Embed Size (px)

Citation preview

Bringing Our Value Into Sharp FocusDr. Jürgen Hambrecht, CEO

2

Volume growth in %

Growing above chemical market*

BASF European Chemicals**(excl. BASF)

US Chemicals***

* Excluding pharma** European peers: Akzo Nobel, Bayer, Ciba, Clariant, Degussa, DSM, Rhodia, Syngenta*** US peers: Dow, PPG, DuPont, Rohm and HaasSource: Company reports

-3

-1

1

3

5

7

9

2001 2002 2003 2004 2005 1st half 2006

3

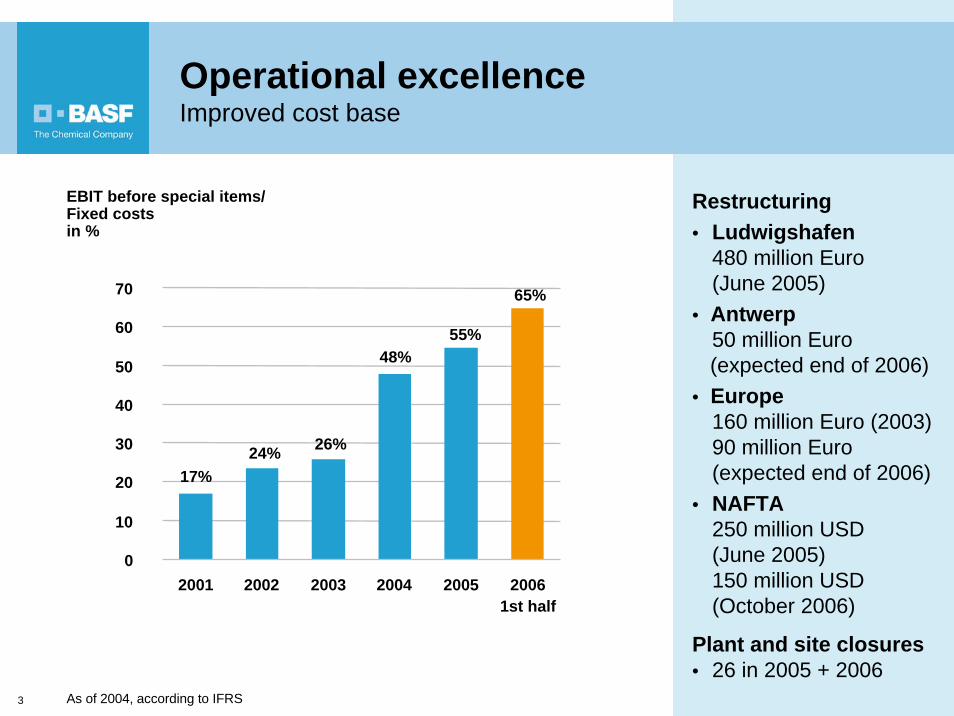

Operational excellenceImproved cost base

Restructuring• Ludwigshafen

480 million Euro (June 2005)

• Antwerp50 million Euro (expected end of 2006)

• Europe160 million Euro (2003)90 million Euro (expected end of 2006)

• NAFTA250 million USD (June 2005)150 million USD(October 2006)

Plant and site closures• 26 in 2005 + 2006

65%

55%48%

26%24%17%

0

10

20

30

40

50

60

70

2001 2002 2003 2004 2005 20061st half

EBIT before special items/Fixed costs in %

As of 2004, according to IFRS

4

Active portfolio management Selected transactions, 2001 to 2006

Acquisitions

• Custom Synthesis (Orgamol)

• Oil&Gas (Dutch gas activities)

• Electronic Chemicals(Merck Electronic Chemicals)

• Engineering Plastics• Catalysts/Pigments

(Engelhard)

• Construction Chemicals (Degussa)

• Water-based Resins(Johnson Polymer)

• Plant Biotechnoloy(CropDesign)

Divestitures

• Pharmaceuticals • Fibers• Printing Systems• BASELL• Polystyrene US• Generic

Agrochemicals(e.g. MicroFlo)

8 billion Euro(Sales)

5 billion Euro(Sales)

Portfolio managed towards higher returns and reduced cyclicality

Partnerships• Total: NAFTA Region

Olefin Complex• Shell: Ellba• Gazprom: Wingas,

Achimgaz, YushnoRusskoye, Nord Stream

• Sinopec (China)• Solvin

BASFCore

Businesses

5

Growth potential

Earningsstability

High

HighLow

Reasons for divestitures

Low profitability:• Generic Agchem• Polystyrene NAFTA• Fibers• Polyolefins (Basell)

Insufficient market position:• Printing Systems• Pharmaceuticals

Active portfolio management Selected transactions, 2001 to 2006

Low

AcquisitionsDivestitures

Printing Systems

Polyolefins (Basell)

Marketing

PharmaceuticalsOil & Gas (NL) CropDesignCatalysts/PigmentsConstruction ChemicalsEngineering PlasticsWater-based ResinsCustom SynthesisElectronic Chemicals

Generic Agchem(MicroFlo, etc.)

Polystyrene NAFTAFibers

6

The Chemical Company=

Intelligent Diversification

6

7

On track to value

ROCE in %

4.0%

8.8%

9.9%

17.2%

18.4%

0

5

10

15

20

2001 2002 2003 2004 2005

As of 2004, according to IFRS

Premium on cost of capital in million Euro

-2,554

1,9822,354

-579 -593

2001 2002 2003 2004 2005-3,000

-2,000

-1,000

1,000

2,000

3,000

0

8

Reduced volatilityEBIT* margin 2001–2005

0%

5%

10%

0% 5% 10% 15% 20%EBIT* margin (in %)

EBIT

* mar

gin

vola

tility

(in

%)

BASF

Degussa CC

Oil & GasEngelhard

ChemicalsAgriculture** & NutritionPerformance

Products

Plastics

* Based on EBIT before special items excluding non-compensable oil-taxes** Higher volatility due to integration of acquisitions and restructuring

9

02001 2002 2003 2004 2005 1st half 2006

5

10

15

EBIT margin* excluding non-compensable oil-taxesin %

BASF

Best Peers

Worst Peers

BASF achieves best in class

* Based on EBIT after special items

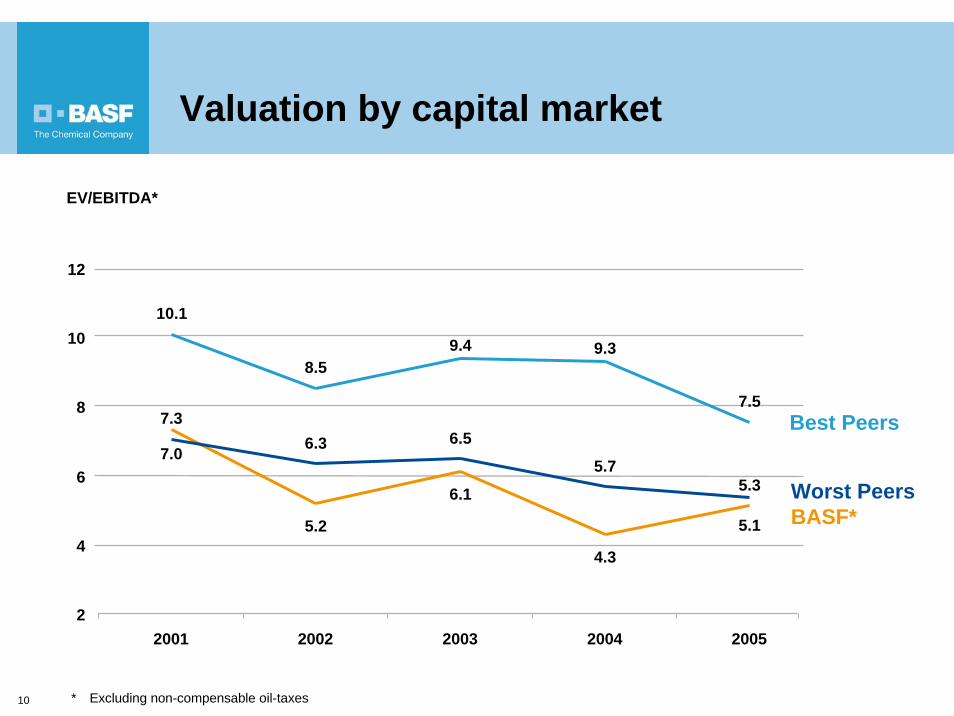

10

7.0

5.2

6.1

4.3

5.1

10.1

8.59.4 9.3

7.57.3

6.3 6.5

5.75.3

4

6

8

10

Best Peers

Worst Peers

22001 2002 2003 2004 2005

12

Valuation by capital market

EV/EBITDA*

* Excluding non-compensable oil-taxes

BASF*

11

On track to profitable growth

11

12

Our target:We will grow sales

on average 2% per year above chemical market

12

Estimated chemical market growth excl. pharma 2007–2009 = 3.3%

13

More than half of strategic business units are targeted for expansion.

Cash flow will predominantly be invested in SBUs targeted for growth.

Strategic positioning of business units

2003

1Divest

Maintain market positionReposition

36

2006

ExpandExpand moderately

35

5

32

34

50-100% cash to beused for growth

<50% cash to be used for remaining businesses

no cash to be used

14

35%

21%11%

13%

20%

• 6,800 employees in R&D (2005)

• Over 1,300 R&D co-operations worldwide

• Split of R&D expenditures (2005):- 650 million Euro

product innovation- 410 million Euro

process innovation, corporate-financed research

• Corporate-financed research:- Exploratory research - Research for growth

clustersTotal R&D expenditures 2005: 1.06 billion Euro+ 20% in 2006: 1.28 billion Euro

ChemicalsCorporate-financed research

PerformanceProducts

Agricultural Products & Nutrition

Plastics

We innovate for growth

15

Product innovation –Targeted sales from pipeline

Targeted annual sales from product innovations*: 2010: 4 billion Euro p.a.2015: 5 billion Euro p.a. thereof 10–20% annual top-line growth

160 430 120No. of projects

* New or improved products or new applications, max. 5 years on market

Lab phase &Proof of concept

Business cases Pilot phase & Launch

16

Business model

Process innovation

Product innovation

Biology

Chemistry

Physics

EnergyManagement Nano-

technology

RawMaterial Change

WhiteBiotechnology

PlantBiotechnology

Targeted annual sales from growth clusters2010: 500–1,000 million Euro2015: 2,000–4,000 million Euro

Focus on five growth clusters

• R&D expenditures for growth clusters approx. 850 million Euro from 2006–2008

• In 2006, approx. 30% funded by divisions, 70% corporate funded

• First projects out of growth clusters to come to market by 2007

17

Growing through investmentsPlanned investments 2006–2010

Plastics

Oil & Gas*

Others(e.g. infrastructure, R&D)

8.2 billion Euro*

13 %

8 %

25 %

17 %

16 %

Agriculture &Nutrition

Performance Products

21 %Chemicals

By segments

Germany

Asia

Site alternatives to be checked16 %

16 %

14 %

19 % NAFTA

Europe (excl. Germany)*

35 %

By regions

8.2 billion Euro*

* Excluding investments in Nord Stream and Yuzhno Russkoye

18

Capex discipline

Capex strategy –past and future• Capex below

depreciation • Capacity creep• Optimized asset

strategy- innovations- partnerships

In billion Euro Depreciaton

Capex*

* Capital expenditures in intangible assets, property, plant and equipment

** IFRS figures

02001 2002 2003 2004** 2005**

3

2.5

2

1.5

1

0.5

19

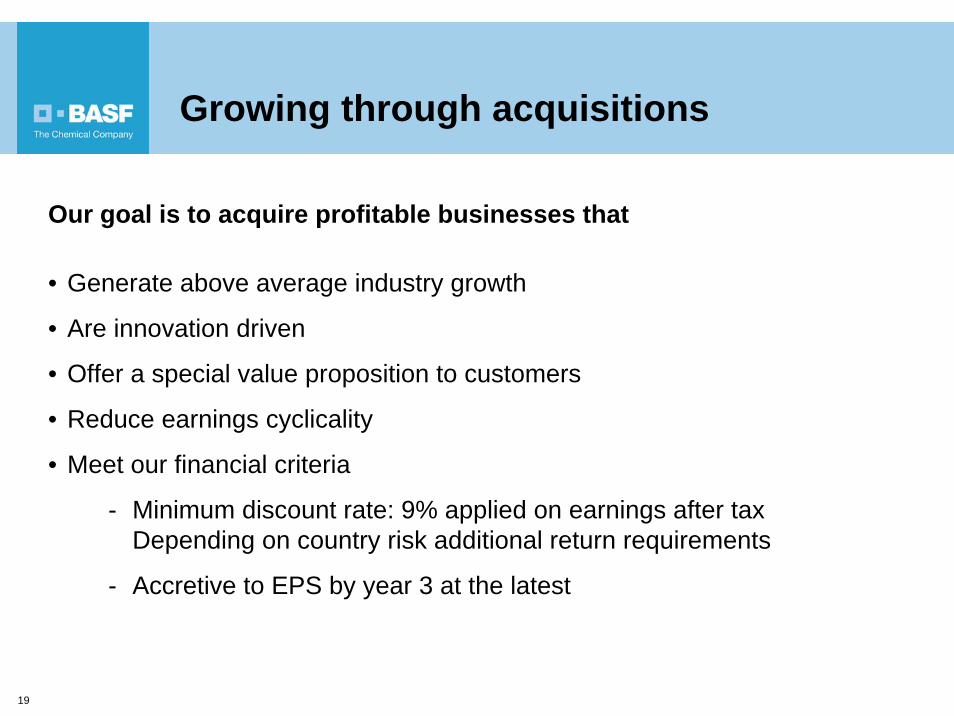

Growing through acquisitions

Our goal is to acquire profitable businesses that

• Generate above average industry growth

• Are innovation driven

• Offer a special value proposition to customers

• Reduce earnings cyclicality

• Meet our financial criteria

- Minimum discount rate: 9% applied on earnings after taxDepending on country risk additional return requirements

- Accretive to EPS by year 3 at the latest

20

Growing through acquisitions

Stand-aloneΔ% y-o-y

Sales Δ% Q3’06

EBIT* Δ% Q3’06

Remarks

Engelhard 23

10

12

14 • Catalyst business up due to demand growth in all segments

• APT business up due to strong paper coatings business

• Material Services up due to higher volumes and metal prices

Johnson Polymer 12

• Above market performance • Admixture Systems up due to strong volume growth

in Europe and Middle East• Construction Systems up mainly due to strong

volume growth in Europe and the Americas

• Sales and EBIT up due to strong volume growth in Printing & Packaging in Europe and price increases in North America

ConstructionChemicals

12

* Before special items

21

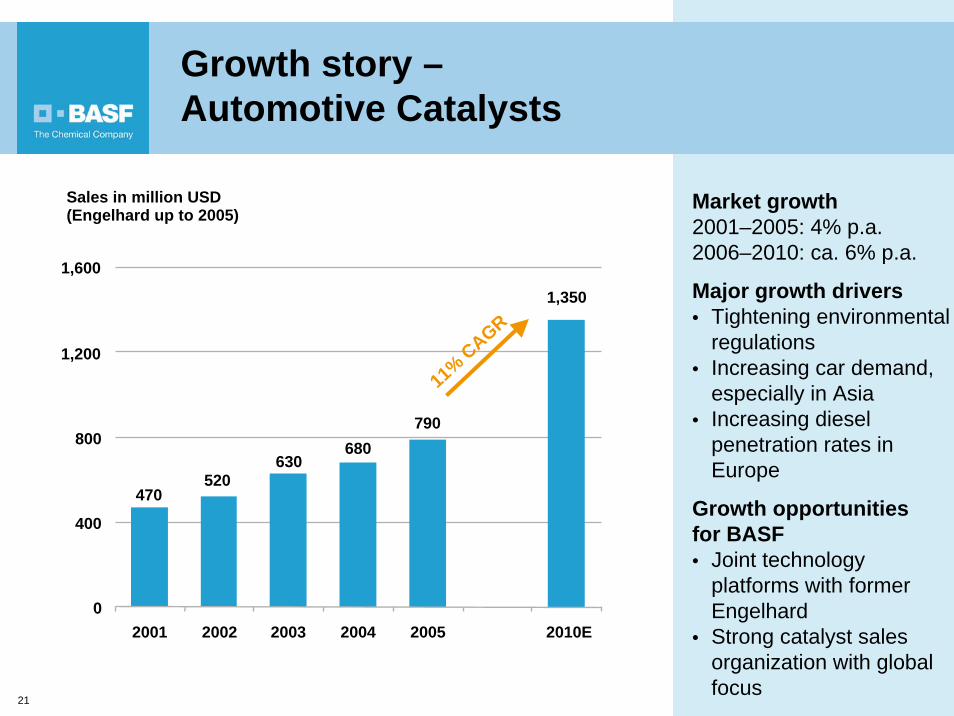

Growth story –Automotive Catalysts

Market growth2001–2005: 4% p.a.2006–2010: ca. 6% p.a.

Major growth drivers• Tightening environmental

regulations• Increasing car demand,

especially in Asia• Increasing diesel

penetration rates in Europe

Growth opportunities for BASF• Joint technology

platforms with former Engelhard

• Strong catalyst sales organization with global focus

Sales in million USD(Engelhard up to 2005)

470520

630680

790

1,350

0

400

800

2001 2002 2003 2004 2005 2010E

11% CAGR

1,200

1,600

22

Growth story –Adhesives & Construction Polymers

Market growth2001–2005: ca. 5% p.a.2006–2010: ca. 4% p.a.

Major growth drivers• Chemical solutions for

intelligent construction material

• Adhesives substitute mechanical fixing

Growth opportunitiesfor BASF• Provide solutions for

stricter environmental policies (e.g. low VOC)

• Strong presence of BASF in all regions to support globalization of our customers

BASF sales in million Euro

1,500

950900850800

0

400

800

2001 2002 2003 2004 2005 2010E

6% CAGR1,600

1,200 1,100

23

Growth story Oil & Gas

Growth in oil demand worldwide2001–2005: ca. 1.6% p.a.2006–2010: ca. 1.5% p.a.

Growth in gas demand in the European Union2001–2005: ca. 2.4% p.a.2006–2010: ca. 2.7% p.a.

Growth opportunities for BASF• Step up exploration• Acquisitions• Partnerships• “Gas for Europe”-

Strategy

~140

112109104

9393

2001 2002 2003 2004 2005 2010E0

50

100

150

Productionin million boe

5% CAGR

24

Business excellence

24

25

The Verbund

• Integrated production• Secured raw material supply• Common infrastructure• Combined logistics• Integral research platforms• Integral customer interaction

Benefits• Highly efficient production = cost leadership • Resource efficiency and waste reduction = leadership in sustainability• Integral knowledge management = leadership in innovations (>1,000 patents p.a.)• Customer orientation = supplier of choice

Agro-Chemicals& Nutrition

Plastics & Performance

ChemicalsIntermediatesBase

ChemicalsOil &Gas

The BASF Verbund-Concept

26

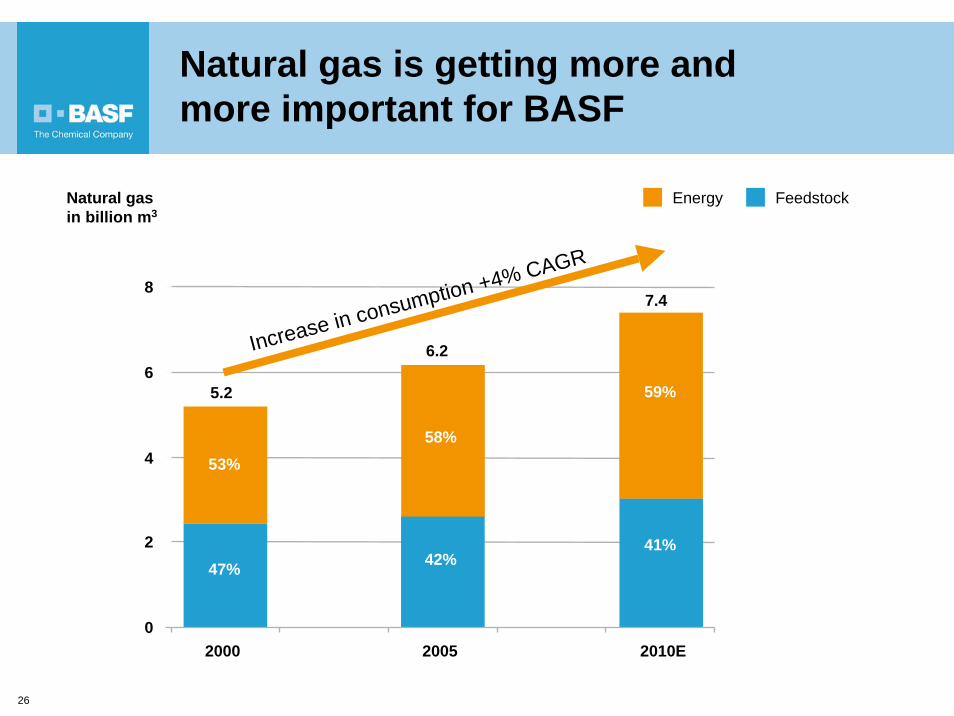

Natural gas is getting more and more important for BASF

Natural gasin billion m3

FeedstockEnergy

5.2

6.2

7.4

53%

47%

58%

42%

59%

41%

0

2

4

6

8

2000 2005 2010E

Increase in consumption +4% CAGR

27

Natural Gas

Methylformiate

Formamide

Formic Acid

HCN Value Chain

Methanol**

Butanediol

THF/Poly-THF

PBT (incl. Ecoflex)

PVP

Acetylene

Syn-Gas(Armgas)

POM

ResinsUrea

** In Ludwigshafen methanol is also produced in co-production with ammonia

Nitric Acid

Ammonia

Amines

Fertilizers

Nitrogen Oxide*

* For Caprolactam (part of the Polyamid value chain)

Simplified example from the Ludwigshafen site

Value chains driven by natural gas as feedstock

Melamine

Formaldehyde

28

Global efficiency improvement program

One-timecost

Write downs

Savingsfrom 2008

13030

160

270 160Process Optimization – 140Total 270 300

Site / Plant Restructuring

Million Euro

• 70% of savings already by 2007• Approximately 60% of one-time cost and write downs already recorded in EBIT

as of September 30, 2006

29

Synergies from acquisitions

Million Euro

Stand-alone sales 2005

Integration cost*

Synergiesby 2010

Remarks

Engelhard 3,897**

1,968

310**

Total 6,175 200 290

100 • Integration cost mainly in 2006 and 2007 • 50% of savings to be realized by 2007• 80% of savings to be realized by 2008• Includes 40 million Euro of growth synergies

160

100

Johnson Polymer

25 • Integration cost mainly in 2006 and 2007 • 60% of savings to be realized by 2007• 90% of savings to be realized by 2008• Includes 10 million Euro of growth synergies

• Integration cost mainly in 2006 and 2007 • 35% of savings to be realized by 2007• 70% of savings to be realized by 2008• Includes 30 million Euro of growth synergies

30

ConstructionChemicals

75

* Excluding use of step-up on inventory and capex ** Euro = 1.1797 USD as of Dec 30, 2005

Synergies > 4% of sales

30

Returning cash to shareholders

30

31

0.00

0.40

0.80

1.20

1.60

2.00

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Dividend in Euro per share

Dividend Special dividend

+10% p.a.

• Increased dividend in 8 of the last 10 years

• 2005 dividend increaseof 18% to 2.00 Euro per share

• Dividend yield of 3.1% in 2005*

• Objective: To further increase dividend

* Based on the share price of December 31, 2005

Ambitious dividend policy

32

Continuous share buyback program

In million Euro • 22 % of shares outstandingbought back for 6.2 billion Euro from 1999 to first nine months 2006

• 500 million Euro program announced in February completed end of October 2006

• Further share buyback of 500 million Euro announced in November 2006

808

256

700

1,300

500 500

726

1,435

0

500

1,000

1,500

2,000

1999 2000 2001 2002 2003 2004 2005 Q1-Q32006

33

Bringing our value into sharp focus

• Consistent year-on-year financial and operational delivery

• Portfolio reshaped toward faster growing and less cyclical businesses

• Innovations and acquisitions drive profitable growth even faster

• Business excellence through intelligent and efficient value chain management

• Strong return orientation

34

![ECOFLEX PARA JOAQUIM - PINHALENSERua Honório Soares, 80 Espírito Santo do Pinhal - SP - Brasil CEP 13.990-000 Fone [19] 3651-9200 Fax [19] 3651-9204 ECOFLEX-1 ECOFLEX-2 ECOFLEX-4](https://img.pdfslide.us/doc/110x75/5fa7aff2cec8d905fc6302cd/ecoflex-para-joaquim-pinhalense-rua-honrio-soares-80-esprito-santo-do-pinhal.jpg)