Embed Size (px)

Citation preview

Cotton after Covid

Request a Trial

Not an Agrimoneyreader yet?

AN AGRIMONEY REPORT

by Gary MeadAgrimoney Lead Analyst

JULY 2021

Cotton’s story for 2020-22 is al l about recovery in demand for cot ton’s pr imary uses inapparel and text i les.Apparel demand held up better than expected and has cont inued to improve as Covid-19 fears have retreated and economies have recovered but th is largely returns us tothe posi t ion pre-pandemic. Longer term cotton faces chal lenges der iv ing f rom cl imate change quest ions.In the very long-term – out to 2039 – the OECD projects that supply growth wi l lmarginal ly outpace that of demand.Macroeconomic factors – economic growth, inf lat ion, loose monetary pol icy by centralbanks – wi l l heavi ly inf luence consumer demand and hence the cotton pr ice. Whi le‘ r isk-on’ has dominated so far in 2021, doubts remain about how effect ively thepandemic has been repressed.Cotton futures have r isen by more than 75% since the low of 2020 to around 90 centsper pound. This is st i l l far below the 2011 spike of above $2 per pound.Global cot ton stocks for 2021-22 are predicted to fa l l to their lowest in three years.The pr ice out look remains much more skewed to a repeat of 2011’s spike than aretreat to 2020’s low.

EXECUTIVE SUMMARY

2

COTTON POST-COVID-19

The immediate background to cot ton’sprospects th is year is undoubtedly Covid-19;but longer- term i t might be water that has thebigger impact. As concerns about c l imatechange r ise higher on the pol i t ical agenda,cotton’s water use, and issues such assustainable cot ton, wi l l come into sharperfocus.

In the very long term, the out look is one ofsupply marginal ly exceeding demand. TheOrganisat ion for Economic Cooperat ion andDevelopment (OECD) forecasts that globalcot ton product ion wi l l grow by 1.5% a yearand by 2039 with reach 30m tonnes. Butconsumption over the same per iod i t projectswi l l grow at the s l ight ly lower level of 1.3% ayear (1). In the intervening 18 years manyfactors can throw such long-term forecasts of fcourse.

Cl imate change is one such factor. There arevast ly di f ferent est imates as to how much andwhat type of water cot ton product ion requires.According to a report publ ished in June thisyear (2) “ the [g lobal ] cot ton system wi l l beforced to change in the face of the dramat icchanges that our warming cl imate wi l lcatalyse…The vast major i ty of cot ton growingregions wi l l be exposed to some degree ofmeteorological drought by 2040 and waterscarci ty is set to be one of the mostsigni f icant c l imate r isks for the wor ld’s mostproduct ive cot ton growing regions…”

Few now bel ieve that the 2015 Par is Cl imateAgreement to hold global temperature r isewel l below a 2ᵒ Cent igrade above pre-industr ia l levels can be achieved. On theother hand whi le agr icul ture accounts formore than 70% of global water use, cot ton isresponsible for just 3% of that (3) . Moreover,cot ton is highly to lerant of drought.

(1) https://www.oecd-ilibrary.org/sites/630a9f76-en/index.html?itemId=/content/component/630a9f76-en(2) http://www.acclimatise.uk.com/wp-content/uploads/2021/06/Cotton2040-GAReport-FullReport-highres.pdf

(3) https://cottontoday.cottoninc.com/wp-content/uploads/2020/06/Cotton-Incorporated-Fact-Sheet-CottonWater_Final-Approved_06.22.20-1.pdf

3

But for 2020-22 cotton’s story is al l about thenegat ive impact of the global coronaviruspandemic, how apparel demand survived theeconomic impact, and how economies wi l lemerge from the rubble created bycoronavirus and the way governments deal twi th i t .

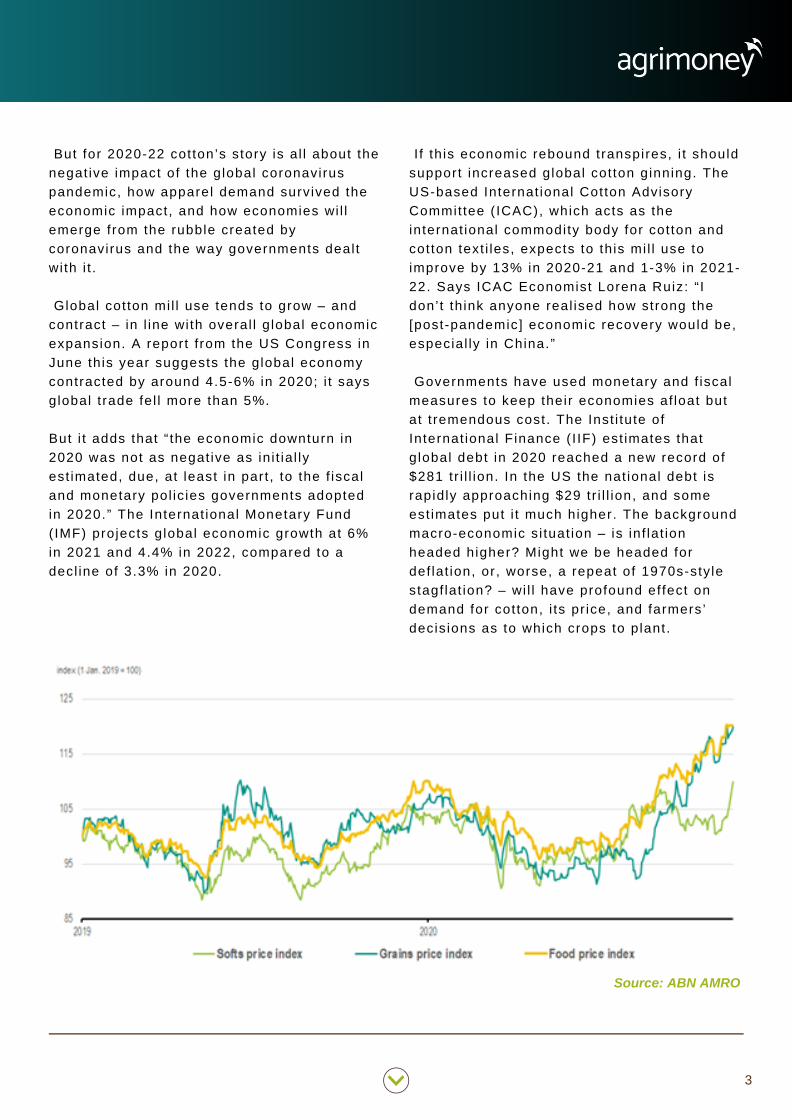

Global cot ton mi l l use tends to grow – andcontract – in l ine wi th overal l g lobal economicexpansion. A report f rom the US Congress inJune this year suggests the global economycontracted by around 4.5-6% in 2020; i t saysglobal t rade fel l more than 5%.

But i t adds that “ the economic downturn in2020 was not as negat ive as in i t ia l lyest imated, due, at least in part , to the f iscaland monetary pol ic ies governments adoptedin 2020.” The Internat ional Monetary Fund(IMF) projects global economic growth at 6%in 2021 and 4.4% in 2022, compared to adecl ine of 3.3% in 2020.

I f th is economic rebound transpires, i t shouldsupport increased global cot ton ginning. TheUS-based Internat ional Cotton AdvisoryCommit tee ( ICAC), which acts as theinternat ional commodity body for cot ton andcotton text i les, expects to th is mi l l use toimprove by 13% in 2020-21 and 1-3% in 2021-22. Says ICAC Economist Lorena Ruiz: “ Idon’ t th ink anyone real ised how strong the[post-pandemic] economic recovery would be,especial ly in China.”

Governments have used monetary and f iscalmeasures to keep their economies af loat butat t remendous cost. The Inst i tute ofInternat ional Finance ( I IF) est imates thatglobal debt in 2020 reached a new record of$281 tr i l l ion. In the US the nat ional debt israpidly approaching $29 tr i l l ion, and someest imates put i t much higher. The backgroundmacro-economic s i tuat ion – is inf lat ionheaded higher? Might we be headed fordef lat ion, or , worse, a repeat of 1970s-sty lestagf lat ion? – wi l l have profound ef fect ondemand for cot ton, i ts pr ice, and farmers’decis ions as to which crops to plant.

Source: ABN AMRO

4

The pr ices of a l l commodit ies dippeddramatical ly in ear ly 2020 as wider economicact iv i ty ground to a hal t ; the BloombergCommodity Index, which t racks 23 commodityfutures markets, h i t an al l - t ime low in Apr i l2020. But many, including agr icommodit ies,rose strongly in the second hal f of the yearand have cont inued to be buoyant so far in2021, thanks to a combinat ion of inherentsupply/demand fundamentals andmacroeconomic factors such as supply-chainbott lenecks that have disrupted supply andfuel led wholesale and retai l inf lat ion.

Corn and soybean futures have this yearreached six-year highs, whi le palm oi l br ief lytouched 10-year highs in January. Accordingto Internat ional Banker (4) in March this year:“With substant ia l money-supply expansionthroughout much of the wor ld, u l t ra- low ratesand f iscal st imulus al l s igni f icant ly boost inginf lat ion expectat ions…money should cont inuef lowing into agr icul tural commodit ies th isyear. And with Chinese demand expected tocont inue recover ing strongly, a long withpersistent notable supply chal lenges, pr icesfor agr icul tural commodit ies are expected tocl imb throughout much of 2021.”

I t was thus fai r ly predictable that sales ofcot ton-based apparel and text i les would fa l ldur ing the ear ly days of the pandemic.According to f igures f rom ICAC, the value ofglobal apparel exports fe l l by 10% to $423bi l l ion in 2020 year-on-year, but manymanufacturers and brands adroi t ly p ivotedmuch of their sales f rom in-store to onl ine.This t rend to onl ine consumer spending wi l lendure long af ter coronavirus is a distantnightmare. According to Cotton Incorporated,69% of consumers surveyed in China, 45% inthe US, and 37% in Mexico, expect topurchase at least hal f of their apparel onl inein the future.

Demand for apparel has thus weathered theCovid-19 storm much better than in i t ia l lyfeared. Bangladesh, for example, the wor ld’ssecond-biggest apparel producer (af terChina), said i ts garment exports rose by 13%year-on-year in i ts 2020-21 f inancial year butwere st i l l 7% lower than the pre-pandemicyear of 2018-19 (5).The largest export ingcountr ies of apparel are also the biggestconsumers of cot ton. Three countr ies —China, India, Pakistan — account forf ract ional ly more than 60% of global cot tonmi l l use and col lect ively saw 74% of the dropin cot ton demand in 2019-20.

(4) https://internationalbanker.com/brokerage/the-outlook-for-commodities-in-2021/(5) https://www.reuters.com/world/asia-pacific/bangladesh-exports-up-15-global-demand-garments-rebounds-2021-07-06/

Source: ICAC

5

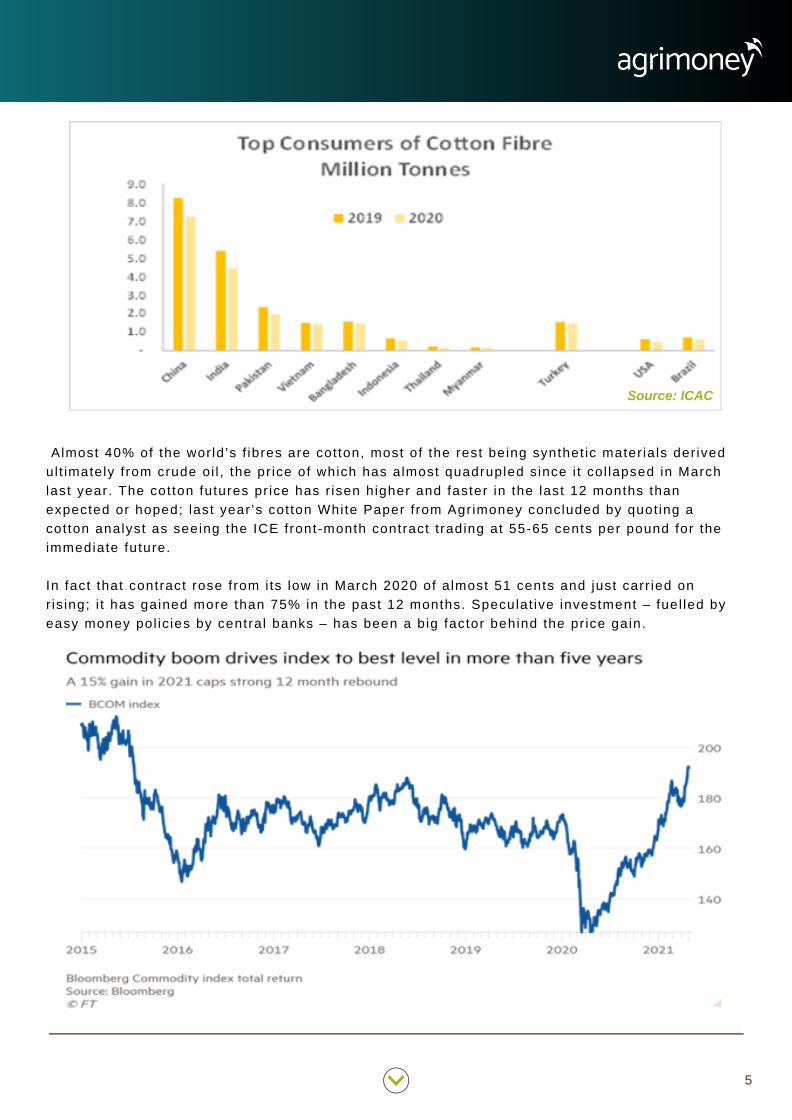

Almost 40% of the wor ld’s f ibres are cot ton, most of the rest being synthet ic mater ia ls der ivedul t imately f rom crude oi l , the pr ice of which has almost quadrupled since i t col lapsed in Marchlast year. The cotton futures pr ice has r isen higher and faster in the last 12 months thanexpected or hoped; last year ’s cot ton White Paper f rom Agrimoney concluded by quot ing acotton analyst as seeing the ICE front-month contract t rading at 55-65 cents per pound for theimmediate future.

In fact that contract rose from i ts low in March 2020 of a lmost 51 cents and just carr ied onr is ing; i t has gained more than 75% in the past 12 months. Speculat ive investment – fuel led byeasy money pol ic ies by central banks – has been a big factor behind the pr ice gain.

Source: ICAC

6

At around 90 cents per pound the cottonpr ice is st i l l far below i ts 20-year peak ofmore than 212 cents of February 2011, butnevertheless i t ’s been a remarkableturnaround.

The spark for 2011’s spike – which pushed thepr ice to i ts highest in 140 years – fo l lowed asigni f icant decl ine f rom March 2008 to Marchthe fol lowing year, when the pr ice fe l l by32.5%.

China’s consumption of more cotton than i tproduced dur ing 2009-10, heavy f loods inPakistan, and the stocks-to-use rat io fa l l ing tojust 12% for 2010-11, i ts lowest s ince 1925,al l helped to fuel the pr ice spike.

China bought 80% of India’s cot ton exports inthe 2011-12 season; by March 2012 Indiabanned cotton exports. For the 2011-12season the USDA est imated that global cot tondemand outstr ipped product ion by 1.3m bales.

Investors in cot ton futures wi l l have takennote of the USDA report f rom February th isyear, which projected that global consumptionwi l l exceed product ion, even as product ionwi l l r ise by almost 5%, and reduce globalstocks by 3.2m bales, more than twice thesupply short fa l l of 2011-12 (6).

This potent ia l ly bul l ish est imate wasreinforced by the USDA in June, when i t saidthe 2021-22 season is l ikely to see “adecrease in global cot ton ending stocks asmi l l use exceeds product ion for the secondconsecut ive season. World stocks areprojected at 89.3m [480-pound] bales…thelowest in 3 years…

China is forecast to account for 40% of the2021-22 global cot ton stock total” wi th India,Brazi l and the US holding (respect ively) 18%,14% and 3%. The USDA adds that globalcot ton product ion wi l l be 5% up year-on-yearat a lmost 119m bales, whi le cot ton mi l l usewi l l r ise to 122.5m bales, 4% higher on theprevious year.

The USDA said: “Along with lower stocks, ar is ing cotton demand is expected to keep2021-22 world cot ton pr ices above recentlevels.” ICAC says ending stocks wi l l decl inefor the f i rst t ime in four years to stand at20.96 mi l l ion tonnes in 2020-21— a levels imi lar to 2015-16. Ending stocks are forecastto decl ine fur ther in 2021-22 to 20.77 mi l l iontonnes, as mi l l use is expected to exceedproduct ion.

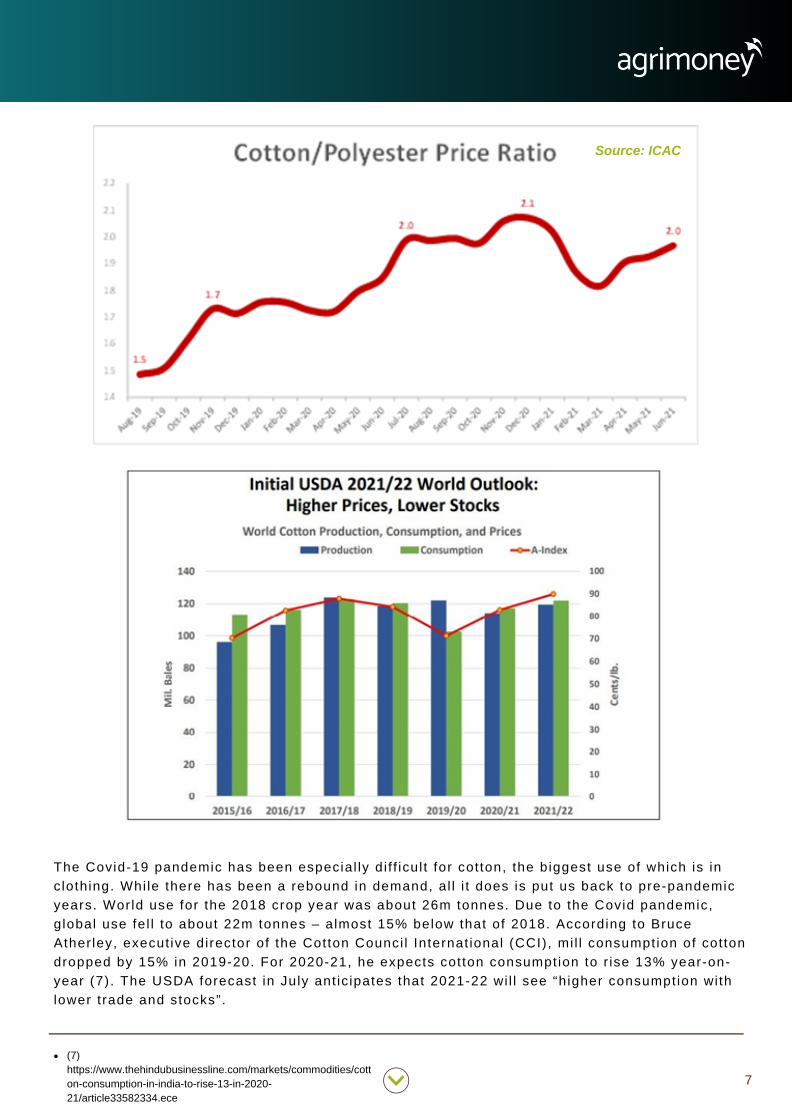

As Lorena Ruiz points out, the majorcompet i tor for cot ton is synthet ic f ibres.“We’re always compet ing against polyester. Ith ink i t ’s very important that people keep aneye on polyester pr ices, and how big is thegap between those and cotton pr ices. I f wesee a big di f ference and cotton pr ices r isesigni f icant ly above those for synthet ic f ibres,then what is the incent ive for cot tonproducers?”

The 2011 cotton pr ice spike encouragedspinners to reduce the proport ion of cot ton intheir b lends in favour of synthet ic f ibres.China is the largest producer of synthet icf ibres. I t produces around 63m tonnes ofpolyester and around 4m tonnes of v iscose.

(6) https://www.usda.gov/sites/default/files/documents/cotton-outlook.pdf

7

The Covid-19 pandemic has been especial ly di f f icul t for cot ton, the biggest use of which is inclothing. Whi le there has been a rebound in demand, al l i t does is put us back to pre-pandemicyears. World use for the 2018 crop year was about 26m tonnes. Due to the Covid pandemic,global use fel l to about 22m tonnes – almost 15% below that of 2018. According to BruceAther ley, execut ive director of the Cotton Counci l Internat ional (CCI), mi l l consumption of cot tondropped by 15% in 2019-20. For 2020-21, he expects cot ton consumption to r ise 13% year-on-year (7). The USDA forecast in July ant ic ipates that 2021-22 wi l l see “higher consumption withlower t rade and stocks”.

(7)https://www.thehindubusinessline.com/markets/commodities/cotton-consumption-in-india-to-rise-13-in-2020-21/article33582334.ece

Source: ICAC

8

About 60% of women’s c lothing i tems containcotton f ibres, wi th 40% made ent i re ly f romcotton; for men, about 75% of c lothingcontains some cotton (8). According to areport f rom the consul tant McKinsey theaverage market capi ta l isat ion of apparel ,fashion, and luxury players fe l l by almost 40%between the start of January and March in2020. In McKinsey’s v iew revenues for theglobal fashion industry (apparel and footwear)contracted by 27-30% in 2020 year-on-year. I texpects the overal l apparel industry mightshow tepid growth of 2-4% in 2021, comparedto 2019.

Onl ine apparel sales enjoyed a red-hotpandemic; in the US such sales grew almost22% in 2020 according to one est imate, whi leof f l ine apparel sales (mainly through stores)fel l a lmost 40% (9). Onl ine apparel sales inthe US accounted for 46% of total apparelsales in 2020, around a th i rd higher than in2018.

According to Mastercard, sales of c lothingonl ine rose by 47% year-on-year in Februarythis year (10). Without the internet anddigi t ised shopping the cotton market – andmany others – would have been in adesperate posi t ion.

(8) https://oureverydaylife.com/characteristics-of-polyester-cotton-12508478.html(9) https://www.digitalcommerce360.com/article/online-apparel-sales-us/

(10) https://www.cnbc.com/2021/03/09/mastercard-almost-75percent-of-apparel-sales-were-made-online-last-month.html(11) https://www.ers.usda.gov/webdocs/outlooks/101610/cws-21g.pdf?v=5843.6

2021 - 2022 SUPPLY AND DEMAND

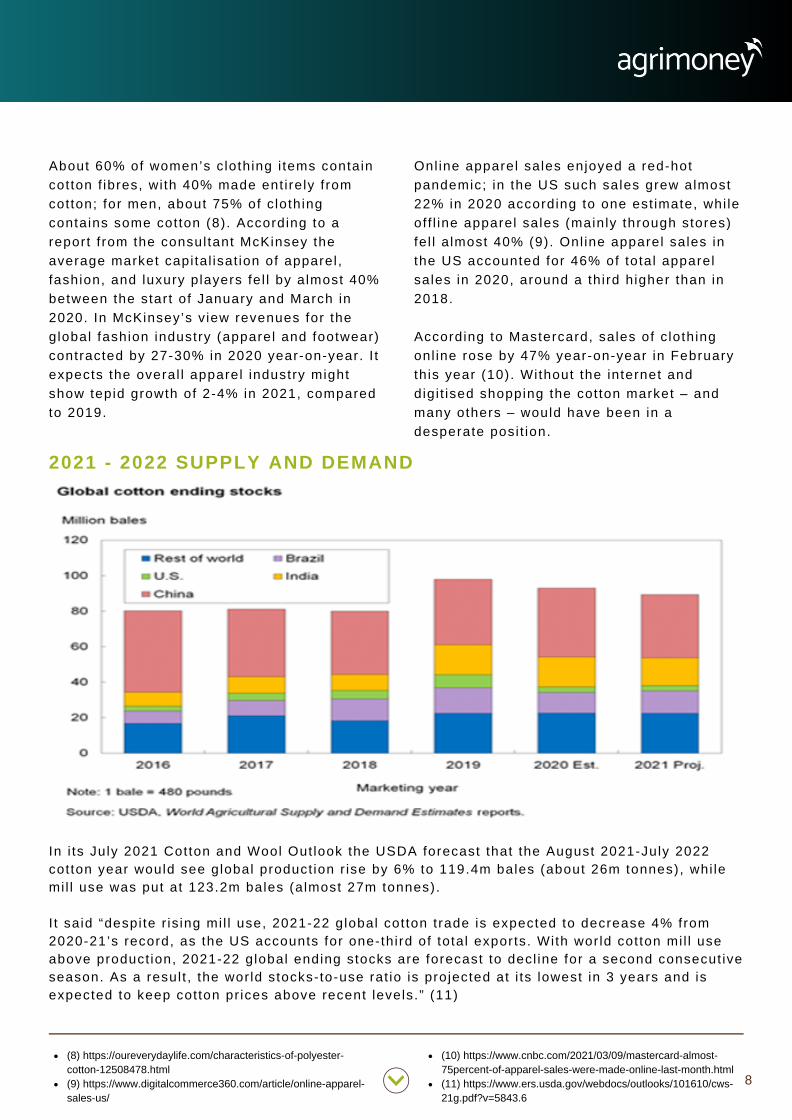

In i ts July 2021 Cotton and Wool Out look the USDA forecast that the August 2021-July 2022cotton year would see global product ion r ise by 6% to 119.4m bales (about 26m tonnes), whi lemi l l use was put at 123.2m bales (almost 27m tonnes).

I t said “despi te r is ing mi l l use, 2021-22 global cot ton t rade is expected to decrease 4% from2020-21’s record, as the US accounts for one-third of total exports. With wor ld cot ton mi l l useabove product ion, 2021-22 global ending stocks are forecast to decl ine for a second consecut iveseason. As a resul t , the wor ld stocks-to-use rat io is projected at i ts lowest in 3 years and isexpected to keep cotton pr ices above recent levels.” (11)

9

Global ending stocks for 2021-22 are put atjust above 19m tonnes, 4% lower than theprevious year. US product ion for 2021-22 isseen at a lmost 4m tonnes, 22% higher year-on-year. Growing condi t ions for much of theUS cotton areas have been good; as of 11July 56% of the cot ton area was rated “good”or “excel lent” compared with 44% by this datein 2020; just 9% was rated “poor” or “verypoor” compared with 26% last year.

2021-22 cotton product ion expectat ions by theUSDA are for larger crops, except for China,with India expected to nudge China from thetop producer s lot by producing around 6.3mtonnes and China 5.8m tonnes, 9% loweryear-on-year. The world 2021-22 stocks-to-use rat io is seen by the USDA at 71%, 6%down year-on-year.

China is the wor ld’s second- largest cot tongrower, represent ing about 25% of globalcot ton product ion. I t ’s a lso the world’s largestcotton spinner, account ing for about a th i rd ofthe wor ld’s raw cotton f ibre consumption, andthe world’s largest producer and exporter ofcot ton fabr ic and apparel .

I ts 2020-21 product ion is l ikely to have beenclose to 6m tonnes, unchanged from theprevious year, whi le i ts consumption wasabove 8m tonnes, almost 9% higher year-on-year.

China has started sel l ing around 600,000tonnes (2.75m bales) f rom state reserves;these sales wi l l last unt i l October. The USDAsaid in July that total stocks are est imated tobe 1.5-1.7m tonnes of foreign cotton(pr imari ly U.S. and Brazi l ian), 1.1m tonnes ofChinese cotton f rom the 2011-2013 crops, and375,000 tonnes from the 2019 crop.

The size of th is season’s of fer ing is onlysl ight ly higher than 2020’s sales and wel lbelow the 1m tonnes sold in 2019.

In recent decades, reforms to cot ton pol ic iesimplemented by the Chinese governmentshi f ted the main cot ton-producing area fromthe Yel low River basin to Xinj iang province.Today Xinj iang province is home to almost90% of Chinese cotton product ion.

In January 2021 the US Custom and BorderProtect ion (CBP), a federal agency, issued aWithhold Release Order (WRO) on cottonproducts f rom the Xinj iang region, fo l lowingwidespread accusat ions of genocide againstthe Uighur ethnic minor i ty group who largelyl ive in Xinj iang province; an accusat ion that isregular ly rebutted by Bei j ing.

The Xinj iang Product ion and Construct ionCorps (XPCC) is responsible for much of thecotton that is grown in the region. The XPCC,a state-af f i l iated ent i ty, was in i t ia l ly foundedfrom mi l i tary uni ts.

The r isk of exposure to Xinj iang cotton mainlystarts wi th fabr ics, as f ibre der iv ing f romXinj iang is blended with other f ibres f romother sources. I t has been est imated that asmuch as 20% of al l cot ton goods sold aroundthe world may contain some cotton fromXinj iang.

The WRO thus seems to us a blunt instrumentand one that cannot be pol iced ef fect ively astracking ‘Xinj iang cotton’ through internat ionalsupply chains is impossible.

10

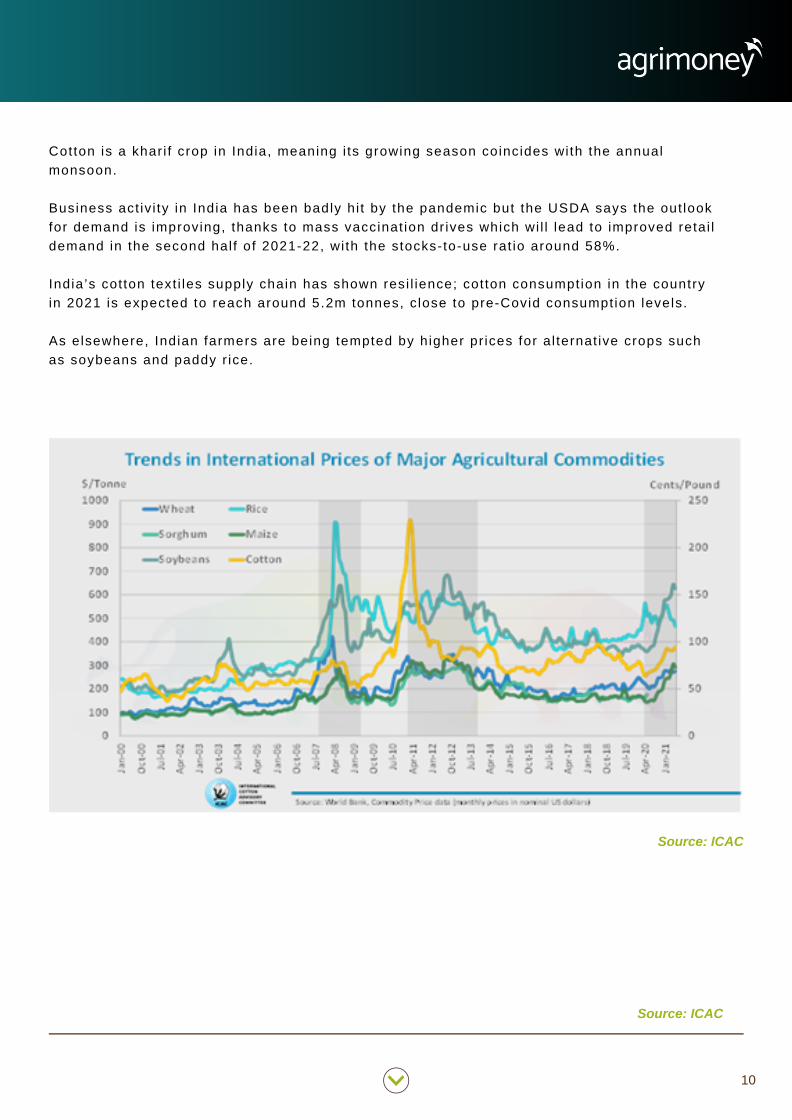

Cotton is a khar i f crop in India, meaning i ts growing season coincides with the annualmonsoon.

Business act iv i ty in India has been badly hi t by the pandemic but the USDA says the out lookfor demand is improving, thanks to mass vaccinat ion dr ives which wi l l lead to improved retai ldemand in the second hal f of 2021-22, wi th the stocks-to-use rat io around 58%.

India’s cot ton text i les supply chain has shown resi l ience; cot ton consumption in the countryin 2021 is expected to reach around 5.2m tonnes, c lose to pre-Covid consumption levels.

As elsewhere, Indian farmers are being tempted by higher pr ices for al ternat ive crops suchas soybeans and paddy r ice.

Source: ICAC

Source: ICAC

11

PRICE OUTLOOK

Many extraneous factors could exert inf luenceover the cotton pr ice dur ing the next 12months.

I ts fate hangs part ly on US/China relat ions;President Biden has so far ta lked toughregarding China but there’s been no of f ic ia linformat ion as to whether the t rade deals igned between his predecessor and Chinastands or wi l l be extended beyond this, i tssecond year.

The at tempt by the US to spurn Xinj iang-produced cotton may gain some tract ionamong consumers, a l though i t is unl ikely thatt racking and ver i f icat ion techniques wi l ldevelop suff ic ient rel iably to ident i fy suchcotton.

Another factor to watch wi l l be the inevi tabledevelopment of Covid-19 var iants, and howgovernments may respond to them by perhapsimposing fresh ‘ lockdown’ measures that wi l lnegat ively impact economic recovery.

Central bank monetary pol ic ies wi l l a lso beimportant. Current ly the US Federal Reserveand the European Central Bank have nai ledtheir colours to the ‘ t ransi tory inf lat ion’ mast;they are anxious not to r isk st i f l ing economicrecovery by rais ing interest rates prematurely.

This factor is cr i t ical to consumer conf idenceand thereby demand for products such asapparel and hence cotton demand.

And then there are ‘b lack swan’ events thatcan surpr ise us al l . As we have seen from therecent f loods in China and Germany, badweather can disrupt assumptions and createunexpected chaos.

Nevertheless, cot ton pr ices rose to more than90 cents per pound in February/March 2021,which is when farmers in the Northernhemisphere made plant ing decis ions for the2021-22 season.

As of the end of June, cot ton sowing had beencompleted in the US, China, Pakistan and thenorthern region of India, which togetheraccount for near ly 70% of the wor ld 's cot tonoutput.

The vast major i ty of 2021-22’s cot tonproduct ion is largely in the ground. Whi le thearea planted to cot ton this year is largely aknown quant i ty, Lorena Ruiz points out thatweather can have a great inf luence over thef inal crop.

The fundamental supply-demand si tuat ion forcotton for 2021-22 is current ly t ighter than i thas been for several years.

Given a sol id economic recovery in westernmarkets and cont inued ‘easy money’ pol ic iesby leading central banks, the out look remainsmuch more skewed to a repeat of 2011 than aretreat to 2020.

Agrimoney would like to acknowledge the invaluable assistance of Mike McCue, Lorena Ruiz and the rest ofthe staff of the International Cotton Advisory Committee (ICAC) in the preparation of this report.

46

Our analysts are independent and steeped in years of industryknowledge, with an enviable list of contacts, an innate understandingof the sector and a global view, giving you 3 key ways to impact yourbusiness:

1. Make the best decisions for your businessThe impacts of key developments can make or break, and so it’s vitalthat you have the tools you need to quickly make the best decisions,or to verify your own research for your business, to their make themost of, or to minimise the effect of market factors.

2. Trade more intelligentlyChoose where and when to trade across the commodities market,through using our unbiased and independent reporting, distillingwhat’s happening, to give you independent analysis of what’shappening in this global sector.

3. Give yourself the edgeReact quickly to the ever-changing conditions throughout the industry,as they happen, with the fastest, most accurate and unbiased sourceof news, pricing analysis and opinion, delving beyond the hype to findout what really matters.

We know that you can’t afford to miss out on critical market-moving newsand analysis. Agrimoney is a subscription service giving you the news,analysis and commentary you need on the commodities and agribusinesssector.

What is Agrimoney?

How can Agrimoney help you?

NEWS AND ANALYSIS OF THE COMMODITY ANDAGRIBUSINESS SECTOR THAT YOU CAN TRUST.

TO FIND OUT MORE ABOUT AGRIMONEY AND BOOK YOUR FREE

TRIAL VISIT MARKETING.AGRIMONEY.COM/TRIAL

www.agrimoney.com