Embed Size (px)

DESCRIPTION

Brazil: Economic Ooutlook, Opportunities and Challenges. Andrea Goldstein. Brazil has resumed growth after a long hibernation, and is bound to grow above the global average over the coming years. GDP per capita (constant prices 2009). GDP per capita has been increasing since 2004 - PowerPoint PPT Presentation

Citation preview

1

Brazil: Economic Ooutlook,

Opportunities and Challenges

Andrea Goldstein

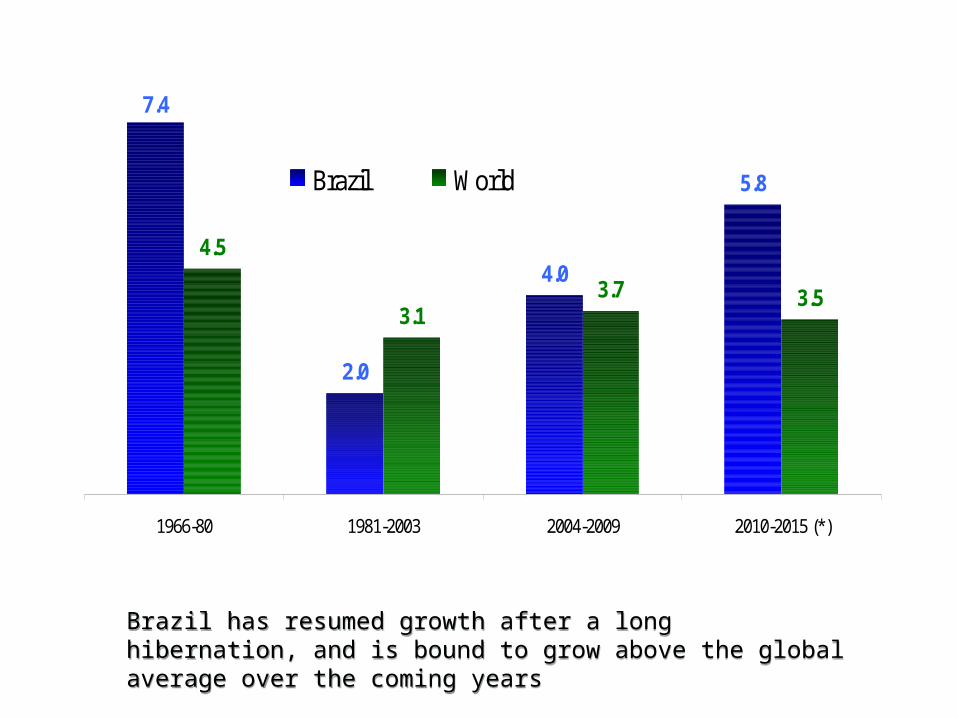

7.4

2.0

4.0

5.8

4.5

3.13.7 3.5

1966-80 1981-2003 2004-2009 2010-2015 (*)

Brazil World

Brazil has resumed growth after a long hibernation, and is bound to grow above the global average over the coming yearsBrazil has resumed growth after a long hibernation, and is bound to grow above the global average over the coming years

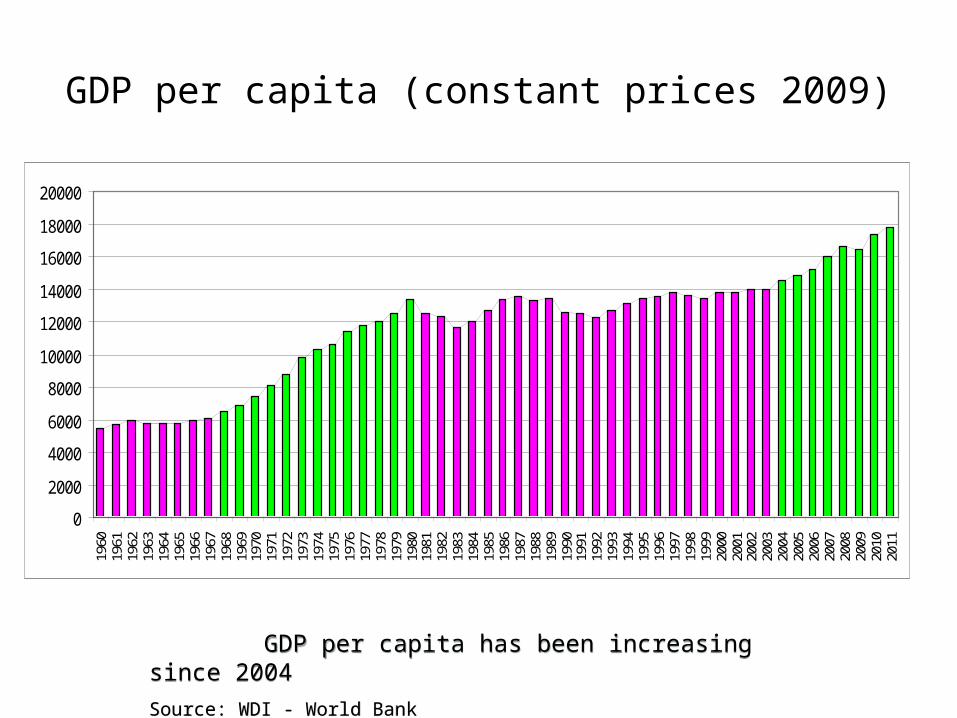

GDP per capita (constant prices 2009)

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

GDP per capita has been increasing since 2004

Source: WDI - World Bank

GDP per capita has been increasing since 2004

Source: WDI - World Bank

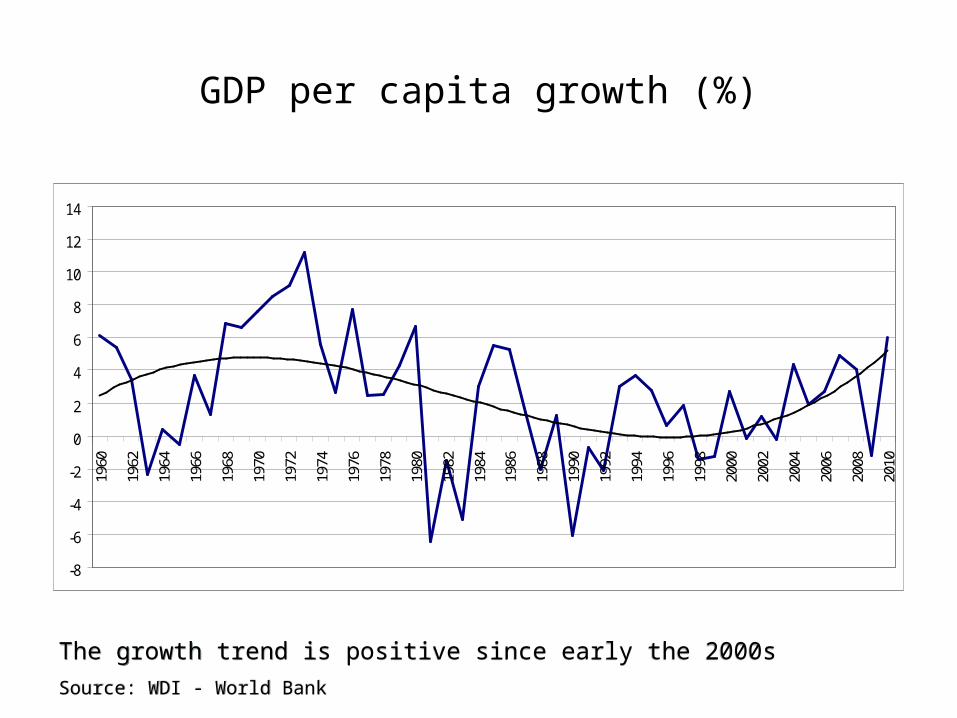

GDP per capita growth (%)

-8

-6

-4

-2

0

2

4

6

8

10

12

14

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

The growth trend is positive since early the 2000s

Source: WDI - World Bank

The growth trend is positive since early the 2000s

Source: WDI - World Bank

5

Schooling5,

1 6,2

6,2 6,5 7,

5

7,5 8,

2

8,4 9,

1

9,3 9,

8 10,1 11

,2

11,3

21,4

19,2

10,7

18,2

17,2

23,0

15,5

14,9

19,7

6,9

12,6

11,0

5,6

13,0

0

5

10

15

20

25

Schooling 15+ in 2010 Growth rate 2000-2010

Source: Barro and Lee 2011

Productivity – growth rate 2000-2009

0,7

9,1

5,2

4,1

0,4

5,2

2,8

4,8

0

1

2

3

4

5

6

7

8

9

10

Brazil China India Russia

Labor productivity Total factor productivity

Source: Wilson 2011

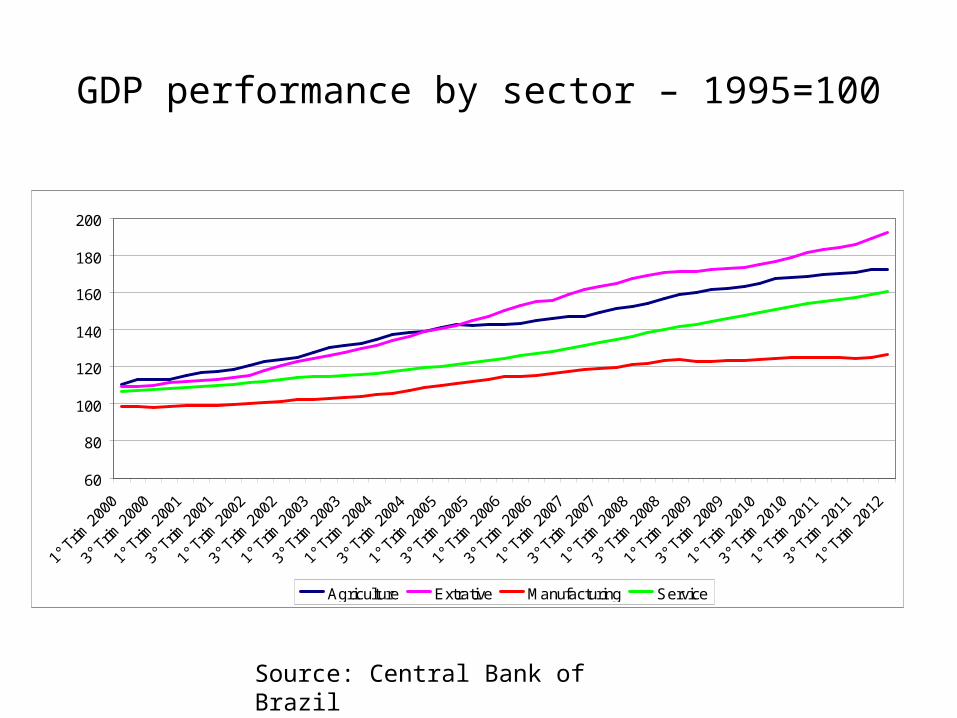

GDP performance by sector – 1995=100

60

80

100

120

140

160

180

200

1° T

rim.2

000

3° T

rim.2

000

1° T

rim.2

001

3° T

rim.2

001

1° T

rim.2

002

3° T

rim.2

002

1° T

rim.2

003

3° T

rim.2

003

1° T

rim.2

004

3° T

rim.2

004

1° T

rim.2

005

3° T

rim.2

005

1° T

rim.2

006

3° T

rim.2

006

1° T

rim.2

007

3° T

rim.2

007

1° T

rim.2

008

3° T

rim.2

008

1° T

rim.2

009

3° T

rim.2

009

1° T

rim.2

010

3° T

rim.2

010

1° T

rim.2

011

3° T

rim.2

011

1° T

rim.2

012

Agriculture Extrative Manufacturing Service

Source: Central Bank of Brazil

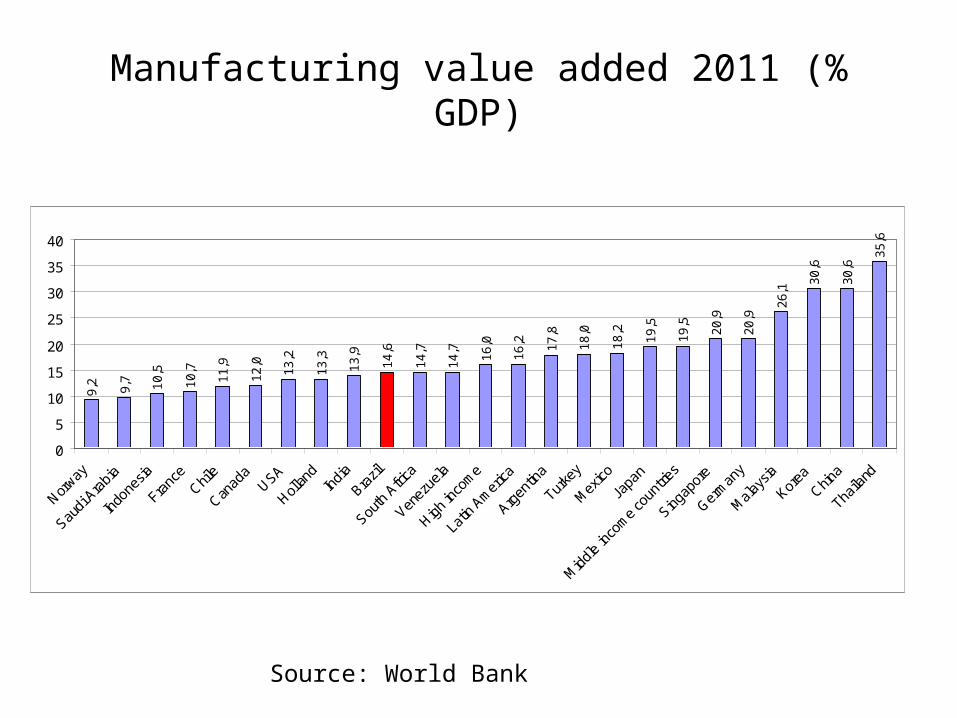

Manufacturing value added 2011 (% GDP)

Source: World Bank

9,2 9,7 10

,5

10

,7

11

,9

12

,0

13

,2

13

,3

13

,9

14

,6

14

,7

14

,7

16

,0

16

,2 17

,8

18

,0

18

,2

19

,5

19

,5

20

,9

20

,9

26

,1

30

,6

30

,6

35

,6

0

5

10

15

20

25

30

35

40

Norway

Saudi

Ara

bia

Indo

nesia

Franc

eChil

e

Canad

aUSA

Hollan

dIn

dia

Brazil

South

Afri

ca

Venez

uela

High in

com

e

Latin

Am

erica

Argen

tina

Turke

y

Mex

ico

Japa

n

Mid

dle in

com

e co

untri

es

Singap

ore

Germ

any

Mal

aysia

Korea

China

Thaila

nd

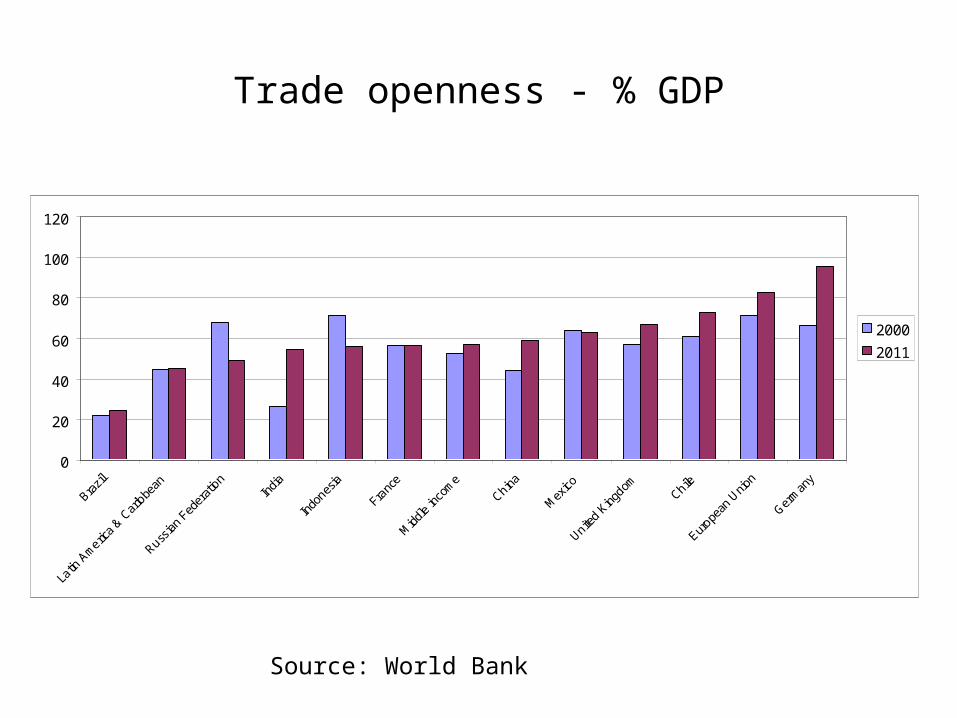

Trade openness - % GDP

0

20

40

60

80

100

120

Brazil

Latin

Americ

a & C

arib

bean

Russian

Fed

erat

ionIn

dia

Indo

nesia

Franc

e

Midd

le inc

ome

China

Mex

ico

United K

ingdom

Chile

Europe

an U

nion

Germ

any

2000

2011

Source: World Bank

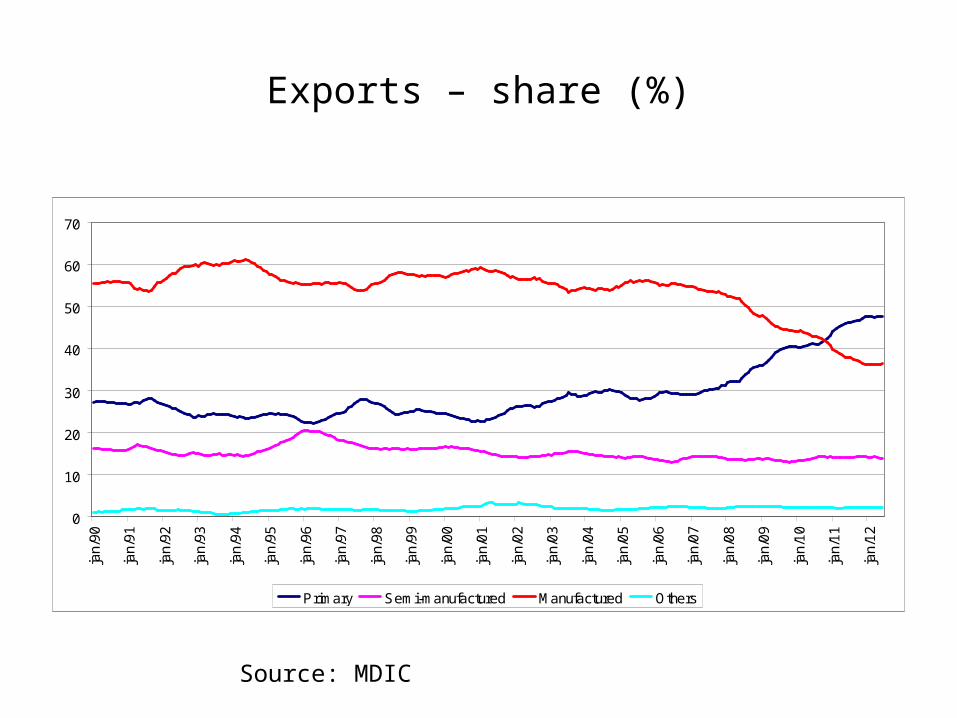

Exports – share (%)

0

10

20

30

40

50

60

70

jan

/90

jan

/91

jan

/92

jan

/93

jan

/94

jan

/95

jan

/96

jan

/97

jan

/98

jan

/99

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

Primary Semi-manufactured Manufactured Others

Source: MDIC

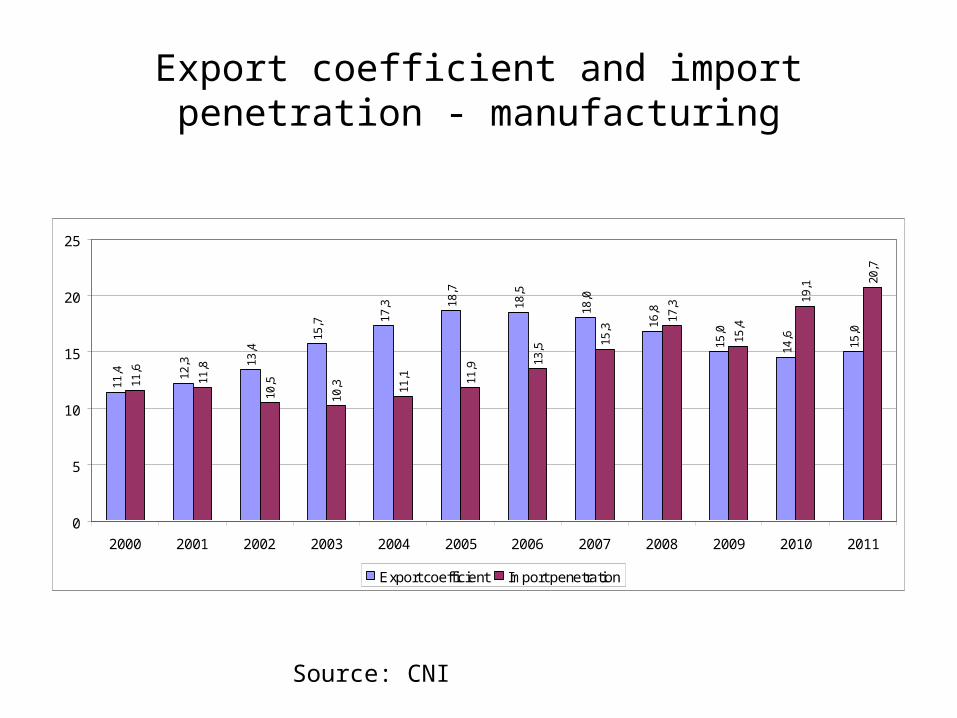

Export coefficient and import penetration - manufacturing

11,4 12

,3 13,4

15,7 17

,3 18,7

18,5

18,0

16,8

15,0

14,6

15,0

11,6

11,8

10,5

10,3 11

,1 11,9 13

,5

15,3

17,3

15,4

19,1 20

,7

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Export coefficient Import penetration

Source: CNI

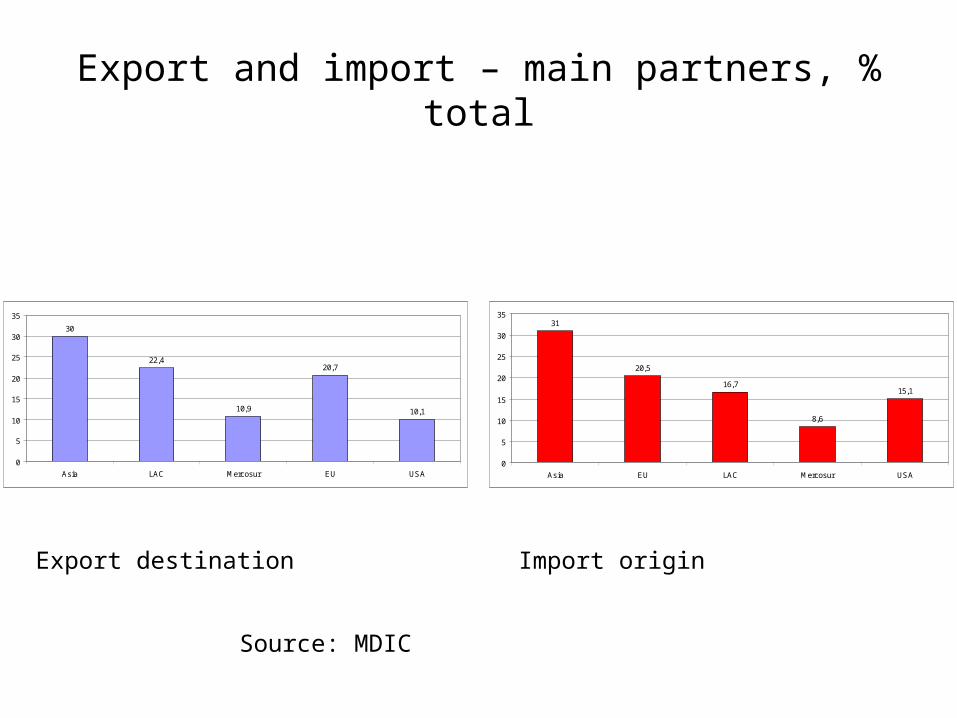

Export and import – main partners, % total

30

22,4

10,9

20,7

10,1

0

5

10

15

20

25

30

35

Asia LAC Mercosur EU USA

31

20,5

16,7

8,6

15,1

0

5

10

15

20

25

30

35

Asia EU LAC Mercosur USA

Source: MDIC

Export destination Import origin

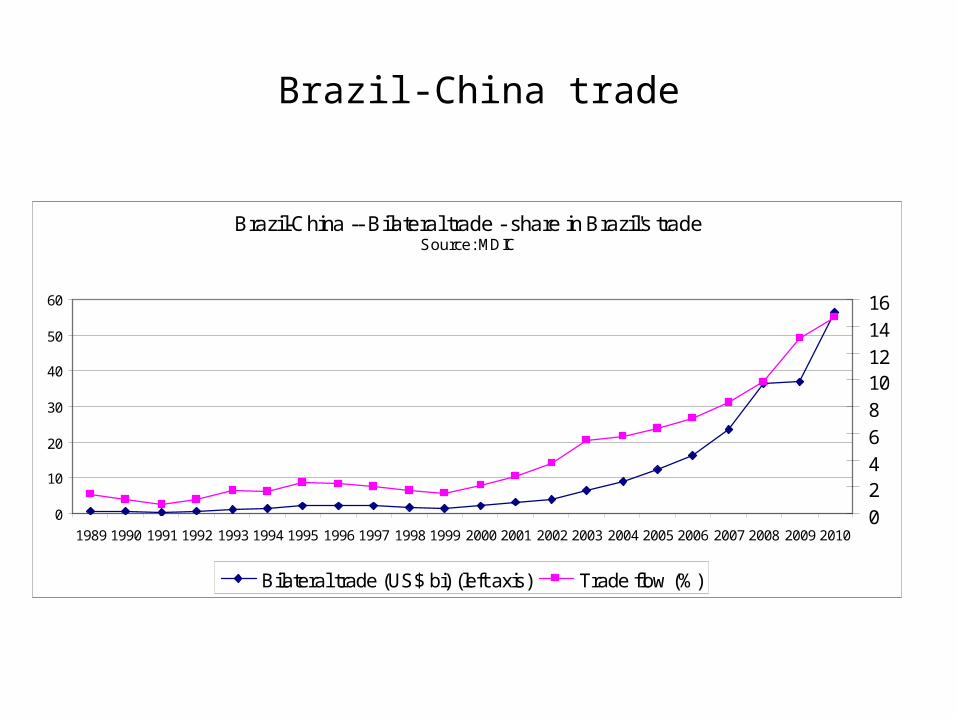

Brazil-China trade

Brazil-China -- Bilateral trade - share in Brazil's tradeSource: MDIC

0

10

20

30

40

50

60

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20100

24

6

8

1012

14

16

Bilateral trade (US$ bi) (left axis) Trade flow (%)

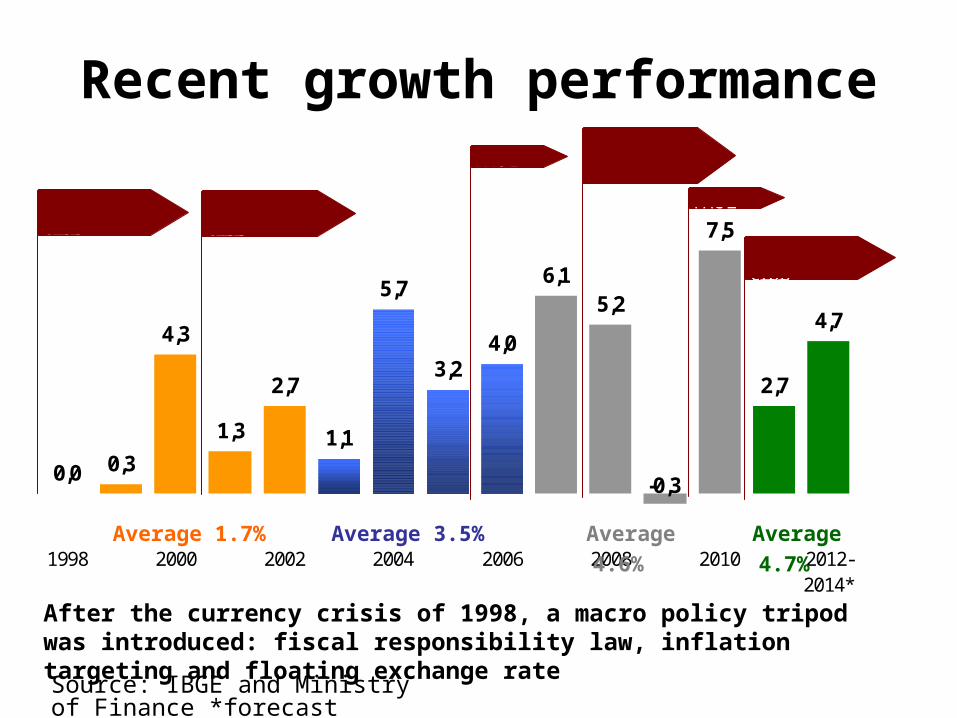

Recent growth performance

Source: IBGE and Ministry of Finance *forecast

0,3

4,3

1,3

2,7

1,1

5,7

3,2

6,15,2

7,5

2,7

0,0

4,04,7

-0,3

1998 2000 2002 2004 2006 2008 2010 2012-2014*

PAC 1

PAC 2

International Crisis

International Crisis

International Crisis

International Crisis

Average 1.7% Average 3.5% Average 4.6% Average 4.7%

After the currency crisis of 1998, a macro policy tripod was introduced: fiscal responsibility law, inflation targeting and floating exchange rate

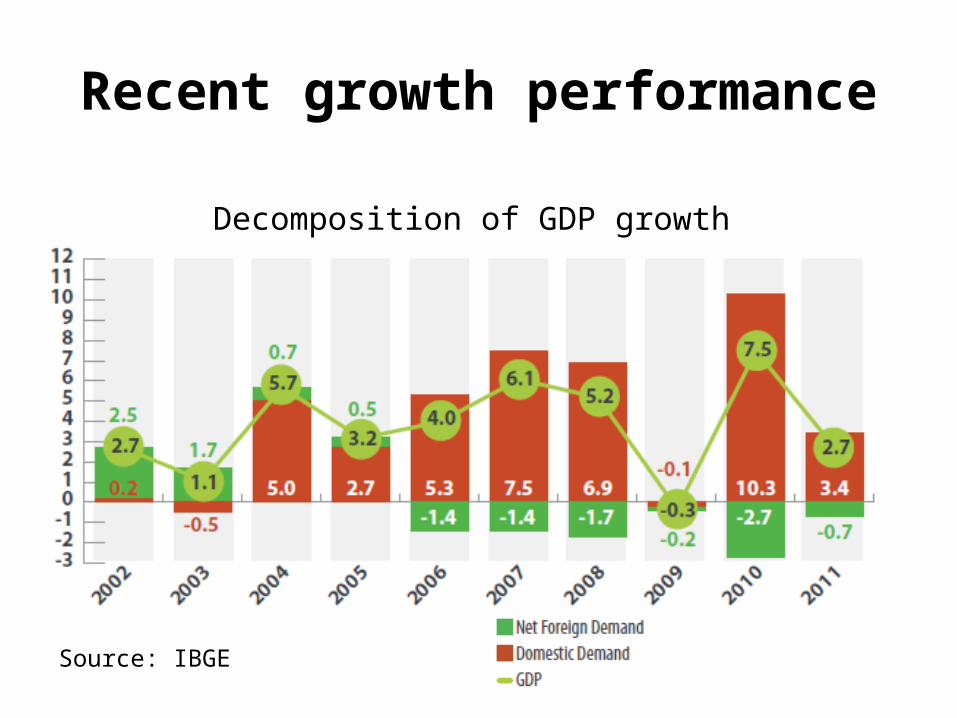

Recent growth performance

Source: IBGE

Decomposition of GDP growth

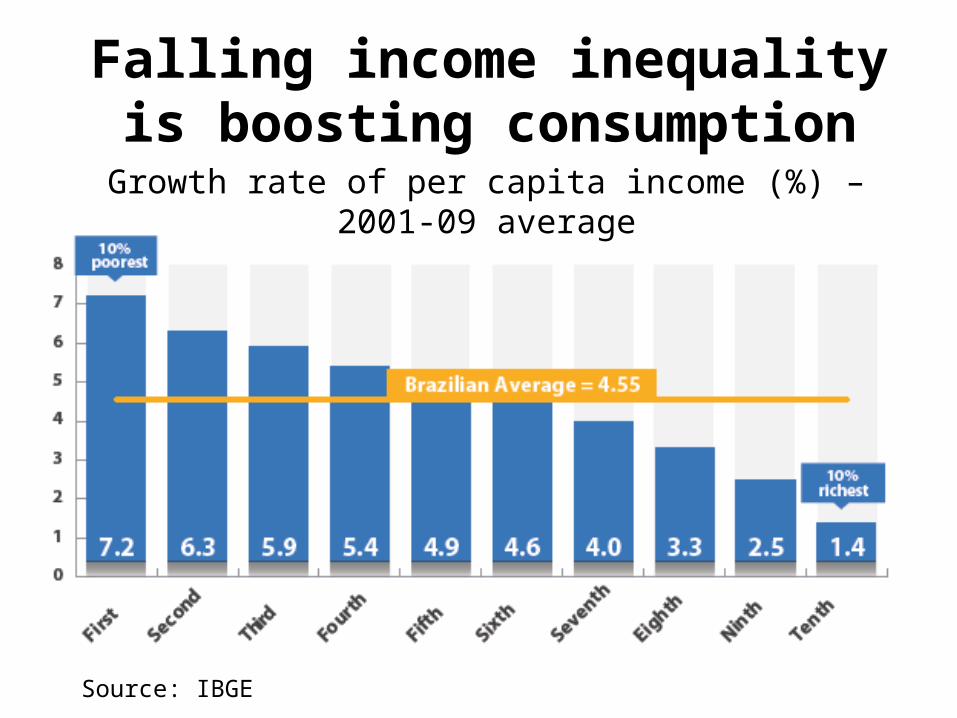

Falling income inequality is boosting consumption

Growth rate of per capita income (%) – 2001-09 average

Source: IBGE

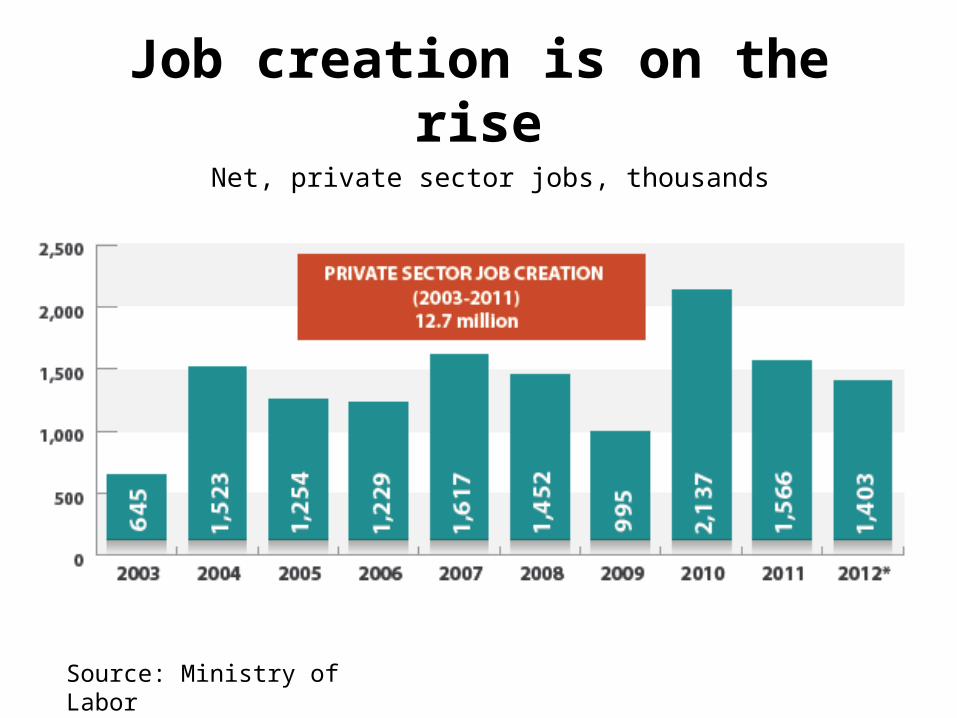

Job creation is on the rise

Source: Ministry of Labor

Net, private sector jobs, thousands

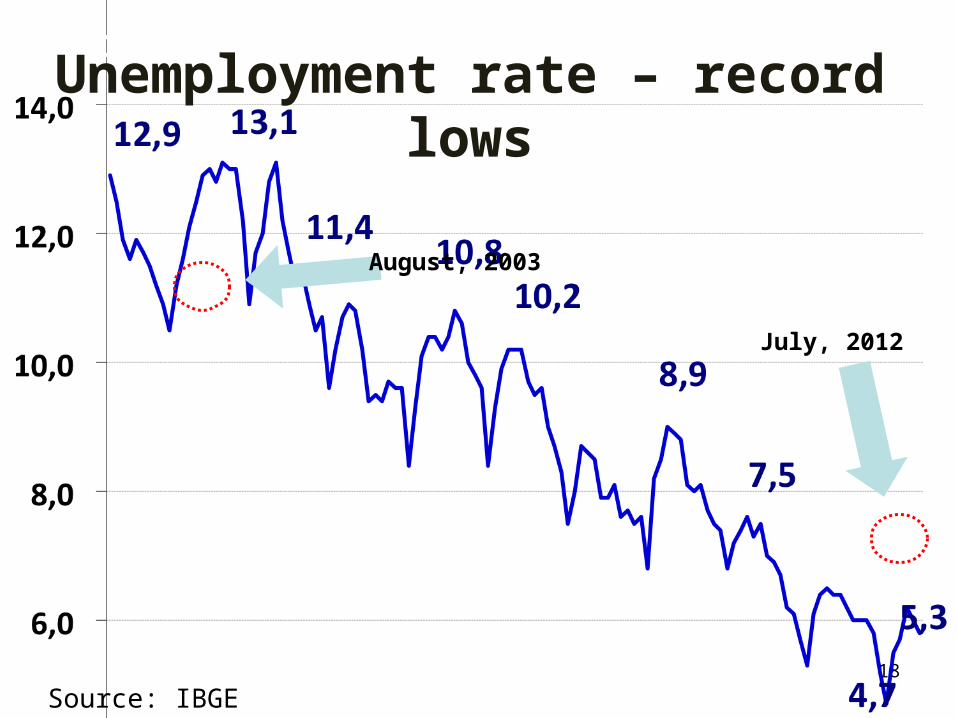

18

Falling unemploymentUnemployment rate – record lows

August, 2003

July, 2012

Source: IBGE

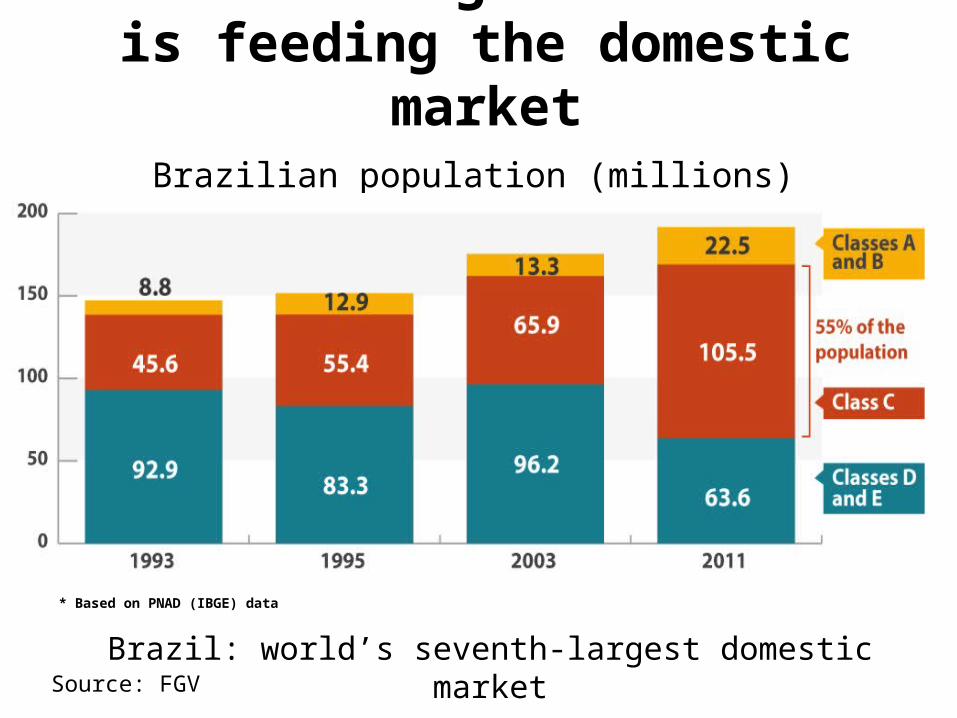

Brazilian population (millions)

Source: FGV

* Based on PNAD (IBGE) data

An increasing middle class is feeding the domestic market

Brazil: world’s seventh-largest domestic market

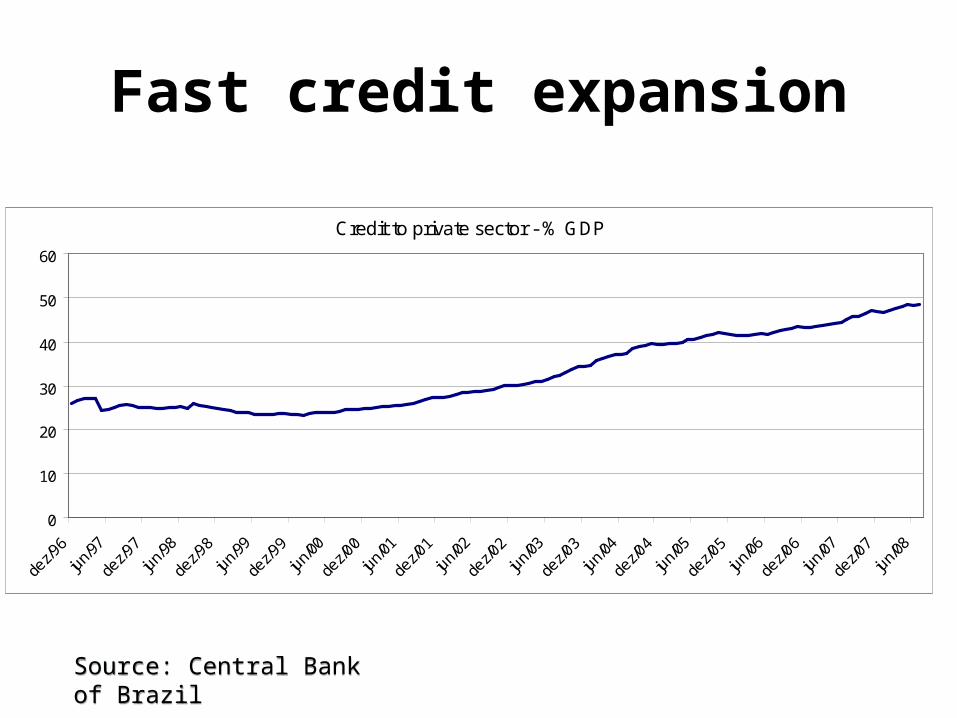

Fast credit expansion

Credit to private sector - % GDP

0

10

20

30

40

50

60

dez/9

6

jun/

97

dez/9

7

jun/

98

dez/9

8

jun/

99

dez/9

9

jun/

00

dez/0

0

jun/

01

dez/0

1

jun/

02

dez/0

2

jun/

03

dez/0

3

jun/

04

dez/0

4

jun/

05

dez/0

5

jun/

06

dez/0

6

jun/

07

dez/0

7

jun/

08

Source: Central Bank of BrazilSource: Central Bank of Brazil

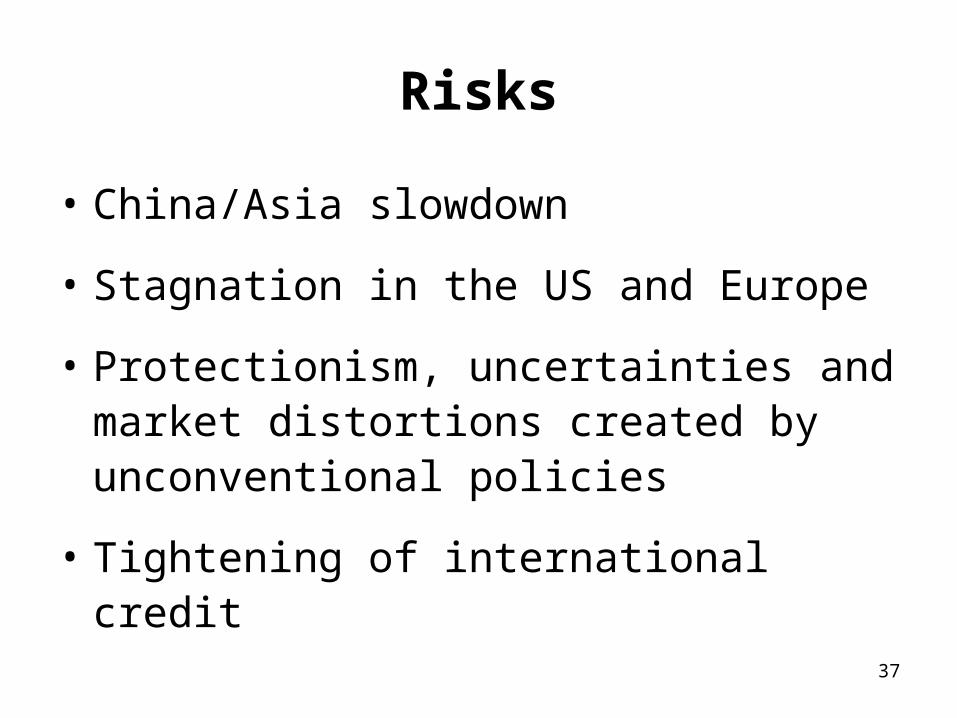

Navigating an increasingly complex world

Slow recovery in the US Crisis in the Euro zone Slowdown in China and other emerging

economies Rising geopolitical risks (protectionism, Northeast

Asia, in oil countries) Capital market distortions and uncertainties

associated to highly heterodox policies, e.g. Qes and Abenomics

Risk aversion on the rise Slowdown in trade, capital flows and FDI

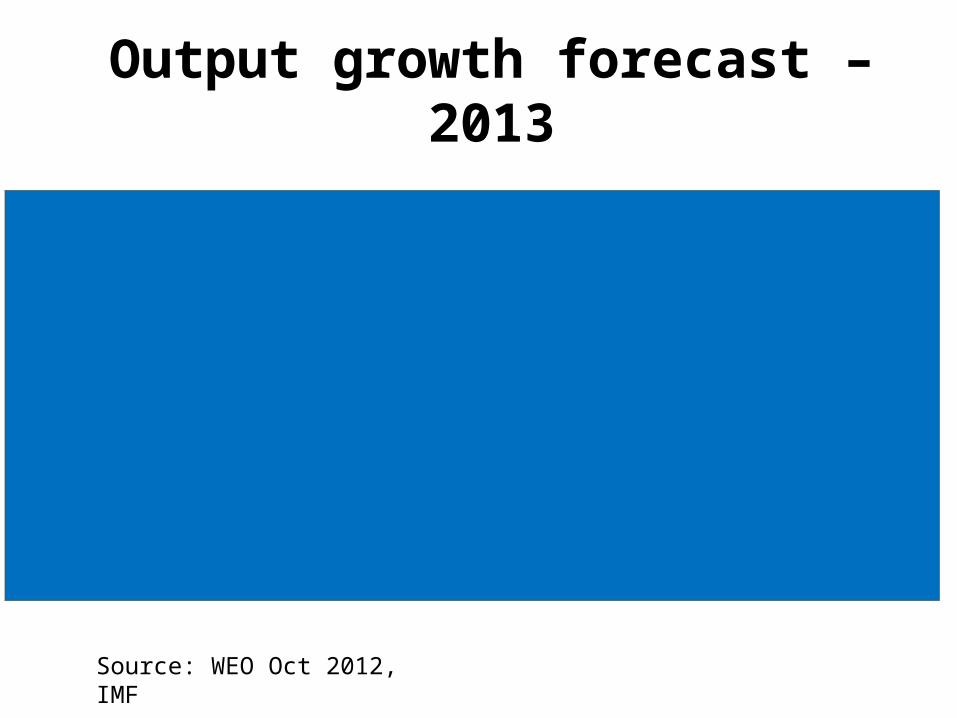

Output growth forecast – 2013

Source: WEO Oct 2012, IMF

Output growth 2013 - WEO IMF (Oct 2012)

8,2

6,0

4,0 3,8 3,53,0 2,8

2,1 2,01,5 1,2 1,1 0,9

0,4 0,20123456789

China

Indi

a

Brazil

Russia

Mex

ico

South

Afri

ca

Wor

ld o

utpu

t

United

Sta

tes

Canad

a

Advan

ced

econ

omie

s

Japa

n

United

Kin

gdom

Germ

any

Franc

e

Euro

Area

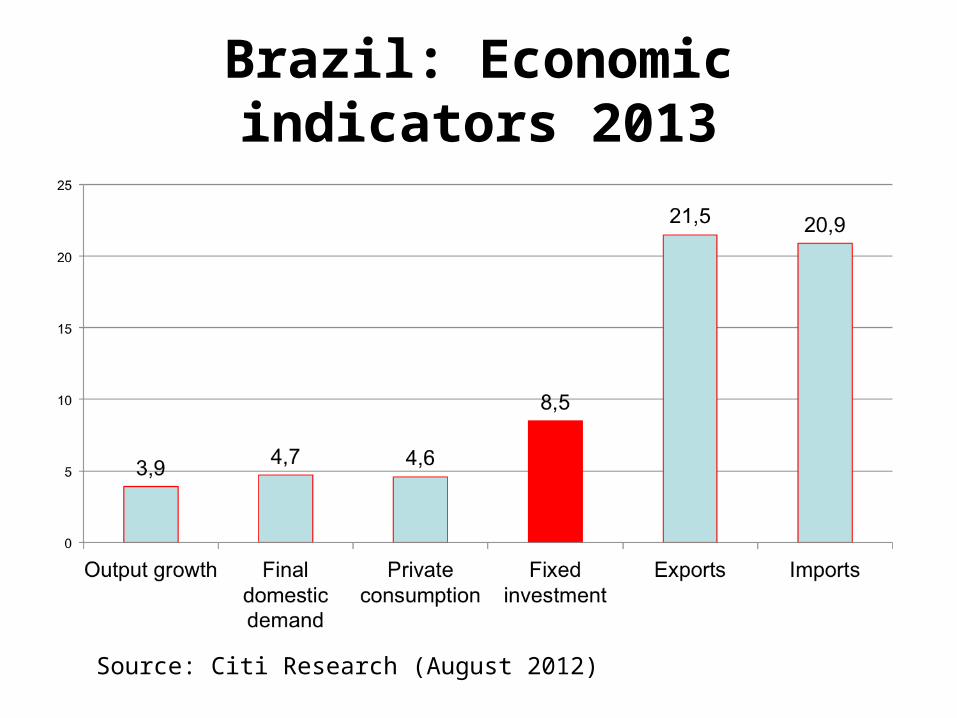

Brazil: Economic indicators 2013

Source: Citi Research (August 2012)

24

Sources of future growth

Domestic demand, but also …

– Increasing competitiveness

– Investments

– Well regulated financial sector -- banking system not exposed to toxic assets

Competitiveness is on the move• 23 new Innovation Institutes• 43 new Technological Centers• Sectorial Innovation Funds• 4 million people in vocational training per year• Science without Borders – 100,000+ scholarships

abroad in engineering and other tech. areas• MNCs state-of-the-art innovation labs• PISA-OECD – “Brazil, a successful reformer”

– “The federal government has launched a major effort to improve education, increasing spending in classrooms and on teacher salaries and providing extra help for poorer families in order to get children into classrooms. By setting quality targets and leaving schools free to choose how best to achieve them, its National Education Plan has transformed the country into a laboratory of best education practices.” OECD

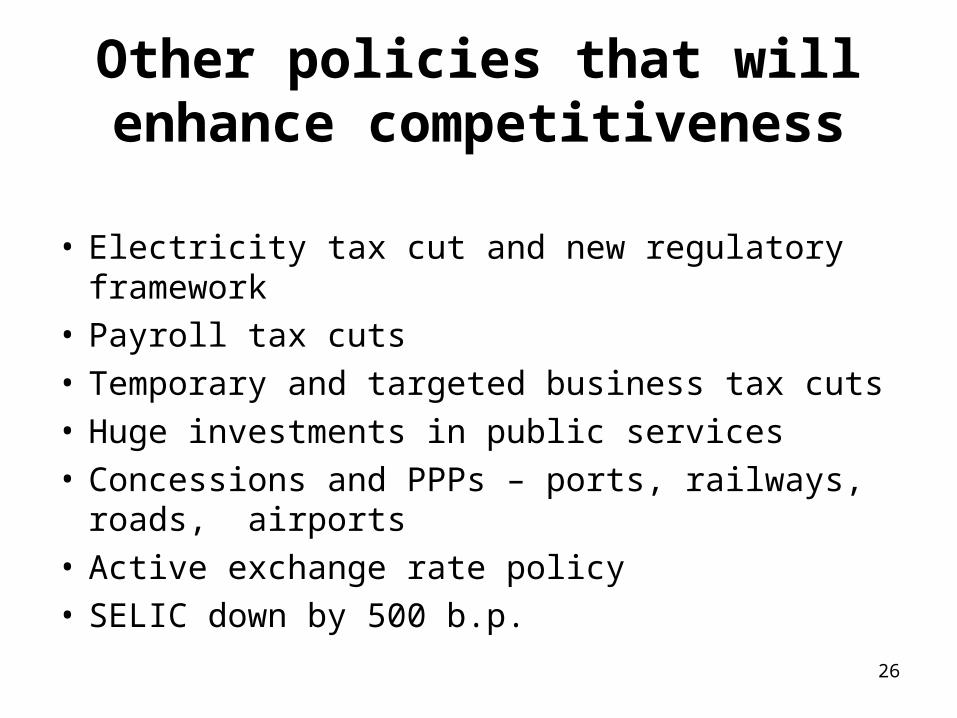

Other policies that will enhance competitiveness

• Electricity tax cut and new regulatory framework• Payroll tax cuts• Temporary and targeted business tax cuts• Huge investments in public services• Concessions and PPPs – ports, railways, roads,

airports• Active exchange rate policy• SELIC down by 500 b.p.

26

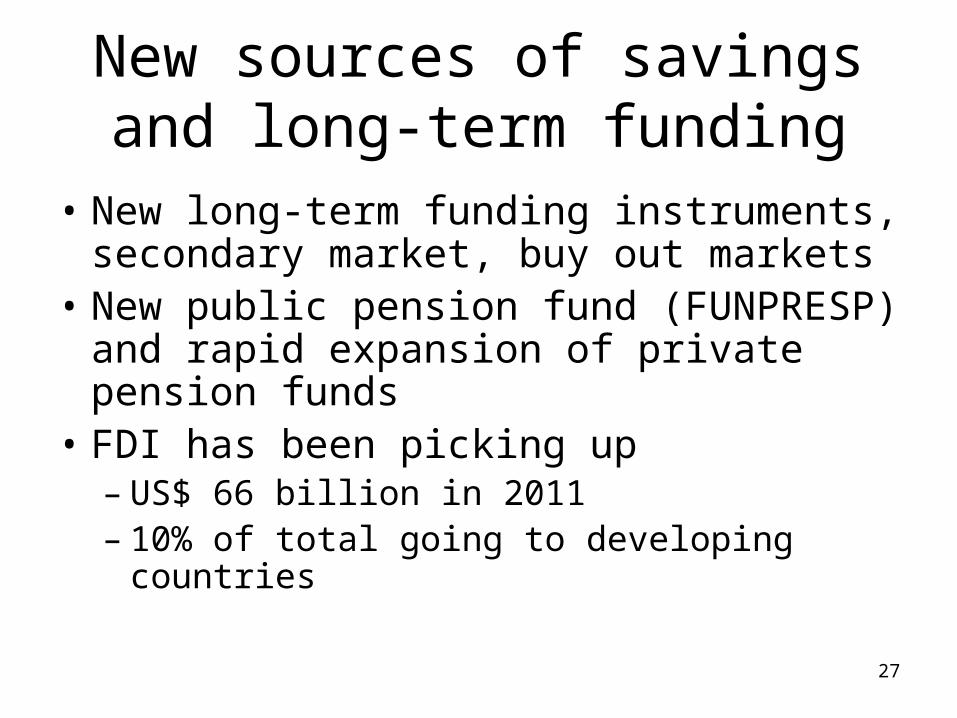

New sources of savings and long-term funding

• New long-term funding instruments, secondary market, buy out markets

• New public pension fund (FUNPRESP) and rapid expansion of private pension funds

• FDI has been picking up – US$ 66 billion in 2011– 10% of total going to developing countries

27

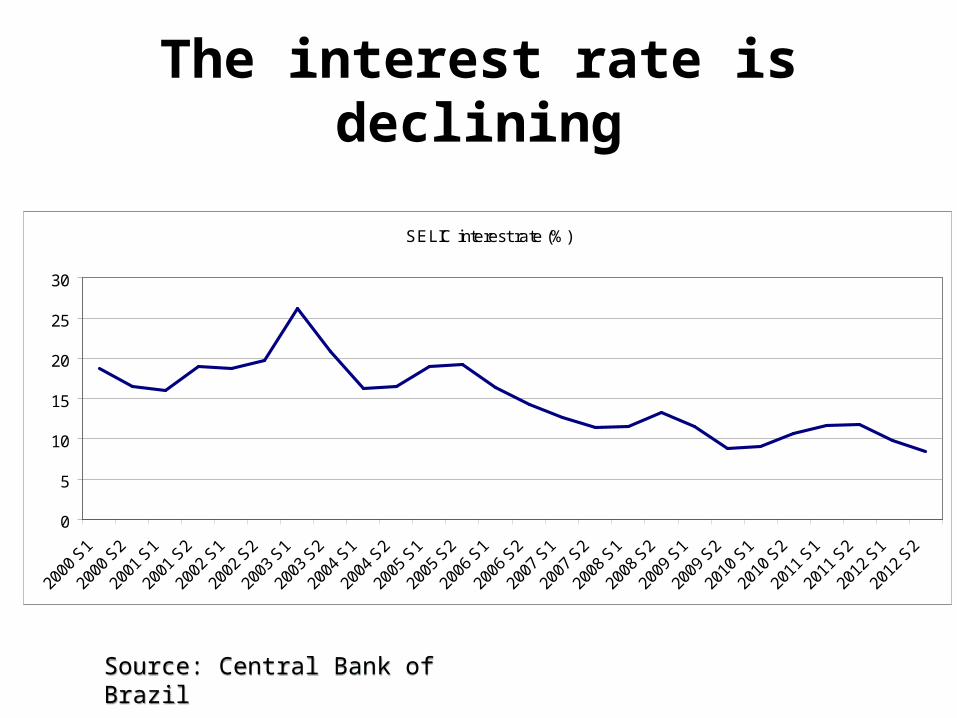

The interest rate is declining

SELIC interest rate (%)

0

5

10

15

20

25

30

2000

S1

2000

S2

2001

S1

2001

S2

2002

S1

2002

S2

2003

S1

2003

S2

2004

S1

2004

S2

2005

S1

2005

S2

2006

S1

2006

S2

2007

S1

2007

S2

2008

S1

2008

S2

2009

S1

2009

S2

2010

S1

2010

S2

2011

S1

2011

S2

2012

S1

2012

S2

Source: Central Bank of BrazilSource: Central Bank of Brazil

29

Growth Acceleration Program 2 - PAC 2

PAC 2 Projects (US$ bn) 2011 - 2014 After 2014 TotalPAC Better City 32.6 - 32.6

PAC Citizens' Community 13.1 - 13.1

PAC Minha Casa Minha Vida

159.0 - 159.0

PAC Water & Electricity for All

17.5 - 17.5

PAC Transport 59.7 2.6 62.3PAC Energy 263.8 358.2 622.0

Total 545.7 360.8 906.5

Electric Energy

Ports

Airports

Highways/Railways

Urban Mobility

2014 World Cup

2016 Olympic Games

Electric Energy

Ports

Airports

Highways/Railways

Urban Mobility

2014 World Cup

2016 Olympic Games

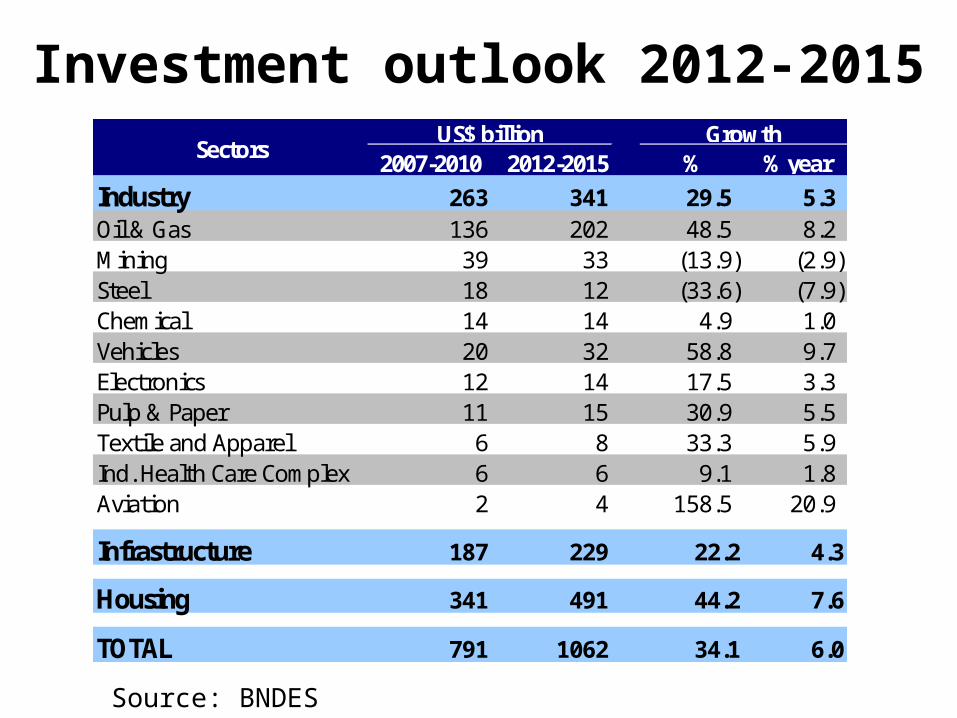

2007-2010 2012-2015 % % yearIndustry 263 341 29.5 5.3Oil & Gas 136 202 48.5 8.2Mining 39 33 (13.9) (2.9)Steel 18 12 (33.6) (7.9)Chemical 14 14 4.9 1.0Vehicles 20 32 58.8 9.7Electronics 12 14 17.5 3.3Pulp & Paper 11 15 30.9 5.5Textile and Apparel 6 8 33.3 5.9Ind. Health Care Complex 6 6 9.1 1.8Aviation 2 4 158.5 20.9

Infrastructure 187 229 22.2 4.3

Housing 341 491 44.2 7.6

TOTAL 791 1062 34.1 6.0

SectorsUS$ billion Growth

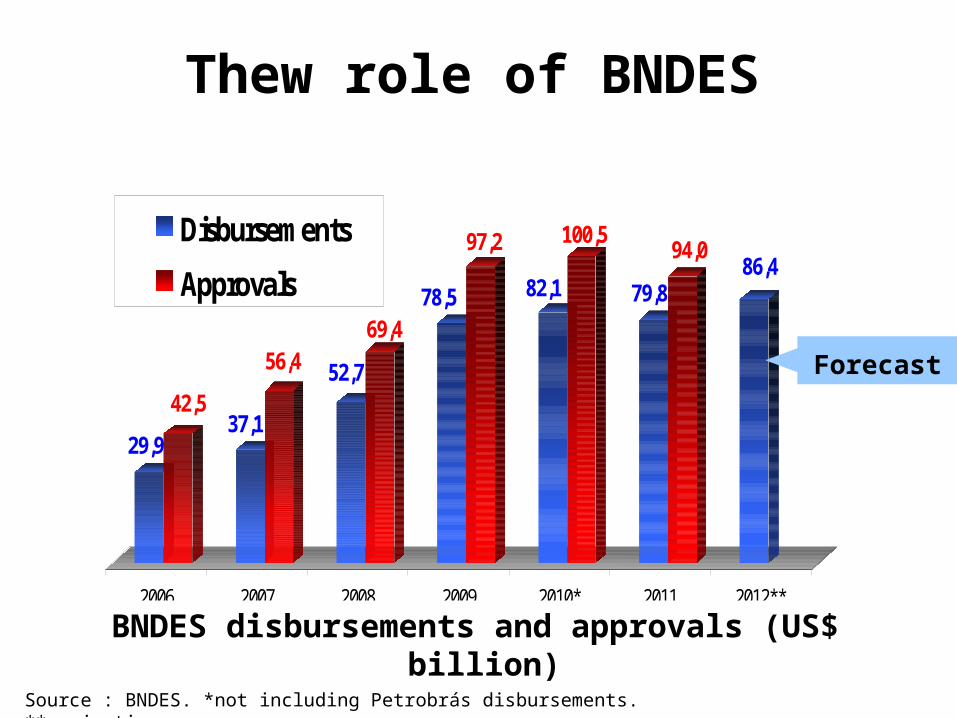

Investment perspectives are firmInvestment outlook 2012-2015

Source: BNDES

29,9

42,537,1

56,4 52,7

69,478,5

97,2

82,1

100,5

79,8

94,086,4

2006 2007 2008 2009 2010* 2011 2012**

Disbursements

Approvals

BNDES disbursements and approvals (US$ billion)

Source : BNDES. *not including Petrobrás disbursements. **projection

Forecast

Thew role of BNDES

• Counter-cyclical role, e.g. 2008/09• Strong support to SMEs• Infrastructure – about 1.5% of GDP• Equity financing• Innovation• Environment• Start-ups, especially in tech. areas• Venture capital• Export finance

32

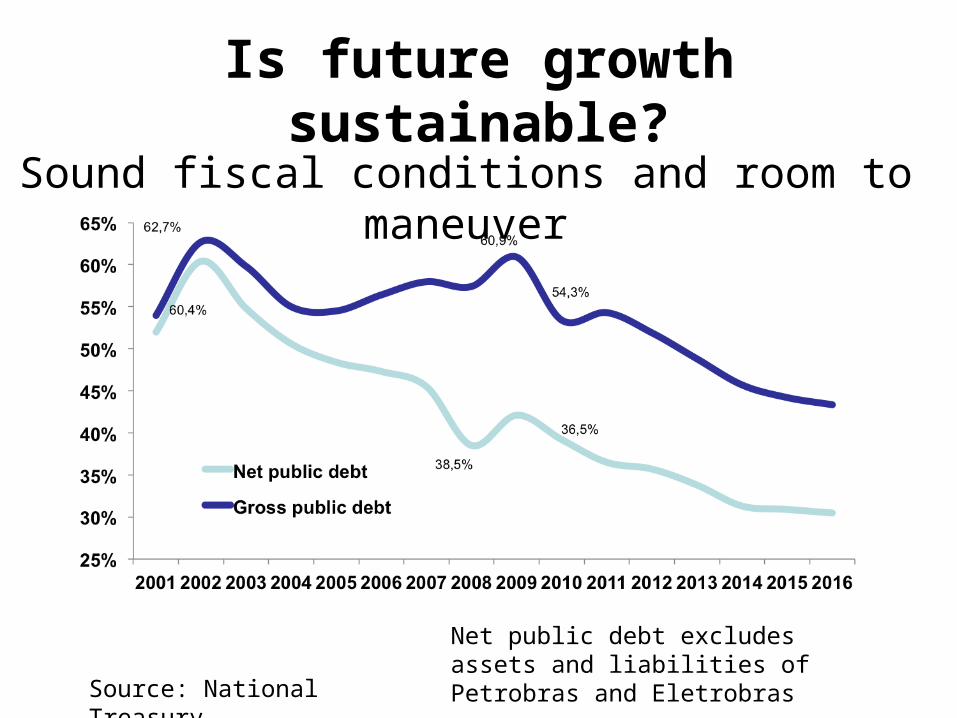

Is future growth sustainable?

Source: National Treasury

Sound fiscal conditions and room to maneuver

Net public debt excludes assets and liabilities of Petrobras and Eletrobras

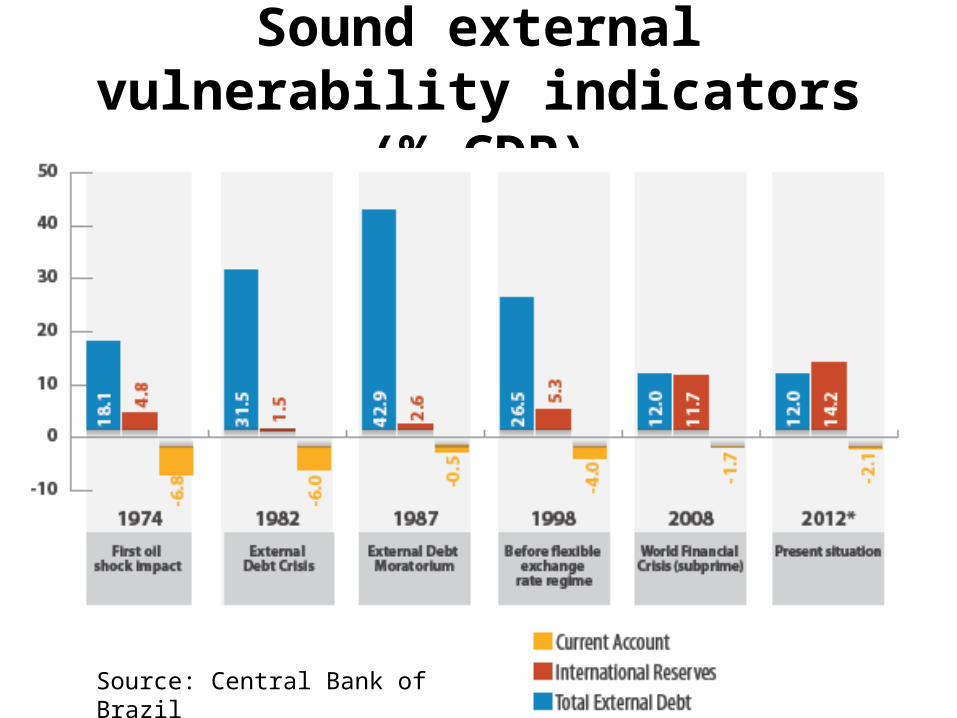

Sound external vulnerability indicators (% GDP)

Source: Central Bank of Brazil

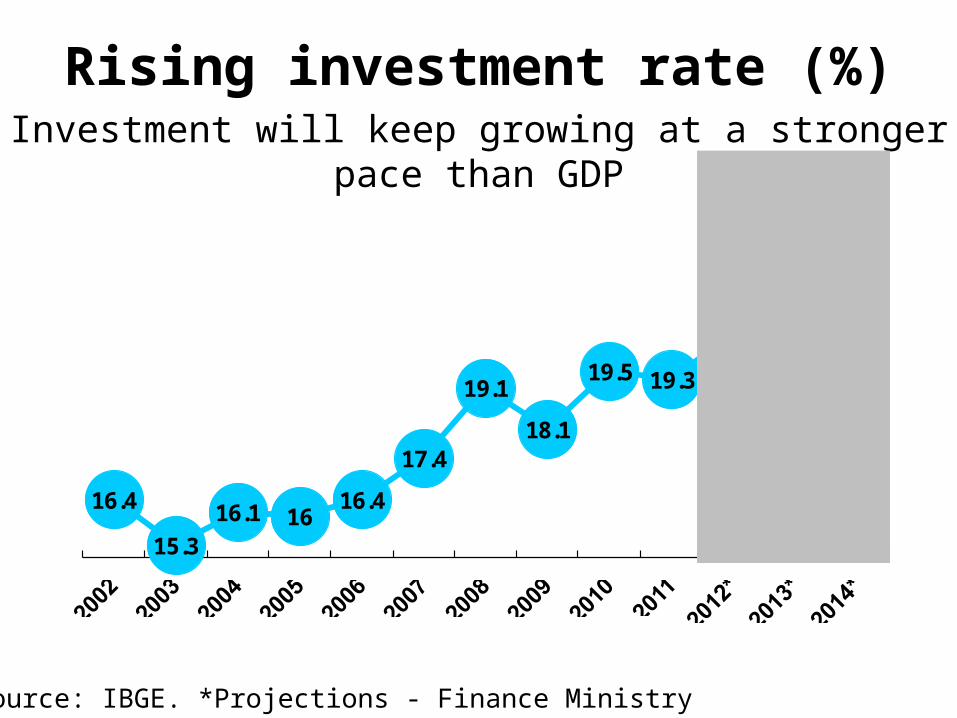

Rising investment rate (%)Investment will keep growing at a stronger pace than GDP

Source: IBGE. *Projections - Finance Ministry

16.4

15.3

16.1 1616.4

17.4

19.1

18.1

19.5 19.3

20.4

22.0

24.0

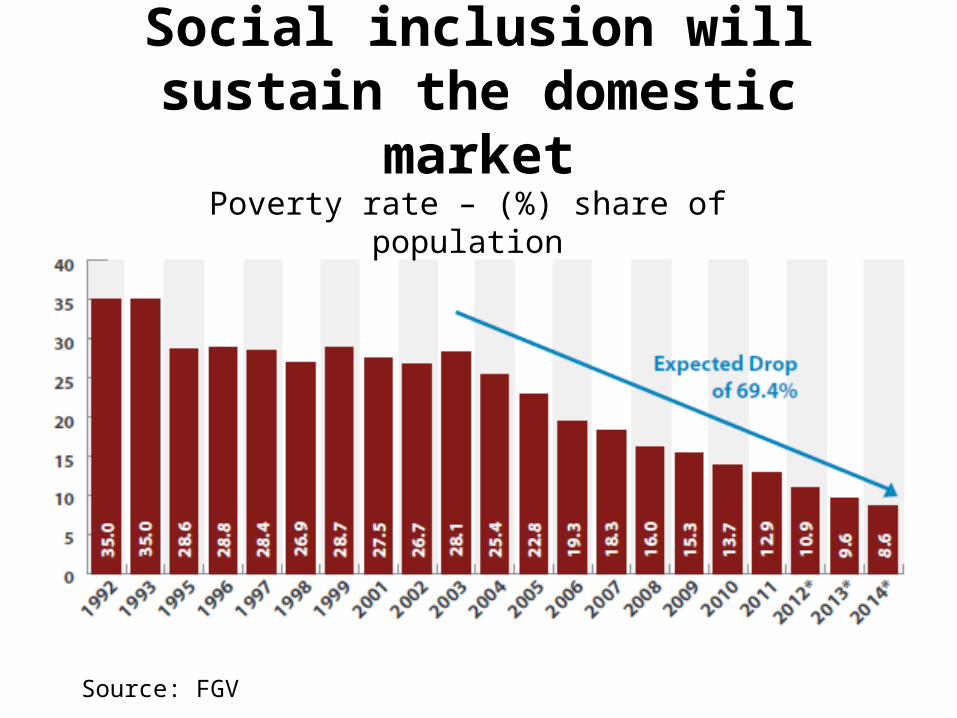

Social inclusion will sustain the domestic market

Source: FGV

Poverty rate – (%) share of population

37

Risks

• China/Asia slowdown

• Stagnation in the US and Europe

• Protectionism, uncertainties and market distortions created by unconventional policies

• Tightening of international credit

38

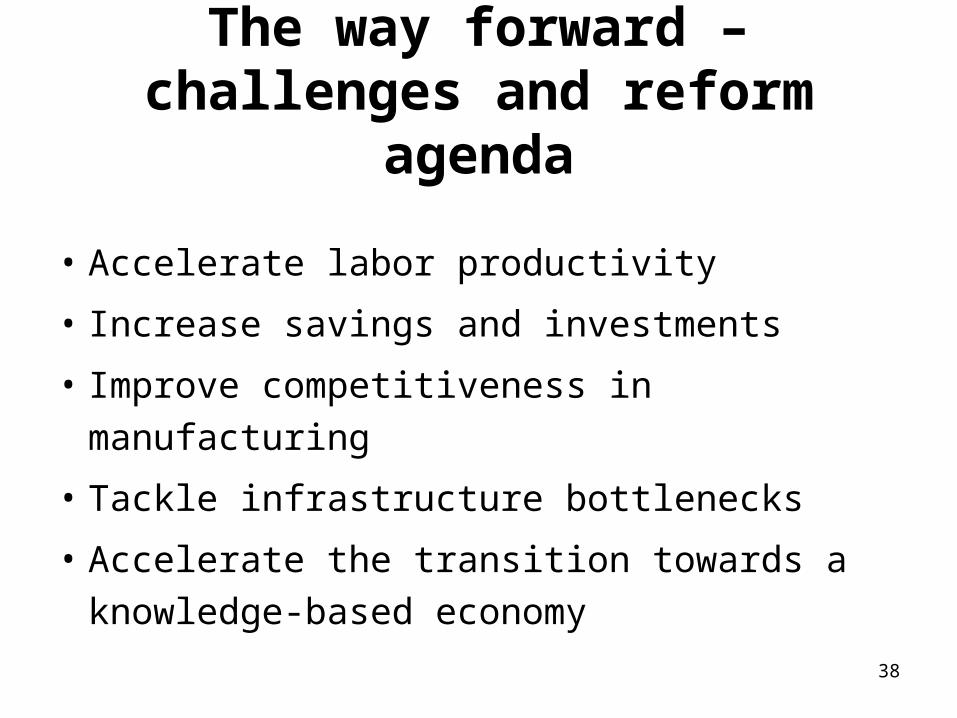

The way forward – challenges and reform agenda

• Accelerate labor productivity

• Increase savings and investments

• Improve competitiveness in manufacturing

• Tackle infrastructure bottlenecks

• Accelerate the transition towards a

knowledge-based economy

Structural reforms

• Diversify sources of long-term funding

• Foster innovation

• Fiscal reform – ICMS (VAT)

• Pension reform

• Labor legislation reform

• Diversify exports and reduce dependency

on commodities39

Conclusions

• Domestic market will enlarge further

• Investments and increasing

competitiveness will also drive growth

• Expanding investment opportunities in

several areas

40

• A bumpy road ahead: poor international environment and uncertainties

• But plenty of room for policy activism at the Government disposal

• Government is aware of the need to address a reform agenda to foster competitiveness and to foment sustained growth

41

Obrigado!!

42