Embed Size (px)

Citation preview

Bond Liquidity and Investment

Laura Casares Fielda, Anahit Mkrtchyanb, Yuan Wangc * aSmeal College of Business, Pennsylvania State University, University Park, PA 16802, USA

bD’Amore-McKim School of Business, Northeastern University, Boston, MA 02115, USA cJohn Molson School of Business, Concordia University, Montreal, QC H3G 1M8, Canada

December 1, 2014

Abstract This paper examines the effect of bond liquidity on investment decisions. We find that firms with higher bond liquidity are more likely to make acquisitions and have higher capital expenditures. We exploit an exogenous shock to bond liquidity – introduction of TRACE, and show that increases in bond liquidity around TRACE implementation expands firms' investment. Our results support the hypothesis that bond liquidity relaxes firms' financial constraints and has a real effect on the firms’ investment decisions. Furthermore, we find that bond liquidity leads to higher firm valuations, through lower discount rate and higher operating profitability. Keywords: Mergers and Acquisitions, Liquidity JEL Classification Numbers: G34, G32 * E-mail addresses: [email protected] (Field); [email protected] (Mkrtchyan); [email protected] (Wang)

Bond Liquidity and Investment

December 1, 2014

Abstract This paper examines the effect of bond liquidity on investment decisions. We find that firms with higher bond liquidity are more likely to make acquisitions and have higher capital expenditures. We exploit an exogenous shock to bond liquidity – introduction of TRACE, and show that increases in bond liquidity around TRACE implementation expands firms' investment. Our results support the hypothesis that bond liquidity relaxes firms' financial constraints and has a real effect on the firms’ investment decisions. Furthermore, we find that bond liquidity leads to higher firm valuations, through lower discount rate and higher operating profitability. Keywords: Mergers and Acquisitions, Liquidity JEL Classification Numbers: G34, G32

1

1. Introduction

Whereas credit risk is an important component of the cost of debt, recent research has

shown the significance of debt liquidity, i.e. the frictions in bonds’ trading environment, as

another determinant of the cost of debt. For any given level of credit risk, more illiquid securities

have lower price or higher cost, as investors demand compensation for expected trading

difficulty. 1 For example, Bao, Pan and Wang (2011) find that illiquidity is by far the most

important factor in explaining the changes in the U.S. aggregate yield spreads of investment

grade bonds. Furthermore, they show that for the bonds with the same rating category, one

standard deviation increase in illiquidity leads to an increase in yield spreads as large as 65 bps.

In addition to its' direct effect on cost of debt, liquidity deterioration in the secondary market also

impacts firms’ credit risk by reducing debt value in renegotiation during financial distress or by

increasing rollover losses from issuing new bonds (He and Xiong (2012), Ericsson and Renault

(2006)).

The idea that supply frictions can impact a firm’s investment patterns has been the

subject of a number of recent papers (e.g., Lemmon and Roberts (2010), Morellec (2010)). In

this paper, we examine whether bond liquidity has an impact on a firm’s investment decisions.

Our focus is on acquisitions, which represent the most visible and large investments firms

undertake. A growing body of M&A research has provided evidence of the important role debt

plays in acquisitions.2 For instance, Harford and Uysal (2013) find that firms’ access to debt

markets increases the likelihood of undertaking acquisitions by comparing firms with and

1 Amihud and Mendelson (1986, 1988), Chen, Lesmond, and Wei (2007), and Dick-Nielsen, Feldhütter and Lando (2012). 2 See also Bharadwaj and Shivdasani (2003); Faccio and Masulis (2005), Harford, Klasa and Walcott (2009) and Uysal (2011)).

2

without credit rating. Karampatsasa, Petmezasa, and Travlos (2014) find that firms with higher

ratings (i.e. lower credit risk) are more likely to use cash financing in a takeover.

Bidders with higher bond liquidity face relatively better opportunities to borrow due to

lower cost and higher demand for their bonds. Lower cost of debt allows firms to borrow more

and therefore expand their investment. We hypothesize that firms with higher bond liquidity will

be more likely to undertake acquisitions, as liquidity reduces cost of debt and potential

acquisitions are discounted at a lower rate. Consistent with this idea, we find that firms with

higher bond liquidity make more acquisitions after controlling for the credit risk. For example,

one standard deviation increase in bond liquidity leads to 8.1% increase in the likelihood of

acquisitions, compared to 1.95% increase for one standard deviation increase in stock liquidity.

This result is robust to the use of different measures of liquidity and alternative model

specifications. We similarly find that bond liquidity is positively associated with increased

capital investment, another proxy for an expanded firm investment.

We then proceed to address the endogeneity of the relationship between bond liquidity

and firm acquisitiveness. A potential concern of our analysis is that firms might issue debt in

anticipation of an acquisition (e.g. Edwards, Harris, Piwowar (2007)). Since recently issued

bonds tend to be more liquid, the relationship between bond liquidity and acquisition likelihood

can be affected by a reverse causality. We address this possibility by dropping firms that have

issued debt in a year prior to acquisition and by using a lagged liquidity measure. The

relationship between bond liquidity and probability of making an acquisition remains positive

and significant. Alternatively, the relationship between bond liquidity and a firm’s acquisition

activity might be spurious and driven by omitted factors. To address this issue we rely on a two-

stage regression model, using an industry median liquidity measure as our instrument, and we

3

obtain very similar results. Lastly, we examine the effect of an exogenous shock to liquidity

(TRACE introduction) to isolate the impact of bond liquidity on the likelihood of making an

acquisition. Exploiting the variation generated by the staggered introduction of TRACE, we

continue to find that higher bond liquidity leads to an expanded investment.

Next, we examine the channel through which bond liquidity affects firms' investments.

We hypothesize that through relaxing financial constraints that firms face, bond liquidity leads to

a greater investment, as investors are willing to provide financing to firms with more liquid

bonds at a lower cost. We study whether the effect of bond liquidity differs for firms with

varying degree of financial constraints. If firms do not need much additional financing, either

because they hold enough cash or because they have easier access to equity markets, then bond

liquidity will not have a big impact. Conversely, firms that are more financially constrained will

benefit more from the liquidity premium, as it makes it easier for them to obtain external

financing. Consistent with this notion, we find that the positive effect of liquidly is stronger for

firms that are more financially constrained, i.e., younger firms and firms with a lower debt rating.

If bond liquidity relaxes financial constraints and increases firms' resources, it can help

firms undertake positive NPV investments which otherwise would be foregone and, therefore,

increase firm valuations. In fact, we find that higher bond liquidity is associated with higher

market valuations. To understand better the effect of bond liquidity on market-to-book ratios, we

decompose market-to-book ratio into: price-to-earnings, equity-to-assets, and earnings-to-assets

ratios, similar to Fang et al. (2009). We find that higher bond liquidity is associated with a higher

price-to-earnings ratio, providing support for the liquidity premium, i.e. the effect of lower

discount rate. Furthermore, we find that firms with higher bond liquidity have higher operating

profitability, suggesting that improvement in bond liquidity allows firms to make good

4

investments which otherwise wouldn’t be undertaken. We perform a number of robustness tests

to ensure that the relationship between bond liquidity and market valuations is not endogenous.

First, we perform firm fixed analysis, which helps control for time-invariant firm characteristics.

Next, we perform two-stage least squares estimation. Last, we use the introduction of TRACE as

an exogenous shock to liquidity and continue to find the positive effect of bond liquidity on firm

value.

This article contributes to an emerging body of empirical literature that examines the

links between corporate finance and the market microstructure of a firm’s bonds. Prior literature

provides ample evidence on the relation between stock liquidity and corporate policies (e.g.

dividends pay-out, debt policy, innovation, governance, CEO pay, acquisitions). Debt is a

principal source of external financing for U.S. firms, however, there is little evidence on the

impact of bond liquidity on corporate events. We contribute to this literature by providing insight

into how frictions in bonds’ trading environment affect a firm’s acquisition activity and firm

valuations.

Our paper similarly adds to the studies linking leverage and access to debt to a firm’s

ability to make acquisitions (Harford and Uysal (2014), Almazan, de Motta, Titman, and Uysal

(2010), Uysal (2011)). We show that bond liquidity is an important determinant of a firm’s

investment even after controlling for leverage and credit ratings.

This paper is also related to the work by Fang et al. (2009) who show a positive effect of

stock liquidity on firm value. We complement their findings by showing that bond liquidity has a

significant impact on market valuations, after controlling for stock liquidity. Fang et al. (2009)

find that higher market-to-book ratios of firms with higher stock liquidity cannot be explained by

a lower discount rate. In contrast, we document that in case of bond liquidity: liquidity has an

5

impact on firm value, not only through increased profitability, but also through the discount rate

effect, which can be explained by the fact that liquidity premium is much larger in bonds than in

stocks.

The remainder of this paper is organized as follows: Section 2 provides descriptive

statistics of the sample and describes our measure of bond liquidity. Section 3 presents empirical

evidence on the relationship between bond’s liquidity, firms’ investment activity and market

valuations. Section 4 concludes.

2. Sample Selection, Variable Measurement and Descriptive Statistics

2.1. Sample

We obtain price and trading data for corporate bonds from Financial Industry Regulatory

Agency’s (FINRA’s) Transaction Reporting and Compliance Engine (TRACE) and ratings and

bond-specific characteristic information from the Fixed Investment Securities Database (FISD).

In January 2001, the Securities and Exchange Commission approved rules requiring the

FINRA (previously National Association of Security Dealers) to report all over-the-counter

corporate bond transactions through TRACE. On July 1, 2002, TRACE began to report bond

transactions, requiring that transaction information be disseminated for investment grade

securities with an initial issue size of $1 billion or greater. TRACE was expanded in stages and

was fully implemented by January 2006, covering essentially all publicly traded bonds. There

appear to be a number of problematic trades during the early period of the database.

Consequently, we eliminate canceled, corrected, and commission trades from the data. Bond

transactions under $100,000 are deleted to avoid the effects of retail investors. We also remove

bonds with time to maturity less than one year because of high pricing errors.

6

The FISD reports detailed information about corporate, U.S. Agency, U.S. Treasury, and

supranational debt securities, including information about issue- and issuer-specific information

such as coupon rate, maturity, issue amount, provisions, and credit ratings for all US corporate

bonds maturing in 1989 or later. We merge the two databases to create a panel of bond

transactions and characteristics.

In order to obtain a firm-level bond liquidity measure in the secondary market, we first

calculate the daily bond-level liquidity using high-frequency transaction data. Next, we calculate

monthly liquidity as the median of the daily bond-level liquidity measures. Lastly, we average

the monthly measures over a fiscal year to construct annualized bond-level liquidity metric. We

aggregate bond-level metrics to the firm-level bond liquidity measure by calculating the offering-

amount weighted average of annual bond-level liquidity. We winsorize the liquidity metric at

1%, so that values above the 99% percentile are set to the 99% percentile and values below the

1% percentile are set to the 1% percentile.

We merge annual firm-level bond data with Center for Research in Security Prices

(CRSP) database and Compustat Industrial Annual Files to obtain stock prices and accounting

information. We obtain 6,664 firm-year observations between 2002 and 2011 for 1,227 firms. To

examine the relationship between bond liquidity and the likelihood of undertaking an acquisition,

for each firm in the sample, we obtain all of its completed domestic acquisitions listed in

Thomson One’s Mergers and Acquisitions database. The sample includes acquisitions of private,

public and subsidiary targets and excludes buybacks, recapitalizations and exchange offers.

Consistent with prior studies, we require that the acquirer obtains at least 51% of the target

shares and that acquisitions represent at least 1% of the acquirer’s market value, measured at the

7

fiscal year end before the announcement. 3 Our sample of acquisitions consists of 954

acquisitions completed by 517 firms.

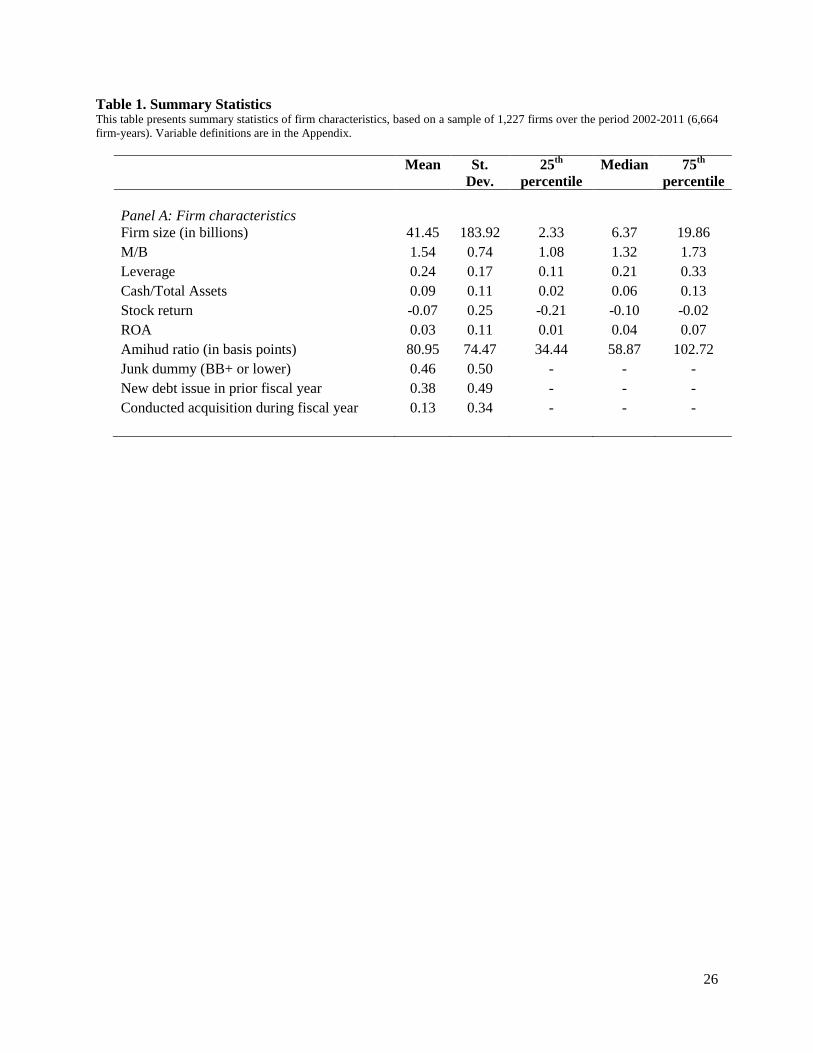

Table 1 reports the descriptive statistics of firms in the sample. Sample firms are quite

large, for example, the median book value of total assets is $6.37 billion. The median firm has a

market-to-book ratio of 1.3, and leverage of 21%. Forty-six percent of our firms have S&P

rating of BB+ or below. The unconditional likelihood of making an acquisition is 13.3%.

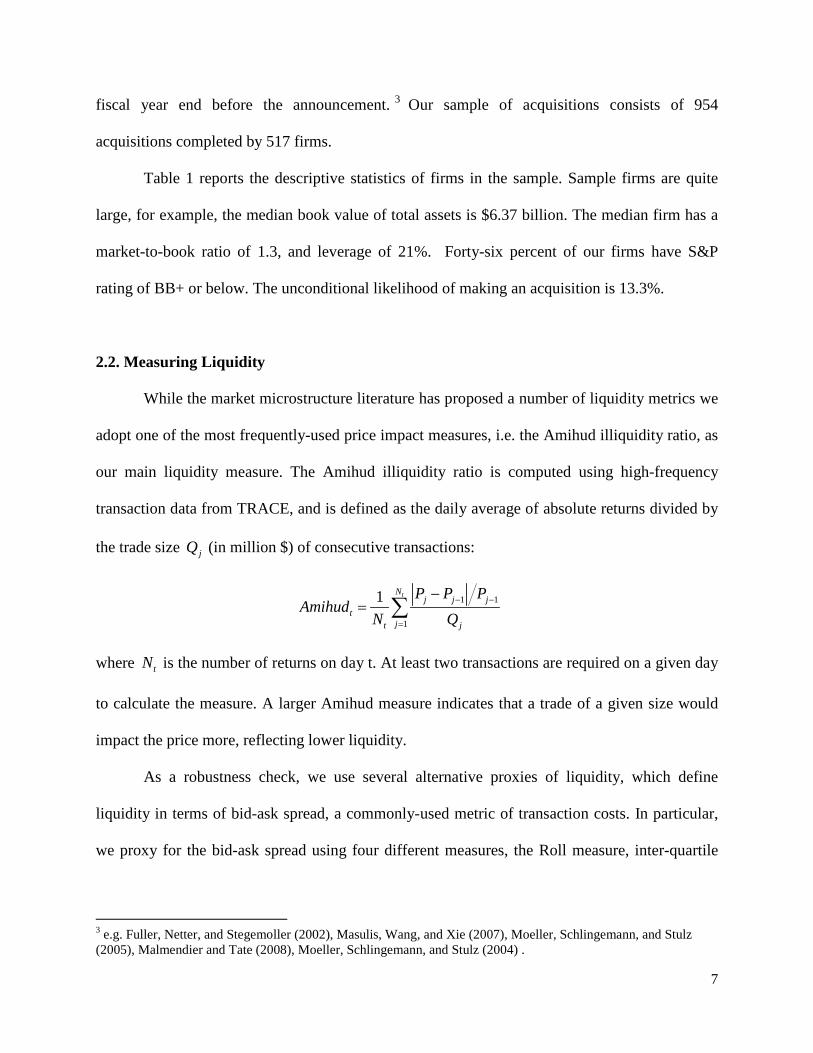

2.2. Measuring Liquidity

While the market microstructure literature has proposed a number of liquidity metrics we

adopt one of the most frequently-used price impact measures, i.e. the Amihud illiquidity ratio, as

our main liquidity measure. The Amihud illiquidity ratio is computed using high-frequency

transaction data from TRACE, and is defined as the daily average of absolute returns divided by

the trade size jQ (in million $) of consecutive transactions:

1 1

1

1 tNj j j

tjt j

P P PAmihud

N Q− −

=

−= ∑

where tN is the number of returns on day t. At least two transactions are required on a given day

to calculate the measure. A larger Amihud measure indicates that a trade of a given size would

impact the price more, reflecting lower liquidity.

As a robustness check, we use several alternative proxies of liquidity, which define

liquidity in terms of bid-ask spread, a commonly-used metric of transaction costs. In particular,

we proxy for the bid-ask spread using four different measures, the Roll measure, inter-quartile

3 e.g. Fuller, Netter, and Stegemoller (2002), Masulis, Wang, and Xie (2007), Moeller, Schlingemann, and Stulz (2005), Malmendier and Tate (2008), Moeller, Schlingemann, and Stulz (2004) .

8

range (IQR), Range, and imputed roundtrip trades. Similar to the Amihud measure, larger values

of these metrics imply lower liquidity. Appendix A describes the measures in more detail.

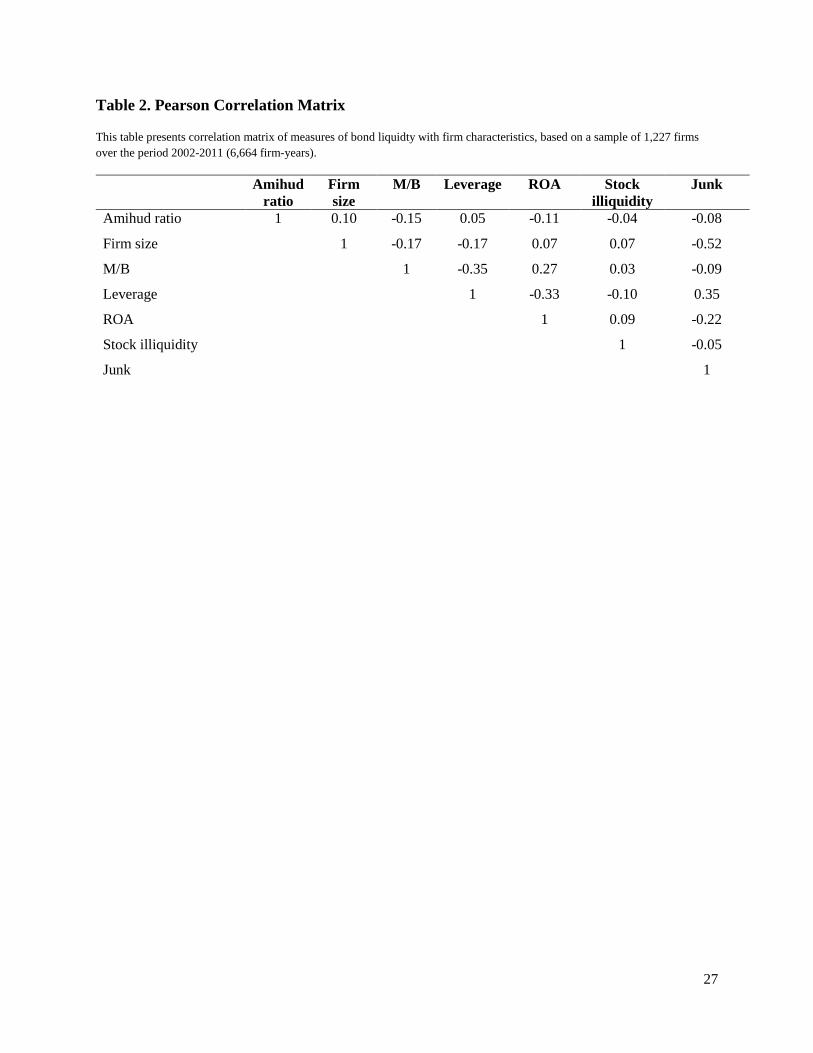

The Pearson correlation matrix in Table 2 shows that Amihud illiquidity ratio is

positively correlated with firm size and leverage, suggesting that larger and more levered firms

have less liquid bonds. Firms with higher market-to-book ratios, higher ROA, and non-

investment grade bonds have bonds with greater liquidity. Whereas all of the correlations are

statistically significant, none of them is particularly high.

3. Results

3.1. Probability of Making Acquisitions

Prior studies indicate that share issues typically account for less than 5% of total new

external finance (e.g. Fazzari et al. 1988a, 1988b, 1988c). Not surprisingly, most acquisitions

involve cash either as a sole component of consideration or in combination with stock. In our

sample, only seven percent of the acquisitions are financed by stock only. A growing body of

studies has provided evidence that cash-financed acquisitions are to a great extent funded by debt

(see, e.g., Bharadwaj and Shivdasani (2003); Faccio and Masulis (2005), Harford, Klasa and

Walcott (2009) and Uysal (2011)). Since debt is the primary marginal source of external funds,

the capital structure decision has been proved to be of great importance in the corporate

financing decision of merger and acquisition (M&As). While prior literature has studied the

impact of leverage and access to credit market on acquisitions, in this paper we study how

another aspect of corporate debt, i.e. liquidity of the firm’s bonds affect a firm’s takeover

decisions.

9

Prior literature has documented a significant effect of liquidity on asset prices and shows

that part of the yield spread differences across bonds is due to illiquidity (e.g., survey by

Amihud, Mendelson, and Pedersen (2005)). Because trading in the US corporate bond market

involves much higher transaction costs compared to the stock market the liquidity premium in

the bond market is significant (Amihud and Mendelson (1986)). For example, Bao et al. (2011)

find that illiquidity is by far the most important factor in explaining the changes in the U.S.

aggregate yield spreads of investment grade bonds, with an R-squared ranging from 47% to 60%.

Bao et al. (2011) further show that for two bonds in the same rating category, a one standard

deviation difference in their bond illiquidity leads to a difference in their yield spreads as large as

65 bps. In addition to a direct effect on bond spreads bond liquidity can also affect a firm’s credit

risk. Ericsson and Renault (2006) find positive correlation between the illiquidity and default

components of yield spreads, and show that the illiquidity of the market for distressed debt

increases a firm’s credit risk by reducing debt value in renegotiation during financial distress. He

and Xiong (2012) show that illiquidity increases the rollover losses from issuing new bonds and

leads to an increase in the cost of debt.

Whereas prior literature has documented the importance of bond liquidity in explaining

yield spreads, in this paper we examine whether bond liquidity is significant enough to influence

a firm’s investment decisions. Bond liquidity lowers the expected return investors require to hold

debt securities therefore it decreases the cost of capital by lowering the cost of debt. When the

cost of capital is low, the value of the potential synergies is high, as the discount rate used to

evaluate potential bids is lower. Furthermore, higher liquidity of a firm’s bonds might allow

firms to issue funds at a short notice and according to their investment needs. Because debt is an

important source of funding in acquisitions, bond liquidity might have a significant impact on the

10

decision to acquire. Therefore, we argue that lower cost of debt, due to higher bond liquidity,

allows firms to borrow more and expand their investment.

Table 3 presents univariate analysis of the relationship between bond liquidity and

probability of acquisition. We classify firms into firms with high and low bond liquidity, based

on the Amihud ratio. Firms are classified as having low liquidity if the Amihud ratio is above the

median, otherwise firms are classified as having high liquidity. As can be seen from Table 2 the

unconditional probability of making an acquisition is 12.7% for firms with high liquidity and it is

only 7.4% for firms with low liquidity. The difference of 5.3%, which is significant at 1%,

represents 37.7% relative to the mean unconditional probability of being an acquirer (13.3%).

During the earlier part of the sample TRACE only captures firms with the largest, highest

rated bonds. Hence, the early and later time periods of our study include different types of firms,

thus we separate our sample period into two periods, one that captures the introduction of

TRACE from 2002 to 2006 and the later, post-TRACE period from 2007 to 2011. We continue

to find that firms with higher bond liquidity make more acquisitions during both sub-periods.

Next, we examine whether this result is driven by such firm characteristics as firm size or

stock liquidity. We split our sample into size terciles and find that firms with higher bond

liquidity continue to have higher acquisition frequencies relative to lower liquidity firms in all

sub-samples. The effect of liquidity is the largest among the smallest firms, which suggests that

bond liquidity is more important for firms that might be financially more constrained, a notion

that we explore further in Section 3.4. Table 3 further shows bond liquidity is associated with

higher acquisition frequencies for firms with high and low stock liquidity.

To alleviate a concern that the effect of bond liquidity on the likelihood of making an

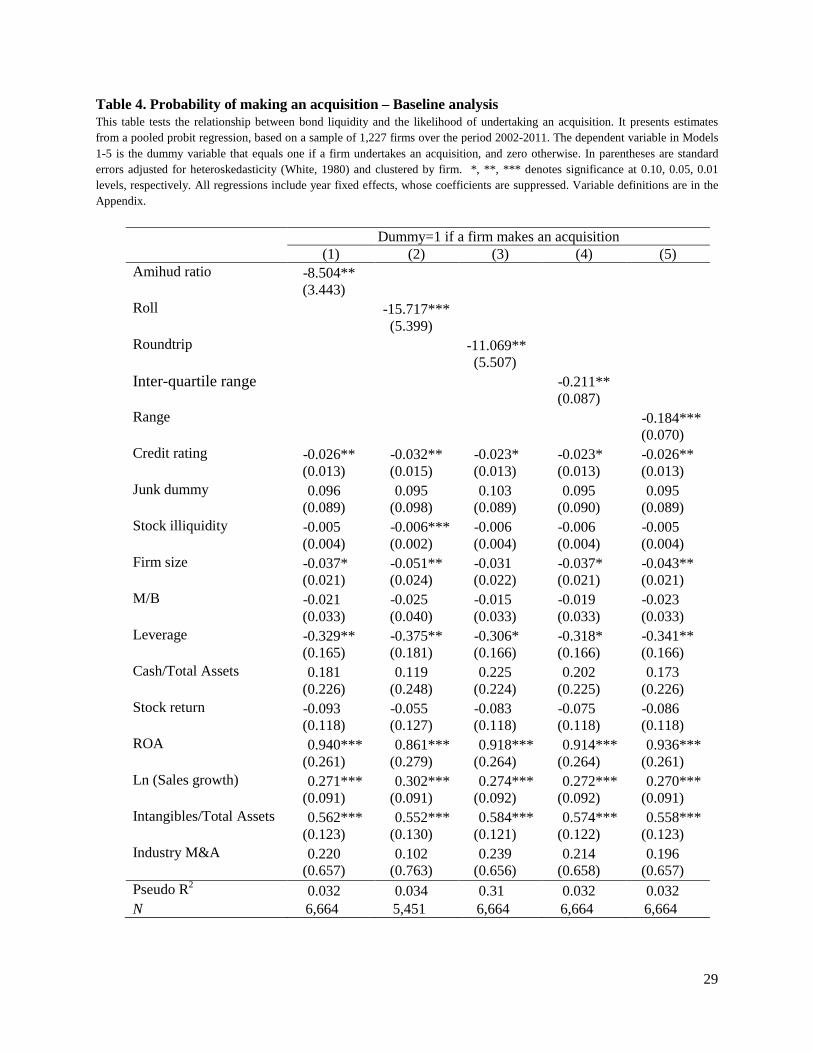

acquisition is driven by firm characteristics, we turn to multivariate analysis. Table 4 presents the

11

results of the probit regression, in which the dependent variable is a dummy variable that equals

one if a firm undertakes at least one acquisition in a given year. We control for several factors

that may potentially affect the likelihood of making an acquisition, by including firm size,

market-to-book ratio, leverage, cash, return on assets ratio, abnormal stock return, sales growth,

intangible assets, scaled by sales, and stock illiquidity, measured by Amihud ratio. Furthermore,

we include a measure of recent mergers and acquisition activity (Industry M&A) and control for

credit rating (based on S&P credit rating), using a conversion process in which AAA-rated bonds

are assigned a value of 1 and C-rated bonds receive a value of 21. To control for the non-

linearity in credit rating we include a non-investment grade dummy which equals one for firms

with a credit rating BB+ or lower.4 We also control for calendar year fixed effects to account for

macroeconomic changes during the sample period and we cluster standard errors at a firm level.5

Consistent with prior literature, we find that better performing firms, as measured by

return on assets, are more likely to undertake acquisitions, whereas excess leverage impairs a

firm’s ability to undertake acquisitions (Asquith, Bruner, and Mullins (1983), Roll (1986),

Harford (1999), Almazan et al. (2010)). Turning to our variable of interest, we find that the

coefficient on the Amihud iliquidity ratio is negative and statistically significant at 1% level. As

higher value of liquidity measures indicates lower bond liquidity, the negative coefficient implies

that firms with higher bond liquidity are more likely to make acquisitions, consistent with our

hypothesis that bond liquidity is positively associated with increase in investment. The effect on

the acquisition likelihood is also economically meaningful. One standard deviation increase in

bond liquidity leads to a 8.1% increase in the likelihood of acquisitions, which is comparable to a

9.0% increase for a one standard deviation increase in credit rating. At the same time, one

4 Our results are robust, if use credit rating dummies instead. 5 As a robustness, we re-estimate p-values based on clustering by firm and time (year), following Petersen (2009). The results remain very similar.

12

standard deviation increase in stock liquidity leads to only a 1.9% increase in the likelihood of an

acquisition. A greater effect of bond liquidity and credit risk relative to stock liquidity is not

surprising, given the relative importance of debt in acquisitions.

To ensure that our finding is not impacted by the way we measure bond liquidity, in

Models 2-5 of Table 4, we employ four alternative measures of bond liquidity and continue to

find a strong positive relationship between bond liquidity and a firm’s decision to undertake an

acquisition. For brevity purposes our later tables only report the results based on the Amihud

ratio, however, our results are robust to the alternative liquidity measures. The results in Table 4

show that bond liquidity has an economically significant effect on a firm’s investments even

after controlling for firm size, leverage and credit ratings.

For robustness, we use alternative model specifications. Specifically, we estimate a

Poisson model with the annual acquisition count as the dependent variable, and a Tobit

regression, in which the dependent variable is the total size of all targets acquired in a year,

scaled by the firm’s market value of equity. The results are robust to these alternative model

specifications (untabulated). Additionally, we conduct probit analyses for the sub-samples of size

to alleviate the concern that our findings are driven by firm size. Similar to the univariate results,

we continue to find the positive effect of bond liquidity on the probability of making acquisitions

across all sub-samples (untabulated).

In the next section we examine the relationship between bond liquidity and the likelihood

of making acquisitions more carefully to alleviate potential endogeneity concerns.

13

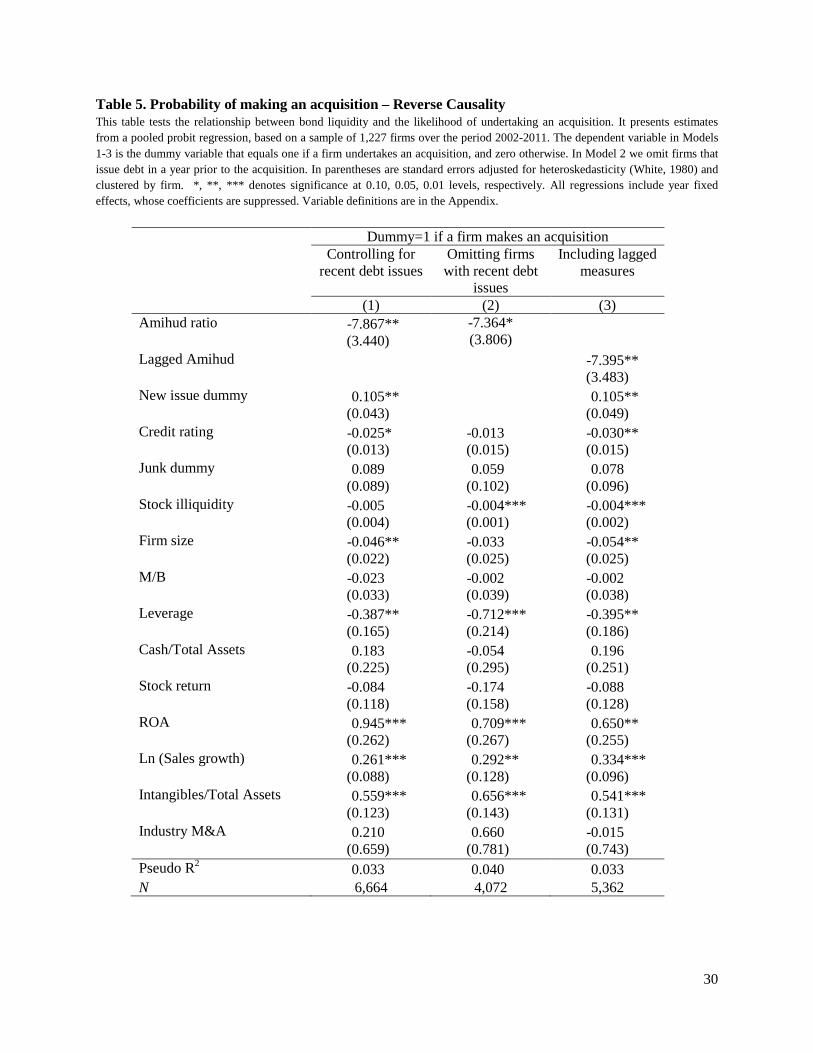

3.2. Endogeneity concerns

3.2.1. Reverse causality

It is possible that firms planning to undertake acquisitions might raise debt shortly prior

to undertaking an acquisition. In fact, 42% of firms undertaking acquisitions issue debt in a year

prior to an acquisition, compared to 37% of firms not making acquisitions. As recently issued

bonds tend to be more liquid (e.g. Edwards, Harris, Piwowar (2007)), the relationship between

bond liquidity and acquisition likelihood can be affected by reverse causality. It is worth nothing,

that even though some firms increase bond liquidity by issuing new bonds prior to an acquisition,

it still implies that bond liquidity influences firm’s acquisition decisions. Yet, to address the

possibility that firms issue debt in the year prior to an acquisition we introduce a dummy

variable, which equals one if a firm issued debt in the fiscal year preceding the acquisition. As

can be seen from Model 1 of Table 5, consistent with the idea that firms foreseeing acquisition

possibilities might raise debt beforehand, the coefficient on the new issue dummy is positive and

significant at 1% level. However, our measure of liquidity remains significant even after

controlling for recently issued debt. Alternatively, we limit our analysis to firms which did not

issue debt in the year prior to an acquisition. Our results are robust to this exclusion, as shown in

Model 2. Additionally, we use lagged liquidity measure in Model 3 of Table 5, and similarly

observe a significant and negative coefficient on the Amihud ratio.

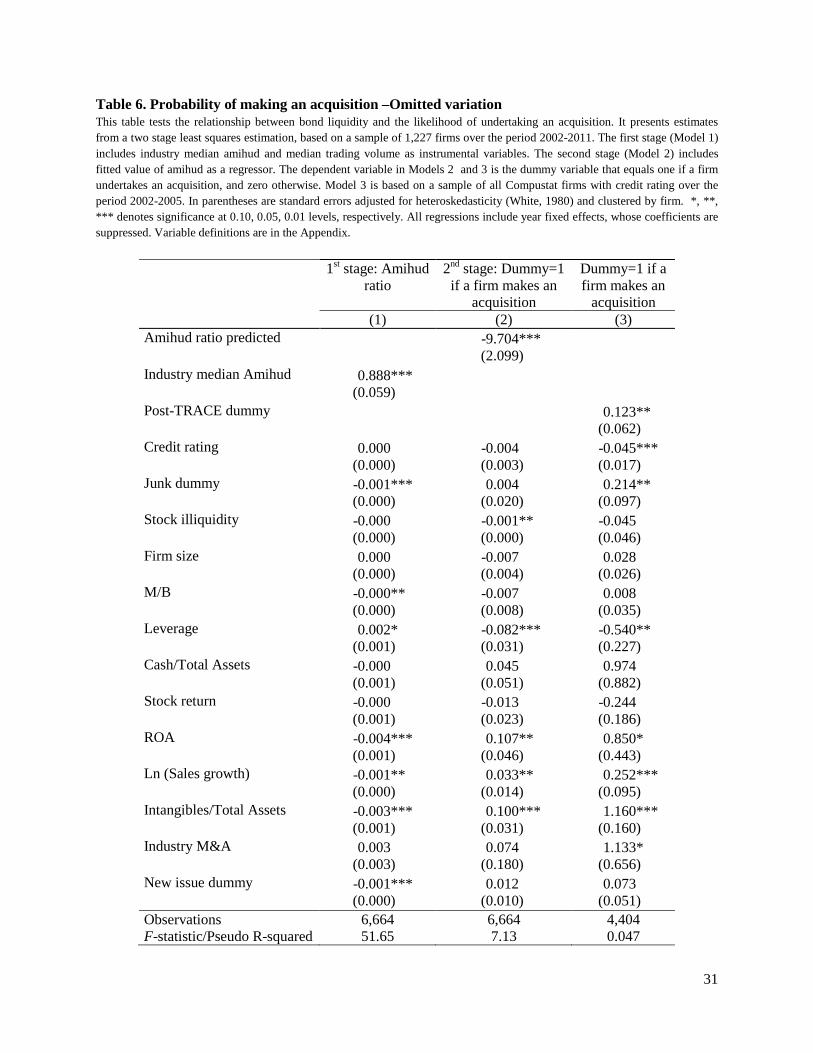

3.2.1. Omitted variation

A more serious concern with the results presented earlier, is that there are firm

characteristics not accounted for in the regression analysis that simultaneously determine a firm’s

acquisition decision and bond liquidity. To address this possibility, we employ a two-stage

14

regression model, which relies on instrumental variables. Following recent literature (Adams et

al (2011), Lin et al. (2011), Lin et al. (2011)) we use industry median liquidity measure as our

instrumental variable. As long as the endogeneity problem is specific to firms, but not to

industries, industry median bond liquidity will be correlated with a firm’s bond liquidity, but not

with an individual firm’s decision to undertake an acquisition. To alleviate the concern that some

industry-level factors might affect an entire industry’s decision to make an acquisition our

regressions include recent industry M&A activity. Table 6 presents the two-stage regression

results. In the first stage, we regress our instrumental variable, along with the control variables

described earlier, on a firm’s Amihud ratio. Consistent with the intuition, the coefficient on

industry median liquidity measure is positive and significant at 1% level. In the second stage we

include a fitted value from the first stage as an explanatory variable. The coefficient on the

predicted liquidity measure is significant, confirming that firms with higher liquidity tend to

make more acquisitions.

Another way to identify the effect of liquidity on the likelihood of making acquisitions is

to use the change in liquidity caused by the exogenous shock of TRACE introduction. Prior

research has shown that bond liquidity improved in response to TRACE, as the introduction of

TRACE improved transparency and reduced transaction costs (e.g. Bessembinder, Maxwell, and

Venkataraman (2006); Edwards, Harris, and Piwowar (2007); Goldstein, Hotchkiss, and Sirri

(2007)). As described in Section 2.1. Securities and Exchange Commission has implemented

TRACE reporting system over the interval between 2002 and 2005. Therefore, to further address

the concern that there could be an omitted variable that is correlated with bond liquidity and

decision to make an acquisition, we use the change in liquidity around the introduction of

TRACE and we make use of the phase-in feature of TRACE introduction. In particular, for this

15

analysis we employ a sample of all COMPUSTAT firms with credit ratings over the period from

2002 to 2005 and exploit the variation generated by staggered introduction of TRACE. We

estimate a model, in spirit of Bertrand and Mullainathan (1999a, 1999b, 2003), as follows:

Acquisition Dummyit=αt+γXit+δPOST-TRACE+εit

where i indexes firm, t indexes years from 2002 to 2005, αt are year fixed effects which

account for any market-wide fluctuations, and Xit represents control variables. The variable of

interest is the POST-TRACE dummy that equals one if a firm’s bonds are covered by TRACE

during year t, and captures the impact of increase in liquidity in the years following TRACE

introduction. As Model 3 in Table 6 shows, the coefficient on POST-TRACE dummy is positive

and significant at the 5% level, suggesting that improvement in bond liquidity leads to higher

probability of making acquisitions.

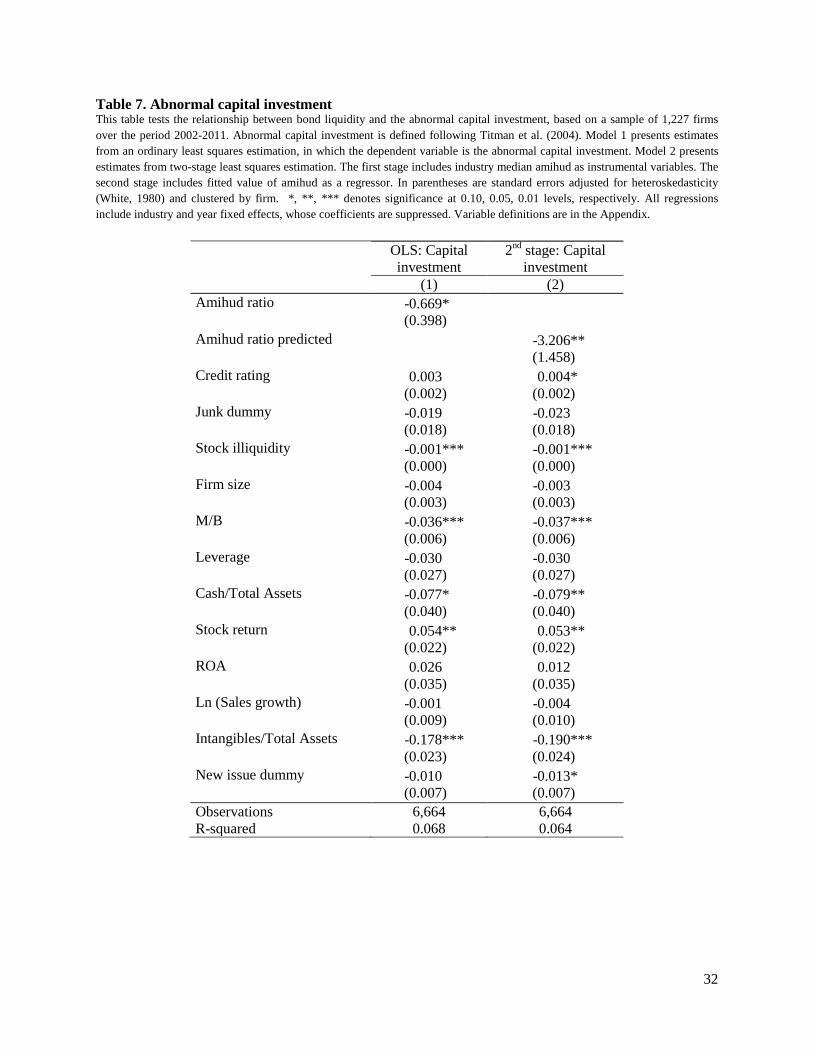

3.3. Capital Expenditure

As an alternative proxy for the expanded investment, we next focus on the increase in the

firm’s capital expenditures, as capital expenditures reflect managerial efforts to exploit current

investment opportunities. Following Titman, Wei, and Xie (2004), we compute the abnormal

capital investment (CIt) in year t-1 as follows:

𝐶𝐶𝑡−1 =𝐶𝐶𝑡−1

(𝐶𝐶𝑡−2 + 𝐶𝐶𝑡−3 + 𝐶𝐶𝑡−4)/3− 1

Where CEt-1 is a firm’s capital expenditure scales by its total assets in yeat t-1.

We then investigate whether bond liquidity affects firm's abnormal capital investments in

the following year. In Model 1 of Table 7, we estimate an ordinary least squares regression, in

which the dependent variable is the measure of abnormal capital investment. Consistent with our

hypothesis that bond liquidity expands plausible investment set we find that the coefficient on

16

the Amihud ratio is negatively significant, suggesting a positive association between a firm’s

bond liquidity and capital investment. Model 2 reports the estimated from the second stage of

the two-stage least squares estimation, in which the Amihud ratio is replaced by its’ predicted

value. Similar to our prior analysis we rely on the industry Amihud ratio as our instrument.

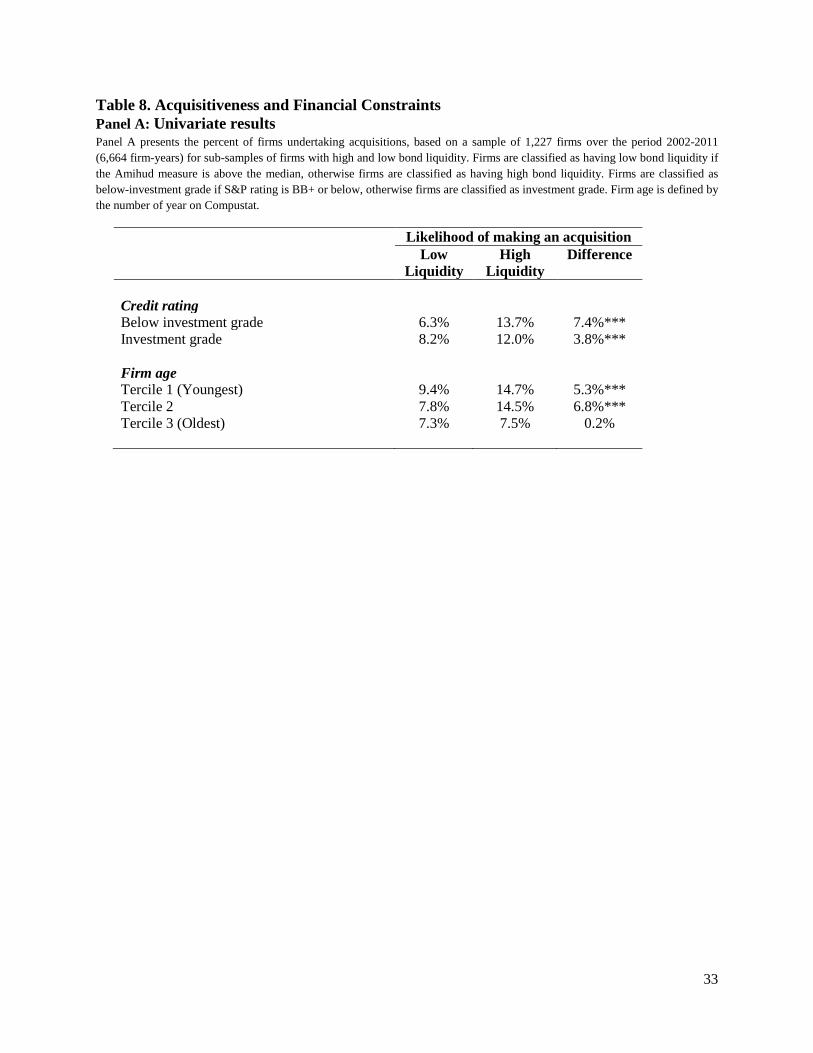

3.4. Bond liquidity and financial constraints

Fazzari et al. (1988) argue that information asymmetry affects firm investment because it

creates financial constraints in the credit markets. A recent survey by Campello, Graham, and

Harvey (2010) reveal that the inability to borrow externally causes firms to bypass attractive

investment opportunities or to postpone investment. If the difference in acquisition activities is

partly attributable to differences in access to financial market, then we would expect that firms

with the least access to financial markets to benefit more from higher bond liquidity. To examine

whether bond liquidity relaxes financial constraints we explore whether bond liquidity has

different impact on acquisition decisions for firms with different levels of financial constraints.

We conjecture that the effect of bond liquidity would be magnified for firms with higher

financial constraints, which we proxy by firm age and credit ratings.

Credit ratings reflect a firm’s access to public bond markets and measure ex ante

information asymmetry and a firm’s financial constraints. The higher the level of credit ratings

the lower the information asymmetry and the adverse selection problem faced by firms

(Faulkender and Petersen (2006), Odders-White and Ready (2006); Easley and O'Hara (1987),

Almeida, Campello, and Weisbach (2004); Frank and Goyal (2009), Rauh and Sufi (2010)).

Since higher credit ratings indicate lower information asymmetry, if we find that low-rated

firms’ merger activity is the most sensitive to bond liquidity it would be consistent with the

17

notion that increased bond liquidity has a bigger impact on firms that are more financially

constrained. Panel A of Table 8 shows that the effect of bond liquidity on acquisition probability

is greater for firms with below-investment-grade ratings, indicating that higher liquidity enables

firms with below investment grade to borrow more or at lower rate to finance acquisitions.

Similarly, it can be argued that younger firms have limited access to debt markets and

thus can benefit substantially by an improvement in bond liquidity, whereas older and more

established firms might have limited upside potential. Panel A of Table 8 shows that bond

liquidity is positively related to a firm’s decision to undertake an acquisition for all, but the most

established firms.

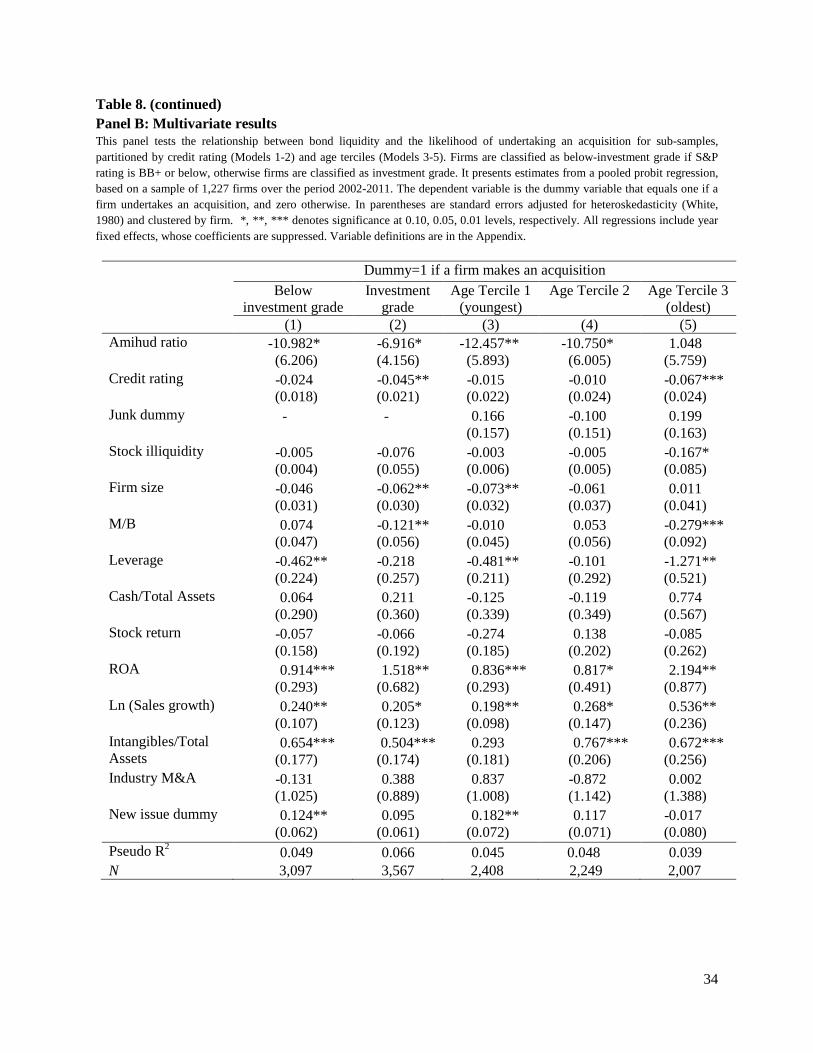

Panel B of Table 8 re-estimates the relationship between bond liquidity and the likelihood

of undertaking an acquisition separately for age terciles and for sub-samples of firms with

investment and non-investment ratings in the multivariate setting. As Panel B shows the effect of

bond liquidity is important for all but the oldest firms. Similarly, the effect of bond liquidity is

larger for firms with below investment grade rating, suggesting that the constrained firms are

affected more by bond liquidity.

3.5. Bond liquidity and firm value

If higher bond liquidity relaxes financial constraints and allows firms to undertake

positive NPV investments, which otherwise would be foregone, it will be positively reflected in

the firm valuations. By enlarging a firm’s investment set, bond liquidity allows a firm to expand

its’ capacity and increase profits by undertaking new value-increasing projects. Furthermore, if

the marginal investor values liquidity, firms with higher liquidity will trade at a premium, as

lower cost of capital means higher valuations for any given cash flows that the company

18

generates (Holmstrom and Tirole, 2001; Amihud and Mendelson, 1988). Thus, we conjecture

that higher bond liquidity, which leads to lower cost of debt and lower required rate of return,

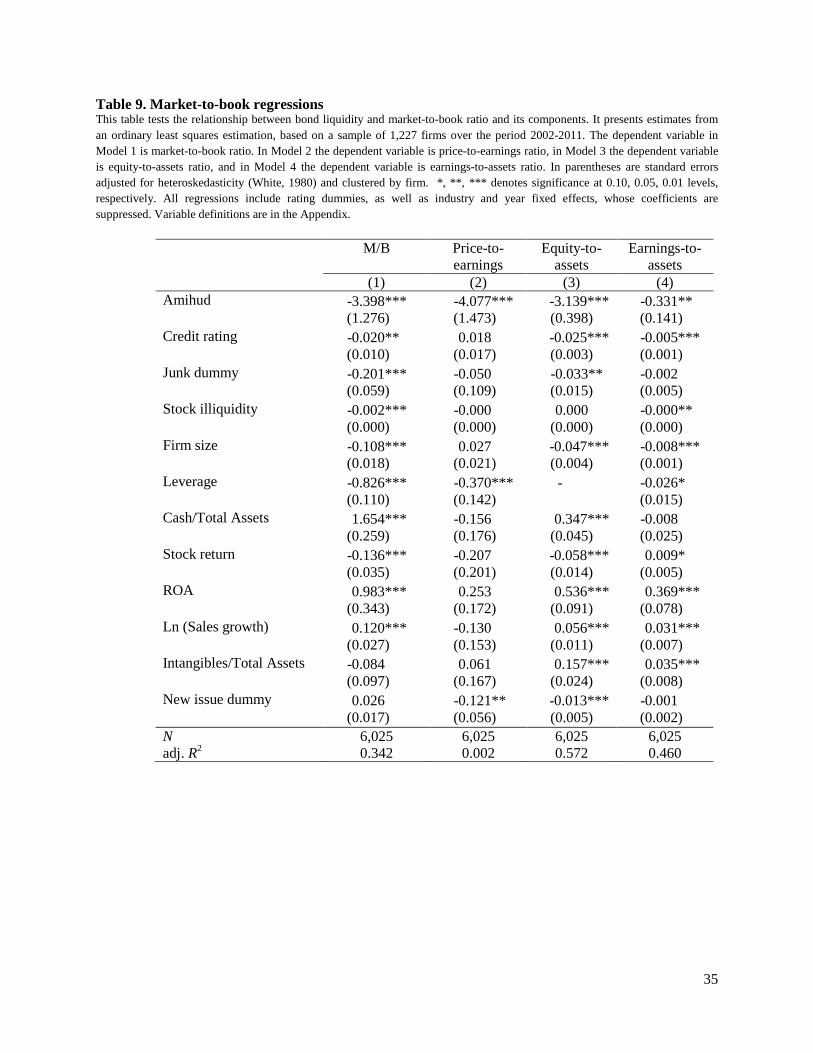

will be associated with higher market-to-book ratios. Model 1 in Table 9 presents the results of

an ordinary least squares regression, in which the dependent variable is market-to-book ratio. We

find that firms with higher bond liquidity are associated with higher market valuations.

To gain further insight into how bond liquidity affects market-to-book ratio, we

decompose it into three components: price-to-earnings, equity-to-assets, and earnings-to-assets,

similar to Fang et al. (2009). In Model 2 of Table 9, the market-to-book ratio is replaced with

price-to-earnings ratio. If higher firm values for firms with more liquid bonds are based on the

liquidity premium, then firms with higher bond liquidity will have higher price-to-earnings

ratios. Consistent with this notion, we find that the coefficient on the Amihud ratio is negative

and significant, indicating that higher liquidity reduces the discount rate. In Model 3 of Table 9,

we replace the dependent variable with Equity-to-assets, which measures the fraction of equity in

the capital structure, and we find that firms with more liquid bonds tend to have a lower

leverage, which is consistent with the negative correlation between bond liquidity and leverage

presented in Table 2. The dependent variable in Model 4 in Table 9 is earnings-to-assets, which

reflect operating profitability. The results show that firms with more liquid bonds tend to be

more profitable, which is consistent with the idea that bond liquidity relaxes a firm’s financial

constraints and allows it to undertake positive NPV projects.

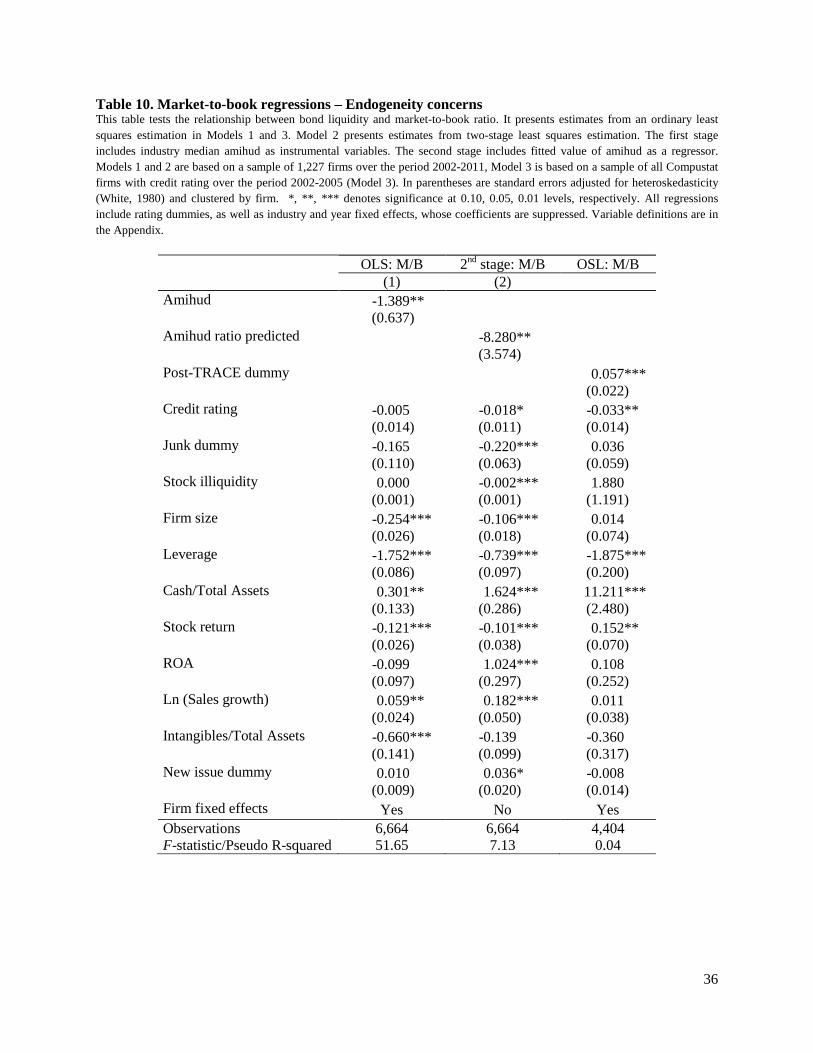

A potential concern with this analysis is that unobservable characteristics correlated with

both bond liquidity and firm performance may make coefficient estimates biased. For example,

firms with high quality managers may tend to be employed by companies with more liquid

bonds. At the same time, high quality managers would also lead to higher market valuations.

19

Thus, bond liquidity will be positively correlated with firm value due to the omitted variables.

One way to account for the unobserved variation at the firm level which is constant over time is

to perform fixed effects analysis. Thus in Model 1 of Table 10 we include firm fixed effects. The

estimates show that firms with higher bond liquidity continue to be positively associated with

higher market valuations. In Model 2 of Table 10, we present estimates from a two-stage least

squares estimation, in which we use industry-median bond liquidity as our instrument and

continue to find a positive effect of bond liquidity on market valuation. Last, we rely on the

introduction of TRACE as an exogenous shock to bond liquidity. Similar to our earlier analysis,

we employ a sample of all COMPUSTAT firms with credit ratings over the period from 2002 to

2005. Additionally we include firm fixed effects in our specification that allows for more precise

controls for any unobserved cross-sectional heterogeneity across firms. Specifically we estimate

a model, as follows:

M/Bit=αt+βi+γXit+δPOST-TRACE+εit

where i indexes firm, t indexes years from 2002 to 2005, αt and βi are year and firm fixed

effects, Xit represents control variables. As Model 3 in Table 10 shows, the coefficient on POST-

TRACE dummy is positive and significant at the 1% level, suggesting that improvement in bond

liquidity leads to higher valuations.

6. Conclusion

This paper studies the impact of bond liquidity on firms' investment. We argue that

higher bond liquidity leads to an expanded investment. We test this hypothesis by focusing in

acquisitions, as they represent the largest investments firms undertake. Our results show that

firms with higher bond liquidity are more likely to make acquisitions and the result is stronger

20

for financially constrained firms, i.e. smaller firms and firms with lower credit ratings.

Furthermore, we find that bond liquidity is associated with higher market valuations, indicating

that higher bond liquidity relaxes firms’ financial constraints and allows them to invest in

positive NPV projects which otherwise would be foregone. Collectively, these findings suggest

that frictions in financial markets have real effects on investment decisions.

21

References

Adams, M., Lin, C., Zou, H., 2011. Chief executive officer incentives, monitoring, and corporate risk management: evidence from insurance use. Journal of Risk and Insurance 78, 551–582. Almazan, A., De Motta, A., Titman, S., Uysal, V., 2010. Financial structure, acquisition opportunities, and firm locations. Journal of Finance 65, 529–563. Almeida, H., Campello, M., Weisbach, M.S., 2004. The cash flow sensitivity of cash. Journal of Finance 59, 1777-1804. Amihud, Y., Mendelson, H., 1986. Asset pricing and the bid-ask spread. Journal of Financial Economics 17, 223–249. Amihud, Y., Mendelson, H., 1988. Liquidity and asset prices: Financial Management Implications. Financial Management 17, 5-15. Amihud, Y., Mendelson, H., Pedersen, L.H., 2005. Liquidity and asset prices. Foundations and Trends in Finance 1, 269–364. Asquith, P., Bruner, R. F., Mullins Jr. D. W., 1983. The gains to bidding firms from merger. Journal of Financial Economics 11, 121-139. Bao, J., Pan, J., Wang, J. , 2011. The illiquidity of corporate bonds. Journal of Finance 66, 911-946. Bertrand, M., Mullainathan, S., 1999a. Is there discretion in wage setting? A test using takeover legislation. Rand Journal of Economics 30, 535-554. Bertrand, M., Mullainathan, S., 1999b. Corporate governance and executive pay: Evidence from takeover legislation. Unpublished working paper. Bertrand, M., Mullainathan, S., 2003. Enjoying the quiet life? Corporate governance and managerial preferences. Journal of Political Economy 111, 1043-1075. Bessembinder, H., Kahle, K. M., Maxwell, W. F., Xu, D., 2009. Measuring abnormal bond performance. Review of Financial Studies 22, 4219–4258. Bharadwaj, A., Shivdasani, A., 2003. Valuation effects of bank financing in acquisitions. Journal of Financial Economics 67, 113-148. Campello, M., Graham, J., Harvey, C., 2010. The real effects of financial constraints: evidence from a financial crisis. Journal of Financial Economics 97, 470-487. Chen, L., Lesmond, D. A., Wei, J., 2007. Corporate yield spreads and bond liquidity. Journal of Finance 62, 119–149. Dick-Nielsen, J., Feldhütter, P., Lando, D., 2012. Corporate bond liquidity before and after the onset of the subprime crisis. Journal of Financial Economics 103, 471–492. Downing, C., Underwood, S., Xing, Y., 2005. Is liquidity risk priced in the corporate bond market? Working Paper, Rice University.

22

Easley, D., O'Hara, M., 1987. Price, trade size, and information in securities markets. Journal of Financial Economics 19, 69-90. Edwards, A. K., Harris, L. E., Piwowar, M., 2007. Corporate bond market transaction costs and transparency. Journal of Finance 62, 1421–1448. Ericsson, J., Renault, O., 2006. Liquidity and credit risk. Journal of Finance 61, 2219–2250. Faccio, M., Masulis, R. W., 2005. The choice of payment method in European mergers and acquisitions. Journal of Finance 60, 1345–1388. Fama, E. F., French, K. R., 1997. Industry costs of capital. Journal of Financial Economics 43, 153-193.

Fang, V. W, Noe, T. H., Tice, S., 2009. Stock market liquidity and firm value. Journal of Financial Economics 94, 150-169. Faulkender, M., Petersen, M. A., 2006. Does the source of capital affect capital structure. Review of Financial Studies 19, 45-79. Fazzari, S., Hubbard, R. G., Petersen, B., 1988a. Finance constraints and corporate investment, Brookings Papers on Economic Activity 1, 141-195. Fazzari, S., Hubbard, R. G., Petersen, B., 1988b. Investment, financing policy, and tax policy. American Economic Review 78 200-205. Fazzari, S., Hubbard, R. G., Petersen, B., Blinder, A., Poterba, J., 1988c. Financing constraints and corporate investment, Brookings Papers on Economic Activity 1, 141-206. Frank, M. Z., Goyal, V. K., 2009. Capital structure decisions: which factors are reliably important? Financial Management 38, 1-37. Fuller, K., Netter, J., Stegemoller, M., 2002. What do returns to acquiring firms tell us? Evidence from firms that make many acquisitions. Journal of Finance 57, 1763–1794. Goldstein, M.A., Hotchkiss, E.S., Sirri, E.R, 2007. Transparency and Liquidity: A controlled experiment on corporate bonds. Review of Financial Studies 20, 235-273. Harford, J., 1999. Corporate cash reserves and acquisitions. Journal of Finance 54, 1969-1997. Harford, J., Klasa, S., Walcott, N., 2009. Do firms have leverage targets? Evidence from acquisitions. Journal of Financial Economics 93, 1-14. Harford, J., Uysal V., 2013. Bond market access and investment. Journal of Financial Economics Forthcoming. He, Z., Xiong, W., 2012. Dynamic Debt Runs. Review of Financial Studies 25, 1799-1843. Helwege, J., Huang, J., Wang, Y., 2013. Liquidity effects in corporate bond spreads. Journal of Banking and Finance, Forthcoming.

23

Holmstrom, B., Tirole J., 2001. LAPM: A liquidity-based asset pricing model. Journal of Finance 56, 1837-1867. Karampatsas, N., D. Petmezas and N. Travlos, 2014. Credit Ratings and the Choice of Payment Method in Mergers and Acquisitions. Journal of Corporate Finance 25, 474-493. Lemmon, M., Roberts, M. R., 2010. The response of corporate financing and investment to changes in the supply of credit. Journal of Financial and Quantitative Analysis 45, 555–87. Lin, C., Officer, M. S., Zou, H., 2011. Directors’ and officers’ liability insurance and acquisition outcomes. Journal of Financial Economics 102, 507–525. Lin, C., Ma, Y., Malatesta, P., Xuan, Y., 2011. Ownership structure and the cost of corporate borrowing. Journal of Financial Economics 100, 1–23. Loughran, T., and Ritter, J. R., 2004. Why has IPO underpricing changed over time? Financial Management 33, 5-37. Malmendier, U., Tate, G., 2008. Who makes acquisitions? CEO overconfidence and the market’s reaction. Journal of Financial Economics 89, 20-43. Masulis, R. W., Wang, C., Xie, F., 2007. Corporate governance and acquirer returns. Journal of Finance 62, 1851-1889. Moeller, S. B., Schlingemann, F. P., Stulz, R. M., 2004. Firm size and the gains from acquisitions. Journal of Financial Economics 73, 201-228. Moeller, S. B., Schlingemann, F. P., Stulz, R. M., 2005. Wealth destruction on a massive scale? A study of acquiring-firm returns in the recent merger wave. Journal of Finance 60, 757-782. Morellec, E. 2010. Credit supply and corporate policies. Working Paper. Odders-White, E.R., Ready, M.J., 2006, Credit ratings and stock liquidity. Review of Financial Studies 19, 119-157. Petersen, M. A., 2009. Estimating standard errors in finance panel data sets: Comparing approaches. Review of Financial Studies 22, 435–480. Roll, R., 1984. A Simple Implicit Measure of the Effective Bid-Ask Spread in an Efficient Market. Journal of Finance 39, 1127–1139. Rauh, J. D., Sufi, A., 2010. Capital structure and debt structure. Review of Financial Studies 23, 4242-4280. Roll, R., 1986. The hubris hypothesis of corporate takeovers. Journal of Business 59, 197-216. Titman, S., Wei, J. K. C., Xie, F., 2004. Capital investments and stock returns. Journal of Financial and Quantitative Analysis 39, 677-700. Uysal, V., 2011. Deviation from the target capital structure and acquisition choices. Journal of Financial Economics 102, 602-620.

24

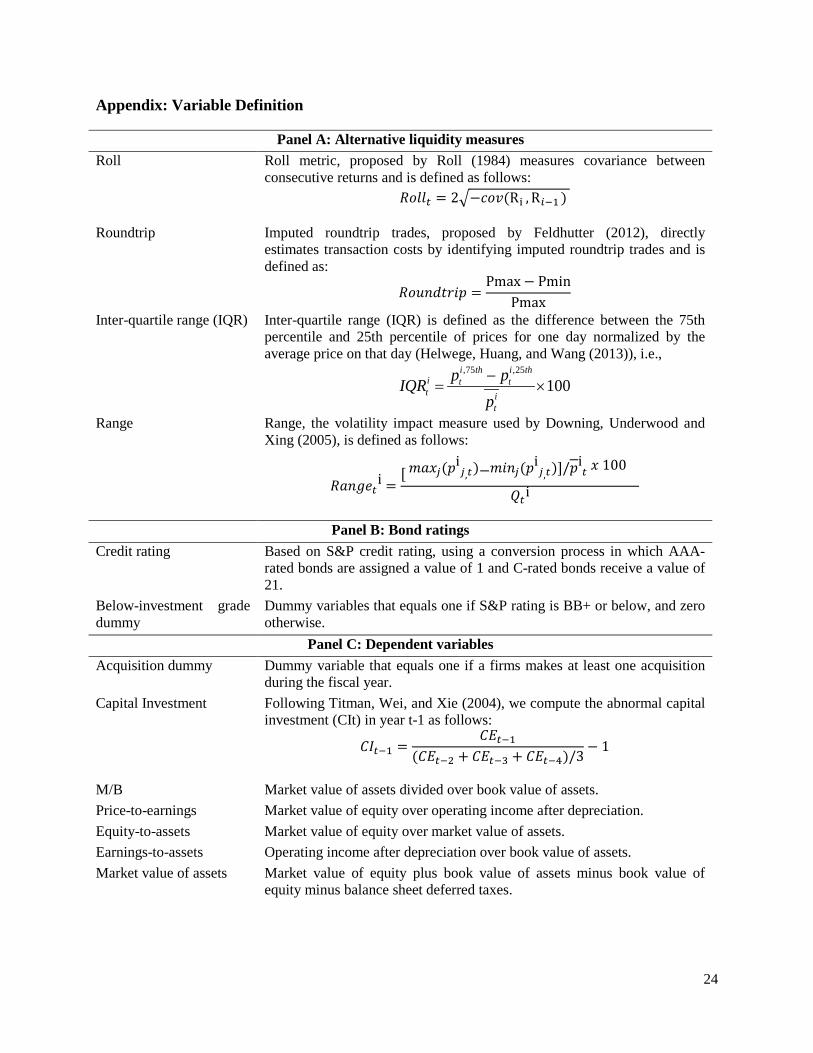

Appendix: Variable Definition

Panel A: Alternative liquidity measures Roll Roll metric, proposed by Roll (1984) measures covariance between

consecutive returns and is defined as follows: 𝑅𝑅𝑅𝑅𝑡 = 2�−𝑐𝑅𝑐(Ri , R𝑖−1 )

Roundtrip Imputed roundtrip trades, proposed by Feldhutter (2012), directly estimates transaction costs by identifying imputed roundtrip trades and is defined as:

𝑅𝑅𝑅𝑅𝑅𝑅𝑅𝑅𝑅 =Pmax − Pmin

Pmax

Inter-quartile range (IQR) Inter-quartile range (IQR) is defined as the difference between the 75th percentile and 25th percentile of prices for one day normalized by the average price on that day (Helwege, Huang, and Wang (2013)), i.e.,

,75 ,25

100i th i th

i t tt i

t

p pIQRp−

= ×

Range Range, the volatility impact measure used by Downing, Underwood and Xing (2005), is defined as follows:

𝑅𝑅𝑅𝑅𝑅𝑡i =[ 𝑚𝑅𝑚𝑗(𝑅i

𝑗,𝑡)−𝑚𝑅𝑅𝑗(𝑅i𝑗,𝑡)]/𝑅i

𝑡 𝑚 100

𝑄𝑡i

Panel B: Bond ratings Credit rating Based on S&P credit rating, using a conversion process in which AAA-

rated bonds are assigned a value of 1 and C-rated bonds receive a value of 21.

Below-investment grade dummy

Dummy variables that equals one if S&P rating is BB+ or below, and zero otherwise.

Panel C: Dependent variables Acquisition dummy Dummy variable that equals one if a firms makes at least one acquisition

during the fiscal year. Capital Investment Following Titman, Wei, and Xie (2004), we compute the abnormal capital

investment (CIt) in year t-1 as follows:

𝐶𝐶𝑡−1 =𝐶𝐶𝑡−1

(𝐶𝐶𝑡−2 + 𝐶𝐶𝑡−3 + 𝐶𝐶𝑡−4)/3− 1

M/B Market value of assets divided over book value of assets. Price-to-earnings Market value of equity over operating income after depreciation. Equity-to-assets Market value of equity over market value of assets. Earnings-to-assets Operating income after depreciation over book value of assets. Market value of assets Market value of equity plus book value of assets minus book value of

equity minus balance sheet deferred taxes.

25

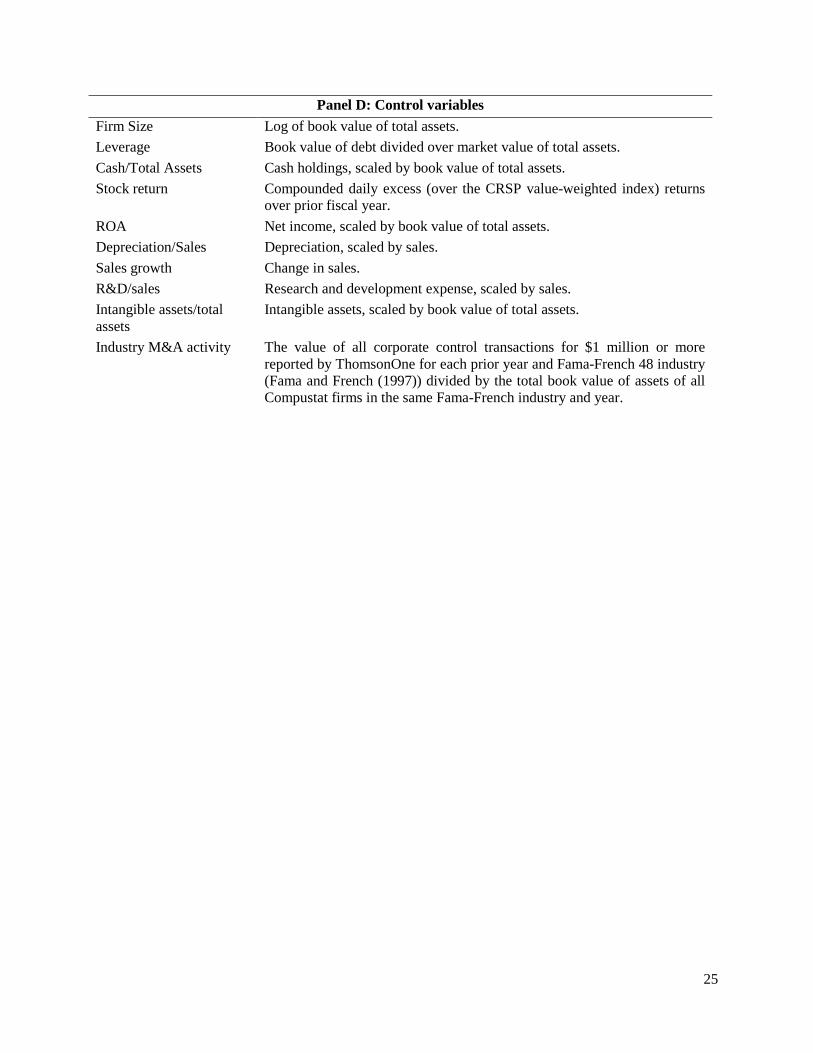

Panel D: Control variables Firm Size Log of book value of total assets. Leverage Book value of debt divided over market value of total assets. Cash/Total Assets Cash holdings, scaled by book value of total assets. Stock return Compounded daily excess (over the CRSP value-weighted index) returns

over prior fiscal year. ROA Net income, scaled by book value of total assets. Depreciation/Sales Depreciation, scaled by sales. Sales growth Change in sales. R&D/sales Research and development expense, scaled by sales. Intangible assets/total assets

Intangible assets, scaled by book value of total assets.

Industry M&A activity The value of all corporate control transactions for $1 million or more reported by ThomsonOne for each prior year and Fama-French 48 industry (Fama and French (1997)) divided by the total book value of assets of all Compustat firms in the same Fama-French industry and year.

26

Table 1. Summary Statistics This table presents summary statistics of firm characteristics, based on a sample of 1,227 firms over the period 2002-2011 (6,664 firm-years). Variable definitions are in the Appendix.

Mean St. Dev.

25th percentile

Median 75th percentile

Panel A: Firm characteristics

Firm size (in billions) 41.45 183.92 2.33 6.37 19.86

M/B 1.54 0.74 1.08 1.32 1.73 Leverage 0.24 0.17 0.11 0.21 0.33 Cash/Total Assets 0.09 0.11 0.02 0.06 0.13 Stock return -0.07 0.25 -0.21 -0.10 -0.02 ROA 0.03 0.11 0.01 0.04 0.07 Amihud ratio (in basis points) 80.95 74.47 34.44 58.87 102.72 Junk dummy (BB+ or lower) 0.46 0.50 - - - New debt issue in prior fiscal year 0.38 0.49 - - - Conducted acquisition during fiscal year 0.13 0.34 - - -

27

Table 2. Pearson Correlation Matrix

This table presents correlation matrix of measures of bond liquidty with firm characteristics, based on a sample of 1,227 firms over the period 2002-2011 (6,664 firm-years).

Amihud ratio

Firm size

M/B Leverage ROA Stock illiquidity

Junk

Amihud ratio 1 0.10 -0.15 0.05 -0.11 -0.04 -0.08

Firm size 1 -0.17 -0.17 0.07 0.07 -0.52

M/B 1 -0.35 0.27 0.03 -0.09

Leverage 1 -0.33 -0.10 0.35

ROA 1 0.09 -0.22

Stock illiquidity 1 -0.05

Junk 1

28

Table 3. Likelihood of making acquisitions – Univariate results This table presents the percent of firms undertaking acquisitions, based on a sample of 1,227 firms over the period 2002-2011 (6,664 firm-years) for sub-samples of firms with high and low bond liquidity. Firms are classified as having low bond liquidity if the Amihud measure is above the median, otherwise firms are classified as having high bond liquidity. Firm size is measured by the log of total assets. Firms are classified as high stock liquidity if Amihud measure is above the median, and are classified as having low stock liquidity otherwise. Differences in the frequency of acquisitions between firms with low and high liquidity are based on the chi-squared test. *, **, *** denotes significance at 0.10, 0.05, 0.01 levels, respectively.

Likelihood of making an acquisition

Low

Liquidity High

Liquidity Difference

Full Sample 7.4% 12.7% 5.3%*** 2002-2006 12.6% 15.4% 2.9%* 2007-2012 6.0% 8.1% 2.1%* Size terciles Tercile 1 (smallest) 8.3% 15.8% 7.4%*** Tercile 2 8.9% 12.3% 3.4%* Tercile 3 (largest) 6.0% 9.1% 3.1%* Stock liquidity Low stock liquidity 11.9% 14.9% 3.0%* High stock liquidity 5.2% 10.0% 4.8%***

29

Table 4. Probability of making an acquisition – Baseline analysis This table tests the relationship between bond liquidity and the likelihood of undertaking an acquisition. It presents estimates from a pooled probit regression, based on a sample of 1,227 firms over the period 2002-2011. The dependent variable in Models 1-5 is the dummy variable that equals one if a firm undertakes an acquisition, and zero otherwise. In parentheses are standard errors adjusted for heteroskedasticity (White, 1980) and clustered by firm. *, **, *** denotes significance at 0.10, 0.05, 0.01 levels, respectively. All regressions include year fixed effects, whose coefficients are suppressed. Variable definitions are in the Appendix.

Dummy=1 if a firm makes an acquisition (1) (2) (3) (4) (5) Amihud ratio -8.504**

(3.443)

Roll

-15.717*** (5.399)

Roundtrip

-11.069** (5.507)

Inter-quartile range

-0.211** (0.087)

Range

-0.184*** (0.070)

Credit rating -0.026** (0.013)

-0.032** (0.015)

-0.023* (0.013)

-0.023* (0.013)

-0.026** (0.013)

Junk dummy 0.096 (0.089)

0.095 (0.098)

0.103 (0.089)

0.095 (0.090)

0.095 (0.089)

Stock illiquidity -0.005 (0.004)

-0.006*** (0.002)

-0.006 (0.004)

-0.006 (0.004)

-0.005 (0.004)

Firm size -0.037* (0.021)

-0.051** (0.024)

-0.031 (0.022)

-0.037* (0.021)

-0.043** (0.021)

M/B -0.021 (0.033)

-0.025 (0.040)

-0.015 (0.033)

-0.019 (0.033)

-0.023 (0.033)

Leverage -0.329** (0.165)

-0.375** (0.181)

-0.306* (0.166)

-0.318* (0.166)

-0.341** (0.166)

Cash/Total Assets 0.181 (0.226)

0.119 (0.248)

0.225 (0.224)

0.202 (0.225)

0.173 (0.226)

Stock return -0.093 (0.118)

-0.055 (0.127)

-0.083 (0.118)

-0.075 (0.118)

-0.086 (0.118)

ROA 0.940*** (0.261)

0.861*** (0.279)

0.918*** (0.264)

0.914*** (0.264)

0.936*** (0.261)

Ln (Sales growth) 0.271*** (0.091)

0.302*** (0.091)

0.274*** (0.092)

0.272*** (0.092)

0.270*** (0.091)

Intangibles/Total Assets 0.562*** (0.123)

0.552*** (0.130)

0.584*** (0.121)

0.574*** (0.122)

0.558*** (0.123)

Industry M&A 0.220 (0.657)

0.102 (0.763)

0.239 (0.656)

0.214 (0.658)

0.196 (0.657)

Pseudo R2 0.032 0.034 0.31 0.032 0.032 N 6,664 5,451 6,664 6,664 6,664

30

Table 5. Probability of making an acquisition – Reverse Causality This table tests the relationship between bond liquidity and the likelihood of undertaking an acquisition. It presents estimates from a pooled probit regression, based on a sample of 1,227 firms over the period 2002-2011. The dependent variable in Models 1-3 is the dummy variable that equals one if a firm undertakes an acquisition, and zero otherwise. In Model 2 we omit firms that issue debt in a year prior to the acquisition. In parentheses are standard errors adjusted for heteroskedasticity (White, 1980) and clustered by firm. *, **, *** denotes significance at 0.10, 0.05, 0.01 levels, respectively. All regressions include year fixed effects, whose coefficients are suppressed. Variable definitions are in the Appendix.

Dummy=1 if a firm makes an acquisition Controlling for

recent debt issues Omitting firms with recent debt

issues

Including lagged measures

(1) (2) (3) Amihud ratio -7.867**

(3.440) -7.364* (3.806)

Lagged Amihud

-7.395** (3.483)

New issue dummy 0.105** (0.043)

0.105** (0.049)

Credit rating -0.025* (0.013)

-0.013 (0.015)

-0.030** (0.015)

Junk dummy 0.089 (0.089)

0.059 (0.102)

0.078 (0.096)

Stock illiquidity -0.005 (0.004)

-0.004*** (0.001)

-0.004*** (0.002)

Firm size -0.046** (0.022)

-0.033 (0.025)

-0.054** (0.025)

M/B -0.023 (0.033)

-0.002 (0.039)

-0.002 (0.038)

Leverage -0.387** (0.165)

-0.712*** (0.214)

-0.395** (0.186)

Cash/Total Assets 0.183 (0.225)

-0.054 (0.295)

0.196 (0.251)

Stock return -0.084 (0.118)

-0.174 (0.158)

-0.088 (0.128)

ROA 0.945*** (0.262)

0.709*** (0.267)

0.650** (0.255)

Ln (Sales growth) 0.261*** (0.088)

0.292** (0.128)

0.334*** (0.096)

Intangibles/Total Assets 0.559*** (0.123)

0.656*** (0.143)

0.541*** (0.131)

Industry M&A 0.210 (0.659)

0.660 (0.781)

-0.015 (0.743)

Pseudo R2 0.033 0.040 0.033 N 6,664 4,072 5,362

31

Table 6. Probability of making an acquisition –Omitted variation This table tests the relationship between bond liquidity and the likelihood of undertaking an acquisition. It presents estimates from a two stage least squares estimation, based on a sample of 1,227 firms over the period 2002-2011. The first stage (Model 1) includes industry median amihud and median trading volume as instrumental variables. The second stage (Model 2) includes fitted value of amihud as a regressor. The dependent variable in Models 2 and 3 is the dummy variable that equals one if a firm undertakes an acquisition, and zero otherwise. Model 3 is based on a sample of all Compustat firms with credit rating over the period 2002-2005. In parentheses are standard errors adjusted for heteroskedasticity (White, 1980) and clustered by firm. *, **, *** denotes significance at 0.10, 0.05, 0.01 levels, respectively. All regressions include year fixed effects, whose coefficients are suppressed. Variable definitions are in the Appendix.

1st stage: Amihud ratio

2nd stage: Dummy=1 if a firm makes an

acquisition

Dummy=1 if a firm makes an

acquisition (1) (2) (3) Amihud ratio predicted

-9.704*** (2.099)

Industry median Amihud 0.888*** (0.059)

Post-TRACE dummy 0.123** (0.062)

Credit rating 0.000 (0.000)

-0.004 (0.003)

-0.045*** (0.017)

Junk dummy -0.001*** (0.000)

0.004 (0.020)

0.214** (0.097)

Stock illiquidity -0.000 (0.000)

-0.001** (0.000)

-0.045 (0.046)

Firm size 0.000 (0.000)

-0.007 (0.004)

0.028 (0.026)

M/B -0.000** (0.000)

-0.007 (0.008)

0.008 (0.035)

Leverage 0.002* (0.001)

-0.082*** (0.031)

-0.540** (0.227)

Cash/Total Assets -0.000 (0.001)

0.045 (0.051)

0.974 (0.882)

Stock return -0.000 (0.001)

-0.013 (0.023)

-0.244 (0.186)

ROA -0.004*** (0.001)

0.107** (0.046)

0.850* (0.443)

Ln (Sales growth) -0.001** (0.000)

0.033** (0.014)

0.252*** (0.095)

Intangibles/Total Assets -0.003*** (0.001)

0.100*** (0.031)

1.160*** (0.160)

Industry M&A 0.003 (0.003)

0.074 (0.180)

1.133* (0.656)

New issue dummy -0.001*** (0.000)

0.012 (0.010)

0.073 (0.051)

Observations 6,664 6,664 4,404 F-statistic/Pseudo R-squared 51.65 7.13 0.047

32

Table 7. Abnormal capital investment This table tests the relationship between bond liquidity and the abnormal capital investment, based on a sample of 1,227 firms over the period 2002-2011. Abnormal capital investment is defined following Titman et al. (2004). Model 1 presents estimates from an ordinary least squares estimation, in which the dependent variable is the abnormal capital investment. Model 2 presents estimates from two-stage least squares estimation. The first stage includes industry median amihud as instrumental variables. The second stage includes fitted value of amihud as a regressor. In parentheses are standard errors adjusted for heteroskedasticity (White, 1980) and clustered by firm. *, **, *** denotes significance at 0.10, 0.05, 0.01 levels, respectively. All regressions include industry and year fixed effects, whose coefficients are suppressed. Variable definitions are in the Appendix.

OLS: Capital investment

2nd stage: Capital investment

(1) (2) Amihud ratio -0.669*

(0.398)

Amihud ratio predicted

-3.206** (1.458)

Credit rating 0.003 (0.002)

0.004* (0.002)

Junk dummy -0.019 (0.018)

-0.023 (0.018)

Stock illiquidity -0.001*** (0.000)

-0.001*** (0.000)

Firm size -0.004 (0.003)

-0.003 (0.003)

M/B -0.036*** (0.006)

-0.037*** (0.006)

Leverage -0.030 (0.027)

-0.030 (0.027)

Cash/Total Assets -0.077* (0.040)

-0.079** (0.040)

Stock return 0.054** (0.022)

0.053** (0.022)

ROA 0.026 (0.035)

0.012 (0.035)

Ln (Sales growth) -0.001 (0.009)

-0.004 (0.010)

Intangibles/Total Assets -0.178*** (0.023)

-0.190*** (0.024)

New issue dummy -0.010 (0.007)

-0.013* (0.007)

Observations 6,664 6,664 R-squared 0.068 0.064

33

Table 8. Acquisitiveness and Financial Constraints Panel A: Univariate results Panel A presents the percent of firms undertaking acquisitions, based on a sample of 1,227 firms over the period 2002-2011 (6,664 firm-years) for sub-samples of firms with high and low bond liquidity. Firms are classified as having low bond liquidity if the Amihud measure is above the median, otherwise firms are classified as having high bond liquidity. Firms are classified as below-investment grade if S&P rating is BB+ or below, otherwise firms are classified as investment grade. Firm age is defined by the number of year on Compustat.

Likelihood of making an acquisition

Low Liquidity

High Liquidity

Difference

Credit rating

Below investment grade 6.3% 13.7% 7.4%*** Investment grade 8.2% 12.0% 3.8%*** Firm age Tercile 1 (Youngest) 9.4% 14.7% 5.3%*** Tercile 2 7.8% 14.5% 6.8%*** Tercile 3 (Oldest) 7.3% 7.5% 0.2%

34

Table 8. (continued) Panel B: Multivariate results This panel tests the relationship between bond liquidity and the likelihood of undertaking an acquisition for sub-samples, partitioned by credit rating (Models 1-2) and age terciles (Models 3-5). Firms are classified as below-investment grade if S&P rating is BB+ or below, otherwise firms are classified as investment grade. It presents estimates from a pooled probit regression, based on a sample of 1,227 firms over the period 2002-2011. The dependent variable is the dummy variable that equals one if a firm undertakes an acquisition, and zero otherwise. In parentheses are standard errors adjusted for heteroskedasticity (White, 1980) and clustered by firm. *, **, *** denotes significance at 0.10, 0.05, 0.01 levels, respectively. All regressions include year fixed effects, whose coefficients are suppressed. Variable definitions are in the Appendix.

Dummy=1 if a firm makes an acquisition Below

investment grade Investment

grade Age Tercile 1

(youngest) Age Tercile 2 Age Tercile 3

(oldest) (1) (2) (3) (4) (5) Amihud ratio -10.982*

(6.206) -6.916* (4.156)

-12.457** (5.893)

-10.750* (6.005)

1.048 (5.759)

Credit rating -0.024 (0.018)

-0.045** (0.021)

-0.015 (0.022)

-0.010 (0.024)

-0.067*** (0.024)

Junk dummy - - 0.166 (0.157)

-0.100 (0.151)

0.199 (0.163)

Stock illiquidity -0.005 (0.004)

-0.076 (0.055)

-0.003 (0.006)

-0.005 (0.005)

-0.167* (0.085)

Firm size -0.046 (0.031)

-0.062** (0.030)

-0.073** (0.032)

-0.061 (0.037)

0.011 (0.041)

M/B 0.074 (0.047)

-0.121** (0.056)

-0.010 (0.045)

0.053 (0.056)

-0.279*** (0.092)

Leverage -0.462** (0.224)

-0.218 (0.257)

-0.481** (0.211)

-0.101 (0.292)

-1.271** (0.521)

Cash/Total Assets 0.064 (0.290)

0.211 (0.360)

-0.125 (0.339)

-0.119 (0.349)

0.774 (0.567)

Stock return -0.057 (0.158)

-0.066 (0.192)

-0.274 (0.185)

0.138 (0.202)

-0.085 (0.262)

ROA 0.914*** (0.293)

1.518** (0.682)

0.836*** (0.293)

0.817* (0.491)

2.194** (0.877)

Ln (Sales growth) 0.240** (0.107)

0.205* (0.123)

0.198** (0.098)

0.268* (0.147)

0.536** (0.236)

Intangibles/Total Assets

0.654*** (0.177)

0.504*** (0.174)

0.293 (0.181)

0.767*** (0.206)

0.672*** (0.256)

Industry M&A -0.131 (1.025)

0.388 (0.889)

0.837 (1.008)

-0.872 (1.142)

0.002 (1.388)

New issue dummy 0.124** (0.062)

0.095 (0.061)

0.182** (0.072)

0.117 (0.071)

-0.017 (0.080)

Pseudo R2 0.049 0.066 0.045 0.048 0.039 N 3,097 3,567 2,408 2,249 2,007

35

Table 9. Market-to-book regressions This table tests the relationship between bond liquidity and market-to-book ratio and its components. It presents estimates from an ordinary least squares estimation, based on a sample of 1,227 firms over the period 2002-2011. The dependent variable in Model 1 is market-to-book ratio. In Model 2 the dependent variable is price-to-earnings ratio, in Model 3 the dependent variable is equity-to-assets ratio, and in Model 4 the dependent variable is earnings-to-assets ratio. In parentheses are standard errors adjusted for heteroskedasticity (White, 1980) and clustered by firm. *, **, *** denotes significance at 0.10, 0.05, 0.01 levels, respectively. All regressions include rating dummies, as well as industry and year fixed effects, whose coefficients are suppressed. Variable definitions are in the Appendix.

M/B Price-to-earnings

Equity-to-assets

Earnings-to-assets

(1) (2) (3) (4) Amihud -3.398***

(1.276) -4.077*** (1.473)

-3.139*** (0.398)

-0.331** (0.141)

Credit rating -0.020** (0.010)

0.018 (0.017)

-0.025*** (0.003)

-0.005*** (0.001)

Junk dummy -0.201*** (0.059)

-0.050 (0.109)

-0.033** (0.015)

-0.002 (0.005)

Stock illiquidity -0.002*** (0.000)

-0.000 (0.000)

0.000 (0.000)

-0.000** (0.000)

Firm size -0.108*** (0.018)

0.027 (0.021)

-0.047*** (0.004)

-0.008*** (0.001)

Leverage -0.826*** (0.110)

-0.370*** (0.142)

-

-0.026* (0.015)

Cash/Total Assets 1.654*** (0.259)

-0.156 (0.176)

0.347*** (0.045)

-0.008 (0.025)

Stock return -0.136*** (0.035)

-0.207 (0.201)

-0.058*** (0.014)

0.009* (0.005)

ROA 0.983*** (0.343)

0.253 (0.172)

0.536*** (0.091)

0.369*** (0.078)

Ln (Sales growth) 0.120*** (0.027)

-0.130 (0.153)

0.056*** (0.011)

0.031*** (0.007)

Intangibles/Total Assets -0.084 (0.097)

0.061 (0.167)

0.157*** (0.024)

0.035*** (0.008)

New issue dummy 0.026 (0.017)

-0.121** (0.056)

-0.013*** (0.005)

-0.001 (0.002)

N 6,025 6,025 6,025 6,025 adj. R2 0.342 0.002 0.572 0.460

36

Table 10. Market-to-book regressions – Endogeneity concerns This table tests the relationship between bond liquidity and market-to-book ratio. It presents estimates from an ordinary least squares estimation in Models 1 and 3. Model 2 presents estimates from two-stage least squares estimation. The first stage includes industry median amihud as instrumental variables. The second stage includes fitted value of amihud as a regressor. Models 1 and 2 are based on a sample of 1,227 firms over the period 2002-2011, Model 3 is based on a sample of all Compustat firms with credit rating over the period 2002-2005 (Model 3). In parentheses are standard errors adjusted for heteroskedasticity (White, 1980) and clustered by firm. *, **, *** denotes significance at 0.10, 0.05, 0.01 levels, respectively. All regressions include rating dummies, as well as industry and year fixed effects, whose coefficients are suppressed. Variable definitions are in the Appendix.

OLS: M/B 2nd stage: M/B OSL: M/B (1) (2) Amihud -1.389**

(0.637)

Amihud ratio predicted

-8.280** (3.574)

Post-TRACE dummy 0.057*** (0.022)

Credit rating -0.005 (0.014)

-0.018* (0.011)

-0.033** (0.014)

Junk dummy -0.165 (0.110)

-0.220*** (0.063)

0.036 (0.059)

Stock illiquidity 0.000 (0.001)

-0.002*** (0.001)

1.880 (1.191)

Firm size -0.254*** (0.026)

-0.106*** (0.018)

0.014 (0.074)

Leverage -1.752*** (0.086)

-0.739*** (0.097)

-1.875*** (0.200)

Cash/Total Assets 0.301** (0.133)

1.624*** (0.286)

11.211*** (2.480)

Stock return -0.121*** (0.026)

-0.101*** (0.038)

0.152** (0.070)

ROA -0.099 (0.097)

1.024*** (0.297)

0.108 (0.252)

Ln (Sales growth) 0.059** (0.024)

0.182*** (0.050)

0.011 (0.038)

Intangibles/Total Assets -0.660*** (0.141)

-0.139 (0.099)

-0.360 (0.317)

New issue dummy 0.010 (0.009)

0.036* (0.020)

-0.008 (0.014)

Firm fixed effects Yes No Yes Observations 6,664 6,664 4,404 F-statistic/Pseudo R-squared 51.65 7.13 0.04