Embed Size (px)

Citation preview

UTAH

Homeowner

Product Guide

Enumclaw Property and Casualty Insurance Company

1215

What’s New Effective Date

Updates

How To Reach Us Phone / FAX / Email

Home Office

Agency Services

Claims

Customer Service (Billing)

Marketing Materials

Policy Services

Supplies

Underwriting

Website

Product Descriptions Link to HO-3/HO-5 Homeowner Comparison

Policy Features

Basic Coverage Limits

Description of Coverage

Program Guidelines Eligibility

Photo Requirements

General Rules Cancellation or Reductions in Limits of Liability or Coverages

Construction Definitions

Mandatory Coverages

Manual Premium Revision

Minimum Premium

Multiple Company Insurance

Other Insurance

Policy Changes

Policy Period

Premium Adjustments

Premium Rounding Rule

Property Renewal Increases

Protection Information

Renewal Plan

Seasonal Dwelling Definition

Secondary Residences

Single Building Definition

Transfer or Assignment

Forms and Endorsements Descriptions Coverages Deductibles

Coverage E – Personal Liability

Coverage F – Medical Payments

Fire Department Service Charge

Loss of Use

New Home Discount

Other Exposures

Other Insured Location Occupied by Insured

Personal Property Reduction in Limit

Residence Employees

Secondary Residence Premises

Discounts Burglary Protection Discount

Claims Free Discount

Fire Protection Discount

Loyalty Discount

Newer Home Discount

Multi-Home Discount

Package Policy Discount

Additional Rating Elements HO-3, MH-3 and HO-5 Age of Insured

Heating Type

Individual Premium Modifier

Number of Additional Interests

Number of Families

Number of Lapses

Number of Stories

Personal Status

Roof Age

Roof Type

Swimming Pool

Total Living Area

Woodstove

Forms and Endorsements List

Utah – Home Program What’s New

Enumclaw Property and Casualty Insurance Company 2

Effective Date December 10, 2015

Updates Rule changes and editorial corrections Prior Updates

Replaced Schedule Personal Property endorsement HO-61 with HO M061 in order to add Replacement Cost loss settlement option.

Added Equipment Breakdown Enhancement endorsement HO M180.

Added Schedule Bicycle endorsement HO M602

Added Service Line Enhancement endorsement HO M108.

Changed specific company references (e.g., Mutual of Enumclaw Insurance Company or Enumclaw Property and Casualty Insurance Company) to generic references (e.g., “we,” “us”).

Adding notation to liability forms that they are not available on secondary or seasonal occupancy policies.

Utah – Home Program How To Reach Us

Enumclaw Property and Casualty Insurance Company 3

General Contacts Home Office ......................................................................................... (800) 366-5551 Agency Services (Help Desk) ......................................................................... Ext. 3520

[email protected] Claims ............................................................................................................ Ext. 3256

To file a Claim --- Claim Response Center ...................................... 877-425-2580 Or online at MutualofEnumclaw.com

Customer Service ........................................................................................... Ext. 3248 Billing Questions ............................................. Ext. 3248 or direct (800) 456-7750 To make Payments ........................................ .Ext. 3654 or direct (888) 475-2823 Payment Address .................................. 1460 Wells Street Enumclaw, WA 98022 [email protected]

Marketing Materials ........................................................................................ Ext. 3179 [email protected]

Personal Lines Underwriting (click for list of staff) FAX Number ................................................................................. (866) 546-0223

Policy Services (click for list of staff) FAX Number ................................................................................. (866) 546-0224

Supplies.......................................................................................................... Ext. 3314 [email protected]

Website MutualofEnumclaw.com

Utah – Home Program Product Descriptions

Enumclaw Property and Casualty Insurance Company 4

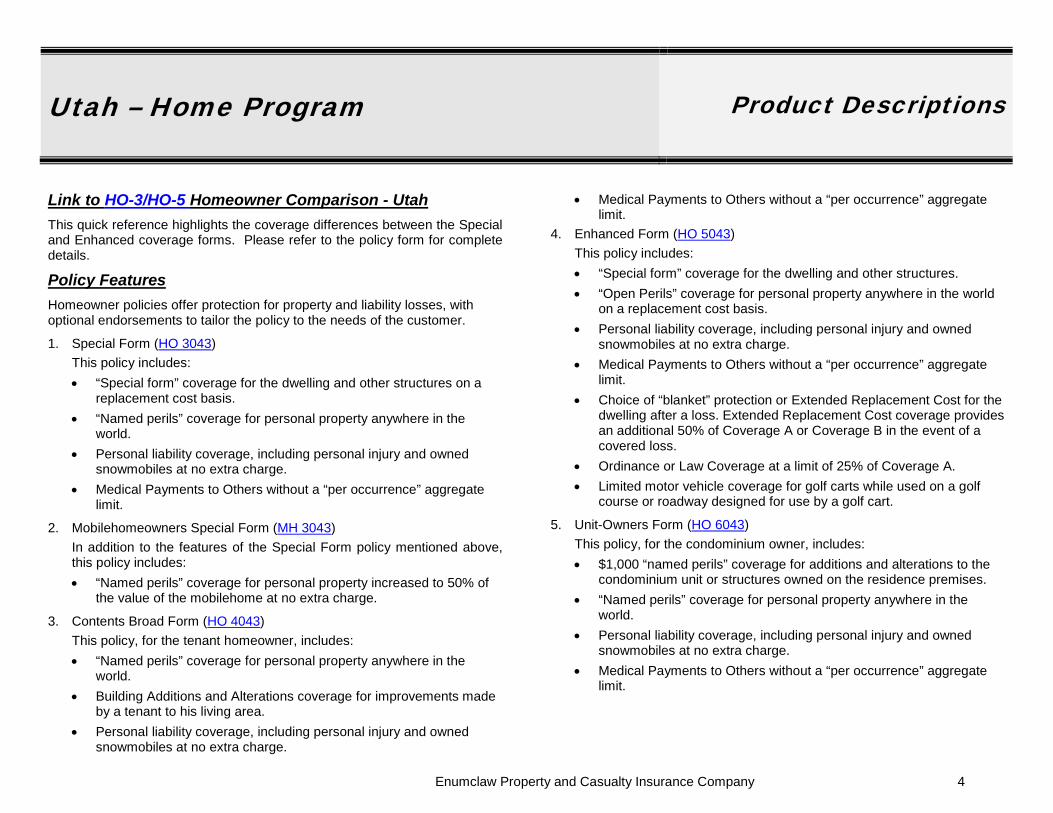

Link to HO-3/HO-5 Homeowner Comparison - Utah This quick reference highlights the coverage differences between the Special and Enhanced coverage forms. Please refer to the policy form for complete details.

Policy Features Homeowner policies offer protection for property and liability losses, with optional endorsements to tailor the policy to the needs of the customer.

1. Special Form (HO 3043) This policy includes: • “Special form” coverage for the dwelling and other structures on a

replacement cost basis. • “Named perils” coverage for personal property anywhere in the

world. • Personal liability coverage, including personal injury and owned

snowmobiles at no extra charge. • Medical Payments to Others without a “per occurrence” aggregate

limit.

2. Mobilehomeowners Special Form (MH 3043) In addition to the features of the Special Form policy mentioned above, this policy includes: • “Named perils” coverage for personal property increased to 50% of

the value of the mobilehome at no extra charge.

3. Contents Broad Form (HO 4043) This policy, for the tenant homeowner, includes: • “Named perils” coverage for personal property anywhere in the

world. • Building Additions and Alterations coverage for improvements made

by a tenant to his living area. • Personal liability coverage, including personal injury and owned

snowmobiles at no extra charge.

• Medical Payments to Others without a “per occurrence” aggregate limit.

4. Enhanced Form (HO 5043) This policy includes: • “Special form” coverage for the dwelling and other structures. • “Open Perils” coverage for personal property anywhere in the world

on a replacement cost basis. • Personal liability coverage, including personal injury and owned

snowmobiles at no extra charge. • Medical Payments to Others without a “per occurrence” aggregate

limit. • Choice of “blanket” protection or Extended Replacement Cost for the

dwelling after a loss. Extended Replacement Cost coverage provides an additional 50% of Coverage A or Coverage B in the event of a covered loss.

• Ordinance or Law Coverage at a limit of 25% of Coverage A. • Limited motor vehicle coverage for golf carts while used on a golf

course or roadway designed for use by a golf cart.

5. Unit-Owners Form (HO 6043) This policy, for the condominium owner, includes: • $1,000 “named perils” coverage for additions and alterations to the

condominium unit or structures owned on the residence premises. • “Named perils” coverage for personal property anywhere in the

world. • Personal liability coverage, including personal injury and owned

snowmobiles at no extra charge. • Medical Payments to Others without a “per occurrence” aggregate

limit.

Utah – Home Program Product Descriptions

Enumclaw Property and Casualty Insurance Company 5

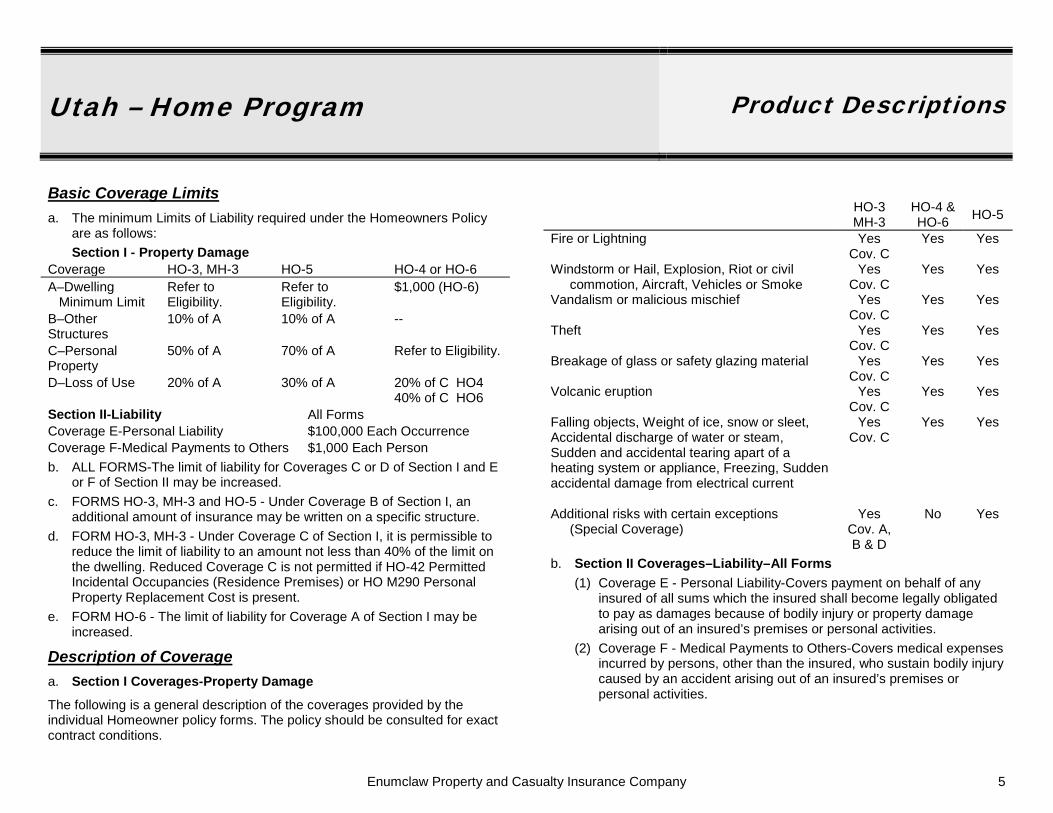

Basic Coverage Limits a. The minimum Limits of Liability required under the Homeowners Policy

are as follows: Section I - Property Damage

Coverage HO-3, MH-3 HO-5 HO-4 or HO-6 A–Dwelling Minimum Limit

Refer to Eligibility.

Refer to Eligibility.

$1,000 (HO-6)

B–Other Structures

10% of A 10% of A --

C–Personal Property

50% of A 70% of A Refer to Eligibility.

D–Loss of Use 20% of A 30% of A 20% of C HO4 40% of C HO6

Section II-Liability All Forms Coverage E-Personal Liability $100,000 Each Occurrence Coverage F-Medical Payments to Others $1,000 Each Person b. ALL FORMS-The limit of liability for Coverages C or D of Section I and E

or F of Section II may be increased. c. FORMS HO-3, MH-3 and HO-5 - Under Coverage B of Section I, an

additional amount of insurance may be written on a specific structure. d. FORM HO-3, MH-3 - Under Coverage C of Section I, it is permissible to

reduce the limit of liability to an amount not less than 40% of the limit on the dwelling. Reduced Coverage C is not permitted if HO-42 Permitted Incidental Occupancies (Residence Premises) or HO M290 Personal Property Replacement Cost is present.

e. FORM HO-6 - The limit of liability for Coverage A of Section I may be increased.

Description of Coverage a. Section I Coverages-Property Damage The following is a general description of the coverages provided by the individual Homeowner policy forms. The policy should be consulted for exact contract conditions.

HO-3

MH-3 HO-4 & HO-6 HO-5

Fire or Lightning Yes Cov. C

Yes Yes

Windstorm or Hail, Explosion, Riot or civil commotion, Aircraft, Vehicles or Smoke

Yes Cov. C

Yes Yes

Vandalism or malicious mischief Yes Cov. C

Yes Yes

Theft Yes Cov. C

Yes Yes

Breakage of glass or safety glazing material Yes Cov. C

Yes Yes

Volcanic eruption Yes Cov. C

Yes Yes

Falling objects, Weight of ice, snow or sleet, Accidental discharge of water or steam, Sudden and accidental tearing apart of a heating system or appliance, Freezing, Sudden accidental damage from electrical current

Yes Cov. C

Yes Yes

Additional risks with certain exceptions

(Special Coverage) Yes

Cov. A, B & D

No Yes

b. Section II Coverages–Liability–All Forms (1) Coverage E - Personal Liability-Covers payment on behalf of any

insured of all sums which the insured shall become legally obligated to pay as damages because of bodily injury or property damage arising out of an insured’s premises or personal activities.

(2) Coverage F - Medical Payments to Others-Covers medical expenses incurred by persons, other than the insured, who sustain bodily injury caused by an accident arising out of an insured’s premises or personal activities.

Utah – Home Program Program Guidelines

Enumclaw Property and Casualty Insurance Company 6

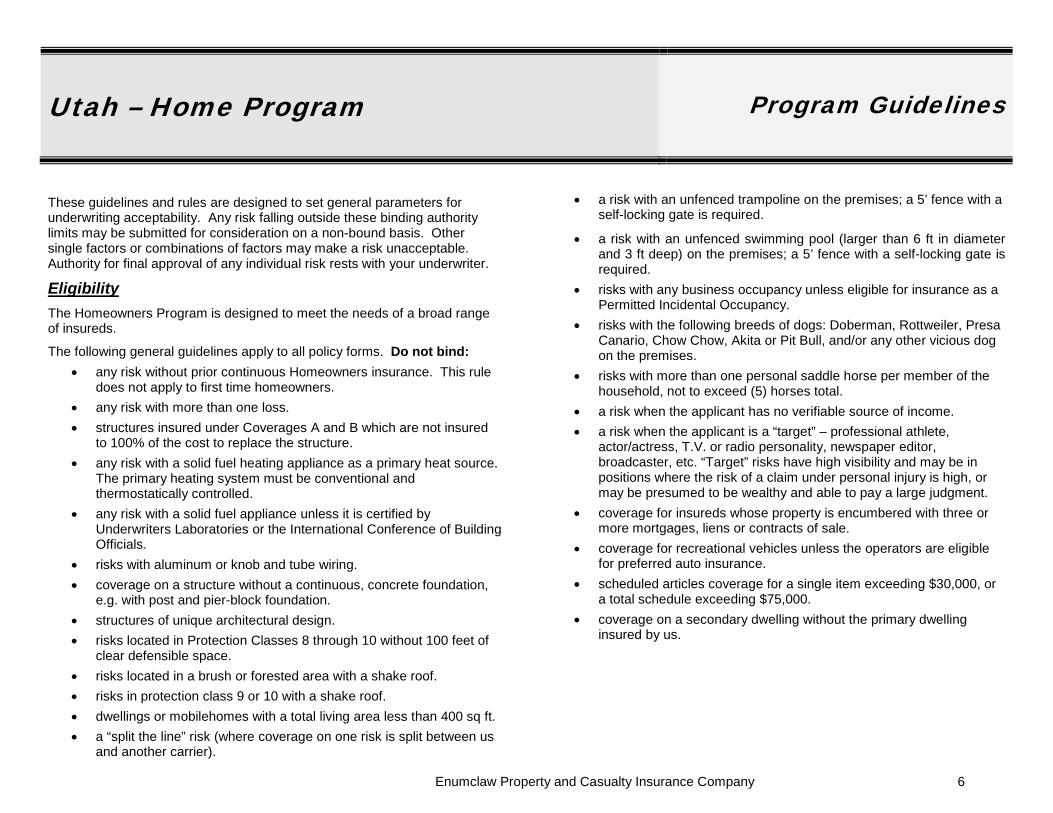

These guidelines and rules are designed to set general parameters for underwriting acceptability. Any risk falling outside these binding authority limits may be submitted for consideration on a non-bound basis. Other single factors or combinations of factors may make a risk unacceptable. Authority for final approval of any individual risk rests with your underwriter.

Eligibility The Homeowners Program is designed to meet the needs of a broad range of insureds.

The following general guidelines apply to all policy forms. Do not bind: • any risk without prior continuous Homeowners insurance. This rule

does not apply to first time homeowners. • any risk with more than one loss. • structures insured under Coverages A and B which are not insured

to 100% of the cost to replace the structure. • any risk with a solid fuel heating appliance as a primary heat source.

The primary heating system must be conventional and thermostatically controlled.

• any risk with a solid fuel appliance unless it is certified by Underwriters Laboratories or the International Conference of Building Officials.

• risks with aluminum or knob and tube wiring. • coverage on a structure without a continuous, concrete foundation,

e.g. with post and pier-block foundation. • structures of unique architectural design. • risks located in Protection Classes 8 through 10 without 100 feet of

clear defensible space. • risks located in a brush or forested area with a shake roof. • risks in protection class 9 or 10 with a shake roof. • dwellings or mobilehomes with a total living area less than 400 sq ft. • a “split the line” risk (where coverage on one risk is split between us

and another carrier).

• a risk with an unfenced trampoline on the premises; a 5’ fence with a self-locking gate is required.

• a risk with an unfenced swimming pool (larger than 6 ft in diameter and 3 ft deep) on the premises; a 5’ fence with a self-locking gate is required.

• risks with any business occupancy unless eligible for insurance as a Permitted Incidental Occupancy.

• risks with the following breeds of dogs: Doberman, Rottweiler, Presa Canario, Chow Chow, Akita or Pit Bull, and/or any other vicious dog on the premises.

• risks with more than one personal saddle horse per member of the household, not to exceed (5) horses total.

• a risk when the applicant has no verifiable source of income. • a risk when the applicant is a “target” – professional athlete,

actor/actress, T.V. or radio personality, newspaper editor, broadcaster, etc. “Target” risks have high visibility and may be in positions where the risk of a claim under personal injury is high, or may be presumed to be wealthy and able to pay a large judgment.

• coverage for insureds whose property is encumbered with three or more mortgages, liens or contracts of sale.

• coverage for recreational vehicles unless the operators are eligible for preferred auto insurance.

• scheduled articles coverage for a single item exceeding $30,000, or a total schedule exceeding $75,000.

• coverage on a secondary dwelling without the primary dwelling insured by us.

Utah – Home Program Program Guidelines

Enumclaw Property and Casualty Insurance Company 7

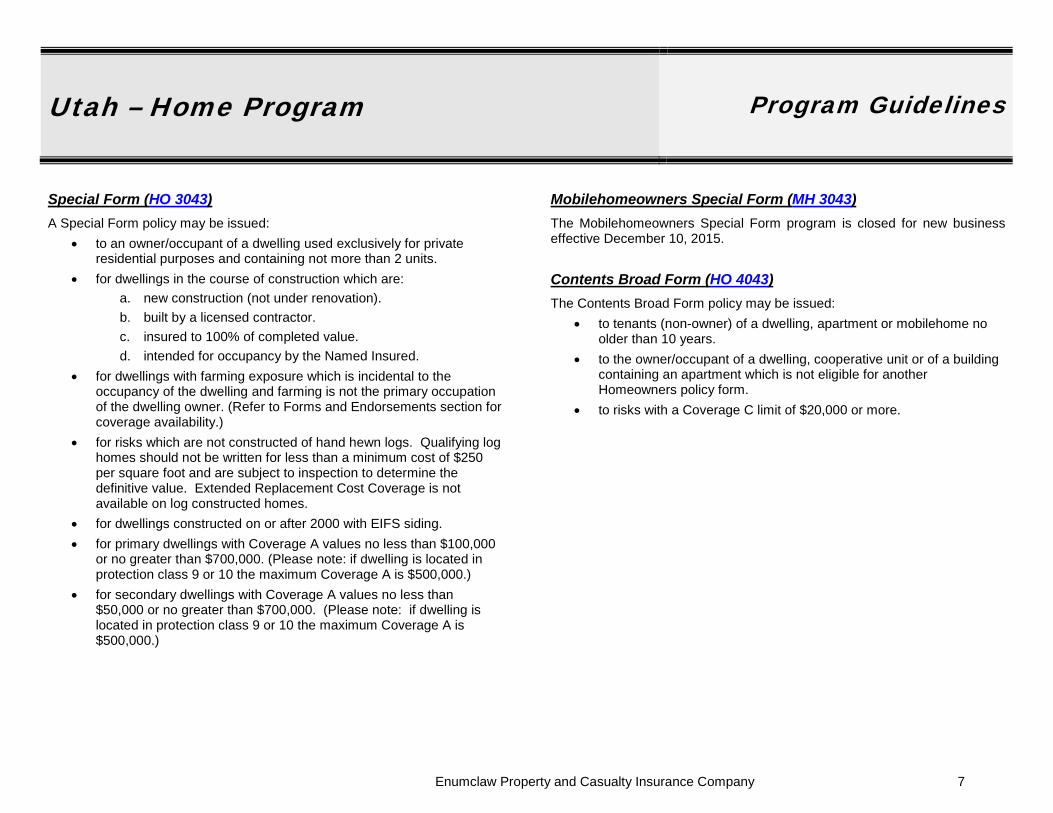

Special Form (HO 3043) A Special Form policy may be issued:

• to an owner/occupant of a dwelling used exclusively for private residential purposes and containing not more than 2 units.

• for dwellings in the course of construction which are: a. new construction (not under renovation). b. built by a licensed contractor. c. insured to 100% of completed value. d. intended for occupancy by the Named Insured.

• for dwellings with farming exposure which is incidental to the occupancy of the dwelling and farming is not the primary occupation of the dwelling owner. (Refer to Forms and Endorsements section for coverage availability.)

• for risks which are not constructed of hand hewn logs. Qualifying log homes should not be written for less than a minimum cost of $250 per square foot and are subject to inspection to determine the definitive value. Extended Replacement Cost Coverage is not available on log constructed homes.

• for dwellings constructed on or after 2000 with EIFS siding. • for primary dwellings with Coverage A values no less than $100,000

or no greater than $700,000. (Please note: if dwelling is located in protection class 9 or 10 the maximum Coverage A is $500,000.)

• for secondary dwellings with Coverage A values no less than $50,000 or no greater than $700,000. (Please note: if dwelling is located in protection class 9 or 10 the maximum Coverage A is $500,000.)

Mobilehomeowners Special Form (MH 3043) The Mobilehomeowners Special Form program is closed for new business effective December 10, 2015. Contents Broad Form (HO 4043) The Contents Broad Form policy may be issued:

• to tenants (non-owner) of a dwelling, apartment or mobilehome no older than 10 years.

• to the owner/occupant of a dwelling, cooperative unit or of a building containing an apartment which is not eligible for another Homeowners policy form.

• to risks with a Coverage C limit of $20,000 or more.

Utah – Home Program Program Guidelines

Enumclaw Property and Casualty Insurance Company 8

Enhanced Form (HO 5043) The Enhanced Form policy may be issued:

• for dwellings and premises constructed on or after 1975 that exhibit above average maintenance and pride of ownership.

• for owner occupied dwellings used exclusively for private residential purposes and containing not more than 2 units.

• for dwellings that are not of log or “earth” construction. • for dwellings that are not of the modular or mobilehome construction

type. • for dwellings constructed on or after 2000 with EIFS siding. • for dwellings with standard, or better, quality construction. • for dwellings in the course of construction which are:

a. new construction (not under renovation) b. built by a licensed contractor c. insured to 100% of completed value d. intended for occupancy by the Named Insured.

• for dwellings with Coverage A values no less than $300,000. Values exceeding the agent binding authority should be discussed with the Underwriter.

• for dwellings in protection classes 1 – 8B. • for dwellings with farming exposure which is incidental to the

occupancy of the dwelling and farming is not the primary occupation of the dwelling owner. (Refer to Forms and Endorsements section for coverage availability.)

Unit-Owners Form (HO 6043) The Unit-Owners Form policy may be issued:

• to the owner/occupant of a cooperative or condominium unit which is used exclusively for private residential purposes.

• to risks with a Coverage C limit of $40,000 or more.

Utah – Home Program General Rules

Enumclaw Property and Casualty Insurance Company 9

Cancellation Or Reductions In Limits Of Liability Or Coverages It is not permissible to cancel any of the mandatory coverages in the policy unless the entire policy is cancelled.

If insurance is cancelled or reduced at the request of either the insured or insurer, any earned premium shall be computed on a pro rata basis.

Construction Definitions Frame - exterior wall of wood or other combustible construction, including wood-iron clad, stucco on wood or plaster on combustible supports.

Includes:

Aluminum or plastic siding over frame.

Log - a building with exterior walls of (natural or manufactured) log construction. (This construction class is not valid for HO-4, HO-6 or HO-5 policy forms. Hand hewn log homes are not acceptable.)

Masonry Veneer - exterior walls of combustible construction veneered with brick or stone. Rate as masonry provided at least 66% of the exterior walls, including gables, are veneered with brick or stone.

Masonry - exterior walls constructed of masonry materials such as adobe, brick, concrete, gypsum block, hollow concrete block, stone, tile or similar materials and floors and roof of combustible construction (disregarding floors resting directly on the ground).

NOTE: Mixed (Masonry/Frame) - a combination of both frame and masonry construction shall be classed and coded as frame when the exterior walls of frame construction (including gables) exceed 33 1/3% of the total exterior wall area; otherwise class and code as masonry.

Mandatory Coverages It is mandatory that insurance be written for all coverages provided under both Sections I and II of the Homeowners Policy. Section II of the policy requires coverage for the following exposures:

(a) all additional insured locations where the Named Insured or spouse maintain a residence other than business or farm properties;

(b) all residence employees of the Named Insured or spouse not covered or not required to be covered by workers compensation insurance; and

(c) permitted incidental occupancies by the insured on residential premises of the Named Insured.

Manual Premium Revision A manual premium revision, meaning any revision of premium applicable to the Homeowners Program, shall be made in accordance with the following procedures:

(a) The effective date of such revision shall be as announced. (b) The revision shall apply to any policy or endorsement in the manner

outlined in the announcement of the revision. (c) When an existing Homeowners Policy is endorsed to take advantage

of a reduction in premium, the adjustment shall be made on a pro rata basis.

(d) Unless otherwise provided, at the time the premium revision becomes effective, the premium revision does not affect in-force policy forms and endorsements until the policy is renewed.

Minimum Premium A minimum annual premium of $150 shall apply to the HO-3, MH-3, HO-5 and HO-6 policy forms. A $75 minimum premium applies to the HO-4 form. . All chargeable endorsements and coverages, written at the inception of the policy, are subject to the minimum premium except Scheduled Personal Property (HO-61) and Scheduled Property - Agreed Value Coverage (HO M5350). When endorsements or coverages are attached after inception of the policy, the charge for each applies in accordance with the minimum premium rule, if any, for the endorsement.

Multiple Company Insurance Not offered in this program.

Utah – Home Program General Rules

Enumclaw Property and Casualty Insurance Company 10

Other Insurance Credit for existing insurance is not permitted.

Policy Changes Endorsements The addition or deletion of coverages will not alter the premium due date or the term of the policy. Adjustments in premium due to the changes will be prorated from the effective date to the end of the policy term and a full adjustment will be made for the next renewal cycle.

Cancellation All cancellations, regardless of whether they are initiated by the company or the policyholder, are calculated on a pro rata basis.

Policy Period The Homeowners Policy shall be written for a period of one year and may be extended for successive policy periods by a renewal declarations page based upon the premiums, forms and endorsements then in effect for the Company. For maintaining common anniversary dates, a Homeowners Policy may be written for a period of less than one year on a pro rata basis.

Premium Adjustments 1. Paid-In-Full Policies

a. Additional premium will be billed as an installment.

b. Return premium will be sent to the insured in 10 days.

2. Installment Bill Policies

a. Additional premium will be spread over remaining installments.

b. Return premium will be spread over the current and remaining installments.

c.

Premium Rounding Rule HO-3, MH-3 and HO-5 policy premiums will be rounded to the penny. HO-4 and HO-6 policy premiums and optional endorsements will be rounded to the nearest whole dollar.

In the event of cancellation by the Company, the return premium may be carried to the next higher whole dollar.

Property Renewal Increases The limits of liability shown in the declarations page for Coverages A, B, C and D will be increased at the annual renewal by the property renewal increase factors adopted by the company. Payment of the renewal premium will constitute acceptance of the revised limits of liability as shown on the Declarations page.

Protection Information The Protection Class assigned will be that developed by the Insurance Services Office. . Temporary override of an assigned protection class may be allowed, based upon the circumstances of the risk and approval by the Company.

Renewal Plan A Homeowners Policy may be written for a term of twelve months. The policy may be continued for successive terms upon payment of the required premium to the Company on or before the inception date of each successive term.

The continuation premium shall be based upon the premiums in effect on the renewal date. The then current editions of the applicable forms and endorsements must be made a part of the policy.

Seasonal Dwelling Definition A seasonal dwelling is a dwelling with continuous unoccupancy of three or more consecutive months during any one year period.

Utah – Home Program General Rules

Enumclaw Property and Casualty Insurance Company 11

Secondary Residences A separate policy may be written to insure the dwelling and other structures at a second residence. The liability for this residence must be extended from the primary policy written with us.

Single Building Definition All buildings or sections of buildings which communicate through unprotected openings will be considered as a single building.

Buildings which are separated by space will be considered separate buildings.

Buildings or sections of buildings which are separated by an 8 inch masonry party wall which pierces or rises to the underside of the roof and which pierces or extends to the innerside of the exterior wall will be considered separate buildings. Communication between buildings with independent walls or through masonry party walls described above will be protected by at least a Class A Fire Door installed in a masonry wall section.

Transfer Or Assignment Subject to all the rules of this manual and any necessary adjustment of premium, a Homeowners Policy may be endorsed to effect transfer to another location within the same state.

No assignments of a policy from one insured to another are allowed.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 12

We are providing general descriptions of endorsements offered. Please consult the actual forms and endorsements for exact terms, conditions and exclusions.

Underwriting guidelines are not intended to be inclusive. Additional information may be required under certain circumstances.

Actual Cash Value Mobilehome MH-202 Amends the mobilehome policy from a replacement cost contract to an actual cash value contract.

Underwriting Guidelines: • Available on MH-3. • The mobilehome must have a minimum value of $15,000. • The mobilehome cannot be over 15 years old.

Additional Insured (Residence Premises) HO-41 Extends Section I Coverages A and B and Section II Coverages E and F to someone other than the Named Insured who has an ownership interest in the dwelling.

Information required to complete the endorsement form: • Name and address of the additional insured. • Interest of the additional insured.

Additional Interests (Residence Premises) HO-310 Used to add a third party, other than a mortgagee, who has an interest in the residence. Affords Section I coverages only.

Information required to complete the endorsement form: • Name and address of the other party. • Description of their interest. • Effective date of their interest.

Additional Residence Rented to Others (1, 2, 3 or 4 Families) HO-70 Extends Personal Liability and Medical Payments to Others coverages to owned residences rented to others.

Underwriting Guidelines: • Extension of liability is limited to maximum of 10 family units (a

duplex counts as 2 units, a triplex is 3 units, etc.). • This endorsement may extend liability only to 1, 2, 3 or 4 Family

dwellings. • Dwelling must be located in a state in which we are licensed to

conduct business.

Information required to complete the endorsement form: • Dwelling location. • Number of families.

Not available on Secondary or Seasonal Occupancy status policies.

Barns, Buildings and Structures HO M007, HO M5007 Named perils coverage on an actual cash value basis for barns, buildings and structures. As these structures are specifically insured, Coverage B of the policy does not apply to them.

Underwriting Guidelines: • Available on HO-3, HO-5 and MH-3 policy forms.

Information required to complete the endorsement form: • Description of structure. • Limit per structure. • Use of structure.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 13

Building Additions and Alterations (Other Residence) HO-49 Used to cover the insured’s interest in additions, alterations, and improvements to rented secondary residences.

Information required to complete the endorsement form: • Location Address. • Limit for each location.

Building Additions and Alterations HO-51—Increased Limit Form HO-4 Used to provide an increased limit for tenants’ building additions, alterations, fixtures, improvements, and installations.

Underwriting Guidelines: • Available on HO-4 policy forms.

Information required to complete the endorsement form:

• Increase amount.

Business Pursuits HO-71 Coverage for liability arising out of business pursuits may be added to the policy through the use of this endorsement. Coverage does not apply to a business owned by the insured or in which the insured is a partner. Professional liability is excluded for other than teaching.

Information required to complete the endorsement form: • Insured’s name. • Business description. • Employment classification. • Corporal punishment liability desired (if insured is a teacher).

Not available on Secondary or Seasonal Occupancy status policies.

Course of Construction HO M005 This endorsement is attached to a new business policy when construction of the dwelling has begun.

Underwriting Guidelines:

• Available on HO-3 and HO-5 policy forms.

• A dwelling being constructed by the insured is not eligible.

• The coverages afforded by this endorsement cease 1 year after the original inception date of the policy. Any dwellings not scheduled to be done within 365 days are not eligible for coverage.

Contract of Sale 137 Provides coverage language specific to contract seller.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 14

Coverage C Increased Special Limits of Liability HO-65 The policy form contains Special Limits of Liability under Coverage C for certain categories of property. This endorsement is used to increase money, securities, jewelry, firearms, and silverware without specifically scheduling each item. The last 3 categories are increased with respect to theft only. The Coverage C perils named in the contract are not changed by this endorsement.

1. Jewelry, Watches and Furs

The special limit on jewelry, watches and furs may be increased to a maximum of $5,000 but not exceeding $1,000 for any one article.

2. Money and Securities

The special limit on money may be increased to a maximum of $1,000. The limit on securities may be increased to a maximum of $2,000.

3. Silverware, Goldware and Pewterware

The special limit for loss by theft of silverware, etc., may be increased to a maximum of $10,000 in increments of $500.

4. Firearms

The special limit for loss by theft of firearms may be increased to a maximum of $6,000 in increments of $100.

Underwriting Guidelines: • Available on HO-3, MH-3, HO-4 and HO-6 policy forms. • This endorsement is not available on HO-3 policy forms written with

the HO M015 endorsement (Use HO-211).

Information required to complete the endorsement form: • The class of property which is to be increased. • The amount of the increase per property class.

Coverage C Increased Special Limits of Liability HO-211, HO M5211 Used to increase the special limits of liability for certain categories.

1. Jewelry, Watches and Furs

The special limit on jewelry, watches and furs may be increased to a maximum of $5,000 but not exceeding $1,000 for any one article.

2. Money and Securities

The special limit on money may be increased to a maximum of $1,000 for HO-3, $2,000 for HO-5. The limit on securities may be increased to a maximum of $2,000.

3. Silverware, Goldware and Pewterware

The special limit for loss by theft of silverware, etc., may be increased to a maximum of $10,000 in increments of $500.

4. Firearms

The special limit on firearms may be increased to a maximum of $10,000.

Underwriting Guidelines: • Available on HO-3 policy form with HO M015 endorsement and HO-5

policy forms. • Only money and firearms are eligible for increased limits on HO-5.

Information required to complete the endorsement form: • Property class to be increased. • Amount of increase per property class.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 15

Credit Card, Fund Transfer Card, Forgery and Counterfeit Money Coverage (Increased Limit) HO-53, HO M5053 Used to increase the automatic limit provided in the policy.

Available limits:

$2500(not applicable to HO-5), $5000, $7,500, $10,000

Information required to complete the endorsement form: • Increase amount.

Equipment Breakdown Enhancement Endorsement HO M180 Coverage for applicable electrical, mechanical, or pressure systems breakdown.

• $100,000 per Occurrence Limit of Liability • $500 Per Occurrence Deductible

o In the event that more than one deductible may be applied to a loss that includes Equipment Breakdown, the single highest deductible will apply.

Underwriting Guidelines:

• Available to HO-3, HO-5, MH-3, HO-4 and HO-6 policy forms.

Extended Home Replacement Coverage HO M5101 This endorsement amends item 3.b. of the Section I – Conditions by stating we will settle covered losses to Coverage A & B up to an additional amount of the Coverage A or Coverage B limit of liability shown on the Declarations pages.

• This is a mandatory form.

Underwriting Guidelines: • Applicable to HO-5 policy form.

Farmers Personal Liability HO M073UT, HO M5073UT This endorsement may be used to cover farm liability exposures when the insured has a farming exposure, by leasing farm land to others, is not actively involved in farming and farming is not his primary occupation. This endorsement form will not be offered only for the purpose of obtaining animal collision coverage.

The following guidelines apply to leased farmland:

a. Lessee must maintain insurance coverage for the farming operations.

b. Our insured must be listed as an additional insured on the lessee’s policy.

c. If the leased land is also the residential premise the named insured must reside in the home.

d. Insured owned equipment should not be used by the lessee.

Information required to complete the endorsement form:

Farm questionnaire PL106 completed by the insured.

Location of all farm premises and type of farming conducted on each.

a. Number of additional farm premises.

b. Number of farm premises without buildings.

c. Acreage.

Description of any business pursuits (other than farming) which are conducted on the insured location(s)

Animal Collision

a. Number of animals ($400 coverage per animal).

Not available on Secondary or Seasonal Occupancy status policies.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 16

Homeowners Extended Replacement Cost Coverage HO M091 When this endorsement is attached to the policy, we agree to settle covered losses to the dwelling up to an additional amount of the limit of liability under Coverage A shown on the Declarations page at the time of loss. Dwellings must be insured to 100% of replacement cost to be eligible for this coverage. Underwriting Guidelines:

• Available on HO-3 policy form. Identity Fraud Expense Coverage HO M5316 This form provides reimbursement for expenses incurred by an insured as a direct result of identity fraud.

• This is a mandatory form. Underwriting Guidelines:

• Applicable to HO-5 policy form.

Incidental Farming Personal Liability HO-72 This endorsement provides Personal Liability and Medical Payments coverages only with respect to “incidental” farming operations of the insured on the residence premises.

Underwriting Guidelines: • In most cases, the farm exposure should:

a. Not exceed gross revenue of $15,000. b. Be for a policyholder who has an “off the farm” primary

occupation (unless retired). c. Not have a riding arena. d. Not have a dairy operation. e. Not exceed (80) acres. f. Be limited to $30,000 of scheduled farm equipment, including a

small amount of irrigation equipment, on an Inland Marine policy. g. Be limited to a combined total of $100,000 for newer structures

at replacement value on an HO48. h. Be limited to a combined total of $50,000 on an HOM007 at ACV

for older structures.

• Exposures not contemplated in Personal Lines include:

a. Employees (full or part time). b. Tree farms. c. U-cut/U-pick operations. d. Roadside sales stands. e. Boarding, breeding, training or renting of animals. f. Exotic animals. g. Custom farmers. h. Nurseries. i. Poultry. j. Processing or dairies. k. Seed operations. l. Kennels. m. Property open for hunting.

• The Farm Liability questionnaire (PL 106) must be completed.

Not available on Secondary or Seasonal Occupancy status policies.

Incidental Motorized Land Conveyances HO M313UT, HO M5313UT This endorsement extends, to the insured and permissive operators, Section II coverages to motorized vehicles excluding:

• motorized bicycles, mopeds or motorized golf carts • any conveyance:

a. with a maximum speed of more than 25 MPH. b. subject to motor vehicle registration. c. while used to carry persons for a charge. d. while used for business purposes. e. while rented to others. f. while operated in any race, speed contest or competition.

If a vehicle is not eligible for coverage under this endorsement, we also have available Recreational Vehicle Liability Coverage under endorsement HO M009.

This is a mandatory endorsement but not applicable when the HO M073UT or HO M5073UT are attached.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 17

Increased Limit on Personal Property in Other Residences HO-50 This endorsement is used when an increased limit is desired.

Underwriting Guidelines: • Verify liability extension to additional residence(s).

Information required to complete the endorsement form: • Location address. • Increase amount.

Increased Limits on Business Property HO-312, HO M5312 The policy form contains special limits on business property. Limits may be increased by means of this endorsement. The increased limit does not apply to business property in storage or held as a sample or for sale or delivery after sale or to business property pertaining to a business actually conducted on the residence premises. The specific dollar increase applies to on premises business property. Off premises business property is covered at 10% of the on premises limit. Underwriting Guidelines:

• Maximum limit is $10,000. Information required to complete the endorsement form:

• Increase in limit. • Description of the business. • Description of the business property.

Landlord’s Furnishings HO-308 This endorsement is used to increase the coverage for property in an apartment regularly rented or held for rental to others by an insured.

Underwriting Guidelines: • Not available on HO-3 with HO M015 or HO-5 policy forms.

Available Limits: • $1,000, $2000, $3,000, $4,000, $5,000

Loss Assessment Coverage HO-35, HO M5035 All policy forms include an automatic limit of loss assessment coverage (excluding earthquake). Please refer to the specific contract for the amount of coverage provided. Increased limits may be obtained with this endorsement. Please note: The policy forms do include a Special Limit applicable to an assessment resulting from a deductible in the policy of insurance purchased by a corporation or association of property owners. Please refer to the desired policy form for the pertinent information. Available Limits:

• Residence Premises: $5,000 to $50,000 in increments of $5,000 o The minimum increase limit for HO-5 is $10,000.

• Additional Locations: $1,000, $5,000 to $50,000 in increments of $5,000

Underwriting Guidelines: • No more than 2 locations can be written in addition to the residence

premises. Information required to complete the endorsement form:

• Increase in limit on the residence premises. • If additional locations are covered the unit location and limit per

location should be provided.

Loss Payable Endorsement (HO M335)

Provides coverage language specific to a mortgagee.Mobilehome Lienholder’s Single Interest MH-85 This endorsement provides coverage only for the interest of the lienholder on the mobilehome for collision or upset while in transit and from conversion, embezzlement, or secretion by the insured.

Underwriting Guidelines: • Available on MH-3 policy form.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 18

Ordinance or Law Coverage HO M277V This endorsement amends the contract to insure the Dwelling and Other Structures against loss resulting from ordinances or laws which regulate construction, repair or demolition of the property. Underwriting Guidelines:

• Available on HO-3 or HO-6 policy forms. • Available with HO-49 Building Additions and Alterations (Other

Residence) endorsement. Information required to complete the endorsement form:

• Aggregate limit desired. • Available options: 25%, 50% or 100% of Coverage A

(Note: if attached to HO-49 Building Additions and Alterations (Other Residence) or HO-6 policies, 100% of Coverage A option must be selected.)

Ordinance or Law Coverage HO M5277V This endorsement amends the contract to insure the Dwelling and Other Structures against loss resulting from ordinances or laws which regulate construction, repair or demolition of the property. Underwriting Guidelines:

• Available on HO-5. Information required to complete the endorsement form:

• Aggregate limit desired. • Available options: 50% or 100% of Coverage A

Other Structures (Increased Limits) HO-48 This endorsement is used to increase coverage on other structures on the residence premises over what is provided in the policy form. The Coverage B Perils Insured Against in the policy extend to the additional limits obtained through the use of this endorsement.

Underwriting Guidelines:

• Available on HO-3, MH-3 and HO-5 policy forms. • This endorsement is not to be used for agricultural type buildings.

For those exposures, see endorsement HO M007 Barns, Buildings and Structures.

Information required to complete the endorsement form: • Structure description including construction type, square footage and

use. • Limit per structure.

Permitted Incidental Occupancies (Residence Premises) HO-42, HO M5042 Section I and II Coverages of the policy are extended to cover an incidental office, professional, private school, or studio occupancy in the dwelling or in a separate structure on the residence premises. If the business is conducted in another structure on the residence premises Coverage B does not apply. The structure is specifically insured for direct physical loss by a Peril Insured Against under Coverages A and B of the policy form under this endorsement. Professional liability is excluded. This endorsement provides that certain property of the permitted business is covered up to the Coverage C limit. However, the endorsement does not increase the Coverage C limit. Underwriting Guidelines:

• The only types of business activities eligible for this endorsement are office, studio, and school operations using less than half of the dwelling area. Day care operations may not be covered by this endorsement.

Information required to complete the endorsement form: • Business description. • Location where the business is conducted. • If conducted in an Other Structure, a description of the structure. • Limit on Other Structure.

Not available on Secondary or Seasonal Occupancy status policies.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 19

Permitted Incidental Occupancies (Other Residence) HO-43, HO M5043 Section II Coverage is extended to cover an incidental office, professional, private school, or studio occupancy in a residence other than the insured residence premises. Professional liability is excluded. Underwriting Guidelines:

• The only types of business activities eligible for this endorsement are office, studio, and school operations using less than half of the dwelling area. Day care operations may not be covered by this endorsement.

Information required to complete the endorsement form: • Business description. • Premises location.

Not available on Secondary or Seasonal Occupancy status policies.

Personal Property Replacement Cost HO M290 This endorsement is used to provide replacement cost coverage on property covered under Coverage C and, if applicable, awnings, carpeting, household appliances, outdoor antennas and outdoor equipment, whether or not attached to buildings. The Coverage C Perils Insured Against are not changed by this endorsement. Coverage also applies to articles or classes of property separately described and specifically insured in the policy (i.e. HO-61). Refer to the endorsement for ineligible property and loss settlement provisions.

Coverage C of HO-3 and MH-3 is automatically increased, at no additional charge, to 70% of Coverage A.

Underwriting Guidelines: • Available on HO-3, MH-3, HO-4 and HO-6 policy forms.

Pollution Exclusion HO M011 If Farmers Personal Liability is endorsed onto the policy it is mandatory that this endorsement also be added. This exclusion amends the pollution exclusion which is found in the Farmers Personal Liability endorsement.

Premises Alarm or Fire Protection System HO-216 This endorsement is attached when a credit is being allowed for an approved alarm system.

Information required to complete the endorsement form: • Type of Protective Device System:

a. Burglar Alarm. b. Fire Alarm. c. Burglar and Fire Alarm.

• Installed to Alert: a. Central Station (copy of contract required). b. Police Station/Fire Department. c. Local only.

Underwriting Guidelines:

• A “local” burglar alarm must include a functional bell or similar sound-generating device mounted on the exterior of the dwelling.

• A “local” fire alarm is required to produce a sound inside the dwelling to alert the occupants.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 20

Property Removed Increased Limit MH-104 Increases the coverage limit found in the policy that applies to moving expense when the mobilehome is endangered by a Peril Insured Against.

Underwriting Guidelines: • Available on MH-3 policy form.

Information required to complete the endorsement form: • Increase Limit.

Recreational Vehicle Liability Coverage HO M009, HO M5009 This endorsement provides, for the insured and permissive operators, off premises Liability and Medical Payments to Others coverage for recreational vehicles (other than snowmobiles and golf carts on a golf course).

Information required to complete the endorsement form: • Make or model name of each vehicle. • Identification number for each vehicle. • Horsepower for each vehicle. • Driver’s license numbers and dates of birth for household members.

Not available on Secondary or Seasonal Occupancy status policies.

Residence Rental Theft HO-80 Extends coverage to loss by theft while the portion of the residence premises usually occupied by the insured is occasionally rented in whole or in part to others, or while there is a roomer or boarder. Refer to the endorsement for the exclusions to this extension of coverage.

Underwriting Guidelines: • Available on HO-3 policy form. Not available on HO-3 with HO M015. • Requires underwriting approval prior to binding. • Regularity of rental. • Portion of the dwelling rented. • Reason for the rental.

Scheduled Bicycle Endorsement HO M602 This endorsement provides coverage for scheduled bicycles that may require higher limits or broader coverage than is provided in the Homeowners policy form.

Underwriting Guidelines: • $30,000 maximum value per item. • Appraisals or bill of sale on items valued at $10,000 and higher. • Items must be insured to 100% of value. • Prior approval from the company is required to bind coverage on

schedules in excess of $75,000. This limit is a combined total of items scheduled under the HO M061 Scheduled Personal Property Endorsement as well as this Scheduled Bicycle Endorsement.

Information required to complete the endorsement form: • Name of article • Description of article (make/model/serial number). • Amount per article. • Appraisal or bill of sale (as per guidelines above).

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 21

Scheduled Personal Property Endorsement HO M061 This endorsement provides protection on specific items of personal property that may require higher limits or broader coverage than is provided in the Homeowners policy form. Eligible classes of property are jewelry, furs, cameras, musical instruments, silverware, golfer’s equipment, fine arts, postage stamps, rare and current coins, and guns.

Underwriting Guidelines: • $30,000 maximum value per item. • Appraisals on items valued at $10,000 and higher. • Items must be insured to 100% of value. • Prior approval from the company is required to bind coverage on

schedules in excess of $75,000. This limit is a combined total of items scheduled under the HO M602 Scheduled Bicycle Endorsement as well as this Scheduled Personal Property Endorsement.

Information required to complete the endorsement form: • Description of article. • Amount per article. • Appraisal (as per guidelines above).

Scheduled Property – Agreed Value Coverage HO M5350 This endorsement provides coverage for scheduled jewelry with losses settled on the basis of the amount shown on the declarations.

Underwriting Guidelines: • Available on HO-5 policy form.

Underwriting Guidelines: • $30,000 maximum value per item. • Appraisals on items valued at $10,000 and higher. • Prior approval from the company is required to bind coverage on

schedules in excess of $75,000.

Information required to complete the endorsement form: • Description of article. • Amount per article. • Appraisal (as per guidelines above).

Service Line Enhancement Endorsement HO M108 Coverage for applicable failure of service lines from the street to the covered home.

• $10,000 per Occurrence Limit of Liability • $500 Per Occurrence Deductible

Underwriting Guidelines:

• Available to HO-3, HO-5 and MH-3 policy forms.

Snowmobile Liability HO M164UT This endorsement provides, for the insured and permissive operators, Personal Liability and Medical Payments to Others coverage for owned snowmobiles off an insured location, subject to certain limitations.

• This is a mandatory endorsement.

Not available on Secondary or Seasonal Occupancy status policies.

Special Computer Coverage HO-314 Computers and related equipment may be insured against additional risks of physical loss subject to certain exclusions. The limit of liability for a computer is not increased by this endorsement.

Underwriting Guidelines: • Not available on HO-3 policy forms with an HO M015 endorsement

attached or HO-5 policies.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 22

Special Personal Property Coverage HO M015 By attachment of this endorsement, the policy is amended to insure Coverage C against additional risks of physical loss subject to certain exclusions.

Underwriting Guidelines: • Earthquake coverage is excluded. • Available only on HO-3 and MH-3 policy forms. • Personal Property Replacement Cost must be written on Coverage C

- Personal Property. • Policy must be written with at least a $500 deductible.

Special Provisions – Utah HO M301UT, HO M401UT, HO M501UT, HO M601UT These forms modify certain provisions in the policy to meet specific state requirements.

Structures Rented to Others (Residence Premises) HO-40 This endorsement extends Section I and Section II Coverage to specified structures on the residence premises rented to anyone other than a tenant of the dwelling for use as a private residence. Coverage B does not apply to structures scheduled on this endorsement.

Information required to complete the endorsement form: • Structure description including construction type, square footage and

use. • Limit per structure.

Not available on Secondary or Seasonal Occupancy status policies.

Theft of Building Materials – Dwelling Under Construction HO M012 This endorsement provides coverage for theft from the insured location of personal property and building materials or supplies for a home under construction. Coverage is limited to 10% of the Coverage A - Dwelling limit. The premium is fully earned when written. Coverage expires at the first policy expiration date or when the dwelling is completed and occupied, whichever comes first. If an extension of coverage past the first expiration date is desired Underwriter approval is required. An additional fully earned premium will be applied. No further coverage extension will be allowed. Underwriting guidelines:

• Available on HO-3 and HO-5 policy forms.

Three or Four Family Dwelling Premises Liability HO-74 (Form HO-4) This endorsement is attached only when the insured owns a 3 or 4 family dwelling and occupies one of the units. While the structure is insured under another policy, the insured may obtain coverage for personal property and personal liability on a Contents Broad Form (HO-4) policy. Personal liability is extended to that portion of the structure which is not occupied by the insured when this endorsement is attached.

Underwriting Guidelines: • Available on HO-4 policy form. • This coverage is not available to a tenant who does not have an

ownership interest in the residence premises.

Not available on Secondary or Seasonal Occupancy status policies.

Utah – Home Program Forms and Endorsements Descriptions

Enumclaw Property and Casualty Insurance Company 23

Transportation/Permission to Move MH-82 Applies coverage against the transportation perils of collision, upset, and stranding or sinking of the mobilehome for 30 days anywhere in the continental United States or Canada.

Underwriting Guidelines: • Available on MH-3 policy form. • Location mobilehome is being moved from. • Location where mobilehome is being moved to.

Information required to complete the endorsement form: • Effective Date. • Deductible Amount.

Unit-Owners Coverage A Special Coverage HO-32 The Section I Perils Insured Against may be broadened for Coverage A to Special Form by adding this endorsement.

Underwriting Guidelines: • Available on HO-6 policy forms.

Unit-Owners Rental to Others HO-33 This endorsement extends both Section I and Section II Coverage when the insured condominium unit is regularly rented to others.

Underwriting Guidelines: • Available on HO-6 policy forms. • Prior approval is required.

Not available on Secondary or Seasonal Occupancy status policies.

Water Backup and Sump Discharge or Overflow HO M095 Provides coverage for for direct physical loss to property covered under Section I caused by water, or waterborne material

Underwriting Guidelines: • Available on HO-3 policy form. • This coverage does not increase the limits of liability for Coverages

A, B, C or D stated in the Declarations.

• $250 deductible applies, no other deductible applies to this coverage. This deductible does not apply with respect to Coverage D.

Utah – Home Program Coverages

Enumclaw Property and Casualty Insurance Company 24

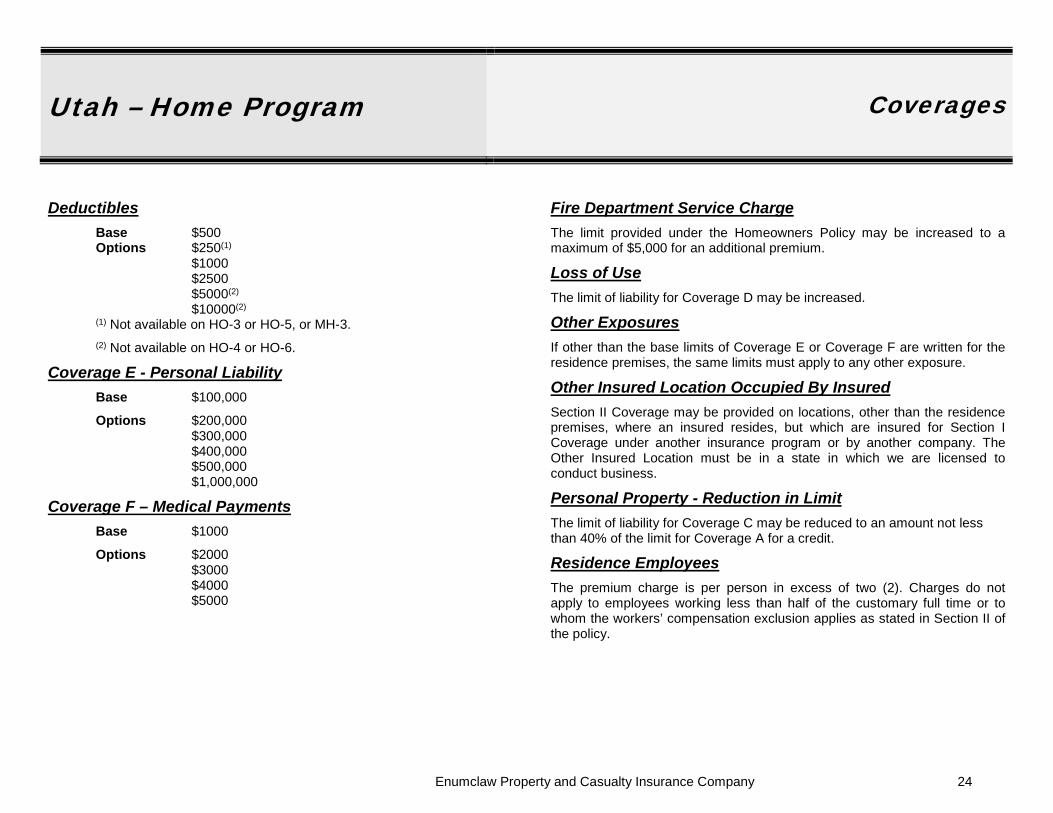

Deductibles Base $500 Options $250(1) $1000 $2500 $5000(2)

$10000(2) (1) Not available on HO-3 or HO-5, or MH-3.

(2) Not available on HO-4 or HO-6.

Coverage E - Personal Liability Base $100,000

Options $200,000 $300,000 $400,000 $500,000 $1,000,000

Coverage F – Medical Payments Base $1000

Options $2000 $3000 $4000 $5000

Fire Department Service Charge The limit provided under the Homeowners Policy may be increased to a maximum of $5,000 for an additional premium.

Loss of Use The limit of liability for Coverage D may be increased.

Other Exposures If other than the base limits of Coverage E or Coverage F are written for the residence premises, the same limits must apply to any other exposure.

Other Insured Location Occupied By Insured Section II Coverage may be provided on locations, other than the residence premises, where an insured resides, but which are insured for Section I Coverage under another insurance program or by another company. The Other Insured Location must be in a state in which we are licensed to conduct business. Personal Property - Reduction in Limit The limit of liability for Coverage C may be reduced to an amount not less than 40% of the limit for Coverage A for a credit.

Residence Employees The premium charge is per person in excess of two (2). Charges do not apply to employees working less than half of the customary full time or to whom the workers’ compensation exclusion applies as stated in Section II of the policy.

Utah – Home Program Coverages

Enumclaw Property and Casualty Insurance Company 25

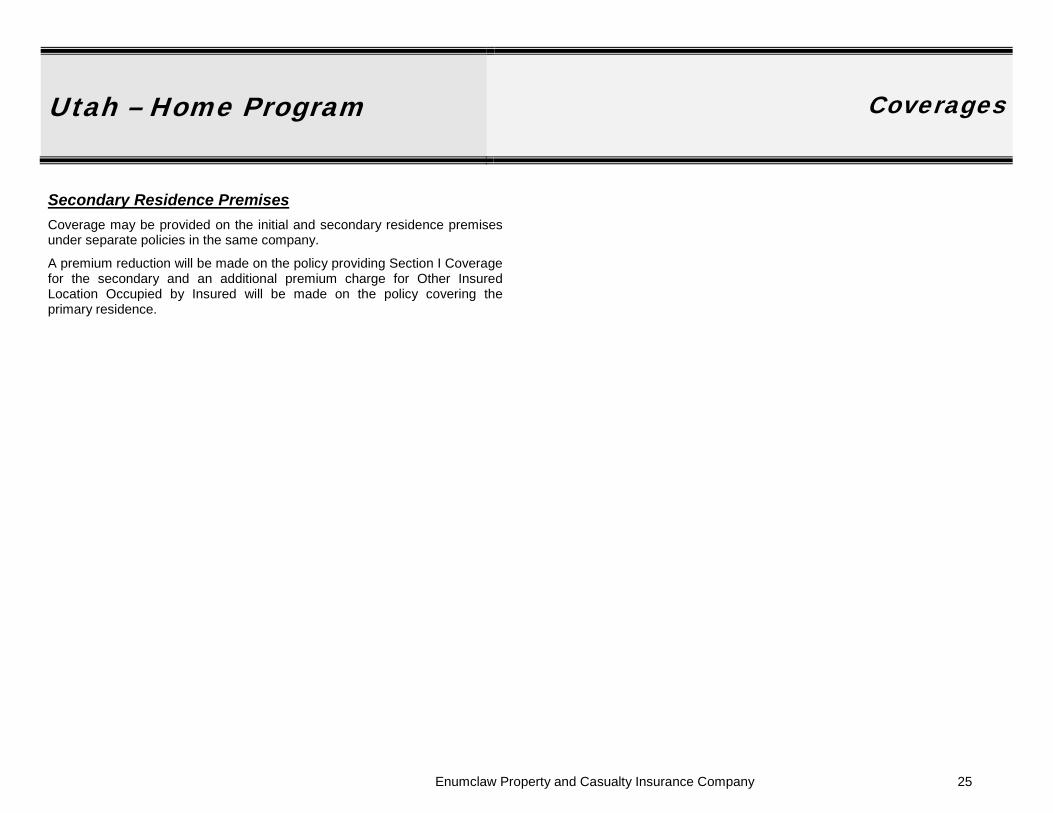

Secondary Residence Premises Coverage may be provided on the initial and secondary residence premises under separate policies in the same company.

A premium reduction will be made on the policy providing Section I Coverage for the secondary and an additional premium charge for Other Insured Location Occupied by Insured will be made on the policy covering the primary residence.

Utah – Home Program Discounts

Enumclaw Property and Casualty Insurance Company 26

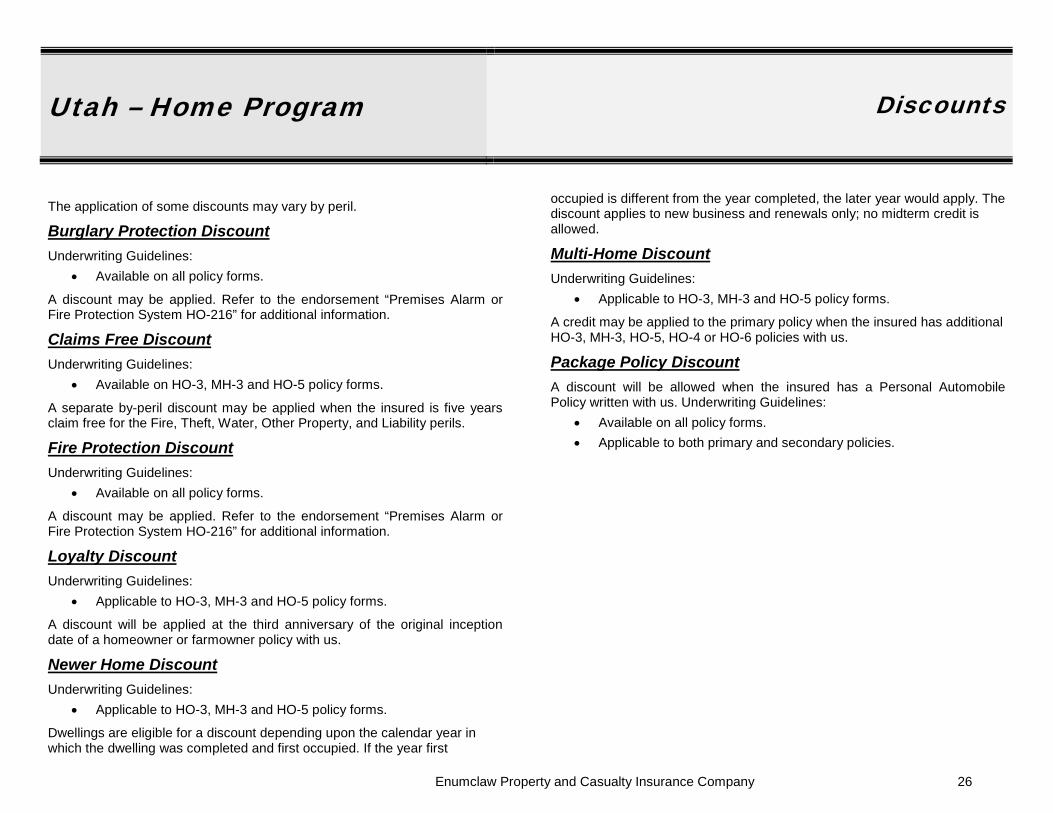

The application of some discounts may vary by peril.

Burglary Protection Discount Underwriting Guidelines:

• Available on all policy forms.

A discount may be applied. Refer to the endorsement “Premises Alarm or Fire Protection System HO-216” for additional information.

Claims Free Discount Underwriting Guidelines:

• Available on HO-3, MH-3 and HO-5 policy forms.

A separate by-peril discount may be applied when the insured is five years claim free for the Fire, Theft, Water, Other Property, and Liability perils.

Fire Protection Discount Underwriting Guidelines:

• Available on all policy forms.

A discount may be applied. Refer to the endorsement “Premises Alarm or Fire Protection System HO-216” for additional information.

Loyalty Discount Underwriting Guidelines:

• Applicable to HO-3, MH-3 and HO-5 policy forms.

A discount will be applied at the third anniversary of the original inception date of a homeowner or farmowner policy with us.

Newer Home Discount Underwriting Guidelines:

• Applicable to HO-3, MH-3 and HO-5 policy forms.

Dwellings are eligible for a discount depending upon the calendar year in which the dwelling was completed and first occupied. If the year first

occupied is different from the year completed, the later year would apply. The discount applies to new business and renewals only; no midterm credit is allowed. Multi-Home Discount Underwriting Guidelines:

• Applicable to HO-3, MH-3 and HO-5 policy forms.

A credit may be applied to the primary policy when the insured has additional HO-3, MH-3, HO-5, HO-4 or HO-6 policies with us.

Package Policy Discount A discount will be allowed when the insured has a Personal Automobile Policy written with us. Underwriting Guidelines:

• Available on all policy forms. • Applicable to both primary and secondary policies.

Utah – Home Program Additional Rating Elements HO-3, MH-3 and HO-5

Enumclaw Property and Casualty Insurance Company 27

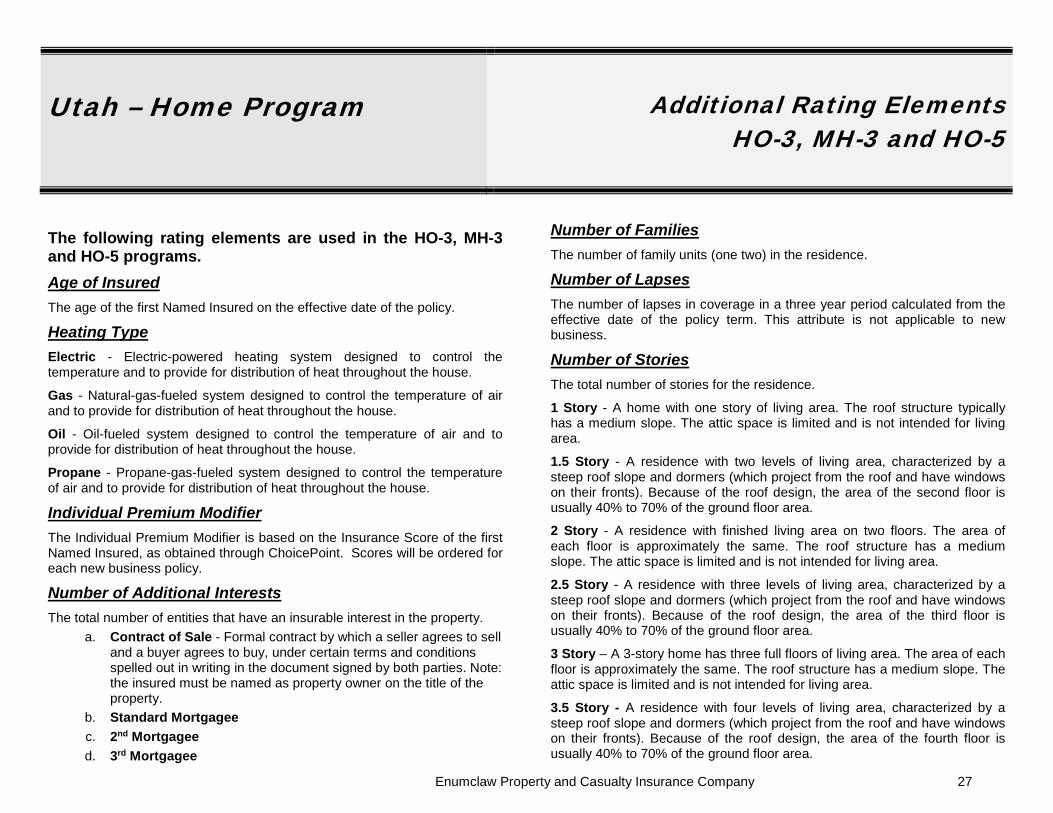

The following rating elements are used in the HO-3, MH-3 and HO-5 programs. Age of Insured

The age of the first Named Insured on the effective date of the policy.

Heating Type Electric - Electric-powered heating system designed to control the temperature and to provide for distribution of heat throughout the house.

Gas - Natural-gas-fueled system designed to control the temperature of air and to provide for distribution of heat throughout the house.

Oil - Oil-fueled system designed to control the temperature of air and to provide for distribution of heat throughout the house.

Propane - Propane-gas-fueled system designed to control the temperature of air and to provide for distribution of heat throughout the house.

Individual Premium Modifier The Individual Premium Modifier is based on the Insurance Score of the first Named Insured, as obtained through ChoicePoint. Scores will be ordered for each new business policy. Number of Additional Interests

The total number of entities that have an insurable interest in the property. a. Contract of Sale - Formal contract by which a seller agrees to sell

and a buyer agrees to buy, under certain terms and conditions spelled out in writing in the document signed by both parties. Note: the insured must be named as property owner on the title of the property.

b. Standard Mortgagee c. 2nd Mortgagee d. 3rd Mortgagee

Number of Families

The number of family units (one two) in the residence.

Number of Lapses The number of lapses in coverage in a three year period calculated from the effective date of the policy term. This attribute is not applicable to new business. Number of Stories

The total number of stories for the residence.

1 Story - A home with one story of living area. The roof structure typically has a medium slope. The attic space is limited and is not intended for living area.

1.5 Story - A residence with two levels of living area, characterized by a steep roof slope and dormers (which project from the roof and have windows on their fronts). Because of the roof design, the area of the second floor is usually 40% to 70% of the ground floor area.

2 Story - A residence with finished living area on two floors. The area of each floor is approximately the same. The roof structure has a medium slope. The attic space is limited and is not intended for living area.

2.5 Story - A residence with three levels of living area, characterized by a steep roof slope and dormers (which project from the roof and have windows on their fronts). Because of the roof design, the area of the third floor is usually 40% to 70% of the ground floor area.

3 Story – A 3-story home has three full floors of living area. The area of each floor is approximately the same. The roof structure has a medium slope. The attic space is limited and is not intended for living area.

3.5 Story - A residence with four levels of living area, characterized by a steep roof slope and dormers (which project from the roof and have windows on their fronts). Because of the roof design, the area of the fourth floor is usually 40% to 70% of the ground floor area.

Utah – Home Program Additional Rating Elements HO-3, MH-3 and HO-5

Enumclaw Property and Casualty Insurance Company 28

4 Story – A 4-story home has four full floors of living area. The area of each floor is approximately the same. The roof structure has a medium slope. The attic space is limited and is not intended for living area.

Bi-Level - A residence with two levels of living area, with the lower level being completely finished and normally partially below grade (with no basement below it). The entrance is a split-foyer entrance.

Tri-Level - A residence that is divided side to side, with three levels of finished living area: lower level, intermediate level and upper level. The lower level is immediately below the upper level as in a two-story residence. The intermediate level, adjacent to the other levels, is built on a grade approximately one-half story higher than the lower level. Split-level residences have a split roof design. Use the Back Split style for homes that are divided front to back.

Personal Status a. Married / Domestic Partners b. Single c. Widowed d. Divorced e. Separated

Roof Age Roof age is defined as age of roof at policy inception. It is then aged one year at renewal of the policy. The roof age may be updated if a total roof replacement has taken place.

Roof Type Built-Up/Tar and Gravel - Three to five layers of roofing felt laminated with coal tar, pitch or asphalt, and topped with a layer of gravel or other aggregate material. Typically found on flat or low-pitched roofs.

Clay Tile - A roof made from different types of clay and fired in kilns to dry.

Composition Single (Comp) - Shingles made of felt or inorganic fiberglass saturated with asphalt and surfaced with mineral granules. These may be made in individual strips, interlocking and self-sealing. Asphalt shingles are normally applied on medium pitched roofs over solid sheathing and building paper.

Concrete Tile - A thin piece of concrete made from Portland cement, fine aggregate, and pigments.

Copper - Sheets of 16 oz. copper connected with interlocking seams used to cover pitched roofs. The seams are either flat or raised.

Rubber - Roof covering using flexible elastomeric plastic/rubberized materials applied in rolls. The seams are vulcanized.

Slate - A dense, fine grained, metamorphic rock produced by the compression of various sediments, cut into thin tiles or slabs. Slate comes in any number of sizes, thicknesses and finishes.

Spanish Tile - Clay tiles that are S-shaped with interlocking sidelaps or side joints.

Steel - Corrugated steel sheets applied over a pitched roof.

Utah – Home Program Additional Rating Elements HO-3, MH-3 and HO-5

Enumclaw Property and Casualty Insurance Company 29

Tin - A thin gauge sheet of tin (terne) that is typically fastened with a standing seam system. Tin roofs are not to be confused with the steel roofs commonly found on pre-engineered structures.

Wood Shakes - Shakes split from a bolt of wood, generally in random dimensions. Wood shakes are normally installed over a pitched roof on spaced sheathing covered with building paper.

Wood Shingle - Overlapping, tapered pieces of wood, generally in random dimensions. Wood pine shingles are installed over a pitched roof on spaced sheathing covered with building paper.

Swimming Pool The presence of a swimming pool (above- or in-ground and larger than 6 ft in diameter and 3 ft deep), whether at the time of application or a subsequent installation, must be disclosed to the Company.

Total Living Area

The total living area is the size of the home (in square feet) based upon the exterior dimensions. This total should include the square footage of the main home as well as the square footage of the wing or addition if one has been specified. This does not include the area for built-in garages, basements, porches, breezeways, decks (which are included in Attached Structures), or one-story attached garages.

Woodstove

The presence of a woodstove, whether at the time of application or a subsequent installation, must be disclosed to the Company.

Utah – Home Program Forms and Endorsements List

Enumclaw Property and Casualty Insurance Company 30

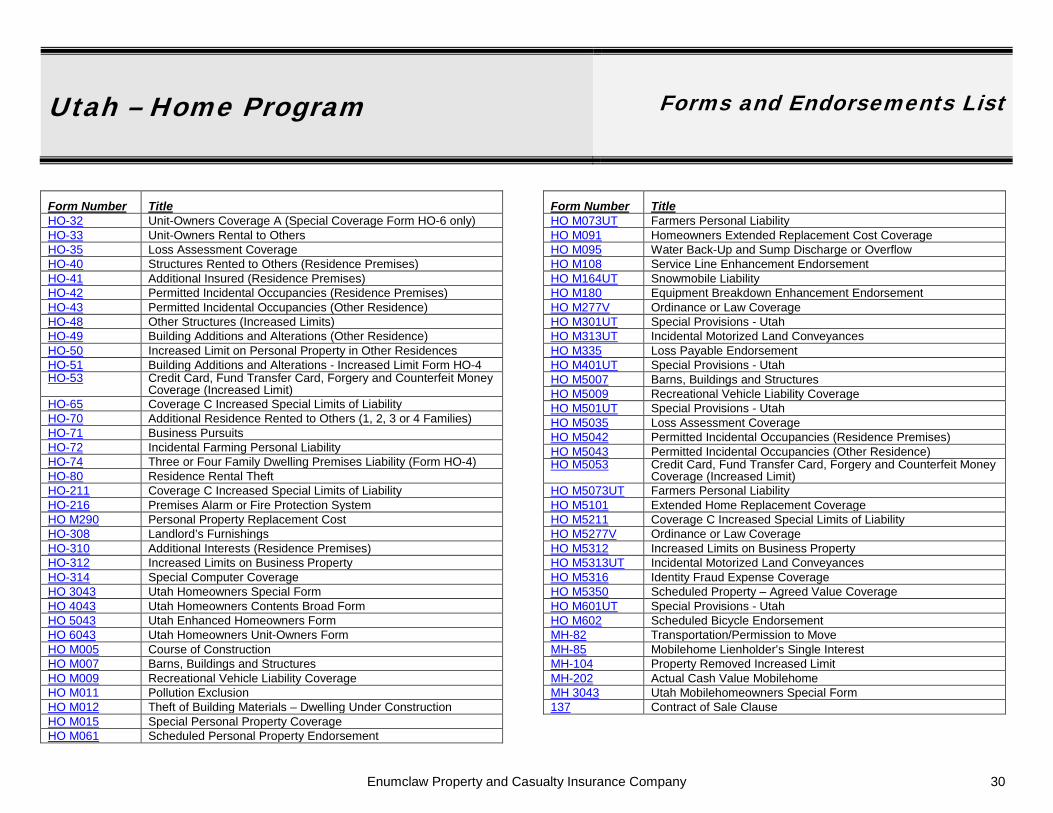

Form Number Title HO-32 Unit-Owners Coverage A (Special Coverage Form HO-6 only) HO-33 Unit-Owners Rental to Others HO-35 Loss Assessment Coverage HO-40 Structures Rented to Others (Residence Premises) HO-41 Additional Insured (Residence Premises) HO-42 Permitted Incidental Occupancies (Residence Premises) HO-43 Permitted Incidental Occupancies (Other Residence) HO-48 Other Structures (Increased Limits) HO-49 Building Additions and Alterations (Other Residence) HO-50 Increased Limit on Personal Property in Other Residences HO-51 Building Additions and Alterations - Increased Limit Form HO-4 HO-53 Credit Card, Fund Transfer Card, Forgery and Counterfeit Money

Coverage (Increased Limit) HO-65 Coverage C Increased Special Limits of Liability HO-70 Additional Residence Rented to Others (1, 2, 3 or 4 Families) HO-71 Business Pursuits HO-72 Incidental Farming Personal Liability HO-74 Three or Four Family Dwelling Premises Liability (Form HO-4) HO-80 Residence Rental Theft HO-211 Coverage C Increased Special Limits of Liability HO-216 Premises Alarm or Fire Protection System HO M290 Personal Property Replacement Cost HO-308 Landlord’s Furnishings HO-310 Additional Interests (Residence Premises) HO-312 Increased Limits on Business Property HO-314 Special Computer Coverage HO 3043 Utah Homeowners Special Form HO 4043 Utah Homeowners Contents Broad Form HO 5043 Utah Enhanced Homeowners Form HO 6043 Utah Homeowners Unit-Owners Form HO M005 Course of Construction HO M007 Barns, Buildings and Structures HO M009 Recreational Vehicle Liability Coverage HO M011 Pollution Exclusion HO M012 Theft of Building Materials – Dwelling Under Construction HO M015 Special Personal Property Coverage HO M061 Scheduled Personal Property Endorsement

Form Number Title HO M073UT Farmers Personal Liability HO M091 Homeowners Extended Replacement Cost Coverage HO M095 Water Back-Up and Sump Discharge or Overflow HO M108 Service Line Enhancement Endorsement HO M164UT Snowmobile Liability HO M180 Equipment Breakdown Enhancement Endorsement HO M277V Ordinance or Law Coverage HO M301UT Special Provisions - Utah HO M313UT Incidental Motorized Land Conveyances HO M335 Loss Payable Endorsement HO M401UT Special Provisions - Utah HO M5007 Barns, Buildings and Structures HO M5009 Recreational Vehicle Liability Coverage HO M501UT Special Provisions - Utah HO M5035 Loss Assessment Coverage HO M5042 Permitted Incidental Occupancies (Residence Premises) HO M5043 Permitted Incidental Occupancies (Other Residence) HO M5053 Credit Card, Fund Transfer Card, Forgery and Counterfeit Money

Coverage (Increased Limit) HO M5073UT Farmers Personal Liability HO M5101 Extended Home Replacement Coverage HO M5211 Coverage C Increased Special Limits of Liability HO M5277V Ordinance or Law Coverage HO M5312 Increased Limits on Business Property HO M5313UT Incidental Motorized Land Conveyances HO M5316 Identity Fraud Expense Coverage HO M5350 Scheduled Property – Agreed Value Coverage HO M601UT Special Provisions - Utah HO M602 Scheduled Bicycle Endorsement MH-82 Transportation/Permission to Move MH-85 Mobilehome Lienholder’s Single Interest MH-104 Property Removed Increased Limit MH-202 Actual Cash Value Mobilehome MH 3043 Utah Mobilehomeowners Special Form 137 Contract of Sale Clause

![2011 Burglary Report [infographic]](https://img.pdfslide.us/doc/110x75/568c48d41a28ab491691bd6e/2011-burglary-report-infographic.jpg)