Embed Size (px)

Citation preview

Business Breakfast

Budget ImpactJune 2010

Finance Bill June 2010 Implications

Ian Cattell ACA

Partner – Crombies Chartered Accountants

©2010 Crombies Accountants Limited. All rights reserved.

CONTENTSThe Budgetary Environment

UK Plc – 2009-10 Financial Report

The office for Budgetary Responsibility

Business Tax Proposals

VAT

Corporation Tax

Capital Allowances

Personal Tax Proposals

Income Tax

Capital Gains Tax

The Tax Compliance Environment

Any questions?

©2010 Crombies Accountants Limited. All rights reserved.

General disclaimers

• We are not authorised to give investment advice

• We make general comments only – not specific advice

• Everyone’s financial affairs are different – what is best for the “man in the pub” may not be best for you

• Tax legislation changes constantly so review your circumstances regularly

• And Remember – Don’t let the tax implications distort the commercial and practical considerations

• The Finance Bill is not yet law. The final provisions enacted in any Finance Act may differ considerably from The Chancellors initial presentations.

©2010 Crombies Accountants Limited. All rights reserved.

The Budgetary Environment

The Micawber Principle"Annual income twenty pounds, annual expenditure nineteen pounds nineteen and six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery

©2010 Crombies Accountants Limited. All rights reserved.

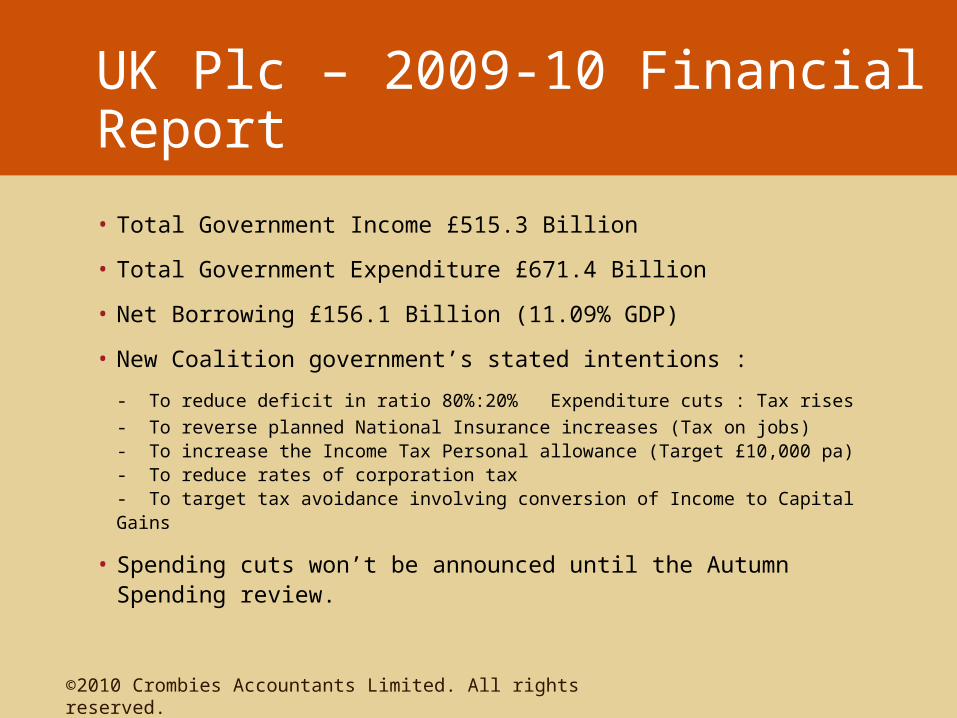

UK Plc – 2009-10 Financial Report

• Total Government Income £515.3 Billion

• Total Government Expenditure £671.4 Billion

• Net Borrowing £156.1 Billion (11.09% GDP)

• New Coalition government’s stated intentions :

- To reduce deficit in ratio 80%:20% Expenditure cuts : Tax rises

- To reverse planned National Insurance increases (Tax on jobs)- To increase the Income Tax Personal allowance (Target £10,000 pa)- To reduce rates of corporation tax- To target tax avoidance involving conversion of Income to Capital Gains

• Spending cuts won’t be announced until the Autumn Spending review.

©2010 Crombies Accountants Limited. All rights reserved.

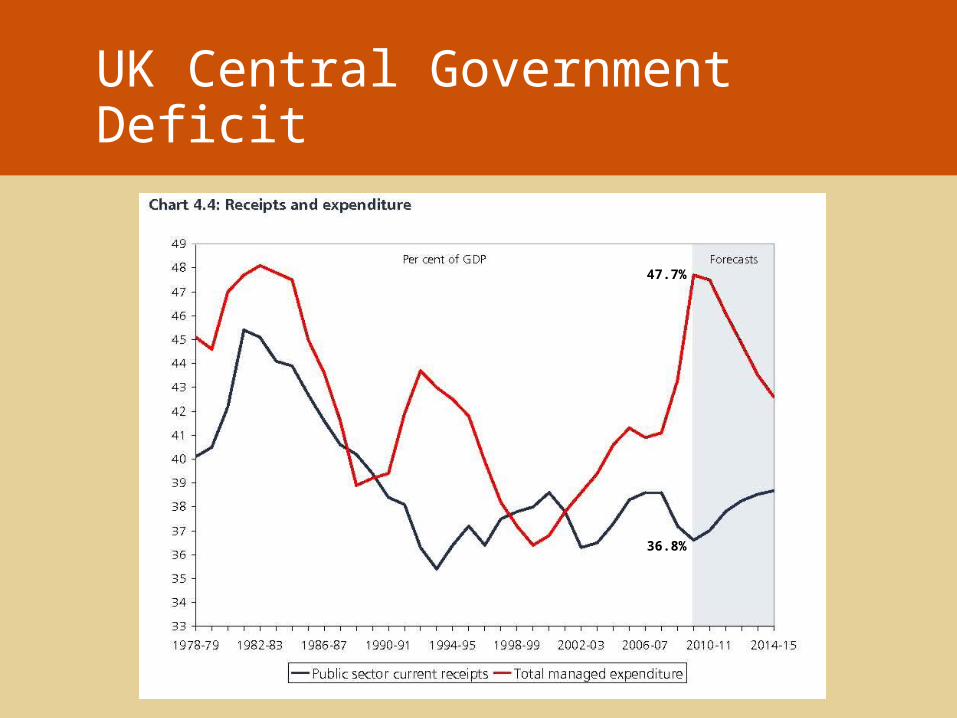

UK Central Government Deficit

36.8%

47.7%

How the deficit is expected to fall

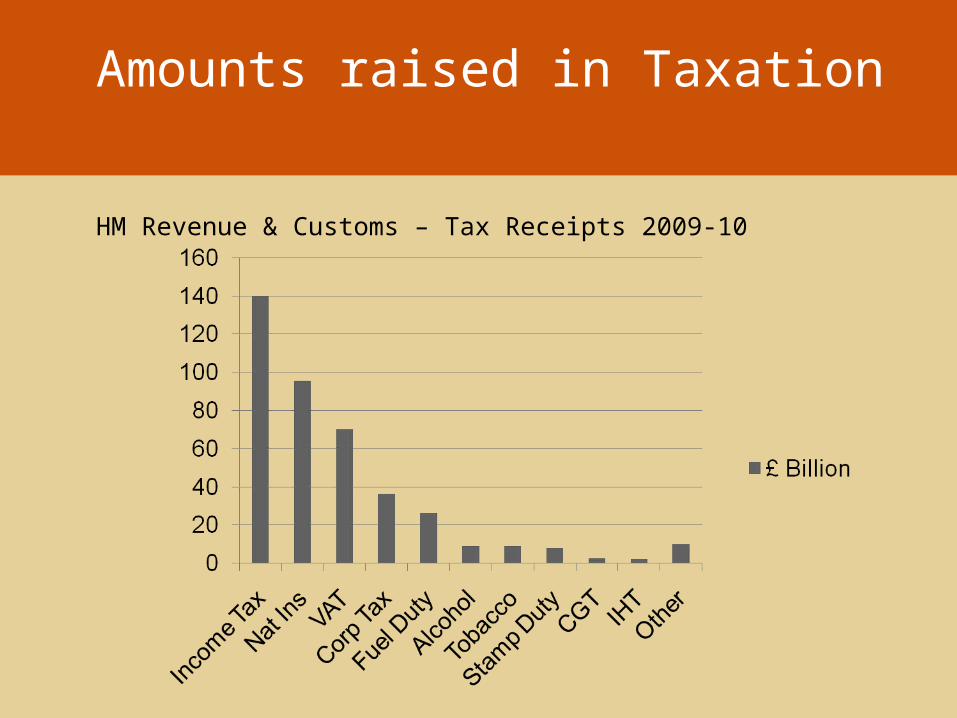

Amounts raised in Taxation

HM Revenue & Customs – Tax Receipts 2009-10

Budget June 2010Business Tax Proposals

Jean-Baptiste ColbertThe art of taxation consists in so plucking the goose as to obtain the largest amount of feathers with the least amount of hissing.

©2010 Crombies Accountants Limited. All rights reserved.

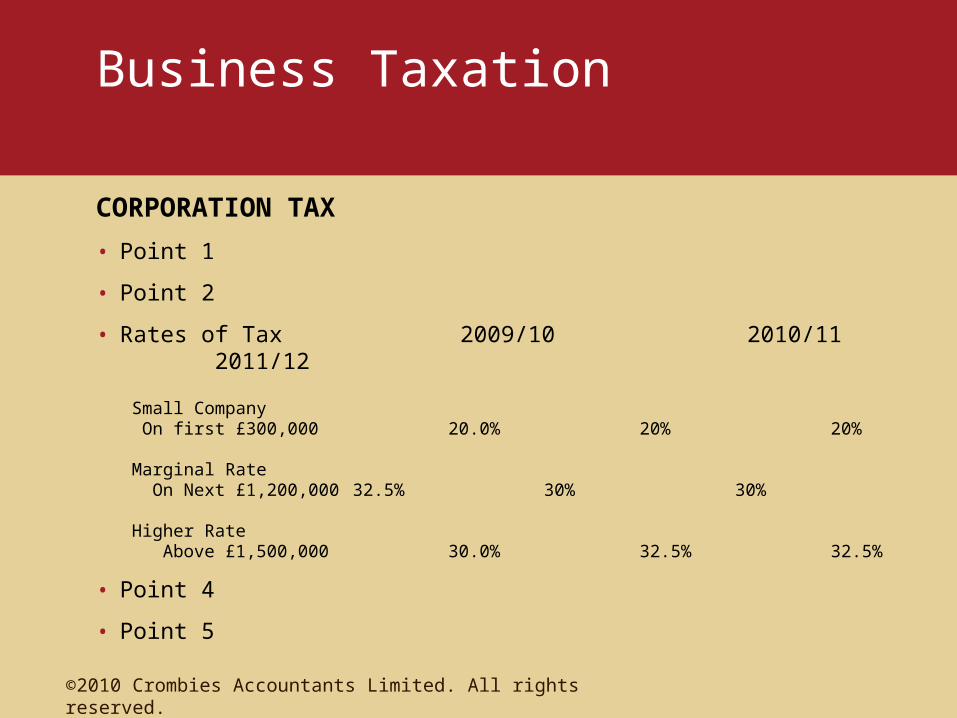

Business Taxation

CORPORATION TAX

• Point 1

• Point 2

• Rates of Tax 2009/10 2010/11 2011/12

Small Company On first £300,000 20.0% 20% 20%

Marginal Rate On Next £1,200,000 32.5% 30% 30%

Higher Rate Above £1,500,000 30.0% 32.5% 32.5%

• Point 4

• Point 5

©2010 Crombies Accountants Limited. All rights reserved.

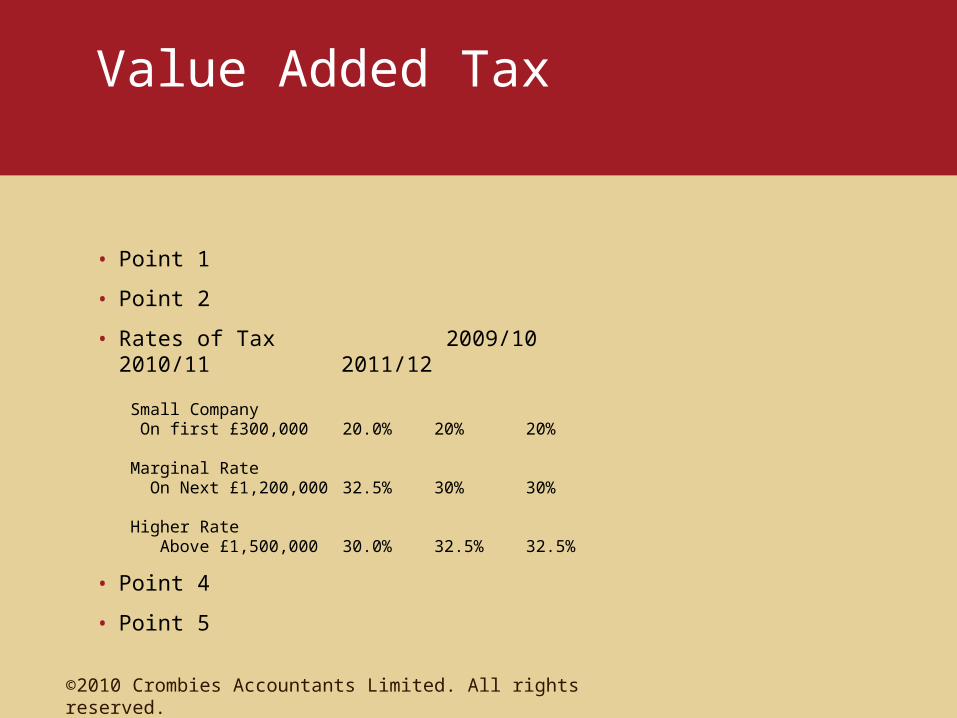

Value Added Tax

• Point 1

• Point 2

• Rates of Tax 2009/10 2010/11 2011/12

Small Company On first £300,000 20.0% 20%

20%

Marginal Rate On Next £1,200,000 32.5% 30% 30%

Higher Rate Above £1,500,000 30.0% 32.5%

32.5%

• Point 4

• Point 5

©2010 Crombies Accountants Limited. All rights reserved.

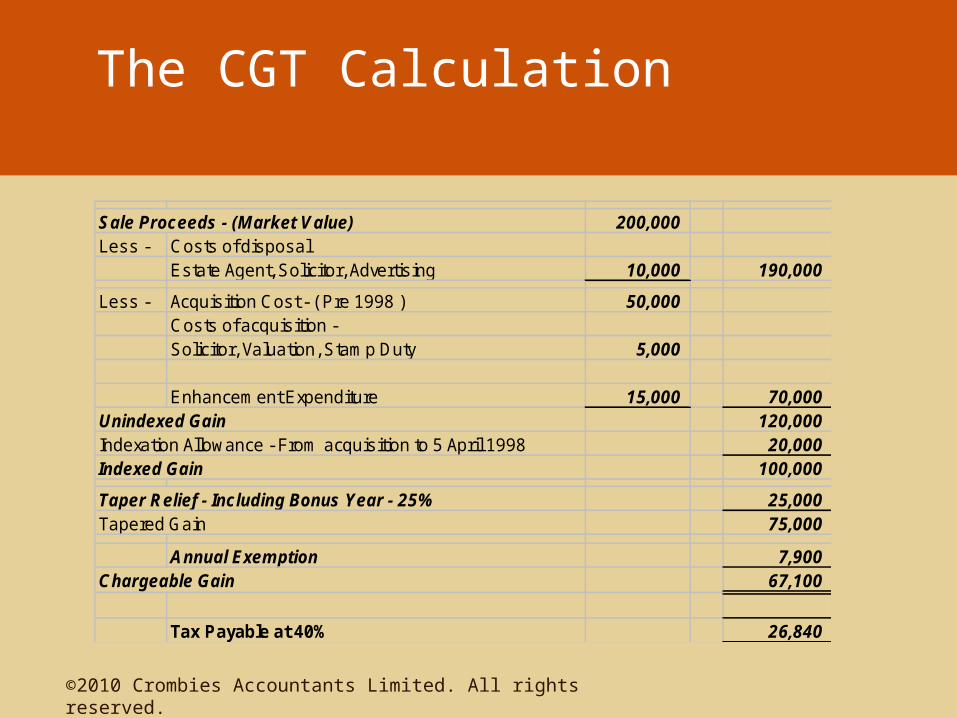

The CGT Calculation

Sale Proceeds - (Market Value) 200,000 Less - Costs of disposal

Estate Agent, Solicitor, Advertis ing 10,000 190,000

Less - Acquisition Cost - ( Pre 1998 ) 50,000 Costs of acquisition - Solicitor, Valuation, Stamp Duty 5,000

Enhancement Expenditure 15,000 70,000 Unindexed Gain 120,000 Indexation Allowance - From acquisition to 5 April 1998 20,000 Indexed Gain 100,000

Taper Relief - Including Bonus Year - 25% 25,000 Tapered Gain 75,000

Annual Exemption 7,900 Chargeable Gain 67,100

Tax Payable at 40% 26,840

©2010 Crombies Accountants Limited. All rights reserved.

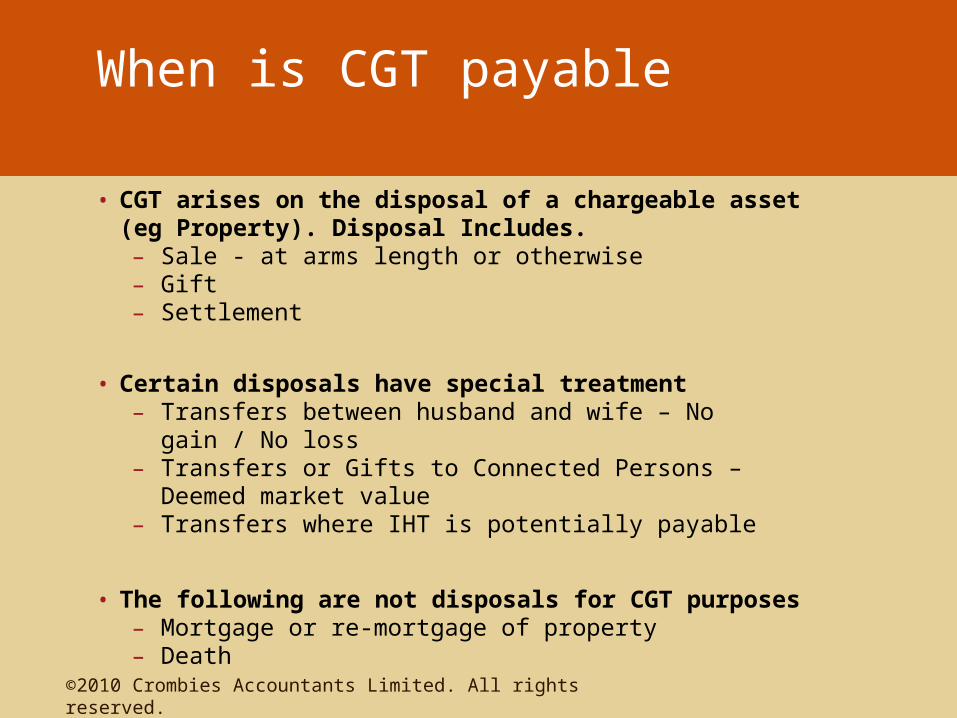

When is CGT payable

• CGT arises on the disposal of a chargeable asset (eg Property). Disposal Includes.– Sale - at arms length or otherwise – Gift– Settlement

• Certain disposals have special treatment – Transfers between husband and wife – No gain / No loss– Transfers or Gifts to Connected Persons – Deemed market

value– Transfers where IHT is potentially payable

• The following are not disposals for CGT purposes– Mortgage or re-mortgage of property– Death

©2010 Crombies Accountants Limited. All rights reserved.

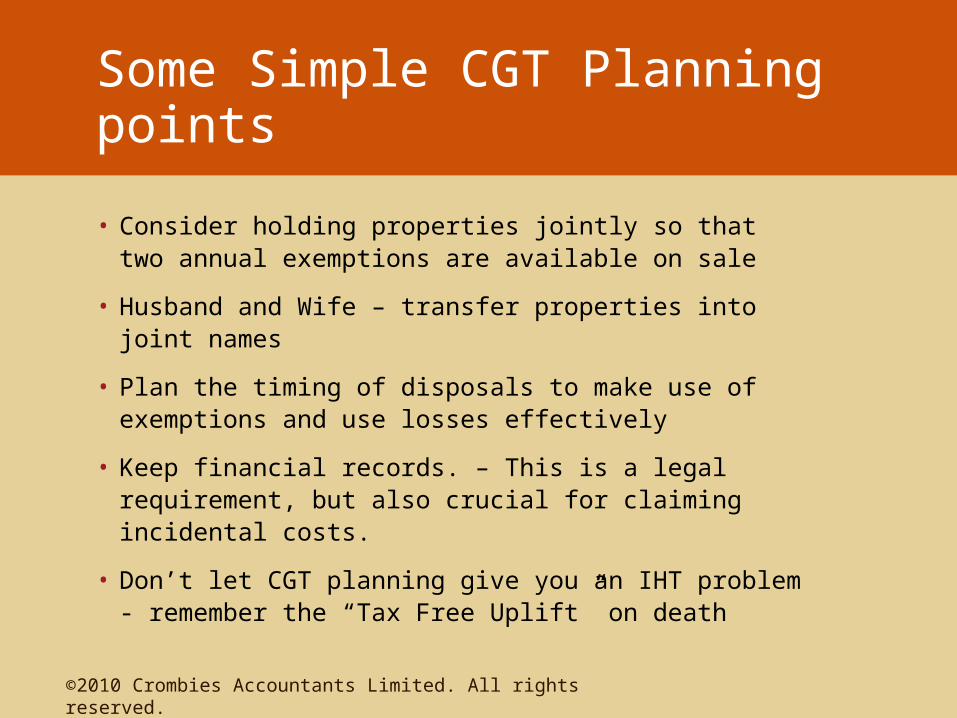

Some Simple CGT Planning points

• Consider holding properties jointly so that two annual exemptions are available on sale

• Husband and Wife – transfer properties into joint names

• Plan the timing of disposals to make use of exemptions and use losses effectively

• Keep financial records. – This is a legal requirement, but also crucial for claiming incidental costs.

• Don’t let CGT planning give you an IHT problem - remember the “Tax Free Uplift” on death

©2010 Crombies Accountants Limited. All rights reserved.

Budget June 2010Personal Tax Proposals

Albert EinsteinThe hardest thing in the world to understand is the income tax.

©2010 Crombies Accountants Limited. All rights reserved.

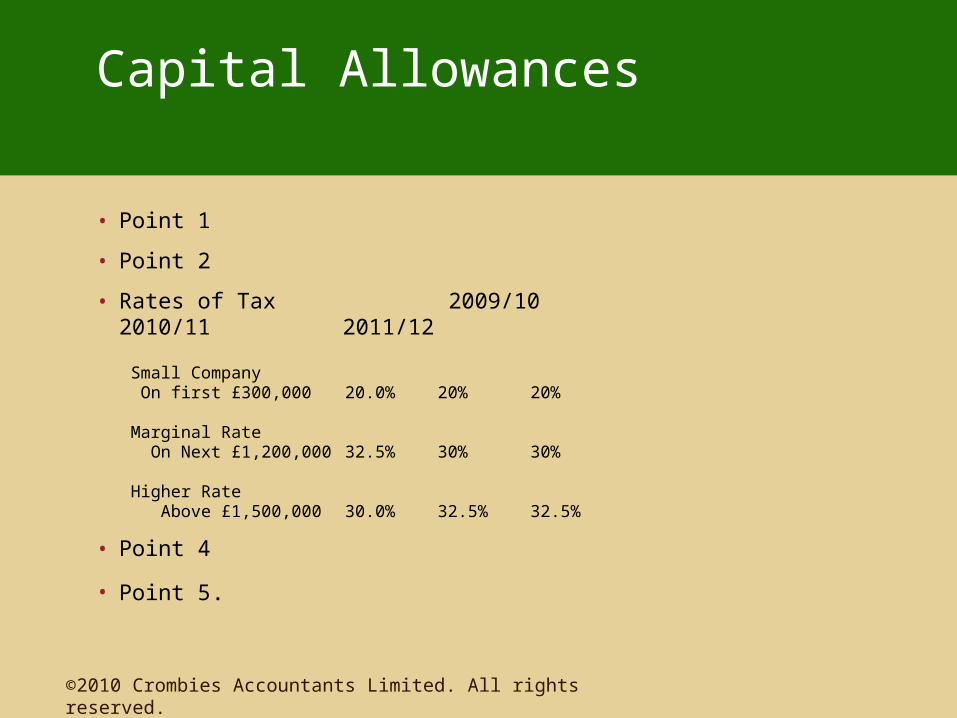

Capital Allowances

• Point 1

• Point 2

• Rates of Tax 2009/10 2010/11 2011/12

Small Company On first £300,000 20.0% 20%

20%

Marginal Rate On Next £1,200,000 32.5% 30% 30%

Higher Rate Above £1,500,000 30.0% 32.5%

32.5%

• Point 4

• Point 5.

©2010 Crombies Accountants Limited. All rights reserved.

The Tax Compliance Environment

Mark TwainThe only difference between a tax man and a taxidermist is that the taxidermist leaves the skin.

©2010 Crombies Accountants Limited. All rights reserved.

HMRC Compliance Environment

• HMRC are targeting in their Published Business Plan an increase of 33% in amounts raised from Inspections & Investigations.

• In 2010/11 this would amount to £4bn. Of which £1.5bn assumed from small business and personal tax enquiries.

• New Penalty Regime. From April 2010 assumption is that enquiry amendments will carry a penalty of at least 20%. (Previously Nil)

• Increased use of informal enquiry powers outside of the usual “Enquiry windows”

• Increased use of “Multi-disciplinary” teams. Cross referencing between what were previously separate departments.

• Utilization of new information sources – Bank data; Land Registry; Benefits Agency; Property Letting Agents; Stock Brokers; Solicitors.

• PAYE, CIS, VAT, Stamp Duty Penalties all increased substantially.

©2010 Crombies Accountants Limited. All rights reserved.

Any Questions ?

Concerns about TAX?

We have the FA TS...

...RELAX

![LouAnn Rivett PhD Aimee Stewart PhD Joanne Potterton PhD · Personality Questionnaire (HSPQ) and 16PF give a valid and reliable picture of personality [Cattell and Cattell, 1975]](https://img.pdfslide.us/doc/110x75/5eab9f642f9fa75cc410e1e3/louann-rivett-phd-aimee-stewart-phd-joanne-potterton-personality-questionnaire-hspq.jpg)