Embed Size (px)

Citation preview

Briefing to the Portfolio Committee of Science and

Technology on 2015-16 audit outcomes of the portfolio 11 October 2016

1

1

2

The AGSA’s promise and focus

2015-16

PFMA

Reputation promise

The Auditor-General of South Africa (AGSA) has a constitutional

mandate and, as the Supreme Audit Institution (SAI) of South

Africa, it exists to strengthen our country’s democracy by

enabling oversight, accountability and governance in the public

sector through auditing, thereby building public confidence.

3

2015-16

PFMA

Role of AGSA in the BRRR process

• Our role as the AGSA is to reflect on the audit work performed to assist

the portfolio committee in its oversight role in assessing the performance

of the entities taking into consideration the objective of the committee to

produce a BRRR.

• To provide the portfolio committee with applicable information and

guidance on the Science and Technology portfolio’s 2015-16 audit

outcomes so that they, the committee, can ensure effective

oversight.

• To enable oversight to focus on areas that will lead to good

governance.

4

Our annual audits examine three areas

1 FAIR PRESENTATION AND

RELIABILITY OF FINANCIAL

STATEMENTS 2 RELIABLE AND CREDIBLE

PERFORMANCE INFORMATION

FOR PREDETERMINED

OBJECTIVES 3

COMPLIANCE WITH KEY

LEGISLATION ON FINANCIAL

AND PERFORMANCE

MANAGEMENT

2015-16

PFMA

5

Auditee:

• produced credible and reliable financial

statements that are free of material

misstatements; and

• reported in a useful and reliable manner

on performance as measured against

predetermined objectives in the annual

performance plan (APP); and

• observed/complied with key legislation in

conducting their day-to-day to achieve on

their mandate.

Unqualified opinion with no findings

(clean audit)

Financially unqualified opinion with

findings

Auditee produced financial statements without

material misstatements but struggled to:

• align their performance reports to the

predetermined objectives they committed to

in their APPs; and/or

• set clear performance indicators and targets

to measure their performance against their

predetermined objectives; and/or

• report reliably on whether they achieved their

performance targets; and/or

• determine which legislation they should

comply with and implement the required

policies, procedures and controls to ensure

compliance.

2015-16

PFMA

6

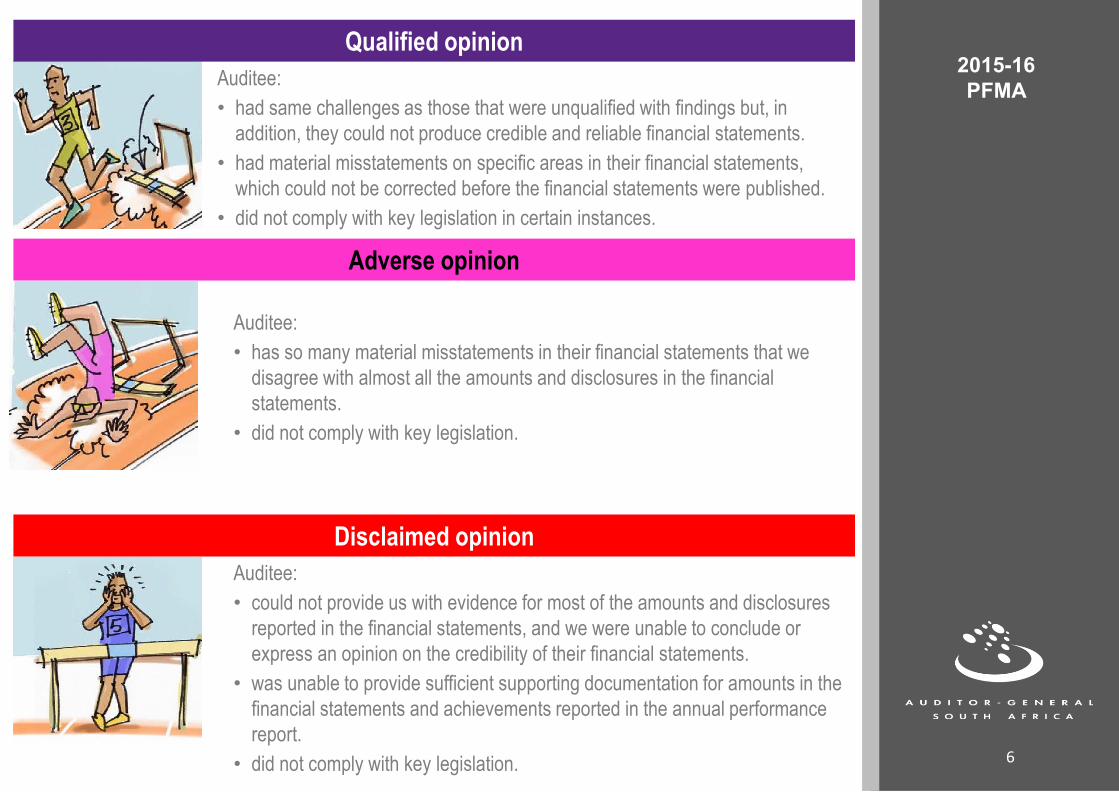

Auditee:

• could not provide us with evidence for most of the amounts and disclosures

reported in the financial statements, and we were unable to conclude or

express an opinion on the credibility of their financial statements.

• was unable to provide sufficient supporting documentation for amounts in the

financial statements and achievements reported in the annual performance

report.

• did not comply with key legislation.

Qualified opinion

Adverse opinion

Disclaimed opinion

Auditee:

• had same challenges as those that were unqualified with findings but, in

addition, they could not produce credible and reliable financial statements.

• had material misstatements on specific areas in their financial statements,

which could not be corrected before the financial statements were published.

• did not comply with key legislation in certain instances.

Auditee:

• has so many material misstatements in their financial statements that we

disagree with almost all the amounts and disclosures in the financial

statements.

• did not comply with key legislation.

2015-16

PFMA

2

2

7

2015-16

PFMA

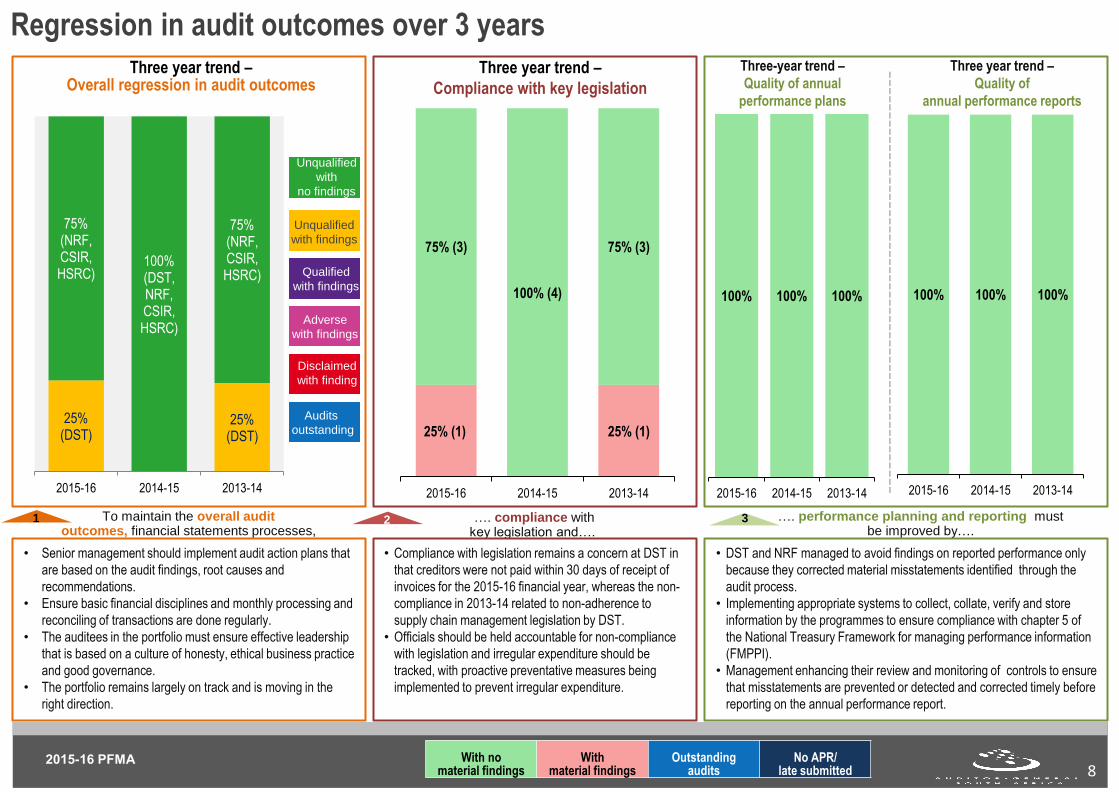

The 2015-16 audit outcomes and key messages

To maintain the overall audit outcomes, financial statements processes,

1 3 …. compliance with key legislation and….

2

Three year trend – Overall regression in audit outcomes

…. performance planning and reporting must be improved by….

25% (DST)

25% (DST)

75% (NRF, CSIR, HSRC)

100% (DST, NRF, CSIR, HSRC)

75% (NRF, CSIR, HSRC)

2015-16 2014-15 2013-14

8

Regression in audit outcomes over 3 years

2015-16 PFMA

• Senior management should implement audit action plans that

are based on the audit findings, root causes and

recommendations.

• Ensure basic financial disciplines and monthly processing and

reconciling of transactions are done regularly.

• The auditees in the portfolio must ensure effective leadership

that is based on a culture of honesty, ethical business practice

and good governance.

• The portfolio remains largely on track and is moving in the

right direction.

• Compliance with legislation remains a concern at DST in

that creditors were not paid within 30 days of receipt of

invoices for the 2015-16 financial year, whereas the non-

compliance in 2013-14 related to non-adherence to

supply chain management legislation by DST.

• Officials should be held accountable for non-compliance

with legislation and irregular expenditure should be

tracked, with proactive preventative measures being

implemented to prevent irregular expenditure.

• DST and NRF managed to avoid findings on reported performance only

because they corrected material misstatements identified through the

audit process.

• Implementing appropriate systems to collect, collate, verify and store

information by the programmes to ensure compliance with chapter 5 of

the National Treasury Framework for managing performance information

(FMPPI).

• Management enhancing their review and monitoring of controls to ensure

that misstatements are prevented or detected and corrected timely before

reporting on the annual performance report.

Three year trend –

Compliance with key legislation

25% (1) 25% (1)

75% (3)

100% (4)

75% (3)

2015-16 2014-15 2013-14

Three-year trend –

Quality of annual

performance plans

Three year trend –

Quality of

annual performance reports

100% 100% 100%

2015-16 2014-15 2013-14

100% 100% 100%

2015-16 2014-15 2013-14

With no material findings

With material findings

Outstanding audits

No APR/ late submitted

Unqualified

with

no findings

Unqualified

with findings

Qualified

with findings

Adverse

with findings

Disclaimed

with finding

Audits

outstanding

----------------------------------------------------

8

DS

T

NR

F

CS

IR

HS

RC

- Audit Action plans

- ICT governance

- Risk management

- Internal Audit

FINANCIAL AND

PERFORMANCE MANAGEMENT

- Oversight responsibility

- Effective HR management

- Policies and procedures

LEADERSHIP

- Effective leadership

- Audit committee

- Proper record keeping

- Daily and monthly controls

- Regular, accurate & complete finanial and

- Review and monitor compliance

- Design and Implement IT controls

GOVERNANCE

Status of Key controls

Good Concerning Intervention required

4 … providing attention to the key controls by…

9

Regression in audit outcomes over 3 years

• Implementing controls at DST to ensure that invoices received are processed and captured timely on

the system for payment.

• Preparing monthly/interim AFS with full disclosures in an effort to reduce the risk of misstatements at

year end.

• Management at DST and NRF by providing adequate oversight on the compliance and related

internal controls surrounding SCM to ensure preventative measures are being implemented. F

irst

leve

l

… the key role players as part of their role in combined assurance

Assurance providers per level

4

4

4

2 2 Senior management

Accounting officer/authority

Executive authority

Internal audit unit

Audit committee

Portfolio committee T

hir

d

leve

l

Sec

on

d

leve

l

Basis for Portfolio Committee evaluation: • Oversight role in terms of robust budget vote process, review of the annual report including the audit

report, quarterly reporting;

• Follow up on progress made by the entities to address poor audit outcomes;

• Recommendations made in relation to key audit matters; and

• Follow up on key matters reported in the committee’s prior year BRRR report.

• The Portfolio committee performed in terms of it’s legislative oversight requirements and it robustly

engages the department and the entities on their role and mandate.

• Senior management of DST and NRF did not follow through on all weaknesses in SCM and

predetermined objectives .

-------------------------------------------------

-------------------------------------------------

Provides assurance

Provides some

assurance

Provides limited/ no assurance

Vacancy Not

established

5

2015-16 PFMA Improved Stagnant Regressed 9

3

3

10

Performance management linked to programmes/ objectives tested

2015-16

PFMA

Quality of submitted annual performance reports after adjustments Outcomes of programmes/objectives selected for testing:

Auditee:

Programmes/

Objectives Usefulness Reliability

Department of

Science and

Technology

Programme 2: Technology innovation No material findings reported.

The department managed to avoid findings on reported

performance only because they corrected material

misstatements identified through the audit process.

Programme 4: Research development

and support No material findings reported. No material findings reported.

National

Research

Foundation

Programme 3: Research and

Innovation Support and

Advancement

No material findings reported.

The entity managed to avoid findings on reported

performance only because they corrected material

misstatements identified through the audit process.

Council for

Scientific and

Industrial

Research

Objective 1 : Scientific and Technical No material findings reported. No material findings reported.

Objective 2 : Learning and growth No material findings reported. No material findings reported.

Human

Sciences

Research

Council

Programme 2 : Research Development

and Innovation No material findings reported. No material findings reported.

2015-16 PFMA No material

findings reported Material

findings reported

4

4

12

Financial management

2015-16

PFMA

Figure 1: Findings on compliance with

key legislation – all auditees

2015-16 2014-15 2013-14

Compliance with legislation and quality of financial statements

Figure 2: Quality of submitted

financial statements

2015-16

Outcome if

NOT corrected

Outcome

after corrections

0 auditees (0%) [2014-15: 0 (%)] avoided qualifications

due to the correction of material misstatements

during the audit process

100% (4)

100% (4)

Outcome if

NOT corrected

Outcome

after corrections

2014-15

100% (4)

100% (4)

With no material misstatements

With material misstatements

2015-16

PFMA

13

25%

25% (DST)

25% (DST)

Management of procurement and/or contracts

Expenditure management (payment within 30 days)

Human Resources Management

Unauthorised, irregular as well as fruitless and wasteful expenditure

decrease over 3 years

14

2015-16

PFMA

R 32 million

R 25 million

R 1 million

R 12 million

Irregular expenditure

Fruitless and wastefulexpenditure

Unauthorisedexpenditure

Expenditure

incurred in

contravention

of key

legislation;

goods

delivered but

prescribed

processes not

followed

Expenditure

not in

accordance

with the

budget vote/

overspending

of budget or

programme

Expenditure

incurred in

vain and

could have

been avoided

if reasonable

steps had

been taken.

No value for

money!

Definition UIFW amounts incurred by entities in portfolio Nature of U.I.FW expenditure R’million

2015-16 2014-15 2013-14

1.00

13.00

10.00

8.00

1.00

22.00

1.00

1.00

1.00

11.00

1.00

Non-compliance with preferentialProcurement Policy Framework Act

Minimum three quotations notobtained/ Competitive bidding

process not followed

Procurement without obtaining validtax clearance certificates

Contracts [and quotations] wereawarded to bidders that did notscore the highest points in the

evaluation process,

Deviations were not approved inaccordance with the SCM policy and

delegations.

Penalties and interest

Irregular expenditure R’million

Fruitless and wasteful expenditure R’million

Follow up action of unauthorised, irregular as well as fruitless and wasteful

expenditure over 3 years

15

2015-16

PFMA Investigations of U.I.FW expenditure

2015-16

100%

3 auditees (100%) [2014-15: 4 (100%)] lodged investigations to determine root cause and consequences of U.I.FW incurred.

DST,

NRF,

HSRC

2014-15

100%

DST,

NRF,

CSIR,

HSRC

Investigated Not investigated

2013-14

100%

DST,

NRF,

HSRC

5

5

16

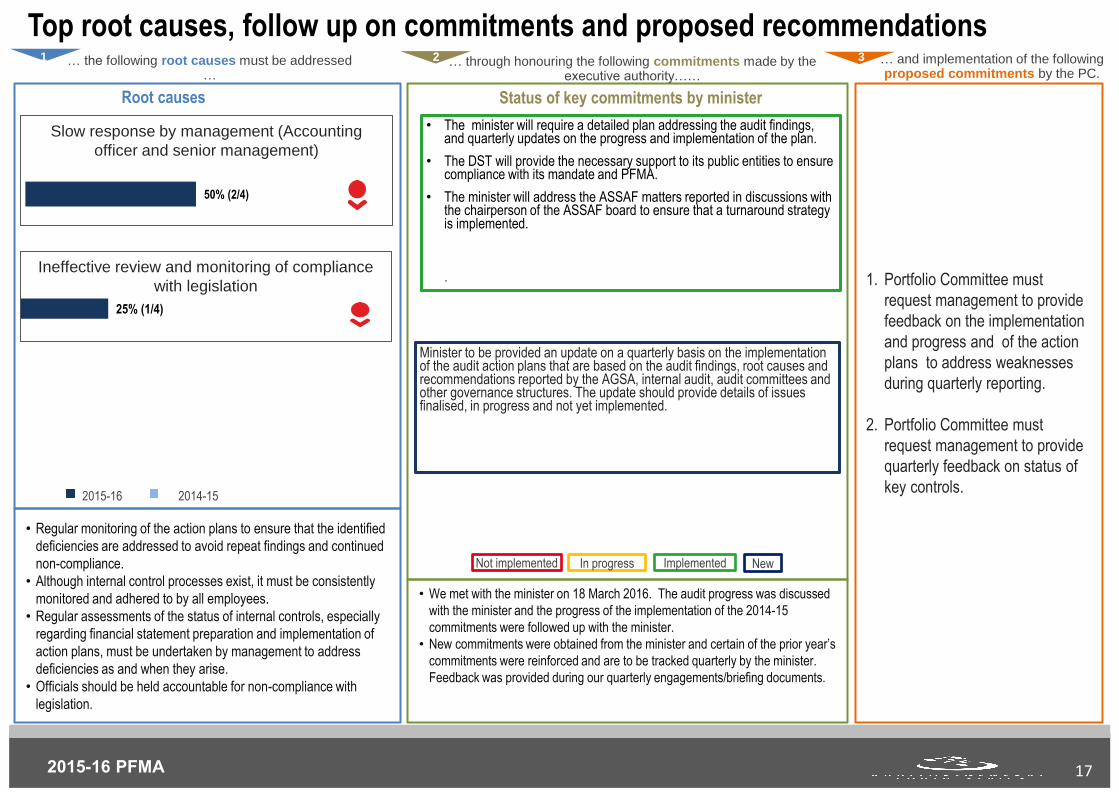

Top root causes, follow up on commitments and proposed

recommendations

2015-16

PFMA

… the following root causes must be addressed …

Root causes

Slow response by management (Accounting

officer and senior management)

Ineffective review and monitoring of compliance

with legislation

Status of key commitments by minister

• The minister will require a detailed plan addressing the audit findings, and quarterly updates on the progress and implementation of the plan.

• The DST will provide the necessary support to its public entities to ensure compliance with its mandate and PFMA.

• The minister will address the ASSAF matters reported in discussions with the chairperson of the ASSAF board to ensure that a turnaround strategy is implemented. .

Minister to be provided an update on a quarterly basis on the implementation of the audit action plans that are based on the audit findings, root causes and recommendations reported by the AGSA, internal audit, audit committees and other governance structures. The update should provide details of issues finalised, in progress and not yet implemented.

Implemented In progress Not implemented New

… through honouring the following commitments made by the executive authority……

2 1

25% (1/4)

50% (2/4)

2015-16 2014-15

17

• Regular monitoring of the action plans to ensure that the identified

deficiencies are addressed to avoid repeat findings and continued

non-compliance.

• Although internal control processes exist, it must be consistently

monitored and adhered to by all employees.

• Regular assessments of the status of internal controls, especially

regarding financial statement preparation and implementation of

action plans, must be undertaken by management to address

deficiencies as and when they arise.

• Officials should be held accountable for non-compliance with

legislation.

• We met with the minister on 18 March 2016. The audit progress was discussed

with the minister and the progress of the implementation of the 2014-15

commitments were followed up with the minister.

• New commitments were obtained from the minister and certain of the prior year’s

commitments were reinforced and are to be tracked quarterly by the minister.

Feedback was provided during our quarterly engagements/briefing documents.

2015-16 PFMA

Top root causes, follow up on commitments and proposed recommendations … and implementation of the following proposed commitments by the PC.

1. Portfolio Committee must

request management to provide

feedback on the implementation

and progress and of the action

plans to address weaknesses

during quarterly reporting.

2. Portfolio Committee must

request management to provide

quarterly feedback on status of

key controls.

3

17

6

6

18

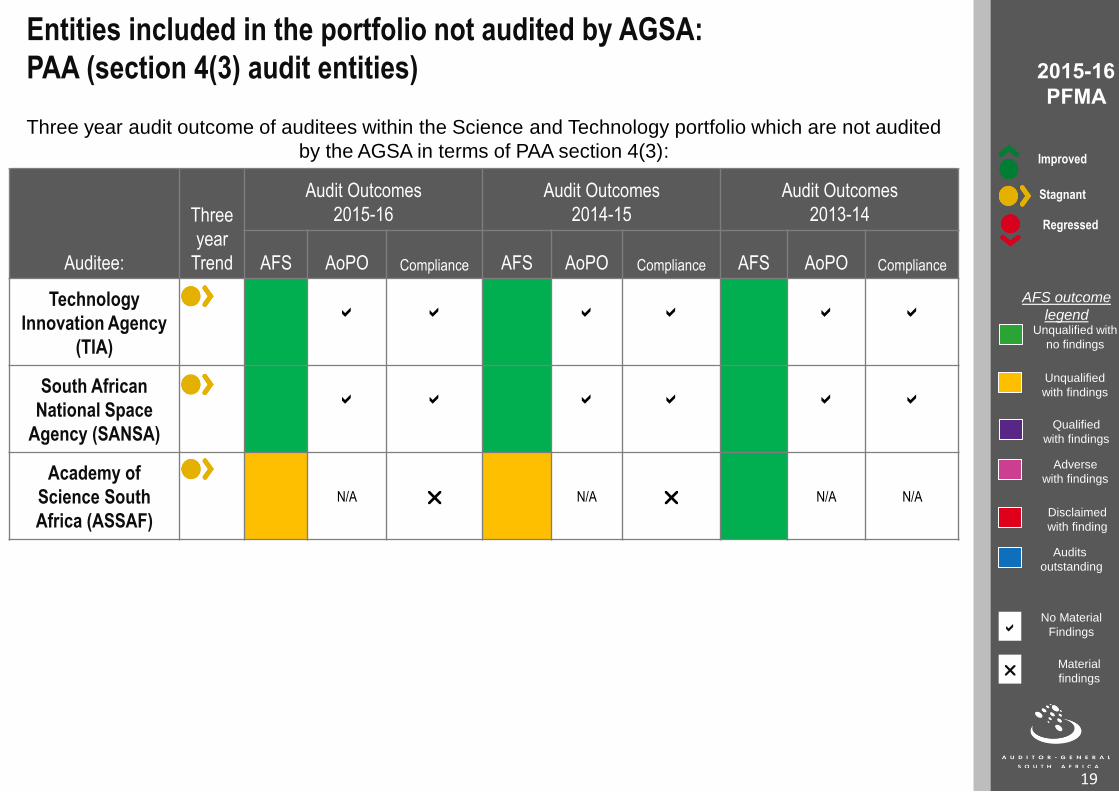

Entities included in the portfolio not audited by AGSA:

PAA section 4(3) audit entities

2015-16

PFMA

Entities included in the portfolio not audited by AGSA:

PAA (section 4(3) audit entities)

Three year audit outcome of auditees within the Science and Technology portfolio which are not audited

by the AGSA in terms of PAA section 4(3):

Auditee:

Three

year

Trend

Audit Outcomes

2015-16

Audit Outcomes

2014-15

Audit Outcomes

2013-14

AFS AoPO Compliance AFS AoPO Compliance AFS AoPO Compliance

Technology

Innovation Agency

(TIA)

a

a

a

a

a

a

South African

National Space

Agency (SANSA)

a

a

a

a

a

a

Academy of

Science South

Africa (ASSAF)

N/A

r

N/A

r

N/A

N/A

19

2015-16

PFMA

Improved

Stagnant

Regressed

AFS outcome

legend Unqualified with

no findings

Unqualified

with findings

Qualified

with findings

Adverse

with findings

Disclaimed

with finding

Audits

outstanding

No Material

Findings

Material

findings

a

r

20

2015-16

PFMA

Questions

Follow the AGSA on Twitter: https://twitter.com/AuditorGen_SA

www.agsa.co.za

Auditor-General of South Africa