Embed Size (px)

Citation preview

Bonds

1AWAD RAHEEL

Bond Characteristics◦ Reading the financial pages

Interest Rates and Bond Prices Current Yield and Yield to Maturity Bond Rates and Returns Corporate Bonds and the Risk of Default

2AWAD RAHEEL

Terminology

Bond - Security that obligates the issuer to make specified payments to the bondholder.

Coupon - The interest payments made to the bondholder.

Face Value (Par Value or Principal Value) - Payment at the maturity of the bond.

Coupon Rate - Annual interest payment, as a percentage of face value.

3AWAD RAHEEL

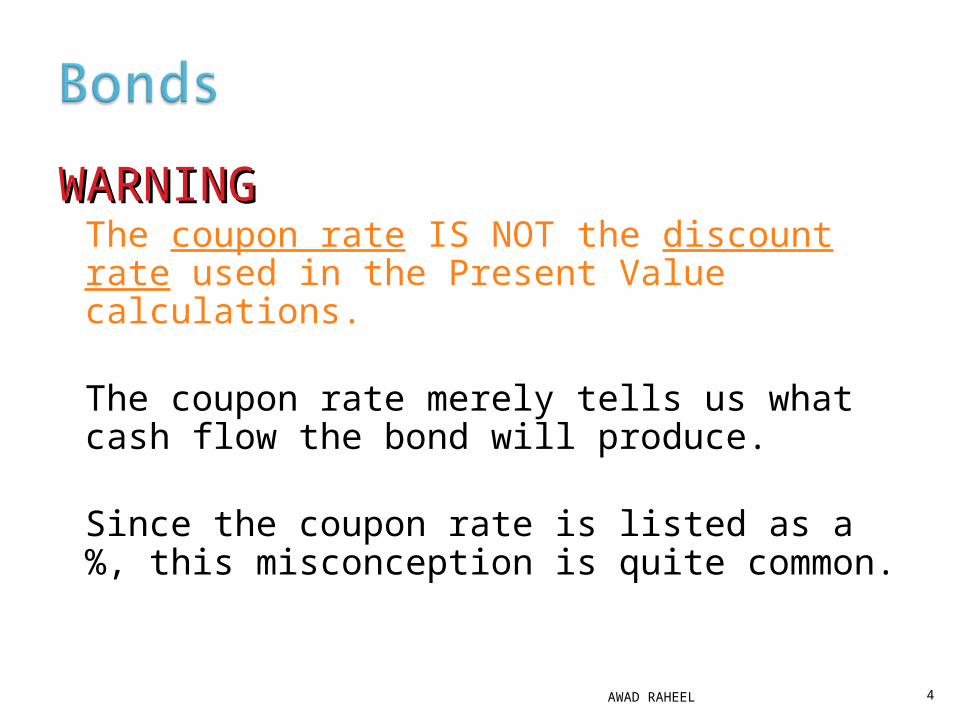

WARNINGWARNINGThe coupon rate IS NOT the discount rate used in the Present Value calculations.

The coupon rate merely tells us what cash flow the bond will produce.

Since the coupon rate is listed as a %, this misconception is quite common.

4AWAD RAHEEL

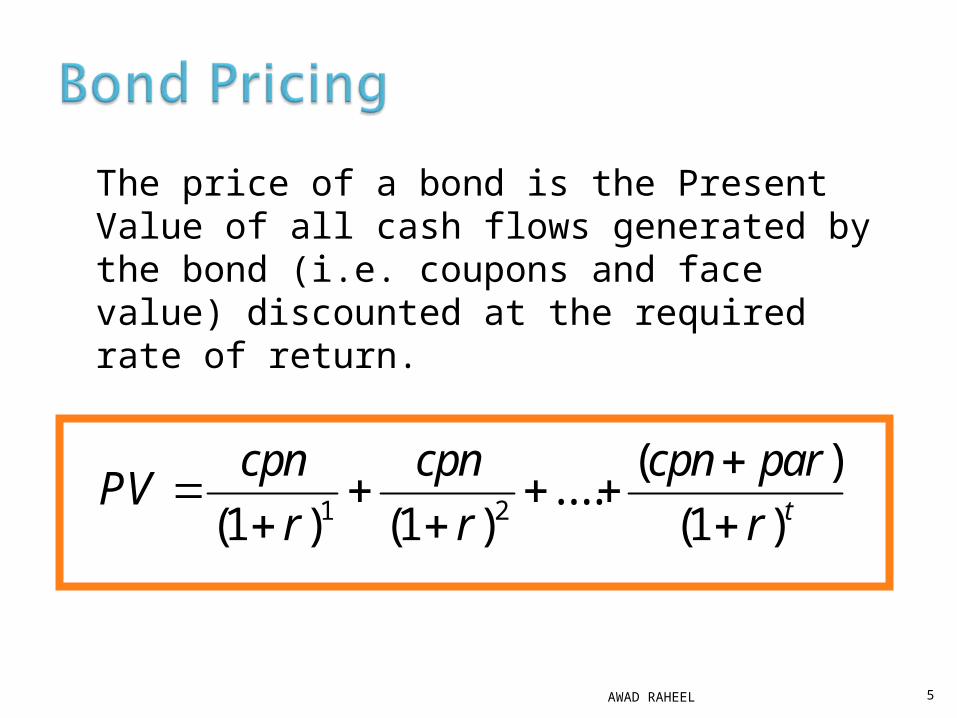

The price of a bond is the Present Value of all cash flows generated by the bond (i.e. coupons and face value) discounted at the required rate of return.

PVcpn

r

cpn

r

cpn par

r t

( ) ( )

....( )

( )1 1 11 2

5AWAD RAHEEL

ExampleWhat is the price of a 5.5 % annual coupon bond, with a Rs1,000 face value, which matures in 3 years? Assume a required return of 3.5%.

03.056,1

)035.1(

055,1

)035.1(

55

)035.1(

55321

RsPV

PV

6AWAD RAHEEL

7AWAD RAHEEL

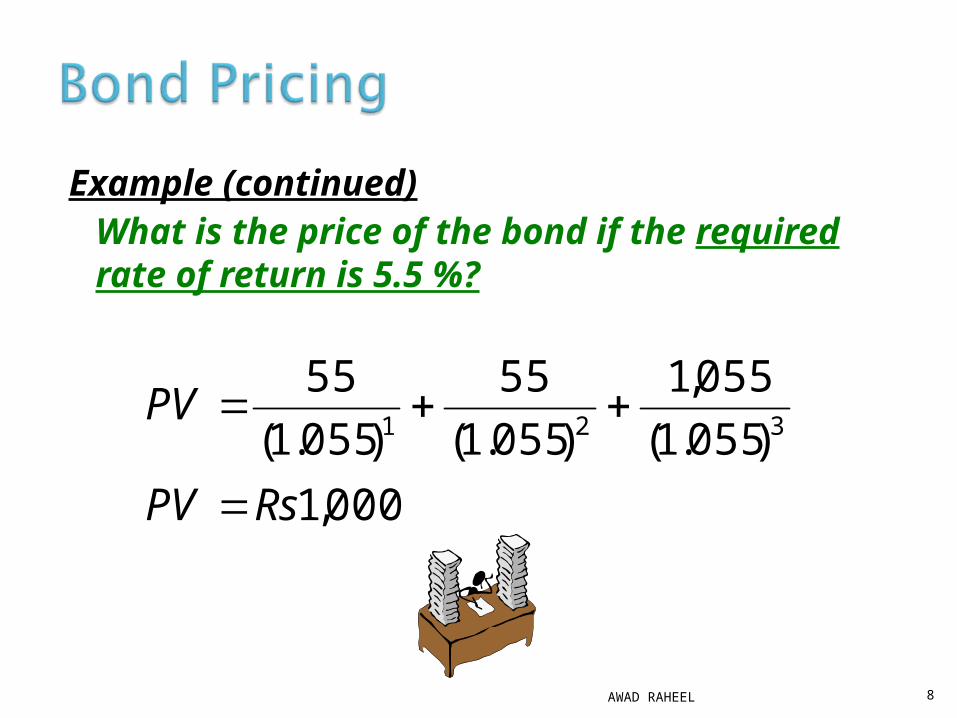

Example (continued)What is the price of the bond if the required rate of return is 5.5 %?

000,1

)055.1(

055,1

)055.1(

55

)055.1(

55321

RsPV

PV

8AWAD RAHEEL

Example (continued)What is the price of the bond if the required rate of return is 15 %?

09.783

)15.1(

055,1

)15.1(

55

)15.1(

55321

RsPV

PV

9AWAD RAHEEL

Example (continued)What is the price of the bond if the required rate of return is 3.5% AND the coupons are paid semi-annually for 3 years?

49.056,1

)0175.1(

50.027,1

)0175.1(

50.27...

)0175.1(

50.27

)0175.1(

50.276521

RsPV

PV

10AWAD RAHEEL

Example (continued)Q: How did the calculation change, given

semi-annual coupons versus annual coupon payments?

11AWAD RAHEEL

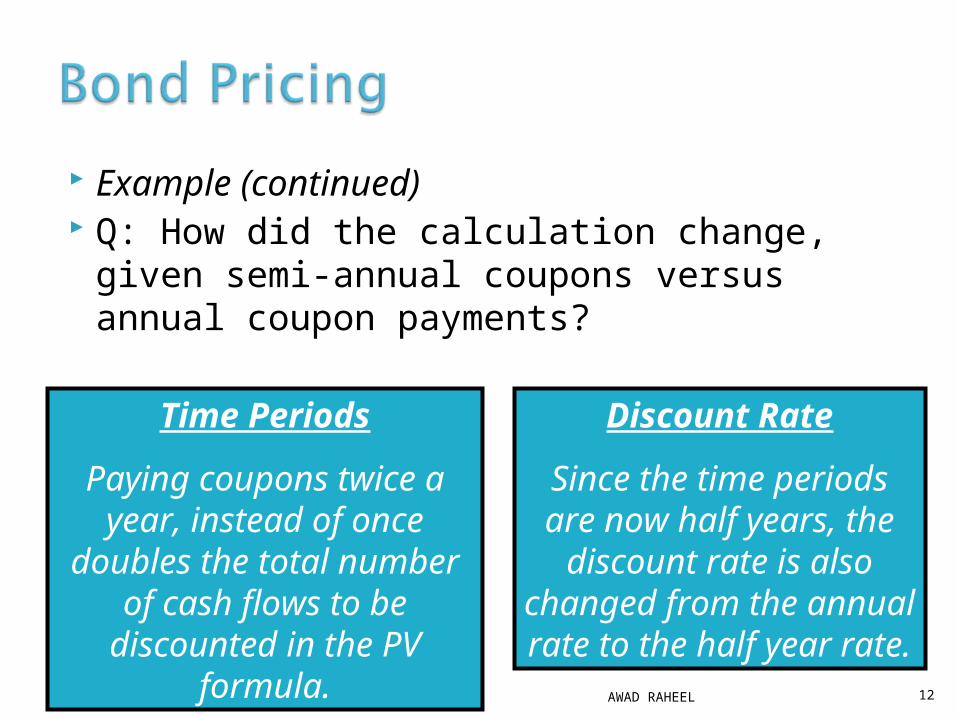

Example (continued) Q: How did the calculation change, given

semi-annual coupons versus annual coupon payments?

Time Periods

Paying coupons twice a year, instead of once doubles the

total number of cash flows to be discounted in the PV

formula.

Discount Rate

Since the time periods are now half years, the discount

rate is also changed from the annual rate to the half

year rate.12AWAD RAHEEL

Current Yield - Annual coupon payments divided by bond price.

Yield To Maturity – Interest/Discount rate for which the present value of the bond’s payments equal to its price.

13AWAD RAHEEL

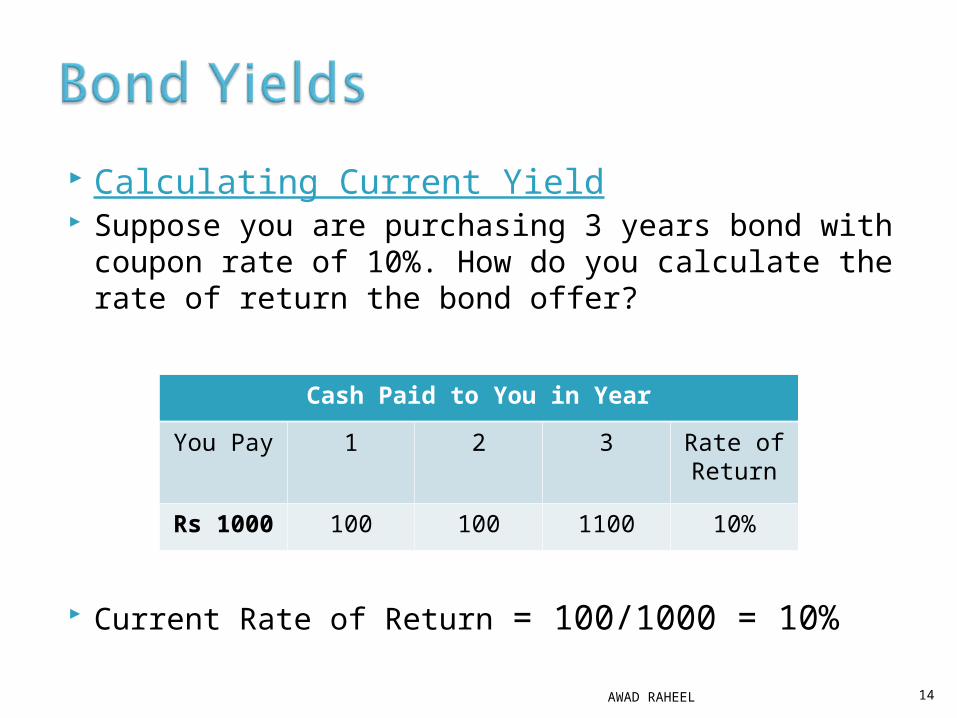

Calculating Current Yield Suppose you are purchasing 3 years bond with

coupon rate of 10%. How do you calculate the rate of return the bond offer?

Current Rate of Return = 100/1000 = 10%AWAD RAHEEL 14

Cash Paid to You in Year

You Pay 1 2 3 Rate of Return

Rs 1000 100 100 1100 10%

Now suppose that the market price of 3 years bond is Rs1136.16 with annual income of Rs100. What is the rate of return now?

So you pay 1136.16 and receive 100 annually. Income as proportion of initial outlay is 100/1136.16 = .088 = 8.8%

AWAD RAHEEL 15

Cash Paid to You in Year

You Pay 1 2 3 Rate of Return

Rs 1136.16

100 100 1100 ?

Problems due to current yield rates

AWAD RAHEEL 16

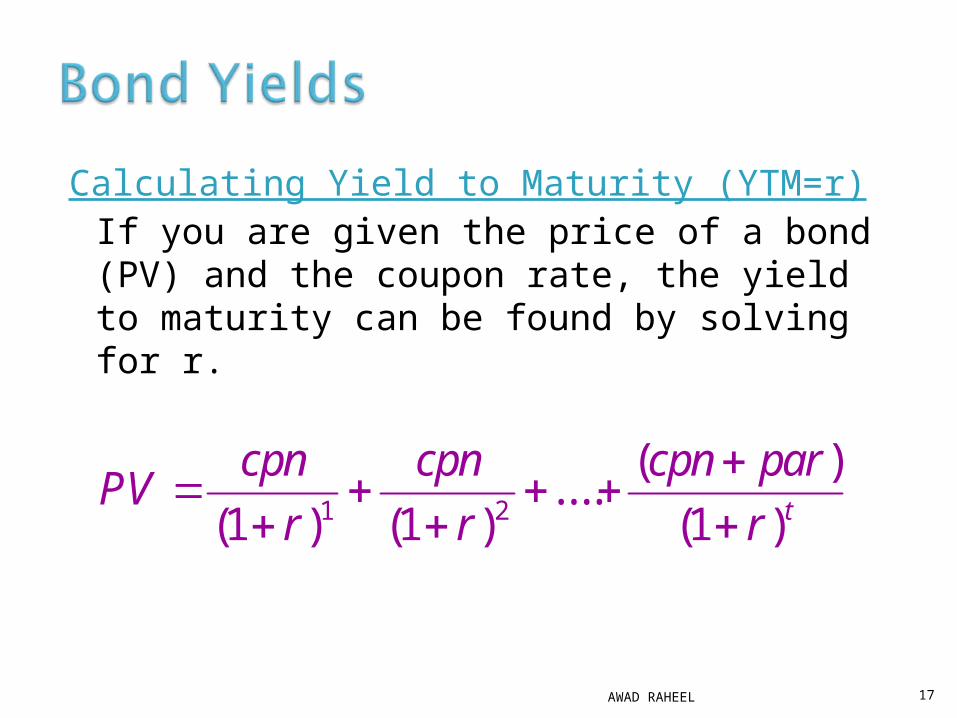

Calculating Yield to Maturity (YTM=r)If you are given the price of a bond (PV) and the coupon rate, the yield to maturity can be found by solving for r.

PVcpn

r

cpn

r

cpn par

r t

( ) ( )

....( )

( )1 1 11 2

17AWAD RAHEEL

ExampleWhat is the YTM of a 5.5 % annual coupon bond, with a Rs1,000 face value, which matures in 3 years? The market price of the bond is Rs1,056.03.

03.056,1

)1(

055,1

)1(

55

)1(

55321

RsPV

rrrPV

18AWAD RAHEEL

WARNINGWARNINGCalculating YTM by hand can be very tedious.

It is highly recommended that you learn to use the “IRR” or “YTM” or “i” functions on a financial calculator.

19AWAD RAHEEL

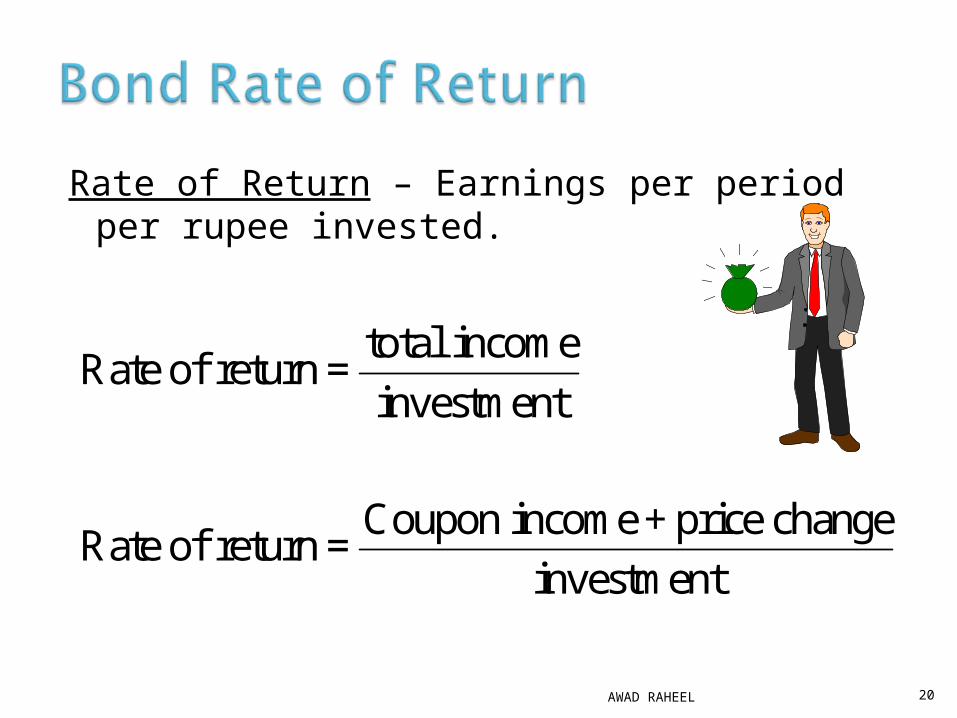

Rate of Return – Earnings per period per rupee invested.

Rate of return =total income

investment

Rate of return =Coupon income + price change

investment

20AWAD RAHEEL

880

900

920

940

960

980

1,000

1,020

1,040

1,060

1,080

0 5 10 15 20 25 30

Bo

nd

Pri

ce

Time to Maturity

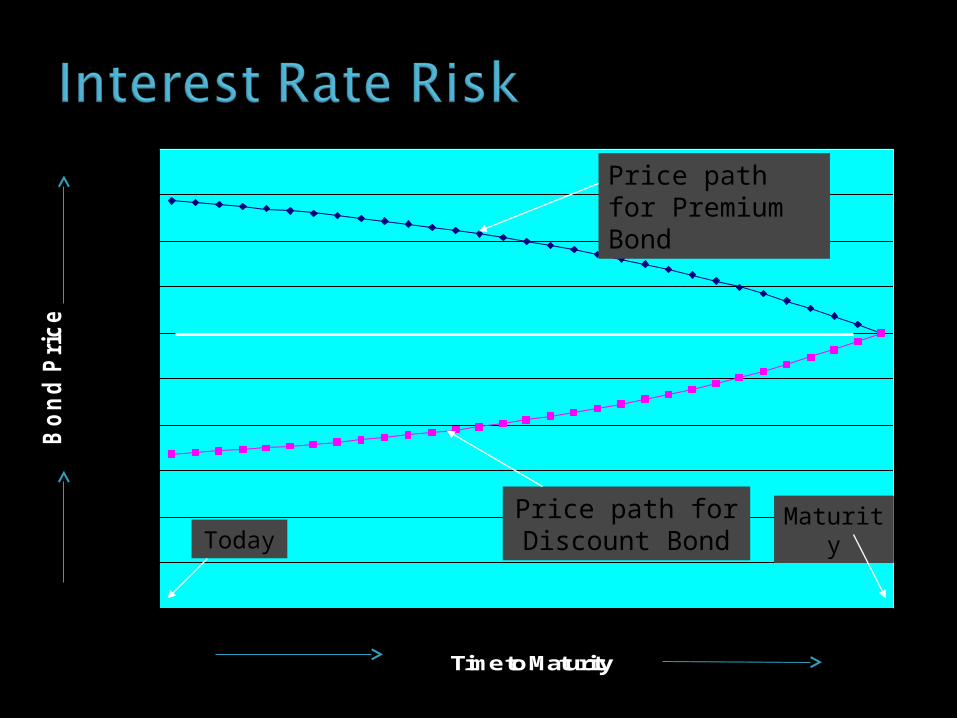

Price path for Premium Bond

Price path for Discount BondToday

Maturity

23AWAD RAHEEL

0

600

1000

1500

30

Bond shows interest rate risk as its price fluctuate with interest rate change.

Do all bonds get effected equally? Long term bonds are more sensitive to interest

rate than prices of short term bonds.

AWAD RAHEEL 24

-

500

1,000

1,500

2,000

2,500

3,000

0 2 4 6 8 10

YTM

$ B

on

d P

ric

e

30 yr bond

3 yr bond

When the interest rate equals the 5.5% coupon rate, both

bonds sell at face value

25AWAD RAHEEL

Interest Rate (%)

Bon

d pr

ice

0

Bonds are also available with real interest rates.

If nominal rate is 3.5% and inflation rate is 2%, then real interest rate will be:

Real interest rate = 1.035 -1 =.0147 = 1.47% 1.02

As inflation rate is uncertain, so is real interest rate.

AWAD RAHEEL 26

1 real interest rate = 1+nominal interest rate1+inflation rate

In inflation indexed bonds real cash flows are fixed while nominal cash flows (interest and principal) are changed as CPI changes.

e.g. Real cash flow of 2 years indexed bonds at 3% would be:

Now suppose that inflation turns out to be 5% in year 1 and 4% in year 2. then nominal cash flow would be:

Here cash payments are justified to give 3% real interest rate

AWAD RAHEEL 27

Year 1 Year 2

Real Cash Flow

Rs 30 Rs 1030

Year 1 Year 2

Nominal Cash Flow

Rs 30x1.05=Rs 31.50

Rs 1030x1.05x1.04 =Rs 1124.76

0

2

4

6

8

10

12

14

Perc

en

t

Year

Yield on UK nominal bonds

Yield on UK indexed bonds

28AWAD RAHEEL

Like governments, corporate also borrow money by selling bonds.

Credit risk – The risk that bond issuer may default on its bonds.

Default premium – The additional yield on a bond investor require for bearing credit risk.

Investment grade – Bonds rated BBB and above. (1% default rate of AAA since 1971)

Junk bonds – Bonds having grade less than BBB (about 50% bonds rated CCC by S&P defaulted within 10 yrs)

29AWAD RAHEEL

StandardMoody' s & Poor's Safety

Aaa AAA The strongest rating; ability to repay interest and principalis very strong.

Aa AA Very strong likelihood that interest and principal will berepaid

A A Strong ability to repay, but some vulnerability to changes incircumstances

Baa BBB Adequate capacity to repay; more vulnerability to changesin economic circumstances

Ba BB Considerable uncertainty about ability to repay.B B Likelihood of interest and principal payments over

sustained periods is questionable.Caa CCC Bonds in the Caa/CCC and Ca/CC classes may already beCa CC in default or in danger of imminent defaultC C C-rated bonds offer little prospect for interest or principal

on the debt ever to be repaid.30AWAD RAHEEL

Zero coupons◦ No coupon offered and receive face value of bond

at maturity date. Floating rate bonds

◦ Rate can be pegged to some measure of current market e.g. T Bills plus 2%

Convertible bonds◦ Option to convert into shares latter.◦ Investor accept lower interest rates on convertible

bonds.

31AWAD RAHEEL

Innovations are always in process for bonds e.g.

Catastrophe (or cat) bonds:◦ Offer high return but reduced when specific type of

disaster occurs. Longevity bonds:

◦ Bond payments get higher if more population survived extra year.

◦ Pension funds are common buyer of these bonds as they have to pay extra if life expectancy increases.

AWAD RAHEEL 32