Embed Size (px)

Citation preview

1 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

Recommendation

Buy at CMP and add on Dips

Add on dips to

Rs. 948-1023

Target

Rs. 1200

Time Horizon

4 Quarters

Industry

EXCHANGES

CMP

Rs. 1023

Established in 1875, BSE Ltd. (formerly known as Bombay Stock Exchange Ltd.), is Asia’s first Stock Exchange

and World’s largest exchange by number of listed securities. BSE provides an efficient and transparent market for

trading in equity, debt instruments, derivatives, mutual funds. It also has a platform for trading in equities of

small-and-medium enterprises (SME). BSE also provides a host of other services to capital market participants

including risk management, clearing, settlement, market data services and education. BSE also provides

depository services through its arm Central Depository Services Ltd. (CDSL).

We have valued BSE on SOTP basis by assigning fair value of Rs 430 to CDSL (~25% premium to CMP) and 25x

to BSE’s core earnings (ex. CDSL). We recommend BUY on BSE at CMP of Rs 1023 and add on dips to Rs 948 with

TP of Rs 1,200, which includes core BSE value at Rs 1,060 and CDSL stake at Rs 140.

Investment Rationale:

Macro tailwinds: India, the fastest growing economy

The outlook for the Indian economy remains strong. Indian Economy is expected to become the third largest in the world by 2030. The strong growth outlook is driven by a number of factors, such as policy reforms like GST, focus on skill development, Make in India initiative, and close monitoring of inflation, resulting in lower interest rates.

Demonetisation was a significant step towards making India a cashless economy. We expect demonetisation to lead to growth opportunities for exchanges in India, based on factors like (1) Allocation of larger portion of household savings in productive financial assets (2) Adoption of digital payments will lead to greater participation in capital markets, owing to the seamless integration of payment and trading platforms and (3) Drop in interest rates will make capital markets more attractive. Indian exchanges catching up with global peers Prominent exchanges in India like NSE and BSE lag behind global peers in various parameters like Market Cap/GDP ratio, cash turnover velocity and free float etc. However, with the Indian economy growing at swift pace, these criteria are expected to catch up gradually. We believe there is a clear case for growth in cash volumes based on the following factors, which includes (1) Increasing retail participation (2) Huge inflows in MFs (3) Greater penetration of capital market products (4) Use of the Mobile trading platform (5) Plans for divestment (6) increasing free float levels (7) Large number of upcoming IPOs and (8) Rising investor confidence.

FUNDAMENTAL ANALYST

Nisha Shankhala

HDFC Scrip Code BSELTD

BSE Code NA

NSE Code BSE

Bloomberg BSE IN

CMP as on 12 Sep’17 1023

Equity Capital (Rs mn) 107.6

Face Value (Rs) 2

Equity O/S (mn) 53.8

Market Cap (Rs mn) 55079

Book Value (Rs) 495

Avg. 52 Week Vol 329121

52 Week High 1200

52 Week Low 806

Shareholding Pattern (%)

Institutions 31.9

Non Institutions 31.1

Other 37.0

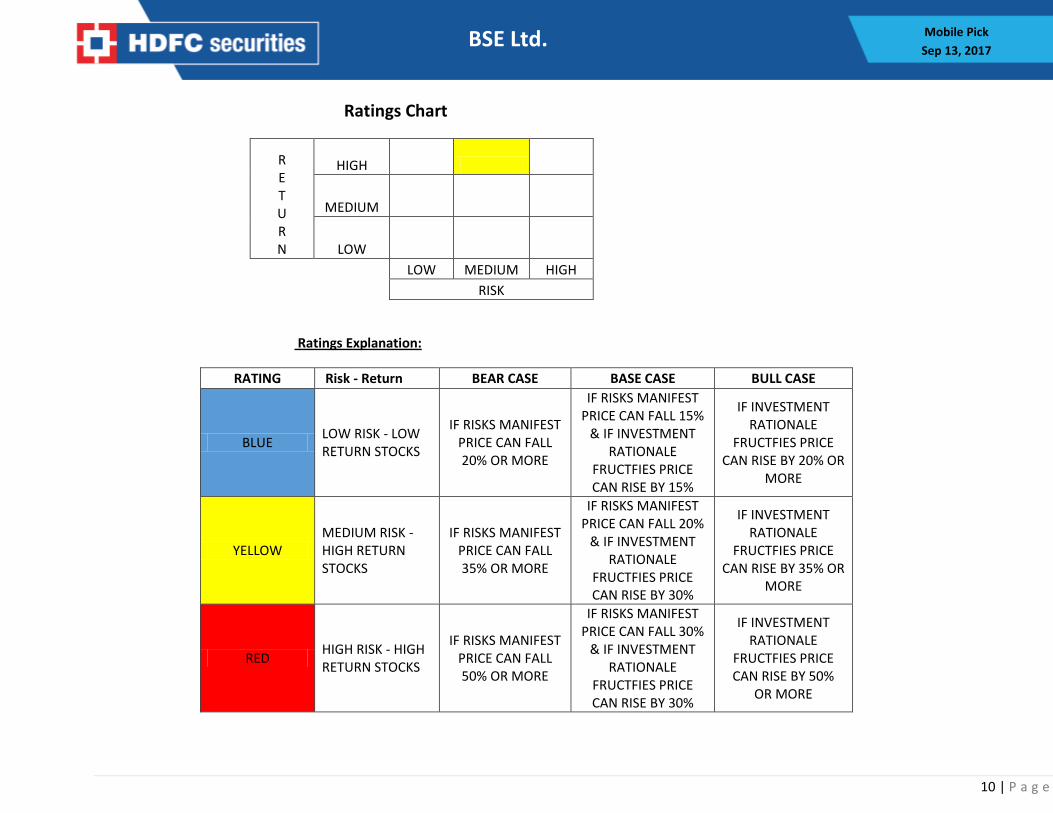

PCG Risk Rating* Yellow

* Refer Rating explanation

2 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

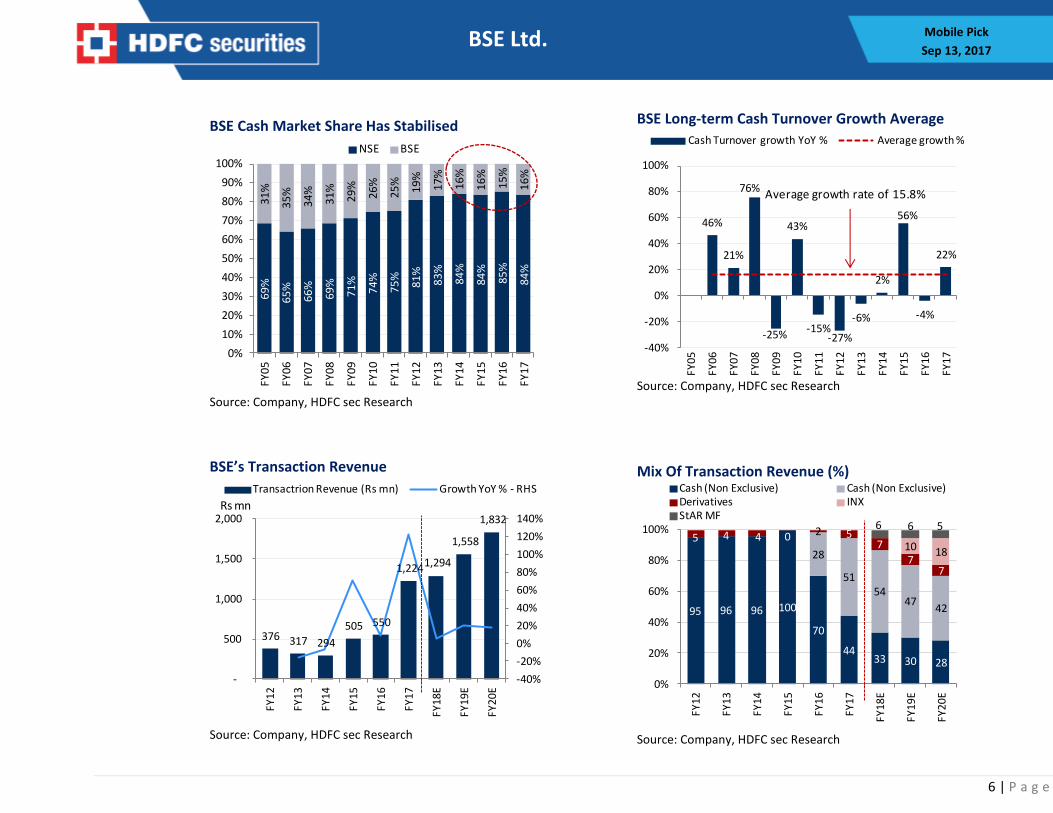

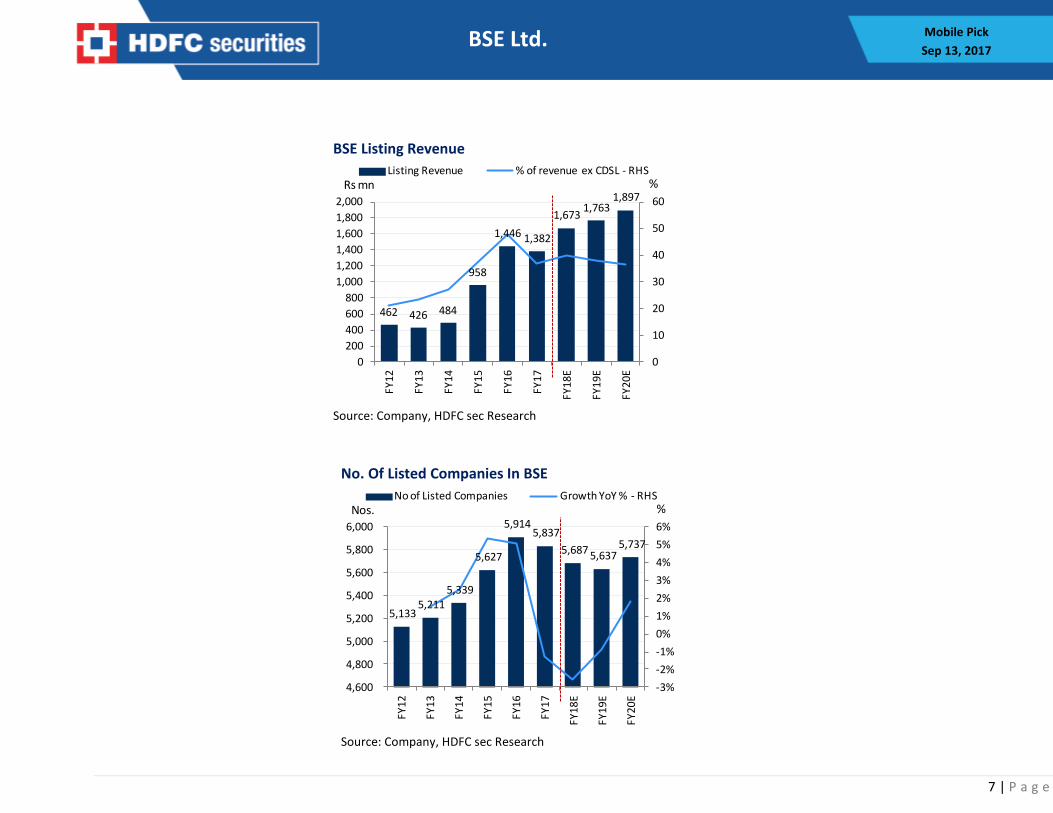

Increase in free float to improve turnover velocity Indian companies have a high promoter holding structure, which leads to lower free float and inferior turnover velocity. Indian listed companies’ free float has increased from ~37% in 2010 to ~46% in 2015, but is still below the levels of developed countries at ~85%. Retail investors constitute only ~13% of stock ownership in India. Number of DeMat accounts in India is less than 10% of the total number of bank accounts which leaves tremendous scope for CDSL and BSE. We believe, with the planned disinvestment of government stake in PSUs, greater number of IPOs, higher retail participation and rising institutional activity can increase further the free float level. BSE: Cash market share stable NSE has dominated the cash and derivative markets. It commands strong market share of ~100% in the derivatives segment, and ~84% in the cash segment. BSE has been losing market share in the cash segment to NSE since 2006, but this has now stabilised in the last 3-4 years. In FY17, BSE had ~16% market share in the cash market (stable at this level for the last four years). BSE has revamped its technology to become the fastest exchange in the world. Management increased focus on generating ways to increase transaction income. BSE has also terminated its efforts to develop the F&O market, where NSE commands a dominant position. Total cash turnover has posted CAGR of 11.4% over FY05 to FY17. BSE/NSE cash turnover increased at CAGR of 5.5/13.2% over FY05 FY17 respectively. In FY17, cash turnover volumes stood at Rs 61tn, which is an all-time high. We expect total cash turnover to post 15% CAGR over FY17-20E. BSE turnover is expected to see strong 17% CAGR due to changed traffic structure (flat fee per trade) for A & B segment stocks. Change in pricing structure to gain market share and attract bulk/block deals BSE has changed the structure of its transaction charges for the equity cash segment from an ‘ad valorem’ basis to ‘per trade’ basis, effective 3-April-17. BSE charged Rs 1 /trade to entities with volumes less than 50k trades per month which it has increased to Rs 1.50/trade from Aug-17(still at discount compared to NSE). BSE has hiked charges across segments (including Listing Fees), which has provided boost to its revenues (especially transaction revenue) in FY17. BSE’s charges were much lower than that of NSE, and the price hikes were largely taken to rationalise the pricing differential. Even after the price hikes, BSE’s charges are at a steep discount to those of NSE.

Figure 1ufuyut

KEY HIGHLIGHTS

Established in 1875, BSE Ltd.,

is Asia’s first Stock Exchange

and World’s largest exchange

by number of listed securities.

BSE has been constantly

innovating and investing in

technology, thus will remain a

valuable franchise.

We see value based on Indian

Macro tailwind, Stable Cash

market share, New &

Attractive pricing structure,

high Conviction-CDSL

business, Huge net cash

(excluding SGF and clearing)

of Rs 30bn (~Rs 567/sh,

~58% of MCap) and High

dividend yield of ~3%.

We have valued BSE on SOTP

basis. We initiate coverage on

BSE with TP of Rs 1,200, which

includes core BSE value at Rs

1,060 and CDSL stake value at Rs 140.

3 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

Investments in new platforms StAR MF platform: is an online platform launched by BSE in Dec-2009, the platform allows mutual fund distributors, investment advisors etc. to purchase and redeem mutual fund units on behalf of their clients. BSE’s StAR MF platform has gained immense popularity and has ~80% market share. The number of orders processed on the platform stood at 6.5mn (+98% YoY) in FY17, with a total value of Rs 743bn (+68% YoY). BSE will now monetise the effort, and will charge on a pay-per-use model. International Exchange (INX): BSE launched India’s first International Exchange in Jan-17 at GIFT City in Gujarat. The objective is to attract volumes from global exchanges. BSE has invested Rs 1.15bn and will invest another Rs 4bn over the next 3 years. The company will use the cash proceeds from the CDSL stake sale to fund the INX capex. The company is confident of witnessing a ramp-up in INX volumes, and views it as the next big opportunity. However, we believe it will take at least two to three years for the volume to ramp up. INX will be margin dilutive in FY18 and FY19, and will break-even in FY20E.

CDSL- High Conviction Business The Central Depository Services Ltd (CDSL) is the 2nd largest depository in India, with 44% market share. In June-17 it came up with the IPO. The size of the IPO was Rs 5.24bn and BSE received ~77% of the proceeds (~Rs 4.03bn). Post IPO, BSE holds 24% stake in CDSL. On financial performance front CDSL is very strong. It operates at robust EBITDA margin (increased from 39.4% in FY13 to 54.4% in FY17). EBITDA has witnessed 22% CAGR over FY13-17 and PAT for FY17 stands at Rs 858mn, with EPS of Rs 8.2. CDSL has RoE of 16.1% in FY17, net cash of Rs 5.15bn (15% of market cap), and a dividend yield of 1.1%. We expect CDSL revenue/EBITDA/PAT to increase at CAGR of 19/23/17% over FY17-20E. This business will command higher multiple, and we arrive at fair value of Rs 430 assigning 35x to Sep-19 EPS.

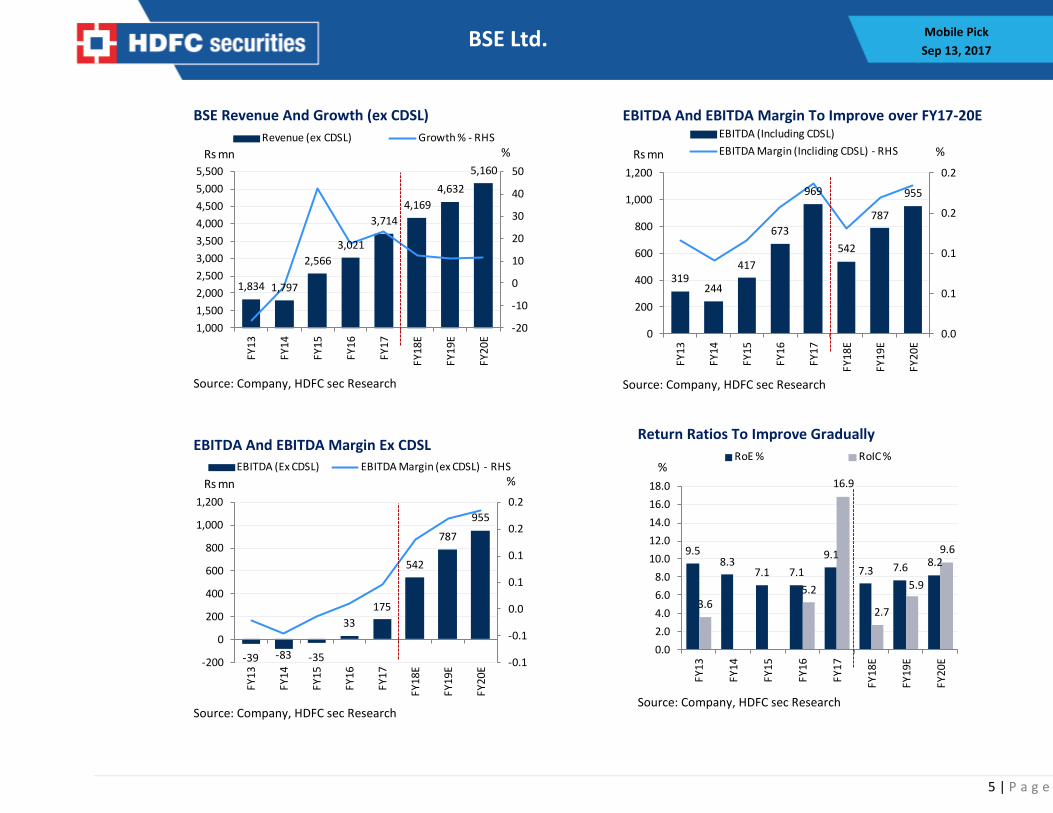

Financial analysis

BSE has diversified revenue stream, which can be broadly classified as (1) Revenue from securities’ services

(51% of revenues ex-CDSL, CAGR of 9.1% over FY12-17) (2) Revenue from services to corporates (42% of

revenue ex-CDSL, CAGR of 15.5% over FY12-17) and (3) Data dissemination revenue (7% of revenue, CAGR

of 3.5 % over FY12-17).

Total revenue ex-CDSL has increased at CAGR of 11% over the last five years, and at 27% over the last three

years to Rs 3.71bn. We expect revenue ex-CDSL to increase at CAGR of 11.6% over FY17-20E. Total revenue

(including CDSL) has seen 10% CAGR over FY12-17 to Rs 5.17bn. We expect PAT (ex-CDSL) to show 15%

CAGR over FY17-20E.

4 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

Risk & Concerns:

Increased Competition from other exchanges, loss of market share

Regulatory delays

Technological risks

Delay in monetization of investments in new platforms like StAR MF and India INX etc.

View & Valuation: BSE has been constantly innovating and investing in technology, thus would continue to remain valuable

franchise. We see value based on Indian Macro tailwind, Stable Cash market share, New & Attractive pricing

structure, high Conviction-CDSL business, Huge net cash (excluding SGF and clearing) of Rs 30bn (~Rs

567/sh, ~58% of MCap) and healthy dividend yield of ~3%.

Moreover NSE listing will drive volume as it has to get listed itself on BSE only and Moreover NSE IPO/listing

on higher valuation may lead to re-rating for BSE also. BSE currently trades at 23.7x FY18E and 21.5x FY19E

EPS (discount of ~2% to the global average).

We have valued BSE on SOTP basis by assigning fair value of Rs 430 to CDSL (~26% premium to CMP) and

25x to BSE’s core earnings (ex CDSL). We initiate coverage on BSE with TP of Rs 1,200, which includes core

BSE value at Rs 1,060 and CDSL stake value at Rs 140.

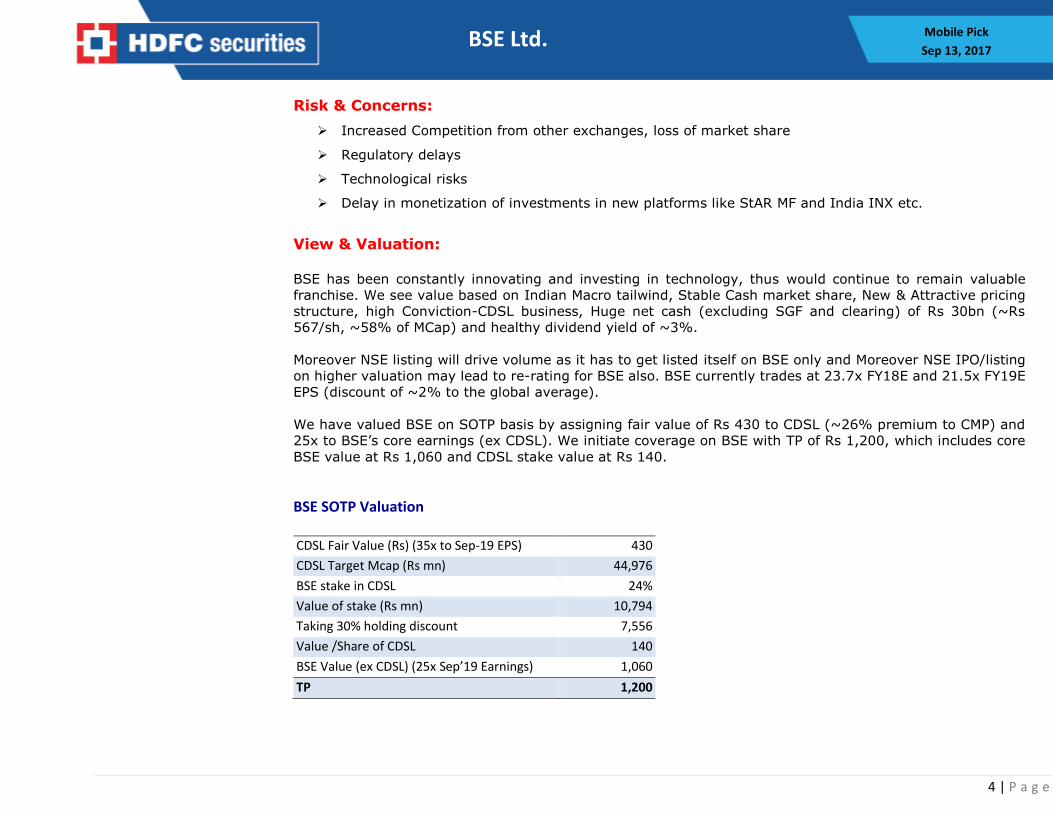

BSE SOTP Valuation CDSL Fair Value (Rs) (35x to Sep-19 EPS) 430

CDSL Target Mcap (Rs mn) 44,976

BSE stake in CDSL 24%

Value of stake (Rs mn) 10,794

Taking 30% holding discount 7,556

Value /Share of CDSL 140

BSE Value (ex CDSL) (25x Sep’19 Earnings) 1,060

TP 1,200

5 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

BSE Revenue And Growth (ex CDSL)

Source: Company, HDFC sec Research

1,834 1,797

2,566

3,021

3,714

4,169

4,632

5,160

-20

-10

0

10

20

30

40

50

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

FY1

3

FY1

4

FY15

FY1

6

FY1

7

FY1

8E

FY1

9E

FY2

0E

Revenue (ex CDSL) Growth % - RHS

Rs mn %

EBITDA And EBITDA Margin To Improve over FY17-20E

Source: Company, HDFC sec Research

319244

417

673

969

542

787

955

0.0

0.1

0.1

0.2

0.2

0

200

400

600

800

1,000

1,200

FY13

FY14

FY15

FY16

FY17

FY1

8E

FY1

9E

FY2

0E

EBITDA (Including CDSL)

EBITDA Margin (Incliding CDSL) - RHSRs mn %

EBITDA And EBITDA Margin Ex CDSL

Source: Company, HDFC sec Research

-39 -83 -35

33

175

542

787

955

-0.1

-0.1

0.0

0.1

0.1

0.2

0.2

-200

0

200

400

600

800

1,000

1,200

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY18

E

FY19

E

FY20

EEBITDA (Ex CDSL) EBITDA Margin (ex CDSL) - RHS

Rs mn %

Return Ratios To Improve Gradually

Source: Company, HDFC sec Research

9.58.3

7.1 7.1

9.1

7.3 7.6 8.2

3.65.2

16.9

2.7

5.9

9.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY18

E

FY19

E

FY20

E

RoE % RoIC %%

6 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

BSE Cash Market Share Has Stabilised

Source: Company, HDFC sec Research

69

%

65

%

66

%

69

%

71

%

74

%

75

%

81

%

83

%

84

%

84

%

85

%

84

%

31

%

35

%

34

%

31

%

29

%

26

%

25

%

19

%

17

%

16

%

16

%

15

%

16

%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

NSE BSE

BSE Long-term Cash Turnover Growth Average

Source: Company, HDFC sec Research

46%

21%

76%

-25%

43%

-15%-27%

-6%

2%

56%

-4%

22%

-40%

-20%

0%

20%

40%

60%

80%

100%

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY12

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

Cash Turnover growth YoY % Average growth %

Average growth rate of 15.8%

Mix Of Transaction Revenue (%)

Source: Company, HDFC sec Research

95 96 96 100

70

4433 30 28

28

5154

4742

5 4 4 0 2 57

77

10 18

6 6 5

0%

20%

40%

60%

80%

100%

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY18

E

FY1

9E

FY2

0E

Cash (Non Exclusive) Cash (Non Exclusive)Derivatives INXStAR MF

BSE’s Transaction Revenue

Source: Company, HDFC sec Research

376 317 294

505 550

1,224 1,294

1,558

1,832

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

-

500

1,000

1,500

2,000

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8E

FY19

E

FY2

0E

Transactrion Revenue (Rs mn) Growth YoY % - RHS

Rs mn

7 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

BSE Listing Revenue

Source: Company, HDFC sec Research

462 426 484

958

1,446 1,382

1,6731,763

1,897

0

10

20

30

40

50

60

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

FY1

2

FY13

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8E

FY1

9E

FY2

0E

Listing Revenue % of revenue ex CDSL - RHSRs mn %

No. Of Listed Companies In BSE

Source: Company, HDFC sec Research

5,133 5,211

5,339

5,627

5,914 5,837

5,687 5,637 5,737

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

4,600

4,800

5,000

5,200

5,400

5,600

5,800

6,000

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY18

E

FY19

E

FY20

E

No of Listed Companies Growth YoY % - RHSNos. %

8 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

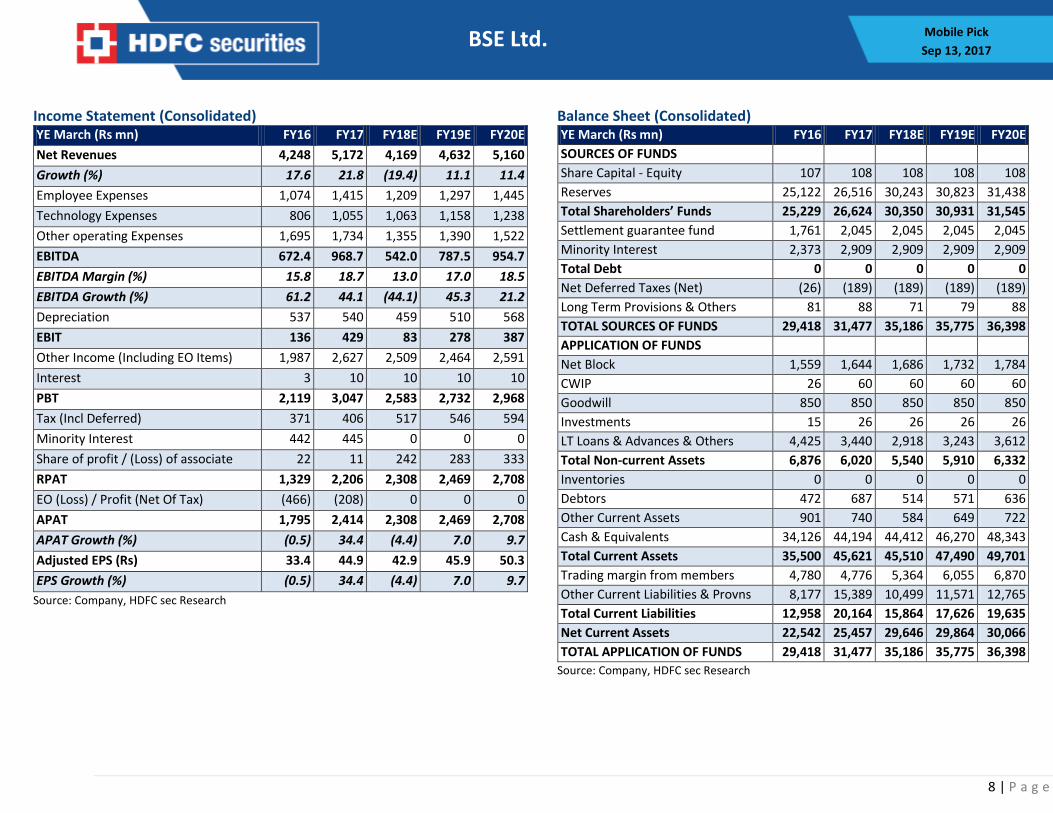

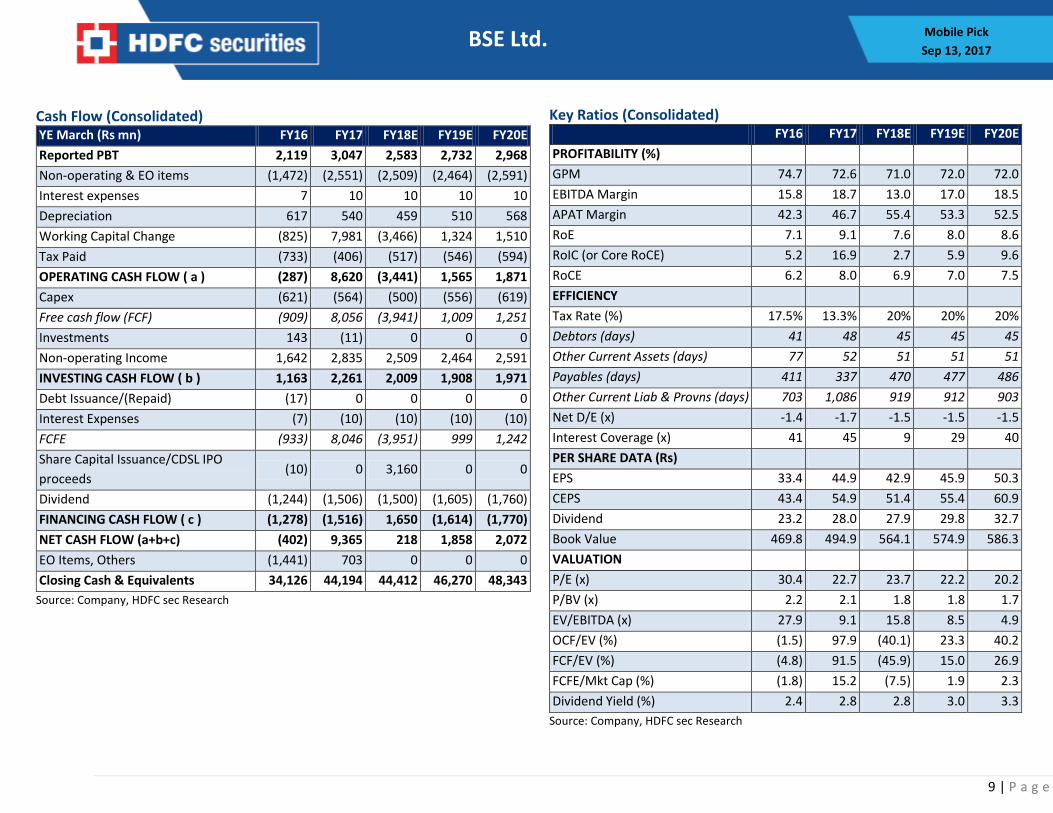

Income Statement (Consolidated) YE March (Rs mn) FY16 FY17 FY18E FY19E FY20E

Net Revenues 4,248 5,172 4,169 4,632 5,160

Growth (%) 17.6 21.8 (19.4) 11.1 11.4

Employee Expenses 1,074 1,415 1,209 1,297 1,445

Technology Expenses 806 1,055 1,063 1,158 1,238

Other operating Expenses 1,695 1,734 1,355 1,390 1,522

EBITDA 672.4 968.7 542.0 787.5 954.7

EBITDA Margin (%) 15.8 18.7 13.0 17.0 18.5

EBITDA Growth (%) 61.2 44.1 (44.1) 45.3 21.2

Depreciation 537 540 459 510 568

EBIT 136 429 83 278 387

Other Income (Including EO Items) 1,987 2,627 2,509 2,464 2,591

Interest 3 10 10 10 10

PBT 2,119 3,047 2,583 2,732 2,968

Tax (Incl Deferred) 371 406 517 546 594

Minority Interest 442 445 0 0 0

Share of profit / (Loss) of associate 22 11 242 283 333

RPAT 1,329 2,206 2,308 2,469 2,708

EO (Loss) / Profit (Net Of Tax) (466) (208) 0 0 0

APAT 1,795 2,414 2,308 2,469 2,708

APAT Growth (%) (0.5) 34.4 (4.4) 7.0 9.7

Adjusted EPS (Rs) 33.4 44.9 42.9 45.9 50.3

EPS Growth (%) (0.5) 34.4 (4.4) 7.0 9.7

Source: Company, HDFC sec Research

Balance Sheet (Consolidated) YE March (Rs mn) FY16 FY17 FY18E FY19E FY20E

SOURCES OF FUNDS

Share Capital - Equity 107 108 108 108 108

Reserves 25,122 26,516 30,243 30,823 31,438

Total Shareholders’ Funds 25,229 26,624 30,350 30,931 31,545

Settlement guarantee fund 1,761 2,045 2,045 2,045 2,045

Minority Interest 2,373 2,909 2,909 2,909 2,909

Total Debt 0 0 0 0 0

Net Deferred Taxes (Net) (26) (189) (189) (189) (189)

Long Term Provisions & Others 81 88 71 79 88

TOTAL SOURCES OF FUNDS 29,418 31,477 35,186 35,775 36,398

APPLICATION OF FUNDS

Net Block 1,559 1,644 1,686 1,732 1,784

CWIP 26 60 60 60 60

Goodwill 850 850 850 850 850

Investments 15 26 26 26 26

LT Loans & Advances & Others 4,425 3,440 2,918 3,243 3,612

Total Non-current Assets 6,876 6,020 5,540 5,910 6,332

Inventories 0 0 0 0 0

Debtors 472 687 514 571 636

Other Current Assets 901 740 584 649 722

Cash & Equivalents 34,126 44,194 44,412 46,270 48,343

Total Current Assets 35,500 45,621 45,510 47,490 49,701

Trading margin from members 4,780 4,776 5,364 6,055 6,870

Other Current Liabilities & Provns 8,177 15,389 10,499 11,571 12,765

Total Current Liabilities 12,958 20,164 15,864 17,626 19,635

Net Current Assets 22,542 25,457 29,646 29,864 30,066

TOTAL APPLICATION OF FUNDS 29,418 31,477 35,186 35,775 36,398

Source: Company, HDFC sec Research

9 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

Key Ratios (Consolidated) FY16 FY17 FY18E FY19E FY20E

PROFITABILITY (%)

GPM 74.7 72.6 71.0 72.0 72.0

EBITDA Margin 15.8 18.7 13.0 17.0 18.5

APAT Margin 42.3 46.7 55.4 53.3 52.5

RoE 7.1 9.1 7.6 8.0 8.6

RoIC (or Core RoCE) 5.2 16.9 2.7 5.9 9.6

RoCE 6.2 8.0 6.9 7.0 7.5

EFFICIENCY

Tax Rate (%) 17.5% 13.3% 20% 20% 20%

Debtors (days) 41 48 45 45 45

Other Current Assets (days) 77 52 51 51 51

Payables (days) 411 337 470 477 486

Other Current Liab & Provns (days) 703 1,086 919 912 903

Net D/E (x) -1.4 -1.7 -1.5 -1.5 -1.5

Interest Coverage (x) 41 45 9 29 40

PER SHARE DATA (Rs)

EPS 33.4 44.9 42.9 45.9 50.3

CEPS 43.4 54.9 51.4 55.4 60.9

Dividend 23.2 28.0 27.9 29.8 32.7

Book Value 469.8 494.9 564.1 574.9 586.3

VALUATION

P/E (x) 30.4 22.7 23.7 22.2 20.2

P/BV (x) 2.2 2.1 1.8 1.8 1.7

EV/EBITDA (x) 27.9 9.1 15.8 8.5 4.9

OCF/EV (%) (1.5) 97.9 (40.1) 23.3 40.2

FCF/EV (%) (4.8) 91.5 (45.9) 15.0 26.9

FCFE/Mkt Cap (%) (1.8) 15.2 (7.5) 1.9 2.3

Dividend Yield (%) 2.4 2.8 2.8 3.0 3.3

Source: Company, HDFC sec Research

Cash Flow (Consolidated) YE March (Rs mn) FY16 FY17 FY18E FY19E FY20E

Reported PBT 2,119 3,047 2,583 2,732 2,968

Non-operating & EO items (1,472) (2,551) (2,509) (2,464) (2,591)

Interest expenses 7 10 10 10 10

Depreciation 617 540 459 510 568

Working Capital Change (825) 7,981 (3,466) 1,324 1,510

Tax Paid (733) (406) (517) (546) (594)

OPERATING CASH FLOW ( a ) (287) 8,620 (3,441) 1,565 1,871

Capex (621) (564) (500) (556) (619)

Free cash flow (FCF) (909) 8,056 (3,941) 1,009 1,251

Investments 143 (11) 0 0 0

Non-operating Income 1,642 2,835 2,509 2,464 2,591

INVESTING CASH FLOW ( b ) 1,163 2,261 2,009 1,908 1,971

Debt Issuance/(Repaid) (17) 0 0 0 0

Interest Expenses (7) (10) (10) (10) (10)

FCFE (933) 8,046 (3,951) 999 1,242

Share Capital Issuance/CDSL IPO

proceeds (10) 0 3,160 0 0

Dividend (1,244) (1,506) (1,500) (1,605) (1,760)

FINANCING CASH FLOW ( c ) (1,278) (1,516) 1,650 (1,614) (1,770)

NET CASH FLOW (a+b+c) (402) 9,365 218 1,858 2,072

EO Items, Others (1,441) 703 0 0 0

Closing Cash & Equivalents 34,126 44,194 44,412 46,270 48,343

Source: Company, HDFC sec Research

10 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

Ratings Chart

R E T U R N

HIGH

MEDIUM

LOW

LOW MEDIUM HIGH

RISK

Ratings Explanation:

RATING Risk - Return BEAR CASE BASE CASE BULL CASE

BLUE LOW RISK - LOW RETURN STOCKS

IF RISKS MANIFEST PRICE CAN FALL 20% OR MORE

IF RISKS MANIFEST PRICE CAN FALL 15%

& IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 15%

IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 20% OR

MORE

YELLOW MEDIUM RISK - HIGH RETURN STOCKS

IF RISKS MANIFEST PRICE CAN FALL 35% OR MORE

IF RISKS MANIFEST PRICE CAN FALL 20%

& IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 30%

IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 35% OR

MORE

RED HIGH RISK - HIGH RETURN STOCKS

IF RISKS MANIFEST PRICE CAN FALL 50% OR MORE

IF RISKS MANIFEST PRICE CAN FALL 30%

& IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 30%

IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 50%

OR MORE

11 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

Price Chart

800

850

900

950

1000

1050

1100

1150

Rating Definition:

Buy: Stock is expected to gain by 10% or more in the next 1 Year. Sell: Stock is expected to decline by 10% or more in the next 1 Year.

12 | P a g e

BSE Ltd. Mobile Pick

Sep 13, 2017

Disclosure: I, Nisha Sankhala, MBA, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Research Analyst or her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or her relative or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest. Any holding in stock –No HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475. Disclaimer: This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction. If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HSL. Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HSL may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments. HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report. HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business. HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report.

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066 Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600 HDFC Securities Limited, SEBI Reg. No.: NSE-INB/F/E 231109431, BSE-INB/F 011109437, AMFI Reg. No. ARN: 13549, PFRDA Reg. No. POP: 04102015, IRDA Corporate Agent License No.: HDF 2806925/HDF C000222657, SEBI Research Analyst Reg. No.: INH000002475, CIN - U67120MH2000PLC152193 Mutual Funds Investments are subject to market risk. Please read the offer and scheme related documents carefully before investing.