Embed Size (px)

Citation preview

Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 3(4):354-360 (ISSN:2141-7024)

354

Budgetary Process and Organizational Performance of Apparel

Industry in Sri Lanka

1L.M.D. Silva and 2Ariyarathna Jayamaha

1University of Kelaniya, Sri Lanka. 2Department of Accountancy, University of Kelaniya, Sri Lanka.

Corresponding Author: L.M.D. Silva ___________________________________________________________________________ Abstract The budgetary process has been a part of management control system of the organization. This process encourages managers to plan, consider the stakeholders involved, provides information for improved decision making, increases and enhances communication and coordination among departments, and for evaluation. This paper seeks to evaluate budgetary process of apparel industry in Sri Lanka (BPA) and see whether budgetary process has significant impact on performance of such industry. The budgetary process of apparel industry was assessed by using variables such as planning, coordination, control, communication and evaluation. The performance of apparel industry in Sri Lanka was examined by using Return on Assets. Based on the data extracted from apparel industry’s financial statements, correlation coefficients and regression analysis showed that budgetary process have significant associations with the organizational performance of apparel industry in Sri Lanka. This confirms that efficient apparel companies maintain sound budgetary process which contributes to higher levels of organizational performance. _________________________________________________________________________________________ Keywords: budgetary process; organizational performance; apparel industry. _________________________________________________________________________________________INTRODUCTION Accounting is the process of identifying, measuring, accumulating, analyzing, preparation, interpreting and communicating information that helps managers fulfills organizational objectives (Horngren, Sundem and Stratton, 2001). An important component of the accounting system is the management accounting system which makes information available to managers, assisting them in decisions such as planning, organizing, and control and coordinating activities within their authority. An important component of the management accounting system in organization is the budgeting system which is essential part of above activities involve the budgetary process (Seaman, Landry Jr, Williams, 2011). Budget, a short term finance planning tool of management, is used to focus attention on company’s’ finance and overall operations of an organization. Budget highlights potential problems and advantages early, allowing management to take steps to avoid these problems or use the advantages wisely a budget is a tool that helps managers in both their planning and control. Budget can be used as a benchmark as a control system, that allows managers to compare actual performance with estimated or desired performance. Hence, the budget widely used as a managerial technique tool in an organization (Horngren, Sundem and Stratton, 2001). Many researchers highlight that effective contribution of budgetary process such helps to improve the overall

performance of the organization. Over time, several studies provide critical evaluations of different aspects of this contingency literature on budgeting and organizational performance (Omolehinwa, 1989; Abdulla, 1998; Hartmann & Moers, 1999; Raili, 2000; Otley, 2001; Welmilla, 2001;Hartmann & Moers, 2003; Hansen, Otley& Van der Stede, 2003;Gustafsson&Parsson, 2010; Caleb, 2011; Collins; 2011). According to Hansen and Van der Stede (2004), there are four potential reasons for budgeting in organizations, operational planning, performance evaluation, communication of goals, and strategy formation. The budget arises in different circumstances and that performance is associated with different budgeting characteristics. LITERATURE REVIEW Apparel Industry Apparel industry becomes Sri Lanka’s largest export industry since 1986(Dheerasena, 2009).In 1992 under garment factory programme, the garment industry had become the largest foreign exchange earner in the country overtaking the tea industry. Apparel industry in Sri Lanka provides better contribution to the Sri Lanka economy (Central bank 2010). Central bank (2010) further reports that the GDP contribution of Apparel industry in Sri Lanka for 2009 is Rs. 376 million and 2010 is Rs. 395 million. The apparel industry is identified as a buyer driven value chain that contains three types of lead firms: retailers, marketers and branded manufacturers (Dias, 2009). The apparel industry of Sri Lanka which producing

Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 3(4): 354-360 © Scholarlink Research Institute Journals, 2012 (ISSN: 2141-7024) jetems.scholarlinkresearch.org

Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 3(4):354-360 (ISSN:2141-7024)

355

high quality readymade garments and the main exporters are USA and Europe. The apparel sector generates nearly 45% of the country’s export earnings. The sector provides direct employment to over 350,000 people and extends its benefits to over a million and keeps the rural economies alive (Chow 2011). Sri Lankan apparel industry is the major export income earner and contributes to the live hood for over 1.2 million people (Perera, 2009). The growth of Sri Lankan garment industry as a manufacturing sub-sector has been remarkable in terms of its contribution to GDP, exports, foreign exchange earnings and employment generation (Thilakaratne, 2006). The most Sri Lankan apparel industries feel comfortable having their own system and the very little data maintained. It is the problems that are created due to unplanned buildings and system and large amounts of labour, staff and equipment used probably to duplicate or triplicate the same function many times. There should be proper system for distribution and faster purchasing patterns at the lowest cost and fastest rotate times to fulfill orders (Masakorala, 2010). Therefore, apparel industry in Sri Lanka needs to have a better management control systems to set of organizational activities to face the global challenge and sustain the apparel industry in Sri Lanka. Further, needs to decision making as well as enhancing the efficient and effective use of the organizational resources towards the achievement of the organizational objectives as well as counties objective. Budgetary Process Hilton, (1997cited in Abdullah, 1998, p.1) defines budget 'as a detailed plan, expressed in quantitative terms, that specifies how resources will be acquired and used during a specified period of time'. The budget is prepared for the primary purposes of planning, facilitating communication, coordination, allocating resources, control profits and operations, evaluating performance and providing incentives. According to Gustafsson and Parsson (2010), the budget has in the past had a control function, however today there are several objectives and purposes of the budget and the purposes vary among organizations. Budgeting in this regard is viewed as enabling the different functions of management control further, state that the budget represents their numbers and their benchmarks against which their performance is measured (Herath and Indrani, 2007). The budget process itself that identifying and understanding the motivational factors. Budget process enhance individual performance to achieve budget goals which granted by the organization through organization planning process. Those goals must be practical within the budget process (Otley, 1978).According to McBain (1999 cited in Akintoye,

2008, p. 9), budgeting is not a substitute for effective decision making. The managers’ planning tool, budgeting is also one of the most effective tools of communication and integration. GFOA (1998, p. 4) states that, “The mission of the budget process is to help decision makers make informed choices for the provision of services and capital assets and to promote stakeholder participation in the Decision process”. According to Dugdale and Lyne 2010, budgets tend to become more important for control, not for planning. Conversely, budgets become less important for control but more important for planning in a more uncertain environment. In addition, budgeting has been integrated with non-financial measures in general and the balanced scorecard in particular. The accounting system of the operation provides information on what has happened in the past and helps mangers to keep track of whether or not they are meeting their current budgets. Budgets are therefore an expectation of what a manager agrees is achievable within the immediate future and are mostly expressed in financial terms (The Institute of working future, 2011, p.3-5).According to Marginson and Sharma (2011), the budgetary practices and procedures encountered may be unique to that organization. They mention that insights into the connections and interdependencies between budgeting and strategizing in day today activities within an organization. It appears that many aspects of the budgetary process, particularly budget implementation and budgetary control in general, may differ from accepted view as firms design strategic objectives from budgetary information whilst simultaneously engaging in budgeting activities as strategies are developed. In these circumstances budgets may be used as a reflection of the performance of those responsible for specific areas of the operation. The budget process must be undertaken with the full cooperation of managers who understand the budgeting process. Budgets should produce figures that represent expected performance under current operational conditions (The Institute of Working Future, 2011, p.3-5). Budgetary Process and Organization performance Omolehinwa (1989) defined a budget as a plan of dominant individuals in an organization expressed in monetary terms and indicate how the available resources may be utilized, to achieve whatever the dominant individuals agreed to be the organization’s priorities. Abdullah (1998) mentions that Budgeting processing interaction with superior has significant relationship to performance goals of the cost centre managers of the institute. According to Hoper and Fisher (2003, p.4), Budgeting is not so much as a financial plan but as the performance management process that leads to and executes that plan. So budget is entire performance management process.

Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 3(4):354-360 (ISSN:2141-7024)

356

This process is about agreeing upon and coordinating targets, rewards, action plans, and resources for the year ahead, and then measuring and Control performance against that agreement. According to Cieslack and Kalling (2007), the inability of rational annual budgetary control to new management control system is required due to new operating conditions for companies caused by the pressure of global competition and constantly changing environment. The rolling budget is allowing assessment of the strategy and resource allocation, coordination and communication learning and strategy creation, performance evaluation and motivation, mainly through reward systems based on budgeting. The wider control framework embraces informal controls and other formal controls. According to John and Ngoasong (2008), the practices of integrating strategic management and budgeting which enables it to be competitive and increase organizational performance. Budget facilitates the creating and sustaining of competitive advantage in the following management functions: forecasting and planning; communication and coordination; motivational device; evaluation and control; and decision making. Qi (2010) mentions that the selected budgetary planning, budgetary control, budgetary sophistication, budgetary participation, budget goal clarity and budget goal difficulty as variables are impact of the budgetary process and organizational performance of SME’s in China. Drury (2004, p.170) states budgetary planning and control are typically more complex in the business firm. There should be five main functions for budget, system of authorization, means of forecasting and planning, channel of communication and coordination, motivational device, and means of performance evaluation and control, as well as of providing a basis for decision making. Blumentritt (2006) note the budgeting provides information on funding and accountability. If apply properly, both processes improve an organization’s ability to create and sustain superior performance. The budgeting and strategic management might be put in practice properly and has the best impact on firm performance. Raili (2000) argues that budget related behaviors of managers are very important for the organizational performance. Therefore, by reviewing above literature in this research were selected five independent variables to measure the budgetary process. Five independent variables are budgetary planning, coordination, Control, communication and evaluation to measure budgetary process of Sri Lankan Apparel Industry. Therefore, a question arises with respect to the identification whether the Sri Lanka apparel industry follow sound budgetary process and is there any impact of performance of the

organization. The following hypotheses are formulated. H1: There is a sound budgetary process in Sri Lankan

apparel Industry. H2:There is a positive relationship between

budgetary process and organizational performance.

METHODOLOGY Five point Likert Scale is used to measure budgetary process of the company. Evaluate budgetary process by using descriptive statistical method (use mean value of budgetary process as measurement technique). In this study, ROA is used to measure the performances of the company for past three years as a performance indicator. Return on assets is a financial ratio which allows the observer to make some determination of the organizations financial performance relative to the assets which are at the firm’s disposal (Richard, Alan and Stwaart, 2004). Sample and Data In this research 50 companies are selected based on convenient judgment sampling method from 513companies in Sri Lankan apparel industry. 228managers were completed the questionnaire. Primary and secondary data were used for this study. Primary data received from the questionnaire and interviews through financial controllers, accountants, financial managers, financial directors, production managers, marketing managers and HR managers. Secondary data were collected from financial statement, publications, such as books, research papers, articles, published case studies and websites. EMPIRICAL RESULTS Budgetary Process Descriptive statistical method was used to analyze the respondent’s data to evaluate the budgetary processes of the selected companies. Table 1 illustrates the descriptive statistics of budgetary process with five variables. \ Table 1: Descriptive Statistics of Budgeting Process

Category N Minimum Maximum Mean

Std. Deviation Variance

Budgetary Planning

50 2.92 4.75 4.09 .51621 .266

Budgetary Coordination

50 2.25 5.00 4.01 .63593 .404

Budgetary Control 50 3.00 5.00 4.06 .56872 .323

Budgetary Communication

50 2.30 4.87 4.01 .55815 .312

Budgetary Evaluation

50 1.67 5.00 3.50 .68344 .467

Budgetary Process 50 2.94 4.61 3.9342 .45064 .203

As shown in Table 1, the minimum and maximum value range were used to classify different levels of the budget planning, budgetary coordination, budgetary control, budgetary communication,

Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 3(4):354-360 (ISSN:2141-7024)

357

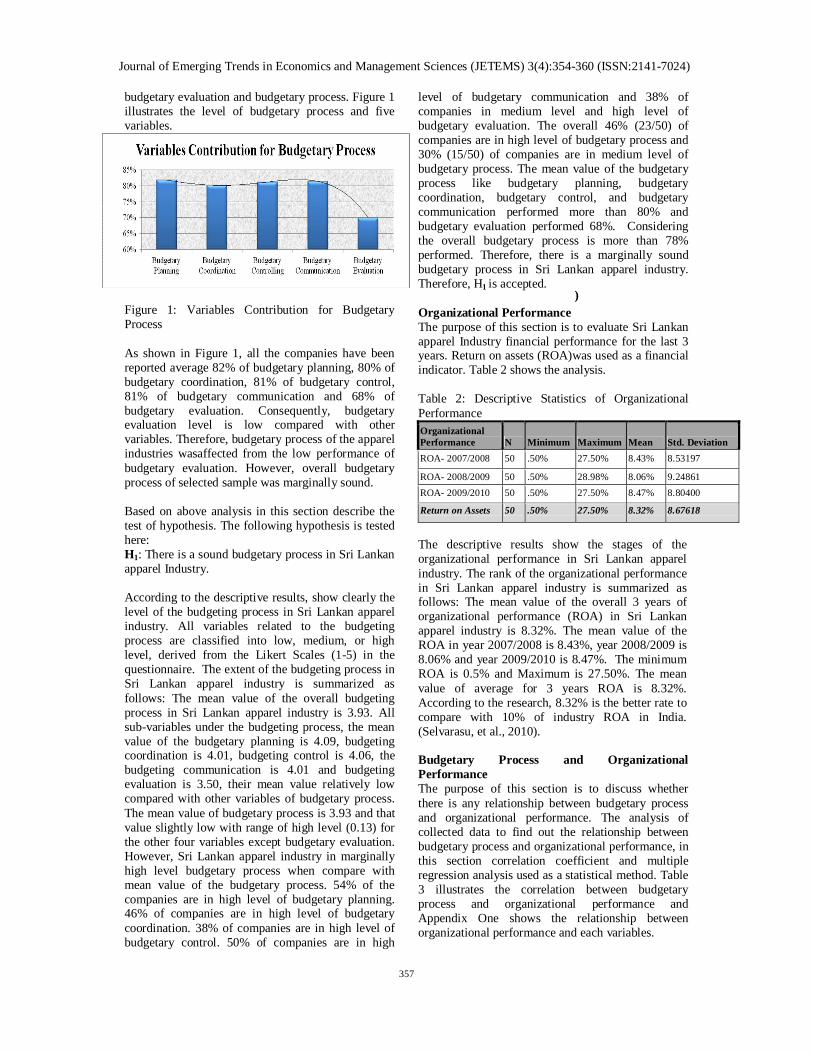

budgetary evaluation and budgetary process. Figure 1 illustrates the level of budgetary process and five variables.

)

Figure 1: Variables Contribution for Budgetary Process As shown in Figure 1, all the companies have been reported average 82% of budgetary planning, 80% of budgetary coordination, 81% of budgetary control, 81% of budgetary communication and 68% of budgetary evaluation. Consequently, budgetary evaluation level is low compared with other variables. Therefore, budgetary process of the apparel industries wasaffected from the low performance of budgetary evaluation. However, overall budgetary process of selected sample was marginally sound. Based on above analysis in this section describe the test of hypothesis. The following hypothesis is tested here: H1: There is a sound budgetary process in Sri Lankan apparel Industry. According to the descriptive results, show clearly the level of the budgeting process in Sri Lankan apparel industry. All variables related to the budgeting process are classified into low, medium, or high level, derived from the Likert Scales (1-5) in the questionnaire. The extent of the budgeting process in Sri Lankan apparel industry is summarized as follows: The mean value of the overall budgeting process in Sri Lankan apparel industry is 3.93. All sub-variables under the budgeting process, the mean value of the budgetary planning is 4.09, budgeting coordination is 4.01, budgeting control is 4.06, the budgeting communication is 4.01 and budgeting evaluation is 3.50, their mean value relatively low compared with other variables of budgetary process. The mean value of budgetary process is 3.93 and that value slightly low with range of high level (0.13) for the other four variables except budgetary evaluation. However, Sri Lankan apparel industry in marginally high level budgetary process when compare with mean value of the budgetary process. 54% of the companies are in high level of budgetary planning. 46% of companies are in high level of budgetary coordination. 38% of companies are in high level of budgetary control. 50% of companies are in high

level of budgetary communication and 38% of companies in medium level and high level of budgetary evaluation. The overall 46% (23/50) of companies are in high level of budgetary process and 30% (15/50) of companies are in medium level of budgetary process. The mean value of the budgetary process like budgetary planning, budgetary coordination, budgetary control, and budgetary communication performed more than 80% and budgetary evaluation performed 68%. Considering the overall budgetary process is more than 78% performed. Therefore, there is a marginally sound budgetary process in Sri Lankan apparel industry. Therefore, H1 is accepted. Organizational Performance The purpose of this section is to evaluate Sri Lankan apparel Industry financial performance for the last 3 years. Return on assets (ROA)was used as a financial indicator. Table 2 shows the analysis. Table 2: Descriptive Statistics of Organizational Performance Organizational Performance N Minimum Maximum Mean Std. Deviation ROA- 2007/2008 50 .50% 27.50% 8.43% 8.53197

ROA- 2008/2009 50 .50% 28.98% 8.06% 9.24861 ROA- 2009/2010 50 .50% 27.50% 8.47% 8.80400

Return on Assets 50 .50% 27.50% 8.32% 8.67618

The descriptive results show the stages of the organizational performance in Sri Lankan apparel industry. The rank of the organizational performance in Sri Lankan apparel industry is summarized as follows: The mean value of the overall 3 years of organizational performance (ROA) in Sri Lankan apparel industry is 8.32%. The mean value of the ROA in year 2007/2008 is 8.43%, year 2008/2009 is 8.06% and year 2009/2010 is 8.47%. The minimum ROA is 0.5% and Maximum is 27.50%. The mean value of average for 3 years ROA is 8.32%. According to the research, 8.32% is the better rate to compare with 10% of industry ROA in India. (Selvarasu, et al., 2010). Budgetary Process and Organizational Performance The purpose of this section is to discuss whether there is any relationship between budgetary process and organizational performance. The analysis of collected data to find out the relationship between budgetary process and organizational performance, in this section correlation coefficient and multiple regression analysis used as a statistical method. Table 3 illustrates the correlation between budgetary process and organizational performance and Appendix One shows the relationship between organizational performance and each variables.

Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 3(4):354-360 (ISSN:2141-7024)

358

Table 3: Correlation between Budgetary Process and Organizational Performance Planning Coordination Control Communication Evaluation Budgetary Process ROA Spearman's rho .732** .809** .715** .823** .341* .866**

Sig. (2-tailed) .000 .000 .000 .000 0.016 .000

N 50 50 50 50 50 50

*. Correlation is significant at the 0.05 level (2-tailed). **. Correlation is significant at the 0.01 level (2-tailed). As shown in Table 3, The Significant level (p-value) of these test, not exceeds alpha (p<0.05and p<.01), it is statistically significant. Almost all of the variables indicated high correlations except budgetary evaluation. In regard to the organizational performance (ROA) is high degree of positively significant correlated with budgetary planning (r = 0.732, p= .000), budgetary coordination (r = 0.809, p= .000), budgetary control (r = 0.715, p= .000), budgetary communication (r = 0.823, p=.000) and low degree of positively significant correlated with budgetary evaluation (r = 0.341, p= .016). Further, overall correlation coefficient results show that the organizational performance is positively significant correlated with budgetary process of the company (r = 0.866, p= .000). Based on the above analysis and explanations, in this section describe the test of hypothesis. The following hypothesis is tested here: H2: There is a positive relationship between budgetary process and organizational performance. Table 4: Regression Model for Budgetary Process and Organizational Performance

Model R R Square Adjusted R Square Std. Error of the Estimate

1 .880a .774 .748 .77001

a. Predictors: (Constant), Mean Score - Evaluation, Coordination, Control, Communication, Planning Based on the analysis of Table 4, a regression analysis, predicting organizational performances from budgetary process of the organization is statistically significant. R square, 77.4% means the budgetary process strongly effect to the organizational performance and budgetary process of the company explained 77.4% of organizational performance in Sri Lankan apparel industry. According to the Table 3, the budgetary communication is higher correlation with organizational performance than other factors. In this research budgetary communication plays an important role by improving the organizational performance of the apparel industry. Organization performance is also influenced by another budgetary practice namely budgetary coordination. The next factor that contributes to the performance of an

organization is budgetary planning. Organization performance is also influenced by another budgetary practice namely budgetary control. The last variable that predicts the performance of an organization is budgetary evaluation. Budgetary evaluation did not much influence the organizational performance compare with other variables. Overall all five variables were showed strong positive correlation with organizational performance. Therefore, budgetary process is an important factor to predict the organizational performance, as it has shown in R square of 77.4%. That means budgetary process predicts 77.4% of organizational performance of apparel industry in Sri Lanka. This analysis was clearly explained that there is a positive relationship with budgetary process and organizational performance. The higher the budgetary process, higher the organizational performance. Therefore, H2 is accepted. CONCLUSION There are small, medium and large - sized companies in Sri Lankan apparel industry. A majority of the companies are private limited companies. Sri Lankan Apparel industry makes up a significant portion of GDP and employment. Apparel industry is the second largest industry in Sri Lanka. Sri Lanka depends on a strong global economy for investment and expansion of its export base. This study examined how budgeting process impacts on the performance of apparel industry in Sri Lanka. It was also; found that there is a marginally sound budgetary process in Sri Lankan apparel industry. Apparel industry performances were better for the last 3 years. Budgetary process and organizational performance have shown strongly positive relationship. Selection techniques and regression analysis were employed in investigating the relationship between the budgetary process and organizational performance of apparel industry in Sri Lanka. Individual organization’s budgetary process of apparel industry in Sri Lanka was evaluated. An optimal analytical model shows an overall association between budgetary processes with organizational performance. The positive sign suggests that there is a positive relationship between budgetary process and organizational performance in the apparel industry in Sri Lanka. The findings of this study suggest that companies in apparel industry who plan to improve their financial performance should give more priority to develop the formality of the budgetary planning, budgetary coordination, budgetary control, budgetary communication and budgetary evaluation. Further, provide guidance to help accounting and finance

Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 3(4):354-360 (ISSN:2141-7024)

359

professionals’ increases their knowledge to targeted practices of budgetary process of apparel industry in Sri Lanka that specifically support private sector organizations. REFERENCES Abdullah, F.J., 1998. Budget Related Behavior and Performance Goals of Cost Centre Managers in a public Institute of Higher Learning in Malaysia. Master of Accounting Curtin University of Technology Akintoye, I.R., 2008. Budget and Budgetary Control for Improved Performance: A Consideration for Selected Food and Beverages Companies in Nigeria. European Journal of Economics and Finance and Administrative Sciences [online], Available at <http://www.eurojournals.com/ejefas_12_01.pdf> [Accessed 24 June 2011] Blumentritt T., 2006. Integrating Strategic Management and Budgeting, Journal of Business Strategy, 27(6), pp.73 – 79 Central Bank of Sri Lanka 2010,Annual report, Central Bank of Sri Lanka, Colombo Caleb, E.B., 2011. Budget Discipline under Military and Civilian Regimes: Any difference in Nigeria. International Journal of research in commerce, It & Management, 1, pp. 13. Chow.J., 2011. Fabric & Garment Accessories expo Sri Lanka In: CP Exhibition, International Organizer and Sales Coordinator, Market Information. Sri Lanka Exhibition & Convention Centre (SLECC). Colombo, Sri Lanka, 23 – 25 June, 2011. Sri Lanka Exhibition & Convention Centre Cieslak, K. and Kalling, T., 2007. Reasons behind Contemporary use of Budgets NFF Conference in Bergen, 3-11 August 2007, Lund University: Sweden. Collins, M., 2011. The Relationship Between self-Reported Budget performance and satisfaction with organizational rewards in a college setting. In: Le Moyne College, Proceedings of ASBBS, February 2011, And ASBBS Annual Conference: Las Vegas Dheerasinghe, R., 2009. Garment Industry in Sri Lanka Challenges, Prospects and Strategies. Staff studies article, 33, pp.34-72 Dias, A., 2009. Global crisis rips garment industry. The Sunday Times, Sri Lanka 01.03.2009 Drury, C., 2004. Management and cost accounting 6th ed. London: Thomson learning.

Dugdale, D. and Lyne, S., 2010. Budgeting Practice and Organizational Structure [online] London: CIMA Publishing. Research Executive Summary Available at<http://www.cimaglobal.com/Documents/Thought_leadership_docs/Budgeting%20and%20planning/cid_ressum_budgeting_practice_organisational_structure_may2010.pdf> [Accessed 21 November 2011] Gustafsson, M. and Pärsson, R., 2010. Budget – a perfect management tool: A case study of AstraZeneca. BMA Gothenburg University Hartmann, F.G.H. and Moers, F., 1999. Testing contingency hypotheses in budgetary research: an evaluation of the use of moderated regression analysis. Accounting, Organizations and Society, 24, pp. 291–315. Hartmann, F.G.H. and Moers, F., 2003. Testing contingency hypotheses in budgetary research: an evaluation of the use of moderated regression analysis: a second look. Accounting, Organizations and Society, 28, pp. 803-809. Hansen, S.C. and Van der Stede, W.A., 2004. multiple facets of budgeting: an exploratory analysis. Management Accounting research, [e-journal] 15(4), pp. 415-439, Available through: Science direct database [Accessed 28 December 2011] Hansen, S.C., Otley, T.D. and Van der Stede, W.A., 2003. Practice Developments in Budgeting: An Overview and Research Perspective. Journal of Management Accounting Research, 15, pp. 95–116 Herath, S.K. and Indrani, M.W., 2007. Budgeting as a Competitive Advantage, Evidence from Sri Lanka Journal of American Academy of Business, Vol.11, Issue 1, pp.79-91. Horngren, C.T., Sundem, G.L. and Stratton,W.O., 2001, Introduction to Management Accounting. 11thed. New Delhi: Prentice-Hall of India (Pvt) Ltd Hope, J. and Fraser, R., 2003. Beyond Budgeting – how managers can break free from the annual performance trap. The United States of America: Harvard Business John, A.O. and Ngoason, L.N., 2008.Budgetary and Management control Process in a Manufacturing: Case of Guinness Nigerian PLC. Master thesis. Malardalen University Kelegama, S., 2005. Ready-Made Garment Industry in Sri Lanka: Facing the Global Challenge, Asia-Pacific Trade and Investment Review, [online]. Available at: <http; //www.unescap.org/tid /publication/aptir2362_research3.pdf> [Accessed 05 May 2011]

Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 3(4):354-360 (ISSN:2141-7024)

360

McBain, L., 2010. Strategic Management in the Public Sector MBA General Management Institute of Management Berlin and School of Economics and Law Berlin pp1-11 Masakorala, R., 2010. Sri Lankan Garment industry gets new orders in 2010. News360. [online] 22 Dec. Available at: <http://www.news360.lk/economy/sri-lankan-garment-industry-gets-new-orders-in-2010>[Accessed 22 June 2011]. Marginson, D. and Sharma, N., 2011.Strategizing through budgetary practices: evidence of a ‘mutually emergent’ interplay between budgeting and strategy, Cardiff Business School. [online]Available at<http://elsevier.conferenceservices.net/resources/247/2182/pdf/CPAC2011_0058_paper.pdf> [Accessed 01 December 2011] Omolehinwa, E., 1989. PPBS in Nigeria: Its origin, progress and problems. Public Administration and Development, Public Budgeting & Finance, 9(2), pp. 43–65. Otley, D.T., 1978. Budget use and managerial performance Journal of Accounting Research, 16 (1), pp.122-148 Otley, D.T., 2001. Extending the Boundaries of Management Accounting Research: Developing Systems for Performance Management Lancaster University, British Accounting Review (2001), 33, pp.243–261 Perea, P.A.D.N., 2009. Impact of Losing Competitiveness of the Garment Industry in Sri Lanka MBA University of Kelaniya Sri Lanka Qi, Y., 2010.The Impact of the Budgeting Process on Performance in Small and Medium sized firms in China. P.hD University of Twente Raili, P.M., 2000. Budgetary criteria in performance evaluation critical appraisal using new evidence Accounting Organization and Society 25, 483-496

Richard, A.B., Alan, J.M. and Stwaart, C.M., 2004. Fundamentals of Corporate Finance4th ed. Boston: Mcgaw-Hill Irwin Seaman, A.E., Jr, R. L. and Williams, J.J., 2011.Budget related behavior: Resolving a portion of the performance puzzle in the management accounting system. The review of Accounting Information Systems, 4(1), pp.51-68 Selvarasu, A. et al., 2010.Model Predicting Profit and Turnover Path of Apparel – Retail Company, Journal of Economics and Engineering, [online].Available at: http://www.lit.az/ijar/pdf/jee/2/JEE2010%282-1%29.pdf [Accessed 29 December 2011] Sri Lanka Export Development Board, 2011 Apparel and Accessories [online]Available at: http://www.srilankabusiness.com/trade_info/srilankaproduct/apparel.htm> [Accessed 05 July 2011]. GFOA (The Government Finance Officers Association), 1998 National Advisory Council on State and Local Budgeting Practice [online]. Available at: <http://www.co.larimer.co.us /budget/budget_practices.pdf> [Accessed on 18 May 2011] The Institute of Working Future, 2011 Monitor and Evaluate Budget, Advance Diploma in Logistics and Management [online] Available at: <http://www.marcbowles.com/courses/adv_dip/module7/chapter1/amc7_ch1three.htm> [Accessed 10 October 2011]. Tilakaratne, W.M., 2006. Phasing out of MFA and the Emerging Trends in the Ready Made Garment Industry in Sri Lanka, The Case of India, Bangladesh and Sri Lanka, Chiba: Institute of Developing Economies [online] Available at : <http:// www.ide.go.jp/English/Publish/Download/Jrp/pdf/140_2.pdf> [Accessed 16 October 2011] Welmilla, I., 2001. The impact of Budget Related Behavior on the performance of companies in Sri LankaM.Com University of Kelaniya, Sri Lanka.

APPENDIX Correlation Matrix Planning Coordination Controlling Communication Evaluation Budgetary Process Planning

1

Coordination .759** 1 Controlling

.565** .636** 1

Communication

.722** .717** .746** 1

Evaluation

.255 .228 .273 .240 1

Budgetary Process

.808** .834** .819** .848** .531** 1

Return on Assets

.732** .809** .715** .823** .341* .866**

**. Correlation is significant at the 0.01 level (2-tailed).*. Correlation is significant at the 0.05 level (2-tailed). N=50