Embed Size (px)

DESCRIPTION

credit npa

Citation preview

PREFACE

Banking business is directly dependent on economic conditions in the country. Due to liberalization, our economy is not insulated. It will have impact of economic conditions of other countries also. This we have witnessed lower rate of GDP and IIP. This has adversely affected the growth in Banking Industry on the one hand and poses a threat of mounting NPA on the other hand. In view of this Credit Monitoring has gained more importance. Credit Monitoring starts from the date bank parts with the funds.

One of the Pillars of our Business Policy Guidelines is continuous improvement in assets quality. In spite of best efforts, if we could not saved account from downgrading, then immediate steps need to be taken for recovery/up gradation of the account. The book contains guidelines on Compromise, DRT, SARFAESI Act etc.

An attempt has been made to give the field level functionaries a concise notes on various aspects of credit monitoring and NPA Management.

I have a pleasure to place this book for all Barodians.

I trust this book will be useful to the credit officers/branch for day to day work. However this cannot be a substitute of our Book of Instructions, circulars & various policies. If you have any suggestions to improve the quality of this book, please send it by e mail on [email protected].

Date:31.03.13 ( Kamlesh Patel)Place: Ahmedabad DGM & Principal I/C

Baroda Academy Inventing Methods for Igniting Minds

1

INDEX

Sr No

Name of the Topic Page No

SECTION I CREDIT MONITORING1.. Credit Monitoring :Prevention is better than cure2 Early Warning Signals And Follow Up 53 Tools for Credit Monitoring 114 Reserve Bank Of India Guidelines For Restructuring 265 Restructuring Of Advance Accounts 356 SME Debt Restructuring 517 CDR 718 BIFR 78

SECTION II NPA MANAGEMENT9 NPA Management : Need of Hour 8910 Guiding Principles of Domestic Recovery Policy 2012 9011 Causes And Consequences Of Non-Performing Assets 9712 IARC Norms 10313 Recovery – Non Legal Measures 12014 Recovery – Legal Measures 13615 Policy for Recovery in Fraud Accounts 15816 Summary 161

Baroda Academy Inventing Methods for Igniting Minds

2

SECTION I - CREDIT MONITORING

`Credit Monitoring- Prevention is better than cure’

Credit Monitoring is an important part of Credit Management. Banking means accepting the deposits from the public for the purpose of lending. It is obligatory for Banks to make payment of these deposits on demand or after expiry of the contractual period. For making timely payment to depositors, we need fund i.e. timely return of money lent. The equilibrium will be maintained only if the money lent by the bank is also returned back well in time.

As we know that lending of money has its own risk,Thus Banks should be very cautious at the time of lending and should continue to follow up till the total money is repaid by the borrower. Credit Monitoring has become unevitable for safeguarding the bank`s interest. Credit monitoring starts the moment bank parts with the fund and continues till the liquidation of account in toto. But in real sense Credit monitoring starts the moment bank identifies the borrower.Good begin half done.

In credit decision, appraisal of the borrower is very important and if selection of borrower is done properly at the beginning; then the monitoring part will also be easy.

If we carefully track small-small, significant changes in the financial situations of the borrower or turnover in the account or we just watch the activity at the time of first default, it may ease to curb the situation and can be handled. But for this Banker is supposed to remain in touch with the borrower and need to pay full attention on monitoring.

Now a days where entire banking industry is facing the problem of rising NPAs and the problem of non-performing assets has shaken the entire Indian banking sector, the monitoring part can play a vital role in prevention of slippage and taking corrective measures in the beginning of problem.

For better credit monitoring, we are to keep our eyes and ears open and follow the different guidelines of the bank.It is easy to find out any adverse features in its beginning and may take corrective measure at once.

There is a need to strengthen the credit monitoring process at the branch level. Proper credit monitoring should be emphasized. There should be proper flow of information from the units regarding their financial area, annual accounts, stock reports etc., which would enable the banker to know the need based credit requirement of borrower and warning signals for taking quick remedial action.

If credit officer of the branch can keep a watch on the following points, credit portfolio of the branch may remain almost healthy.

Turnover in the account Timely repayment of interest and installments Timely submission of Stock Statements, QMR, information demanded by Bank,

Audited financials, Papers for Renewal Inspection of the unit on regular intervals

Baroda Academy Inventing Methods for Igniting Minds

3

Regular conversation with the borrower provides timely help to the borrower in genuine cases within the policy guidelines of the bank.

Timely Review of the facility Compliance of terms and conditions Comparison of performance with projections Transaction in the account Analysis of the performance of the unit with Industry trend

In the following chapters we have tried to discuss various monitoring tools which will be useful for better Credit Management.

Baroda Academy Inventing Methods for Igniting Minds

4

EARLY WARNING SIGNALS AND FOLLOW UP

Quick Bites

The early warning signals The incipient sickness Special mention accounts The follow up of advance accounts Definition of willful Defaulter Guidelines on financing of willful defaulter

Early Warning Signals

Reserve Bank of India has issued broad guidelines on preventing Slippage to NPAs by recognizing the problems early and corrective measures to restructure the accounts after an objective assessment of the viability of the unit and promoter's intention (and his stake). Bank shall put in place 'Early Alert System' that captures early warning signals in respect of accounts showing first signs of weakness. The following features may be treated as early warning signals. Appropriate Credit Monitoring System has been in places at BCC and at Zonal level/ Regional level in order to take care of the above.

Continuous irregularities in cash credit/ overdraft accounts such as inability to maintain stipulated margin on continuous basis or drawings frequently exceeding sanctioned limits, periodical interest debited remaining unrealized.

Outstanding balance in cash credit account remaining continuously at the maximum without appropriate turnover.

Failure to make timely payment of installments of principal and / or interest on term loans

Complaints from suppliers of raw materials, water, power etc about non payment of bills

Non submission or undue delay in submission or submission of incorrect stock statements & other control returns and statements.

Attempts to divert sale proceeds through accounts with other banks Downward trends in credit summations Frequent return of cheques or bills Steep decline in production figures Downwards trends in sales and fall in profits Rising level of inventories, which may include large proportion of slow or non moving

items

Baroda Academy Inventing Methods for Igniting Minds

5

Larger & longer outstanding in bills accounts Longer period of credit allowed on sale Failure to pay statutory liabilities Utilization of funds for purposes other than running the units Not furnishing required information/ data on operations in time Unreasonable variations in sales/ receivables Devolvement of DPG installments and non-payment within a reasonable period. Frequent devolvement of LCs and non-payment within a reasonable period Frequent invocation of BGs and non-payment within a reasonable period Non-payment of bills discounted or under collection. Poor financial performance in terms of declining sales and profits, cash losses, net losses and erosion of net worth etc. Incomplete documentation in terms of creation/registration of charge/Mortgage etc. Non-compliance of terms and conditions of sanction.

Incipient Sickness

Sickness in a unit at its initial stage is called Incipient Sickness. No unit becomes sick suddenly except due to natural calamities like flood, riots or fire or change in government policies and bad intentions. Generally sickness erupts in the unit slowly and such units generally throw signals. These signals may be of financial or non-financial in nature. Some of the signals are as under:

Continuous Irregularity in cash credit account. Low capacity utilization. Profit fluctuations, downward trend in sales and stagnation or fall in profits followed

by contraction of the share of the market. Higher rate of rejection of goods manufactured. Reduction in turnover. Whenever the borrower is in financial difficulty, he may open a

separate account with another bank and deposits all collections therein. Failure to pay statutory liabilities Larger and longer outstanding in the bill accounts Longer period of credit allowed on sale documents negotiated through the bank and

frequent returns by customer of the same Continuous utilization of cash credit facilities to the hilt and failure to pay timely

installment of principal and/ or interest on term loan. Non-submission of periodical financial data/ stock statement, etc. in time. Financing capital expenditure out of funds provided for working capital purposes Decrease in working capital. A general decline in that particular industry. Rapid turnover of key personnel. Existence of a large number of law suits against the borrower. Rapid expansion and too much diversification within a short time. Diversion/Siphoning of funds. Any major change in the share holdings. Frequent requests for 'Stop payment' of cheques. Non compliance of irregularities pointed out in Inspection, Audit Reports.

Baroda Academy Inventing Methods for Igniting Minds

6

Special Mention Accounts

For early recognition of slippage and timely interventions, it is suggested that banks introduce a new asset category between ‘Standard’ and ‘Sub-standard’ for their own internal monitoring and follow up. This asset category may be in line with international practice of ‘Special Mention Assets’ used by U.S.A., Singapore, etc.

2. An asset may be transferred to this category once the earliest signs of sickness/ irregularities are identified. This will help banks to look at account with potential problems in a focused manner right from the onset of the problem, so that monitoring and remedial actions can be more effective.

3. Once these accounts are categorized and reported as such, proper top management attention would also be ensured.

4. Introduction of a ‘Special Mention’ category of assets would be on the basis of not only overdue position in the account but also other factors, which reflect sickness/irregularities in the account.

The following types of accounts in standard category shall be brought under special mention a/cs:

i. Irregularity in the account for 30 days.ii. Non-compliance of terms & conditions for 30 days (unless the Sanctioning authority has given extended time period for compliance ) iii. No turnover in Working Capital account for 30 days.

Follow up of Advance Accounts

As the health of the advance truly lies on proper follow-up, it is obligatory on the part of the authorities concerned to exercise sufficient care to monitor the account. Branch should keep close watch on account like routing of turnover, diversion of funds, proper utilization of funds, frequent excesses and stock inspection remarks etc. Such controls would provide advance information for taking appropriate decision in order to avoid slippage of the account. Some of the major post sanction follow-up systems devised by the bank are:

Submission of Control Returns by the borrower viz., Stock Statements, Quarterly Information System/ Returns etc., and scrutiny of the same, periodical Inspection of Securities, ensuring end use of funds.

The follow up of advances is a sum of all activities starting from the date of disbursement to the date of recovery of last installment/amount.

The important objectives of follow-up of credit facilities are:

1. To ensure proper end use of funds. Funds should be used for the purpose, for which these are given. It should not be used for any other purpose.

Baroda Academy Inventing Methods for Igniting Minds

7

2. To ensure that the operations of the borrower are on expected lines both physically and financially.

3. To test the assumptions of lending. Advance is granted on the basis of projections. All projections depend on a bundle of assumptions. Many of such assumptions can and do go wrong. Actual working only shows whether the assumptions have proved correct or not. Most important are capacity utilisation, costs incurred, price level, market conditions etc.

4. To ensure that the terms and conditions of sanction are satisfied. While sanctioning an advance, bank stipulates certain conditions to be satisfied, such as restrictions on declaration of dividend, expansion in capacity, or acquisition of fixed assets, repayment of private borrowings etc.

5. To ensure that the securities offered/charged are and continue to be in order. Physical existence, valuation, quality turnover etc. are important.

6. To detect whether any danger signals are developing indicating sickness. Many a time, warning signals are thrown up indicating the existence/emergence of a problem situation. Proper follow-up action only can take care of such situation.

7. To see whether there is any change in management structure, reconstitution, death or resignation of a key person leading to the possible failure of the firm.

8. To examine whether there is any change in the environment affecting the unit, like Government Policies, Economic situations, crop failures etc.

9. To evaluate the operations of the borrower in a constructive way and to advise/devise measures for correction/ improvement etc. This will require a total study of the operations, results and trends of the borrower.

10. To formulate future programme/lines of action in the light of the operational results or records.

11. To anticipate problems and reorient plans of action in order to contain such problems effectively. This requires the banker to take a futuristic view of things and advise the borrower suitably.

Wilful Defaulter

Based on recommendations of working group on willful defaulter RBI has w.e.f. Mar 2002 instructed as under:

A Wilful defaulter is one who has adequate resources / cash flows / net worth to pay the dues, but deliberately does not pay, or siphons funds to the detriment of the unit, misrepresents / falsifies the records or conducts fraudulent transactions.

A willful default would be deemed to have occurred if any of the following is noted:

The unit has defaulted in meeting its payment/repayment obligations to the lender even when it has the capacity to honor the said obligations.

The unit has defaulted in meeting its payment /repayment obligations to the lender and has not utilized the finance from the lender for the specific purpose for which finance was availed of but has diverted the funds for other purposes.

Baroda Academy Inventing Methods for Igniting Minds

8

The unit has defaulted in meeting its payment /repayment obligations to the lender and has siphoned off the funds such that funds are not utilized for the specific purpose for which finance was availed of nor are the funds available with the unit in the form of other assets.

The unit has defaulted in meeting its payment /repayment obligations to the lender and has disposed off / removed the assets without the knowledge of the bank.

Further, default in honoring the settlement by the party to be treated as willful default

as per the recent judgment by Delhi High court dated 29.11.05.

As per RBI guidelines, every bank is required to submit a list of suit filed accounts of willful defaulters with outstanding (FB+NFB) of Rs.25 lacs and above, at the end of every quarter (March, June, September and December) to CIBIL or any other RBI registered credit information company and a list of non suit filed accounts of willful defaulters to only RBI.

Guidelines on financing of willful defaulter:

In order to prevent the access to the capital markets by the willful defaulters, a copy ot the list of willful defaulters (non-suit filed accounts) and list of willful defaulters (suit filed accounts) are forwarded to SEBI by RBI and CIBIL respectively.

No additional facilities should be granted by any bank / FI to the listed willful defaulters. In addition, the entrepreneurs / promoters of companies where banks / FIs have identified siphoning / diversion of funds, misrepresentation, falsification of accounts and fraudulent transactions should be debarred from institutional finance from the scheduled commercial banks, Development Financial Institutions, Government owned NBFCs, investment institutions etc. for floating new ventures for a period of 5 years from the date the name of the willful defaulter is published in the list of willful defaulters by the RBI.

Units becoming sick on account of, willful default, unauthorised diversion of funds, should not be considered for rehabilitation and steps should be taken for recovery of bank dues.

Baroda Academy Inventing Methods for Igniting Minds

9

Baroda Academy Inventing Methods for Igniting Minds

10

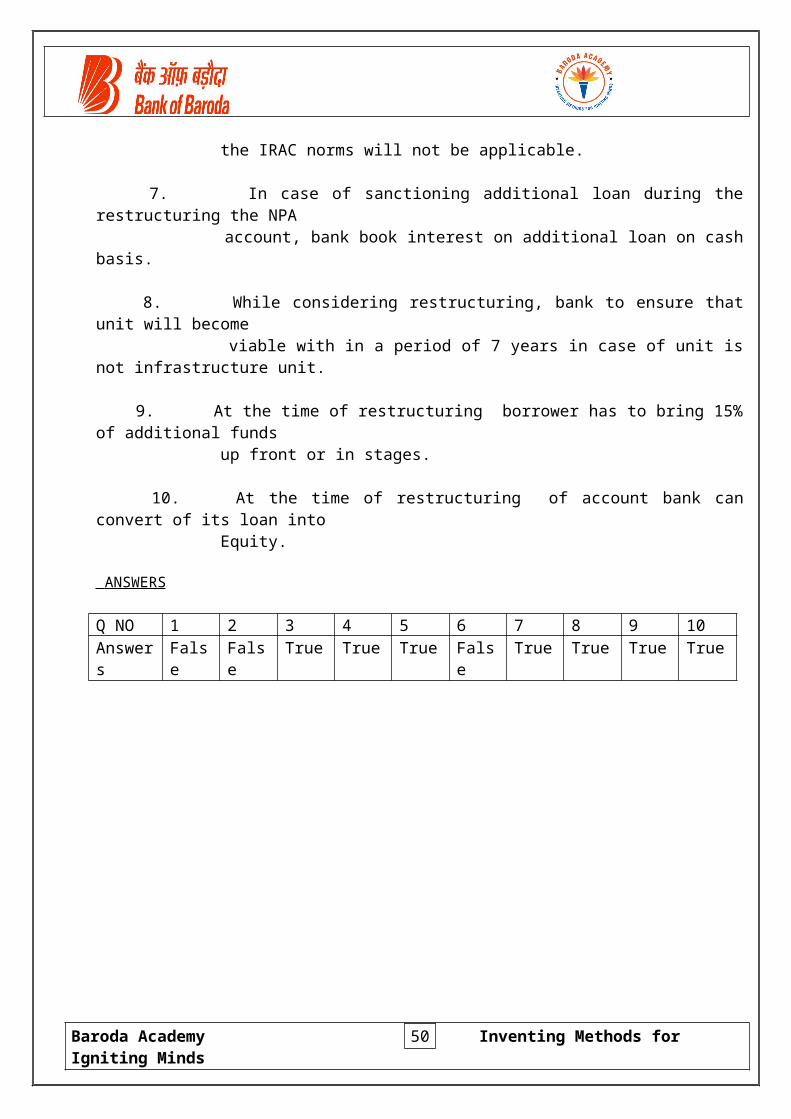

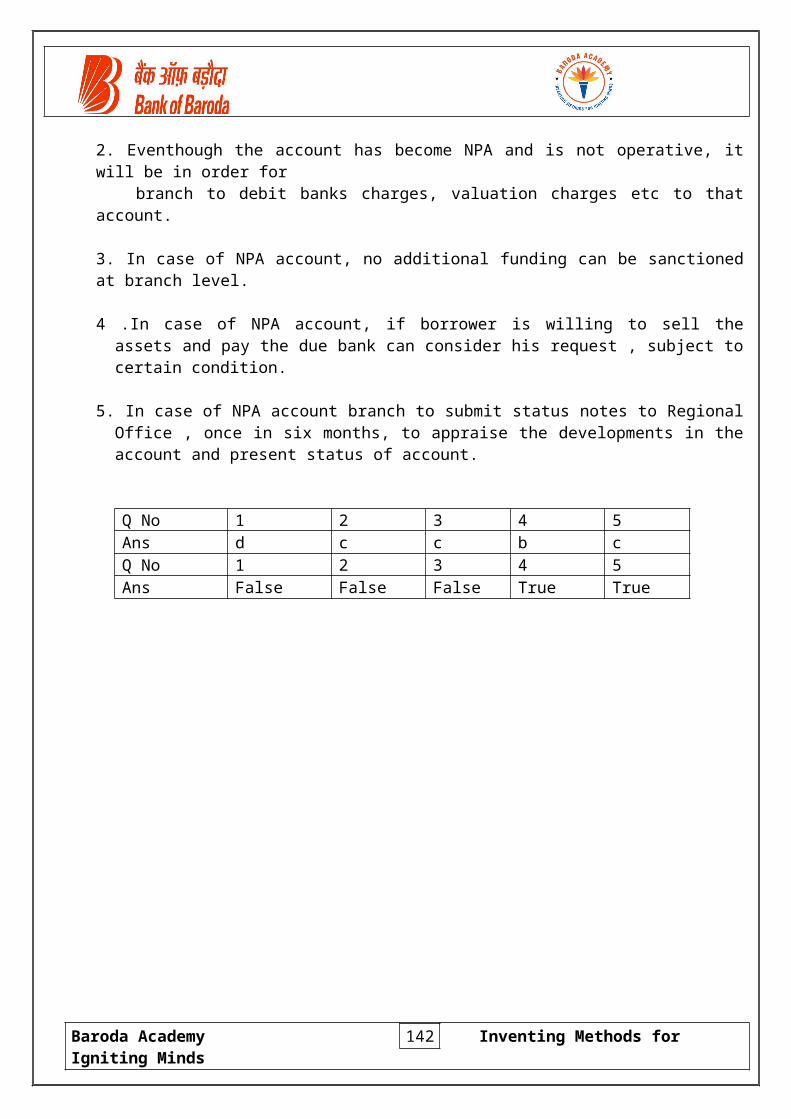

TEST YOUR UNDERSTANDING

State whether the following statements are True or False

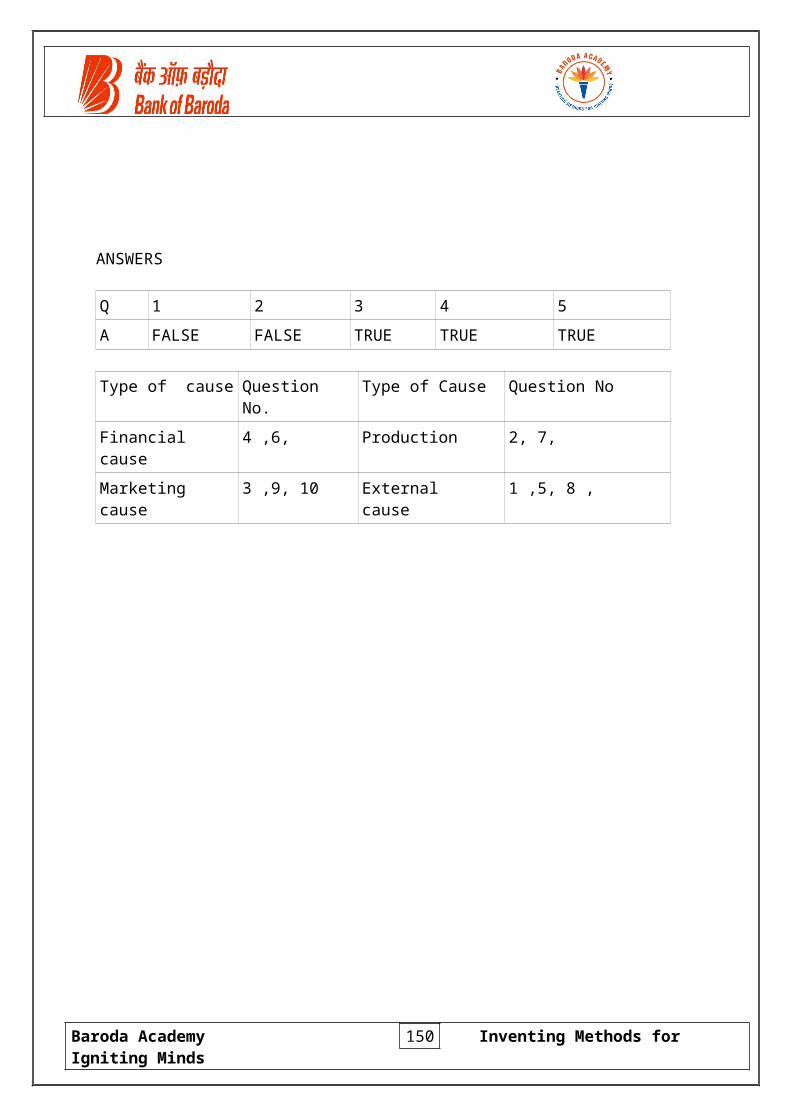

1. Classification of the borrower as Wilful Defaulter will not have any impact, as he can raise the funds from marked.

2. Provisions for classification of Borrower as wilful defaulter are applicable only to those borrowers whose outstanding is of Rs 25 lac and above.

3. If any irregularity persists in any borrowal account for a period of 30 days or more then we have to classify the account as Special Mention Account.

4. If in a borrowal account there are no overdues, but compliance of terms of sanction is pending for 5 weeks, then the account will be classified as Special Mention Account.

5. Incomplete documentations is not a early warning signal.

ANSWERS

Q 1 2 3 4 5

A FALSE TRUE TRUE TRUE FALSE

Baroda Academy Inventing Methods for Igniting Minds

11

CREDIT MONITORING TOOLS

Quick Bites

Various tools of Credit Monitoring Stock / Book Debt Audit Monthly Monitoring Report Credit Audit & Guidelines concurrent auditors for large borrowal accounts Exit policy for high risk borrowers End Use of Funds Review Post Sanction Reporting (PSR) Norms for Risk based inspection/verification of stock & BDs Credit Rating Internal Inspection ASCROM

Important Tools of Credit Monitoring:

1. Monitoring day to day operations in the account at least on a test basis; 2. Stock/ book-debts statements; 3. Review of the account; 4. Periodical inspection / verification of the securities charged to the bank; 5. Credit Rating at stipulated intervals; 6. Satisfying upon whether the borrower is paying statutory dues / Electricity bills

telephone bills / wages etc. in time. 7. Finding whether the borrower has recently cut-down any major activity / expenses

which he was doing otherwise in ordinary course of business. 8. Keeping an ear to the market news / reports. 9. Meeting with the borrowers and discussing with him, besides the business, what else

he is doing / planning and whether something is bothering him in business or in personal life like family separation, sickness of important person in the family, heavy financial commitment of personal nature etc.

1. Stock / Book Debt Audit

As per extant guidelines, major features for Stock/Book Debt Audit are as under:-

• The existing practice of conducting stock inspections and book debts verification by branch officials and random inspection by concurrent auditors to continue as per guidelines.

• Annual Stock/Book Debt Audit (i.e. covering the period 1st April to 31st March every year) is to be carried out in all accounts having fund- based working capital limits (including DA LC limit) of over Rs. 5.00 crores with our Bank.

Baroda Academy Inventing Methods for Igniting Minds

12

• The Stock Audit/Book Debt Audit may be conducted at more frequent intervals (i.e. more than once a year) if deemed necessary by the Bank.

• Initially, this stock audit to be restricted to sole banking accounts, accounts under multiple banking and consortium accounts where our Bank is the leader of the consortium.

• Panel of Chartered Accountants / C.A. firms for entrusting Stock Audit Work to be finalized by Zonal Authorities.

2. Monthly Monitoring Report:

The purpose of MMR is to ensure and facilitate qualitative supervision of the bank’s credit portfolio. The MMR will provide information on early warning signals with a view to trigger timely corrective actions. These will facilitate slippage prevention and impairment of credit quality

The basic purpose is to ensure that branches are following the guidelines of loan policy, Recovery policy, Review of the accounts, Compliance of terms and conditions, Credit rating and other monitoring tools available for the purpose

Objectives: 1. Slippage prevention and improve the credit rating 2. Early detection of warning signals, potential NPA, incipient sickness. 3. To initiate timely and corrective action for preventing impairment. 4. To take necessary action for follow up and review of credit facility. 5. To ensure that no revenue leakage in respect of ROI or charges 6. Weak rated accounts BOB-7, B and C rated, Rescheduled, CDR accounts are to be

closely monitored.

Under the system, branches are required to submit monthly monitoring reports as under:-• Advance accounts of Rs.10 crores (FB+NFB) through Zonal Office to Corporate Centre within 10 days of reporting date (i.e. by 25th of every month)

For a better and efficient system of monitoring of large advances bank has introduced a web based centralized solution for credit monitoring reports for advances accounts with FB and NFB exposure of Rs 10 crores and above . Hence submission of MMRs in word format for advances account of Rs 10 crore and above has been discontinued.

The Software can be opened through the Finacle System by entering the following URS:spgrs.bankofbaroda.co.in/cremon

1. Branch USERID : Branch Alpha Code2. Password : Default password is bob1234* The branch should change the password.

New password should contain 8 characters with alpha, numeric and special characters.3. In case of existing account only necessary changes in the data are to be made in the all

parameters like outstanding, overdues, date of review etc.4. New account should be opened through system.

Baroda Academy Inventing Methods for Igniting Minds

13

• Zonal Manager to monitor all advance accounts above Rs.5 crore to Rs.10 crore (FB+NFB) based on the MMR received through Regional Office. The Zones will also submit copies of the MMRs of these accounts to BCC for further monitoring.

• Regional Manager to monitor all accounts above Rs.1 crore to Rs.5 crores (FB+NFB) based on MMRs received from branches. Regional Office will also submit copies of the MMRs of these accounts to Zonal Office for further monitoring.

• Branch Manager to monitor accounts of Rs.1 crore and below.

Further Regional Offices are also to monitor: - Advance accounts with exposure of Rs.25 lacs to Rs.1 Crore based on Quarterly

Monitoring Reports received from Branches / Scrutiny of ASCROM data. Advance accounts with exposure of RS. 1 lacs to Rs. 25 lacs based on scrutiny of

ASCROM data.

Accounts Causing Concern:

Regional Offices are to submit a summary report in the prescribed format on advance accounts causing concern:

With exposure above Rs. 1 crore to Rs. 5 crore alongwith copy of MMRs to BCC with a copy to Zonal Office at monthly interval, within 7 days of reporting date of MMR i.e. before 22nd of every month.

With exposure above Rs. 25 lacs to Rs.1 crore alongwith copy of Quarterly Monitoring Report (QMR) to BCC with a copy to Zonal Office at quarterly interval within 7 days of reporting dates of QMR which are 15th March, 15th June, 15th

September and 15th December.

As regards to accounts causing concern, officials from RO/ZO may take appropriate decision to visit such accounts on case- to-case basis, to conduct on the spot study of the unit and discussions with the borrower for taking timely remedial actions to prevent slippage in the account.

3. Credit Audit & Guidelines

A. As per the recommendations of Narang Committee, RBI has advised all banks to have lending mechanism for large advances soon after the sanction.

B. The objectives of credit audit are; (i) Review sanction process and compliance status of large loans (ii) Improvement in quality of credit portfolio. (iii) Recommend corrective action to improve credit quality, credit administration and credit skill of staff.

(iv) Pick up early warning signals and suggest remedial actions.

C. Cut off limit for the account - (i) Existing accounts with FB + NFB limit of Rs. 10 crores and above,

Baroda Academy Inventing Methods for Igniting Minds

14

(ii) Fresh sanction including increase/ adhoc with limit Rs. 5 crores and above (iii) 5% of the accounts of the Region on random basis with sanction limit of Rs. 1 crores and above but below Rs. 10 crores.

D. No Credit audit for NPA accounts .

E. The credit audit is required to be carried out within 3 to 6 months from the date of sanction/ review.

F. Credit audit of eligible accounts of one region is to be carried out by officers of another region within the zone.

G. The credit auditor has to study conduct of the account, turn over in the account, excess drawing, return of cheques, inter-firm transactions and compliance of terms and conditions and will submit the report in prescribed format directly to CIAD with a copy to respective branch, Regional office, Zonal office & ZIC through soft copy

4. Appointment of concurrent auditors for large borrowal accounts. With a view to curb the mounting NPA, a continuous on sight monitoring of the borrowal accounts is essentials. Our bank has decided to appoint Concurrent auditors for the purpose. Accounts falling under the criteria are as under: -

(i) Accounts with exposure of Rs. 25 crores and above with B+ rating as per old credit rating models and BOB-6 as per new rating

(ii) Accounts with exposure of Rs. 10 crores and above with B & C rating as per old rating models and BOB-7 & below as per new rating .

(iii) In case of sole banking or multiple banking, concurrent audit should be introduced immediately

(iv) .In case of consortium accounts where we are leader and account falling under any of the above criteria, a joint decision is to be taken by the consortium banks. Where we are not leader, impress upon the lead bank and members to introduce the concurrent audit.

The concurrent audit to be entrusted to empanelled firm of Chartered Accountants. The Zonal Head will allot the assignment to these firms. It is to be noted that such assignment to be restricted to three accounts per firm of CA.

Wherever concurrent auditor is appointed, bimonthly stock inspection is to be carried out by the branch as per extant guidelines.

Concurrent auditor will submit his monthly report regularly. Branches to offer their comments/ action initiated etc to the respective regional offices.

The stipulation of concurrent audit, as above, is to form a part of the sanction/ review terms and conditions and to be advised to the borrowers. The fee for concurrent audit as finalized by the CID is to be borne by the borrowers.

Baroda Academy Inventing Methods for Igniting Minds

15

5. Exit policy for high risk borrowers:

(i) To identify the borrowers accounts at the right time for exit. The early warning signals, market report, Govt. policies etc. are to be studied to identify the account for exit. Followings are the list of early warning signals/resources for identifying the borrowers for exit: -

(ii) Deterioration of credit rating for last two years from ‘BOB-6’ to downwards. (iii) Financial performance is deteriorating during last two years. (iv) The borrower has started suffering from liquidity crunch. (v) Conduct of the account- poor turn over, return of cheques for financial reasons,

consistent overdue in the account ,. Financial indiscipline. (vi) The quality/value of the assets charged to the bank is deteriorating steadily(vii) The borrower is resorting to high cost borrowings to keep afloat. (viii) he regulators are scanning the borrower’s activity. (ix) Name of directors/ promoters /Company appear in the default list of RBI/ECGC

etc. (x) The revenue authorities are raising high value claims on the borrower. (xi) Top management team of the borrower is frequently changing or dispute among the

directors/ promoters. (xii) Continuously requesting for excess/ adhoc etc. (xiii) Account with us is regular but with other bank, highly irregular.

(xiv) The industry trend is sunset.

Action plan: 3. Close monitoring of such accounts. 4. No excess/adhoc to be considered. 5. Inform the borrower about banks disinclination to take any additional exposure. 6. Strategy for hand holding, cut back, take out financing etc. to be adopted. Wherever

needed, gradually to reduce our exposure. 7. The quarterly operative limits should be strictly enforced. 8. In case of consortium, no further increase to be accepted. 9. Try to recover the entire dues without any loss to the bank. 10.A compromise or OTS can also be initiated by waiver of penal interest and reduction

in rate of interest from contractual rate, up to Base Rate+4%, for last 12 months. In case if the borrower is not in a position to pay one time/ lump sum payment, a request can be considered for a maximum up to 12 months with a stipulation to pay 25% as upfront payment.

11.All sanctioning authorities would exercise the powers to exit the account up to their DLP.

The adverse observations are to be immediately reported to the sanctioning authority and measures be taken for correction of the same. Concurrent Audit is also prevalent in the Bank, as an additional support System, which takes care of reporting to the higher management directly on various areas that are to be reported as per the terms of services for which engaged, including revenue leakage, documentation, other relevant observations etc. pertaining to borrowal accounts.

Baroda Academy Inventing Methods for Igniting Minds

16

6. End Use of Funds

In view of recent spurt in capital market RBI has directed that Branches should ensure that the loans sanctioned by bank, particularly the general purpose loans are used for the purpose for which the same are sanctioned and not diverted to the capital market. The Branches should continuously monitor end use of funds and obtain certificates from the borrowers certifying that the funds have been used for the purpose for which these were obtained and not diverted to the capital market.(Ref: BCC/BR/103/22 dt. 18.01.2011)

In light of the above instructions by RBI, the following systems and procedures are advised to be followed by the branches strictly:

(i) While processing any proposal, the purpose for which the advance is given is to be clearly understood / appraised in the proposal.

(ii) After sanction and at the time of disbursement, it is to be ensured that the disbursements are made only in relation to the purpose for which the advance is sanctioned.

(iii) In respect of Working Capital accounts, a continuous monitoring is required to ascertain the nature of payments made and whether such payments are related to the purpose of advance or not

(iv)The monthly stock statements, QIS / QMR statements are to be thoroughly checked for the reasons they are submitted for and not in a routine manner.

(v) All disbursements in term loans to be directly made to the supplier after ensuring that sufficient margin is routed through the account.

(vi) The assets such acquired must be inspected at the earliest possible date and the inspection report containing the details and specifications of the asset are to be kept in records.

(vii) The original invoices / bills relating to the purchase of assets with clear details and specifications of the asset should be obtained and kept in records.

(viii) Wherever it is not possible to make direct payment and the nature of requirement is such that disbursements are to be made only to the credit of their accounts, permission from the sanctioning authorities/ competent authorities should be obtained at the time of sanction itself.

(ix) In respect of Term Loans/Demand Loan, the purpose for which the loans are requested for should be ascertained at the time of the initial application and on sanction, should be ensured that the funds are utilized for the said purpose only.

(x) In no case, the amounts are to be credited to their operative accounts and allow them to divert the funds elsewhere.

(xi) In such cases, invariably an undertaking to be obtained from the borrowers for the end use of funds and their auditor’s certificate to be obtained and kept in records.

(xii) Wherever there is specific requirement for infusion of promoters’ contribution / margin towards acquiring assets, it is to be ensured that the funds are routed through the Bank account with us, with discreetly inquiring about the source of funds brought in. An auditor’s certificate from their regular auditor may be obtained to substantiate the contribution / margin.

Baroda Academy Inventing Methods for Igniting Minds

17

The branches are also advised to strengthen their follow-up and credit monitoring activities and the post sanction supervision may be strictly adhered by the following:

(i) scrutiny of the periodical progress reports and operating / financial statements of the borrowers

(ii) visits to the assisted units and inspection of securities charged to the banks (iii) periodical scrutiny of the books of accounts of the borrowers(iv)Stock audits as per extant guidelines.(v) Obtention of certificates from the borrowers that the funds have been utilized for the

purposes approved(vi) Examination of all aspects of diversion of funds during internal audit / inspection of

the branches and at the time of periodical reviews.

7. Review

Regular Review

Credit facilities sanctioned to borrowers are subjected to annual review (except LABOD, staff loans and the accounts where facilities sanctioned are for a period less than one year etc.) as per the prevailing guidelines.

However in case of borrowal accounts enjoying credit facilities of Rs.10 crores and above and where the credit rating of the account is BOB-7 or below the account should be reviewed on half-yearly basis.

The accounts are required to be reviewed on or before the due date. The review takes a comprehensive view on various issues covering financial health, borrower’s performance and prospects, quality of the management, conduct of the account, compliance, etc. The review will also evaluate the impact of deficiencies observed during inspection / Concurrent / statutory / Credit Audit / RBI inspection and rectification thereof.

Branches have been authorized by the Board to review advances accounts with limit upto Rs. 20 lacs pending receipt of audited financial statements, provided the conduct of the account is satisfactory in terms of: -

(i) Turn over in the accounts.(ii) Fulfillment of repayment obligations (interest / installments)(iii) Adequacy of securities, drawing power, insurance coverage etc.(iv) Rectification of inspection irregularities (other than non-submission of financial

statements)(v) Compliance of all terms and conditions of previous sanction(vi) Satisfactory trend in production and / or sales as per projections.(vii) Documentation and mortgages in the account being complete, valid and

enforceable.(viii) Submission of income tax / sales tax returns filed with the statutory authorities as

per time schedule prescribed, wherever applicable. (This will also indicate about the sales and profitability of operations.)

The objective of the above system / procedure is to ensure timely review of advances accounts so that the slippage of the accounts to NPA category on technical grounds may

Baroda Academy Inventing Methods for Igniting Minds

18

be avoided. However branches should nevertheless obtain latest financial statements within a reasonable time after the review is conducted and satisfy themselves as to the financial parameters emerging out of the Balance Sheet / Profit & Loss a/c. In case any adverse features are observed in the financials of the borrower, Branches should immediately initiate appropriate action as warranted.

Short Review / Status Note:

The bank has also the practice of Short Review / Status Note, which is done when it is not possible to carry out a comprehensive Regular Review of the account within the stipulated period pending receipt of certain particulars/ information or where the account is placed under special monitoring, etc.Consecutive Short Reviews shall be restricted to two with a maximum period of six months for each short review. But in exceptional cases, the next higher authority (not below the level of Chief Manager) may do more consecutive Short Reviews after satisfying himself about the need for the same and reasons duly recorded. Relaxation is also provided to restructured accounts and accounts under rehabilitation where for a variety of reasons only, Short Reviews may have to be done till such time the unit/account becomes normal and healthy.

Where there is impairment of borrower’s quality indicated through various adverse features like default, diminution in value of security etc., suitable communication and if need be a Short Review / Status Note should be placed before competent authority for perusal, direction and necessary action.

Review of Priority Sector Advances. (ref. BCC/BR/103/248 dt. 30.08.11)

Keeping in view to cope up with rush of farmers borrowers at a time and reduce the repetitive laborious work in filling up the information which is already available in the system, a Memorandum of review for small loans under Agriculture and Government Sponsored Schemes (falling under the business line of Rural & Agri. Banking) is available for accounts where there is no need to analyze the balance sheet, in ASCROM package.

The Path for generating the review reports and forwarding letter is as below:“Reports/Reports/Rural And Agri-I/32) Memo. of Review of small Loans Under Agr. Govt. Spon. Schm.” and. “Reports/Reports/credit monitoring-I/23) List of Review of small Loans-PS.”

Advantages of this system are:(i) Branch need not to prepare a review proposal. It can be generated from ASCROM

with basic details along with balance outstanding and overdue etc. under each credit facility of the borrower. Branch only has to verify the same, insert details of inspection queries and present status as well as the decision of the branch.

(ii) All overdue proposals can be generated (iii) Branch can maintain the record in individual borrowers file which will facilitate at the

time of inspection for the review of accounts.

8. Post Sanction Reporting (PSR)

Baroda Academy Inventing Methods for Igniting Minds

19

Bank follows a Post Sanction Reporting. The features are:

(i) Covers all sanctions and credit decisions viz., Fresh / Increase /Renewal / Rejection / Adhoc / Excess / Modifications / Waivers /restructuring / rescheduling etc., excluding sanction of staff advances, LABOD (i.e. post sanction reporting of LABOD and Staff Loans is not required).

(ii) Broad parameters relating to sanction are only examined by the PSR authority whereas the sanctioning authority shall take care of all procedural details on credit appraisal, adequacy of security, documentation etc.

(iii) Observations of PSR authority are to be attended immediately, which shall also serve as guide to the sanctioning authority for future.

(iv)Disbursement of credit facility/ies is not to be withheld merely for want of observations of the competent authority on PSR.

(v) All Sanctions in respect of Fund-Based and Non Fund-Based credit limits (excluding LABOD & Staff Loans) are to be reported to PSR Authority on monthly basis in the prescribed format. However, enclosures such as Appraisal Note, latest financials, credit rating sheets etc; for sanctions up to Rs. 10 lacs, in case of rural and semi urban branches and upto Rs 25 lac in case of Metro and Urban branches (Rs. 5 lacs for Retail Loans) need not be sent with the prescribed formats for PSR.

(vi)Copies of Credit Proposals with Fund Based and Non Fund Based sanctioned limit aggregating above Rs. 10 lacs in case of rural and semi urban branches and above Rs 25 lacs in case of Metro and Urban branches (retail loans above Rs. 5 lacs) should be forwarded to PSR authority within 3 days of sanction along with Appraisal Note, latest financials with necessary comments by the sanctioning authority, latest credit rating sheet, gist of major adverse features and non-compliance of stipulated terms and conditions and the sanctioning authority’s comments there on.

(vii) The PSR authority is required to clear the proposal from PSR angle within a period of –30- days from the date of receipt of proposal. If the PSR authority has not made any observation within the said period, it will be presumed that the PSR authority has no observation to make and the proposal is cleared from PSR angle.

.9. Norms for Risk based inspection/verification of stock & BDs:

Prime Securities charged for WC limits as per BOBRAM rating

Periodicity

Latest Credit Rating is A+ for Old rating BOB 1 to BOB3 as per CRISIL

Half Yearly

Latest Credit Rating is A for Old rating, BOB4 & BOB5 as per CRISIL

Quarterly

Latest Credit Rating is B+ for Old rating, BOB-6 & Below as per CRISIL

Bi-Monthly

Fixed Assets charged against Loans Half yearly (Jan & July) Consortium Accounts As fixed by Consortium Inspection of Collateral securities Annually

Baroda Academy Inventing Methods for Igniting Minds

20

Retail Loans: Housing Loan On every disbursement & thereafter once in -3- years.

Overdraft Against Property On disbursement & then annually Two wheelers / Car loan /Traders Loan & Profess. Loans

Once in a year and the gap between two inspection should not be less than 10 months

(i) Over and above inspection as mentioned above the sanctioning authorities shall have to visit the borrowers once in a year

(ii) Inspection of collateral to be carried out preferably once in a year for all types of facilities.

(iii) To carry out compulsory annual stock audit/ book debt audit in all account having fund based working capital limits including DA Letter of Credit of over Rs. 5.00 crores. This stock audit is to be done by panelled chartered accountant once in a year.

10. Credit Rating

As per extant guidelines, Credit rating cycle is yearly in case of borrowal accounts enjoying credit facilities of Rs. 2 lacs ( Fund Based and Non- Fund Based) and above.

In case of accounts below Rs 25 lac credit rating is to be done for taking credit decision ,but pricing is delinked. For account of Rs 25 lac and above credit rating is important for taking credit decision and also for pricing.

At time of review if there is downgrading in Credit Rating, we have to ascertain the reasons and the same should be discussed with the borrower and corrective steps should be taken to improve the health of the account.

In case of accounts above Rs 5 crores , we should ask the borrower to get the account rated from approved external Credit Rating Agencies.

11. Internal Inspection (RBIA ):

Inspection is a control tool to ensure that day to day activities of the branch, its management, lending decisions, safety of the Bank’s funds are in conformity with the administrative instructions /guidelines issued from time to time & in furtherance of corporate objectives. The objectives of internal inspection are:

(i) To scrutinize the completeness & enforceability of the documents taken for advances & other facilities.

(ii) To carry out physical checking, qualitatively and quantitatively of stocks & other assets charged to the bank by pledge, hypothecation or mortgage.

(iii) To ascertain for sanction for advances(iv)To verify prompt & regular submission of periodical& statutory returns(v) To verify asset classification of advances(vi)To ascertain position of income recognition(vii) Ensure that qualitative rectification has taken place

Baroda Academy Inventing Methods for Igniting Minds

21

Besides, Statutory Audit carried by Statutory Auditor, RBIA is a comprehensive feedback to the management about the degree of compliance of Bank’s norms, classification of assets, and quality of advance portfolio. etc.The compliance is monitored through rectification certificate.

12. Branch to collect periodically details of various statutory dues paid by the borrower e.g. payment of Sales Tax/Service Tax/Excise Duty, MESB Bills ,TDS etc

13.QIS Statement

To know the estimates and performance of the borrower branch to call the QIS statements from all borrowers who are enjoying working capital limits of Rs 1 crore and above of entire banking system. Statement Periodicity Branch actionQIS I One week before

the commencement of the quarter for which it relates

Branch to compare the estimates of sales with projections. For major variance branch to discuss it with borrower. Branch to check the level of estimated current assets and current liabilities and also the operative limit. Branch to modity the operative limit in Finacle and Ascrom

QIS II Within six weeks after end of the quarter, for which it relates

Compare the performance with estimates given in QIS I and also with Projections given earlier. Check the variance . Discuss the reasons with borrower.

QIS III Within two months after close of the half year.

Compare the performance with the projections and check the variance. Discuss the reasons with borrower and take suitable corrective steps.

14. Exchange of Information in case of Consortium /Multiple Banking Accounts.

While sanctioning a loan branch should obtain details of existing facilities enjoyed by the borrower from various banks and financial institutions. Then every quarter branch should exchange the details of credit facilities with the other Banks and FIs and also ensure the exchange of information by them. In case of Consortium advances exchange of information should be done amongst the members and consortium meeting should be hold at least once in a quarter. Branch should also obtain a certificate by a professional, preferably from Company Secretary ( but if it is not possible then from Chartered Accountant or Cost Accountant )regarding compliance of various statutory prescription which are in vogue.

15. Compliance of observations of PSR authority, Statutory Auditors, Concurrent Auditors, Observations received on MMR.

16. Branch to follow following time bound schedule of follow up for prevention of slippage.

Baroda Academy Inventing Methods for Igniting Minds

22

Due Date of EMIS Action to be initiated(-7 – o days ) 7 days before System generated SME reminder

O day ( due date ) System generated SMS 2nd reminder7-30 days 0-6th day Collection of EMI

7th day System generated SMS 3rd reminder8th -9th day 1st Telephonic contact and 1st written

Reminder ( system generator )10th day Personal Meeting of Branch official

with Borrower15th day 2nd Telephone contact21st-25th day System generated 1st Registered

Reminder30th day Personal meeting of official from circle

office alongwith branch official with borrower

31-60 days 37th-40 day 3rd telephonic contact and 1st

telephonic contact with the guarantor41st – 44th day 2nd Registered Reminder with a copy

to guarantor45th day Personal Meeting of official from HO

alongwith branch/CO with the borrower

56th -60th day Personal contact with borrower/family members or guarantors at residence /work place by the incumbent

61-90 days 70th -72nd day 3rd Registered reminder with copy to guarantor.

Before 80th day Personal and /or telephonic contact with guarantor at his residence.

Before 90th day Personal contact by incumbent himself again with borrower/guarantor/family members

17. ASCROM SYSTEM

Genesis

ASCROM SYSTEM:

Asset Classification and Credit Monitoring System.Earlier ASCROM software was developed in DOS and coded in FOXPRO. It was designed to capture comprehensive profile of Advance portfolio at quarterly interval and was implemented in all Domestic branches of the Bank in September 1998.The present ASCROM SYSTEM is developed in VB DOTNET as front end for user interface and MS SQL SERVER as Back end data base. It is implemented in all domestic branches since APRIL 2007. Data is now captured at monthly interval.The ASCROM System in our bank at present is taking care of: -

Baroda Academy Inventing Methods for Igniting Minds

23

(i) Asset Classification and provisioning as per IRAC norms.(ii) Computation of Capital Charge on Credit Risk as per BASEL II Requirements

(Standardized Approach)(iii) Submission of CIBIL data.(iv) ALM Report for Advances.(v) Generation of various MIS reports.

TEST YOUR UNDERSTANDING :

01 Credit audit is based on recommendations of a) Vyas Committee

b) Kapoor committee c) Narang Committee d) Zilani Committee e) Damodaran Committee

02. Short review is carried out whena) When borrower wants additional facility before due date.b) When borrower wants to close the account within 3 months.c) When borrower wants to close the account within 6 monthsd) When it is not possible to carry out regular review on account of

pending information. e) When account becomes NPA

03. PSR in respect of advances is related to following type of advances.a) Restructured accounts.b) All types of sanctions and credit decisionsc) All types of sanctions and credit decisions except staff loans and

LABOD.d) All types of sanctions and credit decisions except staff loans and

LABOD, Loans against NSC/KVPs and LIC policies.

e) All types of sanctions and credit decisions except Gold Loan

04. Large borrowers enjoying facility of RS 10 crores and above should be reviewed

a) On yearly basis when credit rating is BOB-6 or belowb) On quarterly basis when credit rating if BOB-6 or belowc) on half yearly basis when credit rating is BOB-7 or below.d) on half yearly basis when credit rating is below BOB-8

e) On yearly basis when credit rating is BOB 5 or below

05. PSR authority is required to clear the proposal from PSR angle within period of

a) 60 days from the date of receipt of proposal.b) 30 days from the date of receipt of proposal.

Baroda Academy Inventing Methods for Igniting Minds

24

c) 90 days from the date of receipt of proposal.d) No date is fixed for such purpose.

e) 120 days from the receipt of proposal.

06. Submission of CIBIL data is done througha) ASCROM systemb) Finacle

c) a&b d) None e) Cloret

07. RBIA stands fora) Risk Before International Advisorsb) Risk Before Indian Administratorsc) Risk based Internal Auditd) None ofthe above.

e) Regular Branch Inspection and Audit 08. In case of the working capital facilities with Credit rating upto BOB3, the

prime securities charged under working capital facility will be inspected a) Half Yearly b) Quarterly c) Bi-Monthly d) Annually e) No specific periodicity

09. Stock/Book Debt Audit (i.e. covering the period 1st April to 31st March every year) is to be carried out compulsorily in all accounts having fund- based working capital limits (including DA LC limit) of over Rs ----- crores with our Bank. a) 10 crore b) 1 crore c) 25 crore d) 5 crore e) 3 crore

10. Cut off limit for the Credit Audit in respect of existing accounts with FB + NFB limit of Rs. ------ crores and above.

a) 5 crore b) 1 crore c) 10 crore d) 2 crore e) 3 crore

11. Cut off limit for the Credit Audit in respect of fresh accounts with FB + NFB limit of Rs. ------ crores and above.

Baroda Academy Inventing Methods for Igniting Minds

25

a) 5 crore b) 1 crore c) 10 crore d) 20 crore e) 25 crore

12. The credit audit requires to be carried out the audit within --- to --months from the date of sanction/ review.

a) 1 to 2 months b) 2 to 3 months c) 3 to 6 months d) 6 to 12 months e) 6 to 9 months

13. Borrowal accounts with credit rating of BOB 4 or 5 , the periodical inspection in respect of current assets is to be done , once in ________________ a) six months b) three months c) two months d) four months e) 12 months

14. Consecutive Short Reviews shall be restricted to --- with a maximum period of ---- months for each short review.

a) 1 time/ 3 months b) 2 times / 6 months c) 3 times/ 4 monthsd) 1 times onlye) 1 times /6-9 months

15. In case of Retail Lending sanctions above Rs. ---- lacs, copies of Application-cum-Appraisal Note should be sent to PSR authority within three days of sanction. a) 10 lacs b) 5 lacs c) 7 lacs d) 15 lacs e) Irrespective of loan limit

ANSWERS

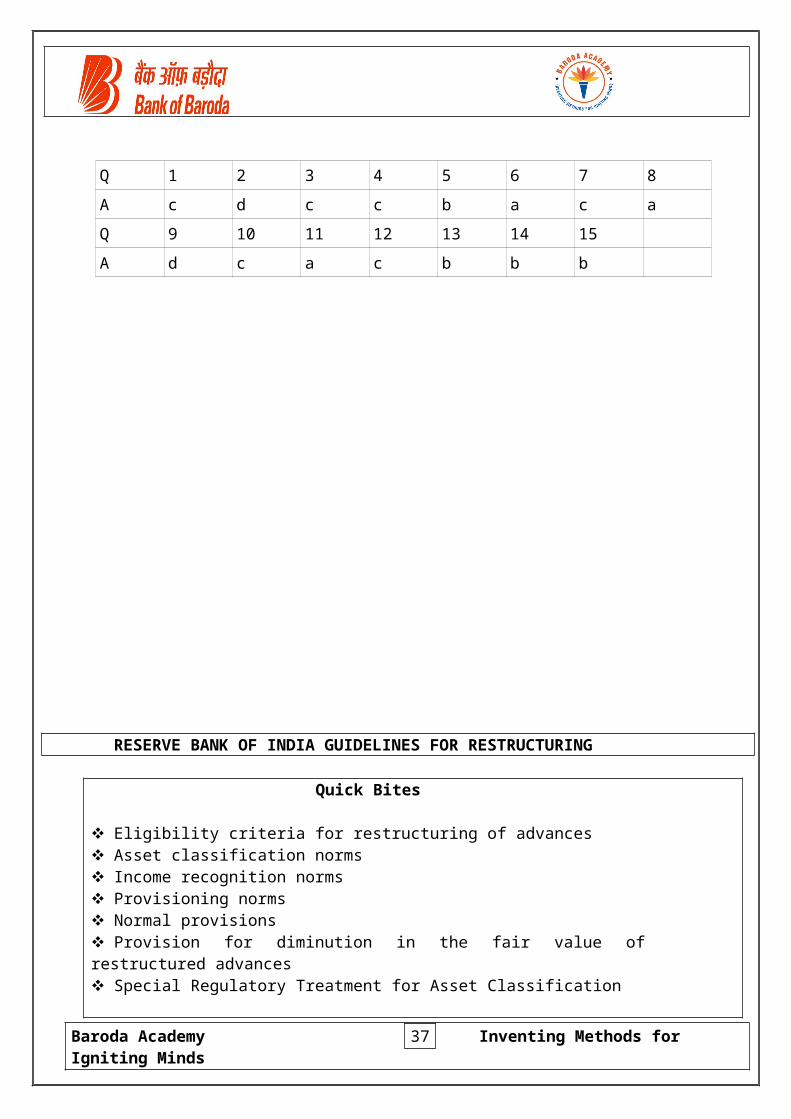

Q 1 2 3 4 5 6 7 8

Baroda Academy Inventing Methods for Igniting Minds

26

A c d c c b a c a

Q 9 10 11 12 13 14 15

A d c a c b b b

RESERVE BANK OF INDIA GUIDELINES FOR RESTRUCTURING

Quick Bites

Eligibility criteria for restructuring of advances Asset classification norms Income recognition norms Provisioning norms Normal provisions Provision for diminution in the fair value of restructured advances Special Regulatory Treatment for Asset Classification

General Principles and Prudential Norms for Restructured Advances

The principles and prudential norms laid down here are applicable to all advances including the borrowers, who are eligible for special regulatory treatment for asset classification.

Eligibility criteria for restructuring of advances

1 Banks may restructure the accounts classified under 'standard', 'sub-standard' and 'doubtful' categories.

Baroda Academy Inventing Methods for Igniting Minds

27

2 Banks can not reschedule / restructure / renegotiate borrowal accounts with retrospective effect. While a restructuring proposal is under consideration, the usual asset classification norms would continue to apply. The process of re- classification of an asset should not stop merely because restructuring proposal is under consideration. The asset classification status as on the date of approval of the restructured package by the competent authority would be relevant to decide the asset classification status of the account after restructuring / rescheduling / renegotiation. In case there is undue delay in sanctioning a restructuring package and in the meantime the asset classification status of the account undergoes deterioration, it would be a matter of supervisory concern.

3 Normally, restructuring can not take place unless alteration / changes in the original loan agreement are made with the formal consent / application of the debtor. However, the process of restructuring can be initiated by the bank in deserving cases subject to customer agreeing to the terms and conditions.

4 No account will be taken up for restructuring by the banks unless the financial viability is established and there is a reasonable certainty of repayment from the borrower, as per the terms of restructuring package. The viability should be determined by the banks based on the acceptable viability benchmarks determined by them, which may be applied on a case-by-case basis, depending on merits of each case. Illustratively, the parameters may include the Return on Capital Employed, Debt Service Coverage Ratio, Gap between the Internal Rate of Return and Cost of Funds and the amount of provision required in lieu of the diminution in the fair value of the restructured advance. The accounts not considered viable should not be restructured and banks should accelerate the recovery measures in respect of such accounts. Any restructuring done without looking into cash flows of the borrower and assessing the viability of the projects / activity financed by banks would be treated as an attempt at ever greening a weak credit facility and would invite supervisory concerns / action.

5 While the borrowers indulging in frauds and malfeasance will continue to remain ineligible for restructuring, banks may review the reasons for classification of the borrowers as willful defaulters specially in old cases where the manner of classification of a borrower as a willful defaulter was not transparent and satisfy itself that the borrower is in a position to rectify the wilful default. The restructuring of such cases may be done with Board's approval, while for such accounts the restructuring under the CDR Mechanism may be carried out with the approval of the Core Group only.

6 BIFR cases are not eligible for restructuring without their express approval. CDR Core Group in the case of advances restructured under CDR Mechanism / the lead bank in the case of SME Debt Restructuring Mechanism and the individual banks in other cases, may consider the proposals for restructuring in such cases, after ensuring that all the formalities in seeking the approval from BIFR are completed before implementing the package.

Asset classification norms

Restructuring of advances could take place in the following stages :

(a) before commencement of commercial production / operation

Baroda Academy Inventing Methods for Igniting Minds

28

(b) after commencement of commercial production / operation but before the asset has been classified as 'sub-standard'

(c) after commencement of commercial production / operation and the asset has been classified as 'sub-standard' or 'doubtful'.

1 The accounts classified as 'standard assets' should be immediately re-classified as 'sub-standard assets' upon restructuring.

2 The non-performing assets, upon restructuring, would continue to have the same asset classification as prior to restructuring and slip into further lower asset classification categories as per extant asset classification norms with reference to the pre-restructuring repayment schedule.

3 All restructured accounts which have been classified as non-performing assets upon restructuring, would be eligible for up-gradation to the 'standard' category after observation of 'satisfactory performance' during the 'specified period'.

4 In case, however, satisfactory performance after the specified period is not evidenced, the asset classification of the restructured account would be governed as per the applicable prudential norms with reference to the pre-restructuring payment schedule.

5 Any additional finance may be treated as 'standard asset', up to a period of one year after the first interest / principal payment, whichever is earlier, falls due under the approved restructuring package. However, in the case of accounts where the prerestructuring facilities were classified as 'sub-standard' and 'doubtful', interest income on the additional finance should be recognised only on cash basis. If the restructured asset does not qualify for upgradation at the end of the above specified one year period, the additional finance shall be placed in the same asset classification category as the restructured debt.

6 In case a restructured asset, which is a standard asset on restructuring, is subjected to restructuring on a subsequent occasion, it should be classified as substandard. If the restructured asset is a sub-standard or a doubtful asset and is subjected to restructuring, on a subsequent occasion, its asset classification will be reckoned from the date when it became NPA on the first occasion. However, such advances restructured on second or more occasion may be allowed to be upgraded to standard category after one year from the date of first payment of interest or repayment of principal whichever falls due earlier in terms of the current restructuring package subject to satisfactory performance.

Income recognition norms

Interest income in respect of restructured accounts classified as 'standard assets' will be recognized on accrual basis and that in respect of the accounts classified as 'non-performing assets' will be recognized on cash basis.

Provisioning norms

1 Normal provisions

Baroda Academy Inventing Methods for Igniting Minds

29

Banks will hold provision against the restructured advances as per the existing provisioning norms.

2 Provision for diminution in the fair value of restructured advances

(i) Reduction in the rate of interest and / or reschedulement of the repayment of principal amount, as part of the restructuring, will result in diminution in the fair value of the advance. Such diminution in value is an economic loss for the bank and will have impact on the bank's market value of equity. It is, therefore, necessary for banks to measure such diminution in the fair value of the advance and make provisions for it by debit to Profit & Loss Account. Such provision should be held in addition to the provisions as per existing provisioning norms and in an account distinct from that for normal provisions.

For this purpose, the erosion in the fair value of the advance should be computed as the difference between the fair value of the loan before and after restructuring. Fair value of the loan before restructuring will be computed as the present value of cash flows representing the interest at the existing rate charged on the advance before restructuring and the principal, discounted at a rate equal to the bank's BPLR as on the date of restructuring plus the appropriate term premium and credit risk premium for the borrower category on the date of restructuring. Fair value of the loan after restructuring will be computed as the present value of cash flows representing the interest at the rate charged on the advance on restructuring and the principal, discounted at a rate equal to the bank's BPLR as on the date of restructuring plus the appropriate term premium and credit risk premium for the borrower category on the date of restructuring.

The above formula moderates the swing in the diminution of present value of loans with the interest rate cycle and will have to follow consistently by banks in future. Further, it is reiterated that the provisions required as above arise due to the action of the banks resulting in change in contractual terms of the loan upon restructuring which are in the nature of financial concessions. These provisions are distinct from the provisions which are linked to the asset classification of the account classified as NPA and reflect the impairment due to deterioration in the credit quality of the loan. Thus, the two types of the provisions are not substitute for each other.

(ii) In the case of working capital facilities, the diminution in the fair value of the cash credit / overdraft component may be computed as indicated above, reckoning the higher of the outstanding amount or the limit sanctioned as the principal amount and taking the tenor of the advance as one year. The term premium in the discount factor would be as applicable for one year. The fair value of the term loan components (Working Capital Term Loan and Funded Interest Term Loan) would be computed as per actual cash flows and taking the term premium in the discount factor as applicable for the maturity of the respective term loan components.

(iii) In the event any security is taken in lieu of the diminution in the fair value of the advance, it should be valued at Re.1/- till maturity of the security. This will ensure that the effect of charging off the economic sacrifice to the Profit & Loss account is not negated.

Baroda Academy Inventing Methods for Igniting Minds

30

(iv) The diminution in the fair value may be re-computed on each balance sheet date till satisfactory completion of all repayment obligations and full repayment of the outstanding in the account, so as to capture the changes in the fair value on account of changes in BPLR, term premium and the credit category of the borrower. Consequently, banks may provide for the shortfall in provision or reverse the amount of excess provision held in the distinct account.

(v) If due to lack of expertise / appropriate infrastructure, a bank finds it difficult to ensure computation of diminution in the fair value of advances extended by small / rural branches, as an alternative to the methodology prescribed above for computing the amount of diminution in the fair value, banks will have the option of notionally computing the amount of diminution in the fair value and providing therefore, at five percent of the total exposure, in respect of all restructured accounts where the total dues to bank(s) are less than rupees one crore till the financial year ending March 2013. The position would be reviewed thereafter.

3 The total provisions required against an account ( normal provisions plus provisions in lieu of diminution in the fair value of the advance) are capped at 100% of the outstanding debt amount.

Special Regulatory Treatment for Asset Classification

1 The special regulatory treatment for asset classification, in modification to the provisions in this regard stipulated, will be available to the borrowers engaged in important business activities, subject to compliance with certain conditions as enumerated below. Such treatment is not extended to the following categories of advances:

i. Consumer and personal advances;

ii. Advances classified as Capital market exposures;

iii. Advances classified as commercial real estate exposures

The asset classification of these three categories accounts as well as that of other accounts which do not comply with the conditions enumerated below, will be governed by the prudential norms in this regard described above.

Elements of special regulatory framework

The special regulatory treatment has the following two components :

(i) Incentive for quick implementation of the restructuring package.

(ii) Retention of the asset classification of the restructured account in the pre-restructuring asset classification category

Incentive for quick implementation of the restructuring package

Baroda Academy Inventing Methods for Igniting Minds

31

During the pendency of the application for restructuring of the advance with the bank, the usual asset classification norms would continue to apply. The process of reclassification of an asset should not stop merely because the application is under consideration. However, as an incentive for quick implementation of the package, if the approved package is implemented by the bank as per the following time schedule, the asset classification status may be restored to the position which existed when the reference was made to the CDR Cell in respect of cases covered under the CDR Mechanism or when the restructuring application was received by the bank in non-CDR cases:

(i) Within 120 days from the date of approval under the CDR Mechanism.

(ii) Within 90 days from the date of receipt of application by the bank in cases other than those restructured under the CDR Mechanism.

Asset classification benefits

Subject to the compliance with the under noted conditions in addition to the adherence to the prudential framework laid down:

(i) an existing 'standard asset' will not be downgraded to the sub-standard category upon restructuring.

(ii) during the specified period, the asset classification of the sub-standard / doubtful accounts will not deteriorate upon restructuring, if satisfactory performance is demonstrated during the specified period.

However, these benefits will be available subject to compliance with the following conditions:

i) The dues to the bank are 'fully secured'. The condition of being fully secured by tangible security will not be applicable in the following cases:

(a) SSI borrowers, where the outstanding is up to Rs.25 lakh.

(b) Infrastructure projects, provided the cash flows generated from these projects are adequate for repayment of the advance, the financing bank(s) have in place an appropriate mechanism to escrow the cash flows, and also have a clear and legal first claim on these cash flows.

(c) Micro Finance Institution accounts, which are standard at the time of restructuring, even if they are not fully secured. However, this relaxation is granted purely as a temporary measure and would be applicable to standard MFI accounts restructured by banks upto 31st

March 2011.

ii) The unit becomes viable in 10 years, if it is engaged in infrastructure activities, and in 7 years in the case of other units.

Baroda Academy Inventing Methods for Igniting Minds

32

iii) The repayment period of the restructured advance including the moratorium, if any, does not exceed 15 years in the case of infrastructure advances and 10 years in the case of other advances. The aforesaid ceiling of 10 years would not be applicable for restructured home loans; in these cases the Board of Director of the banks should prescribe the maximum period for restructured advance keeping in view the safety and soundness of the advances. Lending to individuals meant for acquiring residential property which are fully secured by mortgages on residential property that is or will be occupied by the borrower or that is rented are risk weighted as under the new capital adequacy framework, provided the LTV is not more than 75% , based on board approved valuation policy. However, the restructured housing loans should be risk weighted with an additional risk weight of 25 percentage points to the risk weight prescribed already.

iv) Promoters' sacrifice and additional funds brought by them should be a minimum of 15% of banks' sacrifice. The term 'bank's sacrifice' means the amount of "erosion in the fair value of the advance above. Further, the additional funds required to be brought in by the promoter should generally be brought in up front . However, if the banks are convinced that the promoters face genuine difficulty in bringing their share of the sacrifice immediately and need some extension of time to fulfill their commitments, the promoters could be allowed to bring in 50% of their sacrifice , i.e. 50% of 15%, upfront and the balance within a period of one year. Further, in case the promoters fail to bring in their balance share of sacrifice within the extended time limit of one year, the asset classification benefits derived by banks will cease to accrue and the they will have to revert to classifying such accounts as per the asset classification norms.

v) Personal guarantee is offered by the promoter except when the unit is affected by external factors pertaining to the economy and industry.

vi) The restructuring under consideration is not a 'repeated restructuring'.

Disclosure Requirements on Advances Restructured by Banks :

1. As per paragraph 16 of Reserve Bank of India Master Circular No. DBOD No. BP.BC.9/21.04.048/2012-13 dated July 2, 2012 on Prudential norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances the banks should disclose in their published Annual Balance Sheets, under "Notes on Accounts', Information relating to number and amount of advances restructured, and the amount of diminution In the fair value of the restructured advances under the following categories:

I. Standard Advances Restructured;fl. Sub-Standard Advances Restructured; andiii. Doubtful Advances Restructured.

Under each of the category above, advances restructured under CDR Mechanism, SME Debt Restructuring Mechanism and other categories of restructuring are required to be shown separately.

2. The Working Group (WG) constituted by RBI to Review the existing Prudential Guidelines on Restructuring of Advances which was chaired by Shri B. Mahapatra had

Baroda Academy Inventing Methods for Igniting Minds

33

recommended that once the higher provisions and risk weights (if applicable) on restructured advances (classified as standard either ab Initio or on upgradatton from NPA category) revert back to the normal level on account of satisfactory performance during the prescribed period, such advances should no longer be required to be disclosed by banks as restructured accounts in the "Notes on Accounts" in their Annual Balance Sheets. However, the provisKHi for diminution in the fair value of restructured accounts on such restructured accounts should continue to be maintained by banks as per the existing instructions. The WG also recommended that banks may be required to disclose:

I. details of accounts restructured on a cumulative basis excluding thestandard restructured accounts which cease to attract higher provisionand risk weight (If applicable);II. provisions made on restructured accounts under various categories; andIII details of movement of restructured accounts.

3. Accordingly, Reserve Bank of India vide their circular No. DBOD.BP.BC. No.80/21.04.132/2012-13 dated 31.01.2013 has advised that the banks shouldhenceforth disclose in their published Annual Balance Sheets, under "Notes onAccounts', information relating to number and amount of advances restructured, andthe amount of diminution In the fair value of the restructured advances as per theformat given in the Annexure. Detailed instructions relating to the disclosure are alsogiven In the Annex.

4. The above disclosure requirements will be effective from the financial year2012-13.

These disclosures need to be Audited at the time of Annual dosing henceforth starting with FY ending March,2013.

Some General Principles for Restructured Advances

1) Banks may restructure the accounts classified under 'standard', 'sub-standard’ and 'doubtful' categories.

2) Banks cannot reschedule/ restructure/ renegotiate borrowal accounts with retrospective effect.

3) Normally, restructuring cannot take place unless alteration/changes in the original loan agreement are made with the formal consent/ application of the borrower.

4) No account will be taken up for restructuring by the banks unless the financial viability is established and there is a reasonable certainty of repayment from the borrower, as per the terms of restructuring package.

5) Borrower classified as a willful defaulter / borrower indulging in frauds and malfeasance will continue to remain ineligible for restructuring. The restructuring of such cases may be done only with Board’s approval.

6) BIFR cases are not eligible for restructuring without their express approval.7) It may be noted that while the general principles norms inter-alia stipulate that

'standard' advances should be re-classified as 'sub-standard' immediately on restructuring, all borrowers (except consumer and personal advances, advances classified as capital market and real estate exposure) will be entitled to retain the asset classification upon restructuring, subject to the conditions as enumerated by Reserved Bank of India and advised by respective functionaries from time to time like “Incentive for quick implementation of the restructuring package” etc.

Baroda Academy Inventing Methods for Igniting Minds

34

8) However, extension in repayment tenor of a floating rate loan on reset of interest rate, so as to keep the EMI unchanged provided it is applied to a class of accounts uniformly will not render the account to be classified as ‘Restructured account’.

9) All restructured accounts which have been classified as non-performing assets upon restructuring, would be eligible for up-gradation to the ‘standard’ category after observation of ‘satisfactory performance’ during the ‘specified period’. Specified Period means a period of one year from the date when the first payment of interest or installment of principal falls due under the terms of restructuring package.

10)In case, however, satisfactory performance after the specified period is not evidenced, the asset classification of the restructured account would be governed as per the applicable prudential norms with reference to the pre restructuring payment schedule.

11)Any additional finance may be treated as ‘standard asset’, up to a period of one year after the first interest / principal payment, whichever is earlier, falls due under the approved restructuring package. If the restructured asset does not qualify for up gradation at the end of the above specified one year period, the additional finance shall be placed in the same asset classification category as the restructured debt.

12)In case a restructured asset, which is a standard asset on restructuring, if again subjected to restructuring on a subsequent occasion during period within which the concessions were extended under the terms of the first restructuring, it should be classified as substandard.

TEST OF UNDERSTADING

State whether following statements are true or false.

Restructuring can be done in advances accounts which have been classified as loss.

In case of Advance given to SME the standard account will shift to Substandard Category , after restructuring.

Standard Housing Loan account, if restructured , will go to sub standard

Category.

Additional advance given at the time of restructuring, will remain in in standard category for specific period.

Restructured account attracts additional provision of 2% even thoughit is in standard category.

Baroda Academy Inventing Methods for Igniting Minds

35