Embed Size (px)

Citation preview

WHAT SHOULD YOU KNOW

Buying Electricity andNatural Gas in Today'sRestructured Market

HA

ND

BO

OK

P400-00-001F

Gray Davis, Governor

SEPTEMBER 2000

CALIFORNIA ENERGY COMMISSION

STATE OF CALIFORNIA

ENERGY COMMISSION

20001975

CALIFORNIA ENERGY COMMISSION

Prepared under contract # 400-96-019

Michael S. Sloss, Office Manager

NONRESIDENTIAL OFFICE

Scott W. Matthews, Deputy Director

ENERGY EFFICIENCY DIVISION

Steve Larson,Executive Director

William J. Keese, Chairman

Commissioners:Michal C. MooreRobert A. LaurieRobert PernellArthur H. Rosenfeld

Mary D. Nichols,Secretary for Resources

WHAT SHOULD YOU KNOW

Buying Electricity and

Natural Gas in Today's

Restructured MarketH

AN

DB

OO

K

P400-00-001F

Gray Davis, Governor

SEPTEMBER 2000

CALIFORNIA ENERGY COMMISSION

STATE OF CALIFORNIA

ENERGY COMMIS

SION

2000

1975

Prepared for the

California Energy CommissionEnergy Efficiency DivisionNonresidential Office

By

Henwood Energy Services, Inc.Sacramento, CAContract # 400-96-019

U P D A T E S T O H A N D B O O K

State regulators and lawmakers are occasionally modifying the rules governing directaccess to improve the operation and function of the energy markets. These adjustmentscoupled with electricity supply and transmission line issues can create a volatile energyenvironment. Being well informed and aware of the changes will help you decide on thebest energy-purchasing and usage strategy for your agency.

To keep you updated on these changes, the California Energy Commission will post onour website, amendments to this document that highlight the most up-to date informationregarding the restructured electricity and natural gas markets.

For this handbook and amendments, visit the California Energy Commission website at:www.energy.ca.gov/reports/efficiency_handbooks/index.html

LEGAL NOTICE

This report was prepared as a result of work sponsored by the California EnergyCommission. It does not necessarily represent the views of the California EnergyCommission, its employees, or the State of California. The California EnergyCommission, the State of California, its employees, contractors, and subcontractors makeno warranty, express or implied, and assume no legal liability for the information in thisreport; nor does any party represent that the use of this information will not infringe uponprivately owned rights.

Procuring Electricity and Natural Gas in the Restructured Markets

Acknowledgements

This document, “What You Should Know: Buying Electricity and Natural Gas in Today’sRestructured Market” was prepared by Henwood Energy Services, Incorporated (HESI) for theCalifornia Energy Commission. It is primarily written for public agencies to help themunderstand their energy procurement options. However, others may benefit from the informationprovided. The primary authors of this report from HESI are Douglas Davie, Kristen Kelley,George Givens, and Jon Collins. The California Energy Commission staff responsible for thedevelopment of this handbook are Daryl Mills, Virginia Lew, and Elizabeth Shirakh.

The California Energy Commission and HESI are grateful for the thoughtful comments andsuggestions provided by the following: Antione Abu-Shabakeh, City of Riverside; Bill Knox,Rick Buckingham (now with the Energy Commission), Jonathan Teague, and Marshall Clarke,California Department of General Services; Greg Cook, Northern California Power Agency;Dave Finigan and Eugene Leong, Association of Bay Area Governments; Bud Fish, County ofRiverside; Ray Giles, Community College League; Yvonne Hunter, League of California Cities;Kevin Kelley, City of Palo Alto Utilities; Darren Kettle, County of San Bernardino; Jack Kreig,Modesto Irrigation District; Clay Maynard, Yuba County; Bill McCallum, Fresno Public Utilities;John Moss and Ron Munds, City of San Luis Obispo; Matthew Muniz, County of Alameda;Susan Munves, City of Santa Monica; Otto Radtke, County of Los Angeles; Michael Rochman,School Project Utility Rate Reductions (SPURR); Steve Sachs, San Diego Association ofGovernments; Dan Smith, Association of California Water Agencies; Tony Valenzuela,California State University; Scott Wentworth, City of Oakland; Kurt Kammerer, San DiegoRegional Energy Office; Rita Norton, City of San Jose; and Dennis Kahlie, City of San Diego.

The authors acknowledge California Energy Commission staff: Sylvia Bender, Maxine BottiDennis Fukumoto, Karen Griffin, Mike Jaske, Dan Nix, Monica Rudman, Tim Tutt, and RichardRohrer for assistance in editing the document; and Sue Foster for the cover design.

For information on how to obtain a copy of this report or other Commission Handbooks onEnergy Efficiency, contact the Nonresidential Building Office at (916) 654-4008. All documentscan be downloaded from the Energy Commission’s Web Site at:

www.energy.ca.gov/reports/efficiency_handbooks/index.html

Special A c k n o w l e d g e m e n t

The Commission would like to especially thank the League of California Cities for itsassistance in preparing and distributing this document.

Procuring Electricity and Natural Gas in the Restructured Markets

Procuring Electricity and Natural Gas in the Restructured Markets

TABLE OF CONTENTSI. INTRODUCTION......................................................................................................................... 1

II. IS DIRECT ACCESS RIGHT FOR YOU? KEY ISSUES TO CONSIDER............................... 3

A. DEFINE YOUR GOALS AND OBJECTIVES ........................................................................................ 3B. UNDERSTAND YOUR ENERGY USAGE PATTERNS .......................................................................... 4C. DEFINE EXPECTATIONS................................................................................................................ 7D. UNDERSTAND THE RISKS ............................................................................................................. 7

1. Price Volatility - What are common commodity pricing structures? ......................................... 72. Contract Duration - How long should my contract be? ............................................................ 83. Limits on Changing - What if I want to switch providers? ........................................................ 84. Non-Performance - What if my supplier cannot meet my needs?............................................... 85. Keeping Up With the Market – Why do I need to pay attention to the markets once a contract is

in place? ................................................................................................................................. 86. Protecting Your Interests......................................................................................................... 9

E. IS DIRECT ACCESS FOR YOU? ........................................................................................................ 9

III. YOUR ELECTRICITY CHOICES ............................................................................................ 11

A. YOUR PURCHASING OPTIONS ..................................................................................................... 111. Staying With Your Existing Utility ......................................................................................... 112. Choosing a Competitive Supplier -- Direct Access ................................................................. 123. Participating in or Creating an Aggregation.......................................................................... 134. Municipalization ................................................................................................................... 15

B. PRICING OPTIONS ...................................................................................................................... 191. Existing Regulated Rate Structure ......................................................................................... 192. New Rate Options.................................................................................................................. 19

C. METERING AND BILLING OPTIONS.............................................................................................. 201. Metering ............................................................................................................................... 212. Billing................................................................................................................................... 21

D. BUYING GREEN OR RENEWABLE ELECTRICITY ........................................................................... 22E. ENERGY EFFICIENCY AND ENERGY MANAGEMENT...................................................................... 26

1. Energy Efficiency .................................................................................................................. 262. Managing Energy Usage ....................................................................................................... 293. Choose the Best Rate Schedule .............................................................................................. 294. On Site or Distributed Generation ......................................................................................... 29

IV. COMPETITIVE POWER PROCUREMENT ........................................................................... 31

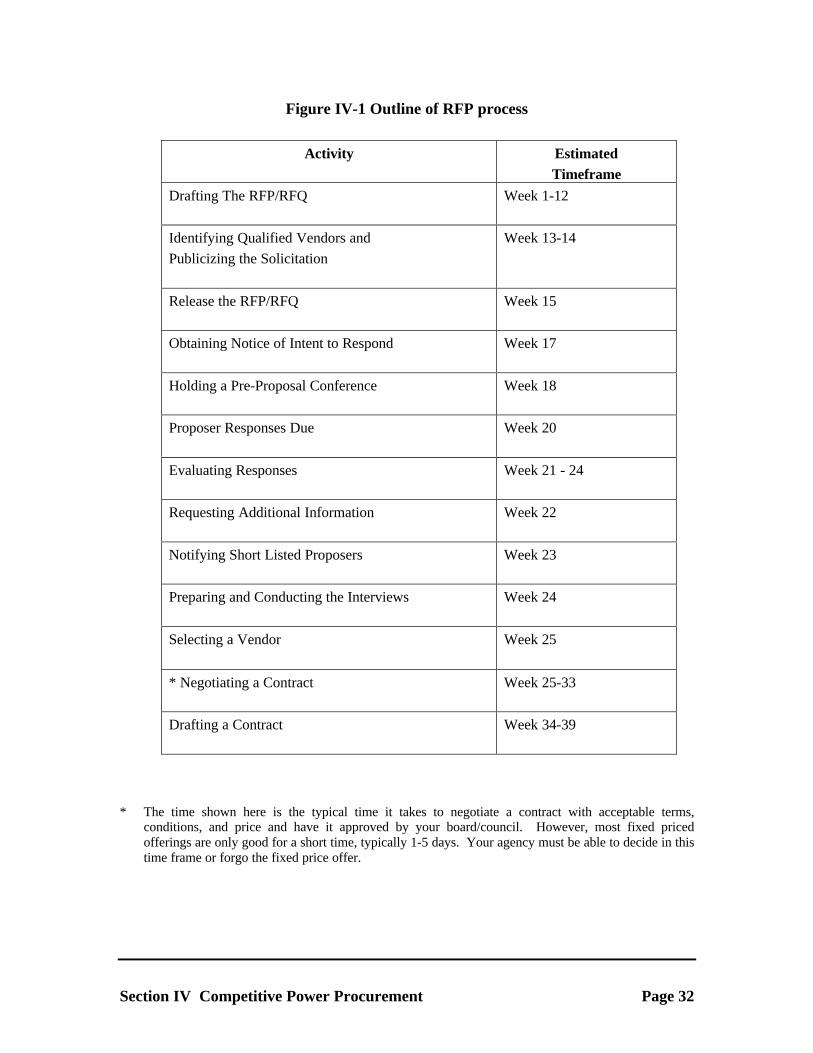

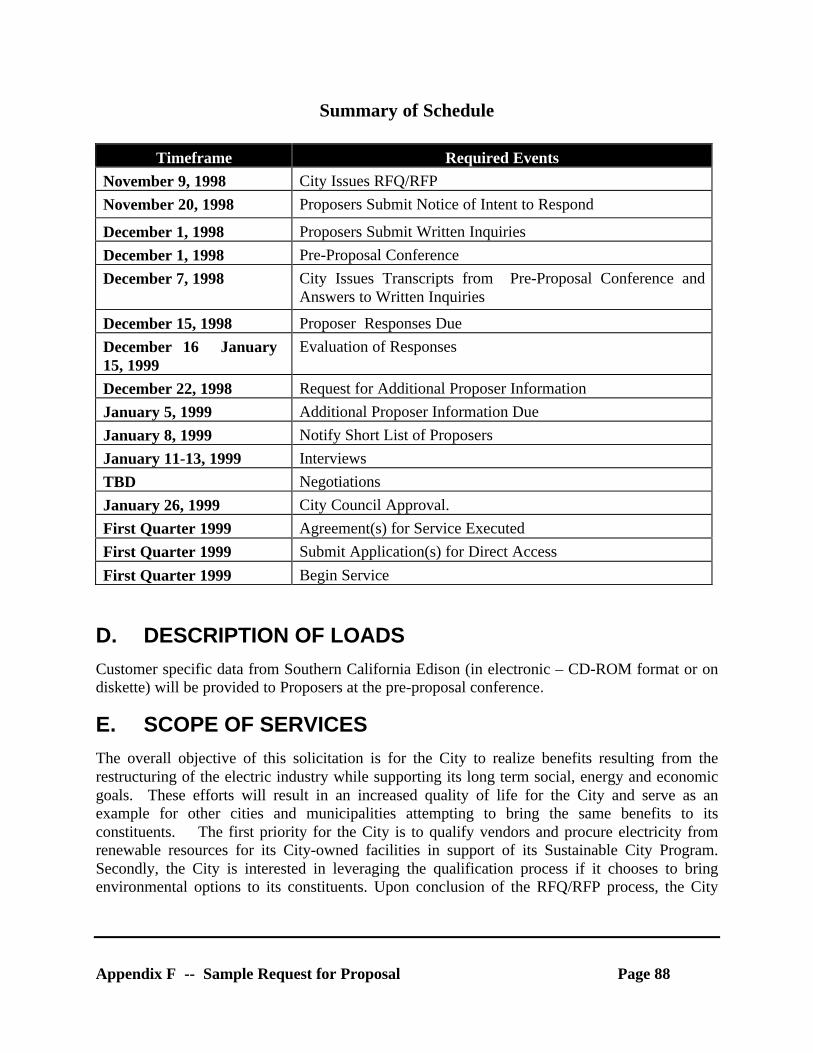

A. THE REQUEST FOR PROPOSAL/REQUEST FOR QUALIFICATIONS PROCESS ...................................... 311. Identifying Qualified Vendors................................................................................................ 312. Timing of solication process .................................................................................................. 313. Drafting the RFP/RFQ .......................................................................................................... 314. Publicizing the Solicitation.................................................................................................... 335. Obtaining Notice of Intent to Respond ................................................................................... 336. Holding a Pre-proposal Conference ...................................................................................... 337. Collecting Responses............................................................................................................. 348. Evaluating Responses............................................................................................................ 349. Requesting Additional Information ........................................................................................ 3410. Notifying Short Listed Proposers ........................................................................................... 3411. Preparing for the Interviews .................................................................................................. 3512. Conducting the Interviews ..................................................................................................... 35

B. SELECTING A VENDOR(S)........................................................................................................... 35C. NEGOTIATING TIPS .................................................................................................................... 35D. DRAFTING THE CONTRACT......................................................................................................... 36E. MANAGING THE TRANSITION FROM THE LOCAL UTILITY TO THE NEW SUPPLIER .......................... 37F. VALIDATE THE BENEFITS........................................................................................................... 37

Procuring Electricity and Natural Gas in the Restructured Markets

G. MONITOR PROJECT RESULTS AND INDUSTRY CHANGES .............................................................. 37

V. NATURAL GAS PROCUREMENT ISSUES............................................................................. 41

A. NATURAL GAS RESTRUCTURING BACKGROUND ......................................................................... 411. How Is The Market Being Restructured?................................................................................ 412. Emerging Trends................................................................................................................... 423. Components of Your Service.................................................................................................. 43

B. NATURAL GAS CHOICES ............................................................................................................ 431. Procurement Process ............................................................................................................ 442. Who Do I Buy From? ............................................................................................................ 443. Expected Savings and Risk Management................................................................................ 45

SUPPLEMENT 1 � CHANGES IN THE ELECTRICITY MARKET ............................................... 47

A. REVIEW OF CHANGES IN THE ELECTRICITY MARKET................................................................... 471. Monopoly Franchise: Prior to 1998....................................................................................... 472. Transition to Customer Choice: 1998 – 2001......................................................................... 473. Customer Choice: post 2001.................................................................................................. 49

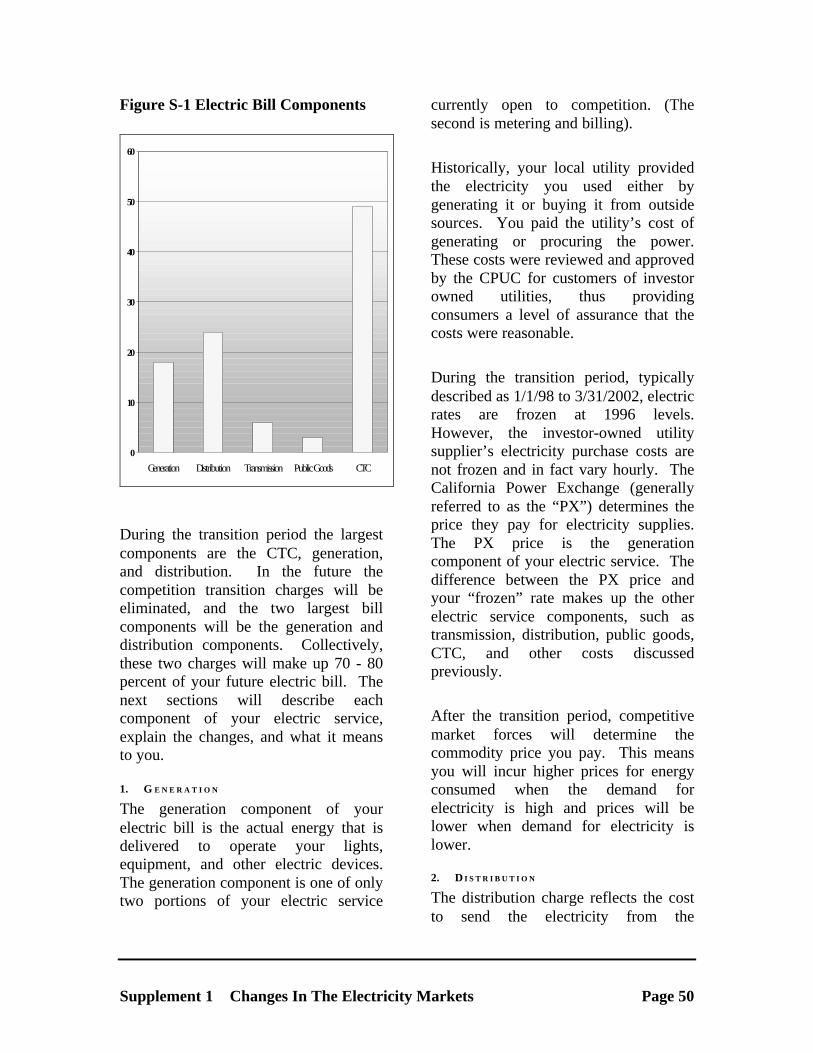

B. COMPONENTS OF ELECTRIC SERVICE.......................................................................................... 491. Generation............................................................................................................................ 502. Distribution........................................................................................................................... 503. Transmission......................................................................................................................... 514. Public Good Charges ............................................................................................................ 515. Competition Transition Charges............................................................................................ 51

C. MARKET PARTICIPANTS............................................................................................................. 531. Direct Players: Providers of Electric Service......................................................................... 532. Indirect Players: Providers of Support Services ..................................................................... 55

D. TRENDS AND ISSUES IN THE NEW MARKET ................................................................................. 571. Green Power......................................................................................................................... 572. Evolving Competition ............................................................................................................ 583. Future Issues Impacting Customer Rates............................................................................... 59

SUPPLEMENT 2 � FREQUENTLY ASKED QUESTIONS .............................................................. 61

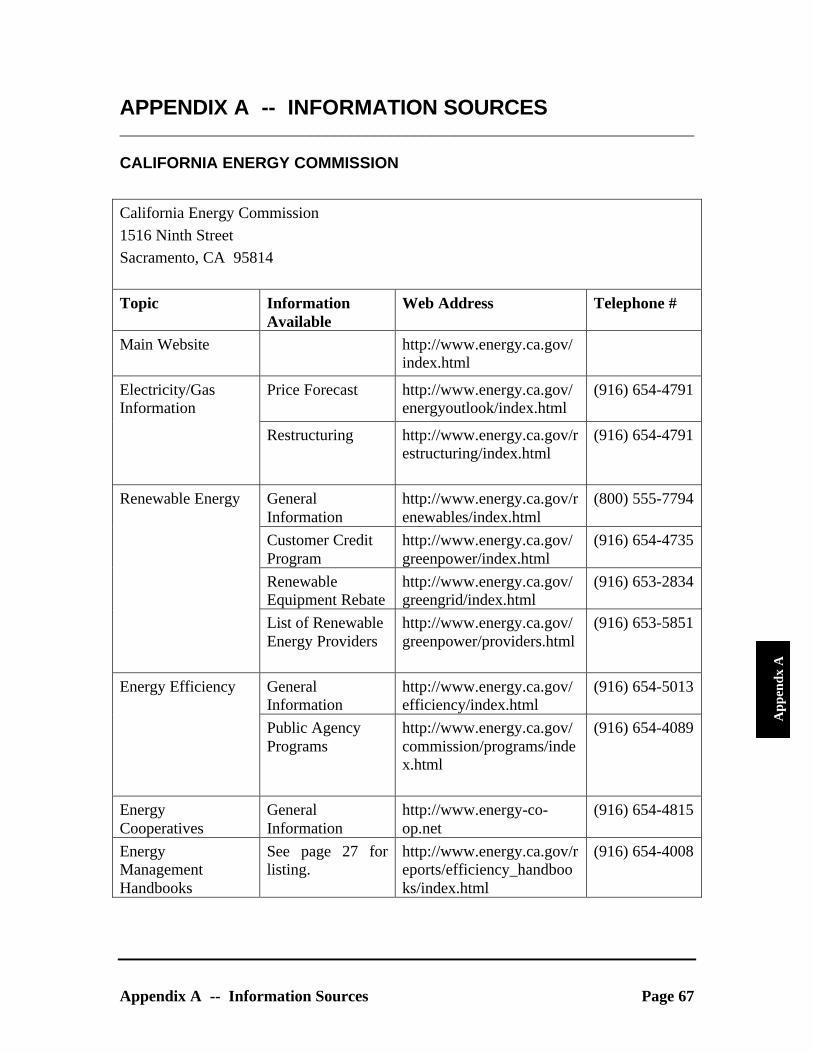

APPENDIX A -- INFORMATION SOURCES.................................................................................. 67

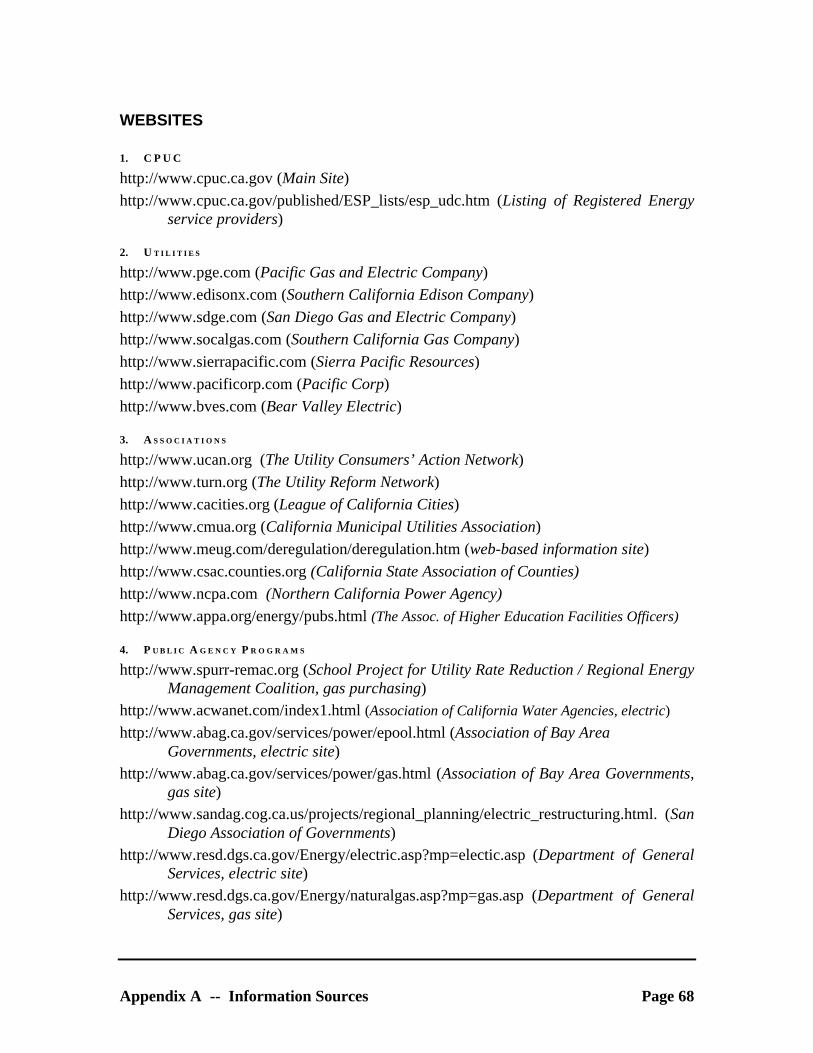

CALIFORNIA ENERGY COMMISSION ...................................................................................................... 67WEBSITES .......................................................................................................................................... 68

1. CPUC ................................................................................................................................... 682. Utilities ................................................................................................................................. 683. Associations .......................................................................................................................... 684. Public Agency Programs ....................................................................................................... 68

PERTINENT CPUC DECISIONS ............................................................................................................. 69PERTINENT LEGISLATION .................................................................................................................... 69

APPENDIX B -- GLOSSARY OF TERMS ....................................................................................... 71

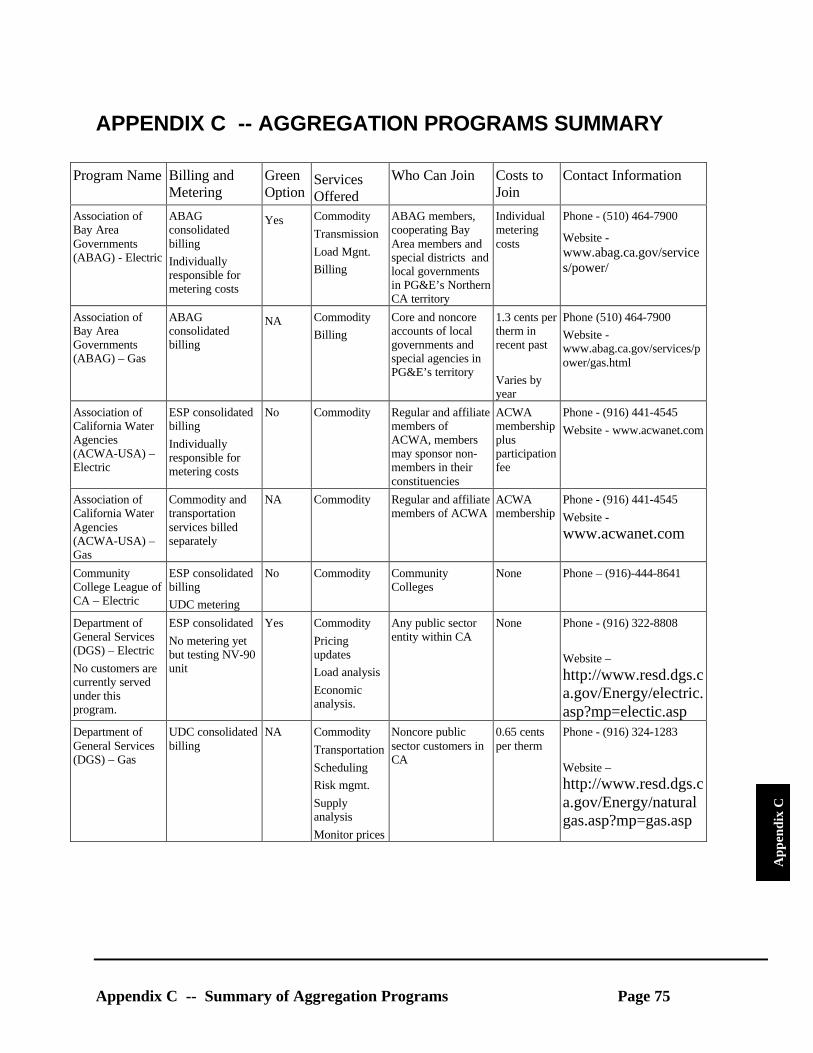

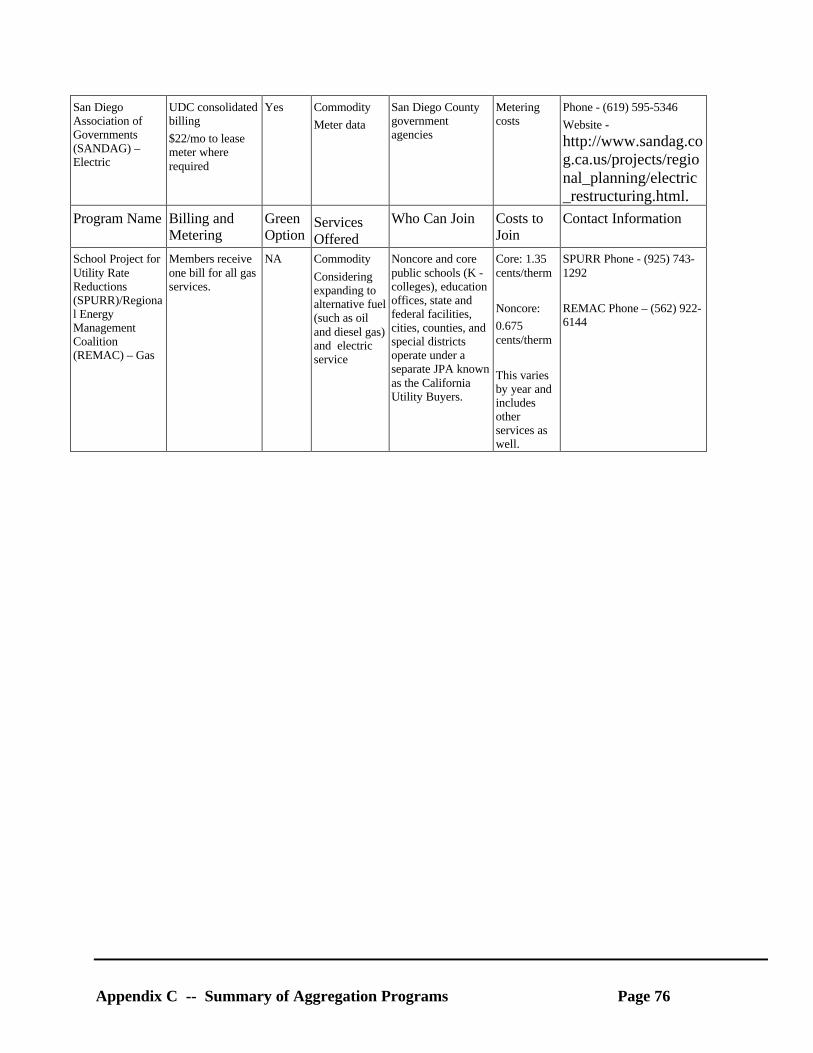

APPENDIX C -- AGGREGATION PROGRAMS SUMMARY ........................................................ 75

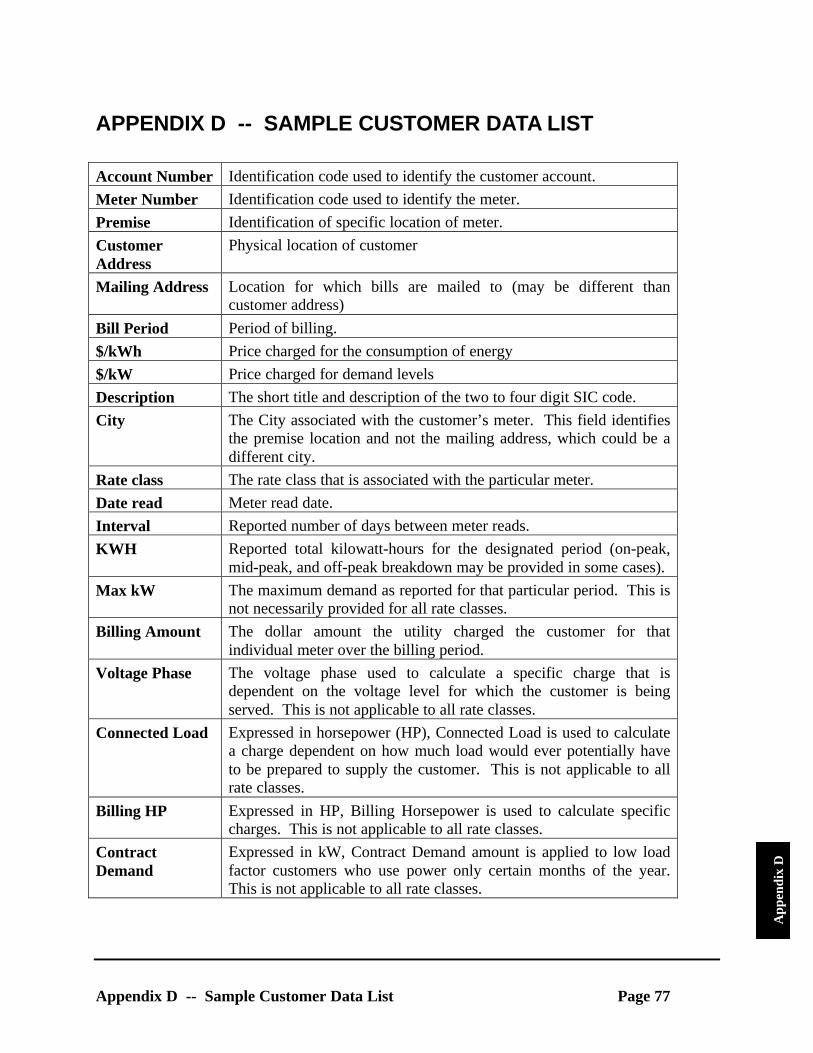

APPENDIX D -- SAMPLE CUSTOMER DATA LIST..................................................................... 77

APPENDIX E -- SAMPLE DATA REQUEST .................................................................................. 79

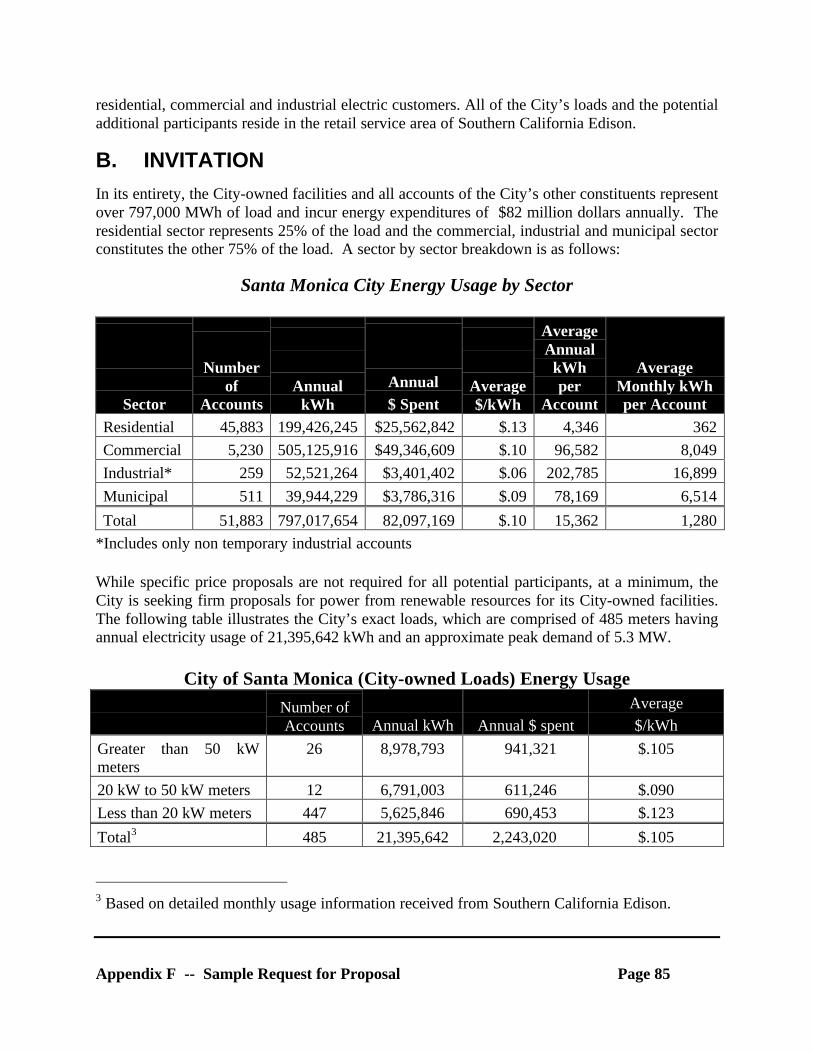

APPENDIX F -- SAMPLE REQUEST FOR PROPOSALS.............................................................. 81

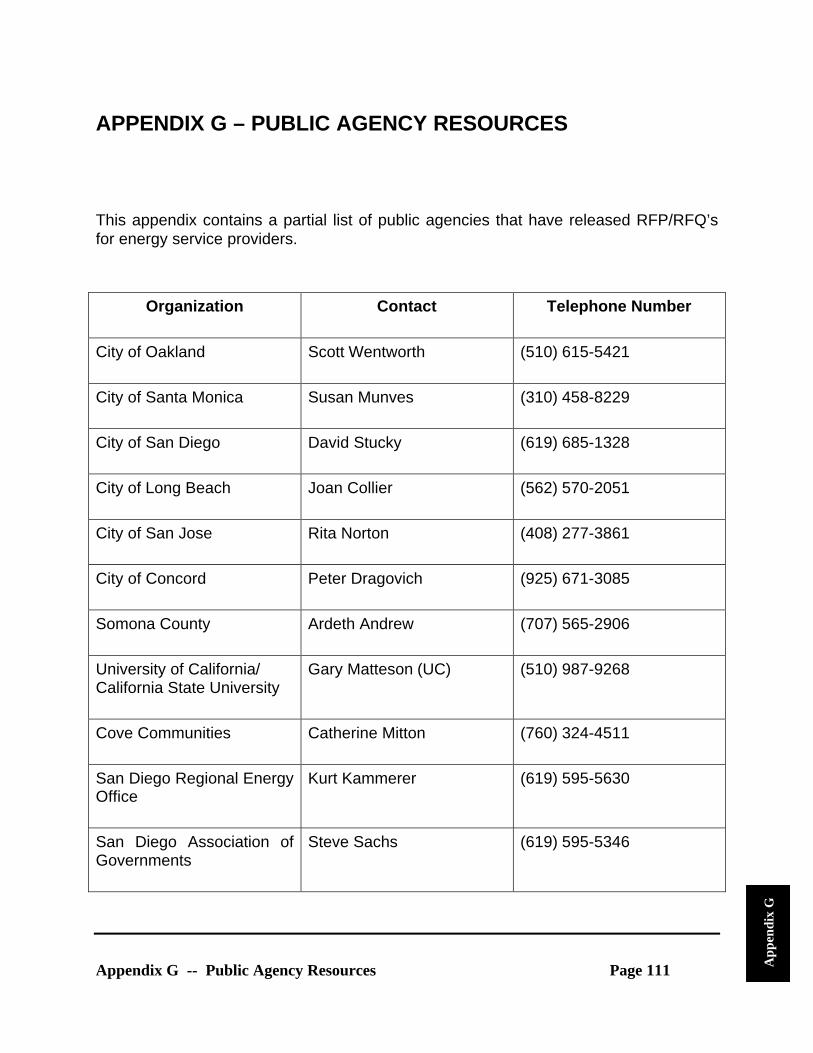

APPENDIX G � PUBLIC AGENCY RESOURCES ..........................................................................111

Section I � Introduction Page 1

Intr

oduc

tion

I. INTRODUCTION

Buying electricity used to be relativelysimple. One company, your local utility,sold you electricity and delivered it toyour meter. The services you paid forincluded electricity generation, longdistance transmission over high voltagelines, transport over local distributionlines, and the costs of meter reading andbilling. The utility company even ranrebate programs for energy efficientequipment to help you reduce yourenergy use and costs.

In 1996, the California Legislaturepassed legislation (AB 1890, Chapter854, Statutes of 1996) restructuring thestate’s electric industry. The start of thetransition to the new electricity marketbegan March 31, 19981. For customersin investor owned utility serviceterritories (Pacific Gas and Electric,Southern California Edison, San DiegoGas and Electric, Sierra Pacific Power,Pacific Corp, Bear Valley Electric, andMountain Utilities), the electric marketstructure changes were mandatory. Forpublicly owned utilities, the decisionwas left to the local governments. Thegoverning body of each municipal utilitymust determine whether they wish toopen their system to the competitivemarket.

With the restructured electric industry,customers can shop around, compareprices and services, and purchaseelectrical power from the supplier whobest meets their needs. No longer are

1 The original January 1, 1998, starting datechanged to March 31, 1998 due to initialimplementation difficulties.

customers restricted to buying poweronly from their local utility company.The ability to purchase electricity fromother suppliers rather than from yourtraditional utility is called direct access.As a result of direct access, you may beable to better manage your energy billsand may have opportunities to cut yourelectricity costs.

These changes to the structure ofCalifornia’s electricity industry areprofound and over time will most likelychange the way you think about electricservices. Unbundling of the variouscomponents of electricity service willgive you opportunities to better manageyour consumption choices and electricitycosts.

The California Energy Commission(Energy Commission) developed thishandbook to help public agenciesunderstand the changes and choices inthe new energy markets, the electricitymarket in particular. The handbookcontains information on:

• industry changes and how they affectyou and your organization;

• things to consider before you decideto switch power providers;

• a process to follow if you decide topurchase energy from a competitivesupplier; and

Section I � Introduction Page 2

• an update on the changing naturalgas markets.

Two supplements included in thishandbook provide a complete discussionof the changes to the structure ofCalifornia’s electric industry andanswers to frequently asked questions.

The Appendices contain a Glossary,Sample Request for Proposal, and otherresources to help you understand thechanging energy marketplace.

The following are the major findings andconclusions discussed in the handbook:

• Prices in the current electricitymarket are very volatile and potentialsavings in the restructured energymarket may be modest at this time.

• The rules governing electricitymarket operation are changing aslawmakers and others work toimprove functioning of therestructured energy markets. Publicagencies need to stay well informed,whether purchasing energy throughdirect access or staying with theirlocal utility.

• Energy efficiency and loadmanagement are critical to reducingenergy cost—even if public agenciesare participating in direct access.They need to understand that the best

strategy to reducing energy cost isthe one that relies on multipleapproaches.

• Unbundling electricity energycommodity costs from other providerservices is key to avoiding confusingand complex offers. Public agenciesneed to separate the cost for value-added services from energy in orderto evaluate bids equivalently.

• Energy price bids are typically validfor a short time, one to five days.Unless there is an individualdesignated to negotiate for them,public agencies may have difficultyobtaining a board or city councildecision within this time frame.

• Meter installation and re-installationis one of the problematic aspects ofdirect access. Switching providerscould mean the need for new metersdue to meter readingincompatibilities.

• Customized billing services canresulted in substantial savings due toreduced internal processingexpenses. These savings can exceedthe electricity price savings.

Section II � Is Direct Access Right for You? Page 3

Sect

ion

II

II. IS DIRECT ACCESS RIGHT FOR YOU? KEY ISSUESTO CONSIDER

Now that the basic elements andoperation of the electricity market arechanged, it may be time to determine ifyour agency could benefit from the newstructure. Many public agencies havefound that competitive services offeredin the restructured electricityenvironment are complex and meet awide variety of needs. By understandingthe reasons for your taking action, youcan select options tailored to yourexpected benefits.

Before starting any efforts to changeyour electric services, understand whatfactors are driving your decisions.Questions to answer include:

• What are your goals for takingadvantage of restructured marketopportunities? Can you clearlydefine them?

• What are your energy consumptionpatterns? When you use energy maybe more important than how muchyou use.

• Will you get a good deal on yourown or should you try to aggregate,or join an existing group?

• What are your expected results? Arethey reasonably achievable? Do theygo beyond what other publicagencies have achieved in therestructured market?

• What are the risks involved? Is youragency prepared to assume thoserisks?

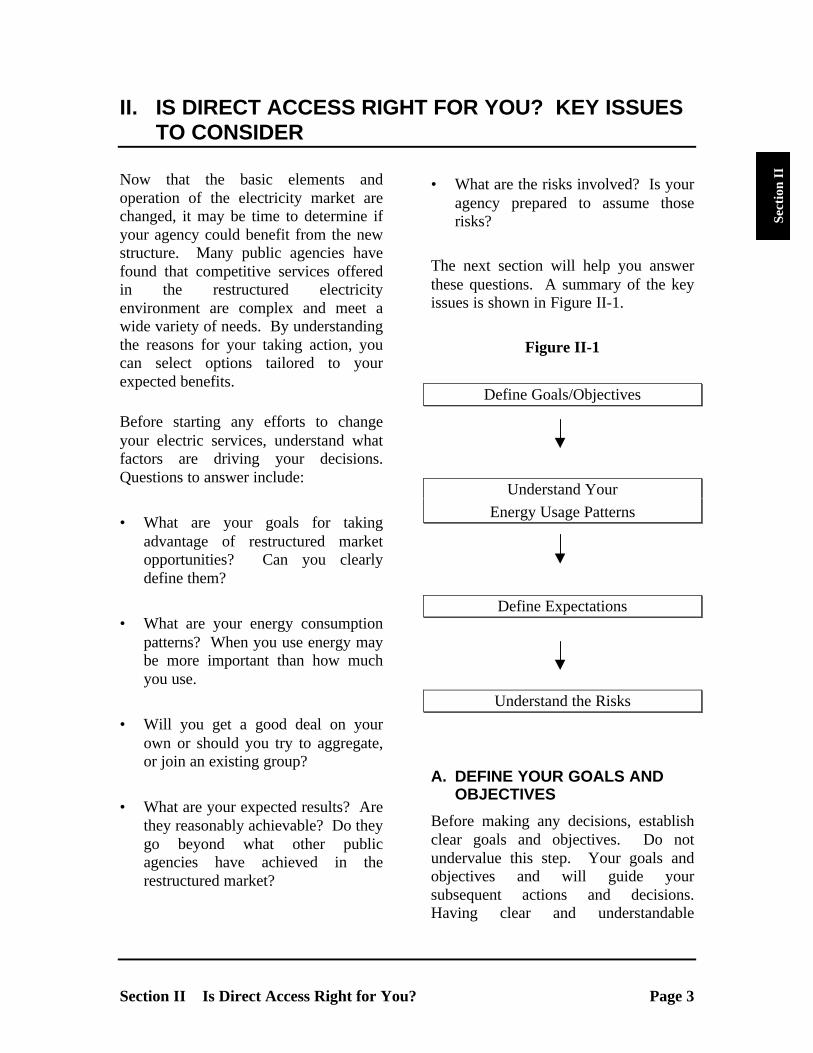

The next section will help you answerthese questions. A summary of the keyissues is shown in Figure II-1.

Figure II-1

Define Goals/Objectives

Understand Your

Energy Usage Patterns

Define Expectations

Understand the Risks

A. DEFINE YOUR GOALS ANDOBJECTIVES

Before making any decisions, establishclear goals and objectives. Do notundervalue this step. Your goals andobjectives and will guide yoursubsequent actions and decisions.Having clear and understandable

Section II � Is Direct Access Right for You? Page 4

objectives will make it easier to justifyeach decision as you go through yourevaluation process. Because of theirimportance, allow adequate time toensure that everyone involved in thedecision process understands and agreeson these goals and objectives, and thatthe potential political implications andramifications are understood.

Here are some key questions to ask tobetter define your agency’s goals andobjectives.

Are you changing services in order to:

• avoid volatile energy costs throughstable and predictable prices?

• reduce energy costs?

• obtain better customer service?

• change or customize your energybilling process?

• support or lead a move toward use ofenvironmentally friendly (e.g.renewable) energy resources?

• improve the reliability of yourenergy services?

• support the development of newcompetitive options?

• better understand your energy usageand service options?

• respond to an unsolicited offer?

There are numerous other questions youmay need to answer to clearly defineyour goals and objectives. Talking withothers who have been through theprocess or engaging qualified expertsmay be helpful. A number of potentiallyhelpful contacts are included inAppendices A and G.

B. UNDERSTAND YOUR ENERGYUSAGE PATTERNS

Understanding your energy usage patternis a critical next step. Providing detailedinformation about your energyconsumption to a supplier increases thelikelihood of obtaining the best possibledeal. Generally, if you have a relativelyconstant energy use pattern, you willreceive a better deal than if your usagefluctuates or spikes during peak periods.

The best way to understand your energyconsumption patterns is to create anannual load profile. This profile willshow the demand patterns for every hourof every day over a 12-month period.Key items include the differencesbetween your maximum and minimumusage, the time of the day, and the timeof the year you use most of your energy.Usage that occurs predominately duringsummer daytime hours is generally themost expensive. This will be reflected inprices offered by a competitive supplier.

If you are going to aggregate a numberof loads, understand the energyconsumption and behavior for allmembers of the group. If you areconsidering joining an existingaggregation group where the savingslevels will be dependent on the usagepatterns of the entire group, make suretheir patterns complement yours. If not,you may receive a better offer on yourown. However, if your usage pattern hasa lot of spikes, you could be better in anaggregation group.

While compiling detailed historical datafor your agency’s electricity accountscan seem overwhelming, it is a critical

Section II � Is Direct Access Right for You? Page 5

step in the decision process. In manycases, your current electricity suppliercan provide you with a load profile. Ifyour organization is not familiar withmanaging and analyzing large databasesof energy information, contract the datacollection and evaluation to a third party.After your data review process, youshould be able to clearly communicatethe following:

• how many meters make up your totalload;

• the number of meters by rate class;

• the time and amount of yourmaximum hourly usage (in kW);

• the typical difference between yourmaximum and minimum hourlyusage (in kW);

• your total annual energyconsumption (in kWh); and

• your annual load factor (which is theratio of your average load to yourannualized maximum load).

If your agency doesn’t have data for allaccounts and meters expected to be partof the aggregation program, request itfrom your local utility or extract it fromyour utility bills. Your utility canprovide 12 to 24 months of usage historyfree of charge. Requests for this data areusually processed within 30 to 60 days.

Some agencies have experiencedproblems verifying the accuracy andcompleteness of data from their utility.Work with the utility to verify the usageand billing data. Make any correctionsto account for missing or inaccuratedata.

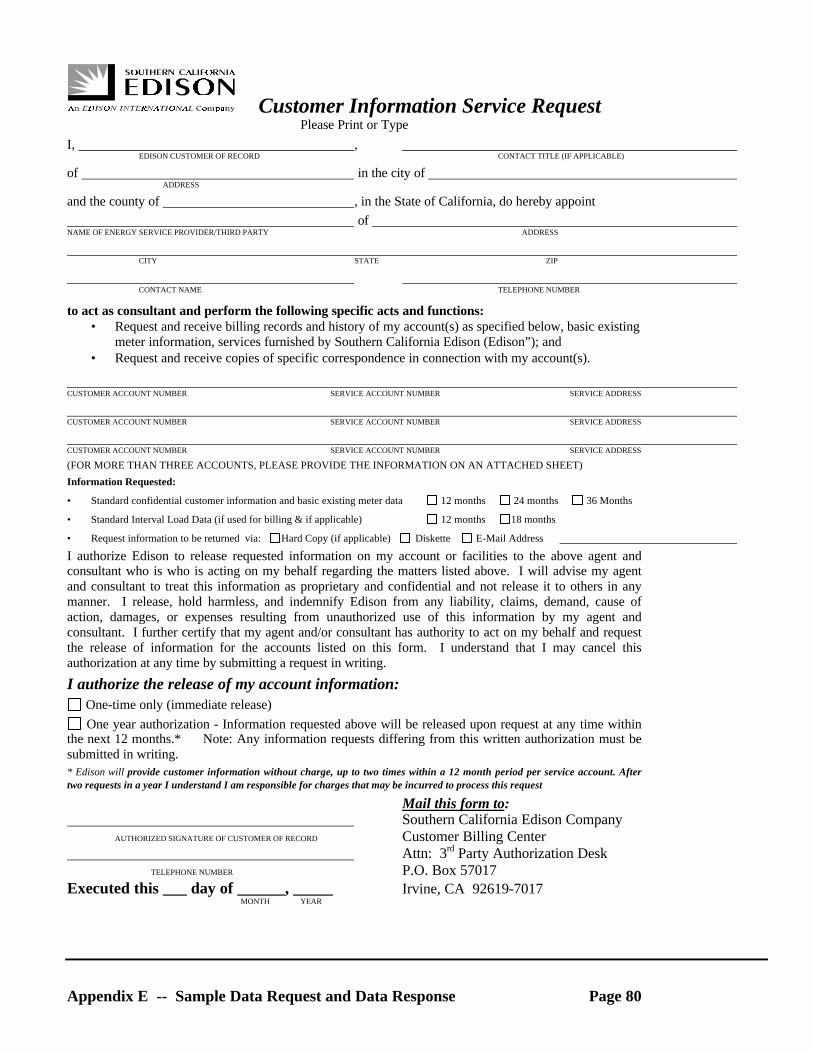

One way to keep mistakes to a minimumis to specify the exact information youneed. A sample form is included asAppendix E to this guidebook.

Most utilities provide standardinformation that is adequate though eachutility’s terminology for the same datamay be slightly different. Theinformation may not be delivered in auser-friendly format, so allow plenty oftime to process and analyze theinformation in order to understand yourusage levels and patterns. Appendix Dcontains a listing and explanation of theterminology found in utility bills. Withthe utility billing information, youshould be able to use it to characterizeyour energy consumption and patterns interms of total usage, kW demand andload factor of the aggregated use pattern.An aggregated load profile is a goodway to demonstrate these characteristics.Appendix F contains summary tablesthat provide examples of effective waysto communicate this information.

A greater understanding of usage levelswill allow your agency to develop a veryinformative Request For Proposal andQualifications (RFP/RFQ) which, shouldlead to more responsive offers fromsuppliers. It will also give you an ideaof potential metering costs due to theinstallation of direct access meters.

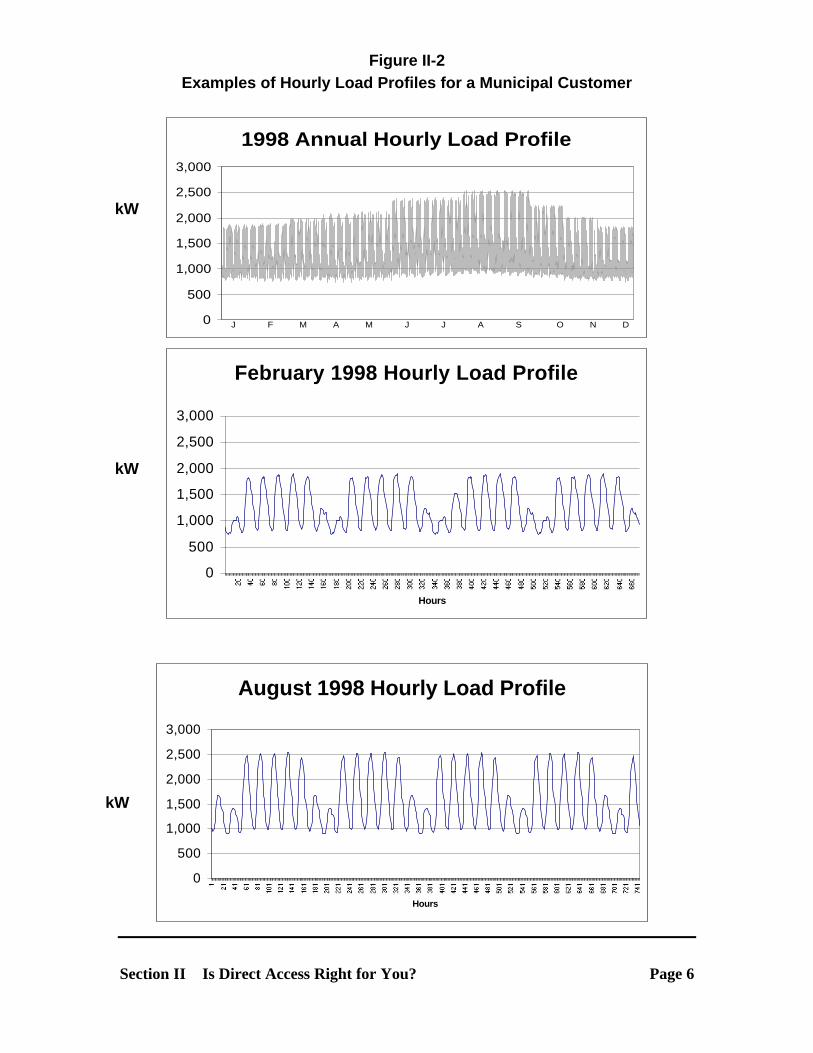

Figure II-2 shows example hourly loadprofiles for a typical municipalcustomer. These graphs show that thetotal annual electricity use is 11,927,796kWh. The maximum hourly load of2,533 kW is occurring in August and aminimum hourly load of 743 kW is

Section II � Is Direct Access Right for You? Page 6

Figure II-2Examples of Hourly Load Profiles for a Municipal Customer

February 1998 Hourly Load Profile

0

500

1,000

1,500

2,000

2,500

3,000

Hours

August 1998 Hourly Load Profile

0

500

1,000

1,500

2,000

2,500

3,000

Hours

kW

kW

kW

1998 Annual Hourly Load Profile

0

500

1,000

1,500

2,000

2,500

3,000

J F M A M J J A S O N D

Section II � Is Direct Access Right for You? Page 7

shown for February. This load has anannual load factor of 53.7%. Themonthly profiles are for the samecustomer for the months of February andAugust, respectively. In the monthlyprofiles, it is easy to see how thecustomer’s load changes over the courseof each day and the lower loads on theweekends are clearly evident. Thedifference between the daytime andnighttime loads as well as the differencebetween the maximum load in thesummer and winter will be keydeterminants of the competitive pricesoffered to this customer.

C. DEFINE EXPECTATIONS

After you have defined your goals andobjectives, and understand your usagepatterns, it is equally important to defineyour expectations. To make the bestpossible decision, your expectationsneed to be realistic and reflect truemarket conditions.

As the market continues to evolve andmature, so will the types of offers andprice offerings. Review the latestmarket conditions and keep abreast ofthe market changes.

Comparing your specific situation to thatof other entities that have achievedenergy savings is a simple and effectivetechnique. However, recognize thatmarket conditions can change rapidly.Competitive providers will respond tothese changes in order to maintain anacceptable business risk/reward balance.This should directly impact the resultsyou can achieve. Be flexible and adjustexpectations as new market conditionsdictate.

D. UNDERSTAND THE RISKS

Just as your energy objectives need to beclearly defined, so do your risks. Thecontinued market restructuring meansthat all customers, even those that staywith the local regulated utility, will beexposed to new risks and changes in theway energy services are priced. Pricevolatility is but one of the risks you mayface in the new competitive energymarket structure. The key areas of riskinclude:

• price volatility risks;

• contract duration risks;

• risks of not being able to changesuppliers;

• supplier non-performance risks; and

• risks of inaction or not payingattention to the evolving market.

Recognize these risks and understandthat you will be exposed to many ofthem even if you stay with your currentutility.

1. P R I C E V O L A T I L I T Y - W H A T A R E C O M M O N

C O M M O D I T Y P R I C I N G S T R U C T U R E S ?

There are three primary types of pricingstructures in today’s energy markets.These include:

• fixed – a guaranteed price per kWh,regardless of any usage patterns ormarket conditions;

• indexed – a price that will rise or fallin relation to certain marketconditions, often the PowerExchange (PX) price; and

• hybrid or portfolio – a combinationof fixed and indexed pricing that

Section II � Is Direct Access Right for You? Page 8

may fluctuate within a fixed pricerange or be linked to the cost of aspecific set of generating resources.

More detailed information on PriceOptions is provided in Section III, B-Pricing Options.

2. C O N T R A C T D U R A T I O N - H O W L O N G

S H O U L D M Y C O N T R A C T B E ?

Many agencies that have undergone anenergy procurement process found it lessrisky to enter into a one to two yearcontract with the option to renew, asopposed to a longer three to five yeardeal at a marginally more attractive rate.

Having shorter contract terms withoptions also allows you to learn moreabout the competitive energy industrybefore making any long termcommitments. Some of the uncertaintiesabout energy prices will be resolved asthe market matures. Having the abilityto change suppliers as market conditionsdictate, rather than being restricted by along-term contract with initially betterterms, is probably a lower risk strategyat this point in the evolution of theCalifornia market.

3. L I M I T S O N C H A N G I N G - W H A T I F I W A N T

T O S W I T C H P R O V I D E R S ?

Your contract terms should clearlyexplain the financial implications if youdecide to switch suppliers or go back tothe local utility. Many agencies thathave gone through the process were ableto negotiate terms that allowed them toswitch with no penalty if a better offerwas presented and proper notice wasgiven.

However, one of the complexities ofswitching between providers involves

meters and meter reading. If you don’town the meters, your new and oldenergy service provider will have tonegotiate the sale or removal of themeters. In some cases, new meters mayneed to be purchased in order for yournew energy service provider or utility toread them.

4. N O N - P E R F O R M A N C E - W H A T I F M Y

S U P P L I E R C A N N O T M E E T M Y N E E D S ?

A supplier’s failure to perform couldexpose your agency to additional costs,because you’ll have to go through atleast some steps of the procurementprocess again. To protect against thispossibility, some agencies have requiredtheir suppliers to post performancebonds or place cash in an escrowaccount that they can access undercertain nonperformance situations. It isimportant to note that suppliernonperformance does not mean yourelectricity supply will be terminated.The Independent System Operatorensures that all consumers receive thepower they demand. However, theremay be financial consequences if yoursupplier fails to pay for power purchasedon your behalf.

5. K E E P I N G U P W I T H T H E M A R K E T � W H Y

D O I N E E D T O P A Y A T T E N T I O N T O T H E

M A R K E T S O N C E A C O N T R A C T I S I N P L A C E ?

Just as understanding your electric usageis important to getting started incompetitive energy procurement, stayingaware of changes in the energy industryis equally important. There are hiddenrisks associated with lack of knowledgeand inaction. If you do not make theeffort to understand the restructuredelectric market, you may lose out oncurrent savings or make energyconsumption decisions that are

Section II � Is Direct Access Right for You? Page 9

unnecessarily costly. And don’t forgetthat there may be risks associated withdoing nothing.

6. P R O T E C T I N G Y O U R I N T E R E S T S

Switching your electricity service to anew provider is a risk. However, theState of California has mandated severalmeasures to protect you from providersthat will not be able to meet their servicecommitments.

This protection is provided throughregistration requirements established bythe California Public UtilitiesCommission (CPUC). The focus ofthese requirements is to ensure thatenergy service providers serving smallcustomers are credible and financiallyviable and will be able to meet theirservice commitments. Also establishedis a process to investigate any allegedinappropriate operations or practices byenergy service providers. Appendix Acontains information on how to obtainthis information from the CPUC website.

Energy service providers serving onlylarge commercial and industrialcustomers are not required to registerwith the CPUC. These customers are ina “buyer beware” situation, and it will beimportant to do appropriate additionalresearch on a prospective energy serviceprovider and the provider’s offer.

E. IS DIRECT ACCESS FOR YOU?

Historically, public agencies that aremost successful in entering into directaccess contracts are those that had welldefined goals and objectives, understood

their electrical loads and usage, andunderstood the risks and costs. Due tothe complexities of evaluating proposals,reviewing contract terms, andnegotiating a contract, many publicagencies or aggregators have hired anindependent consultant to prepare thebid documents, evaluate the proposals,and/or negotiate the final contract.Depending on the assistance needed, theconsultant costs can range from $10,000to $50,000 or more.

Even if you hired a consultant andresponded positively to the questionsraised in this section, you may still notbe a good candidate for direct access norbe successful in negotiating a contractwith an alternate provider. Some publicagencies have gone through extensiveevaluation and bidding processes andfound few acceptable bidders. This iswhy it is good idea to contact publicagencies that have gone through thisprocess, to determine the reasons fortheir successes or failures in negotiatinga direct access contract. A list of publicagencies that have released biddocuments soliciting energy serviceproviders are listed in Appendix G.Once you learn the reasons for their pastsuccesses and failures and understandthat future regulatory and energy marketconditions can evolve and change, thenyou can decide whether direct access isfor you.

Section II � Is Direct Access Right for You? Page 10

Section III � Your Electricity Choices Page 11

III. YOUR ELECTRICITY CHOICES________________________________________________________________________

For customers in investor owned utilityservice territories (Pacific Gas andElectric, Southern California Edison,San Diego Gas and Electric, SierraPacific Power, PacificCorp, Bear ValleyElectric, and Mountain Utilities), thenew restructured electricity market nowoffers many choices when it comes toyour electricity service.

Local governments also have choicesthat give them and their constituentsgreater local control. For instance, theycan play a role in delivering energyefficiency services to their citizens andbusinesses or can serve as an aggregatorfor those businesses and residentialcustomers who wish to participate.Local governments also have the right toexercise their municipalization rightsand authorities, or to support theformation of new municipal utilityservice providers.

In addition, you can choose to purchasegreen power to help the environment andsupport the renewable energy industry.And, as before, you can reduce yourenergy use by changing operationprocedures or installing energy efficientequipment.

This section discusses the five majoroptions of electricity procurement andincludes:

• purchasing;

• pricing;

• metering and billing;

• green or renewable electricity; and

• energy efficiency and energymanagement.

A. YOUR PURCHASING OPTIONS

You now have four choices for obtainingelectric services in California:

• continue to purchase your electricservices from your existing utility;

• participate in direct access − buypower from a competitive energyservice provider (ESP), broker, orpower exchange;

• aggregate (combine with otherorganizations) to form a new buyinggroup or pool; or

• create a municipal serviceorganization to provide your electricservices.

1. S T A Y I N G W I T H Y O U R E X I S T I N G U T I L I T Y

You can continue to rely on your currentutility for electricity without doinganything. The utility will continue toprovide power at rates set by theCalifornia Public Utilities Commission(CPUC) during the transition period,typically from April 1, 1998 to March31, 2002. San Diego Gas and Electricended its transition period in 1999.During the transition period, utilitypricing will be “frozen” at the 1996

Sect

ion

III

Section III � Your Electricity Choices Page 12

rates. After the transition period, thecommodity portion of your bill willchange with the Power Exchange (PX)price. It should be noted that in August2000, the legislature and CPUC wereconsidering options to change thetransition period rate parameters.

If you want to participate in thecompetitive market, but don’t want toswitch to a new supplier, you can choosethe utility’s “Schedule PX”, sometimesreferred to as virtual direct access or realtime pricing.

Schedule PX lets you buy power atmarket-determined, real time pricesrather than at a rate that is based on theaverage consumption pattern ofcustomers in your rate class. It willreward you when PX prices are low butwill also expose you to the risk of higherprices that occur during times of peakdemand and consecutive hot summerdays. If you choose Schedule PX, youmust install – at your expense – intervalmeters to record hourly usage.

Real time pricing may be a beneficialoption if you use a greater percentage ofenergy in off-peak (lower priced) hourscompared to other customers in your rateclass. Real time pricing can offersignificant savings if you have the abilityto reduce energy use during peakperiods.

2. C H O O S I N G A C O M P E T I T I V E S U P P L I E R --D I R E C T A C C E S S

If you choose direct access, there arethree key requirements in addition to theselection of a new supplier. First, aDirect Access Service Request (DASR)

must be filed with your local utility.This is a notification that you are goingto obtain some or all of your electricservices for the specified loads from acompetitive supplier. Second, you mustobtain the services of a SchedulingCoordinator. They will schedule yourelectric load supply with theIndependent System Operator (ISO).Lastly, if your load is greater than 50kW, you will need an interval meter thatwill keep track of your usage on anhourly basis. Your energy serviceprovider should be expected to take careof all of these requirements as part oftheir competitive offer.

All energy service providers offer theelectricity commodity, but many alsooffer packages of energy products andservices. This may include billingservices, meter reading, meter and meterservicing, energy audits, energyefficiency measures, and other energyrelated services. This is often referred toas a “bundled services” offering. Thekey question for you is what servicesyou want and whether bundled orindependent service offerings will bestserve your specific needs.

The advantage of acquiring bundledservices is that you can limit yourprocurement efforts to virtually onebidding process and select a single entityto provide multiple services. Yourenergy service provider will oftenmaintain detailed information about yourloads. That knowledge should give themthe advantage of being able to identifymeasures that could reduce load orenergy use. As many public agencieshave found out, trying to transfer largeamounts of end-use energy data from

Section III � Your Electricity Choices Page 13

one provider to a third party can be along, time-consuming process.

The key disadvantage of bundled serviceofferings is that it is often difficult,confusing, and complex to evaluate thecosts and benefits of each service. Alsothe energy commodity provider may notbe the most competitive or most capablesupplier of the other services.

M e t e r s

If your electricity demand on a singleaccount is greater than 50 kW, you arerequired to install interval meters thatmeasure and record hourly energyconsumption. The meter and installationcost range from $400 - $1500 peraccount. Alternatively, you can lease themeters from your energy serviceprovider. You also may be assessed amonthly fee for meter reading andmaintenance. Though these chargessubstitute for the utility’s otherwiseapplicable meter charges, you need toinclude these costs in the determinationof whether direct access is beneficial foryou.

Currently, for any account whereelectricity demand is less than 50 kW,you can participate in direct accesswithout purchasing a new meter. In thefuture, this could be reduced to 20 kW.Therefore, it is important to understandhow your energy service provider wouldaddress this additional meteringrequirement if changes occur during theterm of your service contract. Thesesmaller customer accounts are assumedto have an hourly usage patternrepresented by “typical” customers inthe same rate class. This process ofconverting total monthly energy usage to

an hourly usage pattern is called loadprofiling.

S c h e d u l i n g

Your energy service provider is requiredto handle the scheduling of generatingresources to meet your energy usage. Ifyour provider does not handle thescheduling themselves, they willcontract with an approved schedulingcoordinator. The provider purchasespower supplies in bulk quantities for allits customers’ loads from a variety ofwholesale market options. When thereare differences between the scheduled(pre-purchased) amounts and actualconsumption by the customers, yoursupplier has to buy or sell power from areal-time market where prices can bequite volatile. To reduce price volatility,your energy service provider tries toclosely match supplies with itscustomer’s actual hourly consumption.

If you are billed based on real timepricing, you have the opportunity andmay be able to reduce total energy costsby shutting off equipment quickly inresponse to high prices. However, thisoption requires you to monitor hourlyenergy prices and have the flexibility toimplement a load shedding plan.

3. P A R T I C I P A T I N G I N O R C R E A T I N G A N

A G G R E G A T I O N

Aggregation means pooling your powerneeds with others to get “volumediscounts” and sharing the startup andadministrative costs. There are severalaggregation programs offered by thestate, joint powers authorities,universities, and other independently runprograms. Before you start your ownaggregation program, look at existing

Section III � Your Electricity Choices Page 14

groups to see if they will meet yourneeds.

In this section we’ll examine the types ofpublic sector aggregation programs andthe possibilities for initiating new groupsthat could serve private citizens orcompanies.

A g g r e g a t i o n P r o g r a m s

There are several existing Joint PowersAuthority and governmental aggregationefforts. Most have focused on specificcustomers.

Joint Powers Authority

A Joint Powers Authority is a singleentity formed by several independentgroups, usually public agencies that wishto exercise common authorities. It isgoverned by law, has procedures inplace to exercise its authority, and has astaff charged with specific tasks. A JointPowers Authority allows its members tobenefit from a larger organization;however, it only has the authorities thateach member has independently. It alsohas an independent identity that allows itto act separately from its memberagencies. For example, it is possible fora Joint Powers Authority to provide taxexempt financing without encumberingthe total liability or bonding limits of itsmembers.

Energy Cooperatives

Electric or energy cooperatives are non-profit corporations that can supplypower to their members. Like JointPowers Authorities, they are tax exemptand can borrow money at low rates.Cooperatives can include privatebusinesses or citizens as well as publicagencies. For further information, the

Energy Commission sponsors an EnergyCooperative Development program,which you can access via the websitehttp://www.energy-co-op.net/index.html

Municipal Aggregation Programs

There are a number of municipalities, ormunicipal groups, that have developedtheir own aggregation programs. Theseprograms are typically designed aroundspecific goals and may include all oronly certain energy accounts.

Some municipal led aggregationprograms have considered includingnon-municipal customers in theirprograms. The benefits of includingnon-municipal participants include:

• the possibility of receiving a betterprice from an energy serviceprovider due to offering it a largerload;

• the public agency leading theprogram may be able to get amarketing credit (a direct payment ora further price reduction) inrecognition of the marketing costsavoided by the energy serviceprovider; and

• positive community relations for theagency providing a value-addedservice to its constituents above andbeyond what most cities offer.

The drawbacks of including privatecustomers include:

• the difficulty of getting privatecustomers interested;

• any uncertainty in who will actuallyjoin the program may be viewed as

Section III � Your Electricity Choices Page 15

added risk by the energy serviceprovider;

• their electrical load and use maybenon-complementary to the usagepatterns of municipalities in theaggregation and negatively impactprice offerings; and

• the energy service providers lack ofinterest in smaller customers due toincreased billing and metering costs.

Appendix C provides a summary ofaggregation programs that have beencreated in the state. Your agency maymeet the qualification requirements forjoining one of them. Even if you donot, the programs can certainly offer youadvice on how to most effectively set upyour own program.

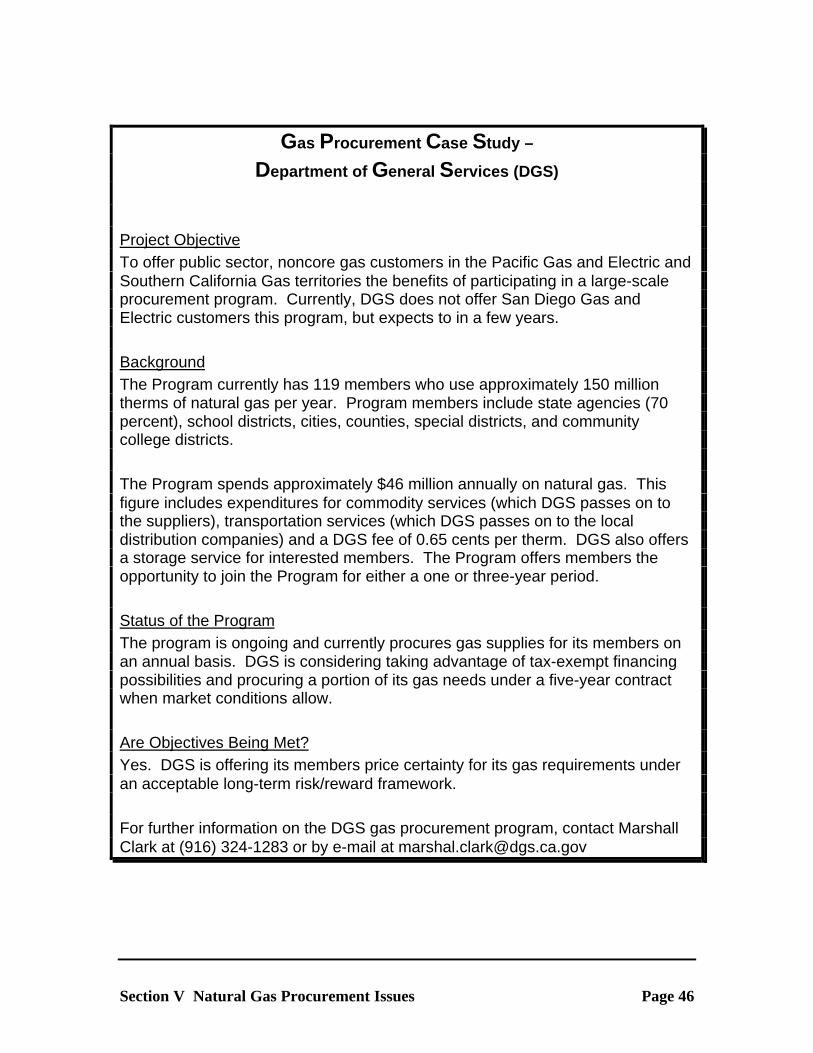

The California Department of GeneralServices (DGS) provides a number ofaggregated purchasing services for stateand other public agencies. Becausethere might be savings from purchasingenergy for numerous facilities under asingle contract purchase, the Departmentof General Services created anaggregation program for governmentalentities. The case study on page 16describes the program.

4. M U N I C I P A L I Z A T I O N

Some communities are looking totraditional public takeover ormunicipalization of electric distributionsystems as a means of enhancing theirconstituents access to competitive powerservices in the restructured market. Anumber of existing municipal electricutilities have demonstrated that they canprovide competitive prices for energy

services in addition to the commodityservice. The primary reason formunicipalization is to take advantage ofadditional ways to reduce the cost ofenergy services.

Municipalization can be a majorendeavor. There have been very fewinstances in which the existing utilityservice company has been receptive to apublic takeover of their existing businessand/or customers. And, the cost to thepublic agency could be significant.

There are two approaches typicallyconsidered by an entity wanting to createa municipal electric system. The first isforming a municipal service functionwithin the existing municipalorganization. The second is to form anew (or use the unexercised rights of anexisting) special district such as aMunicipal Utility District, Public UtilityDistrict, or Irrigation District, which isgoverned by an independent and locallyelected Board of Directors. In eithercase, the new municipal entity willacquire, own, and operate the electricdistribution system and thus provide allof the services of a traditional electricutility.

There are a number of both such entitiesthroughout California and there are newentities that have been recently created.All of these entities recognize the needto offer electric services at prices belowthose offered by their customer’s currentutilities. The use of a municipal serviceorganization is also a way for a localgovernment to influence theircommunities commitment to specificrenewable energy sources.

Section III � Your Electricity Choices Page 16

CASE STUDY

CALIFORNIA DEPARTMENT OF GENERAL SERVICES (DGS)

The objective of the DGS Electricity Services Program is to enable public sectorcustomers to participate in the new competitive electricity market. The goal is to reducecustomers’ operational costs for electrical energy below the customer’s default utilityservice provider. DGS also envisions opportunities to integrate commodity energysupply, new energy production and end use technologies, and enhance information onenergy usage patterns, to provide customers with economical energy services.

BackgroundIn November 1997, potential suppliers were invited to submit standardized bids for bothbundled electrical services (electricity, schedule coordination, and revenue cycleservices) and individual unbundled services under a three-year Master ServicesAgreement. In addition, suppliers were invited to submit offers for additional electricityservices.

Status of the ProgramDGS has amended the Master Services Agreement to open the “pool” of suppliers tonew entrants. Several rounds of price quotations have been requested from suppliersas market conditions have evolved. However, no service orders for direct access tocustomer meters have yet been finalized with any of the energy service providers listedon the Master Services Agreement. DGS continues to review customer loads foreconomic opportunities in the direct access market and to negotiate with its suppliers toensure verifiable customer savings from any direct access contracts.

Are Objectives Being Met?To date, energy service providers’ response to direct access has been disappointing. InDGS’ estimation, this is the result of several factors, including high transaction costs,disincentives resulting from the way continuing traditional utility service costs areseparated from their bundled rates, and uncertainties surrounding the business rules forthe new market. DGS anticipates that the market may achieve greater depth andstability after the end of the rate freeze, when the post-transition ratemaking environmentis more stable.

For more information on the DGS program, call (916) 322-8808.

Section III � Your Electricity Choices Page 17

Examples of recently establishedmunicipal entities include MercedIrrigation District and San JoaquinIrrigation District. Merced IrrigationDistrict began providing retail electricdelivery services in May 1996. SouthSan Joaquin Irrigation District isanticipating it will be able to beginserving retail customers sometime in2000.

A public agency wishing to form its ownmunicipal electric system should consultwith its County Local Agency FormationCommission.

Creation of a new electric service utilityfrequently involves the "condemnation"or forced sale of a portion of the existingutility’s electric distribution facilities.This process is often politically andfinancially challenging to the publicagency.

The experience of the Trinity CountyPublic Utility District within Pacific Gasand Electric Company’s (PG&E) servicearea is an example of a local entityhaving difficulties, but eventuallysucceeding in acquiring local electricfacilities for the formation of amunicipal system. The community ofHayfork, located in Trinity County,wanted to form its own municipalsystem and began the condemnationprocess of the PG&E facilities in itsarea. The condemnation results wereappealed by PG&E in court before thefacilities were finally acquired by the

city and eventually became part of theTrinity County Public Utility District.In Calaveras County, a referendum onwhether to form a municipal electricutility was defeated. However, the costsof pursuing the concept were borne bythe local entities promoting the effort.

The case study on page 18, describes amore recent municipalization effort inDavis, California.

Another way to form a new municipalservice entity is by the incrementalestablishment of the electricity deliverysystem infrastructure. In this approach,there is no need to acquire facilities fromthe existing utility. Rather, the newmunicipal provider builds the newfacilities necessary to serve newcustomers and/or developments. In sodoing, it is possible that some customersof the existing supplier will want to“switch” if the new facilities are locatedin such a way that this can be doneeconomically.

There are circumstances wheresignificant savings may be created byconstructing new energy distributionfacilities to serve multiple customers. Inthese cases, the new entity must simplyhave the authority to provide retailelectric services in the State ofCalifornia. Since private corporationsdo not have that authority (unless theybecome a regulated utility), thedistribution facilities must be owned bya municipal entity with authority to sellelectric retail power.

Section III � Your Electricity Choices Page 18

Case Study – City of Davis Municipalization Effort

In an effort to lower utility costs and focus on alternative and renewable energy, a grass-roots Davis organization, the Sustainable Utility Network Cooperative Inc. (Sun Co-op),began the process of creating the Davis Municipal Utilities District.

Municipalization options include:4 Act as a negotiator and secure lower rates for the customers of Davis by bulk

purchase of energy and services;4 Join with Sacramento Municipal Utility District; or4 Become a full service utility provider.

StatusThe first step is getting the proposition on the ballot. The ballot measure would askvoters to establish a specified geographic district and a board of directors. The Sun Co-op submitted to the Local Agency Formation Commission (LAFCO) the 889 pages ofsignatures totaling 4,024, in addition to the required application. InJuly 2000, due to a lack of information regarding a plan and fiscal analysis, LAFCOrejected Sun Co-op’s request to put the municipalization proposition on the November2000, ballot.

Lessons LearnedForming your own utility district is extremely difficult. One great challenge is the lack ofreliable information from any one source regarding legal guidance on themunicipalization process. For example, more than 4,000 signatures were collected toplace the measure on the ballot. It was understood that 10 percent of registered votersignatures (about 4,000 for Davis) were needed to qualify. However, it was later learnedthat, in fact, only 1,900 signatures were needed (only 10 percent of the number ofpeople who voted in the last election, not including absentee voters).

To create a Davis Municipal Utility District, it will require the mobilization of people tosupport the idea of local control and a good economic study supporting fiscal soundnessof the plan.

For more information write Dennis Dingemans, Coalition for Local Power, 645 C St,Davis, CA 95616.

Section III � Your Electricity Choices Page 19

The owner of the facilities then takesresponsibility for providing powerdelivery services to each of its customersat rates that are competitive with thelocal utility’s transmission anddistribution rates. This is a viable optionin developing areas where much of theutility infrastructure is installed by thedeveloper. If the new area can be servedwithout the use of the local utility’stransmission lines, additional costsavings may be possible. The MountainHouse community developmentnorthwest of Tracy is an example of anew development that is promoting this“incremental” concept.

The formation of new municipal serviceentities is governed by applicablesections of California laws. There aremany pros and cons to each of thepotentially available options. As such,anyone considering such a move will bewell served by obtaining appropriatetechnical and legal advice at an earlystage.

B. PRICING OPTIONS

The cost of electricity depends mainlyon how much you use and when you useit. In existing regulated rates, demandcharges and time-of-use differentialshave a major effect on total cost. Smallcustomers don’t usually pay demand ortime-of-use charges, but pay a higherunit cost than large customers. In thissection we will start by looking atexisting rates. We will explain typicalrates for both small and large customers.Then we will look at other pricingstructures offered by competitive energyservice providers.

1. E X I S T I N G R E G U L A T E D R A T E S T R U C T U R E

Your electric bill is comprised of severalcomponents as discussed in Supplement1. Direct access, however, is focusedprimarily on the commodity orgeneration component of the bill. Inyour current bill, this charge iscalculated based upon the size of yourload and your rate class.

For smaller customers, the bill isgenerally calculated by multiplying anaverage cost for electricity times theamount of electricity used during thebilling period. The cost is independentof when you use the electricity. Thisaverage cost includes the cost ofproducing the energy.

For larger customers, the generationcomponent is calculated as the sum of ademand charge and an energy charge.Both the demand and energy charge aretime and season dependent. Typicallythe highest charges will occur in thesummer between 12 noon and 6 p.m.The demand charge is intended to be areflection of the cost of building ageneration facility to meet your needs.For the large customer, the energycharge is much less than for smallcustomers. This is because for smallcustomers, the cost of building thegenerating facilities is included in theenergy price, whereas large customerspay a separate charge.

2. N E W R A T E O P T I O N S

In the direct access markets, electricitycosts are calculated differently and thereis often only a generation componentthat includes both the commodity anddemand charges. The following are themain pricing options.

Section III � Your Electricity Choices Page 20

(1) F ixed Pric ing

This price structure offers the customer afixed, known price for the electriccommodity. It offers the least exposureto price volatility, although that reducedrisk is usually reflected in a higher price.The electricity provider accepts the riskassociated with the commodity pricevolatility during the period of thecontract. This may be an attractiveoption for customers with a low risktolerance, fixed budget constraints, orlimited flexibility to respond to priceswings.

(2 ) Indexed (Var iab le ) Pr i c ing

This structure links the price of thecommodity to an agreed upon marketindex such as the PX market clearingprice. Due to exposure to market pricingvolatility, this option can be more riskyif you do not have the ability to shiftyour load or curtail your use during highpriced peak usage periods. This optionis particularly attractive to customerswho can shift energy consumption totake advantage of low off-peak priceswhile avoiding high price spikes duringpeak periods. However, there is a riskunder this scenario, especially if youcan’t shift or reduce load during periodsof high price spikes. For publicagencies, with a set energy budget, thiscould be a problem. If you choose thisoption be reasonably confident that youragency can risk exposure to electricityprice volatility during your contactperiod.

At the end of the utility transitionperiods, customers not choosing directaccess will be subject to the pricevolatility of the supplies purchased byutilities on behalf of their customers,including the portion of supply from the

PX. Though this price volatility may bemasked by the utility offering balancedpayment plans or similar programs, thereis usually a subsequent calculation thatresults in the entire price risk beingborne by the customer.

(3) Port fo l io Pric ing

Portfolio pricing allows you to design aspecific program with your supplier thathas price volatility generally linked tospecific resources. This approach willtend to mitigate, though not eliminate,price volatility. It requires that thesupplier thoroughly understand yourelectricity use patterns so that their risksare minimized. If a supplier perceives alow risk of offering a lower price, hewill generally do so. However, in manycases, it may be that the risk is simplybeing transferred to the energyconsumer, for example through penaltyclauses, if certain requirements are notmet.

Despite how any pricing plan isstructured, you must realize thatprotection from volatility has a price andexposure to volatility has risks.

C. METERING AND BILLINGOPTIONS

Metering and billing services are nowunbundled, meaning you don’t have toaccept services offered only by yourtraditional utility company. At thecurrent time, you are restricted to receivethese services from your energy serviceprovider or its agent. If you do chooseto receive offers for metering andbilling, make sure the cost for theseservices are clearly separate from theenergy cost. Unbundling the electricity

Section III � Your Electricity Choices Page 21

commodity from other provider servicescan be key to avoiding confusing andcomplex offers.

1. M E T E R I N G

If you choose a new supplier, you mayneed to install a new interval meterbefore receiving your electricity service.If you need to install a new meter thereare three ownership options:

• Customer owned – You can purchasea meter from the local utility, energyservice provider or other companyoffering CPUC approved intervalmeters. Prices range from $400 to$1,500 including installation costs.

• Energy service provider owned –Many energy service providersinclude a meter leasing optionbundled with the electric commodityservice. Monthly leases can beanywhere from zero to $40 permonth.

• Utility owned – You can lease autility-owned meter, paying amonthly fee for the installation andthe cost of the meter. The fee willdepend on the type of meter andcontract length.

For governmental and small consumers,the trend to date has been for the serviceprovider to take care of the installation,ownership, and servicing of any requirednew meters. The customer has beenresponsible for a lease payment that isnegotiated as part of the service contract.In many cases, the customer hasobtained the right to own the meter at theend of the contract, or they will have an

option to buy the meter at a pre-determined price. However, be aware ofthe possibility that any meters installednow may become obsolete in only a fewyears as new metering technology, withexpanded data access capabilities,becomes available. Also, meter-readingcapabilities vary with the energy serviceprovider or your electric utility. Somepublic agencies that went back to theirlocal utility found that the energy serviceprovider supplied meters that were notcompatible with the electric utility meterreading equipment. As a result, somepublic agencies had to buy new“interval” meters again.

Interval meter installation has been oneof the more problematic aspects of directaccess for some public agencies.Remote locations and installationscheduling problems have sometimescaused this step to take longer thananticipated. If you need new metersinstalled, take a proactive role early inthe installation process to keep theschedule on track and ensure that theinstalled meters can be read by yourutility in the event that you go back tothem in the future.

2. B I L L I N G

There are a number of billing optionsavailable. You can receive either oneconsolidated bill or separate utility andenergy service provider bills. If youchoose a consolidated bill, it will includecharges for the competitive commodityas well as regulated delivery services.You can decide which entity will sendyou the bill. If you are participating inan aggregation program, you maychoose to customize your bill from theenergy service provider. For example,you may choose to receive one summary

Section III � Your Electricity Choices Page 22

bill for your entire program with aspecified level of detail for individualparticipants.

Some direct access customers haveachieved substantial savings throughcustomizing billing services that reducedinternal processing expenses. In onecase, these savings exceeded theirelectricity cost savings.

For many of the aggregation programs,there is continued reliance on theexisting utility provider to supplyconsolidated billing. This optioneliminates the need to set up complicateddata management and customer billingsystems by the new provider, thusallowing focus to be on the provision ofcompetitive commodity services. It islikely that competitive providers willdevelop their own billing systemcapabilities as the market continues todevelop.

D. BUYING GREEN ORRENEWABLE ELECTRICITY

You may be asking yourself, “Whatexactly is green power?” Generallyspeaking, it is electricity generated fromresources that do not run out, or arequickly renewed through naturalprocesses. These sources includegeothermal power, solar power, biomass,wind, and small hydroelectric generationfacilities.

Green power, or renewable electricity,has proven to be a popular option forresidential, municipal, and commercialcustomers in the new competitiveelectricity market. The Center forResource Solutions estimates that about90% of customers who have switched to

a competitive supplier are receivinggreen power. While the majority areresidential customers, some high profilecustomers in the state, like the City ofSanta Monica, City of Oakland, andToyota Motor Sales USA Inc., havedecided to meet their electricity needs bybuying green power.

A customer who purchases renewable orgreen power from a supplier may notactually receive electricity from a greenpower plant. What actually happens isthe green supplier agrees to purchasepower in the amounts and proportionscorresponding to the loads of thecustomers they serve, and they ensurethat amount of renewable power issupplied into the state electric powergrid.

How do I know I’m actually gettinggreen power?Both the California Energy Commissionand the Center for Resource Solutionshave programs that green powersuppliers may use to document howmuch of their mix is renewable-based.

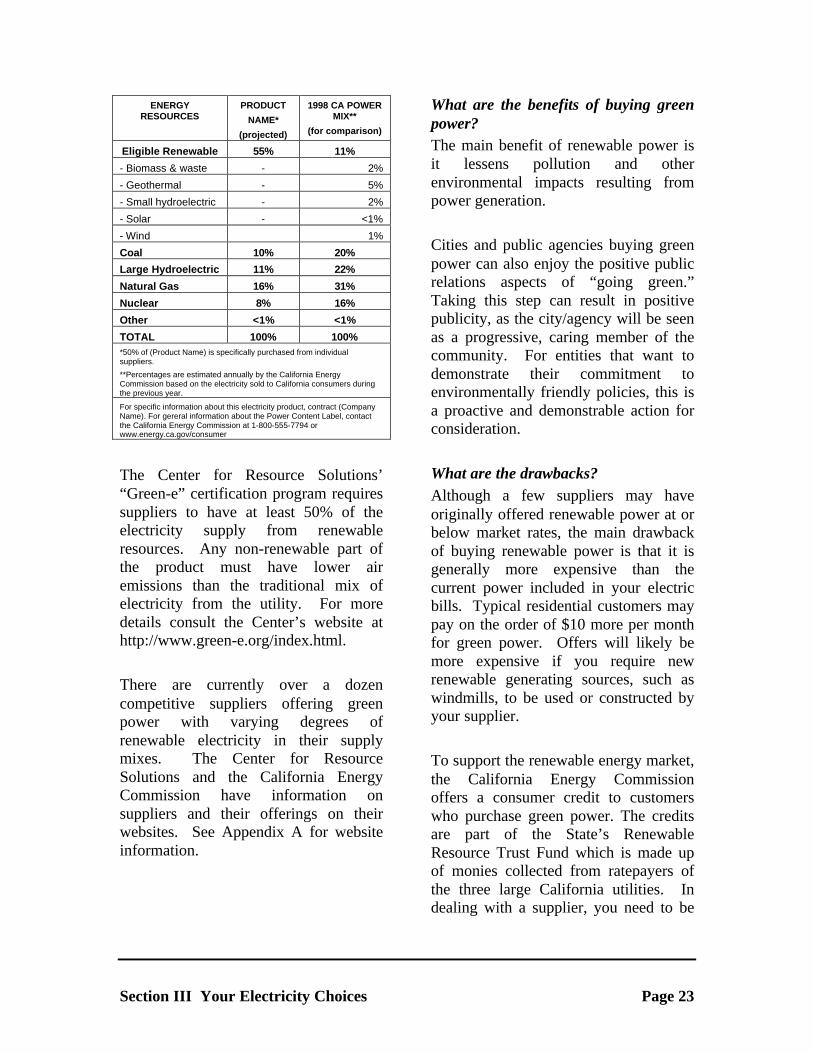

The California Energy Commissionrequires a “Power Content Label” fromany supplier that claims that a portion oftheir supply is renewable energy based.The label, an example of which is shownin Figure III-1, shows the percentage ofelectricity from each source that theprovider feeds into the grid for youraccounts. You should request the labelfrom each electricity provider you wantto consider.

Figure III-1

POWER CONTENT LABEL

Section III � Your Electricity Choices Page 23

ENERGYRESOURCES

PRODUCT

NAME*

(projected)

1998 CA POWERMIX**

(for comparison)

Eligible Renewable 55% 11%

- Biomass & waste - 2%

- Geothermal - 5%

- Small hydroelectric - 2%

- Solar - <1%

- Wind 1%

Coal 10% 20%

Large Hydroelectric 11% 22%

Natural Gas 16% 31%

Nuclear 8% 16%

Other <1% <1%

TOTAL 100% 100%*50% of (Product Name) is specifically purchased from individualsuppliers.

**Percentages are estimated annually by the California EnergyCommission based on the electricity sold to California consumers duringthe previous year.

For specific information about this electricity product, contract (CompanyName). For gereral information about the Power Content Label, contactthe California Energy Commission at 1-800-555-7794 orwww.energy.ca.gov/consumer

The Center for Resource Solutions’“Green-e” certification program requiressuppliers to have at least 50% of theelectricity supply from renewableresources. Any non-renewable part ofthe product must have lower airemissions than the traditional mix ofelectricity from the utility. For moredetails consult the Center’s website athttp://www.green-e.org/index.html.

There are currently over a dozencompetitive suppliers offering greenpower with varying degrees ofrenewable electricity in their supplymixes. The Center for ResourceSolutions and the California EnergyCommission have information onsuppliers and their offerings on theirwebsites. See Appendix A for websiteinformation.

What are the benefits of buying greenpower?The main benefit of renewable power isit lessens pollution and otherenvironmental impacts resulting frompower generation.

Cities and public agencies buying greenpower can also enjoy the positive publicrelations aspects of “going green.”Taking this step can result in positivepublicity, as the city/agency will be seenas a progressive, caring member of thecommunity. For entities that want todemonstrate their commitment toenvironmentally friendly policies, this isa proactive and demonstrable action forconsideration.

What are the drawbacks?Although a few suppliers may haveoriginally offered renewable power at orbelow market rates, the main drawbackof buying renewable power is that it isgenerally more expensive than thecurrent power included in your electricbills. Typical residential customers maypay on the order of $10 more per monthfor green power. Offers will likely bemore expensive if you require newrenewable generating sources, such aswindmills, to be used or constructed byyour supplier.

To support the renewable energy market,the California Energy Commissionoffers a consumer credit to customerswho purchase green power. The creditsare part of the State’s RenewableResource Trust Fund which is made upof monies collected from ratepayers ofthe three large California utilities. Indealing with a supplier, you need to be

Section III � Your Electricity Choices Page 24

sure and ask whether these credits arealready considered in prices offered forrenewable power.

The Customer Credit is distributed on acent-per-kilowatt-hour basis to providersthat deliver power from registered in-state renewable supplies. The creditamount is periodically reviewed by theCalifornia Energy Commission todetermine whether there are adequatefunds to sustain it through the transitionperiod. The credit was initially set at 1.5cents per kilowatt-hour, with an annualcap of $1,000 per meter. For residentialand small commercials there is no yearlycap. In November 1999, the amount wasreduced to 1.25 cents per kilowatt-hour,with the cap remaining unchanged. Andagain in July 2000, the credit was furtherreduced to 1 cent per kilowatt-hour.This rate is effective from July 1, 2000through December 31, 2000. Near theend of 2000, the Energy Commissionwill re-evaluate the credit level (andchange it if necessary) for the periodfrom January 2001 to June 2001. Theprocess will be repeated in the spring of2001 to set the credit level for July toDecember 2001.

One important new developmentconcerning the existing consumer creditlaw specifically effects public agencies.As of August 2000, pending legislation,(AB 995), prohibits public agencies frombeing eligible to receive renewableconsumer credits after January 1, 2002.After this date, cities, counties and otherpublic agencies purchasing green powerwill no longer be eligible to receive thiscredit.

The City of Santa Monica is the first cityin the United States to purchase 100%renewable energy for its own facilities.Santa Monica has also been a leader intaking advantage of the CaliforniaEnergy Commission’s EmergingRenewable Resources buydown programas it has installed photovoltaic powersources to help meet City requirements.

The case study on page 25, describes theprocess the City went through to procuregreen power supplies to support theCity’s overall environmental plan.

Section III � Your Electricity Choices Page 25

Green Power Case Study – The City of Santa Monica

Santa Monica’s objective was to purchase power from renewable resources for City-owned facilities as part of its larger Sustainable City Program. The City also wanted toconduct an outreach program to determine the level of interest of the City’s variousconstituents in joining the renewable procurement program.The City hoped its efforts would support emissions reductions and renewable generationsources in California.

BackgroundIn November 1998, the City prepared an RFQ/RFP to request energy supplies forapproximately five megawatts needed for City owned facilities and any potentialadditional load of the City’s non-municipal customers. In mid December, the Cityreceived responses from 13 suppliers. The City reviewed each offer’s generationsource, pricing, structure, and the overall background of the supplier. (Refer to AppendixG for a copy of the RFQ/RFP).

ResultsAfter an extensive interview and evaluation process, the City contracted withCommonwealth Energy Corporation for renewable power supplies. The contract is forone year and the City has the option to renew for four additional years. The City has justcompleted their first year contract and has renewed with Commonwealth for a secondyear. The California Energy Commission credit has allowed the City to enjoy favorableterms on its renewable energy expenditures.The City conducted an outreach program and decided not to attempt to include non-municipal load in its program. Instead, they will act as an information source for anyconstituent who wants assistance in taking advantage of electric restructuring andpurchasing green power.

Are Objectives Being Met?The City is pleased with its green power procurement process and the results achievedwith its supplier. By taking a proactive attitude and having clear and realisticexpectations, the City has found a way to support its Sustainable City Program whilecontrolling its electricity budget.

For more information on the City of Santa Monica’s efforts, contact Susan Munves at :(310) 458-8229 or [email protected].

Section III � Your Electricity Choices Page 26

E. ENERGY EFFICIENCY ANDENERGY MANAGEMENT