Embed Size (px)

Citation preview

BPK2A

FINANCIAL ACCOUNTING II

1BPK2A - FINANCIAL ACCOUNTING II

BPK2A - FINANCIAL ACCOUNTING II

TM

Syllabus

Hire Purchase & Instalment

Default & Repossession

Stock & Debtors System

Hire Purchase Trading Account

Instalment purchase system

2

BPK2A - FINANCIAL ACCOUNTING II

TM

Definition – Hire Purchase System

• According to the Hire Purchase Act 1972 Section 2(c) ― Hire purchase

agreement is an agreement under which goods are let on hire and under

which the hirer has an option to purchase them in accordance with the

terms of the agreement and includes an agreement under which -

• Possession of goods is delivered by the owner & amount in periodical

instalments.

• The property is passed only on the payment of the last of such instalments.

• Such person has a right to terminate the agreement at any time before the

property so passes.‖

3

BPK2A - FINANCIAL ACCOUNTING II

TM

HP System - Important terms

Cash Price

Hire purchase Price

Interest

Hire or Instalment

Down Payment

Hirer

Hire vendor

or Owner

4

BPK2A - FINANCIAL ACCOUNTING II

TM

HP System - Features

The hirer gets possession of the goods on signing the agreement and

has the right to use them.

The ownership continues to be with the seller or hire vendor. The buyer

gets ownership on payment of the last instalment.

The hirer has the duty to keep the goods in good condition.

Each instalment is treated as hire charges.

5

BPK2A - FINANCIAL ACCOUNTING II

TM

The hirer has the option to return the goods before the last instalment is

paid

The hire vendor can repossess the goods if the buyer fails to pay any

instalment on the due date.

If goods are repossessed, the value of goods on that date and the

instalment paid are added and the total hire purchase price is reduced.

The balance is payable by the hire vendor to the hirer.

HP System - Features

6

BPK2A - FINANCIAL ACCOUNTING II

TM

Instalment purchase system

An agreement is entered into by the seller and buyer.

Down payment is paid and possession as well as ownership

in the goods is transferred to the buyer.

If buyer fails to pay any instalment, the seller cannot

repossess the goods.

He can only sue the buyer in a court for recovery of the dues.

7

BPK2A - FINANCIAL ACCOUNTING II

TM

Distinction between HP & IP System

Nature of agreement

Transfer of ownership

Name of the parties

Relationship

Risk of loss

Right of sale

Repossession of goods

Termination of agreement

Instalment

Governing

8

BPK2A - FINANCIAL ACCOUNTING II

TM

Calculation of Interest

The hire purchase price is always greater than the cash price. Calculations

under the following circumstances:

When the rate of interest, the cash price and the instalments are given

When the rate of interest is not given

When the total cash price is not given

When the instalment price is not given

When cash price is calculated by annuity method

9

BPK2A - FINANCIAL ACCOUNTING II

TM

Default & Repossession Default

◦ If the hire purchaser fails to make payment of any instalment, it is

called default.

Repossession

The hire vendor has the right to take away the goods sold on hire

purchase in the event of default made by the hire purchaser.

The hire vendor can repair or recondition the repossessed goods

and sell them to anyone else.

10

BPK2A - FINANCIAL ACCOUNTING II

TM

Repossession - Types

Complete Repossession

The hire vendor may take away all the goods on

which there is default of instalment.

Partial Repossession

Hire vendor may take away only a portion of

the goods on which there is default of

instalment.

11

BPK2A - FINANCIAL ACCOUNTING II

TM

Computation of Profit -Methods

Debtors Method

Stock and debtors Method

12

BPK2A - FINANCIAL ACCOUNTING II

TM

UNIT – II Syllabus

Branch Accounts

Dependent Branches

Stock & Debtors System

Distinction Between Whole Sale &

Retail Profit

Independent Branches

Departmental accounts

Investment accounts

Accounting for empties and

packages

13

BPK2A - FINANCIAL ACCOUNTING II

TM

Meaning - It is an Establishment or a subordinate division of business

which carry on either the same activity or a substantially the same

activity cariied on by the Head office.

The main place of establishment (i.e) the parent establishment

called HeadOffice

The various division situated at different places is

called Branch Office

Branch Accounts

14

BPK2A - FINANCIAL ACCOUNTING II

TM

OBJECTIVES OF BRANCH ACCOUNTS

Help in controlling branches

Helps in finding the actual financial position of each & every branch

Helps in ascertaining the Profit or loss of each branch

Helps in assessing the Cash and Goods requirement of each branch.

Help in ascertaining the exact expenses and incomes by seeing the Branch

accounts

Helps in providing suggestions on Do‘s & Don‘ts in branches.

Branch

15

BPK2A - FINANCIAL ACCOUNTING II

TM

Types of branches

Dependent branch

Independent branch

Foreign branch

16

BPK2A - FINANCIAL ACCOUNTING II

TM

The Records of these Branches are maintained by head office.

These types of branches that are operated by orders, which are

executed by the head office

Expenses incurred at the branch have to be maintained by them.

17

BPK2A - FINANCIAL ACCOUNTING II

TM

Books of accounts : Methods of accounting

petty cash book

stock register

customer's accounts

Stock and debtors system

Debtors system

Final account system

Wholesale branch system

18

BPK2A - FINANCIAL ACCOUNTING II

TM

This system is adopted in case of branches of small size.

This account is nominal account in nature.

Here the head office maintains account of each branch to know

about profit and loss of each branch.

Goods are despatched at any of these :

cost

Invoice price

Cost + fixed % of loading

19

BPK2A - FINANCIAL ACCOUNTING II

TM

When goods are invoiced at cost

Branch Account (in the books of head office)

To balance b/d By balance c/d(Opening

(assets in the beginning) balance of liabilities accounts if any

Stock creditors

Debtors Outstanding expenses

Petty cash By Bank

Furniture cash sales

Prepaid expenses cash collected from debtors

To Goods sent to branch A/c By Goods sent to branch A/c

To bank (expenses paid by H.O.) (returns to H.O)

To balance c/d (closing balance of By Balance c/d (closing balance of assets)

Liabilities Accounts if any) Stock

Creditors Debtors

Outstanding expenses Petty cash

To General P & L A/c Furniture( at depreciated value)

(Branch Profit) (bal fig) Prepaid expenses

By General P & L A/c (Branch Loss ) (bal fig)

20

BPK2A - FINANCIAL ACCOUNTING II

TM

• Debit side • Credit side

Sale (credit) Cash received

Discount

Goods returned

Bad debts

Allowances

Balance

If cost is 100, but the HO has sent goods to branch at 120 then

there is profit of 20 added in the cost. This 20 has to be adjusted.

This is called stock reserve.

21

BPK2A - FINANCIAL ACCOUNTING II

TM

In this system the head office keeps separate accounts relating to

various types of transaction at the branch instead of one branch.

Following accounts are kept in the head office books relating to a

branch under this system

Branch Stock A/c

Branch Debtors A/c

Branch Adjustment A/c

Branch Expenses A/c

Goods Sent to Branch A/c

22

BPK2A - FINANCIAL ACCOUNTING II

TM

This account deals with all goods received, returned and sold by the branch.

This account gives the surplus or shortage of stock and the closing stock @

the branch, is usually prepared at invoice price.

• Debit side • Credit side

Opening balance Cash account

Goods sent to Branch Debtors a/c

Goods Returned by Drs Goods returns by branch

Goods Spoiled, lost (in weight, pilferage, loss in transit)

Balance c/d

23

BPK2A - FINANCIAL ACCOUNTING II

TM

This account records all the transaction relating to branch debtors

Ascertain either the closing balance of debtors or credit sales.

• Debit side • Credit side

Stock account(B/f denoting total credit sales )

Cash received

Branch adjustment a/c ( Bad debts etc.)

24

BPK2A - FINANCIAL ACCOUNTING II

TM

When goods sent to branch at cost price, then this a/c need not to be prepared.

When the goods are supplied to branch at invoice price ,

It is prepared to ascertain the gross profit made by the branch.

• Debit side • Credit side

Stock reserve Goods sent to branch a/c

Branch stock a/c Loading on goods sent to Branch

Profit element of stock shortages, Defectives, loss on transit, pilferage element of stock surplus

Value of loss in weight (P & L) (full amount)

Gross profit (balancing figure )

25

BPK2A - FINANCIAL ACCOUNTING II

TM

Prepared to ascertain the net profit made by the branch.

Prepared to find out the net value of goods sent to the branch.

Balance of this account is transferred to either purchase account or

trading account depending on the

https://youtu.be/_Gx_1ygl4CU

26

BPK2A - FINANCIAL ACCOUNTING II

TM

Departmental Accounts

Basis for Allocation of Expenses

Inter departmental transfer

Treatment of Expenses

27

BPK2A - FINANCIAL ACCOUNTING II

TM

Meaning – DEPARTMENTS

Division of organization in to independent departments, each of which

may deal in a particular class of goods or render a specified type of

services under the same roof or from the same premises.

DEPARTMENTAL ACCOUNTING

The owners or the management may desire to ascertain the trading results of

each department and the overall result of the organisation and the method of

obtaining such results is known as departmental accounting

28

BPK2A - FINANCIAL ACCOUNTING II

TM

29

BPK2A - FINANCIAL ACCOUNTING II

TM

• Trading & P/L A/c is prepared

P & L A/c

• Firms with Huge Turnover will maintain separate Subsidiary Books

• Closing Stock can be ascertained at the time of stock taking

Maintenance of Records

• Direct Expenses

• Indirect ExpensesExpenses which can be apportionedExpenses which cannot apportioned

Departmentalisationof Expenses

• @ Cost Price

• @ Selling Price or Loaded PriceInter Departmental Transfers

30

BPK2A - FINANCIAL ACCOUNTING II

TM

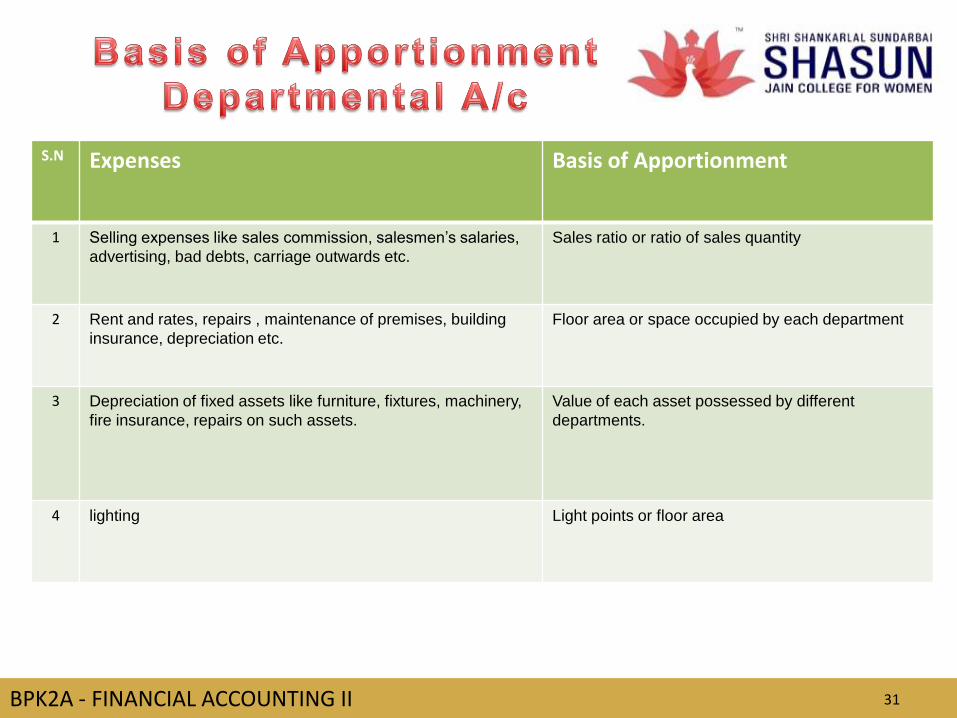

S.N Expenses Basis of Apportionment

1 Selling expenses like sales commission, salesmen‘s salaries,

advertising, bad debts, carriage outwards etc.

Sales ratio or ratio of sales quantity

2 Rent and rates, repairs , maintenance of premises, building

insurance, depreciation etc.

Floor area or space occupied by each department

3 Depreciation of fixed assets like furniture, fixtures, machinery,

fire insurance, repairs on such assets.

Value of each asset possessed by different

departments.

4 lighting Light points or floor area

31

BPK2A - FINANCIAL ACCOUNTING II

TM

32

5 Power Consumption as per meter Or horse power

6 Carriage inward Purchase value

7 workmen‘s amenities, and welfare expenses Workmen‘s

compensation insurance, ESI,PF etc. payable to employer

No. of workers Wages of each department

8 Factory manager‘s salary Time devoted to each dept

9 Premium for loss of profits insurance Profit of each dept in the previous year

BPK2A - FINANCIAL ACCOUNTING II

TM

33

TM

BPK2A - FINANCIAL ACCOUNTING II 33

Investment means to spend money outside the business in order to

earn some income which are non-trading in nature.

Usually, money is invested in Government Bonds, Securities, Shares

and Debentures of companies etc.

INVESTMENT ACCOUNTS

AS13

BPK2A - FINANCIAL ACCOUNTING II

TM

Syllabus

Admission of a Partner

Retirement of a Partner

Death of a Partner

35

BPK2A - FINANCIAL ACCOUNTING II

TM

Definition• According to Section 4 of the Indian Partnership Act 1932, partnership is

defined as - ― The relationship between persons who have agreed to share

the profits of a business carried on by all or any of them acting for all‖.

There must be an agreement entered into between two or more

persons.

The object of the agreement must be to share the profits of a

business.

The business must be carried on by all or any of the persons concerned

acting for all.

It is formed to carry on a lawful business.

It is an association of two or more persons

Features

36

BPK2A - FINANCIAL ACCOUNTING II

TM

Admission• According to Sec 31(1) of the Indian Partnership Act 1932, a new

partner can be admitted only with the consent of all the existing

partners.

• The existing partnership agreement comes to an end and a new

agreement comes into effect.

Whenever a partner is admitted into the partnership firm, he acquires

two rights-

The right to share in the assets of the partnership

The right to share in the profits of the business

37

BPK2A - FINANCIAL ACCOUNTING II

TM

Adjustment in the profit sharing ratio

Adjustment for goodwill

&

Adjustment of capital

Adjustment for revaluation of assets

and liabilities

Adjustment of reserves and other accumulated

profits.

Necessary Adjustments

38

Adjustments in

admission of a partner

BPK2A - FINANCIAL ACCOUNTING II

TM

Calculation of Sacrificing Ratio

• Old partners have to surrender some of their old shares in favour of

the new partner.

• The surrender of share by old partners is made in certain ratio.

• This ratio is called sacrificing ratio.

Sacrificing Ratio = Old Ratio – New Ratio

39

BPK2A - FINANCIAL ACCOUNTING II

TMGoodwill - Meaning

It can be described as a value of all favourable attributes relating to

a business enterprise. Goodwill is nothing more than the probability

that the old customers will resort to the old place.

It is the value of the reputation of the firm in respect of profits

expected in future over and above the normal rate of profits.

40

BPK2A - FINANCIAL ACCOUNTING II

TM

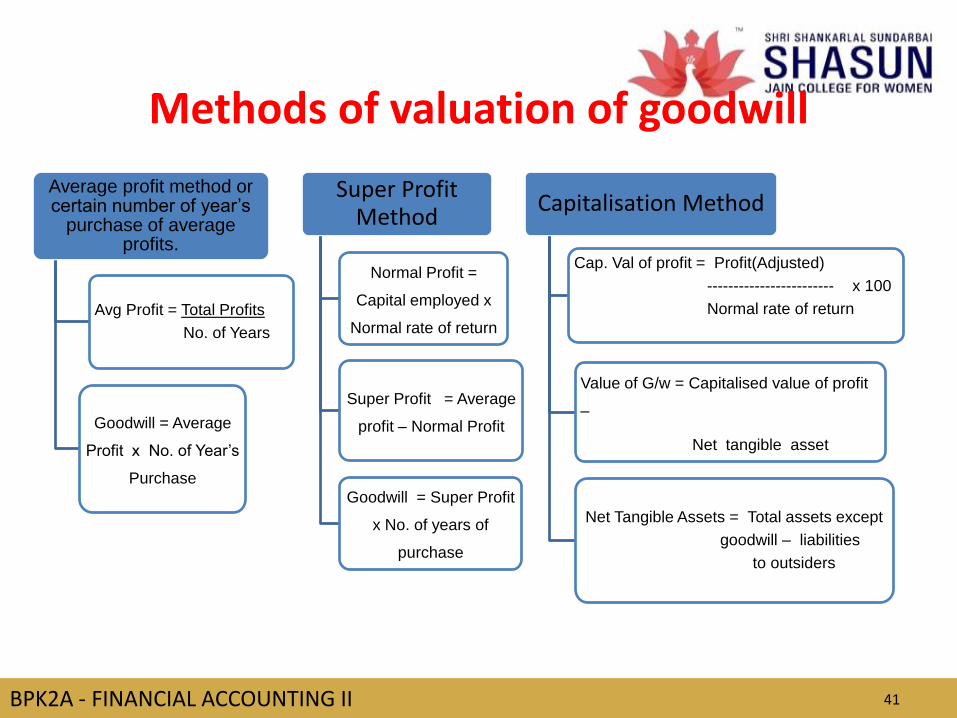

Methods of valuation of goodwill

Average profit method or certain number of year‘s

purchase of average profits.

Avg Profit = Total Profits

No. of Years

Goodwill = Average

Profit x No. of Year‘s

Purchase

Super Profit Method

Normal Profit =

Capital employed x

Normal rate of return

Super Profit = Average

profit – Normal Profit

Goodwill = Super Profit

x No. of years of

purchase

Capitalisation Method

Cap. Val of profit = Profit(Adjusted)

------------------------ x 100

Normal rate of return

Value of G/w = Capitalised value of profit

–

Net tangible asset

Net Tangible Assets = Total assets except

goodwill – liabilities

to outsiders

41

BPK2A - FINANCIAL ACCOUNTING II

TM

Treatment for Goodwill

on the Admission

of a Partner

Inferred or

Hidden Goodwill

Premium Method

Revaluation Method

Memorandum Revaluation

Method

42

BPK2A - FINANCIAL ACCOUNTING II

TM

Retirement of a Partner

• According to Sec 32(1) of the Indian Partnership Act 1932, a partner

may retire from the firm

– With the consent of all the partners

– In accordance with an express agreement by the partners

– Where the partnership is at will by giving notice in writing to all

the other partners of his intention to retire.

43

BPK2A - FINANCIAL ACCOUNTING II

TM

Adjustment regarding profit sharing ratio

Adjustment for goodwill

&

Revaluation of Assets and Liabilities

Adjustments regarding Reserves and other

undistributed profits and losses

Payment to the retiring partner.

Retirement Necessary

Adjustments

44

BPK2A - FINANCIAL ACCOUNTING II

TM

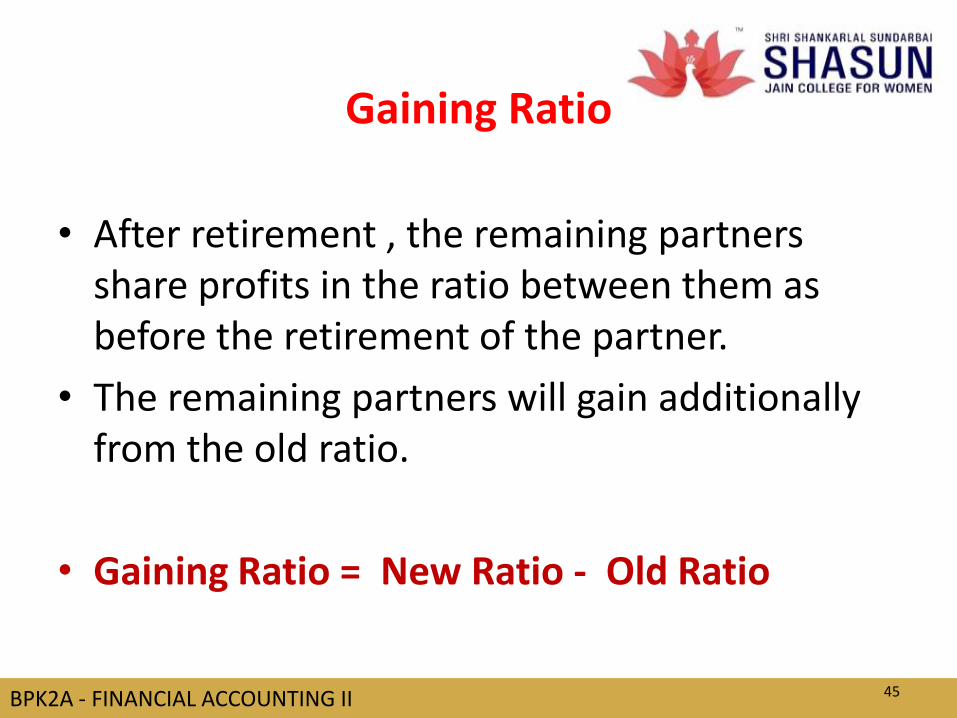

Gaining Ratio

• After retirement , the remaining partners share profits in the ratio between them as before the retirement of the partner.

• The remaining partners will gain additionally from the old ratio.

• Gaining Ratio = New Ratio - Old Ratio

45

BPK2A - FINANCIAL ACCOUNTING II

TM

Distinction between Sacrificing & Gaining Ratio

46

BPK2A - FINANCIAL ACCOUNTING II

TM

Payment to the Retiring Partner

Payment in Instalments

Payment in Lump sum

Payment by Annuity

47

BPK2A - FINANCIAL ACCOUNTING II

TM

Death of a Partner

• Death of a partner dissolves the partnership but the surviving

partners generally carry on the business by purchasing the

deceased partners share.

• In the event of death, the legal representative of the deceased

partner will be entitled to get from the firm, the amount due on

account of the following will be credited:

– Capital standing to the credit of the deceased partner on the date

of his death

– Share of goodwill

48

BPK2A - FINANCIAL ACCOUNTING II

TM

– Share in the profit of the firm earned from the beginning of the year to

the date of death.

– Profit on revaluation of assets and liabilities

– Share of accumulated profits and losses

– Share of the proceeds of the Joint Life Policy.

– Interest on capital from the beginning of the year to the date of death.

– Salary due

49

BPK2A - FINANCIAL ACCOUNTING II

TM

Deceased partner’s cap a/c is debited with the following amount

Drawings

Interest on drawings from the beginning of the year to

the date of death.

Loss on revaluation of assets and liabilities

Loss in the business from the beginning of the

accounting year till the date of death.

50

BPK2A - FINANCIAL ACCOUNTING II

TM

Mode of Payment

Lump sum Payment Method

Instalment Payment Method

Annuity Method

51

BPK2A - FINANCIAL ACCOUNTING II

TM

Syllabus

Dissolution of a Partnership

Insolvency of a partner

Gradual Realization of

Assets & Piecemeal

Distribution.

52

BPK2A - FINANCIAL ACCOUNTING II

TM

Meaning

• It refers to the complete breakdown of a partnership and partners do

not continue the firm.

• The dissolution of partnership between all partners of a firm is called

the dissolution of the firm.

• The assets are disposed off, liabilities are paid off and whatever

remains is paid to the partners in settlement of their accounts.

53

BPK2A - FINANCIAL ACCOUNTING II

TM

Modes of dissolution

Dissolution by Agreement

Compulsory Dissolution

Dissolution on happening of certain events

Dissolution by Notice

Dissolution by Court

54

BPK2A - FINANCIAL ACCOUNTING II

TM

Settlement of accounts

Settlement

Payment of Losses

Distribution of assets

Payment of firm‘s debts and personal debts

55

BPK2A - FINANCIAL ACCOUNTING II

TM

Insolvency of a partner

– When a partner becomes insolvent ,Whatever amount he can bring from his

private estate into the firm will be credited to his capital account.

– The amount which is irrecoverable is a loss to the firm.

– Loss or deficiency of an insolvent partner has to be borne by the solvent partners.

– The rule Garner Vs Murray is applicable in case of insolvency of one or more

partners but not all the partners.

– All the solvent partners should bring cash equal to their share of the loss on

realisation.

– The deficiency of the insolvent partner must be borne by the solvent partners in

the ratio of their capital then standing.

56

BPK2A - FINANCIAL ACCOUNTING II

TM

Insolvency of all partners

When all the partners become insolvent, the loss on account of insolvency of

the partners will have to be borne by the creditors.

only sundry assets are transferred to realisation account.

The external liabilities (creditors, bills payable bank O/D etc) are not to be

transferred to realisation account but separate account may be prepared.

Creditors are paid all cash available together with the amount received from

the private estate of the partners, after meeting the expenses on realisation.

Any balance remaining unpaid to the creditors will be transferred to a

‗Deficiency Account‘.

The amount not paid by the partners will also be transferred to the deficiency A/c.

The deficiency account shall automatically closed and the books will thus be

closed.

57

BPK2A - FINANCIAL ACCOUNTING II

TM

Piecemeal distribution

The assets are sold gradually to realize the best price for them.

The liabilities are paid off gradually depending upon amount

realised from the sale of assets.

when the partners are not able to get their capital immediately,

they will have to suffer a lot due to financial problem.

So they should be paid as and when the firm has funds left with it

after payment of all outside liabilities.

58

BPK2A - FINANCIAL ACCOUNTING II

TM

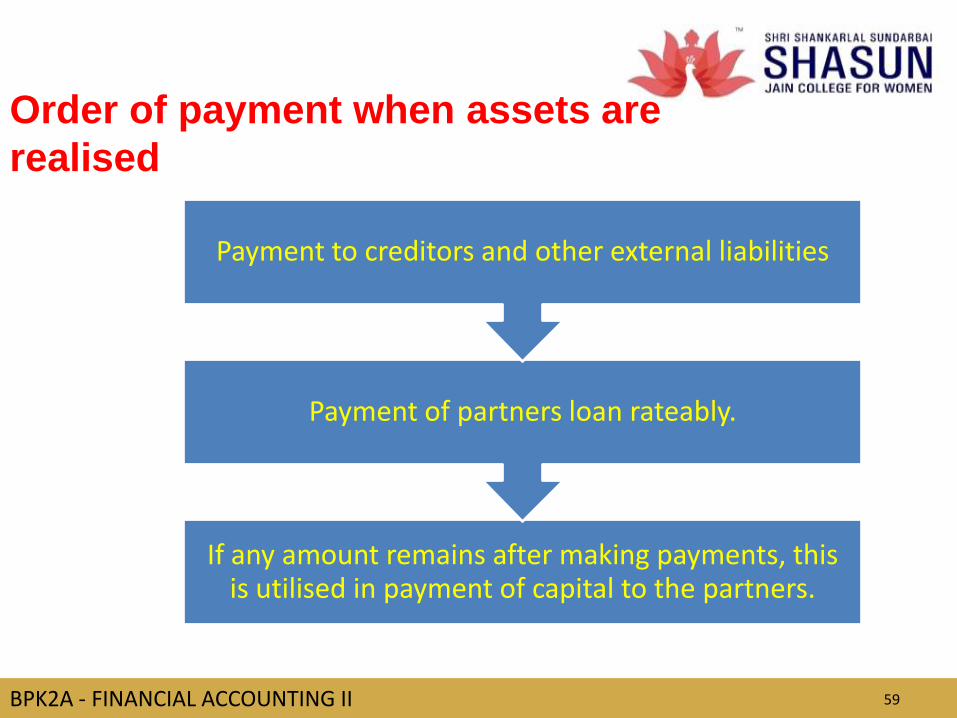

Order of payment when assets are

realised

If any amount remains after making payments, this is utilised in payment of capital to the partners.

Payment of partners loan rateably.

Payment to creditors and other external liabilities

59

BPK2A - FINANCIAL ACCOUNTING II

TM

Methods of payments

Proportionate Capital Method

Maximum Loss Method

60

TM

BPK2A - FINANCIAL ACCOUNTING II

•Introduction to operating system

•Windows

•Tally package

•Introduction to SAP and ERP

UNIT V SYLLABUS

61

TM

BPK2A - FINANCIAL ACCOUNTING II

An operating system (OS) is system software that manages

computer hardware and software resources and provides common

services for computer programs. All computer programs, excluding

firmware, require an operating system to function.

Introduction to operating

system

61

TM

BPK2A - FINANCIAL ACCOUNTING II

Operating system

62

TM

BPK2A - FINANCIAL ACCOUNTING II 63

Operating system

TM

BPK2A - FINANCIAL ACCOUNTING II 64

Operating system

TM

BPK2A - FINANCIAL ACCOUNTING II 65

Microsoft Windows, or simply Windows, is a metafamily of graphical

operating systems developed, marketed, and sold by Microsoft. It

consists of several families of operating systems, each of which cater

to a certain sector of the computing industry with the OS typically

associated with IBM PC compatible architecture. Active Windows

families include Windows NT and Windows Embedded; these may

encompass subfamilies, e.g. Windows Embedded Compact (Windows

CE) or Windows Server. Defunct Windows families include Windows

9x,Windows Mobile and Windows Phone.

Windows

TM

BPK2A - FINANCIAL ACCOUNTING II 66

•Windows 3.1•First widely used successful version of Windows•Replaced MS-DOS

•Windows 95•Introduced Start button, taskbar for multitasking, and My Computer for easier file management

•Windows NT•Intended for business computing•Increased reliability and security

•Windows 98•Active desktop displays Web content•Enables Web conventions on the desktop

•Windows 2000•Security of NT with Windows 98 Interface•Windows 2000 Professional and Windows 2000 Server

•Windows Me (Millennium Edition)•Successor to Windows 98 for home computing

Evolution of Windows

The Windows Desktop

Start Button

Taskbar (multitasking)

My Computer

BPK2A - FINANCIAL ACCOUNTING II 6768

Anatomy of a Window

• Title bar with Min, Max or Restore, and Close buttons• Menu bar, Toolbar, and Address bar• Status bar and Scroll bars

BPK2A - FINANCIAL ACCOUNTING II 6869

The Devices on a

System

• Drive A is always a floppy disk

• Drive B is a second floppy disk (obsolete)

• Drive C is always a fixed disk

• Drives D, E, are variable

– CD ROM

– Zip drive or removable media

– Network drives

BPK2A - FINANCIAL ACCOUNTING II 6970

Pull-down Menus

• Pull-down menu

• Dimmed command

• Ellipsis

• Check

• Bullet

• Arrowhead

• Submenu

BPK2A - FINANCIAL ACCOUNTING II 7071

Dialog Boxes

• Tabbed dialog box

• Option buttons

• Check box

• Text box

• Spin button

• Command buttons

BPK2A - FINANCIAL ACCOUNTING II 7172

Dialog Boxes continued

• Command buttons

• Open List Box

• Scroll bar

• List box

• Tabbed dialog box

• Help button ?

• Cancel button

• OK button

BPK2A - FINANCIAL ACCOUNTING II 7273

Moving and Sizing a

Window

• To Move a Window

– Click and drag the title bar

• To Size a Window

– Click and drag a corner to change the length and width in

proportion with one another

– Click and drag a border to change just the length or the width

BPK2A - FINANCIAL ACCOUNTING II 74

Formatting a Floppy

• Disk capacity

– 720Kb

– 1.44Mb

• Types of formatting

– Quick (erase)

– Full

• Label

BPK2A - FINANCIAL ACCOUNTING II 75

File Management

• My Computer

– Simpler and less sophisticated

– Can result in multiple open windows at one time

• Windows Explorer

– Hierarchical view on left

– Contents of the selected folder on the right

• Multiple views available for both

– Small icons, Large icons, List, and Details view

BPK2A - FINANCIAL ACCOUNTING II 76

Windows Explorer

• Folder

– Expanded

– Collapsed

• Files

– Program file

– Data file

• File names

– Name

– Extension (type)

BPK2A - FINANCIAL ACCOUNTING II 77

Moving and Copying Files

• Moving Files

– Click and drag to a different

folder on the same drive

– Cut and Paste

– Shortcut Menu

• Copying Files

– Click and drag from one

drive to another

– Copy and Paste

– Shortcut Menu

BPK2A - FINANCIAL ACCOUNTING II78

The Help Command

• Accessed from the Start button

• Tabs– Contents tab

– Index tab

– Search tab

– Favorites tab

• Web help

BPK2A - FINANCIAL ACCOUNTING II79

Introduction

You have already known how to maintain accounts manually.

Tally is an accounting package which is used for maintaining your accounts electronically.

BPK2A - FINANCIAL ACCOUNTING II80

General Features of Tally

• It maintains all the primary books of accounts, like Cash Book and Bank Book.

• Tally maintains all registers like Purchase Register, Sales Registers and Journal Registers.

• Tally maintains all statement of accounts like Balance Sheet, Profit and Loss and Trial Balance, Cash Flow and Stock Statement.

BPK2A - FINANCIAL ACCOUNTING II81

General Features of Tally

• A Tally can maintain ‘Outstanding Reports’.

• It may provide complete bill-wise information of amounts receivable as well as payable either party-wise or group-wise.

• It can provide a report for a particular date or reports for any range of dates.

BPK2A - FINANCIAL ACCOUNTING II82

General Features of Tally

• It provides the facility of Bank Reconciliation.

BPK2A - FINANCIAL ACCOUNTING II83

Getting Started with Tally

On the home page of Tally screen ‗Create Company‘ option is available

under the title ‗Company Info‘.

BPK2A - FINANCIAL ACCOUNTING II 84

Create Company

On the home page of Tally screen ‗Create Company‘ option is available

under the title ‗Company Info‘.

To create the company you

would click at ‗Create

Company‘ option

BPK2A - FINANCIAL ACCOUNTING II 85

Create Company

On the home page of Tally screen ‗Create Company‘ option is available

under the title ‗Company Info‘.

To create the company you

would click at ‗Create

Company‘ option

A new window will

appear with various

items on the

screen.

BPK2A - FINANCIAL ACCOUNTING II 86

Create CompanyWhen you click at ‗Create Company‘ option, a new

window will appear with various items on the

screen.

Some important ones are discussed below:

– Name: Type the name of the company you want to create.

– Mailing Name: The mailing name by default is the same as the

name mentioned above. You can type some other mailing name

of the company.

– Address: Type mailing address of the company. There is no limit

on the number if lines used.

BPK2A - FINANCIAL ACCOUNTING II 87

Create Company– Maintain: In Tally accounts can be maintained in a two

different ways:

• Accounts Only

• Accounts-with-inventory

– Use Security Control: This option provides security

control to your company accounts by offering a

comprehensive pass-based access control.

After filling all the required information press enter. A new

window will appear asking for confirmation.

For acceptance press ‗Y‘.

BPK2A - FINANCIAL ACCOUNTING II 88

Create Company

The next window is as follow :

BPK2A - FINANCIAL ACCOUNTING II 89

Company InfoOnce you get your company created, the heading ‗Company

Info‘ has a content of some new options. These options are

as follows:

– Select Company: This option permits you to load any company,

which was created earlier, from the list of companies listed.

– Shut Company: It allows you to exit, from the companies not in

use, from the dialog box.

– Create Company: (same as done above under same heading).

BPK2A - FINANCIAL ACCOUNTING II 90

Company Info– Alter: It allows you to change the information of an existing

company filled at the time of creation of the company.

– Change Tally Vault: To change the password, given earlier at the time of creating the company.

– Split Company Data: Split the companies to form two companies out of the existing one; after the data specify by the user. In this process the closing balance of the first company will become the opening balance of the second company.

– Backup/ Restore: This option allows the user to take a backup either on local hard disk or on any external media. The backup of one or more companies can be taken under a single directory.

BPK2A - FINANCIAL ACCOUNTING II 91

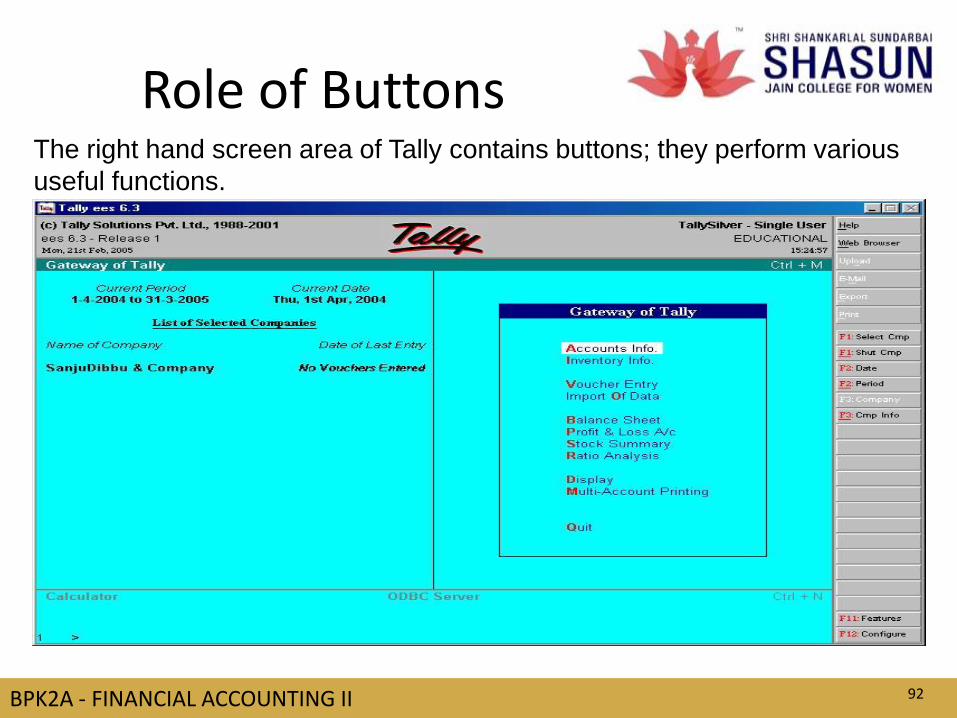

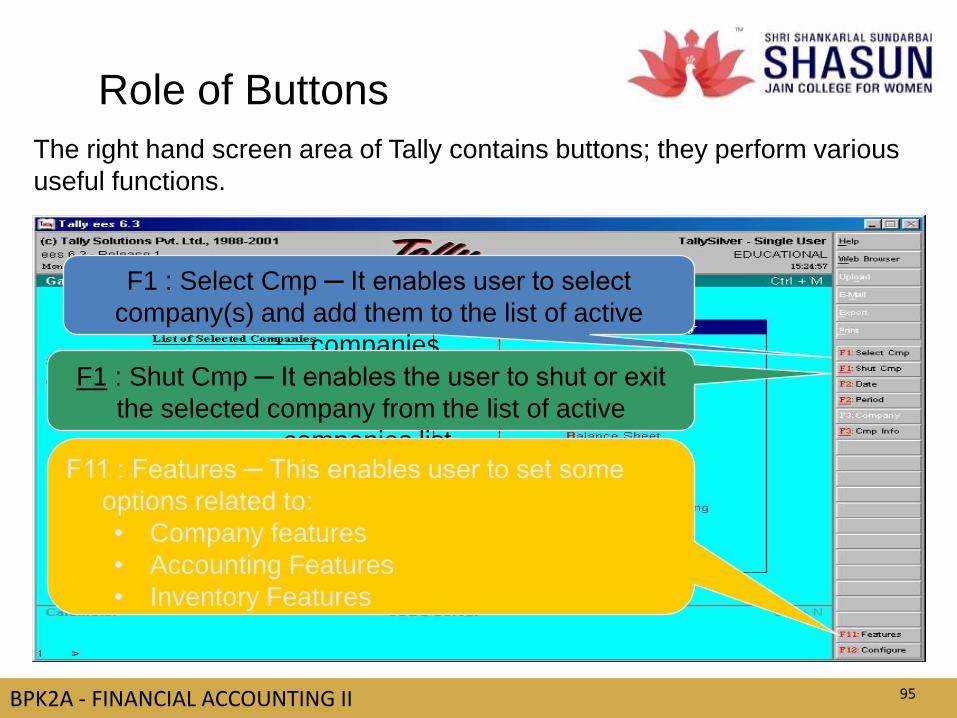

Role of ButtonsThe right hand screen area of Tally contains buttons; they perform various

useful functions.

BPK2A - FINANCIAL ACCOUNTING II 92

Role of ButtonsThe right hand screen area of Tally contains buttons; they perform various

useful functions.

F1 : Select Cmp ─ It enables user to select

company(s) and add them to the list of active

companies.

BPK2A - FINANCIAL ACCOUNTING II 93

Role of Buttons

The right hand screen area of Tally contains buttons; they perform various

useful functions.

F1 : Select Cmp ─ It enables user to select

company(s) and add them to the list of active

companies.

F1 : Shut Cmp ─ It enables the user to shut or exit

the selected company from the list of active

companies list.

BPK2A - FINANCIAL ACCOUNTING II 94

Role of Buttons

The right hand screen area of Tally contains buttons; they perform various

useful functions.

F1 : Select Cmp ─ It enables user to select

company(s) and add them to the list of active

companies.

F1 : Shut Cmp ─ It enables the user to shut or exit

the selected company from the list of active

companies list. F11 : Features ─ This enables user to set some

options related to:

• Company features

• Accounting Features

• Inventory Features

BPK2A - FINANCIAL ACCOUNTING II 95

TM

BPK2A - FINANCIAL ACCOUNTING II

SAP was founded in 1972 in Walldorf, Germany. It stands for

Systems, Applications and Products in Data Processing. Over the

years, it has grown and evolved to become the world premier

provider of client/server business solutions for which it is so well

known today. The SAP R/3 enterprise application suite for open

client/server systems has established a new standards for providing

business information management solutions.SAP product are

consider excellent but not perfect. The main problems with software

product is that it can never be perfect.

The main advantage of using SAP as your company ERP system is

that SAP have a very high level of integration among its individual

applications which guarantee consistency of data throughout the

system and the company itself.

Introduction to SAP

96

TM

BPK2A - FINANCIAL ACCOUNTING II 97

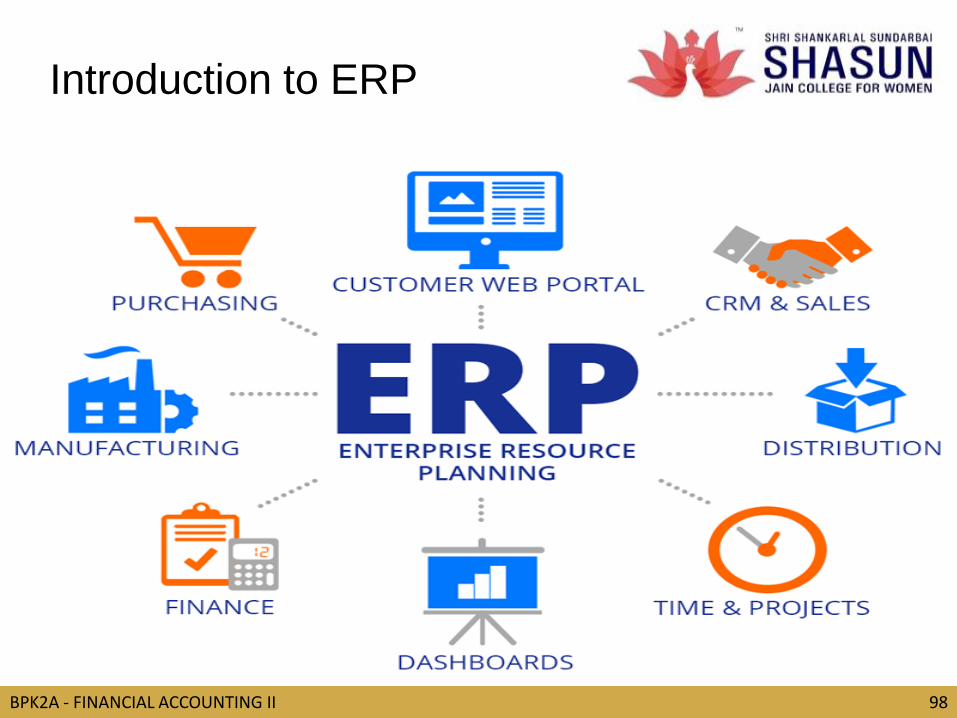

Introduction to ERP

Enterprise resource planning (ERP) is the integrated management

of core business processes, often in real-time and mediated by

software and technology. These business activities can include:

product planning, purchase

production planning

manufacturing or service delivery

marketing and sales

materials management

inventory management

retail

shipping and payment

finance

ERP is usually referred to as a category of business-

management software — typically a suite of integrated applications—

that an organization can use to collect, store, manage and interpret

data from these many businessactivities.

TM

BPK2A - FINANCIAL ACCOUNTING II 98

Introduction to ERP