Embed Size (px)

Citation preview

Tinker, 2015EIA Energy ConferenceJune, 2015

EIA Energy ConferenceJune, 2015

Shale Gas Plays Inevitable Updates

Bureau of Economic GeologyUniversity of Texas at Austin

Tinker, 2015Acknowledgements and DisclosuresAcknowledgements and Disclosures Alfred P. Sloan Foundation IHS and DrillingInfo EIA BHP, ExxonMobil, Southwestern Energy, Devon, Range Resources,

Cimarex, Carrizo for discussions---------------------------------------- Potential conflicts of interest have been fully disclosed: see BEG

website Publications and Press:

Several peer-reviewed journal articles – see BEG website Oil and Gas Journal Articles – Barnett and Fayetteville Mainstream Media including NPR, WSJ and many others

Tinker, 2015

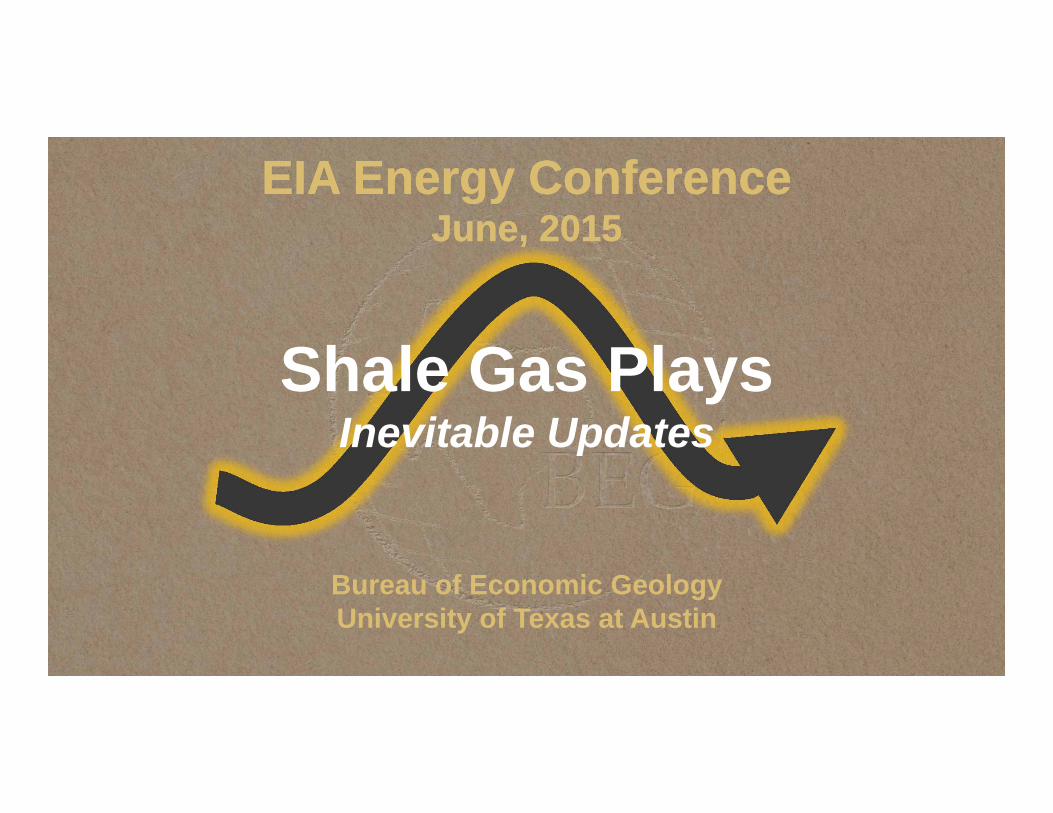

Interdisciplinary approachWell Economics

Results by tier: Breakeven prices and profitability index as a function of completion

Production OutlookResults by tier : Pace of drilling with respect to economic, technical, policy assumptions

Geologic AnalysisResults: geologic

characteristics per mi2, incl. OGIP map

Decline AnalysisResults: Well declines, incl. expected recovery

(EURs)

Productivity Analysis

Results: Productivity functions and

expected productivity“tier”map, inventory of

future wells.

Tinker, 2015

State-of-art BEG outlooks have done well so far But some of the observe changes in producer

behavior are not covered by the models We get access to more data We keep learning from every new play => Need to enhance our approaches

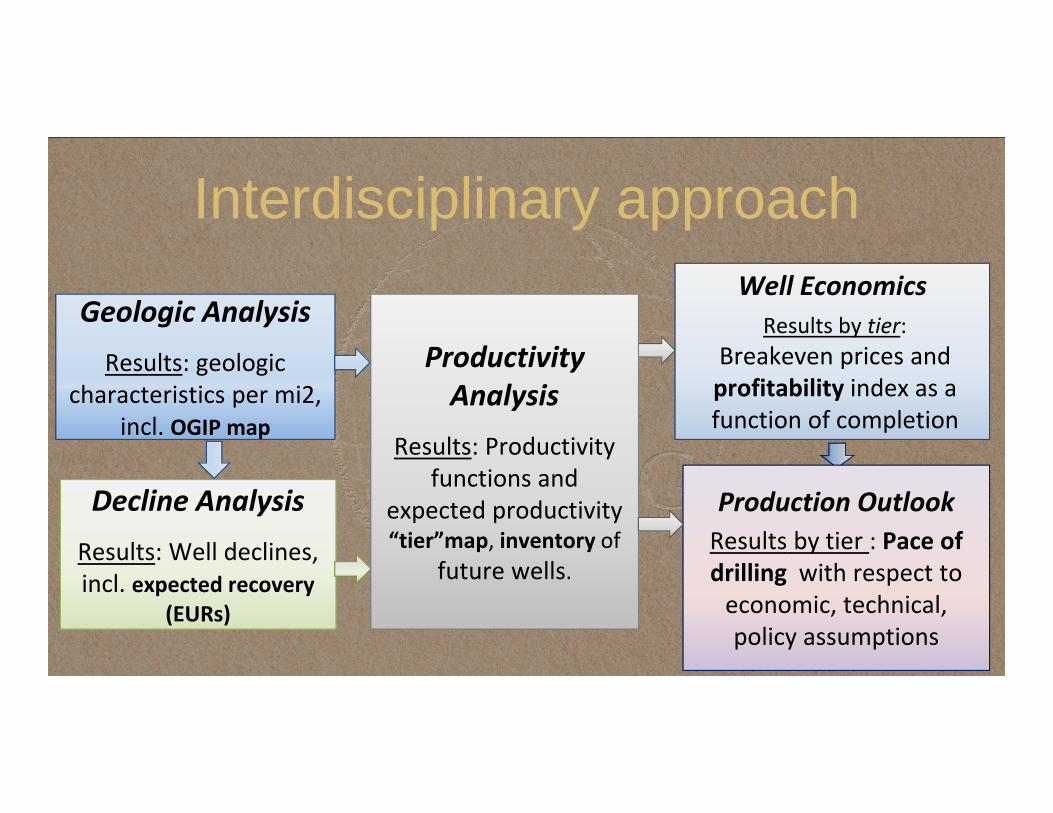

Tinker, 2015Barnett Shale: Price sensitivity

0

0.5

1

1.5

2

2.5

2005 2010 2015 2020 2025 2030 2035 2040 2045

Tcf/

year

$6 HH EIA AEO14$4 HH $3 HH

Total: 44-47 Tcf

Tinker, 2015

How to treat Resource compositionthat affects economics

Barnett ShaleOGIPfree (productivity limit ) Productivity

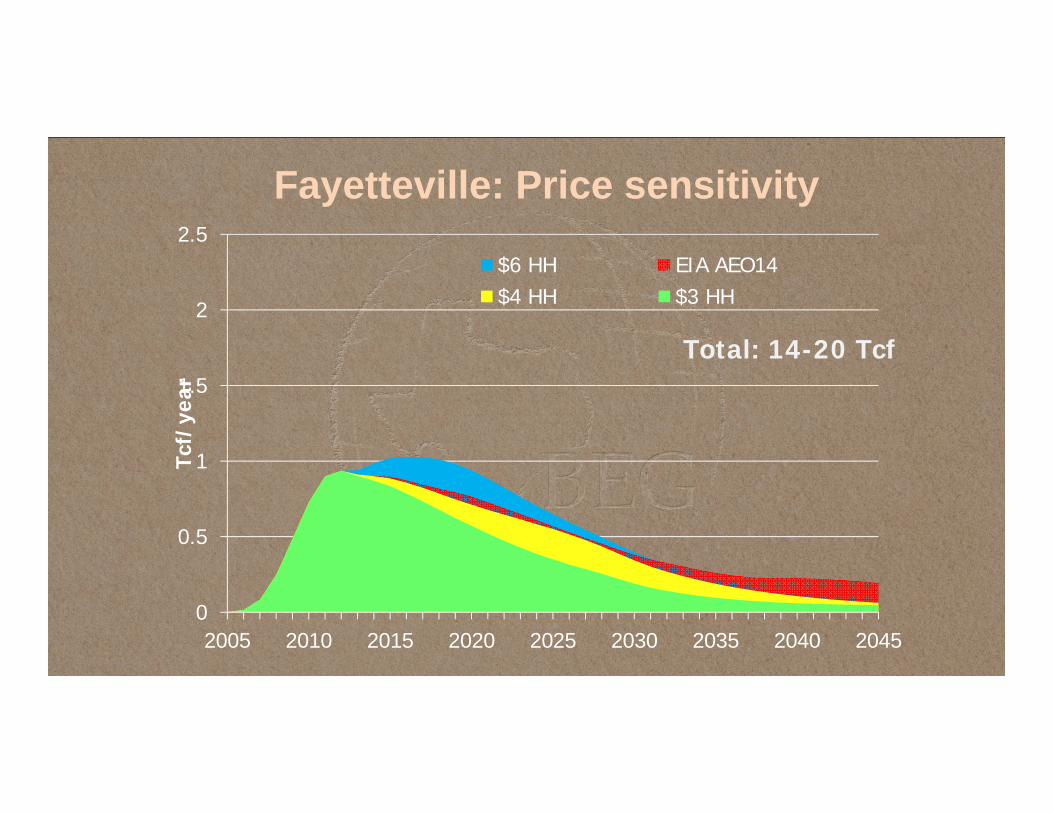

Tinker, 2015Fayetteville: Price sensitivity

0

0.5

1

1.5

2

2.5

2005 2010 2015 2020 2025 2030 2035 2040 2045

Tcf/

year

$6 HH EIA AEO14$4 HH $3 HH

Total: 14-20 Tcf

Tinker, 2015

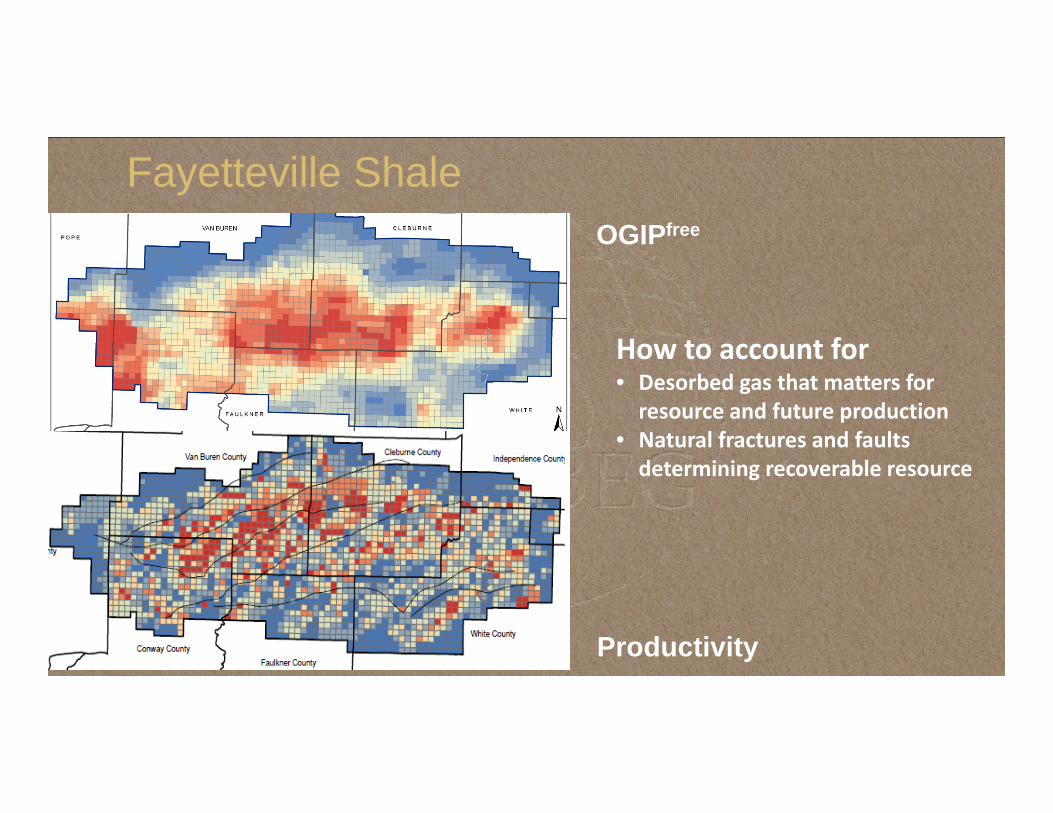

How to account for• Desorbed gas that matters for resource and future production

• Natural fractures and faults determining recoverable resource

Fayetteville ShaleOGIPfree

Productivity

Tinker, 2015Haynesville Shale: Most expensive

0

0.5

1

1.5

2

2.5

2005 2010 2015 2020 2025 2030 2035 2040 2045

Tcf/

year

$6 HH EIA AEO14$4 HH $3 HH

Total: 36-57 Tcf

Tinker, 2015

How to capture• Pressure gradient (extreme values lead to dynamic permeability)

• Clay effect• Potential contributions from adjacent formations

Haynesville ShaleOGIPfree Productivity

Tinker, 2015

Need for Updates Improved geologic knowledge Updates in decline analysis Revised analysis of productivity drivers (structural

changes) Changes in well economics: cost structure and

finances Production incentives w.r.t. new constraints

Tinker, 2015

GEOLOGIC UPDATES:

1. Improved granularity (on characterization)2. Better understanding (of data and features)3. Knowledge expansion (reinterpretation of existing and usage of new data)

GEOLOGIC UPDATES:

1. Improved granularity (on characterization)2. Better understanding (of data and features)3. Knowledge expansion (reinterpretation of existing and usage of new data)

Tinker, 2015

~46,000 square miles

Minimum depth 2000’

Minimum thickness 30’

Outcrop +5 miles Maximum thermal

maturity 3.5% Ro

Marcellus Play

Boundary

Marcellus Play

Boundary

Tinker, 2015

Summary Heterogeneity across plays makes us learn more

about shale geology New data and technological advances lead to

continuous updates Expansion of drilling activity changes

uncertainties Changes in economic environment translate into

improved granularity

Tinker, 2015

WELL PRODUCTIVITY, RECOVERY, TECHNOLOGY, AND STRATEGY:

1. Improved granularity (on characterization)2. Better understanding (of data and features)3. Knowledge expansion (reinterpretation of existing and usage of new data)

WELL PRODUCTIVITY, RECOVERY, TECHNOLOGY, AND STRATEGY:

1. Improved granularity (on characterization)2. Better understanding (of data and features)3. Knowledge expansion (reinterpretation of existing and usage of new data)

Tinker, 2015

Decline Analysis

-- -- -- Estimated decline function • Production decline is a function of geological rock properties;

• Expected production, however, is a function of completion design, geologic and company parameters.

=> Standard well approach, or well normalization, cannot be used

=> Technology and economics determine the productivity along with geology

Tinker, 2015

OGIP vs. EUR Correlation

0

5

10

15

20

25

30

25 35 45 55 65 75 85 95 105 115 125 135

Leng

th n

orm

aliz

ed E

UR

(B

cf)

OGIP Bins, Bcf/mi2

Need to understand production variability and reduce uncertainty

Tinker, 2015

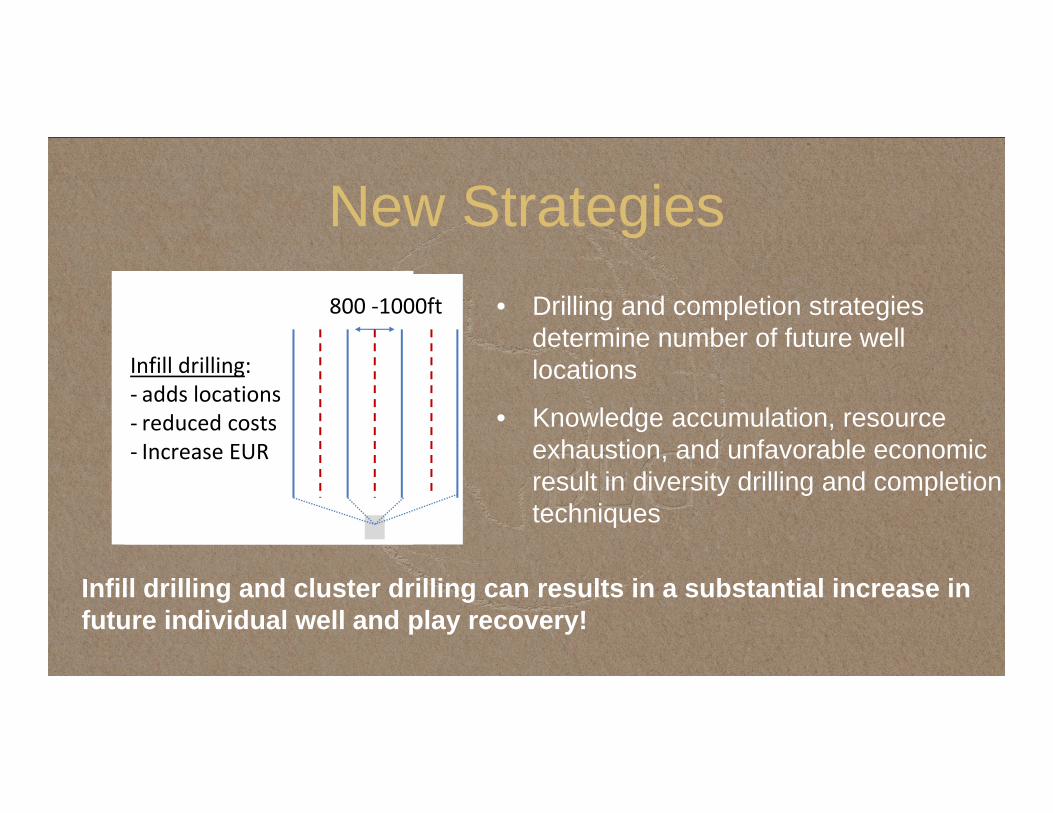

New Strategies• Drilling and completion strategies

determine number of future well locations

• Knowledge accumulation, resource exhaustion, and unfavorable economic result in diversity drilling and completion techniques

Infill drilling and cluster drilling can results in a substantial increase in future individual well and play recovery!

1000ft

Cluster drilling:‐ tighter spacing‐ less water‐ lower costs‐more wells/pad

Infill drilling:‐ adds locations‐ reduced costs‐ Increase EUR

800 ‐1000ft

Tinker, 2015

Completions and Experience matter

‐4

‐2

0

2

4

6

8

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49

average well EUR for a

given

region

(Bcf)

Prefered completion Standardized well

Economic region

Tinker, 2015

WELL ECONOMICS AND PLAY OUTLOOK:

1. Models expand to account for new trends and practices2. Outlooks improve when tested parameters are well defined and mutually consistent

Tinker, 2015

Inventory w.r.t. Producers’ Decisions

Number of locations & productivity depend on completions (HF water, spacing)

Completion choice depends on the market environment and technology

Tinker, 2015

Conclusion Changes in any aspect of play description leads to a

review of all the parts of the analysis

The outlooks results keep changing with: Price (NG/NGL/WTI) ,

Basis differential/Infrastructure,

Costs & Technology improvement;

Regulatory framework.

But resource in place may not by fully known yet.