Embed Size (px)

Citation preview

© Hodder Education 2009

2Understanding financial objectives

Section 1: Financial strategies and accounts

Cha

pter 1

BUSINESS IN FOCUS

Questions:What was Toyota’s profit target?

• Its profit target was $12 billion/6 � 10 � $20 billion.

What other financial targets might the company have set itself?

Answers may include:

• In the current market the company might set itself a cash-flow target (e.g. avoiding high stock levels).

• The company may react to declining profits by adopting an objective of cost minimisation.

• The directors may decide to pursue a ROCE target in an attempt to improve profitability and satisfytheir shareholders.

PROGRESS QUESTIONS

1. Define, with the use of examples, the term ‘financial objective’. (3 marks)

A goal or target pursued by the finance department (or function) within an organisation, e.g. a specificreturn on capital employed (ROCE) figure or cost minimisation.

2. Distinguish between cash flow and profit. (6 marks)

Profit:

• the surplus of revenues over total costs at the end of a trading period

• relates to a trading period.

Cash flow:

• the movement of cash into and out of a business over a period of time

• considers the timing of payments and receipts.

A profitable business can run short of cash.

3. Explain two reasons why a public limited company might use ROCE as a basis for a financial objective.(8 marks)

Answers may include:

• Using ROCE as a target might help the company to attract shareholders.

• It is a financial objective that is easy to measure and publicise – if the company is successful.

• It measures the financial performance of a company in a comparable way, which is likely to be ofinterest to shareholders.

4. What types of businesses might use cash-flow targets as a financial objective? Why? (5 marks)

• Businesses that face long cash cycles, such as house builders.

• Businesses that have experienced cash-flow problems in the past.

• Businesses that are likely to require large long-term loans in the near future.

5. Explain why a business entering an established market might choose to operate cost minimisation as afinancial target. (6 marks)

• It will help the business to ensure that it makes a profit during a difficult period of trading.

• It will help the business to be more price competitive against larger and established rivals.

• The business may be able to use price competitiveness as a USP to help establish customer loyalty.

6. What is meant by the term ‘shareholders’ returns’? (4 marks)

• The current share price and any associated dividends that are due in the near future, or

• a combination of short-term returns (both share prices and dividends) as well as future share pricesand dividends.

7. Explain why a business’s finance department should not set its objectives without consulting the otherfunctions of the business. (6 marks)

• Primarily because it will affect the spending decision of other functions, such as HR and marketing.

• All the functions should set objectives following communication to ensure that they are integrated.

• The finance function’s objectives must assist the other functions in contributing to the achievement ofcorporate objectives.

8. JHG plc builds oil rigs for use in locations across the globe. Explain how the nature of the company’sproduct might influence its corporate objectives. (8 marks)

• A long cash cycle might mean that the company opts for cash-flow targets to reassure creditors.

• However, the business might set a ROCE target or opt to pursue shareholder returns if it requiresincreases in share capital to finance its activities.

• Demand for oil rigs may not be highly price elastic as buyers are more likely to be concerned aboutquality (and thus safety) and also meeting their precise specifications. Hence cost minimisation maynot be a vital financial objective.

9. Why might the business’s corporate objectives be considered the most important influence on itsfinancial objectives? (6 marks)

• The finance function operates to help the business achieve its overall objectives, not for its own reasons.

• Corporate objectives are set first and then functional objectives are decided, to dovetail with corporateobjectives.

• Finance is only one aspect of a business’s operations.

10. Outline how the state of the market in which a business is selling might influence the financial objec-tives that it chooses. (6 marks)

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 1

© Hodder Education 2009

• In a growing market, with the possibility of excess demand, a business might set itself a ROCE targetas trading is profitable.

• Equally, in such a market shareholders’ returns might be vital as a financial objective if the businessneeds to raise share capital on a regular basis.

• In a highly competitive market a business might decide to operate with cost minimisation as a financialtarget to allow more freedom in pricing decisions.

ANALYSIS AND EVALUATION QUESTIONS

1. (a) Analyse the potential advantages to this company of pursuing a financial objective of cost minimi-sation. (10 marks)

Answers may include:

• It entails seeking to reduce to the lowest possible level all the costs of production that a business incursas part of its trading activities.

• The company is a new entrant and cost minimisation will help it to overcome possible absence ofeconomies of scale.

• It will give the company a little more flexibility in its pricing decisions.

• The company may use cost minimisation as the basis for lower prices, a USP and also a focus for itsmarketing campaigns.

(b) Discuss the likely consequences for the entire business of the adoption of the financial objective ofcost minimisation. (15 marks)

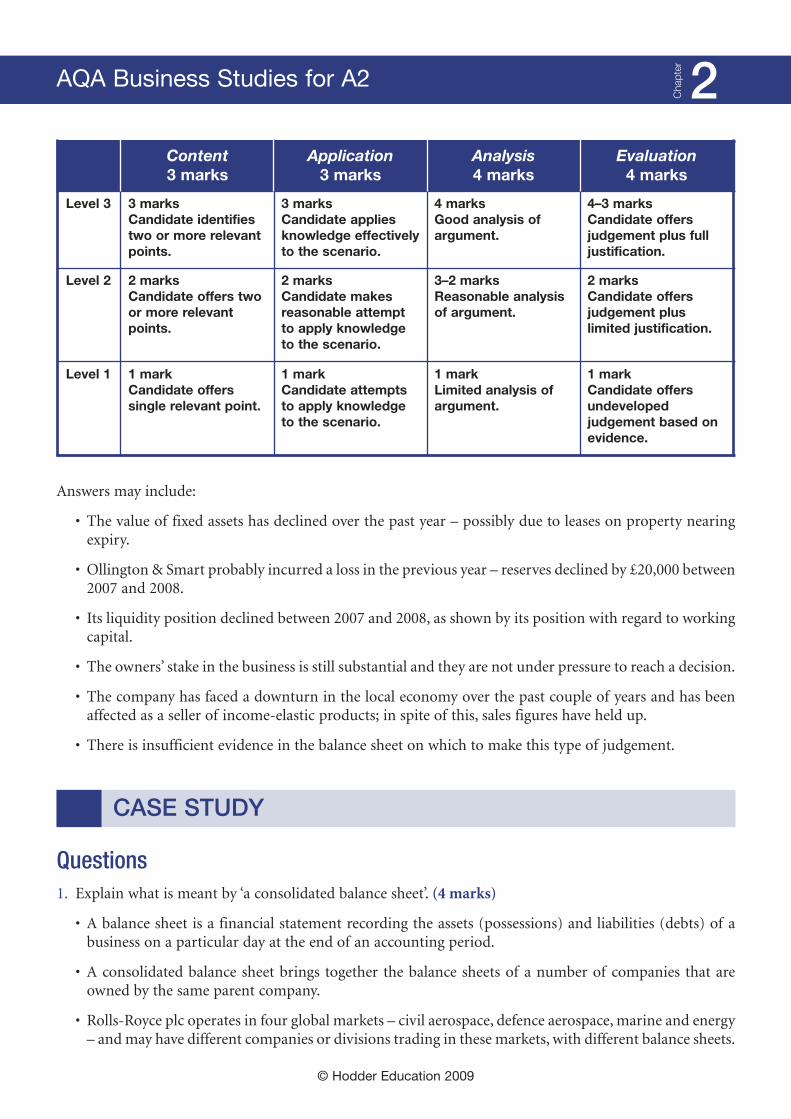

Content3 marks

Application3 marks

Analysis4 marks

Level 3 3 marksCandidate identifies two ormore relevant points andshows understanding of theterm.

3 marksCandidate applies knowledgeeffectively to the scenario.

4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

AQA Business Studies for A2

Cha

pter 1

Answers may include:

• It entails seeking to reduce to the lowest possible level all the costs of production that a business incursas part of its trading activities.

• It will mean that the HR department will seek to keep wage costs to their lowest through negotiatingtough pay settlements and achieving high levels of productivity.

• The operations department may seek to minimise running costs, e.g. through keeping employee breaksto a minimum and operating with cheaper models and specifications of coaches.

• The marketing department will have to operate with a relatively small budget but may also stress thebusiness’s competitive prices in its marketing.

• The consequences will depend on the degree of price elasticity for coach travel (which is likely to behigh).

2. (a) Analyse the likely impact on its choice of financial objectives of the changes in the market. (10marks)

© Hodder Education 2009

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints and showsunderstanding of theterm.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

AQA Business Studies for A2

Cha

pter 1

© Hodder Education 2009

Answers may include:

• A financial objective is a goal or target pursued by the finance department (or function) within anorganisation.

• The retirement of the chief executive may mean that she expects shareholders’ returns to be the keyfinancial target, especially if her pension depends on the company’s share price.

• However, ROCE might be the most important financial objective if her retirement package is deter-mined by the level of profits.

• Falling sales might mean that cost minimisation becomes more important as a target – it might be vitalfor the company to have the flexibility to reduce prices if necessary.

(b) Do you think that external influences are more important as an influence on its financial objectivesthan internal factors? Justify your answer. (15 marks)

Content3 marks

Application3 marks

Analysis4 marks

Level 3 3 marksCandidate identifies two ormore relevant points andshows understanding of theterm.

3 marksCandidate applies knowledgeeffectively to the scenario.

4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

AQA Business Studies for A2

Cha

pter 1

Answers may include:

• A financial objective is a goal or target pursued by the finance department (or function) within anorganisation.

• The fall in sales is likely to be a key influence on the company’s decisions about financial objectives.This will affect its existing customers.

• The new entrant will have an impact, but whether it has a major influence on financial objectives maydepend on its size and competitiveness.

• The retirement of the chief executive could have a significant influence and make the company lookfor more short-term financial targets, such as profits, over the next two years.

• The importance of the two groups of factors depends on a range of factors, including the power andinfluence of the retiring chief executive and the extent and expected duration of the fall in sales.

CASE STUDY

Questions1. Explain what is meant by ‘shareholders’ returns’. (5 marks)

Answers may include:

• A short-term view defines it as the current share price and any associated dividends that are due in thenear future.

© Hodder Education 2009

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints and showsunderstanding of theterm.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

AQA Business Studies for A2

Cha

pter 1

• A longer-term view defines it as a combination of short-term returns (both share prices and dividends)as well as future share prices and dividends.

• In any event, shareholders’ returns focuses on generating profits and increasing the value of thecompany as reflected in its share price.

2. Analyse the possible financial objectives that Cadbury may pursue following this announcement. (8marks)

© Hodder Education 2009

Answers may include:

• A financial objective is a goal or target pursued by the finance department (or function) within anorganisation.

• The company may pursue cost minimisation in order to become more efficient. This means usingfewer resources, and cost minimisation will assist in this aim.

• The company also states that it intends to improve its returns to shareholders, so this will become animportant financial objective.

• The company may need to achieve a specified (and quite high) return on capital if it is to fund theproduct and market development strategies that it is proposing.

Content2 marks

Application3 marks

Analysis3 marks

Level 3 3 marksCandidate applies knowledgeeffectively to the scenario.

3 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

AQA Business Studies for A2

Cha

pter 1

Answers may include:

• It entails seeking to reduce to the lowest possible level all the costs of production that a business incursas part of its trading activities.

• The threat of a takeover by a private equity business is a key factor influencing the company’s decisions– making itself more competitive is a way of preventing this happening.

• If the business increases its shareholders’ returns as a consequence of reducing costs it will make thebusiness more valuable and less vulnerable to a takeover.

• Reducing costs will help the company to raise the funds necessary to enter new markets and developnew products.

• It is almost certainly a combination of these factors, with the threat of a takeover being the mostpressing short-term influence.

© Hodder Education 2009

Content2 marks

Application3 marks

Analysis3 marks

Evaluation4 marks

Level 3 3 marksCandidate appliesknowledge effectivelyto the scenario.

3 marksGood analysis ofargument.

4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

3. Evaluate the likely influences on Cadbury’s decision to establish a financial objective of reducing its costs.(12 marks)

AQA Business Studies for A2

Cha

pter 1

4. To what extent is Cadbury’s decision likely to please all of its stakeholders? (15 marks)

© Hodder Education 2009

AQA Business Studies for A2

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints and showsunderstanding of theterm.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

Cha

pter 1

Answers may include:

• A stakeholder is any person or group with an interest in a business.

• Shareholders might be pleased by the proposed reduction in costs and focus on shareholders’ returns,as this is likely to increase dividends and possibly share prices.

• Employees (and their representatives) will be concerned by the proposed loss of 7,500 jobs, althoughtheir reaction will depend on how these jobs are to be lost.

• Existing customers may be pleased by the commitment to new products and potential customers bythe proposal to enter new markets.

• Managers (if they retain their jobs) could be excited by the prospect of new products and markets andperhaps higher bonuses.

• It is unlikely that the company can please all of its stakeholders by this – or any other major – decision.

BUSINESS IN FOCUS

Question:What other actions might the two companies take to improve the cash position as shown on the balancesheet?

Answers may include:

• The companies may seek to increase sales of cars (using a variety of marketing techniques) to createcash inflows.

• The two businesses might choose to sell fixed assets that are no longer needed (e.g. some land).

• Alternatively, the firms could sell and lease back other fixed assets such as factories.

• The companies might attempt to negotiate loans with banks.

• Given the importance of these two businesses to the American economy, the two management teamsmay approach the American government for grants or loans.

BUSINESS IN FOCUS

Questions:Do you think that Mothercare’s rise in profits is good quality?

• The rise in profits is the result of the company’s expansion – this is good quality as it is likely tocontinue in the future.

Which of the company’s stakeholders might be pleased about this news? Why?

Answers may include:

• Employees may respond well to this news as it increases job security and offers more opportunities ofpromotion.

• For shareholders the rise in Mothercare’s profits is good news in the short term in terms of dividends,and for share prices in the longer term.

• Customers may be satisfied by the rise in profits as it has come about from an increase in onlineretailing, making it easier for customers to buy the company’s products.

© Hodder Education 2009

Using financial data to measure and assess performance

AQA Business Studies for A2

Cha

pter 2

BUSINESS IN FOCUS

Question:Would this slump in profits have been predicted from looking at the company’s most recent balance sheetand income statement?

Answers may include:

• Both documents are historical and do not necessarily indicate future developments.

• The fall in profits is principally due to rising fuel costs, which neither the income statement nor balancesheet would indicate.

• These changes are due to alterations in market conditions which are not likely to be revealed byfinancial statements (though a trend of falling sales might be shown on income statements).

PROGRESS QUESTIONS

1. Merrills Industries manufactures biscuits and other convenience foodstuffs. Identify three stakeholdergroups who may have an interest in the company’s balance sheet. Outline the likely nature of theirinterest. (9 marks)

Answers may include:

• Shareholders – future dividends and trends in the company’s share price.

• Employees – to inform negotiations about wages and salaries.

• Suppliers – to help to make decisions about offering trade credit.

• Competitors – to make decisions on pricing strategies and tactics.

• Revenue and Customs – to check the company’s liability for taxation.

2. Explain two factors that lead to a business’s balance sheet always balancing. (6 marks)

• The ‘dual effect’ of the balance sheet means that transactions always balance each other, e.g. borrowingto purchase a non-current asset has the same effect on assets and liabilities.

• Reserves (the profit accumulated over previous years) is also a mechanism to ensure this financial state-ment always balances. Thus, if the business grows in value, so will reserves (which are a liability).

3. Outline how the information recorded on a business’s balance sheet can be used to assess the cash orliquidity position of the business. (7 marks)

• The business’s current assets can be compared with its current liabilities.

• The same comparison, but excluding inventories, may be carried out to give a better measure ofliquidity (as inventories can be illiquid in certain circumstances).

• The firm’s holdings of cash give a clear indication of its immediate ability to meet commitments.

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 2

4. Explain the difference between the net current assets and the net assets of a public limited company. (6marks)

• Net current assets (also known as working capital) are a business’s current assets less its current liabil-ities.

• Net assets are non-current assets plus non-current or fixed assets.

5. The net assets of Gujarati Products plc is £540 million. The company’s non-current liabilities total £339million. What are the possible implications of this position? (7 marks)

• The company has borrowed a high proportion of its capital employed (high gearing), so it is vulner-able to a rise in interest rates.

• May put off potential shareholders as they fear profits may be reduced due to possibile high interestcharges.

6. Smith and Whyte’s reserves rose by £54 million last year. Outline the possible causes of this. (5 marks)

• The company may have made a handsome profit on its trading activities.

• Its non-current assets may have increased in value.

• It may have revalued its intangible assets, e.g. brands.

7. Explain two possible consequences of a retailer having too much working capital. (6 marks)

Answers may include:

• The business may be less profitable than it could be if it invested these funds in assets that generatedhigh returns.

• Shareholders may be dissatisfied with the business’s financial performance.

• The business would experience no difficulty in meeting its current liabilities.

8. Explain why a manufacturing business that is expanding rapidly might face problems with its workingcapital. (8 marks)

• The business will be increasing purchases of stock and paying for labour before it has received paymentfrom its customers.

• This problem will be serious if the business has a long cash cycle.

• The business may use new suppliers who may be unwilling to grant trade credit initially.

• It may have taken out long-term loans to finance the purchase of non-current assets, placing furtherpressure on its working capital.

9. Explain why a road haulage company will have to depreciate its non-current assets each year. (8 marks)

• The assets may lose value because of obsolescence or wear and tear.

• They will be used over a period of several years and the purchase cost should be spread over the samenumber of years.

10. Outline why it is important to value non-current assets as accurately as possible. (6 marks)

• The value of non-current assets is an important component of the valuation of the entire business.

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 2

• Valuation of non-current assets affects the profits and hence the amount of corporation tax paid bya company.

• HM Revenue and Customs has strict rules on depreciating assets.

11. Explain what is meant by high-quality profit. (4 marks)

High-quality profit is expected to continue into the future. Thus:

• Profit arising from the sale of an asset is low quality since it is unlikely to be repeated.

• Profit arising from sales of a newly introduced product is likely to be high quality.

12. Explain why an extraordinary item should be listed separately in a company’s income statement. (5marks)

• It not part of the business’s normal trading activities and so should be distinct.

• Accounting regulations insist that such transactions should be included separately within the incomestatement.

13. Outline two aspects of a supermarket’s income statement that might be of particular interest to a share-holder considering buying a large quantity of the company’s shares. (8 marks)

Answers may include:

• The revenue of the business, especially when compared with previous years.

• A comparison of gross and net profit (allowing a judgement to be made of the effectiveness of thecontrol of overheads).

• The overall profitability of the business after tax.

• The amount of profit retained within the business (giving an indication of future growth).

• The dividends paid to its shareholders.

14. Explain two reasons why a balance sheet can be considered a valuable document for stakeholders. (6marks)

Answers may include:

• It shows the liquidity position of the business to any actual or potential suppliers.

• It shows the value of a business and how this has changed since the previous balance sheet.

• It shows from where the business raised its finance and how it has been used.

• It shows the amount that the business has borrowed and allows stakeholders to decide whether or notthis is excessive.

15. Outline three sources of information, other than its balance sheet and income statement, that mighthelp an investor to assess the future prospects of a computer manufacturer. (8 marks)

Answers may include:

• The financial statements of close competitors.

• The business’s cash-flow statement.

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 2

• Market data for those markets in which the business trades.

• Information about the business’s workforce, such as absenteeism, productivity and labour turnover.

ANALYSIS AND EVALUATION QUESTIONS

1. (a) Analyse what is meant by the phrase ‘a strong balance sheet’. (10 marks)

© Hodder Education 2009

Answers may include:

• A balance sheet is a financial statement recording the assets (possessions) and liabilities (debts) of abusiness on a particular day at the end of an accounting period.

• A strong balance sheet may mean that the business has raised a large amount of its funds through shareissues rather than borrowing and therefore has a favourable gearing ratio.

• It may also refer to the business’s cash position: holding sufficient cash, but not so much as to beregarded as wasteful of profitable assets.

• The balance sheet may have a large figure for reserves, indicating that the business has been profitablein recent years, increasing the value of the owners’ stakes in the business.

• The term may refer to the value of non-current assets held by the business, possibly in the form of oilnot yet recovered.

Content3 marks

Application3 marks

Analysis4 marks

Level 3 3 marksCandidate identifies two ormore relevant points andshows understanding of theterm.

3 marksCandidate applies knowledgeeffectively to the scenario.

4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

AQA Business Studies for A2

Cha

pter 2

© Hodder Education 2009

Answers may include:

• An income statement shows a firm’s sales revenue over a trading period, and all the relevant costsgenerated to earn that revenue.

• The balance sheet will show the value of the company’s assets and some indication of the value of itsreserves of oil.

• The balance sheet will show whether the company has borrowed excessively in discovering new oilfields.

• The income statement shows the level of net and gross profit achieved by the business, and also theprofit that is available for reinvestment in future oil exploration.

• The income statement and balance sheet will show how much finance is available to the business forreinvestment.

• There are many factors that are not shown by these financial statements – a critical one for thiscompany is the future price of oil.

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints and showsunderstanding of theterm.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

(b) Discuss the value of Benson plc’s balance sheets and income statements in assessing its futureperformance. (15 marks)

AQA Business Studies for A2

Cha

pter 2

© Hodder Education 2009

Answers may include:

• Working capital measures the amount of money available to a business to pay its day-to-day expenses,such as bills for fuel and raw materials, wages and business rates.

• The company is expanding and is a manufacturing business. This means that it has to purchase stocksbefore it can sell them to customers and receive payment. When it is growing it is in danger of over-trading.

• The company’s products are popular, which may result in rapid growth, stretching cash reserves.

• Marine has had to grant Tesco 45 days’ credit, which will add to its difficulties.

Content3 marks

Application3 marks

Analysis4 marks

Level 3 3 marksCandidate identifies two ormore relevant points andshows understanding of theterm.

3 marksCandidate applies knowledgeeffectively to the scenario.

4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

2. (a) Analyse the possible reasons why Marine Ltd might experience problems in managing its workingcapital. (10 marks)

AQA Business Studies for A2

Cha

pter 2

© Hodder Education 2009

Answers may include:

• Cash flow is the money flowing into and out of a business over time.

• The business may not be able to pay its suppliers, e.g. of bottles and flavourings, and may be forced tocease trading.

• If the business is unable to buy sufficiently large quantities of supplies, it may lose its contract withTesco – which would be a major blow.

• The company has been growing for some time and presumably will have planned its cash flow andprepared for some problems, e.g. by arranging an overdraft.

• The implications depend on the size of the cash-flow problems and the attitude of the company’sbankers.

CASE STUDY

Questions1. Identify two stakeholders whomay have an interest in the balance sheet of Ollington. In each case explainthe possible reasons for their interest. (6 marks)

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints and showsunderstanding of theterm.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3-3 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

(b) Discuss the possible implications of the cash-flow problems for Marine Ltd. (15 marks)

AQA Business Studies for A2

Cha

pter 2

© Hodder Education 2009

Content2 marks

Application4 marks

Level 2 2 marksCandidate identifies two stakeholders.

4–3 marksCandidate explains interest effectively inrelation to the scenario.

Level 1 1 markCandidate identifies single stakeholder.

2–1 marksCandidate attempts to explain interest inrelation to the scenario.

Answers may include:

• Employees – interested in security of jobs, particularly if they sense Paul is about to sell the business.

• Suppliers – provide expensive photographic equipment and will want to ensure the business is suffi-ciently liquid to meet its debts, or face substantial bad debts.

• Rivals – if there is takeover talk in the air, Ollington & Smart’s balance sheet will be of great interest toprovide an indication of the worth of the business.

2. Analyse the benefits that Ollington’s Photographers may gain from taking action to window dress itsbalance sheet. (8 marks)

Content2 marks

Application2 marks

Analysis4 marks

Level 3 4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate applies knowledgeeffectively to the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

Answers may include:

• A balance sheet is a financial statement recording the assets (possessions) and liabilities (debts) of abusiness on a particular day at the end of an accounting period.

• An improved liquidity position may make the business more attractive to potential purchasers andattract higher bids.

• Sales could be improved by bringing forward invoices, which could improve profitability.

AQA Business Studies for A2

Cha

pter 2

• Profits may also be improved by altering the business’s depreciation policy to reduce the value of fixedassets more slowly and enhance profits. May be able to negotiate a higher price for the business if itlooks more profitable.

3. Smith Photographic plc is considering the purchase of Ollington & Smart. Consider the disadvantagesof using a balance sheet as the basis of such a decision. (12 marks)

© Hodder Education 2009

Answers may include:

• A balance sheet is a financial statement recording the assets (possessions) and liabilities (debts) of abusiness on a particular day at the end of an accounting period.

• It only relates to a single point in time, which may not be representative of the true position of the busi-ness.

• It excludes any information relating to costs, revenues or profits, which must be a crucial part of theevaluation of any business prior to making a bid.

• It only really includes financial information: much non-financial information would play an importantpart in such a decision.

• It would not provide Smith Photographic with any information about the market in which Ollington& Smart trades.

4. Paul’s accountant has commented that there are strong reasons why he should sell the business at thistime. Discuss the case for and against this view. (14 marks)

Content3 marks

Application3 marks

Analysis3 marks

Evaluation3 marks

Level 3 3 marksCandidate appliesknowledge effectivelyto the scenario.

3 marksGood analysis ofargument.

3 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

2 marksReasonable analysisof argument.

2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

AQA Business Studies for A2

Cha

pter 2

© Hodder Education 2009

Answers may include:

• The value of fixed assets has declined over the past year – possibly due to leases on property nearingexpiry.

• Ollington & Smart probably incurred a loss in the previous year – reserves declined by £20,000 between2007 and 2008.

• Its liquidity position declined between 2007 and 2008, as shown by its position with regard to workingcapital.

• The owners’ stake in the business is still substantial and they are not under pressure to reach a decision.

• The company has faced a downturn in the local economy over the past couple of years and has beenaffected as a seller of income-elastic products; in spite of this, sales figures have held up.

• There is insufficient evidence in the balance sheet on which to make this type of judgement.

CASE STUDY

Questions1. Explain what is meant by ‘a consolidated balance sheet’. (4 marks)

• A balance sheet is a financial statement recording the assets (possessions) and liabilities (debts) of abusiness on a particular day at the end of an accounting period.

• A consolidated balance sheet brings together the balance sheets of a number of companies that areowned by the same parent company.

• Rolls-Royce plc operates in four global markets – civil aerospace, defence aerospace, marine and energy– andmay have different companies or divisions trading in these markets, with different balance sheets.

Content3 marks

Application3 marks

Analysis4 marks

Evaluation4 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

4–3 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant point.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

AQA Business Studies for A2

Cha

pter 2

© Hodder Education 2009

2. Analyse the key trends in the company’s income statements for 2006 and 2007. (9 marks)

Content2 marks

Application3 marks

Analysis4 marks

Level 3 3 marksCandidate applies knowledgeeffectively to the scenario.

4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

Answers may include:

• An income statement shows a firm’s sales revenue over a trading period and all the relevant costs gener-ated to earn that revenue.

• Revenue has risen but gross profit has fallen. This suggests that the company has not been successful incontrolling its cost of sales.

• Expenses have risen, but not in line with revenue, so the company has been more successful in control-ling this aspect of its operations.

• There has been a substantial fall in the company’s finance income (from £1,196 million to £718million.The company may have sold assets that were generating an income for it.

• Profit for the year has fallen considerably, mainly due to rising cost of sales and falling finance income.

AQA Business Studies for A2

Cha

pter 2

© Hodder Education 2009

3. Discuss the strengths and weakness of Rolls-Royce’s balance sheet in 2007. (12 marks)

Content2 marks

Application3 marks

Analysis3 marks

Evaluation4 marks

Level 3 3 marksCandidate appliesknowledge effectivelyto the scenario.

3 marksGood analysis ofargument.

4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

Answers may include:

• A balance sheet is a financial statement recording the assets (possessions) and liabilities (debts) of abusiness on a particular day at the end of an accounting period.

• There was a substantial increase in the value of the company, which was reflected in the value of itsnon-current assets across the two years.

• The working capital position remained strong over the two years – the company had over £2,000million available on the date of the 2007 balance sheet.

• Non-current liabilities decreased while the value of the business rose. This will have reduced thegearing level substantially.

• Inventories are high and increased further in 2007.

• The strengths of the balance sheet appear to outweigh its weaknesses.

• These figures are for two specific days across two years of trading – they may have been windowdressed.

AQA Business Studies for A2

Cha

pter 2

© Hodder Education 2009

4. To what extent could an investor base a decision to purchase 1 million of the Rolls-Royce group’s shareson the basis of this information? (15 marks)

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant point.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

Answers may include:

• The balance sheet provides the investor with valuable information about the company’s liquidityposition and also its gearing position, which is essential to make such a decision.

• The income statement shows profitability and dividends – essential detail for a potential investor.

• There are two years of figures available in this data, giving some indication of the trend on financialperformance.

• There is no information about the company’s position in relation to the various markets in which ittrades and how these markets are performing.

• Rolls-Royce is an engineering company – what patents does it have and what is its position in relationto the development of new products?

• Skilled employees are essential to the long-term performance of a high-technology engineeringcompany and the balance sheet provides no information on labour turnover or similar data.

• A decision to spend such a large sum of money will require more than financial information about thecompany – and this information may have been massaged.

AQA Business Studies for A2

Cha

pter 2

BUSINESS IN FOCUS

Questions:What are the implications of this news for companies with high rates of gearing (over 50 per cent)?

• The rise in effective interest rates (if not the Bank of England’s base rate) will increase the interestcharges faced by businesses.

• For highly geared businesses these costs could become high and possibly unmanageable depending onthe extent of the rise and level of gearing.

What actions might they take in response?

Answers may include:

• Business may respond by selling assets to reduce gearing levels.

• Business may lower dividend payments to allow more of profits to be used to repay loans.

• Afurtheroptioncouldbetorenegotiate loanstoreducemonthlypayments(perhapsbyextendingtheterm).

BUSINESS IN FOCUS

Question:Why might a small business be reluctant to claim interest from a large customer that buys a high propor-tion of its output and regularly delays payment?

• It may be afraid of losing sales (and a large amount of revenue).

BUSINESS IN FOCUS

Question:Why might a supermarket in a highly competitive industry be happy to achieve a net profit margin on salesof less than 3 per cent?

Answers may include:

• This may be acceptable if other businesses in the same market are achieving similar profit margins.

• This figure may be acceptable if the company achieves high sales figures allowing it to generate suffi-cient profits even with a low margin.

• If the figure is in line with the company’s financial forecasts then the management team may find itacceptable – in this case the figure was better than forecasts.

• It may depend on whether this is a gross or a net margin – as a gross margin it would be unacceptable.© Hodder Education 2009

Cha

pter 3Interpreting published accounts

AQA Business Studies for A2

BUSINESS IN FOCUS

Question:Whymight some of Debenham’s shareholders be satisfied to see the company reduce its dividend per share?

Answers may include:

• This allows the company to reduce its debts and may result in higher profits in the future.

• This action of reducing indebtedness may increase the company’s share price.

• The company may be able to finance investment in the business (in this case refurbishing stores),improving the company’s future financial performance.

PROGRESS QUESTIONS

1. Explain, with the aid of an example, why a ratio might provide more detail on a firm’s performance thana single piece of financial information. (7 marks)

• A ratio allows a comparison with some other piece of information, allowing a more informed judge-ment, e.g. expressing profits as a percentage of capital employed.

• Ratios give a figure that can be compared with industry standard figures or with those of rivals.

• Ratios make trend analysis easier, assessing the performance of a company over time.

• Ratios allow stakeholders to place key figures (profits, sales etc.) in some context.

2. Distinguish between efficiency ratios and profitability ratios. (6 marks)

• Efficiency ratios measure the effectiveness with which managers control the internal operation of abusiness. How well are stocks managed, and are creditors chased up promptly?

• Profitability ratios assess the amount of gross or net profit made in relation to the business’s turnoveror the capital available to it.

3. Outline two sources of information that might be important when conducting ratio analysis. (6 marks)

Answers may include:

• The balance sheet and the profit and loss account over recent years provide vital information.

• Norms or benchmarks for the industry in question – these assist in making a judgement about theresults of ratio analysis.

• The economic and market environment. Improvements in profitability might be due to an upswing inthe business cycle rather than improved management of the business.

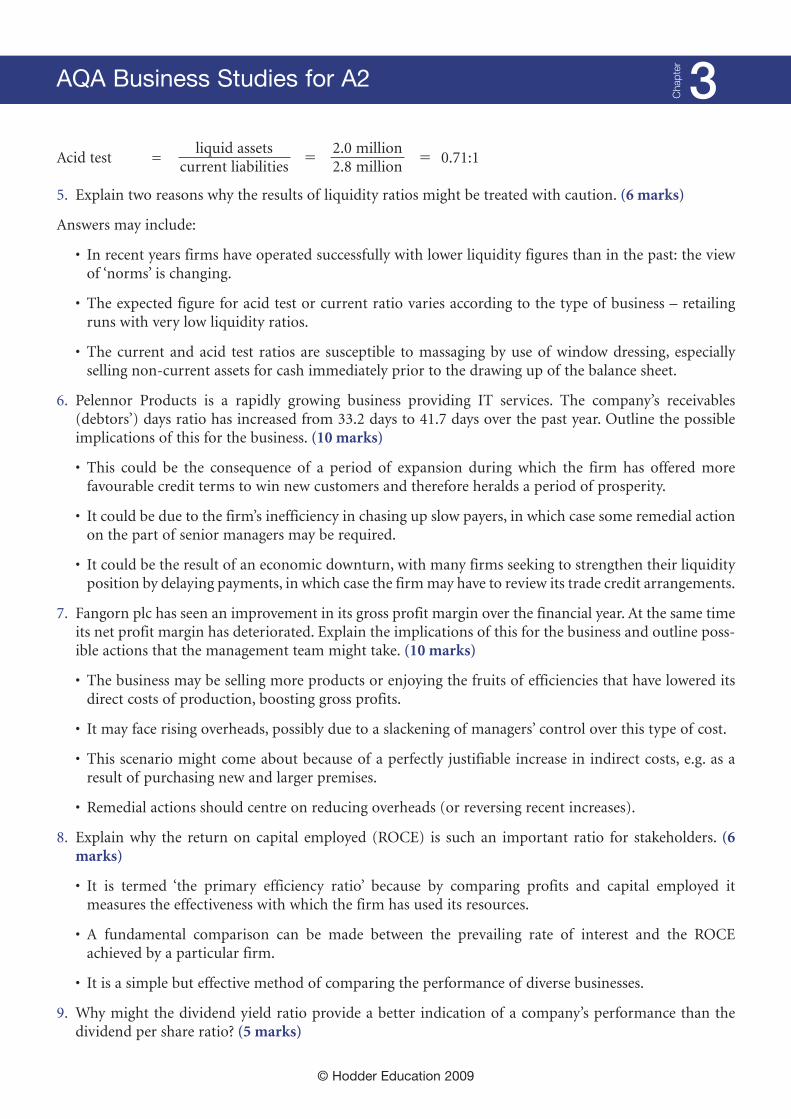

4. Marsham Trading has current liabilities amounting to £2.8m. Its current assets are: receivables £1.1m,inventories £2.0m and cash £0.9m. Calculate the business’s current and acid test ratios. (8 marks)

Current ratio � � = 1.43:1current assetscurrent liabilities

4.0 million2.8 million

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 3

Acid test = � � 0.71:1

5. Explain two reasons why the results of liquidity ratios might be treated with caution. (6 marks)

Answers may include:

• In recent years firms have operated successfully with lower liquidity figures than in the past: the viewof ‘norms’ is changing.

• The expected figure for acid test or current ratio varies according to the type of business – retailingruns with very low liquidity ratios.

• The current and acid test ratios are susceptible to massaging by use of window dressing, especiallyselling non-current assets for cash immediately prior to the drawing up of the balance sheet.

6. Pelennor Products is a rapidly growing business providing IT services. The company’s receivables(debtors’) days ratio has increased from 33.2 days to 41.7 days over the past year. Outline the possibleimplications of this for the business. (10 marks)

• This could be the consequence of a period of expansion during which the firm has offered morefavourable credit terms to win new customers and therefore heralds a period of prosperity.

• It could be due to the firm’s inefficiency in chasing up slow payers, in which case some remedial actionon the part of senior managers may be required.

• It could be the result of an economic downturn, with many firms seeking to strengthen their liquidityposition by delaying payments, in which case the firmmay have to review its trade credit arrangements.

7. Fangorn plc has seen an improvement in its gross profit margin over the financial year. At the same timeits net profit margin has deteriorated. Explain the implications of this for the business and outline poss-ible actions that the management team might take. (10 marks)

• The business may be selling more products or enjoying the fruits of efficiencies that have lowered itsdirect costs of production, boosting gross profits.

• It may face rising overheads, possibly due to a slackening of managers’ control over this type of cost.

• This scenario might come about because of a perfectly justifiable increase in indirect costs, e.g. as aresult of purchasing new and larger premises.

• Remedial actions should centre on reducing overheads (or reversing recent increases).

8. Explain why the return on capital employed (ROCE) is such an important ratio for stakeholders. (6marks)

• It is termed ‘the primary efficiency ratio’ because by comparing profits and capital employed itmeasures the effectiveness with which the firm has used its resources.

• A fundamental comparison can be made between the prevailing rate of interest and the ROCEachieved by a particular firm.

• It is a simple but effective method of comparing the performance of diverse businesses.

9. Why might the dividend yield ratio provide a better indication of a company’s performance than thedividend per share ratio? (5 marks)

liquid assetscurrent liabilities

2.0 million2.8 million

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 3

© Hodder Education 2009

• The dividend per share does not take into account the price of the share in question.

• It is possible and worthwhile to compare the dividend yield with the rate of interest.

• The dividend yield makes inter-firm comparisons possible.

10. Outline two possible external factors that need to be taken into account when conducting ratio analysis.(6 marks)

Answers may include:

• The trends observed in the market in which the firm is trading. A period of growth may produce vastlydifferent results from those achieved in a declining market.

• The quality of the management team and the workforce will not be shown directly through the appli-cation of ratio analysis.

• The position of the firm will also be important: a market leader would be expected to perform betterthan a relatively small new entrant.

ANALYSIS AND EVALUATION QUESTIONS

1. (a) Analyse whether the company’s director is right to be worried about the company’s liquidityposition. (10 marks)

Content3 marks

Application3 marks

Analysis4 marks

Level 3 3 marksCandidate identifies two ormore relevant points andshows understanding of theterm.

3 marksCandidate applies knowledgeeffectively to the scenario.

4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

Answers may include:

• The company’s acid test ratio has declined to a situation where it has little more than £1 available topay each £1 of current liabilities.

• It has a long cash cycle as a house builder.

• However, it has just completed a housing estate and the sale of houses is just starting, so this may alle-viate the position.

AQA Business Studies for A2

Cha

pter 3

(b) The company’s chief executive believes that financial ratios are of little use to analyse Steeple plc’scurrent position. Justify your decision. (15 marks)

© Hodder Education 2009

Answers may include:

• Financial ratios are the result of the comparison of two figures, e.g. profits and capital employed.

• The company is expecting a major cash inflow from the sale of the houses in Dorset, so liquidity ratiosmay be misleading.

• Dividend per share does not tell investors what is happening to the company’s share prices and thismight be more significant financially for the investors.

• The ratios are historical and do not necessarily predict the future.

• However, it appears that the company has borrowed more this year (perhaps to buy the land inBirmingham) and gearing would be a significant ratio for any creditors.

• Suppliers to the company would be interested in the company’s acid test ratio as an indicator of itsability to pay on time.

• The value of ratios varies according to the stakeholder that is involved and the reason for their interest.

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints and showsunderstanding of theterm.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

AQA Business Studies for A2

Cha

pter 3

© Hodder Education 2009

2. (a) Analyse how ratio analysis might help the company to make this decision. (10 marks)

Content3 marks

Application3 marks

Analysis4 marks

Level 3 3 marksCandidate identifies two ormore relevant points andshows understanding of theterm.

3 marksCandidate applies knowledgeeffectively to the scenario.

4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

Answers may include:

• Ratio analysis is a technique for analysing a business’s financial performance by comparing one pieceof accounting information with another.

• The acid test or current ratio will allow the company to assess its ability to finance this plan in the shortterm.

• Calculating gearing will assist the company in assessing its long-term ability to repay the loan.

• Its gearing figure will rise above 50 per cent if it goes ahead with this decision, which may be animportant factor.

• The company’s directors will be able to compare the forecast ROCE from the new project with thatachieved elsewhere in the business (21 per cent) and use this comparison to inform their decision.

(b) To what extent do you agree with the view that information on the market in which the companytrades is the most important information needed to supplement the ratio analysis? (15 marks)

AQA Business Studies for A2

Cha

pter 3

© Hodder Education 2009

Answers may include:

• It will help with the company’s decisions on pricing and will determine profitability to some degree.

• The market that Penhaligon plc is entering is highly competitive and this will be a major influence onthe company’s decision. In particular the likely reaction of competitors must be taken into account.

• The workforce will be an important influence, so an HR plan will be needed. This project is forecast toimprove the company’s cost efficiency.

• Operations will be vital. Will the company have the necessary capacity and can the new productionmethods meet quality standards?

• The results of ratio analysis need to be supplemented by a range of information from across the otherfunctions of the business as well as the market.

• Theimportanceof themarket insuchadecisionwilldependonthemarketpowerof thebusinessconcerned.

CASE STUDY

Questions1. Explain what is meant by ‘net assets’. (4 marks)

• Net assets are an indication of the net worth of a business.

• They are calculated by totalling non-current assets and net current assets (that is, current assets lesscurrent liabilities) and then deducting non-current liabilities.

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints and showsunderstanding of theterm.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

AQA Business Studies for A2

Cha

pter 3

© Hodder Education 2009

AQA Business Studies for A2

2. Analyse the possible implications for Rohan’s shareholders of the announcement of the proposedtakeover of Breckland Stores. (8 marks)

Cha

pter 3

Answers may include:

• Shareholders may be impressed by the long-term possibilities of this deal in terms of profitability andhence higher dividends.

• In the long term this takeover may result in higher share prices, allowing for a capital gain if thecompany is successful.

• Some analysts believe that Rohan paid too much for Breckland Stores – this may result in a fall in theshare price.

• If Rohan plc struggles to pay for the loans it has taken out for this deal (non-current liabilities haverisen significantly) then future profits (and dividends) may be lower.

• The short-term reaction of shareholders was to sell shares – the share price fell by 13.4 per cent in asingle day.

Content2 marks

Application3 marks

Analysis3 marks

Level 3 3 marksCandidate applies knowledgeeffectively to the scenario.

3 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

© Hodder Education 2009

AQA Business Studies for A2

Content2 marks

Application3 marks

Analysis3 marks

Evaluation4 marks

Level 3 3 marksCandidate appliesknowledge effectivelyto the scenario.

3 marksGood analysis ofargument.

4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant point.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

3. Using ratios to support your arguments, assess the case for and against the Rohan Group spending £229million on a takeover of Breckland Stores. (12 marks)

Cha

pter 3

Answers may include:

• The takeover improves the company’s geographical coverage of the UK.

• The company is committed to a period of rapid growth and this takeover is a central part of itsambitious expansion programme.

• The company could be considered to be overstretched, e.g. its gearing ratio is very high.

• Expenses are rising rapidly, suggesting that it is not controlling its costs effectively.

• The key point might be that Rohan is paying a price for Breckland that analysts regard as ‘too high’.

4. Discuss the value of ratio analysis in assessing the financial performance of the Rohan Group. (15 marks)

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 3

Content3 marks

Application3 marks

Analysis4 marks

Evaluation5 marks

Level 3 3 marksCandidate identifiestwo or more relevantpoints and showsunderstanding of theterm.

3 marksCandidate appliesknowledge effectivelyto the scenario.

4 marksGood analysis ofargument.

5–4 marksCandidate offersjudgement plus fulljustification.

Level 2 2 marksCandidate offers twoor more relevantpoints or shows goodunderstanding of theterm or acombination.

2 marksCandidate makesreasonable attemptto apply knowledgeto the scenario.

3–2 marksReasonable analysisof argument.

3–2 marksCandidate offersjudgement pluslimited justification.

Level 1 1 markCandidate offerssingle relevant pointor shows someunderstanding of theterm.

1 markCandidate attemptsto apply knowledgeto the scenario.

1 markLimited analysis ofargument.

1 markCandidate offersundevelopedjudgement based onevidence.

Answers may include:

• Ratio analysis is a technique for analysing a business’s financial performance by comparing one pieceof accounting information with another.

• Ratios provide an effective basis for the comparison of the performances of the business with other,larger, rivals.

• Ratio analysis puts financial investigation into a context – Rohan’s profits will be smaller than itscompetitors, but what about its ROCE figure?

• Ratio analysis ignores an enormous range of non-financial factors that may be critical determinants ofthe future performance of the business, e.g. the company’s need to have a broader geographicalcoverage.

• Ratio analysis is historical and may, particularly in view of Rohan’s expansion plans, be of limitedrelevance.

• Ratio analysis is just one tool for financial analysis and should be used cautiously and in conjunctionwith other types of analysis.

BUSINESS IN FOCUS

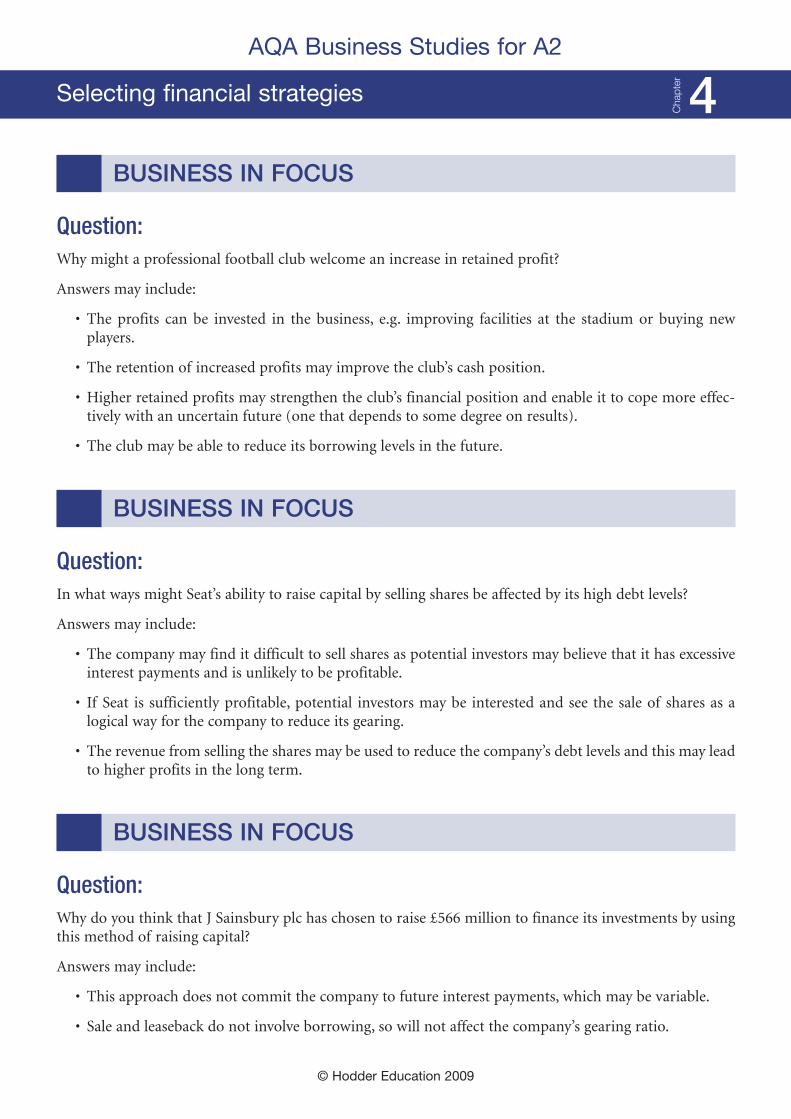

Question:Why might a professional football club welcome an increase in retained profit?

Answers may include:

• The profits can be invested in the business, e.g. improving facilities at the stadium or buying newplayers.

• The retention of increased profits may improve the club’s cash position.

• Higher retained profits may strengthen the club’s financial position and enable it to cope more effec-tively with an uncertain future (one that depends to some degree on results).

• The club may be able to reduce its borrowing levels in the future.

BUSINESS IN FOCUS

Question:In what ways might Seat’s ability to raise capital by selling shares be affected by its high debt levels?

Answers may include:

• The company may find it difficult to sell shares as potential investors may believe that it has excessiveinterest payments and is unlikely to be profitable.

• If Seat is sufficiently profitable, potential investors may be interested and see the sale of shares as alogical way for the company to reduce its gearing.

• The revenue from selling the shares may be used to reduce the company’s debt levels and this may leadto higher profits in the long term.

BUSINESS IN FOCUS

Question:Why do you think that J Sainsbury plc has chosen to raise £566 million to finance its investments by usingthis method of raising capital?

Answers may include:

• This approach does not commit the company to future interest payments, which may be variable.

• Sale and leaseback do not involve borrowing, so will not affect the company’s gearing ratio.

© Hodder Education 2009

AQA Business Studies for A2

Selecting financial strategies

Cha

pter 4

• Sainsbury’s may already have a high gearing level.

• The investments may generate a greater return than the supermarket generates on its property port-folio.

BUSINESS IN FOCUS

Question:How might Volkswagen intend to finance its expansion plans?

Answers may include:

• The company might use retained profits for at least part of the investment, given its increased sales.

• The company’s financial success will mean that it is able to negotiate loans at favourable terms withbanks.

• Shareholders may be willing to buy shares, given Volkswagen’s positive recent financial performance.

What would be the possible implications for other functions within the business of raising finance to builda factory in the United States?

Answers may include:

• The company’s HR function will need to recruit new employees to staff the US factory.

• There will be considerable implications for operations, e.g. managing production lines for new modelsto be manufactured in the United States.

• Marketing will be a key element in this expansion. This represents market development andVolkswagen will need to develop a new marketing strategy.

BUSINESS IN FOCUS

Question:What disadvantages might HSBC experience as a result of operating profit centres?

Answers may include:

• Centres may only consider ‘local’ issues when making decisions.

• The regions are quite different and it is not reasonable to make direct comparisons.

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 4

BUSINESS IN FOCUS

Question:In what ways might the policy of offshoring IT jobs add to the costs of UK businesses in the long run?

Answers may include:

• The move may mean that IT businesses have to pay higher wages to attract people into an industry thatappears to lack prospects.

• IT companies may face increased recruitment costs to attract high-calibre candidates.

• IT companies may suffer from high levels of labour turnover, given the lack of prospects in theindustry. This may add to recruitment and training costs.

BUSINESS IN FOCUS

Question:Why might a fashionable clothing brand decide to allocate its capital in this way?

Answers may include:

• The company’s corporate aims are based on expansion, and this method of allocating capital expendi-ture will assist in achieving this aim.

• Fashion markets are becoming global, making this an obvious financial strategy.

• Consumer spending in America has fallen, and moving into new markets may help to offset this.

• Presumably the new stores in Canada and the United States have been successful, encouraging thisfurther stage of development.

PROGRESS QUESTIONS

1. Outline two reasons why a car manufacturer may need to raise large sums of finance. (6 marks)

• It may need to invest in new production line equipment to improve productivity.

• It will have to invest regularly in newmodels of cars, possibly developing technology to reduce pollution.

• It may need to take over smaller rivals to acquire brands such as Jaguar.

• It may extend its production capacity to allow it to enter new markets.

2. Explain the benefits a business may receive from using retained profits to finance a major investmentprogramme. (6 marks)

• The business will not have to pay interest on this source of finance.

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 4

• It will not have a negative impact on the company’s gearing ratio.

• It will not dilute the existing shareholders’ control of the business.

• It will not dilute the value of shares

3. Explain why raising finance might be an appropriate financial strategy for a business aiming to sell in aglobal market. (8 marks)

• Operating in a global market might mean that the company needs to increase its productive capacity,requiring substantial investment.

• It might be essential to improve productivity and competitiveness to allow the business to operatesuccessfully in the global market.

• The business may need to develop new products to meet the needs of global consumers.

• A strategy of market development will require finance to establish distribution networks, for example.

4. Why might a business with a corporate objective of growth seek to raise finance through a mixture ofselling shares and negotiating bank loans? (8 marks)

• A growth objective may require large amounts of finance and thus a single source may not suffice.

• The sale of shares will not commit the company to fixed interest payments in the future.

• Raising finance through loans will not dilute shareholders’ control or the value of shares.

5. Why have many retailers with large numbers of stores chosen to raise finance through sale and leaseback?(8 marks)

• These are assets which have increased substantially in value over recent years, providing a major sourceof finance.

• The company avoids any interest charges (which may vary).

• There is no impact on share prices.

• Thecompanyavoidspaying tomaintainassets,whichcouldrequire substantial sumstobespent regularly.

6. Explain why implementing profit centres is a common financial strategy for large businesses with diverseproduct ranges. (8 marks)

• A business’s senior managers are not always able to control the diverse elements of the business asclosely or effectively as they would wish – profit centres allow some delegation of authority.

• Businesses can compare the financial performance of the areas which comprise the business.

• This canbe an importantmotivational and training strategy formiddlemanagers in a large organisation.

7. Why might the implementation of profit centres as a financial strategy have significant implications fora business’s HR department? (7 marks)

• The HR department may have to implement a training programme for its employees to operate theprofit centres successfully.

• It may need to recruit employees with financial skills if this strategy is put in place.

• The strategy may have a positive impact on motivation of certain employees, which may influenceother motivational policies that the HR department uses.

© Hodder Education 2009

AQA Business Studies for A2

Cha

pter 4

8. In what ways might a large business manufacturing non-branded T-shirts implement a financial strategyof cost minimisation? (8 marks)

• It may seek to produce much of its product range in less developed countries, thereby benefiting fromreduced labour costs.

• It couldprovidea limited rangeof products,seeking tobenefit as fully aspossible fromeconomiesof scale.

• It could use a flexible workforce to assist in minimising costs.

9. Why might a UK manufacturer choose to allocate finance to investing in technology? (5 marks)

• To reduce wage costs, hence cutting the overall cost of production.

• It should increase the business’s levels of productivity.

• More technology on the production line may enable a company to reduce its unit costs of productionin the long run.

• Quality may improve as defects are likely to be reduced.

10. Which types of business might opt to allocate large sums of capital expenditure to the purchase ofproperty? Explain your answer. (6 marks)

• Retailers frequently invest in high street locations, to be alongside other, similar, businesses.

• Banks require high street locations and secure, expensive properties to conduct their business successfully.

• Hotels, especially luxury hotels, will depend upon having suitable properties, often in expensive citylocations.

ANALYSIS AND EVALUATION QUESTIONS

1. (a) Analyse the possible reasons why Prestige Hotels has selected a financial strategy of allocating capitalexpenditure. (10 marks)

Content3 marks

Application3 marks

Analysis4 marks

Level 3 3 marksCandidate identifies two ormore relevant points andshows understanding of theterm.

3 marksCandidate applies knowledgeeffectively to the scenario.

4 marksGood analysis of argument.

Level 2 2 marksCandidate offers two or morerelevant points or showsgood understanding of theterm or a combination.

2 marksCandidate makes reasonableattempt to apply knowledgeto the scenario.

3–2 marksReasonable analysis ofargument.

Level 1 1 markCandidate offers singlerelevant point or shows someunderstanding of the term.

1 markCandidate makes limitedattempt to apply knowledgeto the scenario.

1 markLimited analysis of argument.

AQA Business Studies for A2

Cha

pter 4

© Hodder Education 2009

Answers may include:

• Capital expenditure is spending on new non-current assets such as property, machinery or vehicles.

• The company’s image and reputation are based on the provision of a luxury service, and purchasingexpensive property is an essential element of this.

• Customers expect the hotels to be equipped with expensive furniture and fittings, requiring substan-tial investment.

• The company has been highly profitable (its ROCE exceeded 30 per cent last year) and therefore it hasfunds available or can afford to finance further loans.

• It is planning to expand into some European cities, so further investment will be required.

(b) Discuss the likely consequences for the other functions within Prestige Hotels of the operation ofthis financial strategy. (15 marks)

© Hodder Education 2009

Answers may include: