Embed Size (px)

Citation preview

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

Fabio BarbosaFabio BarbosaSecretary of the National TreasurySecretary of the National Treasury

Inter-American Development BankInter-American Development Bank Washington,D.C., April 2001 Washington,D.C., April 2001

FEDERATIVE REPUBLIC of BRAZILMinistry of Finance - National Treasury Secretariat

1.1. Adjustment and Reforms Towards a New Fiscal RegimeAdjustment and Reforms Towards a New Fiscal Regime

2.2. Public Debt ManagementPublic Debt Management

3.3. OutlookOutlook

1.1. Adjustment and Reforms Towards a New Fiscal RegimeAdjustment and Reforms Towards a New Fiscal Regime

2.2. Public Debt ManagementPublic Debt Management

3.3. OutlookOutlook

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

BRAZILIAN ECONOMY: OVERCOMING MAJOR CHALLENGESBRAZILIAN ECONOMY: OVERCOMING MAJOR CHALLENGES

– Macroeconomic Stabilization;

– International Crises : Mexico, Asia, Russia;

– Remarkable transition to the floating exchange rate regime:

# Inflation Targeting framework: successful implementation;# Inflation Targeting framework: successful implementation;

# Balance of Payments Adjustment:# Balance of Payments Adjustment:

** Despite the world’s economy slowdown, ** Despite the world’s economy slowdown, exports have been exports have been growing at impressive rates (March growing at impressive rates (March 01 = 15,5%);01 = 15,5%);

** Current Account Deficit financed through ** Current Account Deficit financed through FDI;FDI;

# Economy has rebounded; unemployment is declining;# Economy has rebounded; unemployment is declining;

# New Fiscal Regime:# New Fiscal Regime:

** Strong primary flows; Structural Reforms.** Strong primary flows; Structural Reforms.

Inflation Targeting FrameworkInflation Targeting FrameworkConsumer Price Index - IPCA (Annual % )Consumer Price Index - IPCA (Annual % )

8,94%

7,86%

2,00%3,00%4,00%5,00%6,00%7,00%8,00%9,00%

10,00%11,00%

1998 1999 2000 2001 2002

target observed max. bias

0

2

4

6

8

10

12

1999 2000 2001

Ceiling Central Point Floor Observed

Current Account Deficit X FDICurrent Account Deficit X FDI1994 a 2001* ( US$ Billion)1994 a 2001* ( US$ Billion)

Current Account Deficit X FDICurrent Account Deficit X FDI1994 a 2001* ( US$ Billion)1994 a 2001* ( US$ Billion)

* * 2001: Accumulated 12 months ended in March.2001: Accumulated 12 months ended in March.

Current AccountCurrent Account FDIFDI

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

1994 1995 1996 1997 1998 1999 2000 2001

GDP Growth: 1990 - 2000GDP Growth: 1990 - 2000 GDP Growth: 1990 - 2000GDP Growth: 1990 - 2000

5,200

5,400

5,600

5,800

6,000

6,200

6,400

6,600

6,8001

99

0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

R$

pe

r h

ea

d (

20

00

)

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Re

al G

row

th r

ate

( %

)

Unemployment RateUnemployment RateIBGE Monthly Employment ResearchIBGE Monthly Employment Research

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

Jan-

97

Mar

-97

May

-97

Jul-9

7

Sep

-97

Nov

-97

Jan-

98

Mar

-98

May

-98

Jul-9

8

Sep

-98

Nov

-98

Jan-

99

Mar

-99

May

-99

Jul-9

9

Sep

-99

Nov

-99

Jan-

00

Mar

-00

May

-00

Jul-0

0

Sep

-00

Nov

-00

Jan-

01

%

Central Govt. (1994-1998) Overall Public Sector (1999-2001)

% P

IB

Primary Results - 1995-2000Primary Results - 1995-2000 Primary Results - 1995-2000Primary Results - 1995-2000

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Dec/95 Dec/96 Dec/97 Dec/98 Dec/99 Dec/00 March,2001

Actual Targets

BRAZIL: A NEW FISCAL REGIMEBRAZIL: A NEW FISCAL REGIME

TOTAL

EM

EE

GC

Net PuNet Public Sector Debtblic Sector Debt

SourceSource: : Central Bank

9.4 10.4

3130.426

18.815.9

1312.111.6

13 14.716.4 16.3

2.22.82.72.85.96.56.6

49.549.743.3

34.633.4

29.928.1

0

10

20

30

40

50

60

1994 1995 1996 1997 1998 1999 2000

% G

DP

Strong primary flows must be seen as an integral part of the Strong primary flows must be seen as an integral part of the comprehensive structural reforms agenda, which has been comprehensive structural reforms agenda, which has been implemented in the last few years.implemented in the last few years.

The “fundamentals” of Brazil’s New Fiscal Regime: The “fundamentals” of Brazil’s New Fiscal Regime:

– Privatization

– Administrative Reform

– Social Security Reform

– State & Municipalities Refinancing Agreements

– Fiscal Responsibility Law

BRAZIL: A NEW FISCAL REGIMEBRAZIL: A NEW FISCAL REGIME

Privatization:Privatization:

– Since 1991: About US$ 100,4 billion:

(*) Proceeds: US$ 82,3 billion (mostly to amortize public (*) Proceeds: US$ 82,3 billion (mostly to amortize public debt)debt)

(*) Debt Transferred: US$ 18,1 billion.(*) Debt Transferred: US$ 18,1 billion.

– Positive effects go far beyond debt reduction:

(*) Elimination of potential deficits (capitalization, subsidies);(*) Elimination of potential deficits (capitalization, subsidies);

(*) Important role in FDI flows;(*) Important role in FDI flows;

(*) Productivity and efficiency gains;(*) Productivity and efficiency gains;

(*) New players in domestic capital markets.(*) New players in domestic capital markets.

BRAZIL: A NEW FISCAL REGIMEBRAZIL: A NEW FISCAL REGIME

Fonte: Banco Central

NET PUBLIC SECTOR DEBT

32

42

52

1996 1997 1998 1999 2000

GDP

%

After Privatization

Without Privatization

BRAZIL: A NEW FISCAL REGIMEBRAZIL: A NEW FISCAL REGIME

Source: Central Bank

8.55%

8.14%

0%

2%

4%

6%

8%

10%

% G

DP

(accum

ula

ted)

1995 1996 1997 1998 1999 2000

BRAZIL: A NEW FISCAL REGIMEBRAZIL: A NEW FISCAL REGIME

Administrative Reform:Administrative Reform:

– Elimination of general job tenure;

– Flexible legal regime for civil servants;

– Legislative/Judiciary: Salary increases must be approved by Congress.

Social Security Reform:Social Security Reform:

– Retirement: “Time of Service” replaced by “Time of Contribution”;

– “Benefit Adjustment Factor”: link with minimum age requirements;

– Elimination of the partial benefit at early retirement;

– New regulatory framework for pension funds; public sector contribution as sponsor cannot be higher than civil servants’;

– Retired civil servants contribution (Constitutional Amendment )

BRAZIL: A NEW FISCAL REGIMEBRAZIL: A NEW FISCAL REGIME

State & Municipalities Refinancing Agreements:State & Municipalities Refinancing Agreements:

– 25 out of 27 states, 180 municipalities; US$ 130 billion program; no arrears;

– Main Aspects:

# Debt Service Ceiling = 13% of Net Current Revenue (NCR);# Debt Service Ceiling = 13% of Net Current Revenue (NCR);

# Debt Stock Ceiling equivalent to 100% of NCR;# Debt Stock Ceiling equivalent to 100% of NCR;

# Fiscal Programs, annually revised : Targets for primary surplus, # Fiscal Programs, annually revised : Targets for primary surplus, payroll, total debt;payroll, total debt;

# Multi-annual Debt/NCR trajectory; no “new money” while Debt/NCR > # Multi-annual Debt/NCR trajectory; no “new money” while Debt/NCR > 1;1;

# Implementation of Privatization Programs: responded for 30% total # Implementation of Privatization Programs: responded for 30% total results;results;

# State Banks: privatization, closing, transformation into development # State Banks: privatization, closing, transformation into development agencies (BANERJ, BEMGE, CREDIREAL, BANESPA);agencies (BANERJ, BEMGE, CREDIREAL, BANESPA);

# Incentives to the establishment of balanced pension funds (RJ, PE, # Incentives to the establishment of balanced pension funds (RJ, PE, PR)PR)..

Primary Results (% GDP)1995-2000Primary Results (% GDP)1995-2000States, Municipalities and State EnterprisesStates, Municipalities and State Enterprises

-0.8-0.6-0.4-0.20.00.20.4

0.60.81.0

Dec/95 Dec/96 Dec/97 Dec/98 Dec/99 Dec/00

State&Municipalities Enterprises

BRAZIL: A NEW FISCAL REGIME

Fiscal Responsibility Law: Milestone in Fiscal ManagementFiscal Responsibility Law: Milestone in Fiscal Management

Art.35: No more refinancing between different levels of government;Art.35: No more refinancing between different levels of government;

Budget Guidelines Law (LDO): 3-years targets for fiscal policy;Budget Guidelines Law (LDO): 3-years targets for fiscal policy;

Allows for expenditure cuts in other branches of government;Allows for expenditure cuts in other branches of government;

Debt ceilings for the three levels of governmentDebt ceilings for the three levels of government

– Federal Government: 3,5 NCR, effective immediately; – States: 2 NCR; Municipalities 1,2 NCR;

Convergence period: 15 yearsConvergence period: 15 years;; Implicit reduction of S&M net debt (as of Dec. 2000, 16,3% of the GDP)Implicit reduction of S&M net debt (as of Dec. 2000, 16,3% of the GDP)

No budget commitment without effective funding; No budget commitment without effective funding;

Transparency: reports on fiscal management, budget execution, etc.Transparency: reports on fiscal management, budget execution, etc.

BRAZIL: A NEW FISCAL REGIMEBRAZIL: A NEW FISCAL REGIME

In sum:In sum:

– A comprehensive structural reforms agenda has been implemented.

– The impressive shift in primary flows (about 5% of the GDP if compared to 1997) consolidates the new fiscal regime, thus enhancing the consistency of the Brazilian economic policy :

– (*)TARGETS MET FOR 10 CONSECUTIVE QUARTERS

Sound macroeconomic policies pave the way to:Sound macroeconomic policies pave the way to:

– A more proactive public debt management strategy;

– Development of domestic capital markets.

1.1. Adjustment and Reforms Towards a New Fiscal RegimeAdjustment and Reforms Towards a New Fiscal Regime

2.2. Public Debt ManagementPublic Debt Management

3.3. OutlookOutlook

1.1. Adjustment and Reforms Towards a New Fiscal RegimeAdjustment and Reforms Towards a New Fiscal Regime

2.2. Public Debt ManagementPublic Debt Management

3.3. OutlookOutlook

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

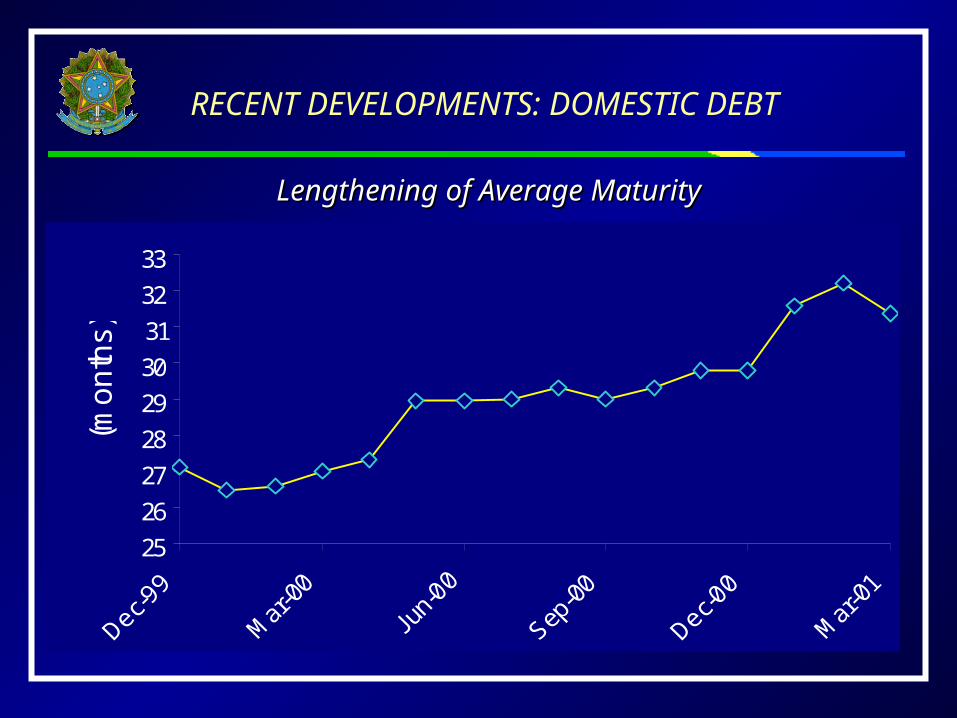

DOMESTIC DEBT:

Maturity lengthening process: reduction of refinancing risk;

Duration: Gradual replacement of floating rate by fixed rate securities;

Rebuilding of domestic yield curve: Fixed rate (LTN): short term benchmarks: up to 2 yearsFloating rate (LFT): 5 yearsIndexed bonds (NTN-C): (3,5,7,10,20 and 30 years)

Standardization of debt instruments; fungibility for floating rate securities; re-offer;

PUBLIC DEBT MANAGEMENTGuidelines

EXTERNAL DEBT

Establishment/consolidation of yield curves in strategic markets; benchmarks in dollar, euro and yen;

Provide and enhance access for other borrowers to the international capital markets;

Gradual substitution of restructured debt (Bradies, Paris Club) by market instruments;

Broadening of the investors base in Brazilian risk.

PUBLIC DEBT MANAGEMENTGuidelines

Lengthening of Average MaturityLengthening of Average Maturity

RECENT DEVELOPMENTS: DOMESTIC DEBT

25

26

27

28

29

30

31

32

33

(mo

nth

s)

% of Total Debt Maturing in 12 months

RECENT DEVELOPMENTS: DOMESTIC DEBT

36

41

46

51

56D

ec-

99

Mar

-00

Jun-

00

Sep-

00

Dec

-00

Mar

-01

%

Replacement of floating rate by fixed rate securities

0%

20%

40%

60%

80%

100%

Jan-

95

May

-95

Sep-

95

Jan-

96

May

-96

Sep-

96

Jan-

97

May

-97

Sep-

97

Jan-

98

May

-98

Sep-

98

Jan-

99

May

-99

Sep-

99

Jan-

00

May

-00

Sep-

00

RECENT DEVELOPMENTS: DOMESTIC DEBT

Reduction of Average Funding Cost - Domestic Bonded DebtReduction of Average Funding Cost - Domestic Bonded Debt

% p.a.

0

10

20

30

40

50

1995 1996 1997 1998 1999 2000

External Debt: Yield CurvesExternal Debt: Yield Curves

Sovereign Bonds Outstanding - Dollar, Euro and YenAs of 04/17/01

0

2

4

6

8

10

12

14

16Dollar

Euro

Yen

EXTERNAL DEBTEXTERNAL DEBT

Source: National Treasury Secretariat

Structure by Holders- Feb/2001

Currency Composition - Feb/2001

Stock outstanding in March /2001

13,6% PIB

Bônus de Captação

40%

Bradies34%

Organismos Multilaterais

12%Clube de Paris

9%

Bancos Privados/Ag.

Govern.5%

Dólar81%

Euro7%

Iene4%

Outros8%

ANNUAL BORROWING PLAN (ABP) STRATEGY FOR 2001

Basic Parameters:Basic Parameters:

Projected Debt Service 2001 *: R$ 201,8 billionProjected Debt Service 2001 *: R$ 201,8 billion

Fiscal resources budgeted Fiscal resources budgeted: R$ 54,4 bilhões: R$ 54,4 bilhões

Gross Borrowing Requirements: R$ 147,4 bilhões Gross Borrowing Requirements: R$ 147,4 bilhões

Hipotheses: Hipotheses:

a) 100% roll-over of dollar linked securitiesa) 100% roll-over of dollar linked securities; and; and

b)b) bond issuance in international capital markets: bond issuance in international capital markets: US$ 6 billion US$ 6 billion

** As of December 31, 2000As of December 31, 2000

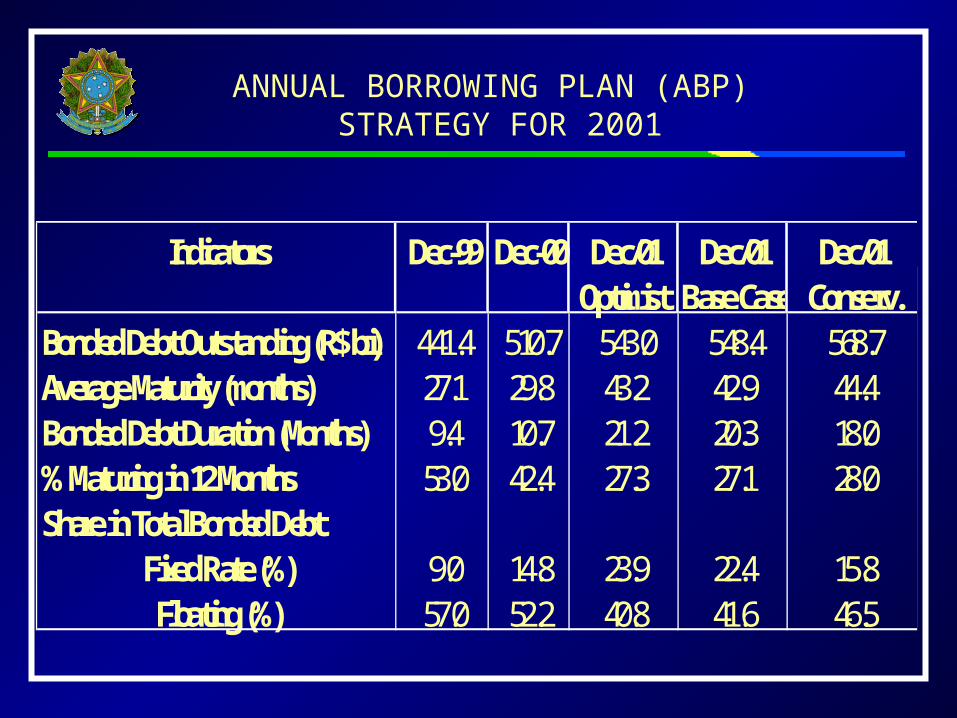

ANNUAL BORROWING PLAN (ABP) STRATEGY FOR 2001

Indicators Dec-99 Dec-00 Dec/01 Dec/01 Dec/01Optimist Base Case Conserv.

Bonded Debt Outstanding (R$ bi) 441.4 510.7 543.0 548.4 568.7Average Maturity (months) 27.1 29.8 43.2 42.9 44.4Bonded Debt Duration (Months) 9.4 10.7 21.2 20.3 18.0% Maturing in 12 Months 53.0 42.4 27.3 27.1 28.0Share in Total Bonded Debt

Fixed Rate (%) 9.0 14.8 23.9 22.4 15.8Floating (%) 57.0 52.2 40.8 41.6 46.5

ANNUAL BORROWING PLAN (ABP) STRATEGY FOR 2001

Estimated Results (Base Case)

Bonded Debt Composition (Dec/00)

Câmbio22%

Índice de Preços

6%

Selic52%

Prefixada15%

TR e Outros

5%

Bonded Debt Composition (Dec/01)

Câmbio22%

Índice de Preços

8%Selic42%

Prefixada22%

TR e Outros

6%

ANNUAL BORROWING PLAN (ABP) 1st. Quarter Results

Indicators 1st Quarter 01 1st Quarter 01 Dec-01ABP Observed ABP

Bonded Debt Outst. (R$ billion) 533.7 536.5 548.4Average Maturity (months) 31.9 31.3 42.9Bonded Debt Duration (Months) 12.9 13.4 20.3% Maturing in 12 Months 43.4 39.5 27.1Share in Total Bonded Debt Fixed Rate (%) 16.2 14.1 22.4 Floating (%) 50.2 50.1 41.6

ANNUAL BORROWING PLAN (ABP) 1st. Quarter Results

26,865

11,000 7,197

-

10,000

20,000

30,000

40,000

LTN LFT NTN-C

Indicative Volumes - Public OfferR$ Billion

MÁX (PAF)

MÉD (PAF)

MÍN (PAF)Realizado

1.1. Adjustment and Reforms Towards a New Fiscal RegimeAdjustment and Reforms Towards a New Fiscal Regime

2.2. Public Debt ManagementPublic Debt Management

3.3. OutlookOutlook

1.1. Adjustment and Reforms Towards a New Fiscal RegimeAdjustment and Reforms Towards a New Fiscal Regime

2.2. Public Debt ManagementPublic Debt Management

3.3. OutlookOutlook

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

OUTLOOKOUTLOOK

GDP Growth:GDP Growth:– Average 2000/2002: above 4.0% p.a.;– Further decline of unemployment rate:

Average Rate in 2001 below 7.0% (1999, 7.6% - 2000, 7.1%);Average Rate in 2001 below 7.0% (1999, 7.6% - 2000, 7.1%);

Balance of Payments:Balance of Payments:– Current Account Deficit: close to 2000 level, mostly (80%)

financed through FDI;

Inflation:Inflation:– IPCA 2001 = 4.0% (+ ou - 2.0%)IPCA 2001 = 4.0% (+ ou - 2.0%)

– IPCA 2002 = 3.5% (+ ou - 2.0%) IPCA 2002 = 3.5% (+ ou - 2.0%)

OUTLOOK (cont.)OUTLOOK (cont.)Fiscal Policy:Fiscal Policy:

– Structural adjustment: reforms implemented;– Privatization/IPO/concessions;– Annual Primary Surpluses: 2001 to 2004: 3.0% of the GDP– 6 consecutive years:primary surpluses of,at least, 3.0 % of the

GDP.

Primary Result - Public Sector* (%GDP)Primary Result - Public Sector* (%GDP)

*Primary Surplus for 2004 in LDO 2001 considers the same trend observed between 2002 and *Primary Surplus for 2004 in LDO 2001 considers the same trend observed between 2002 and 20032003

2 . 0 0

2 . 2 0

2 . 4 0

2 . 6 0

2 . 8 0

3 . 0 0

3 . 2 0

3 . 4 0

2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4

L D O 2 0 0 1 L D O 2 0 0 2

OUTLOOK (cont.)OUTLOOK (cont.)

Public Debt ManagementPublic Debt Management

– Average Maturity Lengthening: Dec/2001 = 42,9 months

– Duration: gradual increase of share and average maturity of fixed rate instruments;

– Consolidation of long term benchmarks ( NTN-C):

Focus on intermediate maturities (today’s auction - 20yr;10.7%p.a.)Focus on intermediate maturities (today’s auction - 20yr;10.7%p.a.)

Standardization of debt instrumentsStandardization of debt instruments..

– Internet Sales : Small investor, enhancing perception about public debt (Brazilian Treasuries: a first class asset).

OUTLOOK (cont.)OUTLOOK (cont.)

Economic Policy: Consistency, Flexibility and ReactionEconomic Policy: Consistency, Flexibility and Reaction

Recent Turbulences: Recent Turbulences:

– Fundamentals must prevail;

Immediate Policy Response:Immediate Policy Response:

– Primary surplus targets increase for 2002/2004 (LDO for 2002);

– Tightening of monetary policy; exchange rate flexibility;

– Tactical adjustment of auctions schedulle.

BRAZIL: RECENT DEVELOPMENTS IN FISCAL BRAZIL: RECENT DEVELOPMENTS IN FISCAL POLICY AND PUBLIC DEBT MANAGEMENTPOLICY AND PUBLIC DEBT MANAGEMENT

Fabio BarbosaFabio BarbosaSecretary of the National TreasurySecretary of the National Treasury

Inter-American Development BankInter-American Development Bank Washington-DC, April de 2001 Washington-DC, April de 2001

FEDERATIVE REPUBLIC of BRAZILMinistry of Finance - National Treasury Secretariat