Embed Size (px)

Citation preview

World One Powerful Presentation Template

Allan Fogwill, CEO

Canadian Energy Research Institute June 2018

CANADIAN OIL SANDS AND CONVENTIONAL OIL AND GAS

PRODUCTION FORECAST, SUPPLY COSTS AND

EMISSIONS

Relevant • Independent • Objective www.ceri.ca

Canadian Energy Research Institute

Overview

Founded in 1975, the Canadian Energy Research Institute (CERI) is an independent,

registered charitable organization specializing in the analysis of energy economics and

related environmental policy issues in the energy production, transportation, and

consumption sectors.

Our mission is to provide relevant, independent, and objective economic research of

energy and environmental issues to benefit business, government, academia and the

public.

CERI publications include:

•Market specific studies

•Geopolitical analyses

•Commodity reports (crude oil, electricity and natural gas)

In addition, CERI hosts an annual Petrochemical Conference.

Canadian Energy Research Institute CERI receives financial support from its core funders which include

Natural Resources Canada, AB Energy and the Canadian Association

of Petroleum Producers.

In addition, the institute benefits from funds provided by donors which

include:

• AB’s Industrial Heartland

• Chemistry Industry Association of Canada

• Government of SK

• Ivey Foundation

• University of Calgary

• Canadian Energy Pipeline Association

CERI also receives in-kind support from the following contributors:

• AB Energy Regulator

• Lithuanian Energy Institute

• Deloitte Canada Ltd. • 360 Energy Inc.

• Atlantic Institute for Market Studies

• Petroleum Services Association of Canada

• Advisian Worley Parsons Group

• Bow Valley College

• Canadian Council for Aboriginal Business

Presentation Outline

Background

Production Outlook

Supply Costs

Emissions

Downstream Markets

Background

Changes in the oil market 2014-2018

Source: Bllomberg

• The WTI oil price rebounded to more than $70 just recently from $40s in September 2016

• OPEC compliance to cuts is 162% as of May 2018

• OECD inventories returned to 5 year averages

Imminent undersupply and price volatility?

Source: IEA

Towards the end of 2022 available spare production capacity will fall below 2 million b/d if there is no significant growth in investments (IEA, March 2017)

Challenges in the Canadian oil and gas industry

Source: Statistics Canada, CANSIM Table 126-0003

• Lack of market access to international and US markets

• Changes in regulatory processes (EIA process, redesign of NEB)

• Widening price differential between Western Canadian Select and WTI

• Production and price risks from the upcoming regulation change in the shipping industry regarding Sulphur levels

• Concerns of lower competitiveness compared to new US tax system

• Depressed service industry due to reduction on drilling

Total Canadian oil production

Source: Statistics Canada, CANSIM Table 126-0003

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2009 2010 2011 2012 2013 2014 2015 2016 2017

(Mb

/d)

Atlantic ON MB SK AB AB -Bitumen & SCO BC NWT

11.1%

US Crude Imports from Canada

Source: US EIA

55% 57%59%

59%59%

60%62% 61% 66%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2009 2010 2011 2012 2013 2014 2015 2016 2017

(Mb

/d

)

Light Sweet Light Sour Medium Heavy Sweet Heavy Sour

18.7%

Market access and crude by rail

Source: JWN, NEB

Canada’s Gas Production, Exports and Imports

Source: JWN, NEB

15.88 16.62 16.81

17.91 18.30

7.63 7.22 7.19 7.99 8.12

2.50 2.11 1.92 2.11 2.51

5.14 5.11 5.27 5.88 5.60

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

2013 2014 2015 2016 2017

Canada's Gas Exports and Production, bcf/d

Gas Production Gas exports to US Gas imports (from US) Net exports

US Gas Industry Developments in 2017

Source: EIA

The Battle for the Central Canada Gas Market

Source: CERI, EIA

• Eastwards throughput of TransCanada Mainline (at the Prairie point) fell from 5.97 bcf/d in 2006 to 2.17 bcf/d in 2017 (-3.8 bcf/d)

• Imports from US increased for the same period (+1.6 bcf/d)

-63%

+170%

Dominion Hub minus Henry Hub

The Battle for the US Gas Market

Source: CERI, EIA

Current Canadian Gas Production

Source: CERI, EIA

• AB – 70%

• BC - 28%

• SK – 2%

• NS – 1%

• Changes

• Deep Panuke declining

• Hydraulic Fracturing bans – QC, NB and NS

Production Outlook

Canadian Oil Sands Production

Source: CERI, Canoils

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,0002

00

7

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

('0

00

bp

d)

Total Bitumen (Production, High Case) Total Bitumen (Production, Reference Case)

Total Bitumen (Production, Low Case)

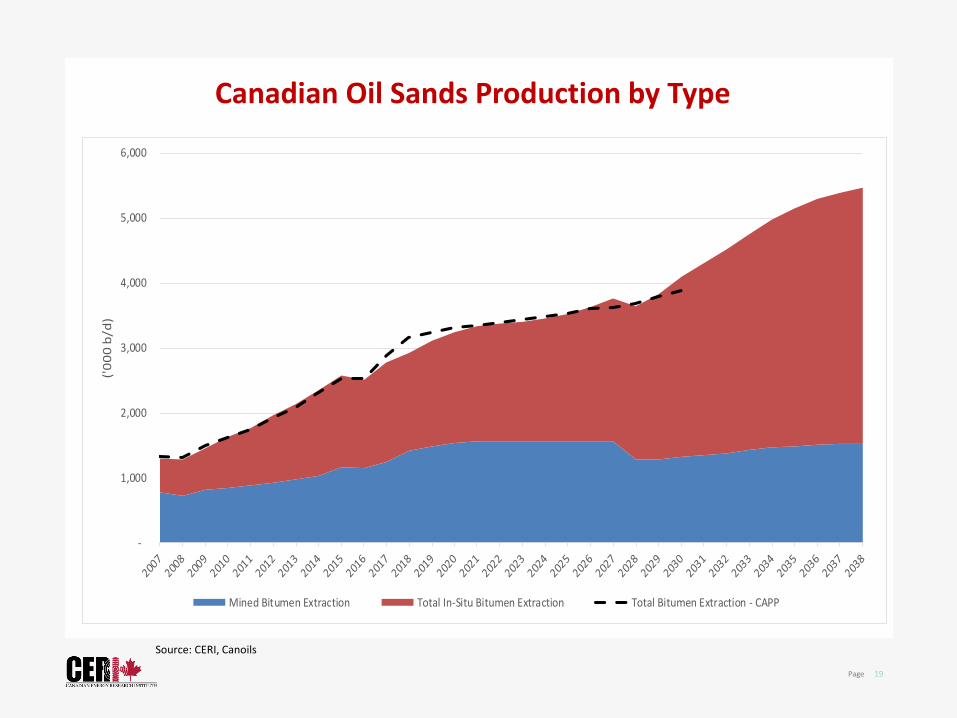

Canadian Oil Sands Production by Type

Source: CERI, Canoils

-

1,000

2,000

3,000

4,000

5,000

6,000

('0

00

b/d

)

Mined Bitumen Extraction Total In-Situ Bitumen Extraction Total Bitumen Extraction - CAPP

Canadian Conventional Crude Oil Production

Source: CERI, BCOGC, AER, Government of SK, Government of MB, CNLOPB, PSAC, CAPP

Source: CERI, BCOGC, AER, Government of SK, Government of MB, CNLOPB, PSAC, CAPP

Total Canadian Oil Production

Source: CERI, BCOGC, AER, Government of SK, Government of MB, CNLOPB, PSAC, CAPP

Source: CERI, BCOGC, AER, Government of SK, Government of MB, CNLOPB, PSAC, CAPP

Canadian Natural Gas Production

Source: CERI, BCOGC, AER, Government of SK, Government of MB, CNLOPB, PSAC, CAPP

Source: CERI, BCOGC, AER, Government of SK, Government of MB, CNLOPB, PSAC, CAPP

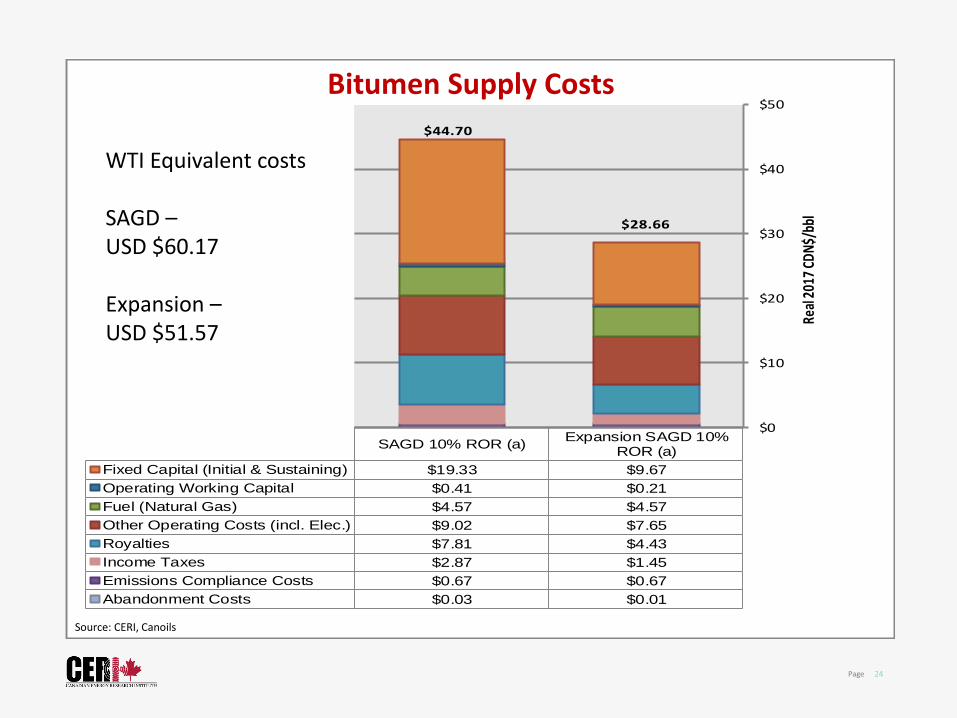

Production Costs

SAGD 10% ROR (a)Expansion SAGD 10%

ROR (a)

Fixed Capital (Initial & Sustaining) $19.33 $9.67

Operating Working Capital $0.41 $0.21

Fuel (Natural Gas) $4.57 $4.57

Other Operating Costs (incl. Elec.) $9.02 $7.65

Royalties $7.81 $4.43

Income Taxes $2.87 $1.45

Emissions Compliance Costs $0.67 $0.67

Abandonment Costs $0.03 $0.01

$0

$10

$20

$30

$40

$50

Real

201

7 CD

N$/

bbl

$44.70

$28.66

Source: CERI, Canoils

WTI Equivalent costs SAGD – USD $60.17 Expansion – USD $51.57

Bitumen Supply Costs

Conventional Oil Supply Costs ($/bbl)

$52

$80-$39 $73-$51

Horn River

Montney

Spirit River

Duvernay

Cardium

Viking

Bakken

$28

$43-$30 $58-$25

$32

$46

$45-$40

$59

$56-$20

$40-$32

Legend: $X (Vertical)-$Y (Horizontal)

Natural Gas Supply Costs ($/mmscf)

Horn River

Montney

Spirit River

Duvernay

Cardium

Viking

Bakken

Legend: $X (Vertical)-$Y (Horizontal)

$1.7-$2.9

$1.8

$1.8-$1.7

$1.7-$1.9

$1.8-$1.7

$1.4-$1.6 $2.2-$1.8

$2.5-$1.6

$2.7

Emissions

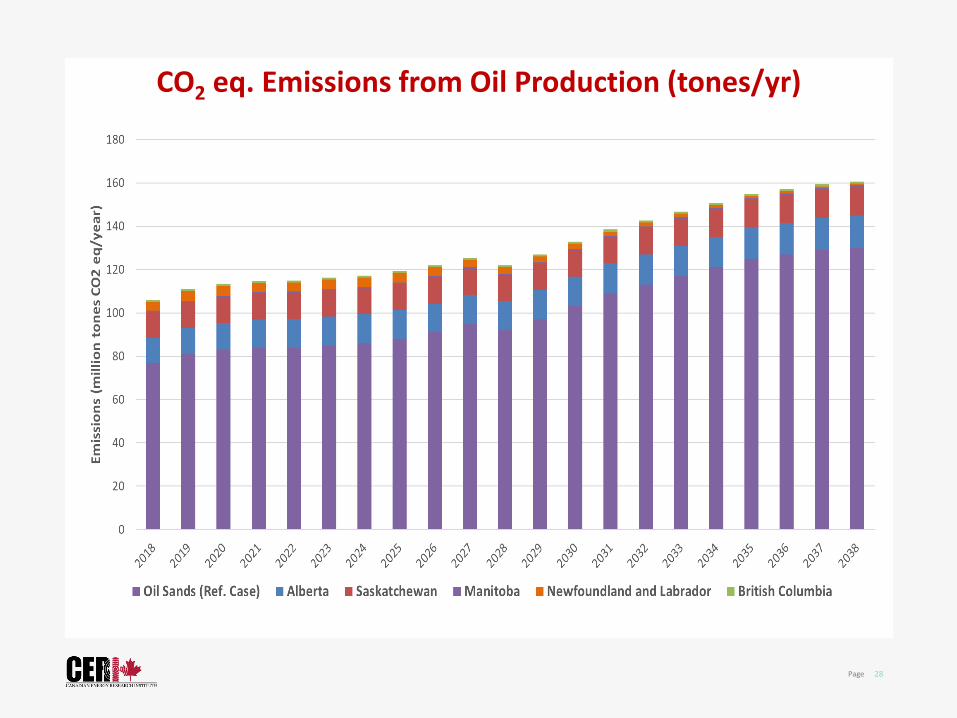

CO2 eq. Emissions from Oil Production (tones/yr)

Source: CERI, BCOGC, AER, Government of SK, Government of MB, CNLOPB, PSAC, CAPP

CO2 eq. Emissions from Gas Production (tones/yr)

Source: CERI, BCOGC, AER, Government of SK, Government of MB, CNLOPB, PSAC, CAPP

Downstream Markets

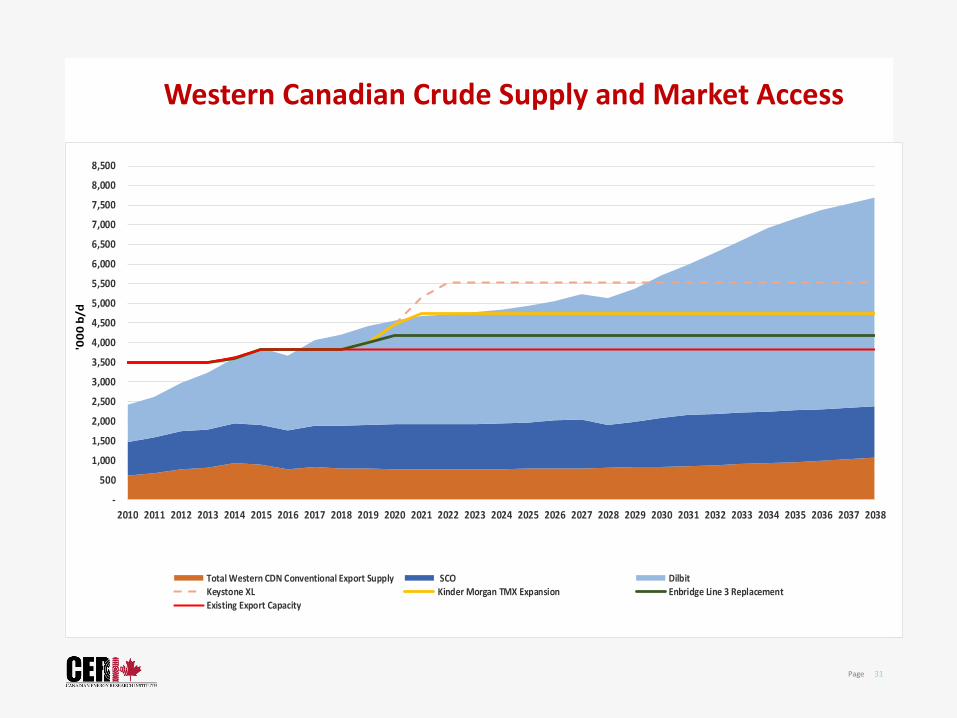

Western Canadian Crude Supply and Market Access

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038

'00

0 b

/d

Total Western CDN Conventional Export Supply SCO DilbitKeystone XL Kinder Morgan TMX Expansion Enbridge Line 3 ReplacementExisting Export Capacity

Conclusions • Reasonable growth expected in Oil Sands and

conventional oil in Canada

• Offshore NL will require new investment to maintain growth

• Growth in Western Canada challenged by Market Access

• Canadian Natural Gas will have to find new markets

• LNG remains the largest opportunity for NG

• NG market will affect NGLs and petrochemical investment

Thank You for Your Time

www.ceri.ca

CANADIAN ENERGY RESEARCH INSTITUTE

@CERI_CANADA

UPCOMING STUDIES:

Competitive Analysis of Canadian LNG

Carbon Management Impacts on Electricity Markets

An Economic Assessment Of The International Marine Organization Sulphur Regulations On Markets For Canadian Crude Oil