Embed Size (px)

DESCRIPTION

Business Finance

Citation preview

BUSINESS FINANCE

UNIT I Business Finance: Introduction – Meaning – Concepts -Scope – Function of Finance Traditional and Modern Concepts – Contents of Modern Finance Functions.

INTRODUCTIONIn our present day economy, finance is defined as the provision of money at the time when it is required. Every enterprise, whether big, medium or small, needs finance to carry on its operations and to achieve its targets. In fact, finance is so indispensable today that it is rightly said to be the lifeblood of an enterprise.

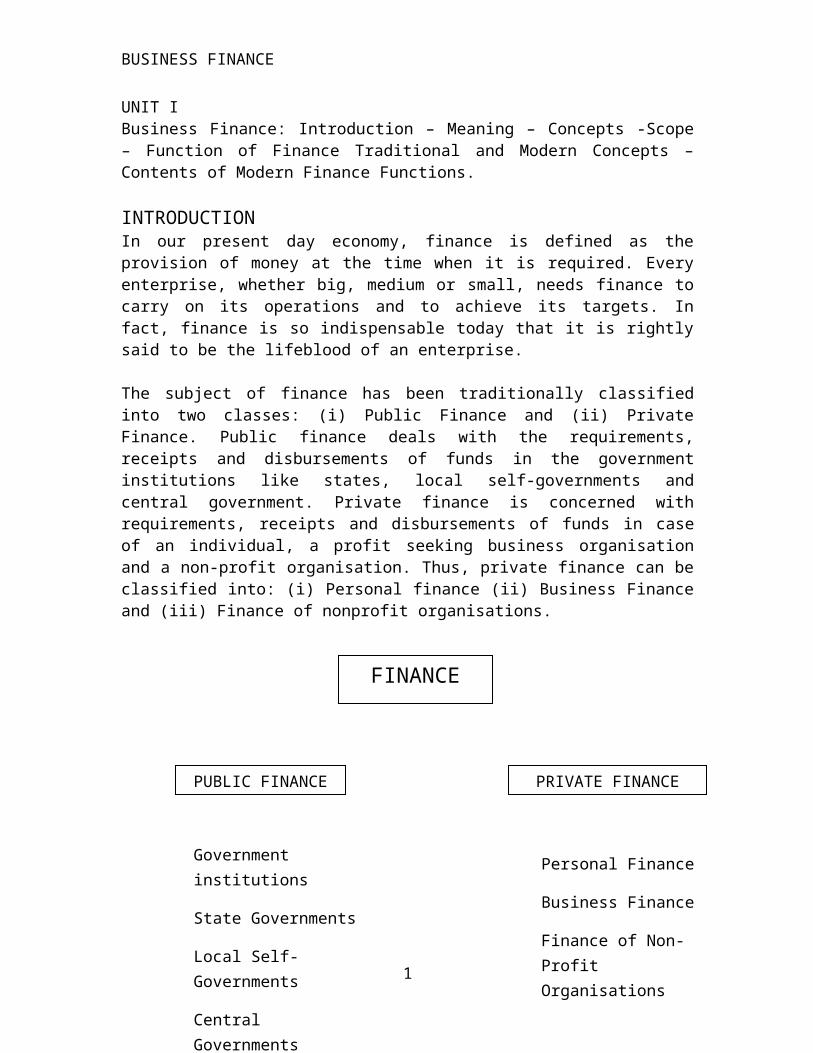

The subject of finance has been traditionally classified into two classes: (i) Public Finance and (ii) Private Finance. Public finance deals with the requirements, receipts and disbursements of funds in the government institutions like states, local self-governments and central government. Private finance is concerned with requirements, receipts and disbursements of funds in case of an individual, a profit seeking business organisation and a non-profit organisation. Thus, private finance can be classified into: (i) Personal finance (ii) Business Finance and (iii) Finance of nonprofit organisations.

MEANING OF FINANCE

The word finance was originally a French word. In the 18 th century, it was adapted by English speaking communities to mean “the management of money.” It is the study of how people allocate their assets over time under conditions of certainty and uncertainty. Today, finance is not merely a word else has emerged into an academic discipline of greater significance. Finance is now organized as a branch of Economics. Every enterprise needs finance to carry on its operations. It is the lifeblood of any business. The objective of the business could not be achieved without finance.

1

FINANCE

PUBLIC FINANCE PRIVATE FINANCE

Government institutions

State Governments

Local Self-Governments

Central Governments

Personal Finance

Business Finance

Finance of Non-Profit Organisations

BUSINESS FINANCE

Finance is nothing but an exchange of available resources. Finance is not restricted only to the exchange and/or management of money. A barter trading system is also a type of finance. Thus, we can say, Finance is an art of managing various available resources like money, assets, investments, securities, etc. Finance is the science of managing financial resources in an optimal pattern i.e. the best use of available financial sources.

Finance consists of three interrelated areas1) Money & Capital markets, which deals with securities markets & financial Institutions.2) Investments, which focuses on the decisions of both individual and institutionalInvestors as they choose assets for their investment portfolios.3) Financial Management, or business finance which involves the actual management of Firms.

DEFINITIONS OF FINANCEIn General sense, "Finance is the management of money and other valuables, which can be easily converted into cash."

According to Entrepreneurs, "Finance is concerned with cash. It is so, since, every business transaction involves cash directly or indirectly."

According to Academicians, "Finance is the procurement (to get, obtain) of funds and effective (properly planned) utilization of funds. It also deals with profits that adequately compensate for the cost and risks borne by the business."

Meaning of Business financeBusiness finance refers to using an outside resource to help cover the financial needs of a business. It is an activity or a process, which is concerned with acquisition of funds, use of funds and distribution of profits by a business firm. Thus it deals with financial planning, acquisition of funds, use and allocation funds and financial controls.

The following characteristics of business finance will make its meaning clearer Business finance includes all types of funds used in business. Business finance is needed in all types of organisations large or small,

manufacturing or trading. The amount of business finance differs from one business firm to another

depending upon its nature and size. It also varies from time to time. Business finance involves estimation of funds. It is concerned with raising funds

from different sources as well as investment of funds for different purposes.

NEED AND IMPORTANCE OF BUSINESS FINANCE

Business finance is required for the establishment of every business organisation. With the growth in activities, financial needs also grow. Funds are required for the purchase of land and building, machinery and other fixed assets. Besides this, money is also needed

2

BUSINESS FINANCE

to meet day-today expenses e.g. purchase of raw material, payment of wages and salaries, electricity bills, telephone bills etc. You are aware that production continues in anticipation of demand. Expenses continue to be incurred until the goods are sold and money is recovered. Money is required to bridge the time gap between production and sales. Besides producers, may be necessary to change the office set up in order to install computers. Renovation of facilities can be taken up only when adequate funds are available.

1. To meet contingenciesFunds are always required to meet the ups and downs of business and unforeseen problems. Suppose, some manufacturer anticipates shortage of raw materials after a period. Obviously he would like to stock raw materials. But he will be able to do so only when money would be available.

2. To promote salesIn this era of competition, lot of money is required to be spent on activities for promoting sales like advertisement, personal selling, home delivery of goods etc.

3. To avail of business opportunitiesFunds are also required to avail of business opportunities. Suppose a company wants to submit a tender but some minimum amount is required to be deposited along with the application. In the case of non-availability of funds it would not be possible for the company to apply.

Financial Management

Financial management refers to that part of the management activity which is concerned with the planning and controlling of firm’s financial resources, it deal with finding out various sources for raising funds for the firm. The sources must be suitable and economical for the needs of business. The most appropriate use of such funds also forms a part of financial management.

EVOLUTION OF FINANCIAL MANAGEMENT

Financial management emerged as a distinct field of study at the turn of this century. Its evolution may be divided into three broad phases (though the demarcating lines between these phases are somewhat arbitrary): the traditional phase, the transitional phase, and the modern phase. The traditional phase lasted for about four decades. The following were its important features

1. The focus of financial management was mainly on certain episodic events like formation, issuance of capital, major expansion, merger, reorganization, and liquidation in the life cycle of the firm.2. The approach was mainly descriptive and institutional. The instruments of financing, the institutions and procedures used in capital markets, and the legal aspects of financial events formed the core of financial management.

3

BUSINESS FINANCE

3. The outsider’s point of view was dominant. Financial management was viewed mainly from the point of the investment bankers, lenders, and other outside interests. The transitional phase begins around the early forties and continues through the early fifties. Though the nature of financial mgmt during this phase was similar to that of the traditional phase, greater emphasis was placed on the day to day problem faced by the finance managers in the area of funds analysis, planning, and control. These problems however were discussed within limited analytical framework. The modern phase begin in mid 50’s and has witnessed an accelerated pace of development with the infusion of ideas from economic theories and applications of quantitative methods of analysis.The distinctive features of modern phase are* The scope of financial management has broadened. The central concern of financial management is considered to be a rational matching of funds to their uses in the light of appropriate decision criteria* The approach of financial management has become more analytical and quantitative* The point of view of the managerial decision maker has become dominant Since the beginning of the modern phase many significant and seminal developments have occurred in the fields of capital budgeting, capital structure theory, efficient market theory, optional pricing theory, agency theory, arbitrage pricing theory, valuation models, dividend policy, working capital management, financial modeling, and behavioral finance. Many more exciting developments are in the offing making finance a fascinating and challenging field.

Goals of financial management

Financial theory in general rests on the premises that the goal of the firm should be maximized the value of the firm to its equity share holders. This means that the goal of the firm should be to maximize the share value of the equity share which represents the value of the firm to its equity share holders. It appears to provide a rational guide for business decision making and promote an efficient allocation of resources in the economic system. Savings are allocated primarily on the basis of expected returns and risk and the market value of the firm’s equity stock reflects the risk return trade off investors in the market place.

If a firm makes decision aimed at maximizing the market value of its equity, it will raise capital only when its investments warrant the use of capital from the overall point of the economy. This suggests that resources are allocated optimally. If a firm does not pursue the goal of shareholders wealth maximization, it implies that its action results in a sub optimal allocation of resources. This in turn leads to inadequate capital formation and lower rate of economic growth. Equity shareholders provide the venture capital required to start a business firm and appoint he management of the firm indirectly through the board of directors.. Therefore it is obligatory on the part of corporate management to take care of the welfare of equity shareholders.

SCOPE OF FINANCIAL MANAGEMENT

Financial management is one of the important parts of overall management, which is

4

BUSINESS FINANCE

directly related with various functional departments like personnel, marketing and production. Financial management covers wide area with multidimensional approaches. The following are the important scope of financial management.

1. Financial Management and Economics Economic concepts like micro and macroeconomics are directly applied with the financial management approaches. Investment decisions, micro and macro environmental factors are closely associated with the functions of financial manager. Financial management also uses the economic equations like money value discount factor, economic order quantity etc. Financial economics is one of the emerging area, which provides immense opportunities to finance, and economical areas.

2. Financial Management and Accounting Accounting records includes the financial information of the business concern. Hence, we can easily understand the relationship between the financial management and accounting. In the olden periods, both financial management and accounting are treated as a same discipline and then it has been merged as Management Accounting because this part is very much helpful to finance manager to take decisions. But nowaday’s financial management and accounting discipline are separate and interrelated.

3. Financial Management or Mathematics Modern approaches of the financial management applied large number of mathematical and statistical tools and techniques. They are also called as econometrics. Economic order quantity, discount factor, time value of money, present value of money, cost of capital, capital structure theories, dividend theories, ratio analysis and working capital analysis are used as mathematical and statistical tools and techniques in the field of financial management.

4. Financial Management and Production Management Production management is the operational part of the business concern, which helps to multiple the money into profit. Profit of the concern depends upon the production performance. Production performance needs finance, because production department requires raw material, machinery, wages, operating expenses etc. These expenditures are decided and estimated by the financial department and the finance manager allocates the appropriate finance to production department. The financial manager must be aware of the operational process and finance required for each process of production activities.

5. Financial Management and Marketing Produced goods are sold in the market with innovative and modern approaches. For this, the marketing department needs finance to meet their requirements. The financial manager or finance department is responsible to allocate the adequate finance to the marketing department. Hence, marketing and financial management are interrelated and depends on each other.

5

BUSINESS FINANCE

6. Financial Management and Human Resource Financial management is also related with human resource department, which provides manpower to all the functional areas of the management. Financial manager should carefully evaluate the requirement of manpower to each department and allocate the finance to the human resource department as wages, salary, remuneration, commission, bonus, pension and other monetary benefits to the human resource department. Hence, financial management is directly related with human resource management.

IMPORTANCE OF FINANCIAL MANAGEMENT In a big organization, the general manger or the managing director is the overall incharge of the organization but he gets all the activities done by delegating all or some of his powers to men in the middle or lower management, who are supposed to be specialists in the field so that better results may be obtained.

For example, management and control of production may be delegated to a man who is specialist in the techniques, procedures, and methods of production. We may designate him “Production Manager'. So is the case with other branches of management, i.e., personnel, finance, sales etc.

The incharge of the finance department may be called financial manger, finance controller, or director of finance who is responsible for the procurement and proper utilisation of finance in the business and for maintaining co-ordination between all other branches of management.

Importance of finance cannot be over-emphasized. It is, indeed, the key to successful business operations. Without proper administration of finance, no business enterprise can reach its full potentials for growth and success. Money is a universal lubricant which keeps the enterprise dynamic-develops product, keeps men and machines at work, encourages management to make progress and creates values. The importance of financial administration can be discussed under the following heads:-

1. Success of Promotion Depends on Financial Administration. One of the most important reasons of failures of business promotions is a defective financial plan. If the plan adopted fails to provide sufficient capital to meet the requirement of fixed and fluctuating capital an particularly, the latter, or it fails to assume the obligations by the corporations without establishing earning power, the business cannot be carried on successfully. Hence sound financial plan is very necessary for the success of business enterprise.

2. Smooth Running of an Enterprise. Sound Financial planning is necessary for the smooth running of an enterprise. Money is to an enterprise, what oil is to an engine. As, Finance is required at each stage f an enterprise, i.e., promotion, incorporation, development, expansion and administration of day-to-day working etc., proper administration of finance is very necessary. Proper financial administration means the

6

BUSINESS FINANCE

study, analysis and evaluation of all financial problems to be faced by the management and to take proper decision with reference to the present circumstances in regard to the procurement and utilisation of funds.

3. Financial Administration Co-ordinates Various Functional Activities. Financial administration provides complete co-ordination between various functional areas such as marketing, production etc. to achieve the organisational goals. If financial management is defective, the efficiency of all other departments can, in no way, be maintained. For example, it is very necessary for the finance-department to provide finance for the purchase of raw materials and meting the other day-to-day expenses for the smooth running of the production unit. If financial department fails in its obligations, the Production and the sales will suffer and consequently, the income of the concern and the rate of profit on investment will also suffer. Thus Financial administration occupies a central place in the business organisation which controls and co-ordinates all other activities in the concern.

4. Focal Point of Decision Making. Almost, every decision in the business is take in the light of its profitability. Financial administration provides scientific analysis of all facts and figures through various financial tools, such as different financial statements, budgets etc., which help in evaluating the profitability of the plan in the given circumstances, so that a proper decision can be taken to minimise the risk involved in the plan.

5. Determinant of Business Success. It has been recognised, even in India that the financial manger splay a very important role in the success of business organisation by advising the top management the solutions of the various financial problems as experts. They present important facts and figures regarding financial position an the performance of various functions of the company in a given period before the top management in such a way so as to make it easier for the top management to evaluate the progress of the company to amend suitably the principles and policies of the company. The financial manges assist the top management in its decision making process by suggesting the best possible alternative out of the various alternatives of the problem available. Hence, financial management helps the management at different level in taking financial decisions.

6. Measure of Performance. The performance of the firm can be measured by its financial results, i.e, by its size of earnings Riskiness and profitability are two major factors which jointly determine the value of the concern. Financial decisions which increase risks will decrease the value of the firm and on the to the hand, financial decisions which increase the profitability will increase value of the firm. Risk an profitability are two essential ingredients of a business concern.

CLASSIFICATION OF FINANCE

PRIVATE FINANCE Personal finance and Business finance.

7

Finance

Private Finance Public Finance

BUSINESS FINANCE

The personal finance is concerned with the acquisition and the proper utilization of economic resource by the individuals and households for meeting their different needs.

The business finance is also a part of private finance. The business finance is concerned with the acquisition, management and utilization of fund by the private business organizations.

PUBLIC FINANCE Is the study supports the financial aspect of the government? Here we study about the government expenditure, public revenue, public borrowing and financial administration. The economic activities of the public enterprises also fall under public finance. The objective of private of business finance is to earn maximum return or profit. On the contrary the objective of public finance is to maximize social welfare.

APPROACHES TO FINANCE FUNCTIONThe finance function also plays a key role in articulating business performance and enabling management to address and react to trends quickly. Financial management has undergone significant changes, over the years in its scope and coverage. Approaches: Broadly, it has two, as mentioned below:

TRADITIONAL APPROACH

The traditional approach to the scope of financial management refers to its subject matter in the academic literature in the initial stages of its evolution as a separate branch of study. According to this approach, the scope of financial management is confined to the raising of funds. Hence, the scope of finance was treated by the traditional approach in the narrow sense of procurement of funds by corporate enterprise to meet their financial needs. Since the main emphasis of finance function at that period was on the procurement of funds, the subject was called corporation finance till the mid-1950's and covered discussion on the financial instruments, institutions and practices through which funds are obtained. Further, as the problem of raising funds is more intensely felt at certain episodic events such as merger, liquidation, consolidation, reorganization and so on. These are the broad features of the subject matter of corporation finance, which has no concern with the decisions of allocating firm's funds. But the scope of finance function in the traditional approach has now been discarded as it suffers from serious criticisms. Again, the limitations of this approach fall into the following categories.

The emphasis in the traditional approach is on the procurement of funds by the corporate enterprises, which was woven around the viewpoint of the suppliers of funds such as investors, financial institutions, investment bankers, etc, i.e. outsiders. It implies that the traditional approach was the outsider-looking-in approach. Another limitation was that internal financial decision-making was completely ignored in this approach.

The second criticism leveled against this traditional approach was that the scope of financial management was confined only to the episodic events such as mergers, acquisitions, reorganizations, consolation, etc. The scope of finance function in this

8

BUSINESS FINANCE

approach was confined to a description of these infrequent happenings in the life of an enterprise. Thus, it places over emphasis on the topics of securities and its markets, without paying any attention on the day to day financial aspects.

Another serious lacuna in the traditional approach was that the focus was on the long-term financial problems thus ignoring the importance of the working capital management. Thus, this approach has failed to consider the routine managerial problems relating to finance of the firm.

During the initial stages of development, financial management was dominated by the traditional approach as is evident from the finance books of early days. The traditional approach was found in the first manifestation by Green's book written in 1897, Meades on Corporation Finance, in 1910; Doing's on Corporate Promotion and Reorganisation, in 1914, etc.

As stated earlier, in this traditional approach all these writings emphasized the financial problems from the outsiders' point of view instead of looking into the problems from managements, point of view. It over emphasized long-term financing lacked in analytical content and placed heavy emphasis on descriptive material. Thus, the traditional approach omits the discussion on the important aspects like cost of the capital, optimum capital structure, valuation of firm, etc. In the absence of these crucial aspects in the finance function, the traditional approach implied a very narrow scope of financial management. The modern or new approach provides a solution to all these aspects of financial management.

According to this approach the scopes of finance function was confined to only procurement of funds needed by a business on most suitable terms. The utilization of funds was considered beyond the purview of finance function. It was felt that decisions regarding application of funds are taken somewhere else in the organization. The scope of finance function was treated, in the narrow sense of procurement or arrangement of funds. It was felt that the finance manager had no role to play in decision making for its utilization

As per this approach, the following aspects only were included in the scope of financial management

1. Estimation of requirements of finance,2. Arrangement of funds from financial institutions,3. Arrangement of funds through financial instruments such as shares, debentures,

bonds and loans, 4. Looking after the accounting and legal work connected with the raising of funds.The limitations are1. It is outsider-looking approach that completely ignores internal decision-making as to

the proper utilization of funds.2. The focus of traditional approach was on procurement of long term funds. Thus, it

ignored the important issue of working capital finance and management.

9

BUSINESS FINANCE

3. The issue of allocation of funds, which is so important today, is completely ignored.4. It does not lay focus on day-to-day financial problems of an organization.

MODERN APPROACH

After the 1950's, a number of economic and environmental factors, such as the technological innovations, industrialization, intense competition, interference of government, growth of population, necessitated efficient and effective utilisation of financial resources. In this context, the optimum allocation of the firm's resources is the order of the day to the management. Then the emphasis shifted from episodic financing to the managerial financial problems, from raising of funds to efficient and effective use of funds. Thus, the broader view of the modern approach of the finance function is the wise use of funds. Since the financial decisions have a great impact on all other business activities, the financial manager should be concerned about deter-mining the size and nature of the technology, setting the direction and growth of the business, shaping the profitability, amount of risk taking, selecting the asset mix, determination of optimum capital structure, etc.

The new approach is thus an analytical way of viewing the financial problems of a firm. According to the new approach, the financial management is concerned with the solution of the major areas relating to the financial operations of a firm, viz., investment, and financing and dividend decisions. The modern financial manager has to take financial decisions in the most rational way. These decisions have to be made in such a way that the funds of the firm are used optimally. These decisions are referred to as managerial finance functions since they require special care with extraordinary administrative ability, management skills and decision - making techniques, etc.

It views finance function in broader sense. It includes both rising of funds as well as their effective utilization under the preview of finance. The modern approach considers the three basic management decisions. i.e., Investment decisions, financing decisions and dividend decisions within the scope of finance function. Financial management is considered as vital and an integral part of overall management. The modern approach is analytical way of looking into the financial problems of the firm.Advice of finance manager is required at every moment, whenever any decision with involvement of funds is taken. Hardly, there is an activity that does not involve funds.

SCOPE OF FINANCIAL MANAGEMENT

Estimating financial requirements: The amount required for purchasing fixed assets as well as needs of funds for working capital will have to be ascertained.

Deciding capital structure: The proportion of how the funds should be raised has to be decided. A decision about various sources for funds should be linked to the cost of raising funds.

10

BUSINESS FINANCE

Selecting a source of finance: After preparation of capital structure, an appropriate source of finance is selected. It includes share capital, debentures. Financial institutions, commercial banks, public deposits etc

Selecting pattern of Investment: Decision has to be taken on where the funds procured or raised should be invested. Techniques such as Capital budgeting, Opportunity Cost Analysis etc. may be applied for this purpose

Proper Cash Management: Various cash needs at different times has to be assessed. The cash management should be in such a way that there is neither shortage of cash nor it is idle.

Proper use of surplus: A judicious use of surpluses is essential for expansion and diversification of plans and also in protecting the interests of shareholders.

Implementing Financial controls: Efficient system of financial management necessitates the use of various control devices.

The control devices and techniques help in evaluating the performance in various areas and take corrective measures.

1. Budgetary control, 2. Break-even analysis, 3. Cost control, 4. Ratio analysis5. Cost and internal audit. 6. Return on investment

AREAS & CONCEPTS OF FINANCIAL MANAGEMENT As already discussed, the general meaning of finance refers to providing funds, as and when needed. However, as management function, the term ‘Financial Management’ has a distinct meaning. Financial management deals with the study of procuring funds and it’s effective and judicious utilization, in terms of the overall objectives of the firm, and expectations of the providers of funds. The basic objective is to maximize the value of the firm.

“Financial Management is concerned with the efficient use of an important economic resource, namely, Capital Funds” – Solomon

“Financial Management is concerned with the managerial decisions that result in the acquisition and financing of short-term and long-term credits for the firm” – Phillioppatus

“Business finance is that business activity which is concerned with the conservation and acquisition of capital funds in meeting financial needs and overall objectives of a business enterprise” - Wheeler

AREAS OF FINANCIAL MANAGEMENT

11

BUSINESS FINANCE

Analysis of Financial StatementsAnalysis of financial statement is one of the most common techniques of financial analysis, in which the financial performance and financial health of the companies are analyzed based on its past performance.

The following financial statements are used in the analysis process. Profit & Loss Statement or Income Statement Balance Sheet Statement of Shareholders’ equity Statement of Cash Flow

Investment Decisions & Capital BudgetingInvestment decisions are the most critical as they usually involve huge sum of money and these decisions are likely to bring prosperity or end to a business. A company’s future income depends on how much investment is made, in what type of assets, and how these assets add to the overall value of the company.

Capital budgeting is a term strictly related to investment in fixed assets. Here, the term capital refers to the fixed assets that are used in production, while budget is a plan which details projected cash inflows and outflows over some future period. The following concepts and techniques are employed while analyzing investment decisions.

Interest rate formulas Time Value of Money Discounted Cash Flows Net Present Value Internal Rate of Return

Risk & ReturnInvestors, individual or institutional, invest their money with the expectations of earning a return on their investment. While investors wish and attempt to earn maximum return, they are constrained by risk. How the risks and returns are related and how do investors make a choice of their portfolios is important for investment decision-making. Following concepts and theories would be discussed while discussing the risk-return choices of the investor.

Uncertainty Risk Portfolio Theory and Capital Asset Pricing Model

Corporate Financing & Capital StructureWhen a firm plans to expand, it needs capital or funds. Acquisition of funds is considered to be a primary responsibility of a finance department in an organization. There are

12

BUSINESS FINANCE

numerous ways to acquire funds, i.e., finances can be raised in the form of debt or equity. The proportion of debt and equity constitutes the capital structure of the firm. Financial experts attempt to find a combination of debt and equity that could increase the overall value of the company, i.e., they try to find the optimal capital structure. The following concepts would be used to understand how an optimal capital structure could be attained.

Cost of Capital Leverage Dividend Policy Debt Instruments Valuation.

Asset or company valuation is important not only for financial managers, but also for creditors and investors. It is important to know the value of the company or its assets to make important financing and investment choices. Different valuation techniques and factors that influence the value of a company or its financial instruments would be discussed

Share Bond Option Corporate

Working Capital & Inventory ManagementWorking capital and inventory management pertains to the effective management of current assets. As we will see, an optimal and effective utilization of working capital and inventory increases the operating efficiency of the firm.

International Finance & foreign exchangeWith the increasing importance of international trade and global markets, the role of international finance has increased manifold. In a global environment, the finance managers have more choices pertaining to investing and financing than ever before. However, it is important to understand the implications of working in a global environment, since fluctuations in the currency rates can convert a good financing or investment decision into a bad one.

ROLE OF FINANCE MANGER Financial manger is the person responsible for carrying out the finance function. He occupies the key position in an organization.

Raising of Fund 1. See that firm has adequate cash to meet the daily needs.2. Make financial decisions3. Raise the needed funds form combination of various sources.

Funds Allocation

13

BUSINESS FINANCE

Using skills and techniques in implementing a system of optimum allocation of firm’s resources. There should be efficient allocation of resources. Financial manger must find a rationale for answering the following questionsi. How large should an enterprise be and how fast should it grow?ii. In What form should it hold its assets?iii. How should the funds required be raised?

The answers will three broad decisions 1. Investment,2. Financing and 3. Dividend.

FUNCTIONS OF FINANCE MANAGER

Finance function is one of the major parts of business organization, which involves the permanent, and continuous process of the business concern. Finance is one of the interrelated functions which deal with personal function, marketing function, production function and research and development activities of the business concern. At present, every business concern concentrates more on the field of finance because, it is a very emerging part which reflects the entire operational and profit ability position of the concern. Deciding the proper financial function is the essential and ultimate goal of the business organization.

Finance manager is one of the important role players in the field of finance function. He must have entire knowledge in the area of accounting, finance, economics and management. His position is highly critical and analytical to solve various problems related to finance. A person who deals finance related activities may be called finance manager.

Finance manager performs the following major functions:

1. Forecasting Financial Requirements It is the primary function of the Finance Manager. He is responsible to estimate the financial requirement of the business concern. He should estimate, how much finances required to acquire fixed assets and forecast the amount needed to meet the working capital requirements in future.

2. Acquiring Necessary Capital After deciding the financial requirement, the finance manager should concentrate how the finance is mobilized and where it will be available. It is also highly critical in nature.

3. Investment Decision The finance manager must carefully select best investment alternatives and consider the reasonable and stable return from the investment. He must be well versed in the field of capital budgeting techniques to determine the effective utilization of investment. The finance manager must concentrate to principles of

14

BUSINESS FINANCE

safety, liquidity and profitability while investing capital.

4. Cash Management Present days cash management plays a major role in the area of finance because proper cash management is not only essential for effective utilization of cash but it also helps to meet the short-term liquidity position of the concern.

5. Interrelation with Other Departments Finance manager deals with various functional departments such as marketing, production, personel, system, research, development, etc. Finance manager should have sound knowledge not only in finance related area but also well versed in other areas. He must maintain a good relationship with all the functional departments of the business organization.

IMPORTANCE OF FINANCIAL MANAGEMENTFinancial management is indispensable in any organization as it helps in 1. Financial planning and successful promotion of an enterprise2. Acquisition of funds as and when required a minimum possible cost.3. Proper use and allocation of funds4. Taking sound financial decisions5. Improving the profitability through financial controls6. Increasing the wealth of the investors and the nation 7. Promoting and mobilizing individual and corporate savings

Finance is the lifeblood of business organization. It needs to meet the requirement of the business concern. Each and every business concern must maintain adequate amount of finance for their smooth running of the business concern and also maintain the business carefully to achieve the goal of the business concern. The business goal can be achieved only with the help of effective management of finance. We can’t neglect the importance of finance at any time at and at any situation. Some of the importance of the financial management is as follows:

Financial PlanningFinancial management helps to determine the financial requirement of the business concern and leads to take financial planning of the concern. Financial planning is an important part of the business concern, which helps to promotion of an enterprise.

Acquisition of FundsFinancial management involves the acquisition of required finance to the business concern. Acquiring needed funds play a major part of the financial management, which involve possible source of finance at minimum cost.Proper Use of FundsProper use and allocation of funds leads to improve the operational efficiency of the business concern. When the finance manager uses the funds properly, they can reduce the cost of capital and increase the value of the firm.

15

BUSINESS FINANCE

Financial DecisionFinancial management helps to take sound financial decision in the business concern. Financial decision will affect the entire business operation of the concern. Because there is a direct relationship with various department functions such as marketing, production personnel, etc.

Improve ProfitabilityProfitability of the concern purely depends on the effectiveness and proper utilization of funds by the business concern. Financial management helps to improve the profitability position of the concern with the help of strong financial control devices such as budgetary control, ratio analysis and cost volume profit analysis.

Increase the Value of the FirmFinancial management is very important in the field of increasing the wealth of the investors and the business concern. Ultimate aim of any business concern will achieve the maximum profit and higher profitability leads to maximize the wealth of the investors as well as the nation.

Promoting SavingsSavings are possible only when the business concern earns higher profitability and maximizing wealth. Effective financial management helps to promoting and mobilizing individual and corporate savings.

Nowadays financial management is also popularly known as business finance or corporate finances. The business concern or corporate sectors cannot function without the importance of the financial management.

FUNCTIONS OF FINANCEFinance function is the most important function of a business. Finance is, closely, connected with production, marketing and other activities. In the absence of finance, all these activities come to a halt. in fact, only with finance, a business activity can be commenced, continued and expanded. Finance exists everywhere, be it production, marketing, human resource development or undertaking research activity. Understanding the universality and importance of finance, finance manager is associated, in modern business, in all activities as no activity can exist without funds.

AIMS OF FINANCE FUNCTION

1. Acquiring sufficient and suitable funds: The primary aim of finance function is to assess the needs of the enterprise, properly, and procure funds, in time. Time is also an important element in meeting the needs of the organisation. If the funds are not available as and when required, the firm may become sick or, at least, the profitability of the firm would be, definitely, affected. It is necessary that the funds should be, reasonably, adequate to the demands of the firm. The funds should be raised from different sources, commensurate to the nature of business and risk profile of the organisation. When the

16

BUSINESS FINANCE

nature of business is such that the production does not commence, immediately, and requires long gestation period, it is necessary to have the long-term sources like share capital, debentures and long term loan etc. A concern with longer gestation period does not have profits for some years. So, the firm should rely more on the permanent capital like share capital to avoid interest burden on the borrowing component.

2. Proper Utilization of Funds: Raising funds is important, more than that is its proper utilization. If proper utilization of funds were not made, there would be no revenue generation. Benefits should always exceed cost of funds so that the organization can be profitable. Beneficial projects only are to be undertaken. So, it is all the more necessary that careful planning and cost-benefit analysis should be made before the actual commencement of projects.

3. Increasing Profitability: Profitability is necessary for every organization. The planning and control functions of finance aim at increasing profitability of the firm. To achieve profitability, the cost of funds should be low. Idle funds do not yield any return, but incur cost. So, the organization should avoid idle funds. Finance function also requires matching of cost and returns of funds. If funds are used efficiently, profitability gets a boost.

4. Maximizing Firm’s Value: The ultimate aim of finance function is maximizing the value of the firm, which is reflected in wealth maximisation of shareholders. The market value of the equity shares is an indicator of the wealth maximisation.

THE MAIN OBJECTIVES OF FINANCIAL MANAGEMENT DEALS WITH

PROFIT MAXIMIZATION Objective of financial management is same as the objective of a company that is to earn profit. But profit maximization cannot the sole objective of a company. It is a limited objective. If profits are given undue Importance then problems may arise as discussed below.

The term profit is vague and it involves much more contradictions. Profit maximization has to be attempted with a realization of risks involved. A positive relationship exists between risk and profits. So both risk and profit objectives should be balanced. Profit Maximization does not take into account the time pattern of returns. Profit maximization fails to take into account the social considerations. It is the main objective of any business.

It is a measure of efficiency of any business. The arguments in favor of Profit maximization are as follows

Profit maximization is the obvious objective Justified on the grounds of its rationality Economic and business conditions do not remain same at all times.

Therefore a business should be survived under unfavorable condition only if it has some past earnings to rely upon.

17

BUSINESS FINANCE

Profits are needed for growth and development. Essential for fulfilling social goals.

Favorable Arguments for Profit MaximizationThe following important points are in support of the profit maximization objectives of the business concern:

(i) Main aim is earning profit. (ii) Profit is the parameter of the business operation. (iii) Profit reduces risk of the business concern. (iv) Profit is the main source of finance. (v) Profitability meets the social needs also.

Unfavorable Arguments for Profit Maximization

The following important points are against the objectives of profit maximization:

(i) Profit maximization leads to exploiting workers and consumers. (ii) Profit maximization creates immoral practices such as corrupt practice, unfair

trade practice, etc. (iii) Profit maximization objectives leads to inequalities among the stake holders such

as customers, suppliers, public shareholders, etc.

Drawbacks of Profit Maximization

Profit maximization objective consists of certain drawback also:

(i) It is vague: In this objective, profit is not defined precisely or correctly. It creates some unnecessary opinion regarding earning habits of the business concern.

(ii) It ignores the time value of money: Profit maximization does not consider the time value of money or the net present value of the cash inflow. It leads certain differences between the actual cash inflow and net present cash flow during a particular period.

(iii) It ignores risk: Profit maximization does not consider risk of the business concern. Risks may be internal or external which will affect the overall operation of the business concern.

PROFIT MAXIMIZATION IS REJECTED BECAUSE OF THE FOLLOWING DRAWBACKS

The term profit is vague Ignores the time value of money It doesn’t take the risk prospective into consideration The market price of the shares is not considered.

WEALTH MAXIMIZATION

18

BUSINESS FINANCE

It is the maximizing of value of stock as course of action to shareholders. When the firm maximizes the stock holder’s wealth, the individual stock holders can use this wealth to maximize his individual utility.

It is commonly agreed that the objective of a firm is to maximize value or wealth. Value of a firm is represented by the market price of the company's common stock. The market price of a firm's stock represents the focal judgment of all market participants as to what the value of the particular firm is. It takes in to account present and prospective future earnings per share, the timing and risk of these earning, the dividend policy of the firm and many other factors that bear upon the market price of the stock. Market price acts as the performance index or report card of the firm's progress.

Prices in the share markets are largely affected by many factors like general economic outlook, outlook of particular company, technical factors and even mass psychology. Normally this value is a function of two factors as given below, the anticipated rate of earnings per share of the company the capitalization rate.

The likely rate of earnings per shares (EPS) depends upon the assessment as to how profitably a company is growing to operate in the future.

The capitalization rate reflects the liking of the investors for the company. Methods of Financial Management: In the field of financing there are various methods to procure funds. Funds may be obtained from long-term sources as well as from short-term sources. Long-term funds may be availed by owners that are shareholders, lenders by issuing debentures, from financial institutions, banks and public at large. Short-term funds may be availed from commercial banks, public deposits, etc. Financial leverage or trading on equity is an important method by which a finance manager may increase the return to common shareholders.

At the time of evaluating capital expenditure projects methods like average rate of return, pay back, internal rate of returns, net present value and profitability index are used. A firm can increase its profitability without affecting its liquidity by an efficient utilization of the current resources at the disposal of the firm. A firm can increase its profitability without affecting its liquidity by an efficient management of working capital.

Similarly for the evaluation of a firm's performance there are different methods. Ratio analysis is a popular technique to evaluate different aspects of a firm. An investor takes in to account various ratios to know whether investment in a particular company will be profitable or not. These ratios enable him to judge the profitability, solvency, and liquidity and growth aspect of the firm.

Arguments favoring Wealth maximization Increases the share holders interest by increasing the value of holdings

19

Stockholders’ current wealth in a firm = (no. of shares owned) * (current stock price per share)

BUSINESS FINANCE

Ensures security to lenders Productivity and efficiency is increased The management may survive for a longer period The shareholders may not like to change a management if the value of holdings is

increased. The economic interest of the society is served.

Criticisms The idea is not descriptive as to what the firms actually do. It is not necessarily socially desirable There is controversy as to whether the objectives is to maximize the stock holders

wealth of the wealth of the firm which includes other financial claim holders such as debenture holders, preference shareholders etc.

There is difficulty when the management and ownership differs. When managers act as agents of real owners there is possibility for them to increase the managerial interests and not the interest of owners.

OBJECTIVES OF FINANCIAL MANAGEMENTThe objectives of financial management are1. Profit maximization

The main objective of financial management is profit maximization. The finance manager tries to earn maximum profits for the company in the short-term and the long-term. He cannot guarantee profits in the long term because of business uncertainties. However, a company can earn maximum profits even in the long-term, if:-i. The Finance manager takes proper financial decisions.

ii. He uses the finance of the company properly.2. Wealth maximization

Wealth maximization (shareholders' value maximization) is also a main objective of financial management. Wealth maximization means to earn maximum wealth for the shareholders. So, the finance manager tries to give a maximum dividend to the shareholders. He also tries to increase the market value of the shares. The market value of the shares is directly related to the performance of the company. Better the performance, higher is the market value of shares and vice-versa. So, the finance manager must try to maximise shareholder's value.

3. Proper estimation of total financial requirements Proper estimation of total financial requirements is a very important objective of financial management. The finance manager must estimate the total financial requirements of the company. He must find out how much finance is required to start and run the company. He must find out the fixed capital and working capital requirements of the company. His estimation must be correct. If not, there will be shortage or surplus of finance. Estimating the financial requirements is a very difficult job. The finance manager must consider many factors, such as the type of technology used by company, number of employees employed, scale of operations, legal requirements, etc.

4. Proper mobilization

20

BUSINESS FINANCE

Mobilisation (collection) of finance is an important objective of financial management. After estimating the financial requirements, the finance manager must decide about the sources of finance. He can collect finance from many sources such as shares, debentures, bank loans, etc. There must be a proper balance between owned finance and borrowed finance. The company must borrow money at a low rate of interest.

5. Proper utilisation of financeProper utilisation of finance is an important objective of financial management. The finance manager must make optimum utilisation of finance. He must use the finance profitable. He must not waste the finance of the company. He must not invest the company's finance in unprofitable projects. He must not block the company's finance in inventories. He must have a short credit period.

6. Maintaining proper cash flow Maintaining proper cash flow is a short-term objective of financial management. The company must have a proper cash flow to pay the day-to-day expenses such as purchase of raw materials, payment of wages and salaries, rent, electricity bills, etc. If the company has a good cash flow, it can take advantage of many opportunities such as getting cash discounts on purchases, large-scale purchasing, giving credit to customers, etc. A healthy cash flow improves the chances of survival and success of the company.

7. Survival of company Survival is the most important objective of financial management. The company must survive in this competitive business world. The finance manager must be very careful while making financial decisions. One wrong decision can make the company sick, and it will close down.

8. Creating reserves One of the objectives of financial management is to create reserves. The company must not distribute the full profit as a dividend to the shareholders. It must keep a part of it profit as reserves. Reserves can be used for future growth and expansion. It can also be used to face contingencies in the future.

9. Proper coordination Financial management must try to have proper coordination between the finance department and other departments of the company.

10. Create goodwillFinancial management must try to create goodwill for the company. It must improve the image and reputation of the company. Goodwill helps the company to survive in the short-term and succeed in the long-term. It also helps the company during bad times.

11. Increase efficiencyFinancial management also tries to increase the efficiency of all the departments of the company. Proper distribution of finance to all the departments will increase the efficiency of the entire company.

12. Financial disciplineFinancial management also tries to create a financial discipline. Financial discipline means:-

21

BUSINESS FINANCE

i. To invest finance only in productive areas. This will bring high returns (profits) to the company.

ii. To avoid wastage and misuse of finance.13. Reduce cost of capital

Financial management tries to reduce the cost of capital. That is, it tries to borrow money at a low rate of interest. The finance manager must plan the capital structure in such a way that the cost of capital it minimised.

14. Reduce operating risks Financial management also tries to reduce the operating risks. There are many risks and uncertainties in a business. The finance manager must take steps to reduce these risks. He must avoid high-risk projects. He must also take proper insurance.

15. Prepare capital structure Financial management also prepares the capital structure. It decides the ratio between owned finance and borrowed finance. It brings a proper balance between the different sources of capital. This balance is necessary for liquidity, economy, flexibility and stability.

FINANCIAL DECISIONSSome of the important functions which every finance manager has to take are as follows:

1. Investment decision2. Financing decision3. Dividend decision

A. INVESTMENT DECISION (CAPITAL BUDGETING DECISION)This decision relates to careful selection of assets in which funds will be invested by the firms. A firm has many options to invest their funds but firm has to select the most appropriate investment which will bring maximum benefit for the firm and deciding or selecting most appropriate proposal is investment decision.The firm invests its funds in acquiring fixed assets as well as current assets. When decision regarding fixed assets is taken it is also called capital budgeting decision.Factors Affecting Investment/Capital Budgeting Decisions1. Cash Flow of the ProjectWhenever a company is investing huge funds in an investment proposal it expects some regular amount of cash flow to meet day to day requirement. The amount of cash flow an investment proposal will be able to generate must be assessed properly before investing in the proposal.2. Return on InvestmentThe most important criteria to decide the investment proposal is rate of return it will be able to bring back for the company in the form of income for, e.g., if project A is bringing 10% return and project В is bringing 15% return then we should prefer project B.3. Risk InvolvedWith every investment proposal, there is some degree of risk is also involved. The company must try to calculate the risk involved in every proposal and should prefer the investment proposal with moderate degree of risk only.

22

BUSINESS FINANCE

4. Investment CriteriaAlong with return, risk, cash flow there are various other criteria which help in selecting an investment proposal such as availability of labour, technologies, input, machinery, etc.The finance manager must compare all the available alternatives very carefully and then only decide where to invest the most scarce resources of the firm, i.e., finance.Investment decisions are considered very important decisions because of following reasons:

1. They are long term decisions and therefore are irreversible; means once taken cannot be changed.

2. Involve huge amount of funds.3. Affect the future earning capacity of the company.

IMPORTANCE OR SCOPE OF CAPITAL BUDGETING DECISIONCapital budgeting decisions can turn the fortune of a company. The capital budgeting decisions are considered very important because of the following reasons:1. Long Term GrowthThe capital budgeting decisions affect the long term growth of the company. As funds invested in long term assets bring return in future and future prospects and growth of the company depends upon these decisions only.2. Large Amount of Funds InvolvedInvestment in long term projects or buying of fixed assets involves huge amount of funds and if wrong proposal is selected it may result in wastage of huge amount of funds that is why capital budgeting decisions are taken after considering various factors and planning.3. Risk InvolvedThe fixed capital decisions involve huge funds and also big risk because the return comes in long run and company has to bear the risk for a long period of time till the returns start coming.4. Irreversible DecisionCapital budgeting decisions cannot be reversed or changed overnight. As these decisions involve huge funds and heavy cost and going back or reversing the decision may result in heavy loss and wastage of funds. So these decisions must be taken after careful planning and evaluation of all the effects of that decision because adverse consequences may be very heavy.B. FINANCING DECISION The second important decision which finance manager has to take is deciding source of finance. A company can raise finance from various sources such as by issue of shares, debentures or by taking loan and advances. Deciding how much to raise from which source is concern of financing decision. Mainly sources of finance can be divided into two categories:

1. Owners fund2. Borrowed fund

Share capital and retained earnings constitute owners’ fund and debentures, loans, bonds, etc. constitute borrowed fund.The main concern of finance manager is to decide how much to raise from owners’ fund and how much to raise from borrowed fund.

23

BUSINESS FINANCE

While taking this decision the finance manager compares the advantages and disadvantages of different sources of finance. The borrowed funds have to be paid back and involve some degree of risk whereas in owners’ fund there is no fix commitment of repayment and there is no risk involved. But finance manager prefers a mix of both types. Under financing decision finance manager fixes a ratio of owner fund and borrowed fund in the capital structure of the company.

Factors Affecting Financing DecisionsWhile taking financing decisions the finance manager keeps in mind the following factors:1. CostThe cost of raising finance from various sources is different and finance managers always prefer the source with minimum cost.2. RiskMore risk is associated with borrowed fund as compared to owner’s fund securities. Finance manager compares the risk with the cost involved and prefers securities with moderate risk factor.3. Cash Flow PositionThe cash flow position of the company also helps in selecting the securities. With smooth and steady cash flow companies can easily afford borrowed fund securities but when companies have shortage of cash flow, then they must go for owner’s fund securities only.4. Control ConsiderationsIf existing shareholders want to retain the complete control of business then they prefer borrowed fund securities to raise further fund. On the other hand if they do not mind to lose the control then they may go for owner’s fund securities.5. Floatation CostIt refers to cost involved in issue of securities such as broker’s commission, underwriters fees, expenses on prospectus, etc. Firm prefers securities which involve least floatation cost.6. Fixed Operating CostIf a company is having high fixed operating cost then they must prefer owner’s fund because due to high fixed operational cost, the company may not be able to pay interest on debt securities which can cause serious troubles for company.7. State of Capital MarketThe conditions in capital market also help in deciding the type of securities to be raised. During boom period it is easy to sell equity shares as people are ready to take risk whereas during depression period there is more demand for debt securities in capital market.

C. DIVIDEND DECISIONThis decision is concerned with distribution of surplus funds. The profit of the firm is distributed among various parties such as creditors, employees, debenture holders, shareholders, etc.

24

BUSINESS FINANCE

Payment of interest to creditors, debenture holders, etc. is a fixed liability of the company, so what company or finance manager has to decide is what to do with the residual or left over profit of the company.

The surplus profit is either distributed to equity shareholders in the form of dividend or kept aside in the form of retained earnings. Under dividend decision the finance manager decides how much to be distributed in the form of dividend and how much to keep aside as retained earnings.To take this decision finance manager keeps in mind the growth plans and investment opportunities.

If more investment opportunities are available and company has growth plans then more is kept aside as retained earnings and less is given in the form of dividend, but if company wants to satisfy its shareholders and has less growth plans, then more is given in the form of dividend and less is kept aside as retained earnings.This decision is also called residual decision because it is concerned with distribution of residual or left over income. Generally new and upcoming companies keep aside more of retain earning and distribute less dividend whereas established companies prefer to give more dividend and keep aside less profit.

Factors Affecting Dividend DecisionThe finance manager analyses following factors before dividing the net earnings between dividend and retained earnings:1. EarningDividends are paid out of current and previous year’s earnings. If there are more earnings then company declares high rate of dividend whereas during low earning period the rate of dividend is also low.2. Stability of EarningsCompanies having stable or smooth earnings prefer to give high rate of dividend whereas companies with unstable earnings prefer to give low rate of earnings.3. Cash Flow PositionPaying dividend means outflow of cash. Companies declare high rate of dividend only when they have surplus cash. In situation of shortage of cash companies declare no or very low dividend.4. Growth OpportunitiesIf a company has a number of investment plans then it should reinvest the earnings of the company. As to invest in investment projects, company has two options: one to raise additional capital or invest its retained earnings. The retained earnings are cheaper source as they do not involve floatation cost and any legal formalities.If companies have no investment or growth plans then it would be better to distribute more in the form of dividend. Generally mature companies declare more dividends whereas growing companies keep aside more retained earnings.5. Stability of DividendSome companies follow a stable dividend policy as it has better impact on shareholder and improves the reputation of company in the share market. The stable dividend policy

25

BUSINESS FINANCE

satisfies the investor. Even big companies and financial institutions prefer to invest in a company with regular and stable dividend policy.There are three types of stable dividend policies which a company may followConstant dividend per shareIn this case, the company decides a fixed rate of dividend and declares the same rate every year, e.g., 10% dividend on investment.Constant payout ratioUnder this system the company fixes up a fixed percentage of dividends on profit and not on investment, e.g., 10% on profit so dividend keeps on changing with change in profit rate.Constant dividend per share and extra dividendUnder this scheme a fixed rate of dividend on investment is given and if profit or earnings increase then some extra dividend in the form of bonus or interim dividend is also given.6. Preference of ShareholdersAnother important factor affecting dividend policy is expectation and preference of shareholders as their expectations cannot be ignored by the company. Generally it is observed that retired shareholders expect regular and stable amount of dividend whereas young shareholders prefer capital gain by reinvesting the income of the company.They are ready to sacrifice present day income of dividend for future gain which they will get with growth and expansion of the company.Secondly poor and middle class investors also prefer regular and stable amount of dividend whereas wealthy and rich class prefers capital gains.So if a company is having large number of retired and middle class shareholders then it will declare more dividend and keep aside less in the form of retained earnings whereas if company is having large number of young and wealthy shareholders then it will prefer to keep aside more in the form of retained earnings and declare low rate of dividend.7. Taxation PolicyThe rate of dividend also depends upon the taxation policy of government. Under present taxation system dividend income is tax free income for shareholders whereas company has to pay tax on dividend given to shareholders. If tax rate is higher, then company prefers to pay less in the form of dividend whereas if tax rate is low then company may declare higher dividend.8. Access to Capital Market ConsiderationWhenever company requires more capital it can either arrange it by issue of shares or debentures in the stock market or by using its retained earnings. Rising of funds from the capital market depends upon the reputation of the company.If capital market can easily be accessed or approached and there is enough demand for securities of the company then company can give more dividend and raise capital by approaching capital market, but if it is difficult for company to approach and access capital market then companies declare low rate of dividend and use reserves or retained earnings for reinvestment.9. Legal RestrictionsCompanies’ Act has given certain provisions regarding the payment of dividends that can be paid only out of current year profit or past year profit after providing depreciation fund. In case company is not earning profit then it cannot declare dividend.

26

BUSINESS FINANCE

Apart from the Companies’ Act there are certain internal provisions of the company that is whether the company has enough flow of cash to pay dividend. The payment of dividend should not affect the liquidity of the company.10. Contractual ConstraintsWhen companies take long term loan then financier may put some restrictions or constraints on distribution of dividend and companies have to abide by these constraints.11. Stock Market ReactionThe declaration of dividend has impact on stock market as increase in dividend is taken as a good news in the stock market and prices of security rise. Whereas a decrease in dividend may have negative impact on the share price in the stock market. So possible impact of dividend policy in the equity share price also affects dividend decision.

Inter-relationship between Investment, Financing and DividendThree major functions of finance department are Financing DecisionThis function is mainly concerned with determination of optimum capital structure of the company keeping in mind cost, control and risk. It is also known as Procurement of Fund.Investment DecisionIt is also known as Effective Utilization of Fund. In this respect finance department has to identify the investment opportunities and to choice the best one , after a proper evaluation.Dividend DecisionThe finance manager is also concerned with the decisions to pay or declare dividend. He assists the top management to decide the portion of profit to be declared as dividend.

So far the objective is concerned; the above stated three functions are same i.e. maximizing shareholders wealth. As their objectives are same the decisions are interrelated. A company having profitable investment opportunities, generally prefer lower dividend payout ratio. On the other hand having a good investment means profit of the company would be more and more dividend can be paid to shareholders. Similarly, finance function and investment functions are also highly correlated. Cost of capital plays a major role whether to accept or not an investment opportunity. Financing decisions also dependent on amount of to be retained in the profit. So, we can conclude that investment, financing and dividend decisions are interrelated and are to be taken jointly keeping in view their joint effect on the shareholders wealth.Investment decisions/ Long-term asset-mix Involve Capital expenditure Referred as Capital budgeting Allocation of funds to long term assets which yield returns in future Evaluation of new projects Measurement of cut off rate against new investments Evaluation on the basis of return and risk Involves replacement decisions

Financing Decision / Capital Mix From where and how to acquire funds

27

BUSINESS FINANCE

Determination of appropriate proposition of equity and debt Debt equity mix is called Capital Structure Change in shareholder’s returns by a change in Capital structure is called Financial

Leverage Best combination of debt-equity that would increase returns with the given risk should

be found out Legal aspects, loan facilities, controls etc should also be considered while deciding

capital structure.

Factors influencing financial decisionsExternal Factors State of economy Structure of capital and money markets Requirements of investors Government policy Taxation policy Lending policy of financial institutions.Internal Factors Nature and size of business Expected return Composition of assets Structure of ownership Trend of earnings Age of the firm Liquidity position Working capital requirements Conditions of debt agreements

RELATIONSHIP BETWEEN RISK AND RETURN

Risk: Risk is defined as the chance of future loss that can be foreseen. Return: The return represents the benefits derived by a business from its

operations.

Measurement of Return: On the basis of Profit On the basis of Income On the basis of Earnings Before Interest and Tax (EBIT) On the basis of Earnings Before Tax (EBT) On the basis of Earnings After Tax (EAT) On the basis of Cash flows generated in the business operations On the basis of different accounting Ratios

28

BUSINESS FINANCE

FUNCTIONS OF A FINANCE MANAGERAs a company grows, the responsibilities of the finance manager expand, with more outsourced functions coming in-house and more long-term strategic planning added to the finance manager's plate. Understanding the roles and responsibilities of a corporate finance manager will help you decide if this career is right for you and how to prepare to land these types of finance jobs.PlanningUnlike a bookkeeper or accountant, a financial manager, often known as a chief financial officer, plans long-term financial strategy for a company, delegating bookkeeping work to lower-level staff. The financial planning aspect of the job includes setting goals for achieving specific revenues, profit margins and gross profits. It also requires setting targets for overhead and production expense levels and debt-service management. The financial manager needs to create a master budget that’s tied to the company’s balance sheet, accounts receivable and payable reports and cash flow and profit-and-loss statements. The financial manager conducts regular reviews of the master budget, called budget variance analyses, to determine if any changes should be made based on the actual performance of the company vs. its financial projections. Financial managers also determine the best investment options for a business’s excess cash and review ways to acquire capital for expansion or acquisitions.Cost ContainmentA key responsibility of a financial manager is to control the company’s expenses. This requires more than simply setting spending levels and cutting costs. Cost containment includes creating requests for proposals, bidding processes and purchasing policies for contractors, vendors and suppliers to ensure the company gets the best combination of quality and price. The financial manager sets benchmarks that determine when it’s most cost-effective to perform activities using in-house staff and when it’s better to use contractors. Cost-containment efforts include managing debt to ensure interest payments don’t wipe out company profits. Financial managers also create strategies that help reduce a company’s tax liability, such as depreciating assets.Cash Flow ManagementOne of the most important functions of a financial manager is to project and manage the company’s cash flow. Cash flow refers to the actual receipt of money and payment of bills, as opposed to the company’s budgeted income and expenses. Assuming that because a business has more income than expenses it can pay its bills can lead to disaster. For example, if the company does not negotiate customer credit terms and vendor and supplier payment terms correctly, the business might be waiting to collect sales invoices long after bills have come due. Cash flow management includes monitoring receivables turnover and keeping enough credit and cash reserves available to keep the company financially stable.Legal ComplianceThe corporate financial manager ensures the business meets all of its legal obligations, such as sales and income tax payments; employee benefits contributions; state and federal labor wage requirements; and Securities and Exchange Commission reporting, if the company is a public corporation. At small and medium-sized businesses, the financial manager often works with tax experts and CPAs who guide the company regarding its legal obligations.

29

BUSINESS FINANCE

THE FINANCIAL MANAGER The financial manager is responsible for budgeting, projecting cash flows, and determining how to invest and finance projects.Key Points

The finance manager is responsible for knowing how much the product is expected to cost and how much revenue it is expected to earn so that s/he can invest the appropriate amount in the product.

The finance manager uses a number of tools, such as setting the cost of capital (the cost of money over time, which will be explored in further depth later on) to determine the cost of financing.

The financial manager must not just be an expert at financial projections; s/he also must have a grasp of the accounting systems in place and the strategy of the business over the coming years.

The head of the financial department is the chief financial officer (CFO) who is responsible for all financial decisions and reporting done in the company.

The Role of the Financial Manager The role of a financial manager is a complex one, requiring both an understanding of how the business functions as a whole and specialized financial knowledge. The head of the financial operations is called the chief financial officer (CFO). The structure of the company varies, but a financial manager is responsible for the same general things across the board. The manager is responsible for managing the budget. This involves allocating money to different projects and segments so that the business can continue operating, but the best projects get the necessary funding.

The manager is responsible for figuring out the financial projections for the business. The development of a new product, for example, requires an investment of capital over time. The finance manager is responsible for knowing how much the product is expected to cost and how much revenue it is expected to earn so that s/he can invest the appropriate amount in the product. This is a lot tougher than it sounds because there is no accurate financial data for the future. The finance manager will use data analyses and educated guesses to approximate the value, but it's extremely rare that s/he can be 100% sure of the future cash flows.