Embed Size (px)

Citation preview

1

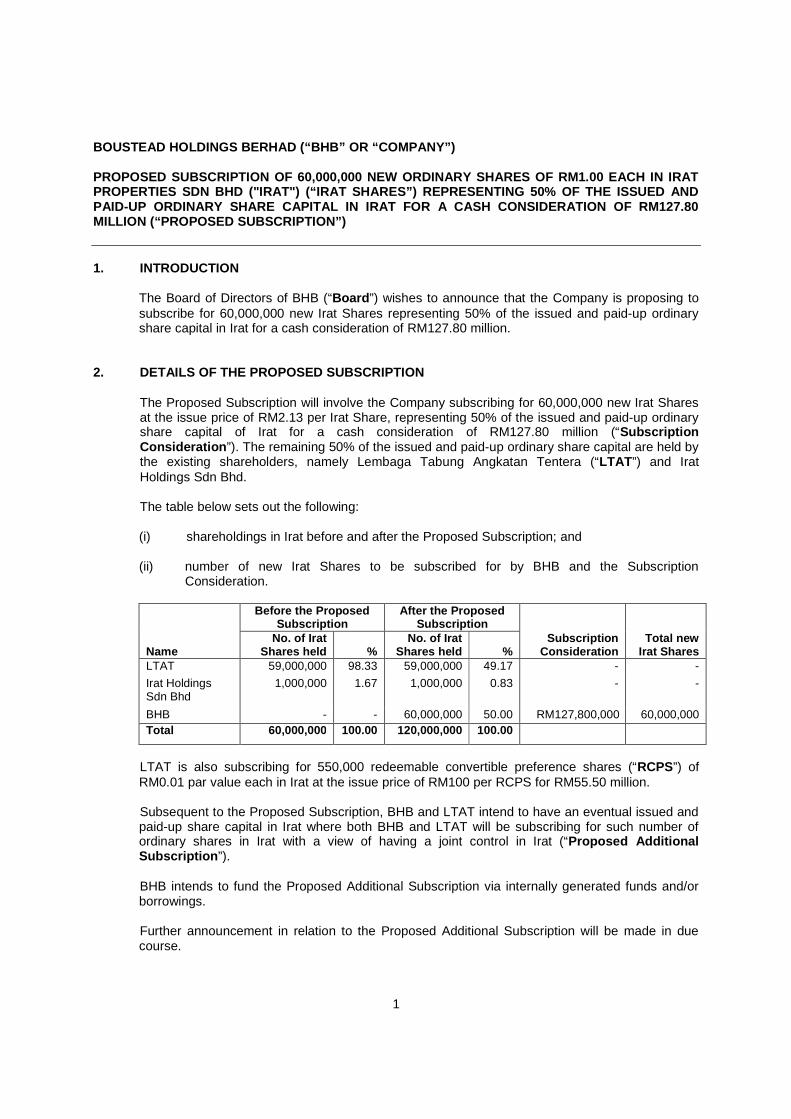

BOUSTEAD HOLDINGS BERHAD (“BHB” OR “COMPANY”)

PROPOSED SUBSCRIPTION OF 60,000,000 NEW ORDINARY SHARES OF RM1.00 EACH IN IRATPROPERTIES SDN BHD ("IRAT") (“IRAT SHARES”) REPRESENTING 50% OF THE ISSUED ANDPAID-UP ORDINARY SHARE CAPITAL IN IRAT FOR A CASH CONSIDERATION OF RM127.80MILLION (“PROPOSED SUBSCRIPTION”)

1. INTRODUCTION

The Board of Directors of BHB (“Board”) wishes to announce that the Company is proposing tosubscribe for 60,000,000 new Irat Shares representing 50% of the issued and paid-up ordinaryshare capital in Irat for a cash consideration of RM127.80 million.

2. DETAILS OF THE PROPOSED SUBSCRIPTION

The Proposed Subscription will involve the Company subscribing for 60,000,000 new Irat Sharesat the issue price of RM2.13 per Irat Share, representing 50% of the issued and paid-up ordinaryshare capital of Irat for a cash consideration of RM127.80 million (“SubscriptionConsideration”). The remaining 50% of the issued and paid-up ordinary share capital are held bythe existing shareholders, namely Lembaga Tabung Angkatan Tentera (“LTAT”) and IratHoldings Sdn Bhd.

The table below sets out the following:

(i) shareholdings in Irat before and after the Proposed Subscription; and

(ii) number of new Irat Shares to be subscribed for by BHB and the SubscriptionConsideration.

Name

Before the ProposedSubscription

After the ProposedSubscription

No. of IratShares held %

No. of IratShares held %

SubscriptionConsideration

Total newIrat Shares

LTAT 59,000,000 98.33 59,000,000 49.17 - -

Irat HoldingsSdn Bhd

1,000,000 1.67 1,000,000 0.83 - -

BHB - - 60,000,000 50.00 RM127,800,000 60,000,000

Total 60,000,000 100.00 120,000,000 100.00

LTAT is also subscribing for 550,000 redeemable convertible preference shares (“RCPS”) ofRM0.01 par value each in Irat at the issue price of RM100 per RCPS for RM55.50 million.

Subsequent to the Proposed Subscription, BHB and LTAT intend to have an eventual issued andpaid-up share capital in Irat where both BHB and LTAT will be subscribing for such number ofordinary shares in Irat with a view of having a joint control in Irat (“Proposed AdditionalSubscription”).

BHB intends to fund the Proposed Additional Subscription via internally generated funds and/orborrowings.

Further announcement in relation to the Proposed Additional Subscription will be made in duecourse.

2

(a) Basis of arriving and justification for the Subscription Consideration

The Subscription Consideration was arrived at on a willing-buyer willing-seller basis aftertaking into consideration the following:

(i) the historical financial performance of Irat and its subsidiary (“Irat Group”) as setout in Appendix I of this announcement;

(ii) the unaudited consolidated net assets (“NA”) of Irat as at 31 December 2014 ofRM127.98 million or the NA of RM2.13 per Irat Share; and

(iii) the future prospects of Irat Group as set out in Section 6.2 of this announcement.

(b) Mode of settlement and source of funding

The Proposed Subscription is to be funded by internally generated funds of BHB and itssubsidiaries (“BHB Group” or “Group”) and/or borrowings.

(c) Information on Irat

Irat was incorporated in Malaysia under the Companies Act, 1965 (“Act”) as a privatelimited company on 15 April 1996. The principal activity of Irat is investment holding whilstits subsidiary is involved in property investment. Irat owns 70% equity interest in IratHotels & Resorts Sdn Bhd.

(The rest of this page is intentionally left blank)

3

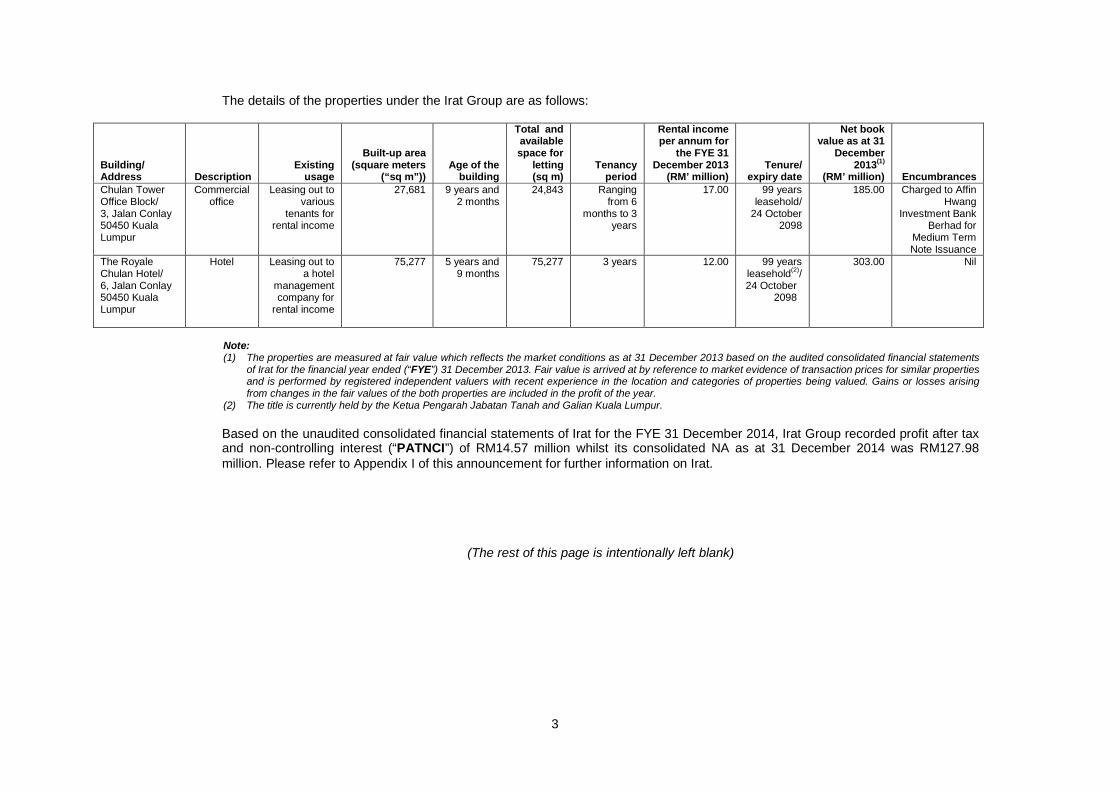

The details of the properties under the Irat Group are as follows:

Building/Address Description

Existingusage

Built-up area(square meters

(“sq m”))Age of the

building

Total andavailablespace for

letting(sq m)

Tenancyperiod

Rental incomeper annum for

the FYE 31December 2013

(RM’ million)Tenure/

expiry date

Net bookvalue as at 31

December2013(1)

(RM’ million) EncumbrancesChulan TowerOffice Block/3, Jalan Conlay50450 KualaLumpur

Commercialoffice

Leasing out tovarious

tenants forrental income

27,681 9 years and2 months

24,843 Rangingfrom 6

months to 3years

17.00 99 yearsleasehold/

24 October2098

185.00 Charged to AffinHwang

Investment BankBerhad for

Medium TermNote Issuance

The RoyaleChulan Hotel/6, Jalan Conlay50450 KualaLumpur

Hotel Leasing out toa hotel

managementcompany for

rental income

75,277 5 years and9 months

75,277 3 years 12.00 99 yearsleasehold(2)/24 October

2098

303.00 Nil

Note:(1) The properties are measured at fair value which reflects the market conditions as at 31 December 2013 based on the audited consolidated financial statements

of Irat for the financial year ended (“FYE”) 31 December 2013. Fair value is arrived at by reference to market evidence of transaction prices for similar propertiesand is performed by registered independent valuers with recent experience in the location and categories of properties being valued. Gains or losses arisingfrom changes in the fair values of the both properties are included in the profit of the year.

(2) The title is currently held by the Ketua Pengarah Jabatan Tanah and Galian Kuala Lumpur.

Based on the unaudited consolidated financial statements of Irat for the FYE 31 December 2014, Irat Group recorded profit after taxand non-controlling interest (“PATNCI”) of RM14.57 million whilst its consolidated NA as at 31 December 2014 was RM127.98million. Please refer to Appendix I of this announcement for further information on Irat.

(The rest of this page is intentionally left blank)

4

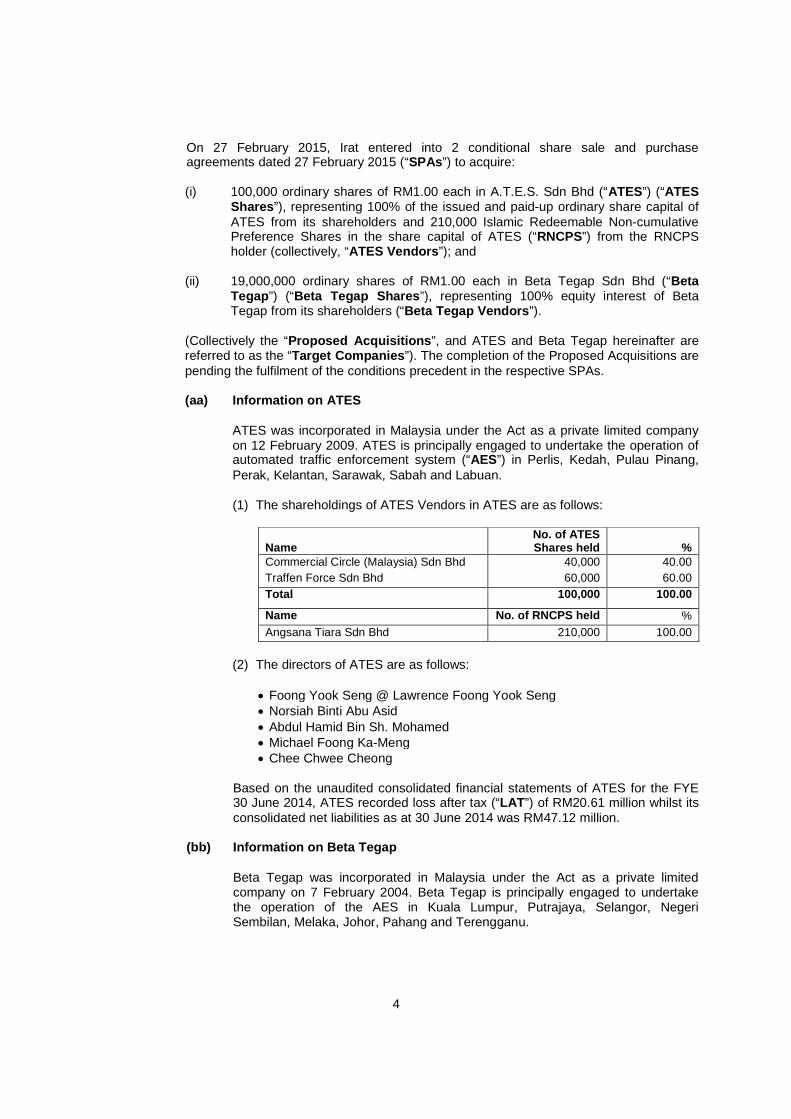

On 27 February 2015, Irat entered into 2 conditional share sale and purchaseagreements dated 27 February 2015 (“SPAs”) to acquire:

(i) 100,000 ordinary shares of RM1.00 each in A.T.E.S. Sdn Bhd (“ATES”) (“ATESShares”), representing 100% of the issued and paid-up ordinary share capital ofATES from its shareholders and 210,000 Islamic Redeemable Non-cumulativePreference Shares in the share capital of ATES (“RNCPS”) from the RNCPSholder (collectively, “ATES Vendors”); and

(ii) 19,000,000 ordinary shares of RM1.00 each in Beta Tegap Sdn Bhd (“BetaTegap”) (“Beta Tegap Shares”), representing 100% equity interest of BetaTegap from its shareholders (“Beta Tegap Vendors”).

(Collectively the “Proposed Acquisitions”, and ATES and Beta Tegap hereinafter arereferred to as the “Target Companies”). The completion of the Proposed Acquisitions arepending the fulfilment of the conditions precedent in the respective SPAs.

(aa) Information on ATES

ATES was incorporated in Malaysia under the Act as a private limited companyon 12 February 2009. ATES is principally engaged to undertake the operation ofautomated traffic enforcement system (“AES”) in Perlis, Kedah, Pulau Pinang,Perak, Kelantan, Sarawak, Sabah and Labuan.

(1) The shareholdings of ATES Vendors in ATES are as follows:

NameNo. of ATESShares held %

Commercial Circle (Malaysia) Sdn Bhd 40,000 40.00

Traffen Force Sdn Bhd 60,000 60.00

Total 100,000 100.00

Name No. of RNCPS held %

Angsana Tiara Sdn Bhd 210,000 100.00

(2) The directors of ATES are as follows:

Foong Yook Seng @ Lawrence Foong Yook Seng Norsiah Binti Abu Asid Abdul Hamid Bin Sh. Mohamed Michael Foong Ka-Meng Chee Chwee Cheong

Based on the unaudited consolidated financial statements of ATES for the FYE30 June 2014, ATES recorded loss after tax (“LAT”) of RM20.61 million whilst itsconsolidated net liabilities as at 30 June 2014 was RM47.12 million.

(bb) Information on Beta Tegap

Beta Tegap was incorporated in Malaysia under the Act as a private limitedcompany on 7 February 2004. Beta Tegap is principally engaged to undertakethe operation of the AES in Kuala Lumpur, Putrajaya, Selangor, NegeriSembilan, Melaka, Johor, Pahang and Terengganu.

5

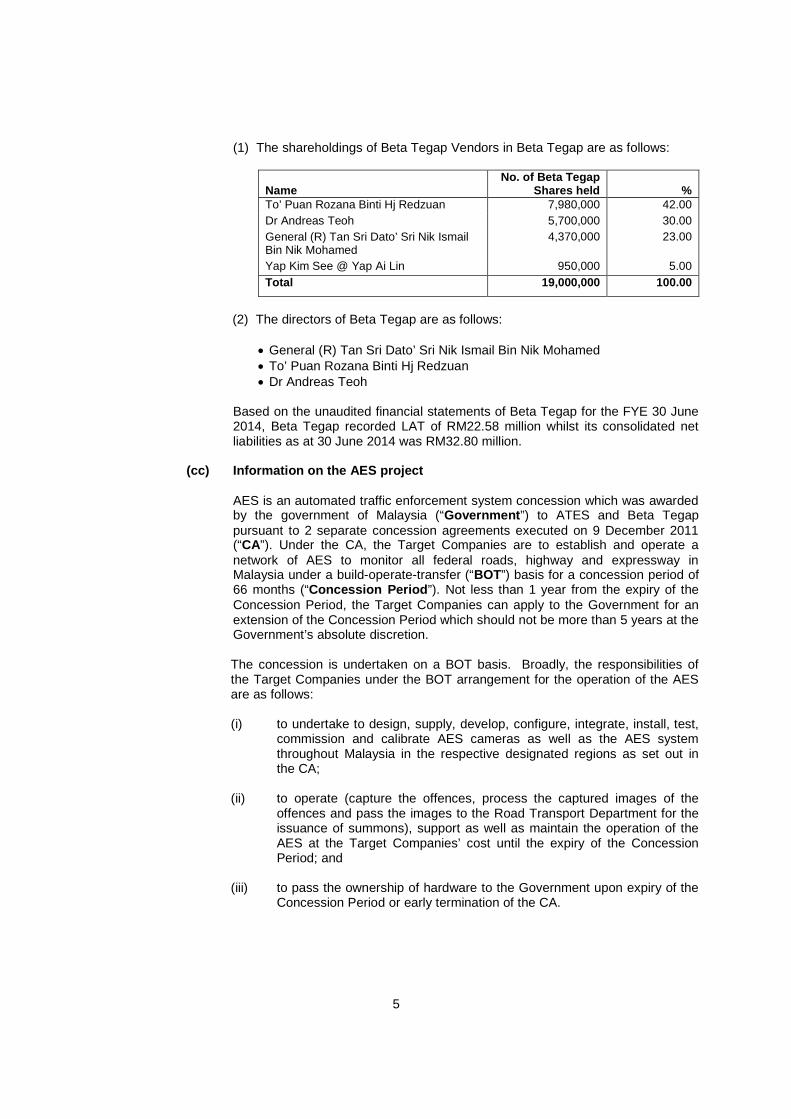

(1) The shareholdings of Beta Tegap Vendors in Beta Tegap are as follows:

NameNo. of Beta Tegap

Shares held %To’ Puan Rozana Binti Hj Redzuan 7,980,000 42.00

Dr Andreas Teoh 5,700,000 30.00

General (R) Tan Sri Dato’ Sri Nik IsmailBin Nik Mohamed

4,370,000 23.00

Yap Kim See @ Yap Ai Lin 950,000 5.00

Total 19,000,000 100.00

(2) The directors of Beta Tegap are as follows:

General (R) Tan Sri Dato’ Sri Nik Ismail Bin Nik Mohamed To’ Puan Rozana Binti Hj Redzuan Dr Andreas Teoh

Based on the unaudited financial statements of Beta Tegap for the FYE 30 June2014, Beta Tegap recorded LAT of RM22.58 million whilst its consolidated netliabilities as at 30 June 2014 was RM32.80 million.

(cc) Information on the AES project

AES is an automated traffic enforcement system concession which was awardedby the government of Malaysia (“Government”) to ATES and Beta Tegappursuant to 2 separate concession agreements executed on 9 December 2011(“CA”). Under the CA, the Target Companies are to establish and operate anetwork of AES to monitor all federal roads, highway and expressway inMalaysia under a build-operate-transfer (“BOT”) basis for a concession period of66 months (“Concession Period”). Not less than 1 year from the expiry of theConcession Period, the Target Companies can apply to the Government for anextension of the Concession Period which should not be more than 5 years at theGovernment’s absolute discretion.

The concession is undertaken on a BOT basis. Broadly, the responsibilities ofthe Target Companies under the BOT arrangement for the operation of the AESare as follows:

(i) to undertake to design, supply, develop, configure, integrate, install, test,commission and calibrate AES cameras as well as the AES systemthroughout Malaysia in the respective designated regions as set out inthe CA;

(ii) to operate (capture the offences, process the captured images of theoffences and pass the images to the Road Transport Department for theissuance of summons), support as well as maintain the operation of theAES at the Target Companies’ cost until the expiry of the ConcessionPeriod; and

(iii) to pass the ownership of hardware to the Government upon expiry of theConcession Period or early termination of the CA.

6

The Government may expropriate the CA by giving notice of not less than 3months to that effect to the Target Companies if it considers that suchexpropriation is in the national interest, public interest, public policy, Governmentpolicy or national security or terminate the CA at any time by giving notice to theTarget Companies in the event of defaults by the Target Companies as set out inthe CA.

The operation of the AES commenced with 14 cameras installed sinceSeptember 2012 and the said operation is financed through bank borrowings,proceeds from issuance of securities and internally generated funds.

3. LIABILITIES TO BE ASSUMED PURSUANT TO THE PROPOSED SUBSCRIPTION

There are currently no liabilities, including contingent liabilities and guarantees to be assumed byBHB pursuant to the Proposed Subscription.

4. RATIONALE FOR THE SUBSCRIPTION

The principal activities of BHB are investment holding, provision of management services to itssubsidiaries and property investment. The subsidiaries, associated companies and joint venturecompanies of BHB are mainly involved in:

(a) planting of oil palm and processing of crude palm oil;

(b) shipbuilding, fabrication of offshore structures as well as the restoration and maintenance ofvessels and defence related products;

(c) property development, construction and leasing of commercial and retail properties as well asowning and operating hotels (“Property Division”);

(d) investing activities of the BHB Group;

(e) manufacturing, trading and marketing of pharmaceutical products, research and developmentof pharmaceutical products and the supply of medical and hospital equipment; and

(f) owning and operating the BHPetrol brand of retail petrol station network and themanufacturing and trading of building materials.

The Proposed Subscription forms part of BHB Group’s strategy to continue exploring growthopportunities with a view of driving and realising its potential to add value to the BHB Group.

The external sales generated by the Property Division in the FYE 31 December 2013 wasRM624.50 million, representing 5.57% of the total revenue of the BHB Group of RM11.21 billion.The Proposed Subscription will allow BHB Group to expand its investment in the property sectoras well as the hospitality and tourism sector which is in-line with its strategic plan to furtherexpand its Property Division to gain more market share in these sectors. Upon completion of theProposed Acquisitions, the BHB Group will also be invested in the AES project in Malaysia byvirtue of Irat being a jointly controlled company of BHB after the Proposed Subscription.

The Board is of the view that the positive outlook of the offices market, leisure sub-sector andvarious government incentives in boosting the tourism industry in Malaysia (as set out in Section6.1 of this announcement) are expected to augur well for the Irat Group’s property segment.

7

The Proposed Acquisitions undertaken by Irat will provide the Irat Group with another source ofrevenue. Nonetheless, the success of the implementation of the AES project is dependent on,inter-alia, the completion of the Proposed Acquisitions, the roll-out of camera installationthroughout the country and support from the suppliers as set out in Section 5 of thisannouncement.

The Board is of the view that the Proposed Subscription also provides the BHB Group anopportunity to participate in a project which aims at reducing the number of road accidents androad fatality in Malaysia upon the completion of the Proposed Acquisitions.

5. RISK FACTORS IN RELATION TO THE PROPOSED SUBSCRIPTION

The risks in relation to the Proposed Subscription include but are not limited to the following:

(a) Business risk

Both the Irat Group and BHB Group are subject to risks inherent in the property sector aswell as the hospitality and tourism sector of which they are already involved in, whichinclude, inter-alia, adverse changes in real estate market prices, changes in demand fortypes of residential and commercial properties, competition from other propertyinvestment companies, changes in economic, social and political condition, labour andmaterial supply shortages, changes in tourists arrival rate and implementation of goodsand services tax which in turn affect the rentals of offices and hotels. Any adversechange in such conditions may have an adverse material effect on the BHB Group.

(b) Investment risk

The investment in Irat is illiquid where there may not be a ready market to dispose ofBHB’s holdings in Irat since it is a privately owned company (unlike holdings of shares ina listed entity). There is a risk that BHB may not be able to find a buyer for its interest inIrat to realise any gain on the investment in the future. Any future sale is subject to, inter-alia, the general market, political and economic conditions, changes in earningsestimates, changes in governmental policy, legislation or regulation, and generaloperational and business risks.

The Irat Group is also potentially facing the following risks with regards to the ProposedAcquisitions and the operation of the AES. These risks include but are not limited to the following:

(a) Non-completion risk

The SPAs are subject to the risk of non-completion if the conditions precedents set out inthe SPAs are not fulfilled or waived (as the case maybe) before the expiration of theagreed period.

In addition, there can be no assurance that the Proposed Acquisitions can be completedwithin the time frame set out in the SPA or that the Proposed Acquisitions will not beexposed to risks such as the inability to obtain the approvals from the relevantauthorities/parties and/or inability to comply with the conditions imposed by the relevantauthorities/parties such as their financier, if any.

8

(b) Business risk

On completion of the Proposed Acquisitions, the Irat Group’s business will include theoperation of the AES. The Irat Group will then be subject to new challenges and risksarising from the operation of the AES. These may include shortage of labour, rapidchanges in technology which are relevant to the AES, changes in the attitude of driverson the road, as well as changes in economic, social and political conditions in Malaysia.

However, it is the intention of Irat to retain the key management and technical personnelof the Target Companies to ensure that Irat together with the Target Companies are keptabreast with the latest development in AES technology and the changes in economic,social and political conditions surrounding the AES.

Currently, there are only 14 cameras in operations. The AES project is pending a full roll-out of camera installation throughout the country. Therefore, there is a gestation periodfor the full implementation of the AES project and there is no assurance that suchimplementation will be timely and successfully completed.

In an effort to mitigate this risk, the Irat Group will continue to engage the relevantauthorities/parties involved in the implementation of the AES project.

Notwithstanding the above and taking into account that the Proposed Acquisitions will bethe Irat Group’s maiden undertaking in the operation of the AES, there is no assurancethat any changes to the abovementioned factors will not materially affect the Irat Group’sperformance which may affect its profit contribution to the BHB Group.

(c) Reliance on the CA awarded by the Government

The Target Companies rely on the CA awarded by the Government. As such, the IratGroup’s business may be materially and adversely affected if thetermination/expropriation clause is invoked by the Government or the CAs arerenegotiated with less favourable terms. Such occurrence will expose the Irat Group tothe risk of being unable to continue to operate the AES which in turn will affect theviability of the Irat Group’s business.

Nonetheless, Irat Group intends to continue discussion with the Government in relation tothe terms and conditions of the CA to ensure the continuity of the CA.

Although the Irat Group seeks to limit this risk by having continuous discussion with theGovernment to ensure the continuity of the CA, no assurance can be given that anyfailure in the discussion will not have a material adverse effect on the operation of theAES.

(d) Reliance on supplier agreements

The Target Companies rely on third party suppliers to provide hardware and software tooperate the AES. As such, the Irat Group’s business may be materially and adverselyaffected if these third party products and services are no longer provided. ATES currentlyhas a key agreement with international hardware and software supplier for the AESequipment. Beta Tegap also has a key agreement with the supplier of the AESequipment. The Irat Group is exposed to the risk of being unable to continue to securethe hardware or software to run the operation of the AES should these agreements berenegotiated or terminated. Nonetheless, the management of the Irat Group together withthe Target Companies are committed to prevent any disruption to the operations of theTarget Companies by reaffirming and/or signing a supplemental agreement with thesuppliers, where necessary.

9

The continuous relationships with these suppliers are important for mutual businesssupport. It is the intention of Irat to retain the key management and technical personnel ofthe Target Companies to also help maintain the said relationships.

In the event that there is any termination of distribution by any supplier, Irat will take thenecessary steps to ensure the continuity of its operations and source the AES equipmentfrom other suppliers.

(e) Financing risk

Following the completion of the Proposed Acquisitions, the Irat Group will consolidate theborrowings of the Target Companies in its financial statements. Accordingly, the IratGroup is subject to risks associated with debt financing, including changes in the level ofinterest rates and liquidity risk. Any adverse fluctuations in interest rates may have asignificant impact on the Irat Group’s financial performance.

While we understand that the management of the Irat Group endeavours to take everyeffort to ensure that no adverse effects will arise from the interest commitments, there isno assurance that it will not have any material impact on the Irat Group’s financialperformance in the future.

Although the BHB Group will continuously take appropriate measures to mitigate such risks, noassurance can be given that any change to these factors will not have a material adverse impacton the BHB Group.

6. OUTLOOK AND PROSPECTS

The Irat Group is currently involved in property investment through the letting out of office spaceand a hotel. Accordingly, the Irat Group is dependent on the prospects of the general Malaysianeconomy, property sector as well as the hospitality and tourism sector. On completion of theProposed Acquisitions, the Irat Group will be involved in the operation of the AES project.

6.1 Outlook

(a) The Malaysian economy

The economic growth momentum in 2014 is expected to continue in 2015 driven byimproving external demand and resilient domestic economic activity. Growth will beprivate-led in line with the Government’s efforts to strengthen the private sector’s role inthe economy.

On the supply side, all economic sectors are expected to record positive growth in 2015,with the services and manufacturing sectors remaining the major contributors to growth.Sustained growth in domestic demand, albeit at a moderate pace, is expected tocontribute to the expansion in domestic-related activities. The economy is projected togrow 5%-6% in 2015.

(Source: Economic Report 2014/2015, Ministry of Finance, Malaysia)

10

The 2015 Budget was formulated based on:

(i) Price of Brent crude oil forecasted at USD100 per barrel;(ii) Gross Domestic Product growth estimated between 5% and 6%;(iii) A stable exchange rate of RM3.20 against the US dollar; and(iv) 2015 world economic growth projected at 3.4% and 3.9% by the World Bank and

International Monetary Fund respectively.

Since then, the World Bank and the International Monetary Fund have revised globalgrowth to 3% and 3.8% respectively. However, the external situation has changed latelyand Malaysia is impacted directly as Malaysia is among the largest trading nations in theworld. Compared to the situation a few months ago, the global economic landscape hassince changed significantly. This necessitates the review and clarification of some of theearlier macro and fiscal assumptions.

In the revised 2015 Budget, the forecast for Malaysia's 2015 economic growth has beenrevised to 4.50% to 5.50% from 5.00% to 6.00% whilst the fiscal deficit target has beenrevised to 3.2% of Gross Domestic Product in 2015 from the earlier fiscal deficit target of3% of Gross Domestic Product.

(Source: Malaysia's revised Budget 2015 speech by YAB Dato' Sri Mohd Najib Tun Haji Abdul Razak, PrimeMinister and Minister of Finance Malaysia on 20 January 2015)

(b) The property sector

Growth in the non-residential subsector turned around sharply by 14% (January to June2013: 1%) in line with healthy business activity during the first half of 2014. This wasreflected by increased construction activities especially for commercial buildings with theincoming supply of shops increasing to 72,117 units (January–June 2013: 66,167 units).

Meanwhile, construction starts for purpose-built offices (“PBO”) decreased substantiallyto 2,965 sq m (January to June 2013: 263,284 sq m), after experiencing strong growth of61.2% in PBO starts in 2013. However, the national occupancy rate of office buildingsremained stable at 83.4% (end-June 2013: 82%) despite an additional 194,798 sq m ofspace.

During the second quarter of 2014, the Purpose-Built Office Rent Index WilayahPersekutuan Kuala Lumpur (”PBO-RI WPKL”) showed that PBO rentals in Kuala Lumpurcontinued to remain stable despite announcements of large planned projects such as theTun Razak Exchange. The PBO-RI WPKL recorded 117 points (second quarter of 2013:114.9 points), increasing 1.8% on account of higher growth Within the City Centre(“WCC”) area. Likewise, the average rental rate of PBO in WCC recorded an increase of5.8% to RM4.41 per square foot (“sq ft”) (second quarter of 2013: 10%; RM4.10 per sqft). The average rental of investment-grade buildings in Kuala Lumpur, particularly KualaLumpur City Centre/Golden Triangle stood at RM6.18 per sq ft (second quarter of 2013:RM6.17 per sq ft), indicating stable rentals for offices in good locations.

(Source: Economic Report 2014/2015, Ministry of Finance, Malaysia)

The office market also moved along the positive trend as indicated by the increase in theoverall occupancy from 82.1% to 83.4%, sustaining a positive take-up of 297,403 sq m(first half of (“H1”) 2013: 290,981 sq m). Ten states recorded positive take-up whereasSabah recorded otherwise. The highest take-up was recorded in Wilayah PersekutuanKuala Lumpur at 188,987 sq m.

11

In terms of performance, 14 states secured more than 80.0% occupancy, of which onewas fully occupied and seven obtained more than 90.0% occupancy. WilayahPersekutuan Kuala Lumpur (80.1%) and Selangor (76.3%) witnessed better performanceagainst H1 2013 whereas Johor (75.7%) dwindled slightly and Pulau Pinang sustained at81.0% occupancy.

(Source: Property Market Report, First Half 2014, Valuation and Property Services Department, Ministry ofFinance, Malaysia)

(c) The hospitality and tourism sector

The wholesale and retail trade as well as accommodation and restaurant subsectors areanticipated to increase 7.1% and 5.9%, respectively in 2015 (2014: 7.7%; 6.1%) driven bystrong domestic consumption and higher tourist arrivals following the Malaysia Year ofFestivals 2015.

The year 2015 has been designated Malaysia Year of Festivals. Boosted by targetedmarketing and promotional activities, tourist spending is expected to remain robust. Theextension of the Visit Malaysia Year into 2015, coupled with continuous efforts to developnew and strengthen niche tourism products, as well as upgrade of existing tourism-related facilities are expected to contribute to higher gross receipts in the travel accountat RM78.2 million (2014: RM76.3 billion).

(Source: Economic Report 2014/2015, Ministry of Finance, Malaysia)

The leisure sub-sector showed a moderate performance as the three to five star hotelsrecorded an overall occupancy of 50.4%, lower than 52.5% in H1 2013. On the contrary,the one to five star hotels recorded an increase in the overall occupancy from 49.1% (H12013) to 53.1% (H1 2014). Although January – May 2014 tourist arrivals (11.53 million)showed a 10.1% increase over the same period of 2013, the Malaysian Institute ofEconomic Research Tourism Market Index recorded a decline at 96.7 points in secondquarter of (“Q2”) 2014 (Q2 2013: 112.6 points).

Performance of three to five star hotels across the states varied. Nine states recordedhigher overall occupancy than the national average. The top three performers wereWilayah Persekutuan Putrajaya, Selangor and Pahang with an overall occupancy of morethan 75.0%.

(Source: Property Market Report, First Half 2014, Valuation and Property Services Department, Ministry ofFinance, Malaysia)

The 2015 Budget is formulated with a focus on the people's economy and outlines sevenmain strategies:

First Strategy: Strengthening Economic Growth;Second Strategy: Enhancing Fiscal Governance;Third Strategy: Developing Human Capital and Entrepreneurship;Fourth Strategy: Advancing Bumiputera Agenda;Fifth Strategy: Upholding Role of Women;Sixth Strategy: Developing National Youth Transformation Programme; andSeventh Strategy: Prioritising Well-Being of the Rakyat.

12

Under the first strategy, strengthening economic growth, the Government will continue toprovide a conducive and comprehensive ecosystem to accelerate domestic and foreigninvestment. One of the measurements is boosting the tourism industry. In conjunctionwith Malaysia - Year of Festivals 2015, the Government is targeting 29.4 million foreigntourist arrivals with expected income of RM89 billion. For this, RM316 million is allocatedfor various programmes under the Ministry of Tourism and Culture.

(Source: Malaysia's Budget 2015 speech by YAB Dato' Sri Mohd Najib Tun Haji Abdul Razak, Prime Ministerand Minister of Finance Malaysia on 10 October 2015)

(d) AES

Following the completion of the SPAs, the Irat Group will also be dependent on theoutlook for the operation of the AES project.

Malaysia is among the top 25 most dangerous countries for road users, with 30 fatalitiesper 100,000 individuals, according to research by the University of Michigan. Conductedby the university’s Transportation Research Institute using 2008 World HealthOrganisation (“WHO”) data on 193 countries, the February 2014 research lists Malaysiaas 17th most dangerous for drivers.

The only other Southeast Asian nation within the 25 most dangerous is Thailand, rankedsecond most dangerous for drivers, with 44 fatalities per 100,000 people. In comparison,the United States of America registered only 14 fatalities, France recorded seven,Germany and Singapore six, and the United Kingdom only five fatalities per 100,000people.

The world average is 18 fatalities per 100,000 people. Namibia topped the mostdangerous list with 45 deaths and the safest place to enjoy a cruise is the small islandnation of the Maldives with two deaths.

(Source: Malaysia has 17th most dangerous roads in the world, according to Michigan university research,dated 22 February 2014, The Star Online, http://www.thestar.com.my/)

In terms of number of vehicles on Malaysian roads, the sales of new motor vehicles (ortotal industry volume (“TIV”)) in 2014 grew 1.6% to 666,465 units eclipsing the previous2013 sales record of 655,793 units. This is a new all-time high record for the localautomotive industry. The TIV achieved had been on the upward trend since 2012 whenthe TIV achieved then was 627,753 units. However, the growth rate achieved in 2014 (i.e.1.6%) was much lower than the growth rates achieved during the previous two years (i.e.4.5% in 2013 and 4.6% in 2012).

The total registration of new passenger vehicles in 2014 rose to 588,341 units from576,657 units in 2013. This was an increase of 11,684 units or a 2.0% growth. Howeverthe total registration for commercial vehicles declined to 78,124 units in 2014 comparedto 79,136 units in 2013. This means commercial vehicles sales had declined by 1,012units or 1.3%.

13

The Malaysian Automotive Association (“MAA”) has forecasted a TIV of 680,000 for theyear 2015 vis-à-vis 666,465 actual TIV for the year 2014 and has taken the followingeconomic and environmental factors into account in their forecast for the TIV in 2015:

(i) The global economy is expected to moderate owing to a number of uncertaintiessuch as the declining crude oil prices, political instability in Middle East etc;

(ii) In tandem with the declining world economic outlook and weakening ringgit, theMalaysian economy is expected to face greater challenges in 2015;

(iii) Inflation and the impending implementation of the Goods and Services Tax (“GST”)in April are two key concerns affecting consumers at large;

(iv) Continuation of the Economic Transformation Programme projects wouldcontribute to the growth momentum of the local economies and help to spur greaterdemand for new vehicles;

(v) Slowdown in consumers' spending in light of the economic uncertainties, impact ofinflationary pressures, and implementation of the GST;

(vi) The tightening of lending guidelines including for hire purchase loans by theauthorities in order to rein in household debts; and

(vii) Aggressive promotional campaigns by car companies.

In view of the above, MAA’s TIV forecast for 2015 versus 2014 is shown in table below:

Market segment 2015(Forecast)

2014(Actual)

VarianceUnits %

Passenger vehicles 600,700 588,341 12,359 2.1Commercial vehicles 79,300 78,124 1,176 1.5Total vehicles 680,000 666,465 13,535 2.0

(Source: Press Conference: Market Review for 2014 and Outlook for 2015 dated 21 January 2015, MAA)

The AES system is an automatic enforcement of traffic laws, and is a continuation of theRoad Safety Plan 2006-2010. It is also part of the on-going efforts of road safety activists(Jabatan Pengangkutan Jalan, Polis Diraja Malaysia, Jabatan Keselamatan Jalan RayaMalaysia, Malaysian Institute of Road Safety Research, Jabatan Kerja Raya Malaysia)focusing on 4E (Engineering, Enforcement, Education and Environment).

The AES system necessitates adaptations of the enforcement system to be sustainable indriving attitude changes regardless of the increase in number of vehicles, drivers orconstraints in enforcement, and is a system based approach that could change theattitude of Malaysian drivers.

(Source: FAQ – Automated Enforcement System, Official Portal of Road Transport Department Malaysia,http://www.jpj.gov.my/en/aes-system)

Accident rates at 14 locations nationwide where the AES cameras were installed havedropped by up to 30% in the first 8 months since the AES was implemented.

Transport Minister Datuk Seri Liow Tiong Lai said studies conducted by the MalaysianInstitute of Road Safety Research (“MIROS”) showed that there were 19 fatal accidents in8 months prior to the AES’ installation at the accident-prone areas. However, that figuredropped to only 12 after the cameras were installed. This translates to a reduction of fatalaccidents by 36.84% or 7 cases within the period of 8 months.

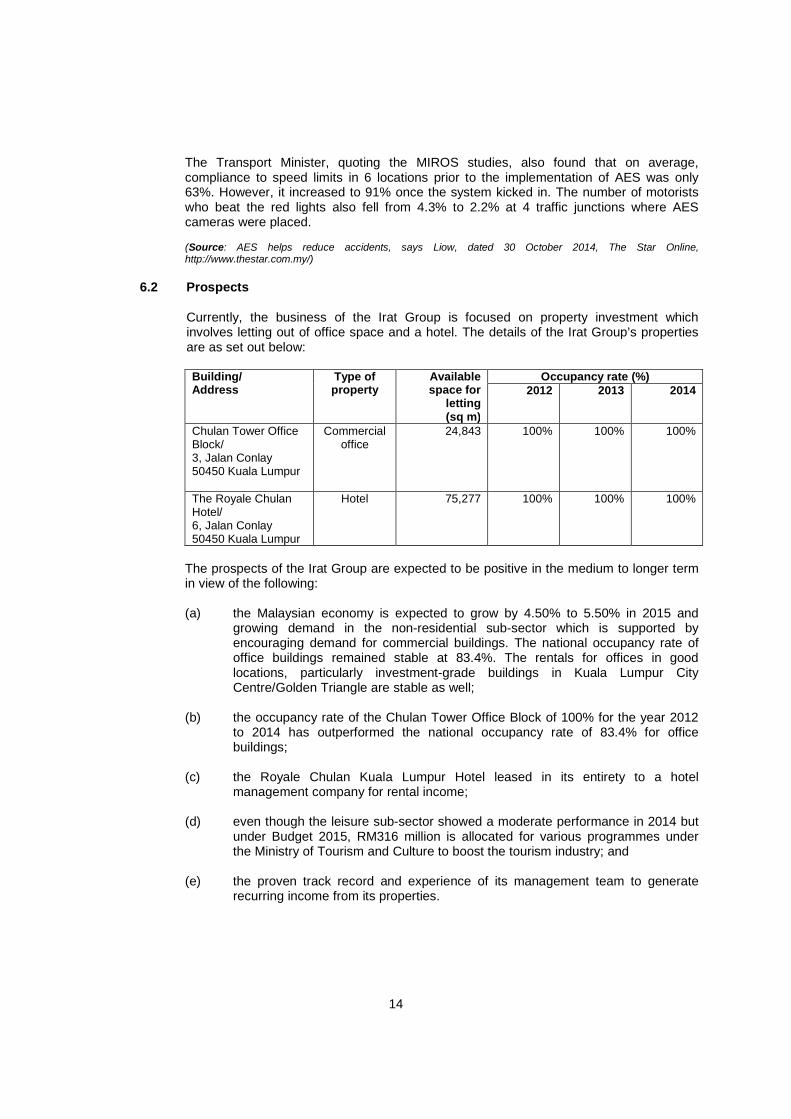

14

The Transport Minister, quoting the MIROS studies, also found that on average,compliance to speed limits in 6 locations prior to the implementation of AES was only63%. However, it increased to 91% once the system kicked in. The number of motoristswho beat the red lights also fell from 4.3% to 2.2% at 4 traffic junctions where AEScameras were placed.

(Source: AES helps reduce accidents, says Liow, dated 30 October 2014, The Star Online,http://www.thestar.com.my/)

6.2 Prospects

Currently, the business of the Irat Group is focused on property investment whichinvolves letting out of office space and a hotel. The details of the Irat Group’s propertiesare as set out below:

Building/Address

Type ofproperty

Availablespace for

letting(sq m)

Occupancy rate (%)2012 2013 2014

Chulan Tower OfficeBlock/3, Jalan Conlay50450 Kuala Lumpur

Commercialoffice

24,843 100% 100% 100%

The Royale ChulanHotel/6, Jalan Conlay50450 Kuala Lumpur

Hotel 75,277 100% 100% 100%

The prospects of the Irat Group are expected to be positive in the medium to longer termin view of the following:

(a) the Malaysian economy is expected to grow by 4.50% to 5.50% in 2015 andgrowing demand in the non-residential sub-sector which is supported byencouraging demand for commercial buildings. The national occupancy rate ofoffice buildings remained stable at 83.4%. The rentals for offices in goodlocations, particularly investment-grade buildings in Kuala Lumpur CityCentre/Golden Triangle are stable as well;

(b) the occupancy rate of the Chulan Tower Office Block of 100% for the year 2012to 2014 has outperformed the national occupancy rate of 83.4% for officebuildings;

(c) the Royale Chulan Kuala Lumpur Hotel leased in its entirety to a hotelmanagement company for rental income;

(d) even though the leisure sub-sector showed a moderate performance in 2014 butunder Budget 2015, RM316 million is allocated for various programmes underthe Ministry of Tourism and Culture to boost the tourism industry; and

(e) the proven track record and experience of its management team to generaterecurring income from its properties.

15

As such, taking into consideration the successes of the Irat Group in property investment,its proven track record and the experience of the existing management, positiveprospects of the property sector, and government incentive in hospitality and tourismsector as set out in Section 6.1 of this announcement, the management of the BHBGroup is optimistic of the sustainability and growth of the financial performance of the IratGroup in the property segment moving forward.

In addition to the existing business of the Irat Group, the Irat Group will potentially ventureinto the operation of the AES project following the completion of the SPAs. The full roll-out of the AES operations are expected to provide another source of revenue to the IratGroup which in turn will contribute to the financial result of BHB in the longer term aftertaking into account the following:

(a) Malaysia is among the top 25 most dangerous countries for road users, with 30fatalities per 100,000 individuals;

(b) MAA has forecasted a TIV of 680,000 for the year 2015 vis-à-vis 666,465 actualTIV for the year 2014; and

(c) the determination of the Government enforcement body to change the attitude ofMalaysian drivers to reduce the fatality rate on the road through theimplementation of the AES.

7. EFFECTS OF THE PROPOSED SUBSCRIPTION

7.1 Issued and paid-up share capital and substantial shareholders’ shareholdings

The subscription will not have any effect on the issued and paid-up share capital and thesubstantial shareholders’ shareholdings in BHB as the Proposed Subscription will notinvolve any issuance of new ordinary share of RM0.50 each in BHB (“Share” or “BHBShare”).

(The rest of this page is intentionally left blank)

16

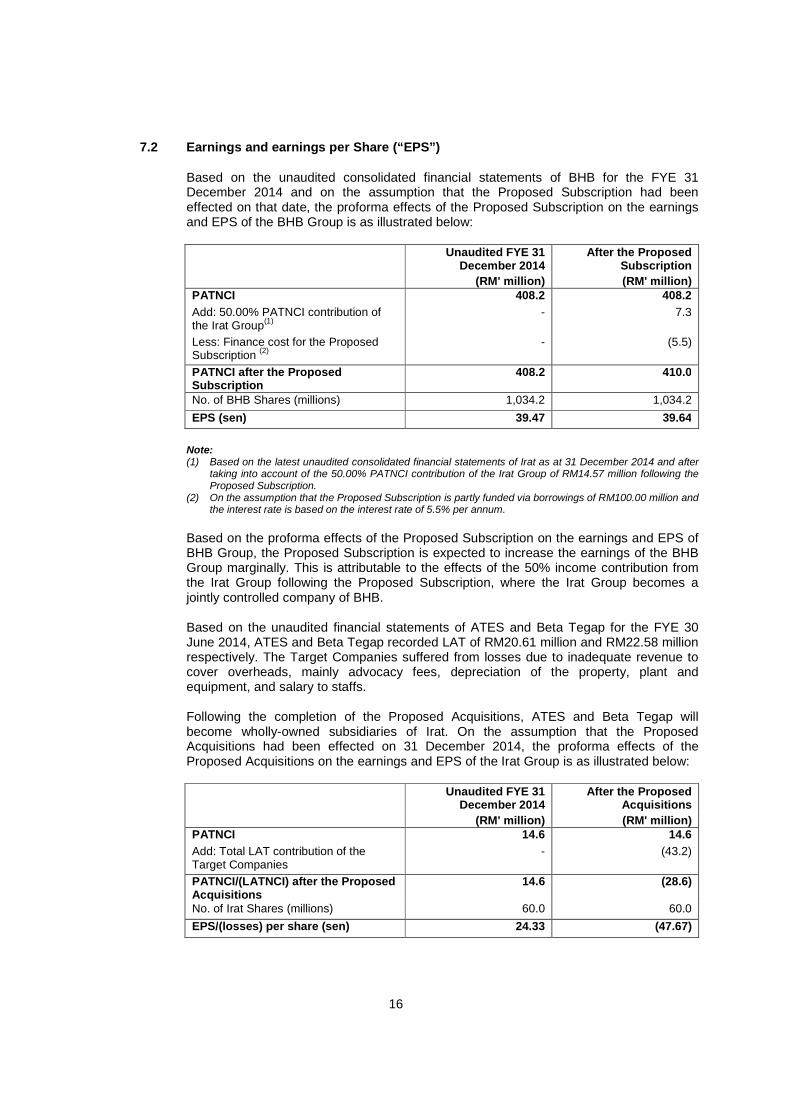

7.2 Earnings and earnings per Share (“EPS”)

Based on the unaudited consolidated financial statements of BHB for the FYE 31December 2014 and on the assumption that the Proposed Subscription had beeneffected on that date, the proforma effects of the Proposed Subscription on the earningsand EPS of the BHB Group is as illustrated below:

Unaudited FYE 31December 2014

After the ProposedSubscription

(RM' million) (RM' million)PATNCI 408.2 408.2

Add: 50.00% PATNCI contribution ofthe Irat Group

(1)- 7.3

Less: Finance cost for the ProposedSubscription

(2)- (5.5)

PATNCI after the ProposedSubscription

408.2 410.0

No. of BHB Shares (millions) 1,034.2 1,034.2

EPS (sen) 39.47 39.64

Note:(1) Based on the latest unaudited consolidated financial statements of Irat as at 31 December 2014 and after

taking into account of the 50.00% PATNCI contribution of the Irat Group of RM14.57 million following theProposed Subscription.

(2) On the assumption that the Proposed Subscription is partly funded via borrowings of RM100.00 million andthe interest rate is based on the interest rate of 5.5% per annum.

Based on the proforma effects of the Proposed Subscription on the earnings and EPS ofBHB Group, the Proposed Subscription is expected to increase the earnings of the BHBGroup marginally. This is attributable to the effects of the 50% income contribution fromthe Irat Group following the Proposed Subscription, where the Irat Group becomes ajointly controlled company of BHB.

Based on the unaudited financial statements of ATES and Beta Tegap for the FYE 30June 2014, ATES and Beta Tegap recorded LAT of RM20.61 million and RM22.58 millionrespectively. The Target Companies suffered from losses due to inadequate revenue tocover overheads, mainly advocacy fees, depreciation of the property, plant andequipment, and salary to staffs.

Following the completion of the Proposed Acquisitions, ATES and Beta Tegap willbecome wholly-owned subsidiaries of Irat. On the assumption that the ProposedAcquisitions had been effected on 31 December 2014, the proforma effects of theProposed Acquisitions on the earnings and EPS of the Irat Group is as illustrated below:

Unaudited FYE 31December 2014

After the ProposedAcquisitions

(RM' million) (RM' million)PATNCI 14.6 14.6

Add: Total LAT contribution of theTarget Companies

- (43.2)

PATNCI/(LATNCI) after the ProposedAcquisitions

14.6 (28.6)

No. of Irat Shares (millions) 60.0 60.0

EPS/(losses) per share (sen) 24.33 (47.67)

17

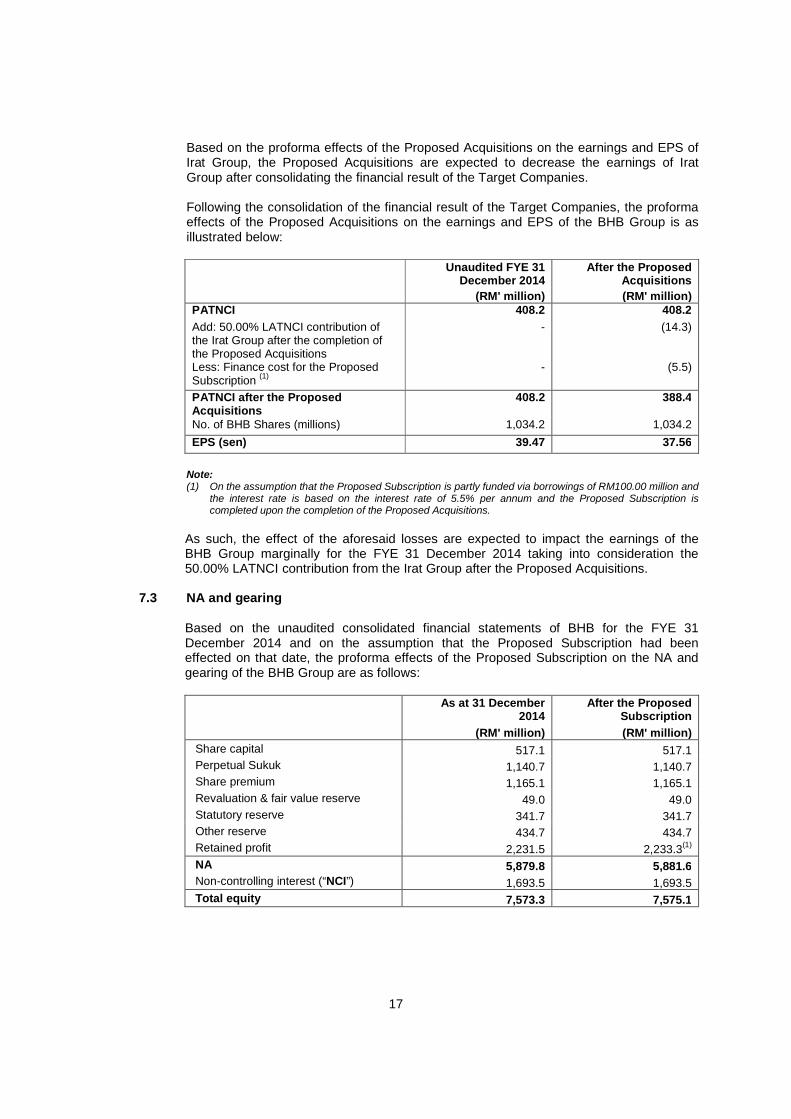

Based on the proforma effects of the Proposed Acquisitions on the earnings and EPS ofIrat Group, the Proposed Acquisitions are expected to decrease the earnings of IratGroup after consolidating the financial result of the Target Companies.

Following the consolidation of the financial result of the Target Companies, the proformaeffects of the Proposed Acquisitions on the earnings and EPS of the BHB Group is asillustrated below:

Unaudited FYE 31December 2014

After the ProposedAcquisitions

(RM' million) (RM' million)PATNCI 408.2 408.2

Add: 50.00% LATNCI contribution ofthe Irat Group after the completion ofthe Proposed Acquisitions

- (14.3)

Less: Finance cost for the ProposedSubscription

(1)- (5.5)

PATNCI after the ProposedAcquisitions

408.2 388.4

No. of BHB Shares (millions) 1,034.2 1,034.2

EPS (sen) 39.47 37.56

Note:(1) On the assumption that the Proposed Subscription is partly funded via borrowings of RM100.00 million and

the interest rate is based on the interest rate of 5.5% per annum and the Proposed Subscription iscompleted upon the completion of the Proposed Acquisitions.

As such, the effect of the aforesaid losses are expected to impact the earnings of theBHB Group marginally for the FYE 31 December 2014 taking into consideration the50.00% LATNCI contribution from the Irat Group after the Proposed Acquisitions.

7.3 NA and gearing

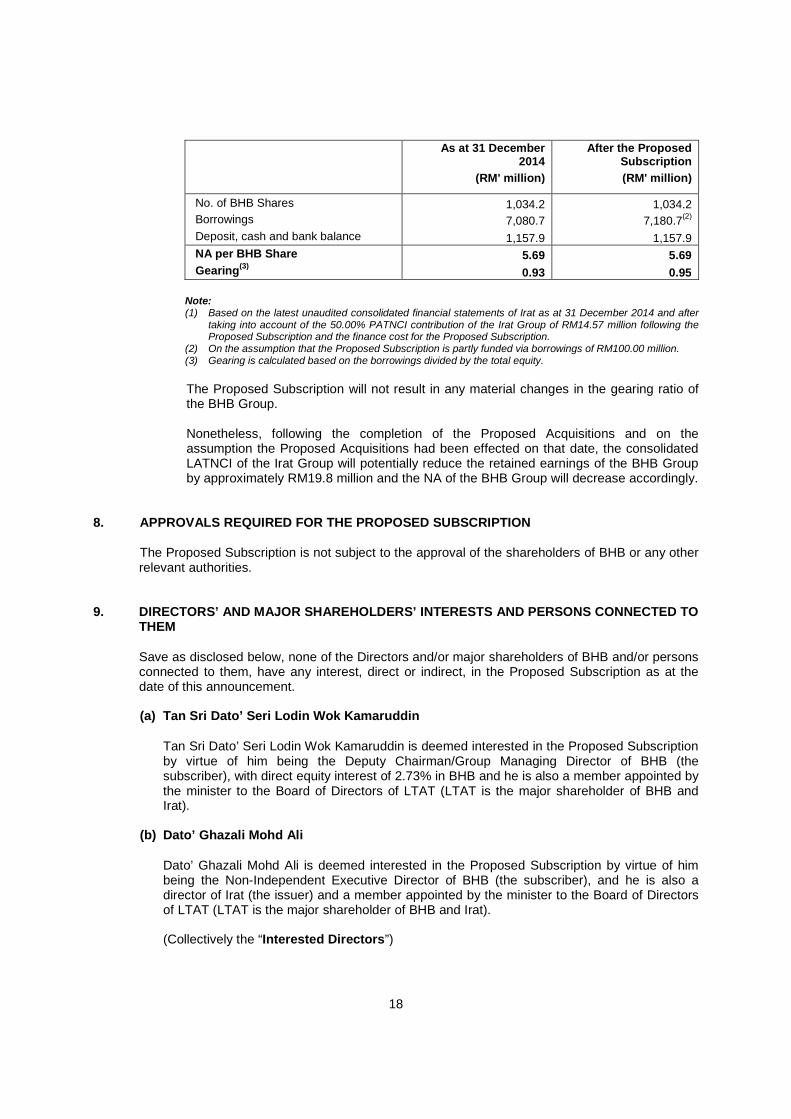

Based on the unaudited consolidated financial statements of BHB for the FYE 31December 2014 and on the assumption that the Proposed Subscription had beeneffected on that date, the proforma effects of the Proposed Subscription on the NA andgearing of the BHB Group are as follows:

As at 31 December2014

After the ProposedSubscription

(RM' million) (RM' million)

Share capital 517.1 517.1

Perpetual Sukuk 1,140.7 1,140.7

Share premium 1,165.1 1,165.1

Revaluation & fair value reserve 49.0 49.0

Statutory reserve 341.7 341.7

Other reserve 434.7 434.7

Retained profit 2,231.5 2,233.3(1)

NA 5,879.8 5,881.6

Non-controlling interest (“NCI”) 1,693.5 1,693.5

Total equity 7,573.3 7,575.1

18

As at 31 December2014

After the ProposedSubscription

(RM' million) (RM' million)

No. of BHB Shares 1,034.2 1,034.2

Borrowings 7,080.7 7,180.7(2)

Deposit, cash and bank balance 1,157.9 1,157.9

NA per BHB Share 5.69 5.69

Gearing(3)

0.93 0.95

Note:(1) Based on the latest unaudited consolidated financial statements of Irat as at 31 December 2014 and after

taking into account of the 50.00% PATNCI contribution of the Irat Group of RM14.57 million following theProposed Subscription and the finance cost for the Proposed Subscription.

(2) On the assumption that the Proposed Subscription is partly funded via borrowings of RM100.00 million.(3) Gearing is calculated based on the borrowings divided by the total equity.

The Proposed Subscription will not result in any material changes in the gearing ratio ofthe BHB Group.

Nonetheless, following the completion of the Proposed Acquisitions and on theassumption the Proposed Acquisitions had been effected on that date, the consolidatedLATNCI of the Irat Group will potentially reduce the retained earnings of the BHB Groupby approximately RM19.8 million and the NA of the BHB Group will decrease accordingly.

8. APPROVALS REQUIRED FOR THE PROPOSED SUBSCRIPTION

The Proposed Subscription is not subject to the approval of the shareholders of BHB or any otherrelevant authorities.

9. DIRECTORS’ AND MAJOR SHAREHOLDERS’ INTERESTS AND PERSONS CONNECTED TOTHEM

Save as disclosed below, none of the Directors and/or major shareholders of BHB and/or personsconnected to them, have any interest, direct or indirect, in the Proposed Subscription as at thedate of this announcement.

(a) Tan Sri Dato’ Seri Lodin Wok Kamaruddin

Tan Sri Dato’ Seri Lodin Wok Kamaruddin is deemed interested in the Proposed Subscriptionby virtue of him being the Deputy Chairman/Group Managing Director of BHB (thesubscriber), with direct equity interest of 2.73% in BHB and he is also a member appointed bythe minister to the Board of Directors of LTAT (LTAT is the major shareholder of BHB andIrat).

(b) Dato’ Ghazali Mohd Ali

Dato’ Ghazali Mohd Ali is deemed interested in the Proposed Subscription by virtue of himbeing the Non-Independent Executive Director of BHB (the subscriber), and he is also adirector of Irat (the issuer) and a member appointed by the minister to the Board of Directorsof LTAT (LTAT is the major shareholder of BHB and Irat).

(Collectively the “Interested Directors”)

19

(c) LTAT (“Major Shareholder”)

LTAT is deemed interested in the Proposed Subscription by virtue of it being the majorshareholder of BHB (the subscriber) with equity interest of 58.89% equity interest in BHB andthe major shareholder of Irat (the issuer) with equity interest of 98.33% equity interest in Irat.

In this regard, the Interested Directors have abstained and will continue to abstain from alldeliberations and voting on the resolution pertaining to the Proposed Subscription at the relevantboard meetings.

10. STATEMENT BY THE DIRECTORS

The Board (save for the Interested Directors), after having considered all aspects of the ProposedSubscription, is of the opinion that the Proposed Subscription is in the best interest of theCompany.

11. AUDIT COMMITTEE’S STATEMENT

The audit committee of the Company, after having considered all aspects of the ProposedSubscription including but not limited to the rationale and effects of the Proposed Subscriptionand the prospects of the Irat Group as set out in Section 6.2 of this announcement, is of theopinion that the Proposed Subscription is in the best interest of the Company, fair, reasonableand on normal commercial terms, and is not detrimental to the interest of the non-interestedshareholders of BHB.

12. HIGHEST PERCENTAGE RATIO APPLICABLE

Based on BHB’s unaudited consolidated financial statements for the FYE 31 December 2014, thehighest percentage ratio pursuant to paragraph 10.02(g) of the Main Market of the ListingRequirements of Bursa Malaysia Securities Berhad resulting from the Proposed Subscription is2.17%.

13. TRANSACTION WITH THE SAME RELATED PARTY FOR THE PRECEDING 12 MONTHS

As at the date of this announcement, there is no transaction entered into by BHB with Irat for thepreceding 12 months.

14. ESTIMATED TIME FRAME FOR COMPLETION OF THE PROPOSED SUBSCRIPTION

Barring any unforeseen circumstances, the Proposed Subscription is expected to be completedby the 2

ndquarter of 2015.

This announcement is dated 6 March 2015.

APPENDIX IINFORMATION ON IRAT

20

1. HISTORY AND BUSINESS OVERVIEW

Irat was incorporated in Malaysia under the Act as a private limited company on 15 April 1996.

The principal activity of Irat is investment holding whilst the subsidiary is principally involved inproperty investment. The business description of the Irat Group is set out in Section 5 of thisappendix.

On 27 February 2015, Irat entered into the 2 SPAs for the Proposed Acquisitions.

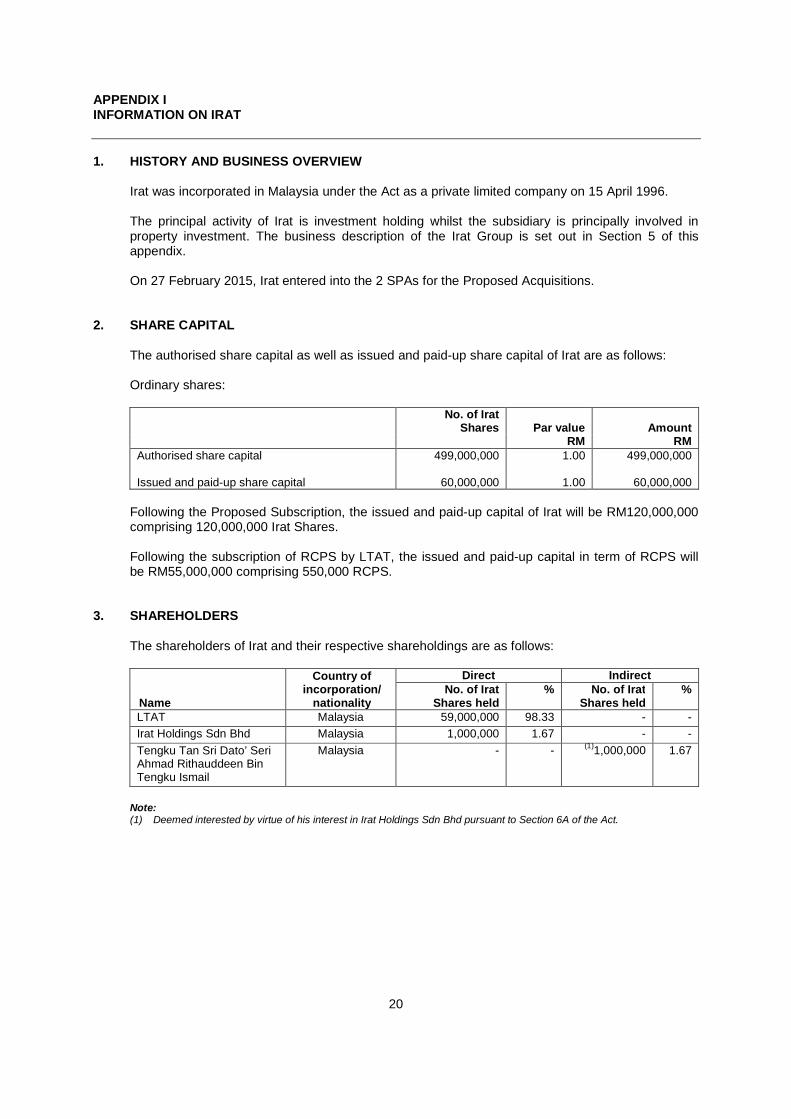

2. SHARE CAPITAL

The authorised share capital as well as issued and paid-up share capital of Irat are as follows:

Ordinary shares:

No. of IratShares Par value Amount

RM RMAuthorised share capital 499,000,000 1.00 499,000,000

Issued and paid-up share capital 60,000,000 1.00 60,000,000

Following the Proposed Subscription, the issued and paid-up capital of Irat will be RM120,000,000comprising 120,000,000 Irat Shares.

Following the subscription of RCPS by LTAT, the issued and paid-up capital in term of RCPS willbe RM55,000,000 comprising 550,000 RCPS.

3. SHAREHOLDERS

The shareholders of Irat and their respective shareholdings are as follows:

Name

Country ofincorporation/

nationality

Direct IndirectNo. of Irat

Shares held% No. of Irat

Shares held%

LTAT Malaysia 59,000,000 98.33 - -

Irat Holdings Sdn Bhd Malaysia 1,000,000 1.67 - -

Tengku Tan Sri Dato’ SeriAhmad Rithauddeen BinTengku Ismail

Malaysia - -(1)

1,000,000 1.67

Note:(1) Deemed interested by virtue of his interest in Irat Holdings Sdn Bhd pursuant to Section 6A of the Act.

APPENDIX IINFORMATION ON IRAT

21

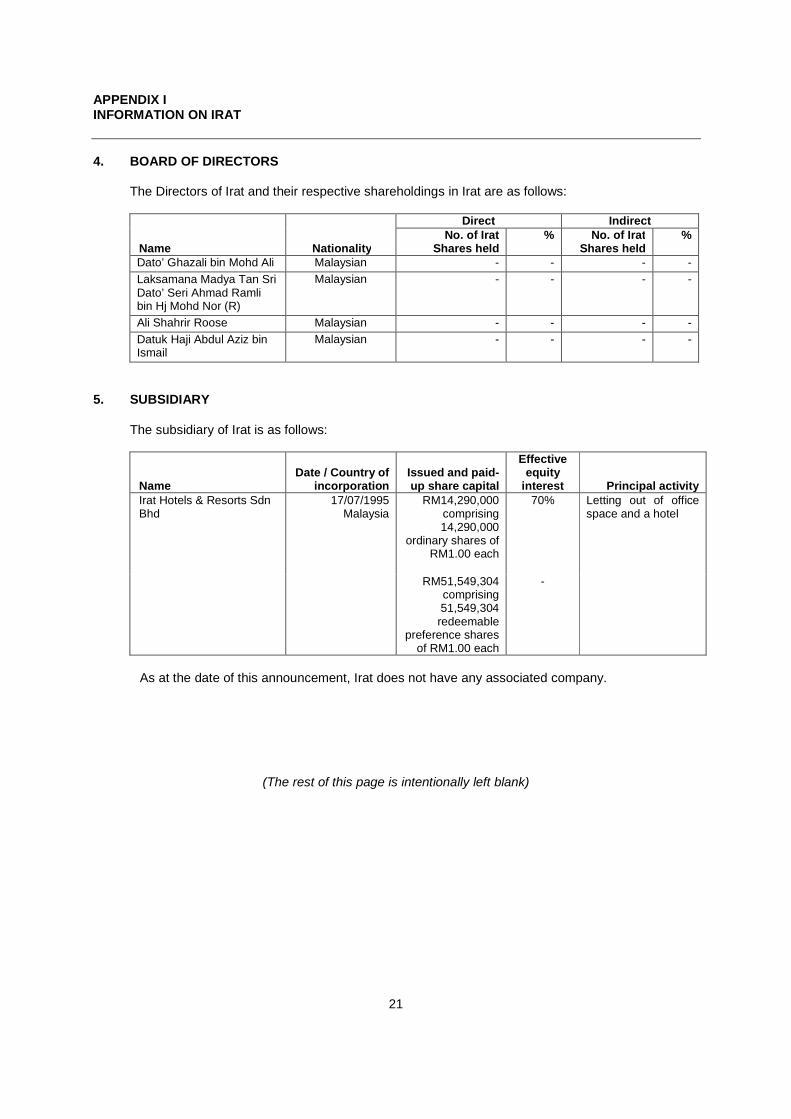

4. BOARD OF DIRECTORS

The Directors of Irat and their respective shareholdings in Irat are as follows:

Name Nationality

Direct IndirectNo. of Irat

Shares held% No. of Irat

Shares held%

Dato’ Ghazali bin Mohd Ali Malaysian - - - -

Laksamana Madya Tan SriDato’ Seri Ahmad Ramlibin Hj Mohd Nor (R)

Malaysian - - - -

Ali Shahrir Roose Malaysian - - - -

Datuk Haji Abdul Aziz binIsmail

Malaysian - - - -

5. SUBSIDIARY

The subsidiary of Irat is as follows:

NameDate / Country of

incorporationIssued and paid-up share capital

Effectiveequity

interest Principal activityIrat Hotels & Resorts SdnBhd

17/07/1995Malaysia

RM14,290,000comprising14,290,000

ordinary shares ofRM1.00 each

70% Letting out of officespace and a hotel

RM51,549,304comprising51,549,304redeemable

preference sharesof RM1.00 each

-

As at the date of this announcement, Irat does not have any associated company.

(The rest of this page is intentionally left blank)

APPENDIX IINFORMATION ON IRAT

22

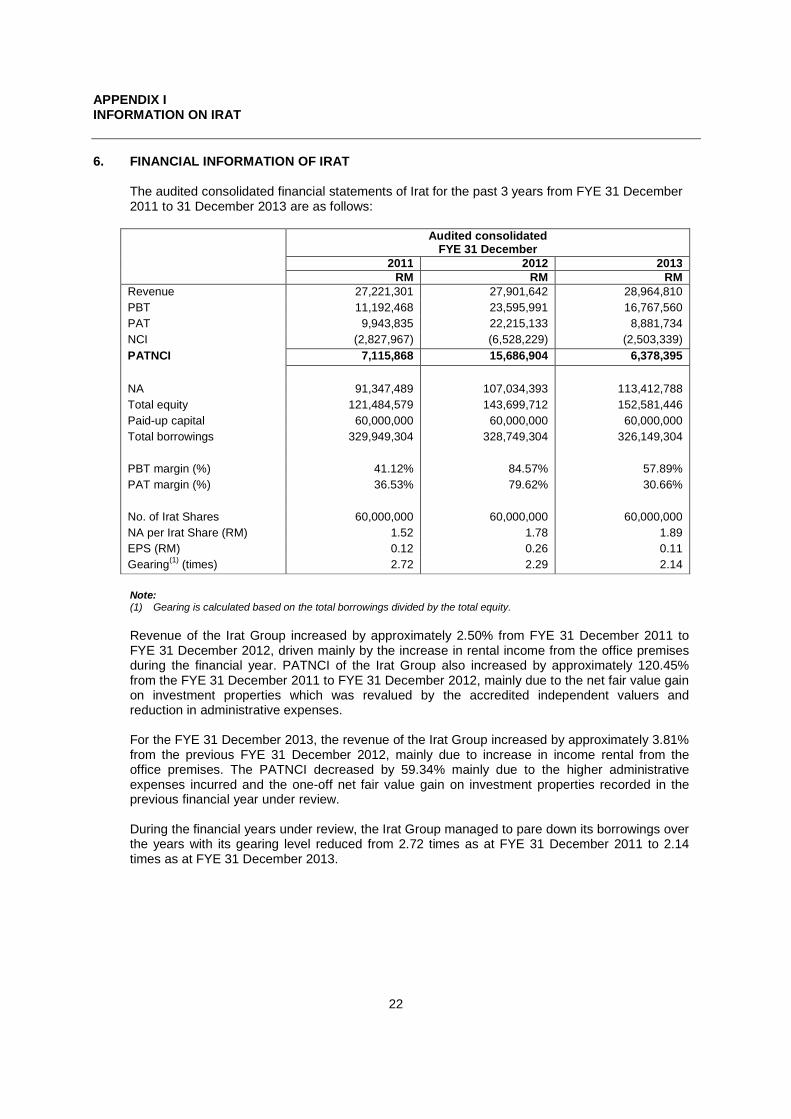

6. FINANCIAL INFORMATION OF IRAT

The audited consolidated financial statements of Irat for the past 3 years from FYE 31 December2011 to 31 December 2013 are as follows:

Audited consolidatedFYE 31 December

2011 2012 2013RM RM RM

Revenue 27,221,301 27,901,642 28,964,810

PBT 11,192,468 23,595,991 16,767,560

PAT 9,943,835 22,215,133 8,881,734

NCI (2,827,967) (6,528,229) (2,503,339)

PATNCI 7,115,868 15,686,904 6,378,395

NA 91,347,489 107,034,393 113,412,788

Total equity 121,484,579 143,699,712 152,581,446

Paid-up capital 60,000,000 60,000,000 60,000,000

Total borrowings 329,949,304 328,749,304 326,149,304

PBT margin (%) 41.12% 84.57% 57.89%

PAT margin (%) 36.53% 79.62% 30.66%

No. of Irat Shares 60,000,000 60,000,000 60,000,000

NA per Irat Share (RM) 1.52 1.78 1.89

EPS (RM) 0.12 0.26 0.11

Gearing(1)

(times) 2.72 2.29 2.14

Note:(1) Gearing is calculated based on the total borrowings divided by the total equity.

Revenue of the Irat Group increased by approximately 2.50% from FYE 31 December 2011 toFYE 31 December 2012, driven mainly by the increase in rental income from the office premisesduring the financial year. PATNCI of the Irat Group also increased by approximately 120.45%from the FYE 31 December 2011 to FYE 31 December 2012, mainly due to the net fair value gainon investment properties which was revalued by the accredited independent valuers andreduction in administrative expenses.

For the FYE 31 December 2013, the revenue of the Irat Group increased by approximately 3.81%from the previous FYE 31 December 2012, mainly due to increase in income rental from theoffice premises. The PATNCI decreased by 59.34% mainly due to the higher administrativeexpenses incurred and the one-off net fair value gain on investment properties recorded in theprevious financial year under review.

During the financial years under review, the Irat Group managed to pare down its borrowings overthe years with its gearing level reduced from 2.72 times as at FYE 31 December 2011 to 2.14times as at FYE 31 December 2013.