Embed Size (px)

Citation preview

CABRI Presentation on PPPs in AfricaHigh-Level Workshop on

Public-Private Partnerships’ implementation in the Energy Sector

Implementation Framework to Enhance Private Sector Investment and Participation in the Energy Sector

30 June – 1 July 2011

Taz Chaponda

Agenda

• Introduction to CABRI

• The Role of PPP Units in Africa

• Nigeria Power Sector Reforms

• Lessons from CABRI Dialogue

Collaborative Africa Budget Reform Initiative• CABRI is a professional network of senior budget officials in African

Ministries of Finance and/or Planning

• CABRI was officially launched in May 2008, and in December 2009 it became a legal and independent membership based organisation

• Its main objective is to promote efficient and effective management of public finances– Developing appropriate approaches, procedures and practices– Capacity building and research programme in public finance management– Develop common positions on budget related issues

• Holds annual conference, regional seminars, e-networking, series of publications and documents

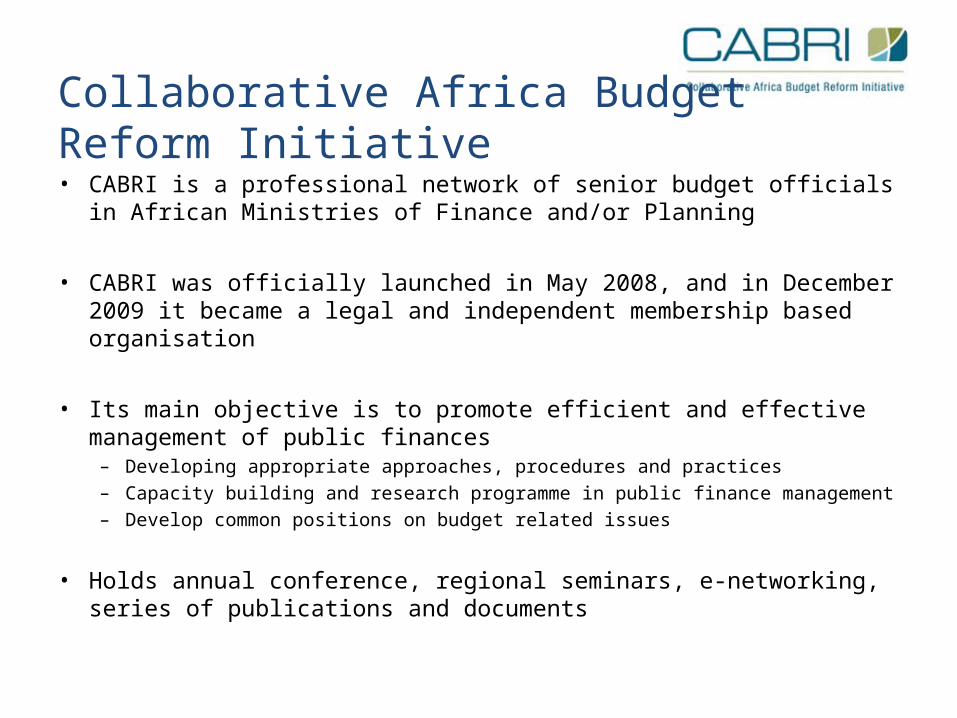

4

Total: US$21.7 billion (2008 US$) Total: US$72.3 billion (2008 US$)

1990–2000 2001–08

Private investment in infrastructure for Sub-Saharan Africa, 1990–2008

Source: World Bank and PPIAF, PPI Project Database.

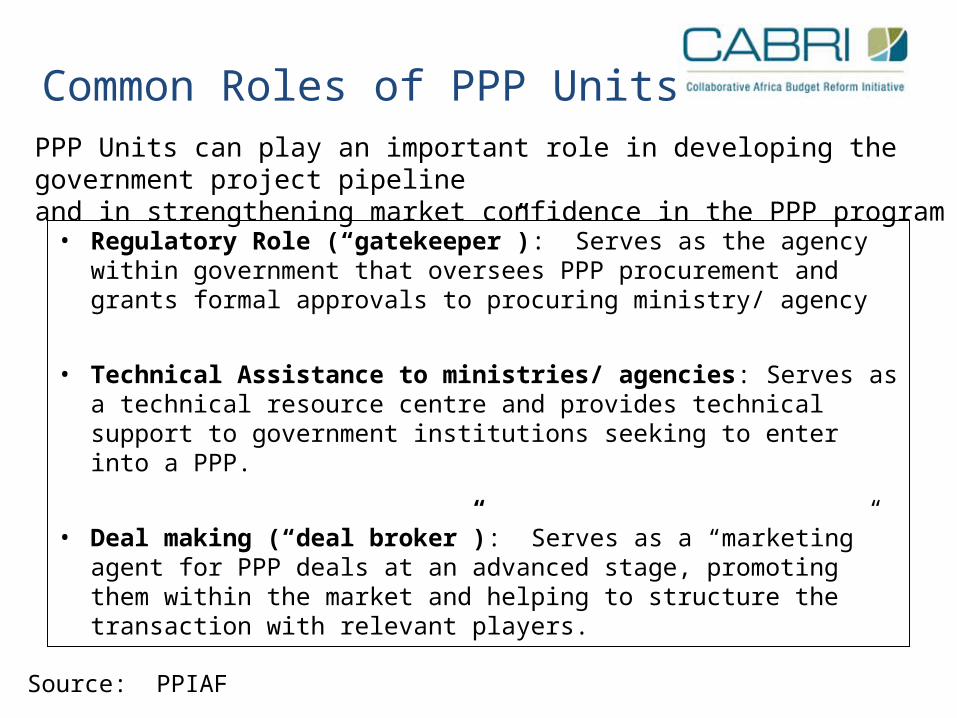

Common Roles of PPP Units

• Regulatory Role (“gatekeeper”): Serves as the agency within government that oversees PPP procurement and grants formal approvals to procuring ministry/ agency

• Technical Assistance to ministries/ agencies: Serves as a technical resource centre and provides technical support to government institutions seeking to enter into a PPP.

• Deal making (“deal broker”): Serves as a “marketing” agent for PPP deals at an advanced stage, promoting them within the market and helping to structure the transaction with relevant players.

PPP Units can play an important role in developing the government project pipelineand in strengthening market confidence in the PPP program

Source: PPIAF

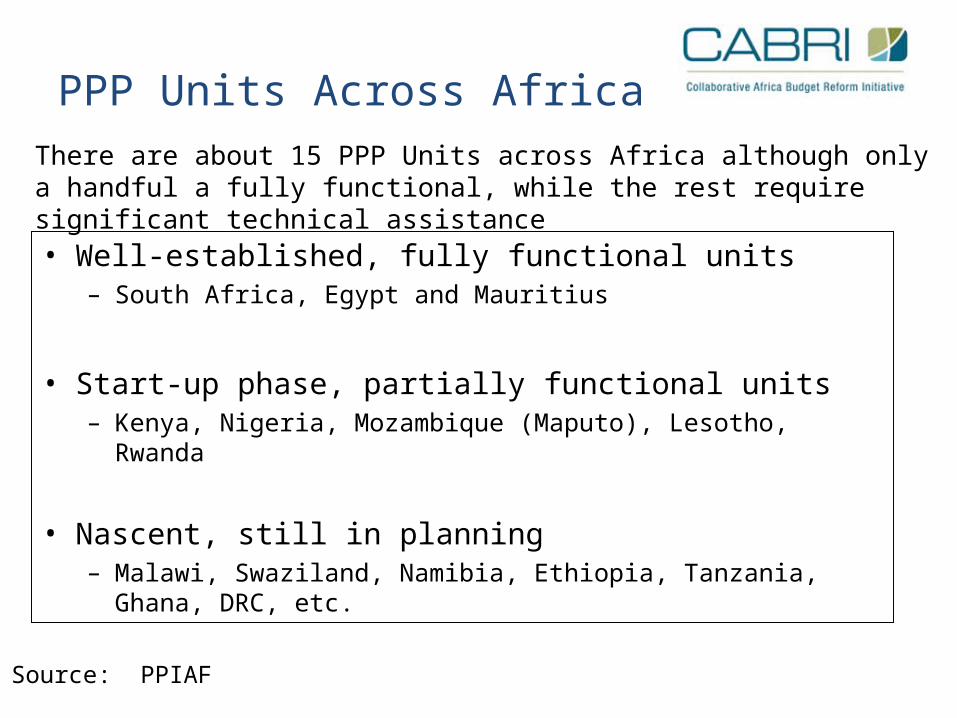

PPP Units Across Africa

• Well-established, fully functional units– South Africa, Egypt and Mauritius

• Start-up phase, partially functional units– Kenya, Nigeria, Mozambique (Maputo), Lesotho, Rwanda

• Nascent, still in planning– Malawi, Swaziland, Namibia, Ethiopia, Tanzania, Ghana, DRC, etc.

There are about 15 PPP Units across Africa although only a handful a fully functional, while the rest require significant technical assistance

Source: PPIAF

Challenges facing new markets• Enabling legislation: Deals can and have proceeded in the absence of a PPP

law. A modern procurement law might suffice. Alternatively, a sector-specific law can cover concessions, or even a project-specific agreement based on international norms. What matters is enforceability.

• Long-term Debt finance: Longer term debt tenors can be achieved when donor support is available, such as partial risk guarantee, political risk/ credit guarantee. Such forms of credit-enhancement can improve risk rating to stretch tenors to about 10 years, followed by refinancing arrangements

• Local Skills: International transaction advisors are increasingly mobile, as long as perception of client government is fair. Advisors are more amenable to donor funded project as payment risk is removed.

• Affordability: In some countries, sector reform will be necessary to raise tariffs to more sensible levels so that user fees can partially close fund gap (eg. power sector). However, for most countries, Viability Gap Funding necessary.

Source: PPIAF

Nigeria: Power Sector Background

8

• In 2005, the FGN initiated the reform of the power sector with the unbundling of PHCN under the EPSRA (2005)

• The following assets are available for privatisation• 6 Power Generation Companies (GenCos)• 11 Distribution & Marketing Companies (DisCos) • 1 Transmission Company (TransCo)

• Assets of Interest to LASG• Eko Electricity Distribution Company Plc• Ikeja Electricity Distribution Company Plc• Ijora Thermal Power Station

• Despite massive investment in electricity infrastructure by the FGN• Only achieved generation of barely 3,200MW – Dec 2010 • Compared with target of 5,379MW

• President Jonathan launched Sector Reform Roadmap – 26 August 2010

Nigeria: Power Sector Background

9

• Critical Enablers

• Multi-Year Tariff Order (MYTO) – 2008 -2013

• Nigerian Bulk Electricity Trading Company (NBETC)

• Power Purchase Agreement (PPA)

• Credit Enhancement & Risk Guarantee (FGN & World Bank)

• Nigerian Electricity Liability Management Company (NELMCO)

• Gas Supply & Purchase Agreement (GSPA)

• New commercial Multi-Year Tariff Order (MYTO)

• 5-Year tax holiday

• Duty exemption for equipment for gas fired GenCos

• Partial Risk Guarantees (PRGs) for GenCos

• Disco Tariffs to be supported by PRGs

• Labour liabilities to be resolved before handover

• NELMCO to take over stranded liabilities

•World Bank MIGA instrument to insure against political risk

Privatisation - Investment Incentives

10

Captive Power Solutions in Lagos State

• AES Nigeria a subsidiary of AES USA was the project sponsor responsible for the implementation of the project

• The project is an Independent Power Project

• It operates nine (9) barge-mounted gas turbines that produce 270MW

• Raised above 120 million US dollars to refinance part of project cost and total project cost was in excess of 200mn US dollars

• Other captive power projects include Akute/ Adiyan Water works 12.15 MW, gas-fired

• Alausa 11.7MW dual-fired plant (gas and diesel)

• Island Power 9.7MW plant commissioned in 2011 (gas-fired with diesel back up)

11April 19, 2023 11

12

• Establish, clarify and consistently apply the legal and policy framework. PPPs depend heavily on contracts that are effective and enforceable.

• Use legal terms and approaches, where possible, that are familiar to the international private sector

• Clear investment plans which, demonstrate both potential project benefits and fit with national plans, will help ensure stakeholder buy-in

• Underlying economics of potential PPP projects should be attractive to the private sector - avoid sending out wish lists of disconnected projects

• Establish a clear and consistent PPP process map that investors can easily reference and access to understand the processes

• A PPP unit within with relevant commercial and legal skills can send a powerful signal to the private sector about the government’s competence and seriousness of intent

• Capitalize on the experience of others (private/public groups) who have managed similar processes to enhance efficiency

Establishing a successful PPP programme

Conclusion• PPPs have emerged as a viable and growing investment vehicle across SSA

with particularly high demand in power, public transport, water and sanitation. Less successful in social infrastructure.

• Major constraint to growing the PPP market is a lack of technical skills in finance, legal, and engineering which limits quality of project preparation and bankability.

• There is considerable diversity across African countries in terms of their readiness for PPP procurement; Capacity Building and Technical Assistance must be tailored for different country contexts

• In the Energy sector, Nigeria has embarked on am ambitious Power Sector reform programme which depends on the ability of key institutions to work together to resolve the huge power deficit.

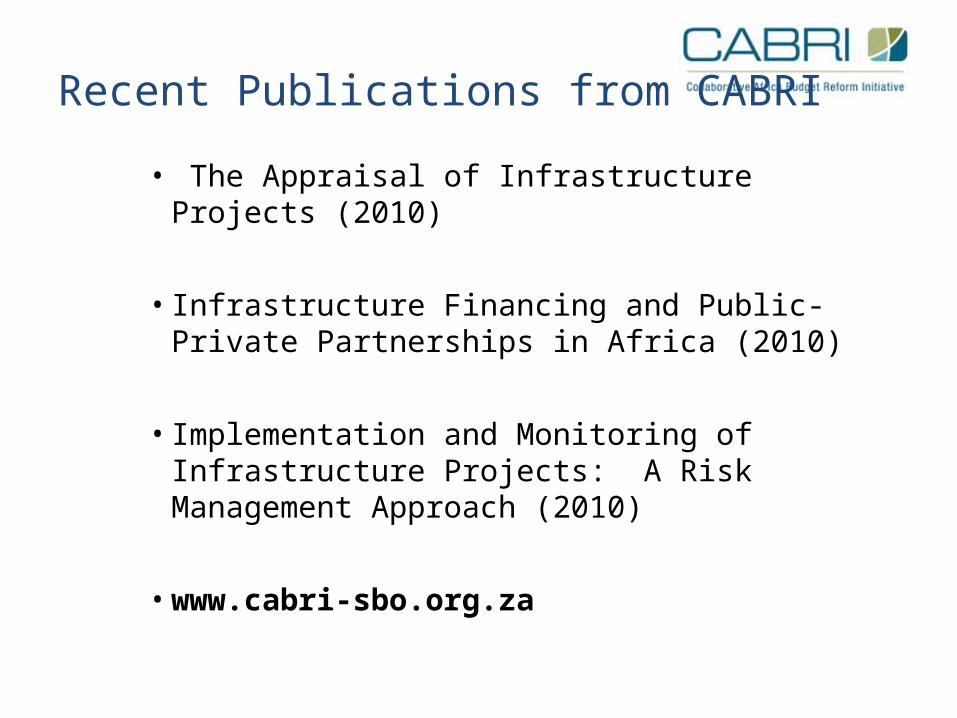

Recent Publications from CABRI

• The Appraisal of Infrastructure Projects (2010)

• Infrastructure Financing and Public-Private Partnerships in Africa (2010)

• Implementation and Monitoring of Infrastructure Projects: A Risk Management Approach (2010)

• www.cabri-sbo.org.za