Embed Size (px)

Citation preview

Canadian Bioenergy AssociationIEA Task 38 Workshop

Status of Forest Biomass StrategyVictoria, BC, Sept 15, 2004

Doug Bradley

President DirectorClimate Change Solutions CANBIO

15 Sept 2004 IEA Bioenergy Task 38 2

Topics

o CanBioo Bioenergy Issues

v Biomass volumes, costsv Technologiesv Financial Requirementsv Incentivesv Biotrade

o Bioenergy Strategy

15 Sept 2004 IEA Bioenergy Task 38 3

CanBio: National, industry driven, non-profit

o Objectivesv Promote bioenergy developmentv National voice for bioenergy industryv Develop national bioenergy strategyv Identify barriers, opportunitiesv Information exchange/ Educatev Influence policies, incentives

15 Sept 2004 IEA Bioenergy Task 38 4

Topics

o CanBioo Bioenergy Issues

v Biomass volumesv Technologiesv Financial Requirementsv Incentivesv Biotrade

o Bioenergy Strategy

15 Sept 2004 IEA Bioenergy Task 38 5

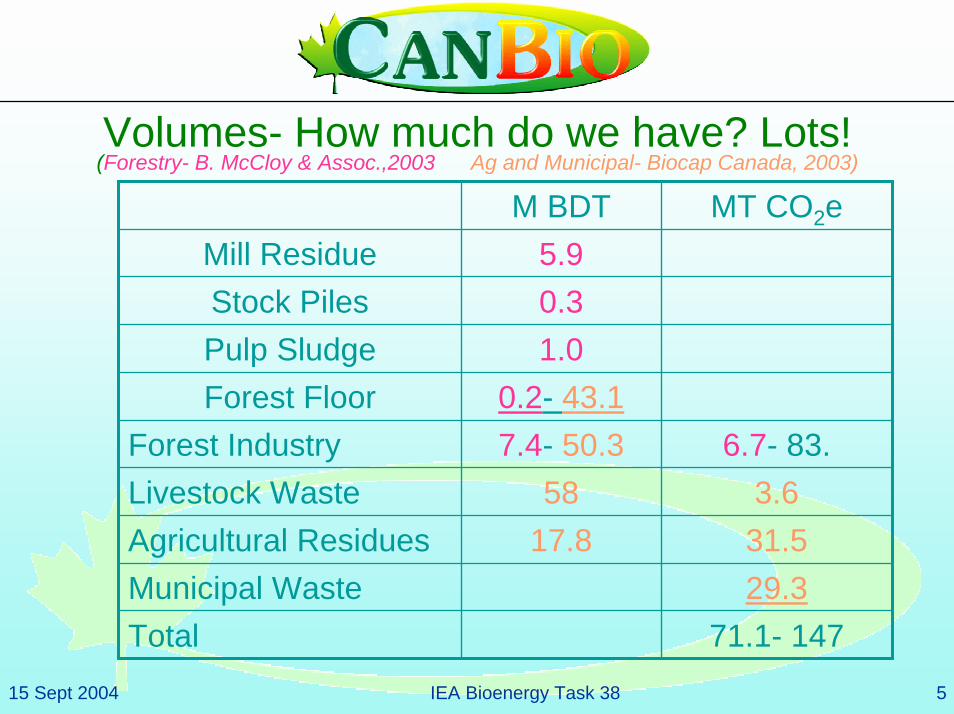

Volumes- How much do we have? Lots! (Forestry- B. McCloy & Assoc.,2003 Ag and Municipal- Biocap Canada, 2003)

M BDT MT CO2eMill Residue 5.9Stock Piles 0.3Pulp Sludge 1.0Forest Floor 0.2- 43.1

Forest Industry 7.4- 50.3 6.7- 83.Livestock Waste 58 3.6Agricultural Residues 17.8 31.5Municipal Waste 29.3Total 71.1- 147

15 Sept 2004 IEA Bioenergy Task 38 6

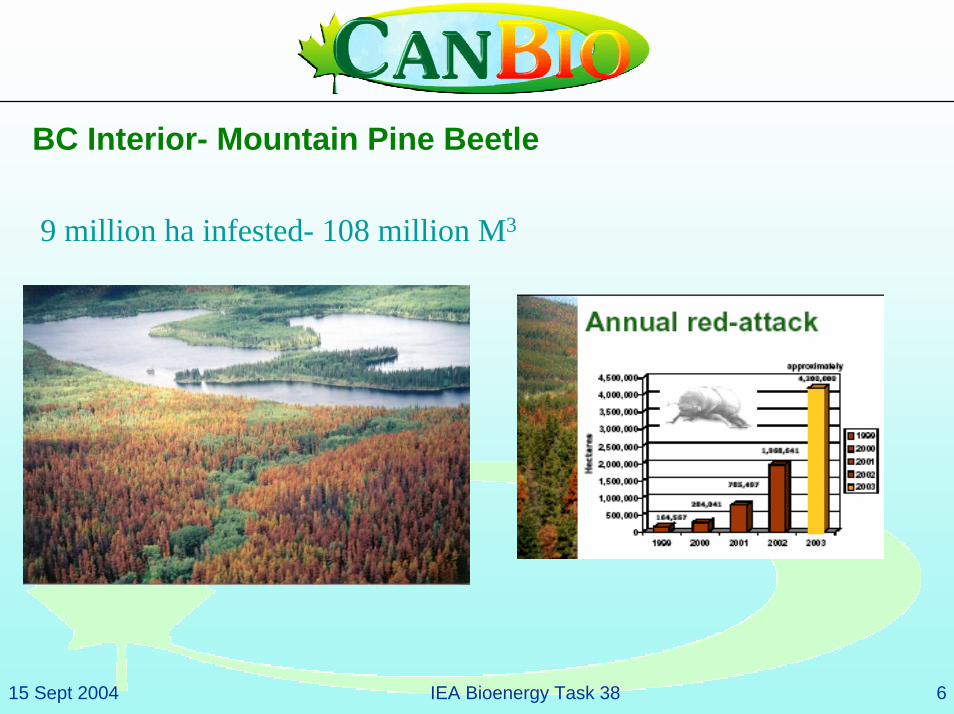

BC Interior- Mountain Pine Beetle

9 million ha infested- 108 million M3

15 Sept 2004 IEA Bioenergy Task 38 7

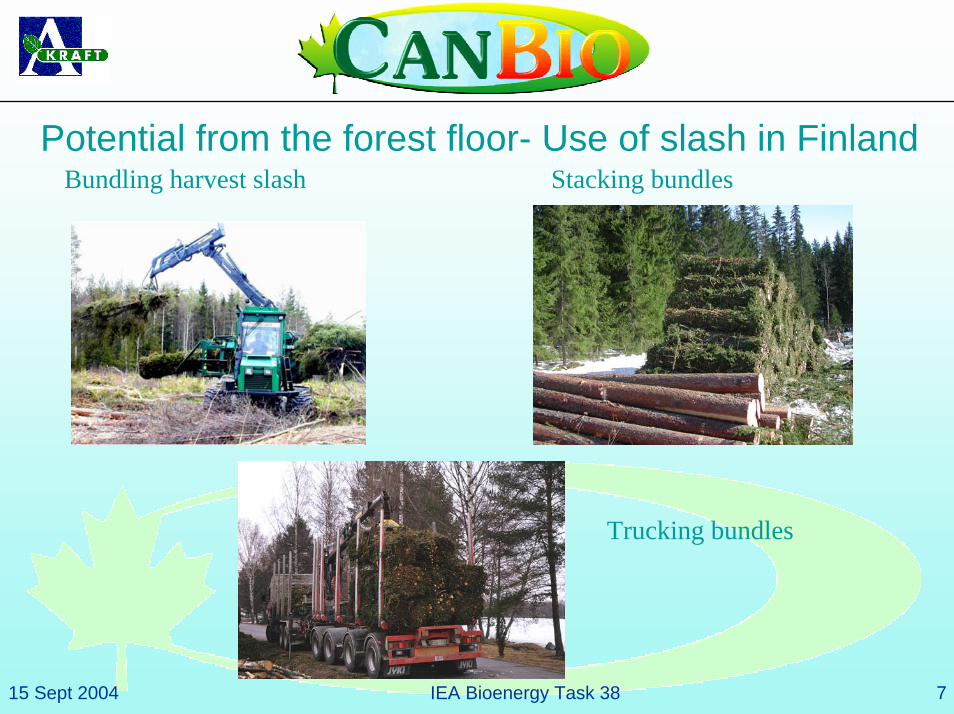

Bundling harvest slash Stacking bundlesPotential from the forest floor- Use of slash in Finland

Trucking bundles

15 Sept 2004 IEA Bioenergy Task 38 8

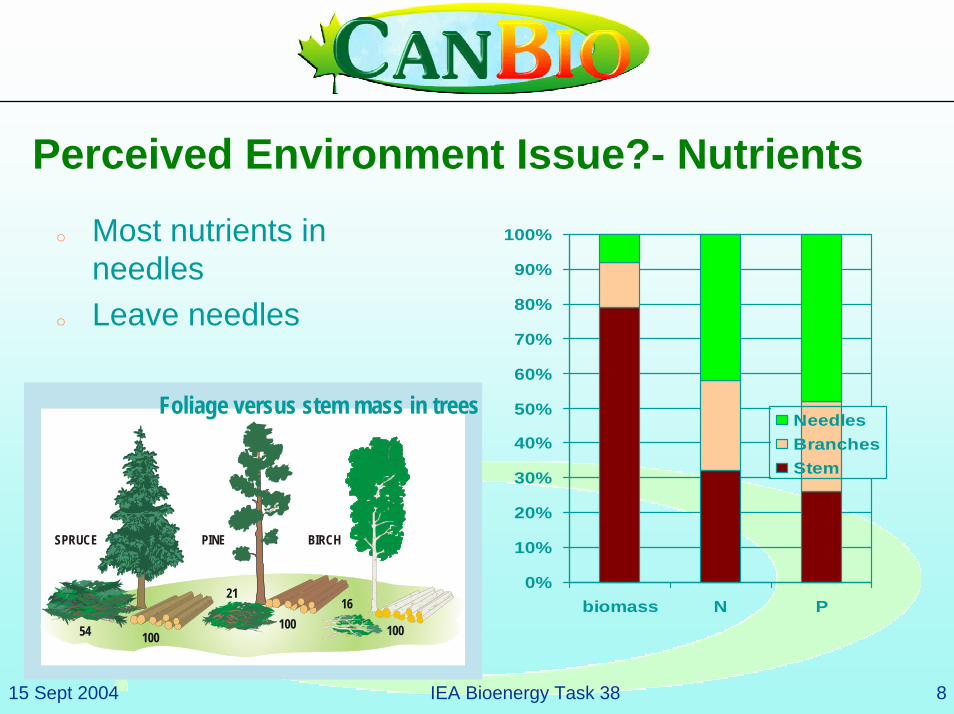

Perceived Environment Issue?- Nutrientso Most nutrients in

needleso Leave needles

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

biomass N P

NeedlesBranchesStem

BIRCHPINESPRUCE

54

2116

100100 100

Foliage versus stem mass in trees

15 Sept 2004 IEA Bioenergy Task 38 9

Topics

o CanBioo Bioenergy Issues

v Biomass volumesv Technologies (Combustion, Bio-oil)v Financial Requirementsv Renewable Energy Incentivesv Biotrade

o Bioenergy Strategy

15 Sept 2004 IEA Bioenergy Task 38

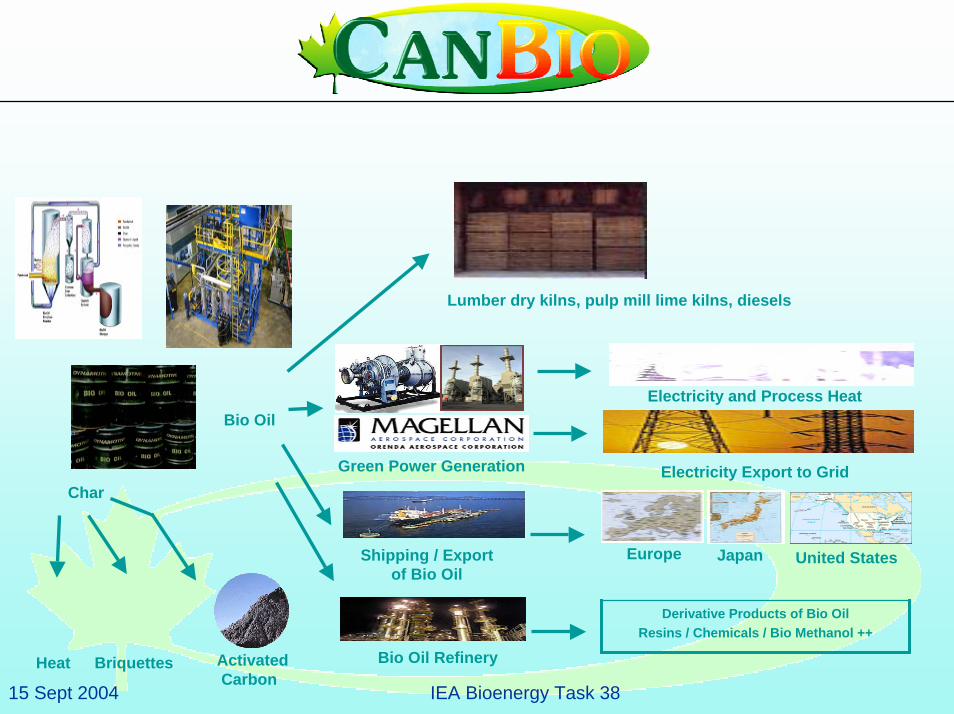

Electricity and Process Heat

Electricity Export to Grid

Lumber dry kilns, pulp mill lime kilns, diesels

Bio Oil

Bio Oil Refinery

Derivative Products of Bio OilResins / Chemicals / Bio Methanol ++

Europe Japan United States

Green Power Generation

Shipping / Export of Bio Oil

Char

Heat Briquettes ActivatedCarbon

15 Sept 2004 IEA Bioenergy Task 38

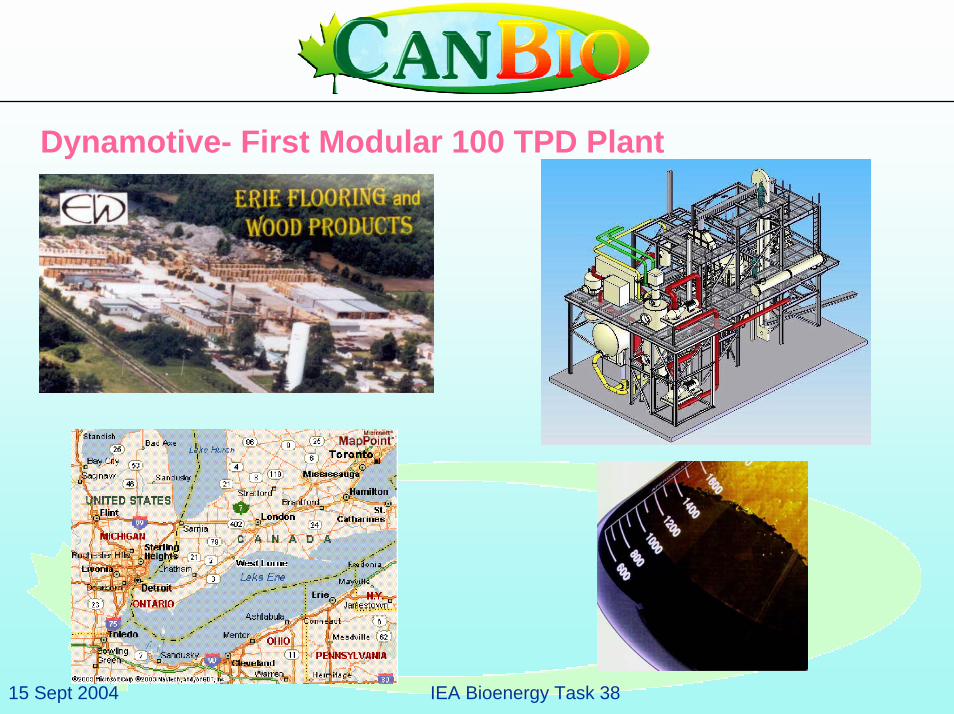

Dynamotive- First Modular 100 TPD Plant

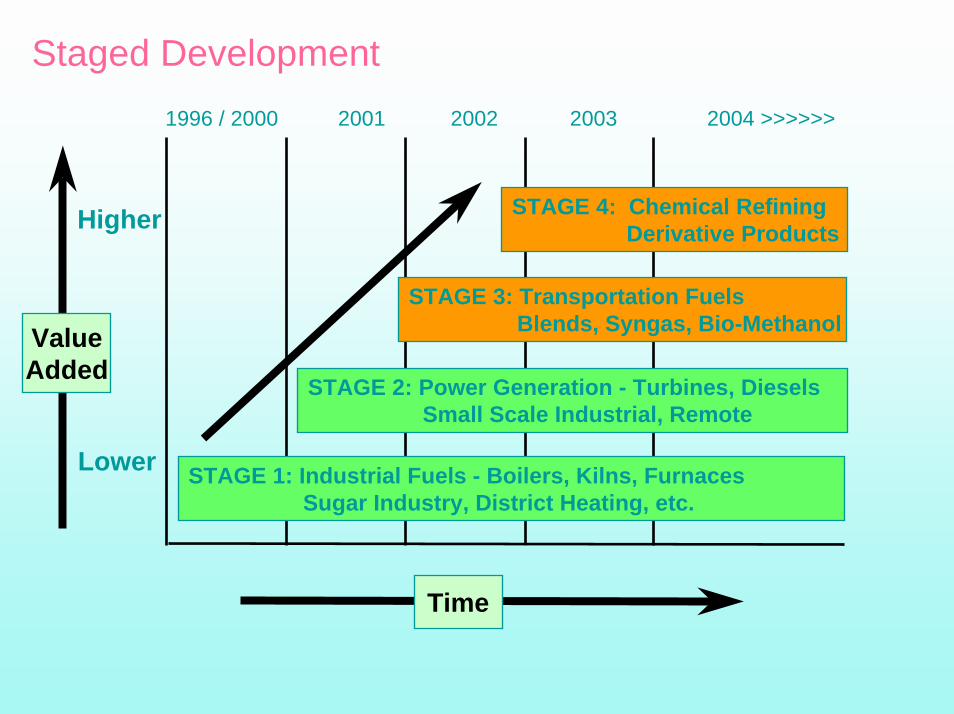

Staged Development

STAGE 1: Industrial Fuels - Boilers, Kilns, FurnacesSugar Industry, District Heating, etc.

STAGE 3: Transportation FuelsBlends, Syngas, Bio-Methanol

STAGE 2: Power Generation - Turbines, Diesels Small Scale Industrial, Remote

Higher

Lower

ValueAdded

STAGE 4: Chemical Refining Derivative Products

1996 / 2000 2001 2002 2003 2004 >>>>>>

Time

15 Sept 2004 IEA Bioenergy Task 38 13

Topics

o CanBioo Bioenergy Issues

v Biomass volumesv Technologiesv Financial Requirementsv Incentivesv Biotrade

o Bioenergy Strategy

15 Sept 2004 IEA Bioenergy Task 38 14

Financing Models Needed

o Much capital neededo Forest Industry has no money!

v $capital on core businesso Need vehicles to funnel investment to bioenergy

v Flow through shares/Investment Fundsv Oil & gas exploration examples

15 Sept 2004 IEA Bioenergy Task 38 15

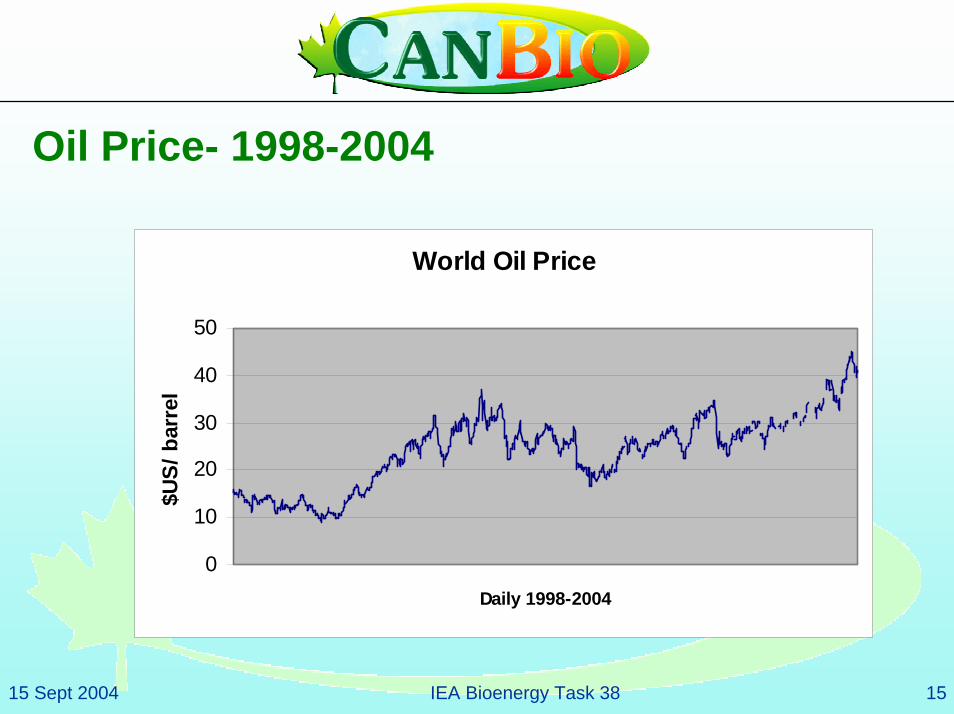

Oil Price- 1998-2004

World Oil Price

0

10

20

30

40

50

Daily 1998-2004

$US/

bar

rel

15 Sept 2004 IEA Bioenergy Task 38 16

Topics

o CanBioo Bioenergy Issues

v Biomass volumesv Technologiesv Financial Requirementsv Incentivesv Biotrade

o Bioenergy Strategy

15 Sept 2004 IEA Bioenergy Task 38 17

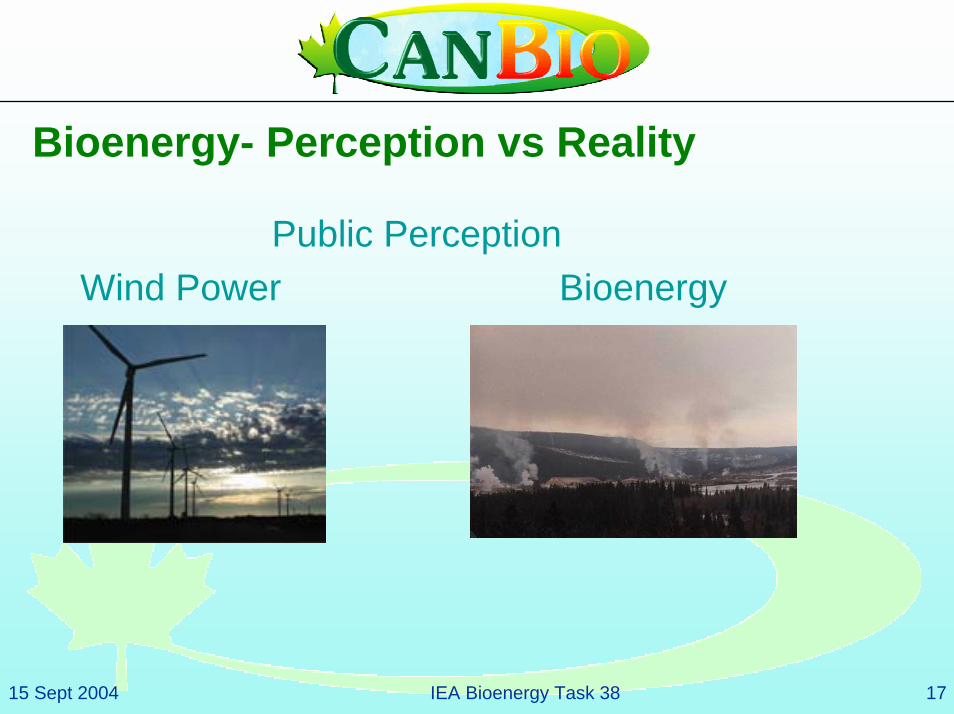

Bioenergy- Perception vs Reality

Public PerceptionWind Power Bioenergy

15 Sept 2004 IEA Bioenergy Task 38 18

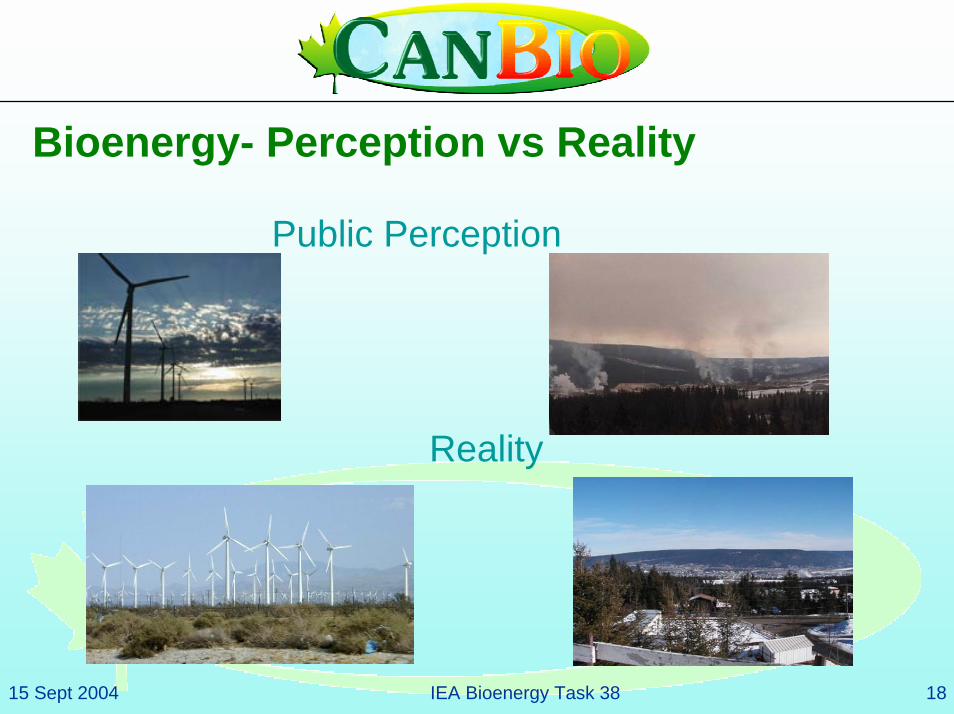

Bioenergy- Perception vs Reality

Public Perception

Reality

15 Sept 2004 IEA Bioenergy Task 38 19

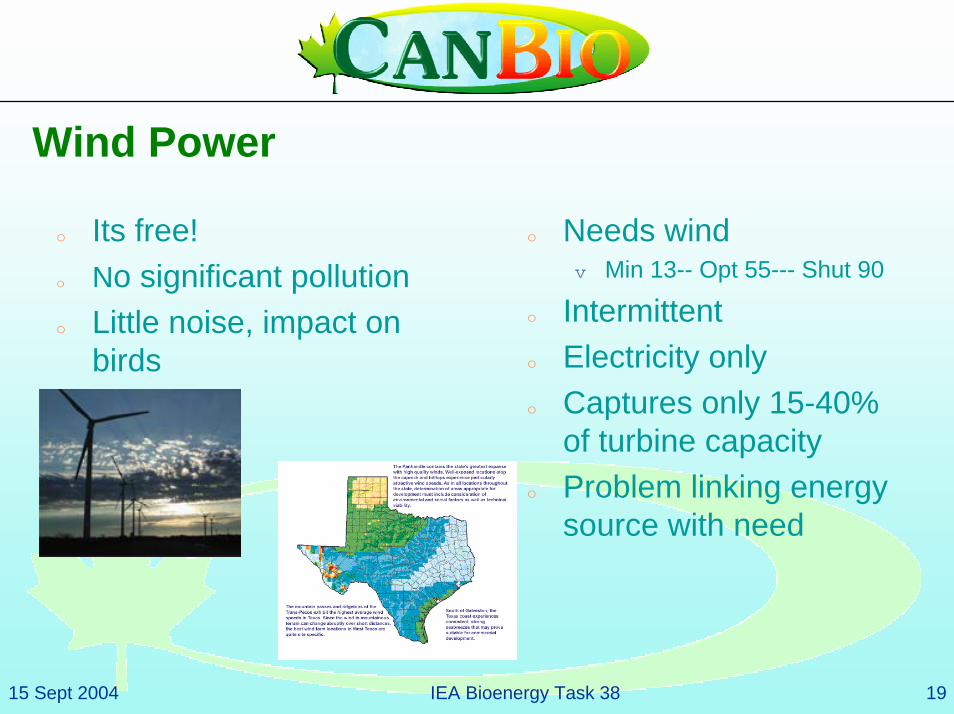

Wind Power

o Its free! o No significant pollutiono Little noise, impact on

birds

o Needs windv Min 13-- Opt 55--- Shut 90

o Intermittent o Electricity onlyo Captures only 15-40%

of turbine capacityo Problem linking energy

source with need

15 Sept 2004 IEA Bioenergy Task 38 20

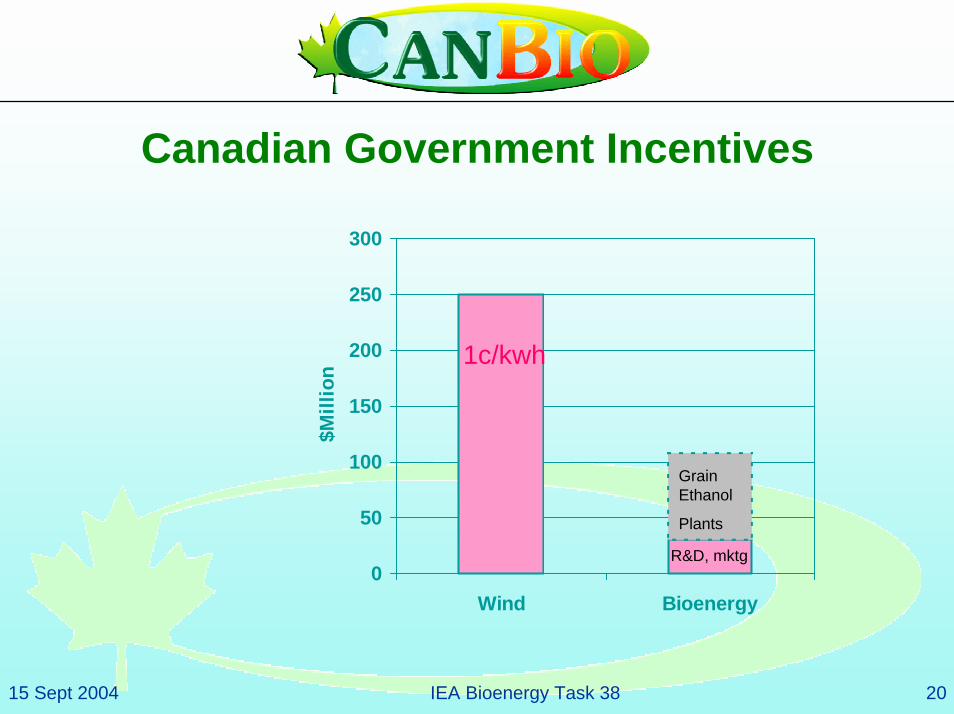

Canadian Government Incentives

0

50

100

150

200

250

300

Wind Bioenergy

$Mill

ion

1c/kwh

Grain Ethanol

Plants

R&D, mktg

15 Sept 2004 IEA Bioenergy Task 38 21

Government Policyo Existing

v REDI (Renewable Energy Deployment Initiative) max $80,000

v Cdn Renewable & Conservation Expenses (Tax)v Tax Depreciation 43.1 for generation equipmentv MIP (Market Incentive Program) 40% refund of marketing costs only

v 10¢ per litre excise tax exemption on ethanol fuel v 20% gov’t power purchases from renewablev Wind Power 1¢/Kwh production incentive $250 million

o Need meaningful incentivesv Feed-in-tariffs (price premiums)v RPS (Renewable Portfolio Standard)v Grants (capital support)

15 Sept 2004 IEA Bioenergy Task 38 22

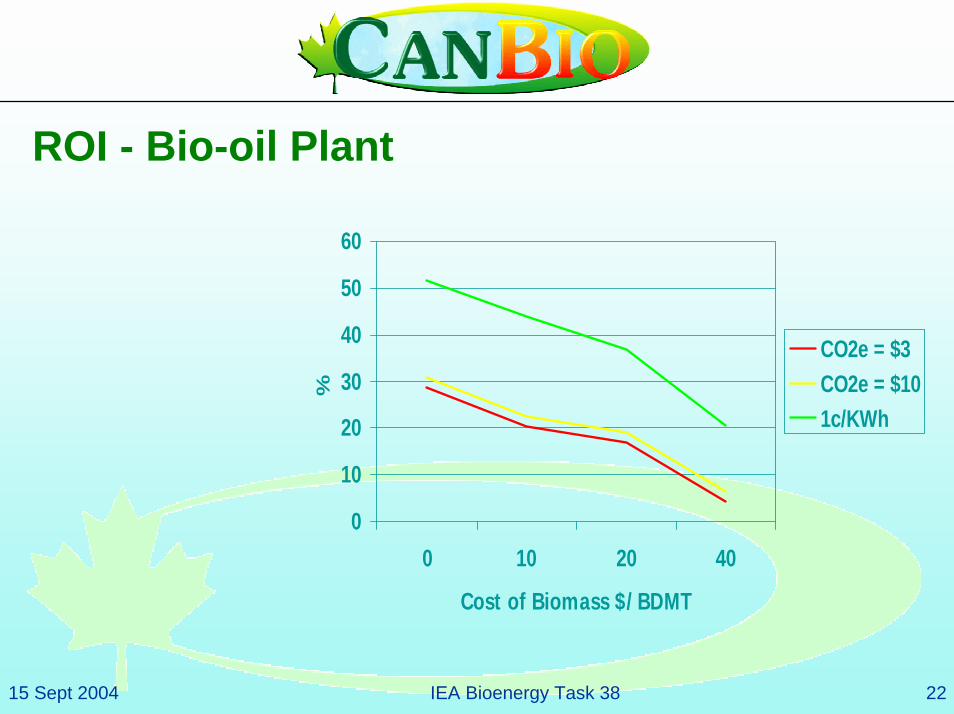

ROI - Bio-oil Plant

0

10

20

30

40

50

60

0 10 20 40

Cost of Biomass $/BDMT

%CO2e = $3CO2e = $101c/KWh

15 Sept 2004 IEA Bioenergy Task 38 23

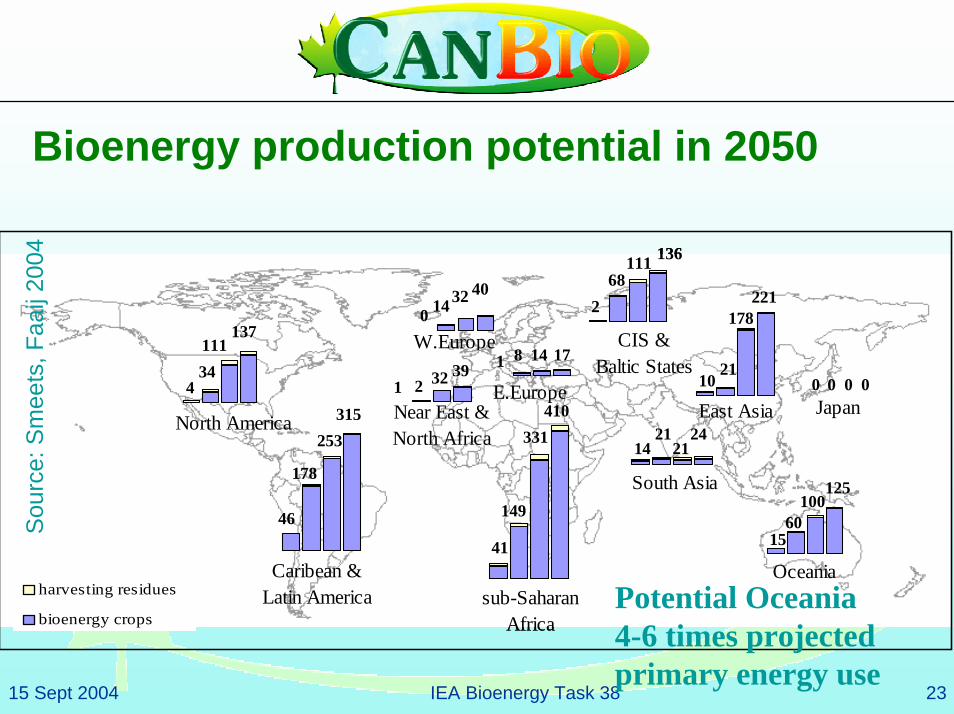

Bioenergy production potential in 2050

434111

137

North AmericaJapan

0 0 0 0

Near East & North Africa

1 2 32 39

W.Europe0 14 32 40

harvesting residues

bioenergy crops

Oceania

1560

100125

E.Europe1 8 14 17

East Asia10

21

178221

410

sub-SaharanAfrica

41

149

331

Caribean &Latin America

178

253315

46

268

111 136

CIS & Baltic States

South Asia

1421

2124

434111

137

North AmericaJapan

0 0 0 0

Near East & North Africa

1 2 32 39

W.Europe0 14 32 40

harvesting residues

bioenergy crops

Oceania

1560

100125

E.Europe1 8 14 17

East Asia10

21

178221

410

sub-SaharanAfrica

41

149

331

Caribean &Latin America

178

253315

46

268

111 136

CIS & Baltic States

South Asia

1421

2124

Sou

rce:

Sm

eets

, Faa

ij 20

04

Potential Oceania 4-6 times projected primary energy use

15 Sept 2004 IEA Bioenergy Task 38 24

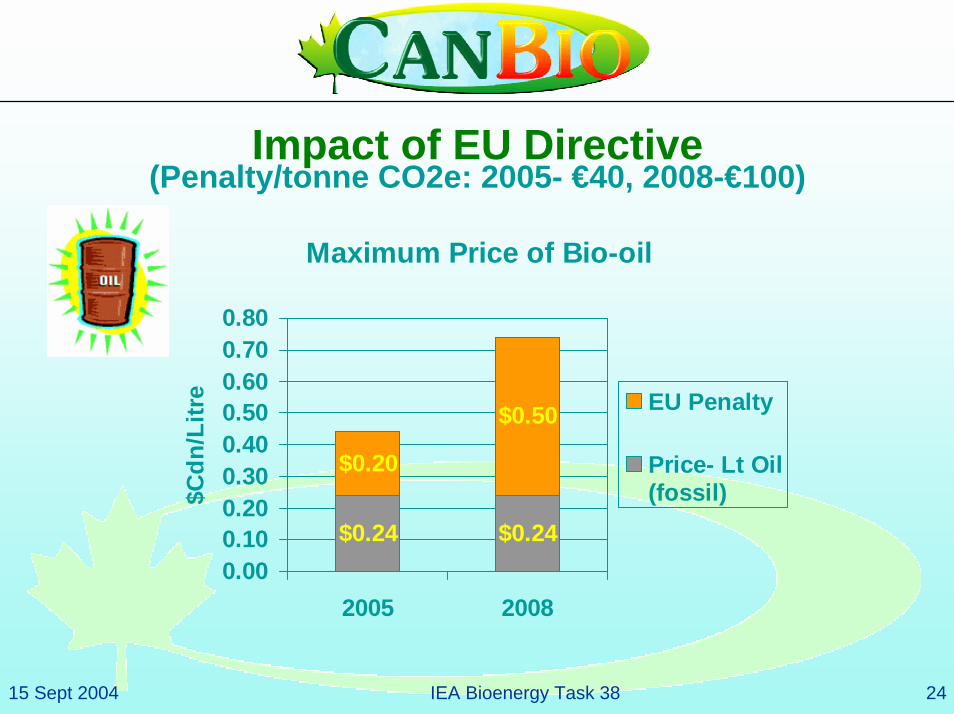

Impact of EU Directive (Penalty/tonne CO2e: 2005- €40, 2008-€100)

Maximum Price of Bio-oil

$0.24 $0.24

$0.20

$0.50

0.000.100.200.300.400.500.600.700.80

2005 2008

$Cdn

/Litr

e EU Penalty

Price- Lt Oil(fossil)

15 Sept 2004 IEA Bioenergy Task 38 25

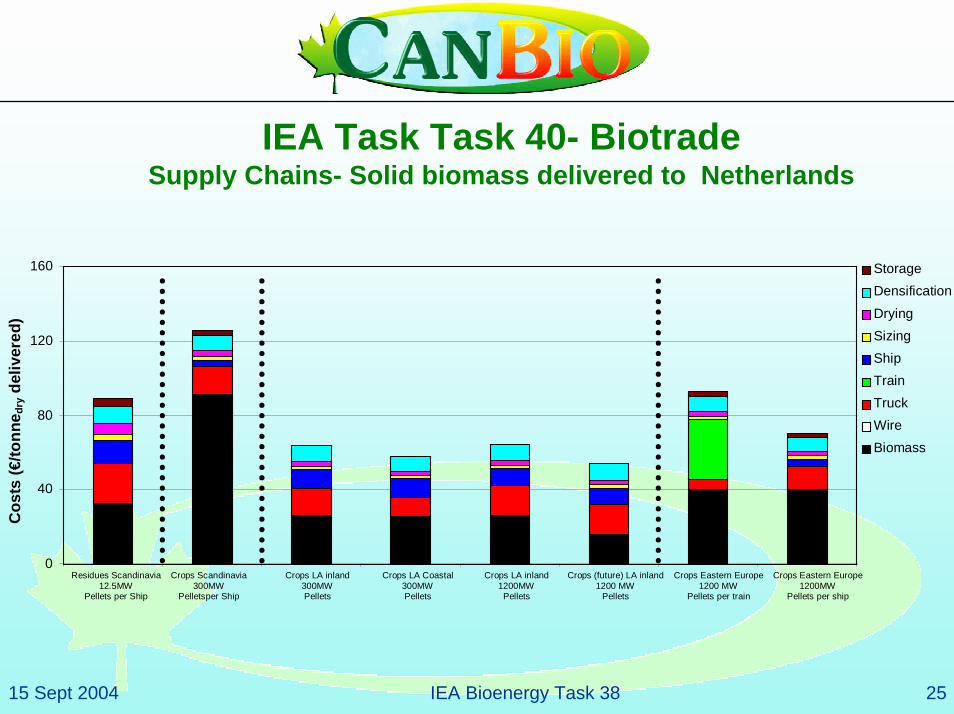

IEA Task Task 40- BiotradeSupply Chains- Solid biomass delivered to Netherlands

0

40

80

120

160

Residues Scandinavia 12.5MW

Pellets per Ship Crops Scandinavia

300MW Pelletsper Ship

Crops LA inland 300MW Pellets

Crops LA Coastal 300MW Pellets

Crops LA inland 1200MW Pellets

Crops (future) LA inland1200 MW

Pellets Crops Eastern Europe

1200 MW Pellets per train

Crops Eastern Europe 1200MW

Pellets per ship

Cos

ts (€

/tonn

e dry

del

iver

ed)

Storage Densification Drying Sizing Ship Train Truck Wire Biomass

15 Sept 2004 IEA Bioenergy Task 38 26

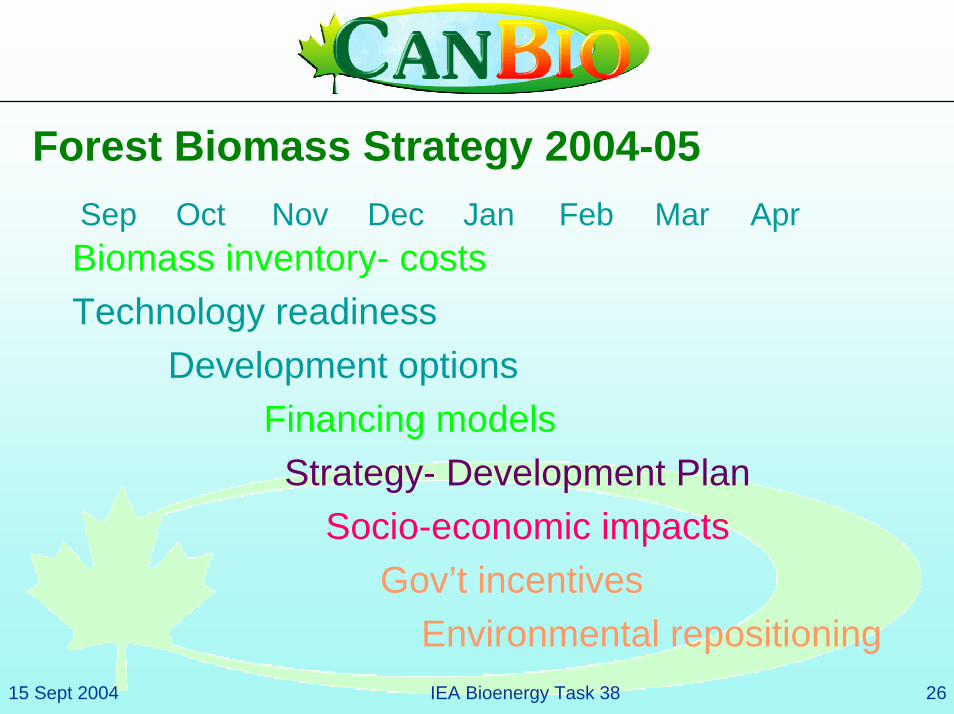

Forest Biomass Strategy 2004-05

Biomass inventory- costsTechnology readiness

Development optionsFinancing modelsStrategy- Development Plan

Socio-economic impactsGov’t incentives

Environmental repositioning

Sep Oct Nov Dec Jan Feb Mar Apr

15 Sept 2004 IEA Bioenergy Task 38 27

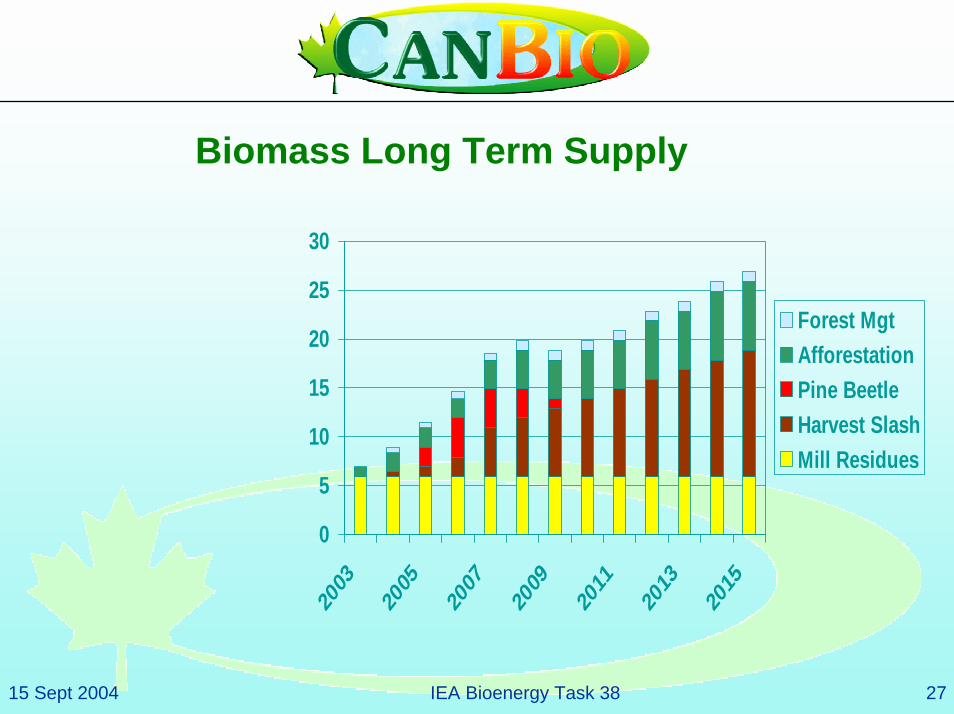

Biomass Long Term Supply

0

5

10

15

20

25

30

2003

2005

2007

2009

2011

2013

2015

Forest MgtAfforestationPine BeetleHarvest SlashMill Residues

15 Sept 2004 IEA Bioenergy Task 38 28

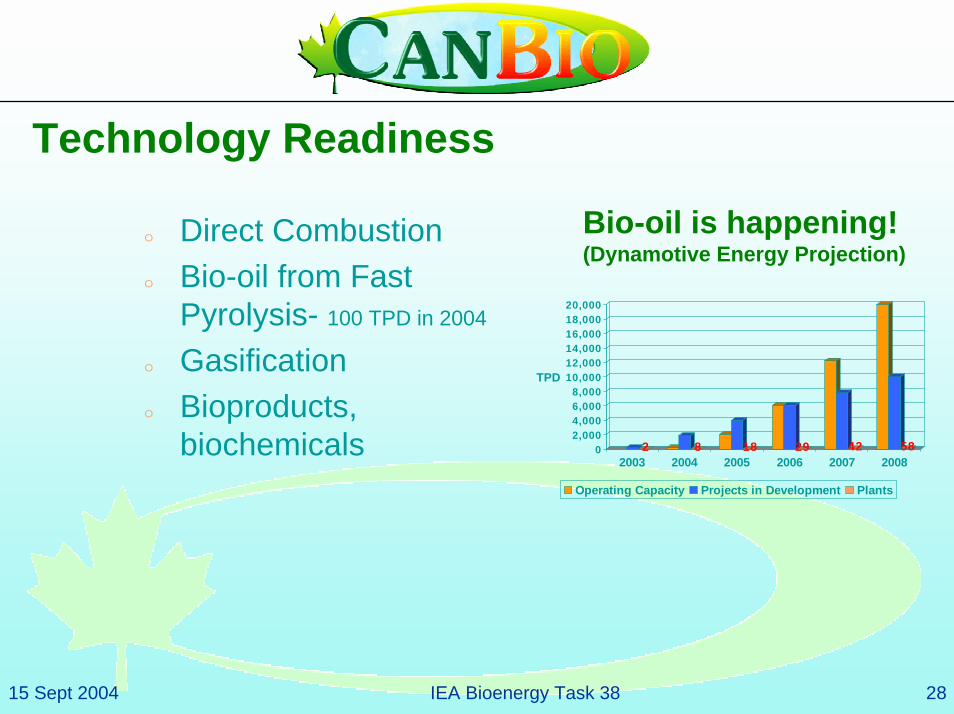

Technology Readiness

Bio-oil is happening!(Dynamotive Energy Projection)

o Direct Combustiono Bio-oil from Fast

Pyrolysis- 100 TPD in 2004

o Gasificationo Bioproducts,

biochemicals 2 8 18 29 42 5802,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

TPD

2003 2004 2005 2006 2007 2008

Operating Capacity Projects in Development Plants

15 Sept 2004 IEA Bioenergy Task 38 29

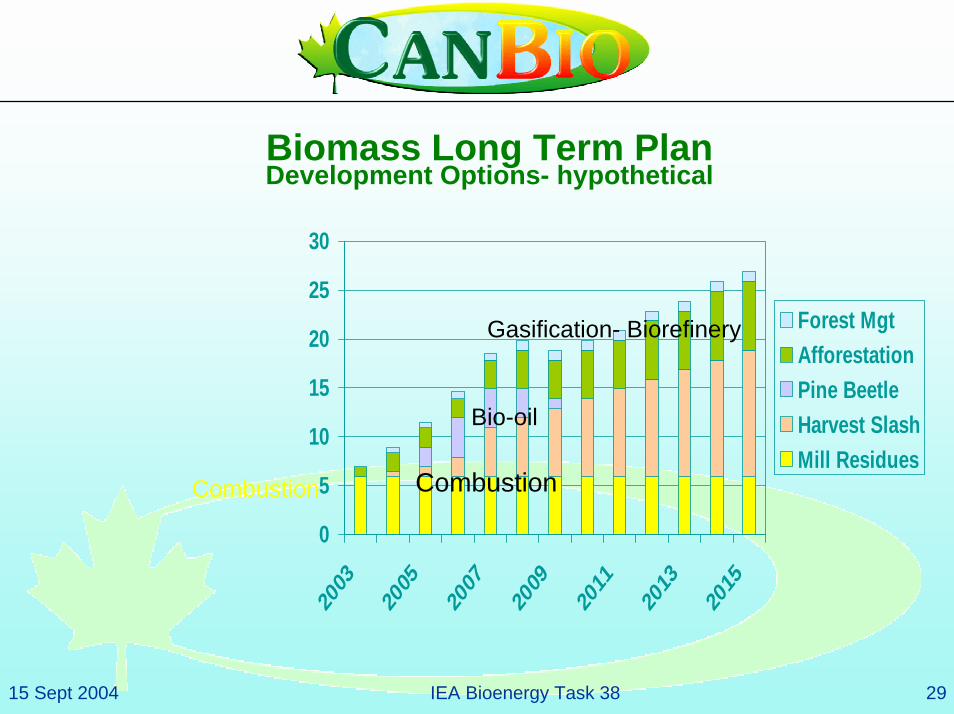

Biomass Long Term Plan Development Options- hypothetical

0

5

10

15

20

25

30

2003

2005

2007

2009

2011

2013

2015

Forest MgtAfforestationPine BeetleHarvest SlashMill Residues

Combustion

Bio-oil

Gasification- Biorefinery

Combustion

15 Sept 2004 IEA Bioenergy Task 38 30

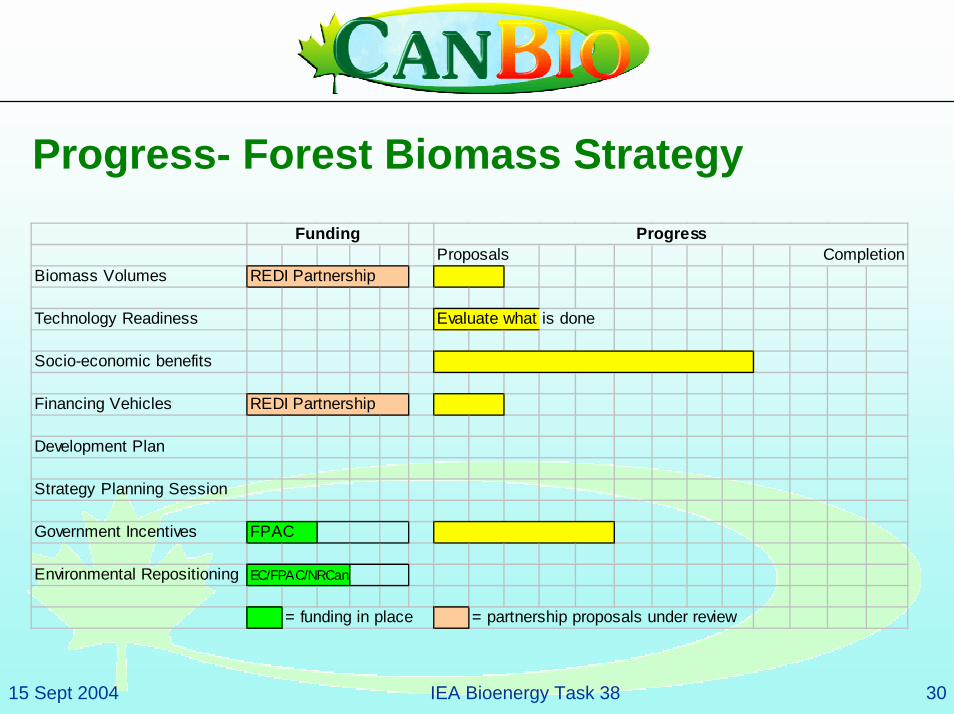

Progress- Forest Biomass StrategyFunding Progress

Proposals CompletionBiomass Volumes REDI Partnership

Technology Readiness Evaluate what is done

Socio-economic benefits

Financing Vehicles REDI Partnership

Development Plan

Strategy Planning Session

Government Incentives FPAC

Environmental Repositioning EC/FPAC/NRCan

= funding in place = partnership proposals under review

15 Sept 2004 IEA Bioenergy Task 38 31

What will a forest biomass strategy show?

o Industry? Impact on shareholder value

o Government? Impact on economic growth, trade

o NGOs? Impact on environment relative to other energy sources

15 Sept 2004 IEA Bioenergy Task 38 32

What have we seen?

o Biomass volumes are sizableo Many technologies are readyo Need innovative investment optionso Recognize socioeconomic benefitso Explore Incentives (equal to wind)o Where we are going? How get there?

A forest biomass strategy!

15 Sept 2004 IEA Bioenergy Task 38 33

Canadian Bioenergy Association3330 White Oak Road, London, Ontario N6E 1L8

E-mail: [email protected] Web: www.canbio.caPhone: (519) 686-8895 Fax: (519) 686-1132

Doug Bradleyo 69 Fulton Avenue ·Ottawa, Ontario ·Canada K1S 4Y7o phone · 613.730.1999 email ·[email protected] web site · www.climatechangesolutions.net

![Forests, bioenergy and climate change mitigationtask38.ieabioenergy.com/wp-content/uploads/2017/01/... · century through large-scale changes in energy systems … [and that] bioenergy](https://img.pdfslide.us/doc/110x75/5f0c94947e708231d4361cc8/forests-bioenergy-and-climate-change-century-through-large-scale-changes-in-energy.jpg)