Embed Size (px)

Citation preview

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 1/9

EXAMTIMES2013P19❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙ In association with THE INSTITUTEOF EDUCATION

Business

EXAMSTRUCTURE

BusinessStudies (Honours)has2 papers

Totalmarks:400

Paper1 -2½ hours(240marks)

SectionA: 80Marks- Answer20 shortquestions(nochoice)

SectionB: 160Marks-Answer4 questionsoutof (Allquestionscarry 40marksin SectionB)

Paper2 -2hours(160marks)

Answer 4 questions out of 6.(All questions carry equalmarks, of 40 marks per ques-tion.)

TIMING

Paper1 -2½hours

■ 5 minutesreadingtime

■ SectionA-45minutes

■ Section B - 25 minutes foreachquestion

Paper2 -2hours

■ 4 minutesreadingtime■ 29 minutes for each ques-tion

Every year there has been aquestion on Budgeting, Trial

Balance, Final Accounts, Eco-nomics, Banking and Finance,Business Documents, and ClubAccounts.

Other very important areasinclude Insurance, At WorkandThe Consumer.

GENERALADVICE

1. Answeryour favourite topicfirst of all. Thiswillgiveyou thefeel good factor and make youmore relaxed when answeringtherestofthepaper.

2.Stick as close as possible tothetimelimitslistedabove.Stu-dentsoftenrunout oftimeandmay have only ten minutes leftwhenansweringtheir lastques-tion.

3.Make sure you have a good

workingcalculator.

4.Purchasepreviousexamina-tion papers and practise asmany questions as possiblefromthese papers.

5.The bookkeeping sectioncan be predicted quite easily.This section cannot be learntand must bepractised continu-ously. Areas like Final Ac-counts, the Trial Balance andClub Accounts are examinedeveryyear.

Inpreviousyearsthese threetopics have accounted for over30 per cent of the total marksfromPaper1 andPaper2.

6. Ifyou have thetime,answermore than the four questionsonPaper1(SectionB)andonPa-per2.

You will be marke d out of yourfour bestquestions.

7.Have plenty of rough workpagesfor calculations andkeepthese closeto therelevantques-tions.

8.Whenansweringany theoryquestion make sure to stateyourpoint,givea briefexplana-tion of your point and capit off withan example.

9. Do not leave the examina-tionhall early.

WHERE STRATEGY COUNTS

FREQUENCY OFEXAM TOPICS(ExcludingSection A ofPaper 1)

Students shouldmake sure theyunderstandexactly how muchtime they shouldspend on eachquestion, advisesArthur Russell

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 2/9

P20EXAMTIMES2013 THEIRISHTIMES ❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙

Thefollowing areas must beincludedin yourstudy plans.It isim-portant to remember that this is not an exhaustive list of topicsnorisitmeanttobealistofquestionsthatwillappearintheJuniorCert2013.

Allfiguresbelowarein¤

FINALACCOUNTSOF LIMITEDCOMPANIES

Thisis a questionwhichisexaminedeveryyearin Paper2.

The following Trial Balance was extracted from the books of N.Halloran and N. Lawlor Ltd. on 31 Dec. 2012. The AuthorisedShareCapitalis 500,000¤1 Ordinary shares.

TrialBalance

You are given the following additional information on December31st,2012.

1) Closingstock¤22,000.2)Insuranceprepaid ¤500.3)Rent receivable prepaid ¤2,000.4)Depreciation: machinery25 percentof costper annum.

motor vehicles20percentof cost perannum.

You are required to prepare the company’s trading, profit and lossand appropriation accounts for the year ending December 31st,2012and a balancesheet ason that date.

Beforewe begin anumberof pointsmustbe considered:

a)On thedebitsideof thetrialbalanceappearsallof theexpensesand assets. On the credit side appears all of the gains andliabilities.

b)Everyiteminthetrialbalanceappearsonceinthetrading,prof-itandlossand balance sheet.

c) All of the adjustments appear twice in the trading, profit andlossand balancesheet asfollows:

1. Closingstock isrecorded in the tradingaccount andin thebal-ance sheetas acurrent asset.

2.Insurance prepaidisrecordedin theprofitand lossaccount asaminusfromtheinsurancepaidfigureandinthebalancesheetasacurrentasset.

3. Rent receivable prepaid is recorded in the profit and lossaccount as a minus from the rent receivable figure and in thebalancesheetas a currentliability.

4.Depreciationis recordedasan expenseinthe profitandlossac-

countand asa minusfromfixedassetsin balance sheet.Thefollowingis a suggestedsolution:

TradingAccountfor yearendingDecember31st, 2012

ProfitandLossAccountfor yearendingDecember31st, 2012

BalanceSheetasat December31st,2012

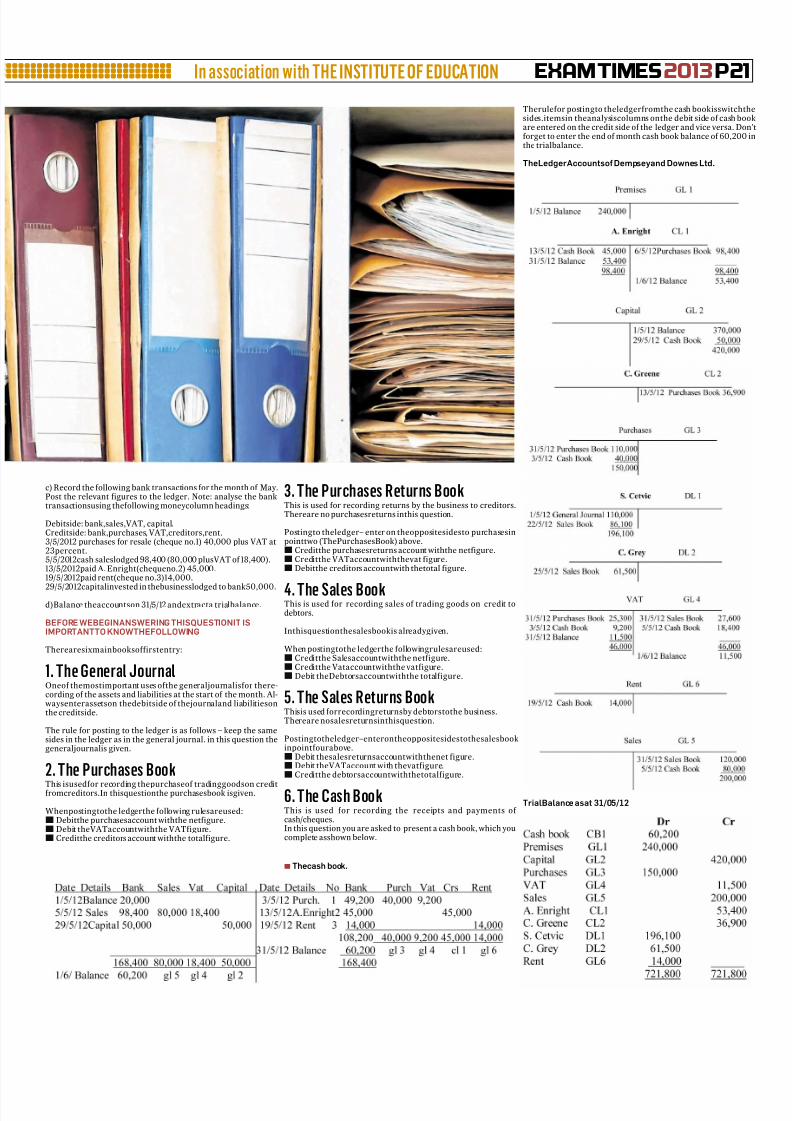

BOOKS OFFIRST ENTRY& LEDGERThisis a questionwhichis examinedeveryyearin Paper2.

KateDempsey andEmerDownesLtd hadthe following balancesinthe generaljournalon theMay1st,2012.

GeneralJournal

a) Post the balancesin the general journalto therelevant ledgeraccounts.

b)Postthe relevant figuresfromthe purchasesand salesbookstothe ledgers.

PurchasesDayBook

SalesDayBook

TYPICALACCOUNTING

QUESTIONS

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 3/9

EXAMTIMES2013P21❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙ In association with THE INSTITUTEOF EDUCATION

c) Record the following bank transactions for the month of May.Post the relevant figures to the ledger. Note: analyse the banktransactionsusing thefollowing moneycolumn headings:

Debitside: bank,sales,VAT, capital.Creditside: bank,purchases, VAT,creditors,rent.3/5/2012 purchases for resale (cheque no.1) 40,000 plus VAT at23percent.5/5/2012cash saleslodged 98,400 (80,000 plusVAT of 18,400).13/5/2012paid A. Enright(chequeno.2) 45,000.19/5/2012paid rent(cheque no.3)14,000.

29/5/2012capitalinvested in thebusinesslodged to bank50,000.

d)Balance theaccountson 31/5/12 andextracta trialbalance.

BEFOREWEBEGINANSWERINGTHISQUESTIONIT ISIMPORTANTTOKNOWTHEFOLLOWING

Therearesixmainbooksoffirstentry:

1. TheGeneral JournalOneof themostimportant uses ofthe generaljournalisfor there-cording of the assets and liabilities at the start of the month. Al-waysenterassetson thedebitside of thejournaland liabilitiesonthe creditside.

The rule for posting to the ledger is as follows – keep the samesides in the ledger as in the general journal. in this question thegeneraljournalis given.

2. The Purchases BookThis isusedfor recording thepurchaseof tradinggoodson creditfromcreditors.In thisquestionthe purchasesbook isgiven.

Whenpostingtothe ledgerthe following rulesareused:■ Debitthe purchasesaccount withthe netfigure.■ Debit theVATaccountwiththe VATfigure.■ Creditthe creditors account withthe totalfigure.

3. The Purchases Returns BookThis is used for recording returns by the business to creditors.Thereare no purchasesreturns inthis question.

Postingto theledger– enter on theoppositesidesto purchasesinpointtwo (ThePurchasesBook) above.■ Creditthe purchasesreturns account withthe netfigure.■ Creditthe VATaccountwiththevat figure.■ Debitthe creditors accountwith thetotal figure.

4. The Sales BookThis is used for recording sales of trading goods on credit todebtors.

Inthisquestionthesalesbookis alreadygiven.

When postingtothe ledgerthe followingrulesareused:■ Creditthe Salesaccountwiththe netfigure.■ Creditthe Vataccountwiththe vatfigure.■ Debit theDebtorsaccountwiththe totalfigure.

5. The Sales Returns BookThisis used forrecordingreturnsby debtorstothe business.Thereare nosalesreturnsinthisquestion.

Postingtotheledger–enterontheoppositesidestothesalesbookinpointfourabove.■ Debit thesalesreturnsaccountwiththenet figure.■ Debit theVATaccount with thevatfigure.■ Creditthe debtorsaccountwiththetotalfigure.

6. The CashBookThis is used for recording the receipts and payments of cash/cheques.In this question you are asked to present a cash book, which youcomplete asshown below.

Therulefor postingto theledgerfromthe cash bookisswitchthesides.itemsin theanalysiscolumns onthe debit side of cash bookare entered on the credit side of the ledger and vice versa. Don'forget to enter the end of month cash book balance of 60,200 inthe trialbalance.

TheLedgerAccountsofDempseyand DownesLtd.

TrialBalanceasat 31/05/12

■ Thecash book.

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 4/9

P22EXAMTIMES2013 THEIRISHTIMES ❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙

RATIOANALYSISThisQuestionmay appearinPaper1 orPaper2.

Thefollowing isa typicalratio analysisquestion.F MaguireandLMorgan Ltd is a squash ball manufacturing company. Examinethefollowingfinalaccountsand balancesheetsfor 2011 and2012and compare and comment on the performance and state of affairs of the company for the two years. Include as part of youranswerthe following:

1.The acidtest ratio.2.The returnon capitalemployed.3.ThegrossProfit Margin.4.Therate ofdividendpaid.5. Thestock turnover ratio.6. Mark-up.

2011Income Statement

Balance Sheet

2012Income Statement

Balance Sheet

SOLUTION

1.AcidTestRatio – thisis a liquidity measurementwhichshowswhetherornotthe companyisableto payitscurrentliabilitiesoutof itsliquid assets.Liquid assetsare assetsthat canbe easilycon- verted into cash.

Formula: CurrentAssets– ClosingStock–––––––––––––––––––––––––––––

CurrentLiabilities

2011 30000 –8,000–– –– –– ––– ––– –– – = 0 .4 1: 1

54,000

2012 74,000 –10,000–––––––––––––––– =2.1:1

30,000

Thenormis1:1.Intheyear2012thecompanyisliquid,ieitcanpay itscurrentliabilitiesoutof itsliquidassets.Forevery¤1of currentliabilitiesthere is¤2.1 ofliquid assets.

2.Returnon CapitalEmployed–thisisameasurementofprofita-bilityor howefficiently managementis using theresourcesmadeavailableto itby itsshareholdersandby thebanks.

Formula: Net Profit––––––––––––––––––––––CapitalEmployedx 100

2011 366,000–––––––––––––––– =54.14%

676,000 x 100

2012 58,000–––––––––––––– = 9 .01%644,000x 100

Thefirmis profitableearninga returnwellin excessof thereturnfromriskfreeinvestmentsof three percent.Howeverprofitabili-

ty is declining so management would want to takestepsto elimi-natethis declinesuch ascutting expenses andraising revenue.

3.GrossProfit Margin – thisis anothermeasureof profitability.

Fo rmula: Gro ss Pro fit––––––––––– X 100

Sales

2011 466,000––––––––– X 100 = 77.67%600,000

2012 208,000––––––––– X 100 = 57.8%360,000

Thegrossmarginhasfallen from 78percent in2011to 58percentin2012butis still wayabove theaverageof 30percent.

4. Rate of Dividend Paid – the dividend is the part of the profitpaidto the shareholders.

Formula: Dividend––––––––––––––––––ShareCapitalX 100

2011 30,000– ––– ––– –– –– ––– ––– = 4 2. 8%

70,000X100

2012 20,000–––––––––––––– = 28.57%70,000 x 100

Thedividendhasworsenedon the2011figurebutisstillwayabovetheaverage of three percent. Shareholders would be veryhappy

withtheir return.

5. Stock Turnover – measures the number of times the averagestock issoldoffeach year.

Formula: Cost of Sales–––––––––––––AverageStock

AverageStock = openingstock +closing stock–––––––––––––––––––––––––––––––––––––––––––

2

2011 134,000–––––––––13.4ti =13.4times

10,000

2012 152,000––––––––– = 1 6.9 t ime s

9,000

In2012the companyis sellingoffits average stocknearly17timeswhich is a big improvement on 2011. The high stock turnovermight indicate that thisbusinessis involvedinthe grocerytrade.

6.The Mark-Up –This isanother measure of profitability.

Formula: GrossProfit––––––––––– X 100

Cost ofSales

2011 466,000––––––––––––– =347.8%

134,000X 100

2012 208,000––––––––––––– =136.84%

152,000 X100

Themark-up hasfallensubstantiallybut isstillextremelyhigh in2012.

CONCLUSIONThefirmisliquid,highlyprofitable(eventhoughprofitabilityisdi-simproving rapidly) and is paying an excellent dividend to itsshareholders.

Otherratiosand percentagesthat couldbe examined are:

1.TheCurrentRatio: CurrentAssets–––––––––––––––

CurrentLiabilities

2. TheNet ProfitPercentage: NetProfit–––––––––––X 100

Sales

THEACIDTEST

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 5/9

EXAMTIMES2013P23❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙ In association with THE INSTITUTEOF EDUCATION

BANKRECONCILIATIONSTATEMENTSRoryMurphyLtd.hasa currentaccountin theKatieMullinBank.Thecompany receivedthe following BankStatement on Decem-ber31st, 2012:

The company compared the above bank statement with its owncash bookrecordsbelow:

CashBook

You are required to:a)Correct thecashbook.b) Prepare a bankreconciliation statement.

From the above you can see that the balance in the cash book of

¤1,145 is different from the balance on the bank statement of ¤275.

PROCEDURE1.Tickofftheitemsthatappearinboththecashbookandthebankstatement andyouwillfinda numberof itemsnot inboth.a) In the cash book and not in the bank statement there are twoitems:

Dec.31 Lodgementof ¤800Dec.19 Chequepaidto C.White(no.133)for¤70

b)Inthebankstatementnotinthecashbooktherearefouritems:Dec.15 StandingOrder ¤130Dec.17 DirectDebit ¤90Dec.19 CreditTransfer ¤110Dec.29 BankCharges ¤30

2.Correctthecashbookby enteringtheitems onthe bankstate-mentnotyetinthecashbookintothecashbookasshownbelow.

Note: remember to switch sides when completing task numbertwoandtasknumberthree.

3. Correct the bank statement by entering the items in the cashbook not yet in the bank statement, into the bank statement asshownbelow.

SOLUTION

CashBook

BankReconciliationStatement as at 31/12/2011

Theclosingbalanceinthecashbookof¤1,005nowequalstheclos-ingbalancein thebankstatementof¤1,005.

CLUBACCOUNTS

Thisquestionnormallyappearsin Paper1.

TheT Hennessy Tennis Club hadthe following assetsand liabili-tiesat 1/1/2012:premises620,000;bar stock3,000;cash 50,000;accumulated fund 673,000. The Clubtreasurer I Byrne has pro-

vided the following account of the clubs activities during the yearfortheChairperson DEppelandfor theSecretary J Fehily.

Receiptsand PaymentsAccount

The following information should also be considered at31/12/2012:1) BarStock ¤14,000.2) Subscriptionsdue ¤8,000.3)Subscriptions prepaid¤3,000.4)DepreciationEquipmentby 20percent.5) Insurancedue 2,000.

Prepare:a)A bartradingaccountforyearending31/12/2012.b) An income and expenditure account for year ending31/12/2012.c)A balancesheetasat 31/12/2012.

SOLUTION

a) BarTrading Accountfory/e 31/12/2012

b) Income& Expenditure Accountfory/e 31/12/2012

c) BalanceSheetas at31/12/2012

Ascanbe seenfromthisquestionclubaccountsareverysimilartofinalaccountsexcept thatthe terminologyis changed:

■ Thereceiptsandpaymentsaccountisthe sameas acashbook.

■ The income and expenditure account is the same as a profitandloss account.

■ Excessofincomeisthesameasnetprofit.

■ Accumulatedfund is thesame ascapital.

CORRECTIONSANDRECONCILIATIONS

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 6/9

P24EXAMTIMES2013

1. CONTROL ACCOUNTSA popular SectionA questionon Paper 1 isone ona Debtors oraCreditors Control Account, e.g. from the following informationprepare theCreditorsControlAccount of Yogi Bear Ltd.

¤T ot al C re di t Pur ch as es 8 5, 00 0TotalPurchasesReturns 9,000TotalCashpaidto Creditors 24,000

CreditorsControl Account

Ifasked tocomplete a Debtors ControlAccount the entriesareontheoppositesidestotheabove:

DebtorsControl Account

2. INSURANCE PREPAIDOn 1 July 2012, N. Garveyand C. GreenblattLtd paid itsinsur-ancepremiumof ¤8,000for12 monthsfromthat date.The insur-ance account had an opening debit balance of ¤3,000 on 1 Jan2012.Showthe Insurance Accountfor the yearended 31/12/2012.

InsuranceAccount

The ¤4,000 balance at 31 December 2012 is the insurance pre-paid for6 monthsof theyear2013.

The¤8,000paidisfor theperiod from1 July 2012 until30 June2013,therefore sixtwelfths of ¤8,000 equalsthe ¤4,000 prepaidgoinginto theyear2013.

Theamountprepaidis subtractedfrom theamountpaidto re-duce the amount sent to the Profit and Loss Account. Also the

¤4,000 prepaid is recorded as a Current Asset in the BalanceSheetat the31/12/2012.

3. LIGHT &HEATDUEM.HarnettLtd. owed¤1,300forlightandheatonthe31/12/2012.Light andHeat paid on the30/9/2012 is ¤4,000. Showthe LightandHeat Accountfor the yearending 31/12/2012.

LightandHeat

The ¤1,300due(notyetpaid) attheend oftheyearis addedtotheamountpaidof¤4,000toincreasetheamountsenttotheProf-itand LossAccount to¤5,300.

Also the¤1,300 dueis recordedas a CurrentLiabilityin theBalanceSheet at the31/12/2012.

4. THE PURCHASEOFFIXEDASSETSE.MatthewsLtd.,agrocer,purchasedacomputeroncreditfromM.McCreaLtd for¤3,000on the30/9/2012.Recordthe aboveinthegeneraljournaland theledger of E.MatthewsLtd.

Because this is the purchase of a non-trading good on credit itshould be enteredin theGeneralJournal of E. Matthews Ltd. asfollows:

GeneralJournal

This transactionis enteredin thebooksby usingthe rule Debitthe Receiving Account (Computer) and Credit the Giving Ac-count,which is(M. McCreaLtd.)

When postingto theledger puttheentrieson thesamesidesasthe GeneralJournalas shownbelow:

CONSUMERQUESTIONThisquestionnormallyappearsin Paper1.

On 5th of April 2012 O. McHale, 62 South Street, NewRoss, Co Wexford bought a new 60-inch colour Smarttelevision for ¤900 from T. Eccles Limited, Rathgar,Dublin6. Itwasdeliveredon 9th AprilandwhenOscarturned it on, all he received was a black and white pic-ture.

On10thofApril2012,Oscarwrotetothe salesmanag-er of Eccles Ltd.describingthe problem. Oscar also in-cluded proof of purchase and sought an immediate re-dress.

a)Write theletterthatOscar sentto Eccles Ltd.on the10th ofApril2012.

b)(i) Explaintwoformsofredressavailableto Oscar.

(ii)Name theconsumerlawthatappliesin thiscase.

(iii)State tworelevant principlesof consumer lawthat have beenbrokenin thiscase.

c)(i) Explain,withan example,the term“impulsebuying”.

(ii)Identify 4 characteristicsof a goodconsumer.

SOLUTION

a) 62 South Street,NewRoss,Co.Wexford

10April 2012SalesManager,T.EcclesLtd.,Rathgar,Dublin6.

Re:Colour Television

THEIRISHTIMES ❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙

OTHERAREASOF

BOOKKEEPING

TYPICAL

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 7/9

Generations of success for Generations of students

f m www.ioe.ie.

tl: 01 661 3511. eml: [email protected]

Why cometo the Institute?

Reasons to join.1. 44 years’

experience2. Gifted, specialist

teachers in everysubject

3. Proven track record of

outstanding results4. ProfessionalCareer Guidance

5. Wide subjectchoice

EXAMTIMES2013P25

DearSir,I wish to register a complaint in relation to a 60 inch colour

Smarttelevision whichI boughtfromyourshopon the5thApril2012for ¤900.

Thetelevisionhas notworkedforme, asit onlyshows a blackand white picture. I now want you to replace it with one thatworksproperly.

Please find an enclosed copy of the receipt as proof of pur-chase and I would like to hear from you as soon as possible. If thismatteris notdealtwithin anexpeditious mannerI will takeittotheSmallClaimsCourt,

Yours faithfully,OscarMcHale.

b)(i) One formof redress isa cashrefund,Oscaris entitledto acashrefund.Anotherformofredressis thatOscarcanchoosetohavethe colourtelevisionreplaced.

(ii)TheSaleof Goodsand Supplyof ServicesAct 1980.

(iii) Goods must be of merchantable quality and must be fitforthe purpose intended.

c) (i) Impulse buying is purchasing an item that you hadn'tplannedto buy,e.g.walkingintoastoretobuymilkandthensub-sequently buyingan unplanned itemsuch as chocolate aswell.

(ii) A good consumer is one who budgets and sticks to thebudget. He is also one that shops around to get the best value.Heknowshisconsumerrightsand doesn'tbuyon impulse.

ECONOMICS QUESTIONThisquestionnormallyappearsin Paper1.

a)Show theNationalBudgetfor 2012in thefollowingcircumstances:

¤m

PAYE 10,000Health 11,000 VAT and Excise Duty 17,000

Privatisationofsemistatebodies 2,000Corporation Tax 8,000Social Welfare 18,000InfrastructuralExpenditure 7,000Education 8,000ServicingoftheNationalDebt 3,000

SOLUTION

TheNationalBudget for2012

b)Inthe abovebudget giveone exampleof CapitalIncomeandone exampleofCapitalExpenditure.

CapitalIncomeis once-off,non-regular incomeof the state,e.g.privatisation of stateassets.Privatisation iswhere thegovernmentsellsoffstateassets,suchas Eircomor AerLingusto theprivate sector.

Capital Expenditureis once-off,non-regular expendi-

ture ofthe stateand anexampleof thistype ofexpenditureisgovernmentspending on theinfrastructure.

c)State theeffectonIrishgovernmentfinancesof thepresent slowdownin thelevelofeconomicactivity.

Duringa recessioncompaniesbegintolay offworkersandunemploymentrises. Thelevel of incometax revenuereceivedbythe governmentfallsandthelevelof govern-mentexpenditureon socialwelfarerises.Consumerspendingalsofallsandthe government'staxtakefromVATdeclinesaswell.Allof thiscombines toworsen thestateof government finances andits budgetdeficit increases.

d)The Irisheconomy isregardedas amixedeconomy,whatdoesthismean?

A mixedeconomyis onewheretheeconomy isorganisedinsucha waythatthereisfree enterpriseandalsogovern-mentcompaniesexistingsideby side.In Irelandwehaveprivate companieslike Airtricityand government compa-nieslike theESBoperatingin thesamebusiness environ-ment.

e)Inrecent timesthe¤ hasfalleninvalueagainstthe£Sterling.Stateoneeffectthismighthaveon theIrisheconomy.

The¤ fallinginvalueagainstthe£, makesimportsfrom theUKintoIreland dearerandIrishexportsgoingintotheUKlessexpensive.Thisincreasesthe levelof economicactivity inIrelandbecause more Irishgoodswillbe sold inthe UK.

f)TimCullenplansto eitherbuya 20yearoldAstonMartinor takean exoticholiday inDonegal.Explaintheopportunitycostofdecidingto buythe car.

Theopportunitycostisthe cost ofthe alternativeforegone.Weallhavelimitedincomesowemustmakechoicesandin

thiscase Mr.Cullenhas decidedto buythecar andthere-foretheopportunitycostis theexoticholiday.

❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙ In association with THE INSTITUTEOF EDUCATION

NON-ACCOUNTINGQUESTIONS

■Minister for Finance Michael Noonan delivering the 2013Budget last December. PHOTOGRAPH:DARAMACDÓNAILL

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 8/9

P26EXAMTIMES2013

HOUSEHOLDBUDGETQUESTION

Thisquestion appearsin Paper1.

When M. Stein checked her analysed cash book at the end of December 2012, she discovered that her actual income andexpenditure forthe 12 monthsdifferedfromher budgetedfig-uresdueto thefollowing:

1. The salaries of the Stein household increased by five percent.

2.Thereare twochildrenin thehouseholdandchildbenefitin-creasedby ¤20per child fromSeptember1st,2012.

3.The actual interestreceivedfor theyear2012 was¤380.

4. TheStein householdreceived ¤900 from thesaleof anan-tiquedressingtable.

5. Mortgage payments increased by ¤15 per month fromMarch1st,2012.

6.The Steinhousehold enjoyed a noclaims bonus,so theircarin-surancewas 25per centlessthanbudgeted.

7.The houseinsurancewas¤325 forthe year.

8.Householdcostswere ninepercent greaterthan budgeted.

9.Car costs were¤375greaterthanbudgeted.

10.Clothingand footwearcostswere¤300 lessthanbudgeted.

11.Lightand heatcostsweresix percentless thanbudgeted.

12.Dentalandmedicalcostswere¤2,500in total forthe year.

13. Entertainmentcostsaveraged¤100 per month except for the3 monthsof June, JulyandDecember, which averaged¤170.

14. Due to an engagement party, presents cost an additional¤300.

15.Holidays werecancelleddue toan illnessin thefamily.

a) Usingthe budget comparison sheetbelow enter the appropri-ate figures into the “Actual” column. Show the differences be-tween the “Actual” and “Budget” figures by completing the col-umnmarked “Difference”.

Note:useaplussignifthe“Actual”isgreaterthanthe“Budget”fig-ureanduseaminussignifthe“Actual”islessthanthe“Budget”fig-

ure.

THEIRISHTIMES ❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙

BANKINGQUESTION

Thisquestion canappearin Paper1 orPaper 2.

JoyMalone, Barrett’sPark,New Ross,Co.Wexford,has a currentaccount in the Bank of Ireland, The Park, New Ross. Thebranchsortingcode number is 93-16-27and hercurrentaccount numberis 51526351.a)In the past Joyhaspaidherelectricitybills bychequeand now,forconvenience, shehas decided topay herfuture bills byDirectDebit. Her electricity account number is 645-778-512. Her con-tacttelephonenumber is051-443567.

OnJuly 12th, 2012shecompleted a direct debit instructionfor theelectricityutility company.

(i) Complete the direct debit instruction using the blank docu-mentbelow.(ii)Explaintwodifferencesbetweenadirectdebitandastandingorder.(iii)Explain howa Lasercardoperates.

b)Joy isapplyingfora loanof ¤2,000to buynew furniture.

(i)Givethreeexamplesof relevantquestionsthat a bankmanagerwouldaskJoy beforegrantingtheloan.(ii)Apart fromcommercialbanks,name twoother types of finan-cialinstitutions thatofferloansto customers.

c) Joy is going on holidays to New York. She goes to her bank tochange¤1,000intoAmerican Dollarsand seesthefollowingratesquoted:

Currency Bank Sells Bank BuysAmerican Dollars 1.30 1.40

(i) Calculate the total amount in American dollars that Joy willreceive.(ii) Explain two suitable methods of payment, other than cash,thatJoycoulduse whileshoppingin NewYork.

SOLUTION

a)(i)Seecompleteddirectdebitbelow.

(ii)1. Astandingorderis aninstructiongivenbyyouto thebank totakemoneyfromyour accountand transferit intosomeone else’saccount,whereasa directdebitiswhereyougiveyourcreditorper-missionto withdrawmoneyfromyouraccount.

2.A standingorder isfor fixedamountsofmoney only,whereasadirectdebitis forvariableandfixedamountsof money.

(iii)A Lasercardis swipedin theretailer’sterminal orcard read-er.The amountis entered bythe shopkeeper plus anycashback.Thebuyerentershis PINnumber. Theamountof thepurchasesisinstantlytransferred fromthe buyer's bankaccount intothe sell-er's bankaccount by electronic means. Then areceipt isgiven tothebuyer.

b)(i)1. HasJoya goodconsistent savingshistory?2.Hasshedefaultedonanyloansinthepast?

3.What isher presentincomeandis herjob secure?

(ii)Building societies, creditunions.

c)(i)$1,300whichis¤1,000multipliedbythesellrateof$1.30

(ii)1.Creditcard:thisiswherethebuyerbuysgoodsbutpayslater.Thecreditcardcompanypaysthe sellerandthensends a monthly statement tothe buyer. If thebuyerpays within a weekto tendaystherewillbenointerestcharged.Iftheaccountisnotclearedwith-inthat timea highrateof interestwill bechargedonthe outstand-ingbalance.

2Travellerscheques:thisiswherechequesarepre-printedinvari-ous amounts of the currency required. They are paid for andsigned in the presence of a bank official when bought. They aresigned again when being cashed and a passport is used to checkthe signatures.

PEOPLEATWORKQUESTION

Thisquestioncan appear inPaper 1 orPaper 2.

Thefollowingadvertisement appearedin a newspaper:

a)(i) Explainthesix underlinedtermsin theadvertisementabove.

(ii)NiallGarveyappliedforthe positionandforwarded hisCurric-ulum Vitae. List three pieces of information, which Niall wouldgive on his CV other than his name, address and telephonenumber.

b)Niall’s applicationfor a jobin MatthewsLtd wassuccessful. Asan employee in the salesdepartment, he may be entitled to com-mission. Also experienced staff often receives benefit-in-kindfromthe company.

(i) Explain, with an example in each case, the terms “benefit-in-kind”and “commission”.

(ii) Explain, with an example, how “work” differs from “employ-ment”.

c)MatthewsLtdpaysovertimeonthebasisthatthefirstfivehoursarepaid attime-and-a-half withdoubletimethereafter.Calculate

Niall’sgrosswage ifheworks52hoursin a week.

SOLUTIONa)(i)Basicpay: thisis paymentfor thenormalworkingweekof 40hours before overtime is added and before deductions are takenaway.Overtime:thisis additional payat a higherrate perhour forwork-ingin excessof thenormal40 hourweek.Flexitime: this iswhereyouremployer allowsyou toworkthe re-quired40 hoursat anytime,withinlimits,duringtheweek.Spreadsheet:thisis acomputerprogrammethat allowsthe opera-tor todo accountsandbudgetson a computer.Anychangeto onefigurewill havea knock-oneffecton allthe other figures.Email: thisis thesendingor receivingof documents, messagesorpictureselectronically by computer.Equal opportunities employer: when employing workers an em-ployer cannot discriminate on thebasis of race,gender,religion,colouror age.

(ii) Information on a CV should contain: (1) educational achieve-ments;(2) workexperience;(3)namesof referees.

b)(i)Benefit-in-kind:this is a non-financialrewardwhichworkersmay receive,eg a companycar, subsidisedmeals.

Commission:a source ofincomefor salespeoplebasedon theval-ue of their sales earned, eg 10per cent of the sales revenue iscommission.

(ii) Employment is work with payment whereas workcan be hu-man effort without any payment received. A homeowner whopaintshisownhouseis not goingto getpaidsothatis anexampleof work. Employment on the other hand is a painting contractorwhoispaidtopaintyourhouse.

c)The answer hereis ¤1,230, andtheworkingsareas follows:

Basic Pay: ( 40 h ours x ¤ 20 ) = ¤ 80 0

Overtime: (5hours@ 1.5x¤20) =¤150

(7hours@2x ¤20) =¤280

–––––––Total Pay: ¤1,230

MICROECONOMIES

MENATWORK

■ Completeddirectdebit.

8/12/2019 Business Junior Cert

http://slidepdf.com/reader/full/business-junior-cert 9/9

EXAMTIMES2013P27

b)(i)Whatwasthebudgetedclosingcashattheendof2012?(ii) How much had the Stein household budgeted to save during2012?(iii) Whatwas theactual closingcashat theendof 2012?(iv)Stateby howmuch theSteinhouseholdexceededtheirbudget-edtotalexpenditure.(v) Explain one possible reason why the “Actual” interest wasmorethan the“Budget” interest.

SOLUTION

Asyou areanswering thequestioncoverthe“Actual”columnandseecan youcalculatethe correctfigures.

a)Householdbudgetof theSteinfamily–seetableat right.

Thetotalexpenditure, linefive, isfoundbyaddinglinestwo, threeandfour.

The net cash, line six, is found by subtracting line five from lineone.

b)(i)¤1,485(ii)¤85(iii)¤2,494(iv)¤1,231(v) Deposit interest rates may have risen during the year or theStein householdmay have investedmoremoney intheir bankac-

count

BUSINESSDOCUMENTSQUESTION

Thisquestionnormallyappearsin Paper2.

On May 28th, 2012 Jorden Bukspan Ltd Ferry Bridge, New Ross, received Order No.4 fromEthan Brady Arnold Ltd., 121 John Street, NewRoss,Co. Wexfordforthefollowinggoods:

50 LeatherFootballs@ ¤60per Football.

50Boxesof SquashBalls@¤80per Box.

20Basketballs@¤30perBall.

Allof thegoodsordered were instockexceptforthe footballs.

Jorden Bukspan Ltd. issued Invoice No. 69 forthegoods instock on June 1st,2012. Theinvoiceincludedthe following terms: trade discount 30percentandVAT23percent.

On receiving the goods and the invoice on June4th, 2012, Ethan Brady Arnold Ltd paid theamountdue infull.

Jorden Bukspan Ltd. issued Receipt No. 67signedby KaraSteinon June7th,2012.

(i) What procedures would you recommend toJorden Bukspan Ltd. when preparing andprocessingreceipts?

(ii) CompleteInvoice No. 69 and Receipt No. 67issuedby JordenBukspanLtd.

(iii) Record the issue of the Invoice and the Re-ceipt in the Sales Book and the Analysed CashBookof JordenBukspanLtd.

SOLUTION

(i) The procedures to be followed when prepar-ingand processingreceiptsinclude:

1.Checkthe amountreceivedagainst theinvoiceandcredit noteand statement.

2.Checktheaccuracyofthe nameand addressof the debtor.

3.Insertthe correctdate.

4.Insertthe amountof moneyreceivedinfiguresandin words.

5.Signthe receipt.

6.Filea copy ofthe receipt.

7. Record the amount received in the analysedcash bookandin thedebtorsledger.

❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙❙ In association with THE INSTITUTEOF EDUCATION