Embed Size (px)

Citation preview

BUSINESS SCOPE REPORT

THIS REPORT MAY NOT BE REPRODUCED IN WHOLE OR IN PART IN ANY FORM OR MANNER WHATSOEVER. This report, furnished pursuant to contract for the exclusive use of the subscriber as one factor to consider in connection w ith credit,

insurance, marketing or other business decisions, contains information compiled from sources which Dun & Bradstreet does not control and whose information, unless otherwise indicated in the report, has not been verified. Dun & Bradstreet in no way assumes any pa rt of the user’s business risk, does not guarantee the accuracy, completeness, or timeliness of the information provided, and shall not be liable for

any loss or injury whatsoever resulting from contingencies beyond its control or from negligence.

P. S. DAIMA AND SONS

D&B D-U-N-S® NUMBER: 91-723-5777

Dun & Bradstreet Information Services India Private Limited.

ICC Chambers

Saki Vihar Road

Powai, Mumbai - 400072

Maharashtra

India

Tel: +91-22-28574190 / 92 / 94

Fax: +91-22-28572060

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 1 -

Scope of the Report

History and legal background

Existing operations

Management background

Bankers

Financial statements and analysis

Information Sources

Information given in this report is compiled on the basis of information obtained from the following sources:

Annual reports

Corporate communiqués

Management Discussion

Information from website

Methodology

Financial information from the audited annual reports of the Entity was studied and analysed for a three year

period i.e. FY 2011, FY 2012 and FY 2013. Information was collated from the sources as stated above.

Date: 30th

September 2013

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 2 -

TABLE OF CONTENTS

SUMMARY ...................................................................................................................................................... 4

LINE OF BUSINESS ....................................................................................................................................... 5

RATING KEY .................................................................................................................................................. 6

CURRENT INVESTIGATION ...................................................................................................................... 6

ENTITY PROFILE ......................................................................................................................................... 7

FINANCIAL SNAPSHOT ............................................................................................................................ 10

PROVISIONAL FINANCIAL PERFORMANCE ..................................................................................... 11

PURCHASES ................................................................................................................................................. 12

REVENUE ...................................................................................................................................................... 13

CUSTOMERS ................................................................................................................................................ 14

SUPPLIERS ................................................................................................................................................... 14

COUNTRY RISK SNAPSHOT .................................................................................................................... 15

FOREIGN EXCHANGE TRANSACTIONS .............................................................................................. 17

EMPLOYEES ................................................................................................................................................ 17

ACTUAL PRODUCTION AND INSTALLED CAPACITY..................................................................... 18

REGISTRATION DETAILS ........................................................................................................................ 19

CAPITAL DETAILS ..................................................................................................................................... 19

PROFIT/LOSS SHARING RATIO ............................................................................................................. 19

AUDITORS .................................................................................................................................................... 20

CORPORATE PARTNERS ......................................................................................................................... 20

EXECUTIVES ............................................................................................................................................... 20

BANK .............................................................................................................................................................. 21

INSURANCE .................................................................................................................................................. 21

HEAD OFFICE LOCATION DETAILS .................................................................................................... 22

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 3 -

BRANCHES ................................................................................................................................................... 22

STATUTORY REGISTRATION ................................................................................................................ 23

ISO CERTIFICATION ................................................................................................................................. 23

MEMBERSHIPS ........................................................................................................................................... 24

FINANCIAL ANALYSIS.............................................................................................................................. 25

ANNEXURE I –PARTNERS ........................................................................................................................ 32

ANNEXURE II - FINANCIAL STATEMENTS ........................................................................................ 35

ANNEXURE III–RATING RATIONALE .................................................................................................. 38

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 4 -

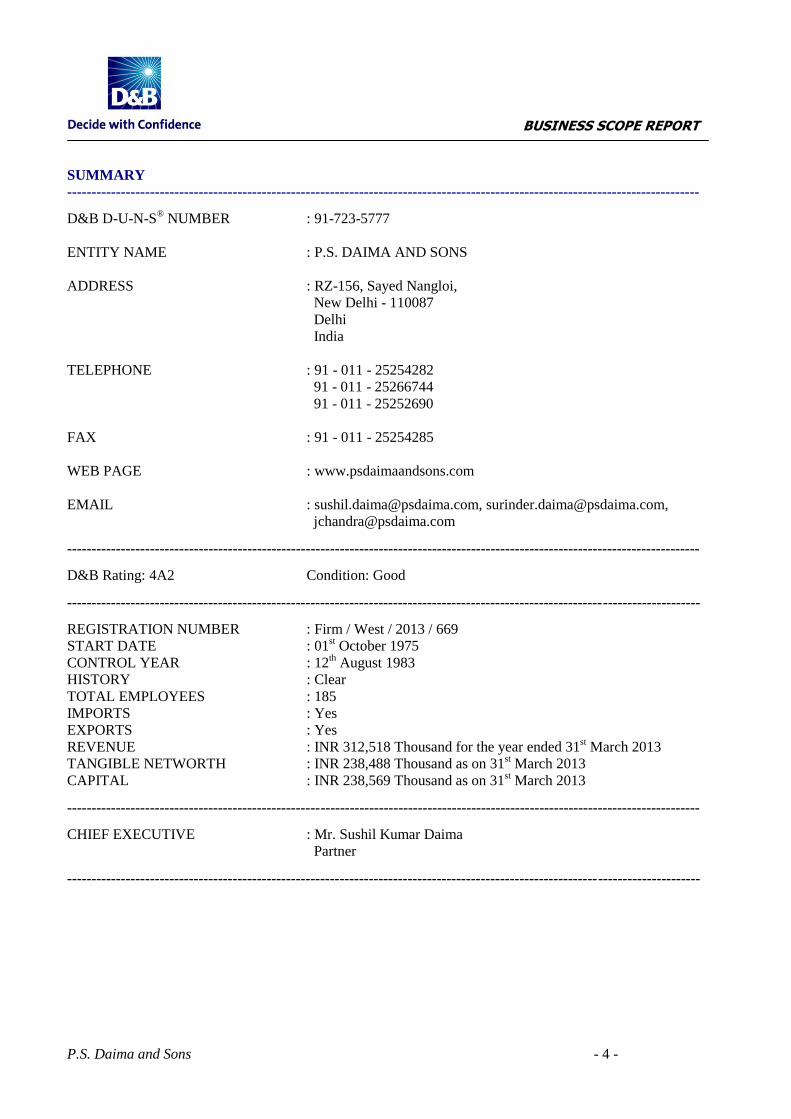

SUMMARY

---------------------------------------------------------------------------------------------------------------------------------- D&B D-U-N-S

® NUMBER : 91-723-5777

ENTITY NAME : P.S. DAIMA AND SONS

ADDRESS : RZ-156, Sayed Nangloi,

New Delhi - 110087

Delhi

India

TELEPHONE : 91 - 011 - 25254282

91 - 011 - 25266744

91 - 011 - 25252690

FAX : 91 - 011 - 25254285

WEB PAGE : www.psdaimaandsons.com

EMAIL : [email protected], [email protected],

[email protected] ---------------------------------------------------------------------------------------------------------------------------------- D&B Rating: 4A2 Condition: Good ---------------------------------------------------------------------------------------------------------------------------------- REGISTRATION NUMBER : Firm / West / 2013 / 669

START DATE : 01st October 1975

CONTROL YEAR : 12th August 1983

HISTORY : Clear

TOTAL EMPLOYEES : 185

IMPORTS : Yes

EXPORTS : Yes

REVENUE : INR 312,518 Thousand for the year ended 31st March 2013

TANGIBLE NETWORTH : INR 238,488 Thousand as on 31st March 2013

CAPITAL : INR 238,569 Thousand as on 31st March 2013

---------------------------------------------------------------------------------------------------------------------------------- CHIEF EXECUTIVE : Mr. Sushil Kumar Daima

Partner ----------------------------------------------------------------------------------------------------------------------------------

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 5 -

LINE OF BUSINESS

----------------------------------------------------------------------------------------------------------------------------------

The Entity is engaged in manufacturing of leather products, beads, cotton and nylon cords, brushes and

readymade garments.

Standard Industrial Classification Code (SIC)

2298-0202

Manufactures cord, braided

3111 -0406

Manufactures leather lace

3172-0201

Manufactures leather key cases

3199-0300

Manufactures belting and strapping

3199-9906

Manufactures embossed leather goods

3199-9906

Manufactures novelties, leather

3999-0801

Manufactures beads, unassembled

3999-0816

Manufactures stringing beads

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 6 -

RATING KEY

-----------------------------------------------------------------------------------------------------------------------------

D&B’s Rating consists of two parts, the Financial Strength and the Composite Appraisal / Condition.

Financial Strength is an indication of the tangible networth (that is, the shareholder’s funds less any

intangible assets). The Composite Appraisal / Condition is linked to the level of risk and is an overall

evaluation of credit worthiness. It takes into account the financial condition and several factors such as trade

reference history, legal structure, management experience and any adverse listings.

D&B Indicative Risk Rating of 4A2 implies that the Entity has a tangible networth between INR

129,190,000 and INR 645,949,999 as per latest available audited financial statements. Composite appraisal 2

indicates that the overall status of the Entity is good.

Risk

Indicator Level of Risk Guide to Interpretation

1 Minimal risk May proceed with transaction - offer extended

terms if required

2 Low risk May proceed with transaction

3 Slightly greater than average risk May proceed with transaction but monitor closely

4 Significant level of risk May take suitable assurance before extending

credit - e.g. personal guarantees

- Insufficient information to assign a

Rating

No public information or D&B proprietary

information available to indicate trading activity

CURRENT INVESTIGATION

----------------------------------------------------------------------------------------------------------------------------------

On 09th September 2013 Mr. Sushil Kumar Daima, Managing Partner provided relevant information in this

report. On 25th September 2013, Mr. Jagdish Chandra, Senior Manager – finance and accounts provided

additional information during management discussion.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 7 -

ENTITY PROFILE

----------------------------------------------------------------------------------------------------------------------------------

P.S. Daima and Sons (hereinafter referred to as “the Entity”) was established in October 1975 by Mr. P. S.

Daima as a proprietary concern. In August 1983, it was converted to partnership firm with the same name. In

April 2013, it was reconstituted by induction of Mr. Mehul Daima in the firm.

The Entity began its operations as a manufacturer of leather laces and leather strings. Later on, the Entity

diversified into manufacture of leather products, beads, cotton & nylon cords, brushes and readymade

garments. Refer annexure A for list of products manufactured by the Entity. The Entity also provides

customized packaging solutions based on customer’s logistic plans.

The Entity derives its entire revenue from the overseas market. It exports its products to Japan, Germany,

Italy, United States of America (USA), United Kingdom, Australia, PR China, South Korea, Europe, Far

East, etc. Its major customers include Ashro Inc. Pandora Production Company Limited, Hoapon

Development, etc.

The Entity controls its activities from its corporate office located at Delhi. It has a manufacturing unit at

Village Rohad, Bahadurgarh, Haryana.

Infrastructure

The Entity uses spiral cutting machines, skiving machines, rounding machines, coloring machines, braiding

machines, laser machines, electroplating plant and e-coating plants for manufacturing leather cords and

accessories. Also, it uses sand cleaning machines, drum polishing machines, fire polishing machines and

luster/rainbow finish machines for bead production.

The Entity was awarded best Export Oriented Unit (SSI: leather and leather products category) award by Mr.

Kamal Nath, Hon'ble Union Minister of Commerce and Industry for outstanding export performance for FY

2006.

The Entity is accredited with ISO 14001:2004 and ISO 9001:2008 and Registration, Evaluation,

Authorization and Restriction of Chemicals (REACH) norms for quality.

Source: as provided by management and entity website

Future Expansion Plans

As informed, the Entity was mainly manufacturing beads in the past. However, due to change in fashion and

declining demand for beads, it shifted its focus to leather products. Recently, it has bagged orders for leather

jewellery (artificial) and will continue to focus on leather jewellery in the future. The Company is also

started manufacturing readymade garments in FY 2013.

The Entity started leather fashion jewellery division in FY 2013. The Entity has appointed commission

agents for marketing purposes and is planning for participation in exhibitions United States of America and

Russia.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 8 -

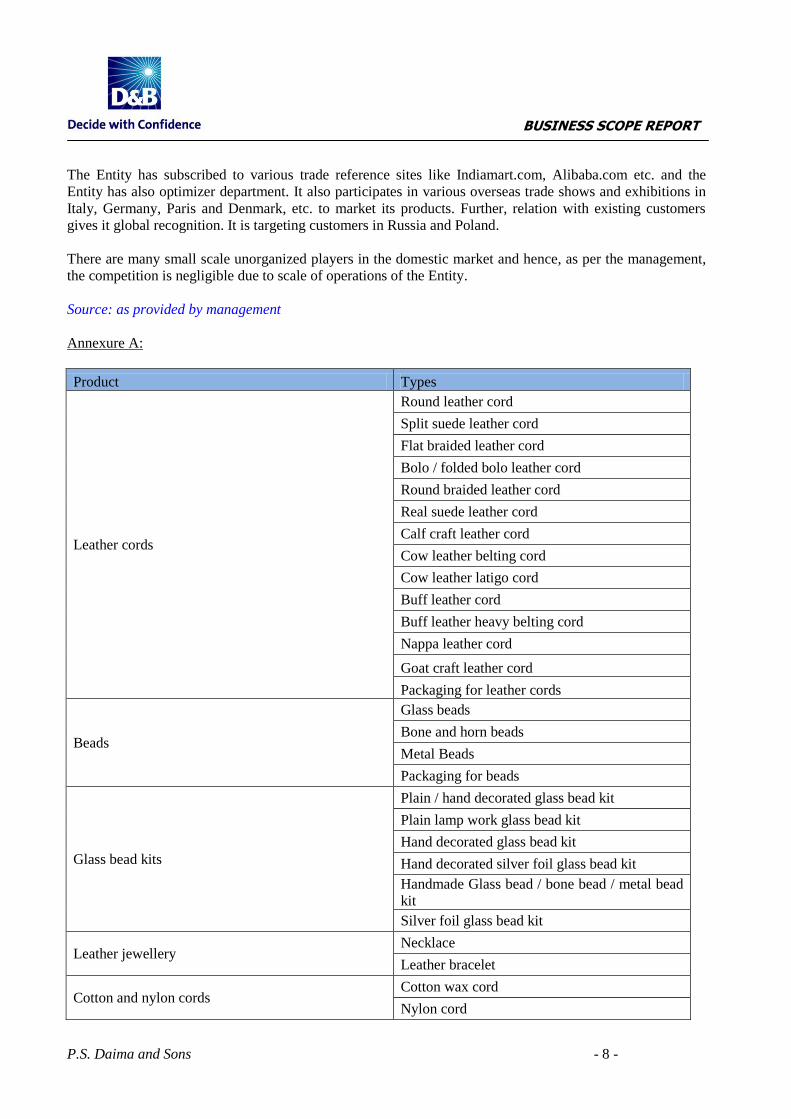

The Entity has subscribed to various trade reference sites like Indiamart.com, Alibaba.com etc. and the

Entity has also optimizer department. It also participates in various overseas trade shows and exhibitions in

Italy, Germany, Paris and Denmark, etc. to market its products. Further, relation with existing customers

gives it global recognition. It is targeting customers in Russia and Poland.

There are many small scale unorganized players in the domestic market and hence, as per the management,

the competition is negligible due to scale of operations of the Entity.

Source: as provided by management

Annexure A:

Product Types

Leather cords

Round leather cord

Split suede leather cord

Flat braided leather cord

Bolo / folded bolo leather cord

Round braided leather cord

Real suede leather cord

Calf craft leather cord

Cow leather belting cord

Cow leather latigo cord

Buff leather cord

Buff leather heavy belting cord

Nappa leather cord

Goat craft leather cord

Packaging for leather cords

Beads

Glass beads

Bone and horn beads

Metal Beads

Packaging for beads

Glass bead kits

Plain / hand decorated glass bead kit

Plain lamp work glass bead kit

Hand decorated glass bead kit

Hand decorated silver foil glass bead kit

Handmade Glass bead / bone bead / metal bead

kit

Silver foil glass bead kit

Leather jewellery Necklace

Leather bracelet

Cotton and nylon cords Cotton wax cord

Nylon cord

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 9 -

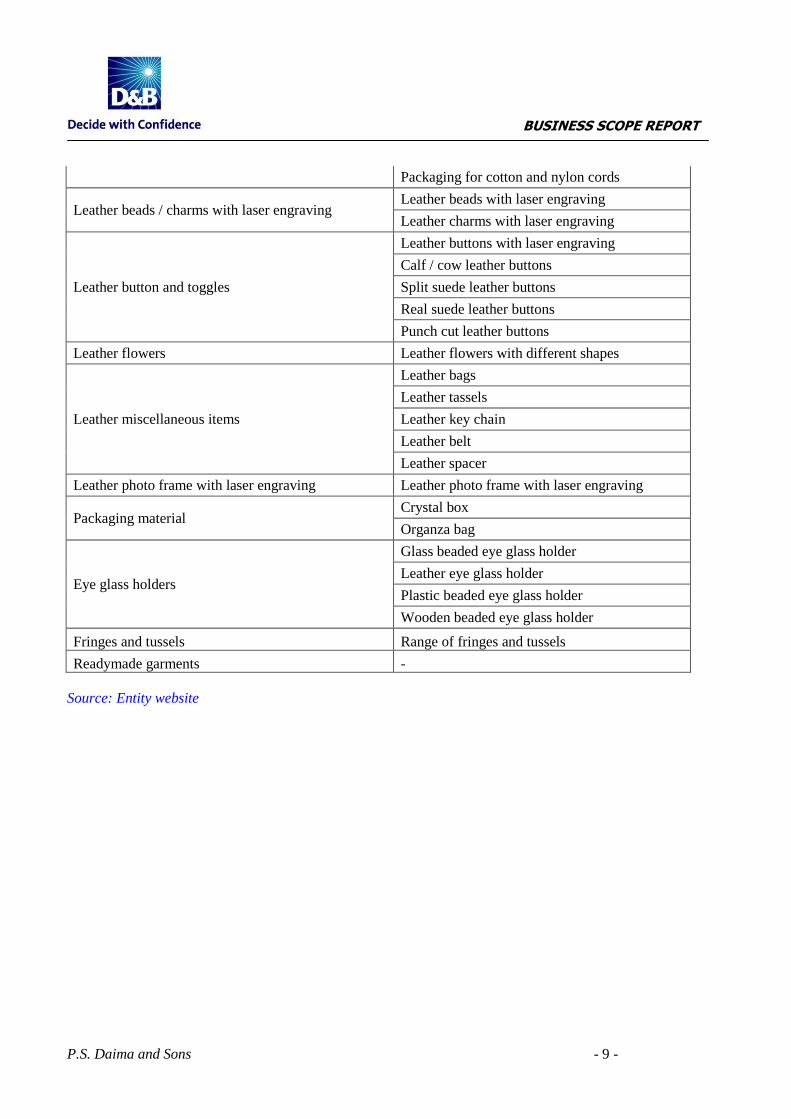

Packaging for cotton and nylon cords

Leather beads / charms with laser engraving Leather beads with laser engraving

Leather charms with laser engraving

Leather button and toggles

Leather buttons with laser engraving

Calf / cow leather buttons

Split suede leather buttons

Real suede leather buttons

Punch cut leather buttons

Leather flowers Leather flowers with different shapes

Leather miscellaneous items

Leather bags

Leather tassels

Leather key chain

Leather belt

Leather spacer

Leather photo frame with laser engraving Leather photo frame with laser engraving

Packaging material Crystal box

Organza bag

Eye glass holders

Glass beaded eye glass holder

Leather eye glass holder

Plastic beaded eye glass holder

Wooden beaded eye glass holder

Fringes and tussels Range of fringes and tussels

Readymade garments -

Source: Entity website

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 10 -

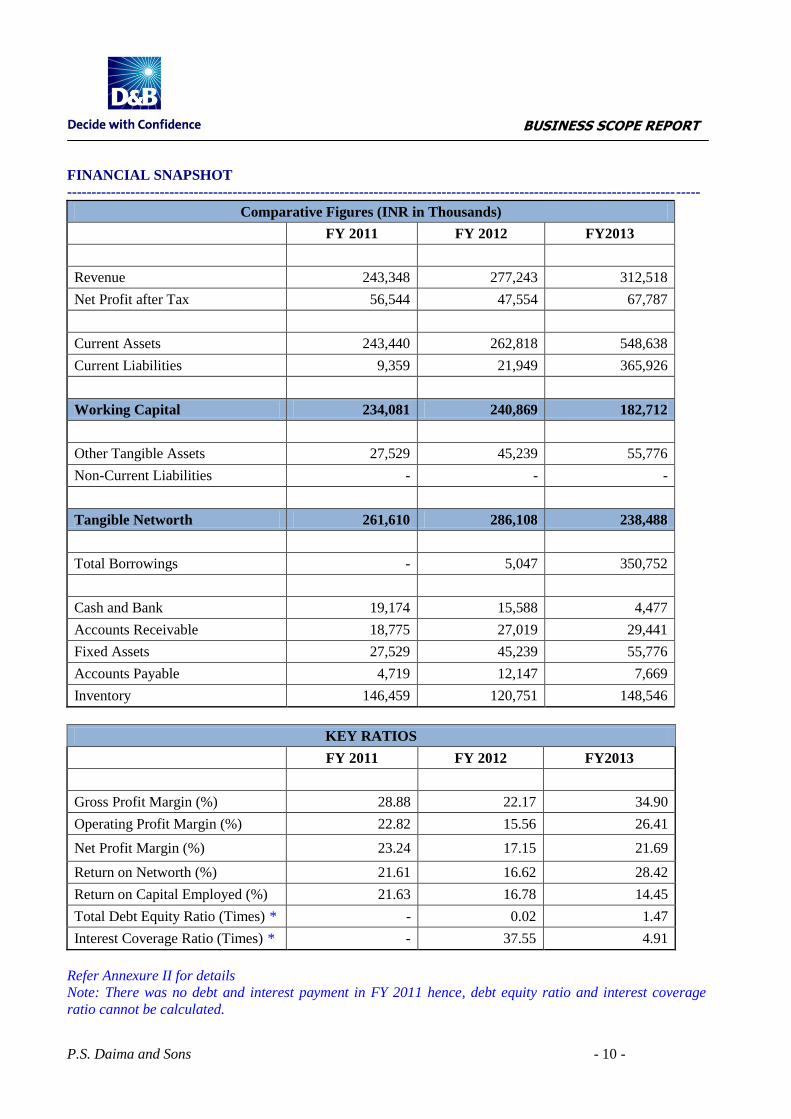

FINANCIAL SNAPSHOT

----------------------------------------------------------------------------------------------------------------------------------

Comparative Figures (INR in Thousands)

FY 2011 FY 2012 FY2013

Revenue 243,348 277,243 312,518

Net Profit after Tax 56,544 47,554 67,787

Current Assets 243,440 262,818 548,638

Current Liabilities 9,359 21,949 365,926

Working Capital 234,081 240,869 182,712

Other Tangible Assets 27,529 45,239 55,776

Non-Current Liabilities - - -

Tangible Networth 261,610 286,108 238,488

Total Borrowings - 5,047 350,752

Cash and Bank 19,174 15,588 4,477

Accounts Receivable 18,775 27,019 29,441

Fixed Assets 27,529 45,239 55,776

Accounts Payable 4,719 12,147 7,669

Inventory 146,459 120,751 148,546

KEY RATIOS

FY 2011 FY 2012 FY2013

Gross Profit Margin (%) 28.88 22.17 34.90

Operating Profit Margin (%) 22.82 15.56 26.41

Net Profit Margin (%) 23.24 17.15 21.69

Return on Networth (%) 21.61 16.62 28.42

Return on Capital Employed (%) 21.63 16.78 14.45

Total Debt Equity Ratio (Times) * - 0.02 1.47

Interest Coverage Ratio (Times) * - 37.55 4.91

Refer Annexure II for details

Note: There was no debt and interest payment in FY 2011 hence, debt equity ratio and interest coverage

ratio cannot be calculated.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 11 -

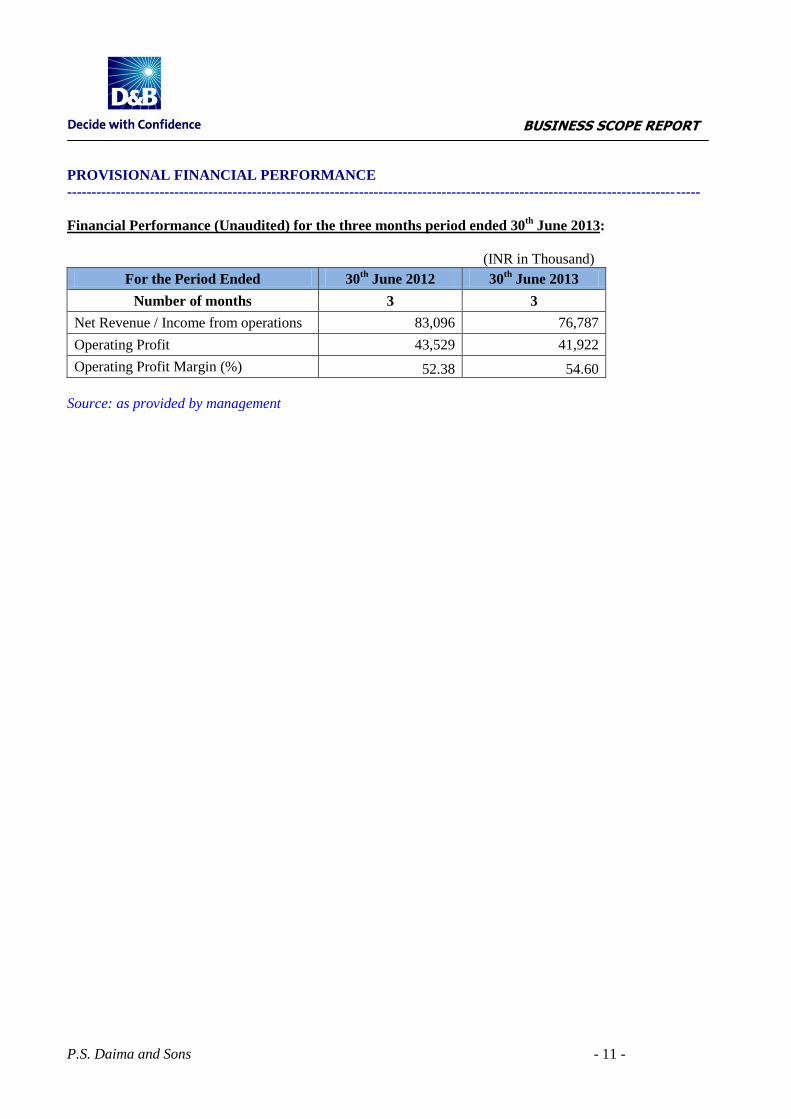

PROVISIONAL FINANCIAL PERFORMANCE

----------------------------------------------------------------------------------------------------------------------------------

Financial Performance (Unaudited) for the three months period ended 30th

June 2013:

(INR in Thousand)

For the Period Ended 30th

June 2012 30th

June 2013

Number of months 3 3

Net Revenue / Income from operations 83,096 76,787

Operating Profit 43,529 41,922

Operating Profit Margin (%) 52.38 54.60

Source: as provided by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 12 -

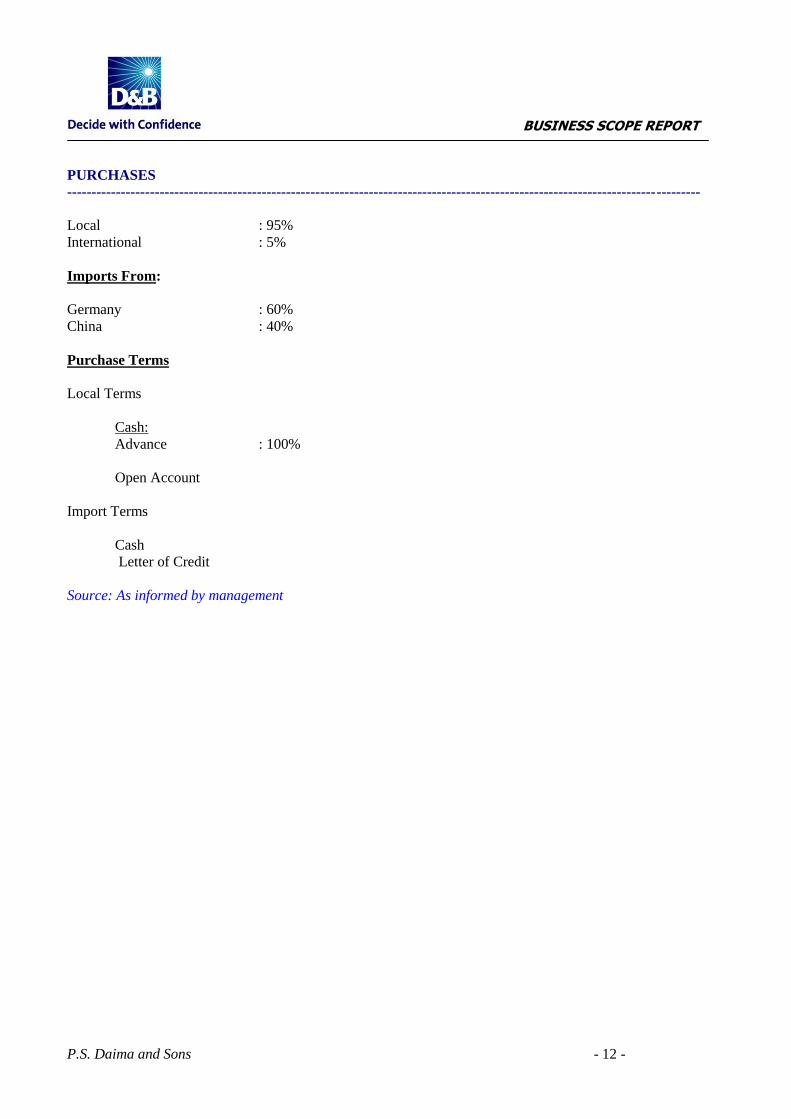

PURCHASES

----------------------------------------------------------------------------------------------------------------------------------

Local : 95%

International : 5%

Imports From:

Germany : 60%

China : 40%

Purchase Terms

Local Terms

Cash:

Advance : 100%

Open Account

Import Terms

Cash

Letter of Credit

Source: As informed by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 13 -

REVENUE

----------------------------------------------------------------------------------------------------------------------------------

International : 100%

Exports To:

Japan

Germany

Italy

United States of America

China

United Kingdom

Australia

South Korea

Europe

Far East

Sales Terms

Export Terms

Cash:

Advance : 30%

Balance on delivery

Source: As informed by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 14 -

CUSTOMERS

----------------------------------------------------------------------------------------------------------------------------------

The Entity maintains around 100 customers.

Major Customer Types

Departmental Stores

Distributor

Manufactures

Wholesalers

Trading Firms

Major Customer Names

Name of Customer Country % of Total

Revenue

Length of

Relationship

(in Years)

Ashro Inc. United States of

America

23 08

Clarks Fork Enterprises United States of

America 05 06

Helby Import Co. United States of

America 04 13

Pandora Production Company Limited Thailand 18 3

Hoapon Development Hong Kong 10 10

Melever Fashion ACC Hong Kong 06 15

SUPPLIERS

----------------------------------------------------------------------------------------------------------------------------------

Name of Supplier Country % of total

Purchases

Length of

Relationship

(Years)

Nazer Niyaz Leathers India 39 5

Jildh India India 15 5

Bhatla Trading Co. India 6 10

Jildh Marketing India 4 5

P. S. Chawla Fabrics India 2 5

Source: As informed by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 15 -

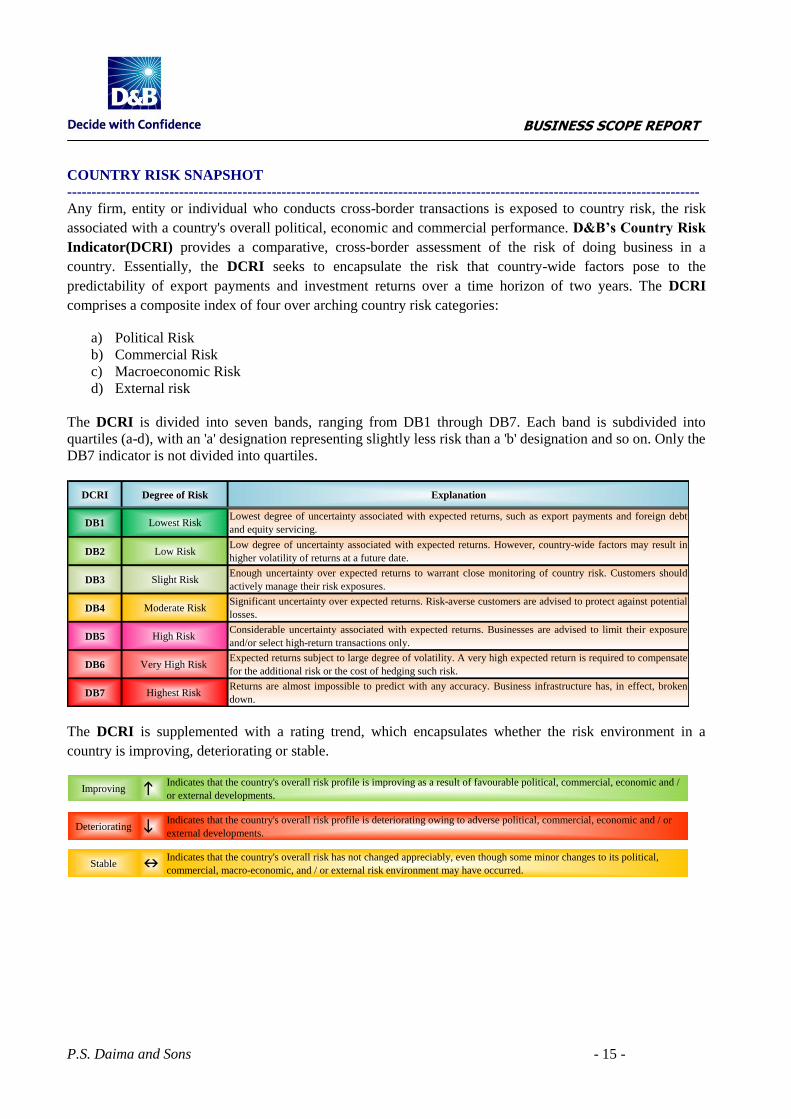

COUNTRY RISK SNAPSHOT

----------------------------------------------------------------------------------------------------------------------------------

Any firm, entity or individual who conducts cross-border transactions is exposed to country risk, the risk

associated with a country's overall political, economic and commercial performance. D&B’s Country Risk

Indicator(DCRI) provides a comparative, cross-border assessment of the risk of doing business in a

country. Essentially, the DCRI seeks to encapsulate the risk that country-wide factors pose to the

predictability of export payments and investment returns over a time horizon of two years. The DCRI

comprises a composite index of four over arching country risk categories:

a) Political Risk

b) Commercial Risk

c) Macroeconomic Risk

d) External risk

The DCRI is divided into seven bands, ranging from DB1 through DB7. Each band is subdivided into

quartiles (a-d), with an 'a' designation representing slightly less risk than a 'b' designation and so on. Only the

DB7 indicator is not divided into quartiles.

The DCRI is supplemented with a rating trend, which encapsulates whether the risk environment in a

country is improving, deteriorating or stable.

DCRI Degree of Risk Explanation

DB1 Lowest RiskLowest degree of uncertainty associated with expected returns, such as export payments and foreign debt

and equity servicing.

DB2 Low RiskLow degree of uncertainty associated with expected returns. However, country-wide factors may result in

higher volatility of returns at a future date.

DB3 Slight RiskEnough uncertainty over expected returns to warrant close monitoring of country risk. Customers should

actively manage their risk exposures.

DB4 Moderate RiskSignificant uncertainty over expected returns. Risk-averse customers are advised to protect against potential

losses.

DB5 High Risk Considerable uncertainty associated with expected returns. Businesses are advised to limit their exposure

and/or select high-return transactions only.

DB6 Very High Risk Expected returns subject to large degree of volatility. A very high expected return is required to compensate

for the additional risk or the cost of hedging such risk.

DB7 Highest Risk Returns are almost impossible to predict with any accuracy. Business infrastructure has, in effect, broken

down.

Improving hIndicates that the country's overall risk profile is improving as a result of favourable political, commercial, economic and /

or external developments.

Deteriorating iIndicates that the country's overall risk profile is deteriorating owing to adverse political, commercial, economic and / or

external developments.

Stable nIndicates that the country's overall risk has not changed appreciably, even though some minor changes to its political,

commercial, macro-economic, and / or external risk environment may have occurred.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 16 -

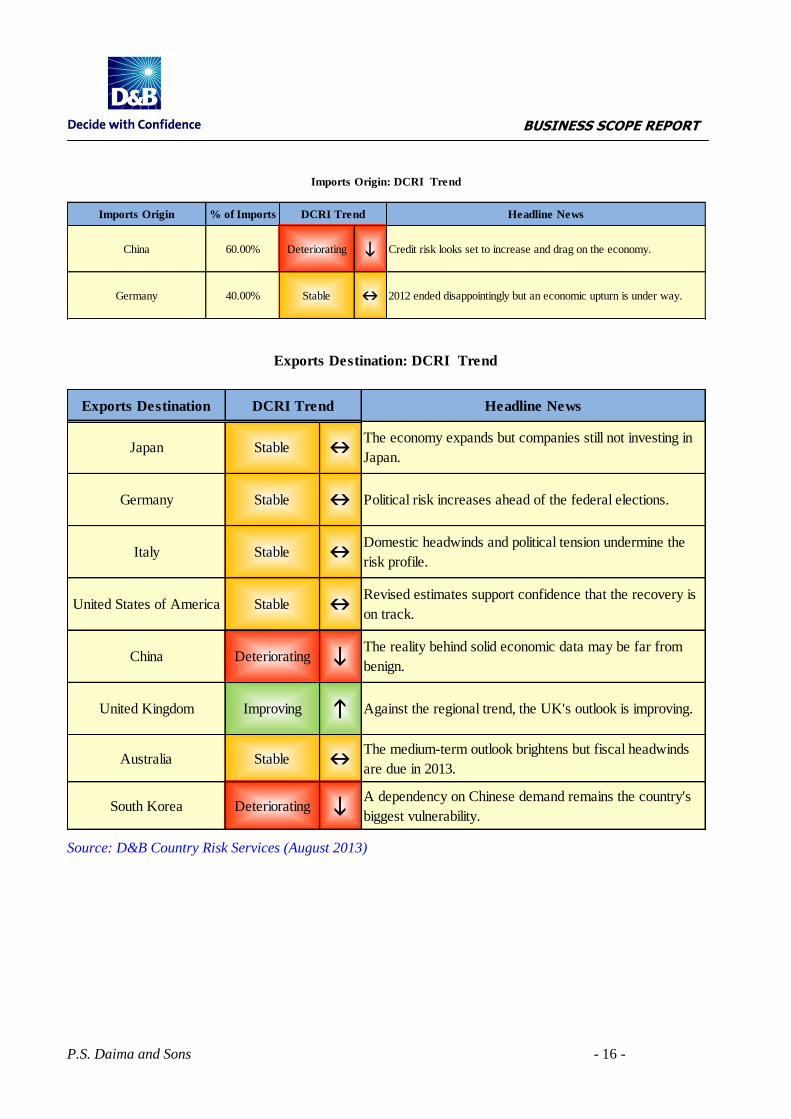

Source: D&B Country Risk Services (August 2013)

Imports Origin % of Imports Headline News

China 60.00% Deteriorating i Credit risk looks set to increase and drag on the economy.

Germany 40.00% Stable n 2012 ended disappointingly but an economic upturn is under way.

DCRI Trend

Imports Origin: DCRI Trend

Exports Destination Headline News

Japan Stable nThe economy expands but companies still not investing in

Japan.

Germany Stable n Political risk increases ahead of the federal elections.

Italy Stable nDomestic headwinds and political tension undermine the

risk profile.

United States of America Stable nRevised estimates support confidence that the recovery is

on track.

China Deteriorating iThe reality behind solid economic data may be far from

benign.

United Kingdom Improving h Against the regional trend, the UK's outlook is improving.

Australia Stable nThe medium-term outlook brightens but fiscal headwinds

are due in 2013.

South Korea Deteriorating iA dependency on Chinese demand remains the country's

biggest vulnerability.

DCRI Trend

Exports Destination: DCRI Trend

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 17 -

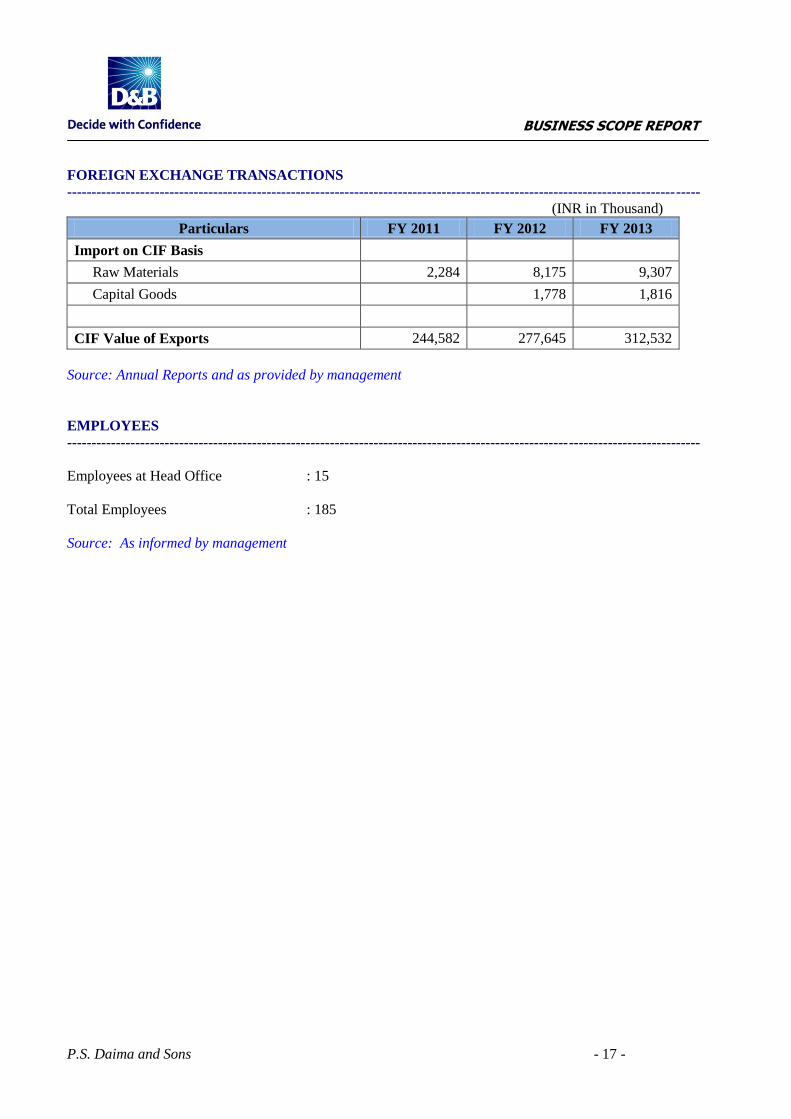

FOREIGN EXCHANGE TRANSACTIONS

----------------------------------------------------------------------------------------------------------------------------------

(INR in Thousand)

Particulars FY 2011 FY 2012 FY 2013

Import on CIF Basis

Raw Materials 2,284 8,175 9,307

Capital Goods 1,778 1,816

CIF Value of Exports 244,582 277,645 312,532

Source: Annual Reports and as provided by management

EMPLOYEES

----------------------------------------------------------------------------------------------------------------------------------

Employees at Head Office : 15

Total Employees : 185

Source: As informed by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 18 -

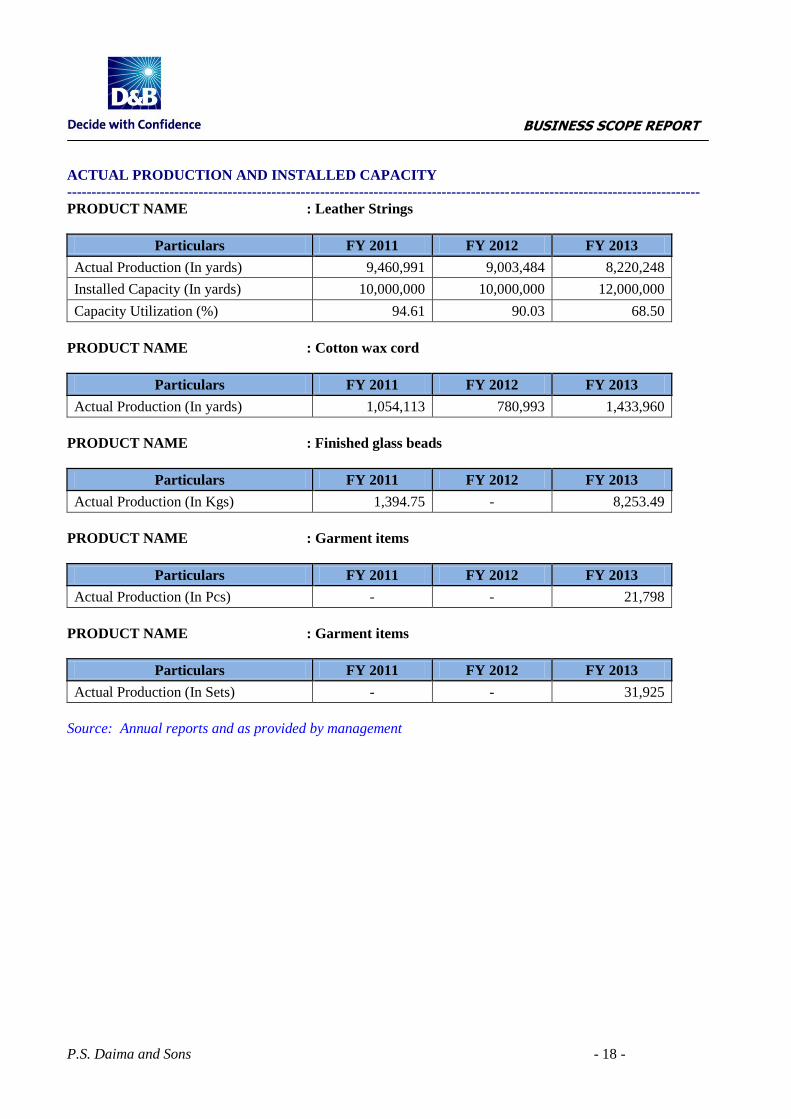

ACTUAL PRODUCTION AND INSTALLED CAPACITY

----------------------------------------------------------------------------------------------------------------------------------

PRODUCT NAME : Leather Strings

Particulars FY 2011 FY 2012 FY 2013

Actual Production (In yards) 9,460,991 9,003,484 8,220,248

Installed Capacity (In yards) 10,000,000 10,000,000 12,000,000

Capacity Utilization (%) 94.61 90.03 68.50

PRODUCT NAME : Cotton wax cord

Particulars FY 2011 FY 2012 FY 2013

Actual Production (In yards) 1,054,113 780,993 1,433,960

PRODUCT NAME : Finished glass beads

Particulars FY 2011 FY 2012 FY 2013

Actual Production (In Kgs) 1,394.75 - 8,253.49

PRODUCT NAME : Garment items

Particulars FY 2011 FY 2012 FY 2013

Actual Production (In Pcs) - - 21,798

PRODUCT NAME : Garment items

Particulars FY 2011 FY 2012 FY 2013

Actual Production (In Sets) - - 31,925

Source: Annual reports and as provided by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 19 -

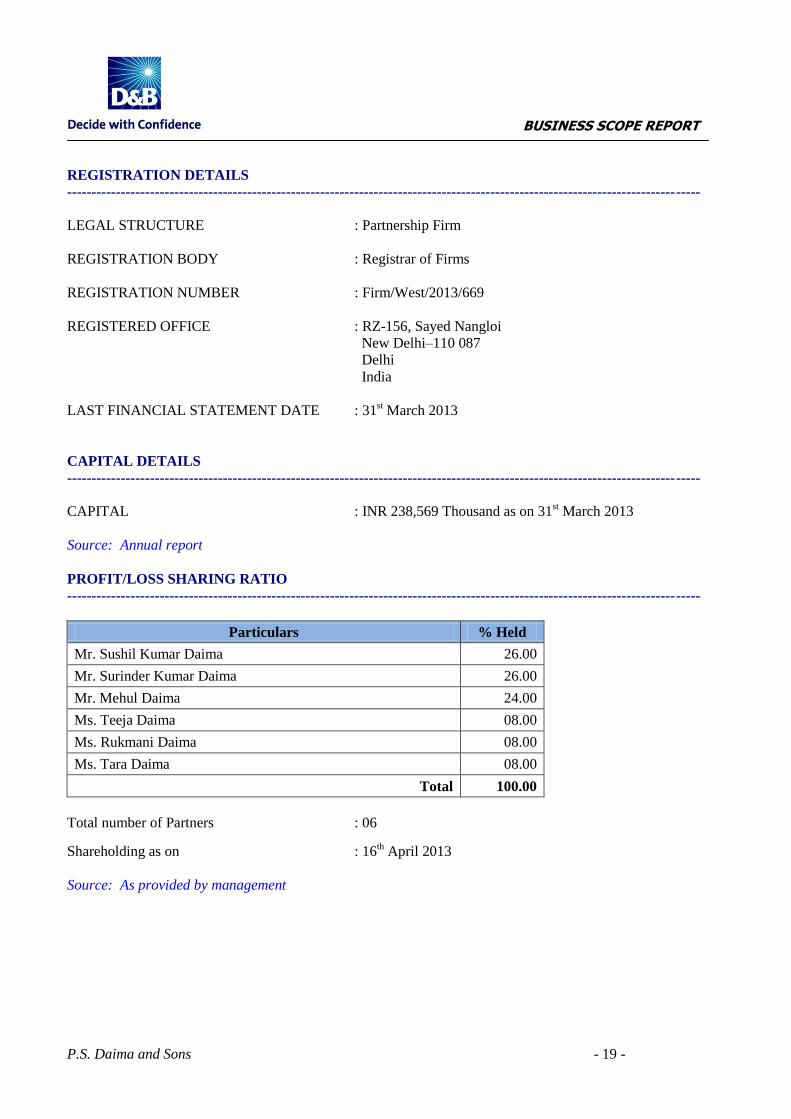

REGISTRATION DETAILS

----------------------------------------------------------------------------------------------------------------------------------

LEGAL STRUCTURE : Partnership Firm

REGISTRATION BODY : Registrar of Firms

REGISTRATION NUMBER : Firm/West/2013/669

REGISTERED OFFICE : RZ-156, Sayed Nangloi

New Delhi–110 087

Delhi

India

LAST FINANCIAL STATEMENT DATE : 31st March 2013

CAPITAL DETAILS

----------------------------------------------------------------------------------------------------------------------------------

CAPITAL : INR 238,569 Thousand as on 31st March 2013

Source: Annual report

PROFIT/LOSS SHARING RATIO

----------------------------------------------------------------------------------------------------------------------------------

Particulars % Held

Mr. Sushil Kumar Daima 26.00

Mr. Surinder Kumar Daima 26.00

Mr. Mehul Daima 24.00

Ms. Teeja Daima 08.00

Ms. Rukmani Daima 08.00

Ms. Tara Daima 08.00

Total 100.00

Total number of Partners : 06 Shareholding as on : 16

th April 2013

Source: As provided by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 20 -

AUDITORS

----------------------------------------------------------------------------------------------------------------------------------

S. S. Poddar & Co.

204-205, Ansal Imperial Tower

C-Block, Community Center

Naraina Vihar

New Delhi-110028

Delhi

India

CORPORATE PARTNERS

----------------------------------------------------------------------------------------------------------------------------------

Name of Directors Current Title

Mr. Sushil Kumar Daima Partner

Mr. Surinder Kumar Daima Partner

Mr. Mehul Daima Partner

Ms. Rukmani Daima Partner

Ms. Tara Daima Partner

Ms. Teeja Daima Partner

Refer Annexure I for details

EXECUTIVES

----------------------------------------------------------------------------------------------------------------------------------

Name of Executives Current Title

Mr. Jagdish Chandra Senior Manager Finance & Accounts

Mr. C. L. Saini Manager Documentation

Mr. Khyal Singh Negi Manager Production (Leather section)

Mr. Granth Singh Manager Production (Garments)

Mr. Ashok Saini Manager Production (Jewellery)

Mr. Sukant Kumar Administration officer

Mr. Satish Kumar Human Resources Officer

Mr. Bamdeo Jha and Mr. Sunder Pal Accounts Officer

Mr. Neak Mohd. Rizvi Purchase Officer

Mr. Anoop Gupta Merchandiser

Mr. Rajesh Kumar Search Engine Optimizer

Source: As provided by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 21 -

BANK

----------------------------------------------------------------------------------------------------------------------------------

NAME : Standard Chartered Bank

BRANCH : New Delhi

BANKER’S REPORT:

The Entity deals with the Standard Chartered Bank since April 2000.

The Entity enjoys the following credit facilities from the bank as on 26thAugust 2013:

(INR in Thousand)

Nature of Facilities Amount

Sanctioned

Amount

Disbursed

Amount

Overdrawn

Pre Shipment Finance/

Post Shipments Finance

50,000 32,100 Nil

LER Limits 6,000 Nil Nil

Total 56,000 32,100 Nil

INSURANCE ----------------------------------------------------------------------------------------------------------------------------- -------------------

The Company has taken insurance coverage on its assets from the United India Insurance Company Limited.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 22 -

HEAD OFFICE LOCATION DETAILS

----------------------------------------------------------------------------------------------------------------------------------

SIZE OF PREMISES : 6,000 square feet

TYPE OF OCCUPATION : Owned

PREMISES USED AS : Administrative & Registered Office

BRANCHES

----------------------------------------------------------------------------------------------------------------------------------

Address Location Type Type of

Occupation

Size of

Premises

45 KM Mile Stone, Delhi –

Rohtak Road, Village Rohad

Tehsil Bahadurgarh, District

Jhajjar, Haryana, India

Factory

Owned 87,120

Square Feet

Source: As provided by management

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 23 -

STATUTORY REGISTRATION

----------------------------------------------------------------------------------------------------------------------------------

Permanent Account Number : AADFP8371L

Import Exporter Code Number : 0500011958 dated 31st May 2000

Entrepreneurs Memorandum Number : 060151200422 (Part-II)

ISO CERTIFICATION

----------------------------------------------------------------------------------------------------------------------------------

The Entity has been awarded ISO 14001:2004 Certification by United Registrar of System B.V. for

Organization’s Environmental Management System

Certificate number : 31058/B/0001/UK/En

Valid from : 2nd

February 2013

Valid till : 1st February 2016

The Entity has been awarded ISO 9001:2008 Certification by TUV SUD for Quality Management

System

Certificate number : TUV100 07 2501

Valid from : 25th February 2013

Valid till : 24th February 2016

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 24 -

MEMBERSHIPS

----------------------------------------------------------------------------------------------------------------------------------

Export Promotion Council for EOUs and SEZ Units.

Delhi Skin & Wool Merchants Association.

Council for Leather Exports.

Apparel Export Promotion Council.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 25 -

FINANCIAL ANALYSIS

----------------------------------------------------------------------------------------------------------------------------------

Revenue and Net Profit

The Entity is engaged in manufacturing and export of leather & leather products, bead kits and beads.

REVENUE

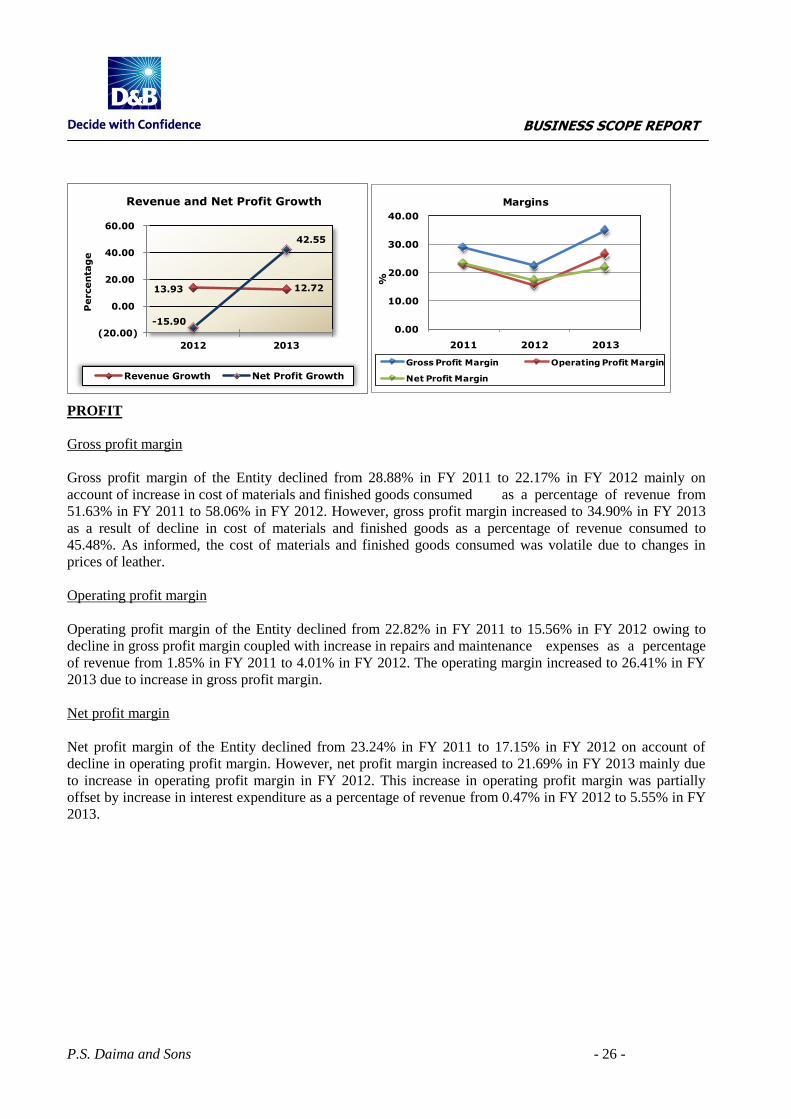

Revenue of the Entity increased by 13.93% in FY 2012 due to increase in sales volume of cotton wax cord.

Revenue of the Entity increased, further, in FY 2013 by 12.72% due to increase in sale of garment items,

upward revision in leather product prices and sale of readymade garments.

56,544

47,554

67,787

0

20,000

40,000

60,000

80,000

2011 2012 2013

IN

R (

In

'0

00

)

Net Profit

Net Profit

243,348 277,243 312,518

0

100,000

200,000

300,000

400,000

2011 2012 2013

IN

R (

In

'0

00

)

Revenue

Revenue

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 26 -

PROFIT

Gross profit margin

Gross profit margin of the Entity declined from 28.88% in FY 2011 to 22.17% in FY 2012 mainly on

account of increase in cost of materials and finished goods consumed as a percentage of revenue from

51.63% in FY 2011 to 58.06% in FY 2012. However, gross profit margin increased to 34.90% in FY 2013

as a result of decline in cost of materials and finished goods as a percentage of revenue consumed to

45.48%. As informed, the cost of materials and finished goods consumed was volatile due to changes in

prices of leather.

Operating profit margin

Operating profit margin of the Entity declined from 22.82% in FY 2011 to 15.56% in FY 2012 owing to

decline in gross profit margin coupled with increase in repairs and maintenance expenses as a percentage

of revenue from 1.85% in FY 2011 to 4.01% in FY 2012. The operating margin increased to 26.41% in FY

2013 due to increase in gross profit margin.

Net profit margin

Net profit margin of the Entity declined from 23.24% in FY 2011 to 17.15% in FY 2012 on account of

decline in operating profit margin. However, net profit margin increased to 21.69% in FY 2013 mainly due

to increase in operating profit margin in FY 2012. This increase in operating profit margin was partially

offset by increase in interest expenditure as a percentage of revenue from 0.47% in FY 2012 to 5.55% in FY

2013.

0.00

10.00

20.00

30.00

40.00

2011 2012 2013

Margins

Gross Profit Margin Operating Profit Margin

Net Profit Margin%

13.93 12.72

-15.90

42.55

(20.00)

0.00

20.00

40.00

60.00

2012 2013

Percen

tag

e

Revenue and Net Profit Growth

Revenue Growth Net Profit Growth

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 27 -

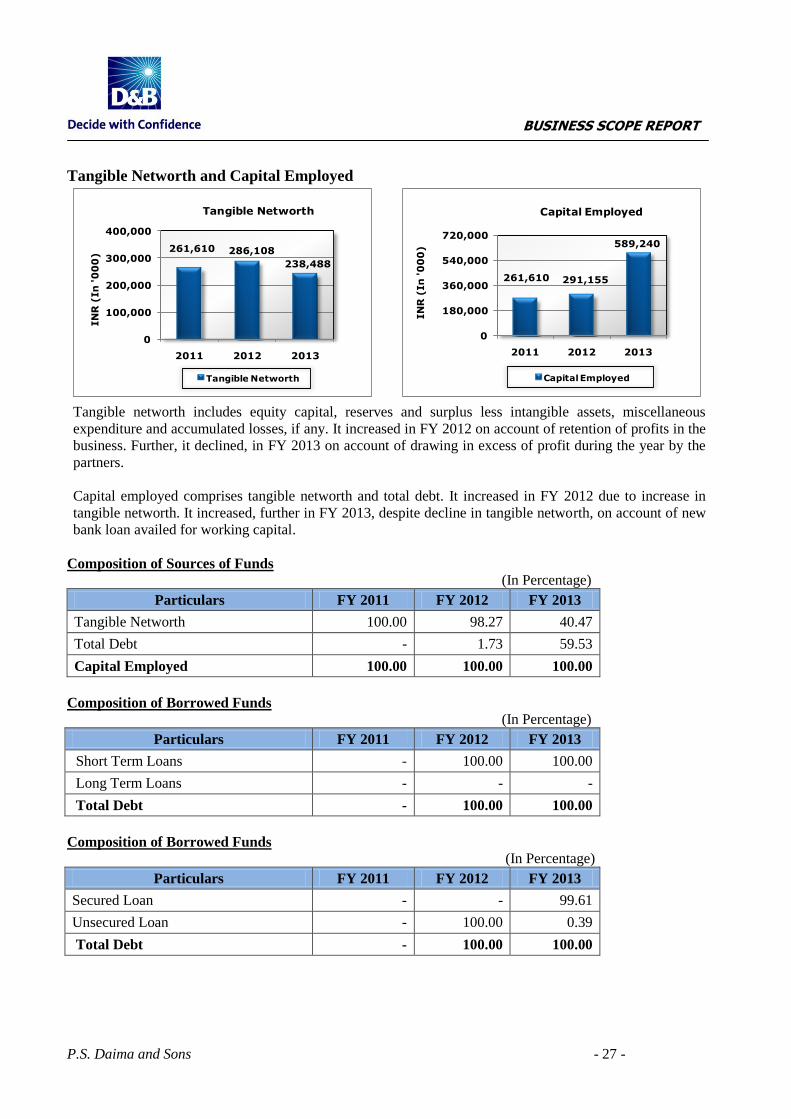

Tangible Networth and Capital Employed

Tangible networth includes equity capital, reserves and surplus less intangible assets, miscellaneous

expenditure and accumulated losses, if any. It increased in FY 2012 on account of retention of profits in the

business. Further, it declined, in FY 2013 on account of drawing in excess of profit during the year by the

partners.

Capital employed comprises tangible networth and total debt. It increased in FY 2012 due to increase in

tangible networth. It increased, further in FY 2013, despite decline in tangible networth, on account of new

bank loan availed for working capital.

Composition of Sources of Funds

(In Percentage)

Particulars FY 2011 FY 2012 FY 2013

Tangible Networth 100.00 98.27 40.47

Total Debt - 1.73 59.53

Capital Employed 100.00 100.00 100.00

Composition of Borrowed Funds

(In Percentage)

Particulars FY 2011 FY 2012 FY 2013

Short Term Loans - 100.00 100.00

Long Term Loans - - -

Total Debt - 100.00 100.00

Composition of Borrowed Funds

(In Percentage)

Particulars FY 2011 FY 2012 FY 2013

Secured Loan - - 99.61

Unsecured Loan - 100.00 0.39

Total Debt - 100.00 100.00

261,610 286,108

238,488

0

100,000

200,000

300,000

400,000

2011 2012 2013

IN

R (

In

'0

00

)

Tangible Networth

Tangible Networth

261,610 291,155

589,240

0

180,000

360,000

540,000

720,000

2011 2012 2013

IN

R (

In

'0

00

)

Capital Employed

Capital Employed

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 28 -

Return on Networth and Return on Capital Employed

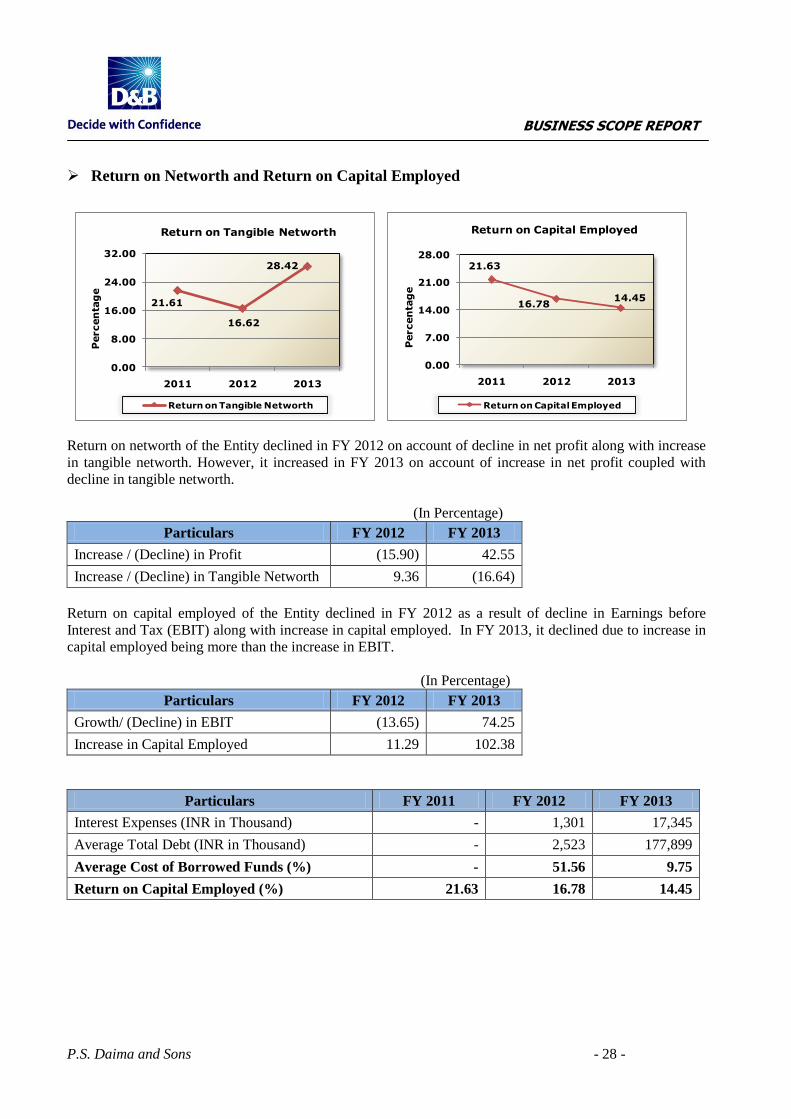

Return on networth of the Entity declined in FY 2012 on account of decline in net profit along with increase

in tangible networth. However, it increased in FY 2013 on account of increase in net profit coupled with

decline in tangible networth.

(In Percentage)

Particulars FY 2012 FY 2013

Increase / (Decline) in Profit (15.90) 42.55

Increase / (Decline) in Tangible Networth 9.36 (16.64)

Return on capital employed of the Entity declined in FY 2012 as a result of decline in Earnings before

Interest and Tax (EBIT) along with increase in capital employed. In FY 2013, it declined due to increase in

capital employed being more than the increase in EBIT.

(In Percentage)

Particulars FY 2012 FY 2013

Growth/ (Decline) in EBIT (13.65) 74.25

Increase in Capital Employed 11.29 102.38

Particulars FY 2011 FY 2012 FY 2013

Interest Expenses (INR in Thousand) - 1,301 17,345

Average Total Debt (INR in Thousand) - 2,523 177,899

Average Cost of Borrowed Funds (%) - 51.56 9.75

Return on Capital Employed (%) 21.63 16.78 14.45

21.61

16.62

28.42

0.00

8.00

16.00

24.00

32.00

2011 2012 2013

Percen

tag

e

Return on Tangible Networth

Return on Tangible Networth

21.63

16.78 14.45

0.00

7.00

14.00

21.00

28.00

2011 2012 2013

Percen

tag

e

Return on Capital Employed

Return on Capital Employed

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 29 -

Total Debt Equity Ratio and Interest Coverage Ratio

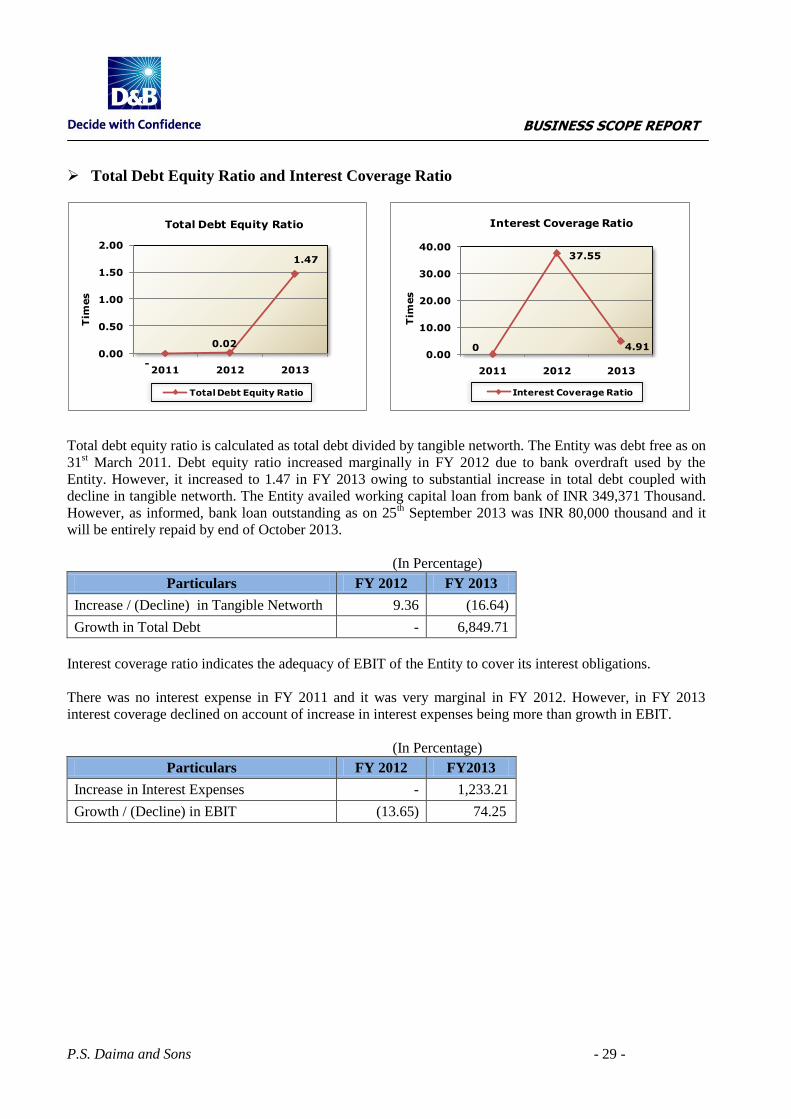

Total debt equity ratio is calculated as total debt divided by tangible networth. The Entity was debt free as on

31st March 2011. Debt equity ratio increased marginally in FY 2012 due to bank overdraft used by the

Entity. However, it increased to 1.47 in FY 2013 owing to substantial increase in total debt coupled with

decline in tangible networth. The Entity availed working capital loan from bank of INR 349,371 Thousand.

However, as informed, bank loan outstanding as on 25th September 2013 was INR 80,000 thousand and it

will be entirely repaid by end of October 2013.

(In Percentage)

Particulars FY 2012 FY 2013

Increase / (Decline) in Tangible Networth 9.36 (16.64)

Growth in Total Debt - 6,849.71

Interest coverage ratio indicates the adequacy of EBIT of the Entity to cover its interest obligations.

There was no interest expense in FY 2011 and it was very marginal in FY 2012. However, in FY 2013

interest coverage declined on account of increase in interest expenses being more than growth in EBIT.

(In Percentage)

Particulars FY 2012 FY2013

Increase in Interest Expenses - 1,233.21

Growth / (Decline) in EBIT (13.65) 74.25

-

0.02

1.47

0.00

0.50

1.00

1.50

2.00

2011 2012 2013

Tim

es

Total Debt Equity Ratio

Total Debt Equity Ratio

0

37.55

4.91 0.00

10.00

20.00

30.00

40.00

2011 2012 2013

Tim

es

Interest Coverage Ratio

Interest Coverage Ratio

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 30 -

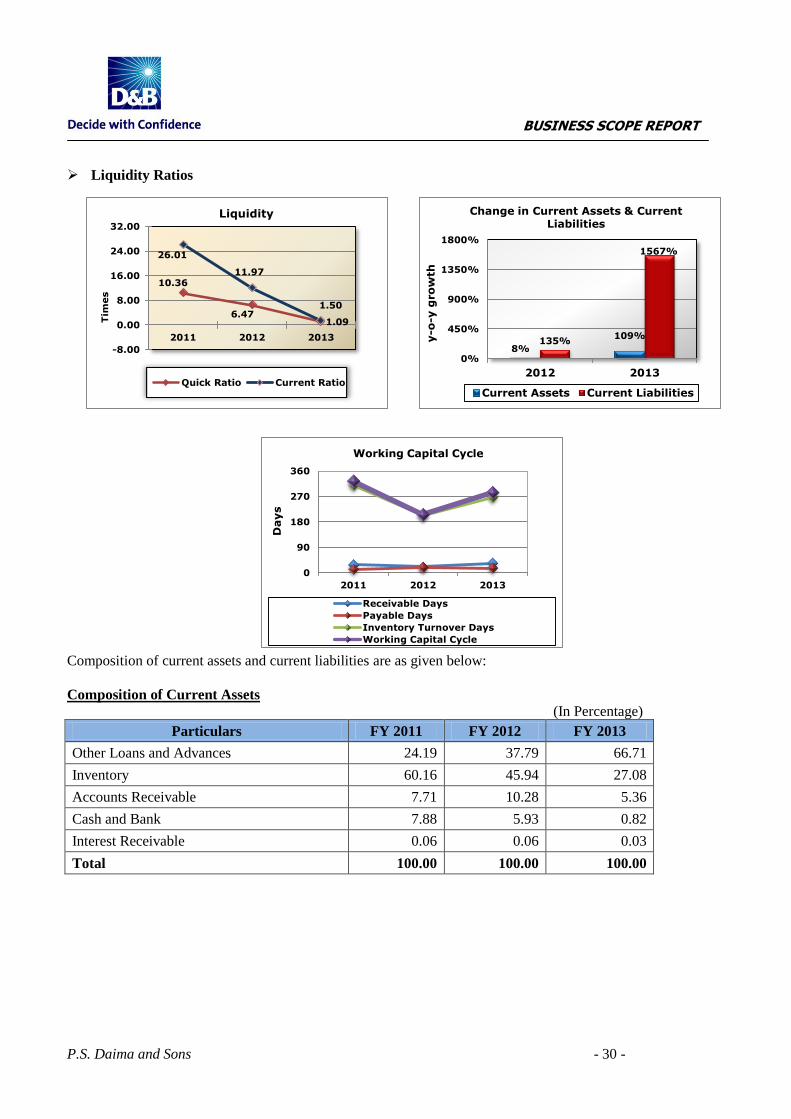

Liquidity Ratios

Composition of current assets and current liabilities are as given below:

Composition of Current Assets

(In Percentage)

Particulars FY 2011 FY 2012 FY 2013

Other Loans and Advances 24.19 37.79 66.71

Inventory 60.16 45.94 27.08

Accounts Receivable 7.71 10.28 5.36

Cash and Bank 7.88 5.93 0.82

Interest Receivable 0.06 0.06 0.03

Total 100.00 100.00 100.00

0

90

180

270

360

2011 2012 2013

Receivable Days

Payable Days

Inventory Turnover Days

Working Capital Cycle

Days

Working Capital Cycle

8%

109%135%

1567%

0%

450%

900%

1350%

1800%

2012 2013

y-o

-y g

ro

wth

Change in Current Assets & Current Liabilities

Current Assets Current Liabilities

10.36

6.471.09

26.01

11.97

1.50

-8.00

0.00

8.00

16.00

24.00

32.00

2011 2012 2013

Tim

es

Liquidity

Quick Ratio Current Ratio

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 31 -

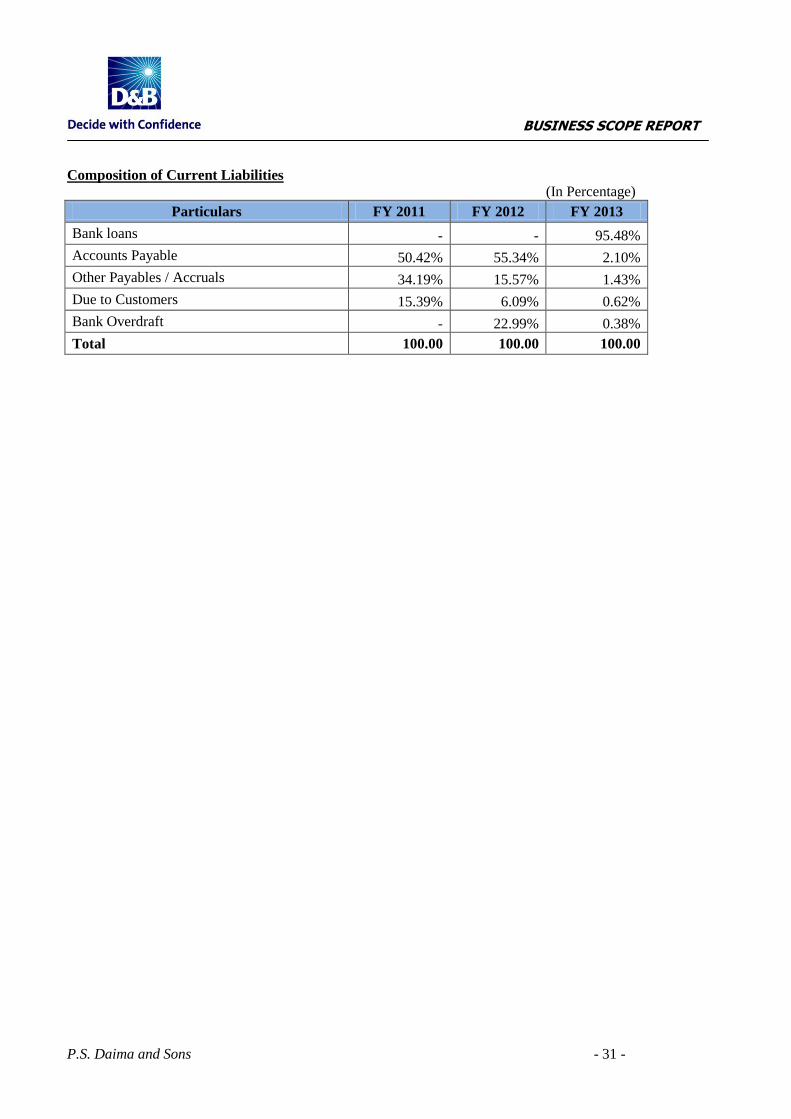

Composition of Current Liabilities

(In Percentage)

Particulars FY 2011 FY 2012 FY 2013

Bank loans - - 95.48%

Accounts Payable 50.42% 55.34% 2.10%

Other Payables / Accruals 34.19% 15.57% 1.43%

Due to Customers 15.39% 6.09% 0.62%

Bank Overdraft - 22.99% 0.38%

Total 100.00 100.00 100.00

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 32 -

ANNEXURE I –PARTNERS

----------------------------------------------------------------------------------------------------------------------------------

Name : Mr. Sushil Kumar Daima

Address : A-1/257, Paschim Vihar

New Delhi - 110065

Delhi

India

Date of Birth : 12thAugust 1965

Passport Number : G2763618

Current Title : Partner

Started with the Entity : 1988

Appointed to Present Position : 04th June 2003

Education : Graduated from University

Related Experience since : 1983

Active in Daily Operations : Yes

Founder of the Entity : Yes

Name : Mr. Surinder Kumar Daima

Address : A-1/257, Paschim Vihar

New Delhi - 110065

Delhi

India

Date of Birth : 25th July 1967

Passport Number : G2488925

Current Title : Partner

Started with the Entity : 1988

Appointed to Present Position : 04th June 2003

Education : Graduated from University

Related Experience since : 1985

Active in Daily Operations : Yes

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 33 -

Name : Mr. Mehul Daima

Address : A-1/257, Paschim Vihar

New Delhi - 110065

Delhi

India

Date of Birth : 08th August 1994

Current Title : Partner

Started with the Entity : 1st April 2013

Appointed to Present Position : 1st April 2013

Education : Under Graduate

Active in Daily Operations : No

Name : Ms. Rukmani Daima

Address : A-1/257, Paschim Vihar

New Delhi - 110065

Delhi

India

Date of Birth : 30th May 1971

Current Title : Partner

Started with the Entity : 31st May 2000

Appointed to Present Position : 31st May 2000

Education : Graduate

Active in Daily Operations : No

Name : Ms. Tara Daima

Address : A-1/257, Paschim Vihar

New Delhi - 110065

Delhi

India

Date of Birth : 08th August 1973

Current Title : Partner

Started with the Entity : 31st May 2000

Appointed to Present Position : 31st May 2000

Education : Under Graduate

Active in Daily Operations : No

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 34 -

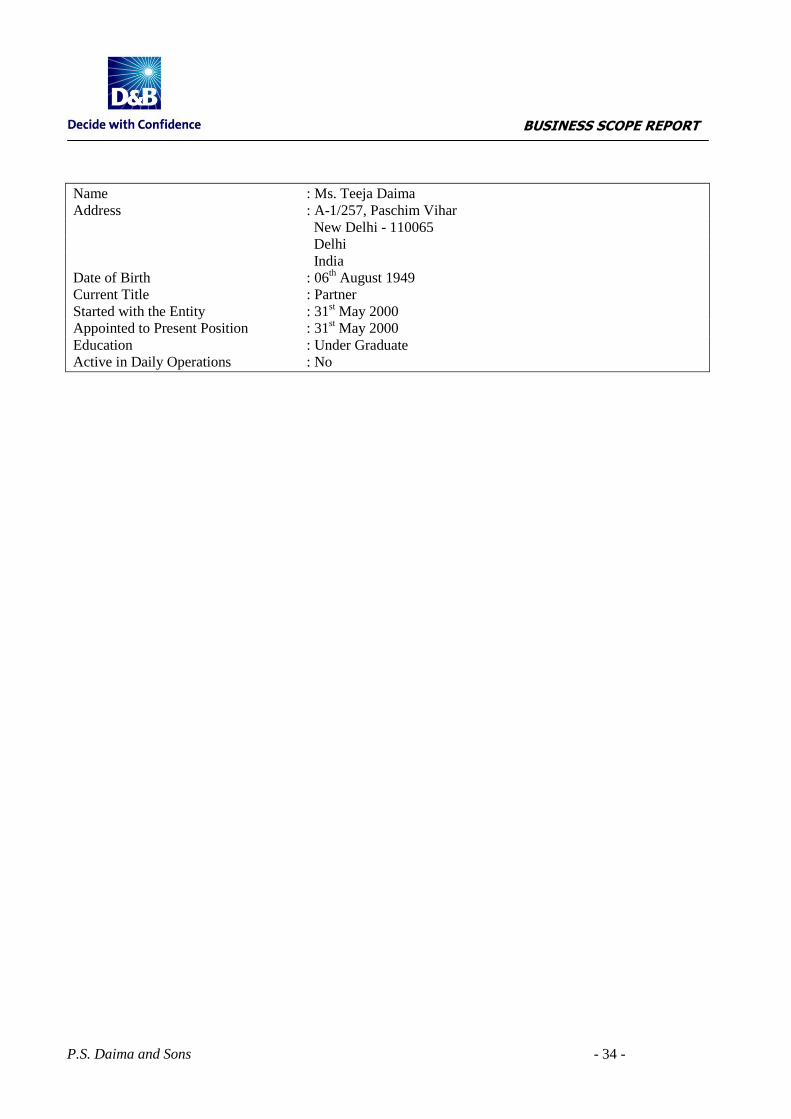

Name : Ms. Teeja Daima

Address : A-1/257, Paschim Vihar

New Delhi - 110065

Delhi

India

Date of Birth : 06th August 1949

Current Title : Partner

Started with the Entity : 31st May 2000

Appointed to Present Position : 31st May 2000

Education : Under Graduate

Active in Daily Operations : No

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 35 -

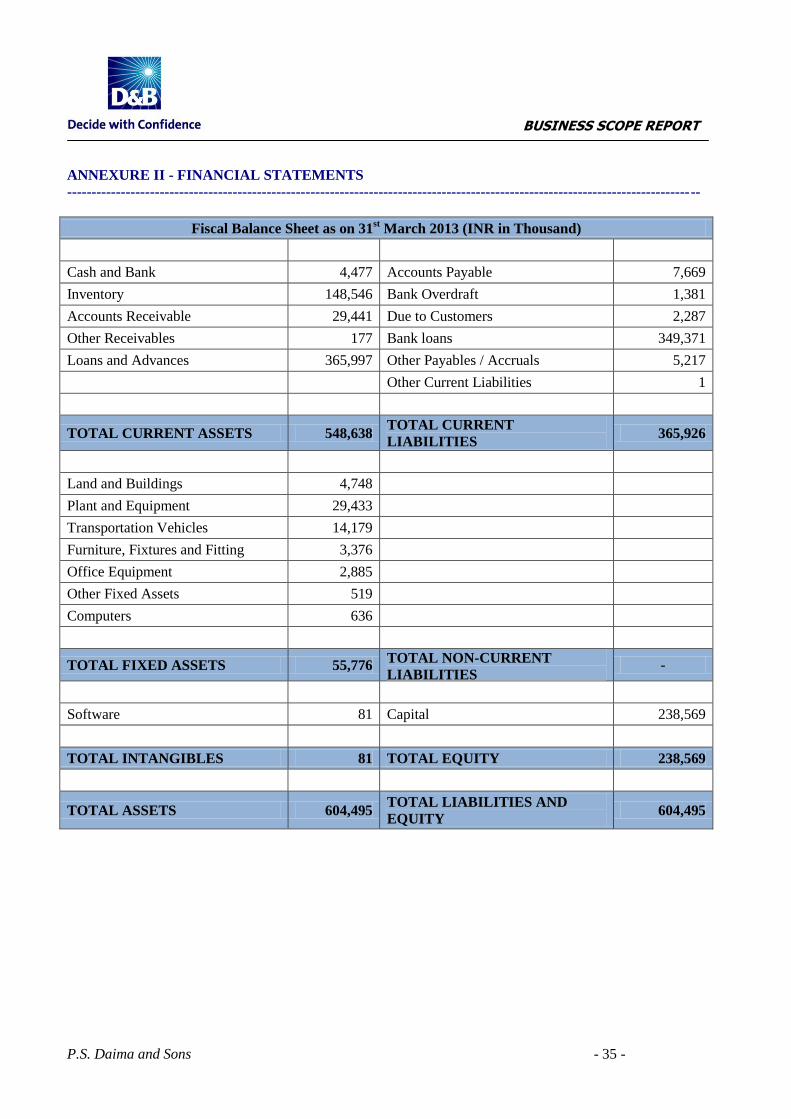

ANNEXURE II - FINANCIAL STATEMENTS

----------------------------------------------------------------------------------------------------------------------------------

Fiscal Balance Sheet as on 31st March 2013 (INR in Thousand)

Cash and Bank 4,477 Accounts Payable 7,669

Inventory 148,546 Bank Overdraft 1,381

Accounts Receivable 29,441 Due to Customers 2,287

Other Receivables 177 Bank loans 349,371

Loans and Advances 365,997 Other Payables / Accruals 5,217

Other Current Liabilities 1

TOTAL CURRENT ASSETS 548,638 TOTAL CURRENT

LIABILITIES 365,926

Land and Buildings 4,748

Plant and Equipment 29,433

Transportation Vehicles 14,179

Furniture, Fixtures and Fitting 3,376

Office Equipment 2,885

Other Fixed Assets 519

Computers 636

TOTAL FIXED ASSETS 55,776 TOTAL NON-CURRENT

LIABILITIES -

Software 81 Capital 238,569

TOTAL INTANGIBLES 81 TOTAL EQUITY 238,569

TOTAL ASSETS 604,495 TOTAL LIABILITIES AND

EQUITY 604,495

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 36 -

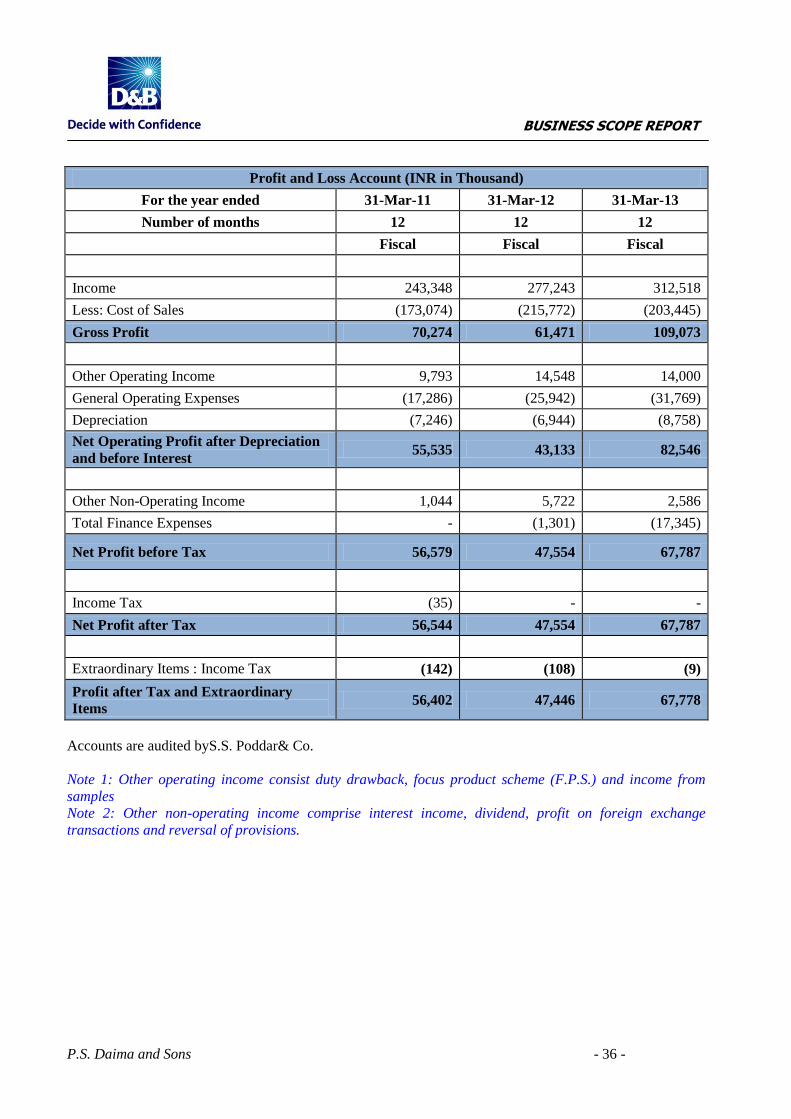

Profit and Loss Account (INR in Thousand)

For the year ended 31-Mar-11 31-Mar-12 31-Mar-13

Number of months 12 12 12

Fiscal Fiscal Fiscal

Income 243,348 277,243 312,518

Less: Cost of Sales (173,074) (215,772) (203,445)

Gross Profit 70,274 61,471 109,073

Other Operating Income 9,793 14,548 14,000

General Operating Expenses (17,286) (25,942) (31,769)

Depreciation (7,246) (6,944) (8,758)

Net Operating Profit after Depreciation

and before Interest 55,535 43,133 82,546

Other Non-Operating Income 1,044 5,722 2,586

Total Finance Expenses - (1,301) (17,345)

Net Profit before Tax 56,579 47,554 67,787

Income Tax (35) - -

Net Profit after Tax 56,544 47,554 67,787

Extraordinary Items : Income Tax (142) (108) (9)

Profit after Tax and Extraordinary

Items 56,402 47,446 67,778

Accounts are audited byS.S. Poddar& Co.

Note 1: Other operating income consist duty drawback, focus product scheme (F.P.S.) and income from

samples

Note 2: Other non-operating income comprise interest income, dividend, profit on foreign exchange

transactions and reversal of provisions.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 37 -

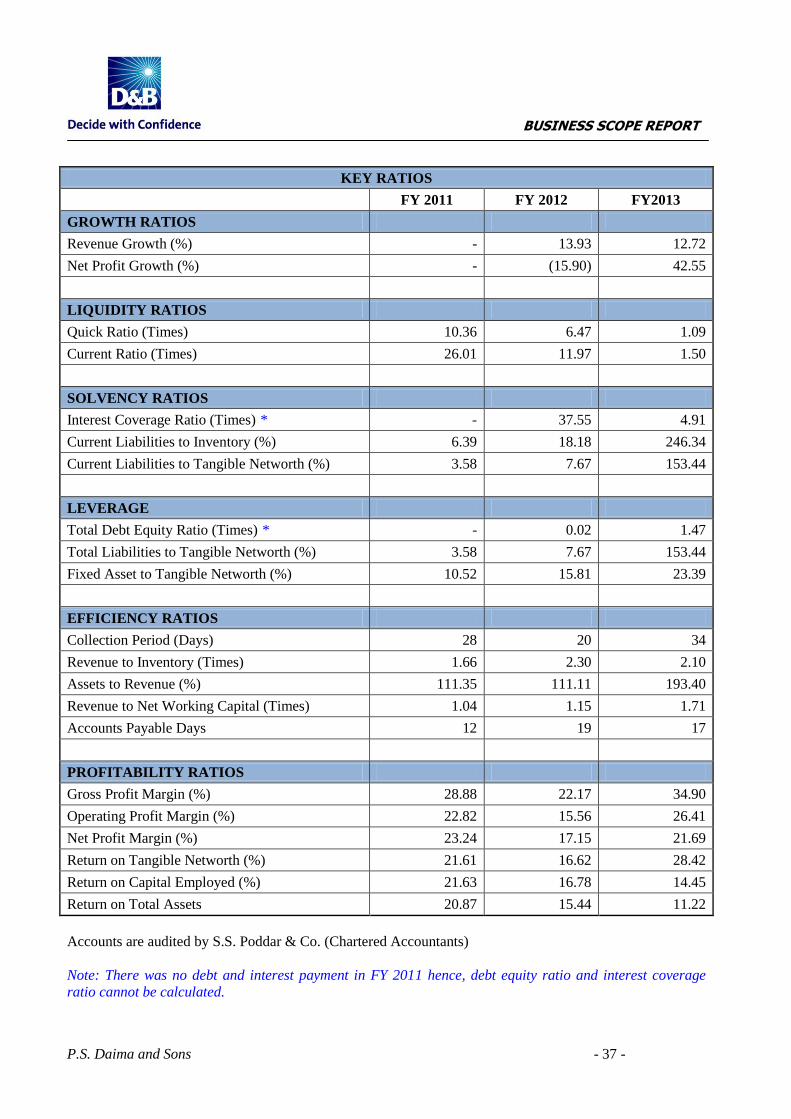

KEY RATIOS

FY 2011 FY 2012 FY2013

GROWTH RATIOS

Revenue Growth (%) - 13.93 12.72

Net Profit Growth (%) - (15.90) 42.55

LIQUIDITY RATIOS

Quick Ratio (Times) 10.36 6.47 1.09

Current Ratio (Times) 26.01 11.97 1.50

SOLVENCY RATIOS

Interest Coverage Ratio (Times) * - 37.55 4.91

Current Liabilities to Inventory (%) 6.39 18.18 246.34

Current Liabilities to Tangible Networth (%) 3.58 7.67 153.44

LEVERAGE

Total Debt Equity Ratio (Times) * - 0.02 1.47

Total Liabilities to Tangible Networth (%) 3.58 7.67 153.44

Fixed Asset to Tangible Networth (%) 10.52 15.81 23.39

EFFICIENCY RATIOS

Collection Period (Days) 28 20 34

Revenue to Inventory (Times) 1.66 2.30 2.10

Assets to Revenue (%) 111.35 111.11 193.40

Revenue to Net Working Capital (Times) 1.04 1.15 1.71

Accounts Payable Days 12 19 17

PROFITABILITY RATIOS

Gross Profit Margin (%) 28.88 22.17 34.90

Operating Profit Margin (%) 22.82 15.56 26.41

Net Profit Margin (%) 23.24 17.15 21.69

Return on Tangible Networth (%) 21.61 16.62 28.42

Return on Capital Employed (%) 21.63 16.78 14.45

Return on Total Assets 20.87 15.44 11.22

Accounts are audited by S.S. Poddar & Co. (Chartered Accountants)

Note: There was no debt and interest payment in FY 2011 hence, debt equity ratio and interest coverage

ratio cannot be calculated.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 38 -

ANNEXURE III–RATING RATIONALE

-------------------------------------------------------------------------------------------------------------------------------

Rating Assigned – 4A2

Tangible Networth- INR 238,488 Thousand as on 31st March 2013.

D&B Indicative Risk Rating of 4A2 implies that the Entity has a tangible networth between INR

129,190,000 and INR 645,949,999 as per latest available audited financial statements. Composite appraisal 2

indicates that the overall status of the Entity is good.

Key Strengths

Experienced management

Long and established relationship with its customers

Stable revenue growth with high margins

Key Constraints

High inventory and advances to supplier resulting in stretched working capital cycle

Demand subject to economic cycles and changes in fashion

Volatility in raw material prices leading to volatile margins and returns

Foreign currency rate fluctuation risk

Concentrated customer base

Compliance with Government regulations

Key sensitivity factors

Ability to maintain gearing at reasonable levels

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 39 -

Key Strengths

Experienced management

Mr. Sushil Kumar Daima and Mr. Surinder Kumar Daima, partners of the Entity have more than 25 years of

experience in the related field. This relevant experience and business networking facilitates in driving the

business of the Entity.

Long and established relationship with its customers

The Entity supplies a range of leather products, nylon and cotton cords to its customers. It has long and

established relations with Helby Import Co., Pandora Production Company Limited, Melever Fashion ACC,

Ashro Inc. with average relationship of around 10 years and derives 51% of total revenue from these

customers. This long term relationship provides revenue visibility to the Entity.

Stable revenue growth with high margins

Revenue of the Entity increased by 13.93% and 12.72 % in FY 2012 and FY 2013 respectively. The Entity

was able to maintain the revenue growth despite decline in revenue from bead products. Revenue from bead

products declined due to it becoming out of fashion. The Entity managed to keep the revenue growth due to

its change in focus to new products like leather jewellery. Though the margins were volatile due to changes

in raw material prices and product mix, those remained at comfortable level. Operating profit margin of the

Entity increased from 22.82% in FY 2011 to 26.41% in FY 2013. Though, it declined in FY 2012, was still

at comfortable level at 15.56%. Net profit margin was also in the comfortable range between 17.15% -

23.24%.

Key Constraints

High inventory and advances to suppliers resulting in stretched working capital cycle

The Entity maintained inventory on average of around 9 months during the review period. As informed, the

irregular supply of raw materials specifically leather compels it to procure and store bulk quantity of raw

materials. Further, leather being moisture sensitive needs special storage and temperature control facilities.

Also, as informed, the Entity needs to pay 2 months advance payments to suppliers to ensure availability of

qualitative and smooth supply of leather. Though, in turn, the Entity receives advances of 30% of order

value from customers, thus mitigating the cash flow mismatch. High inventory level and large funds being

blocked in advances to suppliers resulted in stretched working capital cycle during the review period.

Working capital cycle was high in the range of 204 days to 309 days during review period. Stretched

working capital cycle may lead to short term borrowings to fund short term liquidity gap.

Demand subject to economic cycles and changes in fashion

The Entity is engaged in manufacturing of leather and leather products, beads, cotton and nylon cords.

Demand for beads, one of the major products of the Entity declined sharply during the review period due to

it becoming out of fashion. All the major products of the Entity are subject to cyclical nature of demand due

to changes in fashion and economic cycles. Further, the Entity needs to constantly keep itself updated with

changes in fashion and customize the products as per latest designs.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 40 -

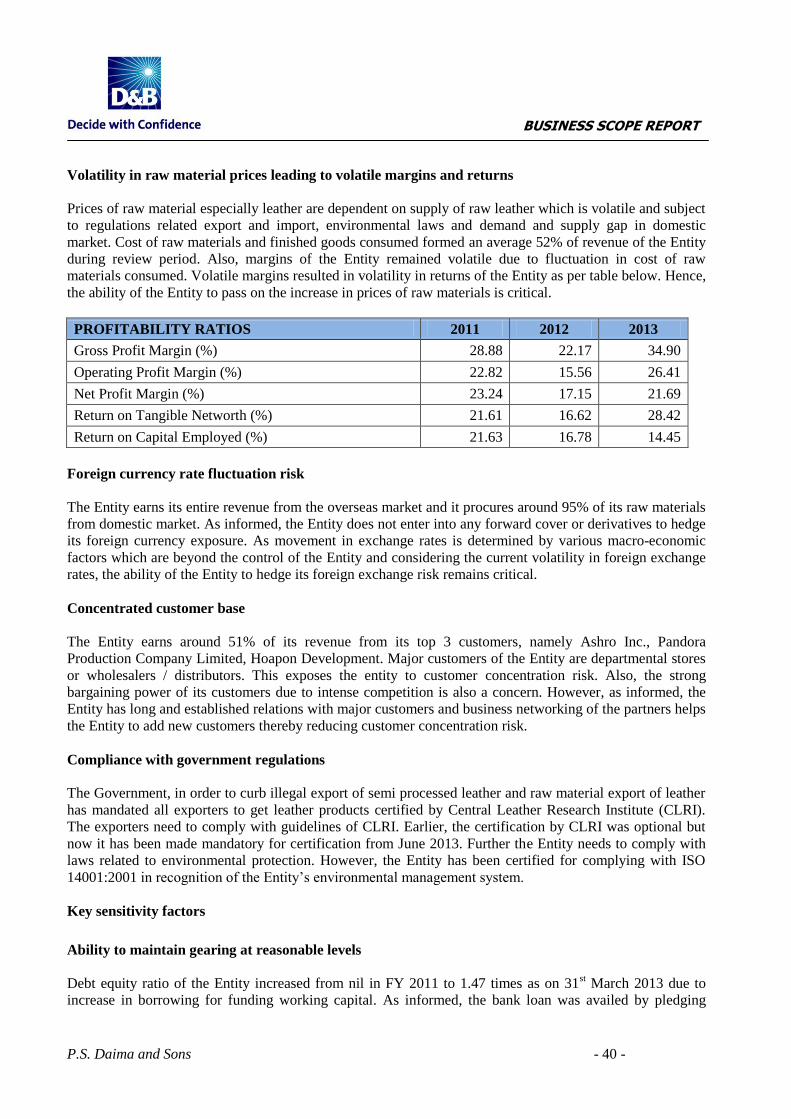

Volatility in raw material prices leading to volatile margins and returns

Prices of raw material especially leather are dependent on supply of raw leather which is volatile and subject

to regulations related export and import, environmental laws and demand and supply gap in domestic

market. Cost of raw materials and finished goods consumed formed an average 52% of revenue of the Entity

during review period. Also, margins of the Entity remained volatile due to fluctuation in cost of raw

materials consumed. Volatile margins resulted in volatility in returns of the Entity as per table below. Hence,

the ability of the Entity to pass on the increase in prices of raw materials is critical.

PROFITABILITY RATIOS 2011 2012 2013

Gross Profit Margin (%) 28.88 22.17 34.90

Operating Profit Margin (%) 22.82 15.56 26.41

Net Profit Margin (%) 23.24 17.15 21.69

Return on Tangible Networth (%) 21.61 16.62 28.42

Return on Capital Employed (%) 21.63 16.78 14.45

Foreign currency rate fluctuation risk

The Entity earns its entire revenue from the overseas market and it procures around 95% of its raw materials

from domestic market. As informed, the Entity does not enter into any forward cover or derivatives to hedge

its foreign currency exposure. As movement in exchange rates is determined by various macro-economic

factors which are beyond the control of the Entity and considering the current volatility in foreign exchange

rates, the ability of the Entity to hedge its foreign exchange risk remains critical.

Concentrated customer base

The Entity earns around 51% of its revenue from its top 3 customers, namely Ashro Inc., Pandora

Production Company Limited, Hoapon Development. Major customers of the Entity are departmental stores

or wholesalers / distributors. This exposes the entity to customer concentration risk. Also, the strong

bargaining power of its customers due to intense competition is also a concern. However, as informed, the

Entity has long and established relations with major customers and business networking of the partners helps

the Entity to add new customers thereby reducing customer concentration risk.

Compliance with government regulations

The Government, in order to curb illegal export of semi processed leather and raw material export of leather

has mandated all exporters to get leather products certified by Central Leather Research Institute (CLRI).

The exporters need to comply with guidelines of CLRI. Earlier, the certification by CLRI was optional but

now it has been made mandatory for certification from June 2013. Further the Entity needs to comply with

laws related to environmental protection. However, the Entity has been certified for complying with ISO

14001:2001 in recognition of the Entity’s environmental management system.

Key sensitivity factors

Ability to maintain gearing at reasonable levels

Debt equity ratio of the Entity increased from nil in FY 2011 to 1.47 times as on 31st March 2013 due to

increase in borrowing for funding working capital. As informed, the bank loan was availed by pledging

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 41 -

personal investments of partners and bank loans outstanding as on 25th September 2013 is of INR 80,000

thousand and will repay entire remainder loan by end of October 2013 through proceeds from personal

savings of the partners. However, considering the working capital intensity of operations, ability of the

Entity to maintain gearing at reasonable levels is critical.

BUSINESS SCOPE REPORT

P.S. Daima and Sons - 42 -

CURRENCY: All amounts in this report are in local currency unless otherwise stated.

-----------------------------------------------------------------------------------------------------------------------------

COPYRIGHT (2013) WITH DUN & BRADSTREET

THIS REPORT MAY NOT BE REPRODUCED IN WHOLE OR

IN PART IN ANY FORM OR MANNER WHATSOEVER. ALL RIGHTS RESERVED.

-----------------------------------------------------------------------------------------------------------------------------

This report is forwarded to the Subscriber in strict confidence for the use by the Subscriber as one factor to

consider in connection with credit and other business decisions. This report contains information compiled

from information which Dun & Bradstreet does not control and which has not been verified unless otherwise

indicated in this report. Dun & Bradstreet therefore cannot accept responsibility for the accuracy,

completeness or timeliness of the report. Dun & Bradstreet disclaims all liability for any loss or damage

arising out of or in anyway related to the contents of this report. This material is confidential and proprietary

to Dun & Bradstreet and/or third parties and may not be reproduced, published or disclosed to others without

the express authorization of Dun & Bradstreet or the General Counsel of Dun & Bradstreet.

-- End of Report --

![Epidemiological week 17 of 2013 [22 – 28 April 2013 ... · Epidemiological week 17 of 2013 [22 – 28 April 2013] National Summary Completeness & Timeliness of Reporting This week,](https://img.pdfslide.us/doc/110x75/5fa50fcd9f2c4578e01d1032/epidemiological-week-17-of-2013-22-a-28-april-2013-epidemiological-week-17.jpg)

![Epidemiological week 41 of 2014 [6th October 12th October ... · Epidemiological week 41 of 2014 [6th October– 12th October 2014] National Summary Completeness & Timeliness of Reporting](https://img.pdfslide.us/doc/110x75/5fab43f25ee882655f225ba9/epidemiological-week-41-of-2014-6th-october-12th-october-epidemiological-week.jpg)