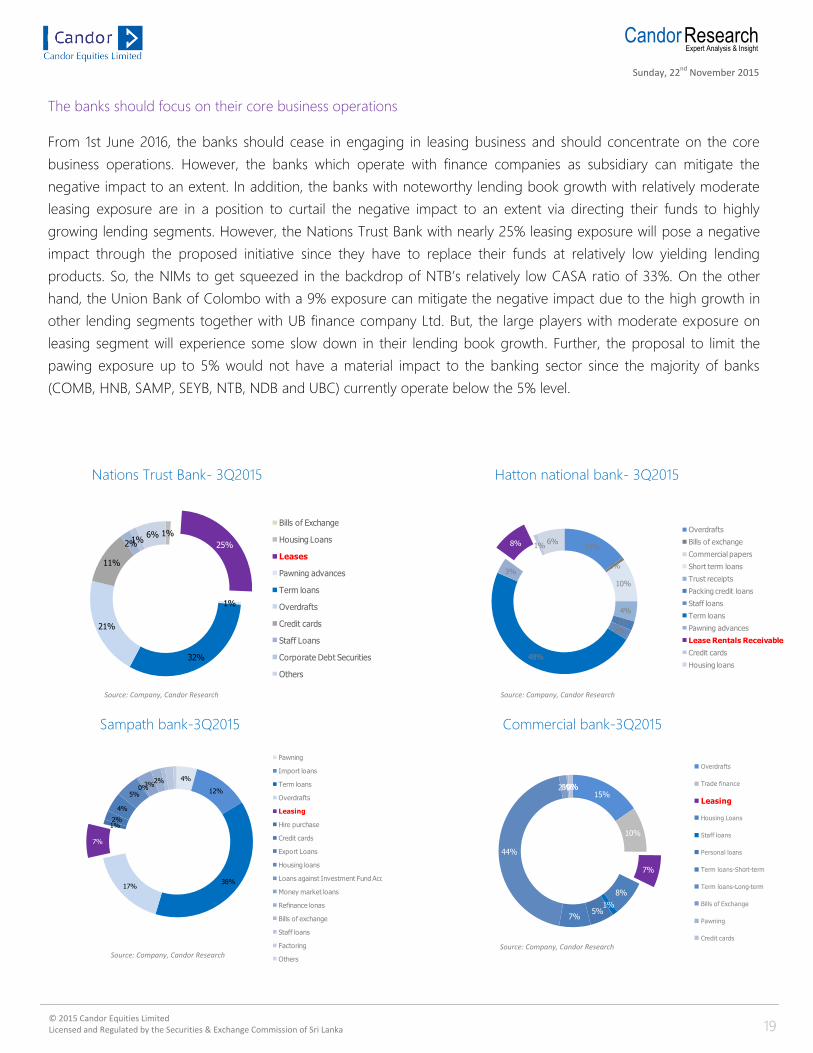

The banks should focus on their core business operations

From 1st June 2016, the banks should cease in engaging in leasing business and should concentrate on the core

business operations. However, the banks which operate with finance companies as subsidiary can mitigate the

negative impact to an extent. In addition, the banks with noteworthy lending book growth with relatively moderate

leasing exposure are in a position to curtail the negative impact to an extent via directing their funds to highly

growing lending segments. However, the Nations Trust Bank with nearly 25% leasing exposure will pose a negative

impact through the proposed initiative since they have to replace their funds at relatively low yielding lending

products. So, the NIMs to get squeezed in the backdrop of NTB’s relatively low CASA ratio of 33%. On the other

hand, the Union Bank of Colombo with a 9% exposure can mitigate the negative impact due to the high growth in

other lending segments together with UB finance company Ltd. But, the large players with moderate exposure on

leasing segment will experience some slow down in their lending book growth. Further, the proposal to limit the

pawing exposure up to 5% would not have a material impact to the banking sector since the majority of banks

(COMB, HNB, SAMP, SEYB, NTB, NDB and UBC) currently operate below the 5% level.

Nations Trust Bank- 3Q2015 Hatton national bank- 3Q2015

Sampath bank-3Q2015 Commercial bank-3Q2015

1%

25%

1%

32%

21%

11%

2%1%6%

Bills of Exchange

Housing Loans

Leases

Pawning advances

Term loans

Overdrafts

Credit cards

Staff Loans

Corporate Debt Securities

Others

15%

1%

10%

4%

2%2%

48%

3%

8% 1%6%

Overdrafts

Bills of exchange

Commercial papers

Short term loans

Trust receipts

Packing credit loans

Staff loans

Term loans

Pawning advances

Lease Rentals Receivable

Credit cards

Housing loans

4%

12%

38%17%

7%

1%2%

4%

5%0%3%

2%

Pawning

Import loans

Term loans

Overdrafts

Leasing

Hire purchase

Credit cards

Export Loans

Housing loans

Loans against Investment Fund Account

Money market loans

Refinance lonas

Bills of exchange

Staff loans

Factoring

Others

15%

10%

7%

8%

1%5%

7%

44%

2%0%0%0%

Overdrafts

Trade finance

Leasing

Housing Loans

Staff loans

Personal loans

Term loans-Short-term

Term loans-Long-term

Bills of Exchange

Pawning

Credit cards

Source: Company, Candor Research

Source: Company, Candor Research

Source: Company, Candor Research

Source: Company, Candor Research

19

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

NDB Bank-3Q2015 Seylan Bank-3Q2015

Union bank of Colombo-3Q2015

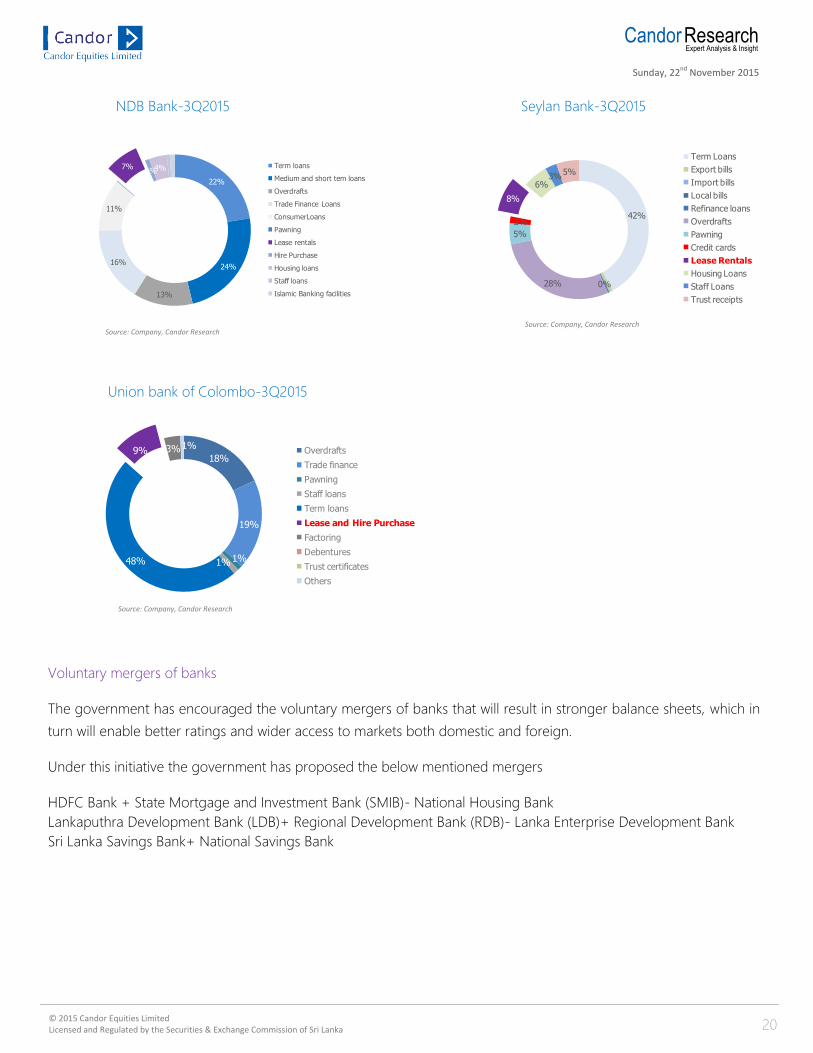

Voluntary mergers of banks

The government has encouraged the voluntary mergers of banks that will result in stronger balance sheets, which in

turn will enable better ratings and wider access to markets both domestic and foreign.

Under this initiative the government has proposed the below mentioned mergers

HDFC Bank + State Mortgage and Investment Bank (SMIB)- National Housing Bank

Lankaputhra Development Bank (LDB)+ Regional Development Bank (RDB)- Lanka Enterprise Development Bank

Sri Lanka Savings Bank+ National Savings Bank

22%

24%

13%

16%

11%

7%1%4% Term loans

Medium and short tem loans

Overdrafts

Trade Finance Loans

ConsumerLoans

Pawning

Lease rentals

Hire Purchase

Housing loans

Staff loans

Islamic Banking facilities

42%

0%28%

5%

2%

8%

6%3%

5%

Term Loans

Export bills

Import bills

Local bills

Refinance loans

Overdrafts

Pawning

Credit cards

Lease Rentals

Housing Loans

Staff Loans

Trust receipts

18%

19%

1%1%48%

9% 3%1%Overdrafts

Trade finance

Pawning

Staff loans

Term loans

Lease and Hire Purchase

Factoring

Debentures

Trust certificates

Others

Source: Company, Candor Research Source: Company, Candor Research

Source: Company, Candor Research

20

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

The proposed initiatives to abolish the 2.5% withholding tax on deposits, removing stamp duty on credit cards and

expand the salaries accounts will be positively affected on the Sri Lankan Banking Sector. But, the cease in engaging

in leasing business will slow down the banking sector lending growth whilst curtailing the NIMs. Further a 2%

increase in the corporate tax rate to 30% and NBT to 4% would be negatively impacted all players in the industry.

Notably, we presume a substantial increase in the leasing segment during 1H2015 owing to improved vehicle

importation and lack of lending avenues for banks amidst slow down in the construction sector. Thus, due to the

proposed impetus on construction sector we expect a resilient lending book growth from the banking sector over

long term horizon. In addition, the proposed investment promotions and foreign currency inflows will facilitate a

stable interest rate and exchange rate regime in Sri Lanka too. Thus, the downside risk of the banking sector

profitability over long term horizon is highly remote.

Plantation sector

The government has proposed following initiatives on plantation sector

Liberalize the tea imports to the country to encouraging value addition through blending.

A two year tax exemption period will be granted for companies engaged in tea and rubber plantation.

We presume that the liberalization of the tea imports will encourage value additions; therefore this will aid to

improve the tea exports whilst expanding to new markets. Thus, this would have a positive impact for the tea

exporting counters. On the other hand, we do not see a clear direction to address the prevailing issues (Low Rubber

prices) in the rubber sector. However, a two year tax exemption will be positively affected to the cash flows of the

plantation (tea &rubber) companies. Thus, the downside risk of the dividend distribution of the plantation sector

companies is relatively low.

Import Driven companies

The policy makers proposed to increase the PAL to 7.5% and NBT to 4% while resulting a significant cost increase to

importers, curtailing their profitability. Hence, this could negatively impact on import driven companies such as LLUB,

LIOC etc. However, the magnitude of the impact depends on the nature of price elasticity of demand for the

product. On a broader view, this could create a cost push inflation in Sri Lanka over long term horizon.

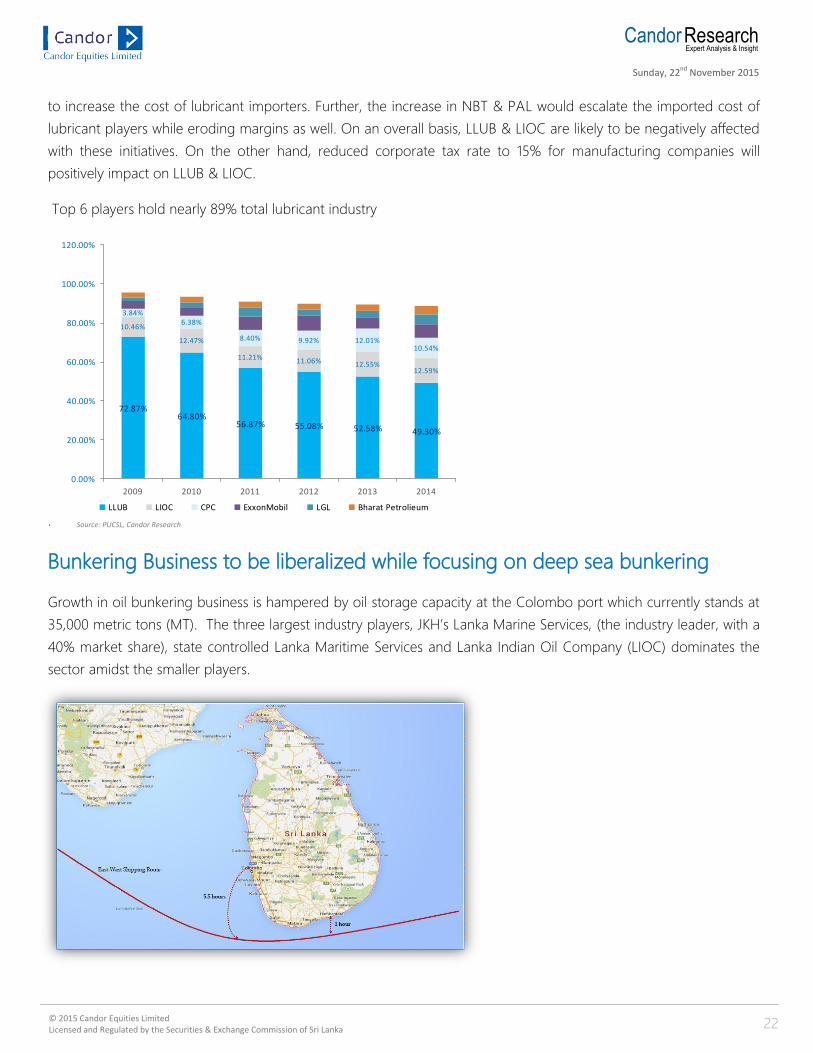

Local Lubricant Manufacturers to face stiff competition from importers

Local lubricant industry currently consists of 13 players including 2 local blenders, Chevron Lubricant Lanka PLC

(LLUB) & Lanka IOC (LIOC). Given the decision of liberalization of lubricant market will lead the lubricant market’s

competition to be more stringent. Further, the removing the lubricant from BOI negative list will prompt the import

duty to be removed and hence the local blenders may lose the advantage of 13% tariff advantage over importers.

Therefore, importers may have a competitive edge over local blenders causing more challenges for local blender’s

market share. Further, the present exemption of NBT on lubricant has also been abolished and therefore, this is likely

21

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

to increase the cost of lubricant importers. Further, the increase in NBT & PAL would escalate the imported cost of

lubricant players while eroding margins as well. On an overall basis, LLUB & LIOC are likely to be negatively affected

with these initiatives. On the other hand, reduced corporate tax rate to 15% for manufacturing companies will

positively impact on LLUB & LIOC.

Top 6 players hold nearly 89% total lubricant industry

.

Bunkering Business to be liberalized while focusing on deep sea bunkering

Growth in oil bunkering business is hampered by oil storage capacity at the Colombo port which currently stands at

35,000 metric tons (MT). The three largest industry players, JKH’s Lanka Marine Services, (the industry leader, with a

40% market share), state controlled Lanka Maritime Services and Lanka Indian Oil Company (LIOC) dominates the

sector amidst the smaller players.

72.87%64.80%

56.87% 55.08% 52.58% 49.30%

10.46%

12.47%

11.21% 11.06% 12.55%12.59%

3.84%6.38%

8.40% 9.92% 12.01%10.54%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

2009 2010 2011 2012 2013 2014

LLUB LIOC CPC ExxonMobil LGL Bharat Petrolieum

Source: PUCSL, Candor Research

22

Sunday, 22nd

November 2015

Candor2Research

Expert Analysis & Insight

© 2015 Candor Equities Limited Licensed and Regulated by the Securities & Exchange Commission of Sri Lanka

The proposed deep sea bunkering is planned to be operated in Hambantota port where 35,000 ships passes

through this channel annually. Hence, this will provide greater opportunity to Sri Lanka to compete with other ports

within a radius of few hours. Therefore, the government plans to issue licenses for the private sector through a

competitive bidding process. We believe JKH & LIOC will also seek to secure a license given the threat to their

existing bunkering operations at Colombo port due to the proposed deep sea bunkering operations. Currently,

bunkering business is the biggest revenue generator to the JKH transportation sector revenue which in turn

contributes nearly 19% to the total group revenue. Therefore, we believe JKH would pose a negative impact from

liberalizing the bunkering business (Which will attract more private players into the industry). Further, the degree of

impact could be neutralized based on the JKH’s ability to secure a license through the competitive bidding process.

The similar impact could be expected with LIOC as it is currently engaging in oil bunkering at the Colombo port.

Finance Companies given the right scope

Since Commercial Banks are restricted on providing leasing, finance companies are going to have a positive impact

since credit worthy leasing clients will also look at large scale finance companies such as Peoples Leasing, Central

Finance, LB Finance etc for their leasing facilities. Hence, the top tier finance companies may improve their asset

quality going forward. Given the possible dull sentiment in vehicle market due to increased fee structures in vehicle

registration we believe the leasing market would not be exciting going forward causing challenges to the Finance

Companies. Further, the corporate tax rate adjusted upwards from 28% to 30% will pose an additional tax burden.

Moreover, through creating a Financial Institution Restructuring Agency (FIRA), the Central Bank of Sri Lanka will give

a 100 percent guarantee on all deposits of all the registered finance companies by end January 2016. This may lead

the finance companies to mobilize more deposits at low costs which will positively impact on their net interest

margins. Therefore, we believe the large scale finance companies including PLC, CFIN, LFIN may have a positive

impact on these proposals.

Additionally, the current senior citizen interest rate scheme to be further continued by giving current 15% interest

rate for deposits up to LKR 1.5mn.(previously stand at LKR 1mn) through finance companies. This may lead to

increase the deposit base of finance companies whilst government will ensure an interest subsidy of 1.5%. However,

this will prompt the NIMs to be squeezed given the possible dull outlook in-terms of leasing industry. On the other

hand, possible prospects in SME sector may drive the lending book growth for Finance Companies going forward.

But, the stiff competition from Commercial Banks may partly hinder the prospects.

Further, we believe this will be an indirect move to induce commercial banks to acquire finance companies.

Local tile manufactures to face new challenges

Royal Cremic Lanka PLC (RCL) is currently enjoying the monopoly in local tile manufacturing industry through Lanka

Ceramics (CERA), Lanka Floortiles(TILE), and Lanka Walltiles(LWL). With downward revision of import duties via

removing tiles from BOI negative list, gives importers a better competitive edge over RCL. Therefore, this may

negatively impact RCL and its subsidiary tile manufactures.

23

Candor Research

Expert Analysis & Insight

Contact Us

Disclaimer

The report has been prepared by Candor Equities limited (CEL). The information and opinions contained herein are based upon information obtained from sources

believed to be reliable and made in good faith. Such information has not been independently verified and no guarantee, representation or warranty, express or

implied is made as to their accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for

information purposes only, and the description of any company or their securities mentioned herein is not intended to be complete and this document is not, and

should not be construed as, an offer, or solicitation of an offer, to buy or sell any securities or other financial instruments.

Sales

Mohammed Riyas Director Sales +94 11 2359102 /+94 777325270 [email protected]

Chaminda Mahanama Assistant Vice President – Equities +94 11 2359113 /+94 777556582 [email protected]

Auburn Senn Assistant Vice President - Equities +94 11 2359117 /+94 714943304 [email protected]

Buddhike Payoe Senior Manager- Equities + 94 11 2359116 /+94712737956 [email protected]

Damayanthi Madawalage Assistant Manager – Equities +94 11 2359114 /+94 777781001 [email protected]

Dilanjan Perera Assistant Manager – Equities +94 11 2359108 /+94 772544444 [email protected]

Bishen Mendez Senior Investment Advisor +94 11 2359121 /+94 779368660 [email protected] Vishvajith Nayakarathne Investment Advisor +94 11 2359112 /+94 772331355 [email protected]

Swanthri Ekanayake Executive - Business Development +94 11 2359122 /+94 770071304 [email protected]

International Desk

Indula Wickramasinghe Executive- Business Development +94 11 2359115 /+94 771503808 [email protected]

Research

Pasindu Perera Head of Research +94 112359137 / +94712452413 [email protected]

Usama Jiffry Assistant Manager –Research +94 112359135 /+94 777245605 [email protected]

Shadhir Jannath Assistant Manager – Technical Analysis +94 112359162 / +94777073411 [email protected]

Ranuka De Silva Assistant Manager – Research +94 112359134 / +94777726852 [email protected]

Dushan Virantha Research Analyst +94 112359138 /+94 776449410 [email protected]